GOLD: $1274.60 DOWN $0.10 (COMEX TO COMEX CLOSING)

Silver: $14.99 UP 1 CENT (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1274.00

silver: $14.99

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING:78/91

GOLDMAN ISSUING: 5

EXCHANGE: COMEX

CONTRACT: APRIL 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,272.600000000 USD

INTENT DATE: 04/16/2019 DELIVERY DATE: 04/18/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

365 C ED&F MAN CAPITA 1

661 C JP MORGAN 78

686 C INTL FCSTONE 1

737 C ADVANTAGE 82 12

773 C G.H. FINANCIALS 2

845 C GOLDMAN SACHS C 5

905 C ADM 1

____________________________________________________________________________________________

TOTAL: 91 91

MONTH TO DATE: 5,455

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 91 NOTICE(S) FOR 9100 OZ (0.283 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 5455 NOTICES FOR 545500 OZ (16.967 TONNES)

SILVER

FOR APRIL

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 774 for 3,870,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE :$5194 UP $20

Bitcoin: FINAL EVENING TRADE: $5196 UP 22

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI AFTER A ONE DAY HIATUS, CONTINUED TO MARCH HIGHER TO THE TUNE OF A STRONG SIZED 1666 CONTRACTS FROM 223,117 UP TO 224,783 DESPITE YESTERDAY’S 3 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE MUST HAVE HAD CONSIDERABLE NEW SPREADS INITIATED BY OUR SPREADERS (BANKERS).

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A VERY STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 2960 FOR MAY, 0 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2960 CONTRACTS. WITH THE TRANSFER OF 2960 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2960 EFP CONTRACTS TRANSLATES INTO 14.80 MILLION OZ ACCOMPANYING:

1.THE 3 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

AND NOW 3.870 MILLION OZ STANDING FOR SILVER IN APRIL.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

24,296 CONTRACTS (FOR 13 TRADING DAYS TOTAL 24,296 CONTRACTS) OR 121.48 MILLION OZ: (AVERAGE PER DAY: 1868 CONTRACTS OR 9.344 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 121.48 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 17.34% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 689.65 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1666 DESPITE THE 3 CENT FALL IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2960 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GIGANTIC SIZED: 4,626 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2960 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1732 OI COMEX CONTRACTS. AND ALL OF THIS HUMONGOUS DEMAND HAPPENED WITH A 3 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.98 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.116 BILLION OZ TO BE EXACT or 160% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR nil OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ AND NOW APRIL AT 3.870 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A FAIR SIZED 1073 CONTRACTS, TO 440,581 DESPITE THE HUGE DROP IN THE COMEX GOLD PRICE/(A LOSS IN PRICE OF $13.60//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GIGANTIC SIZED 15,164 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 15,164 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 440,581. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 16,237 CONTRACTS: 1073 OI CONTRACTS INCREASED AT THE COMEX AND 15,154 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 16,237 CONTRACTS OR 1,623,700 OZ OR 50.50 TONNES. YESTERDAY WE HAD A HUGE FALL IN THE PRICE OF GOLD TO THE TUNE OF $13.60.…AND YET WITH THAT, WE STILL HAD A HUMONGOUS GAIN IN TONNAGE OF 50.50 TONNES!!!!!!.??????????????????????????????????????????

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 87,551 CONTRACTS OR 8,755,100 OR 272.32 TONNES (13 TRADING DAYS AND THUS AVERAGING: 6734 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAYS IN TONNES: 272.32 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 272.32/3550 x 100% TONNES = 7.67% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1647.90 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIR SIZED INCREASE IN OI AT THE COMEX OF 1073 DESPITE THE HUGE LOSS IN PRICING ($13.60) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A HUMONGOUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 15,164 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 15,164 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC GAIN OF 16,237 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

15,164 CONTRACTS MOVE TO LONDON AND 1073 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 50.50 TONNES). ..AND THIS HUGE DEMAND OCCURRED WITH A FALL IN PRICE OF $13.60 IN YESTERDAY’S TRADING AT THE COMEX.????

we had: 91 notice(s) filed upon for 9100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $0.10 TODAY

A BIG CHANGE WITH RESPECT TO GOLD INVENTORIES AT THE GLD:

A HUGE WITHDRAWAL OF 1.76 TONNES OF GOLD//THIS GOLD WAS PROBABLY USED YESTERDAY IN THEIR RAID AGAINST GOLD//

INVENTORY RESTS AT 752.27 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 1 CENT TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV//

/INVENTORY RESTS AT 309.167 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A STRONG SIZED 1666 CONTRACTS from 223,117 UPTO 224,783 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

HERE IS HOW THE CROOKS USED SPREADING AS WE ENTER AN ACTIVE DELIVERY MONTH. THUS SILVER HAS THE ACTIVE MONTH OF MAY COMING UP AND THUS SPREADERS DO THE FOLLOWING:

“YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF APRIL BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

THE CROOKS DID NOT DISAPPOINT US TODAY AS THE OI INCREASED BY A HUGE AMOUNT DESPITE THE SILVER LOSS. OF 3 CENTS

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 2960 FOR MAY AND JULY: 0 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2960 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1666 CONTRACTS TO THE 2960 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUMONGOUS SIZED GAIN OF 4626 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 23.46MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH. AND NOW 3.870 MILLION OZ FOR APRIL.

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 3 CENT FALL IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 2960 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 9.52 POINTS OR 0.29% //Hang Sang CLOSED DOWN 5.19 POINTS OR 0.02% /The Nikkei closed UP 56.31 POINTS OR 0.25%/ Australia’s all ordinaires CLOSED DOWN .35%

/Chinese yuan (ONSHORE) closed UP at 6.6892 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 64.41 dollars per barrel for WTI and 72.15 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.6892 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6861 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA

b) REPORT ON JAPAN

Japan/China/HUAWEI

After cutting off ZTE equipment last year, Japan may stop the use of Huawei 5 G technology in Japan and that is upsetting the Chinese to no end

( zerohedge)

3 China/Chinese affairs

i)China/

Although the huge stimulus in March had a strong effect on the numbers today, the internal consumption is of great concern to China. They point to three areas to show China’s continual problems:

the collapse in land sales, weak imports, and the unexpected decline in electricity consumption.

( zerohedge)

ii)Obviously last month’s stimulus was not enough: China is now preparing a new stimulus to subsidize car and appliance purchases

( zerohedge)

iii)China’s bond vigilantes are watching closely as data suggests a huge spike in their PMI due to the massive stimulus. However bond yields are also rising.

( zerohedge)

4/EUROPEAN AFFAIRS

i)UK

Tory support is faltering and Nigel Farage’s new Brexit party is picking up steam.

( Mish Shedlock/Mishtalk)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

IRAN

IRAN passes a vote declares the USA Central Command (CENTCOM) A “TERROR ORGANIZATION” meaning uSA troops in the Middle East will be treated as terrorists.

(courtesy zerohedge)

6. GLOBAL ISSUES

The Bureau of Economic Policy in the Netherlands reveal that trade volume dropped a considerable 1.8% from last November until January. No doubt that this was the reason for China’s huge stimulus move in March

( zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning/FOMC

ii)Market data

a)The deficit shrinks as exports to China surge. Imports fell a bit. However the big gain in trade was due to the exports of aircrafts and that will shrink badly due to the grounding of the Boeing’s troubled planes.

