GOLD: $1287.00 UP $3.30 (COMEX TO COMEX CLOSING)

Silver: $15.08 DOWN 2 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1287.90

silver: $15.14

For comex gold and silver:

MARCH

NUMBER OF NOTICES FILED TODAY FOR MAR CONTRACT: 39 NOTICE(S) FOR 3900 OZ (0.1213 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 263 NOTICES FOR 26300 OZ (.8180 TONNES)

SILVER

FOR MARCH

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

372 NOTICE(S) FILED TODAY FOR 1,860,000 OZ/

total number of notices filed so far this month: 4700 for 23,500,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3858:UP $2

Bitcoin: FINAL EVENING TRADE: $3852 DOWN 3

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 22/39

EXCHANGE: COMEX

CONTRACT: MARCH 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,282.000000000 USD

INTENT DATE: 03/05/2019 DELIVERY DATE: 03/07/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 2

661 C JP MORGAN 22

686 C INTL FCSTONE 3

690 C ABN AMRO 3

737 C ADVANTAGE 4 12

800 C MAREX SPEC 2

905 C ADM 30

____________________________________________________________________________________________

TOTAL: 39 39

MONTH TO DATE: 302

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A TINY SIZED 36 CONTRACTS FROM 190,060 DOWN TO 190,024 WITH YESTERDAY’S 1 CENT GAIN IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE ALWAYS WITNESS A CONTRACTION IN TOTAL OI AS WE APPROACH FIRST DAY NOTICE AND IT SEEMS THE CULPRIT IS THE FORCED LIQUIDATION OF SPREADERS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A VERY STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 2192 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2192 CONTRACTS. WITH THE TRANSFER OF 2192 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2192 EFP CONTRACTS TRANSLATES INTO 10.96 MILLION OZ ACCOMPANYING:

1.THE 1 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.

AND NOW: 25.325 MILLION OZ STANDING IN MARCH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

12,798 CONTRACTS (FOR 4 TRADING DAYS TOTAL 12,798 CONTRACTS) OR 63.99 MILLION OZ: (AVERAGE PER DAY: 3199 CONTRACTS OR 15.99 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 63.99 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 9.14% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 428.884 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 36 WITH THE 1 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD STRONG SIZED EFP ISSUANCE OF 2192 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A CONSIDERABLE SIZED: 2156 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2192 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 36 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 1 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.10 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.975 BILLION OZ TO BE EXACT or 139% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 372 NOTICE(S) FOR 1,860,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/AND NOW MARCH: 25.325 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 2976 CONTRACTS UP TO 471,311 DESPITE THE FALL IN THE COMEX GOLD PRICE/(A LOSS IN PRICE OF $1.70//YESTERDAY’S TRADING). HOWEVER…….

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY STRONG SIZED 7293 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 7293 CONTRACTS,JUNE: 0 CONTRACTS DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 471,311. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8,269 CONTRACTS: 2976 OI CONTRACTS INCREASED AT THE COMEX AND 7,293 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 8269 CONTRACTS OR 826,900= 25.72 TONNES.

YESTERDAY WE HAD A LOSS IN THE PRICE OF GOLD TO THE TUNE OF $1.70…. AND THUS WE HAD THIS SOLID GAIN IN OI DESPITE THE LOSS IN PRICE????

YESTERDAY, WE HAD 10,670 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 40,552 CONTRACTS OR 4,055,200 OZ OR 126.13 TONNES (4 TRADING DAYS AND THUS AVERAGING: 10,138 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAYS IN TONNES: 126.13 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 126.13/2550 x 100% TONNES = 4.94% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1001..68 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 2976 DESPITE THE LOSS IN PRICING ($1.70) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A CONSIDERABLE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7293 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7293 EFP CONTRACTS ISSUED, WE HAD A STRONG GAIN OF 8269 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7293 CONTRACTS MOVE TO LONDON AND 2976 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE STRONG GAIN IN TOTAL OI EQUATES TO 25.72 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $1.70 IN YESTERDAY’S TRADING AT THE COMEX

we had: 39 notice(s) filed upon for 3900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $3.30 TODAY

NO ADDITIONS OR SUBTRACTIONS TODAY

INVENTORY RESTS AT 766.59 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 1 CENT IN PRICE TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV..///

/INVENTORY RESTS AT 308,503 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TINY SIZED 36 CONTRACTS from 196060 DOWN TO 190,024 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 2192 FOR MAY AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2192 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 36 CONTRACTS TO THE 2192 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE SURPRISINGLY OBTAIN ONLY A STRONG GAIN OF 2156 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 10.78 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY AND NOW 25.325 MILLION OZ FOR MARCH.

RESULT: A TINY SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 1 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A STRONG SIZED 2136 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. THE LOSS IN OPEN INTEREST CONTRACTS IN SILVER WAS CAUSED BY THE FORCED LIQUIDATION OF SPREADERS…IT HAD NO EFFECT ON PRICE..TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 47.85 POINTS OR 1.57% //Hang Sang CLOSED UP 76.00 POINTS OR 0.26% /The Nikkei closed DOWN 129.47 POINTS OR 0.60%/ Australia’s all ordinaires CLOSED UP .72%

/Chinese yuan (ONSHORE) closed DOWN at 6.7085 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 56.17 dollars per barrel for WTI and 65.78 for Brent. Stocks in Europe OPENED MIXED

ONSHORE YUAN CLOSED DOWN // LAST AT 6.7085 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7176: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/

Not good: North Korea already has re-started building its long range missile sites and these were revealed by satellite images

( zerohedge)

b) REPORT ON JAPAN

3 C/ CHINA

i) CHINA/

i)Spot rates for 40 foot containers being shipped from China to North America is showing a continual slowdown. Another evidence of a contraction in the global economy

( zerohedge)_

( Jeffrey Snider/Alhambra Investment Partners)

4/EUROPEAN AFFAIRS

i)EU/ECB

ii)Are we heading for another QE?(courtesy RanSquawk)

iii)The rumours are true; The ECB is poised to launch QE as a TLTRO

( zerohedge)

iv)Germany/Deutsche bank

Our good friends over at Deutsche bank lost another 750 million dollar in equity trading this quarter

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

a)Today, the OECD slashes GDP global growth forecasts and warns that it will probably get weaker

(OECD/zerohedge)

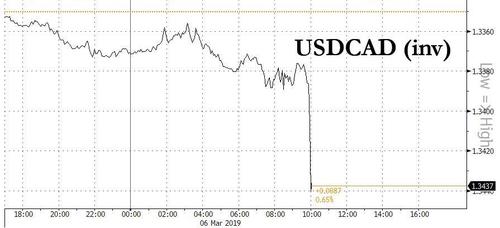

b)OH Oh! The Canadian loonie tumbles after the Bank of Canada warns that there is uncertainty about future rate hikes

( zerohedge)

c)Mac Slavo points out the obvious: the global economy is sinking fast

(courtesy Mac Slavo/SHFTplan.com

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data

iv)SWAMP STORIES

Nadler is a man in search of a crime and that will be the Democrats modus operandi for the next 2 years.

