GOLD: $1292.00 UP $2.10 (COMEX TO COMEX CLOSING)

Silver: $15.02 UP 11 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1291.35

silver: $15.00

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING:6/49

EXCHANGE: COMEX

CONTRACT: APRIL 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,288.600000000 USD

INTENT DATE: 04/11/2019 DELIVERY DATE: 04/15/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 H HSBC 32

657 C MORGAN STANLEY 1

657 H MORGAN STANLEY 42

661 C JP MORGAN 6

737 C ADVANTAGE 7 10

____________________________________________________________________________________________

TOTAL: 49 49

MONTH TO DATE: 4,211

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 49 NOTICE(S) FOR 4900 OZ (.1524 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 4211 NOTICES FOR 421,100 OZ (13.0979 TONNES)

SILVER

FOR APRIL

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR NIL OZ/

total number of notices filed so far this month: 773 for 3,865,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

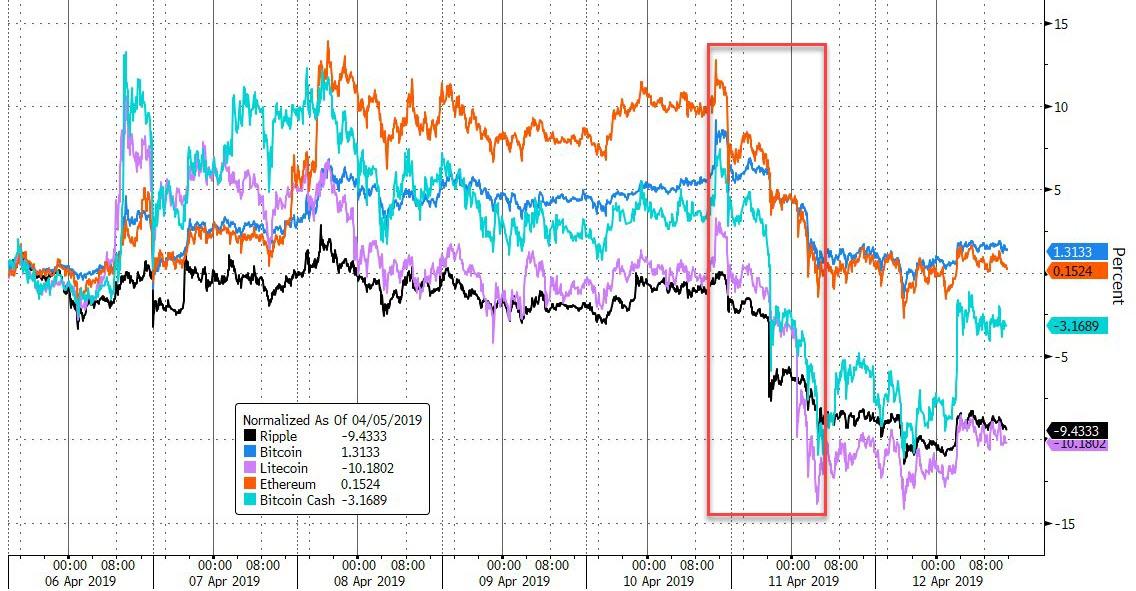

Bitcoin: OPENING MORNING TRADE :$5004 UP $33

Bitcoin: FINAL EVENING TRADE: $5051 UP $24

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY AN ATMOSPHERIC SIZED 8439 CONTRACTS FROM 211,404 UP TO 219,843 DESPITE YESTERDAY’S HUGE 37 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE MUST HAVE HAD CONSIDERABLE SHORT COVERING AGAIN TODAY. NO DOUBT THAT A GOOD PERCENTAGE OF THE RISE AT THE COMEX WAS DUE TO THE SPREADERS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 2054 FOR MAY, 0 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2054 CONTRACTS. WITH THE TRANSFER OF 2054 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2054 EFP CONTRACTS TRANSLATES INTO 6.529 MILLION OZ ACCOMPANYING:

1.THE 37 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

AND NOW 3.870 MILLION OZ STANDING FOR SILVER IN APRIL.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

12,529 CONTRACTS (FOR 10 TRADING DAYS TOTAL 12,529 CONTRACTS) OR 62.65 MILLION OZ: (AVERAGE PER DAY: 1253 CONTRACTS OR 6.265 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 62.65 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 8.94% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 630,82 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 8439 DESPITE THE HUGE 37 CENT FALL IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2054 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED AN ATMOSPHERIC SIZED: 10,493 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2054 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 8951 OI COMEX CONTRACTS. AND ALL OF THIS HUMONGOUS DEMAND HAPPENED WITH A 37 CENT FALL IN PRICE OF SILVER ???? AND A CLOSING PRICE OF $14.91 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.102 BILLION OZ TO BE EXACT or 157% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ AND NOW APRIL AT 3.870 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL AND THIS TIME BY A VERY STRONG SIZED 7518 CONTRACTS, TO 447,425 WITH THE DROP IN THE COMEX GOLD PRICE/(A FALL IN PRICE OF $19.85//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUMONGOUS SIZED 12165 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 12,165 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020l 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 447,425. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY STRONG GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4,647 CONTRACTS: 7518 OI CONTRACTS DECREASED AT THE COMEX AND 12,165 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 4647 CONTRACTS OR 464700 OZ OR 14.45 TONNES. YESTERDAY WE HAD A HUGE FALL IN THE PRICE OF GOLD TO THE TUNE OF $19.85….AND YET WITH THAT, WE HAD A HUGE GAIN IN TONNAGE OF 14.45 TONNES!!!!!!.???

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 56,736 CONTRACTS OR 5,673,600 OR 176.47 TONNES (10 TRADING DAYS AND THUS AVERAGING: 5674 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAYS IN TONNES: 176.47 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 176.47/3550 x 100% TONNES = 4.97% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1552.07 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A VERY STRONG SIZED DECREASE IN OI AT THE COMEX OF 7518 WITH THE LOSS IN PRICING ($19.85) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A HUMONGOUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 12,165 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 12,165 EFP CONTRACTS ISSUED, WE HAD A GOOD GAIN OF 4,647 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

12,165 CONTRACTS MOVE TO LONDON AND 7518 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 14.45 TONNES). ..AND ALL OF THIS VERY STRONG DEMAND OCCURRED WITH A HUGE FALL IN PRICE OF $19.85 IN YESTERDAY’S TRADING AT THE COMEX????

we had: 49 notice(s) filed upon for 4900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD up $2.10 TODAY

I wrote the following yesterday:

“NO CHANGE TODAY, BUT I WILL EXPECT A HUGE WITHDRAWAL TOMORROW”

I am totally shocked: no withdrawal as gold inventory remains the same:

INVENTORY RESTS AT 757.85 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 37 CENTS TODAY:

A BIG CHANGES IN SILVER INVENTORY AT THE SLV

A DEPOSIT OF 750,000 OZ BUT NOT DOUBT THAT THEY WILL REMOVE THAT LATER TONIGHT DUE TO THE RAID.

/INVENTORY RESTS AT 309.917 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY AN ATMOSPHERIC SIZED 8439 CONTRACTS from 211,404 UP TO 219,843 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET….. I WROTE THE FOLLOWING ON THURSDAY AND FRIDAY:

“YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF APRIL BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

AND TODAY WAS NO DIFFERENT WITH THE RISE IN OPEN INTEREST AS WE ARE HEADING INTO AN ACTIVE DELIVERY MONTH FOR SILVER..NO DOUBT A CONSIDERABLE AMOUNT OF THE INCREASE IN OPEN INTEREST WAS DUE TO SPREADERS.

we now have the COT report and scroll down to see spreading and you will see the gain in spreading of a net: 1301 contracts.

this report is from April through to April 9 when spreading is just beginning to mount. Next week you will see a much higher number of spreading as the oI in silver advances.

| Silver COT Report – Futures | |||||||

| Large Speculators | Commercial | Total | |||||

| Long | Short | Spreading | Long | Short | Long | Short | |

| 76,410 | 59,992 | 19,044 | 78,785 | 116,547 | 174,239 | 195,583 | |

| -2,583 | -2,218 | 1,301 | 6,409 | 9,813 | 5,127 | 8,896 | |

| Traders | |||||||

| 108 | 61 | 57 | 42 | 36 | 181 | 126 | |

| Small Speculators | |||||||

| Long | Short | Open Interest | |||||

| 34,545 | 13,201 | 208,784 | |||||

| 4,065 | 296 | 9,192 | |||||

| non reportable positions | Change from the previous reporting period | ||||||

| COT Silver Report – Positions as of | Tuesday, April 9, 2019 | ||||||

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 2054 FOR MAY AND JULY: 0 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2054 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 8439 CONTRACTS TO THE 2054 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF 10,493 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 55.03 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH. AND NOW 3.870 MILLION OZ FOR APRIL.

RESULT: A VERY STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 37 CENT FALL IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A SMALL SIZED 2054 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 1.34 POINTS OR 0.04% //Hang Sang CLOSED UP 70.31 POINTS OR .24% /The Nikkei closed UP 159.16 POINTS OR 0.73%/ Australia’s all ordinaires CLOSED UP .84%

/Chinese yuan (ONSHORE) closed UP at 6.7071 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 64.57 dollars per barrel for WTI and 71.66 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.7071 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7114 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA

b) REPORT ON JAPAN

japan has a serious demographic problem as around 25% of heterosexual Japanese adults between the ages of 18 and 39 have NEVER had sex. Thus there are a lot of 40 year old virgins floating around Japan

( zerohedge)

3 China/Chinese affairs

i)The markets around the world go gangbusters as Beijing injects the most ever credit for March.

