GOLD: $1303..00 UP $7.50 (COMEX TO COMEX CLOSING)

Silver: $15.33 UP 16 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1302.30

silver: $15.29

Today is options expiry for all USA equities in the Dow and Nasdaq. Gold/silver is effected for two reasons:

- gold/silver equity shares

- GLD/SLV trading on New York

We only witnessed minor whacking yesterday. We start in earnest the expiry of the comex/LBMA options beginning next week.

Comex options expiry ends: Wednesday March 26/2019

London/LBMA expires Monday March 31/2019.

The crooks continue with their whacking right in front of the authorities/regulators despite the criminal probe of precious metals manipulations.

For comex gold and silver:

MARCH

NUMBER OF NOTICES FILED TODAY FOR MAR CONTRACT: 1 NOTICE(S) FOR 100 OZ (0.0031 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 337 NOTICES FOR 33700 OZ (1.0482 TONNES)

SILVER

FOR MARCH

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

10 NOTICE(S) FILED TODAY FOR 50,000 OZ/

total number of notices filed so far this month: 5302 for 26,510,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3913:UP $44

Bitcoin: FINAL EVENING TRADE: $3931 UP 51

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 1/1

EXCHANGE: COMEX

CONTRACT: MARCH 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,293.400000000 USD

INTENT DATE: 03/14/2019 DELIVERY DATE: 03/18/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 1

905 C ADM 1

____________________________________________________________________________________________

TOTAL: 1 1

MONTH TO DATE: 337

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A CONSIDERABLE SIZED 1403 CONTRACTS FROM 188,266 DOWN TO 186,863 WITH YESTERDAY’S STRONG 30 CENT LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE MUST HAVE HAD CONSIDERABLE SHORT COVERING AGAIN TODAY.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A CONSIDERABLE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 2714 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2714 CONTRACTS. WITH THE TRANSFER OF 2714 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2714 EFP CONTRACTS TRANSLATES INTO 13.570 MILLION OZ ACCOMPANYING:

1.THE 30 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.

AND NOW: 26.835 MILLION OZ STANDING IN MARCH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

24,126 CONTRACTS (FOR 11 TRADING DAYS TOTAL 24,126 CONTRACTS) OR 120.63 MILLION OZ: (AVERAGE PER DAY: 2193 CONTRACTS OR 10.966 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 120.63 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 17.23% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 486.02 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1403 WITH THE 30 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD CONSIDERABLE SIZED EFP ISSUANCE OF 2714 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GOOD SIZED: 1617 TOTAL OI CONTRACTS ON THE TWO EXCHANGES: (DESPITE THE LOSS IN PRICE)

i.e 2714 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 1403 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 30 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.17 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.936 BILLION OZ TO BE EXACT or 133% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 10 NOTICE(S) FOR 50,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/AND NOW MARCH: 26.835 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY ANOTHER VERY STRONG 8,337 CONTRACTS UP TO 541,737 DESPITE THE FALL IN THE COMEX GOLD PRICE/(A LOSS IN PRICE OF $13.60//YESTERDAY’S TRADING). HOWEVER…….

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7547 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 7292 CONTRACTS,JUNE: 255 CONTRACTS DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 541,737. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A HUMONGOUS SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 18,068 CONTRACTS: 8,337 OI CONTRACTS INCREASED AT THE COMEX AND 7547 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 15,884 CONTRACTS OR 1,588,400= 49.40 TONNES.

YESTERDAY WE HAD A LOSS IN THE PRICE OF GOLD TO THE TUNE OF $13.60.…AND WITH THAT, WE HAD A HUMONGOUS GAIN IN TONNAGE OF 49.40 TONNES?????!!!!!!.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 80,360 CONTRACTS OR 8,036,000 OZ OR 249.95 TONNES (11 TRADING DAYS AND THUS AVERAGING: 7305 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAYS IN TONNES: 249.95 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 249.95/2550 x 100% TONNES = 9.80% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1123.9 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUMONGOUS SIZED SIZED INCREASE IN OI AT THE COMEX OF 8,337 DESPITE THE LOSS IN PRICING ($13.60) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7547 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7547 EFP CONTRACTS ISSUED, WE HAD A GIGANTIC GAIN OF 15,884 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7547 CONTRACTS MOVE TO LONDON AND 8,337 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE STRONG GAIN IN TOTAL OI EQUATES TO 49.40 TONNES). ..AND ALL OF THIS HUGE DEMAND OCCURRED WITH A LOSS OF $13.60 IN YESTERDAY’S TRADING AT THE COMEX???????!!!!!

we had: 1 notice(s) filed upon for 100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $7.80 TODAY

NO CHANGES IN GOLD INVENTORY AT THE GLD//

INVENTORY RESTS AT 772.46 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 16 CENTS IN PRICE TODAY:

/INVENTORY RESTS AT 310.848 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A CONSIDERABLE SIZED 1403 CONTRACTS from 188,266 DOWN TO 186,863 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 2714 FOR MAY AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2714 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 1403 CONTRACTS TO THE 2714 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 1311 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 6.555 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY AND NOW 26.835 MILLION OZ FOR MARCH.

RESULT: A CONSIDERABLE SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 30 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A GOOD SIZED 2714 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 31.07 POINTS OR 1.04% //Hang Sang CLOSED UP 160.87 POINTS OR 0.56% /The Nikkei closed UP 163.83 POINTS OR 0772%/ Australia’s all ordinaires CLOSED DOWN .03%

/Chinese yuan (ONSHORE) closed UP at 6.7134 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 58.62 dollars per barrel for WTI and 66.92 for Brent. Stocks in Europe OPENED GREEN

ONSHORE YUAN CLOSED UP // LAST AT 6.7134 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7145 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/

Bankrupt North Korea is mulling the suspension of nuclear talks with the USA. Kim will announce his decision shortly. However the sanctions are killing the country.

( zerohedge)

b) REPORT ON JAPAN

3 C/ CHINA

i)China/Last night:

4/EUROPEAN AFFAIRS

( Alasdair Macleod)

ii)DENMARK

Gatestone comments on the failed immigration policies and how this is destroying the country of Denmark

(courtesy Gatestone Institute/Hasselbalch)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Iran

Iran holds massive drone drills officially named “Way to Jerusalem” and this is alarming Israel

(courtesy zerohedge)

ii) Middle East

6. GLOBAL ISSUES

i)Boeing:

a)The flight pattern showed something was extraordinarily wrong as the plan swung up and down by hundred of feed

( zerohedge)

b)And then they found the “jackscrew” which confirmed that the Boeing 737 max 8 was set to dive:

ii)Multiple fatalities on a raid on a mosque in New Zealand’s southern most city of Christ Church.

(courtesy zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

( Hugo Salinas Price/GATA)

ii)Italy resists both the USA and the EU as they plan to invest into China’s Sick road initiative. They plan to borrow plenty of dollars form China on this matter

( London’s Financial Times/GATA)

iii)The Hong Kong dollar has been on the weaker side of its peg with the dollar and as such the Monetary authority has been spending billions of dollars defending the peg

