GOLD: $1290.15 DOWN $0.90 (COMEX TO COMEX CLOSING)

Silver: $15.13 DOWN 0 (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1292.30

silver: $15.13

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today: 132/881 STOPPED/869 ISSUANCE

EXCHANGE: COMEX

CONTRACT: APRIL 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,289.900000000 USD

INTENT DATE: 04/03/2019 DELIVERY DATE: 04/05/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

132 C SG AMERICAS 1

323 H HSBC 167

657 H MORGAN STANLEY 58

661 C JP MORGAN 869 132

686 C INTL FCSTONE 5

730 C PTG DIVISION SG 2

737 C ADVANTAGE 8 61

800 C MAREX SPEC 1 16

880 H CITIGROUP 441

905 C ADM 1

____________________________________________________________________________________________

TOTAL: 881 881

MONTH TO DATE: 3,923

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 881 NOTICE(S) FOR 88,100 OZ (2.74 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 3923 NOTICES FOR 392,300 OZ (12.202 TONNES)

SILVER

FOR APRIL

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

2 NOTICE(S) FILED TODAY FOR 10,000 OZ/

total number of notices filed so far this month: 697 for 3,485,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE :$5006 UP $1

Bitcoin: FINAL EVENING TRADE: $4910 DOWN 130

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A STRONG SIZED 1637 CONTRACTS FROM 199,592 UP TO 201,229 DESPITE YESTERDAY’S TINY 2 CENT RISE IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE MUST HAVE HAD CONSIDERABLE SHORT COVERING AGAIN TODAY.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR MAY, 349 FOR MARCH 2020 0 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 349 CONTRACTS. WITH THE TRANSFER OF 349 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 349 EFP CONTRACTS TRANSLATES INTO 1.745 MILLION OZ ACCOMPANYING:

1.THE 2 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

AND NOW 3.860 MILLION OZ STANDING FOR SILVER IN APRIL.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

4891 CONTRACTS (FOR 4 TRADING DAYS TOTAL 4891 CONTRACTS) OR 24.46 MILLION OZ: (AVERAGE PER DAY: 1222 CONTRACTS OR 6.114 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 24.46 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 3.49% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 597,15 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1637 DESPITE THE TINY 2 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 349 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A CONSIDERABLE SIZED: 1986 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 349 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1637 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 2 CENT GAIN IN PRICE OF SILVER ???? AND A CLOSING PRICE OF $15.13 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.997 BILLION OZ TO BE EXACT or 143% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 2 NOTICE(S) FOR 10,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ AND NOW APRIL AT 3.860 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FINALLY ROSE AND THIS TIME BY A TINY SIZED 90 CONTRACTS, TO 440,260 DESPITE THE LOSS IN THE COMEX GOLD PRICE/(A FALL IN PRICE OF $0.20//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 2398 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 2398 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020l 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 440,260. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A NET GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2488 CONTRACTS: 90 OI CONTRACTS INCREASED AT THE COMEX AND 2398 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 2488 CONTRACTS OR 248,800 OZ OR 7.738 TONNES. YESTERDAY WE HAD A FALL IN THE PRICE OF GOLD TO THE TUNE OF $0.20….AND YET WITH THAT, WE HAD A STRONG GAIN IN TONNAGE OF 7.738 TONNES!!!!!!.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 19071 CONTRACTS OR 1,907,100 OR 59.91 TONNES (4 TRADING DAYS AND THUS AVERAGING: 4767 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAYS IN TONNES: 59.91 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 58.81/3550 x 100% TONNES = 1.65% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1436.37 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIR SIZED INCREASE IN OI AT THE COMEX OF 90 DESPITE THE LOSS IN PRICING ($0.20) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A VERY SMALL SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 2398 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 2398 EFP CONTRACTS ISSUED, WE HAD A GOOD GAIN OF 2488 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

2488 CONTRACTS MOVE TO LONDON AND 90 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 7.738 TONNES). ..AND ALL OF THIS STRONG DEMAND OCCURRED WITH A FALL IN PRICE OF $0.20 IN YESTERDAY’S TRADING AT THE COMEX???

we had: 881 notice(s) filed upon for 88,100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $0.90 TODAY

NO CHANGE IN GOLD INVENTORY AT THE GLD

INVENTORY RESTS AT 764.29 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER FLAT IN PRICE TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 309.167 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A STRONG SIZED 1637 CONTRACTS from 199.592 UP TO 201,229 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF APRIL BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 349 FOR MAY AND MARCH 2020: 0 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 349 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1637 CONTRACTS TO THE 349 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A CONSIDERABLE GAIN OF 1986 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 9.93 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH. AND NOW 3.860 MILLION OZ FOR APRIL.

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE TINY 2 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 349 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 30.28 POINTS OR 0.94% //Hang Sang CLOSED DOWN 50.07 POINTS OR 0.17% /The Nikkei closed UP 11.14 POINTS OR 0.05%/ Australia’s all ordinaires CLOSED DOWN .76%

/Chinese yuan (ONSHORE) closed DOWN at 6.7154 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 62.69 dollars per barrel for WTI and 69.52 for Brent. Stocks in Europe OPENED GREEN

ONSHORE YUAN CLOSED UP // LAST AT 6.7154 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7171 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

4/EUROPEAN AFFAIRS

i)BREXIT/EU/

The pound rallies as the commons passes a bill requiring Theresa May to request another Brexit delay. The farce over there continues

( zerohedge)

iii)Europe/5G

iv)Italy

(courtesy zerohedge)

v)Germany

vi)Germany/Deutsche bank

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)TURKEY

Turkey issues a counter ultimatum to Pence: Either you stand with us fighting the terrorists or you are with the terrorists. Pence will not fall for it. The key problem here is the fact that the S400 is a far superior defense system that what the uSA has but the 5 35 is a far superior fighting jet. The West is afraid that Turkey if they receive the F 35 can copy the designs and forward them onto Russia. If Russia turns towards Russia then the west will bankrupt Turkey in dollars..so Turkey must get funding through China/Russia./

(courtesy zerohedge)

6. GLOBAL ISSUES

The World Trade Organization came out again today and slashed growth highlighting trade tensions

(courtesy zerohedge)/WTO)

7. OIL ISSUES

the real truth behind the true reserves of Ghawar

(courtesy checkpointasia)

8 EMERGING MARKET ISSUES

VENEZUELA

9. PHYSICAL MARKETS

(Wall Street Journal)

