GOLD: $1283.70 DOWN $1.70 (COMEX TO COMEX CLOSING)

Silver: $15.10 UP 1 CENT (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1287.90

silver: $15.14

GOLD/SILVER EQUITY SHARES HELD TODAY SO MAYBE WE HIT THE BOTTOM OF THIS CONTINUAL RAID CYCLE.

For comex gold and silver:

MARCH

NUMBER OF NOTICES FILED TODAY FOR MAR CONTRACT: 19 NOTICE(S) FOR 1900 OZ (0.0590 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 263 NOTICES FOR 26300 OZ (.8180 TONNES)

SILVER

FOR MARCH

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

108 NOTICE(S) FILED TODAY FOR 540,000 OZ/

total number of notices filed so far this month: 4328 for 21,640,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3769:UP $40

Bitcoin: FINAL EVENING TRADE: $3858 UP 131

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 0/19

EXCHANGE: COMEX

CONTRACT: MARCH 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,284.800000000 USD

INTENT DATE: 03/04/2019 DELIVERY DATE: 03/06/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 6 12

685 C RJ OBRIEN 1

690 C ABN AMRO 1

737 C ADVANTAGE 9 4

800 C MAREX SPEC 3 2

____________________________________________________________________________________________

TOTAL: 19 19

MONTH TO DATE: 263

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A CONSIDERABLE SIZED 4940 CONTRACTS FROM 195,000 DOWN TO 190,060 WITH YESTERDAY’S 14 CENTS LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE ALWAYS WITNESS A CONTRACTION IN TOTAL OI AS WE APPROACH FIRST DAY NOTICE AND IT SEEMS THE CULPRIT IS THE FORCED LIQUIDATION OF SPREADERS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A VERY STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 3843 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 3843 CONTRACTS. WITH THE TRANSFER OF 3843 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3843 EFP CONTRACTS TRANSLATES INTO 19.215 MILLION OZ ACCOMPANYING:

1.THE 14 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.

AND NOW: 25.325 MILLION OZ STANDING IN MARCH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

10,603 CONTRACTS (FOR 3 TRADING DAYS TOTAL 10,603 CONTRACTS) OR 53.015 MILLION OZ: (AVERAGE PER DAY: 3534 CONTRACTS OR 17.67 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 53.015 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 7.57% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 417.88 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4940 WITH THE 14 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD VERY STRONG SIZED EFP ISSUANCE OF 3843 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A CONSIDERABLE SIZED: 1097 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 3843 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 4940 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 14 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.09 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.975 BILLION OZ TO BE EXACT or 139% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 108 NOTICE(S) FOR 540,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/AND NOW MARCH: 25.325 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A STRONG SIZED 6823 CONTRACTS DOWN TO 468,335 WITH THE FALL IN THE COMEX GOLD PRICE/(A LOSS IN PRICE OF $12.50//YESTERDAY’S TRADING). HOWEVER…….

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY STRONG SIZED 10,670 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 10,670 CONTRACTS,JUNE: 0 CONTRACTS DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 468,335. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3847 CONTRACTS: 6,823 OI CONTRACTS DECREASED AT THE COMEX AND 10,670 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 3847 CONTRACTS OR 3847,00= 11.96 TONNES. IT IS IMPORTANT TO NOTE THAT ALTHOUGH WE HAD A CONSIDERABLE DROP IN OPEN INTEREST AT THE COMEX, MANY DID NOT LEAVE THE GOLD ARENA..THEY JUST MORPHED INTO LONDON BASED FORWARDS. YESTERDAY WE HAD A LOSS IN THE PRICE OF GOLD TO THE TUNE OF $12.50.

YESTERDAY, WE HAD 11,397 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 33,259 CONTRACTS OR 3,325,900 OZ OR 103.44 TONNES (3 TRADING DAYS AND THUS AVERAGING: 11,086 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAYS IN TONNES: 103.44 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 103.44/2550 x 100% TONNES = 4.05% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 979.00 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED DECREASE IN OI AT THE COMEX OF 6823 WITH THE LOSS IN PRICING ($12.50) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A CONSIDERABLE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 10,670 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 10,670 EFP CONTRACTS ISSUED, WE HAD A STRONG GAIN OF 5083 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

10,670 CONTRACTS MOVE TO LONDON AND 6823 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE STRONG GAIN IN TOTAL OI EQUATES TO 11.96 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $12.50 IN YESTERDAY’S TRADING AT THE COMEX

we had: 19 notice(s) filed upon for 1900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $1.70 TODAY

THE CROOKS DID IT AGAIN: A WHOPPING 5.87 WITHDRAWAL WITH A TINY PRICE DROP?

GLD INVENTORY 766.59 TONES

INVENTORY RESTS AT 766.59 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 1 CENT IN PRICE TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV..///

/INVENTORY RESTS AT 308,503 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A HUGE SIZED 4940 CONTRACTS from 195,000 DOWN TO 190,060 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 3843 FOR MAY AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3843 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 4940 CONTRACTS TO THE 3843 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE SURPRISINGLY OBTAIN ONLY A SMALL LOSS OF 1097 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 5.485 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY AND NOW 25.325 MILLION OZ FOR MARCH.

RESULT: A HUGE SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 14 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A STRONG SIZED 3843 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. THE LOSS IN OPEN INTEREST CONTRACTS IN SILVER WAS CAUSED BY THE FORCED LIQUIDATION OF SPREADERS…IT HAD NO EFFECT ON PRICE..TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

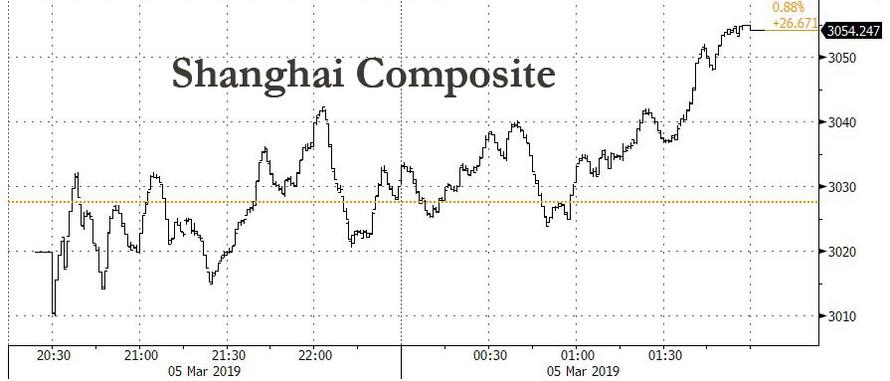

SHANGHAI CLOSED UP 26.67 POINTS OR 0.88% //Hang Sang CLOSED UP 2.84 POINTS OR 0.01% /The Nikkei closed UP 96.76 POINTS OR 0.44%/ Australia’s all ordinaires CLOSED DOWN 0.34%

/Chinese yuan (ONSHORE) closed UP at 6.7020 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 56.73 dollars per barrel for WTI and 65.85 for Brent. Stocks in Europe OPENED RED EXCEPT LONDON//.

ONSHORE YUAN CLOSED UP // LAST AT 6.7020 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7047: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA

b) REPORT ON JAPAN

3 C/ CHINA

i) CHINA/

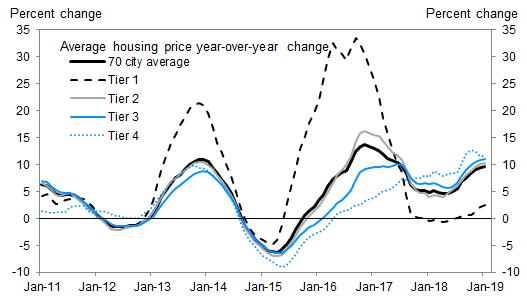

Important: Housing is where China keeps all of its wealth..a drop in home prices will no doubt cripple their economy. China’s largest property developwer is now selling all homes with a 10% discount.

