GOLD: $1291.50 UP $1.35 (COMEX TO COMEX CLOSING)

Silver: $15.11 DOWN 2 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1291.60

silver: $15.11

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today ISSUING: 25/105

EXCHANGE: COMEX

CONTRACT: APRIL 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,289.000000000 USD

INTENT DATE: 04/04/2019 DELIVERY DATE: 04/08/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 H HSBC 15

657 H MORGAN STANLEY 32

661 C JP MORGAN 25

686 C INTL FCSTONE 6

737 C ADVANTAGE 51 22

800 C MAREX SPEC 16 4

880 H CITIGROUP 39

____________________________________________________________________________________________

TOTAL: 105 105

MONTH TO DATE: 4,028

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 105 NOTICE(S) FOR 10,500 OZ (.326 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 4028 NOTICES FOR 402,800 OZ (12.528 TONNES)

SILVER

FOR APRIL

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 697 for 3,485,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE :$4975 UP $76

Bitcoin: FINAL EVENING TRADE: $4991 UP 92

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A STRONG SIZED 3668 CONTRACTS FROM 201,229 UP TO 204,897 DESPITE YESTERDAY’S 0 CENT RISE IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE MUST HAVE HAD CONSIDERABLE SHORT COVERING AGAIN TODAY. NO DOUBT THAT THE ENTIRE RISE AT THE COMEX WAS DUE TO THE SPREADERS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 0 FOR MAY, 2716 FOR MARCH 2020 0 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2716 CONTRACTS. WITH THE TRANSFER OF 2716 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2716 EFP CONTRACTS TRANSLATES INTO 13.58 MILLION OZ ACCOMPANYING:

1.THE 0 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

AND NOW 3.860 MILLION OZ STANDING FOR SILVER IN APRIL.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

7607 CONTRACTS (FOR 5 TRADING DAYS TOTAL 7607 CONTRACTS) OR 38.04 MILLION OZ: (AVERAGE PER DAY: 1521 CONTRACTS OR 7.607MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 38.04 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 5.43% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 610.73 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3688 DESPITE THE 0 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY..HOWEVER AS INDICATED ABOVE, MOS OF THE GAIN IN OI WAS DUE TO SPREADERS. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 2716 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A HUMONGOUS SIZED: 6384 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2716 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 3604 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 0 CENT GAIN IN PRICE OF SILVER ???? AND A CLOSING PRICE OF $15.13 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.997 BILLION OZ TO BE EXACT or 143% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR nil OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ AND NOW APRIL AT 3.860 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST AGAIN FELL AND THIS TIME BY A CONSIDERABLE SIZED 3604 CONTRACTS, TO 436,656 DESPITE THE TINY LOSS IN THE COMEX GOLD PRICE/(A FALL IN PRICE OF $0.90//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUMONGOUS SIZED 11,005 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 11,005 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020l 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 436,656. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A NET GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7401 CONTRACTS: 3604 OI CONTRACTS DECREASED AT THE COMEX AND 2716 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 7401 CONTRACTS OR 740,100 OZ OR 23.02 TONNES. YESTERDAY WE HAD A FALL IN THE PRICE OF GOLD TO THE TUNE OF $0.90….AND YET WITH THAT, WE HAD A STRONG GAIN IN TONNAGE OF 23.02TONNES!!!!!!.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 30076 CONTRACTS OR 3,007,600 OR 93.54 TONNES (5 TRADING DAYS AND THUS AVERAGING: 6015 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAYS IN TONNES: 93.54 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 93.54/3550 x 100% TONNES = 2.63% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1470.60 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 3604 WITH THE LOSS IN PRICING ($0.90) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A HUMONGOUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11005 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11005 EFP CONTRACTS ISSUED, WE HAD A STRONG GAIN OF 7754 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

11005 CONTRACTS MOVE TO LONDON AND 3604 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 24.11 TONNES). ..AND ALL OF THIS STRONG DEMAND OCCURRED WITH A FALL IN PRICE OF $0.90 IN YESTERDAY’S TRADING AT THE COMEX???

we had: 105 notice(s) filed upon for 10500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP 1.35 TODAY

A BIG CHANGE IN GOLD INVENTORY AT THE GLD

ANOTHER WITHDRAWAL OF GOLD FROM THE GLD: 1.74 TONNES

THE CROOKS NEED THIS GOLD TO PUT OUT DEMAND FIRES HERE AND ABROAD.

WE ARE COMING TO THE BOTTOM OF THE BARREL WITH RESPECT TO PHYSICAL GOLD HELD AT THE GLD.

INVENTORY RESTS AT 762.55 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 2 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV

IT SURE LOOKS LIKE THERE IS NO PHYSICAL SILVER AT THE SLV TO ROB.

/INVENTORY RESTS AT 309.167 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A STRONG SIZED 3668 CONTRACTS from 201,229 UP TO 204,897 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET….. I WROTE THE FOLLOWING YESTERDAY:

“YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF APRIL BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

AND TRUE TO FORM, THE COMEX OI ROSE BY A HUGE 3819 CONTRACTS YESTERDAY DESPITE THE ZERO GAIN IN PRICE AND NO DOUBT THAT MOST OF THIS GAIN WAS DUE TO THE SPREADERS.

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 2716 FOR MAY AND MARCH 2020: 0 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2716 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 3668 CONTRACTS TO THE 2716 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN OUT OF THIS WORLD GAIN OF 6384 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 31.92MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH. AND NOW 3.860 MILLION OZ FOR APRIL.

RESULT: A HUMONGOUS SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE TINY 0 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 2716 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED //Hang Sang CLOSED BOTH CHINESE HOLIDAY /The Nikkei closed UP 82.55 POINTS OR 0.38%/ Australia’s all ordinaires CLOSED DOWN .79%

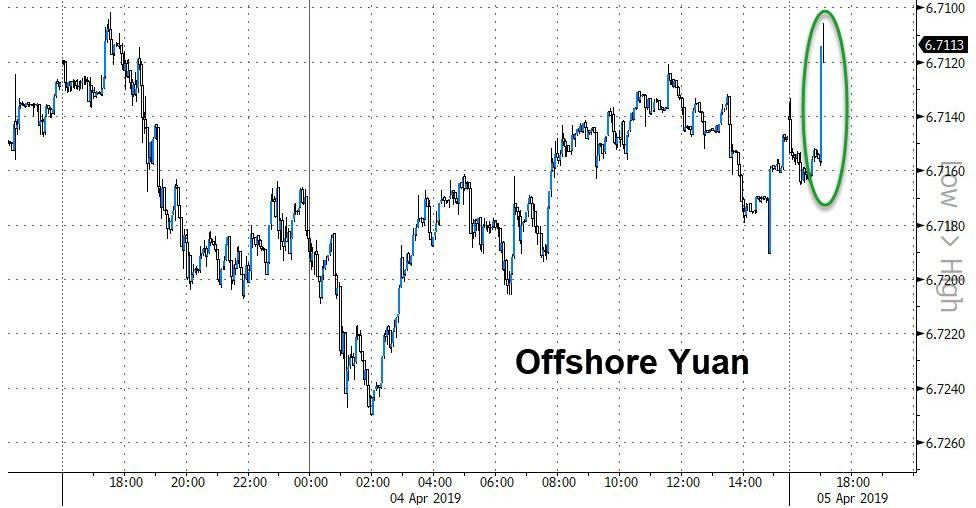

/Chinese yuan (ONSHORE) closed UP at 6.7079 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 62.69 dollars per barrel for WTI and 69.52 for Brent. Stocks in Europe OPENED GREEN