( Bloomberg/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning

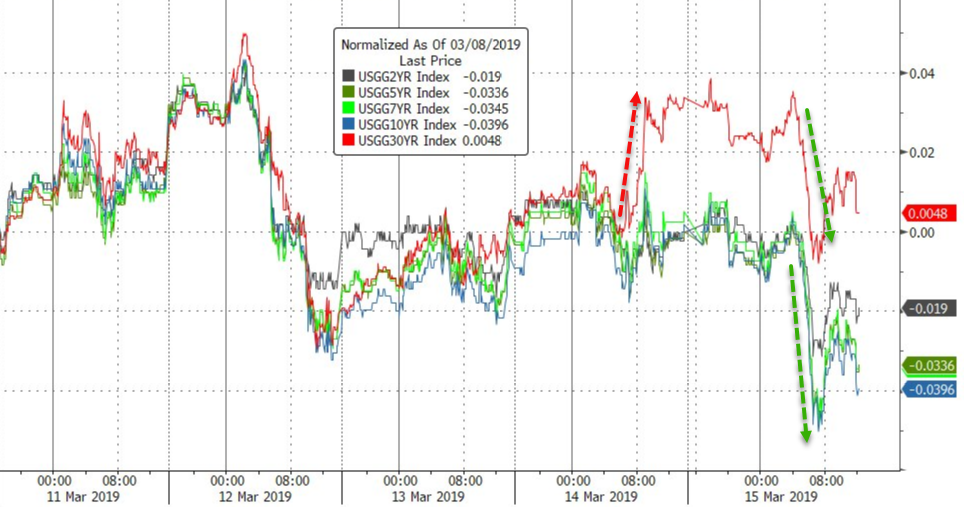

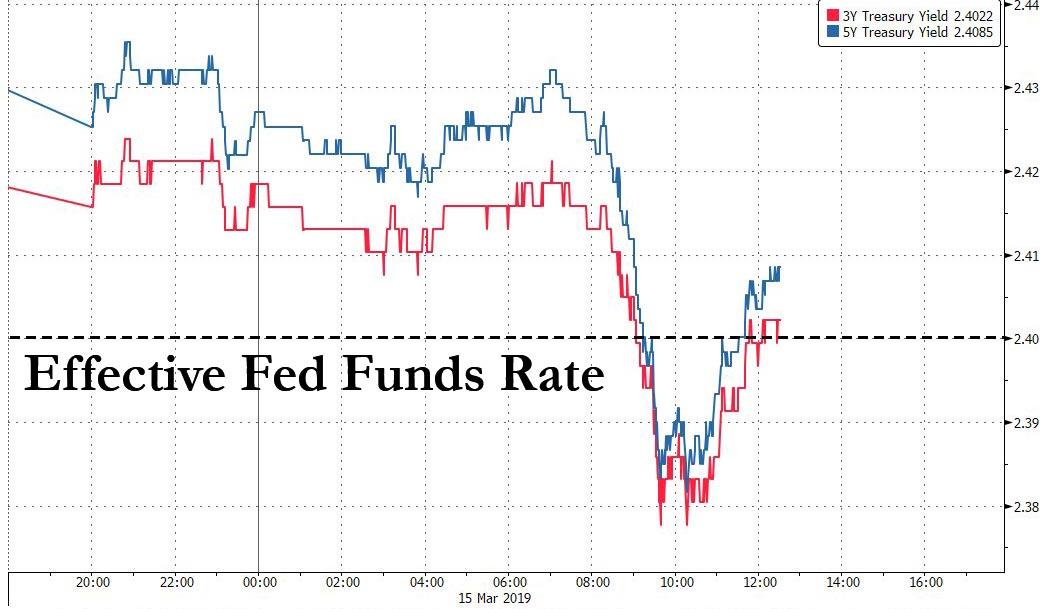

a) Very dangerous; USA 10 yr bond yield plummets to 2.58%

( zerohedge)

b) stocks falter in the early morning

(zerohedge)

ii)Market data

a)The very important NY (Empire Manufacturing Survey) reveals a huge slump and this soft data manufacturing report is at a 22 month low

( zerohedge)

c)The JOLT report shows a soaring number of job openings as well as a huge number of quits (take your job and shove it). This will probably force Powell to raise rates sometime during 2019

ii)USA ECONOMIC/GENERAL STORIES

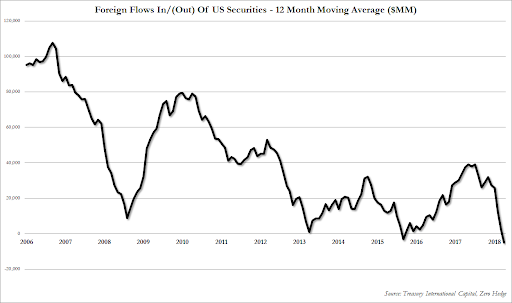

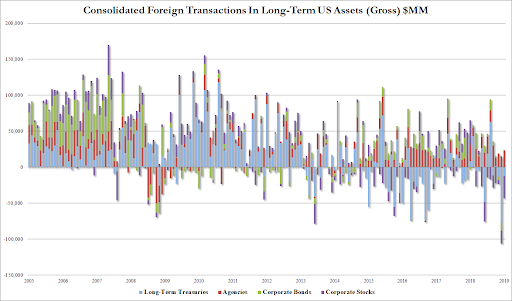

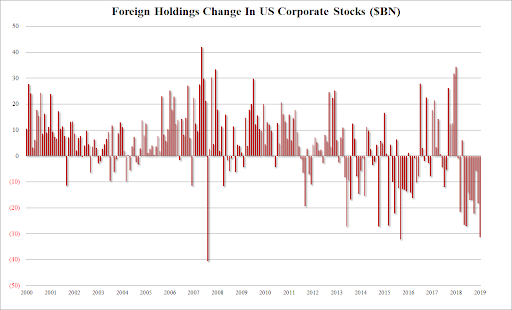

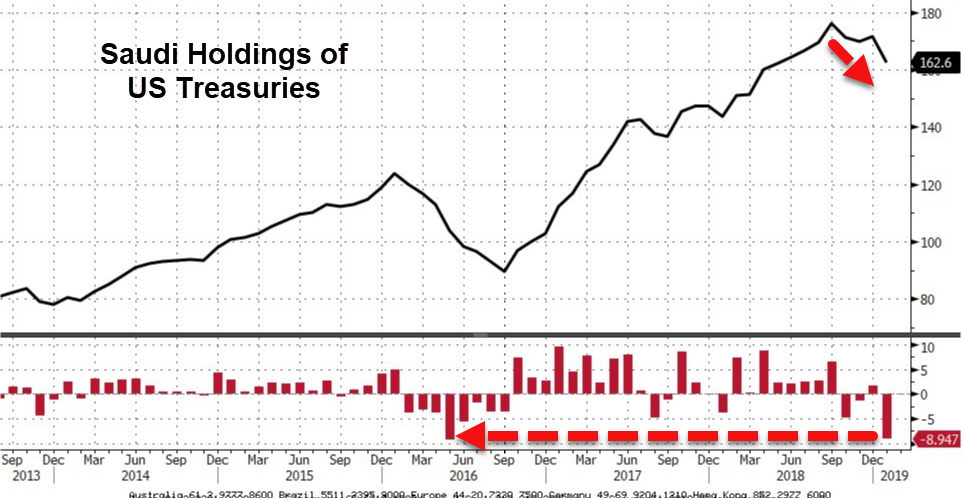

TIC report:

This is rather alarming: Foreigners dumped the most USA investments in a decade during the December through January period

(courtesy zerohedge)

iv)SWAMP STORIES

What crooks!! The DOJ and the Clinton lawyers struck a secret deal to block the FBI access to the Clinton Foundation emails. This was in the Strzok testimony held behind closed doors and kept from the public

( zerohedge)

end

Let us head over to the comex:

AFTER MARCH, WE HAVE THE NON ACTIVE DELIVERY MONTH OF APRIL. HERE: APRIL ROSE TO 799 CONTRACTS FOR A GAIN OF 11 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI FELL BY 1986 CONTRACTS DOWN TO 134,863 CONTRACTS. WE HAVE WITNESSED A MASSIVE SHORT COVERING AT THE BANKS WITH RESPECT TO SILVER COUPLED WITH CONTINUE QUEUE JUMPING……SOMETHING IS SCARING THEM TO DEATH!!!

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

Our good friend Hugo Salinas Price is interviewed by a Russian bullion dealer and he discusses government intervention into the gold/silver market.

(courtesy Hugo Salinas Price/GATA)

‘Gold bug from way back’ Salinas Price in broad interview with Russian gold advocate

Submitted by cpowell on Fri, 2019-03-15 04:47. Section: Daily Dispatches

11:47a ICT Friday, March 16, 2019

Dear Friend of GATA and Gold:

Entrepreneur and philanthropist Hugo Salinas Price, president of the Mexican Civic Association for Silver, this week was interviewed by Russian bullion dealer and gold advocate Dmitry Balkovskiy, proprietor of Goldenfront.ru, discussing government interventions against gold, destruction of the dollar-based financial system by President Trump, Russia’s increasing recognition of gold’s monetary functions, and his philosophy of life and his history in business and monetary metals causes. Salinas Price calls himself “a gold bug from way back” and explains why.