(zerohedge)

iii)ChinaWith their downturn, we now witness many Chinese tech companies fire thousands of employees.

( zerohedge)

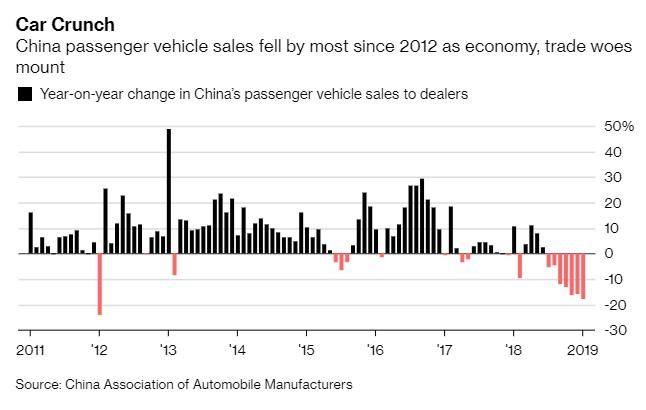

iv)Here is another sign of problems inside China: Chinese car dealers are slashing prices

( zerohedge)

4/EUROPEAN AFFAIRS

EUROPE/RUSSIA

More European banks are being collared in this widening Russian money laundering scandal

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

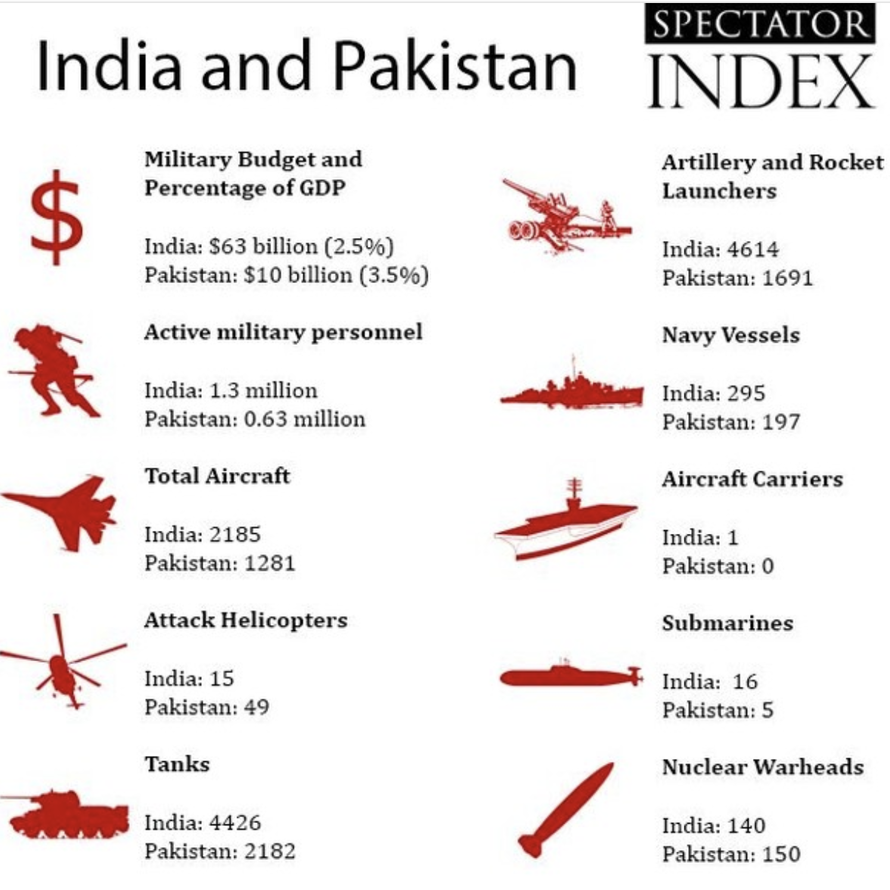

INDIA/PAKISTAN

After Pakistan shoots down last week an Indian fighter jet, it now intercepts an Indian submarine as the border conflict continues to rage on.

( zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data

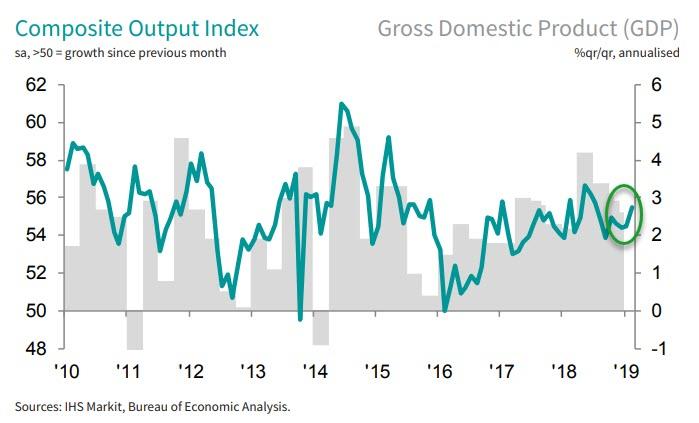

a)We now have our “fake” ISM numbers. Do not pay any attention to them. They showed USA service surging while Manufacturing slumping.Garbage numbers in this soft data report

( zerohedge)

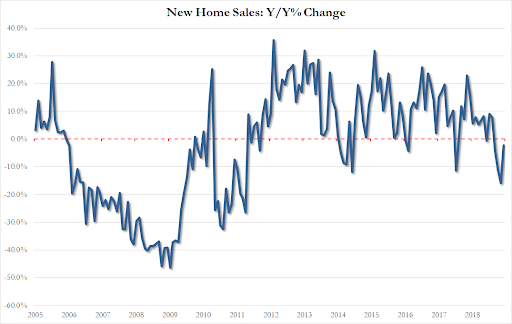

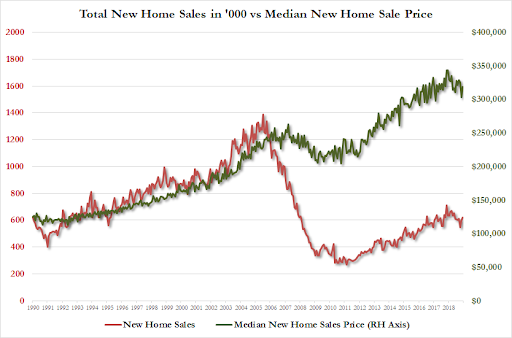

b)This data entry is far more important than the ISM numbers. It is a hard data and again new home sales falter and this is the longest streak of lower numbers since 2011

(courtesy zerohedge)

iv)SWAMP STORIES

a)Funny! Steel cancels his appearance at a friendly forum as no doubt he was spooked by Cohen’s testimony which basically destroyed his dossier allegation

(courtesy zerohedge))

b)The Democrats are planning a resolution condemning this nut care Omar.

(courtesy zerohedge)

end

Let us head over to the comex:

AFTER MARCH, WE HAVE THE NON ACTIVE DELIVERY MONTH OF APRIL. HERE: APRIL RISES TO 796 CONTRACTS FOR A GAIN OF 24 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI FELL BY 5193 CONTRACTS DOWN TO 139,986 CONTRACTS.

i) out of Delaware: 10,375.529 oz

Should 175 Million Lottery Winners Invest In Gold?

Money Doctor John Lowe: Invest In Gold In 2019

By John Lowe, The Money Doctor via RTE

Diamonds may have the edge when it comes to a girl’s best friend but as the world becomes more volatile year by year, investing in the yellow metal is de rigueur and a prudent strategy in a balanced portfolio.

They say 10% of your wealth should be in precious metals.