ONSHORE YUAN CLOSED UP // LAST AT 6.7079 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7136 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

Where have we seen this before: yuan and stock futures rise on substantive progress in trade

( zerohedge)_

4/EUROPEAN AFFAIRS

i)BREXIT/EU/

Theresa May has formally requested another short term Article 50 extension letter to Donald Tusk asking the EU 27 to delay Britain’s exit until June 30. She conditions that the UK would participate in the upcoming EU parliamentary elections. She states that the UK could leave earlier if it passes her deal.

( zerohedge)

ii)Graham Summers points out that the ECB is going to have negative rates for quite some time. He is also warning that the USA is heading in that direction

( Graham Summers)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Iran/Syria/Russia//Israel

This is not a good development as Iran is to establish its first ever Mediterranean Port on the Syrian coast next to Latakia. This will strength its land bridge from Tehran through to Lebanon. The Russians are not happy that they will give up some of the port to Iran. Israel is furious and no doubt when the time comes, they will bomb the port.

( zerohedge)

6. GLOBAL ISSUES

i)This is going to heart the global production of pork as African Swine Fever breaks out.

( Michael Snyder)

7. OIL ISSUES

The Saudi’s are panicking as the USA is threatening anti trust action on OPEC

( zerohedge)

8 EMERGING MARKET ISSUES

VENEZUELA

9. PHYSICAL MARKETS

(two commentaries/Wall Street Journal and Rabobank)

ii)More on the commentary by Bart Chilton where Chris Powell asserts that the evidence of manipulation was not enough for charges as it was the government itself the perpetrator

( Chris Powell/GATA)

iii)The Central Bank of Russia has decided it needs to bring up its gross international reserves to 500 billion dollars worth and gold will play a much bigger role

( BNE/Berlin/GATA)

iv)The article is outlined below under oil. The Saudi are angry and they may ditch the dollars

( Reuters)

v)This was written prior to the Butler/Chilton commentary. Gold and silver are manipulated constantly

(courtesy Kranzler/Hemke

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning/FOMC

a)Wage payrolls rise by 196,000 but the all important wage growth disappoints badly. The phony birth/death plug was 56,000.

(zerohedge)

b) the real story

(zerohedge)

ii)Market data

TRUMP is truly aware of what is going on. He is now calling for QE 4 as yields and the dollar slide

( zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

a)Boeing admits its software was behind the 737 max crash. I am no so sure

(zerohedge)

a ii)this will hurt GDP and the Dow: Boeing slashes 737 production by 20%

( zerohedge)

c)More bricks and mortar stores bite the dust

( Mish Shedlock/Mishtalk)

iv)SWAMP STORIES

a)A good one: Was John Brennan the ringleader? It sure looks so

( Monica Crowley/Washington Times)

b)Interesting: The Chicago Police Dept. is suing Jussie Smollett for overtime it paid to officers investigating his case

( zerohedge)

c)Kim Strassel, of the Wall Street Journal rails against the New York Times for shoddy reporting on the Mueller report. She feels that the anonymous sources are not really sources at all. The big question is this: if it is a cover up, why hasn’t anyone in the Mueller gone public with their feelings on the matter.

d)I do not know if you agree with me but I think Pelosi and her crazies move to block Trump’s border wall is treasonous

end

Let us head over to the comex:

AFTER APRIL, WE HAVE THE ACTIVE DELIVERY MONTH OF MAY AND HERE THE OI FELL BY 186 CONTRACTS DOWN TO 128,681. CONTRACTS.. THE NEXT MONTH OF JUNE ADDED 4 CONTRACTS TO TOTAL 32. AFTER JUNE, THE VERY BIG DELIVERY MONTH OF JULY HAD A GAIN OF 3125 CONTRACTS UP TO 46,299 CONTRACTS.

Silver Bullion Set to Soar to $50 an Ounce (GoldCore Video)

– Silver bullion is the most undervalued precious metal, commodity and asset today

– Silver very rarely covered in the media and thus the fundamentals are not understood

– Supply demand fundamentals are very positive indeed as seen in recent report from Capital Economics

– While industrial demand may weaken, investment and safe haven demand for silver coins and bars will surge in the next crisis

– Silver mine production falling: Dozen of the largest silver mines in the world fell by 8% in 2018

– Silver bear market was exacerbated by manipulation and pushing silver lower

– Silver is going higher and $50 per ounce is a conservative target in the next 3 or 4 years

– In 2007 and 2009 we said gold would surge in the crisis and target $50 per ounce

– Long term charts are very bullish and show undervalued versus all assets and even gold

– Gold to silver ratio over 80 to 1 today: 15 to 1 is likely in the coming years (see chart)

– Silver prices adjusted for inflation are cheaper than 1916! (see chart)

– Record high for silver adjusted for inflation is over $115/oz (based on U.S. CPI) and over $700/oz (based on John Williams of Shadow Stats inflation data and methodology)

– Silver at lowest prices in history; T ime to buy and dollar cost average into position is now

– Avoid digital and ETF gold and silver and only own coins and bars in your possession or in allocated and segregated storage

Until April 18, when you purchase the minimum amount of 10,000 ($€£) in physical gold and or silver, you receive complimentary Storage In Zurich For 6 Months

News and Commentary

Gold dips to four-week low as dollar rises on robust weekly jobs data (GoldReview.com)

Gold futures finish slightly lower as dollar index bucks up (MarketWatch.com)

Trump Selects Gold Standard Advocate Cain for Fed Board – Sources (Bloomberg.com)

Trump says U.S. economy strong despite ‘destructive actions’ by Fed (Reuters.com)

Italy’s ruling populists push ahead to seize central bank gold reserves (ForexLive.com)

Source: Bloomberg

Ray Dalio Sounds a New Alarm on Capitalism’s Flaws, Warns of Revolution (Bloomberg.com)

Millions of Facebook Records Found on Amazon Cloud Servers (Bloomberg.com)

The Manhattan Housing Market Is On Its Worst Streak In 30 Years (ZeroHedge.com)

Manhattan Home Sales Drop to Decade Low for a First Quarter (Bloomberg.com)

Trump nominates a second gold standard advocate for Fed (WSJ.com)

Royal Canadian Mint releases three new bullion coins (Mining.com)

Gold Prices (LBMA PM)