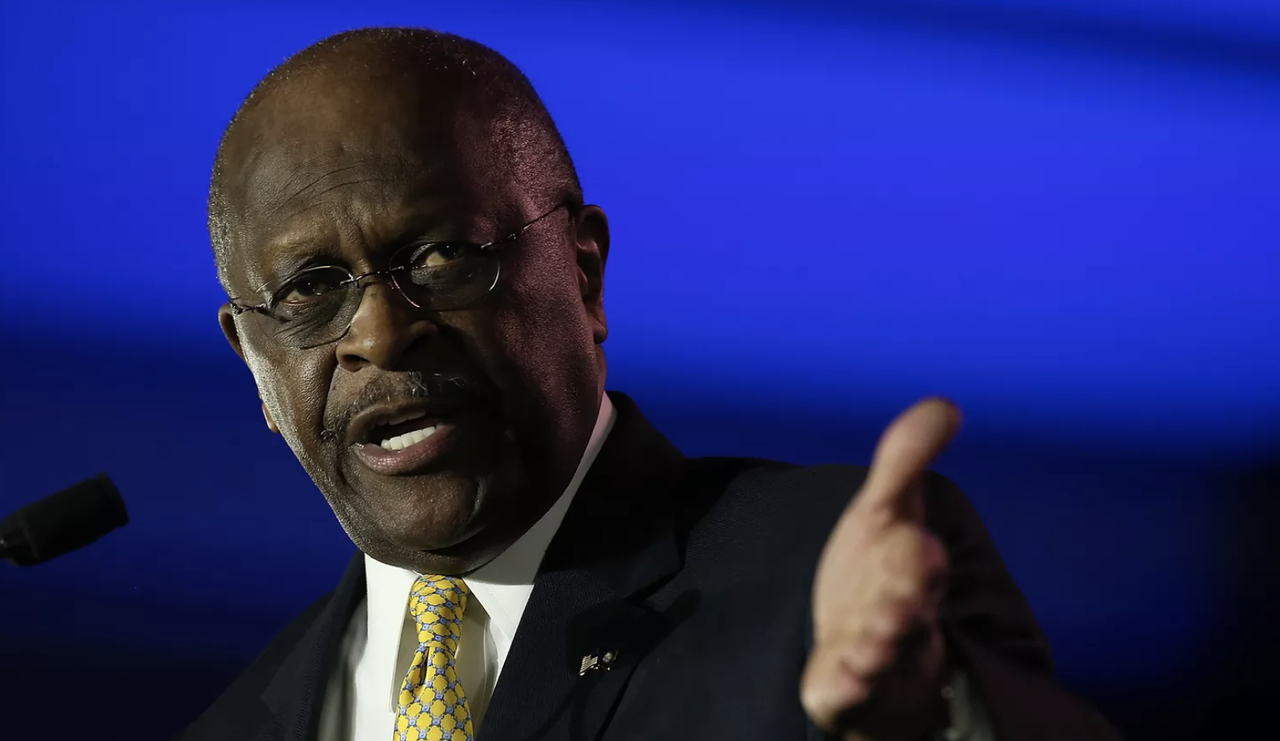

ii)This ought to be interesting: Trump, who discovered he cannot fire Powell, is probably making sure that all of the other

Fed governors walk_–he is nominating Herman Cain to the last Fed seat. Herman Cain was Fed Chairman, of the Kansas City Fed and that allows him to be nominated.

I can assure you that all of the other board members are thrilled.

( zerohedge)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning

A joke: stocks up and rumours denied

( zerohedge)

ii)Market data

ii)USA ECONOMIC/GENERAL STORIES

a)the true state of affairs of our average American: he need to borrow dollars to cover their medical bills

( Michael Snyder)

b)The devastation caused by the storms which inflicted huge damage to our farmers in the Mid west.The farmers are now in dire straits

c)Manhattan housing continues to falter and it is the worst ever seen in 30 years

( zerohedge)

iv)SWAMP STORIES

a)It looks to be over for Biden’s attempt at becoming President

(courtesy zerohedge)

b)The Wall Street Journal are now reporting that the Democrats are now inventing something entirely new: a coverup on the Mueller report

end

Let us head over to the comex:

AFTER APRIL, WE HAVE THE ACTIVE DELIVERY MONTH OF MAY AND HERE THE OI FELL BY 216 CONTRACTS DOWN TO 128,867. CONTRACTS.. THE NEXT MONTH OF JUNE ADDED 3 CONTRACTS TO TOTAL 28. AFTER JUNE, THE VERY BIG DELIVERY MONTH OF JULY HAD A GAIN OF 1037 CONTRACTS UP TO 43,176 CONTRACTS.

Perth Mint’s Gold Bullion Sales Surge 68% In March

Perth Mint’s Gold Bullion Sales Surge 68% In March

(Reuters) – The Perth Mint said on Monday its gold products sales in March surged about 68 percent from the previous month, touching the highest level since November last year.

Sales of gold coins and minted bars in March rose to 32,757 ounces from 19,524 ounces in February, the mint said in a blog post.

Silver sales last month jumped 60.2 percent from the previous month and touched their highest since October last year at 935,819 ounces.

In March, benchmark spot gold prices posted their second straight monthly decline, falling about 1.6 percent, hurt by a strong dollar.

The Perth Mint refines more than 90 percent of newly mined gold in Australia, the world’s second-largest gold producer behind China.

Until April 18, when you purchase the minimum amount of 10,000 ($€£) in physical gold and or silver, you receive complimentary Storage In Zurich For 6 Months

News and Commentary

Gold edges higher as dollar eases, equities rally pauses (Reuters.com)

Gold little changed with risk concerns on U.S.-China trade talk (MarketWatch.com)

Escalating U.S.-China trade war would hit manufacturing, agricultural jobs: IMF (Reuters.com)

U.S. services, private payrolls data highlight slowing economy (Reuters.com)

NATO chief warns of Russia threat, urges unity in U.S. address (Reuters.com)

Source: MoneyWeek

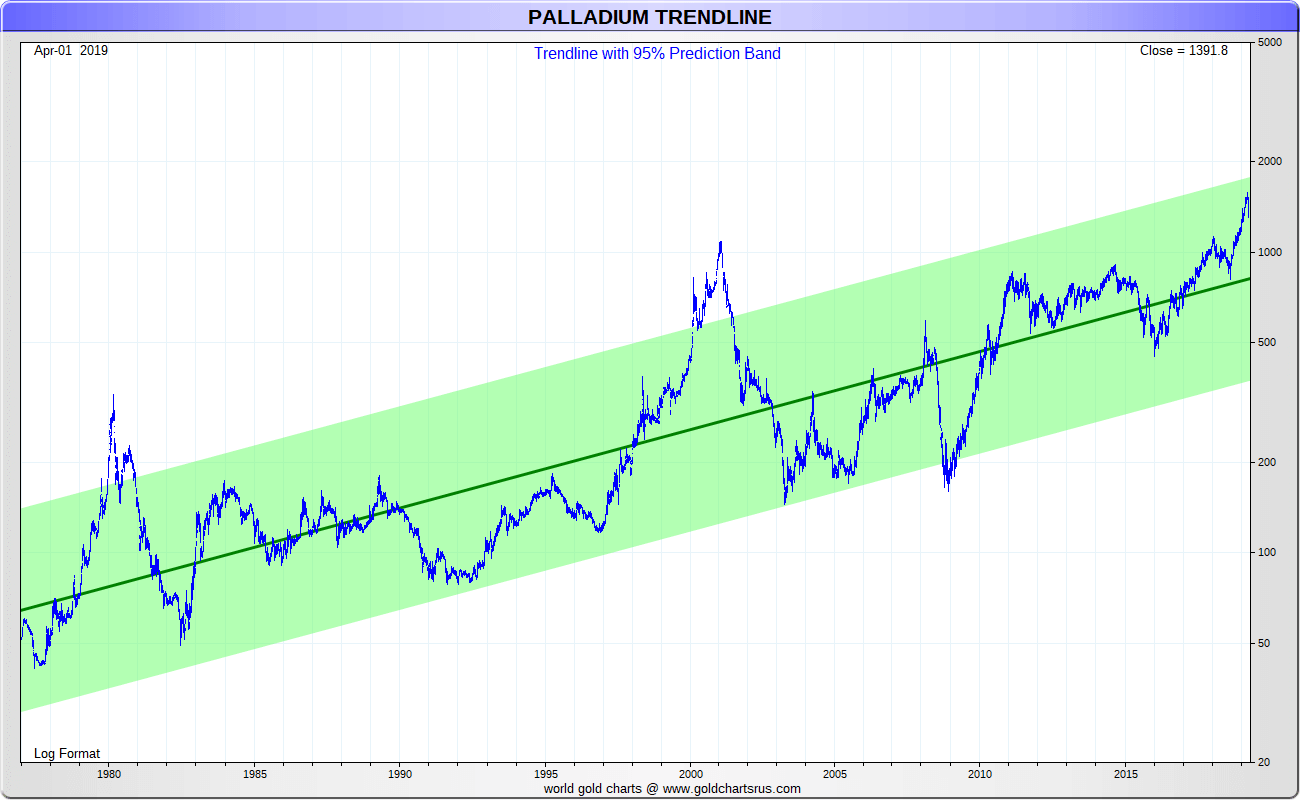

Palladium’s rise has been epic – will platinum ever catch up? (MoneyWeek.com)