(courtesy Sara Carter)

end

Let us head over to the comex:

AFTER MARCH, WE HAVE THE NON ACTIVE DELIVERY MONTH OF APRIL. HERE: APRIL RISES TO 798 CONTRACTS FOR A GAIN OF 2 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI FELL BY 929 CONTRACTS DOWN TO 139,057 CONTRACTS.

i) out of Scotia: 7720.018 oz

JPMorgan Is Bullish on Gold as a Hedge Against Rising Inflation

Precious Metals SWOT Analysis: JPMorgan Is Bullish on Gold

by Frank Holmes via GoldSeek

Precious Metal Strengths

- The best performing metal this week was palladium, up 2.81 percent with continued price strength. Gold traders were split between bullish, bearish and neutral on the yellow metal this week as prices struggled to recover and posted a monthly loss for February. Lawmakers in Romania are drafting legislation aiming to repatriate the country’s gold stored in the United Kingdom. The bill is to amend a Romanian central bank law that allows only 5 percent of its gold reserves abroad. This is a positive signal of countries wanting to hold their gold domestically. Palladium saw a seventh monthly gain in February and is up an amazing 83 percent since mid-August. The precious metal has been rallying due to a supply shortage as car manufacturers increasingly need palladium to meet emission standards.

- Another precious metal getting attention as of late? Platinum. In the month of February, platinum saw the biggest inflows into ETFs in almost six years. The palladium rally has helped renew investor interest in its sister metal. Impala Platinum Holdings, the world’s second largest platinum miner, made a significant reduction in its debt and share prices rose more than 9 percent on Thursday to the highest since October 2016.

- Kitco News reports that the drama between the world’s two largest mining companies intensified this week. Newmont Mining rejected an all-stock merger proposed by Barrick Gold. Newmont released a statement saying that it prefers to move forward with its acquisition of Goldcorp, with that new company surpassing Barrick to become the world’s largest miner.

Precious Metal Weaknesses

- The worst performing metal this week was silver, down 4.74 percent on hedge funds cutting their net long position by about 10 percent this past week. American Eagle gold coin sales fell 81 percent in February to just 12,500 ounces after posting a two-year high in January, according to U.S. Mint data. This comes as spot gold prices hit their highest level since April on February 20, and then slid to post the first monthly loss in five, writes Bloomberg. The London Bullion Market Association reported that gold trading in January declined to an average 19.6 million ounces per day, a 17 percent drop from the previous month. Gold suffered a narrow loss in February after four straight months of gains. Michael McCarthy, chief market strategist at CMC Markets, said that the “U.S. dollar strength is a key danger for gold, and the technical picture for gold has deteriorated with the failure around $1,340.”

- Turkey continues to sell its gold reserves. Central bank data from Ankara shows that reserves fell 4.5 tons month-over-month in January to 440.8 tons. At least eight tons of gold were removed from Venezuela’s central bank last week, according to unidentified government sources who did not say where the gold was going to. In 2018, 23 tons of Venezuelan gold was transported to Istanbul, and some speculate that is the same place this going is going to as well.

- Centamin Plc, an Egyptian gold miner, saw its shares fall as much as 22 percent on Monday after forecasting production estimates below analyst expectations. The company forecast production from 490,000 to 520,000 ounces in 2019, which is less than the amount mined in 2017.

Precious Metal Opportunities

- According to Australia & New Zealand Banking Group Ltd, palladium consumption by the auto sector will grow 1.1 percent in 2019 due to stricter environmental laws requiring more usage of the metal. This comes despite the recent contraction in car sales in both Europe and China. Strategists Daniel Hynes and Soni Kumari wrote in a report that “with emission regulations getting tighter across major countries, we see higher loadings requirements offsetting a slowdown in the auto sector’s palladium demand.” Bloomberg reports that Impala Platinum Holdings plans to start building a new palladium mine that could begin producing as early as 2024. The miner plans to start work on the Waterberg project in South Africa in 2021, says CEO Nico Muller. Anglo American Platinum Ltd, the world’s top platinum miner, is looking at plans to boost its palladium output through the expansion of one of its current mines.

- JPMorgan is bullish on gold as a hedge against rising inflation. Strategists led by John Normand wrote in a note last week that “TIPS and gold seem like the most durable inflation hedges for a unique macro environment when the Fed’s reaction function isn’t the only regime change impacting real assets.” Bloomberg’s Joanna Ossinger writes that “the Fed appears to be considering trying to let inflation run hotter than its 2 percent target to make up for years below that level.”

- Heraeus wrote this week the geopolitical risks should keep central banks buying gold. IMF data shows that at the end of 2018 central bank gold reserves reached their highest level since 1997 at 33,800 tons. The company writes that current geopolitical risks and growing concern about the U.S. dollar should drive more purchases of gold as a hedge against instability and a way to diversify.

Precious Metal Threats

- In regards to Barrick’s attempt to takeover Newmont, Doug Groh, a portfolio manager at Tocqueville Asset Management had some harsh words. “It seems arrogant on Barrick’s behalf to assume shareholders will believe in the value creation of the merged Barrick-Newmont entity as the offset to a premium that’s not paid in the marketplace directly in the bid. It’s cheeky on their part to assume shareholders are so naïve as to assume premium value will come through their execution.” According to Bloomberg Intelligence analyst Andrew Cosgrove, the top 20 holders in Barrick, who own 55 percent of total shares outstanding, also own 91 percent of Newmont’s shares. This fact makes it clear that Barrick’s management may have a hard time fighting against shareholders if they support Newmont and demand a higher premium. Another potential issue regarding this potential merger? Review by the Federal Trade Commission and Department of Justice about it possibly substantially lessening competition in the gold mining space in the United States. Would America want its largest domestically based gold company to be taken over by foreign hands? Barrick would dominate Nevada, potentially stifling competition in the nation’s biggest gold mining state.

- Goldcorp could be left at the altar, so to speak, if Newmont merges with Barrick. Under that proposed merger, Newmont would need to abandon its already planned acquisition of Goldcorp. Additionally, Barrick would need to sell several small Australian miners as a part of the deal. But would anyone be there to buy them? Or will the other miners allow Barrick to struggle to rationalize its assets instead of helping it turn noncore assets into cash?

- The Environmental Project Agency (EPA) is facing negligence claims after workers triggered the release of millions of gallons of mining wastewater and toxic sediment into the Animas River in New Mexico. The 2015 Gold King Mine spill occurred when the EPA accidentally opened a passage leading into the mine when trying to identify actions needed to address contamination flowing from the site, writes Bloomberg. The government isn’t required to clean up their spill.Courtesy of GoldSeek.com

Gold edges above five-week low as market rally pauses (Reuters.com)

Gold dips as dollar gains on robust U.S. data (Reuters.com)

Wall Street slips as GE swoons, key market level looms (Reuters.com)

Stocks stall, dollar stands tall as China trims growth targets (Reuters.com)

Death of Bond Volatility Has Pimco Fearing for Europe’s Future (Bloomberg.com)

It’s Payback Time for Stocks as Balance-Sheet-Be-Damned Ends (Bloomberg.com)

China’s Largest Property Developer Will Sell All Homes At A 10% Discount (AsiaTimes.com)

EU, ECB Activate Emergency Currency Swap Line To Brace For ‘No Deal’ Brexit (ZeroHedge.com)

JPMorganChase has just flushed the silver futures market again, (Gata.org)

05 Mar: USD 1,285.00, GBP 975.19 & EUR 1,134.78 per ounce

04 Mar: USD 1,287.45, GBP 972.93 & EUR 1,135.14 per ounce

01 Mar: USD 1,309.95, GBP 989.27 & EUR 1,152.23 per ounce

28 Feb: USD 1,325.45, GBP 996.21 & EUR 1,162.82 per ounce

27 Feb: USD 1,326.45, GBP 998.02 & EUR 1,164.09 per ounce

26 Feb: USD 1,327.55, GBP 1005.79 & EUR 1,168.11 per ounce

Silver Prices (LBMA)

05 Mar: USD 15.11, GBP 11.47 & EUR 13.33 per ounce

04 Mar: USD 15.16, GBP 11.50 & EUR 13.38 per ounce

01 Mar: USD 15.56, GBP 11.75 & EUR 13.67 per ounce

28 Feb: USD 15.81, GBP 11.89 & EUR 13.85 per ounce

27 Feb: USD 15.86, GBP 11.91 & EUR 13.92 per ounce

26 Feb: USD 15.83, GBP 11.98 & EUR 13.93 per ounce

Recent Market Updates

– Gold – It Might Be Different This Time

– Euromillions Winners To Invest In Gold In 2019?

