GOLD: $1289.55 DOWN $3.80 (COMEX TO COMEX CLOSING)

Silver: $15.11 DOWN 1 CENT (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1287.60

silver: $15.11

For comex gold and silver:

it seems that this month JPMorgan and Goldman Sachs are not stopping anything:

APRIL 0/858

yet JPM issued 700/823

EXCHANGE: COMEX

CONTRACT: APRIL 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,293.000000000 USD

INTENT DATE: 03/29/2019 DELIVERY DATE: 04/02/2019

FRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

104 C MIZUHO 1

323 C HSBC 3

657 C MORGAN STANLEY 2

657 H MORGAN STANLEY 204

661 C JP MORGAN 700

686 C INTL FCSTONE 17 4

690 C ABN AMRO 53 15

737 C ADVANTAGE 26 35

800 C MAREX SPEC 16 19

880 H CITIGROUP 544

905 C ADM 6 1

____________________________________________________________________________________________

TOTAL: 823 823

MONTH TO DATE: 1,780

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 823 NOTICE(S) FOR 82300 OZ (2.559 tonnes

TOTAL NUMBER OF NOTICES FILED SO FAR: 1780 NOTICES FOR 178,000 OZ (5.5365 TONNES)

SILVER

FOR APRIL

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

413 NOTICE(S) FILED TODAY FOR 2,065,000 OZ/

total number of notices filed so far this month: 554 for 2,770,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $4128:UP $26

Bitcoin: FINAL EVENING TRADE: $4151 UP 33

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL ON FRIDAY : THIS TIME BY A STRONG SIZED 1692 CONTRACTS FROM 194,082 DOWN TO 195,711 DESPITE FRIDAY’S 12 CENT RISE IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE MUST HAVE HAD CONSIDERABLE SHORT COVERING AGAIN TODAY.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR MAY, 3119 FOR MARCH 2020 0 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 3119 CONTRACTS. WITH THE TRANSFER OF 3119 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3119 EFP CONTRACTS TRANSLATES INTO 15.59 MILLION OZ ACCOMPANYING:

1.THE 12 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

AND NOW 3.565 MILLION OZ STANDING FOR SILVER IN APRIL.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

6431 CONTRACTS (FOR 1 TRADING DAYS TOTAL 6431 CONTRACTS) OR 32.155 MILLION OZ: (AVERAGE PER DAY: 3215 CONTRACTS OR 16.077 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 32.155 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 4.59% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 588.28 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1359 DESPITE THE 12 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 3119 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A VERY CONSIDERABLE SIZED: 1760 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 3119 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 1359 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 12 CENT GAIN IN PRICE OF SILVER ???? AND A CLOSING PRICE OF $15.12 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.988 BILLION OZ TO BE EXACT or 141% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 413 NOTICE(S) FOR 2,065,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ AND NOW APRIL AT 3.565 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY ANOTHER UNBELIEVABLE SIZED 10,465 CONTRACTS, TO 445,714 DESPITE THE RISE IN THE COMEX GOLD PRICE/(A GAIN IN PRICE OF $2.70//FRIDAY’S TRADING).

WE JUST HAD OUR FOURTH STRAIGHT DAY OF AN OPEN INTEREST COLLAPSE DUE TO THE ANTICS OF THE SPREADERS. IT LOOKS LIKE THE SPREADERS LIQUIDATE THEIR CONTRACTS NOT SIMULTANEOUSLY BUT AT DIFFERENT TIMES DURING THE TRADING DAY TO CAUSE THE CASCADE OF PRICING IN OUR PRECIOUS METALS AND THAT IS HOW THEY ALWAYS WIN ON OPTION EXPIRY..THEY ARE SO CROOKED. AT THE END OF THE DAY THEY ELIMINATE THE OTHER HALF OF THE SPREAD TRADE. THE COLLAPSE OF OPEN INTEREST SHOULD END WITH THIS READING AND ADVANCE FROM TUESDAY ON..

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7,677 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 7,677 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020l 100 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 445.714. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A NET LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2788 CONTRACTS: 10,465 OI CONTRACTS DECREASED AT THE COMEX AND 7,677 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 2788 CONTRACTS OR 278800 OZ OR 8.617 TONNES. FRIDAY WE HAD A RISE IN THE PRICE OF GOLD TO THE TUNE OF $2.70....AND YET WITH THAT, WE HAD A STRONG LOSS IN TONNAGE OF 8.617 TONNES!!!!!!. (HOWEVER ALL OF THE COMEX LOSS IS NO DOUBT DUE TO THE LIQUIDATION OF THE SPREADERS ALBEIT AT DIFFERENT TIMES DURING THE DAY)

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 7677 CONTRACTS OR 767,700 OR 23.87 TONNES (1 TRADING DAYS AND THUS AVERAGING: 7677 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAYS IN TONNES: 23.87 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 23.87/2550 x 100% TONNES = 0.936% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1396.59 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED DECREASE IN OI AT THE COMEX OF 10,465 DESPITE THE GAIN IN PRICING ($2.70) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A VERY STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7,677 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7677 EFP CONTRACTS ISSUED, WE HAD A TINY GAIN OF 107 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7677 CONTRACTS MOVE TO LONDON AND 10,465 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE LOSS IN TOTAL OI EQUATES TO 8.6718 TONNES). ..AND ALL OF THIS LACK OF DEMAND OCCURRED WITH A RISE IN PRICE OF $2.70 IN YESTERDAY’S TRADING AT THE COMEX!!!!! HOWEVER THERE IS NO DOUBT THAT AGAIN WE HAD CONSIDERABLE LIQUIDATION OF SPREADERS AS WE LANDED INTO FIRST DAY NOTICE AND AN ACTIVE DELIVERY MONTH AND IT IS THEIR ACTION THAT LED TO A FALL IN PRICE SO UNDERWRITTEN CONTRACTS WOULD NOT BE EXERCISED. THIS IS HOW THE CROOKS WIN ALWAYS ON OPTIONS EXPIRY.

we had: 823 notice(s) filed upon for 82,300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $3.80 TODAY

VERY STRANGE!! AGAIN NO CHANGES IN GOLD INVENTORY

I GUESS THEY CANNOT FIND ANY PHYSICAL METAL AT THE COMEX!!

INVENTORY RESTS AT 784.26 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 1 CENT IN PRICE TODAY:

WE LOST 656,000 OZ THROUGH A WITHDRAWAL

/INVENTORY RESTS AT 309.301 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A STRONG SIZED 1692 CONTRACTS from 197,403 DOWN TO 195,711 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 3119 FOR MAY AND MARCH 2020: 0 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3119 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 1359 CONTRACTS TO THE 3319 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A CONSIDERABLE GAIN OF 1427 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 7.135 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH. AND NOW 3.565 MILLION OZ FOR APRIL.

RESULT: A STRONG SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 12 CENT RISE IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 3119 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 79.60 POINTS OR 2.58% //Hang Sang CLOSED UP 510.66 POINTS OR 1.76% /The Nikkei closed UP 303.02 POINTS OR 1.43%/ Australia’s all ordinaires CLOSED UP 0.61%

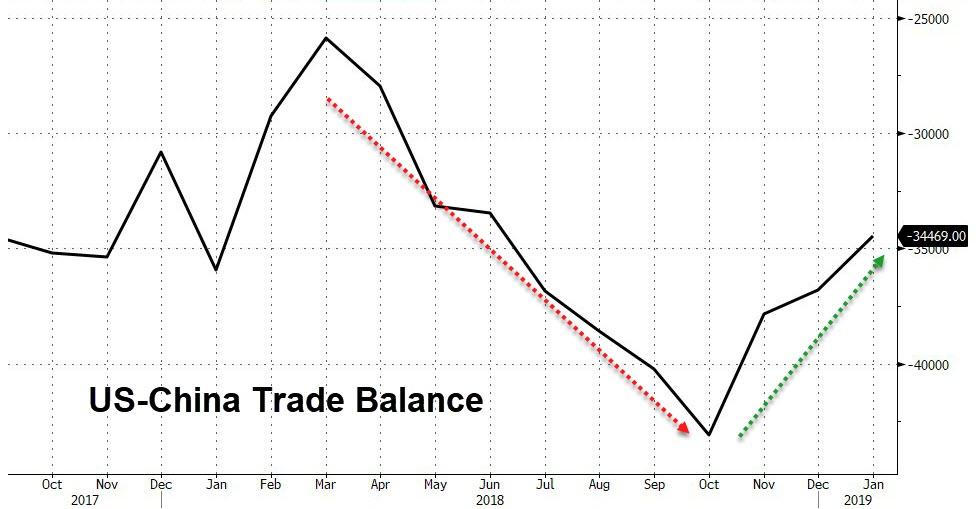

/Chinese yuan (ONSHORE) closed UP at 6.7117 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 60.62 dollars per barrel for WTI and 68.53 for Brent. Stocks in Europe OPENED GREEN