‘Dream come true’ – Family syndicate wins €175m EuroMillions jackpot

‘Dream come true’ – Family syndicate wins €175m EuroMillions jackpot

Wonder will this apply to the Euromillions 6 and their €30 million each? John Lowe the Money Doctor gives the background.

If the so-called ‘gold bugs’ – investors who believe passionately in the long-term value of buying gold – are right, then this could be a good time to add a little glitter to your portfolio. Over the last few years, we have seen massive swings in the price of gold from its all-time 1980 high then of US$850 per troy ounce – in today’s money, about $2,500 – to its current price of c. US$1305 ( c. €1,154.87) per troy ounce.

Bear in mind the gold price in 2011 stood at its highest ever at US$1913 per troy ounce – slightly heavier than avoirdupois ounces – and was expected at the time to go even higher. It didn’t but with such recent global uncertainty – gold is now a barometer of volatility in the world – and its effect on the financial markets plus a natural desire to stay solvent and have an asset that is easily bartered, gold could still be the very commodity to take off. Self administered pensions (SSAPs) are ideal for this investment, too.

There are three sound reasons to believe that prices will rise:

Firstly, the growing economies of Asia and the Middle East have resulted in a huge surge in demand – especially for gold jewellery. For proof one need look no further than global gold jewellery sales, which increased at a very steady pace over the last few years.

Secondly, a rising number of private investors all over the world have been putting some or all of their savings into gold as a hedge against economic or political instability and, as in maybe the case of Syria and ISIS war.

When investors feel the future is uncertain (as many appear to at the moment) demand for gold always surges. This is doubtless in no small part due to the fact that the price of gold tends to move in the opposite direction to virtually all other conventional asset classes – making it ideal when investors wish to diversify.

Thirdly, the mining industry can’t keep up with demand. Figures show that in excess of 4,000 tonnes of gold were purchased, but only 2,700 tonnes were mined in 2011 and 2,860 tonnes in 2014 – 260 tonnes more than the previous highest peak in 2001.

What’s more, production is falling by an average of 4% a year and it will take the industry anything up to ten years to increase supply by the required volume. In the past, when demand outstripped supply, the shortfall was met by many of the world’s central banks. No longer. Countries, which had been disposing of their gold reserves, have slowed down sales or even stopped selling altogether. Many central banks, notably those of Russia, Iran and China, are actually now buying bullion.

Although I believe that gold prices are likely to carry on moving upward after the recent drops, I would only suggest buying if you already have a range of other investments including shares, bonds and property.

I would recommend various ways of investing in gold:

Gold bullion

Gold bullion coins and bars weighing nearly 2,000 troy ounces (over 60 kilos) and worth more than €2m were recently transferred in recent weeks into the country from the UK. This is believed to be the largest legitimate movement of gold bullion into Ireland in decades.

Brexit, of course, is helping but the leading bullion dealer in Ireland, GoldCore, said it is seeing a growing preference amongst Irish investors to store their gold domestically here rather than Perth, Zurich, Singapore, Hong Kong, Singapore and especially London.

Gold held in the company’s Dublin vaults is a fraction of GoldCore’s client holdings in other jurisdictions, and has already surpassed Hong Kong as a favoured jurisdiction for storing gold with Goldcore clients. Zurich remains the favourite location with client bullion holdings there worth nearly €40 million. Zurich is followed by Singapore, then London, Dublin and Hong Kong.

Perth Mint Gold Certificate programme

The bullion is held in Perth Mint, the only mint in the world guaranteed by a AAA-rated government (the Western Australian government) The fee is 2% to 3.9% depending on the amount bought and 1.5% when you sell. Minimum investment is €7,000 but it is safe in every respect.

Pensions

Incidentally, if you are planning to invest in gold it is worth noting that it can be held in self-administered pension schemes (SSAPs or Self Directed Trusts for company owners, directors and senior executives), which could mean some tasty tax savings depending on your circumstances.

Conclusion

Chess grandmaster, Professor of Economics in Harvard and former IMF Chief Economist, Ken Rogoff advises that gold is an “extremely low risk asset” and “investing in and owning gold as a hedge will become more important as it will have enormous value in a cashless society.”

Courtesy of John Lowe, The Money Doctor and full article on RTE Lifestyle

News and Commentary

Gold hits two-week low as upbeat U.S. data lifts dollar (Reuters.com)

Romania Ruling Party Battles Bank Over Gold Reserves, Return 95% back (BalkanInsight.com)

Growing China downdraft chills Asia factory activity (Reuters.com)

Oil climbs amid OPEC-led supply cuts, but economic weakness drags (Reuters.com)

Stocks Post Year’s First 3-Day Slide; Dollar Gains: Markets Wrap (Bloomberg.com)

Gold’s Four-Month Winning Streak on the Line Today (GoldCore in Barrons) (Barrons.com)

Gold – here’s why it just might be different this time (MoneyWeek.com)

Trump Returns Home to Face the Mueller Music (Bloomberg.com)

Home Prices in Sydney & Melbourne Spiral Down, Bust Spreads (WolfStreet.com)

Murphy and Hemke on Silver and Palladium Manipulation (Youtube.com)

Stockman on Peak Trump, The Undrainable Swamp & the Fantasy of MAGA (Youtube.com)

Gold Prices (LBMA PM)

01 Mar: USD 1,309.95, GBP 989.27 & EUR 1,152.23 per ounce

28 Feb: USD 1,325.45, GBP 996.21 & EUR 1,162.82 per ounce

27 Feb: USD 1,326.45, GBP 998.02 & EUR 1,164.09 per ounce

26 Feb: USD 1,327.55, GBP 1005.79 & EUR 1,168.11 per ounce

25 Feb: USD 1,329.15, GBP 1016.80 & EUR 1,170.32 per ounce

22 Feb: USD 1,322.25, GBP 1016.15 & EUR 1,166.49 per ounce

Silver Prices (LBMA)

01 Mar: USD 15.56, GBP 11.75 & EUR 13.67 per ounce

28 Feb: USD 15.81, GBP 11.89 & EUR 13.85 per ounce

27 Feb: USD 15.86, GBP 11.91 & EUR 13.92 per ounce

26 Feb: USD 15.83, GBP 11.98 & EUR 13.93 per ounce

25 Feb: USD 15.95, GBP 12.19 & EUR 14.04 per ounce

22 Feb: USD 15.87, GBP 12.20 & EUR 14.00 per ounce

Recent Market Updates

– “Gold Is A Global Thermometer Of Risk” – CEO Q+A: Stephen Flood, GoldCore

– U.S. Mint Suspends Silver Bullion Coin Sales After Sales Double In February

– MMT: Modern Monetary Madness Will Lead To Higher Taxes and Inflation

– Gold Broker Has Good Sense and Prefers Gold To All That Glitters (The Times)

– The Utterly Unbelievable Scale of U.S. Debt Right Now

– The Best Time In History To Buy GOLD

– Jim Willie Interviews Mark O’Byrne – Prepare Now For Global Financial Crisis II

– 7 Major Flaws Of The Global Financial System – Excellent Infographic

– The Case for Gold In 2019 – The Economist

– Invest In Gold As a Hedge In Cashless Society – Ex IMF Rogoff

Newmont’s board rejects Barrick’s hostile offer

Submitted by cpowell on Mon, 2019-03-04 14:58. Section: Daily Dispatches

By Danielle Bochove and Ed Hammond

Bloomberg News

Monday, March 4, 2019

Newmont Mining Corp. rejected Barrick Gold Corp.’s $17.8 billion unsolicited takeover bid, a deal that would’ve created the world’s largest gold producer.

The board unanimously rejected the proposal, saying it would not be better than Newmont’s previously announced takeover of Goldcorp Inc., the Colorado-based company said in a statement today. Instead, Newmont submitted a joint venture proposal to Barrick that would encompass the two companies’ Nevada operations.