( zerohedge)

ii)China/uSA

In the latest trade discussion, China might accept a “penalty” for currency violations however it has not been spelt out

(courtesy zerohedge)

4/EUROPEAN AFFAIRS

i)/EU/UK

Already Farage is attracting names to his new BREXIT party. He has 70 candidates for the May European Parliament election to be held May 23.2019

(ZEROHEDGE)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)LIBYA

A good commentary explaining how General Haftar became the strongman in Libya. He is friendly to the USA and he was set to remove the UN’s al_Serraj, the beleaguered Prime Minister of Libya. Once he takes over Libya oil should begin to flow from the country and migrants should return.

( Prashad/Common Dreams)

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning/FOMC

ii)Market data

a)Import prices come in red hot caused by fuel costs increases. China has also brought to the West the most deflation since 2007

( zerohedge)

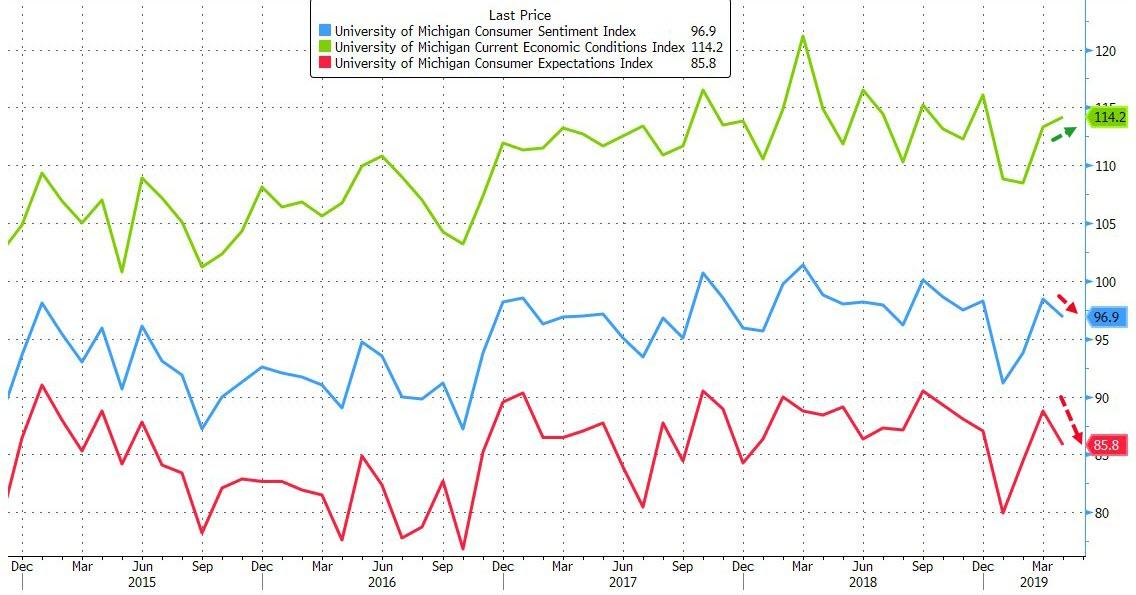

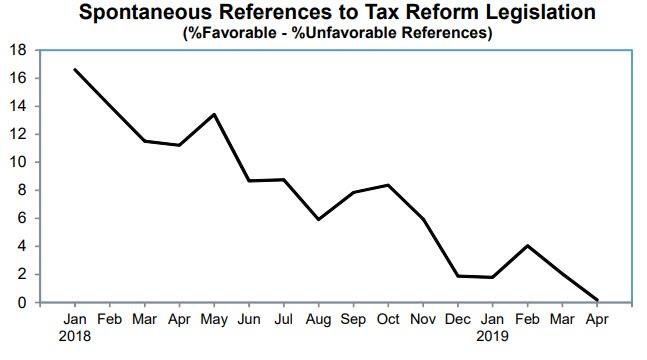

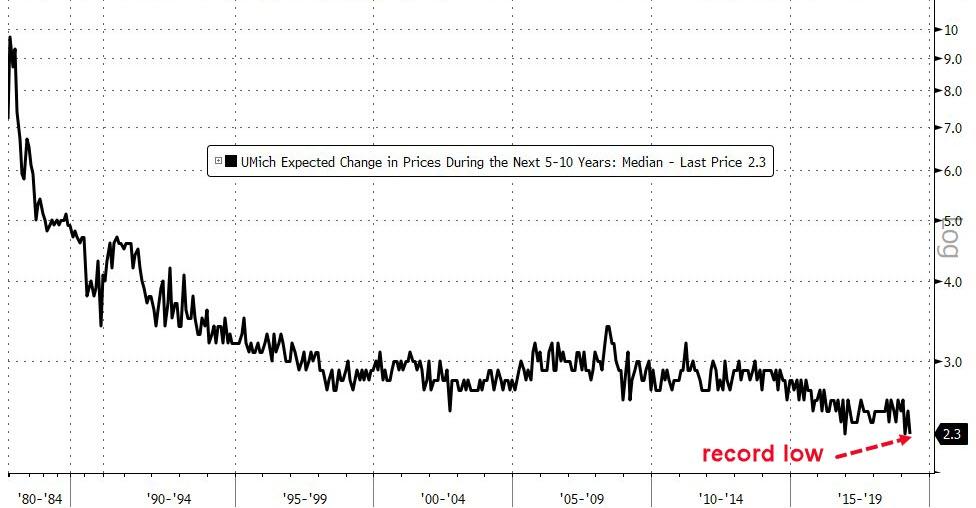

b)Soft data U. of Michigan Sentiment slides

ii)USA ECONOMIC/GENERAL STORIES

a)Meijer comments on the arrest of Assange on dubious charges

( Raul Meijer)_

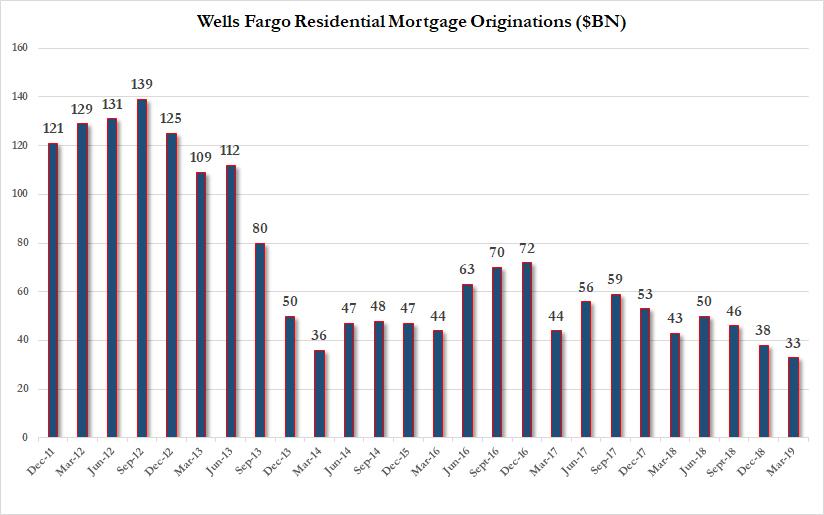

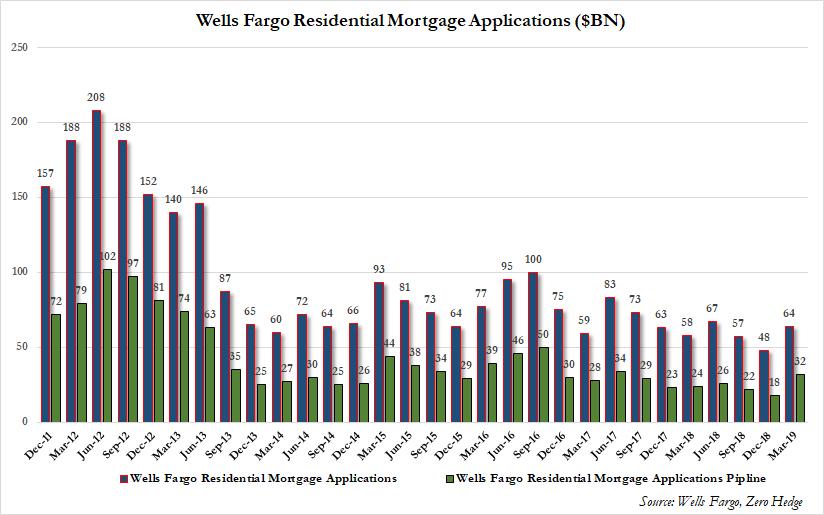

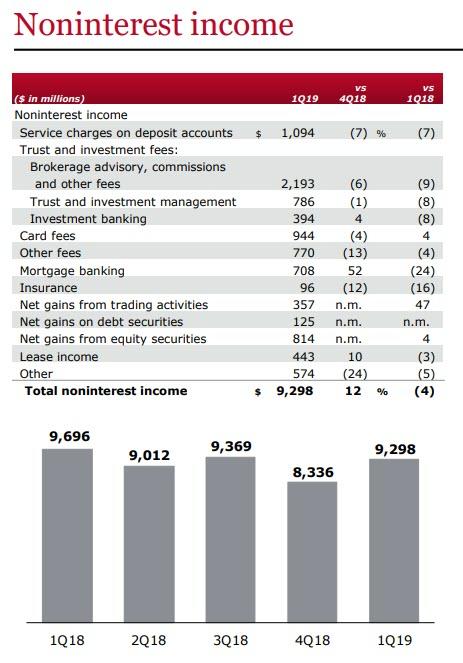

b)Mortgage lending, the bread and butter for Wells continues to disappoint. This number fully reflects the decline in our average American household vs JPMorgan’s strong earnings this morning.