ONSHORE YUAN CLOSED UP // LAST AT 6.7117 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7193 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA

b) REPORT ON JAPAN

3 C/ CHINA

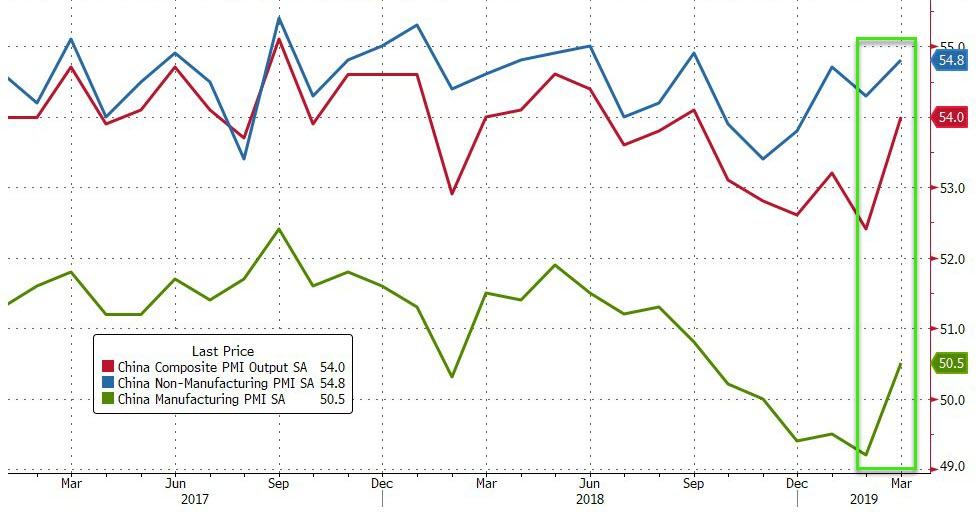

i)This weekend, China’s manufacturing pMI jumps huge due to the strong stimulus provided by the POBC last month. It ends 5 months of contraction but this stimulus will wear off quite quickly as the world’s global trade growth disintegrates.

( zerohedge)

ii)Good reason for gold to being held in check early this morning: Beijing orders 200 ships to the Spratly Islands and thus provoking a panic in Manila

( zerohedge)

4/EUROPEAN AFFAIRS

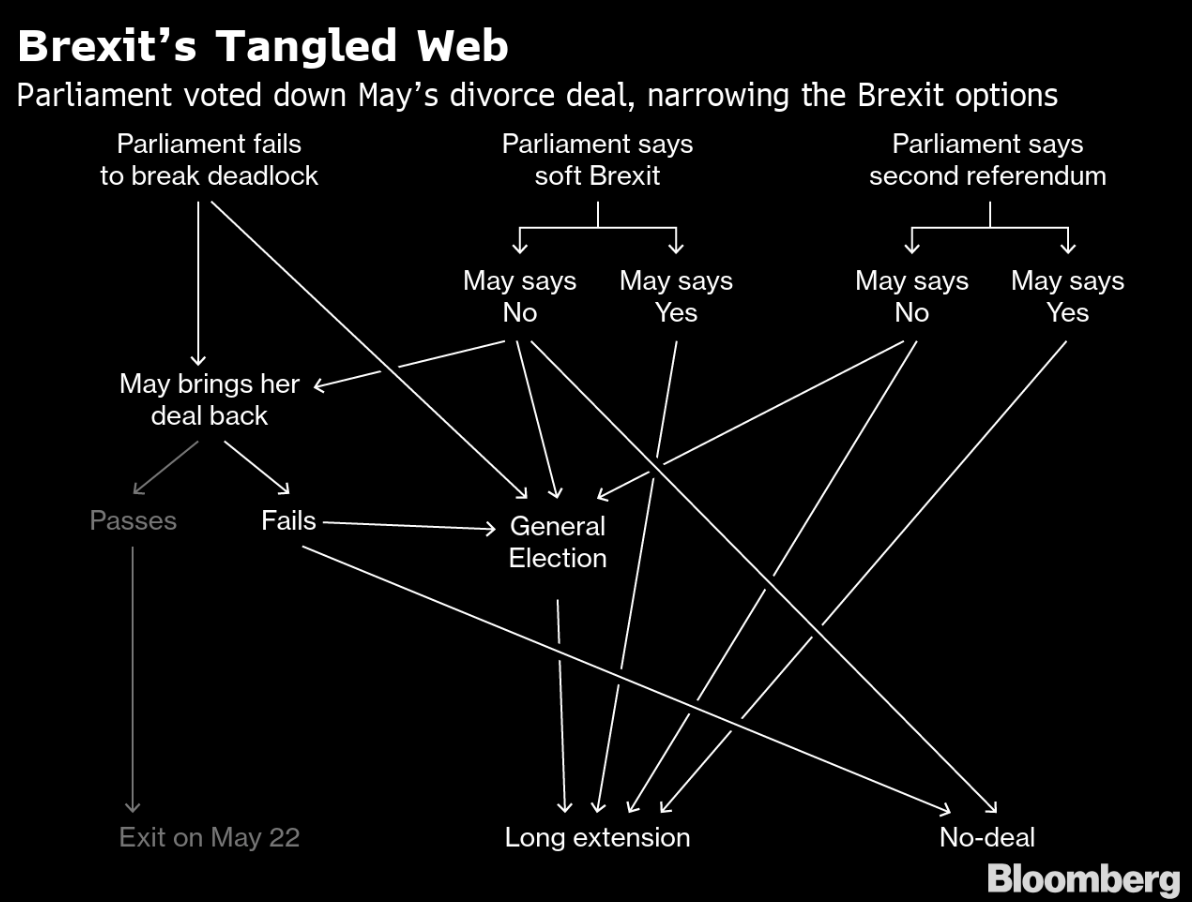

i)BREXIT/EU//Saturday

Theresa May is now planning a 4th vote to bring the Brexit plan (which is a terrible exit plan)

( zerohedge)

ii)UK MONDAY

( zerohedge)

iii)The machinations of the meaningful vote (MV4) that is being scheduled. …the ulterior motives behind Theresa May and how she might win her awful Brexit plan.

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)TURKEY/SATURDAY

Tom Luongo zeros in on one country that will no doubt provide global contagion when it fails…the country is Turkey and this is a must read..

(courtesy Tom Luongo)

ii)TURKEY/SUNDAY

iii)TURKEY/USA TODAY

6. GLOBAL ISSUES

Interesting: according to the Netherlands Bureau for Economic policy (CPB) world trade plunged to its weakest levels since 2009

( zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

VENEZUELA

Well that did not last long; Venezuela plunges into darkness again over the weekend

(courtesy zerohedge)

9. PHYSICAL MARKETS

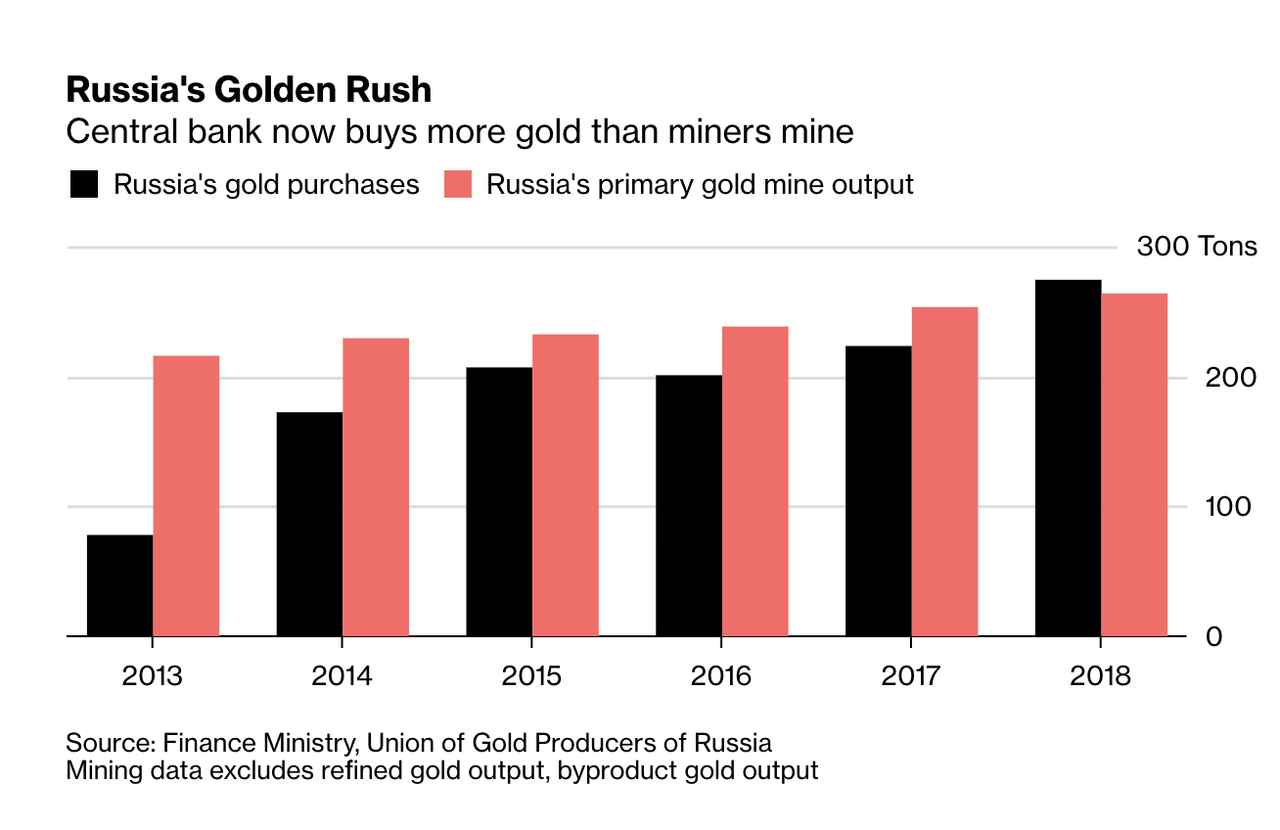

i)We have brought this to story to you last week but it is worth repeating:

Russia is dumping USA dollars to hoard gold

( Bloomberg/GATA)

ii)Andrew Maguire correctly states that the BIS is orchestrating smashing gold/silver due to mark to market losses on gold derivatives. He also outlines how the crooks use the spreading trade to cause options to expire worthless.

