GOLD: $1291.05 DOWN $0.20 (COMEX TO COMEX CLOSING)

Silver: $15.13 UP 2 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1290.40

silver: $15.16

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today: 0/131

EXCHANGE: COMEX

CONTRACT: APRIL 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,290.000000000 USD

INTENT DATE: 04/02/2019 DELIVERY DATE: 04/04/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 H HSBC 19

657 H MORGAN STANLEY 11

661 C JP MORGAN 29 21

686 C INTL FCSTONE 6

730 C PTG DIVISION SG 6 2

737 C ADVANTAGE 59 8

800 C MAREX SPEC 26 1

880 H CITIGROUP 69

905 C ADM 5

____________________________________________________________________________________________

TOTAL: 131 131

MONTH TO DATE: 3,042

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 131 NOTICE(S) FOR 13100 OZ (0.407 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 3042 NOTICES FOR 304,200 OZ (9.46 TONNES)

SILVER

FOR APRIL

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

20 NOTICE(S) FILED TODAY FOR 100,000 OZ/

total number of notices filed so far this month: 695 for 3,475,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

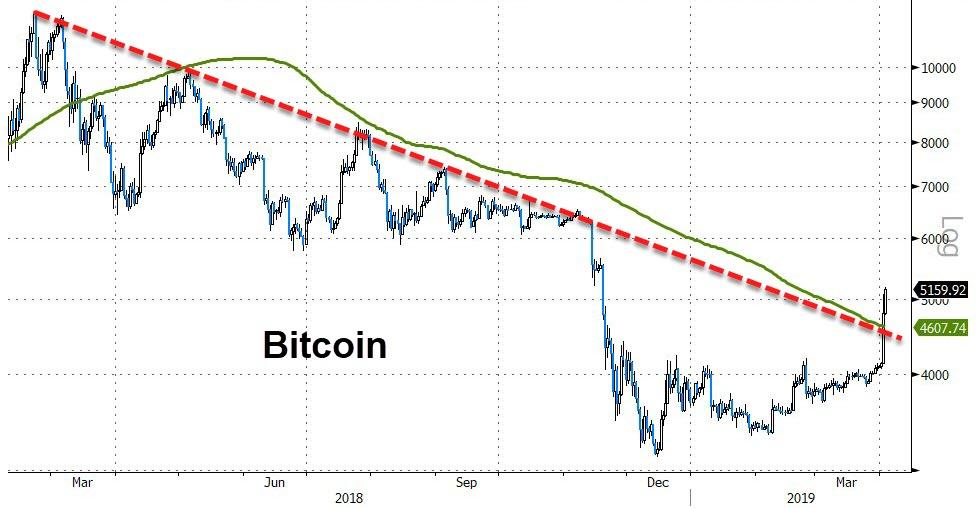

Bitcoin: OPENING MORNING TRADE :$4916 UP $57

Bitcoin: FINAL EVENING TRADE: $5265 up $413

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, THE SILVER COMEX IS PRELIMINARY DATA//THE JERKS AT THE CME STILL CANNOT GET THEIR FINAL DATA

THIS TIME BY A SMALL SIZED 322 CONTRACTS FROM 199,556 UP TO 199,592 DESPITE YESTERDAY’S 1 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE MUST HAVE HAD CONSIDERABLE SHORT COVERING AGAIN TODAY.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR MAY, 1044 FOR MARCH 2020 0 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1044 CONTRACTS. WITH THE TRANSFER OF 1044 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1044 EFP CONTRACTS TRANSLATES INTO 5.22 MILLION OZ ACCOMPANYING:

1.THE 1 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

AND NOW 3.860 MILLION OZ STANDING FOR SILVER IN APRIL.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

4542 CONTRACTS (FOR 3 TRADING DAYS TOTAL 4542 CONTRACTS) OR 22.71 MILLION OZ: (AVERAGE PER DAY: 1514 CONTRACTS OR 7.570 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 22.71 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 3.24% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 595,40 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 322 DESPITE THE 1 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1044 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A CONSIDERABLE SIZED: 1366 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 322 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1044 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 1 CENT LOSS IN PRICE OF SILVER ???? AND A CLOSING PRICE OF $15.11 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.997 BILLION OZ TO BE EXACT or 143% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 20 NOTICE(S) FOR 100,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ AND NOW APRIL AT 3.860 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY ANOTHER CONSIDERABLE SIZED 2641 CONTRACTS, TO 440,170 DESPITE THE GAIN IN THE COMEX GOLD PRICE/(A RISE IN PRICE OF $1.50//YESTERDAY’S TRADING).

WE JUST HAD OUR FIFTH STRAIGHT DAY OF AN OPEN INTEREST COLLAPSE DUE TO THE ANTICS OF THE SPREADERS. IT LOOKS LIKE THE SPREADERS LIQUIDATE THEIR CONTRACTS NOT SIMULTANEOUSLY BUT AT DIFFERENT TIMES DURING THE TRADING DAY TO CAUSE THE CASCADE OF PRICING IN OUR PRECIOUS METALS AND THAT IS HOW THEY ALWAYS WIN ON OPTION EXPIRY..THEY ARE SO CROOKED. AT THE END OF THE DAY THEY ELIMINATE THE OTHER HALF OF THE SPREAD TRADE. THE COLLAPSE OF OPEN INTEREST SHOULD END WITH THIS READING AND ADVANCE FROM TUESDAY ON..

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4646 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 4646 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020l 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 440,170. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A NET GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2005 CONTRACTS: 2641 OI CONTRACTS DECREASED AT THE COMEX AND 4646 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 2005 CONTRACTS OR 200,500 OZ OR 6.446 TONNES. YESTERDAY WE HAD A RISE IN THE PRICE OF GOLD TO THE TUNE OF $1.50….AND YET WITH THAT, WE HAD A GOOD GAIN IN TONNAGE OF 6.446 TONNES!!!!!!.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 16,673 CONTRACTS OR 1,667,300 OR 51,86 TONNES (3 TRADING DAYS AND THUS AVERAGING: 5557 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAYS IN TONNES: 51.86 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 51.86/2550 x 100% TONNES = 1.05% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1428.91 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIR SIZED DECREASE IN OI AT THE COMEX OF 2641 DESPITE THE GAIN IN PRICING ($1.50) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A VERY STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 4646 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 4646 EFP CONTRACTS ISSUED, WE HAD A GOOD GAIN OF 2005 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

4646 CONTRACTS MOVE TO LONDON AND 2641 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 6.446 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH A RISE IN PRICE OF $1.50 IN YESTERDAY’S TRADING AT THE COMEX!!!!!

we had: 131 notice(s) filed upon for 131 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $0.20 TODAY

A MASSIVE E3.81 TONNES OF GOLD REMOVED FROM THE GLD

THIS GOLD WAS USED AT THE COMEX FOR RAIDING PURPOSES. NO QUESTION ABOUT IT; THE COMEX IS VOID OF GOLD…

INVENTORY RESTS AT 764.29 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 2 CENTS IN PRICE TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 309.167 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A SMALL SIZED 322 CONTRACTS from 199.556 UP TO 199,592 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 1044 FOR MAY AND MARCH 2020: 0 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1044 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 322 CONTRACTS TO THE 1044 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A CONSIDERABLE GAIN OF 1366 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 6.83 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH. AND NOW 3.860 MILLION OZ FOR APRIL.

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 1 CENT FALL IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1044 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 39.47 POINTS OR 1.24% //Hang Sang CLOSED UP 361.72 POINTS OR 1.22% /The Nikkei closed UP 207.90 POINTS OR 0.97%/ Australia’s all ordinaires CLOSED UP 0.65%

/Chinese yuan (ONSHORE) closed UP at 6.7083 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 62.67 dollars per barrel for WTI and 69.65 for Brent. Stocks in Europe OPENED GREEN

ONSHORE YUAN CLOSED UP // LAST AT 6.7083 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7133 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)Algos misread the USA/China headlines that they have resolved most of the trade deal issues. No they have not…

it does not matter… global stocks surge!

( zerohedge)

ii)Not a good harbinger of things to come; Apple slides as Chinese iphone prices are crashed

( zerohedge)

4/EUROPEAN AFFAIRS

i)BREXIT/EU/

It is the uncertainty that it killing Britain. Our bet is that Britain escapes the clutches of the EU and will be better off but will suffer a bit in the short term

( zerohedge)

The big German Institutes are now cutting GDP growth in half down to .8% year/year

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)TURKEY

( Benny Anvi/New York Sun)

i b)this is very important: Mike Pence issues Turkey an ultimatum: choose being a ember of NATO or buy Russian S400

ii)ISRAEL/UK/USA

The UK condemns Trump’s recognition of the Golan Heights, territory that the Israeli’s will never give up especially with the Iranians inside Syria. However this condemnation will further hurt European relations with the uSA. The Europeans are trying to skirt sanctions against Iran

a real mess

( zerohedge)

6. GLOBAL ISSUES

My favourite Bellwether stock indicating global growth is Caterpillar. Today Deutsche Bank downgraded this company slashing its price target from $152 down to $128.

( zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

VENEZUELA

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning

ii)Market data

a)Very unusual: the always bullish and biased ADP report for the first since in many moons shows the weakest jobs gains as manufacturing and construction tumbled:

( ADP)

b)Next on tap is USA auto sales and March was dismal

( zerohedge)

c)We knew that this will happen: mortgage refi’s soar due to the plummeting interest rates;

( zerohedge)

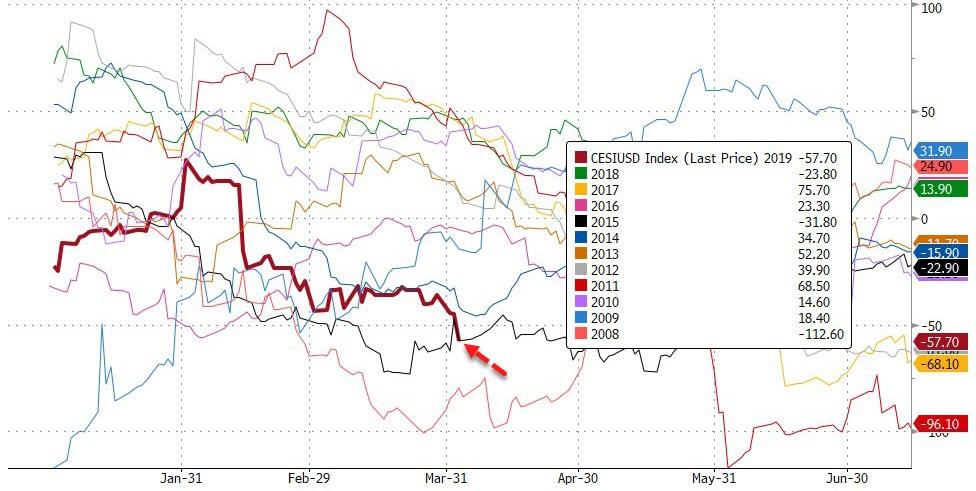

d)This data point caught everybody in bewilderment: the usually strong ISM service survey plunges to 19 month lows. Usually ISM, a soft data entry, is generally very bullish.

(courtesy zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

a)Interesting: 25% of all Millennials are now longer having sex due to financial problems..plus other goodies

( Simon Black/Sovereign Man)

b)We now have preliminary findings as to how the Boeing 737 Max 8 went down. It seems the pilots first correctly de-activated the MCAS software once the nose of the plan pointed down. However by accident they must have re engaged the software.

bad news for Boeing…

( zerohedge)

c)This is no joke: Trump is to give China until 2025 to commit to the trade deal. What a farce!

iv)SWAMP STORIES

a)this is one big joke: the Democrats are going to go on a nationwide tantrum if the Mueller report is not released forthwith

( zerohedge)

b)And it is done: the House democrats vote to subpoena the Mueller report because they cannot wait two weeks

c)Comey is one big joke!

( Earle/Daily Mail)

e)the Ukrainian episode with his son to which we have highlighted to you in the past, is finally coming to light. A closed probe is now revived

end

Let us head over to the comex:

AFTER APRIL, WE HAVE THE ACTIVE DELIVERY MONTH OF MAY AND HERE THE OI FELL BY 3814 CONTRACTS DOWN TO 129,083. CONTRACTS.. THE NEXT MONTH OF JUNE ADDED 23 CONTRACTS TO TOTAL 25. AFTER JUNE, THE VERY BIG DELIVERY MONTH OF JULY HAD A GAIN OF 2838 CONTRACTS UP TO 42,137 CONTRACTS.

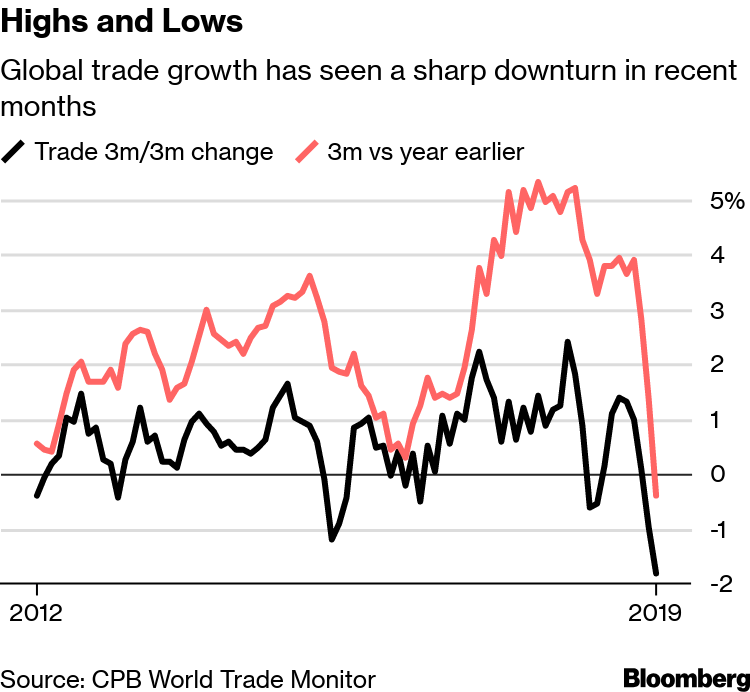

7 Reasons To Worry About the Global Economy In Charts

a) Trade Uncertainty: Global trade has seen a sharp downturn in recent months

b) Policy Uncertainty: Brexit, U.S., China & global economic policy uncertainty surges

c) Financial Conditions: Financial markets are beginning to show signs of stress

d) Dollar Strength: Greenback strength impacts emerging markets such as Turkey

e) Economic Surprises: Economic data globally has been surprising to the down side

f) Low-flation: Despite unprecedented monetary support, deflation remains a risk

g) Debt: U.S. leveraged loan market showing stress

– The global economy is wobbling and is predicted to grow at just 3.3 percent this year

– Trade tensions, policy uncertainty taking a toll on confidence

– WTO on Tuesday cut its forecast for trade growth in 2019

Source: Organisation for Economic Cooperation and Development

The global economy is wobbling in 2019, giving rise to recession fears and forcing the world’s central banks to consider renewed policy easing.

The stresses have prompted repeated forecast downgrades by governments and other authorities. On Tuesday, the World Trade Organization slashed its 2019 trade projection to the weakest in three years. The OECD cut its economic forecast last month and warned of downside risks that could mean an even worse outcome.

Across trade, equities, currencies and interest rates, here are a few reasons analysts are worried about the global economic outlook:

1. Trade

U.S.-China trade talks sputter on, without any clear sign of resolution. The Chinese economy has been a difficult one to pin down, sliding more than expected and then improving in fits and starts. That’s feeding into a broader malaise in global demand, which has shown up in the form of dramatically slower trade flows.

While quarterly data show a frightening drop at the start of 2019, a more timely Bloomberg Economics dashboard of 10 critical gauges has pointed to ongoing weakness. German companies’ sentiment showed a glint of hope in March after six straight declines.

Highs and Lows

Global trade growth has seen a sharp downturn in recent months

Source: CPB World Trade Monitor

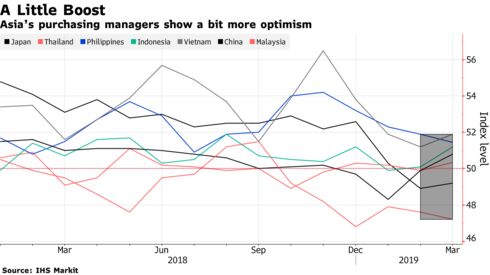

And the pain is felt acutely in Asia, home to some of the world’s most export-reliant economies. Purchasing manager indexes across the continent are only starting to show hints of a China-led rebound after several months of souring.

2. Policy Uncertainty

Trade talks and the tariff wars have fed into the guessing game around how politics and policy will interfere with the fundamentals. Also in the mix are Brexit, a spate of elections — some of them messy, like Thailand — and the sharp turn in the global monetary policy cycle. China’s policy uncertainty has been especially pronounced as analysts try to pick apart how officials will manage the slowdown there.

In the U.K., Brexit has become the weight that won’t go away, still holding back capital spending and broader economic growth, as London-based Bloomberg Economics economist Dan Hanson shows. The British Chambers of Commerce said this week that investment intentions are at the lowest in eight years as firms refuse to commit to projects in such an uncertain backdrop.

3. Financial Conditions

The financial markets have taken some of the developments in stride, while still showing signs of stress.

It’ll be a gauge to keep an eye on, but for now, the Bloomberg U.S. Financial Conditions Index — which measures the overall level of financial stress in money, bond and equity markets — is at least looking better than it did since touching a 2 1/2-year low in December. A positive value in that measure indicates accommodative financial conditions, while a negative value indicates tighter financial conditions relative to pre-crisis norms.

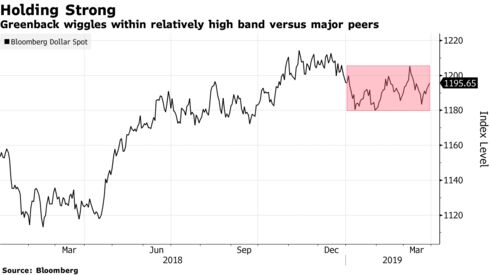

4. Dollar Strength

Emerging-market officials especially are attuned to any durable signs that the greenback will return to the strengthening path that added a lot of pressure in 2018. The dollar remains in a relatively stronger band against a basket of major currencies, particularly compared with its position a year ago.