The interview is a half-hour long and can be viewed at YouTube here:

https://www.youtube.com/watch?v=e8qeM6KXZZA

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

The Hong Kong dollar has been on the weaker side of its peg with the dollar and as such the Monetary authority has been spending billions of dollars defending the peg

(courtesy Bloomberg/GATA)

Hong Kong seen spending billions more to defend currency peg

Submitted by cpowell on Fri, 2019-03-15 05:23. Section: Daily Dispatches

By Tian Chen

Bloomberg News

Thursday, March 14, 2019

This round of currency intervention in Hong Kong is far from over.

That’s according to analysts, who are watching the interplay between the amount of money in the city’s financial system and local borrowing costs. Shorting the Hong Kong dollar will remain profitable until the latter starts to go up sharply, and the monetary authority will spend at least another HK$50 billion (US$6.4 billion) defending the peg before that happens, according to Bank of America Merrill Lynch and OCBC Wing Hang Bank Ltd.

…

Hong Kong’s currency has hit the weak end of its trading band repeatedly over the past week, spurring intervention that’s cost nearly $700 million.

At the heart of the analysts’ calculus is a call on how low the city’s aggregate balance can go before banks start feeling a funding squeeze. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-03-15/hong-kong-seen-spendi…

* * *

Join GATA here:

Mining Investment Asia

Marina Bay Sands Conference and Exhibition Center

Singapore

Tuesday-Thursday, March 26-28

https://www.mininginvestmentasia.com/

Mines and Money Asia

Hong Kong Conference and Exhibition Center

Wan Chai, Hong Kong

Tuesday-Thursday, April 2-4

https://asia.minesandmoney.com/

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

Italy resists both the USA and the EU as they plan to invest into China’s Sick road initiative. They plan to borrow plenty of dollars form China on this matter

(courtesy London’s Financial Times/GATA)

Resisting U.S. and E.U., Italy plans to go into hock with China

Submitted by cpowell on Fri, 2019-03-15 05:33. Section: Daily Dispatches

Italy Eyes Loans from China’s Development Bank for ‘Belt and Road Initiative’ Projects

By Davide Ghiglione, Rachel Sanderson, and James Kynge

Financial Times, London

Friday, March 15, 2019

Italy is considering borrowing from China’s Asian Infrastructure Investment Bank as part of plans to become the first G7 country to endorse Beijing’s contentious “Belt and Road” global investment programme.

The two countries are planning to “explore all opportunities for co-operation” in Italy and “third countries,” according to the five-page draft accord obtained by the Financial Times. The wide-ranging agreement would span areas including politics, transport, logistics, and infrastructure projects.

…

In a departure from previous Belt and Road Initiative accords, the two countries would “work together with the Asian Infrastructure Investment Bank,” according to the working document.

The draft shows that Italy is in advanced talks with China and resisting pressure from Washington and Brussels to drop those discussions at a time of rising concerns over Beijing’s ambitions and potential security threat. …

… For the remainder of the report:

https://www.ft.com/content/29f4814c-467e-11e9-a965-23d669740bfb

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7134/

//OFFSHORE YUAN: 6.7145 /shanghai bourse CLOSED UP 31.87 POINTS OR 1.04% /

HANG SANG CLOSED UP 160.87 POINTS OR 0.56%

2. Nikkei closed UP 163.83 POINTS OR 0.77%

3. Europe stocks OPENED GREEN

/USA dollar index FALLS TO 96.64/Euro RISES TO 1.1319

3b Japan 10 year bond yield: RISES TO. –.03/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.70/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 58.62 and Brent: 66.92

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP /OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.09%/Italian 10 yr bond yield UP to 2.49% /SPAIN 10 YR BOND YIELD UP TO 1.19%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.40: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.81

3k Gold at $1303.80 silver at:15.37 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 13/100 in roubles/dollar) 65.31

3m oil into the 58 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.70 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0042 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1364 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.09%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.63% early this morning. Thirty year rate at 3.04%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.4673