( Andrew Maguire/Kingworldnews/GATA)

iii)Trump calls on the Fed to reverse interest rates

( Reuters/GATA)

iv)A must see interview of Chris Powell and Stefan Gleason on the gold/price suppression etc

( Stefan Gleason/Chris Powell/Money Metals Exchange/GATA)

v)Perhaps the only national that can accomplish this: Russia can nover cover its entire debt dolar for dollar with its foreign reserves.

( BNE/Berlin//GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning

ii)Market data

a)The all important retail sales..a strong component of GDP tumbles in February, dropping .2% month over month instead of rebounding to a .2% rise

( zerohedge)

b)What a joke: two firms offer two polar opposite views on the USA economy and this has been going on for years. Put your money on the ISM data which continues to show a faltering economy

(courtesy zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

a)The sad case of the City of Chicago along with the no 1 basket case state in the union: Illinois

(John Rubino/DollarCollapse)

b)This portends something awful: a huge 70% of credit card holders say that they cannot pay off their debt this year

c)This sent the grocers tumbling as Whole Food flashes prices on hundreds of items

iv)SWAMP STORIES

a)Steve Bannon states that Trump will now go over his opponents as the Mueller investigation is over. Grab your popcorn.

( zerohedge)_

( zeroedge)

( zerohedge)

end

Let us head over to the comex:

AFTER APRIL, WE HAVE THE ACTIVE DELIVERY MONTH OF MAY AND HERE THE OI FELL BY 3469 CONTRACTS DOWN TO 133,449. CONTRACTS.. WE NOW HAVE OUR FIRST OPEN INTEREST FOR JUNE 2019 TO TOTAL ONE CONTRACT. AFTER JUNE, THE VERY BIG DELIVERY MONTH OF JULY HAD A GAIN OF 1687 CONTRACTS UP TO 35,237 CONTRACTS.

i)xx

ItalExit and Cyber Risks in a Cashless World Are Bigger Risks Than Brexit

Brexit Bringing Gold From London To Dublin: My Job with GoldCore CEO Stephen Flood

– Italy-exit or ItalExit: While all of the media and public attention is on the fallout from Brexit and Trump’s policies; ‘Italexit’ is possibly a bigger threat to European investors

– Digital risks to deposits: Gold will become even more valuable as a tangible asset and form of hard money hedge against fiat digital currencies and savings. A cashless society, while it boasts many benefits, it also exposes investors and savers to more concentrated digital risks and greater cyber risks. So, like an investment portfolio we should diversify our savings and not hold all our eggs in the one digital basket.

– Being Brexit ready: What does this actually mean for individuals? Lots of air time given to how businesses can prepare but what about people themselves – what can and should we be doing?

– Safe haven gold: Why gold has never really gone out of fashion and remains a hedge and safe haven; particularly as concerns grow about the dollar as the world reserve currency; where gold’s price will go in the long term – gold back near $2,000 an ounce within the next 24 months is likely.

by John Daly for the Irish Examiner:

THE movement of a large quantity of gold bullion from London to Dublin following the opening of GoldCore vaults earlier this year reflects a growing demand from investors to relocate tangible assets out of the UK. The first consignment consisted of gold bullion coins and bars weighing 2,000 troy ounces and worth more than €2 million.

“Brexit is a threat to the UK, to Ireland and the entire EU project, it is a phenomenon that has ramifications for the entire 27 countries in the EU and its citizens,” says Stephen Flood, CEO of Goldcore. “With the rise of both left-wing and right-wing political movements, people are railing against the impact of globalisation including mobile workforces, corporatism and rising inequalities.

“Ireland’s open economy means that we are more exposed than most to Brexit and threats posed to the EU, and while much air-time has been devoted to how businesses need to take stock and prepare, less has been said about what individuals can and should do to protect themselves and their assets. Everyone needs to be aware of the risks that lie ahead and, as such, be prudent by taking steps to reduce exposures in the event of a negative outcome,” he adds.

As Brexit comes to a head, GoldCore report a growing preference amongst Irish investors to store their gold domestically in Ireland rather than Perth, Zurich, Singapore, Hong Kong, Singapore and especially London. While Zurich continues to be the most sought-after storage location, Dublin has already surpassed Singapore and Hong Kong and may now usurp the second spot from London.

“In the event that Brexit is delayed or postponed, then demand for gold stored in Ireland may be more subdued and see a more gradual uptake. Other global threats and uncertainties around trade wars etc could see the demand ramp up further.”

Founded in Dublin in 2003, GoldCore has over 16,000 private, pension and corporate clients in over 150 countries, with over €150 million in precious metals under management. Bullion coins and bars are individually allocated and segregated, ensuring direct and outright asset ownership for clients.

The company began offering storage in the Perth Mint of Western Australia in 2005 and introduced GoldCore Secure Storage in 2009. Having since grown to include specialist vaults in Zurich, London, Singapore, Hong Kong and now Dublin through vault partners. Loomis International and Brinks, GoldCore is set to expand its storage offering to additional locations, including Dubai and New Zealand, in the near future. Prudence must be a watch-word undertaken in every household and every business to mitigate the potential worst impacts of Brexit, Flood believes.

“The Irish Government have adopted a purely pro-European tactical position which infers that we must have trust in the European authorities to keep as sacrosanct our interests. This is a fallacy, as De Gaulle said: ‘nations have no friends, only interests.’ We note that in a recent German opinion poll, Brexit barely registered as a concern among the public — there is something in this. For Irish people the time has come to take a cold hard look at the reality of the situation.”

In the midst of the continual focus on Brexit in Ireland and the UK, the potentially larger threat of a so called ‘ItalExit’ and the possible departure of Italy from the EU and the European monetary union presents an even graver prospect, Flood believes.

“Italy is in political crisis, and anti-EU politicians of the left and right have been put in power by an increasingly disgruntled Italian electorate. But the risk is not simply from people power and radical politicians, there is also the real risk of another Italian debt crisis, centred on very heavily indebted Italians banks and an indebted sovereign.”

Italy’s sovereign debt is €2.3 trillion, much of which is owned by Italian banks, the highest EU debt-to-GDP ratio after Greece.

“There are concerns that Italy will have a new debt crisis which could see a default and potentially an exit from the EU and the euro,” he said. “Banks in France, Germany and Belgium are most at risk of contagion from Italy’s debt crisis. French banks are the most exposed to a sell-off in Italian bonds with €285.5billion in credit extended by French banks.”

Flood takes a contra view to the idea that a cashless society would eliminate gold from use and hence be less valued as a store of value.

“A cashless society, while it boasts many benefits, also exposes people to greater cyber risks as digital assets, like deposits, are exposed to hacking, cyber terror and war. So, as with all investments, we should diversify and not hold all our eggs in one cashless basket, or indeed on one digital or paper basket.”

He cites the opinion of Ken Rogoff — the former chief economist at the International Monetary Fund — that gold’s role is likely to increase as cash will be used less and “the trend towards digital currencies” will also benefit gold which “as a hedge, has enormous value.”

While gold has become less popular in recent years as the Irish and global economy recovered and stock and property markets surged in value, investors concerned about Brexit, trade wars and other global risks have continued to diversify into the precious metal.

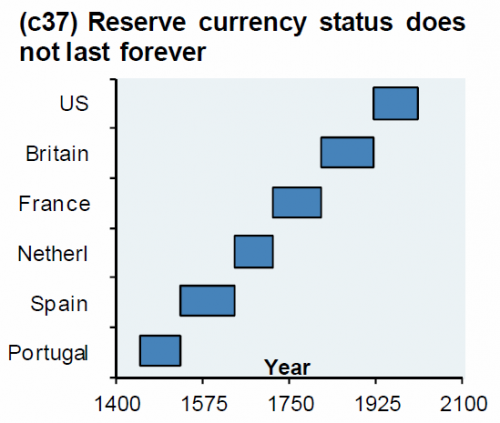

“History and recent history and indeed academic and independent research has shown that gold is a hedge and a safe haven. Today, the biggest gold buyers in the world are the largest central banks, including the People’s Bank of China. There are increasing concerns about the medium and long-term outlook for the dollar and, in time, its status as the world’s reserve currency will come to an end.”

