GOLD: $1288.30 DOWN $3.70 (COMEX TO COMEX CLOSING)

Silver: $15.01 DOWN 1 CENT (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1288.05

silver: $15.00

Something To Ponder…

Remember what you’re told by The Fed – 2% inflation per annum is ‘stable prices’…

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 9/10

EXCHANGE: COMEX

CONTRACT: APRIL 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,290.600000000 USD

INTENT DATE: 04/12/2019 DELIVERY DATE: 04/16/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 9

737 C ADVANTAGE 10 1

____________________________________________________________________________________________

TOTAL: 10 10

MONTH TO DATE: 4,221

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 10 NOTICE(S) FOR 1000 OZ (.0311 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 4221 NOTICES FOR 422,100 OZ (13.129 TONNES)

SILVER

FOR APRIL

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1 NOTICE(S) FILED TODAY FOR 5,000 OZ/

total number of notices filed so far this month: 774 for 3,870,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE :$5114 DOWN $17

Bitcoin: FINAL EVENING TRADE: $5020 DOWN 111

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI TOOK A LITTLE BREATHER BY FALLING BY A CONSIDERABLE SIZED 1553 CONTRACTS FROM 219,843 DOWN TO 218,290 DESPITE FRIDAY’S 11 CENT RISE IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE MUST HAVE HAD CONSIDERABLE SHORT COVERING AGAIN. TODAY NEW SPREADS WERE INITIATED.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A VERY STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 2617 FOR MAY, 221 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2838 CONTRACTS. WITH THE TRANSFER OF 2838 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2838 EFP CONTRACTS TRANSLATES INTO 14.19 MILLION OZ ACCOMPANYING:

1.THE 11 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

AND NOW 3.870 MILLION OZ STANDING FOR SILVER IN APRIL.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

15,367 CONTRACTS (FOR 11 TRADING DAYS TOTAL 15,367 CONTRACTS) OR 76.84 MILLION OZ: (AVERAGE PER DAY: 1397 CONTRACTS OR 6.985 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 76.84 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 10.98% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 645,01 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1533 DESPITE THE 11 CENT RISE IN SILVER PRICING AT THE COMEX /FRIDAY... THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2832 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GOOD SIZED: 1285 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2838 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 1553 OI COMEX CONTRACTS. AND ALL OF THIS GOOD DEMAND HAPPENED WITH A 11 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $15.02 WITH RESPECT TO FRIDAY’S TRADING. YET WE HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.092 BILLION OZ TO BE EXACT or 156% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 1 NOTICE(S) FOR 5,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ AND NOW APRIL AT 3.870 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL AND THIS TIME BY A CONSIDERABLE SIZED 3145 CONTRACTS, TO 444,280 DESPITE THE RISE IN THE COMEX GOLD PRICE/(A GAIN IN PRICE OF $2.10//FRIDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6302 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 6302 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 444,280. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3157 CONTRACTS: 3145 OI CONTRACTS DECREASED AT THE COMEX AND 6302 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 3157 CONTRACTS OR 315700 OZ OR 9.819 TONNES. FRIDAY WE HAD A SMALL RISE IN THE PRICE OF GOLD TO THE TUNE OF $2.10….AND YET WITH THAT, WE STILL HAD A GOOD GAIN IN TONNAGE OF 9.819 TONNES!!!!!!.???

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 63,038 CONTRACTS OR 6,303,800 OR 196.07 TONNES (11 TRADING DAYS AND THUS AVERAGING: 5730 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAYS IN TONNES: 196.07 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 196.07/3550 x 100% TONNES = 5.52% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1571,67 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 3145 DESPITE THE GAIN IN PRICING ($2.10) THAT GOLD UNDERTOOK FRIDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6302 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6302 EFP CONTRACTS ISSUED, WE HAD A GOOD GAIN OF 3602 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6302 CONTRACTS MOVE TO LONDON AND 3145 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 9.819 TONNES). ..AND ALL OF THIS GOOD DEMAND OCCURRED WITH A SMALL RISE IN PRICE OF $2.10 IN YESTERDAY’S TRADING AT THE COMEX.

we had: 10 notice(s) filed upon for 1000 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $3.70 TODAY

NO CHANGES WITH RESPECT TO GOLD INVENTORIES AT THE GLD

INVENTORY RESTS AT 757.85 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 1 CENT TODAY:

A SMALL CHANGES IN SILVER INVENTORY AT THE SLV//

A WITHDRAWAL OF 750,000 OZ

/INVENTORY RESTS AT 309.167 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY AN CONSIDERABLE SIZED 1553 CONTRACTS from 219,843 DOWN TO 218,290 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

HERE IS HOW THE CROOKS USED SPREADING AS WE ENTER AN ACTIVE DELIVERY MONTH. THUS SILVER HAS THE ACTIVE MONTH OF MAY COMING UP AND THUS SPREADERS DO THE FOLLOWING:

“YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF APRIL BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 2617 FOR MAY AND JULY: 221 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2832 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 1553 CONTRACTS TO THE 2832 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD SIZED GAIN OF 1285 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 7.098MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH. AND NOW 3.870 MILLION OZ FOR APRIL.

RESULT: A CONSIDERABLE SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 11 CENT RISE IN PRICING THAT SILVER UNDERTOOK IN PRICING// FRIDAY. WE ALSO HAD A STRONG SIZED 2832 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i))MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED DOWN 10.84 POINTS OR 0.34% //Hang Sang CLOSED DOWN 99.04 POINTS OR .33% /The Nikkei closed UP 298.55 POINTS OR 1.37%/ Australia’s all ordinaires CLOSED UP .01%

/Chinese yuan (ONSHORE) closed UP at 6.7072 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 64.57 dollars per barrel for WTI and 71.66 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.7072 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7077 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA

Funny: Kim gives Trump until the end of the year to become more flexible re sanctions or else he walks

(courtesy zerohedge)

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/USA:

As far as the trade talks are proceeding, the answer is quite clear: they are not getting real progress on the essential beefs that the USA has with China. The USA is now backtracking on enforcement and they are caving on demands Beijing scrap industrial subsidies.