– Gold Still on a Long Term Track to Reach $2,000 An Ounce

– “Gold Is A Global Thermometer Of Risk” – CEO Q+A: Stephen Flood, GoldCore

– U.S. Mint Suspends Silver Bullion Coin Sales After Sales Double In February

– MMT: Modern Monetary Madness Will Lead To Higher Taxes and Inflation

– Gold Broker Has Good Sense and Prefers Gold To All That Glitters (The Times)

– The Utterly Unbelievable Scale of U.S. Debt Right Now

Sho

Craig Hemke at Sprott Money: Comex silver ‘market’ dynamics

Submitted by cpowell on Tue, 2019-03-05 22:12. Section: Daily Dispatches

5:12p ET Tuesday, March 5, 2019

Dear Friend of GATA and Gold:

JPMorganChase has just flushed the silver futures market again, the TF Metals Report’s Craig Hemke writes today at Sprott Money, and now will let the price rise in preparation for another flush. Hemke suggests that there’s money to be made following the investment bank’s market manipulation.

His analysis is headlined “Comex Silver ‘Market’ Dynamics” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/comex-silver-market-dynamics-craig-hemk…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

This topic has been covered already this week: Romania joins the gold repatriation exodus from storage at the Bank of England. We wish the country well in their attempt to get their gold back

(courtesy Manly/Bullionstar/GATA)

Ronan Manly: Romania joins gold repatriation exodus

Submitted by cpowell on Wed, 2019-03-06 02:25. Section: Daily Dispatches

9:26p ET Tuesday, March 5, 2019

Dear Friend of GATA and Gold:

Bullion Star gold researcher Ronan Manly today examines the effort in Romania’s parliament to repatriate the country’s gold reserves from the Bank of England and concludes that it opens a new front between democracy and the arrogance and unaccountability of the central bank.

If legislators enact the bill, Manly writes, “Romania looks set to join the ranks of Hungary, Austria, Germany, and the Netherlands in bringing gold bars back into domestic storage. Which European nation will be next after Romania? Poland is a likely candidate, with 102.9 tonnes of gold stored at the Bank of England.”

Manly’s analysis is headlined “The Domino Effect: Romania Joins Gold Repatriation Exodus” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/the-domino-effect-romania-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7085/

//OFFSHORE YUAN: 6.7176 /shanghai bourse CLOSED UP 47.85 POINTS OR 1.57% /

HANG SANG CLOSED UP 76.00 POINTS OR 0.26%

2. Nikkei closed DOWN 129.47 POINTS OR 0.60%

3. Europe stocks OPENED MIXED

/USA dollar index RISES TO 96.72/Euro FALLS TO 1.1303

3b Japan 10 year bond yield: FALLS TO. +.00/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.86/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 56.17 and Brent: 65.78

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN /OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

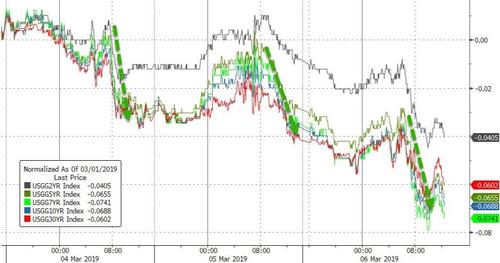

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.15%/Italian 10 yr bond yield UP to 2.69% /SPAIN 10 YR BOND YIELD UP TO 1.14%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.54: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.73

3k Gold at $1286.40 silver at:15.09 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

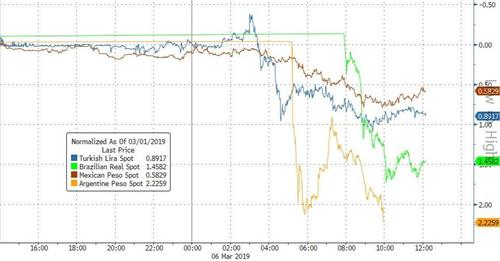

3l USA vs Russian rouble; (Russian rouble DOWN 4/100 in roubles/dollar) 65.84

3m oil into the 56 dollar handle for WTI and 66 handle for Brent/

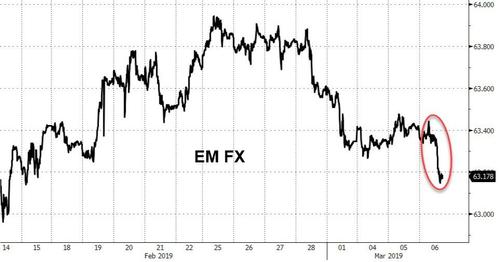

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.86 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0017 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1357 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.15%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.71% early this morning. Thirty year rate at 3.08%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.4011

US Futures Slide On Lack Of New “Trade Deal Optimism”; Dollar Ramps Higher

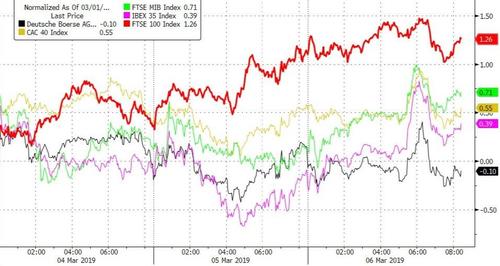

The historic, post-Christmas rally struggled for a second day, with the S&P still unable to decisively cross the critical 2800 resistance level and sliding in a quiet overnight session, while European shares also faded after a mixed Asian session as investors await fresh catalysts on trade and monetary policy. Meanwhile, the dollar advanced for a sixth day as Treasuries edged higher.

Carmakers fell and miners rose, leaving the Stoxx Europe 600 Index little changed with the DAX underperforming peers as auto names weigh alongside banks and insurance names with markets shrugging off a downbeat global economic assessment from the OECD. European banks were again hit by the ever-widening money-laundering scandal which seems to add more names with every passing day. On Wednesday, RBS said it was looking into allegations of money laundering through certain Dutch banks and reports this may concern an ABN Amro business line acquired by RBS. Investors can now add regulatory penalties to the list of bank sector worries after bank were the second-worst Stoxx 600 performer in 2018, hit by political uncertainty, a flattening yield curve and low rates. That relative peformance has continued to send the price ratio vs the Stoxx 600 lower this year, with the earnings season disappointing and consensus 12-month forward EPS estimates falling almost 4%.

Unable to rise above 2,800 for two weeks in a row, S&P 500 futures had no other choice but to decline. Eminis have now been trading in a tight, 20 point range sine mid-February.

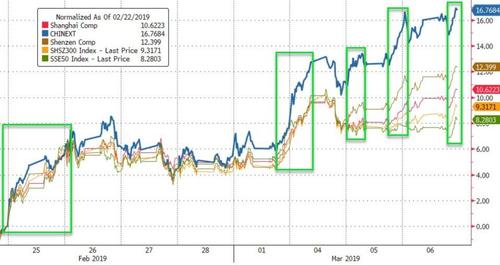

Earlier in Asia, a familiar pattern emerged as Chinese shares once again outperformed as the local stock bubble is rapidly scrambling to recreate its 2015 majesty while Japanese equities dropped. The Shanghai Composite surged another 1.6%, rising above 3,100 after a last hour ramp perhaps the result of China’s National Team attempts to herd even more mom and pop investors into the rising momentum. Volumes were again massive, with over 1 trillion yuan trading on Wednesday.