Italy’s populists covet central bank and its gold (WSJ.com)

Precious metal prices rigged down for first-quarter valuation purposes (KingWorldNews.com)

US government’s net worth is now NEGATIVE $75 TRILLION (SovereignMan.com)

Gold Prices (LBMA PM)

03 Apr: USD 1,291.85, GBP 980.38 & EUR 1,148.84 per ounce

02 Apr: USD 1,287.20, GBP 984.97 & EUR 1,148.95 per ounce

01 Apr: USD 1,291.90, GBP 987.27 & EUR 1,149.15 per ounce

29 Mar: USD 1,291.15, GBP 991.09 & EUR 1,151.19 per ounce

28 Mar: USD 1,306.90, GBP 995.20 & EUR 1,161.18 per ounce

27 Mar: USD 1,318.25, GBP 997.78 & EUR 1,168.23 per ounce

Silver Prices (LBMA)

03 Apr: USD 15.16, GBP 11.51 & EUR 13.49 per ounce

02 Apr: USD 15.02, GBP 11.51 & EUR 13.42 per ounce

01 Apr: USD 15.07, GBP 11.50 & EUR 13.42 per ounce

29 Mar: USD 15.10, GBP 11.52 & EUR 13.45 per ounce

28 Mar: USD 15.19, GBP 11.58 & EUR 13.53 per ounce

27 Mar: USD 15.40, GBP 11.65 & EUR 13.65 per ounce

Recent Market Updates

– Perth Mint’s Gold Bullion Sales Surge 68% In March

– Central Banks Continue to Buy Gold at a Record Clip

– ItalExit and Cyber Risks in a Cashless World May Be Bigger Risks Than Brexit : Interview with GoldCore CEO

– Ireland and EU Countries Must Seek ECB Approval to Manage Gold Reserves – Draghi

– Global Risks Increasing – Underlining The Case For Gold in 2019 (GoldCore Video Presentation)

– Brexit and Learning To “Live With Boom and Bust Economic Cycles”

– ‘No Deal’ Brexit Risk Impacting UK and Irish Economies – Gold Gains On Recession Concerns

– America’s “Debt Crisis Is Coming Soon”

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

The Italian Government covets the central bank gold held outside of Italy. However it also wants the gold to be placed under their jurisdiction and not the “peoples” gold

Wall Street Journal

Italy’s populists covet central bank and its gold

Submitted by cpowell on Thu, 2019-04-04 06:38. Section: Daily Dispatches

By Giovanni Legorano

The Wall Street Journal

Wednesday, April 3, 2019

https://www.wsj.com/articles/italys-populists-covet-central-bank-and-its…

ROME — Italy’s ruling populists pushed ahead this week with efforts to seize control of the central bank and its gold reserves, stepping up their confrontation with a symbol of the country’s establishment.

With two laws targeting the Bank of Italy under debate in parliament, the campaign is the latest attack on Italy’s independent institutions by leaders of the governing coalition, which is led by the antiestablishment 5 Star Movement and the nativist League.

…

The parties depict the central bank as a symbol of a technocratic elite aloof from the needs of ordinary Italians. Hundreds of thousands of small individual investors lost billions of dollars after several Italian banks failed in recent years, causing widespread anger against the Bank of Italy and previous governments.”We need a change of course at the Bank of Italy if we think about what happened in the last years,” Deputy Prime Minister Luigi Di Maio, leader of the 5 Star Movement, said in February.

Lawmakers from 5 Star are asking Parliament to pass two draft laws that have ignited a national controversy over the independence of the Bank of Italy. While the fate of the bills is uncertain, the prolonged scrutiny is testing an institution whose credibility is crucial for the stability of the Italian economy.

One law would instruct the central bank’s owners, most of them private banks, to sell their shares to the Italian Treasury at prices from the 1930s.

The other law would declare the Italian people to be the owners of the Bank of Italy’s reserve of 2451.8 metric tons of gold, worth around $102 billion at current prices. Such a move could in theory widen the scope for selling the gold and reduce the bank’s reserves, which help underpin the financial system.

“The gold belongs to the Italians, not to the bankers,” said Giorgia Meloni, leader of the Brothers of Italy, a far-right opposition party that supports both bills. “We are ready to battle everywhere in Italy and to bring Italians to the streets if necessary.”

The 5 Star Movement and the League support public ownership of the gold reserves, and with backing from parties comprising 60% of lawmakers, the draft law has enough support to pass. Lawmakers from 5 Star also support nationalizing the central bank, while the League hasn’t decided yet, leaving the bill short of a majority with around 40% support.

Central banks, such as the U.S. Federal Reserve, the Bank of England and Bank of Japan , have become independent branches of governments in most advanced economies in recent decades, regardless of whether their formal ownership is in the public or private sector.

The Bank of Italy is a member of the European Central Bank, which sets monetary policy for the 19-country euro currency zone and supervises its banking sector. If the Italian government were to become the owner of the Bank of Italy, its independence would still be granted by Italian and European laws.

Independent institutions, however, are a bugbear of populist politicians who say that all government should be a direct expression of the popular will, which they claim they themselves represent. Italy’s leaders have consistently accused independent institutions, from the civil service and the media to supervisory authorities such as the stock-market regulator, of trying to frustrate the popular will.

Five Star and the League have repeatedly attacked the Bank of Italy for not preventing the banking crises, and blamed it for the losses suffered by mom-and-pop savers who had bought bank shares and bonds.

“If you are here with your current account in the red, it’s because the people who were supposed to control things didn’t do so,” League’s leader, Interior Minister Matteo Salvini, told a group of former investors in Banca Popolare di Vicenza, which was liquidated in 2017, in February.

That month, Messrs. Salvini and Di Maio said the central bank’s top brass should be replaced because it had failed to effectively supervise the crisis. Since then, they created an institutional standoff by withholding approval for the appointment of one of the bank’s top executives.

As of last week they had forced the creation of a parliamentary commission to look into the failure of Italian banks, launching what could be months of tense scrutiny.

President Sergio Mattarella, who as head of state is positioned above the political fray, asked leaders to make sure the commission doesn’t interfere with the activity of independent authorities, including the Bank of Italy. Central banks, he warned on Friday, can’t accept instructions from governments.

Promoters of the two draft laws argue that having private-sector banks as shareholders creates a conflict of interest for the Bank of Italy, since it is involved in supervising banks.

Critics see an attempt to undermine the Bank of Italy’s independence, and to spend the nation’s gold reserves on populist policies.

“Gold is part of the assets of the Bank of Italy and can’t be used for monetary financing of the Treasury,” said Bank of Italy Governor Ignazio Visco.

