2

GOLD: $1293.35 UP $2.70 (COMEX TO COMEX CLOSING)

Silver: $15.12 UP 12 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1292.70

silver: $15.13

For comex gold and silver:

APRIL

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 957 NOTICE(S) FOR 195700 OZ (2.9766 tonnes

TOTAL NUMBER OF NOTICES FILED SO FAR: 957 NOTICES FOR 95700 OZ (2.9766 TONNES)

SILVER

FOR APRIL

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

141 NOTICE(S) FILED TODAY FOR 705,000 OZ/

total number of notices filed so far this month: 141 for 705,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $4087:UP $71

Bitcoin: FINAL EVENING TRADE: $4099 UP 71

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 0/957

however JPMorgan issued 895 out of the 957 contracts

XCHANGE: COMEX

CONTRACT: APRIL 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,289.800000000 USD

INTENT DATE: 03/28/2019 DELIVERY DATE: 04/01/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

104 C MIZUHO 2

132 C SG AMERICAS 2

323 C HSBC 3

657 C MORGAN STANLEY 21

657 H MORGAN STANLEY 228

661 C JP MORGAN 895

685 C RJ OBRIEN 18

686 C INTL FCSTONE 1 17

690 C ABN AMRO 53

737 C ADVANTAGE 12 26

800 C MAREX SPEC 16

880 H CITIGROUP 606

905 C ADM 10 4

____________________________________________________________________________________________

TOTAL: 957 957

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST WENT UP AGAIN : THIS TIME BY A STRONG SIZED 3321 CONTRACTS FROM 194,082 UP TO 197,403 DESPITE YESTERDAY’S 31 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE MUST HAVE HAD CONSIDERABLE SHORT COVERING AGAIN TODAY.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR MAY, 5639 FOR MARCH 2020 0 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 5639 CONTRACTS. WITH THE TRANSFER OF 5639 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 5639 EFP CONTRACTS TRANSLATES INTO 28.195 MILLION OZ ACCOMPANYING:

1.THE 31 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

AND NOW 3.53 MILLION OZ STANDING FOR SILVER IN APRIL.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

41,567 CONTRACTS (FOR 21 TRADING DAYS TOTAL 41,567 CONTRACTS) OR 207.835 MILLION OZ: (AVERAGE PER DAY: 1979 CONTRACTS OR 9.896 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 207.835 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 29.68% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 572.69 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3321 DESPITE THE 31 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 5639 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A VERY STRONG SIZED: 8960 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 5639 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 3321 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 31 CENT FALL IN PRICE OF SILVER ???? AND A CLOSING PRICE OF $15.00 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.988 BILLION OZ TO BE EXACT or 141% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 141 NOTICE(S) FOR 705,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ AND NOW APRIL AT 3.530 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY AN UNBELIEVABLE SIZED 48,565 CONTRACTS, TO 456.179 WITH THE FALL IN THE COMEX GOLD PRICE/(A DROP IN PRICE OF $20.60//YESTERDAY’S TRADING).

I KNOW FOR SURE THAT WE JUST HAD OUR THIRD STRAIGHT DAY OF AN OPEN INTEREST COLLAPSE DUE TO THE ANTICS OF THE SPREADERS. IT LOOKS LIKE THE SPREADERS LIQUIDATE THEIR CONTRACTS NOT SIMULTANEOUSLY BUT AT DIFFERENT TIMES DURING THE TRADING DAY TO CAUSE THE CASCADE OF PRICING IN OUR PRECIOUS METALS AND THAT IS HOW THEY ALWAYS WIN ON OPTION EXPIRY..THEY ARE SO CROOKED. AT THE END OF THE DAY THEY ELIMINATE THE OTHER HALF OF THE SPREAD TRADE.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 16,172 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 19 CONTRACTS,JUNE: 16,068 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020l 100 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 457,650. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 32,393 CONTRACTS: 48,565 OI CONTRACTS DECREASED AT THE COMEX AND 16,172 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 32,393 CONTRACTS OR 3,239,300 OR 100.75 TONNES.

YESTERDAY WE HAD A FALL IN THE PRICE OF GOLD TO THE TUNE OF $20.60....AND YET WITH THAT, WE HAD A HUMONGOUS LOSS IN TONNAGE OF 100.75 TONNES!!!!!!. (HOWEVER ALL OF THE COMEX LOSS IS NO DOUBT DUE TO THE LIQUIDATION OF THE SPREADERS ALBEIT AT DIFFERENT TIMES DURING THE DAY)

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 159,836 CONTRACTS OR 15,983,600 OR 497.16 TONNES (21 TRADING DAYS AND THUS AVERAGING: 7611 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAYS IN TONNES: 497.16 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 497.16/2550 x 100% TONNES = 19.49% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1372.72 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUMONGOUS SIZED DECREASE IN OI AT THE COMEX OF 48,565 WITH THE LOSS IN PRICING ($20.60) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A VERY STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 16,162 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 16,162 EFP CONTRACTS ISSUED, WE HAD A HUGE LOSS OF 32,393 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

16,172 CONTRACTS MOVE TO LONDON AND 48,565 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE LOSS IN TOTAL OI EQUATES TO 100.75 TONNES). ..AND ALL OF THIS LACK OF DEMAND OCCURRED WITH A FALL IN PRICE OF $20.60 IN YESTERDAY’S TRADING AT THE COMEX!!!!! HOWEVER THERE IS NO DOUBT THAT AGAIN WE HAVE HUGE LIQUIDATION OF SPREADERS AS WE HEAD INTO AN ACTIVE DELIVERY MONTH AND IT IS THEIR ACTION THAT LEAD TO A FALL IN PRICE SO UNDERWRITTEN CONTRACTS WOULD NOT BE EXERCISED. THIS IS HOW THE CROOKS WIN ALWAYS ON OPTIONS EXPIRY.

we had: 957 notice(s) filed upon for 95,700 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $2.70 TODAY

VERY STRANGE!! AGAIN NO CHANGES IN GOLD INVENTORY

INVENTORY RESTS AT 784.26 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 12 CENTS IN PRICE TODAY:

STRANGE!!! AGAIN NO CHANGE IN SILVER INVENTORY

/INVENTORY RESTS AT 309.957 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A STRONG SIZED 3321 CONTRACTS from 194,082 UPTO 197,403 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 5639 FOR MAY AND MARCH 2020: 0 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 5639 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 3321 CONTRACTS TO THE 5639 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUMONGOUS GAIN OF 8960 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 44.80 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH. AND NOW 3.530 MILLION OZ FOR APRIL.

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 31 CENT FALL IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 5639 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 95.82 POINTS OR 3.20% //Hang Sang CLOSED UP 276.15 POINTS OR 0.96% /The Nikkei closed UP 172.85 POINTS OR 0.82%/ Australia’s all ordinaires CLOSED UP 0.08%

/Chinese yuan (ONSHORE) closed UP at 6.124 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 58.52 dollars per barrel for WTI and 67.05 for Brent. Stocks inEurope OPENED MIXED

ONSHORE YUAN CLOSED UP // LAST AT 6.7134 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7228 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA

b) REPORT ON JAPAN

3 C/ CHINA

i)China is testing long range missiles from a concealed ship. The Israelis were also working on something like this

( zerohedge)

ii)Huawei profits soar in 2018 along with revenue despite the uSA shutdown its products. The Chairman tells Washington to drop its “loser attitude”

(courtesy zerohedge)

4/EUROPEAN AFFAIRS

i)BREXIT/EU

Mark Mobius of Templeton fame describes the deteriorating financial conditions inside the uK..their balance of payments is awful accompanied by huge debt. He feels that once the tether is broken from the EU, the country will be forced to raise rates to keep funds in the country. He feels that there is a risk of a downgrade in their sovereign debt

( Mark Mobius/zerohedge)

ii)UK/8 AM

iii)Bill Blain on the Brexit and Boeing..

a must read…

(courtesy Bill Blain)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Turkey

It seems that there are 5 banks in trouble with huge exposure to a Turkish failure, namey the big Italian banks Intessa and Unicredit along with the French bank BNP Paribas. I noted that Turkish foreign reserves were down 1/3 down to about 24 billion USA./ They own 261 tonnes of gold or 10 billion dollars which is included in this foreign reserve calculation. Turkey is down to their last remaining USA dollars.