( zerohedge)

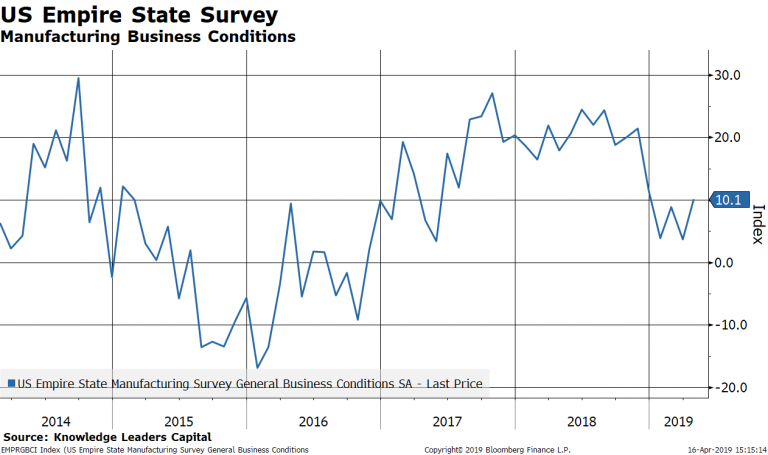

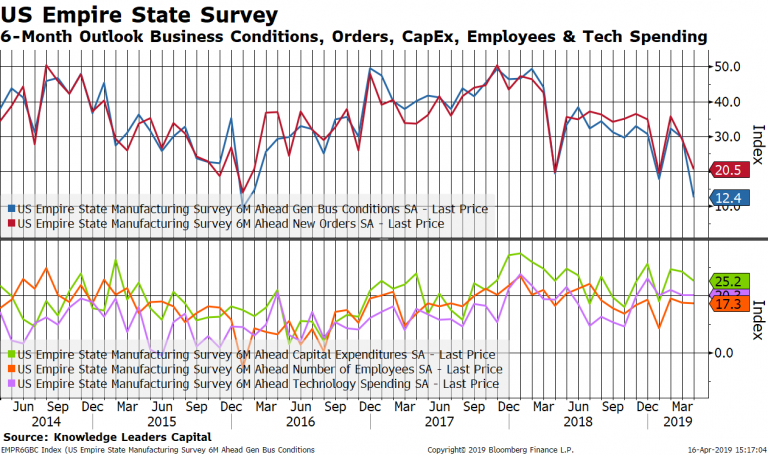

b)Manufacturing weakness continues as it is near its two year nadir

( zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

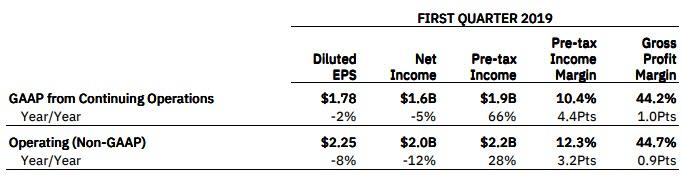

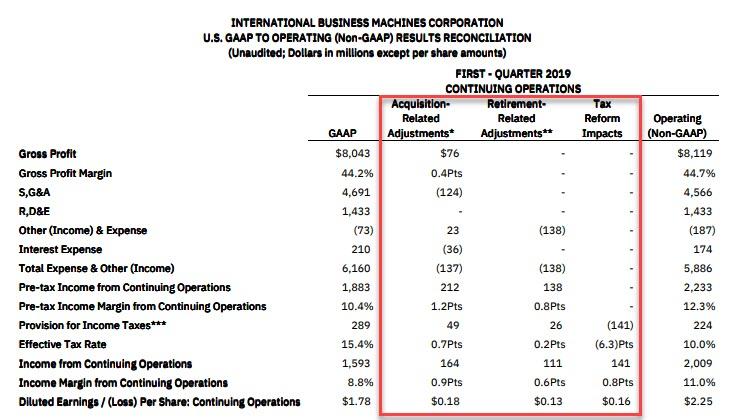

a)IBM tumbles after reporting its worst revenue in 17 years.

( zerohedge)

(courtesy Michael Snyder)

c)That escalated fast: the beige book downgrades the USA economy as it is slowing down at a great pace

(courtesy zerohedge)

iv)SWAMP STORIES

There seems to be a secret pack between Cummings, Waters and Schiff to target Trump as they try to subpoena all of his financial and banking records

(courtesy Sara Carter)

b)Barr clamps down on the catch and release program in the USA. Illegal immigrants will now longer be allowed to be released on a bond that they promise to appear before an immigration judge. It also means that Barr expands the “indefinite detention” period for migrants

(courtesy zerohedge)

c)Yuma shuts its doors to illegals as it declares a state of emergency

( Sara Carter.Jennie Taer)

end

Let us head over to the comex:

AFTER APRIL, WE HAVE THE ACTIVE DELIVERY MONTH OF MAY AND HERE THE OI FELL BY 1979 CONTRACTS DOWN TO 100,492. CONTRACTS.. THE NEXT MONTH OF JUNE GAINED 13 CONTRACTS TO 134. AFTER JUNE, THE VERY BIG DELIVERY MONTH OF JULY HAD A GAIN OF 3346 CONTRACTS UP TO 85,699 CONTRACTS.

World Trade Suffers Biggest Collapse Since Financial Crisis

The recent collapse in world trade volume is the worst since the financial crisis and as dangerous as during the dot-com bubble of the early 2000s, according to The Telegraph.

Data from the CPB Netherlands Bureau for Economic Policy Analysis revealed that world trade volume dropped 1.8% in the three months to January compared to the preceding three months as a synchronized global downturn gained momentum.

“An industrial slump has been triggered by a perfect storm of factors, including China’s slowdown, the car industry downturn, Brexit paralysis and Donald Trump’s attempt to upend the international trade system with tariffs on European and Chinese goods,” explained The Telegraph.

A further escalation of the trade war between the U.S. and China could spark a world trade recession. Already, Washington has imposed steep tariffs on Chinese imports worth $250bn in a tit-for-tat battle with industrial centers in Asia and Germany experiencing sharp drops in trade in recent months.

The Telegraph describes the sudden loss in trade momentum is equivalent to the months after the dot com bubble imploded in 2001 when trade volumes sank as much as 2.2%. Today’s current move is the biggest fall since the financial crisis of 2007–2008 when global trade plummeted, diving as much as 12.7%.

The International Monetary Fund warned last week that this is a “delicate moment” for the global economy as many countries are in the midst of a severe slowdown.

The global economy has “lost further momentum” in the last six months, said IMF Managing Director Christine Lagarde.

Lagarde pinned trade volume deterioration on decelerating global growth and “the impact of increased trade tensions on spending” on producer goods.

The global downturn in trade is widespread geographically. The synchronized slowdown is expected to stabilize beyond 2020; however, in the meantime, it’s likely the world could be headed for a trade recession, if not already in one.

Secure Storage In Zurich For Free For Six Months

Until this Thursday (April 18), when you invest the minimum amount of $€£ 10,000 (no maximum) in physical gold and or silver for storage in our Loomis vaults in Zurich, Switzerland, you will pay zero storage fees for the first six months from the date of your purchases. This applies to all investments for Secure Storage in Zurich.

All gold and silver is stored in professionally managed, specialist, high security precious metals vaults. In addition to this gold and silver stored in GoldCore Secure Storage is stored on a fully allocated and fully segregated basis – the safest way to store precious metals – ensuring liquidity, competitive pricing and ownership.

Complimentary Silver Bullion Coin

In addition to the 6 months’ worth of free Secure Storage we also appreciate that our clients enjoy seeing and holding their precious metals and that’s why we will also be delivering to you fully insured, a freshly minted, 2019, one ounce, legal tender, silver bullion coin. You can choose between two of the world’s most popular silver coins: the 2019 American Silver Eagle or the beautifully minted 2019 British Silver Britannia.

Complimentary Book

Because our mission is to ensure that our clients and community are kept informed and protected, each order also comes with a copy of “The New Case for Gold”, the fascinating and insightful book by gold expert and New York Times Best Selling author Jim Rickards.

More information about the offer can be accessed here and if you wish to avail of the offer simply wire funds and transact online or on the phone by close of business this Thursday (1700, April 18). Mention the Exclusive Offer code ‘offermarch2019’ on the phone or by email – support@goldcore.com

News and Commentary

Gold near 4-month low as China GDP fuels risk sentiment (Reuters.com)

Gold falls 1 pct to 2019 low as equities, dollar gain (Reuters.com)

White House talking to other possible Fed candidates: Kudlow (Reuters.com)

Oil prices rise for a second day, high of year, on China demand, U.S. stockpile drop (Reuters.com)

Precious Metals Update Video: Silver pointing to $14.55 support (SilverSeek.com)

World Trade Suffers Biggest Collapse Since Financial Crisis (ZeroHedge.com)

China’s Bond Vigilantes Loom As Economic Data Stabilizes (ZeroHedge.com)

Gold Prices (LBMA PM)

16 Apr: USD 1,283.75, GBP 981.30 & EUR 1,137.40 per ounce

15 Apr: USD 1,286.75, GBP 982.43 & EUR 1,137.23 per ounce

12 Apr: USD 1,296.15, GBP 991.68 & EUR 1,146.06 per ounce

11 Apr: USD 1,304.65, GBP 997.01 & EUR 1,152.43 per ounce

10 Apr1: USD 1,304.80, GBP 998.04 & EUR 1,157.44 per ounce

09 Apr: USD 1,303.00, GBP 995.13 & EUR 1,155.00 per ounce

Silver Prices (LBMA)