…

Newmont had raised serious doubts about Toronto-based Barrick’s proposal — a hostile all-share no-premium bid — from the day it was announced Feb. 25. Newmont said its previously announced agreement to take over Goldcorp offered better benefits, and Chief Executive Officer Gary Goldberg called Barrick’s takeover offer “desperate” and “bizarre.”

“The combination with Goldcorp is significantly more accretive to Newmont’s shareholders on all relevant metrics compared to Barrick’s proposal, even when factoring in Barrick’s own synergy estimates,” Goldberg said in the statement. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-03-04/newmont-is-said-to-re…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Good morning Bill/Harvey, (from Africa),

Consistency is a very valuable quality in these days of so much change. Let us give an accolade to the LBMA and BOE. The total London vault gold holdings represent consistency personified. The public dissemination of loco London LBMA vault gold holdings started as at 31st July 2016 .The total was 234 million ounces and the BOE holding included in this figure was 68% at 159 million ounces. Fast forward to 30th November 2018 (the LBMA considers it prudent to disclose data 90 days in arrears) and the total is disclosed at 239 million ounces (being 7,434, tonnes) and the BOE portion is again 68% at 162 million ounces. I have not looked at the exchange for physical volumes for a while, but I looked just now and the YTD 2019 figure is 945 tonnes to be added to the total for 2018 of 7,310 tonnes (combined total 8,255 tonnes). The figures are an insanity and only two explanations seem feasible. The EFP mechanism is merely an opaque netting- off of collusive criminal manipulation between collaborating counter parties whereby short and long contracts disappear from sight to prevent the open interest figure going stratospheric, or else China is the counter party receiving a handsome reward by way of unrecorded fees in order to be persuaded to delay the introduction of physical gold into the monetary system.

China is apparently happy to concentrate for the time being on the roll out of the One Belt, One Road series of projects and I read that the payment mechanism for much of this capital development is achieved via the release of its USA Bonds, which still retain value with the USD index circa 96-97. Additionally I am sure that some of these bonds are utilized in settling the cost of the importation of the reported figures for West to East physical gold exports. John Bolton desperately needs another war so why would the Sino/Russo alliance do anything provocative? The cancer within the USA is metastasizing at a visible rate on a daily basis as society atrophies into complete oblivion. I can understand why the Democrats are so opposed to border security since they need to enlist the support of the influx of refugees in order to gain back control and start the distribution of free stuff; whilst the constituency for this free stuff will expand to (say) four hundred million, that is not really a cost at all-you must understand that free stuff has no cost-that is why it is such a good idea. I do not, however, understand why ‘’abortion after birth’’ has been elevated to a principal war cry-maybe stevequale.com provides the answer as the role out of pure evil is chronicled scores of times every day. What are the odds of USA stumbling in a reasonably orderly fashion towards free and credible elections next year? China, Russia and Iran and others need merely to accumulate the last dribblings of physical gold available and just wait. But then, according to Dane Wigington, it is game set and match against humanity within the next decade so things will get more than interesting in the coming days.

Regards

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7020/

//OFFSHORE YUAN: 6.7047 /shanghai bourse CLOSED UP 26.67 POINTS OR 0.88% /

HANG SANG CLOSED UP 2.84 POINTS OR 0.01%

2. Nikkei closed DOWN 96.76 POINTS OR 0.44%

3. Europe stocks OPENED RED

/USA dollar index RISES TO 96.68/Euro FALLS TO 1.1331

3b Japan 10 year bond yield: RISES TO. +.01/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.96/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 56.73 and Brent: 65.83

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP /OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.18%/Italian 10 yr bond yield UP to 2.71% /SPAIN 10 YR BOND YIELD UP TO 1.16%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.53: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.70

3k Gold at $1285.35 silver at:15.09 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 7/100 in roubles/dollar) 65.83

3m oil into the 56 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.96 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0013 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1343 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.17%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.74% early this morning. Thirty year rate at 3.10%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3804

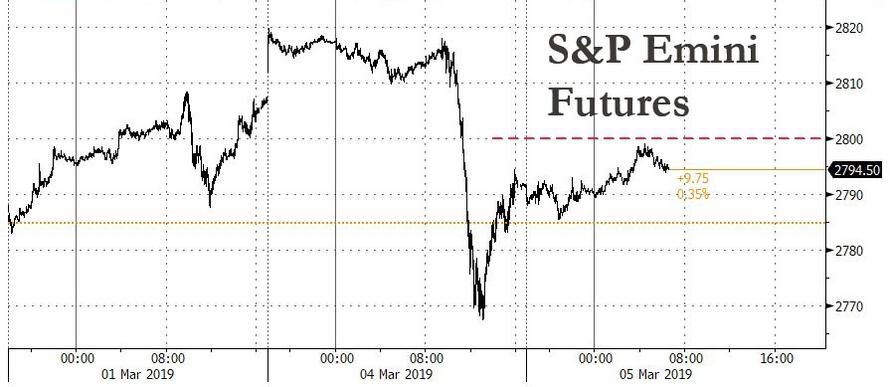

Global Rally Fizzles, S&P Futures Capped At 2,800

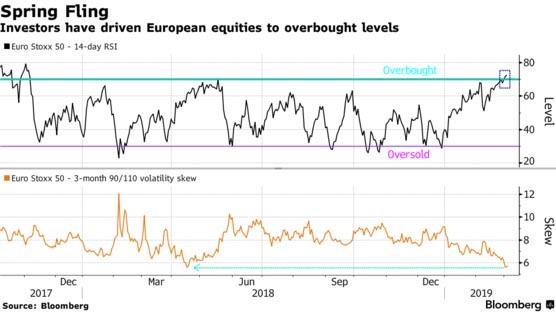

European stocks and US futures were higher on Tuesday following a mixed session in Asia, although traders faded earlier euphoria and the Stoxx 600 was little changed, erasing a gain of as much as 0.3% as traders awaited more details on a potential US-China trade deal, after earlier in the day China pledged more stimulus to stabilize slowing growth when it predicted its 2019 GDP would shrink to “6-6.5%.”

Europe’s Stoxx 600 Index inched fractionally higher, led by gains in telecommunications shares, pushing the broader index deeper into overbought territory…

… with traders pleasantly surprised for once by stronger European Services PMIs across the board, suggesting Europe’s economic slowdown may have found the reverse gear:

- EU Markit Services Final PMI (Feb) 52.8 vs. Exp. 52.3 (Prev. 52.3)

- Italian Markit/IHS Services PMI (Feb) 50.4 vs. Exp. 49.4 (Prev. 49.7)

- French Markit Services PMI (Feb) 50.2 vs. Exp. 49.8 (Prev. 49.8)

- UK Markit/CIPS Services PMI (Feb) 51.3 vs. Exp. 49.9 (Prev. 50.1)

Tobacco, healthcare, consumer staples, and other safe havens led the gains amid broader gloom about the global economy. British American Tobacco, Anheuser Busch and Unilever were up between 1.2% and 2.1%. Among individual movers, Evonik shares were close to four-month highs after the German chemicals group reported a slight rise in profits thanks to its coating additives and engineering plastics division. Vodafone added 2.3 percent after announcing plans to issue 4 billion euros ($4.5 billion) worth of convertible bonds to help finance its takeover of some Liberty assets. Elsewhere in the UK, British product testing company Intertek was the biggest faller in London, with a dealer attributing the drop to profit taking after largely in line full-year results. Luxury goods companies Richemont and Moncler were each down more than 3 percent after downgrades.

Meanwhile, in the US. S&P index futures traded higher following a lackluster start, although off their highs as the critical resistance at 2,800 is once again proving a solid barrier for the bulls.