04 Apr: USD 1,291.60, GBP 981.87 & EUR 1,149.78 per ounce

03 Apr: USD 1,291.85, GBP 980.38 & EUR 1,148.84 per ounce

02 Apr: USD 1,287.20, GBP 984.97 & EUR 1,148.95 per ounce

01 Apr: USD 1,291.90, GBP 987.27 & EUR 1,149.15 per ounce

29 Mar: USD 1,291.15, GBP 991.09 & EUR 1,151.19 per ounce

28 Mar: USD 1,306.90, GBP 995.20 & EUR 1,161.18 per ounce

Silver Prices (LBMA)

04 Apr: USD 15.08, GBP 11.48 & EUR 13.44 per ounce

03 Apr: USD 15.16, GBP 11.51 & EUR 13.49 per ounce

02 Apr: USD 15.02, GBP 11.51 & EUR 13.42 per ounce

01 Apr: USD 15.07, GBP 11.50 & EUR 13.42 per ounce

29 Mar: USD 15.10, GBP 11.52 & EUR 13.45 per ounce

28 Mar: USD 15.19, GBP 11.58 & EUR 13.53 per ounce

Recent Market Updates

– Perth Mint’s Gold Bullion Sales Surge 68% In March

– Central Banks Continue to Buy Gold at a Record Clip

– ItalExit and Cyber Risks in a Cashless World May Be Bigger Risks Than Brexit : Interview with GoldCore CEO

– Ireland and EU Countries Must Seek ECB Approval to Manage Gold Reserves – Draghi

– Global Risks Increasing – Underlining The Case For Gold in 2019 (GoldCore Video Presentation)

– Brexit and Learning To “Live With Boom and Bust Economic Cycles”

– ‘No Deal’ Brexit Risk Impacting UK and Irish Economies – Gold Gains On Recession Concerns

– America’s “Debt Crisis Is Coming Soon”

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

Trump nominates a second gold standard candidate for the Fed

(two commentaries/Wall Street Journal and Rabo bank)

Trump nominates a second gold-standard advocate for Fed

Submitted by cpowell on Fri, 2019-04-05 04:09. Section: Daily Dispatches

Trump Picks Herman Cain for Fed Seat

By Nick Timiraos and Alex Leary

The Wall Street Journal

Thursday, April 4, 2019

President Trump said Thursday he intends to nominate former GOP presidential candidate Herman Cain to the Federal Reserve’s board of governors, signaling his desire to remake the nation’s central bank after complaining about it for months.

The selection of Mr. Cain, following the president’s decision to nominate his former campaign adviser Stephen Moore, marks an effort to install two Fed critics and loyal Trump supporters on the central bank’s powerful seven-seat board.

…

Rabo: “Stocks Are Trading As If Cain Has Already Been Appointed – Everybody Wants A Slice”

Submitted by Michael Every of Rabobank

An offer he can’t refuse

More than a few news agencies are now reporting that President Trump intends to nominate former CEO of Godfather’s Pizza, Herman Cain, for a seat on the Federal Reserve Board of Governors. Mr. Cain did serve for one year as Chairman to the Federal Reserve Bank of Kansas City. Other than that he has a proven track record in food, restaurants, retail and, more recently also being a contributor to Fox News. In 2011/12 Mr. Cain even made a bid for becoming President of the United States, calling for a much simplified US tax-code, where a flat tax rate of 9% would be the key feature in corporate, income and sales taxes. Although he did well during the campaign, he was forced to abandon his bid following allegations of sexual harassment.

According the NY Times, Mr. Cain used to be a proponent of a return to the gold standard (which would actually suggest he is an inflation hawk), but that he has changed his mind and has now embraced the notion that the risk of deflation outstrips that of inflation. So whether Mr. Cain is truly the best candidate out there remains to be seen (and the Senate has to confirm Mr. Trump’s nominees), but President Trump clearly appreciates Mr. Cain’s qualities (pizza, Fox News and a proponent of low interest rates). Indeed, Mr. Trump has already called Mr. Cain “a truly outstanding individual”. Did Trump make him an offer he cannot refuse?

So picture this: everyday could be “pizza day”! Surely equities are trading as if Mr. Cain has already been appointed – everybody wants a slice! The S&P500 made a y-t-d high yesterday, although bond investors, again, showed their more bearish nature with a flattening of the German curve (3m Bills +3bp, 30y -4bp) as well as the US Treasury curve.

In addition to Trump’s dovish nominees, the conviction of sitting hawks is also slowly fading. While Ms. Mester reiterated that she doesn’t see rate cuts yet, she did admit that “it is possible” that the hiking cycle may be over. So on balance, the FOMC is starting to get more dovish, as also radiated from the March meeting.

And as we’ve noted before, the Fed isn’t alone in that respect. Yesterday’s accounts of the March ECB meeting showed no urgent concerns, but whichever way they slice or dice it, there is clearly increasing unease among the Council members. Against this background, there was support for the broad measures announced in March. In fact, some had called for a longer extension of forward guidance, into 2020Q1. This suggests that the Council isn’t yet very convinced that it will be able to hike rates early in 2020, and adds to the risk that the ECB may need to postpone its guidance at a later date.

Additionally the accounts note that “concerns were voiced” over the potential effects of persistent low rates. No conclusions were drawn, however, and thus no policy measures to address any potential effects were discussed either. As we concluded in our earlier note on tiered rates, these concerns and potential measures suggest that the Council sees rates on hold for a longer period than their guidance suggests. This also chimes with the abovementioned calls for a longer extension of guidance.

In other words, risks are clearly skewed to low(er) rates for longer, and notwithstanding the implications this may have for the economic outlook, equities are enjoying this prospect.

Day ahead

Data from Germany this morning seemingly contradicted the downside risks highlighted above, but when you dig deeper, a different picture emerges. In contrast to yesterday’s astonishingly weak German factory orders for February, industrial output for that same month actually rose 0.7%, largely offsetting the drop in production in the first month of the year. At least this takes the sharp edges of yesterday’s numbers, although we need to bear in mind that whilst the orders data tend to be more volatile, the causality usually runs from orders to output rather than the other way around. Moreover, digging deeper into the details shows that it was the construction sector that saved the day, reporting a 6.8% m/m increase in output. Since the average daily temperature in Germany was 5.8 degrees higher than in the same month last year, this probably goes quite some way in explaining the boost in construction output. Excluding the construction sector, output fell by 0.4% m/m and this seems to be a better fit with the recent data on orders as well as purchasing managers’ indices. In other words, don’t get too excited yet.

Today’s Non-Farm Payrolls in the US for March is one of the key reports to watch. The ADP figures released earlier this week surprised to the downside, but given the recent distortions due to the partial government shutdown, there is additional uncertainty surrounding the March figures. Following a slow 20K jobs gain in February, the consensus is looking for a 177K gain in March, basically re-establishing monthly jobs growth at the lower end of the range of previous years. More important perhaps are the average hourly earnings data. Last month, earnings growth reached 3.4% y/y, its highest level since April 2009 and – given the tightening labour market – providing some support for the view that the tightening labour markets is slowly but surely starting to exert upward pressure on wages. Although it would require a fairly strong monthly 0.3% gain to maintain the annual growth rate at its February rate, one can only assume that – against the backdrop of the Fed’s recent U-turn – it is the assumption among policy makers that the labour market recovery is in its final stages and will soon reverse. If not, expect an interesting debate to develop at some point.