16 Apr: USD 14.94, GBP 11.42 & EUR 13.22 per ounce

15 Apr: USD 14.93, GBP 11.39 & EUR 13.20 per ounce

12 Apr: USD 15.06, GBP 11.51 & EUR 13.31 per ounce

11 Apr: USD 15.25, GBP 11.66 & EUR 13.53 per ounce

10 Apr: USD 15.25, GBP 11.66 & EUR 13.53 per ounce

09 Apr: USD 15.25, GBP 11.66 & EUR 13.53 per ounce

Recent Market Updates

– Exclusive Offer: Secure Gold and Silver Storage In Zurich For Free For Six Months

– There Is Too Much Debt In The World – World Bank

– How to Store Gold in an Uncertain World

– The ECB Is Struggling With Inflation, Interest Rates and The Outlook

– Russia Dumps U.S. Dollars and Buys Gold As “Safety Metal”

– How A ‘No Deal’ Brexit Could Lead To The “Lehmanization” Of Europe

Exclusive Offer: S

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.6892/

//OFFSHORE YUAN: 6.6861 /shanghai bourse CLOSED UP 9.52 or 0.29%

HANG SANG CLOSED DOWN 5.19 points or 0.02%

2. Nikkei closed UP 56.31 POINTS OR 0.25%

3. Europe stocks OPENED GREEN/EXCEPT LONDON

USA dollar index FALLS TO 96.93/Euro RISES TO 1.1309

3b Japan 10 year bond yield: RISES TO. –.01/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.88/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 64.41 and Brent: 72.15

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +09%/Italian 10 yr bond yield UP to 2.63% /SPAIN 10 YR BOND YIELD UP TO 1.12%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.54: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.31

3k Gold at $1276.00 silver at:15.00 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 25/100 in roubles/dollar) 63.83

3m oil into the 64 dollar handle for WTI and 71 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.00 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0088 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1408 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.09%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.61% early this morning. Thirty year rate at 3.01%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.7402..GETTING VERY DANGEROUS

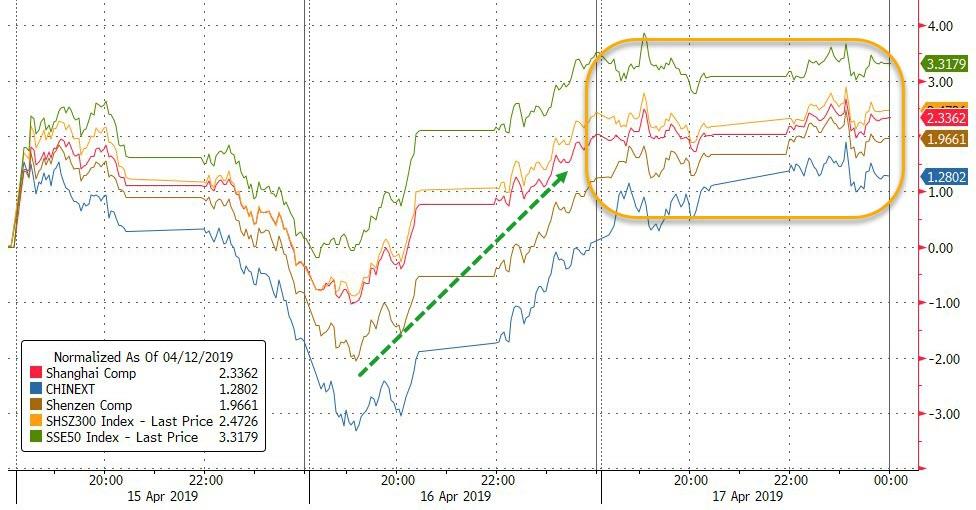

Global Stocks Rise Following Blowout Chinese Data

Following last night’s blockbuster Chinese data, when virtually every key data point beat expectations in some cases notably, global markets and bond yields are broadly higher, if mutedly so, as traders evaluated whether China’s economic recovery will be enough to put rate hikes back on the table even as Germany’s economy ministry revised its growth forecast lower to just 0.5%. Global markets and futures are a sea of green but tentatively so as

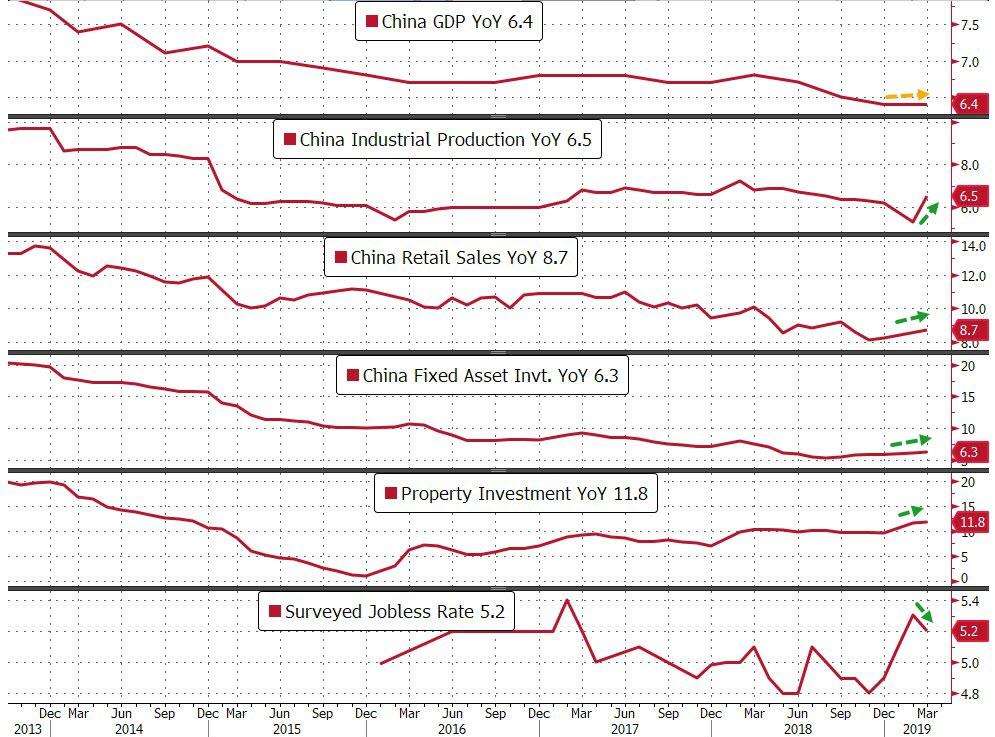

As reported last night, China’s Q1 GDP came in one tenth above expectations at 6.4% yoy while all of the March activity indicators surprised on the upside with industrial production surging at +8.5% yoy (vs. +5.9% yoy expected) – the highest since July 2014. Retail sales printed at +8.7% yoy (vs. +8.4% yoy expected), YTD fixed assets ex rural came in line with consensus at +6.3% yoy and the jobless rate fell one tenth to 5.2%. This data confirms what many had been expecting given the massive injection in credit helped push China’s credit impulse numbers higher in recent months and should help European data over the coming weeks. The downside to the numbers will be a more hawkish PBOC. Their monetary policy statement yesterday described the appropriate policy stance as “moderately tight” and it seems today they injected much less liquidity into the market as was expected. So that’s the only sting in the tail to these numbers.

The far stronger Chinese data appears to have also helped short circuit rate cut expectations for the time being, and as a result the risk asset response was marginal at best, with US equity futures rising less than 0.2% with gains were capped by disappointing quarterly reports from Netflix and IBM, while the Shanghai Composite flirted with the unchanged line for much of the session before closing just 0.3% higher.

Meanwhile a forecast of faster growth due to demand from China by semiconductor equipment maker ASML, pushed U.S. chipmakers higher in premarket trading, adding to yesterday’s historic Qualcomm gains after the company settled its long-running litigation with Apple; Intel, Advanced Micro Devices and Nvidia gained between 0.5% and 3.6%. At the same time, IBM declined 3.5% after reporting a bigger-than-expected drop in quarterly revenue.