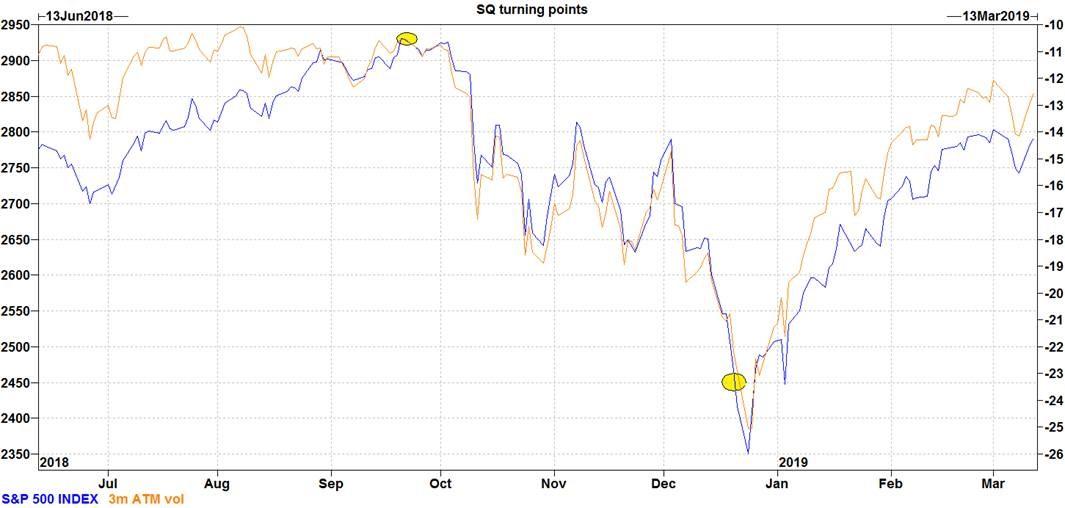

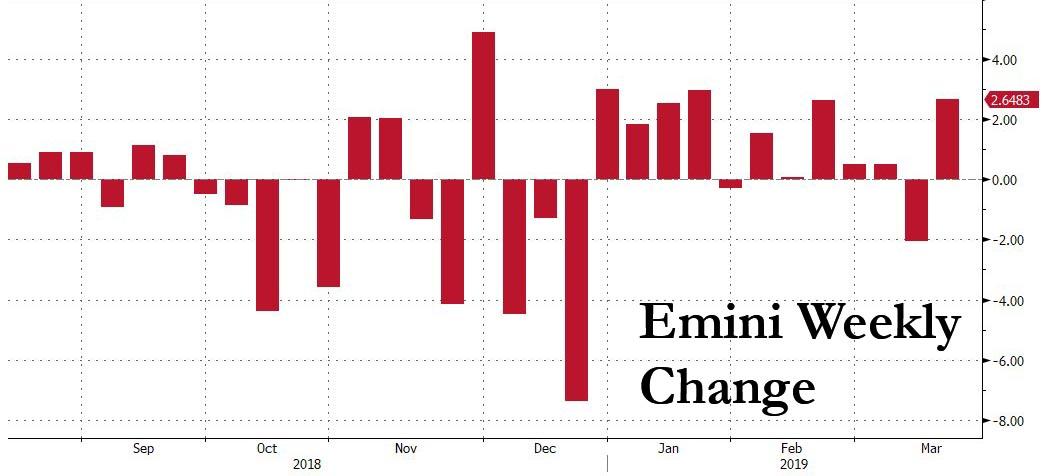

Stocks Surge As Traders Cheer “Quad Witching” Ides Of March

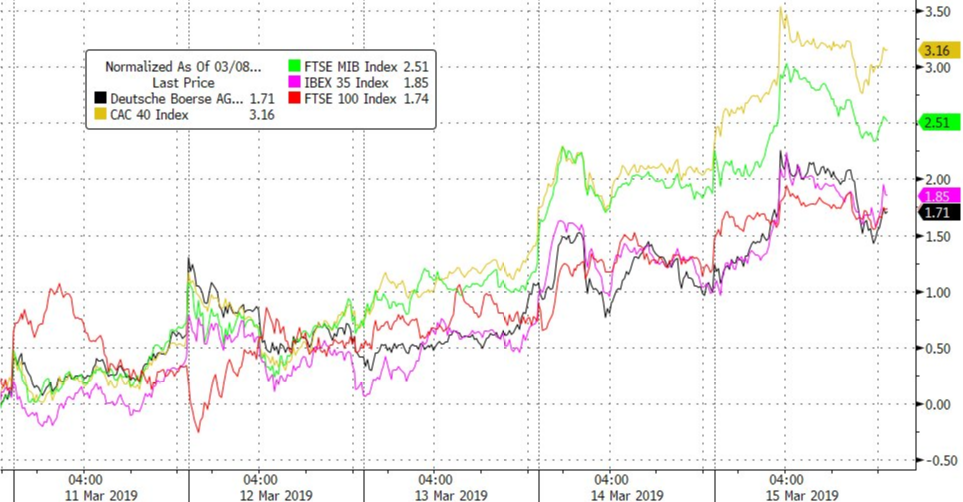

Global stocks rebounded and US equity futures jumped overnight, ignoring concerns over a delay in the Trump-Xi meeting to at least April and North Korea’s threat to resume nuclearization, after a report that U.S.-China trade talks were making progress as fears about a global slowdown faded (even as China’s latest data showed a continued slowdown) and the UK voted to reject a no deal Brexit. European stocks just printed at session highs, rising 0.8%, alongside U.S. index futures which were trading at 2,824, above the 2,817 key resistance level, as emerging-market shares advanced, even as the dollar and Treasuries held steady.

The question, as both Nomura and Goldman warned, is what happens after today’s “Quad Witching” Ides of March ends: as a reminder, today is “quadruple witching” Friday, when contracts for stock-index futures, stock-index options, individual stock options and individual stock futures all expire. The risk is that both prior “witches” took place just ahead of major reversals in the S&P, the first in September, just as the market peaked, the second in December, just before the trough.

For now, however, it is shaping up as another impressive week for US stocks, which have not only erased all of last week’s losses but are set for their second best week of the year.

Sentiment was boosted after China’s Xinhua reported – for the nth time – that Chinese Vice Premier Liu He spoke by telephone with Treasury Secretary Steven Mnuchin and Trade Representative Robert Lightizer, and the two sides made substantive progress on trade, the news agency Xinhua reported.

Gains in U.K. shares and European technology companies led Europe’s Stoxx 600 to a five-month high after Britain’s parliamentary vote on Brexit, lifting futures on the S&P 500, Dow and Nasdaq. Earlier, Asian markets rose from Tokyo to Beijing, where the Chinese government said it would cut value-added taxes, reinforcing expectations for an eventual pick-up in the second-largest economy and helping push the Australian and New Zealand currencies higher.

“We view the overall outcome of this week’s votes … as positive for UK assets,” strategists at BNP Paribas wrote in a research note. “Indeed, the pound has risen by 2 percent on the week. Yet, while most of the routes ahead now look net positive, we still expect a bumpy path.”

In Asia, MSCI’s broadest index of Asia-Pacific shares outside of Japan gained over half a percent. MSCI’s broadest, All-Country World Index was up 1 percent on the day and was set for its best week since early January.

The Shanghai Composite Index added 1 percent and Japan’s Nikkei climbed 0.8 percent. South Korea’s KOSPI rose nearly 1 percent. The index had risen as much as 1.2 percent but gave up some gains following reports that North Korea might suspend nuclear talks with the United States. Comments from Chinese Premier Li Keqiang also helped sentiment. His remarks suggested Beijing is ready to roll out more forceful stimulus to bolster China’s economy.

To boost optimism, China also promised billions in tax cuts and infrastructure spending, as weakening domestic demand and the trade war with the United States curbs economic growth.

“China and Europe had been two of the key areas of concern at the start of 2019 and even though there is still much uncertainty, targeted fiscal stimulus in China (VAT cut April 1) and potentially some clarity emerging on Brexit over coming weeks could improve sentiment,” strategists at ING Bank wrote in a note to clients.

In the latest trade news, the most notable development was that Chinese Vice Premier Liu He conducted a phone call with US Treasury Secretary Mnuchin and Trade Representative Lighthizer in which China and US were said to have made further substantive progress on trade discussions, while Mnuchin had earlier commented that he is pleased with progress on trade talks with China and expects elements of Chinese trade talks to be resolved in the near future. Separately President Trump said we will have news on China trade deal in the next 3-4 weeks one way or the other, while he added that China has been very responsible and very reasonable. In related news, there were also earlier reports which suggested China was proposing tying in an official state visit by President Xi to a US trade deal.

In other China-related news, Premier Li said China faces new downward pressure but added they will not let growth slip out of reasonable range and that China can use reserve requirements as well as interest rates to support the economy. Premier Li added China will cut VAT tax from April 1st and will tighten its belt due to tax cuts, while he hopes US-China trade talks achieve results.

In the top overnight geopolitical news, North Korea is considering suspending nuclear discussions with US and does not intend to yield to US demands, while leader Kim is set to make an official announcement of his position, according to the Deputy Foreign Minister Choe Son Hui. Elsewhere other reports also noted that Kim Jong Un may rethink moratorium on missile launches and that the US threw away a golden opportunity at the Hanoi summit.

In currencies the dollar index slipped 0.2 percent to 96.619 after rising 0.25 percent on Thursday to recover from a nine-day trough of 96.385. The U.S. currency was flat at 111.74 yen. It had dipped to 111.49 yen after the Bank of Japan’s left interest rates unchanged. The central bank offered a bleaker assessment of exports and output, as global demand waned. Observers said, that it may be too early to expect the BOJ to ease policy further.

The pound strengthened at the end of a week made volatile by critical votes on Brexit in Parliament. Prime Minister Theresa May won the endorsement of British politicians to seek a Brexit delay. The euro edged up 0.1 percent to $1.1315 after slipping 0.2 percent overnight.

Elsewhere, in commodities oil prices rose as investors focused on global production cuts and supply disruptions in Venezuela. U.S. crude futures rose 0.2 percent to $58.74 per barrel, holding close to Thursday’s four-month peak of $58.74. Brent was 0.25 percent higher at $67.39.

Today’s expected data include industrial production and Empire State Manufacturing Survey. Linde and Stella-Jones are reporting earnings

Market Snapshot

- S&P 500 futures up 0.3% to 2,814.25

- STOXX Europe 600 up 0.2% to 379.13

- MXAP up 0.7% to 158.86

- MXAPJ up 0.6% to 524.65

- Nikkei up 0.8% to 21,450.85

- Topix up 0.9% to 1,602.63

- Hang Seng Index up 0.6% to 29,012.26

- Shanghai Composite up 1% to 3,021.75

- Sensex up 1% to 38,131.78

- Australia S&P/ASX 200 down 0.07% to 6,175.17

- Kospi up 1% to 2,176.11

- German 10Y yield fell 0.3 bps to 0.083%

- Euro up 0.2% to $1.1325

- Italian 10Y yield fell 5.0 bps to 2.147%

- Spanish 10Y yield rose 0.3 bps to 1.194%

- Brent futures up 0.5% to $67.57/bbl

- Gold spot up 0.6% to $1,303.35

- U.S. Dollar Index down 0.2% to 96.62

Top Overnight News from Bloomberg

- Chinese Premier Li Keqiang said China will stick to its current targeted economic support strategy and resist the temptation to engage in large-scale stimulus like quantitative easing or a massive expansion in public spending

- Prime Minister Theresa May kept her deal with the European Union on life support by winning the backing of British politicians to seek a delay to Brexit just 48 hours after her plan looked dead and buried

- Bank of Japan Governor Haruhiko Kuroda defended the 2 percent inflation target that guides his monetary-stimulus program after the government advocated taking a flexible approach to the goal; The Bank of Japan left its monetary stimulus program unchanged as it downgraded its assessment of exports, factory output and overseas economies

- A meeting between President Donald Trump and President Xi Jinping to sign an agreement to end their trade war won’t occur this month and is more likely to happen in April at the earliest, three people familiar with the matter said

- North Korean Vice Foreign Minister Choe Son Hui said Kim Jong Un would decide soon whether to keep talking with the U.S. and maintaining his moratorium on missile launches and nuclear tests, AP reports

- China won’t resort to using quantitative easing or massive deficit spending in order to support the economy because such approaches would store up problems for the future, Premier Li Keqiang said.