( zerohedge)

6. GLOBAL ISSUES

BOEING/LION AIR

Somehow the anti stall software was mistakenly activated before the deadly crash. Not sure what that means..

(courtesy zerohedge)

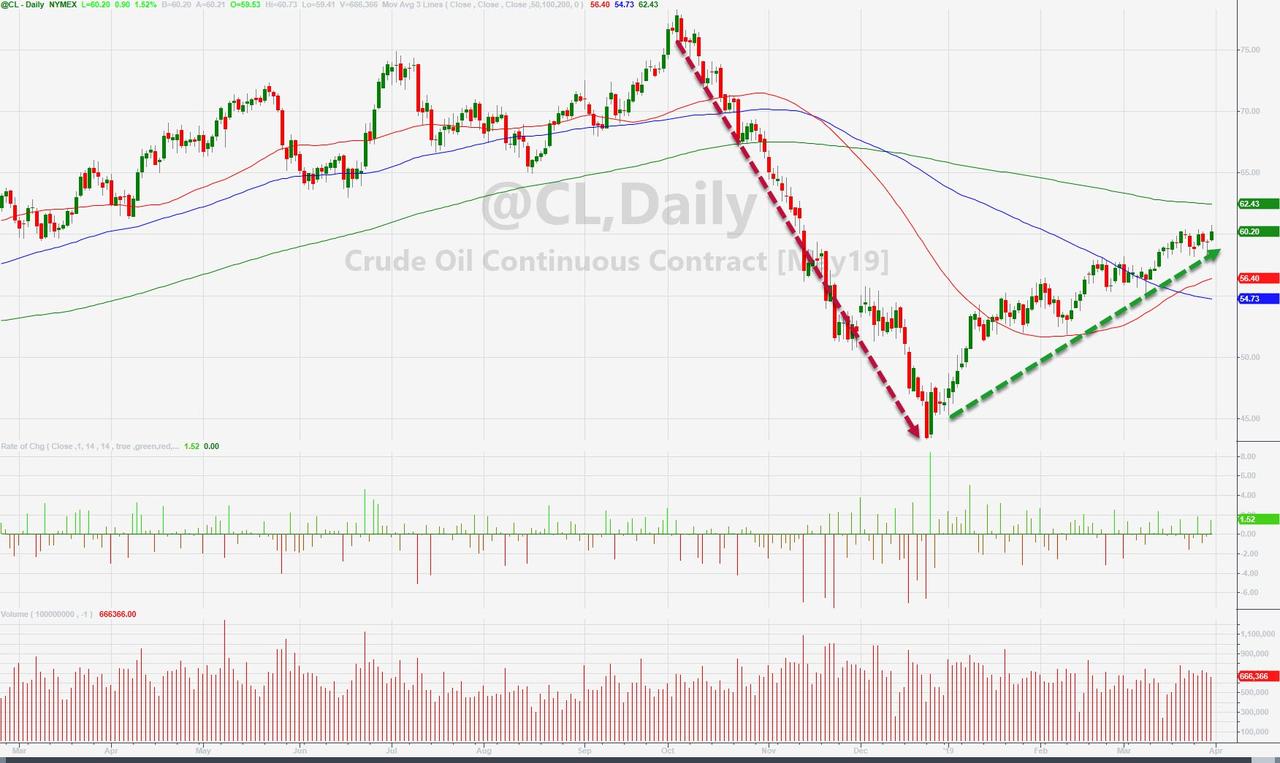

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

ii)Kranzler explains how the crooks orchestrated their paper raid on gold/silver last night. My commentary explains the mechanics behind the raid

( Dave Kranzler/GATA)

iii)Palladium hammered by over 200 dollars as car sales plummet

( Lawrie Williams)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning

ii)Market data

a)As mortgage rates plummet, new home sales surge

(zerohedge)

b)U. of Michigan soft data rebounds in March and it was hope in the low income American category that sparked the gain.

( zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

Brandon Smith is one smart cookie. He believes that the Fed is controlling the demolition of its own economy. He states that the Fed should have cut rates right now and not paused. Why continue with balance sheet run off until September when already the economy is faltering badly and the yield curves are inverting. He believes that we know have a perfect storm where England is in a mess with Brexit, the European economies including Germany’s are badly in a rot and the uSA is engaging in a trade war with China. The Fed does not like to be blamed so now it surely looks like a perfect storm is developing globally.

a must read…

( Brandon Smith)

iv)SWAMP STORIES

Trump is set to hold Democrat officials behind the collusion hoax accountable

( zerohedge)

end

end

Let us head over to the comex:

AFTER APRIL, WE HAVE THE ACTIVE DELIVERY MONTH OF MAY AND HERE THE OI ROSE BY 2281 CONTRACTS UP TO 136.918. CONTRACTS.. WE STILL HAVE 0 OPEN INTEREST FOR JUNE 2019. AFTER JUNE, THE VERY BIG DELIVERY MONTH OF JULY HAD A GAIN OF 1025 CONTRACTS UP TO 33,550 CONTRACTS.

i) Out of HSBC:

197.792 oz

EU Countries Must Seek ECB Approval to Manage Gold Reserves – Draghi

– European Central Bank in effect tells euro-zone countries your gold is the ECB’s

by Francesco Canepa on Reuters

The European Central Bank needs to approve any operation in the foreign reserves of euro zone countries, including gold and large foreign currency holdings, the ECB’s President Mario Draghi said on Thursday.

“The ECB shall approve both the operations in foreign reserve assets remaining with the NCBs (national central banks)…and Member States’ transactions with their foreign exchange working balances above a certain threshold,” Draghi told two Italian members of the European Parliament.

“The purpose of this competence is to ensure consistency with the exchange rate and monetary policy of the Union.”

Editors note: This is an interesting and important story that should have been picked up more widely in Europe’s media and not solely on Reuters. The context is not given despite it being very important indeed.

The ECB and its President Mario Draghi realise gold is very important in terms of protecting the euro from collapsing both in terms of nations reverting to their national currencies but also in terms of the euro, dollar, pound and other fiat currencies collapsing in value, if the public loses faith in them.

The ECB President said of gold in October 2013 that gold is a “reserve of safety” that “gives you a value-protection against fluctuations against the dollar.” Draghi told an open forum at Harvard’s Kennedy School of Government, why central banks want gold and what value it offers. He said that there were “several reasons” to own gold including “risk diversification.”

The largest buyers of gold in 2018 were central banks and the largest holders of gold remain the U.S., the Bundesbank and other central banks in the indeed the IMF and the ECB itself.

Investors should prudently follow the lead of central banks internationally and gradually accumulate gold and dollar, euro or pound cost averaging into an allocated and segregated physical gold position.