Where things got interesting, is that after a subdued start, European stocks pushed into positive territory after reports China was considering even more stimulus measures to bolster consumption, with autos the notable outperformer, shrugging off weak sales numbers. Meanwhile, the German Government cut its 2019 GDP growth forecast to 0.5% vs. prev. 1.0%, in line with expectations, even as it projects a rebound to 1.5% in 2020; Inflation is seen at 1.5% in 2019, 1.8% in 2020.

This followed an advance in Asian shares, with Japan and Shanghai rising modestly after data showed China’s economic growth, industrial production and retail sales all better-than-expected

With earnings season in full swing, analysts now expect first-quarter S&P 500 profits to have dropped 1.8% year-on-year, according to Refinitiv data. While a solid improvement over recent estimates, it would still mark the first earnings contraction since 2016. Of the 42 S&P 500 companies that have posted so far, 81% have beaten consensus, compared with the 65% average beat rate going back to 1994.

While Brexit news are on the backburner this week, local UK Conservative party chairmen are circulating a petition which seeks an Extraordinary General Meeting to pass a no-confidence vote in PM May. The report states that the party will be obliged to hold a meeting if more than 65 association chairmen sign the motion; so far between 40-50 have signed it, with expectations that the threshold could be passed next week.

In global rates, Bund and USTs grind lower, 10Y German yields rise ~2bps with the long end steady after a decent auction. Gilt curve bear flattens slightly, 10Y Gilt futures find support at Monday’s lows after U.K. inflation stays below target. BTPs trade sideways, peripheral yield spreads all marginally tighter to core.

US Treasury futures broadly held earlier losses spurred by strong Chinese economic data. Yields were cheaper by 1.5bp-2bp from 5-year to long end, less in front end, steepening 2s10s by ~1bp; 10-year yields 2.605% after touching 2.612% during European morning, highest since March 20. Futures volumes were robust through 7am ET, 20% above 20-day average in TYM9.

In FX, the Bloomberg dollar index traded lower but within Tuesday’s range while commodity currencies traded well, with AUD the best performer in G-10, NZD continues to lag after soft inflation data. Yuan strength continues in Europe, rising ~0.4% vs USD following China’s data report.

In commodities, WTI crude traded sideways around Tuesday’s best levels as base metals predictably pushed higher led by copper and aluminium.

On the economic front, a Commerce Department report, due at 8:30 a.m. ET, is expected to show U.S. trade deficit widening to $53.5 billion in February; we also get data on wholesale inventories and the Fed’s Beige Book. Abbott, Morgan Stanley, PepsiCo, and Alcoa are among companies reporting earnings.

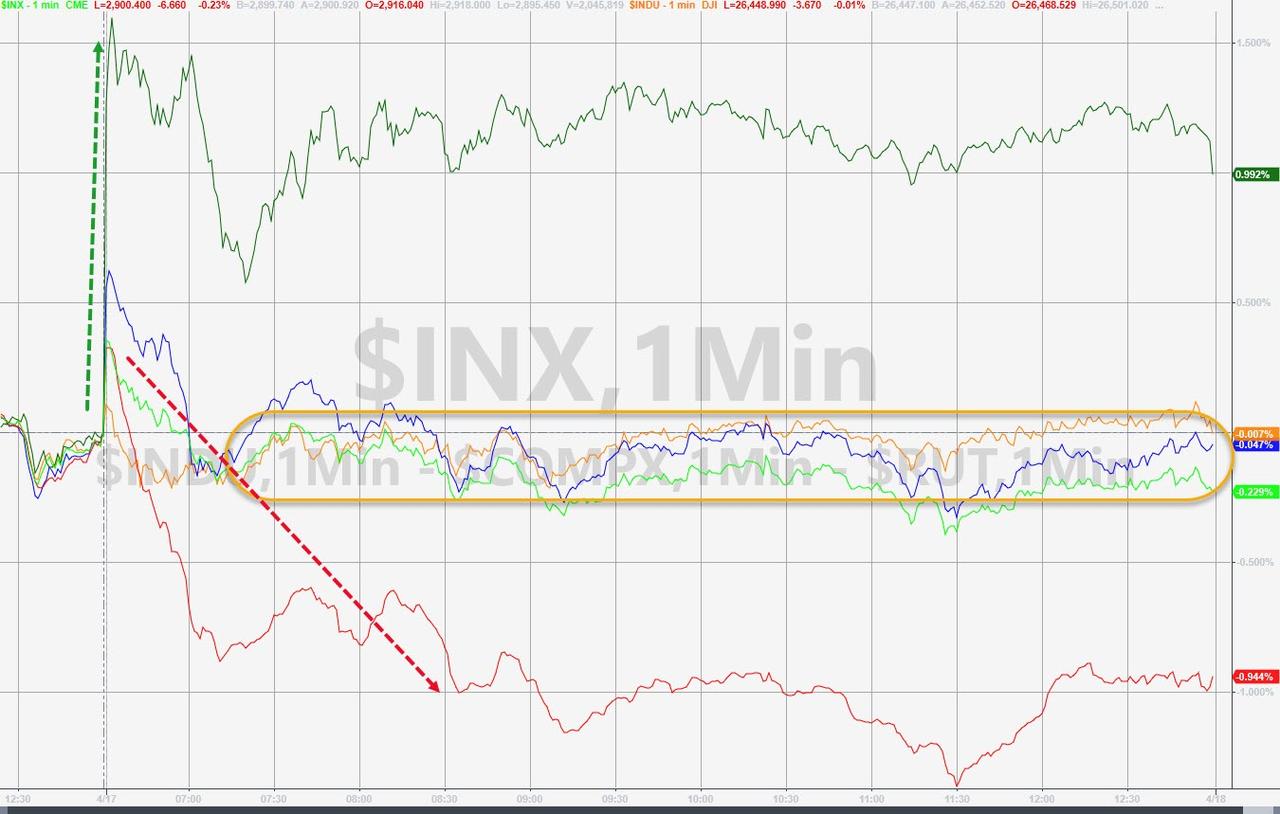

Market Snapshot

- S&P 500 futures up 0.2% to 2,916.25

- STOXX Europe 600 down 0.2% to 388.37

- MXAP up 0.2% to 163.92

- MXAPJ up 0.2% to 546.39

- Nikkei up 0.3% to 22,277.97

- Topix up 0.3% to 1,630.68

- Hang Seng Index down 0.02% to 30,124.68

- Shanghai Composite up 0.3% to 3,263.12

- Sensex up 1% to 39,275.64

- Australia S&P/ASX 200 down 0.3% to 6,256.38

- Kospi down 0.1% to 2,245.89

- German 10Y yield rose 1.9 bps to 0.085%

- Euro up 0.3% to $1.1316

- Italian 10Y yield rose 1.6 bps to 2.223%

- Spanish 10Y yield fell 0.4 bps to 1.082%

- Brent futures up 0.7% to $72.23/bbl

- Gold spot little changed at $1,276.03

- U.S. Dollar Index down 0.2% to 96.88

Top Overnight News from Bloomberg

- China’s economy rebounded through the first quarter, offering the government room for maneuver as trade negotiations with the U.S. enter a crucial stage. The economy expanded 6.4%, exceeding economist estimates. Factory output and retail sales also beat expectations in March to ease concerns about a slowdown

- Investors are the most optimistic on the euro in a year as conviction grows that Europe’s economy is recovering. Three-month risk reversals on the common currency, a gauge of sentiment, have turned in favor of calls over puts

- U.K. inflation unexpectedly stayed below target last month. The figures means wages are rising faster than prices, a boost for consumer spending, key for the British economy. The lack of headline inflationary pressure gives policy makers breathing space to keep interest rates on hold until the Brexit crisis is resolved

- Germany’s gross domestic product is to grow 0.5%, half as much as previously forecast amid slowing global expansion and concerns over Brexit and trade disputes, the economy ministry said on Wednesday.