- The Senate voted to block President Donald Trump’s declaration of a national emergency to pay for a wall at the border with Mexico, setting up his first veto and highlighting a growing willingness by Republicans in the chamber to split with their president

- Uncertainty over U.S. waivers for buyers of Iranian oil is starting to grip the market again, under very different circumstances than when American sanctions were set to go into effect last year

- Mario Draghi’s latest stimulus salvo means his successor as European Central Bank chief may not be forced into the kind of monetary policy U-turn he once faced; Draghi has set in place the conditions to keep the euro zone in easing mode until he leaves office

- One of the potential candidates to succeed Mario Draghi as European Central Bank president is pushing a review of the institution’s monetary-policy strategy to deal with the risk it may never reach its inflation goal

- OPEC nations have enough spare crude oil to make up for any supply shock from the escalating crisis in Venezuela, the International Energy Agency said

Asian stocks traded mostly positive across the board as US-China trade optimism helped the region shake off the negative lead from the US, where sentiment was subdued by growth concerns following recent discouraging data from China and the reported delay in the Trump-Xi summit. ASX 200 (-0.1%) and Nikkei 225 (+0.8%) were mixed with upside in Australia capped as weakness in mining names and financials offset the continued outperformance in energy, while the Japanese benchmark coat-tailed on recent currency moves. Elsewhere, Hang Seng (+0.6%) and Shanghai Comp. (+1.0%) were higher as overnight trade-related news flow spurred optimism including comments from President Trump that we will have news regarding a China trade deal in the next 3-4 weeks and although he included a ‘one way or the other’ caveat, he suggested that people will be talking about it for a long time and that China has been very reasonable. In addition, Chinese officials also contributed to the trade hopes after the NPC approved Foreign Investment law reforms dealing with forced tech transfers and IP theft which is seen as an attempt to appease US concerns, while Chinese Premier Li noted that China can use reserve requirements as well as interest rates to support the economy and confirmed VAT tax cuts will begin from next month. Finally, 10yr JGBs were relatively flat with demand dampened as focus centred on riskier assets and after the BoJ policy announcement proved to be a non-event in which it maintained policy settings and downgraded assessments on exports and output as expected.

Top Asian News

- China Vows to Stick to Targeted Stimulus Amid Jobless Pressure

- King of India Bond Sales Warns of Worst Crisis Since Lehman

Major European indices have remained firm after opening with mild gains [Euro Stoxx 50 +1.4%], continuing from overnight where risk sentiment improved following US-China trade optimism. Sectors are largely in the green, although there is some mild underperformance in healthcare names. Weighed on simultaneously by a downgrade at Citi Group and reports that the Co’s India operations are the focus of a Singapore probe are Wirecard (-9.1%) who are at the bottom of the Stoxx 600, although this was later refuted by the Co. Elsewhere, and towards the top of the Dax, are BMW (+1.0%) who have been in focus after warning of headwinds impacting the sector and reported FY18 revenue slightly above expectations and EBIT margin above target; which subsequently led to short-term volatility in Co. shares. Separately, UBS (-0.9%) are in the red after their annual trade report where the Co. stated that provisions for litigation, regulatory and other matters reduced FY18 operating profit before tax and net profit for shareholders by USD 382mln.

Top European News

- UBS Setting Aside Just $516 Million to Cover Record French Fine

- H&M’s Lower Prices Lift Sales as It Narrows Gap With Zara

- Hedge Funds Fighting Over Interserve Head for Showdown in London

- Swedbank May Have Handled Over $10 Billion in Suspect Flows

In FX, The Kiwi has rebounded firmly from lows close to 0.6800 vs its US counterpart after a more conciliatory tone from both sides of the US-China trade divide overnight compared to reports circling on Thursday highlighting ongoing issues that remain unresolved and have rolled back the likely date of a Trump-Xi official signing-off Summit. Nzd/Usd is currently towards the top of a 0.6858-24 range, but hampered somewhat by cross-winds as Aud/Nzd consolidates recovery gains above 1.0300 and the Aussie also reclaims lost ground against the Usd to retest resistance ahead of 0.7100.

- CAD/EUR/GBP – Also benefiting from the Greenback’s broad loss of momentum as the DXY failed to sustain yesterday’s more bullish technical impulses beyond 96.821 and closer to the 97.000 handle. The Loonie is also deriving some impetus from steadier oil prices and could get a helping hand from Canadian manufacturing sales if expectations for a rebound are confirmed. Usd/Cad is hovering just above 1.3300 and back to within striking distance of the 200 DMA. Meanwhile, the single currency continues to try and establish/build a base on the 1.1300 handle, but resistance around the recent 1.1340 high and mega option expiry interest remain formidable barriers to overcome, with 1.9 bn at the big figure and 3.3 bn running off between 1.305-25 at Friday’s NY cut. Turning to the Pound, and a bout of selling saw Cable test underlying bids/support ahead of 1.3200, while Eur/Gbp spiked to 0.8575, but with little obvious in the way of a catalyst and for once relative quiet on the Brexit front the relatively rapid moves have subsequently reversed to circa 1.3275 and 0.8525 respectively.

- JPY/CHF – Both relatively flat vs the Dollar and still rangebound, as Usd/Jpy meanders from 111.90 to 111.50 and just above the 200 DMA (111.44) in wake of a dovish BoJ policy meeting, as widely anticipated. Decent expiries from 111.50-65 (1.1 bn) could underpin the headline pair, while 112.00 and a Fib at 112.08 are keeping the upside in check. The Franc is even more contained within 1.0045-20 and vs the Eur around 1.1350 ahead of next week’s quarterly SNB policy review.

- SEK/NOK – The Scandi Crowns looks set to end the week on the front foot having regained the initiative over the Euro and crossed psychological/technical levels, and with some added backing from a US bank advocating long positions via the Eur/Sek cross and Usd/Nok – see our headline feed for more details.

In commodities,Brent and WTI prices are softer heading into the weekend, a sharp decline this morning saw prices drop significantly below the day’s ranges, with no significant fundamental news behind this. This morning saw the release of the IEA’s monthly report, which maintained the 2019 global oil demand growth forecasts at 1.4mln BPD, which has been supported by strong non-OECD consumption. IEA state that OPEC crude production in Feb was 30.68mln BPD, a decrease of 240k BPD; due to losses in Venezuela and lower output from both Saudi Arabia and Iraq. Adding that preliminary data for February points to a sharp drop in inventories. Looking ahead on the calendar sees the Baker Hughes rig count at 17:00 GMT due to the US time change, where total rigs decreased by 11 to 1027. Gold (+0.4%) is firmer in spite of the improvement in risk sentiment, potentially due to the yellow metal retracing some of yesterday’s decline where it dropped below USD 1300/oz, for reference spot gold is currently trading around USD 1302/oz. Separately, Indian gold demand may drop in May due to restrictions surrounding cash movement an Industry Official has reported. Elsewhere, copper prices improved overnight on the risk sentiment.

Looking at the day ahead, we get February industrial production (+0.4% mom expected), March empire manufacturing (+10.0 expected), January JOLTS report and preliminary March University of Michigan consumer sentiment report (95.7 expected). The ECB’s Rehn is also due to speak while the IEA monthly oil report is due out.