Futures rebounded after yesterday’s surprising selloff, which took place despite the latest bout of “trade talk optimism”, and after stocks in Europe and Asia were buoyed on Monday by news that the world’s two-largest economies were close to a trade deal, investors are now hungry for concrete details before they push a global equities rally further. Meanwhile, trade and slowing growth are on the agenda as China’s most powerful officials gather in Beijing, while investors will get the latest read on the U.S. economy with the monthly jobs report Friday.

Earlier, during the Asian session shares declined in Japan, Korea and Australia and posted modest gains; the Shanghai Comp. nursed some opening losses following the release of the NPC work report which pledged to expand infrastructure investments and cut manufacturing VAT to 13% from 16%, whilst transport and construction VAT is to be reduced to 9% from 10%. Although the release of a dismal Caixin services PMI briefly dented the index, Chinese stocks closed at session highs, up 0.8%. The unchanged Hang Seng conformed to the overall risk-averse tone with its heavy-weight financial sector as the marked underperformer.

As part of the annual work report to the National People’s Congress, China lowered its 2019 GDP growth target to the range of 6.0-6.5% from “around 6.5%” and maintained CPI target at 3.0%, both as expected. Budget deficit for 2019 was set at 2.8% vs. 2.6% in 2018. China stated that fiscal policy to be proactive and monetary policy to be prudent will not resort to flood-like stimulus, whilst also saying it will keep the Yuan basically stable at reasonable equilibrium and is to increase the flexibility of the Yuan exchange rate while keeping liquidity reasonably ample. China will expand infrastructure investments in 2019 and plans to cut manufacturing VAT to 13% from 16%, as touted, VAT for transport and construction sectors to be reduced to 9% from prior 10%. China will make economic policy for forward-looking, targeted and effective whilst maintaining pace and strength in risk prevention, and higher budget deficit ration will leave more policy room for resolving potential risks. China will also step up targeted RRR cuts for smaller and medium-sized banks to support private and smaller firms. Growth in M2 Money Supply and social financial to be in-line with nominal GDP growth and basically the same as in 2018. China is to implement consensus reached between US and Chinese leaders in Argentina, but said it needs to brace for a tough economic battle.

While China’s GDP cut underlined the strain that has slowed growth and roiled global markets, stimulus steps reassured investors that Beijing was serious about steadying the economy. “I think we all saw it coming. The growth trend was going to be cut and they’re saying the right things about stimulus. They have plenty of policy levers to pull if needed,” said Peel Hunt economics and strategy research analyst Ian Williams.

Still, European autos and suppliers, which rely on Chinese demand, were under pressure, with Continental and Daimler among the biggest fallers in Frankfurt.

In FX, the Bloomberg Dollar Spot Index headed for a fifth day of gains, with the greenback trading stronger versus most G-10 peers. China cutting its growth target kept high-beta currencies under pressure, while the euro failed to gain momentum after PMI data from the currency bloc beat expectations. Loonie drops to its lowest since Jan. 25 amid a deepening crisis in Justin Trudeau’s government. The yen dipped while the Australian dollar recovered somewhat after falling earlier to a three-week low, after the central bank left its benchmark interest rate unchanged.

In other overnight news, President Trump plans to terminate India and Turkey as Generalised System of Preferences beneficiaries. The move comes as India has not assured the US that it will provide “equitable and reasonable” market access and Turkey is now “sufficiently economically developed”; according to US Trade officials. Indian Trade Ministry Official, in response, said US and India were able to work out an extensive and reasonable package which covered almost all US concerns, although the advantages under the US GSP are “minimal and moderate”.

In the latest Brexit tragicomedy news, UK PM May has been warned that she must whip her MPs to keep a no-deal Brexit on the table, whilst Senior Eurosceptics are convinced PM May will lose the vote on her Brexit deal and they do not expect Attorney General Cox to win concessions on the Northern Irish backstop. May is also reportedly considering a parliamentary vote on the UK’s future relationship with the EU, as per demands from Labour MPs. A source close to a cabinet minister also stated that there seemed to be “no chance” that her deal would pass next week. Meanwhile, the FT reported that UK Trade Secretary Fox’s department has cancelled its regular meetings with business after the details of a prior meeting were leaked to the media.

In other news, Treasury Secretary Mnuchin has urged Congress to lift the debt limit as soon as possible and added that the new debt issuance suspension will be from March 4th to June 5th, although the Treasury can easily extend debt suspension measures into September and perhaps October

Elsewhere, West Texas Intermediate crude oil ticked lower though remained above the $56 a barrel level. Brent (+0.2%) and WTI (+0.1%) prices are firmer although they were initially weighed on by the deteriorating risk tone, and Chinese Caixin Services PMI coming in below expectations at 51.1 vs. Exp. 53.5; with the complex also affected by dollar strength. Elsewhere, the El Sharara oil field has reopened at a current output of 30k BPD, far below the field’s capacity of around 300k BPD; although NOC has stated that a return to regular output is expected in the next few days. Looking ahead we have API Weekly release later in the session, which last week saw crude stocks fall by -4.2mln.

Gold (-0.1%) is relatively unchanged with the metal affected by both the stronger dollar and the deterioration in the risk tone seen overnight; Gold futures slid for a seventh straight session, the longest slump since March 2017.

Market Snapshot

- S&P 500 futures up 0.2% to 2,796.50

- STOXX Europe 600 up 0.2% to 375.70

- MXAP down 0.3% to 159.41

- MXAPJ down 0.06% to 525.58

- Nikkei down 0.4% to 21,726.28

- Topix down 0.5% to 1,619.23

- Hang Seng Index up 0.01% to 28,961.60

- Shanghai Composite up 0.9% to 3,054.25

- Sensex up 1% to 36,410.29

- Australia S&P/ASX 200 down 0.3% to 6,199.29

- Kospi down 0.5% to 2,179.23

- German 10Y yield rose 2.0 bps to 0.178%

- Euro down 0.1% to $1.1329

- Brent Futures down 0.6% to $65.30/bbl

- Italian 10Y yield rose 0.5 bps to 2.38%

- Spanish 10Y yield fell 0.3 bps to 1.169%

- Brent Futures down 0.6% to $65.30/bbl

- Gold spot down 0.2% to $1,284.73

- U.S. Dollar Index up 0.04% to 96.72

Top Overnight News

- China’s GDP growth target in Premier Li Keqiang’s annual work report to the National People’s Congress was set at a range of 6-6.5% for 2019, compared with last year’s “about” 6.5% goal

- Services expanded across the 19-nation euro area, bolstered by gains in Germany, Ireland and Spain, according to IHS Markit. That pushed a composite Purchasing Managers’ Index to 51.9, the highest in three months. An initial reading was for an increase to 51.4

- The BOE is launching a new liquidity facility in euros in the final few weeks before the scheduled date for Britain to leave the European Union

- Bank of Japan board members are likely to discuss a possible downgrade of their assessments of industrial production, exports and overseas economies when they meet to set policy next week, according to people familiar with the matter

- The U.S. is giving American exporters a sizable tax break on the goods and services they sell overseas. But the benefit might not be enough to convince Corporate America to expand its U.S. operations beyond what it was already planning

- Australia is no stranger to heated debate about the direction of its housing market. This week, that spread to mortgage debt too. Suncorp Group Ltd. said Monday that arrears on one parcel of securities are creeping past the level that triggers a change in how principal repayments are carved up

Asian stocks traded lacklustre following a disappointing lead from Wall Street after the Dow slipped 0.8%, weighed on by Boeing and Goldman Sachs shares, whilst the S&P shed 0.4% amid underperformance in healthcare names. Both indices marked their worst turnaround since early February. ASX 200 (-0.3%) extended losses from the open amid underperformance in the Consumer Discretionary and Material sectors, whilst Nikkei 225 (-0.4%) was weighed on by commodity exposed stocks. Elsewhere, Shanghai Comp. (+0.8%) nursed some opening losses following the release of the NPC work report which pledged to expand infrastructure investments and cut manufacturing VAT to 13% from 16%, whilst transport and construction VAT is to be reduced to 9% from 10%, although the release of dismal Caixin services PMI briefly dented the index. Finally, Hang Seng (U/C) conformed to the overall risk-averse tone with its heavy-weight financial sector as the marked underperformer.