( zerohedge)

iv)SWAMP STORIES

a)Chicago uses Jussie Smollett over his refusal to reimburse the city for the hoax investigation

( zerohedge)

end

Let us head over to the comex:

AFTER APRIL, WE HAVE THE ACTIVE DELIVERY MONTH OF MAY AND HERE THE OI FELL BY 3738 CONTRACTS DOWN TO 107,832. CONTRACTS.. THE NEXT MONTH OF JUNE ADDED 9 CONTRACTS TO TOTAL 98. AFTER JUNE, THE VERY BIG DELIVERY MONTH OF JULY HAD A GAIN OF 9718 CONTRACTS UP TO 74,679 CONTRACTS.

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7071/

//OFFSHORE YUAN: 6.7114 /shanghai bourse CLOSED DOWN 1.34 or 0.04%

HANG SANG CLOSED UP 70.31 points or .24%

2. Nikkei closed UP 159.16 POINTS OR 0.73%

3. Europe stocks OPENED GREEN

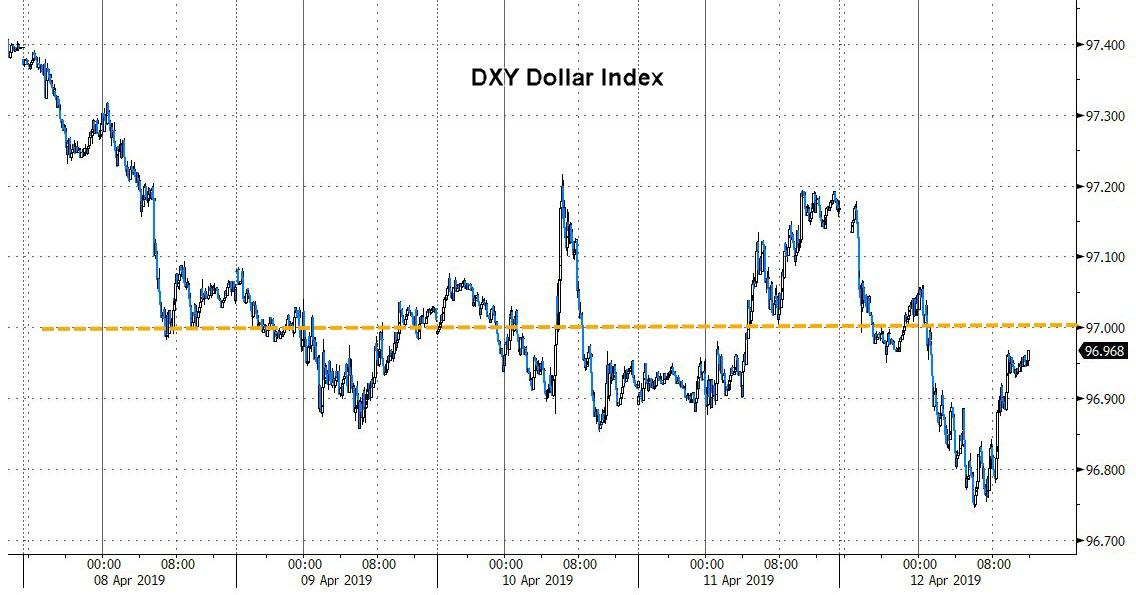

USA dollar index FALLS TO 96.82/Euro RISES TO 1.1318

3b Japan 10 year bond yield: FALLS TO. –.06/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.98/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 64.57 and Brent: 71.66

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +04%/Italian 10 yr bond yield UP to 2.52% /SPAIN 10 YR BOND YIELD UP TO 1.07%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.48: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.31

3k Gold at $1293.20 silver at:15.05 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 47/100 in roubles/dollar) 64.15

3m oil into the 64 dollar handle for WTI and 71 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.98 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0006 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1321 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.04%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.55% early this morning. Thirty year rate at 2.96%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.7957..GETTING VERY DANGEROUS

S&P Surges Above 2,900 On Chinese Credit Creation Flood, Trade Data Bounce

What was a muted overnight session, with traders wearily awaiting today’s earnings from JPM and Wells, officially starting Q1 earnings season, and with mixed Asian equities prompting a nervous start in Europe, a sharp rebound in Chinese trade data coupled with a surge in Chinese credit creation, bolstered risk assets across the board, helping underpin “signs of resilience” in the global economy, and prompted a broad bid for risk. As a result, S&P futures rallied sharply back above 2,900, the highest since September 2018m ahead of the first major bank earnings in this cycle.

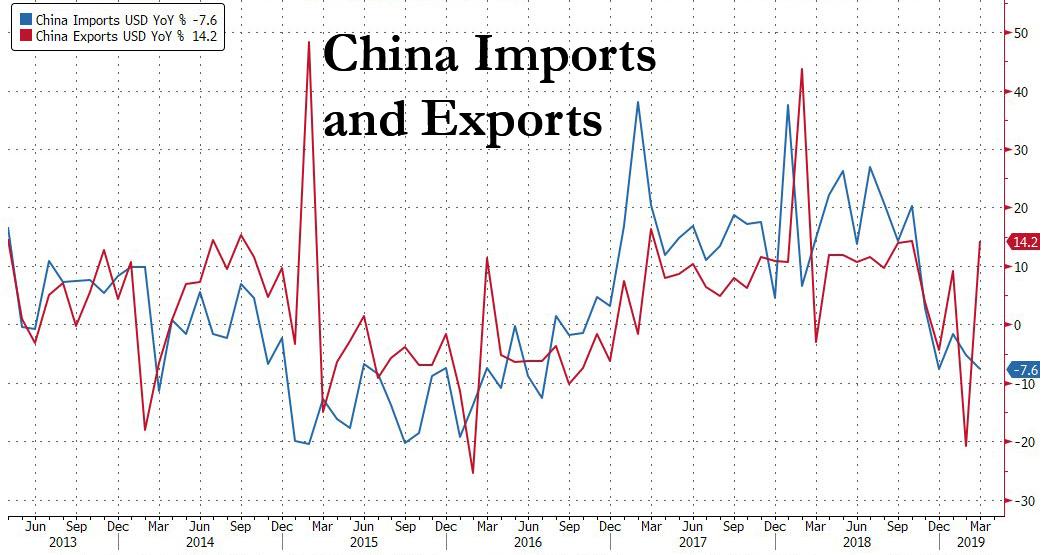

Europe Stoxx 600 Index erased earlier losses and U.S. futures extended gains after China reported a sharp rebound in March exports even as imports shrank for a fourth straight month and at a sharper pace, painting a mixed picture of the economy as trade talks with the United States reach their endgame. Export growth rebounded significantly to +14.2% yoy in March,the strongest growth in five months and well above consensus expectations, and up from -20.8% year-on-year in February, primarily on the Chinese New Year distortion.

Shipments picked up around 3% month-on-month, suggesting some improvement in foreign demand, Julian Evans-Pritchard, senior China economist at Capital Economics, said in a note. But he said exports have yet to fully recover from a sharp slowdown late last year.

Adding to the worries, China’s imports fell more than expected, suggesting its domestic demand remains weak: imports were down 7.6% yoy in March, below consensus. That left the country with a trade surplus of $32.64 billion for the month, much larger than forecasts of $7.05 billion.

Veteran China watchers told Reuters that export gains may be due more to seasonal factors than any sudden turnaround in lackluster global demand, as shipments were expected to jump after long holidays in February.

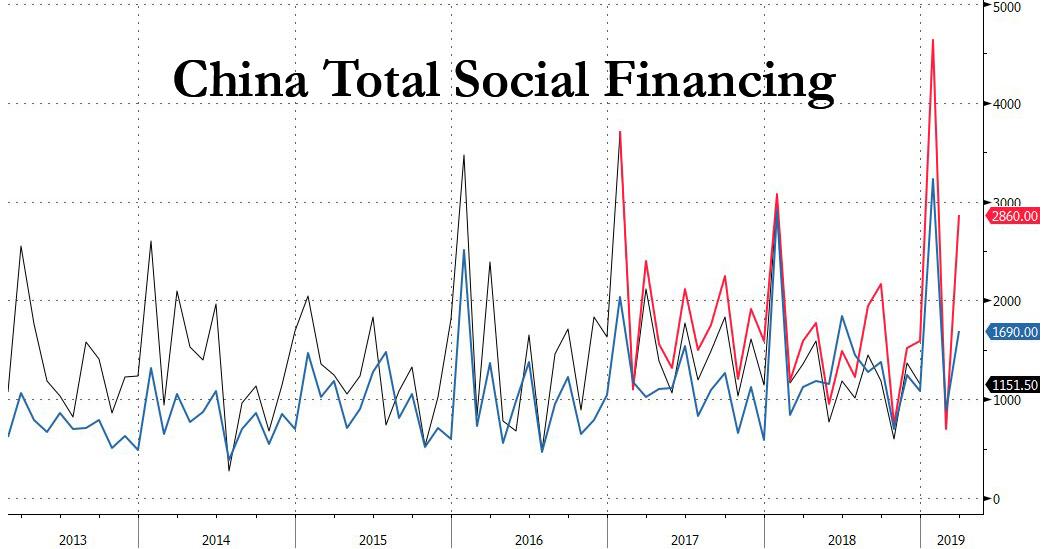

However, the catalyst for the spike in futures and sending the S&P sharply higher from 2894 to above 2,900 what China’s release of far stronger lending growth, signaling a further firming of its nascent economic recovery. The PBOC reported new yuan loans of 1.69 trillion, far above 1.25 trillion estimate, while total aggregate financing in March soared higher 2.86t yuan, the highest March increase on record; smashing the 1.85t yuan estimate, and more than four times the February 703BN yuan increase. In total, March M2 rose +8.6% y/y; also stronger than the est. +8.2%, and well above the February +8%. In other words, it once again appears that China is doing everything in its power to flood the economy with new credit and reversing concerns from the sharp February TSF drop.