Elsewhere in Asia, RBA Governor Lowe reiterated his neutral stance nothing that the RBA has flexibility to adjust monetary policy in either direction, probabilities of a rate hike or cut are evenly balanced. He also stated it is hard to imagine a rate hike this year, and it is unlikely inflation will be a problem anytime soon. Lowe added that he is confident inflation will get back to the middle of 2-3% target range, Q3 and Q4 GDP likely to be significantly below trend. The AUD was hit hard when the Australian Real GDP for Q4 printed at 0.2% vs. Exp. 0.3% (YY Q4 2.3% vs. Exp. 2.5%).

Investors remain jittery, looking for hints on what Trump will do next on negotiations with China as trade remains high on the agenda. Meanwhile, the bond market signals more caution and Morgan Stanley is now predicting Treasury yields will drop as low as 2.35% by the end of the year. Traders will also get a jolt from the ECB’s policy decision today when Mario Draghi may announce the long overdue TLTRO.

In rates, traders saw a pop higher in German Bund futures, with 10y and 30y yields initially -3bps as the curve bull flattened, before gains were pared dragging USTs off the highs, while peripheral bonds tightened modestly to core. Gilt yields were ~2bps lower across the curve as Brexit anxiety remains elevated. The Bloomberg dollar index traded in the middle of its overnight range, stronger for the sixth day and defying Trump’s latest dollar bashing.

The pound weakened on speculation U.K. Prime Minister Theresa May could be in for another bruising vote in Parliament on Brexit, and the Australian dollar sank after weak GDP data on the economy spurred bets on interest-rate cuts. Emerging-market stocks gained for a fourth day and currencies were steady.

In Central bank news, BoJ Board Member Harada (Dissenter) opposed the BoJ’s new forward guidance due to the view that guidance must be data-dependent and not calendar-dependent. In his view, forward guidance must have a commitment to keep rate low until inflation beats expectations. He also said underlying inflation weakness could weigh on inflation expectations and delay the acceleration of inflation, and despite the rising household income.

In geopolitical news, North Korea was reportedly taken aback by the sudden end to the Trump-Kim summit; and it will take North Korea some time to review what happened; according to Korean press citing the South Korean government. US National Security Adviser Bolton said US will increase sanctions on North Korea if it does not move towards denuclearisation.

In the latest Brexit news, EU and UK Brexit talks ended with no agreement but are to continue on Wednesday; according to sources. Furthermore, an EU official said the talks did not go well. A senior UK minister, who is directly involved in Brexit planning, said: “It’s inevitable there would have to be a technical extension” and added that a month is unlikely to be enough, two months would be needed to get the legislation through, and this is accepted in government. If UK MPs reject PM May’s deal a second time next week, parliament would take control and force a softer Brexit; according to Chief Whip Smith.

Elsewhere, commodities were led lower by oil after API showed a massive buildup in U.S. crude stockpiles. Brent (-0.2%) and WTI (-0.9%) prices are in the red following the larger than expected build in API Crude Inventories yesterday of 7.4mln vs. Exp. 1.2mln. If the API build is confirmed by EIA data later on today this would be a large contrast to the prior draw. That said, UBS highlighted that a build of this size would not mean a major deviation from the seasonal average within the context of the prior two months data, as such should not result in a lasting impact on oil prices. Elsewhere, China have cancelled Canadian Co. Richardson Internationals registration to ship canola to China; following this, China’s foreign ministry state that harmful pests have been discovered in samples taken from Canadian Canola oil and a serious problem has been highlighted in one Co’s shipments. Although, it is currently not clear which company this refers to. Gold (-0.1%) is approaching the bottom of its narrow USD 4/oz range, but is largely unchanged on the day. Elsewhere, the World Platinum Investment Council stated that the global platinum market will this year experience the largest surplus since around 2013.

Besides the ECB, data on ADP private payrolls, mortgage applications, and the trade balance are due. Earnings include Dollar Tree and Brown-Forman.

Market Snapshot

- S&P 500 futures down 0.2% to 2,786.50

- STOXX Europe 600 unchanged at 375.63

- MXAP down 0.04% to 159.45

- MXAPJ up 0.1% to 526.46

- Nikkei down 0.6% to 21,596.81

- Topix down 0.3% to 1,615.25

- Hang Seng Index up 0.3% to 29,037.60

- Shanghai Composite up 1.6% to 3,102.10

- Sensex up 0.6% to 36,646.46

- Australia S&P/ASX 200 up 0.8% to 6,245.62

- Kospi down 0.2% to 2,175.60

- German 10Y yield fell 1.5 bps to 0.153%

- Euro down 0.04% to $1.1303

- Brent Futures down 0.6% to $65.46/bbl

- Italian 10Y yield fell 3.1 bps to 2.349%

- Spanish 10Y yield fell 1.7 bps to 1.137%

- Brent Futures down 0.6% to $65.46/bbl

- Gold spot down 0.1% to $1,286.42

- U.S. Dollar Index up 0.05% to 96.92

Top Overnight News by Bloomberg

- President Donald Trump is pressuring U.S. trade negotiators to cut a deal with China soon in hope of fueling a market rally, as he grows increasingly concerned that the lack of an agreement could drag down stocks, according to people familiar with the matter

- Wall Street could face fresh restrictions on bonus payments as regulators appointed by President Trump consider dusting off post-crisis rules that have long been on the back burner, according to two people familiar with the matter

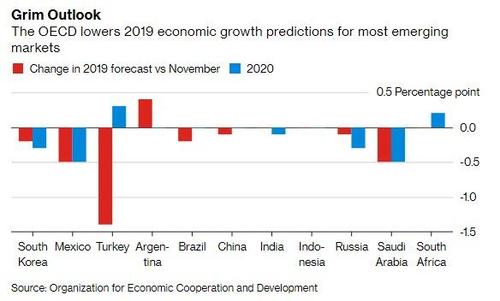

- The global economy is suffering more than expected from trade tensions and political uncertainty which are clouding prospects particularly in Europe, according to a gloomy report from the OECD

- Japan’s economy is at risk of sliding into a recession after a demand-sapping sales tax hike planned later this year, despite a raft of government measures to limit its impact, according to Bank of Japan board member Yutaka Harada

- China’s yuan has been the hottest carry trade in Asia this year, thanks to its rapid advance and muted price swings

- When Qatar sells debt, it sells big. The gas-rich nation is planning a three-part issuance less than a year after raising $12 billion in one of the largest offerings in emerging markets. It’s joining a host of borrowers across developing nations that raised $336 billion in 2019, a record on a year-to-date basis, according to data compiled by Bloomberg

Asian stocks were mixed following a muted lead from Wall Street in which the Dow, S&P and Nasdaq all closed just below breakeven. ASX 200 (+0.7%) shrugged off poor economic data and advanced as the material and mining sectors lead the gains, while Nikkei 225 (-0.6%) underperformed as the index is weighed on by a marginally firmer domestic currency alongside China-exposed sectors after China’s announcement of tax cuts yesterday. Elsewhere, Shanghai Comp. (+1.6%) and Hang Seng (+0.2%) gained momentum following yesterday’s NPC announcement alongside effects from the MSCI upgrade last week. RBA Governor Lowe reiterated his neutral stance; RBA has flexibility to adjust monetary policy in either direction, probabilities of a rate hike or cut are evenly balanced. He also stated it is hard to imagine a rate hike this year, and it is unlikely inflation will be a problem anytime soon. Lowe added that he is confident inflation will get back to the middle of 2-3% target range, Q3 and Q4 GDP likely to be significantly below trend. Australian Real GDP QQ SA Q4 0.2% vs. Exp. 0.3% (Prev. 0.3%) Australian Real GDP YY SA Q4 2.3% vs. Exp. 2.5% (Prev. 2.8%).