Happy – Pizza – Friday!

end

More on the commentary by Bart Chilton where Chris Powell asserts that the evidence of manipulation was not enough for charges as it was the government itself the perpetrator

(courtesy Chris Powell/GATA)

(courtesy BNE/Berlin/GATA)

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7079/

//OFFSHORE YUAN: 6.7139 /shanghai bourse CLOSED HOLIDAY

HANG SANG CLOSED HOLIDAY

2. Nikkei closed UP 82.55 POINTS OR 0.38%

3. Europe stocks OPENED GREEN EXCEPT SPAIN

USA dollar index FALLS TO 97.31/Euro RISES TO 1.1229

3b Japan 10 year bond yield: RISES TO. –.03/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.71/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 61.96 and Brent: 69.11

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP /OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +02%/Italian 10 yr bond yield DOWN to 2.50% /SPAIN 10 YR BOND YIELD UP TO 1.12%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.48: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.55

3k Gold at $1287.10 silver at:15.11 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 11/100 in roubles/dollar) 65.36

3m oil into the 61 dollar handle for WTI and 69 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.71 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0004 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1232 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISING to +0.02%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.54% early this morning. Thirty year rate at 2.94%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.6016..GETTING DANGEROUS

Global Stocks Rise On, What Else, “Trade Talk Optimism”

Another day, another round of “US-China trade talk optimism.”

Global stocks continued their drift higher to close the week, with the MSCI World Index on track for a second straight week of gains while emerging-market stocks extended their winning streak to seven days, the longest stretch in more than a year, as both China and the U.S. claimed progress in trade talks.

“Buy algos” were encouraged after both China and the US claimed progress in talks to end their trade war, with President Xi Jinping pushing for a rapid conclusion and President Donald Trump talking up prospects for a “monumental” agreement that might be announced within four weeks, although he warned that it would be difficult to allow trade to continue without an agreement. Benchmark bond yields ground higher and the dollar reached a three-week high against the yen before U.S. job data. Better-than expected industrial output data out of Germany and receding fears of a disorderly Brexit also helped perk up sentiment.

While Chinese markets were closed, US equity-index futures advanced alongside Asian stocks, European bourses and Chinese stock futures after a Xinhua report that President Xi Jinping said substantial progress had been made on the text for a trade deal. “The main overnight news, which is positive if not very substantial, is around the U.S.-China trade deal,” said Mizuho strategist Antoine Bouvet. “German industrial orders yesterday added to worries in the manufacturing sector, but industrial production today actually surprised to the upside.”

“There’s a little bit of a risk that it’s a sell-on-the-news event,” Ann Miletti, a fund manager at Wells Fargo Asset Management, said of U.S.-China trade talks. “The devil is really in the details – how good is this deal going to look?”

Europe’s Stoxx 600 traded sideways, shrugging off trade optimism and Brexit news ahead of today’s U.S. payrolls. Eurostoxx 50 is little changed, Markets in Paris and London added 0.1%. German stocks were treading water, with modest gains in basic resources and autos sectors offset by weakness in real estate and telecoms, though the index was on track for its best week since December 2016. German industrial output rose by 0% percent in February, better than the 0.5% expected, as mild weather helped a surge in construction activity. But manufacturing production dipped as Germany continues to suffer from trade friction with China and Brexit angst after narrowly avoiding recession last year. Leading economic institutes slashed their forecasts for 2019 growth on Thursday and warned a long-term upswing had come to an end.

Earlier in the session, trading volumes throughout Asia were muted, with cash markets in China and Hong Kong shut for a holiday.

S&P futures pointed to modest gains for stocks on Friday, with S&P 500 edging up 0.16% to 2,887, only 1.75% away from its Sept 2019 closing high, which is prompting some caution: “Share markets have run hard and fast from their December lows and are vulnerable to a short-term pullback,” said Shane Oliver, head of investment strategy at AMP Capital. “But valuations are okay, global growth is expected to improve into the second half of the year, monetary and fiscal policy has become more supportive of markets and the trade war threat is receding.”

Attention now turns to the March payrolls report, which is forecast to rebound to 177,000 in March, following February’s surprisingly low 20,000 rise. As Jim Reid writes overnight, “how markets fare today will likely be dictated by the March employment report.”

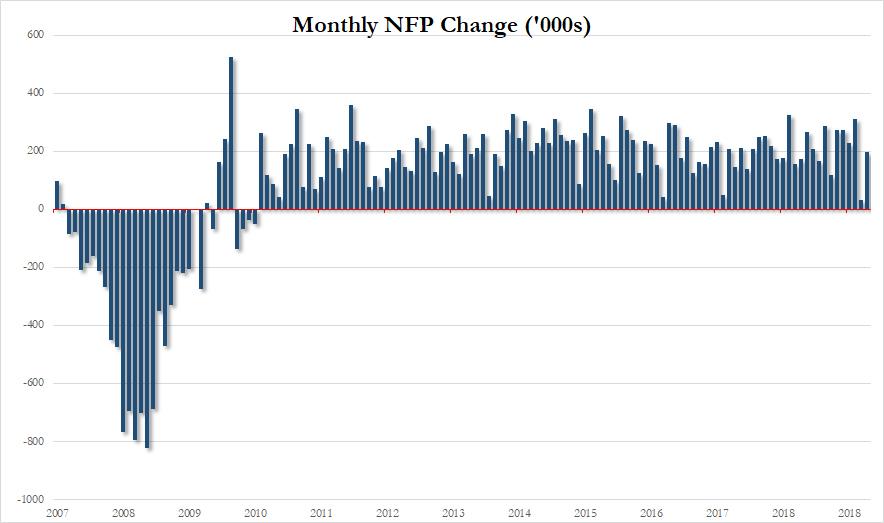

A reminder that last month we had that huge plunge in payroll growth to just +20k which was the lowest since September 2017 and the third lowest since January 2011. Expectations are for a bounce back 177k print however that is still below the average of the last three (186k), six (190k) and twelve (212k) months. To be fair there is a decent range on the Bloomberg survey at 110k to 277k. Our US economists have a 165k forecast and they note that the hostile weather in mid-March also raises the risk of another downside miss. As for earnings, the consensus is for a solid +0.3% mom reading (DB at +0.2% mom) which should keep the annual rate at +3.4% yoy. The unemployment rate is also expected to hold steady at 3.8%. So lots to look out for as ever.