China’s gift to markets, and the shift in sentiment came hours before the first-quarter reporting period begins in earnest Friday, with results from JPMorgan Chase & Co. and Wells Fargo & Co. The 10-year Treasury yield climbed above 2.54% and the greenback weakened versus most major currencies, particularly against the euro.

European equities moved back into positive territory, led by autos and basic resource sectors. 10Y German yields rose ~2.5bp back above 0%, with bund and UST futures snapping back towards the week’s lows in decent volume. Gilts followed, with yields up ~2bp across the curve; peripheral and semi-core European spreads tightened in tandem. WTI crude gained over 1%, lifting commodity currencies. Chinese yuan strength providing support for EMFX and metals markets.

Also of note, Chevron announced an agreement to acquire Anadarko for USD 33bln at USD 65/share; will assume estimated net debt of USD 15bln. Anadarko shares soared higher by around 20% in pre-market.

Elsewhere, the euro rose above $1.13 for the first time in more than two weeks, with its more favorable prospects reflected in options across tenors. Cable advanced before paring gains; market focus is on whether U.K. Prime Minister Theresa May can compromise on a post-Brexit customs union with the EU in talks with opposition Labour Party. Aussie rises versus the U.S. dollar; it dipped earlier after the central bank warned of the danger of a sharper global downturn and steeper losses in the local housing market in its Financial Stability Review.

In commodities, West Texas oil futures rose and headed into their sixth consecutive weekly advance, the best streak since 2016. The pound was steady after Prime Minister Theresa May accepted the European Union’s offer to push the Brexit deadline out to October.

Expected data include the University of Michigan Consumer Sentiment Index. JPMorgan, PNC and Wells Fargo are among companies reporting earnings.

Market Snapshot

- S&P 500 futures up 0.4% to 2,902.00

- STOXX Europe 600 up 0.03% to 387.04

- MXAP unchanged at 162.14

- MXAPJ up 0.3% to 541.62

- Nikkei up 0.7% to 21,870.56

- Topix down 0.07% to 1,605.40

- Hang Seng Index up 0.2% to 29,909.76

- Shanghai Composite down 0.04% to 3,188.63

- Sensex up 0.2% to 38,695.19

- Australia S&P/ASX 200 up 0.9% to 6,251.32

- Kospi up 0.4% to 2,233.45

- German 10Y yield rose 1.7 bps to 0.008%

- Euro up 0.4% to $1.1303

- Italian 10Y yield fell 4.2 bps to 2.017%

- Spanish 10Y yield fell 0.4 bps to 1.0%

- Brent futures up 0.8% to $71.37/bbl

- Gold spot little changed at $1,293.38

- U.S. Dollar Index down 0.3% to 96.93

Top Overnight News from Bloomberg

- China’s exports rebounded after the Lunar New Year holiday amid a pickup in trade talks optimism, while a continued slide in imports underscored the fragility of the domestic economy

- Federal Reserve Chairman Jerome Powell asserted the central bank’s independence in remarks to Democratic lawmakers, telling them the Fed doesn’t consider political pressure in any way, according to two people in the room for the closed-door event

- President Donald Trump has said privately that he knows Herman Cain will have trouble getting confirmed to the Federal Reserve Board, people familiar with the matter said Thursday

Asian equity markets traded mixed following an indecisive lead from Wall St. with participants tentative ahead of the latest Chinese trade data and big bank earnings in US. ASX 200 (+0.8%) benefitted from early outperformance in its largest weighted financials sector as top lender CBA gained on the reports it plans to reduce 10k workers, while Nikkei 225 (+0.7%) exporters found solace from favourable currency flows. Elsewhere, Hang Seng (+0.3%) and Shanghai Comp (U/C) lagged amid weakness in tech and gambling names, as well as cautiousness heading into the latest Chinese trade data. Finally, 10yr JGBs were lower as stocks in Japan remained afloat although downside for bonds was stemmed amid the BoJ’s presence in the market for nearly JPY 1tln of JGBs and with SoftBank pricing a record JPY 500bln offering.

Top Asian News

- Philippines Central Bank Chief Says Rate Cut on the Table in May

- Singapore Central Bank Keeps Policy Settings as Growth Slows

- Arcelor’s $6 Billion Essar Deal Stymied by Fight Between Lenders

- Another Warning on Asia’s $4 Trillion Stock Rally Is Flashing

European equities are marginally higher thus far [Eurostoxx 50 +0.2%] after having erased losses seen at the open. Broad-based gains are being seen across major bourses given the recent upturn of risk appetite wherein DAX breached 12k to the upside. Similarly, E-mini Jun’19 futures reclaimed the 2900 level ahead of the all time high just under 2940, last seen in October 2018. Back to Europe, sectors are mixed with outperformance in material names given the spike higher in sentiment-driven base metals. In terms of notable movers, Plus500 (-25%) fell over 40% at one point after reporting an 82% drop in revenue Y/Y, with IG Group (-3.0%) dragged lower in sympathy. Finally, markets are awaiting earnings from JP Morgan (11:55BST) and Wells Fargo (13:00BST) to kick off US earnings season.

Top European News

- Thomas Cook May Have Inadvertently Breached Borrowing Limits

- Stadler Rail Soars in Swiss Trading Debut After $1.3 Billion IPO

- Carl Zeiss Meditec Boosts Full Year Ebit Margin Forecast

- Plus500 Plummets After Losing $28 Million on Clients’ Bets

In FX, Eur/Usd and Usd/Jpy are both testing big figure levels, at 1.1300 and 112.00 respectively where decent option expiries lie (1.2 bn and 1.1 bn), but the move appears to be M&A driven and via the Eur/Jpy cross that spiked through 126.00 at the Tokyo fix overnight. Specifically, a 3 bn buy order is said to have been filled between 125.70 and 126.29, with the proceeds touted to be related to MUFJ’s purchase of a DZ Bank unit. Note, Eur/Jpy has now extended gains to circa 126.60 and the single currency is seeing spill-over buying across the board to around 1.1310 vs the Dollar and 0.8656 against Sterling where stops were expected on a break of 0.8650. Technically, 1.1316 in Eur/Usd may cap the upside as it forms 55 DMA and Fib resistance, while for Usd/Jpy several chart levels reside not far above 112.00, including the 200 WMA (112.04), a Fib (112.06) and the 112.13-16 ytd peak.

- AUD/CAD/NZD – All benefiting from a more risk-on tone unfolding during the EU session and rebounding from lows vs their US counterpart, with the Aussie retesting 0.7150+ and Loonie paring losses from 1.3390 through 1.3350, but the Kiwi hampered to a degree by some weak NZ data overnight as it falls short of 0.6750. Note, Aud/Usd is now back within the realms of 1 bn expiries between 0.7150-55, as the DXY slips back under 97.000 again, albeit mainly due to the aforementioned Eur’s ascent and its biggest weighting in the index.

- CHF/GBP – Also firmer vs the Greenback, as the Franc pares more losses from multi-week lows and inches closer to parity and Cable retains the bulk of its Brexit extension optimism within a 1.3050-80 range, but remains toppy on approaches to 1.3100 or just above given resistance around earlier April highs.

- EM – Usd/Try has advanced further amidst the political turmoil and uncertainty over recent regional elections as the official Board has deferred a decision on a recount in one area of Istanbul that the ruling AK Party is contesting. The Lira lurched down below 5.8100 at one stage and closer to lows seen last month around 5.8490.

In commodities, WTI and Brent recently received a bout of demand as risk-on sentiment took the wheel, wherein the former reclaimed USD 64/bbl whilst the latter gained more ground above USD 71/bbl. Oil is poised for its third consecutive week of gains, as the benchmarks price in potential supply disruptions emanating from Libyan tensions. NOC Head Sanala warned that a renewal of fighting could wipe out the nation’s crude production which stood at 1.1mln BPD in March, according to secondary sources. Elsewhere, Europe’s largest oil refinery, Shell’s 404K BPD Pernis remains restricted at 65% of its normal output amid strikes conducted by a Dutch trade union which is expected to last until at least Monday. Finally, China’s trade report noted that the country’s crude oil imports in the first quarter rose 8.2% Y/Y, although March imports fell to the lowest since 2018. In the metals complex, gold remains below the USD 1300/oz level after having lost the mark as the Greenback recouped some recent losses. Elsewhere, copper prices received a boost from the risk appetite around the market. The red metal breached its 100 DMA to the upside at 2.8974/lb before briefly trading above the 2.950/lb level. Libya NOC chief said oil and gas exports face biggest threat since 2011 given the recent fighting, subsequently stating that a renewal of fighting could wipe out the nations crude production

US Event Calendar

- 8:30am: Import Price Index MoM, est. 0.4%, prior 0.6%; Export Price Index MoM, est. 0.2%, prior 0.6%

- 10am: U. of Mich. Sentiment, est. 98.2, prior 98.4; Current Conditions, prior 113.3; Expectations, prior 88.8