Top Asian News

- BOJ Is Said to Discuss Downgrading Its Views of Output, Exports

- What Analysts Are Saying About New Philippine Central Bank Head

- Mandiri Said to Eye Deal for $2 Billion StanChart- Backed Rival

- Tencent Jumps to 6-Month High on Optimism Over Key Game

Major European indices are moving towards negative territory, after starting the session somewhat firmer [Euro Stoxx 50 U/C] moving more in-line with the relatively poor performance seen overnight in Asia which was dictated largely by a disappointing lead from Wall Street. Sectors are mixed, with some slight underperformance in consumer discretionaries; the sector is weighed on by poor performance in Daimler (-0.8%), which represents around 7% of the sectors weighting, who are in the red after executives at the Co. stated they may have to lift prices to pass on potential US tariffs. Other notable movers include, Evonik (+3.8%) who are at the top of the Stoxx 600 after earnings where they beat on Q4 revenue. At the other end of the Stoxx 600, and weighed on by broker moves, are Altice (-9.1%) as are Richemont (-3.2%), who were both downgraded at Barclays and BOFA Merrill Lynch respectively. Elsewhere, Vodafone (+1.9%) are higher after after the Co. state they intend to raise around EUR 4bln through sterling denominated MCBS and there is the potential for a share buyback as part of this. Separately, British American Tobacco (+1.0%) are higher as the Co. state there will be no impact from the Quebec charge to their ratio of adj. net debt to adj. EBITDA.

Top European News

- Euro Area’s Resilient Services Sector Puts Mild Gloss on Economy

- BOE Starts Euro Lending Facility to Cushion Brexit Risks

- Italy’s State Lender May Back Elliott at Tel Italia Vote: Stampa

In FX, the DXY is off best levels, but the index continues to edge higher and just surpassed another chart resistance level (96.784) ahead of the next big figure on its way to a 96.815 high. The Greenback is still benefiting from weakness in rival currencies to an extent if not large part, or by default as a combination of negative/bearish factors inflict damage elsewhere (ranging from weaker macro fundamentals relative to the US, geopolitical instability/uncertainty and Central Bank policies aligning to Fed patience or even turning more dovish in certain cases, to name just a few). The DXY is now holding around 96.750 and well above Monday’s 96.331 low.

- NZD/CAD – The 2 biggest G10 losers, with the Kiwi slipping below 0.6800 amidst a broader fall-out in risk currencies following a considerably weaker than forecast Chinese Caixin services PMI and confirmation that the NPC has downgraded its GDP sights to 6-6.5% from 6.5% previously. Meanwhile, the Loonie has extended recent losses to fresh multi-month lows circa 1.3350 vs its US counterpart with the added weight of heightened strains between Canada and China, plus another downturn in crude prices.

- EUR/AUD/JPY/CHF – Also weaker vs Usd, as the single currency fails to derive much/any real support from surprise beats and upward tweaks to the Eurozone services PMIs, including the Italian headline that rebounded over 50.0 and was supplemented by an unexpected Q4 GDP revision to -0.1% q/q from -0.2%. Eur/Usd is hovering just above yesterday’s 1.1309 base and Fib support at 1.1305, but looks technically weak after breaching 1.1350 and key chart levels not far above. Similarly, the Aussie is struggling to mount a concerted recovery from recent lows towards 0.7100 after a dovish RBA policy statement on balance and yet more poor data overnight (Q4 net exports), and Aud/Usd could become increasingly drawn to a hefty option expiry down at 0.7050 as a result (1.6 bn). Meanwhile, the Yen and Franc continue to trade defensively on constructive US-China trade deal vibes, with Usd/Jpy edging back up to 112.00 and Usd/Chf straddling parity. Note also, decent option expiries in Usd/Jpy may impact into the NY cut, with 1 bn running off between 111.80-90 and 1.9 bn at the 112.00 strike.

- GBP/SEK – Relative outperformers on better than expected UK and Swedish services PMIs vs other more downbeat economic indicators. However, Cable remains capped ahead of 1.3200 and the 100 WMA (1.3207), with the 10 DMA (1.3161) and a Fib (1.3130) now flanking the pair as it pivots 1.3150 awaiting any further Brexit developments. Eur/Sek has retreated through 10.6000 again and retesting bids around 10.5500.

- EM – More angst for the Try and Inr after the US pulled the GSP plug from both nations, with the Lira attempting to pare losses and stay above 5.4000, but the Rupee staging a firmer recovery from almost 71.0000 at one stage as India’s Trade Ministry downplayed the impact of the trade pact being terminated.

In commodities, Brent (+0.2%) and WTI (+0.1%) prices are firmer although they were initially weighed on by the deteriorating risk tone, and Chinese Caixin Services PMI coming in below expectations at 51.1 vs. Exp. 53.5; with the complex also affected by dollar strength. Elsewhere, the El Sharara oil field has reopened at a current output of 30k BPD, far below the field’s capacity of around 300k BPD; although NOC has stated that a return to regular output is expected in the next few days. Looking ahead we have API Weekly release later in the session, which last week saw crude stocks fall by -4.2mln. Gold (-0.1%) is relatively unchanged with the metal affected by both the stronger dollar and the deterioration in the risk tone seen overnight. Elsewhere, metals were weighed on by China lowering its GDP growth target to 6.0-6.5% from the prior of around 6.5%. Separately, the amount of copper available in LME system, fell to the lowest level since 2005 of 21.6k tonnes.

Looking at the day ahead, we’ll get the final PMIs as well as the February ISM non-manufacturing (+0.6pts to 57.3 expected) and December new home sales (-8.7% mom expected). Away from that we’re due to hear from Italy’s finance minister Tria this morning, before the BoE’s Carney speaks this afternoon before the House of Lord’s Economic Affairs Committee. The Fed’s Rosengren is also set to speak today.

US Event Calendar

- 9:45am: Markit US Services PMI, est. 56.2, prior 56.2; Markit US Composite PMI, prior 55.8

- 10am: ISM Non-Manufacturing Index, est. 57.4, prior 56.7

- 10am: New Home Sales, est. 600,000, prior 657,000; New Home Sales MoM, est. -8.68%, prior 16.9%

- 2pm: Monthly Budget Statement, est. $12.0b, prior $13.5b deficit

Central Banks

- 8am: Fed’s Rosengren Speaks on Current Economic Outlook

- 9:30am: Fed’s Kashkari Testifies Before Minnesota Senate Finance Panel

- 11:30am: Fed’s Barkin Speaks at the Rural Economy

DB’s Jim Reid concludes the overnight wrap

The flu-inspired daze continues. I can’t remember a four day period where I’ve slept as much as this one, albeit punctuated at regular intervals with choking coughing fits. If I make it into the city today please give me a wide berth for the sake of you and your family.

Markets seemed like they were suddenly struck down by a nasty ailment yesterday as the early optimism sparked by Asia this time yesterday reversed spectacularly by US lunchtime. Despite opening +0.47% higher, the S&P 500 ended up closing -0.39% lower, albeit well off the intraday lows of -1.29%. The DOW (-0.79%) and NASDAQ (-0.23%) had similar trajectories. There was not a clear macro catalyst, but it seemed like political tensions played a prominent role in the selloff, as headlines (per Bloomberg) surfaced about House Democrats deepening and broadening their investigations of the President. The House Judiciary Committee sent requests for documents to 81 entities, including the President’s son, his former CFO, and his lawyer. The VIX index mirrored the move in cash equities, rising as much as +3.1pts and on track for its sharpest rise since Christmas Eve before moderating in the afternoon to end end +1.06pts higher at 14.63.