The proposals have sparked outrage among the Bank of Italy’s shareholders. The proposed nationalization would value the central bank at just €156,000—the euro equivalent of the price that fascist dictator Benito Mussolini made banks, insurers and other institutions pay for their stakes in the 1930s, when the Bank of Italy was recapitalized.

A 2014 law revalued the Bank of Italy’s share capital at E7.5 billion. Shareholders, including Italy’s biggest lenders, UniCredit SpA and Intesa Sanpaolo SpA, paid a hefty capital-gains tax after the revaluation of their stakes. Now the banks would get only the fascist-era price in compensation.

“This looks like revolutionary expropriation,” said Gianluca Garbi, chief executive of Banca Sistema SpA, which bought its central-bank stake at the new, revalued price and would see its investment wiped out.

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

This ought to be interesting: Trump, who discovered he cannot fire Powell, is probably making sure that all of the other

Fed governors walk_–he is nominating Herman Cain to the last Fed seat. Herman Cain was Fed Chairman, of the Kansas City Fed and that allows him to be nominated.

I can assure you that all of the other board members are thrilled.

(courtesy zerohedge)

Trump To Nominate Herman Cain For Last Open Fed Seat

When Bloomberg reported a few months back that President Trump had interviewed former Godfather’s Pizza CEO and one-time presidential challenger Herman Cain for a seat on the Fed board of governors, Eccles watchers largely wrote him off as a novelty, and focused on cracking jokes about the monetary policy implications of Cain’s infamous 9-9-9 plan.

But others swiftly pointed out that as a former chairman of the Kansas City Fed’s board of directors, Cain was technically qualified for the position, and not really an outlandish pick.

Ellen L. Carmichael

Ellen L. Carmichael✔@ellencarmichael

As the resident Herman Cain historian, it’s important to note that Herman actually has loads of experience with the Federal Reserve and a pretty strong understanding of monetary policy.

So when BBG again reported that Cain was seriously being considered for one of the two open seats – one of which has since gone to Steve Moore – Fed watchers took notice, despite concerns about Cain’s expressly hawkish views on monetary policy (which apparently wasn’t a problem for self-styled “growth hawk” Moore) and worries about the Senate confirmation process.

Jennifer Jacobs

Jennifer Jacobs✔@JenniferJJacobs

White House is considering 2 political figures for board that governs the independent central bank and conducts nation’s monetary policy: Steve Moore, Herman Cain.

Concerns in the WH, though, about whether Cain could clear Senate confirmation process.https://www.bloomberg.com/news/articles/2019-03-22/trump-said-to-consider-stephen-moore-for-federal-reserve-board?srnd=politics-vp …

Jennifer Jacobs✔@JenniferJJacobs

Scoop: White House is considering @StephenMoore for a seat on the Federal Reserve Board, sources tell @SalehaMohsin and me.

Moore, a visiting fellow at Heritage Foundation, was founder of the conservative Club for Growth and served on editorial board of the Wall Street Journal.

Two weeks later, it appears Trump has made up his mind.

According to Axios, Trump has settled on Cain to fill the last remaining open seat on the board, but will wait until his background check is cleared before making the official announcement.

To be sure, there’s a possibility that the background check could pose a problem. Cain’s candidacy during the 2012 Republican primary was cut short following a sexual harassment scandal (Axios’s sources were careful to note that they would attach an “asterisk” to his candidacy). But them again, the president’s favor can often outweigh such considerations.

“He won’t formally announce until the vet is completed…But he likes Cain and wants to put him on there,” said one senior official.

The last few weeks have been crammed with Fed-related news. Not only is Trump nominating Steve Moore, who is expected to do everything in his power to keep rates low, but he reportedly once considered trying to replace Jerome Powell with Kevin Warsh, before concluding that it wasn’t worth it, and telling Powell that “I’m stuck with you.” But that hasn’t stopped him from griping about how nominating Powell was “one of the worst decisions I ever made.”

And since he can’t get rid of Powell, perhaps the president has come up with an alternative plan…

Dan Hurley@ApexHurley

Dan Hurley@ApexHurleyAfter Trump learned he couldn’t fire Powell he devised a plan to make him want to walk into oncoming traffic

Then again, if Trump is so concerned about keeping interest rates low, we could think of another even more suitable candidate.

zerohedge@zerohedge

zerohedge@zerohedgeIf Trump is smart he will nominate AOC for Fed chair

There is an article posted on the monetary-metals.com site (reproduced in Zero Hedge) titled WILL BASEL 111 SEND GOLD TO THE MOON. Extracted from this article is the following:“However, the Office of the Comptroller of the Currency, the Fed, the FDIC, and the Office of Thrift Supervision, put out a document that shows otherwise:

“A bank may assign a risk-weighted asset amount of zero … for gold bullion held in the bank’s own vaults or held in another bank’s vaults on an allocated basis, to the extent the gold bullion assets are offset by gold bullion liabilities[emphasis added].”

Yes, a gold metal asset has the same zero risk-weighting as cash—if the gold asset is funded by a gold liability. What is a gold liability? It is everything that the gold commentariat hates: short gold futures positions, gold swaps, etc.

In other words, it’s the carry trade that we write about every week in our Supply and Demand Report!

Banks can own physical and sell futures, to make a small spread. In this case, the banks don’t need to reserve extra funding for gold, as the market risk of the gold price is hedged. In the parlance of our day, this whole assertion of physical gold being treated preferentially to paper is a big nothingburger“.

Unfortunately this line of argument appears to be accordance with the wording of BASEL 111.I would very much like to read a rebuttal of this argument, because ,as things stand, it appears that just about every gold commentator,including those on my most trusted list,have interpreted this BASEL 111 amendment absolutely incorrectly, and the BIS is in fact encouraging paper gold speculation, which is exactly what I would have expected all along.

Regards

NICHOLAS

Andrew Maguire responds telling up that Basel iii is a big time and it is causing nightmares to our bankers

All,

Aside from the fact that industry apologist Jeffery Christian is paid to sit on the Monetary Metals Advisory board https://monetary-metals.com/?s=christian it also beggars belief that anyone, (producers included), benchmarks and makes trading decisions based on the grossly incorrect dilutive GOFO , Basis -Cobasis ,data that Monetary Metals outputs.

There is so much else wrong with their Basil 111 ‘analysis’ as it fails to take a global view which is why it is necessary for the TBTF banks to build PHYSICAL DELIVERABLE hedges.

We already have the OCC & the BOE on its heels on record looking at these massive undeliverable mismatched paper liabilities held by our Tax payer funded banks.

I am traveling at this time but will address this in more detail when I return.

Warm regards

Andrew

Bill Murphy…

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7154/

//OFFSHORE YUAN: 6.7171 /shanghai bourse CLOSED UP 30.28 POINTS OR 0.94% /

HANG SANG CLOSED DOWN 50.07 POINTS OR 0.17%

2. Nikkei closed UP 11.14 POINTS OR 0.05%

3. Europe stocks OPENED GREEN

/USA dollar index RISES TO 97.18/Euro FALLS TO 1.126

3b Japan 10 year bond yield: RISES TO. –.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.42/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 62.69 and Brent: 69.52

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN /OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO –.01%/Italian 10 yr bond yield DOWN to 2.54% /SPAIN 10 YR BOND YIELD DOWN TO 1.11%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.55: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.63

3k Gold at $1289.85 silver at:15.04 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 11/100 in roubles/dollar) 65.36

3m oil into the 62 dollar handle for WTI and 69 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.42 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9989 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1211 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.01%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.50% early this morning. Thirty year rate at 2.90%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.6258..GETTING DANGEROUS

Global Markets Flatline Ahead Of He-Trump Meeting, US Jobs Report

One day after a global “trade optimism”-inspired rally fizzled at the closing minute of US cash trading, European and Asian shares eased back from eight-month highs while bonds, the dollar and gold rallied as investors took money off the table amid, what else, “fresh concerns” about U.S.-China trade talks while dismal data from Germany signaled trouble for Europe as investors awaited further news from U.S.-China trade negotiations and tomorrow’s US jobs report.