DB’s Jim Reid concludes the overnight wrap

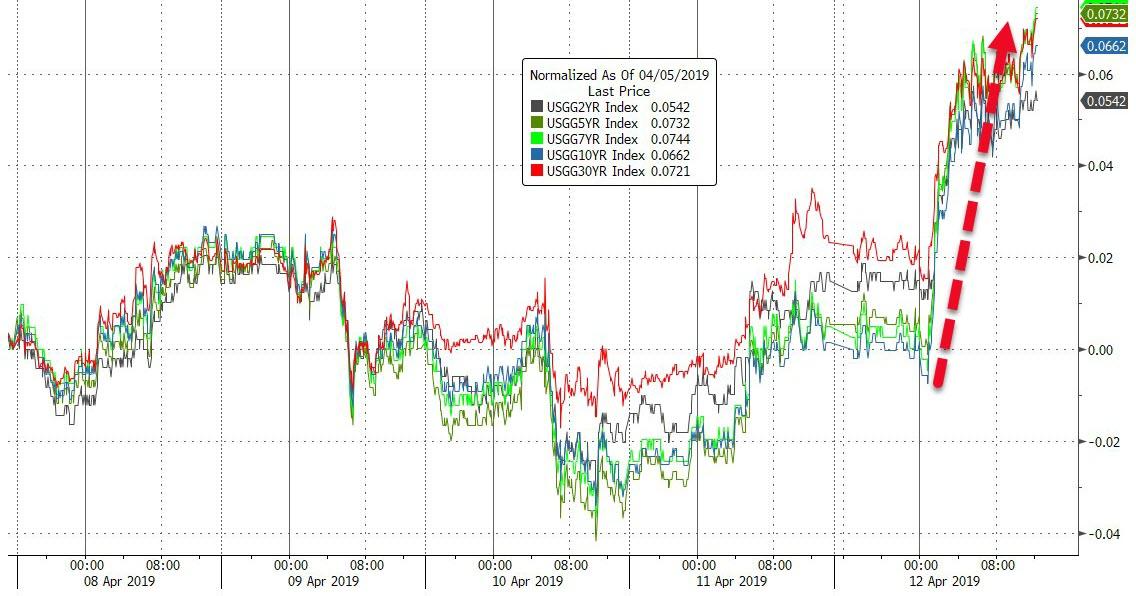

Happy Friday. Given that we barely had a moment to catch our breath on Wednesday the duller last 24 hours in markets has been most appreciated. Volumes in equities were certainly lower than of late. Indeed a bit of a lull in newsflow means we’ve been broadly back to trading a narrow range in equities with the S&P 500 last night closing with the smallest of gains that didn’t quite round up to +0.01% but technically ensured 10 winning days out of 11 now. It was a similar low key story for the DOW but that fell (-0.05%) slightly along with the NASDAQ (-0.21%) while the STOXX 600 nudged up +0.06%. Needless to say vol has been depressed as a result with the VIX (-2.1%) back down to around 13 at the close again yesterday and testing the YTD lows. The V2X in Europe is now at 12.60 and the lowest since August. So Q2 so far has very much been more of the same for vol. It’s worth noting though that we’re due to get results from JP Morgan and Wells Fargo today so there’s always the possibility of a bit of earnings headline news to inject some energy back into markets again. It’s worth noting that banks have been the worst performing sector over the past month. Those results are due out just prior to the US open.

As for other markets yesterday, Treasuries made a bit of 180 degree turn with yields creeping back up towards 2.50% again and closing at 2.497% and up +3.2bps on the day with the move coming despite a softish PPI print beneath the high headline print (more below) which as a reminder followed a similarly soft CPI reading on Wednesday. A fresh 49-year low on jobless claims seemed to be more important. There were some comments from the Fed however. Vice-Chair Clarida spoke and said that the outlook means current policy and the patient stance to further changes remains appropriate. He also said that he’s seeing some slowing in global macro data and that inflation remains muted but that he expects an upturn in global growth later in 2019. So by and large consistent with what he’s said in the past. Later on Williams spoke and said that the US economy still has positive momentum and that worries about a slowdown had receded. He was a bit more dovish on inflation however, and highlighted concerns about inflation expectations heading lower still.

Staying with the Fed, proposed Trump Fed nominee Herman Cain received a fourth GOP Senate rejection yesterday meaning that if Democrats all vote against them his nomination wouldn’t pass. This shows how difficult it will be for Mr Trump to deviate too far from the mainstream in terms of potential Fed board members.

In Europe yesterday we heard from a number of ECB speakers. Visco confirmed that the ECB is discussing and analysing the effects of negative rates and that the precise parameters of the new TLTRO will be clearly defined by June. There was a similar comment from Knot who also added that the next TLTRO needs to be more conservative and less generous relative to the last. Meanwhile Villeroy confirmed that there was a consensus within the ECB to analyse the effects of negative rates for banks. Bunds traded back up at the dizzying heights of -0.009% yesterday (+1.7bps) while BTPs (-4.2bps) were strong following a fairly solid auction.

This morning in Asia markets are trading mixed with the Hang Seng (-0.36%) and Shanghai Comp (-0.44%) down while the Nikkei (+0.44%) and Kospi (+0.10%) are up. Elsewhere, futures on the S&P 500 are up +0.09%. Crude oil prices (WTI +0.31% and Brent +0.25%) are again up this morning after falling yesterday (WTI -1.59% and Brent -1.25% ) as data indicated a 7.03 million-barrel jump in the US crude inventories last week to the highest levels since 2017.

Overnight, Bloomberg reported that Fed Chair Powell made an appearance at a Democratic retreat in Leesburg Virginia to address the concerns of lawmakers around the Fed’s independence. He asserted the Fed’s independence saying that the Fed doesn’t consider political pressure in any way while adding that interest rates are at about the right level given current economic conditions and that the benefits of U.S. economic growth haven’t been as widely spread as the Fed would like. He also endorsed the Earned Income Tax Credit as a way to distribute wealth more widely.

As for the latest on Brexit, there isn’t much to report. Theresa May confirmed in her statement that her government is to push for a deal by the European Parliamentary elections which in theory would enable the UK to leave before June. Opposition leader Corybn talked up the cross party talks while May also indicated that the gap on trade proposals between the Conservatives and Labour is actually fairly minimal. Sterling was fairly directionless yesterday and this morning trades at $1.3075 which is roughly where it started the day yesterday. Elsewhere, The Times reported that the DUP leader Arlene Foster and DUP deputy leader Nigel Dodds met Boris Johnson and members of his team in the commons for 40 minutes on Wednesday.

As for the latest data, fresh off a soft but albeit distorted CPI report on Wednesday, yesterday’s PPI report for March in the US was also disappointing at the core level (0.0% mom vs. +0.2% expected) even if the headline came in well above expectations at 0.6%. It’s worth flagging was the healthcare component, which at +0.07% mom was also soft and therefore will likely result in a drag to the core PCE health care reading. On a more positive note, claims set a new 49-year low record after dropping to 196k. More notably, the four-week average is now down to 207k and also more or less at a 49-year low. It’s possible that there is some distortion due to the timing of Easter this year however the data continues to paint a picture of a sturdy labour market.

Prior to this on the continent we had final March CPI revisions in Germany and France, however no changes were made to the +0.5% mom and +0.9% mom readings for each, respectively.

Finally to the day ahead, where this morning there should be some focus on the February industrial production print for the Euro Area. Expectations are for a -0.5% mom reading however much better than expected readings for France and Italy this week raise the risk of an upside surprise and something more akin to only a marginal decline. Meanwhile in the US this afternoon we’ve got the March import price index reading, and preliminary April University of Michigan consumer sentiment survey. Away from that we’re expecting comments from the BoE’s Carney at the IMF meetings this afternoon, while the ECB’s Praet is also due to speak. The aforementioned US bank earnings will also be worth a watch.

end

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 1.34 POINTS OR 0.04% //Hang Sang CLOSED UP 70.31 POINTS OR .24% /The Nikkei closed UP 159.16 POINTS OR 0.73%/ Australia’s all ordinaires CLOSED UP .84%

/Chinese yuan (ONSHORE) closed UP at 6.7071 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 64.57 dollars per barrel for WTI and 71.66 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.7071 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7114 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/

3 b JAPAN AFFAIRS

japan has a serious demographic problem as around 25% of heterosexual Japanese adults between the ages of 18 and 39 have NEVER had sex. Thus there are a lot of 40 year old virgins floating around Japan

(courtesy zerohedge)

Japan: The Land Of 40-Year-Old Virgins

Japanese adults are not getting laid, according to a new study which found that around 25% of heterosexual Japanese adults between ages 18 and 39 have never had sex.

When broken down by age group, nearly 80% of those under 20 who are virgins, 40% of those between 20-24, and nearly 10% aged 35-39 reporting never having had sex. Of course, this means that if things don’t change – there’s a whole lot of 40-year-old virgins roaming around Japan.

Perhaps unrealistic expectations set by tentacle porn, large-breasted hentai girls and used-panty vending machines have intimidated Japanese women into closing up shop until later in life. Or maybe high levels of soy combined with the #MeToo era have created a population of ultra-feminized men afraid to make the first move?

The study also found that – brace yourself – men who make more money have more sex than those with lower incomes.

“Although the discussion around cause and effect becomes very complex when considering who becomes sexually experienced and who remains a virgin, we show that heterosexual inexperience is at least partly a socioeconomic issue for men. Simply put, money talks,” said lead author Cyrus Ghaznavi.

The decline in sexually active Japanese adults during their reproductive years is worrisome, and the Japanese government is well aware of what’s to come if things don’t change, and soon.

In recent years, local governments have boosted their efforts to pair off heterosexual singles in a bid to reverse the country’s declining fertility rate.

“There seems to be a national push to get people to really think about this issue and feel a sense of urgency,” Choo said.

Furthermore, despite Japan’s multibillion-dollar porn industry, Choo said discussions around porn and sex remain taboo. “Sex is seen as dirty and corrupting in Japan,” Choo said.

“My students can’t use the word ‘penis’ or ‘vagina,’ and if a woman expresses any knowledge or interest in sex, you’re seen as a fallen women. Men don’t talk about it, either.” –CNN

According to Kukhee Choo, a media studies professor at Sophia University in Tokyo, Japan actually began to embrace the Western concepts of free love and sexual liberation following WWII. As Japan’s economy skyrocketed into the ’80s – at one point becoming the world’s second-largest economy, working stiffs became the dominant idea of masculinity. After Japan’s economy went tits up in the ’90s, the ensuing period of financial insecurity and economic stagnation was a real confidence killer when it comes to getting laid, according to Japanese studies professor Shigeru Kashima of Meiji University.