Further weighing on sentiment was negative news in the healthcare sector, with the S&P 500 healthcare index dropping -1.34%. Despite making up only 14% of the S&P 500 by market cap, it drove over half of yesterday’s declines. Drugmaker Eli Lilly (-1.07%) announced that it would offer its insulin product at half price, possibly in response to political pressure over high pharmaceutical prices. The managed care sector (-4.41%) had its worst day since 2015, partially on worries over political risks and partially due to a positioning unwind. Data showed that the largest US-traded healthcare ETF saw outflows of -$855million last week, its most since 2015 as well.

This morning the focus has quickly turned to China’s National People’s Congress where the early headlines (per Bloomberg) are suggesting that China will resort to moderate fiscal stimuli to support slowing growth as China announced a fiscal deficit target of 2.8% of GDP in 2019 versus 2.6% in 2018 while pledging a “noticeable decrease” in the tax burdens for major industries. Premier Li Keqiang’s annual work report announced total tax and social security fees cuts of CNY 2tn ($ 298bn). China is now targeting GDP growth in the range of 6%-6.5% in 2019 (vs. last year’s goal of c. 6.5%), marking a shift from previous practice of using a point figure. The work report also indicated that further cuts to the required reserves ratio for smaller banks are planned. At first glance much of the above has been expected so no major surprises here. Chinese equity markets are seeing small gains this morning though with the Shanghai Comp (+0.11%) and Shenzhen Comp (+0.75%) both up following the news on tax breaks and also on the story yesterday that China is planning a three percentage point cut to the top VAT bracket – news that was also anticipated. We should note that we’ve had the remaining February Caixin PMIs in China too this morning with the composite reading at 50.7 (vs. 50.9 last month) and services PMI decelerating to 51.1 (vs. 53.5 expected). So a bit disappointing.

Sentiment is not as rosy across the remainder of Asia with markets largely following Wall Street’s lead from yesterday. The Nikkei (-0.46%), Hang Seng (-0.03%) and Kospi (-0.55%) are all down. Not helping sentiment overnight was news from China’s Commerce Minister Zhong Shan that it will take more efforts by China and the US to reach an agreement on trade. He suggested talks were difficult due to differences in culture and stages of development and that both sides need to meet each other half way to get a deal. So a slightly more cautious view than that seen of late. Elsewhere, futures on the S&P 500 are largely trading flat (-0.03%) while all G-10 currencies are trading weak (down in the range of -0.1% to -0.4%) this morning. In terms of other data releases, Japan’s February composite PMI came at 50.7 (vs. 50.9 last month) with the services PMI reading at 52.3 (vs. 51.6 last month).

Back to markets yesterday and early weakness for the Greenback post the Trump comments over the weekend quickly reversed after Europe walked in and then later once the US session kicked off. The Dollar index eventually ended +0.09% while EM FX was flat. Meanwhile the one laggard in the rates’ market yesterday was Greek bonds where 10y yields rose +3.0bps to 3.65% after the news that Greece had mandated six banks for a new 10y bond. The nation did do a 10y deal in 2017 albeit as part of a bond exchange. However prior to that the last syndicated deal was in 2010. It’s amazing that just 3 years ago Greek 10y bonds were trading around 10%.

Italian yields also underperformed a touch, with 10-year BTP yields up +0.5bps while bunds rallied -2.6bps. Attention focused on Bank of Italy Governor Visco’s comments ahead of this Thursday’s ECB meeting, in which he said that the “ECB’s money cannot be used to buy government bonds.” This suggests that any new TLTRO facilities could come with additional strings attached, to discourage banks from using cheap lending to finance carry trades, and to instead encourage lending to the corporate sector. Italian bank stocks ended the session flat.

In other central banks speak, Bank of Japan Governor Kuroda said that it will be difficult to reach the 2% inflation target in the current outlook period, but that factors slowing an acceleration in inflation will fade moving forward. This was interpreted as a signal that additional easing is not imminent, despite a deterioration in economic data, and Japanese government yields rose above 0.0% for the first time since January. This helped the yen appreciate +0.13% versus the dollar.

As for Brexit, there wasn’t a great deal of new news to report yesterday. Reuters did report that the Irish Prime Minister was supposedly willing to offer clarifications and reassurances to get a deal over the line. Today the UK’s Cox and Barclay are due to travel to Brussels so we may well get further headlines as the day progresses. While we’re on the UK it’s worth flagging a report from our UK economists yesterday on the domestic housing market. The headline conclusion is that underlying fundamentals remain strong, but Brexit, tighter macro prudential policy and tax changes have weighed on prices lately. That being said, they expect the housing market to start to recover from later this year – assuming ratification of a Brexit deal – so it’s not all doom and gloom. More in their report here .

On the data front, US construction spending fell -0.6% mom in December versus expectations for a 0.1% improvement and down from a 0.8% expansion previously. Our economists viewed the data as distorted by California wildfires, and they still expect a rebound in housing sector activity over the next few months as lower interest rates feed through to mortgage activity. An index of US homebuilder stocks rallied +2.43% yesterday. In the UK, the construction PMI printed at 49.5 from 50.6, dipping into contractionary territory for the first time in a year as the Brexit uncertainty weighs on activity.

Looking at the day ahead, this morning it’s all eyes on the remaining February services and composite PMIs in Europe including a first look at the data for the non-core and UK. We’ll also get the final Q4 GDP revisions for Italy where, as a reminder, the advanced reading (-0.2% qoq) confirmed a technical recession, and January retail sales data for the Euro Area. In the US we’ll also get the final PMIs as well as the February ISM non-manufacturing (+0.6pts to 57.3 expected) and December new home sales (-8.7% mom expected). Away from that we’re due to hear from Italy’s finance minister Tria this morning, before the BoE’s Carney speaks this afternoon before the House of Lord’s Economic Affairs Committee. The Fed’s Rosengren is also set to speak today.

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 26.67 POINTS OR 0.88% //Hang Sang CLOSED UP 2.84 POINTS OR 0.01% /The Nikkei closed UP 96.76 POINTS OR 0.44%/ Australia’s all ordinaires CLOSED DOWN 0.34%

/Chinese yuan (ONSHORE) closed UP at 6.7020 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 56.73 dollars per barrel for WTI and 65.85 for Brent. Stocks in Europe OPENED RED EXCEPT LONDON//.

ONSHORE YUAN CLOSED UP // LAST AT 6.7020 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7047: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

i) CHINA/

Important: Housing is where China keeps all of its wealth..a drop in home prices will no doubt cripple their economy. China’s largest property developwer is now selling all homes with a 10% discount.

(zerohedge)

It Begins: China’s Largest Property Developer Will Sell All Homes At A 10% Discount

Back in 2017, we explained why the “fate of the world economy is in the hands of China’s housing bubble.” The answer was simple: for the Chinese population, and growing middle class, to keep spending vibrant and borrowing elevated, it had to feel comfortable and confident that its wealth would keep rising. However, unlike the US where the stock market is the ultimate barometer of the confidence boosting “wealth effect”, in China it has always been about housing as three quarters of Chinese household assets are parked in real estate, compared to only 28% in the US, with the remainder invested in financial assets.

Beijing knows this, of course, which is why China periodically and consistently reflates its housing bubble any time it feels the broader economy is slowing, hoping that any subsequent popping of the bubble, which happened in late 2011 and again in 2014, will be a controlled, “smooth landing” process. For now, Beijing has been successful in maintaining price stability at least according to official data, allowing the air out of the “Tier 1” home price bubble which peaked in early 2016, while preserving modest home price appreciation in secondary markets.