Looking to the future, Flood sees gold back near $2,000 an ounce within the next 24 months as a more than likely scenario.

“We would be surprised if gold does not surpass $2,000. Much higher levels are likely in the longer term, and in a currency reset scenario or new Bretton Woods style monetary agreement, it could go to over $5,000. As ever, exactly predicting the future price of any asset is a fool’s errand.”

Courtesy of the Irish Examiner

Mario Draghi and the Case for Gold in 2019 – Watch On YouTube

News and Commentary

Gold slips as equities gain on trade talk progress, China data (Reuters.com)

Russian banks join Chinese alternative to SWIFT payment system (RT.com)

Oil prices rise, adding to biggest quarterly gain in 10 years (Reuters.com)

Asia lifted as Wall Street climbs on trade developments, pound sags (Reuters.com)

U.S. Mint American Eagle gold coin sales fall 8 pct in March (Reuters.com)

Source: Bloombrg via Yahoo

Russia is dumping U.S. dollars to hoard gold (Yahoo.com)

Why Russia Is Dumping Dollars And Buying Gold At The Fastest Pace In Decades (ZeroHedge.com)

Global Bond-Market Investors Are Getting Really Nervous (Bloomberg.com)

Russia now can cover its debt dollar for dollar in cash (IntelliNews.com)

White House calls for Fed to reverse U.S. rate hikes (Reuters.com)

Hunter for Nazi Gold Train Finds Renaissance Wall Portraits Instead (TheVintageNews.com)

Gold Prices (LBMA PM)

29 Mar: USD 1,291.15, GBP 991.09 & EUR 1,151.19 per ounce

28 Mar: USD 1,306.90, GBP 995.20 & EUR 1,161.18 per ounce

27 Mar: USD 1,318.25, GBP 997.78 & EUR 1,168.23 per ounce

26 Mar: USD 1,315.25, GBP 993.15 & EUR 1,162.02 per ounce

25 Mar: USD 1,319.35, GBP 1001.39 & EUR 1,165.82 per ounce

22 Mar: USD 1,311.10, GBP 998.80 & EUR 1,159.41 per ounce

Silver Prices (LBMA)

29 Mar: USD 15.10, GBP 11.52 & EUR 13.45 per ounce

28 Mar: USD 15.19, GBP 11.58 & EUR 13.53 per ounce

27 Mar: USD 15.40, GBP 11.65 & EUR 13.65 per ounce

26 Mar: USD 15.44, GBP 11.66 & EUR 13.65 per ounce

25 Mar: USD 15.52, GBP 11.77 & EUR 13.72 per ounce

22 Mar: USD 15.46, GBP 11.75 & EUR 13.68 per ounce

Recent Market Updates

– Ireland and EU Countries Must Seek ECB Approval to Manage Gold Reserves – Draghi

– Global Risks Increasing – Underlining The Case For Gold in 2019 (GoldCore Video Presentation)

– ‘No Deal’ Brexit Risk Impacting UK and Irish Economies – Gold Gains On Recession Concerns

– America’s “Debt Crisis Is Coming Soon”

– Russia Buys 1 Million Ounces Of Gold In February – Become Your Own Central Bank

– 5 Ways to Prosper In the Coming Crisis – Goldnomics Podcast

– Deutsche Bank and Commerzbank May Become EU’s “Too Big To Fail” Bank

– Happy Saint Patrick’s Day from GoldCore

– 188 Internet Shutdowns In 2018 Show Why Physical Gold Is Ultimate Protection

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

We have brought this to story to you last week but it is worth repeating:

Russia is dumping USA dollars to hoard gold

(courtesy Bloomberg/GATA)

Russia is dumping U.S. dollars to hoard gold

Submitted by cpowell on Fri, 2019-03-29 13:58. Section: Daily Dispatches

By Andrey Biryukov, Rupert Rowling, and Yuliya Fedorinova

Bloomberg News

Thursday, March 28, 2019

Vladimir Putin’s quest to break Russia’s reliance on the U.S. dollar has set off a literal gold rush.

Within the span of a decade, the country quadrupled its bullion reserves and 2018 marked the most ambitious year yet. And the pace is keeping up so far this year. Data from the central bank show that holdings rose by 1 million ounces in February, the most since November.

…

The data shows that Russia is making rapid progress in its effort to diversify away from American assets. Analysts, who have coined the term de-dollarization, speculate about the global economic impacts if more countries adopt a similar philosophy and what it could mean for the dollar’s desirability compared with other assets, such as gold or the Chinese yuan. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-03-29/russia-is-stocking-up…

end

Why Russia Is Dumping Dollars And Buying Gold At The Fastest Pace In Decades

Nine months ago, as US Treasury yields were drifting lower from a seven-year high reached in May of last year, we pointed out a curious development in the market for US sovereign debt that to our complete lack of surprise had been overlooked by the mainstream financial press: In April and May, Russia’s central bank liquidated $81 billion in Treasurys, nearly its entire holdings.

The drop was so significant, that Russia fell off the Treasurys list of the 30 or so largest Treasury holders. And in the months that have followed, as the US has imposed more economic sanctions and feuded with Putin over the fate of Venezuelan leader Nicolas Maduro, Vladimir Putin has turned instead to alternative reserves as the country’s de-dollarization push continued.

Over the same period of time, Russia was a conspicuously large buyer of Chinese yuan, as Goldman Sachs noted (and as we highlightedwell earlier today), helping contribute to a spike in yuan buying by reserve managers last year, as the IMF pointed out in a recent report.

But given the yuan’s still-limited convertibility, it has its limitations as a reliable reserve for foreign central banks. Which is probably why Moscow has relied on another reserve option that’s popularity has endured for most of the history of human civilization: Gold.

Data from the Russian central bank cited by Bloomberg show that its gold reserves have nearly quadrupled over the past ten years, and that 2018 marked the most “ambitious year yet” for Russia gold-buying, which coincided with the Central Bank of Russia’s mass-dumping of its Treasury holdings.

And in a rare, if muted, acknowledgement from the American financial press that de-dollarization is a contemporary threat that should be taken seriously, BBG said that “analysts, who have coined the term de-dollarization, speculate about the global economic impacts if more countries adopt a similar philosophy and what it could mean for the dollar’s desirability compared with other assets, such as gold or the Chinese yuan.”

While Russia’s dependence on exporting commodities like gold means it must continue to depend, at least in part, on the greenback (three-quarters of Russia’s $600 billion of trade is conducted in dollars, per BBG), this voracious gold buying is setting an example for other countries – in the west as well as in the east. Last year, Russia’s gold buying outstripped its gold production for the first time. And as relations with the US continue to deteriorate as longstanding arms control treaties are torn up and belligerent rhetoric spouted by both Trump and Putin, the Russian central bank might start importing more gold, which could have a positive impact on the global price.

Per two analysts, Russia has single handedly “put a floor” under the price of gold. Though some suspect that, since the CBR is now a known quantity in international gold markets, it would need to markedly accelerate its purchases to have a material impact on the price. Though few expect Russia to stop buying now.

Central bank buying has helped “strengthen gold from a weak hand to a strong hand” and supported gold prices in recent years, according to Ronald-Peter Stoeferle, managing partner at Liechtenstein-based asset manager Incrementum AG. Bullion has risen more than 20 percent since the start of 2016. It traded up 0.5 percent at $1,297.15 per ounce at 12:40 p.m. in London.

“If it wasn’t for Russia’s central bank, last year would have been the worst year for gold buying in a decade, so it helped put a floor on the price,” said Adrian Ash, head of research at gold brokerage BullionVault Ltd. “However, Russian buying is now well known so it would take a significant increase in their purchases to materially impact the gold price.”

But perhaps the most notable aspect of Putin’s rhetoric about de-dollarization is how it’s apparently influencing leaders of states that are still – at least nominally – friendly toward the US. French President Emmanuel Macron said in an interview late last year that Europe is too dependent on the greenback, declaring it “an issue of sovereignty” (this from one of the most ardently pro-EU politicians on the Continent). And last year, Poland and Hungary surprised the market by making the first substantial purchases of gold by EU member states in more than a decade.

So the next time you hear an analyst on CNBC categorically dismiss the notion that the loss of the dollar’s reserve currency status isn’t something that markets should take seriously (even as several credible voices have warned that it should be), you’d do well to remember this chart.

Nothing lasts forever.

Andrew Maguire correctly states that the BIS is orchestrating smashing gold/silver due to mark to market losses on gold derivatives. He also outlines how the crooks use the spreading trade to cause options to expire worthless.

(courtesy Andrew Maguire/Kingworldnews/GATA)

BIS smashed metals this week to avoid bad Q1 mark-to-market for gold derivatives, Maguire tells KWN

Submitted by cpowell on Sat, 2019-03-30 08:16. Section: Daily Dispatches

4:15p HKT Saturday, March 30, 2019

Dear Friend of GATA and Gold:

This week’s smashdown in the monetary metals, London metals trader Andrew Maguire tells King World News, was engineered by the Bank for International Settlements to avoid a nasty first-quarter marking-to-market of gold derivatives held by bullion banks. Maguire adds that the smash pushed gold and silver futures into “actionable” backwardation and that strong hands are accumulating real metal at current prices. The interview is excerpted at KWN here:

https://kingworldnews.com/andrew-maguire-unprecedented-gold-silver-backw…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Trump calls on the Fed to reverse interest rates

(courtesy Reuters/GATA)

Trump calls on Fed to reverse interest rate hikes

Submitted by cpowell on Sat, 2019-03-30 08:51. Section: Daily Dispatches

From Reuters

Friday, March 29, 2019

U.S. President Donald Trump said on Friday that the Federal Reserve made a mistake by raising interest rates and blamed the central bank for hurting the U.S. economy and stock market.