Related Content

Gold Is A ‘Reserve Of Safety’ Says ECB President – Watch Video

Eurozone Increases “Reserve of Safety” Gold Holdings To 10,792 Tonnes

News and Commentary

ECB Tells Euro-zone Countries Your Gold Is Ours (Reuters.com)

Gold’s 1.6% Decline Leaves It Firmly Below Key $1,300 (MarketWatch.com)

Palladium sinks 6 pct in free fall, gold sheds 1 pct (Reuters.com)

U.S. fourth-quarter GDP revised down; profits weak (Reuters.com)

Why Central Bank Gold Demand Is Reaching New Highs (TheStreet.com)

What People Are Stocking Up on in Case Brexit Goes Bad (Bloomberg.com)

Inverted yield curve suggests the stock market has already peaked – Analysts (MarketWatch.com)

Be prepared to dump stocks ‘very quickly’ – Former Morgan Stanley Asia Chairman (MarketWatch.com)

Italy’s debt spiralling out of control and threatens the ‘single’ currency (ZeroHedge.com)

Gold Prices (LBMA PM)

28 Mar: USD 1,306.90, GBP 995.20 & EUR 1,161.18 per ounce

27 Mar: USD 1,318.25, GBP 997.78 & EUR 1,168.23 per ounce

26 Mar: USD 1,315.25, GBP 993.15 & EUR 1,162.02 per ounce

25 Mar: USD 1,319.35, GBP 1001.39 & EUR 1,165.82 per ounce

22 Mar: USD 1,311.10, GBP 998.80 & EUR 1,159.41 per ounce

21 Mar: USD 1,317.30, GBP 1002.99 & EUR 1,155.80 per ounce

Silver Prices (LBMA)

28 Mar: USD 15.19, GBP 11.58 & EUR 13.53 per ounce

27 Mar: USD 15.40, GBP 11.65 & EUR 13.65 per ounce

26 Mar: USD 15.44, GBP 11.66 & EUR 13.65 per ounce

25 Mar: USD 15.52, GBP 11.77 & EUR 13.72 per ounce

22 Mar: USD 15.46, GBP 11.75 & EUR 13.68 per ounce

21 Mar: USD 15.54, GBP 11.85 & EUR 13.64 per ounce

Recent Market Updates

– Global Risks Increasing – Underlining The Case For Gold in 2019 (GoldCore Video Presentation)

– ‘No Deal’ Brexit Risk Impacting UK and Irish Economies – Gold Gains On Recession Concerns

– America’s “Debt Crisis Is Coming Soon”

– Russia Buys 1 Million Ounces Of Gold In February – Become Your Own Central Bank

– 5 Ways to Prosper In the Coming Crisis – Goldnomics Podcast

– Deutsche Bank and Commerzbank May Become EU’s “Too Big To Fail” Bank

– Happy Saint Patrick’s Day from GoldCore

– 188 Internet Shutdowns In 2018 Show Why Physical Gold Is Ultimate Protection

– Buy Gold as Basel III Means “Central Banks and Banks Are Going To Be Buying Gold”

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

Not to sure that Italy is going to like this: Italy’s gold is the EU’s gold and for that matter: all EU countries’ gold belongs to the EU/ECB

(courtesy Reuters/GATA)

Your gold is ours, European Central Bank tells euro-zone countries

Submitted by cpowell on Thu, 2019-03-28 14:37. Section: Daily Dispatches

Countries Must Seek ECB Approval to Manage Gold Reserves, Draghi Says

By Francesco Canepa

Reuters

Thursday, March 28, 2019

https://www.reuters.com/article/ecb-reserves-draghi/countries-must-seek-…

FRANKFURT, Germany — The European Central Bank needs to approve any operation in the foreign reserves of euro zone countries, including gold and large foreign currency holdings, the ECB’s President Mario Draghi said today.

…

“The ECB shall approve both the operations in foreign reserve assets remaining with the national central banks … and member states’ transactions with their foreign exchange working balances above a certain threshold,” Draghi told two Italian members of the European Parliament.

“The purpose of this competence is to ensure consistency with the exchange rate and monetary policy of the Union.”

* * *

end

Kranzler explains how the crooks orchestrated their paper raid on gold/silver last night. My commentary explains the mechanics behind the raid

(courtesy Dave Kranzler/GATA)

Dave Kranzler: The paper raid on gold

Submitted by cpowell on Fri, 2019-03-29 09:48. Section: Daily Dispatches

By Dave Kranzler

Investment Research Dynamics, Denver

Thursday, March 28, 2019

Gold was smacked $22 from top to bottom overnight and this morning. It was a classic paper derivative raid on the gold price, which was implemented after the large physical gold buyers in the eastern hemisphere had closed shop for the day. This is what it looks like visually:

[See chart at link below]

As you can see, as each key physical gold trading/delivery market closes, the price of gold is taken lower. The coup de grace occurs when the Comex gold pit opens. The Comex is a pure paper market, as very little physical gold is ever removed from the vaults and the paper derivative open interest far exceeds the amount gold that is reported to be held in the Comex vaults. (The warehouse reports compiled by the banks that control the Comex are never independently audited.) …

… For the remainder of the analysis:

http://investmentresearchdynamics.com/the-paper-raid-on-the-gold-price

end

.end

Palladium hammered by over 200 dollars as car sales plummet

(courtesy Lawrie Williams)

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7134/

//OFFSHORE YUAN: 6.7228 /shanghai bourse CLOSED UP 95.82 POINTS OR 3.20% /

HANG SANG CLOSED UP 276.15 POINTS OR 0.96%

2. Nikkei closed //UP 172.85 POINTS OR 0.82%

3. Europe stocks OPENED GREEN

/USA dollar index FALLS TO 97.12/Euro RISES TO 1.1231

3b Japan 10 year bond yield: RISES TO. –.08/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.31/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 60.12 and Brent: 67.77

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP /OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO –.06%/Italian 10 yr bond yield DOWN to 2.48% /SPAIN 10 YR BOND YIELD DOWN TO 1.08%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.56: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.74

3k Gold at $1293.60 silver at:15.10 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 19/100 in roubles/dollar) 64.79

3m oil into the 60 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.79 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9955 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1182 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISING to –0.06%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.42% early this morning. Thirty year rate at 2.83%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.6428..GETTING DANGEROUS

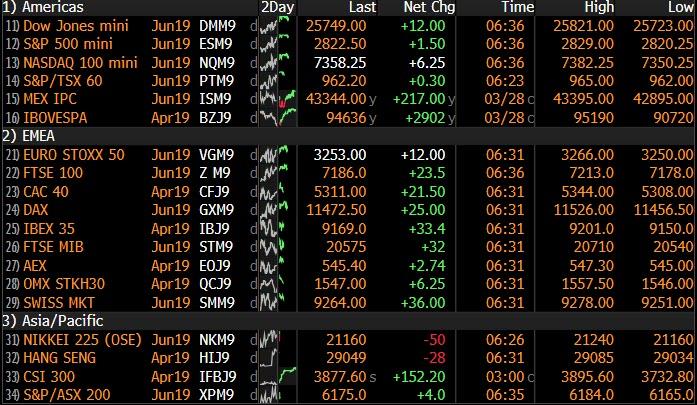

S&P Futures Jump On Renewed “Trade Talk Optimism”, Set For Best Quarter Since 2009

Global stocks and US equity futures rose in a broad rally to end the strongest quarter since 2012 while global bond yields rebounded after a prolonged slide on growth worries amid renewed “trade talk optimism” after Bloomberg reported overnight that U.S. negotiators have been working “line-by-line” through the text of the trade truce agreement and Steven Mnuchin said he had a “productive working dinner” the previous night in Beijing.