( zerohedge)

4/EUROPEAN AFFAIRS

i)Italy

Salvini is positioning Italy ready for the confrontation with Brussels

( TomLuongo)

ii)Germany

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Turkey

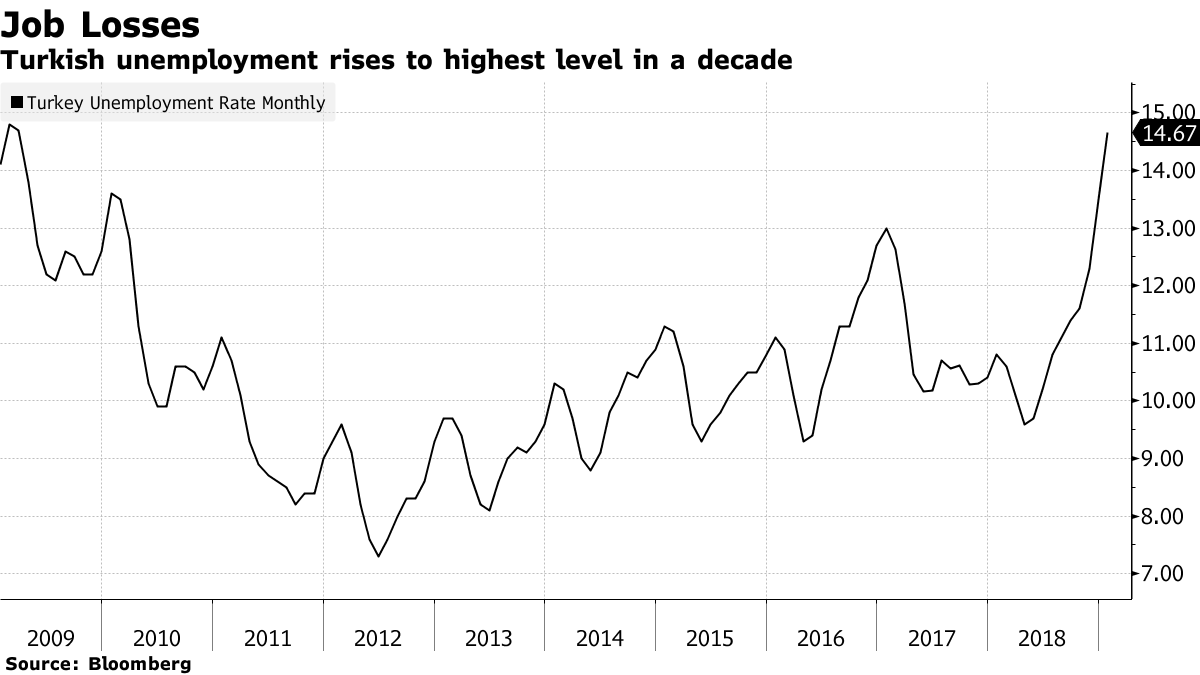

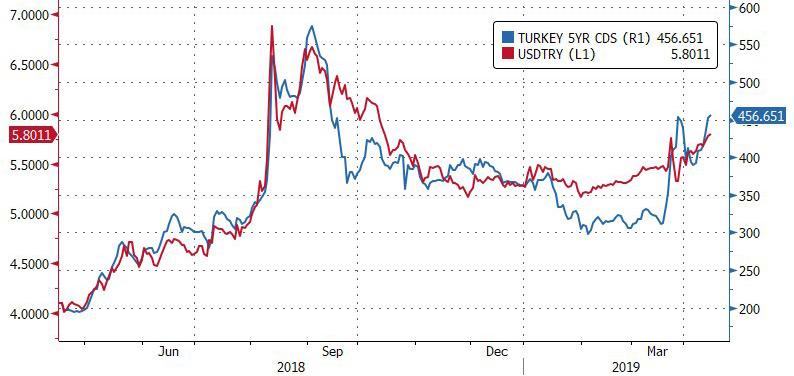

There are two countries that we must pay close attention to to see if a collapse is coming. I have now elevated Turkey to being the country that can send the entire global finances into chaos. The Lira plummeted to 5.8043 to the dollar on soaring unemployment, rising to 14.7% and youth unemployment at almost 27%. My question to Turkey is this: how can a country’s corporates function with an interest rate at almost 18%. No wonder unemployment skyrocketed.A few things to note: see the huge rise in Turkey’s credit default swaps. These are simply bets on either the sovereign will default on its bonds. It is rising because Turkey cannot get a hold of enough USA dollars along with its corporate citizens.

( zerohedge)

ii)TURKEY//RUSSIA

Turkey continues to face Russia against the wishes of the USA. Watch for the USA to weaponize the dollar dollar against Turkey.)

( zerohedge)

iii)ISRAEL/SYRIA

Israel launches an attack Friday night on Syria targeting warehouses of military weapons stored by Iran

( Leith Aboufadel/AlNasdarNews)

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA

9. PHYSICAL MARKETS

ii)When the next crisis hits, hard assets will be safe: it will be financial assets that will disappear. Very important interview of James Turk with Kingworldnews

( James Turk/Kingworldnews)

iii)Chris Powell admonishes Jim Grant for not saying the gold market is rigged like stocks and interest rates

(courtesy Chris Powell/GATA/Jim Grant)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning/FOMC

ii)Market data

ii)USA ECONOMIC/GENERAL STORIES

a)Now wonder the Fed is worried about Stephen Moore as he sets to challenge the status quo over there.

( zerohedge)

b)A good article for you today on the printing of money by the state: whether it is done by the Fed or by a private individual it is counterfeiting money..if done by the state it is legal counterfeiting

iv)SWAMP STORIES

Pelosi is having great difficulty reining in AOC and her gang of 5.

( zerohedge)

end

Let us head over to the comex:

AFTER APRIL, WE HAVE THE ACTIVE DELIVERY MONTH OF MAY AND HERE THE OI FELL BY 4279 CONTRACTS DOWN TO 105,553. CONTRACTS.. THE NEXT MONTH OF JUNE LOST 19 CONTRACTS TO 79. AFTER JUNE, THE VERY BIG DELIVERY MONTH OF JULY HAD A GAIN OF 2218 CONTRACTS UP TO 76,897 CONTRACTS.

There Is Too Much Debt In The World – World Bank

World Bank President, David Malpass, warns there is too much debt in the world and blames China rather than U.S.

- China has lent trillions of dollars to other countries, including the U.S.

- “There are challenges facing the world in terms of how do you have transparent projects that are high quality, where the debt is transparent. China moved so fast that in some part of the world there is just too much debt,” Malpass says. “That’s something that we can work on with China.”

There is too much debt floating around the world and China is a big reason why, World Bank President David Malpass said Thursday.

“There are challenges facing the world in terms of how do you have transparent projects that are high quality, where the debt is transparent. China moved so fast that in some part of the world there is just too much debt,” Malpass told CNBC’s Sara Eisen on “Squawk on the Street. ” “That’s something that we can work on with China.”

China has lent trillions of dollars to other countries, including the U.S. As of January, China owns $1.12 trillion in U.S. Treasurys, according to data from the Treasury Department.

Malpass has been a critic of China’s lending efforts to fund its “One Belt, One Road” infrastructure initiative. Last year, he said these loans leave weaker countries with “excessive debt and low-quality projects. ”

On Thursday, Malpass indicated China is willing to scale back on these efforts, noting: “They want to see a better relationship with other countries and be part of the world system. I expect to be successful in that and have a good relationship with China.”