“Had the Fed not mistakenly raised interest rates, especially since there is very little inflation, and had they not done the ridiculously timed quantitative tightening, the 3.0 percent GDP, & Stock Market, would have both been much higher & World Markets would be in a better place!,” Trump tweeted.

The remarks were part of a new attack the White House has launched against the independent central bank in their unusual public split. The Fed’s Board of Governors did not immediately comment. …

… For the remainder of the report:

https://www.reuters.com/article/us-usa-fed-trump/white-house-calls-for-f…

end

A must see interview of Chris Powell and Stefan Gleason on the gold/price suppression etc

(courtesy Stefan Gleason/Chris Powell/Money Metals Exchange/GATA)

In Money Metals Exchange interview, GATA secretary updates gold price suppression

Submitted by cpowell on Mon, 2019-04-01 04:20. Section: Daily Dispatches

12:18p HKT Monday, April 1, 2019

Dear Friend of GATA and Gold:

Money Metals Exchange’s Mike Gleason has interviewed your secretary/treasurer about recent developments with gold price suppression. Among the topics:

— The refusal of mainstream financial news organizations to put any critical questions to central banks.

— The refusal of the monetary metals mining industry generally to protest price suppression because the industry is so vulnerable to governments and their investment bank agents.

— The renewal by CME Group, operator of the major U.S. futures exchanges, of its “Central Bank Incentive Program,” under which governments and central banks receive discounts for surreptitiously trading all major futures contracts in the United States.

— The regular monthly interventions in the gold market by the Bank for International Settlements to control the gold price on behalf of its member central banks.

The interview is headlined “GATA’s Chris Powell Reveals Why Governments Are Manipulating the Precious Metals,” begins at the 7:08 mark here —

https://www.moneymetals.com/podcasts/2019/03/29/why-government-manipulat…

— and continues for 22 minutes. It is accompanied by a transcript.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Perhaps the only national that can accomplish this: Russia can nover cover its entire debt dolar for dollar with its foreign reserves.

(courtesy BNE/Berlin//GATA)

Russia now can cover its debt dollar for dollar in cash

Submitted by cpowell on Mon, 2019-04-01 04:27. Section: Daily Dispatches

By Ben Aris

BNE Intellinews, Berlin

Sunday, March 31, 2019

Russia’s gross international reserves, including gold, continue to creep upwards and reached $487.1 billion as of March 22 — enough to cover Russia’s external debt dollar for dollar in cash.

In February during his state of the nation speech President Vladimir Putin boasted that for the first time Russia has enough money in its reserves to cover all its external debt with cash.

…

At the end of the last quarter of 2018 Russia had an external debt of $453.7 billion and the debt has been falling steadily over the 12 months as the government makes use of the windfall from rising oil prices and falling expenditures to pay off more debt early.

Russia already had one of the lowest levels of debt of any major country. While most western countries have debt-to-GDP ratios well above the Maastricht rules-recommended maximum of 60 percent (and some like Italy are well over 100 percent), Russia’s debt-to-GDP ratio has been hovering around 15 percent for years. …

… For the remainder of the report:

http://www.intellinews.com/russia-can-cover-its-debt-dollar-for-dollar-i…

* * *

Join GATA here:

Mines and Money Asia

Hong Kong Conference and Exhibition Center

Wan Chai, Hong Kong

Tuesday-Thursday, April 2-4

https://asia.minesandmoney.com/

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

All central banks are failing to maintain their own currency values as well as prevent recessions

(Egon Non Greyerz/GATA)

Central banks fail to maintain currency values and prevent recessions, von Greyerz writes at KWN

Submitted by cpowell on Mon, 2019-04-01 06:54. Section: Daily Dispatches

2:50p HKT Monday, April 1, 2019

Dear Friend of GATA and Gold:

Central banks, Swiss gold fund manager Egon von Greyerz writes at King World News today, claim to maintain the value of their currencies, but they don’t, even as the U.S. Federal Reserve adjusts interest rates in the name of maintaining prosperity but always fails to avert recessions. Von Greyerz’s commentary is posted at KWN here:

https://kingworldnews.com/greyerz-the-fed-may-revalue-gold-to-14000-as-m…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Peter Schiff: This Is Permanent Debt Monetization, A Dollar Collapse Is Next

In his most recent media appearance, Peter Schiff blasts the mainstream financial media and Fed policies, which he believes to be inflating the “biggest bubble yet”. Schiff appeared on the Quoth the Raven Podcast on Sunday and spent an hour and a half explaining his case as to why the United States is heading to a currency crisis.

Schiff On the Financial Media

Schiff led off talking about why he doesn’t get any mainstream financial media attention anymore, partly responding to recent commentsby CNBC contributor Guy Adami that Schiff was “bad for TV”.

“They abruptly cancelled my appearance a day before I was supposed to go on,” he said of a scheduled interview with Rick Santelli on CNBC. “They haven’t tried to book me since. Obviously Santelli’s team didn’t get the memo that Peter Schiff’s not allowed on.”

“I think they want to shield the audience from my perspective,” he continued. “Maybe they think they’re doing their audience a favor by keeping me off the air.”

Schiff On Gold

He continues the interview, explaining why he suggests his clients constantly keep 5-10% of their capital in gold. When asked about how he personally invests versus how he advises his clients, he explains why he is the most overweight gold miner stocks that he’s ever been.

Schiff also says we will need a gold standard again, which he thinks is inevitable, much to the dispassion of the government. “When they choose gold, which is the right choice, it’ll only be because they’ve exhausted everything else that wouldn’t work. When they admit we need a gold standard, the party’s over”.

“Gold keeps government honest, which is why the government doesn’t want it,” he said.

Schiff on the Fed’s Reversal

Schiff also talked at length about the Fed’s most recent decision to not raise rates again in 2019.

“The Fed did a reversal. A complete 180,” Schiff says about the Fed’s most recent minutes. “They’re never going to complete the normalization process,” Schiff recounts saying in late 2018 interviews. “I’m one of the only people out there saying the Fed is BSing, but the markets believed it.”

Schiff said either the Fed was deliberately lying in late 2018 when they said they would continue to taper and hike, or that they just didn’t know. Either way, Schiff believes that we are now in the midst of a bear market rally – not a bull market – as a result.

“I said they were going to wait for an excuse to abort normalization because they couldn’t tell the truth. They can’t raise interest rates because there’s too much debt,” he says. “It has nothing to do with problems abroad, it has nothing to do with Brexit.”

“This is permanent debt monetization,” he says.

You can list to the full 90 minute podcast here:

Peter Schiff is Chairman of SchiffGold, CEO and Chief Global Strategist of Euro Pacific Capital, Inc, and host of The Peter Schiff Show. Peter is an economic forecaster and investment advisor influenced by the free-market Austrian School of economics. He is one of the few forecasters who accurately and publicly predicted the 2007 housing market collapse and subsequent 2008 financial crisis.

Visit www.schiffgold.com for more on Peter Schiff.

Visit www.quoththeravenresearch.com for more on Quoth the Raven Research.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7117/

//OFFSHORE YUAN: 6.7193 /shanghai bourse CLOSED UP 79.60 POINTS OR 2.58% /

HANG SANG CLOSED UP 510.66 POINTS OR 1.76%

2. Nikkei closed //UP 303.02 POINTS OR 1.43%

3. Europe stocks OPENED GREEN

/USA dollar index FALLS TO 97.11/Euro RISES TO 1.1230

3b Japan 10 year bond yield: RISES TO. –.07/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.98/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 60.62 and Brent: 68.53

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP /OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO –.04%/Italian 10 yr bond yield UP to 2.51% /SPAIN 10 YR BOND YIELD UP TO 1.13%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.55: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.71

3k Gold at $1290.80 silver at:15.09 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 13/100 in roubles/dollar) 65.54

3m oil into the 60 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.98 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9951 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1176 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISING to –0.04%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.44% early this morning. Thirty year rate at 2.85%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.5702..GETTING DANGEROUS

Global Stocks Soar On Chinese Economic Optimism

Over the weekend China reported a key inflection point in its manufacturing PMI , which had its first expansionary print in 5 months, and the market saw right through this attempt to generate optimism that global economic headwinds are finally abating, and promptly sold off.

Just kidding, April fools!

As happens every single time, global stocks surged higher on Monday, extending gains from their best quarter in nearly 10 years, as algos and traders dutifully ignored the fact that every single number out of China is carefully goalseeked and politically motivated – in this case meant to shift the trade war balance of power in favor of China whose economy is now on the rebound despite the ongoing US tariffs – and overnight global markets were a sea of green as “Chinese economic optimism” is now the dominant narrative, taking over from “US-China trade talk optimism.”