Top Asian News

- Trump Is Said to Push for China Deal With Market Gains in Mind

- U.S., China Trade Deal Leaves Currencies as Fighting Ground

- Midea Is the Latest China Stock to Near Foreign Holding Limit

Major European indices are moving towards being unchanged [Euro Stoxx 50 -0.1%] after opening lower and subsequently extending losses; in spite of largely stronger performance overnight. The FTSE 100 (+0.1%) is marginally outperforming its peers boosted by strong performance in DS Smith (+4.1%) after the Co. announced they are selling their plastics division for GBP 585mln. Additional support for the index stems from heavyweights British American Tobacco (+3.8%) and Imperial Brands (+1.3%) in the green following FDA Chief Gottlieb resigning, as his tenure was highlighted by a high-profile push to lower youth smoking including e-cigarettes; this may have also result in some upside for US tobacco names such as Phillip Morris. Other notable movers include Schaeffler (-8.4%) at the bottom of the Stoxx 600 following the announcement of a restructuring program and issuing a warning about a challenging and demanding auto market ahead. Separately, Subsea 7 (+3.7%) are higher after they were awarded 3 contracts by Woodside, describe as major contracts, which may exceed USD 750mln in value.

Top European News

- Not Enough Votes Yet as Brussels Talks Continue: Brexit Bulletin

- Greek Stocks Party Like It’s 1999 as No-Growth Era Seen Over

- L&G Tumbles as Cash Boost From Retirement Business Disappoints

- Biggest Fortune in EU’s East Gets Caught Up in Huawei Scandal

In FX, the DXY hovers just shy of the 97.000 handle and Fib resistance a whisker above (97.004 vs Tuesday’s 97.017 peak). Usd/Jpy is back below 112.00 after what appears to have been a false break-out to circa 112.12 yesterday (and also a fleeting Fib breach), but the pull-back could be shallow given 1.2 bn option expiries running off from 111.80-112.00 at the NY cut. The Franc is holding just off 1.0055 lows and pivoting 1.1350 vs the single currency, while Eur/Usd remains anchored around 1.1300 with 1.1305 eyed as a key chart point on a closing basis and expiries also in the mix as 1 bn resides at the 1.1300 strike.

- AUD/NZD – No respite for the Aussie as a disappointing Q4 growth update extends the run of mainly sub-forecast data releases and adds more justification for the RBA’s shift to neutral policy mode. In fact, comments from Governor Lowe in the run up to the GDP update could be construed as more dovish on balance given that he effectively ruled out any prospect of tightening this year, while reiterating equal odds of a hike or cut in terms of the next rate move, and the market certainly took heed as Aud/Usd collapsed from just under 0.7100 to circa 0.7024 amidst a cascade of calls for 2 OCR eases of 25 bp by the end of 2019 in line with Westpac’s pre-emptive downgraded forecasts in February. Predictably, the Kiwi saw some contagion to a low not far from 0.6750 at one stage, but Nzd/Usd has rebounded relatively firmly to 0.6780+ on favourable cross-winds as Aud/Nzd extends losses through 1.0400 to 1.0360. Note, however, Aud/Usd may yet derive some traction and get a reprieve to stave off a more concerted test of 0.7000 via decent option expiry interest between 0.7045-50 (1 bn).

- GBP/CAD – The Pound continues to be buffeted by fluctuating Brexit sentiment after a brief boost courtesy of hawkish-leaning remarks from BoE Governor Carney late yesterday, with Cable back down near 1.3100 and a recent double-base a few pips short of the big figure, while Eur/Gbp has rebounded to the 0.8600 area again. Back to Brexit, and the bottom line remains no further progress after latest high level talks between UK and EU officials and apparently quite terse negotiations in Brussels as the baton passes to less senior personnel today. Turning to the Loonie, another downturn in crude prices and ongoing angst between Canada and China has culminated in Usd/Cad creeping up further towards the 1.3400 level, as offers said to be layered from 1.3375 to the next round number are soaked up, but the looming BoC policy meeting will likely provide more impetus. On that note, options pricing suggest a break-even of 67 pips for the impending event.

In commodities, Brent (-0.2%) and WTI (-0.9%) prices are in the red following the larger than expected build in API Crude Inventories yesterday of 7.4mln vs. Exp. 1.2mln. If the API build is confirmed by EIA data later on today this would be a large contrast to the prior draw. UBS highlight that a build of this size would not mean a major deviation from the seasonal average within the context of the prior two months data, as such should not result in a lasting impact on oil prices. Elsewhere, China have cancelled Canadian Co. Richardson Internationals registration to ship canola to China; following this, China’s foreign ministry state that harmful pests have been discovered in samples taken from Canadian Canola oil and a serious problem has been highlighted in one Co’s shipments. Although, it is currently not clear which company this refers to. Separately, US National Security Advisor Bolton says he is looking at fresh sanctions against Venezuela to increase the pressure on President Maduro. Gold (-0.1%) is approaching the bottom of its narrow USD 4/oz range, but is largely unchanged on the day. Elsewhere, the World Platinum Investment Council stated that the global platinum market will this year experience the largest surplus since around 2013.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 5.3%

- 8:15am: ADP Employment Change, est. 190,000, prior 213,000

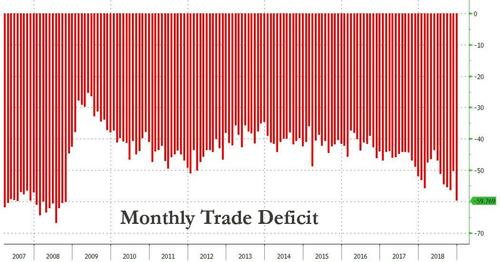

- 8:30am: Trade Balance, est. $57.9b deficit, prior $49.3b deficit

- 2pm: U.S. Federal Reserve Releases Beige Book

Central Banks

- 12pm: Fed’s Williams Speaks to Economic Club of New York

- 12pm: Fed’s Mester Participates in Moderated Discussion

- 2pm: U.S. Federal Reserve Releases Beige Book

DB’s Jim Reid concludes the overnight wrap

The “March Flu” lives on with some power but I’m returning to functioning adult duties but yesterday was another day to reflect on getting older and being more out of touch. To set the scene as a music geek there was a time between around 1980 and maybe the early 2000s when I could have probably recited every number one single over the period in the UK in chronological order. However at some point in the last 10-15 years I lost touch with the charts even if I still try to discover new music when I can. Anyway at the beginning of the year I heard this great new song on a random Spotify (venue of some great DB podcasts) playlist and have played it to death on my headphones since. It was my little discovery/secret and made me feel cool that I still had an ear for music. Anyway on randomly flicking through the newspaper yesterday I stumbled across the U.K. singles chart and to my confusion discovered that the song I thought was my little secret is actually number 1 in the charts. Nice to be so out of touch that you’re secretly in touch. The song is called “Someone You Loved” by Lewis Capaldi. To be honest there are a lot of similarities to “Someone Like You” by Adele. So if that song is your bag then please hunt out. If it’s not you probably should avoid. But then again if you’re under 30-35 you probably know all this already.