Malpass has also criticized China for taking low-cost loans from the World Bank despite being the second largest economy in the world and surpassing the bank’s income threshold for low-cost loans in 2016.

“China recognizes that its role as a borrower in the bank needs to diminish,” Malpass said. He also noted that World Bank loans to China have been decreasing, adding he expects this to continue over the next three years.

Malpass was elected to his post last Friday. Before joining the World Bank, Malpass served as under secretary of international affairs at the Treasury Department.

News and Commentary

Gold slips to one-week low as global slowdown fears ease (CNBC.com)

Criticism mounts of Trump’s pro-gold pick for U.S. Federal Reserve (Reuters.com)

Trump Slams Fed Again, Says Stocks Should Be 5,000-10,000 Higher (Bloomberg.com)

Draghi, in Rare Move, Sounds Concern Over Fed’s Independence (Bloomberg.com)

Another 8 tonnes of gold taken from Venezuela’s central bank for sale (Reuters.com)

Why You Should Prepare for Deflation (24HGold.com)

Until this Thursday (April 18), when you purchase the minimum amount of 10,000 ($€£) in physical gold and or silver, you receive complimentary Storage In Zurich For 6 Months

Until this Thursday (April 18), when you purchase the minimum amount of 10,000 ($€£) in physical gold and or silver, you receive complimentary Storage In Zurich For 6 Months

Economy will start to fade ‘very dramatically’ because of entitlement burden – Greenspan (CNBC.com)

Gold Speculator’s Bullish Bets Rebounded This Week (Investing.com)

Would a political Fed rescue the world? (Reuters.com)

These 40 cities may see housing prices decline, survey says (CNBC.com)

Shadow banking is now a $52 trillion industry, posing a big risk to the financial system (CNBC.com)

Gold Prices (LBMA PM)

12 Apr: USD 1,296.15, GBP 991.68 & EUR 1,146.06 per ounce

11 Apr: USD 1,304.65, GBP 997.01 & EUR 1,152.43 per ounce

10 Apr1: USD 1,304.80, GBP 998.04 & EUR 1,157.44 per ounce

09 Apr: USD 1,303.00, GBP 995.13 & EUR 1,155.00 per ounce

08 Apr: USD 1,297.10, GBP 993.58 & EUR 1,154.29 per ounce

Silver Prices (LBMA)

12 Apr: USD 15.06, GBP 11.51 & EUR 13.31 per ounce

11 Apr: USD 15.25, GBP 11.66 & EUR 13.53 per ounce

10 Apr: USD 15.25, GBP 11.66 & EUR 13.53 per ounce

09 Apr: USD 15.25, GBP 11.66 & EUR 13.53 per ounce

08 Apr: USD 15.14, GBP 11.60 & EUR 13.47 per ounce

Recent Market Updates

– How to Store Gold in an Uncertain World

– The ECB Is Struggling With Inflation, Interest Rates and The Outlook

– Russia Dumps U.S. Dollars and Buys Gold As “Safety Metal”

– How A ‘No Deal’ Brexit Could Lead To The “Lehmanization” Of Europe

– Silver Bullion Set to Soar to $50 an Ounce (GoldCore Video)

– Perth Mint’s Gold Bullion Sales Surge 68% In March

– 7 Reasons – Including Brexit – To Worry About the Global Economy In Charts

Until April 18, when you purchase the minimum amount of 10,000 ($€£) in physical gold and or silver, you receive complimentary Storage In Zurich For 6 Months

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

How true: accountability and transparency in central banking..not in our life time as long as major news organizations refuse to ask the right questions and attempt at proper journalism

(courtesy Chris Powell/GATA/Reuters)

Bill Holter: Public commentary for today

A couple of topics for you today that are connected, obvious, yet not understood or even contemplated at this point. First, have you ever wondered why the names of many fiat currencies refer to “weight”? Such as the Peso, Peseta, Lira, or Pound amongst many others? This is similar to the names of various roads, like “Saw Mill Rd.”. It was named that because years ago there was actually a sawmill down the lane. These fiat currencies with “weighty” names started out as receipts for either gold or silver. They were convertible into a specific amount of metal when presented at a bank.

In essence these currencies were representations of physical metal since they were redeemable but far easier to carry around due to the lack of weight. In today’s jargon, paper currencies that were redeemable in specie were “derivatives” of the metals themselves. Then as time went on, the redeemability was cancelled and the currencies became true fiat, unbacked by anything except the credit worthiness of the issuer.

Over time, ALL currencies have become fiat and these currencies steadily devalued. I would ask, how can anyone have the thought these currencies can gain value versus gold or silver over a long period of time if they were originally spawned as derivatives? Can a derivative ever become more valuable than that it originated from? The answer of course is no and should be followed by another question; can a monetary guarantee from any government ever be more ironclad than that of physical metal itself?

Next, we know for a fact Russia, China and other nations have been accumulating gold for years now. Why? I can assure you it is not to “trade” for profit to accumulate more fiat. They fully understand their own issued fiats and those of other central banks were at best only derivatives historically and not even remotely a derivative of gold now. Now, they are only poor joking derivatives of the various central banks and in no way a store of value.

One of our readers passed this commentary regarding a Zerohedge article along yesterday to us;

“This graph is pure transparency to those who understand the Chinese. Whether in trade agreements, military power, or their economic goals, they never show their hand.

Some estimate they are holding 20,000+ tons of gold.

I believe they will shock the world with twice that (40,000 tons).

That will be the day everything changes and it will be by their design.

Does anyone truly believe Russia doesn’t know this ?”

https://www.zerohedge.com/s3/files/inline-images/china%20gold%204.7.2019.jpg?itok=Z3xFc0Q_

Think about what is said here and truly what it means? When China does fully announce their gold holdings, they will most likely not make the yuan convertible into gold. Their gold holdings will simply act as a backstop for confidence in the currency. As Jim puts it, the gold hoard will act as the Hope Diamond around a woman’s neck as she walks into the room. No one will really look at the woman, so whether she is homely or not does not matter, only what is around her neck …and this would be China’s gold holdings and to a lesser degree Russia’s.

We are talking about “financial warfare” here. Russia and China fully understand the fraudulent nature of Western fractional reserve banking and finance. They understand how and why the West will fail and have been acting to accumulate gold as buffer against (or in place of) any dollar holdings. They have set up trade deals, lending/credit and clearing facilities, and treaty’s of all sorts with many nations. Put simply, they are making ready for the coming failure of the West!

Putting this together, China will be moving the currency pendulum back toward derivative status. As mentioned, I do not think the yuan will become convertible because if it was convertible …conversion is exactly what will happen. Instead, they will use their gold holdings as a sign of fiscal and monetary responsibility. Though not truly a derivative because no direct connection to their gold, the yuan will be favored versus other fiats because of the held gold. If you understand that we are currently at war, financial war, then you understand “why” foreign nations are accumulating gold. The old saying “he who owns the gold makes the rules” will apply here.