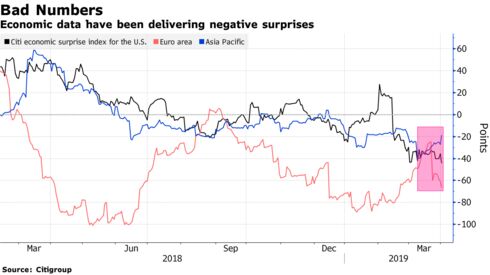

5. Economic Surprises

Adding to the gloomy hard data is the fact that analysts just haven’t been very good at forecasting recently. Releases have been surprising on the negative side more often — across the U.S., Europe and Asia-Pacific.

It’s even more concerning when you consider economists’ terrible record on predicting recessions.

6. Low-flation

Since Federal Reserve chief Jerome Powell branded it “one of the major challenges of our time,” stubbornly low inflation has garnered even more attention around the world. Despite unprecedented monetary support, central bankers have been constantly frustrated in their attempts to generate sustainable price growth. Central bankers’ worries about price growth aren’t going away.

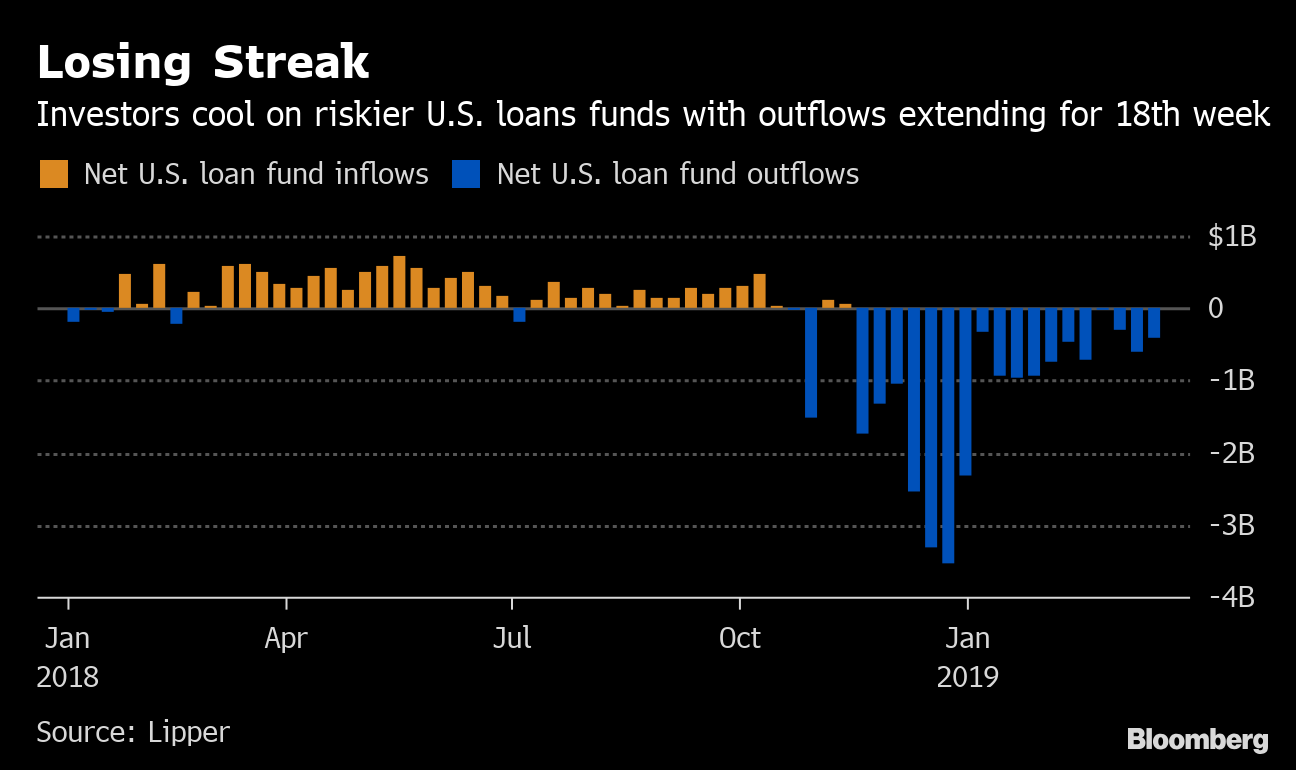

7. Debt

While debt worries might vary by economy, one area getting extra attention lately — including from former Fed chief Janet Yellen — is the U.S. leveraged loan market. UBS Group AG and Deutsche Securities Inc. analysts have cited the risk, and Taimur Baig, chief economist at DBS Bank Ltd. in Singapore, said last week that he shares Yellen’s concern.

Losing Streak

Investors cool on riskier U.S. loans funds with outflows extending for 18th week

Source: Lipper

News and Commentary

Gold books slight gain as stock-market bulls take a breather (MarketWatch.com)

Gold firms as U.S. stocks retreat; strong dollar caps gains (Reuters.com)

Italy to pass decree on Thursday to reimburse savers hit by bank rescues (Reuters.com)

U.S. new construction plunged about 53.9% (GoldReview.com)

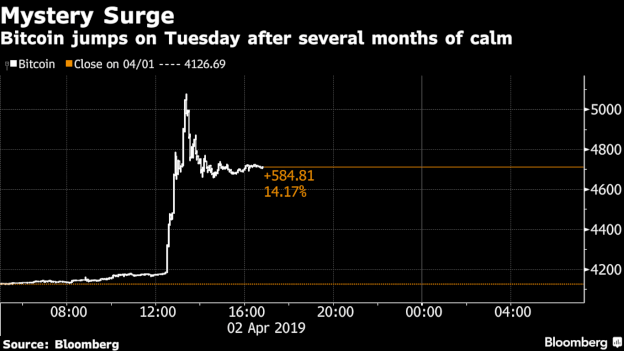

Bitcoin’s Sudden Surge Propels It Above $5,000 (Bloomberg.com)

Source: Bloomberg

Gold Is Heading Towards $1,400, Not $1,200 — Bloomberg Intelligence (Bloomberg.com)

All the Reasons to Fret About the Global Economy, in Charts (Bloomberg.com)

How A ‘No Deal’ Brexit Could Lead To The “Lehmanization” Of Europe (ZeroHedge.com)

Brexit batters businesses and the economy as cliff edge looms (Independent.co.uk)

Ireland Property Rush Risks Repeat of Crisis (Bloomberg.com)

Gold breaks out from trendline resistance (IG.com)

Gold Prices (LBMA PM)

02 Apr: USD 1,287.20, GBP 984.97 & EUR 1,148.95 per ounce

01 Apr: USD 1,291.90, GBP 987.27 & EUR 1,149.15 per ounce

29 Mar: USD 1,291.15, GBP 991.09 & EUR 1,151.19 per ounce

28 Mar: USD 1,306.90, GBP 995.20 & EUR 1,161.18 per ounce

27 Mar: USD 1,318.25, GBP 997.78 & EUR 1,168.23 per ounce

26 Mar: USD 1,315.25, GBP 993.15 & EUR 1,162.02 per ounce

Silver Prices (LBMA)

02 Apr: USD 15.02, GBP 11.51 & EUR 13.42 per ounce

01 Apr: USD 15.07, GBP 11.50 & EUR 13.42 per ounce

29 Mar: USD 15.10, GBP 11.52 & EUR 13.45 per ounce

28 Mar: USD 15.19, GBP 11.58 & EUR 13.53 per ounce

27 Mar: USD 15.40, GBP 11.65 & EUR 13.65 per ounce

26 Mar: USD 15.44, GBP 11.66 & EUR 13.65 per ounce

Recent Market Updates

– Central Banks Continue to Buy Gold at a Record Clip

– ItalExit and Cyber Risks in a Cashless World May Be Bigger Risks Than Brexit : Interview with GoldCore CEO

– Ireland and EU Countries Must Seek ECB Approval to Manage Gold Reserves – Draghi

– Global Risks Increasing – Underlining The Case For Gold in 2019 (GoldCore Video Presentation)

– Brexit and Learning To “Live With Boom and Bust Economic Cycles”

– ‘No Deal’ Brexit Risk Impacting UK and Irish Economies – Gold Gains On Recession Concerns

– America’s “Debt Crisis Is Coming Soon”

– Russia Buys 1 Million Ounces Of Gold In February – Become Your Own Central Bank

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

GATA) Sprott portfolio manager is suspicious of last week’s flash crash in monetary metals

Sprott senior portfolio manager Reik wonders if last week’s flash crash was perhaps due to the antics of one or more big players trying to rig markets

(courtesy Kingworldnews/Sprott/Reik)

Submitted by cpowell on 04:43PM ET Wednesday, April 3, 2019. Section: Daily Dispatches

12:35a Thursday, April 4, 2019

Dear Friend of GATA and Gold:

In commentary posted at King World News, Sprott USA Senior Portfolio Manager Trey Reik can’t help wondering if last week’s flash crash in the monetary metals was not the product of ordinary market action but that of one or more big players trying to rig prices down for first-quarter valuation purposes.