On Friday, Treasury Secretary Steven Mnuchin and U.S. Trade Representative Robert Lighthizer held meetings in Beijing to ensure there were no discrepancies in the English and Chinese-language versions of the text, and also to balance the number of working visits to each capital,

Steven Mnuchin

✔@stevenmnuchin1

.@USTradeRep and I concluded constructive trade talks in Beijing. I look forward to welcoming China’s Vice Premier Liu He to continue these important discussions in Washington next week. #USEmbassyChina

And yet, while traders saw this as signs of optimism, the reality is that this was only necessary because the two sets of drafts appeared to differ substantially, and the focus on the joint wording “has become a key issue after U.S. officials complained that Chinese versions of the text had walked back or omitted commitments made by negotiators.” The two sides have very different understandings of certain words, according to one of the officials, who noted that China’s Vice Commerce Minister Wang Shouwen started his career as a translator at the ministry.

As always expect lots of noise on the trade front and little to no signal, although markets will look for any excuse to window dress stocks sharply higher today. Sure enough, futures on the S&P 500, Nasdaq and Dow Jones all rose, and despite recent turbulence, the S&P 500 gained 12.3% so far this quarter, on pace for the best quarterly performance since 2009.

The MSCI World Index was up 0.17% on the day, and was set to post its best quarterly performance since March 2012

European markets opened higher, with the European STOXX 600 index up 0.4 percent. France’s CAC 40 index led gains, up 0.77 percent, while Britain’s FTSE 100 index was up 0.6 percent. Germany’s DAX rose 0.4 percent with miners and retailers leading the way higher.

Earlier, stocks rose across Asia, with China stocks leading gains across regional equity markets with U.S.-China trade talks underway in Beijing; Shanghai Composite and CSI 300 indexes both on course for their best quarter since 2014; The MSCI Asia Pacific Index was up 9% in 1Q.

“Our base case is for the current tariff truce extension to yield only a partial resolution, including select U.S. tariff rollbacks in exchange for some Chinese concessions on imports, market access and intellectual property,” strategists at UBS wrote in a note to clients.

European sovereign bond yield were marginally higher and the euro slumped even as German unemployment fell to a fresh record low. Even so, German and French government bond yields were poised on for their biggest monthly falls since June 2016, ending a month where heightened anxiety about global growth prospects have sparked a flood into fixed income globally.

“We have moved a lot in the last two weeks so there is a bit of pause for now,” said Pooja Kumra, European rates strategist, TD Securities.

In the US, the 10Y Treasury yield edged up to 2.4263% from a 15-month low of 2.352% touched on Thursday after an almost relentless fall since the Federal Reserve’s dovish tone last week sparked worries about the U.S. economic outlook, after Thursday’s latest Q4 GDP revision showed U.S. economic growth was slower than initially thought growing a revised 2.2% from an earlier reading of 2.6%.

In overnight central bank news, Fed’s Bullard said the normalization process in US is at an end and suggested they have gone as far as they can. Bullard also commented that it is premature to consider a rate cut now and that he sees a likely rebound in economic growth during Q2 and the rest of 2019.

In the latest Brexit news, UK House of Commons speaker selects no amendments for debate today. A UK government source confirmed they were laying a motion to give MPs a vote on the withdrawal agreement only for Friday without the political declaration on the future relationship between the EU and the UK, while a government source said the vote to approve the withdrawal agreement would meet the EU’s test to extend A50 to May 22nd and is said to be substantially different to MV3. UK government ministers privately suggested a general election will be called if Friday’s vote is rejected or things “fall apart”, according HuffPost’s Paul Waugh. Elsewhere, there were comments from House Speaker Bercow that the new government motion meets his tests and only covers withdrawal agreement, while Sun’s Tom Newton Dunn reports it will occur at 14:30GMT/10:30EDT. In any case, there is little expectation in the EU today that the Withdrawal Agreement will pass and as such, the EU mood is one of resignation now, according to BBC’s Adler. However, a last minute burst of optimism emerged after SNP’s Gray says some Labour MP’s are preparing to back PM May’s agreement.

In FX, the Bloomberg Dollar Spot Index headed for its best week in seven amid stronger equity markets and optimism about a possible U.S.-China trade agreement. Quarter-end flows clouded the short-term outlook in the major currencies, providing choppy price action at times. The euro was initially lower, sliding as much as 1.121, before rebounding sharply to $1.1235, following speculation that today’s Brexit vote just may pass; even so it was headed for its worst month since October, weighed down by fears about economic growth and cautious signals from the European Central Bank. The Euro has also been weighed down by speculation the ECB will introduce a tiered deposit rate, providing a sign that policymakers plant to keep interest rates low for longer.

The Turkish lira continued its slid, dropping 1.7%, a day after it had plunged 4 percent. President Tayyip Erdogan blamed the currency’s weakness on attacks by the West ahead of nationwide local elections on Sunday. TD Securities recommended a lira short whereby it urged clients to buy USDTRY calls targeting 7.9 after this weekend’s elections pass.

The big mover, however, was the British pound, which fired slumped as low as $1.3004 after sliding more than 1 percent the previous day, before rebounding sharply higher above 1.31 on speculation that some Labour MPs may back May’s deal. It looks like it will be another nailbiter until the end.

Sterling had taken a knock as the prospect of a swift agreement on Brexit faded with the British parliament yet again failing to agree on a way forward.

In commodities, oil extended gains as the OPEC+ coalition’s production cuts supported prices, putting crude markets on track for their biggest quarterly rise since 2009. WTI trade at $59.76 per barrel, up 0.8 percent on the day and recovering from Thursday’s low of $58.20.

Market Snapshot

- S&P 500 futures up 0.4% to 2,832.25

- STOXX Europe 600 up 0.4% to 378.18

- German 10Y yield unchanged at -0.068%

- Euro up 0.06% to $1.1228

- Brent Futures up 0.4% to $68.08/bbl

- Italian 10Y yield rose 3.2 bps to 2.132%

- Spanish 10Y yield fell 0.4 bps to 1.086%

- MXAP up 0.6% to 159.47

- MXAPJ up 0.7% to 527.75

- Nikkei up 0.8% to 21,205.81

- Topix up 0.6% to 1,591.64

- Hang Seng Index up 1% to 29,051.36

- Shanghai Composite up 3.2% to 3,090.76

- Sensex up 0.1% to 38,595.64

- Australia S&P/ASX 200 up 0.08% to 6,180.73

- Kospi up 0.6% to 2,140.67

- Brent Futures up 0.4% to $68.08/bbl

- Gold spot down 0.1% to $1,288.79

- U.S. Dollar Index up 0.05% to 97.25

Top Overnight News from Bloomberg

- Chinese and U.S. negotiators are working line-by-line through the text of an agreement that can be put before President Donald Trump and counterpart Xi Jinping to defuse a nearly year-long trade war, according to officials familiar with the matter

- Theresa May is putting the main part of her divorce deal back to Parliament on Friday, after a dramatic promise to quit if it gets approved. Her pledge has changed the arithmetic, but probably not enough

- London continued to lead the U.K.’s weakening property market at the start of 2019, with values falling the most since the financial crisis a decade ago

- German unemployment fell to a fresh record low, suggesting that the country’s buoyant services sector is offsetting weakness in manufacturing

- Russia and Iran’s energy ministers will discuss a possible extension of the OPEC+ agreement to curb oil production when they meet in Moscow next week

- As Treasury issuance outstrips crisis-era records, the rising share of government bonds in market-weighted fixed-income indexes is pulling in more global investors

Asian equity markets were higher across the board as the region took impetus from the US, where all major indices finished positive and trade-sensitive sectors outperformed on optimism as US-China high-level talks resumed in Beijing. ASX 200 (+0.1%) eked mild gain as most sectors remained afloat heading into quarter-end although gold miners were heavily weighed after the precious metal succumbed to the pressure from a firmer greenback. Nikkei 225 (+0.8%) was driven by currency weakness with Daiichi Sankyo surging nearly 16% to hit limit up and a record high after it signed a USD 6.9bln collaboration and commercialization deal for its cancer drug with AstraZeneca in which it will receive an upfront payment of USD 1.35bln. Elsewhere, Hang Seng (+1.0%) conformed to the upbeat tone and the Shanghai Comp. (+3.2%) outperformed as trade discussions continued in Beijing and after China announced electricity and fuel costs reductions ahead of incoming VAT cuts. Huawei also supported the risk appetite after it posted a 25% increase in annual profits despite the ongoing US tiff, although not all stocks benefitted as some contended with disappointing earnings including China’s largest lender ICBC which fell short of FY net forecasts after flat Q4 profits. Finally, 10yr JGBs were lower as the fixed income complex eased from the rampant inflows seen this week and as gains in stocks dampened demand for safe-haven assets, although downside was limited with the BoJ also in the market for JPY 710bln of JGBs in the belly to super long-end.