To finish, if you are waiting for gold to break out above the five+ year trading range before you position yourself, good luck! As a nation, we will be completely screwed without gold holdings because our dollar will be shunned internationally as one issued by a central bank with paltry if any actual gold holdings. China will mark up the price of gold making their hoard mighty …and making it very difficult for anyone ever to catch up if trying to pay with fiat and no Hope Diamond around their neck!

Standing watch,

Bill Holter

Holter-Sinclair collaboration

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7072/

//OFFSHORE YUAN: 6.7077 /shanghai bourse CLOSED DOWN 10.84 or 0.34%

HANG SANG CLOSED DOWN 99.04 points or .33%

2. Nikkei closed UP 298.55 POINTS OR 1.37%

3. Europe stocks OPENED GREEN

USA dollar index FALLS TO 96.85/Euro RISES TO 1.1311

3b Japan 10 year bond yield: RISES TO. –.03/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.93/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 63.38 and Brent: 70.81

3f Gold DOWN/JAPANESE Yen UP CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +06%/Italian 10 yr bond yield UP to 2.53% /SPAIN 10 YR BOND YIELD UP TO 1.08%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.47: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.28

3k Gold at $1286.35 silver at:14.94 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 47/100 in roubles/dollar) 64.15

3m oil into the 63 dollar handle for WTI and 70 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.98 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0027 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1341 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.06%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.56% early this morning. Thirty year rate at 2.97%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.7988..GETTING VERY DANGEROUS

Global Stocks Hit 6 Month High On, Drumroll, Renewed “Trade Talk Optimism”

This is the part in Groundhog Day where Phil Connors kills himself again, and again, and again.

With stocks itching for a new excuse to levitate higher, they got that overnight when a Reuters report on fresh “progress” in the U.S.-China trade talks and renewed “optimism” in a trade deal helped propel world stock markets to a 6-month high on steered investors away from save havens such as the Japanese yen, even as 10Y treasury yields dipped modestly, as the same catalyst that has driven stocks higher on virtually every single day in the past quarter has continued to do so again and again, right out of the cult groundhog movie.

“It seems like bullish sentiment has decent grip for now and everyone is focused on the year to date performance of the equity markets,” said Naeem Aslam, chief market analyst at TF Global Markets (UK) Ltd in London.

Overnight Reuters reported that US negotiators tempered demands that China curb industrial subsidies as a condition for a trade deal after strong resistance from Beijing, marking a retreat on a core U.S. objective for the trade talks. According to the report, in the push to secure a deal in the next month or so, U.S. negotiators have become resigned to securing less than they would like on curbing those subsidies and are focused instead on other areas where they consider demands are more achievable, Reuters sources said. Those include ending forced technology transfers, improving intellectual property protection and widening access to China’s markets, the sources said. China has already given ground on those issues.

“It’s not that there won’t be some language on it, but it is not going to be very detailed or specific,” one source familiar with the talks said in reference to the subsidies issue.

Separately, on Saturday during the latest IMF conclave, Treasury Secretary Steven Mnuchin said the US is “hopefully very close” to final round of China talks; adding that the U.S. is open to facing enforcement penalties which work “in both directions.” all of which helped spawn a fresh sense of optimism that a deal announcement was imminent.

In addition to the new trade optimism, thanks to the pleasant aftertaste from China’s credit flood in March, which exceeded all estimates, concern over global growth has also eased, fueling demand for riskier assets. MSCI’s gauge for equities saw its 100-day moving average rise above the 200-day equivalent as the index rose 12 out of the past 13 days, signaling potential for further gains.

Following a muted Asian session, the European Stoxx 600 Index erased an earlier loss and extended gains to session highs with bank stocks contributing most to the increase. A gauge tracking lenders climbs for a third session as it holds above a barrier it breached last week. The European index advances 0.3% as of 11:30 a.m. in London, reversing a decline of as much as 0.1% earlier. BNP Paribas rose 2.5%, adding the most to the increase by index points. Other banks also stronger: Credit Suisse +2.2%; ING Groep +1.3%, Unicredit +2.2%

S&P500 futures nudged up after spending most of the session in the red, as results from Goldman Sachs and Citigroup loomed. In Asia, equities headed for a fresh six-month high, propelled by markets in Japan and Korea, after the Bank of China released upbeat credit data, although earlier, Chinese stocks closed in the red, fading initial trade-related gains as expectations for rate cuts fizzled following the latest credit deluge.

With Chinese trade and lending data showing signs of improvement for the world’s second-biggest economy, investors are turning to the US earnings season to confirm the resilience of corporate America in the face of numerous challenges to growth. JPMorgan Chase posted strong first-quarter results last week, Goldman and Citi report today and Bank of America is up on Tuesday.

“The environment of easier financial conditions is beginning to have an impact on the broader economy,” Principal Global’s Binay Chandgothia told Bloomberg TV. “If that is the case and growth does pick up, you’ll see an uptick in analyst expectations and earnings as well, which should help continue the rally.”

Bunds, US Treausrys and Gilts were confined to very tight ranges, as BTPs trade in a choppier range with peripheral yield spreads widening to core at the margin. G-10 currencies drift sideways in quiet trade, SEK marginally outperforms peers, CAD and NOK lag on commodities weakness.

In FX, South Korea’s won led an advance among emerging-market currencies, while Turkey’s lira underperformed as the unemployment rate climbed to the highest level in a decade. G-10 currencies drifted sideways in quiet trade, with the SEK marginally outperforming peers, CAD and NOK lag on commodities weakness. The yen dropped toward its 2019 low on Monday and the Swiss franc hit its weakest in nearly a month. The dollar also weakened slightly, allowing the euro to cement gains above $1.13.

In commodities, oil slipped after the longest run of weekly gains in three years as a report showed increased U.S. oil-rig activity. Oil provided big milestones last week, with Brent breaking through the $70 threshold and the U.S. benchmark posting six straight weeks of gains for the first time since early 2016. Brent crude oil futures was last off 23 cents at $71.32 while crude futures, the U.S. benchmark, eased 33 cents to $63.56.

Expected data include Empire State Manufacturing Survey. Schwab, Citigroup and Goldman Sachs are reporting earnings.