US Event Calendar

- 8:30am: Empire Manufacturing, est. 10, prior 8.8

- 9:15am: Industrial Production MoM, est. 0.4%, prior -0.6%; Manufacturing (SIC) Production, est. 0.1%, prior -0.9%

- 10am: JOLTS Job Openings, est. 7,225, prior 7,335

- 10am: U. of Mich. Sentiment, est. 95.7, prior 93.8; Current Conditions, est. 112, prior 108.5; Expectations, est. 88.1, prior 84.4

- 4pm: Net Long-term TIC Flows, prior $48.3b deficit; Total Net TIC Flows, prior $33.1b deficit

DB’s Jim Reid concludes the overnight wrap

Last week I discussed a new box set I’d been watching. Well this week’s evening entertainment has been streamed live from the House of Commons. I even missed a bit of Liverpool’s glorious victory in Munich on Wednesday to keep an eye on the manoeuvrings of our politicians. I’ve always loved politics and was a member of a UK political party as a teenager (partly in a failed attempt to impress a young lady). However nothing has beaten this week for drama, subterfuge and sub-plots. Last night’s votes were slightly on the more tame side but there were still some surprises. The main (and expected) event was the House of Commons overwhelmingly voting (412-202) to extend Article 50 out to June 30th. Earlier, an amendment to enable a second referendum suffered a big defeat (344-85) so we’re a very long way from such an outcome but Mr Corbyn left it firmly on the table in comments after the votes which reflects their strategic position. The more interesting vote was a narrow defeat (314-312) for an amendment that would have allowed Parliament to take control of the process with indicative votes in the last week of March. The government had already promised this in early April if no other deal is reached beforehand so the big difference is timing and the fact that the government and not Parliament will be still be controlling it. The pound had depreciated as much as -0.98% early in the session ahead of the votes, but partially pared its losses to end the day -0.72% weaker versus the dollar. It’s still +1.74% stronger this week as the direction of travel still appears to be toward a softer Brexit and reduced risks of a no-deal outcome.

So what next? It looks likely that Mrs May will bring the 3rd version of the WA to Parliament on Tuesday, ahead of the European summit next Thursday/Friday. If she fails the EU will likely insist on a long extension and then we’ll either move straight to indicative votes or Mrs May will try a 4th time first. There was some evidence yesterday that more Tory MPs and the DUP are engaging with the government to see how they can back the WA. According to Reuters, Attorney General Cox is in active discussions about how the UK could legally and unilaterally exit the Irish backstop if it wanted to in the future. The key will be if anything ends up changing the DUP’s mind. So far there are no firm conclusions but it’s clear discussions are ongoing.

In the world outside of Westminster risk took a bit of a pause for breath last night in the US following what had been a strong start to the week. Indeed on a light newsflow day, the S&P 500, DOW and NASDAQ closed -0.09%, +0.03% and -0.16% respectively after Europe closed higher with the STOXX 600 finishing +0.78%. Banks also had a good day in Europe (+0.68%), boosted by a +2.1bps rise in bund yields and sentiment towards Italy improved as well. Italian banks gained +1.09% and BTP yields fell -5.1bps, helped by optimistic comments from the ECB’s Benoit Coeure who said that Italy is not a threat to the euro area. The VIX held steady around 13.50,within 0.1pts of its year-to-date low, while the same can be said for the MOVE index (+0.7pts yesterday) and less than a point off its year-to-date low. The same situation applies the V2X in Europe, while the CVIX index of currency volatility has actually dropped to its lowest level in 14 months. So it’s very much back to the bottom of the range for volatility across asset classes. Meanwhile, cash HY spreads were bps -5bps and -1bps tighter in Europe and the US while Treasuries were close to flat.

In Asia this morning we’ve had the BoJ meeting where the central bank decided to maintain its policy rates and asset purchases, as was widely expected, while taking a gloomier outlook for the economy. The BoJ said that Japan’s economy continued to expand moderately, but the global slowdown had caused “some weakness” recently in exports and industrial production but added that the global economy would keep growing moderately and in turn support a rising trend in Japanese exports and a further expansion of the domestic economy. In the meantime, Japan’s Finance Minister Taro Aso said that the BoJ should take a flexible view of the 2% inflation target.

Yields on 10y JGBs are up +0.7bps to -0.045%. We should get further clarity on the BoJ’s view of the economy and the BoJ’s likely appetite for flexibility around the 2% inflation target from Governor Kuroda’s presser (06:30 GMT) which would have already started by the time this reaches your inbox. Elsewhere, China’s Premier Li Keqiang said in a speech at the NPC that China will use tools like reserve-requirement ratios and interest rates to support a slowing economy and won’t take the route of monetary easing (QE or massive deficit spending) as such approaches would lead to problems in the future. He also confirmed that announced tax cuts and social security reductions at the NPC would take effect from April 1 and May 1 respectively while adding that China won’t let the major economic indicators slide out of their proper range. Signifying the continued focus of China’s government towards easing credit access for the SMEs, Li Keqiang said that China will take multiple measures to lower the funding cost for SMEs by 1% this year. On the sticking points in the trade negotiations with the US, Li said that China will revise its intellectual property protection law and added that China will “certainly” implement measures to further open up its market.

In other news, as per Bloomberg Mao Shengyong, the spokesman of China’s National Bureau of Statistics attributed the recent weakness in China’s economic data to the Lunar New Year holidays. He said that many factories and companies close near the holidays thereby usually hurting industrial output in the 4 days ahead of Lunar New Year holidays and 15 to 20 days after it. Meanwhile, China also passed a foreign investment law today which will take effect from January 1, 2020. Under the updated new law China will treat all companies registered in China equally, as opposed to the current division between local and foreign businesses, according to lawmakers. Chinese government support will also apply equally to foreign firms, and their applications for operating licenses won’t be treated differently from domestic rivals while forced technology transfer will be banned. Elsewhere, Russian News Agency Tass has reported – citing North Korean deputy foreign minister Choe Son Hui – that North Korea is reviewing plans to suspend denuclearization talks with the US while adding that North Korea’s leader Kim Jong Un will make an announcement about his decision on this.

Markets in Asia are heading higher with China’s bourses leading the advance – the Shanghai Comp (+1.54%), CSI (+1.85%) and Shenzhen Comp (+1.88%) are all up on the back of above mentioned growth supportive speech from China’s Premier Li Keqiang with Trump’s favorable comments on China (mentioned below), likely also playing a part. The Nikkei (+1.02%), Hang Seng (+0.65%) and Kospi (+0.63%) are also up. Elsewhere, futures on the S&P 500 are up +0.24% and 10y treasury yield is down -0.9bp this morning. In the US, markets could experience higher levels of volatility today on account of “quadruple witching.”

The trade headlines yesterday included the news that President Trump and President Xi Jinping’s meeting was likely to be pushed back to April at the earliest according to Bloomberg. Further, late yesterday evening President Trump said that we will probably know in next three or four weeks about possible trade deal with China, thereby seconding the above Bloomberg story. He also added that China has been behaving very responsible and reasonable. Will there be a Brexit or US/China deal first? Risk was a bit weaker when that trade headline emerged although quickly reversed much of it. More durably, the dollar strengthened +0.22% on the day and the offshore yuan traded -0.32% weaker. The prospect of tariffs remaining in place for longer would be bullish the dollar, all else equal. A reminder that Lighthizer sounded a bit more cautious on trade talks following comments earlier this week. Late afternoon Trump reiterated that “we’re doing very well with China talks” and that “we’re getting what we have to get”. However he also added the caveat that we “can’t say if we’ll strike a final deal with China”.

On a more micro note, General Electric’s share price rose +2.96% and as much as +4.79% earlier after the market latched onto the latest guidance from management that cash flow bleed this year will be no more than $2bn. Credit investors also welcomed the news with 2.7% 22s for example -10.5bps tighter. A reminder that it was General Electric that spooked credit markets towards the back end of last year.

While we’re on that subject, yesterday we published a note looking at USD BBB ‘Super Issuers’. In it we find that these issuers are significantly on the rise and have more debt outstanding than ever before. However, the market is no less concentrated and is below the extremes of the early 2000s. That being said, fundamentals for this cohort are trending in the wrong direction. The fact that the majority of issuers appear to be deleveraging or at least still targeting an IG rating should lend some support, but intention and reality do not always turn out to be the same thing. See the link to the report here .

Staying with credit Michal Jezek has just written up DB’s 9th annual bank capital conference that took place on Wednesday. This included an interview with myself and ECB governor Nowotny. See here for the report.

In other news, yesterday’s data didn’t add much to the mix. In the US the latest weekly initial jobless claims print came in at 229k, a shade higher than the 225k expected and up from 223k the week prior. While that is a four-week high, the four-week moving average nudged down to 224k and has now dropped for three consecutive weeks. Meanwhile the February import price index reading came in at +0.1% mom ex petrol (vs. -0.1% expected) – a still benign reading – while March new home sales slumped (-6.9% vs. +0.2% expected), albeit offset by upward revisions in the prior two months.