In focus will be hourly earnings, which climbed to 3.4% in February, the fastest pace since April 2009. Hopes for a solid number were boosted by data on jobless claims, which fell to a 50-year low last week. With traders betting that the next Fed move will be to lower interest rates, not raise them, the fixed-income market could be affected by any signs of wage strength in today’s report.

In other overnight news, President Trump commented that there would be a 25% tariff on car imports from Mexico if he decides to apply tariffs but also said that Mexico has done good regarding the border during past 4 days, while he added that he did not say the border would stay open for a year but that he would place tariffs first. Trump also confirmed he has recommended Herman Cain to the Fed board.

In the latest Brexit news, UK PM May sent a letter to EU’s Tusk proposing an extension for Brexit until 30th June 2019 with potential to terminate early should a deal be ratified before then. Letter states that the UK will begin to prepare to host European elections and that the UK needs to provide a clear plan by Tuesday (the day before the EU Council meeting). Separately, there were reports EU’s Tusk is preparing to offer the UK a 12-month flexible extension, according to a senior EU source; which has since been confirmd by a Senior EU Official. EU Council President Tusk’s proposal of a year long extension to Brexit would permit the UK to leave as early as 1st July if the UK has passed with Withdrawal Agreement by that point, according to a senior EU official.

The optimistic mood again weighed on safe-haven debt, with government bond yields in Europe and the United States rising in early trade. 10 Year US and German bond yields climbed to a two-week high, the latter just above zero, the former rising to 2.535%.

In currencies, the progress on trade was enough to keep the safe-haven yen under pressure and lift the dollar to a three-week high of 111.79. The dollar steadied before the release of U.S. payrolls data, while sterling initially advanced after the U.K. asked the EU to kick the Brexit can down the road once again, only to sink below Thursday lows after.

An index of developing-nation currencies was little changed, with Indonesia’s rupiah leading gains versus the dollar along with South Africa’s rand and Mexico’s peso. President Xi Jinping reportedly said substantial progress had been made on the text for a trade deal, raising hopes of a swift end to the dispute that has weighed on the global economy

In commodities, Brent crude futures were off 23 cents at $69.17 after touching $70 a barrel for the first time since November, as expectations of tight global supply outweighed rising U.S. production. WTI priced at $62.16 a barrel. Spot gold dipped to $1,291.61 per ounce but held above a near 10-week low hit overnight.

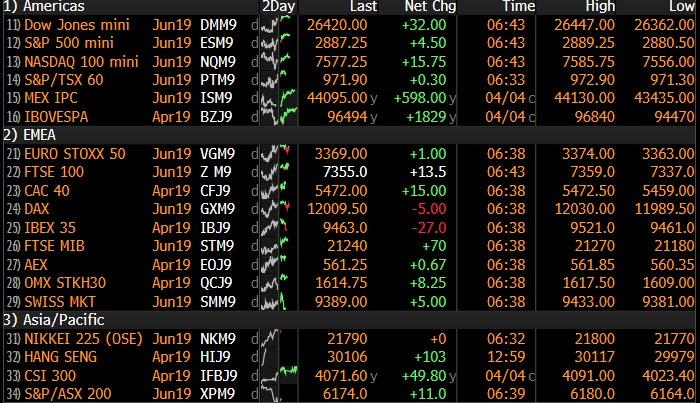

Market Snapshot

- S&P 500 futures up 0.2% to 2,887.00

- STOXX Europe 600 unchanged at 387.88

- MXAP up 0.02% to 162.40

- MXAPJ down 0.1% to 538.85

- Nikkei up 0.4% to 21,807.50

- Topix up 0.4% to 1,625.75

- Hang Seng Index down 0.2% to 29,936.32

- Shanghai Composite up 0.9% to 3,246.57

- Sensex up 0.3% to 38,802.54

- Australia S&P/ASX 200 down 0.8% to 6,181.26

- Kospi up 0.1% to 2,209.61

- German 10Y yield rose 1.5 bps to 0.009%

- Euro up 0.05% to $1.1227

- Brent Futures down 0.5% to $69.08/bbl

- Italian 10Y yield fell 2.1 bps to 2.165%

- Spanish 10Y yield rose 0.7 bps to 1.117%

- Brent Futures down 0.1% to $69.35/bbl

- Gold spot down 0.2% to $1,289.19

- U.S. Dollar Index little changed at 97.27

Top Overnight News

- Through a message passed to U.S. President Donald Trump via Chinese Vice Premier Liu He, President Xi called for an early conclusion to trade negotiations, the official Xinhua News Agency said. Liu, who took part in talks this week in Washington, said the two sides had “reached new consensus on such important issues as the text” of a trade agreement, according to Xinhua

- A potential U.S.- China trade agreement could face challenges from other World Trade Organization members depending on the details and whether other nations feel it unfairly hurts them, the group’s chief said.

- May’s request for another Brexit postponement sets up a battle with the EU ahead of a key summit next week. Tusk favors a 12-month extension that could be ended early if a withdrawal deal is approved before the year is up, according to an EU official

- German Chancellor Angela Merkel reiterated her vow to do everything she could to avoid a no-deal Brexit, while maintaining solidarity with Ireland

- Cleveland Fed President Loretta Mester, answering a question about the likelihood the next policy move will be a cut rather than a hike, says “I’m biased to either keeping rates where they are or moving them up a little bit”

- President Trump intends to nominate Herman Cain, the former pizza company executive who ran for the 2012 Republican presidential nomination, for a seat on the Fed Board, according to people familiar

- China has drafted rules to regulate the nation’s $109 billion peer-to-peer lending sector as part of a plan to clean up the market by 2020, according to a document seen by Bloomberg

- Norway’s $1 trillion sovereign wealth fund got the go-ahead to cut emerging markets from its fixed income holdings as part of an overhaul of its $310 billion bond portfolio

- Italy’s cabinet approved a series of measures to boost the economy, even as the Treasury prepares to slash growth forecasts for the year and raise its projected budget deficit

Asian equity markets traded slightly mixed following a similar indecisive lead from Wall St. as US-China trade optimism was partially offset by pre-NFP caution and holiday thinned conditions from closures across the Greater China region. ASX 200 (-0.8%) was the laggard and extended on its pullback from 7-month highs, with the declines led by tech which mirrored the underperformance of the sector stateside. Nikkei 225 (+0.4%) was positive with the index underpinned by favourable currency moves and trade-related hopes, while the KOSPI (+0.1%) remained afloat as index giant Samsung Electronics weathered a miss on its Q1 earnings guidance. Chinese markets were shut for national holidays although there was certainly no lack of relevant news flow with trade talks remaining in the limelight, in which leaders from both sides noted substantial progress was made and President Trump suggested that a deal could be announced in the next 4 weeks. Finally, 10yr JGBs were pressured amid spill-over selling from T-notes and as stocks in Japan remained afloat, while the BoJ were only present in the market today for T-bills. US President Trump said rapid progress is being made in trade discussions with China and we’re getting very close to trade deal, but added it is not yet made and could be announced in the next 4 weeks, maybe more or less. Furthermore, US President Trump said he will hold a summit with Chinese President XI in Washington if there is a deal and that he will discuss tariffs with Chinese Vice Premier Liu He, while he cited tariffs as well as IP theft when asked about sticking points.