Top Asian News

- Japan’s Job Outlook Brightest in Decades. Pity About the Wages

- Foreigners Dive Back Into China Stocks, Buy Most Since December

- Bet on Philippine Boom Pays Off for This Top-Performing Manager

- Jet Airways Is Said to Miss Paying $109 Million Loan From HSBC

A relatively upbeat start for European equities [Euro Stoxx 50 +0.5%] following on from a stellar performance in Asia, wherein the Shanghai Composite ended the week higher in excess of 3% as US-Sino talks concluded on a seemingly positive note. Broad based gains are seen across major indices, UK’s FTSE (+0.5%) is keeping its composure amid the Brexit-induced weakness in the Sterling and as heavyweight mining names benefit from the surge in base metal prices: [Antofagasta (+2.6%), Glencore (+2.4%), Anglo American (+2.1%) and Rio Tinto (+2.0%)]. Sector-wise, material names lead the gains, whilst consumer discretionary names benefit from positive broker moves for Kering (+1.4%), LVMH (+1.2%) and Richemont (+0.9%). Looking at individual movers, Wirecard (-6.9%) shares plumb the depths following yet another FT article which noted that half the company’s revenues come from partners whilst noting that at some of them there is a mismatch with reality on the ground. A Wirecard executive has noted the article in incorrect and misleading. Elsewhere, yet more trouble for Scandi banks with Swedbank (-9.5%), Nordea Bank (-9.8%) lower after New York regulators reportedly expanded money laundering scandal probe into Nordea Bank.

Top European News

- H&M Surges as Earnings Beat Analyst Estimates on Fewer Discounts

- Altice Jumps as Drahi’s Carrier Predicts Higher French Growth

- Italy’s Nexi Says IPO Offering Value Seen at EU1.9b- EU2.2b

- Pound Reverses Gains as Chance May’s Brexit Deal Passes Seen Low

In FX, USD – The Greenback remains firm overall, but has lost a bit of momentum against a few G10 and other counterparts at the start of the final trading session of the week, month and quarter as latest US-China trade talk reports suggest more progress made. However, the DXY has nudged above the 97.300 level that capped its advances yesterday and in doing so crossed a key Fib at 97.245 (76.4% retrace of the fall from 97.711 to 95.735), which bodes well from a chart standpoint ahead of potentially pivotal data including Chicago PMI and a trio of Fed speakers (Williams, Kaplan and Quarles).

- NZD/AUD/CAD – Bucking the broad trend on the aforementioned constructive US-China vibes, but with the Kiwi also getting a much needed fillip from ANZ’s consumer sentiment survey overnight showing an improvement in March. Nzd/Usd rebounded to just over 0.6800 at one stage, but then pared gains on more dovish RBNZ impulses, albeit indirectly as JPM updated its 2019 outlook for NZ rates with back-to-back cuts now seen in May and June. Similar story for the Aussie that briefly reclaimed 0.7100 before fading, while the Loonie is still relatively rangebound between 1.3420-45 ahead of Canadian PPI data.

- JPY/EUR/CHF/GBP – All softer vs the Usd, with the Jpy extending its retreat from a fraction shy of 110.00 to circa 110.92 amidst reports of Japanese selling for FY end on top of the general improvement in risk sentiment. However, supply is said to be sitting at 111.00 and the recent 110.96 peak is still providing technical resistance. The single currency is holding just above 1.1200 with buying interest touted from 1.1210 down to the figure and decent option expiry interest also supporting as 1.5 bn rolls off at the NY cut vs 1.2 bn from 1.1250-60. The Franc is essentially flat vs the Buck and Euro around 0.9950 and within 1.1190-65 parameters respectively following SNB comments on Thursday reinforcing the commitment to maintain NIRP and intervention given the Chf’s ongoing high valuation and fragility in the currency markets. Last, but by no means least heading into yet another crucial Brexit vote in the HoC, the Pound is depressed with Cable almost losing the 1.3000 handle despite a big buy order at 1.3010 and Eur/Gbp pivoting 0.8600 where a sizeable 1 bn expiries reside and run-off only 30 minutes or so before the Parliament decide whether to back the WA.

- EM – In contrast to partial recoveries elsewhere, the Lira has lurched to new lows vs the Dollar not far from 5.6600 as the run continues almost relentlessly, and with little last respite from a narrower than forecast Turkish trade deficit.

In commodities, WTI (+0.8%) and Brent (+0.6%) futures are on the front foot thus far amid the overall positive risk sentiment around the market as US-China talks are to continue next week after concluding in Beijung on a positive note. WTI futures extended gains above USD 59.00/bbl and remain in relatively close proximity to USD 60.00/bbl whilst Brent futures reside around USD 67.50/bbl. In the month of March, Brent Crude advanced around 1.6% whilst WTI crude posted gains in excess of 4%. In terms of recent energy news-flow Russian Energy Minister denied the report that Russia will only agree to extend output cut deal by 3 months and said Russia and Iran potential extension of OPEC+ deal. This follows source reports yesterday that OPEC and Russia could agree to a 3-month extension of the current agreement at the June meeting. Elsewhere, Gold ekes mild gains following yesterday’s slump below USD 1300/oz. Meanwhile, copper and iron are extending on earlier gains as optimism surrounding trade talks bolster the base metals. Russia Energy Minister denies report that Russia will only agree to extend output cut deal by 3 months and said Russia and Iran potential extension of OPEC+ deal. (Newswires) This follows source reports yesterday that OPEC and Russian could agree to a 3-month extension of the current agreement at the June meeting.

US Event Calendar

- 8:30am: Personal Income, est. 0.3%, prior -0.1%; Personal Spending, est. 0.3%, prior -0.5%

- 8:30am: PCE Deflator YoY, est. 1.4%, prior 1.7%; PCE Core YoY, est. 1.9%, prior 1.9%

- 9:45am: MNI Chicago PMI, est. 61, prior 64.7

- 10am: New Home Sales, est. 619,500, prior 607,000; New Home Sales MoM, est. 2.06%, prior -6.9%

- 10am: U. of Mich. Sentiment, est. 97.8, prior 97.8; Mich. Current Conditions, prior 111.2; Expectations, prior 89.2

DB’s Jim Reid concludes the overnight wrap

Welcome to the last business day of Q1, a quarter that most market participants will remember more fondly than Q4 2018. Craig is skiing at the moment but assuming he’s not like me and doesn’t get injured every time he steps foot on the snow, he’ll be doing the usual performance review when he’s back on Monday. Today is also the day that 1008 days after the Brexit vote, the UK was supposed to leave the EU. However if I had to make a spread as to how many more days the UK will continue to be in the EU I don’t think I’d quite know where to start. Anywhere from 14 to infinity. I’m happy to trade on this spread if anyone wants to. I’ve ordered a bit of furniture for our new house from Italy and yesterday I enquired as to when it might arrive. The guy on the other end of the phone then proceeded to tell me that there was something called Brexit that was going on and told me all about how it was going, his views on every politician involved, and that the risks to his business (and to my table) of a no deal Brexit. By the end of the conversation I was none the wiser about when it will arrive. Suffice to say that if you’re reading this in Italy and you need a new table and there’s a no deal Brexit, then I may be in a position to do business.