- Foxconn billionaire founder Terry Gou announced Wednesday he’s running for Taiwan’s presidency, shaking up a race that will determine whether the island moves closer to China. Foxconn Technology Group is the main assembler of iPhones

- GAM Holding AG jumped the most since December after the company reported slowing outflows and said it would soon complete the liquidation of its scandal-hit bond fund

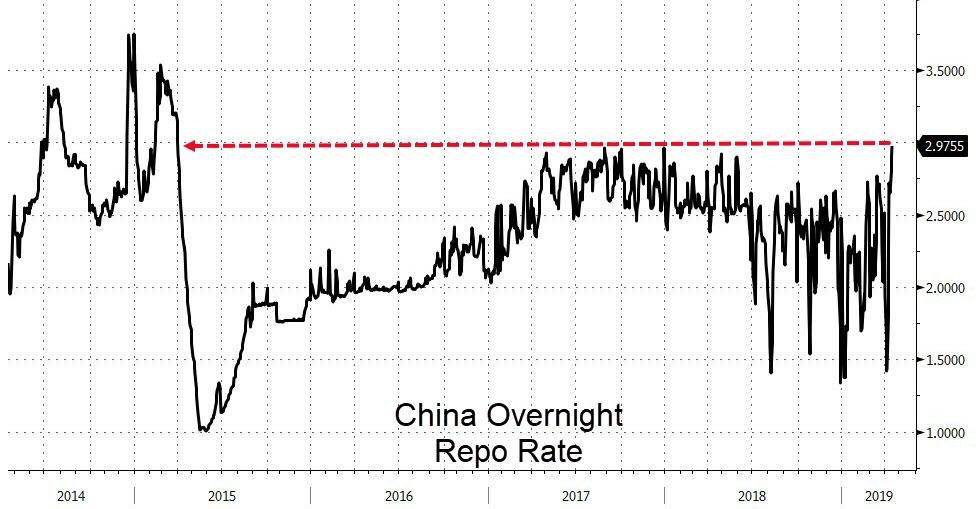

Asian equity markets traded indecisively following the cautious gains on Wall St due to mixed earnings and as the region failed to fully benefit from a slew of better than expected Chinese data. ASX 200 (-0.3%) was negative with the index led lower by underperformance in the mining sector after BHP reported weaker quarterly production numbers and amid declines in Chinese iron ore prices after Vale received approval to resume Brucutu mine operations, while Nikkei 225 (+0.2%) was positive although initial price action had mirrored a choppy currency. Hang Seng (U/C) and Shanghai Comp. (+0.3%) were indecisive with only brief support seen despite the better than expected Chinese GDP, Industrial Production and Retail Sales, as some suggested the data dampens prospects of PBoC action and after the central bank also recently suggested a preference for restraint in its quarterly monetary policy document. Furthermore, the PBoC conducted a liquidity injection of CNY 160bln through 7-day reverse repos but only announced CNY 200bln in MLF loans vs. the expiring CNY 366.5bln. Finally, 10yr JGBs were marginally lower as Japanese stocks remained afloat and on spillover selling from T-notes, while the US 30yr yield eyed the 3.0% level for the first time in nearly a month. Japan and the US have agreed to accelerate trade talks after an initial meeting in Washington suggested the two nations will stick to a narrow range of subjects

Top Asian News

- PBOC Trims Liquidity Supply in Sign It’s Dialing Back Stimulus

- Nippon Paint Buying Australia’s DuluxGroup for $2.7 Billio

- Jokowi Takes Early Lead in Unofficial Indonesia Vote Counts

- Turkish Opposition Claims Win in Istanbul After Vote Recount

- Singapore Takes Over Water Plant at Heart of Hyflux Debacle

Major European indices are little changed [Euro Stoxx 50 +0.1%] following on from indecisive overnight trade as Asian equity market were unable to capitalise on the strong Chinses data. The AEX (+0.2%) is marginally outperforming its peers, boosted by index heavyweight ASML (+1.5%) who have around a 12% weighting in the AEX and are higher following their earnings and the Co. confirming their full year guidance. Sectors are mixed, with underperformance seen in material names at the open, with the sector weighed on by BHP (-2.6%) after the Co. lowered their FY19 output guidance and Rio Tinto (-2.8%) in the red after being downgraded. Other notable movers this morning include ABB (+5.4%) following earnings and the surprise resignation of the Co’s CEO Spiesshofer, after being unable to placate shareholders with the sale of their power grid division in December. Elsewhere, Roche (+0.1%) have fallen from opening highs of around 1.6%; however, price action for the Co. was initially driven by the announcement that they are raising FY19 outlook to mid-single digit growth vs. Prev. low-mid single digit range, alongside expectations for further dividend increases.

Top European News

- Tech Stocks Outperform on ASML, Ericsson Results, Chip Gains

- Italy’s Populist Leaders Besiege the Central Bank, Lenders

- Juventus Plunges as Champions League Upset Sends Ajax Soaring

- ABB Chief Steps Down After Power-Grid Split Fails to Impress

- Pendragon Tumbles as U.K. Car-Price Slump Forces Strategy Review

In FX, first we look at USD, CNY – China’s economy unexpectedly held up in Q1 despite a slew of calls for a March bottom. GDP growth for the quarter topped estimates at 6.4% Y/Y, within the country’s 2019 target of 6.0-6.5%, whilst March IP and retail sales beats also provided extra impetus for the Yuan which breached 6.70 to the downside against the Dollar to print a low of just above 6.68. Hence, DXY lost the 97.000 handle upon the release and continues to edge lower in early EU trade. The Dollar index currently resides just off lows of 96.810 ahead of its 50 DMA at around 96.800. A light calendar for the US sees February trade data released at 13:30BST, ahead of Fed voter (and notorious dove) Bullard’s speech on the US economy and monetary policy.

- AUD, NZD – The Aussie is the marked beneficiary from the upbeat Chinese data wherein the jump in industrial production and a maintained GDP growth aided AUD/USD to briefly reclaim 0.7200 to the upside (from an intraday low of 0.7150) for the first time since February. The pair currently resides just below the figure, albeit above its 200 DMA at 0.7193 with Aussie jobs data on the overnight docket. Note: around USD 1.5bln options are set to expire between strikes 0.7190-7200. Conversely, the Kiwi does not bode so well amid dismal CPI figures in which markets pricing for a May OCR cut shifted to above 50%. On a brighter note for the NZD/USD, the overnight Chinese data resurrected the currency from a low of 0.6670 (vs. pre-data high of 0.6775) before stabilising above its 200 DMA at around 0.6730.

- EUR, GBP – An upbeat day for the Euro thus far amid the weakness in the Buck. The single currency was little swayed by the release of unrevised EZ inflation finals and the German government’s cut to 2019 GDP growth forecasts as was widely expected. EUR/USD breached its 50 DMA at 1.1300 to the upside in early hours and remains north of the figure where 1.4bln in options are set to expire at today’s NY cut. Elsewhere, Sterling took a hit from the benign inflation figures in which headline inflation printed at 1.9%, below the forecast 2.0%. As such, Cable lost the 1.3050 handle and resides close to session lows at 1.3033 ahead of its 50 WMA at 1.3029. ING argues that “British Retail Consortium had suggested that wholesale food costs had risen, on the back of adverse weather and higher global commodity prices”, hence overall inflation could be bumped up next month, possibly to the 2% target when combined with the rise in household energy caps. GBP now awaits for any potential direction from BoE Governor Carney scheduled to speak at 14:00BST.

- CAD – Another G10 winner from the pullback in the Dollar, also underpinned from the rise in oil prices following last night’s surprise drawdown in API stocks. USD/CAD currently resides below its 100 DMA at 1.3327, having briefly breached its 50 DMA to the downside at 1.3314 ahead of Canadian inflation data this afternoon, with headline expected to tick up to 1.9% from 1.5%.

- New Zealand CPI (Q1) Q/Q 0.1% vs. Exp. 0.3% (Prev. 0.1%). (Newswires) New Zealand CPI (Q1) Y/Y 1.5% vs. Exp. 1.7% (Prev. 1.9%) New Zealand RBNZ Sectoral Factor Model Inflation 1.7% (Prev. 1.7%)

In commodities, Brent (+0.6%) and WTI (+0.6%) prices are firmer with prices supported by the unexpected API draw of 3.1M vs. Exp. build of 1.7M. Elsewhere, strike action at Shells Pernis oil refinery [capacity of 404k BPD] is still ongoing, with most recent updates that union leaders state that the refinery is to remain at 65% operating rate, and there is currently no indication of when the refinery will return to full operation. Separately, Saudi Aramco are reportedly to purchase the 50% stake that Shell currently owns in SASREF, which is a joint venture between the two Co’s with a refining capacity in excess of 300k BPD. Later in the session we have the EIA weekly report, and due to scheduling for Easter holidays the Baker Hughes rig count will be released Thursday April 18th. Gold is flat and trading within a narrow USD 4/oz range, with price action from the softer dollar and stronger than expected Chinese data largely cancelling each other out. As such the yellow metal, is trading just above the prior sessions low of around USD 1272, which was the metals lowest level since December 27th. Elsewhere, the world’s largest iron ore miner Vale say they intend to resume operations at their Brucutu operations within the next 72 hours weighing on both the mining index and iron ore prices.