US index futures were flat, while Asian markets and Europe’s Stoxx 600 index fell, led by declines in oil companies and miners.

The biggest economic news of the day was Germany’s latest industrial orders which tumbled at the fastest rate in over five years in February, driven largely by a collapse in foreign demand.

The report compounded fears that Europe’s largest economy, which yesterday slashed its GDP forecast by more than half from 1.9% to 0.8%, has had a feeble start to the year and left the euro stuck at $1.12, sent German Bund yields back below zero in the bond market and ended a four-day run of gains for share traders. Eslewhere, Italian shares and bonds also dropped after Bloomberg reported the country is set to slash this year’s growth forecast and raise the projected budget deficit.

In key company-related news, in the preliminary Ethiopian crash report of the Boeing 737 MAX, anti-stall software is not explicitly mentioned; Chief investigator says they cannot yet say if there is a structural problem with Max 8’s. Meanwhile, Tesla is tumbling after the company’s Q1 vehicle deliveries tumbled and missed badly, with just 63.0k deliveries vs. 90.7k previously.

Earlier in the session, the MSCI Asia index also lost 0.4% overnight after five straight days of gains had taken it to the highest level since late August. Losses were led by Australia and New Zealand while Hong Kong, the Philippines and Indian markets were also in red. The trend was bucked by Shanghai as Chinese shares rose 0.6% while Japan’s Nikkei paused near a recent one-month top.

Emerging-market stocks and currencies also lost momentum on Thursday after recent gains as investors awaited fresh good (or perhaps bad) data for signs the global economy is regaining a firmer footing (or else that central banks will ease more). The MSCI index of developing-market equities fell for a first day in six: the Indian rupee led declines among currencies following a rate cut and dovish outlook from the nation’s central bank. South Africa’s rand weakened after failing to strengthen beyond a key technical level, while the Indonesian rupiah rose after its monetary authority said it would allow further appreciation.

Analysts pointed to investor fatigue and a lack of fresh headlines on the Sino-U.S. trade talks for Thursday’s sell-off while disappointing U.S. economic data this week also weighed on sentiment. “We are expecting quite a constructive agreement between the U.S. and China when it comes to trade,” said AllianceBernstein China Portfolio Manager John Lin. He added it was probably now a consensus view among major investors and if it proved right, would raise other questions such as whether China’s government would “keep its foot on the (stimulus) pedal or ease off a bit.”

Risk sentiment has been supported by constant signs of progress in Sino-U.S. trade talks. White House economic adviser Larry Kudlow said on Wednesday the two sides aimed to bridge differences during talks, while Bloomberg reported that the US would grant China until 2025 to meet trade pledges. The plan would see China committing to buy more U.S. commodities, including soybeans and energy products, and allow full foreign ownership for U.S. companies operating in China as a binding pledge. Investors are also looking if ongoing talks lead to an earlier-than-anticipated meeting between U.S. President Donald Trump and his Chinese counterpart Xi Jinping to sign an accord.

At 2pm all eyes will be on the White House, where President Trump will meet Chinese Vice Premier Liu He as trade deal negotiations enter what could be the final stages.

While investors have become more optimistic that a trade deal will be signed, Bloomberg quotes Nick Twidale, chief operating officer at Rakuten Securities Australia, who said it “may just be another step in the process.” The implementation of any deal “will most probably provide obstacles in the process and may weigh on sentiment further down the track.”

“Also an important question would be whether an agreement would be sufficient to revive business sentiment and the global trade cycle,” J.P. Morgan Asset Management Asia Pacific Chief Market Strategist Tai Hui added. “We believe on the margin it would help, but practically all investors we’ve spoken to in Asia in the past six months believe friction will still flare up from time to time.

In FX, overnight moves were muted after bigger swings overnight when all major currencies gained against the safe-haven yen. The dollar gained broadly with Treasuries while Sterling dipped after U.K. lawmakers moved to block a no-deal Brexit; the euro largely shrugged off soft German data, and was waiting for the minutes of the European Central Bank’s last meeting, when it pushed back rate hike expectations. Euro-area bonds edged higher, and the yen and equities traded with a defensive tone

In commodities, oil prices slipped a second day, with Brent edging down further from the $70 mark after weekly U.S. oil data showed a surprise build up in crude inventories and record production; Global benchmark Brent has gained nearly 30 percent this year, while WTI has gained nearly 40 percent. Prices have been underpinned by tightening global supplies and signs of demand picking up. “There is a clear bias to the upside with the supply restrictions,” said Michael McCarthy, chief market strategist at CMC Markets in Sydney, pointing to supply cuts by OPEC and others, along with sanctions on Iran.

Spot gold traded lacklustre as markets were tentative ahead of the ECB minutes, US-China trade talks and payrolls, with investors pulling money out of gold ETFs with around $153MM removed out of the $10BN VanEck Vectors Gold Miners ETF over the last five days. Meanwhile, copper (-0.3%) succumbs to the cautious risk tone but remains above its 100 WMA of just under $2.90/lb. Finally, Dalian iron ore futures saw its best day in seven-weeks, extending its record-breaking rally, as supply-side woes (largely from cyclones in Western Australia) and a pick-up in demand (steel mills replenishing stocks) boosted the base metal to a new peak of USD 103.49/tonne.

On today’s docket, initial jobless claims are due, while companies reporting earnings include Constellation Brands and RPM International.

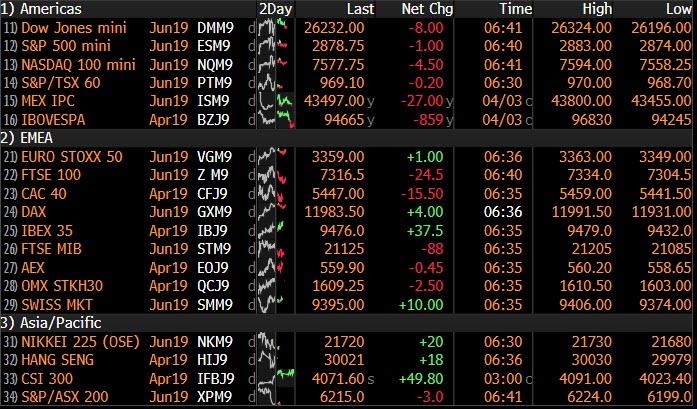

Market Snapshot

- S&P 500 futures down 0.1% to 2,876.25

- STOXX Europe 600 down 0.4% to 387.49

- MXAP down 0.2% to 162.37

- MXAPJ down 0.4% to 538.98

- Nikkei up 0.05% to 21,724.95

- Topix down 0.1% to 1,620.05

- Hang Seng Index down 0.2% to 29,936.32

- Shanghai Composite up 0.9% to 3,246.57

- Sensex down 0.3% to 38,761.75

- Australia S&P/ASX 200 down 0.8% to 6,232.80

- Kospi up 0.2% to 2,206.53

- German 10Y yield fell 0.9 bps to -0.001%

- Euro up 0.04% to $1.1237

- Brent Futures down 0.6% to $68.88/bbl

- Italian 10Y yield rose 1.5 bps to 2.186%

- Spanish 10Y yield fell 0.7 bps to 1.134%

- Brent Futures down 0.4% to $69.05/bbl

- Gold spot up 0.1% to $1,291.33

- U.S. Dollar Index unchanged at 97.10

Top Overnight News from Bloomberg

- U.S. President Donald Trump will meet Chinese Vice Premier Liu He at the White House on Thursday as speculation grows that negotiations over a trade deal are entering their final stages