Today we will get a fresh vote on the Withdrawal Agreement (WA) at about 2:30pm but only the WA part and not the Political Declaration on the Future Relationship as with the two previous votes. Maybe I’ll get my chairs but not my table then. The government hopes that by separating out the two, the WA could have a greater chance of success. Furthermore, it satisfies Speaker Bercow’s criteria that the vote must be on something different to last time. The other thing it satisfies is the EU’s criteria from their European Council meeting last week that in order to get an extension of the Brexit deadline from the 12 April to 22 May (the day before the European Parliament elections begin), the House of Commons just needs to approve the WA.

However, it’s not obvious that this will help the government win, with Labour’s shadow Brexit Secretary, Sir Keir Starmer, saying that if the two were separated, “that would mean leaving the EU with absolutely no idea where we’re heading. That cannot be acceptable, and we wouldn’t vote for that.” And on the other side, one of the main reasons the ERG and DUP MPs have been opposed to the deal has been the backstop, which is a part of the WA.

Another issue is that this risks complicating the ratification process, as in UK law under the European Union (Withdrawal) Act 2018, to ratify the WA it requires that both the WA and the framework for the future relationship have been approved in a motion by the House of Commons. Therefore, unless new legislation were passed that changed this requirement, the political declaration on the future relationship would still need to be approved in a motion by the House of Commons before the WA could be ratified. Maybe the benchmark for any defeat today will be how it compares to the indicative votes supporting a second referendum and the Customs Union – the two that got closest to a majority.

Sterling weakened against every other G10 currency yesterday (-1.10% vs USD but +0.2% this morning), although other UK assets performed strongly, with sterling’s decline supporting the FTSE 100 (+0.56%) to outperform other European indices yesterday, while UK 10yr gilt yields fell -1.2bps yesterday, the only major European country to see ten-year debt yields fall.

In the US-China trade negotiations, Trade Representative Lighthizer and Secretary Mnuchin will be continuing talks today, before China’s Vice Premier, Liu He, returns to Washington for further talks next week. Treasury Secretary Mnuchin has said overnight that they had a “very productive” working dinner yesterday with Chinese negotiators. National Economic Council Director Kudlow said yesterday that they are willing to extend the talks if necessary, saying that “If it takes a few more weeks, or if it takes months, so be it.” Kudlow also addressed the Commerce Department’s report on auto tariffs, which President Trump is currently reviewing. A decision on whether or not to impose broad import tariffs on the sector was supposed to come within 90 days of the report’s submission. That would put the deadline at May 19 for an announcement, but Kudlow said that Trump “could take longer” to reach a final decision.

Asian markets are responding to the Mnuchin headline and the positive Wall Street lead this morning with China’s bourses leading the advance – the Shanghai Comp (+2.54%), CSI (+3.21%) and Shenzhen Comp (+2.60%) are all up. The Nikkei (+0.78%), Hang Seng (+0.77%) and Kospi (+0.42%) are also up. Elsewhere, futures on the S&P 500 are up +0.18%. In terms of overnight data releases, we saw Japan’s February industrial production in line with consensus at +1.4% mom, marking the first gain after three consecutive negative readings while the February unemployment rate came in at 2.3% yoy (vs. 2.5% yoy expected), matching the 25 year low set in May 2018. February retail sales came in at +0.2% mom (vs. +1.0% mom expected) with an upward revision to the previous month to -1.8% mom from -2.3% mom. South Korea’s February industrial production was at -2.6% mom (vs. -0.7% mom expected), the largest decline since February 2017, due to a drop in the production of cars and transportation equipment. Meanwhile the UK’s March GfK consumer confidence number was unchanged compared to prior month at -13 (vs. -14 expected).

Before this US equities advanced yesterday perhaps helped by some slightly positive real-time economic data (more below). The S&P 500, DOW, and NASDAQ rose +0.36%, +0.36%, and +0.34%, with gains fairly broad-based. The main laggard was utilities, as rising rates pressured the bond-proxy sectors. Earlier in the day, European indexes had a mostly negative day, with the STOXX 600 down -0.12%, though the DAX did eke out a +0.08% gain. Bund and treasury yields rose +1.2bps and +2.3bps, respectively, and the US move was encouragingly driven entirely by inflation breakevens. The 10y breakeven rate rose +3.3bps, its biggest rise since January, though at 1.86%, it’s likely still a bit low for the Fed to be completely comfortable. Notably, Japanese 10-year yields are down to -0.094%. The Bank of Japan’s stated policy is to keep them “around zero percent,” so they’re approaching the edge of the potential policy range, though it’s not clear how concerned the BoJ would be at falling yields, as opposed to rising yields.

Early yesterday, President Trump asked in a tweet that “OPEC increase the flow of Oil” because “price of Oil (is) getting too high.” That initially caused WTI oil prices to drop -2.04%, but they subsequently retraced higher as the session continued to end the day near flat at $59.38 per barrel. Energy sector stocks performed in-line with the broader index, rising +0.37%. The rebound was especially striking, since it coincided with a further rally for the dollar, with the DXY index gaining +0.47%. That sent an index of emerging market currencies to its lowest level since January 3, falling -0.16% on the day.

The Turkish Lira plunged again against the dollar, down -4.16% yesterday to reach 5.5603. The central bank announced that its foreign exchange reserves rose by $2.4bn last week, easing some concerns that it was using up its firepower trying to prevent currency depreciation, which helped the currency strengthen around +1.07% off its trough. Funding markets normalized a bit, with overnight liquidity back down to 32%, down from Wednesday’s peak of over 1,300%. This morning lira is down further -0.43%.

Turning to the Fed Speakers, James Bullard, president of the St. Louis Fed, said that he expects growth to rebound in second-quarter after a sluggish start to the year while adding that calls for a rate cut were “premature.” Elsewhere, John Williams, president of the New York Fed, said that “the most likely case” was for U.S. growth of 2% with the economy continuing to add jobs amid low unemployment and added that “I still see the probability of a recession this year or next year as being not elevated relative to any year.” On inversion of the yield curve, he said that “there’s a lot of reasons to think that it has been a recession predictor for reasons in the past that kind of don’t apply today,” and “I think it’s telling us that growth will be pretty modest” in the U.S. and global economies going forward.

Data releases were mixed yesterday but there was some positive more real-time signs in the US. US Q4 GDP saw a downward revision to an annualised QoQ rate of 2.2% (vs. 2.6% in the previous estimate), while the personal consumption reading was revised down to 2.5% from 2.8%. Pending home sales also fell by -1.0% in February (vs. -0.5% expected), bringing the YoY total to -5.0%. However, initial jobless claims came in beneath expectations at 211k (vs. 220k expected), the lowest reading in nine weeks, while the previous reading was also revised down by 5k. Furthermore, the Kansas City Fed manufacturing index rose sharply to 10 in March (vs. 0 expected), with the 9 point increase being the largest since December 2016.