“Over the past two decades, some Japanese men have found it hard to face external hardships and fear rejection,” said Kashima. “There’s also an attitude of men devoting themselves more to their hobbies compared to women dedicating themselves to work.”

“Some people are in a relationship and they’re sexless. Some people don’t want to be in a relationship because they don’t want to be sexual. This is all going on at the same time among young people in Japan,” said Choo.

As we noted last May, sexless men are known as “otaku,” – a Japanese term for socially awkward gents who have isolated themselves from their families and romantic prospects alike. “[T]hese “geeks” tend to be diehard anime and manga fans who have little interest in dating,” wrote Luisa Tam in the South China Morning Post.

Taking it one step further are the “soshoku danshi,” which translates to “grass-eating men” or “herbivore men” – a term coined by Japanese columnist Maki Fukasawa who describes these particular isolationists as having a “monk-like approach to life and relationships,” which of course includes no sex.

Studies in Japan estimate that this class of men, normally in their 20s and 30s, account for around 60 per cent to 70 per cent of the male population. Obviously, their reluctance to procreate is a major cause for concern. Japan has had one of lowest birth rates in the world for nearly a decade now. –SCMP

“These herbivore men don’t connect with others, they don’t establish their own families or have children and don’t really contribute anything meaningful to society, either tangibly or intangibly,” says Dr. Paul Wong Wai-ching, associate professor of the Department of Social Work and Social Administration at the University of Hong Kong. “They are like parasites who often live with their parents. So you can imagine how it’s going to affect society in the long run, socially and economically.”

It didn’t always used to be this way. During the Edo period (1603 – 1868), Japan was downright freaky – as evidenced by Shunga – erotic art typically made using woodblock print techniques. And while contemporary Japanese porn blurs out genitals, Shunga artists tended to draw oversized naughty bits.

During the Heian period (794-1185) there was an entire Japanese school of Shingon Buddhism devoted to sexual energy, known as Tachikawa-ryu. While most of its rites have been destroyed, we know that Devotees used ritual sex to reach enlightenment.

“Sexual intercourse between a man and a woman is the supreme buddha activity. Sex is the source of intense pleasure, the root of creation, necessary for every living being, and a natural act of regeneration. To be united as a man and woman is to united with Buddha,” reads one of the sacred Tantras.

Alas, Tachikawa-ryu is no more – having been outlawed in the 13th century, with most of its writings either burned or sealed away at various monasteries.

And now, Japan has a serious virgin epidemic.

end

3 C CHINA/CHINESE AFFAIRS

The markets around the world go gangbusters as Beijing injects the most ever credit for March.

(courtesy zerohedge)

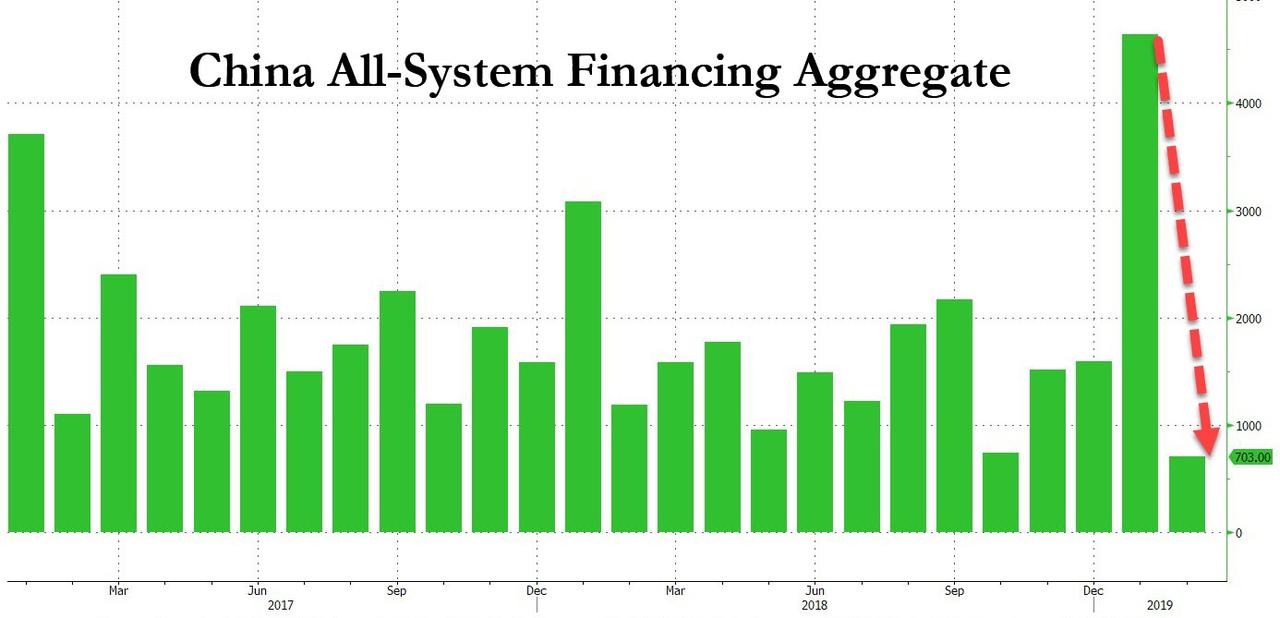

China’s Debt Bomb Is Back: Beijing Injects Most Ever Credit For Month Of March

One month ago, we asked if that was it for China’s “Shanghai Accord 2.0”? Turns out the answer was a resounding “no.”

As we noted at the time, one month after the PBOC injected a gargantuan 4.64 trillion yuan ($685 billion) into the economy – more than the GDP of Saudi Arabia – in the month of January in the country’s broadest credit measure, the All-System Financing Aggregate a credit injection that was so massive it even prompted the fury of China’s prime minister Li Keqiang who lashed out at the central bank for its unprecedented debt generosity in a time when China was still pretending to be on a deleveraging path, in February the PBOC again surprised China-watchers, this time to the downside, when the Chinese central bank reported that aggregate financing increased by a paltry 703 billion yuan, roughly half the expected 1.3 trillion, the lowest print in the revised series history.

However, to assuage fears that China was turning off the credit taps just one month after the release of weak February TSF, PBOC governor Yi commented in his press conference during the NPC that (although February TSF data was weak) the data should be viewed in light of strong January data. He also noted that even combined Jan-Feb data could be distorted by the Chinese New Year, and one needed to wait for March data.

Well, we got just that overnight (as reported previously) and it was a monster: just after 4am ET, the S&P futures surged above 2,900 when the PBOC reported that in March, new yuan loans jumped by 1.69 trillion, far above 1.25 trillion estimate, while total social financing in March soared higher 2.86t yuan, the highest March increase on record; smashing the 1.85 trillion yuan estimate, and more than four times the February 703BN yuan increase.

According to the PBOC, adjusted TSF growth (after adding local government special bond issuance) was 10.7% yoy in March, vs 10.1% yoy in February. If one adds all local government bond net issuance to TSF flow data (excluding special bond issuance to avoid double counting), Goldman estimates that adjusted TSF stock growth at 11.6% yoy in March, higher than 11.0% in February. The implied month-on-month growth of adjusted TSF was 11.6% SA ann, higher than 11.3% in February.

Putting the staggering jump in China’s All-System Financial Aggregate in context, the March number was 80% higher than the year ago March print, and the YTD TSF cumulative total is 40% higher than a year ago!Run-rated, and assuming no further growth at any month in the rest of 2019, China’s TSF is set to close 2019 some 12% higher than a year ago, and nearly twice as high as China’s official GDP growth rate.

Also worth noting: unlike most of 2018, when China shadow banking creation was negative every month starting in March through December, March shadow banking once again printed in the green, following January’s surprising jump (and following February’s drop), suggesting that China has once again eased the reins on its local shadow banking creation in order to spark both the credit impulse and pad China’s economic rebound.

Looking at some other monetary aggregates, in March M2 rose +8.6% y/y; also stronger than the est. +8.2%, and well above the February +8%. In other words, it once again appears that China is doing everything in its power to flood the economy with new credit and reversing the concerns we noted last month emerging from the sharp February TSF drop. It also explains why futures surged above 2,900 once the number hit.

So what is going on? Is Beijing trying to stuff excess credit into the system, which is then appearing in “unexpected” places like the Shanghai Composite and Vancouver real estate, or is there actual demand? According to Goldman, “demand for credit might be improving as well on the back of better domestic sentiment, in turn driven by policy changes such as trade negotiations and support for private companies.” Also, the bank adds that as inflationary expectations are rising, perceived real interest rates might be falling. Finally, the recent profit-boosting VAT cut may be one factor that conceivably increases credit demand.

The last question: will this credit surge persists, and has China now fully thrown in the towel on even pretending to deleverage its $40 trillion economy? The jury is still out: as Goldman’s Yu Song writes, given the recent data on PMI, export, TSF and inflation data and likely strength in upcoming hard data, especially GDP and IP, “we believe it is likely that the policy stance will turn slightly less supportive.” In short: don’t extrapolate the current surge in TSF into the future; additionally, Goldman also sees no current urgency to cut RRR or interest rates further.

Of course, whether market interest rates go up – and as we noted earlier this week, Chinese 10Y yields have soared the most in years in the past month – will depend on inflation, activity growth and equity market performance, and it could be a real possibility if growth surprises to the upside. On the flip side, Goldman also believes “it is unlikely that policy will be tightened aggressively.“ This is because, while the economy and market improved in recent months, policy-makers understand this recovery is still highly policy-dependent, and tightening could lead to a double dip in the economy and equity market. That, to Xi, is not acceptable, and such a double dip is out of the question given the 70th anniversary of the founding of the PRC is due on October 1, 2019. Because of this “policy put”, upside risks (relative to the baseline consensus view of steadily strengthening growth throughout the year) may be greater in the first half of the year, with less policy support thereafter.