Reik writes: “The tenor for precious metals markets heading into March month-end may have been set on Thursday morning, March 27. At 9:37 a.m. 7,000 Comex gold contracts were sold at-the-market in the space of one minute. This means that 700,000 ounces (or 21.77 tonnes) with a notional value of $921 million was dropped into Comex (electronic) pits without price limitation. While spot gold did decline roughly $7 during the ‘flash crash,’ it finished the day in orderly trading above $1,300 (at $1,309.57).

“Perhaps in recognition that a far more concerted effort would be required to achieve a month-end mark below $1,300, volume in Comex gold futures on Friday, March 28, exploded to 528,626 contracts, or roughly $69 billion in notional value. For context, the World Gold Council reports that average daily trading volume for Comex gold futures totaled just $28 billion in February 2019 and $36 billion year to date in 2019. Related to the massive March 28 trading volume was an outstanding-interest drop of 48,565 (9.62 percent) for the day, almost all of which was related to a 93.3 percent collapse in remaining April (front month) outstanding interest. That such a large percentage of remaining April open interest was liquidated without traditional roll into June contracts only heightens the pointed nature of trading last week.”

Reik’s analysis is headlined “Trey Reik Asks WTF Is Going On At the Comex?” and it’s posted at KWN here:

https://kingworldnews.com/trey-reik-asks-wtf-is-going- on-at-the-comex/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7083/

//OFFSHORE YUAN: 6.7133 /shanghai bourse CLOSED UP 39.47 POINTS OR 1.24% /

HANG SANG CLOSED UP 361.72 POINTS OR 1.22%

2. Nikkei closed //UP 207.90 POINTS OR 0.97%

3. Europe stocks OPENED GREEN

/USA dollar index FALLS TO 97.03/Euro RISES TO 1.1246

3b Japan 10 year bond yield: RISES TO. –.05/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.52/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 62.67 and Brent: 69.65

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP /OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO –.00%/Italian 10 yr bond yield DOWN to 2.50% /SPAIN 10 YR BOND YIELD UP TO 1.14%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.50: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.66

3k Gold at $1293.85 silver at:15.16 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 11/100 in roubles/dollar) 65.21

3m oil into the 62 dollar handle for WTI and 69 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.52 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9967 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1209 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISING to –0.00%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.52% early this morning. Thirty year rate at 2.92%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.6233..GETTING DANGEROUS

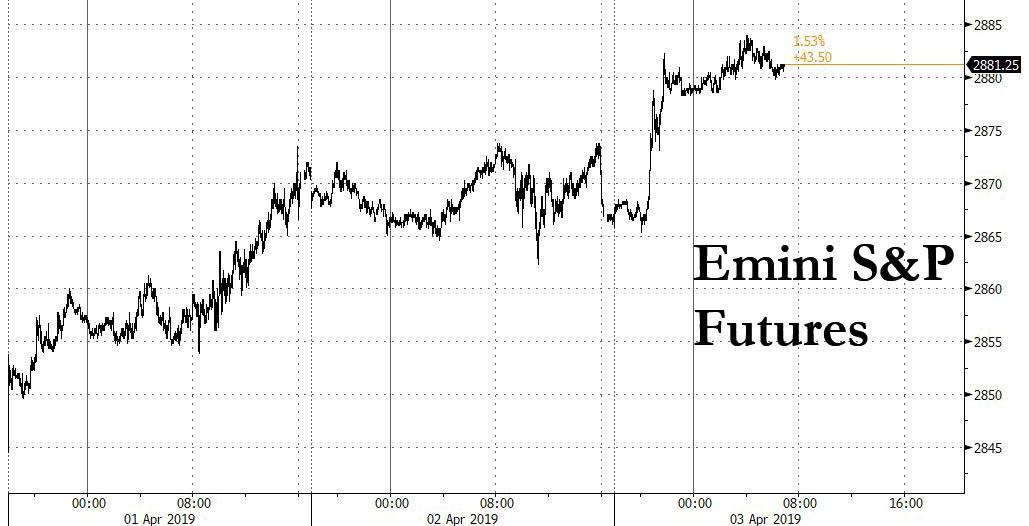

Futures Jump, World Stocks Hit 6 Month High On Trade Deal Optimism

US futures jumped and world stocks rallied to a six-month high following the latest dose of daily “trade deal optimism” when the FT reported what everyone already knows (but algos, who have a 10 millisecond memory, have forgotten), namely that the US and China have already resolved most of the easy issues standing in the way of a deal to end their long-running trade dispute but are still haggling over the difficult parts, namely how to implement and enforce the agreement.

That, coupled with some more reassuring economic data, helped S&P futures jump 14 points, fast approaching their Sept all time highs, pushed Germany’s 10-year bond yield back above zero percent, hit the dollar as the euro strengthened for the first time in seven sessions as oil neared the key $70 per barrel mark — a multi-month high — on supply concerns.

“We’re being told that we’re 90 percent of the way there which is obviously encouraging but the final 10 percent — which apparently includes the enforcement mechanism and the removal of tariffs — could take some time to iron out,” said Craig Erlam, senior market analyst at Oanda in London. “Investors are happy to be patient here in the hope that the two sides get this right and put an end to a trade war that has clearly taken its toll on markets.”

And since algos quickly calculated that 10% is less than 90% and ignored the actual politics behind the calculus, they promptly activated buy programs and U.S. equity-index futures rose and the Stoxx Europe 600 index jumped, led by miners, as the latest batch of Service PMI data from Italy to Germany also helped ease some of the concern over the euro area’s growth outlook.

Europe’s Stoxx 600 index rose almost 0.8% to their highest since August. German stocks rose 1 percent to its highest level since October, while in Paris, French stocks scaled a similar high.

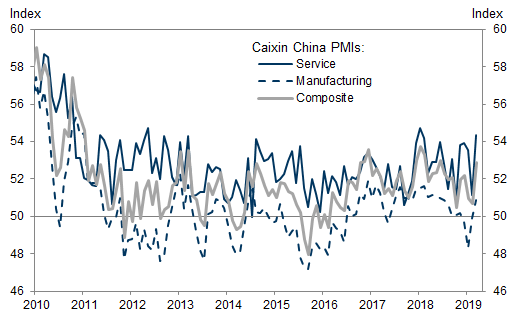

Europe’s strong session followed overnight gains in Asia where MSCI’s broadest index of Asia-Pacific shares outside Japan climbed to a seven-month peak, buoyed by stronger-than-expected Chinese services data as China’s Caixin Services PMI printed stronly in March, at 54.4 vs. Exp. 52.3 (Prev. 51.1), the highest since January 2018.

Hopes for a deal to end the trade war between the world’s two largest economies were also prompted by fresh comments from White House economic adviser Larry Kudlow that Washington expects “to make more headway” in talks this week. To be sure, analysts were giddy at the prospect of an imminent deal:

- “What we’re seeing is that markets have climbed a world of worry but there is progress on trade, a recession is unlikely, central banks have made nods to more dovish policy,” said Chris Bailey, European Strategist at Raymond James. “If you put that into the mix I’m not surprised risk assets have moved up.”

- “We are going to get a deal done in China and the U.S.,” said Luke Hickmore, senior investment manager at Aberdeen Standard Investments. “That, with the stimulus China has put in place, and a slightly calmer tone in the U.K. as well, I think is stoking a market that’s wanted to run hotter than it has done for a while.”

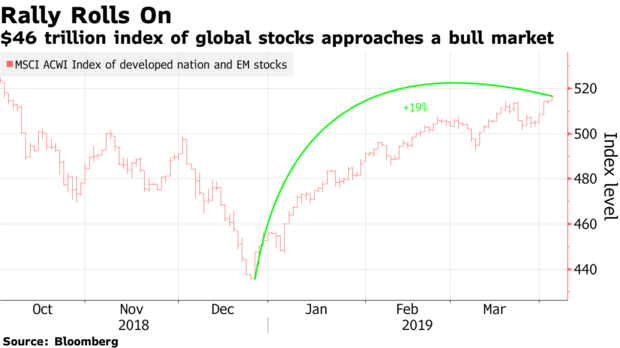

Not only have they moved up, but the MSCI World index is now just shy of a bull market from its December lows.

Generally strong world stocks and hopes of a softer Brexit sparked a sell-off in safe-haven government bonds, pushing yields off recent lows. U.S. 10-year Treasury yields rose almost 4 basis points to 2.52%. Germany’s benchmark 10-year German Bund yield rose back above 0, printing at 0.005%. A week ago it hit a 2-1/2 year low at around minus 0.09 percent on concern about the weak economic growth backdrop.

One fly in the Fed’s “rate hike pause” ointment is that oil prices stood near multi-month highs amid concerns about supply. Brent crude rose to as high as $69.92 per barrel, its highest since November and near the psychologically important level of $70 per barrel. It was last up 0.6 percent at $69.80. U.S. West Texas Intermediate (WTI) crude rose 0.34% to $62.79 per barrel. As Reuters noted, news that the US is considering more sanctions against Iran, the fourth-largest producer of the Organization of the Petroleum Exporting Countries (OPEC), and the halting of production at a crude terminal in Venezuela threatened to squeeze supply and pushed oil prices up on Tuesday.

As oil prices surge, the Fed will be hard pressed to explain why it is ignoring what is arguably the biggest cause of consumer anger aimed at higher prices and instead focusing solely on boosting stock rices.