In the Eurozone, the economic sentiment indicator released by the European Commission fell once again in March, reaching 105.5 (vs. 105.9 expected), its lowest level since October 2016 and the 9th consecutive monthly decline. Meanwhile, German consumer prices rose by 1.5% in March (vs. 1.6% expected), the lowest level for 11 months. It’ll be interesting to see whether today’s French and Italian inflation data and Monday’s for the Eurozone paint a similar picture.

Looking to the day ahead, we have the latest big Brexit vote as well as more trade talks in Beijing between the US and China. It’s also another busy day for data. From Europe, we’ve got French and Italian CPI readings for March, in Germany we’ve got February’s retail sales figures and March’s change in unemployment, and from the UK, we’ll get the latest reading of Q4 GDP, along with February’s mortgage approvals, consumer credit, and M4 money supply. From the US, we’ll get the final University of Michigan sentiment reading for March, personal income for February, personal spending for January, the MNI Chicago PMI for March, along with February’s new home sales. In Canada, we’ll get January’s GDP figure.

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 95.82 POINTS OR 3.20% //Hang Sang CLOSED UP 276.15 POINTS OR 0.96% /The Nikkei closed UP 172.85 POINTS OR 0.82%/ Australia’s all ordinaires CLOSED UP 0.08%

/Chinese yuan (ONSHORE) closed UP at 6.124 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 58.52 dollars per barrel for WTI and 67.05 for Brent. Stocks in Europe OPENED MIXED

ONSHORE YUAN CLOSED UP // LAST AT 6.7134 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7228 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/

3 b JAPAN AFFAIRS

3 C CHINA

China is testing long range missiles from a concealed ship. The Israelis were also working on something like this

(courtesy zerohedge)

China Testing Long-Range Cruise Missile Fired From Concealed Ship Container

Could the next great Chinese advanced missile threat come disguised as an innocuous looking shipping transport vessel? A new report in The Washington Free Beacon suggests so, as it details China’s new long-range cruise missile which can be launched directly from a shipping container device, which is meant to conceal detection of the threat right up until the moment of launch.

Alarmingly, it’s already being flight tested, according to analysts cited in the report, which further finds the technology “could turn Beijing’s large fleet of freighters into potential warships and commercial ports into future missile bases.” If cruise missiles can be hidden in international shipping containers, China could be a major threat to western targets simply as it moves millions of tons of goods every year.

Rick Fisher, a senior fellow at the International Assessment and Strategy Center, told the Free Beacon, “Shipping container missile launchers can be smuggled through ports or via highway ports of entry and stored for years in a climate-controlled building within range of U.S. military based and taken out when needed for military operations.”

“Potentially, Chinese missile launching containers could be stored near the Port of Seattle, waiting for the day they can launch an electromagnetic pulse warhead-armed missiles over the Bangor nuclear ballistic missile submarine base,” he speculated.

The concealed nature of a launch-ready long-range missile also presents the nightmare scenario of ease of proliferation to rogue actors such as Iran or North Korea. “Containerized missiles give China, Russia, and its rogue state partners new options for directly or indirectly for attacking the United States and its allies,” Fisher added.

However, it should be noted that a defense company in Russia appears to have been the first to develop and market shipping container weapons nearly a decade ago. Yet even at that time analysts began to worry of that Russian private sector defense technology development, “Unless sales are very tightly controlled, there is a danger that it could end up in the wrong hands.”

The new missile being developed as part of the container-launch device program is said to be a variant of an advanced anti-ship missile called YJ-18C, according to US defense officials cited in the report.

One career US military officer and former Pacific Fleet intelligence chief described how a container concealed Chinese cruise missile could be a game changer in terms of assessing threats near US waters and ports:

Retired Navy Capt. Jim Fanell, a former Pacific Fleet intelligence chief, said a containerized YJ-18 anti-ship cruise missile would add a significant threat to the Navy given the volume of Chinese container ships that enter U.S. ports on the west and east coast, well within range of the vast majority of the U.S. fleet.

“If this capability is confirmed, it will require a completely new screening regime for all PRC flagged commercial ships bound for U.S. ports,” Fanell said.

Additionally the container-launched missiles could be targeted in foreign ports used by Chinese-flagged merchant vessels.

On that front, Washington military planners say there is much to be concerned about. One adviser and research professor at the US Army War College described China’s military activities in Latin America and the Caribbean as “extensive”.

A Russian company had previously simulated how its “container weapons” systems would operate.

Professor R. Evan Ellis said that during a conflict, “China’s substantial commercial base, its access to ports, and its military-to-military contacts in the Caribbean might prove useful,” as cited in the Free Beacon.

“All of these add up to growing Chinese influence in a region located close to the U.S. as well as its most important Atlantic coast military facilities,” he added.

The report noted that Israel has also for years been developing a similar container launch system for a short range ballistic missile, called the “LORA”.

end

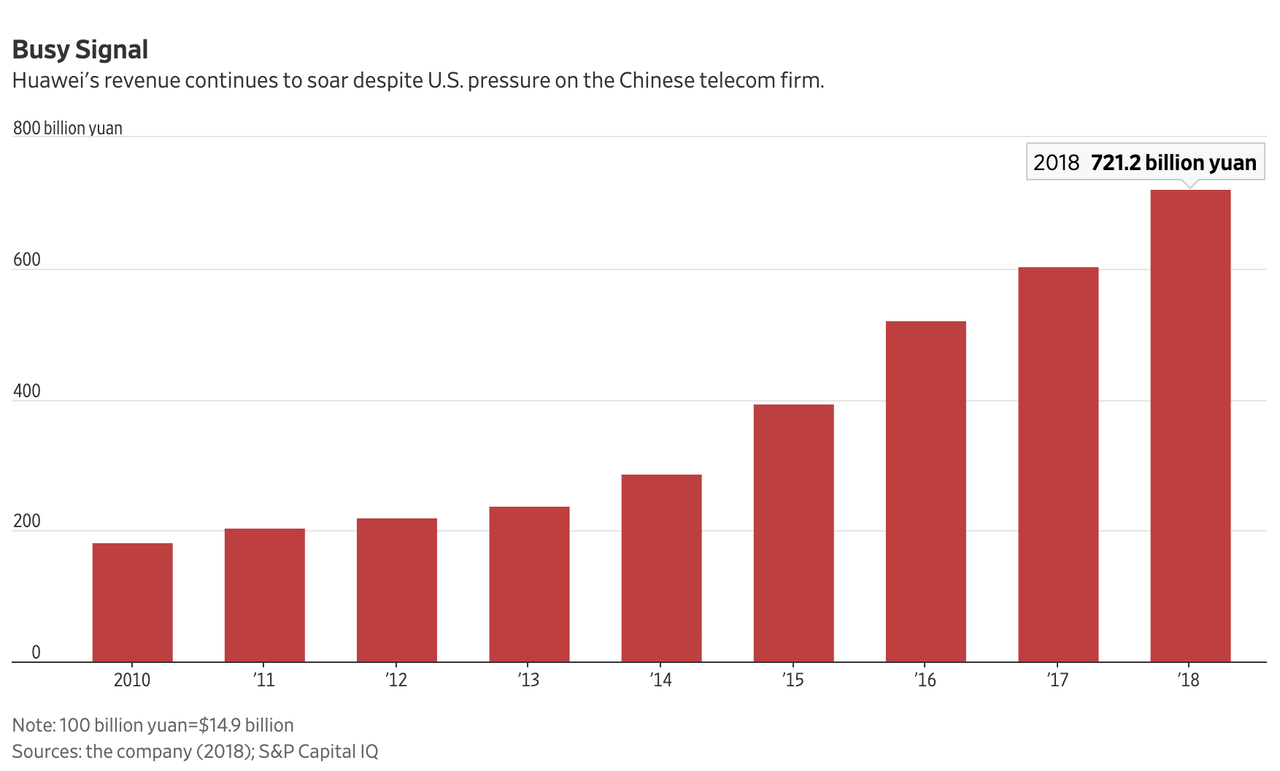

Huawei profits soar in 2018 along with revenue despite the uSA shutdown its products. The Chairman tells Washington to drop its “loser attitude”

(courtesy zerohedge)

Huawei Profits Soar in 2018; Chairman Tells Washington To “Drop Its Loser Attitude”

When it first launched its global lobbying campaign to shut Chinese telecoms giant Huawei out of the West, Washington was probably, in retrospect, feeling a little overconfident. After a ban on selling American-made components to ZTE (another Chinese telecoms giant) nearly precipitated the company’s collapse, a coordinated smear campaign – including the arrest of one of the company’s top executives, a pair of criminal indictments, and a ban on selling its products in the US – designed to weaken Huawei’s 5G leadership should at least have curbed the company’s torrid revenue and profit growth.