After the trade euphoria that kick started the week, markets have quickly become stuck in a soggy patch with no real catalysts to push them one way or the other with any conviction. The good news is that we’ve got an ECB meeting and a payrolls Friday to look forward to in the last two days of this week so hopefully that will inject a bit of energy back into markets again. In the meantime, equity markets were a little directionless yesterday before the S&P 500 ended -0.11%. That is now five down days in the last six however the cumulative loss during that run is only -0.23% so it’s hardly been a material move. Elsewhere, the NASDAQ (-0.02%) and DOW (-0.05%) also just about closed in the red while the STOXX 600 (+0.15%) managed to finish onside having clawed back earlier losses. Part of the underperformance in the US might have been due to Secretary of State Pompeo talking about Trump being ready to walk away from a trade agreement with China unless he secures a “perfect deal” however the reality is that Pompeo has been less directly involved in talks between the two sides so the comment was taken with a bit of a pinch of salt.

Corporate headlines also impacted markets, the biggest impact coming from comments from GE’s CEO Larry Culp. He said at a conference that he expects free cash flow from the firm’s industrial business to be negative this year, after a healthy positive cash flow of $4.5bn last year. GE stock fell -4.72% and its 2035 bonds traded +10bps. Weakness in GE had weighed on corporate credit last year, but indexes of US IG and HY cash credit closed near flat yesterday. In broader equities, the industrials sector led declines in the S&P 500, dropping -0.64%. On the other hand, a bright spot was the US retail sector, which advanced +0.26% after Target (+4.60%) and Kohl’s (+7.33%) both announced profit projections for this year that topped consensus expectations.

As for government bond markets, well Bunds traded as high as 0.1838% intraday yesterday post the more palatable PMIs (more on the below) but ultimately yields faded as sentiment turned with Bunds eventually finishing just +1.0bps higher at 0.168%. BTPs (-3.1bps) actually outperformed after Italy’s Q4 GDP reading was revised up to a slightly smaller contraction (-0.1% qoq from -0.2%) – albeit one that still left Italy in a technical recession at the end of last year.

Meanwhile, Treasuries also retraced an early selloff of +2.5bps to close the day flat at 2.72% (-1.4bps this morning). A fairly decent ISM non-manufacturing (see below) was offset somewhat by dovish comments from the Fed’s Rosengren. This was a little bit of a surprise given that he was one of the more hawkish officials who had worried about overheating risks in the past. Instead, Rosengren said that “it may be several meetings before the Fed has a clear read on whether economic risks are becoming reality”. So that puts Rosengren more in the patience camp for now.

This morning in Asia markets are trading mixed with the Nikkei (-0.69%) and Kospi (-0.32%) down while the Hang Seng (+0.31%) and Shanghai Comp (+0.94%) are up. Elsewhere, futures on the S&P 500 (-0.28%) are heading lower and the Australian dollar is weak (-0.71%) this morning as Australia’s Q4 GDP came in one tenth lower than expected at +0.2% qoq leading to traders increasing their probability of a rate cut. In other news, the BoJ has increased the buying of bonds in the 5y-10y maturity bucket by JPY 50bn at today’s regular operation (JPY 480bn today vs. JPY 430bn in last week). However, the increase was expected after the BOJ last week tweaked its monthly bond-purchase plan and reduced the number of days it would buy 5-10yr bonds to four in March, from five in February.

Overnight, BoJ board member Yutaka Harada has said that Japan’s economy might slide into a recession after a planned sales tax hike later this year, despite a raft of government measures to limit its impact. He cited the example of the 2014 sales tax hike which hit consumption hard and as a result the BoJ ramped up its stimulus 6 months into the hike. Harada is definitely at the dovish end of the committee.

Staying in the region, with China’s NPC into its second day, yesterday our China Chief Economist Zhiwei Zhang outlined his summary of the government’s 2019 work plan which you can find here . Zhiwei believes that the speech sent more signals of policy easing – both fiscal and monetary – and as such he now expects two cuts to the benchmark lending rate of 25bps each in Q2 and Q3.

Back to the PMIs, upward revisions to the core and better than expected non-core readings meant we saw the services reading for the Euro Area revised up half a point to 52.8 and therefore the highest since November. That left the composite at 51.9 which means it finally snapped a run of five consecutive monthly declines. So finally some signs of improving momentum in Europe, or at least in the services sector. Germany’s services reading was revised up from 55.1 to 55.3, France to 50.2 from 49.8 while there were beats for Italy (50.4 vs. 49.5 expected) and Spain (54.5 vs. 54.3 expected). All eyes turn to the ECB tomorrow however one has to expect that the data plays into the wait-and-see message that we’ve been getting from officials of late.

We should also note that the services reading for the UK also surprised to the upside yesterday at 51.3 (vs. 49.9 expected) – up 1.2pts from January. That being said the underlying details were weaker including the employment component. Sterling closed flat, with downside pressure from Brexit headlines offset by positive monetary policy signals. First, Bloomberg headlines popped up just after lunch suggesting that no breakthrough was expected at the Brexit talks yesterday in Brussels. A further story suggested that no agreement was likely on the backstop before the end of this week and that talks could potentially stretch into the weekend (how many times have we said that on both pure EU issues and with Brexit). On the other hand, the pound got some support via comments from Bank of England Governor Carney, who said that “the path of interest rates is not quite high enough,” suggesting that current pricing for the next rate hike for Q4 this year may not be in-line with his own expectations. Staying in the U.K., Bloomberg reported (citing sources) yesterday that the UK PM May’s chief whip Julian Smith is not confident that he has the numbers for March 12th Brexit vote and has predicted that in the votes that follow, a no-deal Brexit would be taken off the table, and the government would be instructed to seek an extension to talks. He also said that he expected lawmakers to put down further amendments that would pass and put the UK on course to staying in the customs union. Sterling is trading weak (-0.32%) this morning as Reuters overnight confirmed the above Bloomberg story that the Brexit talks yesterday didn’t yield any progress and cited an EU official as saying they didn’t go well!

Back to yesterday’s data and as well as the PMIs, we also got the February ISM non-manufacturing reading in the US which looked particularly impressive at a headline level (59.7 vs. 57.4 expected) after jumping 1.7pts and to the highest since November last year. The new orders component also rose 7.5pts to 65.2 and the highest since 2005 however the one small negative was a slight drop in the employment component to 55.2 from 57.8 last month. That said, today’s ADP (190k expected) is likely to be more important for setting payrolls expectations this Friday.

As for the other US data yesterday, new home sales for December printed at 621,000, better than expected but along with a downward revision to the prior month, leaving the overall outlook roughly unchanged. The Treasury’s monthly budget statement showed a surplus of $8.7bn for January, marginally smaller than expected. These statement will become more interesting when we get deeper into tax season over the next few months, to help us better gauge the impact of last year’s tax cuts. Finally, the final Markit composite PMI for February was revised lower by 0.3pts to 55.5, still its highest level since last July.