US Event Calendar

- 7am: MBA Mortgage Applications -3.5%, prior -5.6%

- 8:30am: Trade Balance, est. $53.4b deficit, prior $51.1b deficit

- 10am: Wholesale Inventories MoM, est. 0.3%, prior 1.2%; Wholesale Trade Sales MoM, est. 0.3%, prior 0.5%

- 12:30pm: Fed’s Harker Speaks on the Economic Outlook

- 12:45pm: Fed’s Bullard Speaks at Hyman Minsky Conference

- 2pm: U.S. Federal Reserve Releases Beige Book

- 5:30pm: New York Fed’s Logan Speaks at Money Marketeers of New York

DB’s Jim Reid concludes the overnight wrap

Over the last two days I’ve been doing an internal DB scheme where MD’s have multiple open door slots for more junior staff. The expectation is that we connect with people at an earlier stage of their career from all over the firm and offer them any guidance we can give. There were quite a few recent graduates signed up and in having the enjoyable meetings I couldn’t help chuckle at how different my experience as a graduate was in the mid 1990s to those we hire today. In my first two years (in sales) I got 30 people’s breakfast and coffees every day, burned through two suits with all the loose change making holes in my pockets, photocopied 100 x 50 pages of corporate bond price sheets everyday to be on all sales and traders desk by the time they got in at 7am and was generally treated like an errand boy. At one point I was asked to go 5 miles in a taxi to get food from my then boss’s favourite fish and chip shop one Friday lunchtime. My favourite memory though was that every grad was given an older mentor outside of his area to use as a sounding board. However my one was a grumpy guy in his late 40s who couldn’t think of anything worse than being a mentor. He was forced to take me out to lunch in my earliest days but instead took a friend of his and asked me to sit at the bar while he dined with his friend. I didn’t go back to him for any subsequent advice I sought. So it’s fair to say that the City has changed for the better over the last 25 years. So if any graduate wants some advice I’ll be very happy to provide it… in return for a coffee, a bacon sarnie and a fish supper!!! And maybe some painting and decorating at home!

We’re straight to Asia this morning where the latest Chinese growth data and activity indicators are out. They confirm our 2019 belief that the economy is improving as China’s mini stimulus filters through the economy. To start with China’s Q1 GDP came in one tenth above expectations at 6.4% yoy while all of the March activity indicators surprised on the upside with industrial production surging at +8.5% yoy (vs. +5.9% yoy expected) – the highest since July 2014. Retail sales printed at +8.7% yoy (vs. +8.4% yoy expected), YTD fixed assets ex rural came in line with consensus at +6.3% yoy and the jobless rate fell one tenth to 5.2%. This data confirms what we’d been expecting given the credit impulse numbers in recent months and should help European data over the coming weeks. The downside to the numbers will be a more hawkish PBOC. Their monetary policy statement yesterday described the appropriate policy stance as “moderately tight” and it seems today they injected much less liquidity into the market as was expected. So that’s the only sting in the tail to these numbers.

China’s markets have probably been weighing up these conflicting forces as the Shanghai Comp is currently trading flat after oscillating between gains and losses of as much as +0.47% and -0.42% respectively. Meanwhile, the Hang Seng (-0.22%) is down while the Nikkei (+0.29%) and Kospi (+0.02%) are up. Elsewhere, futures on the S&P 500 are trading flat (+0.07%).

In other news, Japan’s economy minister Toshimitsu Motegi said that the first phase of trade talks with the US focused on agriculture and cars, with digital trade set to be discussed at a later date. He added, “From the next session onwards we will speed up discussions toward an early agreement, and will discuss digital trade at an appropriate time.” This morning we saw Japan’s March trade data with the adjusted trade balance standing at -JPY 177.8bn (vs. -JPY 242.5bn expected) as a slowdown in imports (at +1.1% yoy vs. +2.8% yoy expected) outpaced a slowdown in exports (at -2.4% yoy vs. -2.6% yoy expected), marking the fourth consecutive month where exports have shrunk.

The moves this morning follow another fairly damp squib of a day on Wall Street yesterday, albeit one which ended with markets nudging a bit higher. Indeed global equities edged up across the board as did bond yields. The S&P 500 finished +0.05% with volumes over 10% below average and with an intraday range of 0.96% which was the 6th smallest this year. It wasn’t a lot different for the NASDAQ (+0.30%) and DOW (+0.26%), with all three major US indexes now hovering within 2% of their all-time highs. Prior to this, the STOXX 600 edged up +0.29%. US HY spreads ended -3bps tighter while Treasuries (+3.6bps) nudged back up to 2.591%, their highest level in a month, with the move driven by real yields not inflation breakevens. The 2s10s yield curve steepened 1.8bps to 17.9 bps, edging toward the top of its year-to-date range of between 12-20 bps.

With bigger fish to fry for markets including this morning’s China data and the PMIs tomorrow though, it was earnings which by and large dictated the tempo yesterday with the headline reporters being Bank of America before the bell and Netflix after. Like all the other US banks so far, BoA earnings beat while sales also came ahead of consensus, though management also pointed towards an expected slowdown in net interest income for the remainder of the year. The share price pared a loss of -2.82% to end the session +0.10%, as the broader banks index advanced +1.35%, partially boosted by the rise in treasury yields. Morgan Stanley numbers – the last of the big US banks to report – are out today.

Away from BofA we also saw earnings beats for Blackrock (shares +3.24%) and Johnson & Johnson (+1.10%), though UnitedHealth (-4.01%) disappointed. Their CEO said that US political proposals for universal health insurance would result in “wholesale disruption” to the existing healthcare industry. After the close Netflix’s earnings basically met expectations overall as first quarter subscriber growth beat consensus forecasts but the company’s estimates moving forward were lower than expected. The share price slipped -0.84% overnight. Separately, freight giant CSX shares rose +4.63% after the close on strong profits and shipping volumes. It’s still very early in earnings season with just under 10% of the names having reported so far but the trend has been for a large number beating earnings expectations (39 out of 46) but only half (23 out of 46) beating sales expectations. Separate from the earnings reports, news (Bloomberg) broke late in the session that Qualcomm and Apple had settled all of their worldwide litigation, with Apple agreeing to pay a one-time fee as well as royalties for the next six years. Qualcomm said they expected a $2 per share boost to earnings, and its shares led gains for the NASDAQ, advancing +23.21%. Apple shares closed flat.

There was also a little bit of macro news to feed off, specifically a couple of ECB stories. The first was a headline on Reuters stating that “several” ECB policymakers had doubts about projections for a growth rebound in the second half of this year, however this appeared to be more about forecasting methodology rather than policy. About an hour later though a story on Bloomberg suggested that ECB officials lacked enthusiasm for sub-zero tiering. The full story suggested that ECB policy makers weren’t opposed to examining the impact however were yet to be convinced of the merits of a switch to tiering. European Banks lost about half a percent post the story hitting however within minutes had pared that move and ultimately ended the day with a steady +1.06% gain as bond yields climbed. The euro actually reacted more to the first story but also retraced the move to end the day -0.18%. 10y Bunds saw a mini rollercoaster after hitting 0.072% early on (ZEW helped – see below) before hitting an intraday low of 0.038% an hour later around the ECB headlines before ending 0.065%, +1.0bps higher on the day. Tomorrow’s PMIs are the next major landmark for bunds.

Also on the macro front, our global economic research teams from Europe, the US, Japan, and China pooled their expertise and published a report yesterday examining the policy space available to combat the next recession. Their report looks at the monetary and fiscal options in the four major economic zones. The US and China have the most scope to use monetary policy, while all countries have the potential to employ fiscal measures. The full report with details for each region is available here .

In other news, the data that was out yesterday played second fiddle to earnings and the ECB stories. Nevertheless for completeness in the US industrial production disappointed a bit in March, coming in at -0.1% mom versus expectations for +0.2%. Manufacturing production also came in below market (0.0% mom vs. +0.1% expected), while it was noted that vehicle production dropped -2.5%. A drop in capacity utilisation also followed to 78.8% while later on the April NAHB housing market index reading printed 1pt higher at 63, as expected.