In short, China’s credit-based easing will likely continue to accelerate until the summer, and which point Beijing will step off the gas, and while the residual credit momentum will carry China for the next few months, the next deleveraging-based slowdown will likely take place in the second half of 2019 and into 2020, roughly at the same time with what consensus now believe is when the next US recession will take place.

end

China/uSA

In the latest trade discussion, China might accept a “penalty” for currency violations however it has not been spelt out

(courtesy zerohedge)

Today’s Trade Deal Farce: China Might Accept ‘Penalty’ For Currency Pact

We haven’t heard much about currency manipulation provisions of the US-China trade pact over the past four weeks, as reports suggested that the talks had stalled after the two sides had come ever so close to a workable agreement. But with the Trump Administration desperate to keep the market rally going after a few days of sputtering returns, the Wall Street Journal has brought us the latest courtesy of a handful of “current and former” officials.

The paper’s latest ‘scoop’ is essentially a rehash of what we heard a month ago: That the deal on currency is almost finally done. That both Washington and Beijing have agreed to abide by the G-20’s prohibition of currency manipulation, while Beijing has consented to allowing more transparency into how it manages its FX reserves.

This ‘revelation’ begs the question: If this is just a retread of what we heard a month ago, then why is this a story?

But that misses the point. Team Trump wants to keep the market in rally mode, and recent history has shown that nothing pumps the American equity market quite like a well-timed trade-deal scoop.

To be sure, Friday’s story featured one important new detail, however tenuous: Beijing might concede to an enforcement mechanism that would call for some kind of punishment should either side violate the currency rules.

What form will these measures take? Well, we don’t know exactly: All WSJ’s sources said is that the agreement might resemble the currency clause in the USMCA trade agreement hashed out last year. But although the details remained murky, WSJ was able to find an expert source who was willing to take a few guesses.

Treasury officials declined to provide more information on the currency enforcement rules and a spokeswoman for U.S. Trade Representative Robert Lighthizer declined to comment. A spokesman for the Chinese embassy in Washington didn’t immediately respond to a request for comment.

A senior Treasury official said the U.S.-China agreement on currency has similarities to the North American Free Trade Agreement revamp that the Trump administration signed last year with Canada and Mexico. The forex deal also has “certain aspects that go beyond” the new, unratified Nafta deal, known as the U.S.-Mexico-Canada Agreement, or USMCA.

[…]

Some expect the China pact to go further on enforcement than just requiring transparency, with penalties for violating international economic principles in ways that cheapen a national currency.

Mr. Bertsten said there is a “possibility that the enforcement mechanism may have broader coverage, which would be significant and would represent a further step forward into bringing discipline to the currency-manipulation issue.”

Mr. Bergsten said the U.S. and China would likely solve currency disputes in similar fashion to strictly trade-related issues, perhaps with sets of consultations among economic or Treasury officials from the two nations, with tariffs and perhaps other sanctions allowed as penalties.

As WSJ reminds us, Trump slammed China as a currency manipulator during the campaign, but his Treasury Department has demurred from officially labeling them as such. But with the yuan having weakened substantially during this latest bout of dollar strength, it’s not unreasonable that the administration would want to head off any further depreciation.

But just like all the reports about deals being (almost) reached on a broader enforcement mechanism (opening enforcement offices), tech transfers and market access, this one too comes with a caveat: Nothing is set in stone and everything is subject to change.

In other words, while the market continues to price in trade deal optimism, traders won’t know whether they’ve made a colossal miscalculation until it’s too late.

4/EUROPEAN AFFAIRS

i)/EU/UK

Already Farage is attracting names to his new BREXIT party. He has 70 candidates for the May European Parliament election to be held May 23.2019

(ZEROHEDGE)

Farage Says His New Brexit Party Is “UKIP Without The Far Right”

Nigel Farage has only just launched his new ‘Brexit’ Party, but it’s already becoming a force in UK politics, attracting some Tory defectors, including the sister of European Research Group leader Jacob Rees-Mogg, one of the leading Brexiteers.

Jacob Rees-Mogg

✔@Jacob_Rees_Mogg

The Brexit party is fortunate to have such a high calibre candidate but I am sorry that Annunziata has left the Conservative party.https://www.conservativehome.com/video/2019/04/watch-annunziata-rees-mogg-our-prime-minister-will-not-listen-not-only-to-her-membership-but-to-the-people.html …

WATCH: Annunziata Rees-Mogg – “Our Prime Minister will not listen, not only to her membership but…

The former Conservative candidate, and sister to Jacob, urges the Brexit Party to “fight to win”.

conservativehome.com

Prominent Conservative Party fundraiser Richard Tice has agreed to become the chairman of the party as it gears up for EU Parliamentary elections.

Richard Tice

✔@TiceRichard

I’ve been a lifelong member of the Conservative Party.

But like many I’ve concluded that enough is enough.

We cannot, we must not, and we will not allow this shambles in Westminster to continue. We can do much, much better.

That’s why I’ve agreed to Chair the @brexitparty_uk

Farage officially launched the party during an event in Coventry on Friday that was well-attended.

Nigel Farage

✔@Nigel_Farage

BREXIT PARTY LAUNCH – LIVE https://www.pscp.tv/w/b4BZlzFvUEtMTXdvZG5uamR8MXpxS1ZhbWpYVll4QtL0MJe02IwEsNZ0fBmz2gZlIy_SCX0KFmDzG6mjY6EI …

Nigel Farage @Nigel_Farage

BREXIT PARTY LAUNCH – LIVE

pscp.tv

During an interview before the event, Farage introduced the new party as a ‘mirror’ of UKIP on policies, but without what he described as the Islamophobic, far-right faction.

Farage, who has been credited as one of the godfathers of Brexit, left UKIP, the party that he helped create and build into a force on the right of British politics, claiming that the party had been taken over by racists and Islamophobes and that its brand was now ‘tarnished’.

He promised the Brexit Party would be “deeply intolerant of all intolerance” and would represent a cross-section of society.

“In terms of policy, there’s no difference (to UKIP), but in terms of personnel there is a vast difference.”

“UKIP did struggle to get enough good people into it but unfortunately what it’s chosen to do is allow the far right to join it and take it over and I’m afraid the brand is now tarnished.”

With Parliament on recess until April 23, Farage apparently timed the party launch so as to grab maximum media coverage. When it came his turn to speak at the launch, Farage again called for a “Democratic revolution” to ensure that the outcome of the Brexit referendum is honored, and once again “start to put the fear of god into our MPs.” He also declared that the Brexit Party wouldn’t be taking donations from Aaron Banks, a millionaire mining mogul who helped to bankroll UKIP and was recently the target of an extensive investigative report published by the New Yorker that delved into suspicions that Banks helped launder foreign money – specifically, from Russia – into the Brexit campaign.

BBC Politics

✔@BBCPolitics

“The brand is now tarnished” – Nigel Farage attacks his old party, UKIP, for allowing the far right to join – saying his new Brexit Party will put “competence back into British politics”http://bbc.in/2Ieeafo @BBCr4today pic.twitter.com/fpPaf0JqoJ

The Brexit party already has 70 candidates to stand in the European elections, which are expected to begin on May 23.

In response to UKIP leader Gerard Batten rebutted Farage’s claims about the Brexit Party being a mirror image of UKIP, arguing that UKIP has “a manifesto and policies” while the Brexit Party is just a “vehicle” for Farage. But if the party wins at least a few seats in the EU Parliament, it would likely join with the growing populist coalition being organized by Italy’s Matteo Salvini, leader of the League, helping to establish a powerful eurosceptic bloc in the legislature.

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

TURKEY/USA/RUSSIA

LIBYA

A good commentary explaining how General Haftar became the strongman in Libya. He is friendly to the USA and he was set to remove the UN’s al_Serraj, the beleaguered Prime Minister of Libya. Once he takes over Libya oil should begin to flow from the country and migrants should return.

(courtesy Prashad/Common Dreams)

6.GLOBAL ISSUES

7 OIL ISSUES

8. EMERGING MARKETS

VENEZUELA

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:00 AM….

Euro/USA 1.1318 UP .0058 REACTING TO MERKEL’S FAILED COALITION/ REACTING TO +GERMAN ELECTION WHERE ALT RIGHT PARTY ENTERS THE BUNDESTAG/ huge Deutsche bank problems ///ITALIAN CHAOS /AND NOW ECB TAPERING BOND PURCHASES/JAPAN TAPERING BOND PURCHASES /USA RISING INTEREST RATES /FLOODING/EUROPE BOURSES ALL GREEN

USA/JAPAN YEN 111.98 UP .332 (Abe’s new negative interest rate (NIRP), a total DISASTER/NOW TARGETS INTEREST RATE AT .11% AS IT WILL BUY UNLIMITED BONDS TO GETS TO THAT LEVEL…

GBP/USA 1.3087 UP 0.0033 (Brexit March 29/ 2019/ARTICLE 50 SIGNED/BREXIT FEES WILL BE CAPPED/BREXIT EXTENDED TO OCT 31/2019//

USA/CAN 1.3328 DOWN .00050 CANADA WORRIED ABOUT TRADE WITH THE USA WITH TRUMP ELECTION/ITALIAN EXIT AND GREXIT FROM EU/(TRUMP INITIATES LUMBER TARIFFS ON CANADA/CANADA HAS A HUGE HOUSEHOLD DEBT/GDP PROBLEM)

Early THIS FRIDAY morning in Europe, the Euro ROSE by 58 basis points, trading now ABOVE the important 1.08 level RISING to 1.1318 Last night Shanghai COMPOSITE CLOSED DOWN 1.34 POINTS OR 0.04%.