Elsewhere, as the Brexit chaos continues, UK Tory Lawmaker Letwin said the process of seeking an Article 50 extension will go ahead as planned, adding that we can work with the government now; adds that Labour leader Corbyn is ‘someone we can do business with’ regarding Brexit. If negotiations with Labor collapse, PM May is said to consider asking lawmakers to rank Brexit outcomes. Separately, the EU is preparing to offer PM May a long Brexit extension with strict conditions including taking part in European Parliament elections and a possible “gentleman’s agreement” regarding Britain’s conduct (e.g. potentially abstaining from taking part in important decisions over the EU’s future), according to FT. Finally, French President Macron has led other EU leaders in warning that UK PM May’s apparent move to take no-deal Brexit off the table offers no guarantees UK will not crash out of the EU on April 12th. In any case, this shitshow isn’t ending any time soon, and certainly won’t end by fulfilling the will of the majority as May will do everything in her power to prevent or delay an actual Brexit.

In FX, the dollar was pressured as risk sentiment improved amid fresh hope for progress in U.S.-China trade talks and better-than-expected services PMI data in all four of the euro-area’s largest economies. The euro rose as stops were triggered. Sterling extended its gains after British Prime Minister Theresa May said late on Tuesday she would seek another Brexit delay to agree an EU divorce deal with the opposition Labour Party leader, raising hopes of a “softer” Brexit. The Australian dollar led a risk-on rally, boosted by expectations for a U.S.-China trade deal; New Zealand dollar and Scandinavian currencies followed suit while the allure of traditional havens, such as Treasuries and the yen, faded.

Bitcoin, which inexplicably surged 18.7 percent on Tuesday following a major order by an anonymous buyer, extended its gains by another 1.6 percent to $4,977.48. Spot gold dipped 0.08 percent to trade at $1,291.31 per ounce.

On the macro side, data includes ADP employment change as well as Markit services and composite PMIs.

Market Snapshot

- S&P 500 futures up 0.5% to 2,882.25

- STOXX Europe 600 up 0.7% to 387.70

- MXAP up 0.8% to 162.76

- MXAPJ up 1% to 541.18

- Nikkei up 1% to 21,713.21

- Topix up 0.6% to 1,621.77

- Hang Seng Index up 1.2% to 29,986.39

- Shanghai Composite up 1.2% to 3,216.30

- Sensex up 0.3% to 39,170.16

- Australia S&P/ASX 200 up 0.7% to 6,285.05

- Kospi up 1.2% to 2,203.27

- German 10Y yield rose 4.5 bps to -0.004%

- Euro up 0.3% to $1.1235

- Brent Futures up 0.7% to $69.84/bbl

- Italian 10Y yield rose 1.8 bps to 2.171%

- Spanish 10Y yield rose 1.8 bps to 1.134%

- Brent Futures up 0.7% to $69.84/bbl

- Gold spot down 0.06% to $1,291.66

- U.S. Dollar Index down 0.3% to 97.10

Top Overnight News from Bloomberg

- U.S. and China officials have resolved most of the issues surrounding the deal though they have yet to agree on what happens to existing U.S. duties on Chinese goods and the terms of an enforcement mechanism to ensure China keeps to the trade deal, Financial Times said, citing people briefed on the talks

- China’s Vice Premier Liu He will resume negotiations with his U.S. counterparts in Washington Wednesday as both governments push towards an agreement to end their trade dispute

- A woman carrying two Chinese passports illegally entered President Trump’s Mar-a-Lago resort in Palm Beach, Florida, Saturday and lied to a Secret Service agent, according to court documents filed in West Palm Beach

- Larry Kudlow said the president stands by his choice of Stephen Moore for an open seat on the Fed Board despite recent reports about the possible nominee’s failure to fully pay taxes and alimony

- U.K. Prime Minister Theresa May on Tuesday abandoned her strategy of making Brexit a project of her Conservative Party and Democratic Unionists and asked Jeremy Corbyn, leader of the opposition Labour Party, to rescue her

- Crude advanced to the highest this year after a further reduction in supply from OPEC signaled that global markets are tightening

- Prime Minister Scott Morrison’s government pledged sweeping tax cuts and forecast Australia’s first surplus in more than a decade in a budget aimed at engineering a come-from- behind election victory

- China is drafting rules for overseas investments to be considered part of President Xi Jinping’s Belt and Road Initiative, according to people familiar with the matter, marking the first attempt to better define his signature policy

- Attorney General William Barr hasn’t discussed any part of Mueller’s report with the White House, according to a Justice Department official, but plans to rely instead on his own judgment in deciding whether some details in the report should be withheld under executive privilege

- Cryptocurrency traders may not know what caused the abrupt surge in Bitcoin on Tuesday, but they’re going along for the ride anyway; the virtual currency climbed to a fresh 2019 high on Wednesday, building on a spike yesterday that many market participants struggled to explain

Asian equity markets were mostly higher as trade optimism and Chinese PMI data helped the region shrug-off the indecisive lead from the US, where the global stock rally had stalled amid thin volumes, weak durable goods data and ahead of upcoming risk events. ASX 200 (+0.6%) and Nikkei 225 (+1.0%) were positive with Australia led by miners amid strength in iron ore prices which hit record levels in China and as participants also digested the budget which included an upward revision to the first projected surplus in over a decade and proposed AUD 158bln in tax cuts. Japanese stocks were lifted as risk appetite was stimulated by reports US and China are nearing a final trade agreement with most issues resolved but continue to haggle on enforcement and implementation. Hang Seng (+1.2%) and Shanghai Comp. (+1.2%) also benefitted from the trade hopes and after further encouraging data from China in which Caixin Services PMI topped estimates and printed its highest since January 2018. However, the performance of the mainland was somewhat fatigued after its recent bullish streak and with Bank of Communications underperforming on reports China National Council for Social Security Fund plans to sell 1.49bln of Bocom’s A-shares. Finally, 10yr JGBs were lower as trade hopes ensured a lack of safe-haven demand and with selling exacerbated as prices ran through stops at 153.00. SMBC also suggested the BoJ may reduce its purchases today, although this failed to materialize as the BoJ maintained its Rinban amounts which totalled JPY 1.23tln in 1yr-10yr JGBs and which helped alleviate some of the pressure.

Top Asian News

- RBI Has Scope to Cut India Rate by 50Bps on Thursday: Quantum

- Brookfield Said to Consider $2 Billion China Property Deal

- Trio of Troubles Has Malaysia’s IHH Losing $800 Million in Value

- Pound Volatility Curve Retains Inversion Before May-Corbyn Talks

Major European indices are firmer [Euro Stoxx 50 +0.7%] as the positivity continues from overnight where sentiment was driven by US-China trade optimism and positive Chinese PMI data, although the FTSE 100 (Unch) is the exception to this with the index weighed on by the Brexit-related Sterling strength. Sector wise, material names (sector +1.5%) lead the gains as copper and iron prices are bolstered by the seemingly positive trade news alongside supply-side woes. On the flip side, healthcare names lag (sector -0.8%) with heavyweights Novartis (-1.0%) and Roche (-0.9%) weighed on by Walgreen’s cut in guidance yesterday. Elsewhere, the tech sector (+1.3%) is supported by advances in AMD yesterday (+3% pre-market) alongside Taiwan Semiconductor stating that they expect chip orders to pick up.

Top European News

- Lira Drop Helps Dubai Bank Save $400 Million in Turkey Deal

- Euro Extends Advance on Italy PMI Data, Renewed Trade Optimism

- Euro- Area Services Resilience Softens Manufacturing Blow for Now

- Istanbul Vote Recount Outcome ‘Must Be Accepted by All’: Guven

- Suddenly Inflation Isn’t Turkish Central Bank’s Only Worry

In FX, this week’s risk roller-coaster continues, and the latest turn of the ride has lifted stocks and high beta currencies to the detriment of so-called safe havens, like the Dollar and core bonds. Hence, the Greenback has handed back gains made on Tuesday vs most G10 counterparts and EMs, with the index retreating towards 97.000 again from just over 97.500. The catalysts, another strong Chinese PMI and similar beats across the Eurozone/Europe, bar the UK, reports that the US and China are getting close to a trade agreement and Brexit developments raising prospects of some kind of deal as opposed to no deal.

- AUD/NZD – The Aussie and Kiwi have benefited most from the resurgence in broad risk appetite, with the former also deriving independent impetus from data in the form of retail sales and trade overnight. Aud/Usd has recovered from near 2019 lows to 0.7100+, but may be hampered by more hefty option expiry interest as 1.6 bn runs off between 0.7100-10 at the NY cut. Meanwhile, Nzd/Usd is hovering just below 0.6800 compared to sub-0.6750 at worst as the Aud/Nzd cross holds close to the upper end of a 1.0495-50 range.