Market Snapshot

- S&P 500 futures little changed at 2,912.00

- STOXX Europe 600 up 0.01% to 387.56

- MXAP up 0.6% to 163.25

- MXAPJ up 0.1% to 543.51

- Nikkei up 1.4% to 22,169.11

- Topix up 1.4% to 1,627.93

- Hang Seng Index down 0.3% to 29,810.72

- Shanghai Composite down 0.3% to 3,177.79

- Sensex up 0.3% to 38,897.72

- Australia S&P/ASX 200 unchanged at 6,251.44

- Kospi up 0.4% to 2,242.88

- German 10Y yield rose 0.5 bps to 0.06%

- Euro up 0.2% to $1.1319

- Italian 10Y yield rose 15.4 bps to 2.171%

- Spanish 10Y yield rose 1.5 bps to 1.064%

- Brent futures down 0.7% to $71.04/bbl

- Gold spot down 0.3% to $1,286.95

- U.S. Dollar Index down 0.2% to 96.80

Top Overnight News from Bloomberg

- The release of the almost 400-page Special Counsel Robert Mueller report this week could help President Trump put two years of suspicion and risk from the investigation behind him — or ensure that controversy over the Russia probe hangs over his re-election bid.

- Trump, renewing his attack on the Federal Reserve, claimed the stock market would be “5000 to 10,000” points higher had it not been for the actions of the U.S. central bank. “Quantitative tightening was a killer, should have done the exact opposite!” he tweeted.

- Job vacancies in London’s finance industry have halved in two years as uncertainty over Brexit knocks down business confidence, a survey by recruiter Morgan McKinley has found.

- The mass production of iPhones will shift to India this year from China, Foxconn Technology Group Chairman Terry Gou said. The company is the largest assembler of Apple Inc.’s handsets and has long concentrated on China.

- Finland looks set to get a more left-leaning government as voters rejected years of austerity in the tightest election in over half a century. Former trade unionist Antti Rinne is poised to become Finland’s first Social Democrat prime minister in 16 years, winning by fewer than 7,000 votes.

Asian equity markets began the week mostly positive as the region took impetus from last Friday’s gains on Wall St. where sentiment was underpinned by a strong start to earnings season and encouraging Chinese data. Nonetheless, ASX 200 (U/C) was dampened amid tentativeness ahead of key earnings and underperformance in gold miners, as well as trade-related news including a further decline of Chinese imports and dispute at the WTO on Australia’s restriction on Chinese 5G technology. The rest of the major Asia-Pac indices are mixed as recent advances in USD/JPY fuelled the upside in Nikkei 225 (+1.4%), while Hang Seng (-0.3%) and Shanghai Comp. (-0.3%) finished lower but were initially boosted as most of the recent Chinese data surpassed estimates including New Yuan Loans, Aggregate Financing, Trade Balance and Exports with the latter at a 5-month high. Furthermore, reports the US softened its demands on China for reducing state industrial subsidies and that both sides have agreed to measures to avoid China currency manipulation, added to the hopes for a looming trade deal. Finally, 10yr JGBs were softer as they tracked the recent losses in T-notes and with demand also dampened by gains in riskier assets as well as a lack of BoJ presence in the market today.

Top Asian News

- The $18 Billion Electric-Car Bubble at Risk of Bursting in China

- Turkey Bleeds Jobs as Unemployment Climbs to Highest in a Decade

- Economist Snatched at Night, Questioned for ‘Insulting’ Erdogan

- Jack Ma Again Endorses Extreme Overtime as Furor Rages On

A tepid start to the week for European equities thus far (Eurostoxx 50 Unch) after the optimism seen in Asia somewhat waned, although Japan’s Nikkei 225 closed higher by almost 1.5% amid currency tailwind. In Europe, Italy’s FTSE MIB (+0.5%) bodes well as the bourse hit eight-month highs, bolstered by banking names amidst the optimism surrounding US banks’ earnings (ahead of Goldman Sachs and Citigroup earnings today). As such the banking sector in Europe outperforms (Stoxx 600 Banks +0.9%) whilst its peers remain mixed. In terms of individual movers, France’s Publicis Groupe (+3.2%) leads the gains in the CAC 40 (+0.1%) on the back of an optimistic revenue update, whilst also supporting its UK peer WPP (+1.3%) in tandem. Elsewhere, Covestro (-4.2%) is the marked laggard in the DAX (Unch) amid ex-dividend trade. Finally, IWG (+22.4%) rests at the top of the Stoxx 600 [Unch] after reports that Japan’s TKP are to acquire the Co.’s workspace leading unit for JPY 50bln coupled with a broker upgrade.

Top European News

- Trafigura to Take Control of Europe’s Biggest Zinc Smelter

- Finns Eject Austerity Government as Leftists Win Election

- Draghi Sticks to Cautious Optimism About Euro-Area Bounceback

- SNB to Raise Rate at Start of 2020, Same Time as ECB, UBS Says

In FX, the Sterling remains underpinned and relatively optimistic after another Article 50 extension to avoid a no deal Brexit and amidst reports that talks between the Conservative and Labour Parties have been more detailed and constructive than some expected, per UK Foreign Secretary Hunt. Cable is eyeing 1.3100 again, albeit with a hefty helping hand from a broadly soft Dollar, as Eur/Gbp trades largely sideways within a 0.8633-50 range. Technically, 1.3132 (last Friday’s high) forms nearest resistance, but data could become pivotal as the week unfolds given jobs and earnings on tap tomorrow, then CPI on Wednesday and retail sales ahead of the long Easter break.

- EUR – As noted above, the single currency is also firm and outperforming the Greenback as the DXY slips a bit further below 97.000 to just under 96.800. Eur/Usd is inching towards 1.1300+ upside chart levels, like a 50% Fib circa 1.1324 and the 200 WMA around 1.1341. Note also, 2 banks are long of the headline pair and looking for sizeable rallies to 1.1650 and even 1.1800.

- NZD/AUD/JPY/CHF/CAD – All narrowly mixed vs the Usd with the Kiwi and Aussie both deriving some support from reports overnight suggesting the US has relaxed some demands over Chinese industrial subsidies in ongoing trade negotiations, as Nzd/Usd hovers between 0.6763-82 and Aud/Usd in a 0.7164-80 range. However, Usd/Jpy has not advanced as much as risk-on sentiment might have suggested overnight with the pair fading just shy of the 2019 peak (112.14) amidst supply from Japanese exporters according to market contacts and now revisiting the 200 WMA (111.98). Meanwhile, the Franc is sitting tight within 1.0010-28 parameters and Loonie between 1.3320-47 ahead of the BoC’s Business Outlook Survey and against the backdrop of softer oil prices that are also undermining the NOK (sub-9.6100 vs the Eur as SEK holds above 10.4700).

- EM – The Try has been hit hard again and got closer to recent lows vs the Usd in wake of latest Turkish jobs data revealing a spike in the rolling 3 month average unemployment rate to 14.7% vs 13.5% previously. The Lira has nursed some losses since on the aforementioned Buck weakness, but remains on the backfoot in a 5.7600-8115 band in stark contrast to the Rand that has extended gains through 14.0000 even though one institution is anticipating a reversal in the Zar’s fortunes and rebound to 14.2700.