How long China will be able to avoid a sharp price decline remains to be seen, but in the meantime another problem faces China’s housing market: in addition to being the primary source of household net worth – and therefore stable and growing consumption – it has also been a key driver behind China’s economic growth, with infrastructure spending and capital investment long among the biggest components of the country’s goalseeked GDP. One result has been China’s infamous ghost cities, built only for the sake of Keynesian spending to hit a predetermined GDP number that would make Beijing happy.

Meanwhile, in the process of reflating the latest housing bubble, another dangerous byproduct of this artificial housing “market” has emerged: tens of millions of apartments and houses standing empty across the country. As we reported recently, according to recent research, roughly 22% of China’s urban housing stock is unoccupied, according to Professor Gan Li, who runs the main nationwide study. That amounts to more than 50 million empty homes.

![]()

The reason for the massive empty inventory glut: to keep supply low and prices artificially elevated by taking out as much inventory off the market as possible. This, however, works both ways, and while it helps boost prices on the way up as the economy grow and speculators flood the housing market with easy money, the moment the trend flips the spike in supply as empty units are offloaded will lead to a panic liquidation of homes, resulting in what may be the biggest housing market crash ever observed, and putting the US home bubble of 2006 to shame.

Indeed, as Bloomberg noted, the “nightmare scenario” for Chinese authorities is that owners of unoccupied dwellings rush to sell when cracks start appearing in the property market, causing a self-reinforcing downward price spiral.

Which is why preserving the narrative (or rather myth) of constantly rising prices is so critical for China: any cracks in the facade of the price appreciation story could have a dire consequence first for the housing market, and then, the broader economy whose growth is already the slowest in modern Chinese history, as any scramble to liquidate inventory could promptly result in a bidless market as the tens of millions of empty units are suddenly exposed for both buyers and sellers to see.

* * *

While the key role of China’s housing market in the country’s economy, and thus the world’s, has long been known, a recent troubling development is that despite what Beijing deems stable home prices, the foundations behind the housing market are starting to crack. As the WSJ recently reported, in early December, a group of homeowners stormed the sales office of their Shanghai complex, “Central Washington”, whose developer, Shanghai Zhaoping Real Estate Development, was advertising new apartments at a fraction of the prices of the ones sold earlier in the year. One apartment owner said the new prices suggested the value of the apartment she bought from the developer in March had dropped by about 17.5%.

“There are people who bought multiple homes who are now trying to sell one to pay off the mortgage on another,” said Ran Yunjie, a property agent. One of his clients bought an apartment last year for about $230,000. To find a buyer now, the client would have to drop the price by 60%, according to Ran.

Meanwhile, in a truly concerning demonstration of what will happen when the bubble finally bursts, in October we reported that angry homeowners who paid full price for units at the Xinzhou Mansion residential project in Shangrao attacked the Country Garden sales office in eastern Jiangxi province last week, after finding out it had offered discounts to new buyers of up to 30%.

Hao Hong 洪灝, CFA@HAOHONG_CFACountry Garden cut the selling price at one of its residential developments by 1/3. Those who paid full price smashed the sales office. Similar incidents had happened before, and will again. It’s impossible to remove “the guarantee of principal”(刚性兑付)in China.

“Property accounts for roughly 70 per cent of urban Chinese families’ total assets – a home is both wealth and status. People don’t want prices to increase too fast, but they don’t want them to fall too quickly either,” said Shao Yu, chief economist at Oriental Securities. “People are so used to rising prices that it never occurred to them that they can fall too. We shouldn’t add to this illusion,” Shao added, echoing Ben Bernanke circa 2005.

The bottom line is that just like true price discovery for US capital markets is prohibited (and sees Fed intervention any time there is an even modest, 10-20% drop in asset prices) or else the risk of an all out panic is all too real, in China true price discovery is also not permitted, however when it comes to the country’s all important, and wealth effect boosting, real estate.

Which is a problem, because whereas China suddenly appears to be suffering from all the conventional signs of deflation in the auto retail sector, where as we noted previously, neither lower prices nor easier loans have managed to put a dent the ongoing demand plunge…

… the same ominous price cuts – which are clearly meant to boost flagging demand – are starting to emerge in China’s housing sector.

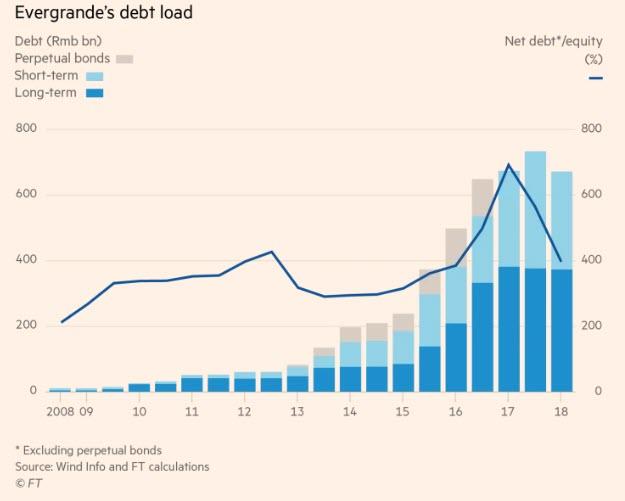

Case in point, according to China’s Paper, Hui Ka Yan, the Chairman of Evergrande, China’s biggest property developer, and China’s second richest person announced it must ramp up home sales and to do that it would sell all its properties at a 10% discount after its home sales tumbled in January amid a cooling market.

The fact that Evergrande has had financial difficulties for the past year is not new. In November, Evergrande, which carries the industry’s largest debt pile of any Chinese housing developer, was caught in a vicious funding squeeze and raised eyebrows with a $1.8BN, 5-year bond deal, which it had to pay a whopping 13.75% coupon, prompting analysts to say the move “carried a whiff of desperation.” The fact that chairman Hui Ka Yan, China’s second-richest person, bought $1bn of it himself, added to a sense that outside investors were shunning the company.

In many ways, Evergrande had no choice: after the property market boomed for the past three years, helping to power the economy through Xi Jinping’s crucial political transition year of 2017, in 2018 the market slowed sharply, after local governments shifted focus to controlling frothy prices and China Development Bank, the policy lender, phased out a $1 trillion subsidy program for homebuyers in smaller cities, where Evergrande’s projects are concentrated, the FT reported.

Even the official China News Service, usually a cheerleader for the economy, acknowledged recently that the property market “was a bit chilly”. Nomura chief China economist Ting Lu put it more starkly, forecasting a “frigid winter”.

The bigger problem for Evergrande, which had $208 billion in total liabilities at the end of June 2018 — the most of any Chinese developer — including $43bn maturing in 2019, is that should China’s housing market suffer a steep downturn, it will likely be the company to suffer the most, if for no other reason than its massive leverage which stood at a net debt to equity ratio of 400%.

Commenting on the bond sale, a high-yield debt underwriter at a western bank in Hong Kong told the FT that “Evergrande is very levered, so, yes, they do need cash,” said “That said, they are not a name we see as having a near-term liquidity crisis. That cannot be said about other smaller players.”

That was in November; and while there are no signs that the funding situation at Evergrande has deteriorated sharply since then – especially since the company is widely seen as systematically important and Beijing would never let it fail (although the same was said about Kaisa, another Chinese property developer that did default not too long ago), it now appears that the company has decided to start liquidating properties in an unexpected scramble to either gain market share, or to obtain much needed funding.

In any case, the fact that China’ largest property developer is now slashing prices across the board by as much as 10%, means that a deflationary hurricane is about to blow across what most see as the most important sector in China’s economy, and worse, should other property developers follow in slashing prices launching a race to the bottom, nobody knows how far prices could truly fall should a liquidation domino effect ensue.

What is most troubling however, is that as recently as November, the property slowdown was seen to be in large part due to efforts by city governments to restrain runaway price increases, which has included draconian interventions such as price controls and sales bans.