- Britain took a decisive step away from a damaging no-deal Brexit as members of Parliament and political leaders backed efforts to prevent a disorderly departure from the EU

- Though the U.K. is better prepared for a no-deal Brexit than it was a number of months ago, it would still cause a large economic shock, the Times reports, citing Bank of England governor Mark Carney

- European Union increasingly sees a long Brexit delay as the most likely outcome of an emergency leaders’ summit next week, according to EU officials

- Trade deal that the U.S. and China are crafting would give Beijing until 2025 to meet commitments on commodity purchases and allow American companies to wholly own enterprises in the Asian nation, according to people familiar with the talks

- Bank of Japan is likely to unveil its lowest two-year inflation forecast under Haruhiko Kuroda’s governorship at a meeting later this month, according to a former chief economist of the central bank

- Trump administration is examining options for shutting entry points to the U.S. from Mexico in case the president follows through with his threat to close the border, a White House official said

- Nomura will fire about 100 workers at its troubled European business as Japan’s biggest brokerage embarks on its latest attempt to achieve sustained profitability overseas; the job cuts in Europe will mostly target rates and credit traders in London, one of the people said, asking not to be identified as the numbers aren’t public

- Italy is set to slash its growth forecast for this year and raise its projected budget deficit, according to two senior officials with knowledge of the draft outlook. Italy’s economy is set to grow just 0.1 percent this year, according to the draft, the officials said. The government’s previous forecast was for a 1 percent expansion

- India’s central bank delivered a back-to-back interest rate cut on Thursday and fueled speculation of more policy easing after lowering inflation and economic growth forecasts

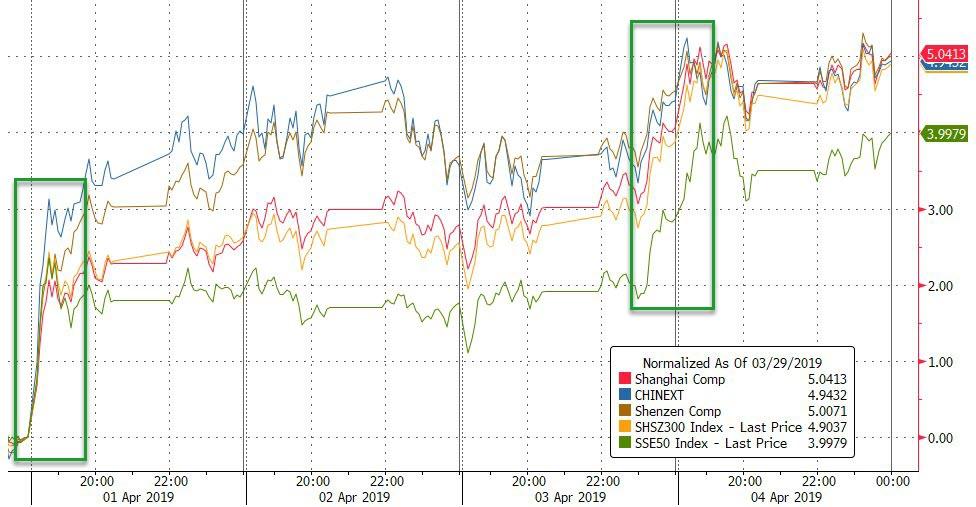

Asian equity markets traded cautiously with the region tentative ahead of looming risk events and after a positive lead from Wall St. where US-China trade optimism kept stocks afloat despite poor ISM & ADP data. ASX 200 (-0.8%) and Nikkei 225 (Unch.) were subdued with broad weakness seen across all sectors in Australia as the post-budget euphoria faded and profit-taking set in following a 7-day win streak, while the Japanese benchmark was indecisive amid a choppy currency. Chinese markets were mixed ahead of an extended weekend in which the Hang Seng (-0.2%) stalled after it briefly rose above 30k for the first time since June last year, while the Shanghai Comp. (+0.9%) was boosted on hopes US and China are nearing a trade deal and with reports also suggesting a Trump-Xi meeting date to sign off on a deal could be announced as early as today. Finally, 10yr JGBs were lower as prices tracked the recent weakness in T-notes and as Japanese stock markets held above water for most the session, while mixed results at the 30yr auction also failed to spur demand.

Top Asian News

- India Central Bank Cuts Interest Rate to Boost Flagging Economy

- Bank Indonesia Chief Says Rate Is on Hold Amid Global Risks

- China Willing to Work With U.S. on Agreement Reached by Leaders

- Japan Post Insurance to Sell $3.7 Billion Shares in Global Deal

A subdued start to the fourth European session of the week with stocks treading water thus far [Eurostoxx 50 U/C] following a mixed Asia-Pac session, ahead of key risk events including the ECB minutes and US-Sino trade talks. The FTSE 100 (-0.6%) marginally lags in the equity-space as a slew of ex-divs [Direct Line (-5.0%), St James’ Place (-3.4%) and DS Smith (-2.4%)] coupled with a firmer Pound pressure the index. Broad-based losses are seen across European sectors, although energy names are faring slightly worse amidst marginal downside in the oil complex. In terms of individual movers, Commerzbank (+2.4%) trades near the top of the Stoxx 600 amid reports that UniCredit (-1.4%) may bid on the German bank if a Deutsche Bank (-1.7%) deal fails. Meanwhile, Software AG (+3.0%) shares were bolstered by a broker upgrade at UBS. On the flip side, Maersk (-11.2%) shares declined following the separate listing of its drilling unit.

Top European News

- Commerzbank Shares Rise on Report of Possible UniCredit Offer

- ICG Said to Near $1.2 Billion Deal for Italy’s Doc Generici

- German Institutes Slash 2019 Growth Forecast by More Than Half

- Miners Fall as Iron Ore Rally Pauses on Anglo and GS Warnings

In FX, the Dollar index is holding around the 97.000 level within an extremely narrow 97.013-225 range, and symptomatic of the listless tone in the G10 currency markets overall after choppy trade from Monday through Wednesday amidst fluctuating risk on, off and on again sentiment. However, today and Friday offer some prospect of more decisive moves or at least price action if not clear direction, with the ECB Minutes, Fed speakers and NFP on the agenda.

- GBP – The Pound remains underpinned as UK Parliament passed another motion to avoid a no deal Brexit and request that PM May go back to the EU seeking a further A 50 extension if no alternative is found to the WA by April 12 or May 22 (assuming no sudden change of heart and the current proposal with Brussels is accepted as the better of evils vs a CU). Cable has rebounded from yesterday’s sub or circa 1.3120 lows to retest 1.3200, but not quite as near the big figure this time as 21/30 DMA convergence around 1.3165 continues to exert some gravitational influence. Similarly, Eur/Gbp has retreated through 0.8550 towards 0.8500 again, though has not managed to get as close as it did on Wednesday.

- JPY/EUR – Both firmer vs the Greenback, albeit fractionally given the relatively constrained trade noted above, with the Jpy inching higher within a 111.50-35 band and potentially capped by decent option expiry interest from 111.50-60 (1.3 bn) and the 200DMA (111.49). Meanwhile, the single currency continues to meet resistance around 1.1250 and has not been helped by abysmal German industrial orders data or confirmation that the country’s group of Economic Institutes has become the latest to slash the 2019 GDP to under 1%.