Finally, in terms of the day ahead, we’ve got no data releases scheduled in Europe this morning while in the US the focus should be on the February ADP employment change reading, and the December trade balance. Later this evening we’ll also get the Fed’s Beige Book while the Fed’s Williams and Mester are due to speak this evening in New York and Ohio, respectively. The BoE’s Cunliffe and Saunders are also slated to speak while the OECD’s interim economic outlook is also due to be released.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 47.85 POINTS OR 1.57% //Hang Sang CLOSED UP 76.00 POINTS OR 0.26% /The Nikkei closed DOWN 129.47 POINTS OR 0.60%/ Australia’s all ordinaires CLOSED UP .72%

/Chinese yuan (ONSHORE) closed DOWN at 6.7085 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 56.17 dollars per barrel for WTI and 65.78 for Brent. Stocks in Europe OPENED MIXED

ONSHORE YUAN CLOSED DOWN // LAST AT 6.7085 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7176: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

i) CHINA/

Spot rates for 40 foot containers being shipped from China to North America is showing a continual slowdown. Another evidence of a contraction in the global economy

(courtesy zerohedge)_

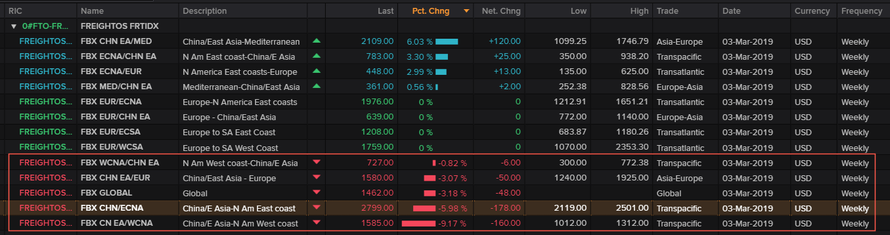

Trade Panic: China To US Weekly Spot Rates For 40′ Containers Collapse

A continued slowdown in the rate at which weekly spot rates for 40′ shipping containers are being shipped from China to North America suggests US demand for Chinese goods continues to stumble, and signals a broader economic slowdown globally looms.

The Freightos Baltic Index (FBX) represents ocean freight prices for 40′ shipping containers, is published weekly on Sundays and represents the price of the previous week (Sunday through Saturday). Prices used in the index are rolling short term freight spot tariffs between carriers, freight forwarders, and high-volume shippers. Index values are calculated by taking the median price for all prices on active lanes with weighting by the shipper.

During the last sixteen weeks, FBX 40′ shipping container rates from China to North America have seen a dramatic move lower, raising concerns about the health of underlying demand.

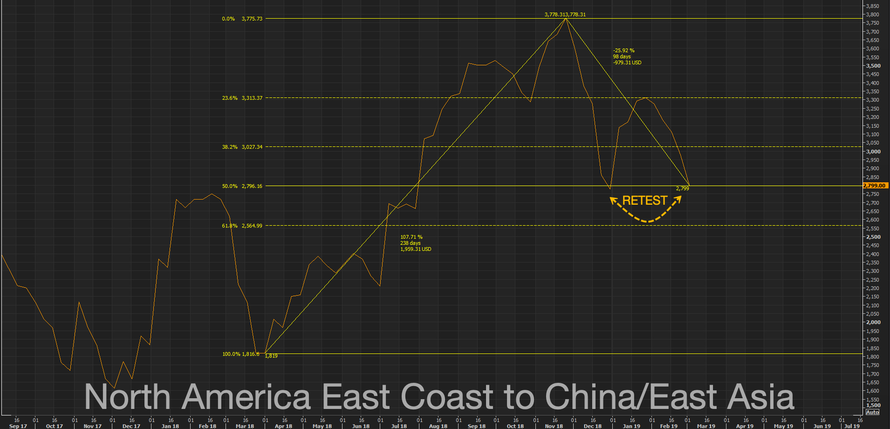

The North America West Coast to China/East Asia Index (FBX02) is down 39% since early November highs, retesting the 50% Fibonacci retracement level late last month and recently broke below December’s lows, is expected to probe 61.8%-Fib in the coming weeks.

The index had a notable impulse starting in March/April 2018, the move lasted 224 days and sent the index up 218% – thanks to President Trump’s trade war against China, which forced US importers to pull orders forward to get ahead of tariffs. However, by early November, rates collapsed after the importers were finished, with no signs of a trough in early March.

The North America East Coast to China/East Asia Index (FBX04) is down 26% since the end of November highs, is currently retesting the December lows when global markets were in a panic about slowing growth.

FBX shipping data shows 40′ shipping container rates are experiencing the worst pressure in North America East Coast to China/East Asia, China/East Asia to Europe, and North America West Coast to China.

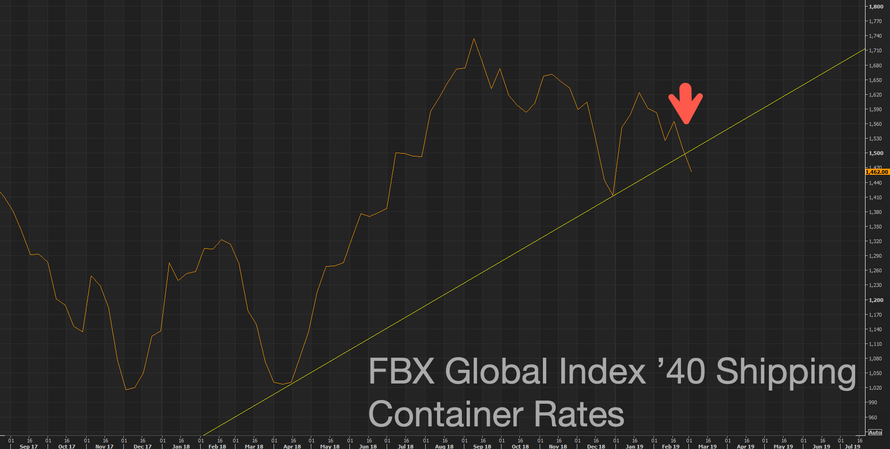

As a whole, the FBX Global Index shows container rates are in danger of taking out their December lows, signaling that the global slowdown is not a “glitch,” but rather the start of a severe synchronized downturn.

On top of container rates plummeting, world trade has slowed in recent months, and leading indicators point to ongoing deceleration.

Of course, the FBX data is just the latest in a long line of worrying news for the Chinese economy but now shows the global slowdown is contagious, infecting the US economy where growth is expected to be less than 1% to near zero for 1Q19.

end

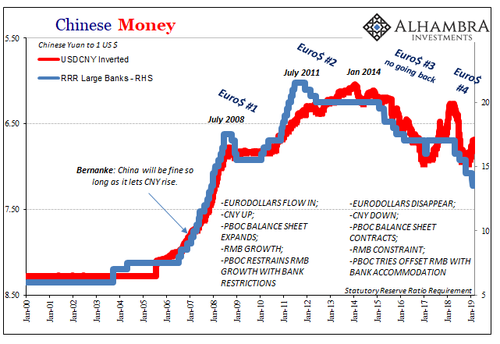

China’s dilemma: dollars (Eurodollars) leaving her shore as it seems that the real enemy is deflation and notinflation

(courtesy Jeffrey Snider/Alhambra Investment Partners)

China Has No Choice

Authored by Jeffrey Snider via Alhambra Investment Partners,

China’s central bank was given more independence to conduct monetary policies in late 2003. It had been operating under Order No. 46 of the President of the People’s Republic of China issued in March 1995, which led the 3rd Session of the Eighth National People’s Congress (China’s de facto legislature) to create and adopt the Law of the People’s Republic of China on the People’s Bank of China. This was amended in December 2003 by the 6th Meeting of the Standing Committee of the Tenth National People’s Congress.

Already by then, the PBOC had begun using more of its monetary toolkit. It had experimented in 2002 with Open Market Operations, or OMO’s. The central bank would issue “bills” to Chinese banks, selling them in order to “soak up” excess liquidity under its definitions.