In commodities, there has been subdued trade in the energy complex as WTI (-0.8%) and Brent (-0.8%) futures gave up some of Friday’s gains, with the latter now straddling around the psychological USD 71.00/bbl level. Friday’s CFTC data showed that hedge funds raise bullish ICE WTI crude bets by 30.7k to 281.7k lots, whilst speculators increased net long positions in Brent crude (for a fifth consecutive week) by almost 9.5k to just over 358k in the week to April 9th. Over the weekend, Russia’s Finance Minister stated that OPEC+ could decide to raise production (at the June 25/26 meeting) to fight for market share with the US. Currently OPEC+ have agreed to curb output by 1.2mln BPD until June 2019, with IFX noting that Russia’s April production fell by 150k BPD vs the benchmark October level. Back in December, Russia committed to reducing output by 228k BPD from October levels of 11.4mln BPD in a gradual manner which would take place over several months. Elsewhere, the precious metals sector is mostly in the red with gold (-0.4%) edging lower and breaching its 100 DMA (USD 1288/oz) to the downside as last week’s Chinese data somewhat eases fears of a global growth slowdown. Meanwhile, copper (-0.3%) gave up its overnight gains as the risk sentiment became more cautious during early EU trade. Finally, Shanghai steel futures hit a seven-and-a-half year high as the alloy is supported by firm demand, whilst its base metal, Dalian iron ore futures remained near record highs on dwindling Chinese stockpiles which declined the most since 2015, according to SteelHome data.

US Event Calendar

- 8:30am: Empire Manufacturing, est. 8, prior 3.7

- 4pm: Net Long- term TIC Flows, prior $7.2b deficit

- 4pm: Total Net TIC Flows, prior $143.7b deficit

DB’s Jim Reid concludes the overnight wrap

Right. I’m writing this only an hour or so after the first episode of the final Game Of Thrones season had its global premier and am selectively looking through my normal newsfeeds very nervous that I’m going to see spoilers. So if I’ve missed anything today that’s my excuse. I’m not going to watch it until we move into our new house immediately after Easter so I will unleash my dragons to anyone that tells me what happens. Someone important is bound to have died already so that’s going to be tough to avoid if true!! Rather aptly the most difficult spoiler I’ve ever had to avoid was 30 years ago this week around the Masters. In my Easter school holidays I had a paper round and had to be up at 4.30am. As such I had to go to bed early and video tape my hero Nick Faldo’s attempt at the Masters with the view of watching it when I’d finished. Obviously all the papers had the result on the back page (he won). So I had to deliver them all with my eyes closed. I remember it well and the great difficulty involved. The locals must have thought me very odd. The modern equivalent will be me closing my eyes every time I open the internet for the next 10 days. Staying with the Masters, I did find it emotional to see a remarkable comeback victory for Tiger Woods yesterday. Our careers have moved in parallel. He’s a year younger than me, has had 4 knee surgeries to my 3 and 4 back operations while I’ve had several injections in the spine. The only real difference is 15 major championships. But has he ever won an II analyst award? Anyway, nice to see that 40-somethings still have a place in the world.

It might be Easter holiday from Friday but we should know a bit more about the global economy before we go away. The continuation of our tactically bullish view relies a lot on China data bouncing back and dragging Europe along with it. Well on Wednesday we see the important monthly data dump with the release of March’s industrial production and retail sales data and also Q1 Chinese GDP. March’s data will be especially important in assessing whether the recent tick up in PMIs were a genuine positive signal or not. Last Friday’s bumper credit numbers (more later) reinforces our view that China is going through another mini credit cycle. Indeed our Chinese economists put out a note yesterday ( link here ) suggesting that there is upside to their 2019 forecasts. They’ll update these after Wednesday’s numbers.

The other main highlight will be the flash April PMIs on Thursday, with releases for the Eurozone, Germany, France and the United States. It’ll be particularly interesting to see the manufacturing PMI for the Eurozone, which fell for an eighth consecutive month in March, moving deeper into contractionary territory with a 47.5 reading. The German manufacturing PMI was even more contractionary last month, with a 44.1 reading. If we’re right on China these should be turning up soon.

In a similar vein, Germany’s ZEW survey for April comes out on Tuesday, which is an important number in light of the above. In March, the ZEW survey of current activity fell to 11.1, its lowest level since December 2014, although the expectation reading rose to -3.6, which was its highest since March 2018, so it’ll be worth looking to see if there are any signs of improvements here.

The main other highlights are US Retail Sales (Thursday) and Q1 US earnings season picking up through the week. Retail Sales will be looked at for signs the consumption soft patch either side of the turn of the year is behind us. In terms of earnings today we’ll see Goldman Sachs and Citigroup reporting. Tomorrow there’ll be earning releases from Bank of America, Netflix, IBM and Johnson & Johnson. On Wednesday, there’ll be Morgan Stanley and PepsiCo, and on Thursday, there’ll be Philip Morris International and American Express. The day by day week ahead is at the end.

Over the weekend, the US President Trump renewed his criticism of the Fed by tweeting, “If the Fed had done its job properly, which it has not, the Stock Market would have been up 5000 to 10,000 additional points.” I can only assume he means the Dow rather than the S&P 500! He further added, “Quantitative tightening was a killer, should have done the exact opposite!” President Trump’s comments came after the IMF conference in Washington where ECB President Draghi said that he was “certainly worried about central bank independence” and especially “in the most important jurisdiction in the world.” Elsewhere, at the same IMF conference Germany came under pressure from global policy makers to ease fiscal policy.

Meanwhile, on US/China trade talks, Treasury Secretary Steven Mnuchin said that the US and China are discussing whether to hold more in-person meetings after talks in recent weeks while adding that “we’re hopefully getting very close to the final round of these issues.” He also said on the enforcement mechanism that, “I would expect that the enforcement mechanism works in both directions, that we expect to honor our commitments, and if we don’t, there should be certain repercussions, and the same way in the other direction.”

Asian markets have started the week on a positive note with the Nikkei (+1.47%), Hang Seng (+0.58%), Shanghai Comp (+1.12%) and Kospi (+0.49%) all up. Elsewhere, futures on the S&P 500 are trading flattish (-0.04%).

In other news, Finland will likely get a more left-leaning government after voters, in the tightest election in memory, rejected years of austerity and seemingly demanded more spending on welfare. Former trade unionist Antti Rinne is poised to become Finland’s first Social Democrat prime minister in 16 years after winning by fewer than 7,000 votes but his party faces tough coalition talks ahead as the ultra nationalist Finns Party emerged as the second-biggest party, beating the establishment conservative National Coalition for the first time.

On Brexit, David Lidington, PM May’s de facto deputy, said on Sunday that the government believed it would be possible to get “the benefits of a customs union” – which Labour wants – “but still have a flexibility for the U.K. to pursue an independent trade policy on top of that.” He added that even though parliament is in recess until April 23, negotiations will continue. Sterling is up +0.18% this morning.