Prior to this, in Germany the ZEW survey of expectations for April rose more than expected to +3.1 (vs. +0.5 expected) from -3.6 in the month prior. A reminder that the March reading saw an improvement of 9.8pts and in fact we’ve now seen this reading rise for six consecutive months and turn positive for the first time in over a year. There’s a bit of debate as to how useful this is as a macro forecasting tool however with the PMIs a much bigger focus unsurprisingly. Meanwhile, here in the UK wage growth stayed put at +3.4% 3m/yoy and the unemployment also held steady at 3.9%. Both signalling continued strength in the labour market.

To the day ahead now, which this morning includes more data out of the UK where the March CPI/RPI/PPI data docket is due. Not long after that we’ll get the final March CPI revisions along with the February trade balance for the Euro area, while this afternoon in the US we’ve also got the February trade balance, as well as February wholesale inventories and trade sales data. The Fed’s Beige book is also due tonight while scheduled speakers include the BoE’s Carney, ECB’s de Galhau and Lautenschlaeger, and the Fed’s Harker, Bullard and Logan. Germany’s Economy Minister Altmaier will also present Germany’s latest economic forecasts, while the earnings highlights include PepsiCo and Morgan Stanley.

end

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 9.52 POINTS OR 0.29% //Hang Sang CLOSED DOWN 5.19 POINTS OR 0.02% /The Nikkei closed UP 56.31 POINTS OR 0.25%/ Australia’s all ordinaires CLOSED DOWN .35%

/Chinese yuan (ONSHORE) closed UP at 6.6892 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 64.41 dollars per barrel for WTI and 72.15 for Brent. Stocks inEurope OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.6892 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6861 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/

3 b JAPAN AFFAIRS

Japan/China/HUAWEI

After cutting off ZTE equipment last year, Japan may stop the use of Huawei 5 G technology in Japan and that is upsetting the Chinese to no end

(courtesy zerohedge)

China Confronts Japan Over Huawei 5G Ban During High Level Talks

According to a new exclusive in Nikkei Asian Review Huawei Technologies’ planned 5G roll out is a source of tension between China and Japan. Amid a general backdrop of otherwise improving relations, Japan late last year banned integration of the fifth-generation wireless technology over telecommunications security concerns, in a move that mirrored US action.

But on Sunday during high level economic talks in Beijing, Chinese foreign minister Wang Yi urged Japan not to single out Huawei: “Why is the Japanese government excluding Huawei?” he said.The Nikkei report painted a picture of a long and contentious meeting in which “sparks were flying” over Tokyo’s intent to wall itself off from Huawei 5G business.

Nikkei cites that Huawei was invoked repeatedly by Chinese representatives at the meeting, which ran nearly four hours. “The Chinese side was interested mainly in Huawei issues,” a source cited in the report said.

In the meeting Japan’s foreign minister Taro Kono claimed that Tokyo “does not have any specific Chinese company in mind” with regard to the ban.

However, the Chinese side was reportedly unconvinced — this after ZTE equipment was also banned by the Japanese policy, outlined last December, ostensibly to avoid hacks and intelligence leaks.

Nikkei summarized the extent of Japan’s ban on Huawei’s 5G in the following:

Tokyo’s directive followed in December, banning government purchases of communications circuits, devices, servers and six other types of equipment should they pose a security risk.

Japan also aims to protect telecommunications equipment in 14 areas of infrastructure, including finance and air travel, against cyberattacks and other threats.

Huawei Technologies is touting its 5G “revolution” at the same time many western countries are shining a spotlight on Chinese espionage and stealing of trade secrets.

The fear is that the cutting edge network technology will act as a backdoor for cyber spying by Beijing.

Meanwhile Huawei representatives have recently touted that the company has signed 40 commercial 5G network contracts and shipped 100,000 base stations globally, to facilitate its super-fast networks.

Australia and New Zealand have also alongside the US and Japan banned the technology from being sold in their territory. And other so-called “Five Eyes” intelligence sharing countries the UK and Canada are reportedly strongly considering a blanket ban.

3 C CHINA/CHINESE AFFAIRS

China/

Although the huge stimulus in March had a strong effect on the numbers today, the internal consumption is of great concern to China. They point to three areas to show China’s continual problems:

the collapse in land sales, weak imports, and the unexpected decline in electricity consumption.

(courtesy zerohedge)

Three Reasons To Question China’s Blockbuster Economic Data

On the surface, China’s March data was surprisingly strong, largely as a result of strong policy easing and in light of China’s massive 40% surge in Total Social Financing, even adjusting for the Chinese New Year factor, the data indicated a recovery in economic momentum, if only for the time being.

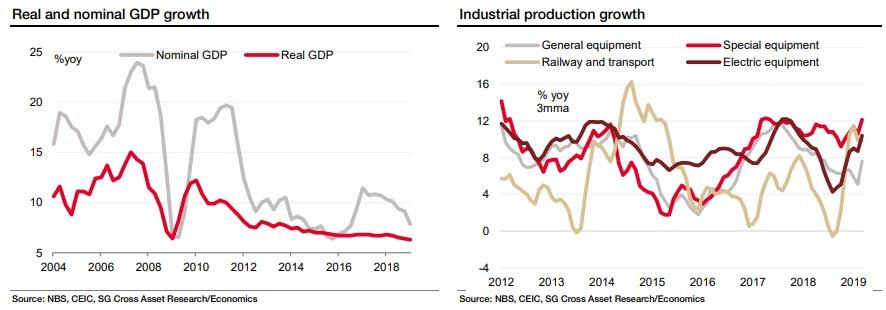

As DB’s Jim Reid recapped this morning, starting with China’s Q1 GDP, the print came in one tenth above expectations at 6.4% yoy while all of the March activity indicators surprised on the upside with industrial production surging at +8.5% yoy (vs. +5.9% yoy expected) – the highest since July 2014. Retail sales printed at +8.7% yoy (vs. +8.4% yoy expected), YTD fixed assets ex rural came in line with consensus at +6.3% yoy and the jobless rate fell one tenth to 5.2%.

Among the other positive highlights, export momentum stabilized, consumption looked to be bottoming out and investment remained supported by the surprisingly resilient housing market. The outlook also seems bit more secure, as credit growth embarked on an upward trend.

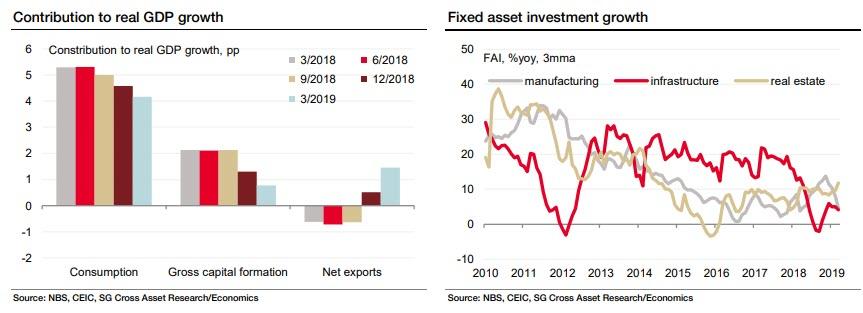

That said, as SocGen’s Wei Yao pointed out this morning, the expenditure breakdown was not as positive. According to the NBS, net exports were the only improving segment, while both consumption and investment (including inventories) weakened notably in 1Q. Furthermore, the pick-up in net exports had more to do with weak imports than better exports. Consistently, overall fixed asset investment (FAI) growth moderated from 7.2% in 4Q to 6.3% in 1Q, although in real terms. By sector, infrastructure investment growth slowed from 6.0% to 4.2%, and manufacturing investment growth continued to moderate, from 11.5% to 4.6%. However, property investment picked up again from 8.4% to 11.8%.

However, three pieces of data have prompted questions about the consistency and veracity of the latest uptick in Chinese data: the collapse in land sales, weak imports, and the unexpected decline in electricity consumption.