These were supplemented beginning in September 2003 by the first increase in the RRR, the reserve requirement ratio. This bank lever had been around since the eighties though rarely was it ever used. During China’s rough experience with the Asian flu in the late nineties, the RRR had been deeply reduced to help cushion the economic impact of massive eurodollar irregularities sweeping across its front.

This was an economic response in terms of a debt policy, not a monetary decision.

The RRR told banks how much they needed to keep in liquid reserves (a ledger entry, satisfied via cash holdings or on account with the central bank). If it was reduced, theoretically banks would be able to increase lending because they would be increasingly freed from the reserve constraint. This would include lending in China’s nascent wholesale money markets.

By 2003, the winds of eurodollar influence were blowing heavily in China’s favor again. That meant an excess of monetary resources for the banking sector, only some of which was scooped up by the PBOC as a consequence of pegging CNY’s exchange value to the dollar. To head off harmful inflation, the central bank required the more flexible mandate which was finally sanctioned at the Tenth Congress.

In those early years of it, authorities stuck to mostly OMO’s. There were only two RRR increases in the beginning, an experiment, too, of sorts. The Chinese central bank was new to this potential liquidity framework and the last thing they wanted was to do too much.

As the middle 2000’s progressed, and “hot money” eurodollar inflows only intensified, a more aggressive campaign was called for. By the middle of 2006, RRR increases became as regular as OMO’s.

The thing is, these didn’t really work all that well individually or in combination(s). There were several reasons for the lack of control, including the bureaucratic structure of China’s official apparatus, government to central bank and back again.

But most of all, RRR and/or OMO’s are blunt instruments of indeterminate pathologies. Exactly how does a 50 bps increase in the RRR effect a Chinese bank’s proclivity to lend? No one really knows but a higher reserve requirement does sound a lot like tightening.

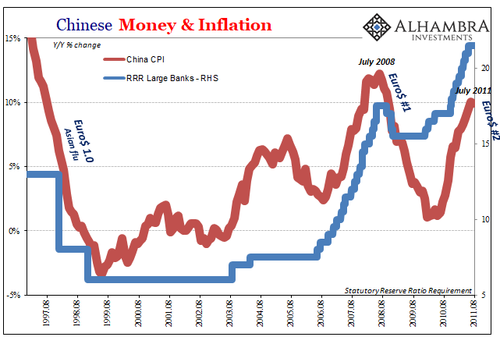

As you can see above, China’s economy came to be plagued by high inflation anyway, especially damaging food price inflation.The country’s CPI suggested still the deflationary drag at the end of 2002, a decrease of 0.4% in the month of December 2002, but rising to a breakout +3.2% in December 2003.

It had at first seemed like the OMO’s were working, with inflation rates falling in the middle of 2005 before another sharp surge which triggered the aggressive response relying more on the uncertain RRR mechanics. By early 2008, despite the RRR having been pushed as high as 17.5% (for large banks), consumer price inflation was rampant the CPI reaching 8.5%. Food prices were rising by more than 20% per year.

The only thing that stopped the onslaught was Euro$ #2. The Global Financial Crisis of 2008, Euro$ #1, had been a temporary reprieve before the same massive money imbalances revisited China in its immediate aftermath. The RRR was pushed up to as much as 21.5% before the second global deflationary wave finally erased its momentum.

Since the middle of 2011, inflation is no longer a problem for the Chinese. Rather, monetary authorities now have nothing but the opposite concern.

Their patchwork response has been to do the same things only in reverse; for eurodollar outflows the RRR is reduced. At times, the central bank even refrains from issuing central bank bills. As with the period before 2008, from 2011 to 2013 it didn’t go well.

By the middle of 2014, the PBOC had added new capacities for more targeted bank liquidity, lending windows such as the MLF or SLF.

Here’s the thing, though. Chinese monetary authorities after relying heavily on tools like the MLF in 2016 and 2017 are no longer as much interested in them. They increased the RMB part of the central bank balance sheet to no avail.

This then left the RRR as China’s main monetary line of defense against deflationary forces in 2018 and going forward. Given its obviously poor performance as an inflation-fighting instrument, why would anyone be optimistic on its chances of succeeding now? You could try to make the case that it could possibly be more effective when used in reverse, but that’s just silly.

China’s Communists aren’t silly; they are authoritarian monsters, meaning they have to be pragmatic for their own survival especially where economic growth (the peasant-to-middle class pipeline) is concerned.

China’s Premier Li Keqiang announced today that the national growth target for 2019 was reduced to a range between 6.0% and 6.5% real GDP expansion. This is lower still than 2018’s mandate for “about” 6.5%, which came in as expected at exactly 6.5%. What are the chances China’s GDP sees the top end of its newly set corridor? If the bottom, this would be the lowest growth since the eighties.

Perhaps a significant sign, China’s Communist leadership appears to have given up entirely targeting both retail sales growth and fixed asset investment.

Li warned:

China will face a graver and more complicated environment as well as risks and challenges that are greater in number and size. China must be fully prepared for a tough struggle.

This is not a new theme except if you have been listening exclusively to the wishful thinking of Western Economists and central bankers. Since the 19th Communist Party Congress (the political apparatus, a separate entity from the National People’s Congress) held in October 2017, government officials have been consistent about this “tough struggle.” There never was globally synchronized growth at least not at a level that would meaningfully change the world’s economic circumstance.

Behind everything is the same thing. Keynes was right. Inflation is one monetary evil, but its twin is far, far worse. At least with inflation things are moving, Chinese peasants are progressed up into the middle class even if it is more expensive when they get there.

Deflation, however, is when everything stops; Dante’s Hell was freezing cold. It doesn’t have to be all at once like in the early thirties, this can be a prolonged affair dragging out across more years than anyone cares to remember. The frog isn’t being slowly boiled, it is being progressively frozen. It is now almost completely frigid, too cold to be able to leap out of the icy water. Stuck here without any other options, it must conserve its energy as best it can and hope that it can somehow survive.

If given a choice, you pick the heat of high inflation over this every day of the week; until you realize it isn’t your choice. It never really was.

end

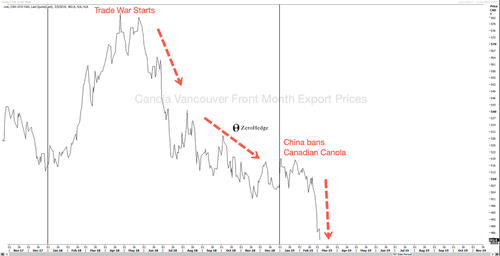

China/Canada

China is furious with Canada so they banned shipments of Canadian Canola to China. The Huawei arrests is certainly have an effect on Canada

(courtesy zerohedge)

Trade War Deepens: China Bans Canadian Canola Shipments Amid Soaring Diplomatic Tensions

Canada’s largest grain processor said Tuesday that Beijing has canceled its registration to ship canola seed to China, fueled by the arrest of a top executive for the Chinese tech giant Huawei, The Wall Street Journal reported.

The move suggests that rising diplomatic tensions between China and Canada are damaging commerce between the two countries. Tensions have already crushed hopes that senior officials in Ottawa and Beijing would develop further trade ties.

The import ban against Richardson International Ltd. is due to a series of Chinese non-compliance notices declaring some shipments of canola seed from Canada were contaminated with “hazardous pests.” Canadian officials disputed that claim.

“I am very concerned by what we’ve heard has happened to Richardson. We do not believe there’s any scientific basis for this,” Canadian Foreign Affairs Minister Chrystia Freeland said in Montreal.

“We are working very, very hard with the Chinese government on this issue.”