- CHF/NZD/AUD/CAD – All underperforming, but again in context only marginally. Indeed, the Franc is meandering between 0.9987-72, Kiwi hovering from 0.6800 to 0.6773 and Aussie just keeping its head above 0.7100, and at this stage not looking likely to arouse expiry interest at 0.7140-50 in 1 bn. For choice, the Loonie is lagging against the backdrop of softer crude prices and back below 1.3350 ahead of Canada’s Ivey PMI.

- EM – Literally no respite for the Lira it seems, as economic, fiscal and political issues continue to weigh on the currency and Turkish assets in general. Indeed, Usd/Try has nudged up to 5.6600 again after Wednesday’s mixed inflation data and another hike in swap limits, as investors eye next week’s Economic Program conscious of the fact that the CBRT may not be able to loosen its grip on the monetary policy reins given that headline CPI remains so high.

In commodities, the energy complex had consolidated following yesterdays advances and was edging lower for the majority of the session, though WTI & Brent futures have recently reverted much of this downside and are now just edging into positive territory for the day. Brent and WTI are currently trading around sesson highs of USD 69.34 and USD 62.50 respectively. Earlier in the session, Brent prices edged lower after hitting resistance at its 200 DMA around USD 69.60/bbl, meanwhile WTI remains north of its 200 DMA (USD 61.40/bbl). Elsewhere, spot gold (+0.1) trades lacklustre as markets are tentative ahead of the ECB minutes, US-China trade talks and NFP. It is also worth noting that investors are pulling money out of gold ETFs with around USD 153mln removed out of the USD 10bln VanEck Vectors Gold Miners ETF over the last five days. Meanwhile, copper (-0.3%) succumbs to the cautious risk tone but remains above its 100 WMA of just under USD 2.90/lb. Finally, Dalian iron ore futures saw its best day in seven-weeks, extending its record-breaking rally, as supply-side woes (largely from cyclones in Western Australia) and a pick-up in demand (steel mills replenishing stocks) boosted the base metal to a new peak of USD 103.49/tonne.

US Event Calendar

- 7:30am: Challenger Job Cuts YoY, prior 117.2%

- 8:30am: Initial Jobless Claims, est. 215,000, prior 211,000; Continuing Claims, est. 1.75m, prior 1.76m

- 9:45am: Bloomberg Consumer Comfort, prior 60

DB’s Jim Reid concludes the overnight wrap

After a pause on Tuesday, Monday’s risk rally on stronger manufacturing PMIs extended further yesterday on the previous night’s trade news and then a mostly positive global round of non-manufacturing PMIs. It was so good that 10 year bund yields now give you a positive yield again (0.008% – up +5.7bps yesterday). Hurry while stocks last. It makes me want to work out how much the average person would have to invest in them to give them their required retirement income given the 1bps yield! The move was helped by signs of hope from the services PMIs in Europe (more on that below) and Kudlow’s comments that US and China negotiators are “making good headway”. Later in the session, Bloomberg reported that the US requested a six-year timetable for China to implement changes to its import purchases and market access reforms, possibly an indication that a deal is being formalised. The FT reported that there are still a couple of sizeable outstanding issues; 1) what happens to existing US levies on Chinese goods, which Beijing wants to see removed, and 2) the terms of a US enforcement mechanism that ensures that China abides by the deal. Overnight, the White House has said that President Trump will meet Chinese Vice Premier Liu He today in the Oval Office at 16:30 ET (21:30 UK Time). It really feels like progress is being made even if tough work remains.

The tech sector really led the charge yesterday with the NASDAQ closing up +0.60%, albeit off its highs of +1.14%, which means it’s now closed up four days in a row – good for a +2.95% spurt during that time. The FANGs weren’t to be left out with the NYSE FANG index rallying +0.93% – the fifth consecutive daily gain – to put it at the highest level since early October. Amazingly the NASDAQ is also back to being just 2.64% off its all-time highs from late August again. Meanwhile the S&P 500 climbed +0.21% and DOW +0.15%. The latter’s underperformance was entirely driven by Boeing’s -1.54% drop. The Wall Street Journal reported that last month’s 737 Max crash in Ethiopia came despite the fact that pilots followed Boeing’s instructions on how to compensate for a software defect. Ethiopian authorities will release their report on the crash today, potentially opening Boeing up to legal liability.

European equities had a better session, with the Stoxx 600 advancing +1.01% to its highest level since August 9th last year. Bourses rallied across the continent, led by the DAX (+1.70%), the IBEX (+1.33%), and by banks (+1.61%). The only major laggard was the FTSE 100 (+0.37%), which was pressured by the stronger pound on perceived positive Brexit news as well as by the sharp rise in gilt yields, which rose +9.4bps for their biggest selloff in 13 months. Treasury yields rose as well, climbing +4.5bps while the 2s10s curve steepened another 1.0bps to 18.0bps. High yield spreads were also 5bps tighter in both Europe and the US. Oil prices traded flat, though US inventory data showed a surprisingly large 7.2 million barrel increase in stockpiles last week, taking some air out of the narrative of robust demand so far this year.

On Brexit, Prime Minister May and Labour Leader Corbyn held discussions yesterday on a cross-party proposal that both sides described as “constructive” even if Mr Corbyn said that there had not been “as much change as (he) had expected” in Mrs May’s stance.

Their teams will continue negotiations today, and the most likely date for another vote is Monday or Tuesday next week. Last night, Parliament voted 313-312 to pass the Cooper-Letwin amendment, which would try to force a long Article 50 extension. The bill will now move to the House of Lords today and, assuming it is passed cleanly, will take no-deal Brexit off the table – from the U.K. side at least. That has enraged the hard-Brexit supporting wing of May’s party, but it could still push them to back her deal next week if she ends up bringing it to a vote. Prior to the May and Corbyn meeting, European markets were mostly busy watching any Parliament reaction to May’s pivot and any reaction from the EU. On the former two MPs resigned however significantly neither were Cabinet ministers. Is this the calm before the storm in terms of resignations? It’s fair to say that there are a vast number of unhappy Tory MPs over the talks with Mr Corbyn. On the latter there wasn’t too much to highlight. The EU seem to be mostly watching for now. Elsewhere, the Sun has reported overnight that PM May is likely to request 9 month delay to Brexit during the EU summit.

In Asia this morning markets are trading mixed with the Shanghai Comp (+0.56%) and Kospi (+0.19%) up while the Hang Seng (-0.52%) is down and the Nikkei is trading flat. Elsewhere, futures on S&P 500 are trading flattish (-0.06%).

Back to the PMIs where the big talking point, and in contrast to the manufacturing data, was the 0.6pt upward revision to the March services reading for the Euro Area to 53.3, helping to lift the composite to 51.6 (vs. 51.3 flash). With the services sector more domestically orientated than the manufacturing sector it helps to boost the case that the domestic European economy is generally doing ok. The positive revision was helped by a boost from most countries. Germany and France were revised up 0.5pts to 55.4 and 0.4pts to 49.1, respectively, while Italy (53.1 vs. 50.8 expected) and Spain (56.8 vs. 55.0 expected) both came in ahead of expectations.