As we reported previously, on Sunday China’s NBS said that the country’s manufacturing PMI rebounded strongly in March from a contractionary 49.2, printing at 50.5, its first expansion since September 2018, and beating estimates of a 49.6 reading. The non-manufacturing PMI continued its recent improvement, rising to 54.8, also the best reading since last September, as both the services and construction PMIs strengthened, and resulted in the composite PMI rising to 54.0 from 52.4.

Predictably, Asian stocks, European bourses and S&P 500 futures all jumped as traders woke up to news of “strong manufacturing data” out of the world’s second largest economy which helped ease investor worries about a slowdown in global growth.

Just as predictably, analysts were effusive in their praise of this goalseeked Chinese number:

- “Investors’ sentiment seems to be tilting to the side of optimism at the beginning of the second quarter, following a robust manufacturing report from China,” said Konstantinos Anthis, head of research at ADSS. “This news helps ease market participants’ worries over the odds of an upcoming recession on a global scale, even though there are plenty of signs suggesting caution,” Anthis said.

- China’s PMI reading “was encouraging,” said Thomas Harr, global head of fixed income and commodity research at Danske Bank. “There is still a good chance that global and euro-zone growth will improve in coming quarters, as the U.S. and China will reach a trade deal, while the Fed’s dovish shift and China’s stimulus will help.”

Confirming China’s renaissance, the private Caixin/Markit PMI business survey released on Monday also showed the manufacturing sector in the world’s second biggest economy returning to growth.

The immediate result was investor euphoria which swept across Asia as MSCI’s index of Asia-Pacific shares outside Japan added 1%, Chinese shares surged 2.6% to the highest since May, while Hong Kong stocks entered a bull market. Australian stocks climbed 0.6 percent, South Korea’s KOSPI gained 1.3 percent and Japan’s Nikkei advanced 1.4 percent.

“The rebound likely reflects both the resumption of production after the Chinese New Year break and renewed stimulus and policy easing,” UBS strategists wrote in a note to clients. “We expect China to continue easing policy, with signs of economic stabilization backing our overweight position on offshore Chinese equities in our Asia portfolios” they added.

Asian optimism quickly went global as European stocks posted their best daily gains since mid-February, as the pan-European STOXX 600 index surged 0.8% in early trading. Germany’s trade-sensitive DAX outperformed with a 1 percent rise helped by gains in auto maker stocks as European carmakers advanced more than 2 percent. That’s despite manufacturing data for Europe coming in at the lowest since 2013, which briefly caused the euro to pare some of its gains.

The German manufacturing Purchasing Managers Index slipped to 44.1 in March, worse than a flash reading of 44.7 that was already well below economist estimates. With sentiment at Asian factories stabilizing, German bonds fell, pushing the yield on 10-year securities up 3 basis points to minus 0.04 percent at 9:34 a.m. Frankfurt time.

French manufacturing also shrank more than expected as the PMI there was revised down to 49.7, however all this was generally ignored in light of the newly-found Chinese economic optimism.

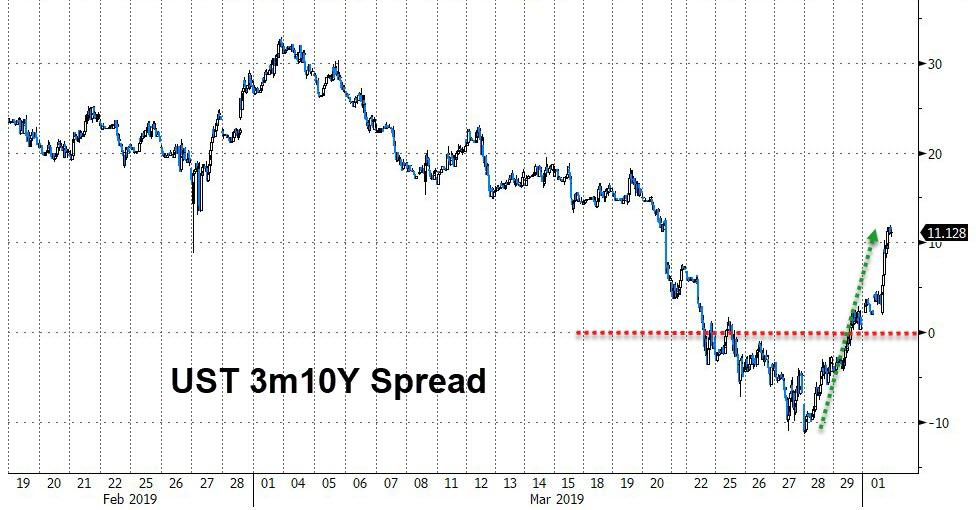

As Bloomberg notes, global equities are building on their strongest quarter since 2010 amid bets that dovish tilts by major central banks will help prop up earnings. The Chinese data went some way toward easing worries about a slowdown prior to the release of American monthly jobs numbers at the end of the week, while Treasury 10-year yields have also increased. U.S.-China trade talks will resume when Vice Premier Liu He leads a delegation to Washington later this week, potentially offering more positive developments for investors.

China’s recovery pushed yields higher, and the closely watched 3-month/10-year yield spread has pulled back from negative territory and stood around 3 basis points after investing two weeks ago.

In currencies, the dollar traded lower versus most of its G-10 peers after better-than-expected China data eased concern global growth was slowing. The Bloomberg Dollar Spot Index dropped 0.2%, snapping a four-day winning streak amid strong demand for upside exposure through options; it briefly pared losses after German mfg PMI data misses estimates, before falling to a new day low amid strong risk sentiment. Major emerging-market currencies advanced while sterling gains ahead of a U.K. parliamentary debate on various Brexit options.

Sterling was 0.6% higher to the dollar at $1.3114 on Monday, after taking its latest knock after British lawmakers rejected Prime Minister May’s Brexit deal for a third time on Friday. The Australian dollar advanced 0.45 percent to $0.7127, also benefiting from the China data. The Aussie is sensitive to shifts in the economic outlook for China, the country’s main trading partner.

Treasury 10-year yield climbed as much as 4bps to 2.4475%; Risk-sensitive currencies lead gains in the G-10, while the yen drops; Antipodean and Scandinavian currencies gain along with China’s yuan as Chinese Vice Premier Liu He scheduled to lead a delegation of trade negotiators to Washington on Wednesday after officials held talks in Beijing. The yen declined, while the Turkish lira slipped initially as preliminary results from the weekend’s municipal elections showed that Turkey opposition party claimed victory in Istanbul and Ankara, while the ruling AK Party also initially claimed to have won in Istanbul following local elections over the weekend which was seen as a referendum on President Erdogan. However. President Erdogan later commented that although the Mayorship may have been lost in Istanbul, they won in many of its municipalities; the lira initially slumped lower before it exploded higher after it emerged that Turkey is once again cracking down on shorts as the overnight swap rate surged to 260%.

In commodities, oil prices rose, adding to gains in the first quarter when the major benchmarks posted their biggest increases in nearly a decade, as concerns about supplies outweigh fears of a slowing global economy. Crude oil prices added to Friday’s gains, with U.S. West Texas Intermediate futures gaining 0.9 percent to $60.69 per barrel. Brent was 1.3 percent higher at $68.46 per barrel.

Economic data include retail sales, ISM manufacturing, construction spending and business inventories.