Top Asian News

- Jokowi Gambles on Rural Voters as Discontent Grows in Cities

- India Didn’t Shoot Down Pakistan’s F-16, U.S. Magazine Says

- Energy Tycoon $1 Billion Richer as Vietnam Bet Boosts Stock

- Lucrative Coal Trade Beckons Those Bold Enough to Test China

A cautious start for European equities [Euro Stoxx 50 Unch] after a relatively mixed Asia-Pac session, as is usually the case ahead of US jobs data. Italy’s FTSE MIB (+0.4%) modestly outperforms its peers as Saipem (+3.0%) rose to the top of the Stoxx 600 on the back of a positive JP Morgan broker move. Sectors are mixed with no clear standout.

Top European News

- May Writes to Tusk Seeking to Delay Brexit to June 30

- France Backs Banking Consolidation Amid German Merger Talks

- Swedbank Chairman Quits as Scandal Rips Through Top Ranks

- There Is an Art to Issuing a ‘Good’ Profit Warning, RBC Argues

In FX, AUD/NZD/GBP/EUR all bucked the broader trend of consolidation and sideways trading into NFP and Canada’s latest employment report, albeit not by much in terms of moves vs the Greenback. However, the Aussie has extended its rebound from post-RBA lows and outperformance vs the Kiwi in the process. Aud/Usd has retested recent 0.7100+ peaks as Aud/Nzd advances through 1.0550 towards 1.0575 and Nzd/Usd declines to new early April lows below 0.6740. The catalysts, more momentum towards a US-China trade agreement, per latest reports from Beijing especially, another rise in iron ore prices and a supportive Aussie note from GS that Is going against the grain with an unchanged RBA policy call to support its revised forecasts for Aud/Usd over 3 and 6 month horizons (0.7400 and 0.7500 from 0.7200 and 0.7300 respectively). Recall, the US bank also went long of Aud/Nzd yesterday and decent option expiry interest sits at the 0.7100 strike (1.6 bn). Elsewhere, Cable remains volatile and fixated on Brexit headlines around the 1.3100 handle amidst latest reports about a potential lengthier A 50 extension to mid-year or end March 2020 with a flexible early termination option. Eur/Usd is still rangebound between 1.1200-50 after topping out not far above a 1.1246 Fib again on Thursday, but deriving some underlying support from better than expected German IP data and Italy’s ISTAT suggesting that its leading economic indicator points to signs of a recovery or base. Note also, hefty option expiries may be keeping the headline pair in check, as 2 bn resides between 1.1185-1.1200 and 2.5 bn from 1.1240-50.

- CHF/CAD/JPY – Minimal deviation against the Usd that is equally restrained pre-US and Canadian labour updates, with the DXY firm, but confined between 97.177-331. The Franc is pivoting parity and Loonie straddling 1.3350, while Usd/Jpy is just off a marginal new wtd high of 111.80 having breached its 200 DMA (111.49).

- EM – Contrasting fortunes for regional currencies as the Lira continues to lick wounds amidst the ongoing political contention following local Turkish elections and wrangling with the US over its S-400 order from Russia. Moreover, Usd/Try remains elevated near 5.6000 ahead of next week’s Economic Plan and the next CBRT policy meeting, in contrast to Usd/Zar below 14.1000 and not far from the 100 DMA (14.0625) in wake of SA’s ratings reprieve for the Rand by Moody’s earlier this week.

In commodities, tentative trade in the energy complex as WTI (Unch) and Brent (-0.3%) gear up for this week’s US jobs data. WTI rests just above its 200 DMA at 61.38, whilst its global counterpart straddles just below its 200 DMA at 69.54. Oil is on track for its longest weekly winning streak since the back-end of 2017, overall supported by the output decline in Venezuela coupled with growing hope of a US-Sino trade truce. Crude has advanced around 40% this year thus far as OPEC+ supply curbs counter record high US shale production. As a reminder, tonight will see the release of the Baker Hughes rig count, although price-action may be muted amidst macro-newsflow. Not much price action in the metals complex (thus far) with gold (U/C) treading water around yesterday’s close after briefly breaching its 200 DMA (1283) to the downside yesterday, whilst copper (-0.1%) remains tentative amidst the cautious risk-tone. Finally, Australia’s Port Hedland’s iron ore shipments to China declined by 8% M/M, totalling 30.7mln tonnes vs. 33.5mln tonnes in February after the port was shut for almost 4 days due to cyclones hitting Western Australia.

US Event Calendar

- 8:30am: Change in Nonfarm Payrolls, est. 177,000, prior 20,000

- Unemployment Rate, est. 3.8%, prior 3.8%

- Average Hourly Earnings MoM, est. 0.3%, prior 0.4%; YoY, est. 3.4%, prior 3.4%

- Average Weekly Hours All Employees, est. 34.5, prior 34.4

- 3pm: Consumer Credit, est. $17.0b, prior $17.0b

DB’s Jim Reid concludes the overnight wrap

Good morning from Munich, one of my favourite cities in Europe and not just because Liverpool beat them in the Champions League last month. It always brings back memories when I pass the Bayerischer Hof in Munich as when I was staying there in 2002 on a work trip unbeknown to me Liam Gallagher of Oasis was also there at the same time and evidently required some major dental work after a fracas in the hotel nightclub. It was all over the newspapers on my return. Fortunately I was long tucked up in bed when it happened.

Markets were certainly waiting for something to get their teeth stuck into for most of yesterday as everyone awaited the news of the Trump-China VP Liu He meeting and also held fire ahead of today’s payrolls. The former ended after the US markets closed last night. The officials announced no major breakthrough on trade talks but the direction of travel seems to continue to be positive. Trump did float a potential timeline: four more weeks of talks, then two weeks to schedule and attend a summit with President Xi. He said that IP protections, certain tariffs, and enforcement are all still being negotiated. In the meantime, Chinese President Xi Jinping said that substantial progress has been made in trade talks with the US and called for an early conclusion of the US-China trade text.

Equity markets in the US were already shut by the time those headlines hit however sentiment overnight in Asia is slightly on the positive side with the Nikkei (+0.41%) up and Kospi (+0.04%) flatish. Markets in China and Hong Kong are closed for a holiday. Elsewhere futures on the S&P 500 are up +0.15% and 2y and 10y treasury yields are up c. 1bps this morning.

How markets fare today will likely be dictated by the March employment report in the US this afternoon. A reminder that last month we had that huge plunge in payroll growth to just +20k which was the lowest since September 2017 and the third lowest since January 2011. Expectations are for a bounce back 177k print however that is still below the average of the last three (186k), six (190k) and twelve (212k) months. To be fair there is a decent range on the Bloomberg survey at 110k to 277k. Our US economists have a 165k forecast and they note that the hostile weather in mid-March also raises the risk of another downside miss. As for earnings, the consensus is for a solid +0.3% mom reading (DB at +0.2% mom) which should keep the annual rate at +3.4% yoy. The unemployment rate is also expected to hold steady at 3.8%. So lots to look out for as ever.