In Europe the final February CPI revisions for both Germany (+0.5% mom) and France (+0.1% mom) were left unchanged versus the initial estimates. As you’ll see below we get revisions to the broader Euro Area reading today.

Outside of the usual Brexit drama, the highlights from the scheduled data releases today are the final February CPI revisions for the Euro Area (no change in the +1.0% yoy core expected), and February industrial production (+0.4% mom expected), March empire manufacturing (+10.0 expected), January JOLTS report and preliminary March University of Michigan consumer sentiment report (95.7 expected) in the US. The ECB’s Rehn is also due to speak while the IEA monthly oil report is due out.

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 31.07 POINTS OR 1.04% //Hang Sang CLOSED UP 160.87 POINTS OR 0.56% /The Nikkei closed UP 163.83 POINTS OR 0772%/ Australia’s all ordinaires CLOSED DOWN .03%

/Chinese yuan (ONSHORE) closed UP at 6.7134 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 58.62 dollars per barrel for WTI and 66.92 for Brent. Stocks in Europe OPENED GREEN

ONSHORE YUAN CLOSED UP // LAST AT 6.7134 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7145 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

3 C CHINA

China/Last night:

The plunge protection team abandons the Chinese stock market. The small cap Chi Next has seen the last 3 days of notable absence from the PPT

(courtesy zerohedge)

The Ever-Changing Time-Line Of Trump’s Trade Deal With China

Authored by Mike Shedlock via MishTalk,

Trump has changed his tune on a trade deal with China so many times it’s hard to count.

- In December, Trump gave China 90 days to conclude a deal Otherwise. Trump said he would boost tariffs on $200 billion of Chinese goods to 25% from the current 10%.Those 90 days ended March 1.

- On December 31, I noted Trump Hails “Big Progress” on Trade Deal With China. I commented “Supposedly there is ‘big progress’ on a comprehensive trade deal with China. Color me skeptical.”

- On January 19, I noted China Pledges US Buying Spree to Reduce Trade Surplus With US to Zero By 2024. I commented “In discussions that are not yet public, and will likely be empty promises, sources say China Offers a Path to Eliminate U.S. Trade Imbalance.”

- On February 22, the Washington Post reported Trump says he expects to meet with China’s Xi and finalize new trade deal but Trump would not rule out extending the deadline beyond March 1.

- On February 24, Trump Tweeted there was “substantial progress on intellectual property” and suspended tariffs.

- On February 25, I noted Hooray! “Substantial” Progress With China (Just Don’t Ask Where) in response to Trump’s Tweets.

- At the end of February, Trump expected a small delay in signing.

- On March 2, I noted Trump Assails WTO “Straitjacket”, Attempts Pocket Veto of Entire Organization.

- On March 12, the Washington Post stated U.S. Trade Representative Robert E. Lighthizer told the Senate Finance Committee “Our hope is that we are in the final weeks” of negotiations. However, Schumer said on the Senate floor, “It is abundantly clear that China is playing us.”

- On March 13, Trump stated that he is in No Rush to Complete China Trade Deal. “I think things are going along very well – we’ll just see what the date is,” Trump told reporters at the White House.

Drum Roll Please…….

Today, Bloomberg reports China and U.S. to Push Back Trump-Xi Meeting to at Least April

The key words here are “at least” April. Lighthizer warned ‘major issues’ remained outstanding in talks.

90 Days Till Who Knows When

We have gone from the certainty of “90 days or else” to canceled tariffs and who knows when.

As I said at the outset, there will be a deal, just don’t expect much substance to it or for China to honor it if there is.

Meanwhile, I am sure a pause in Tariffs and a delay in the deal suits China just fine.

For the record, I think the pause in tariffs is a good thing because tariffs are a bad idea in the first place. US farmers were getting killed by China’s retaliations.

Any deal that eliminates tariffs and retaliations will be a good thing, even if it otherwise accomplishes nothing.

end

Interesting: Chinese Premier Li vows no massive stimulus despite the fact that Beijing has already launched its massive QE

(courtesy zerohedge)

China Premier Vows No Massive Stimulus As Beijing Launches Massive Stimulus

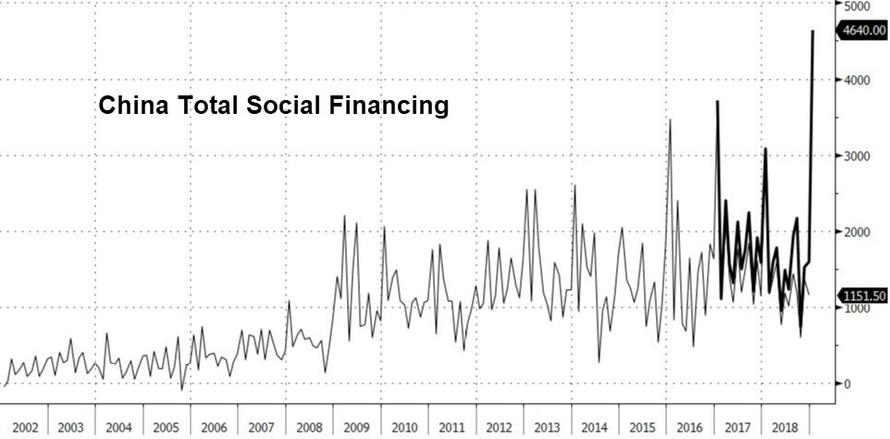

When it comes to China, the past decade revealed two things beyond a shadow of a doubt: i) all of the country’s economic data is utterly meaningless as it is entirely fabricated (in this measure it is not much different from other developed nations), goalseeked to fit a specific political narrative, and ii) Beijing has an annoying Trotskyite habit of doing precisely what it vows not to do or accuses others of doing.

A good example of the latter was again observed last night, when Premier Li Keqiang said that China will stick to its current targeted economic support strategy and resist the temptation to engage in large-scale stimulus like quantitative easing or a massive expansion in public spending.

“We certainly need to take strong measures to face the downward pressure,” Li told a news conference Friday at the close of the annual National People’s Congress session in Beijing. “An indiscriminate approach may work in the short run but may lead to future problems. Thus it’s not a viable option. Our choice is to energize market players.”

This is ironic because just over a month ago, China quietly launched a quasi-QE program in the form of the PBOC buying perpetual bonds issued by local banks, to flood the system with liquidity and achieve the same end goal as more conventional quantitative easing, and which Rabobank described as a means to keep China’s “Ponzi scheme afloat.”

Just as ironic was Li’s vow not to flood the economy with stimulus, read new debt, one month after the PBOC flooded the economy with a record amount of new debt. Of course, this being China, nobody inside the country will dare to call out Beijing on its hypocrisy for fears of immediate incarceration, as for outside economists, all they care about is to make sure that China will continue its massive reflation of both the domestic and global economy, just to make sure their own optimistic forecast are met, even it means even more pain down the road.

It wasn’t just Li’s double-faced narrative that dominated the last day for the NPC: China’s annual gathering of leaders that started last week has delivered a raft of policy initiatives, while maintaining a focus on using tax cuts and other “targeted” measures to address the weakness in output, Bloomberg reports. Sparking fears in Beijing – which is mostly terrified of a lower/middle class uprising resulting from mass layoffs – China’s deepening slowdown has pushed unemployment higher, intensifying pressure on that calibrated stimulus strategy.

Sure enough, Li reiterated the government’s new emphasis on preventing large-scale job losses in the wake of the slowdown, a day after data showed the unemployment jumped to 5.3 percent in February, the highest level in two years.

Taking a cue from the Trump playbook, Li said the “employment first” strategy put jobs on the same level of priority as fiscal and monetary policy. He also elevated the number of jobs the economy will create “in practice” this year to 13 million from the 11 million target announced last week in his economic policy report although amid reports of mass layoffs in trade-linked companies, it is not exactly clear how Beijing will force companies to hire more people than they are currently firing.

Meanwhile, as part of a separate massive fiscal stimulus, the tax cuts announced last week could exceed the proposed plan of 2 trillion yuan ($298 billion) this year. Included in that total is a cut of 3% to the top bracket of value-added tax aimed at benefiting the manufacturing sector. Policy makers have also cut bank reserve requirements multiple times since last year, releasing liquidity for lending. Li indicated use of that tool would continue.