Market Snapshot

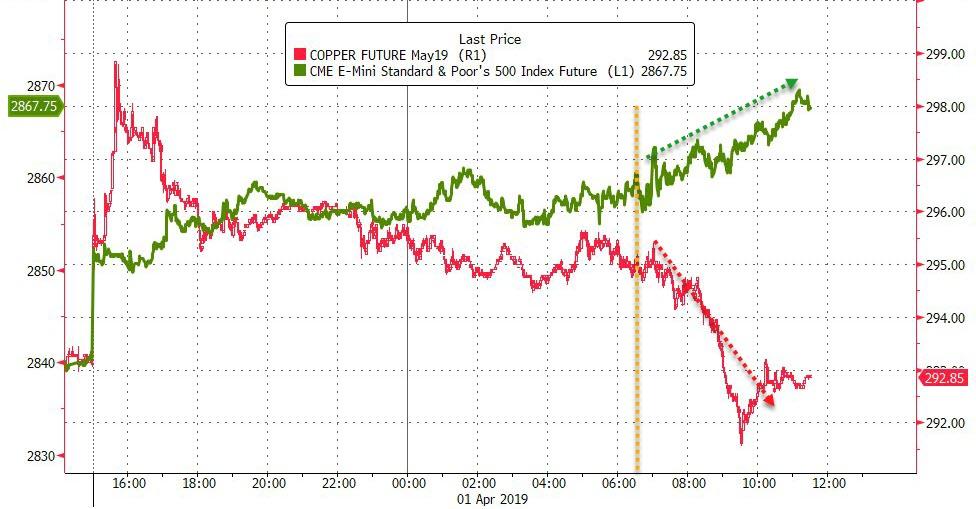

- S&P 500 futures up 0.8% to 2,859.75

- STOXX Europe 600 up 1.1% to 383.38

- MXAP up 1% to 161.44

- MXAPJ up 1% to 534.46

- Nikkei up 1.4% to 21,509.03

- Topix up 1.5% to 1,615.81

- Hang Seng Index up 1.8% to 29,562.02

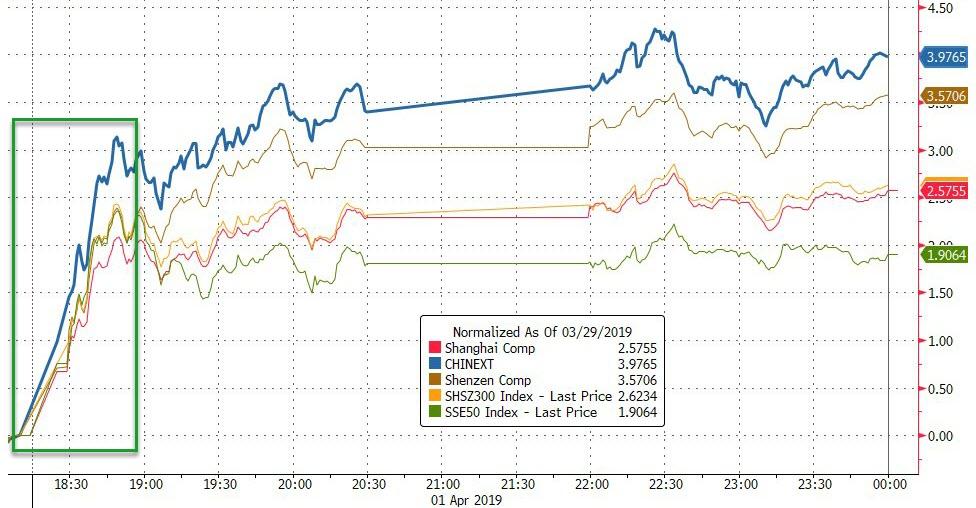

- Shanghai Composite up 2.6% to 3,170.36

- Sensex up 0.9% to 39,024.05

- Australia S&P/ASX 200 up 0.6% to 6,216.96

- Kospi up 1.3% to 2,168.28

- German 10Y yield rose 4.5 bps to -0.025%

- Euro up 0.3% to $1.1248

- Italian 10Y yield rose 0.2 bps to 2.134%

- Spanish 10Y yield rose 3.7 bps to 1.134%

- Brent Futures up 1.7% to $68.71/bbl

- Gold spot down 0.1% to $1,290.74

- U.S. Dollar Index down 0.3% to 97.04

Top Overnight News from Bloomberg

- IHS Markit’s Purchasing Managers’ Index for Germany slipped to 44.1 in March, worse than a flash reading of 44.7 that was already well below economist estimates

- U.K. manufacturers intensified stockpiling last month as they prepared for Brexit. IHS Markit’s Purchasing Managers Index rose to 55.1 in March, the highest since February 2018, from 52.1 the previous month, the firm said on Monday

- The Chinese government said it will extend a suspension of retaliatory tariffs on U.S. autos and include the opioid fentanyl in a list of controlled substances, two steps that could generate a positive atmosphere for trade negotiations due to resume this week. Beijing temporarily scrapped the 25 percent tariff imposed on vehicles as a tit-for- tat measure on Jan. 1, after the White House delayed a rise in tariffs on $200 billion of products that had been due that day

- Saudi Aramco was the world’s most profitable company in 2018, easily surpassing U.S. behemoths including Apple Inc. and Exxon Mobil Corp., according to an extract of the firm’s accounts published by Fitch Ratings

- Asset managers switched to net long NZD from short, CFTC data for week ended March 26 show. Leveraged funds raised their net GBP long positions and boosted net EUR shorts

Asian equity markets began the new quarter on the front-foot with momentum sustained from last Friday’s global rally in which the S&P 500 notched its best quarterly performance in nearly a decade and as the region also cheered encouraging Chinese PMI data. ASX 200 (+0.6%) and Nikkei 225 (+1.4%) gained from the open in which Consumer Staples led the broad gains across Australia’s sectors after Woolworths completed the sale of its petrol business and announced to return funds through a AUD 1.7bln off-market buyback, while the Japanese benchmark shrugged off a weak Tankan survey and was among the best performers with risk appetite fuelled by favourable currency flows. Hang Seng (+1.8%) and Shanghai Comp. (+2.6%) were uplifted by strong Chinese data in which the Official Manufacturing, Non-Manufacturing and Caixin Manufacturing PMIs all topped estimates with the official reading in expansionary territory for the first time since October. Furthermore, trade optimism and the inclusion of China’s onshore bonds in the Bloomberg Barclays Global Aggregate Index from today further added to the optimism with the mainland firmly extending on the over-3% gains seen on Friday and with the Hang Seng now in bull market territory. Finally, 10yr JGBs were lower amid similar weakness in T-notes and as a rally across riskier assets dampened safe-haven demand, while the BoJ recently announced its purchase intentions for the month in which it kept all amounts unchanged.

Top Asian News

- Analysts Downgrade China’s Stocks at Fastest Clip Since 2011

- Why Trump’s Sale of Fighter Jets Designed in 1970s Spooks China

- China Stocks Start April With Bang, Bonds Slide After Data Boost

- Philippine Stocks Falls Most in Asia as World Bank Cuts Forecast

A stellar start to the week for European stocks [Eurostoxx 50 +0.7%] following an inspiring performance in Asia where mainland China advanced in excess of 2% on the back of optimistic China manufacturing PMIs. Broad-based gains are being seen across major European indices, although Germany’s DAX (+1.5%) modestly outperforms peers, driven forward by the likes of auto names [Daimler +3.5%, Volkswagen +2.6% and BMW +1.8%] after Chinese PMIs topped estimates. Furthermore, the release also bolstered other China exposed sectors, i.e. luxury names, with Swatch (+1.4%), Richemont (+0.8%), LMVH (+1.0%) all performing well in their respective bourses. Sectors are also showing broad-based positivity, although utilities are underperforming as investors move away from defensive stocks. In terms of notable movers, WPP (+3.2%) rests at the top of the FTSE after a Deutsche Bank upgrade, whilst easyJet (-7.9%) shares declined after company CEO warned of a cautious H2 outlook as he expects softer yields from UK and European tickets.