Back to yesterday and it wasn’t an overly exciting day in markets with the S&P 500 (+0.21%) advancing a bit as gains for energy and materials were offset by losses for utilities and tech. The index has traded in a tight 0.93% range over the last three sessions, its second tightest of the year. The NASDAQ closed -0.05% to leave the winning run behind at five days with Tesla (-8.23%) doing some of the damage, however the DOW (+0.64%) did outperform helped by gains for Boeing (+2.89%). In Europe the STOXX 600 (-0.27%) faded to a small loss. WTI oil remained tame (-0.58%), capping its narrowest three-day trading range since last September. The moderate risk off lifted bonds with 10y Treasuries down -1.1bps and Bunds (-0.6bps) back into negative territory again. At my Munich dinner last night of 10-15 clients, I asked who thought Germany should take advantage of ultra low yields and borrow 50yr or 100yr money and invest it in their economy. Everyone raised their hands. I thought there would be a more conservative balanced response and was therefore pleasantly surprised.

Elsewhere the USD (+0.20%) was firmer which weighed on some EM currencies. The Turkish lira outperformed, advancing +0.64% (down -0.48% this morning) after Bloomberg reported that the European Bank for Reconstruction and Development as well as the World Bank’s International Finance Corporation are looking at increasing their Turkish NPL portfolios. It wasn’t clear if this was a policy change or just consistent with their standard operating procedure, but the currency rallied sharply on the headlines.

The fact that it’s taken this many paragraphs to get to Brexit suggests that there’s been a dip in the newsflow. Indeed, perhaps fitting of the current state of affairs in Parliament, the most entertaining story was a water leak forcing a debate on tax legislation in the Commons to be suspended yesterday. So a rare chance for MPs to discuss a non-Brexit topic was scuppered by rusty pipes. The only notable Brexit news was the suggestion that any more votes on Brexit proposals might not take place before PM May travels to Brussels next week. That raises the risks that Mrs May goes to Brussels next Wednesday and asks for an extension with no firm plan. That will increase the risks of a hard Brexit a week from today. I still think that’s unlikely but it will put the EU in a difficult position if no progress has been made. Talks between May and Corbyn are ongoing with Tories saying they were “productive” whereas Labour didn’t offer up any descriptive word about them. One gets the sense that both sides realise they have a lot to lose by agreeing a grand bargain however both BBC’s Laura Kuenssberg and ITV’s Robert Peston tweeted last night that their sources suggested the talks are credible and could result in something. It’s possible we’ll learn more this afternoon. Sterling closed -0.62% yesterday as the stakes were raised.

In other news, it’s worth flagging another ECB deposit tiering story yesterday, this time from the FT. The article suggested that the arguments in favour of tiering are building within the ECB camp. The story made the point that the key argument is the increasing likelihood of rates remaining at current low levels for an extended period of time. As such, tiering could be part of a package in which the ECB adjusts its forward guidance to endorse market pricing, which is no hikes until at least later in 2020.

Speaking of the ECB and tiering, the minutes from the March meeting which were out yesterday didn’t offer much in the way of new hints. The text revealed that “concerns were voiced that over time the effects of persistently low rates could depress banks’ interest margins and profitability with negative effects on bank intermediation and financial stability in the longer run. It was recalled that the consequences of low rates differed across the maturity spectrum and across banks, depending on their business models and the structure of their assets and liabilities”. Crucially, there was no direct reference to tiering.

As a final point on Europe, there were a couple of GDP downgrade headlines which hit the screens early yesterday. The first was Germany where “institutes” revised down their 2019 growth forecast to 0.8% from 1.9%. However it turned out that the 1.9% was from back in September so it wasn’t all that surprising given the six months of slowing data since then, and compares to the IFO forecast at 0.6%. Shortly after, Bloomberg reported that the Italian Treasury is set to slash its 2019 growth forecast to 0.1% from a 1.0% forecast previously. Again though, this is closer to where the market is. So both headlines were really more noise than anything else.

Turning quickly to yesterday’s Fedspeak, where the overall message was consistent with the existing policy stance. NY Fed President Williams said that “policy is in the right place” and that growth should slow to around 2% this year. Separately, two of the more hawkish committee members, Cleveland’s Mester and Philadelphia’s Harker, maintained their positions for a pause in policy for now, with Mester arguing for “no urgency to change our policy stance” and Harker saying “I continue to be in wait-and-see mode.” They both left the door open for future hikes though. Mester said if the economy evolves as she expects, then “rates may need to move a bit higher” and Harker said “my outlook for rates remains, at most, one hike for 2019 and one for 2020.” Finally, Bloomberg reported that President Trump plans to nominate former presidential candidate Herman Cain for one of the vacant Fed Governorships. He would need to be confirmed by the senate.

Wrapping up the few data prints that were out yesterday. In the US claims continued their trend of reversing the Q4 spike, dropping 10k to 202k (vs. 215k expected) and in fact to a new 49-year low. The four-week moving average is now down to 214k and the lowest since October. Prior to this, we had another disappointing factory orders print in Germany where orders fell -4.2% mom versus expectations for a +0.3% mom lift.

Finally to the day ahead now, where this morning we’ve got more data out of Germany with the February industrial production print, followed by the February trade balance print and March house price data and Q4 labour costs data in the UK. The aforementioned March employment report in the US is the highlight today while late this evening we’ll get the February consumer credit print for the US. Away from that, the Fed’s Bostic speaks this evening while the big US banks will today submit their capital plans with stress test results announced in June.

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED //Hang Sang CLOSED BOTH CHINESE HOLIDAY /The Nikkei closed UP 82.55 POINTS OR 0.38%/ Australia’s all ordinaires CLOSED DOWN .79%

/Chinese yuan (ONSHORE) closed UP at 6.7079 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 62.69 dollars per barrel for WTI and 69.52 for Brent. Stocks in Europe OPENED GREEN

ONSHORE YUAN CLOSED UP // LAST AT 6.7079 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7136 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/

3 b JAPAN AFFAIRS

3 C CHINA

Where have we seen this before: yuan and stock futures rise on substantive progress in trade

(courtesy zerohedge)_

US Futures, Yuan Surge As China’s Xi Says “Substantive Progress” Made In Trade Talks

US Futures spiked (along with Treasury yields)…

Along with the Chinese Yuan…

After Xinhua reports that Chinese President Xi Jinping calls for an early conclusion of negotiations on text of China-U.S. economic and trade and agreement.

Via Xinhuanet’s Weibo site (google translation):

Liu He, the Chinese leader of the China-US comprehensive economic dialogue. Liu He first conveyed President Xi Jinping’s sincere regards to President Trump and his message to President Trump.