- EUR/GBP/CAD/CHF – All firmer vs the Usd following underperformance yesterday, with the single currency boosted by better than expected Eurozone services PMIs across the board and marginally topping Tuesday’s 1.1250 peak, but capped by layered off said to be sitting up to 1.1270. Cable tested the water and resistance into 1.3200 on the back of the aforementioned Brexit manoeuvres aimed at reaching a pact to trigger an extension from April 12 that could lead to a softer withdrawal agreement or terms. However, the Pound was derailed to a degree by a significantly weaker than forecast UK services PMI as the headline recoiled below 50 and IHS predicted this means Q1 GDP stagnation before a downturn in H2. The Loonie continues to recoup losses vs its US peer post-contrasting manufacturing PMIs/ISM on Monday with the aid of firmer crude prices and the overall rebound in risk sentiment to probe over 1.3300, while the Franc is back up around 0.9960 from parity at one stage on Tuesday, but softer vs the Eur within 1.1177-1.1208 trading parameters after more dovish/intervention talk from the SNB.

- SEK/NOK – The Scandi Crowns are still tracking broader swings in risk, along with technical and fundamental impulses, as Eur/Sek and Eur/Nok retreat towards recent lows and chart support levels circa 10.4100 and 9.6000 respectively.

- EM – The Lira remains embroiled in political uncertainty as the main parties wrangle over regional election results against the backdrop of renewed diplomatic angst between Turkey and the US, while latest inflation data has piled more pressure on the Try and CBRT given a firmer than forecast CPI rate. Unsurprisingly, Usd/Try is holding above 5.6100 vs other Usd/regional pairings that are reversing recent rallies, and even the Rand in wake of a weak SA services PMI.

In commodities, prices are on the front foot amidst the overall risk appetite couple with a falling buck. WTI (+0.1%) and Brent (+0.6%) futures have been grinding higher since last night, shrugging off the surprise build in API crude stocks (+3.0mln vs. Exp. -0.4mln) with the former residing just above USD 62.60/bbl having hit resistance at USD 63.00/bbl. The support the oil complex has seen has mostly been due to supply disruptions rather than demand improvement. Traders will be eyeing the DoE release today, although price action may be muted as Iranian and Venezuelan supply woes/ market risk appetite hold onto the spotlight. Elsewhere, metals across the board are benefiting from the easing buck with spot gold (+0.1%) remaining below USD 1300/oz (for now), whilst copper (+1.2%) surges on trade optimism after reports that US and China are inching closer to a deal, with the Chinese trade delegation heading to Washington today for another round of talks. Furthermore, Barclays noted that copper supply-side disruptions have the potential to boost the red metal to USD 7000/tonne. Finally, Dalian iron ore prices were bolstered to record highs, also hit by supply issues, as damage is calculated from the cyclones in Western Australia. Barclays also raised its 2019 iron ore price forecast to USD 75/tonne (Prev. USD 69/tonne).

US Event Calendar

- 7am: MBA Mortgage Applications, prior 8.9%

- 8:15am: ADP Employment Change, est. 175,000, prior 183,000

- 9:45am: Markit US Services PMI, est. 54.8, prior 54.8; Markit US Composite PMI, prior 54.3

- 10am: ISM Non-Manufacturing Index, est. 58, prior 59.7

DB’s Jim Reid concludes the overnight wrap

I visited our new house last night to see how it was progressing with less than three weeks to go of a 9-month renovation project. To say I was blown away was an understatement….. blown away by how much work was needed to be done in 2 and a half weeks! I would say there’s more chance of a Brexit plan being agreed by all parties than it being ready on time but as you’ll see below hopes have been raised on that front last night. Back to the house and the builder told me not to worry and said that it all “usually” comes together at the last minute. Between you and me, the thing I’m most looking forward to is our greatest extravagance. A hot tub? a sauna room? aircon? A wrapping room? No we have none of those… instead the luxury is having designed the kitchen so as to have two dishwashers! Who needs extra cupboard space! Since we’ve had three kids I’ve done more washing up than the rest of my time on this planet. I don’t understand how they can need so many eating and cooking implements and how messy it can get. Life is too short for this so I’m looking forward to opening both doors and shovelling it all in and heading down the golf course instead!

So what will come first, Brexit or me moving in? The chances of the former went up last night as PM May’s press conference after Europe closed was more constructive than expected. Following her marathon cabinet session, May said that she will seek another short Article 50 extension from the EU, will engage with Jeremy Corbyn on an alternative Brexit solution, and will agree to implement whatever solution Parliament passes if these talks break down. This is huge news. She is seemingly now prepared to back down on her prior red lines and also prepared to let Parliament decide on the outcome if she and Mr Corbyn can’t. Recall that the customs union option came within 3 votes of passage on Monday. If parliament could muster the votes to pass that plan or an even softer outcome, PM May has now, for the first time, implied that she would negotiate that with the EU without calling for elections. The removal of that risk and that of hopes of a compromise supported the pound as it rallied +0.88% off its intraday lows after her words. In theory this is very positive news for the pound assuming the Conservative government survives the shrapnel from the internal party in-fighting that this will bring.

In total, the main risks now hinge on the reaction from Labour, the ERG within her own party, from May’s coalition partners the DUP, and from the EU. On the first, opposition leader Corbyn said that he is “very happy” to meet with May, so that’s a positive start. On the ERG, there have been a number of negative comments from members of the group but the worst is probably to come. In a statement, the DUP criticised May’s “lamentable handling” of the negotiations, but said that they will continue to “judge all Brexit outcomes against our clear unionist principles”. That at least leaves open the possibility that the DUP would accept a solution that avoids a border between Northern Ireland and the rest of the UK. Finally, the EU may be unwilling to grant another extension without forcing the UK to participate in EU elections, though we may learn more when Juncker speaks to the European Parliament later today. Donald Tusk seemed to be encouraging patience from his own side.

Prior to last night we learned that there would be no indicative votes today and instead we’re supposed to see MPs debate the new Cooper/Letwin bill, which is designed to prevent a no-deal Brexit next week. We will see if that still occurs given the latest developments. We have until next Wednesday before the emergency EU summit.

Over in markets, it hasn’t quite been so one way in the last 24 hours as it was on Monday with a bit of a lull in newsflow to blame although the Asia session has seen new news. In addition, today’s global non-manufacturing PMIs, tomorrow’s ECB minutes and Friday’s payrolls will also provide us with fresh impetus. We’d expect trade headlines to pick up as China Vice Premier Liu He is scheduled to travel to Washington today to lead a delegation of trade negotiators.

Indeed overnight, the FT has reported that the US and Chinese officials have resolved most of the issues surrounding the deal. The only issues which are yet to be agreed on are what happens to the existing US duties on Chinese goods and the terms of an enforcement mechanism to ensure China keeps to the trade deal. This news, along with better than expected Chinese March Caixin services (at 54.4 vs. 52.3 expected – the highest since January 2018) and composite (52.9 vs. 50.7 last month, highest since June 2018) PMIs, sent Asian markets higher. The Nikkei (+0.83%), Hang Seng (+0.86%), Shanghai Comp (+0.23%) and Kospi (+0.52%) are all up. China’s onshore yuan is up +0.17% to 6.7119. Elsewhere, futures on the S&P 500 are up +0.42%. We also saw Japan’s March services and composite PMIs overnight at 52.0 (vs. 52.3 last month) and 50.4 (vs. 50.7 last month), respectively.

Back to yesterday and after European equity markets marched higher, with the STOXX 600 (+0.35%) closing at its highest level since late September, US equities traded in a bit more of a holding pattern yesterday following the decent three-day run prior to this. The S&P 500 was flat and the DOW -0.30% – the latter hurt by a profit warning from Walgreens Boots, which saw shares fall -12.81%. The NASDAQ (+0.25%) outperformed a bit, mostly thanks to a strong session by Facebook (+3.26%). DB’s Lloyd Walmsley published a bullish report on the stock early yesterday morning (link here ).

Over in rates, Treasuries partially retraced Monday’s steep rise, with 10y yields back down -3.2bps to 2.469% after Monday’s +9.6bps rise. The 2s10s curve steepened slightly to 17bps as two-year yields slid -3.4bps. That came despite a +3.2bps rise in 2y inflation breakevens, partially driven by the oil rally (more below), as the move was driven solely by declining real yields. This morning, yields on 2-year and 10-year treasuries are up 2.1bps and 2.7bps, respectively, thereby further steepening the 2s10s curve to 17.8bps. EM currencies retraced a bit of Monday’s rally as well, with an EM FX index down -0.10%. The Turkish lira remains the most volatile currency in EM space, weakening -1.93% yesterday to within 3% of its 6-month lows.

Bunds also fell -2.2bps and are back down to -0.052% again while Gilts fell -4.3bps in tandem with the Sterling move. BTPs (+2bps) underperformed after Juncker warned that the Italian economy “hasn’t stopped regressing”. In credit, HY spreads were -9bps tighter in Europe but +3bps wider in the US, while WTI oil rose +1.64% following the latest OPEC estimates, which suggested production was down in March. Plus, a regulatory filing by Saudi Aramco showed that the Ghawar oil field – the world’s largest – can pump an estimated 3.8mn barrels per day, notably less than prior estimates of almost 6mn. Oil prices are now up to their highest levels in 5 months, with WTI at $62.60 per barrel and Brent at $69.43.