//Hang Sang CLOSED DOWN 70.31 POINTS OR .24%

/AUSTRALIA CLOSED UP .84%// EUROPEAN BOURSES GREEN

The NIKKEI: this FRIDAY morning CLOSED UP 159.16 POINTS OR 0.73%

Trading from Europe and Asia

1/EUROPE OPENED GREEN

2/ CHINESE BOURSES / :Hang Sang CLOSED UP 70.31 POINTS OR .24%

/SHANGHAI CLOSED DOWN 1.34 POINTS OR 0.04%

Australia BOURSE CLOSED UP .84%%

Nikkei (Japan) CLOSED UP 159.16 POINTS OR 0.73%

INDIA’S SENSEX IN THE GREEN

Gold very early morning trading: 1294.20

silver:$15.08

Early FRIDAY morning USA 10 year bond yield: 2.55% !!! UP 5 IN POINTS from THURSDAY’S night in basis points and it is trading WELL ABOVE resistance at 2.27-2.32%.

The 30 yr bond yield 2.96 UP 3 IN BASIS POINTS from THURSDAY night.

USA dollar index early FRIDAY morning: 96.82 DOWN 36 CENT(S) from THURSDAY’s close.

This ends early morning numbers FRIDAY MORNING

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now your closing FRIDAY NUMBERS \12: 00 PM

Portuguese 10 year bond yield: 1.17% UP 4 in basis point(s) yield from THURSDAY/

JAPANESE BOND YIELD: -.06% DOWN 0 BASIS POINTS from THURSDAY/JAPAN losing control of its yield curve/

SPANISH 10 YR BOND YIELD: 1.05% UP 5 IN basis point yield from THURSDAY

ITALIAN 10 YR BOND YIELD: 2.54 UP 17 POINTS in basis point yield from THURSDAY/

the Italian 10 yr bond yield is trading 149 points HIGHER than Spain.

GERMAN 10 YR BOND YIELD: RISES +.05% IN BASIS POINTS ON THE DAY//

THE IMPORTANT SPREAD BETWEEN ITALIAN 10 YR BOND AND GERMAN 10 YEAR BOND IS 2.49% AND NOW ABOVE THE THE 3.00% LEVEL WHICH WILL IMPLODE THE ENTIRE ITALIAN BANKING SYSTEM. AT 4% SPREAD THERE WILL BE A MASSIVE BANK RUN…

END

IMPORTANT CURRENCY CLOSES FOR FRIDAY

Closing currency crosses for FRIDAY night/USA DOLLAR INDEX/USA 10 YR BOND YIELD/1:00 PM

Euro/USA 1.1306 UP .00046 or 46 basis points

USA/Japan: 111.98 UP 0.339 OR YEN DOWN 34 basis points/

Great Britain/USA 1.3096 DOWN .0041 POUND UP 41 BASIS POINTS)

Canadian dollar UP 46 basis points to 1.3331

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The USA/Yuan,CNY closed AT 6.7037 0N SHORE (UP)

THE USA/YUAN OFFSHORE: 6.7071 (YUAN UP)

TURKISH LIRA: 5.7630

the 10 yr Japanese bond yield closed at -.06%

Your closing 10 yr USA bond yield UP 6 IN basis points from THURSDAY at 2.55 % //trading well ABOVE the resistance level of 2.27-2.32%) very problematic USA 30 yr bond yield: 2,96 UP 4 in basis points on the day /

Your closing USA dollar index, 96.81 DOWN 37 CENT(S) ON THE DAY/1.00 PM/

Your closing bourses for Europe and the Dow along with the USA dollar index closing and interest rates for FRIDAY: 12:00 PM

London: CLOSED UP 9.91 0.05%

German Dax : UP 64.44 POINTS OR 0.54%

Paris Cac CLOSED UP 18.40 POINTS OR 0.34%

Spain IBEX CLOSED UP 26.70 POINTS OR 0.28%

Italian MIB: CLOSED UP 162.31 POINTS OR 0.75%

WTI Oil price; 64.28 1:00 pm

Brent Oil: 71.58 12:00 EST

USA /RUSSIAN / ROUBLE CROSS: 64.32 THE CROSS LOWER BY 0.29 ROUBLES/DOLLAR (ROUBLE HIGHER BY 29 BASIS PTS)

TODAY THE GERMAN YIELD RISES TO +.05 FOR THE 10 YR BOND 1.00 PM EST EST

END

This ends the stock indices, oil price, currency crosses and interest rate closes for today 4:30 PM

Closing Price for Oil, 4:00 pm/and 10 year USA interest rate:

WTI CRUDE OIL PRICE 4:30 PM : 63.76

BRENT : 71.47

USA 10 YR BOND YIELD: … 2.56… STILL DEADLY//

USA 30 YR BOND YIELD: 2.97..STILL DEADLY

EURO/USA DOLLAR CROSS: 1.1296 ( UP 36 BASIS POINTS)

USA/JAPANESE YEN:112.02 UP .371 (YEN DOWN 37 BASIS POINTS/..

USA DOLLAR INDEX: 96.97 DOWN 21 cent(s)/

The British pound at 4 pm: Great Britain Pound/USA:1.3072 UP 17 POINTS

the Turkish lira close: 5.7762 GETTING VERY DANGEROUS

the Russian rouble 64.37 UP .23 Roubles against the uSA dollar.( UP 23 BASIS POINTS)

Canadian dollar: 1.3333 UP 44 BASIS pts

USA/CHINESE YUAN (CNY) : 6.7037 (ONSHORE)/

USA/CHINESE YUAN(CNH): 6.7094 (OFFSHORE)

German 10 yr bond yield at 5 pm: ,+0.04%

The Dow closed UP 269.25 POINTS OR 1.03%

NASDAQ closed UP 36.81 POINTS OR 0.46%

VOLATILITY INDEX: 12.06 CLOSED DOWN .96

LIBOR 3 MONTH DURATION: 2.596%//

FROM 2.603

And now your more important USA stories which will influence the price of gold/silver

TRADING IN GRAPH FORM FOR THE DAY/WEEKLY SUMMARY/FOLLOWED BY TODAY

Disney, Dimon, & A China Debt Surge Lift Stocks As Economic Data Collapses

Just keep repeating: “the market is not the economy“…

Except that is the exact opposite of what former Fed Chair Alan Greenspan told the world this morning, explaining that much of the improvement has come from a rise in stock market prices:

He sees a “stock market aura” in the economy.

A rise of 10 percent in the S&P 500 corresponds to a 1 percent real GDP increase, he said. The S&P 500 has risen nearly 16 percent in 2019 and is on track for its best performance in history should current trends hold.

A rise of 10 percent in the S&P 500 corresponds to a 1 percent real GDP increase, he said. The S&P 500 has risen nearly 16 percent in 2019 and is on track for its best performance in history should current trends hold.

So who is right …

So who is right – Greenspan or the asset-gatherers and commission-takers?

* * *

China was weak on the week with ChiNext’s worst week since before Thanksgiving (after rising for 9 straight weeks)…

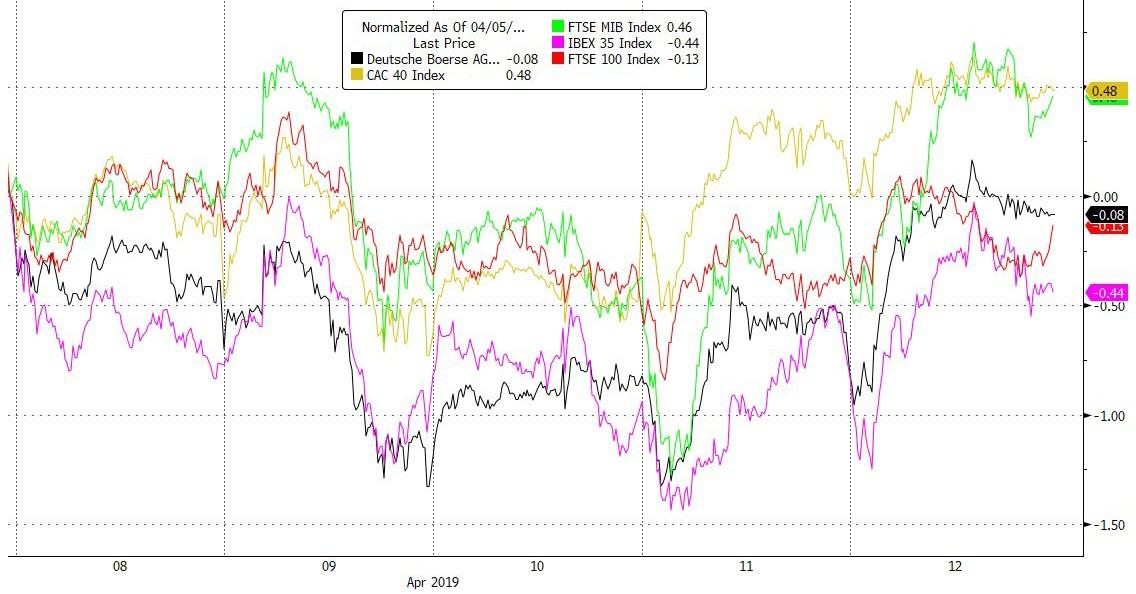

Mixed picture in Europe this week with Italy and France outperforming and Spain the laggard…

US futures show the moment that China credit and trade data hit, sending stocks soaring…

On the week, Trannies were the big winners as Small Caps clung to gains and The Dow scrambled today to get back to breakeven on the week…(despite utter desperation in the algos, The Dow ended the week red)