In his oral letter, Xi Jinping pointed out that over the past month or so, the economic and trade teams of the two sides have conducted intensive consultations in various forms and made new substantive progress on the key issues of the texts of the economic and trade agreements between the two countries.

It is hoped that the economic and trade teams of the two sides will continue to resolve the concerns of both sides in the spirit of mutual respect, equality and mutual benefit, and complete the negotiation of the text of the Sino-US economic and trade agreement as soon as possible.

Under the current situation, the healthy and stable development of Sino-US relations is related to the interests of the Chinese and American peoples and to the interests of the people of all countries in the world.

In particular, we need to play our strategic leadership. I would like to maintain close ties with the President through various means. I believe that under the joint guidance of Mr. and President, China-US relations will surely achieve new and greater progress.

Liu He said that in the past two days, the economic and trade teams of the two sides have conducted fruitful consultations, especially on important issues such as the text of economic and trade agreements. Under the guidance of the consensus of the two heads of state, the two sides will continue to work hard, hold close consultations, make more progress on issues of mutual concern, live up to the major responsibilities of the two heads of state and the people, complete negotiations on economic and trade agreements between the two countries as soon as possible, and promote the two country’s economic and trade relations have developed in a healthy and stable manner.

Trump thanked President Xi Jinping for his oral message and asked Liu He to convey his cordial greetings to President Xi. Trump said that the current US-China relationship is developing well, strong and powerful, and at a historically high level. I am very happy to see that the economic and trade consultations between the two sides have made great progress.

I hope that the economic and trade teams of the two sides will make persistent efforts to solve the remaining problems and strive for an early and comprehensive agreement. This will not only benefit the United States and China but also the whole world. . I look forward to meeting with President Xi after the two sides reached an agreement to witness this great moment. I would also like to pay a special tribute to President Xi for making an important decision on the entire class of fentanyl substances in China. This matter is of great significance to the American people and the US-China anti-drug cooperation.

U.S. trade representatives Wright Hize, Finance Minister Mnuchin, Agriculture Minister Perdue, Commerce Secretary Ross, Presidential Senior Advisor Kushner and other US officials attended the meeting.

This comes just a few short hours after President Trump remarked that the trade deal was not done and would likely need an additional two weeks over the remaining four weeks already scheduled for negotiation.

end

4/EUROPEAN AFFAIRS

i)BREXIT/EU/

Theresa May has formally requested another short term Article 50 extension letter to Donald Tusk asking the EU 27 to delay Britain’s exit until June 30. She conditions that the UK would participate in the upcoming EU parliamentary elections. She states that the UK could leave earlier if it passes her deal.

(courtesy zerohedge)

May Request Another Brexit Extension Until June 30

Theresa May has formally requested another short-term Article 50 extension in a letter to Donald Tusk, asking the EU27 to delay Britain;’s exit date until June 30 on the condition that the UK would participate in the upcoming EU parliamentary elections, while leaving open the possibility that the UK could leave earlier if it manages to pass her deal.

When May first requested a short term extension last month, the EU27 rejected her proposed date of June 30, and instead countered with an offer for a two-week extension, with a longer delay contingent on whether Parliament would manage to pass the withdrawal agreement. At the time, observers whined that a two-week extension wasn’t long enough, and…well…

Steven Swinford

✔@Steven_Swinford

Here it is:

The PM’s letter to Donald Tusk in which she ‘reluctantly’ requests an extension of Article 50 to 30 June, 2019

As analysts scramble to read the tea leaves, a team from Credit Agricole reasoned that the EU probably wouldn’t accept a short-term delay, citing the stated preference for a longer extension by some key officials.

“We will have to wait until next week to see whether we will get an extension at all,” said strategist Valentin Marinov.

“GBP is a bit weaker on the back of that potentially because the request for a lengthier extension is seen as a recognition that May may not be able to get the Withdrawal Agreement through Parliament next week as hoped.”

According to Buzzfeed, Brussels suspects May’s talks with opposition leader Jeremy Corbyn are likely to fail, and that the PM will instead be forced to hold another series of ‘indicative votes’ to try and suss out a plan that would actually have a chance of passing in the increasingly divided commons.

The extension could be until the end of the year – or even as late as March 2020.

Ultimately, whether to accept May’s request must be decided by the EU27 at next week’s summit.

The decision on whether to grant a long extension and its terms will ultimately be one for the 27 leaders when they meet in Brussels on 10 April. However, in the lead up to next week’s summit, some governments, including France, have adopted a tougher stance than others on the prospect of granting the UK a long extension to simply keep debating its options, an EU27 leader told BuzzFeed News.

One senior official, quoting Tusk, said the UK needs a “long but flexible extension” – or “flextension.”

A senior EU official quoted Tusk saying: “The only reasonable way out would be a long but flexible extension. I would call it a ‘flextension’.

How would it work in practice? We could give the UK a year-long extension, automatically terminated once the Withdrawal Agreement has been accepted and ratified by the House of Commons.”

The EU official added: “And even if this were not possible, then the UK would still have enough time to rethink its Brexit strategy. Short extension if possible and a long one if necessary. It seems to be a good scenario for both sides, as it gives the UK all the necessary flexibility, while avoiding the need to meet every few weeks to further discuss Brexit extensions.”

Still, according to reports earlier in the week, the EU wants another extension to be accompanied by commitments and a “gentleman’s agreement” with the UK that it will hold the parliamentary vote, and that May would continue to push for her thrice-rejected withdrawal agreement.

As the bloc debates May’s proposal, it’s worth remembering that any extension would need to be approved by the entire EU27. That leaves plenty of room for one reluctant party to send Britain crashing out of the EU at the end of the summit.

end

Graham Summers points out that the ECB is going to have negative rates for quite some time. He is also warning that the USA is heading in that direction

(courtesy Graham Summers)

Why US-Based Investors Should Be Terrified About What the ECB Admitted About NIRP

As I have been warning for years, Central Banks CANNOT normalize the Everything Bubble they created between 2008 and 2016.

Last week, yet another major Central Bank confirmed that I was correct. In this particular case, it was the European Central Bank (ECB).

The ECB first cut interest rates to NEGATIVE in 2014. It then lowered them an additional three times to -0.4% in 2016.

With negative interest rates, this means that EU banks are forced to PAY to sit in cash. Suffice to say, this has been a major drain on EU bank profits.

The ECB was able to pull this off by promising this was only an Emergency Situation, however it’s now been three years and the ECB has yet to raise rates even once. In fact, the ECB is now revealing it will probably NEVER be able to bring rates back to positive.

Last week, ECB President Mario Draghi revealed that the ECB is current analyzing whether or not to implement a “tiered deposit rate” through which certain banks wouldn’t have to pay as much interest for sitting in cash.

This was an implicit admission that rates will have to stay NEGATIVE for a long time… possibly forever.

A so-called tiered deposit rate would mean banks are exempted in part from paying the ECB’s 0.40 percent annual charge on their excess reserves, boosting their profits as they struggle with an unexpected growth slowdown…