Moving on. Yesterday’s data in the US proved to be mostly a non-event. Headline durable goods orders in February declined less than expected (-1.6% mom vs. -1.8% expected), however, these were offset by a downward revision to January. The opposite was true for core capex orders, which were down -0.1% mom (vs. +0.1% expected) but offset by an upward revision to January. So net-net a bit of a wash. Last night we also got the March vehicle sales data from several major carmakers. For Fiat Chrysler, Toyota, Honda, and Nissan in aggregate, sales fell -5.5% yoy, modestly better than the -6.2% yoy expected, but still consistent with a slight deceleration in economic activity this year compared to last year. GM reported its Q1 aggregate figures and also showed a drop yoy, while Ford will report tomorrow.

Finally to the day ahead where the data highlight is likely to be the remaining services and composite PMI revisions for March in Europe this morning. We’ll also get February retail sales data for the Euro Area while in the US this afternoon we kick off with the March ADP employment change print (175k expected), followed then by the PMIs and March ISM non-manufacturing (58.0 expected). We’ve also got Fed speakers scheduled with Bostic, George and Barkin speaking in the afternoon at an ABA event (I wanted to put an extra “B” in) while Kashkari then speaks this evening. China Vice Premier Liu He is also scheduled to travel to Washington to lead a delegation of trade negotiators while NATO foreign ministers are due to gather in Washington.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 39.47 POINTS OR 1.24% //Hang Sang CLOSED UP 361.72 POINTS OR 1.22% /The Nikkei closed UP 207.90 POINTS OR 0.97%/ Australia’s all ordinaires CLOSED UP 0.65%

/Chinese yuan (ONSHORE) closed UP at 6.7083 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 62.67 dollars per barrel for WTI and 69.65 for Brent. Stocks in Europe OPENED GREEN

ONSHORE YUAN CLOSED UP // LAST AT 6.7083 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7133 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/

3 b JAPAN AFFAIRS

3 C CHINA

Algos misread the USA/China headlines that they have resolved most of the trade deal issues. No they have not…

it does not matter… global stocks surge!

(courtesy zerohedge)

Stocks & Bond Yields Jump As Algos Misread US-China Trade Headlines

US equity futures are up along with bond yields as the dollar fades (and yuan gains) following misleading headlines from The FT reporting US and China officials have “resolved most of trade deal issues.”

“We’re getting into the end-game stage,” said Myron Brilliant, executive vice-president for international affairs at the US Chamber of Commerce.

All sounds awesome right? Bond prices are down (yields up) …

And stocks are surging…

There’s just one big thing wrong: Both countries have yet to agree on what happens to existing U.S. duties on Chinese goods and the terms of an enforcement mechanism to ensure China keeps to the trade deal, Financial Times reports, citing people briefed on the talks.

“Ninety per cent of the deal is done, but the last 10 per cent is the hardest part, it’s the trickiest part and it will require trade-offs on both sides,” he told reporters on Tuesday.

So, in other words – no progress whatsoever as enforcement is all that matters and Trump’s threats of maintaining the tariffs as a mechanism of enforcement is certainly something the Chinese – whose economy is awesome again, remember – will not stand for.

Nasdaq futs just took out the highs of the year…

We suspect once the humans read The FT article, things might fade.

As we note AUD already is – a currency that should be jubilant on this…

So finally – summarizing The FT article – besides the sticking points that US and China have been unable to resolve for the past 4 months, everything else is resolved.

Trade Accordingly.

end

Not a good harbinger of things to come; Apple slides as Chinese iphone prices are clahsed

(courtesy zerohedge)

4.EUROPEAN AFFAIRS

BREXIT/EU/

It is the uncertainty that it killing Britain. Our bet is that Britain escapes the clutches of the EU and will be better off but will suffer a bit in the short term

(courtesy zerohedge)

German Institute Cuts GDP Growth Forecast In Half To 0.8%

With European stocks surging to levels not seen since last August, the European economy continues to slump ever closer to recession.

One month after Germany avoided a technical recession by the skin of its teeth, when it just barely avoided posting two consecutive quarter of negative GDP growth…

… on Wednesday Germany’s leading economic institutes slashed their growth forecast for Europe’s biggest economy by 60%, to 0.8% from a previous estimate of 1.9% a source told Reuters.

The sharp revision reflects the scale of the slowdown in Germany, whose economy continues to tread recessionary waters and is facing headwinds from a slowing world economy, international trade disputes and the threat of Brexit.

Most of all, Germany is facing continued pain from the ongoing trade deterioration with its most important trading partner, China:

As Reuters adds, the institutes’ estimates feed into the government’s own growth projections which will be updated later this month. The government said in January it forecast growth of 1.0 percent this year.

To be sure, whereas German economic as recently as February was nothing short of abysmal…

… yet wonders if this latest outlook cut may be coming too late – according to the Citi Eurozone econ surprise index, while it remains deep in negative territory, the index had posted steady improvement for the past three months, which however hit a brick wall at the end of March.

Ultimately, Germany’s fate will depend entirely on whether China’s economy has indeed troughed or if the recent PMI rebound ends up being a transitory spike, one which will be promptly squashed by the economy’s downward momentum.

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

6.GLOBAL ISSUES

My favourite Bellwether stock indicating global growth is Caterpillar. Today Deutsche Bank downgraded this company slashing its price target from $152 down to $128.

(courtesy zerohedge)

7 OIL ISSUES

8. EMERGING MARKETS

VENEZUELA

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:00 AM….

Euro/USA 1.1246 UP .0043 REACTING TO MERKEL’S FAILED COALITION/ REACTING TO +GERMAN ELECTION WHERE ALT RIGHT PARTY ENTERS THE BUNDESTAG/ huge Deutsche bank problems + USA election:///ITALIAN CHAOS /AND NOW ECB TAPERING BOND PURCHASES/JAPAN TAPERING BOND PURCHASES /USA RISING INTEREST RATES /FLOODING/EUROPE BOURSES GREEN

USA/JAPAN YEN 111.52 UP .211 (Abe’s new negative interest rate (NIRP), a total DISASTER/NOW TARGETS INTEREST RATE AT .11% AS IT WILL BUY UNLIMITED BONDS TO GETS TO THAT LEVEL…

GBP/USA 1.3163 UP 0.0037 (Brexit March 29/ 2019/ARTICLE 50 SIGNED/BREXIT FEES WILL BE CAPPED

USA/CAN 1.3306 DOWN .0037 CANADA WORRIED ABOUT TRADE WITH THE USA WITH TRUMP ELECTION/ITALIAN EXIT AND GREXIT FROM EU/(TRUMP INITIATES LUMBER TARIFFS ON CANADA/CANADA HAS A HUGE HOUSEHOLD DEBT/GDP PROBLEM)

Early THIS WEDNESDAY morning in Europe, the Euro ROSE by 14 basis points, trading now ABOVE the important 1.08 level RISING to 1.1231 Last night Shanghai composite closed UP 39.47 POINTS OR 1.24%/

//Hang Sang CLOSED UP 361.72 POINTS OR 1.22%

/AUSTRALIA CLOSED UP 0.65%// EUROPEAN BOURSES GREEN/

The NIKKEI: this WEDNESDAY morning CLOSED UP 207.90 POINTS OR 0.97%

Trading from Europe and Asia

1/EUROPE OPENED GREEN

2/ CHINESE BOURSES / :Hang Sang CLOSED UP 361.72 POINTS OR 1.22%

/SHANGHAI CLOSED UP 39.47 POINTS OR 1.24%

Australia BOURSE CLOSED UP 0.65%

Nikkei (Japan) CLOSED UP 207.90POINTS OR 0.97%

INDIA’S SENSEX IN THE GREEN

Gold very early morning trading: 1294.00

silver:$15.17

Early WEDNESDAY morning USA 10 year bond yield: 2.52% !!! UP 2 IN POINTS from TUESDAY’S night in basis points and it is trading WELL ABOVE resistance at 2.27-2.32%.

The 30 yr bond yield 2.92 UP 3 IN BASIS POINTS from TUESDAY night.

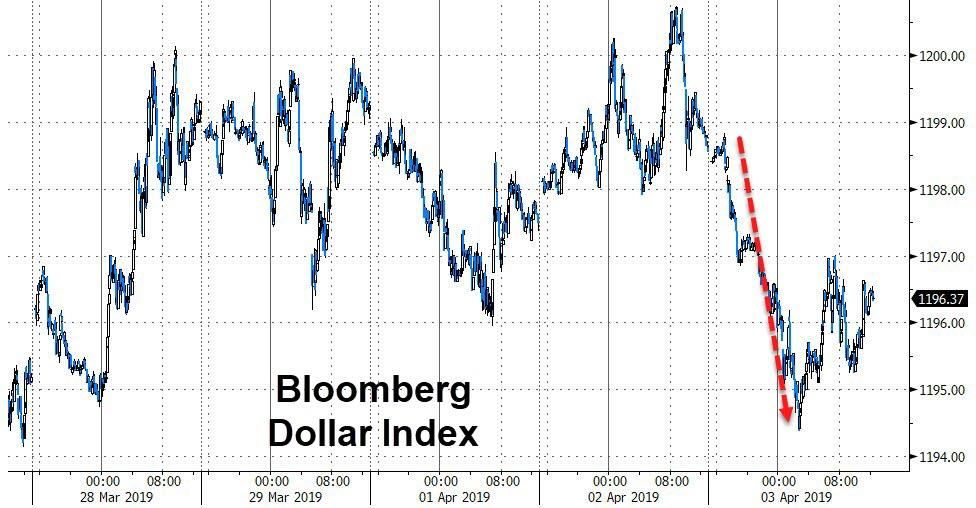

USA dollar index early WEDNESDAY morning: 97.03 DOWN 33 CENT(S) from TUESDAY’s close.