Separately, Li also hinted at more wholesale monetary easing: “We can use price tools such as reserve-requirement ratios, interest rates,” Li said. “We are not going toward monetary easing, but effectively supporting the real economy.”

The bottom line, according to Li: keep the economy stable and within its historical range: “We won’t let the major economic indicators slide out of their proper range.” Supposedly this means Beijing will be forced to hire even more excel goalseekers to make sure “data” does not deviate from its political mandate.

Curiously, the record size of the tax cut wasn’t matched by an equivalent expansion in the size of the government’s targeted budget deficit, which was nudged wider to 2.8% of gross domestic product from 2.6% in 2018. As part of measures to plug the gap, Li announced that the government has already raised 1 trillion yuan in transferred profits from state-owned enterprises and banks.

How will the government achieve this seemingly impossible mathematical quest? Simple: by admitting that China is a ponzi, where the profits generated from new debt are recycled into the government:

“The central government is determined to ask specific financial institutions and some state-owned enterprises to increase the profits they turn into the national treasury,” Li said. “We’ll also take back the idle funds accumulated over a long time.”

* * *

Besides unveiling how China hopes to kick the financial can for a few more years, Li also touched on some other key topics such as U.S.-China ties, where Li stuck to the message China has pushed for months, reiterating that there were “broad common interests” between the two sides and that they should seek “win-win” outcomes. He said that trade talks between were still underway and that China hoped that “good outcomes will be delivered out of those consultations.”

Li also responded to criticisms from the U.S. and other Western countries that Chinese tech giant Huawei Technologies Co. helps the Chinese government spy. Chinese national security laws require that any organizations must cooperate with national intelligence work – raising fears that the government could lean on Huawei to compromise a telecommunications network in another country.

“Let me tell you explicitly. This is not consistent with Chinese law, this is not how China behaves,” Li said. “We did not do that in the past and will not do that in the future.”

Coming from a man who vowed not to engage in massive stimulus just as China is engaging in massive stimulus, the last statement is hardly a surprise.

4.EUROPEAN AFFAIRS

(courtesy Alasdair Macleod)

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

Iran

Iran holds massive drone drills officially named “Way to Jerusalem” and this is alarming Israel

(courtesy zerohedge)

Iran Holds Massive Drone Drills Called “Way To Jerusalem” In Persian Gulf

Iran unveiled that it launched a massive drone exercise to showcase its military and technological prowess on Thursday. Given that it involves some 50 Iranian-made drones and is officially named “Way to Jerusalem” exercises (or “Towards al-Quds 1”), it has been met with alarm in Israel especially considering many were armed drones operating along key choke points in the Persian Gulf.

The Islamic Revolutionary Guard Corps (IRGC) described the military drills as Iran’s largest exercise of its kind to date, and occurred mostly near the strategic Strait of Hormuz. State-run Fars and Tasnim news agencies described the operation as including, “for the first time, 50 Iranian drones on the RQ-170 [US Sentinel] model operated with a number of assault and combat drones.”

According to Iranian defense officials, including IRGC Ground Force commander Maj.-Gen. Golam Ali Rashid, who helped command the operation, the drone “offensive operation” saw UAVs operate simultaneously at distances of more than 1,000 km away from each other (about 620 miles) and struck remote targets with “high precision.”

Gen. Rashid told state sources that contrary to the western perception that the Iranian Republic is failing in technological advancement, instead “today we are witnessing the strongest maneuvers of the IRGC’s Aerospace Forces.” He bragged that enemies would be “humiliated and feel shame,” according to state media.

And the IRGC’s second-in-command, Brigadier General Hossein Salami, said ironically while commenting on the massive drone exercises that US “sanctions bore fruit.”

He said, “Despite the empty and satanic dreams of the US and other ill-wishers of the Iranian nation, we witnessed tens of modern and advanced domestic RQ-170s and other types of combat drones in flight during a major drill and unique offensive operation.”

The drills were reportedly conducted across several provinces of Iran, but mostly concentrated on simulations close to the Strait of Hormuz, a key international oil shipping choke point in the Persian Gulf which the IRGC has long threatened to block.

In addition, Iran touted successful battlefield tests of a drone it “reverse-engineered” based on an American UAV used by the US military and CIA. According to the AP:

Iran in 2014 reverse-engineered a Lockheed Martin RQ-170 drone it captured three years earlier, producing a domestic version of the RQ-170, modified to carry out both bombing and reconnaissance missions.

Gen. Amir Ali Hajizadeh of the Guard’s aerospace division further described that Iran possesses “the region’s biggest offensive drone fleet.”

Iran’s IRGC leaders last month touted that Iran is among the world’s top five powers capable of building combat drones, and also emphasized that “sanctions have had no impact” on this key defense sector.

6.GLOBAL ISSUES

Boeing:

The flight pattern showed something was extraordinarily wrong as the plan swung up and down by hundred of feed

(courtesy zerohedge)

7 OIL ISSUES

8. EMERGING MARKETS

Venezuela

end

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:00 AM….

Euro/USA 1.1319 UP .0012 REACTING TO MERKEL’S FAILED COALITION/ REACTING TO +GERMAN ELECTION WHERE ALT RIGHT PARTY ENTERS THE BUNDESTAG/ huge Deutsche bank problems + USA election:///ITALIAN CHAOS /AND NOW ECB TAPERING BOND PURCHASES/JAPAN TAPERING BOND PURCHASES /USA RISING INTEREST RATES /FLOODING/EUROPE BOURSES GREEN

USA/JAPAN YEN 111.70 DOWN .051 (Abe’s new negative interest rate (NIRP), a total DISASTER/NOW TARGETS INTEREST RATE AT .11% AS IT WILL BUY UNLIMITED BONDS TO GETS TO THAT LEVEL…

GBP/USA 1.3261 UP 0.0003 (Brexit March 29/ 2019/ARTICLE 50 SIGNED/BREXIT FEES WILL BE CAPPED

USA/CAN 1.3328 UP .0003 CANADA WORRIED ABOUT TRADE WITH THE USA WITH TRUMP ELECTION/ITALIAN EXIT AND GREXIT FROM EU/(TRUMP INITIATES LUMBER TARIFFS ON CANADA/CANADA HAS A HUGE HOUSEHOLD DEBT/GDP PROBLEM)

Early THIS FRIDAY morning in Europe, the Euro ROSE by 12 basis points, trading now ABOVE the important 1.08 level RISING to 1.1319 Last night Shanghai composite closed UP 31.07 POINTS OR 1.04%/

//Hang Sang CLOSED UP 160.87 POINTS OR 0.56%

/AUSTRALIA CLOSED DOWN 0.03%/EUROPEAN BOURSES GREEN

The NIKKEI: this FRIDAY morning CLOSED UP 163.83 POINTS OR 0.77%

Trading from Europe and Asia

1/EUROPE OPENED GREEN

2/ CHINESE BOURSES / :Hang Sang CLOSED UP 160.83 POINTS OR 0.77%

/SHANGHAI CLOSED UP 31.07 POINTS OR 1.04%

Australia BOURSE CLOSED DOWN .03%

Nikkei (Japan) CLOSED UP 163.83 POINTS OR 0.77%

INDIA’S SENSEX IN THE GREEN

Gold very early morning trading: 1303.95

silver:$15.39

Early FRIDAY morning USA 10 year bond yield: 2.63% !!! UP 0 IN POINTS from THURSDAY’S night in basis points and it is trading WELL ABOVE resistance at 2.27-2.32%. (POLICY FED ERROR)/

The 30 yr bond yield 3.04 UP 0 IN BASIS POINTS from THURSDAY night. (POLICY FED ERROR)/

USA dollar index early FRIDAY morning: 96.64 DOWN 14 CENT(S) from THURSDAY’s close.

This ends early morning numbers FRIDAY MORNING

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now your closing FRIDAY NUMBERS \12: 00 PM

Portuguese 10 year bond yield: 1.31% DOWN 2 in basis point(s) yield from THURSDAY/

JAPANESE BOND YIELD: -.03% UP 1 BASIS POINTS from THURSDAY/JAPAN losing control of its yield curve/