Recapping last Friday and the week overall now. Equity markets advanced on Friday with the S&P 500 +0.66% (+0.51% for the week), the NASDAQ +0.46% (+0.57%) and the STOXX 600 +0.16% (-0.18%). This was the third consecutive weekly gain for the S&P 500, which closed at its highest level for six months. Financials led the advance following strong earnings from JPMorgan, which reported net income of $9.2bn in the first quarter, sending its shares up +4.69% on Friday. They also reported net interest income of $14.6bn in the first quarter, up 8% on the same quarter a year ago, while return on common equity reached 16%. Impressive numbers. The STOXX Banks index ended the day +2.78% (+3.05% – week) to reach its highest level since October (also helped by the China data and rising bund yields). The S&P 500 Banks index was also up +2.40% (+2.39%).

The market was also supported by stronger-than-expected data releases. Firstly, we had the credit numbers out of China where new total social financing came in at RMB2.86tr, much stronger than the market consensus forecast of RMB1.85tr. New bank loans also surprised on the upside at RMB1.69tr compared with consensus of RMB1.25tr. M2 (broad money) growth rebounded to 8.6% in March from 8.0% in Feb but the most significant part, according to our economists, was the rebound in M1, whose growth rate jumped to 4.6% in March, up more than 4ppts from its trough at 0.4% in Jan. Again see their report mentioned earlier for more.

The Chinese trade data was also positive, with the March trade balance coming in at $32.65bn (vs. $5.70bn expected) indicating that exports had recovered. In Europe, the Eurozone industrial production figures fell by -0.2% mom in February but above the -0.5% decline expected, while January’s figure was revised up to 1.9% mom (from 1.4% previously). However, in the US the University of Michigan consumer sentiment index fell more than expected, coming in at 96.9 (vs. 98.2 expected).

Government bond yields rose as the global data was generally pretty positive, with ten-year bund yields +6.4bps on Friday (+4.9bps on the week) to return to positive territory (0.054%). 10yr Treasury yields rose +6.8bps on Friday (+7.0bps – week), and the US 2s10s curve steepened to end the day +2.9bps (+1.8bps). Bond yields in the European periphery came off their recent lows with the rise in yields but spreads edged tighter. In Greece though, ten-year yields fell to their lowest level since September 2005.

end

3. ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED DOWN 10.84 POINTS OR 0.34% //Hang Sang CLOSED DOWN 99.04 POINTS OR .33% /The Nikkei closed UP 298.55 POINTS OR 1.37%/ Australia’s all ordinaires CLOSED UP .01%

/Chinese yuan (ONSHORE) closed UP at 6.7072 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 64.57 dollars per barrel for WTI and 71.66 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.7072 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7077 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/

Funny: Kim gives Trump until the end of the year to become more flexible re sanctions or else he walks

(courtesy zerohedge)

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

China/USA:

As far as the trade talks are proceeding, the answer is quite clear: they are not getting real progress on the essential beefs that the USA has with China. The USA is now backtracking on enforcement and they are caving on demands Beijing scrap industrial subsidies.

(courtesy zerohedge)

Washington Backtracks On Enforcement Progress, Caves On Demands Beijing Scrap Industrial Subsidies

Despite Trade Rep. Robert Lighthizer’s insistence that Washington leverage its position of advantage – i.e. the unassailable fact that its tariffs had contributed to a precarious deceleration in Chinese economic growth – the Trump Administration’s trade team has repeatedly caved to Beijing. First, the administration compromised on enforcement (the administration has reportedly punted it to 2025) to the currency manipulation. And now it has reportedly softened its demands for the ‘structural economic reforms’ that Trump had insisted on as part of the final deal.

According to Reuters, US negotiators have ‘tempered’ their demands that Beijing roll back some of its industrial state subsidies as part of the trade deal. Washington’s demands were reportedly met with ‘strong resistance’ from Beijing.

The issue is a thorny one because China’s brand of state-directed capitalism is deeply tied up with the tax breaks and other advantages that Beijing bestows on state-owned firms, and it’s possible that many of these firms could fail without the government’s support, potentially setting off a destabilizing chain reaction.

The issue of industrial subsidies is thorny because they are intertwined with the Chinese government’s industrial policy. Beijing grants subsidies and tax breaks to state-owned firms and to sectors seen as strategic for long-term development. Chinese President Xi Jinping has strengthened the state’s role in parts of the economy.

And as the Trump administration looks to secure a deal in the next month or so, expect them to cave on more of their demands and focus on priorities that they consider “achievable.”

These include: Ending forced technology transfers, improving intellectual property protection, expanding access to Chinese markets for American firms (and in particular American tech firms).

In what sounded like an attempt to spin Washington’s walk-backs on subsidies and enforcement, Treasury Secretary Steve Mnuchin – one of the officials tasked with leading the trade delegation – said during a Monday morning interview that there was “more work to do” including on the issue of enforcement, after saying last week that the two sides had agreed to opening ‘enforcement offices’.

When it comes to restrictions on state subsidies, expect any language in the deal to be vague, allowing Beijing substantial wiggle room to largely maintain the status quo.

So, if China’s economy is in such dire straits, why is the US caving? Well, because President Xi can’t accept a deal that would make him look weak, which gives him very little room to concede.

Washington has detailed more than 500 different subsidies it has said China applies in notifications to the WTO.

“It’s not that there won’t be some language on it, but it is not going to be very detailed or specific,”one source familiar with the talks said in reference to the subsidies issue.

“If U.S. negotiators define success as changing the way China’s economy operates, that will never happen,” said the other source with knowledge of the trade talks.

“A deal that makes Xi look weak is not a worthwhile deal for Xi. Whatever deal we get, it’s going to be better than what we’ve had, and it’s not going to be sufficient for some people. But that’s politics,” that source said.

China promised to end its subsidies earlier this year, but never said how it would accomplish this. To be sure, as Reuters points out, there are ways that maintaining subsidies could work to America’s advantage, since most of the firms that would be making the tens of billions of dollars of annual agricultural purchases are mostly recipients of these subsidies.

One of the key sticking points in the negotiations is the removal of the $250 billion in U.S. tariffs. It is broadly expected in the trade community that U.S. negotiators want to keep some tariffs on Chinese goods, which Washington sees as retaliation for the years of damage done to its economy by Beijing’s unfair trade practices.

The role of the state firms may benefit the United States in another part of the trade deal. The Trump administration wants China to make big-ticket purchases of over a trillion dollars of U.S. goods in the next six years to reduce its trade surplus. The companies likely to make the purchases are the state-run firms, both sources said.

“The purchasing, for example, reinforces the role of the state sector because the purchasing is all being done through state enterprises,” one of the sources said.