Staying with the PMIs, yesterday DB’s Peter Sidorov highlighted the fascinating stat that while Germany’s manufacturing PMI is in the deepest downturn outside of the Great Recession, Germany’s services PMI is in the top 25% of readings since the start of the euro area recovery in late 2013. In standardised terms, that is the largest underperformance of manufacturing vs services we have seen since the start of the data in 1997.

Overall the data should be welcomed by the ECB however it doesn’t hide the fact that any recovery back to trend growth still requires the manufacturing sector to lift out of the doldrums. On the subject of the ECB yesterday we got a fresh story from MNI under the title “ECB tiering more likely if rates cut further”. A word of warning that MNI hasn’t proved to be the most reliable of sources in recent times. The headline seemed to be a bit punchier than the actual story too, with the main message being that the tiering debate is still in its infancy right now with no clear outcome.

There’s a chance that we learn a bit more about the ECB’s thinking today with the minutes from last month’s confused policy meeting. Confused in the sense that it felt like the ECB sent out various contradicting messages. A reminder that in the end that they opted to announce the bare bones of the new TLTRO replacement facility but downgraded growth and inflation without suggesting any cohesive future policy implications.

In contrast to the data in Europe yesterday it wasn’t quite so good a day for US data. The March ADP print came in at 129k versus 175k expected, and in fact was the lowest reading since September 2017. We should however caveat that the ADP reading overstated NFPs by 163k in February, which isn’t the first time we’ve seen such a big divergence. So there is a bit of a question about the ADP survey being a reliable spot indicator of payrolls. More important though was the miss in the March ISM non-manufacturing (56.1 vs. 58.0 expected) and -3.6pt drop from February. New orders was the big driver of the decline (59.0 from 65.2), however, the employment component did nudge up +0.7pts to 55.9. The gap between the US and the RoW is closing through a slight dip in the former and a welcome rise in the latter.

To the day ahead now where shortly after this hits your emails we’ll get February factory orders data out of Germany, followed by the March construction PMI. In the US this afternoon the early data release is March challenger job cuts before we get the latest weekly initial jobless claims reading. We’ve also got the aforementioned ECB minutes due out at lunchtime while the Fed’s Mester and Harker are speaking this evening. Keep an eye on potential trade headlines too with China Vice Premier Liu He now in Washington.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 30.28 POINTS OR 0.94% //Hang Sang CLOSED DOWN 50.07 POINTS OR 0.17% /The Nikkei closed UP 11.14 POINTS OR 0.05%/ Australia’s all ordinaires CLOSED DOWN .76%

/Chinese yuan (ONSHORE) closed DOWN at 6.7154 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 62.69 dollars per barrel for WTI and 69.52 for Brent. Stocks in Europe OPENED GREEN

ONSHORE YUAN CLOSED UP // LAST AT 6.7154 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7171 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/

3 b JAPAN AFFAIRS

3 C CHINA

i)BREXIT/EU/

The pound rallies as the commons passes a bill requiring Theresa May to request another Brexit delay. The farce over there continues

(courtesy zerohedge)

Pound Rallies As Commons Passes Bill Requiring May To Request Another Brexit Delay

Succeeding in their latest attempt to head off a no-deal Brexit, the Commons has passed the Cooper Letwin bill legally requiring Prime Minister Theresa May to request another delay of Article 50 if the UK looks to be on the cusp of leaving the EU without a deal.

After rejecting all of the proposed amendments, the Commons passed the bill by a margin of just one vote, winning 313 to 312. It now heads to the House of Lords, which is expected to vote on the measure on Thursday.

Faisal Islam

✔@faisalislam

Basically unamended Cooper Letwin Bill has passed its committee stage 4 hours after its second reading….

MPs now voting on its third reading – ie the big final vote.

Peter Bone furious asking Speaker to “make this farce stop” and order “There can be no third reading”. pic.twitter.com/728OX8WN0B

The pound climbed as the bill’s passage appeared to lessen the chances of the UK leaving the EU without a deal (though, even if May does request another extension, the EU could still opt to deny her request, which European Commission Jean Claude Juncker has suggested would be the case).

GBP/USD climbed as much as 0.2% to 1.3179.

However, while top officials in Brussels have insisted that the won’t grant another extension unless the Commons passes the withdrawal agreement, anonymously sourced reports published earlier in the day on Wednesday said the EU27 was leaning toward an arrangement where they would grant an extension if the UK agrees to certain ‘conditions’ like participating in the EU Parliamentary elections next month. May is reportedly leaning toward requesting a nine-month delay, as reports published late in the day suggested that her talks with the opposition haven’t been going as well as Labour said.

Unsurprisingly given the gathering momentum for a ‘no deal’ Brexit among the Tories and DUP, the vote to demand another request for a delay has prompted some to question the Commons’ wisdom in so openly defying the referendum.

Nigel Farage

✔@Nigel_Farage

How can a single vote in parliament supersede the 1.3m vote majority for Brexit?

It is now clear we will have to fight our political classes again.

I’m up for it.

Press Association

✔@PA

#Breaking Proposed legislation to further delay the date of Brexit clears the Commons after MPs give it a third reading by 313 votes to 312

An Open Letter To The UK Prime Minister (From One Of The Seventeen Million)

Dear Prime Minister,

The main argument put forward by the Treasury etc against Brexit has been the potential economic damage which may or may not be accurate.

What is fact however is that, according to the U.S. Federal Reserve Bank – the most important central bank in the world – U.K. total factor productivity growth has fallen from 3.84% in 1973 – (2.88% per annum in the 10 years ending 1973) – to 0.14% in 2016, the most recent data, and negative 0.17% per annum in the 10 years ending 2016. Based on the difference between the 10-year average up to 1973 and the subsequent growth, productivity is just 43% of the size it would otherwise have been. Whilst an opportunity cost rather than a real loss of wealth, the damage is all too clear.

The data gets worse. Even stripping out the 2008 and 2009 crisis years, the last 20 years of productivity is the worst since the 20 years ending 1922 which obviously encompassed WW1 and the enormous loss of capital funding the war.

Referring to U.S. Conference Board data, which allows comparisons with the rest of the world since 1990, over the 28 years to 2017, U.K. total factor productivity was up 4.8%, France was up 3.6%, Italy -5.3% and Spain -8.3%. Whilst true that Germany was up a more respectable 13.9%, over a 28-year period that is very disappointing, and most of that was catch-up productivity from Eastern Germany. The European Union has failed its people economically, and without economic strength, it has undermined its security as we have unfortunately been suffering in recent years with the growing number of terrorist attacks.

Economic growth over and above productivity is a measure of capital depletion; either under-investment if productivity growth is slowing or actual physical decline if productivity is falling as in recent years; U.K. productivity is down 5.1% since peaking in 2006. It is somewhat ironic therefore that companies are threatening to pull out of the country in the event of Brexit, because that is precisely what they have been doing through underinvestment for many years. It is also worth remembering that we are consumers as well as producers, so taking production out of the country would undermine the market for their products and would therefore be akin to shooting themselves in the foot.

The fall in productivity growth reflects an unproductive allocation of capital, either directly from government fiscal and spending policy or as a result of the regulatory and monetary boundaries imposed by the government and central bank which distort pricing signals and investment decisions.

With the greatest of respect, Nigel Farage is not to blame for the public demanding Brexit as so many politicians claim. He has simply opened a channel through which the public have been able to express their frustrations with this stagnation, and in recent years, loss of productivity, from which all the other ills stem. Even immigration stems from the underinvestment in plant and equipment that has driven the need for low paid immigration to compensate. The blame should not be put on Mr Farage therefore, but rather the politicians themselves whose values, and policies, are simply unaffordable to the population.