Top European News

- Euro-Area Inflation Slows as Core Measure Falls to 11-Month Low

- Turkey Election Board Says Opposition Leading Race in Istanbul

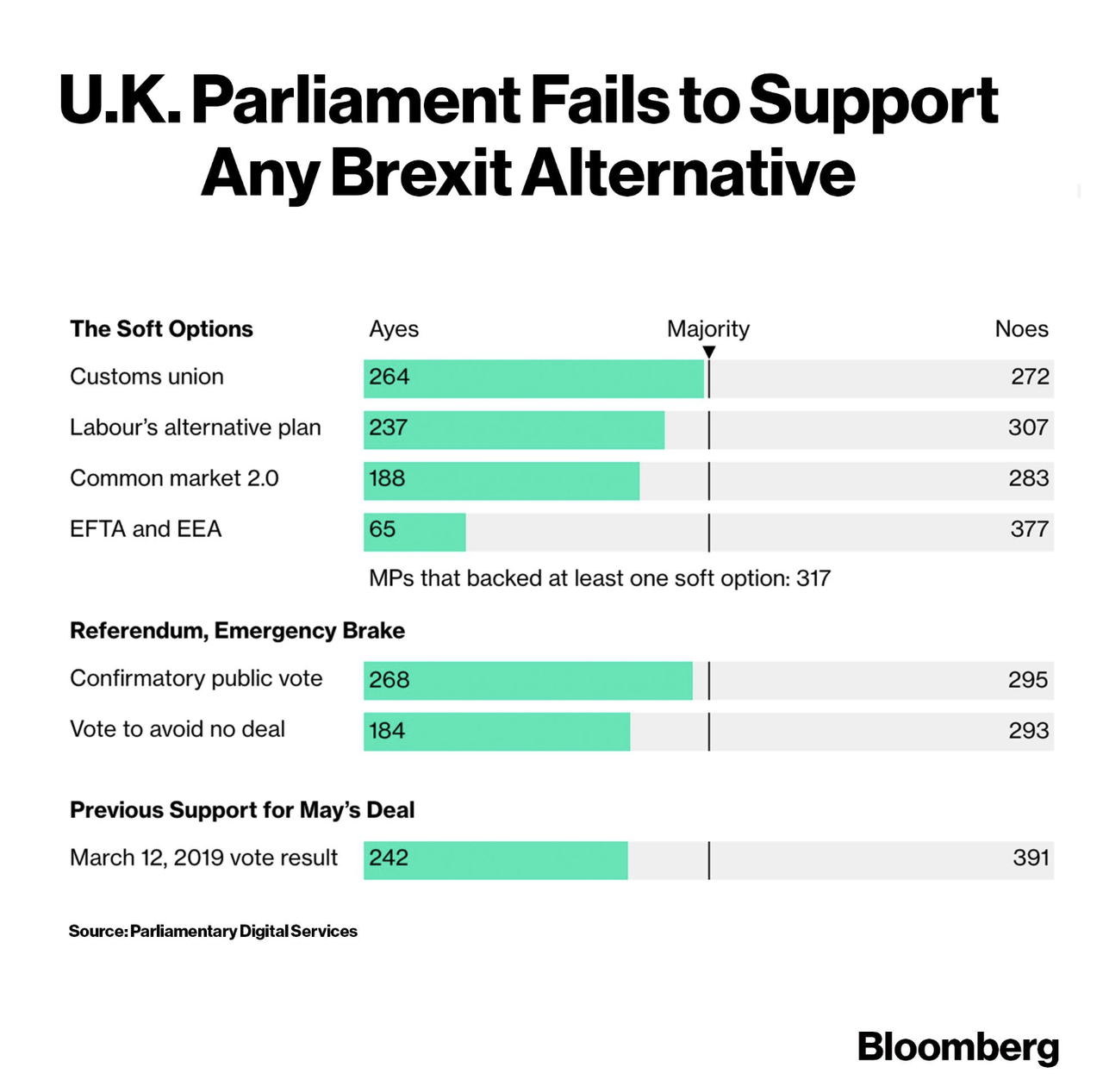

- U.K. Parliament Seizes Control Amid Brexit Rift in May’s Tories

- U.K. Factory Index Climbs to 13-Month High on Brexit Stockpiling

- Korian Shares Fall After Deaths at French Retirement Home

In FX, AUD/NZD/GBP/NOK/SEK – All beneficiaries of forecast-beating PMIs, albeit indirectly in the case of the Antipodean Dollars, as encouraging Chinese surveys overnight lifted broad risk sentiment and the Aussie and Kiwi accordingly. Meanwhile, a significantly better than expected UK headline print was mainly boosted by further pre-Brexit stock-piling, although output, new orders and jobs sub-components also improved and activity in both Scandi manufacturing sectors expanded at a faster pace. Hence, Aud/Usd and Nzd/Usd are both looking firmer above big figure levels at 0.7100 and 0.6800 respectively, with the former also probing above its 50 DMA (0.7119), while Cable extended its rebound from last week’s lows and back over 1.3000 to circa 1.3100, breaching its 55 DMA (1.3075) on the way. However, the latest round of IVs present more risk and uncertainty for the Pound with up to 8 amendments up for selection around 2.30 pm before debates and voting tonight – for a more detailed schedule and analysis see our headline feed. Elsewhere, Eur/Nok is back down below 9.6500 and Eur/Sek sub-10.4000 to test multi technical support levels including the 30 DMA (10.3844), 200 DMA (10.3812) and the bottom of a chart cloud (10.3785). Back down under, and the Aud will be looking for independent impetus via the RBA tomorrow with options pricing a 35 pip break-even for the event – full preview also available via the headline feed.

- EUR/CHF – Also firmer vs the Usd as the DXY retreats towards 97.000 again, but capped around 1.1250 and 0.9935 respectively in wake of relatively downbeat PMIs and Swiss retail sales.

- CAD/JPY – The G10 laggards, as the Loonie meanders between 1.3340-30 vs its US counterpart and the Jpy pivots 111.00 amidst the aforementioned general revival in risk appetite post-Chinese PMIs, and with the headline pair also underpinned by a downbeat Japanese Tankan report. However, 111.20 is holding (just) and represents a 61.8% Fib retracement of the 112.13-109.70 downmove.

- EM – Contrasting fortunes for the Lira and Rand, as weekend municipal elections in Turkey saw some key losses for the ruling AK Party to main opposition CHP, but not enough to threaten President Erdogan’s overall majority and result in regime change. Usd/Try has been up to 5.7000+ in response vs Usd/Zar that has been as low as 14.2225 after Moody’s delayed its latest credit review of SA and any potential cut in the rating and/or outlook, for the time being at least.

In commodities, the upbeat sentiment emanating from the optimistic China metrics overnight has supported sentiment alongside the demand outlook for the energy complex. Brent futures are marching with gains of around USD 1.0/bbl while WTI futures advance over USD 0.50/bbl. Brent oil has reached levels last seen in November, and from a technical front, the 200 DMA for Brent resides around USD 69.68/bbl and around USD 61.50/bbl for WTI. Furthermore, BAML expects Brent to average USD 74/bbl in Q2 2019, and USD 70/bbl in 2019. Meanwhile, the bank sees WTI averaging USD 56/bbl in 2019 and USD 60/bbl in 2020. Elsewhere, the latest CFTC data shows that speculative net long NYMEX WTI by almost 26k lots over last week, with a bulk of the buying coming from fresh longs. Of note, this month sees the EIA short-term energy outlook release on the 9th, OPEC monthly report on the 10th and IAE oil market report the day after. It is also worth noting that traders will be keeping an eye on trade developments as US is to host a Chinese trade delegation on the 3rd. In metals, gold prices succumbed to the positive risk tone as the yellow metal remains below the USD 1300/oz, albeit off lows. Meanwhile, the aforementioned China data bolstered copper prices to levels just shy of USD 3.00/lb, to levels last seen in June 2018. Elsewhere, iron ore prices have been supported by the Caixin-beat alongside a force majeure by Rio Tinto which will result in a loss of around 14mln tonnes of production this year. As such, Goldman Sachs raised iron ore price forecasts with 3-month estimate at USD 85/ton (Prev. USD 80), 6-month estimate at USD 80/ton (Prev. USD 75/ton) and 1-year estimate at USD 70/ton (Prev. USD 65).

US Event Calendar

- 8:30am: Retail Sales Advance MoM, est. 0.3%, prior 0.2%; Retail Sales Ex Auto MoM, est. 0.3%, prior 0.9%

- Retail Sales Control Group, est. 0.3%, prior 1.1%

- 9:45am: Markit US Manufacturing PMI, est. 52.5, prior 52.5

- 10am: ISM Manufacturing, est. 54.5, prior 54.2;

- 10am: Construction Spending MoM, est. -0.2%, prior 1.3%

- 10am: Business Inventories, est. 0.5%, prior 0.6%

DB’s Jim Reid concludes the overnight wrap

Happy April Fool’s Day, the day I first met my wife 9 years ago. Insert your own gag here. I can guarantee she has no idea of this anniversary. The problem or advantage (depending on your view) with doing a market’s related April Fool’s is that there have been so many strange things happen over the last few years that nearly anything could be true! Anyway I hope you all had a good weekend. On Saturday I played golf in shorts in the blazing sun and on Sunday I took the family out for Mother’s Day lunch to find that tables were only available outside. Problem was that it was freezing as the weather had completely turned. A lot of tears followed. The children were also upset. The clocks also went forward here in Europe and my wife thinks it must have been a male conspiracy to ensure that Mother’s Day was only 23 hours long this year.

There is some good news to start the week and the new quarter as yesterday saw the crucial Chinese manufacturing PMI number rise to 50.5 from 49.2 last month, the biggest increase since 2012 and beating all consensus estimates. Sub components that are very closely watched for forward looking momentum – new orders (51.6 from 50.6) and new export orders (47.1 from 45.2) – both rose to the highest levels in six months. The non-manufacturing also rose to 54.8 from 54.3 last month and 54.4 expected. The composite number increased from 52.4 to 54 the highest since September 2018. Overnight, China’s Caixin March manufacturing PMI also beat expectations at 50.8 from 49.9 last month (50.0 expected). The accompanying commentary along with the Caixin release said that the sub-index for new orders climbed to its highest level in four months while the new export orders returned to expansionary territory. Given the recent domestic stimulus – which our rates strategist Francis Yared has written about being around half the size of the growth bursting 2016 version – we have been expecting a bounce back in China but it had been a little elusive until now. The data could have elements of lunar holiday distortions depressing the comparisons from February but for now it will be a tentative welcome relief for global growth, especially for the Europeans. Our Chinese economists point out that we’ll know more as to whether this is an upswing when March’s activity data is released on April 17th.

In response, Chinese equities are leading the gains in Asia with the Shanghai Comp (+2.29%), CSI (+2.31%) and Shenzhen Comp (+3.03%) all up. The Nikkei (+1.72%), Hang Seng (+1.65%) and Kospi (+1.18%) are also up alongside most Asian markets. The Japanese yen is down -0.17% this morning and the yield on 10yr JGBs is up +1.4bps to -0.087%. Elsewhere, futures on the S&P 500 are up +0.63% and the 2yr and 10yr treasury yields are both up c. +3bps this morning.

Overnight China’s government has said that it will extend a suspension of retaliatory tariffs on US autos and include the opioid fentanyl in a list of controlled substances. The moves comes ahead of a visit by China’s Vice Premier Liu He later in the week to the US for continuing trade talks. The statement from China’s Minsitry of Finance said that the move seeks to “continue to create a good atmosphere for China-U.S. economic and trade talks” and is a “positive response” to the U.S. decision to delay tariff increases.

Elsewhere over the weekend, we had local elections in Turkey yesterday where President Erdogan’s party lost in the country’s capital Ankara and key cities along the Mediterranean coast while retaining its control in rural interiors and Istanbul (Bloomberg). The Turkish lira is down c. 1% overnight as market participants remain concerned about the ruling party announcing further populist policies to shore up declining support. Ahead of the elections, the BIST 100 equity index fell -6.1% last week, its worst weekly performance since October. The overnight swap rate ended the week at 28.98%, having risen over 1300% during last week.