This ends early morning numbers WEDNESDAY MORNING

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now your closing WEDNESDAY NUMBERS \12: 00 PM

Portuguese 10 year bond yield: 1.27% DOWN 1 in basis point(s) yield from WEDNESDAY/

JAPANESE BOND YIELD: -.05% UP 2 BASIS POINTS from TUESDAY/JAPAN losing control of its yield curve/

SPANISH 10 YR BOND YIELD: 1.14% UP 0 IN basis point yield from TUESDAY

ITALIAN 10 YR BOND YIELD: 2.54 UP 3 POINTS in basis point yield from TUESDAY/

the Italian 10 yr bond yield is trading 142 points HIGHER than Spain.

GERMAN 10 YR BOND YIELD: RISES TO –.00% IN BASIS POINTS ON THE DAY//

THE IMPORTANT SPREAD BETWEEN ITALIAN 10 YR BOND AND GERMAN 10 YEAR BOND IS 2.53% AND NOW ABOVE THE THE 3.00% LEVEL WHICH WILL IMPLODE THE ENTIRE ITALIAN BANKING SYSTEM. AT 4% SPREAD THERE WILL BE A MASSIVE BANK RUN…

END

IMPORTANT C44RENCY CLOSES FOR WEDNESDAY

Closing currency crosses for WEDNESDAY night/USA DOLLAR INDEX/USA 10 YR BOND YIELD/1:00 PM

Euro/USA 1.1256 UP .0037 or 37 basis points

USA/Japan: 111.48 UP 0.172 OR YEN DOWN 17 basis points/

Great Britain/USA 1.3183 UP .0057 POUND UP 57 BASIS POINTS)

Canadian dollar UP 27 basis points to 1.3163

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The USA/Yuan,CNY closed AT 6.7114 0N SHORE (UP)

THE USA/YUAN OFFSHORE: 6.7137 YUAN UP)

TURKISH LIRA: 5.6046

the 10 yr Japanese bond yield closed at -.05%

Your closing 10 yr USA bond yield UP 4 IN basis points from TUESDAY at 2.52 % //trading well ABOVE the resistance level of 2.27-2.32%) very problematic USA 30 yr bond yield: 2,93 UP 5 in basis points on the day /

THE RISE IN BOTH THE 10 YR AND THE 30 YR ARE VERY PROBLEMATIC FOR VALUATIONS

Your closing USA dollar index, 97.09 DOWN 27 CENT(S) ON THE DAY/1.00 PM/

Your closing bourses for Europe and the Dow along with the USA dollar index closing and interest rates for WEDNESDAY: 12:00 PM

London: CLOSED UP 27.16 0.37%

German Dax : UP 199,61 POINTS OR 1.70%

Paris Cac CLOSED UP 45.44 POINTS OR 0.84%

Spain IBEX CLOSED UP 124.30 POINTS OR 1.33%

Italian MIB: CLOSED UP 232.96 POINTS OR 1.08%

WTI Oil price; 62.28 1:00 pm;

Brent Oil: 69.11 12:00 EST

USA /RUSSIAN / ROUBLE CROSS: 65.13 THE CROSS LOWER BY 0.19 ROUBLES/DOLLAR (ROUBLE HIGHER BY 19 BASIS PTS)

TODAY THE GERMAN YIELD RISES TO –.00 FOR THE 10 YR BOND 1.00 PM EST EST

END

This ends the stock indices, oil price, currency crosses and interest rate closes for today 4:30 PM

Closing Price for Oil, 4:00 pm/and 10 year USA interest rate:

WTI CRUDE OIL PRICE 4:30 PM : 62.49

BRENT : 69.44

USA 10 YR BOND YIELD: … 2.52… STILL DEADLY//

USA 30 YR BOND YIELD: 2.93..STILL DEADLY

EURO/USA DOLLAR CROSS: 1.1236 ( UP 33 BASIS POINTS)

USA/JAPANESE YEN:111.48 UP .168 (YEN DOWN 17 BASIS POINTS/..

USA DOLLAR INDEX: 97.10 DOWN 26 cent(s)/

The British pound at 4 pm: Great Britain Pound/USA:1.3150 UP 27POINTS

the Turkish lira close: 5.6251

the Russian rouble 65.24 UP .01 Roubles against the uSA dollar.( UP 1 BASIS POINTS)

Canadian dollar: 1.3340 UP 3 BASIS pts

USA/CHINESE YUAN (CNY) : 6.7114 (ONSHORE)/

USA/CHINESE YUAN(CNH): 6.7136 (OFFSHORE)

German 10 yr bond yield at 5 pm: ,-0.00%

The Dow closed UP 39.00 POINTS OR 0.15%

NASDAQ closed UP 46.67 POINTS OR 0.60%

VOLATILITY INDEX: 13.74 CLOSED UP .38

LIBOR 3 MONTH DURATION: 2.602%//

FROM 2.599

And now your more important USA stories which will influence the price of gold/silver

TRADING IN GRAPH FORM FOR THE DAY/WEEKLY SUMMARY/FOLLOWED BY TODAY

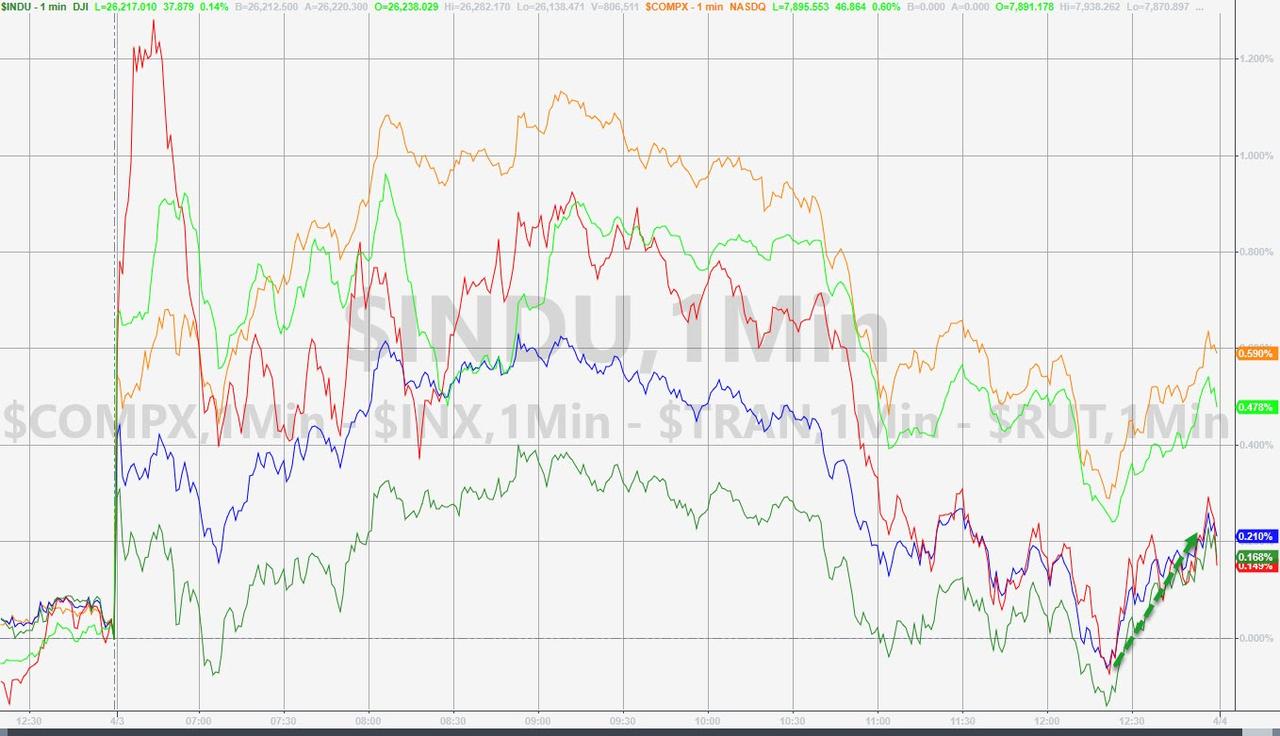

Credit, Curves & Crypto Jump As Stocks Shrug Off Dismal Data Dump

Stocks, bitcoin, and bond yields were up on the day despite US macro data crashing to its weakest since April 2017…

Time flies when you’re having fun ignoring reality…

Catastrophic failure@SafetyFlrstClock falls during replacement

After a quiet Tuesday, Chinese stock investors reawakened their bullish enthusiasms…

European markets refused to stop surging led by the DAX on trade hope…

Nasdaq and Small Caps outperformed as S&P, Dow, and Trannies all bounced off ‘unch’ late on… US-China trade headlines 3 minutes before the close confused algos as it was clear the deal was not done…

Nas daq triggered a ‘golden cross’ today…

daq triggered a ‘golden cross’ today…

After S&P triggered on Monday

Facebook floundered…

Notably, Credit and equity protection costs rose considerably from their opening highs…