Unfortunately for rival US telecoms giants, America couldn’t have been more wrong, as the Wall Street Journal pointed out.

Though Huawei is a privately held company, it has made a habit of releasing earnings figures. And the numbers from 2018 are simply staggering. Despite being effectively shut out of the US and several of its allies in the “Five Eyes” intelligence alliance (Australia and New Zealand), Huawe’s revenue for 2018 rose 20% to 721.2 billion yuan ($107 billion) from 603.6 billion yuan a year earlier. Meanwhile, net income for 2018 rose 25% to 59.3 billion yuan.

Heaping more embarrassment on the US, the EU, one of Washington’s staunchest “allies”, earlier this week refused to call for a ban or any restrictions on Huawei’s products. This after the UK and Germany had declared Huawei’s telecoms equipment suitable to be used in the country’s soon-to-be-built 5G infrastructure.

Although Huawei saw a slight dip (1.3%) in its carrier business, Huawei rotating chairman Guo Ping said this dip was expected, as company’s hold off on repairs and upkeep before breaking ground on their new 5G networks. The company recorded rapid growth in its consumer business, which includes smartphones, and its enterprise cloud-computing business. In a major milestone for the company, its smartphone shipments rose 35% last year to 206 million units, making Huawei the world’s second largest supplier of handsets.

Despite Washington’s ‘national security threat’ warnings, Huawei won 30 new 5G contracts from carriers in 2018. The company recently won contracts from customers in South Korea and the UAE.

Guo, who has never shied away from mocking the US, celebrated the company’s numbers by lobbing yet another insult Washington’s way, as Reuters reported, Guo said he hoped the US government would drop its “loser’s attitude” and drop its smear camapign.

“The U.S. government has a loser’s attitude. It wants to smear Huawei because it cannot compete against Huawei,” Guo Ping said. President Trump is going to love hearing that.

4.EUROPEAN AFFAIRS

BREXIT/EU\\

Mark Mobius of Templeton fame describes the deteriorating financial conditions inside the uK..their balance of payments is awful accompanied by huge debt. He feels that once the tether is broken from the EU, the country will be forced to raise rates to keep funds in the country. He feels that there is a risk of a downgrade in their sovereign debt

(courtesy Mark Mobius/zerohedge)

Mark Mobius: Brexit Has Turned UK Into “An Emerging Market Economy”

With all hell breaking loose in Turkey this week, one would think Mark Mobius, the pioneering portfolio manager who launched one of the first EM-focused funds more than 30 years ago, would be focusing his attention on an issue more germane to his area of expertise – like whether Turkey’s deteriorating financial position might breed contagion – or something along those lines.

Instead, he’s become the latest standard-bearer for “Project Fear”, warning during an interview with the FT that the UK already resembles an “emerging economy” and that the situation will only get worse once it finally departs the EU – particularly if it does so without a. deal.

“The UK is like an emerging market now. Their balance of payments is terrible; their government debt is terrible; their fiscal debt is terrible,” said Mr Mobius, who spent most of his career working for the US asset manager Franklin Templeton.

Subtly equating the UK with Greece and Portugal, Mobius argued that once the UK leaves the EU, ratings agencies will be forced to downgrade its sovereign credit rating once it no longer can “ride the coattails” of the trade bloc.

“Up to now, the UK is riding on the coat-tails of the EU, in the sense that [the UK] can have very low interest rates,” Mr Mobius told the FT at an event in New York this week hosted by the Emerging Markets Investors Alliance.

“As soon as they break, people are going to start looking hard and fast. The rating agencies will say ‘wait a minute, no more EU association? We’ve got to downgrade.'”

But getting at the real reasons behind his antipathy toward Brexit, Mobius lamented the fact that the UK might lose its status as a center for emerging market countries, thanks to its dominance in global FX markets, and the fact that many companies based in emerging markets list their shares in the UK. As it stands, Mobius can just hang out in London and “these people will come to us”. But that could easily change.

“The unfortunate thing for us in emerging markets is that the UK is really a centre for emerging countries for [public] listings or for company meetings,” Mr Mobius said.

“We can sit in London and these people will come to us.”

If the UK leaves without a deal, some 5,500 UK businesses would lose their “passporting” privileges – meaning they would need to deal with a separate set of regulatory guidelines to do business in the EU. If the UK leaves wiithout a deal, Mobius said his firm would likely leave London for “Paris, Munich or somewhere else.”

“We’ll have to go to Paris, Munich or somewhere else in the EU,” Mr Mobius said of his firm.

“I would like to go to Spain. I want warm weather.”

Does Mobius really feel that the British people “made a mistake” when they voted for Brexit? Or is he just cranky that his firm might face a heap of new regulatory hurdles and might need to move?

Pound Surges, Erasing Earlier Losses, As Former Brexit Secretary Backs Deal

Update (7:07 am ET): The pound just won’t stop…up 80 pips and counting…

For those who are catching up on all the Brexit drama that has unfolded over the past 24 hours, here’s a quick recap courtesy of Ransquawk:

*LONG STORY SHORT: The Brexit deal PM May brought forth is essentially made up of two parts, the Withdrawal agreement (which sets out the terms of the UK’s departure from the EU) and the Political Declaration (which outlines the shape of future UK-EU relations). To get around House Speaker Bercow’s requirements of a “changed” deal to be put for a third vote, PM May decided to split the deal and only vote on the first part, i.e. the WA.

*TODAY’S SCHEDULE [GMT]

14:30 – Vote on the Withdrawal Agreement

*AMENDMENTS: House Speaker Bercow has selected no amendments for debate in Parliament today

*WHAT PM MAY NEEDS

NUMBERS: For PM May to get majority for her deal, she needs to:

Retain all 242 existing votes

Win over all 75 opponents in her own party, including 69 Brexiteers (5 already indicated they will oppose it, one Tory MP abstained from MV2, a vote which could give PM a majority of 2)

For every Tory MP who opposes the deal, PM May needs one MP from another party or two opponents willing to abstain

Total excludes the 4 tellers, 3 deputy speakers, 7 Sinn Fein MPs

*WHAT IS EXPECTED:

PM May is expected to again be defeated in Parliament as she is unlikely to conjure up support from Labour and DUP (who have confirmed they will vote against the WA). There is still no confirmed direction from the ERG, although the group has said that they are likely to follow the DUP’s lead.

Cabinet sources have also noted that the WA is unlikely to pass as there is not enough time to get the votes.

MPs claim that just 12 hardcore Tory ERG MPs are left opposing PM May’s deal; according to Sun’s Deputy Political Editor Steve Hawkes

A UK Minister reportedly believes that PM May’s WA will be voted down by 20 votes; according to Mail on Sunday’s Deputy Political Editor Cole