Another point of contention between the two countries, telecommunications, may drive China to increase the state’s role rather than reduce it, the source said.

In a separate report, Bloomberg said that China is weighing a request from Washington to shift some tariffs on key agricultural goods to other products to help the administration sell the trade deal to farmers, a key voting bloc for Trump, ahead of the 2020 election. While the exact nature of the arrangement proposed by the US wasn’t reported, it shows that political considerations are increasingly becoming a factor as the talks enter their final stretch.

While some have argued that Trump could tout any deal as a win, even if China refuses to meet Washington’s core demands and instead focuses on agricultural purchases, the political problem could become a serious Catch-22 for Trump.

4/EUROPEAN AFFAIRS

i)Italy

Salvini is positioning Italy ready for the confrontation with Brussels

(courtesy TomLuongo)

Salvini Is Positioning Italy For Confrontation

Authored by Tom Luongo via The Strategic Culture Foundation,

Italy’s Matteo Salvini is riding high right now. Having weathered a couple of cheap legal moves to derail his assault on the European Parliament this May, Salvini is working to galvanize Euroskepticism across the continent into a viable political force.

He’s got his work cut out for himself.

But, he has at least two major allies. Marine Le Pen of the National Rally in France and Viktor Orban, the leader of Hungary. Salvini and Le Pen met last week to announce they would be campaigning together for the European elections as well as a major summit in Milan soon.

This is only the beginning, however.

I’ve been saying for over a year now that Salvini needs to be the person who lays the foundation for a wholesale revolt against the European Union and Italy’s participation in the euro.

His Lega party have skyrocketed in the polls, reversing the dynamic between it and coalition partner Five Star Movement. It’s a coalition that is of the kind which frightens the political establishment in Europe because it isn’t formed on the traditional left-right false divide.

It is a populist one united on the common cause of overthrowing the corrupt, corporatist system which most western governments are fronts for.

And since coming to power last year there have been multiple attempts to drive wedges between these supposedly strange bedfellows. All of them have failed. And part of the reason for that has been the surging popularity of Lega and Salvini.

Having survived to this point and scared the EU a few times with Trump-like ‘big asks’ on the budget and immigration reform, Salvini and his partner in populism Luigi Di Maio are looking towards the EP elections as a first major test of their government.

And being able to bring together groups from all over Europe to agree on a common platform to challenge the French/German axis of power would put them in a good position in the second half of 2019 to push things farther, especially as it pertains to Italy’s insane fiscal situation.

I realized early on that Salvini was two things. He was both a radical who was also methodical. He’s not flaming out in a blaze of glory here. He’s building his case against the EU slowly, allowing history to come to him.

He’s stayed far away from the Brexit debacle, even though he knows he has the power to stop the betrayal of the vote and force the divorce. But rather than do that it’s better to let the process play itself out and reveal the ugly truth of it all while he takes notes and reloads for the next attack on the EU.

If Euroskeptics outperform the current polling which has them at around 30-32% of the seats and Salvini can rally them under one banner to become the biggest party in the EP, then that would send the right kind of message back home to Italy.

There is something big brewing between Salvini and Di Maio. First, they sign up with China’s Belt and Road Initiative, whose second major summit is later this month. This angered both Trump and Angela Merkel.

All in a day’s work.

But the bigger news, in my mind, is the Italian parliament is pushing to repatriate the nation’s gold reserves from the Bank of Italy. Two laws are under consideration:

One law would instruct the central bank’s owners, most of them private banks, to sell their shares to the Italian Treasury at prices from the 1930s.

The other law would declare the Italian people to be the owners of the Bank of Italy’s reserve of 2451.8 metric tons of gold, worth around $102 billion at current prices.

The Bank of Italy is mostly owed by Italian commercial banks who are now both insolvent and at risk of EU banking rules. This puts them at risk of seeing depositors bailed-in and the banks forcibly restructured overnight by the European Central Bank.

Don’t believe me? Go back and look at what happened to Banco Popular of Spain in 2017. It was sold off to Santander for $1 after the ECB declared it non-viable. It wiped out the shareholders over a weekend and life went on as if nothing had happened.

But it did happen and that did nothing to reassure investors that there is even a hope in hell of getting your investment back out of a European bank if that’s how the ECB can act. In some ways, why do you think it’s going to be so difficult for Deutsche Bank to raise the necessary capital ($6 to $10 billion) to merge with equally-insolvent Commerzbank?

If you had a choice between Deutsche and J.P. Morgan Chase at this point what would you do? US banking system may be corrupt but it isn’t stupid enough to toss aside the one thing that ensures safe-haven foreign capital flows, that investors come first.

I may not like Chase, but I’m putting my money on it over Deutsche any day of the week and especially not on a Sunday evening while Mario Draghi is on the scene.

If those Italian banks are dealt with similarly by the ECB as Banco Popular we could easily see their ownership transferred to their creditors and, by extension, the ownership of the Bank of Italy right along with it.

Talk about undermining national sovereignty!

And what’s the only thing of value on the Bank of Italy’s balance sheet? The gold.

Salvini and Di Maio’s government urging the Bank of Italy to sell the gold back to the government at 1930’s prices is a way to ensure that Italy’s gold reserves stay unencumbered and available to back any new version of the lira if things get to that point.

Like Brexit negotiations the nuclear option, clean divorce, must be a credible threat, i.e. a No-Deal Brexit and unilateral withdrawal from the euro.

This threat by the Italians has been simmering for a while and every time it comes up the talking points from the regime press are the same. It threatens the independence of the central bank. The gold could be sold to pay for populist spending programs. Blah blah blah.

No, the real threat is with the Italian gold owned by the Italian people the Italian government could start all over again with a new currency.

And that is what this is all about.

So, first, Salvini goes into the European Parliament with a solid voting bloc to disrupt proceedings and further undermine Angela Merkel’s powerbase. Second, he and Di Maio take that success back to Rome and use that to engage real EU reform of the financial system.

And if they don’t get what they want, if Merkel holds fast to her policy of Germany strip-mining of Europe via austerity, then they go on the offensive with 2410 tonnes of gold in their back pocket. This will be an easy sell as the European economy implodes further.

It’s not like Germany is in a position to drive a strong bargain with its economy rapidly plunging towards recession.

Any small shock at this point will cause a massive run on European assets. We’ve just seen a enormous move into safe-haven assets in the past month.

The European bond markets are ripe for a sharp reversal on any catalyst.

To pull all off their ‘revolution’ in the EP, however, Salvini and Le Pen will likely have to play nice with Poland on Russia, not pushing for sanctions relief just yet. To unite Euroskeptics over the next seven weeks will be difficult. But, Salvini has shown flexibility to this point with his own coalition.

What makes you think he’s not capable of bringing Poland on side?

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

Turkey