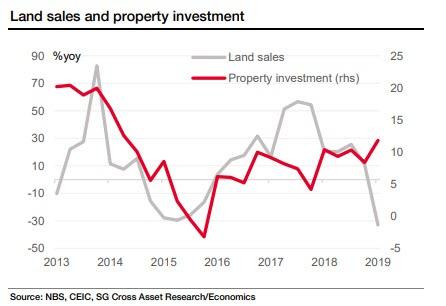

First, overall housing activities did stage a come-back in March as property sales recovered from -4% in the first two months of 2019 to 2%, lifting the quarterly growth from -2% in 4Q to 0.9% in 1Q. Yet while growth in new starts rebounded quite sharply in March to 18% from 6%, this was not enough to stop the quarterly deceleration from 19% in 4Q to 12%. But the big question is regarding the outlook. On the positive front, housing policy seems to be easing more notably from less stringent credit conditions for developers to relaxation in the 2nd-tier cities’ Hukou policy. However, ominously, land sales revenue growth collapsed to -33% in 1Q from 11.8% in 4Q18. This, as SocGen notes, “clearly does not augur well for property investment in the coming quarters.”

Second, whereas the all important net trade metrics appear to have stabilizied, import growth slid further, from -0.3% in February to -1.8%, tanking the quarterly growth rate from 9% in 4Q to 0% in 1Q, or 5% to -4% in USD terms. By destination, the deceleration in quarterly nominal growth was broad-based, mainly driven by commodity-exporting countries (Russia and Brazil), followed by the US and Korea. By product, import volume growth of major goods such as crude oil and semiconductors all moderated in 1Q. Metal import volumes also remained sluggish, with iron ore down from 1% in 4Q to -4%, copper down from 5% to -4% and steel down from -3% to 16%.

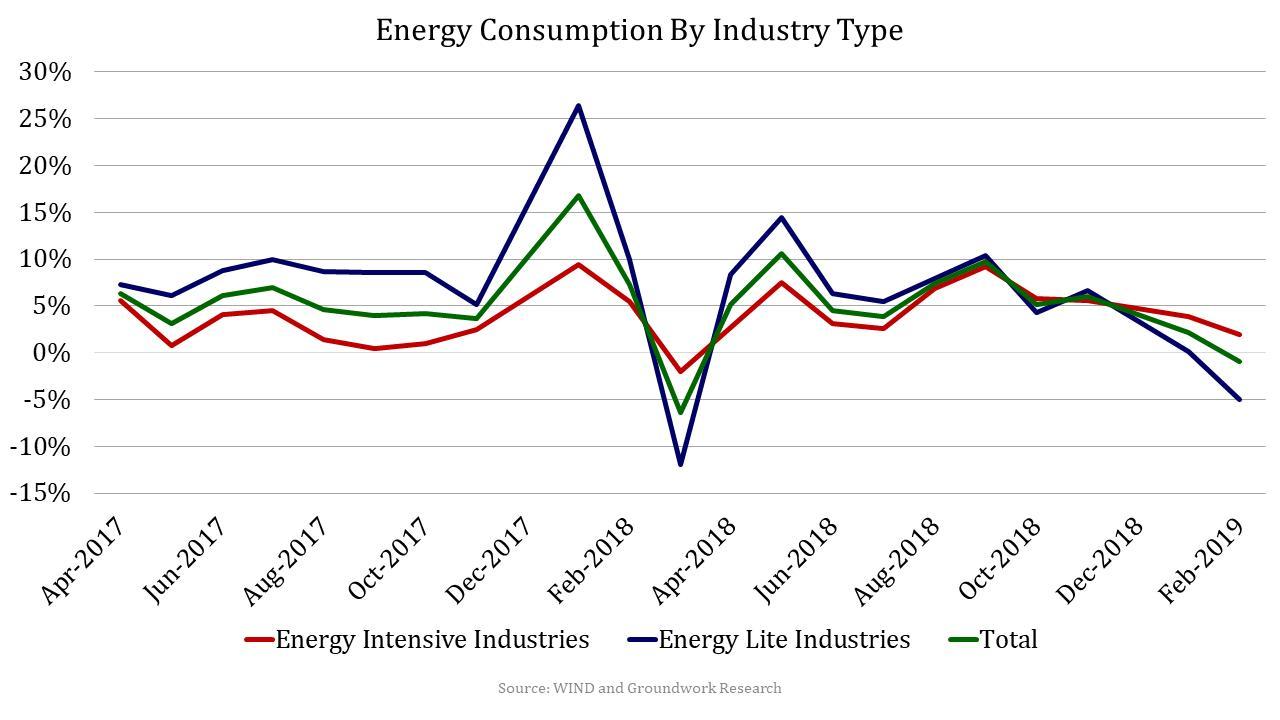

Last, but not least, was the latest energy consumption data, which while not highlighted in yesterday’s report, was certainly a concern because in a quarter in which industrial production reportedly soared higher, we also saw the first contraction in total energy consumption, which shrank by 1%. That this took place when China’s economy allegedly grew by 6.4% certainly puts the veracity of China’s data under the microscope yet again.

So whether China’s data was real or not, and there is enough historical precedent to lean toward the latter, the question is what this means for Beijing’s future policy. Here, as SocGen notes, “together with a stronger fiscal impulse and more positive economic data – whether they last or not, it is only logical for the PBoC to pause headline easing for now.” Additionally, the sharp upward trend in credit growth also does suggests that the economy may not need as much liquidity easing in the future, which in turn will likely cause the rebound in China’s credit impulse to fizzle in the coming months.

Echoing this take, Deutsche Bank’s Jim Reid wrote that “the downside to the numbers will be a more hawkish PBOC” and indeed, on Wednesday the PBOC injected much less liquidity into the market than was expected. In short: while China has clearly benefited from the trillions in new credit injected into the system, the question is how long will this impulse last, how sustainable is the resultant reflationary ripple, and what happens when the “sugar high” from China’s stimulus once again fizzles, especially if a US-China trade deal is still to be finalized.

end

Obviously last month’s stimulus was not enough: China is now preparing a new stimulus to subsidize car and appliance purchases

(courtesy zerohedge)

China Prepares New Stimulus: Will Subsidize Car, Appliance Purchases

Earlier today we presented three reasons to doubt the veracity of China’s unabashedly strong Q1 economic data: the collapse in land sales, weak imports, and the unexpected decline in electricity consumption. We can now add one more: according to Bloomberg, China is now preparing to take even more stimulus steps to boost growth.

According to the report, Chinese officials are drafting measures to bolster sales of objects which have seen a surprising decline in consumer demand, namely cars and electronics. Notably, the report coincided with the latest GDP data showing a stronger than expected 6.4% expansion in the first quarter. Yet that appears to be insufficient for Beijing – which remains stuck in a protracted trade war with the US – and Chinese leaders are “stepping up attempts to bolster consumption and mitigate the threats posed by trade tensions with the U.S.”

As Bloomberg reports, “the proposals include subsidies for new-energy vehicles, smartphones and home appliances, and are at a consultation stage with other government branches, with no guarantee that they’ll be approved.”

Among the other components of the proposal, via Bloomberg:

- An increase in the number of automobile licenses

- A waiver on car-ownership quotas for families who don’t own vehicles

- Subsidies for people who exchange vehicles that are as many as 10 years old for electric, hybrid or fuel-cell vehicles

- No limits or traffic controls for new-energy vehicles

- Encouraging banks to increase auto loans in tier-3 cities or below

- Considering deducting auto purchases from personal income tax

- Subsidies of up to 13 percent for a home appliance purchase at a maximum of 800 yuan ($120) per purchase

- Exemption of value-added taxes for used-car transactions until the end of 2020

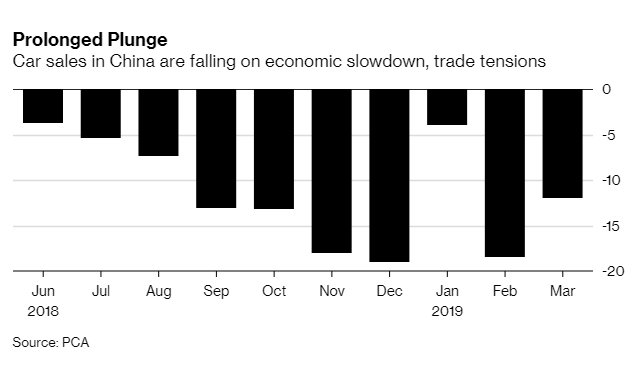

The target of the latest stimulus is clear: to boost flagging auto sales. As we reported last week, dropped 12% to 1.78 million units, according to the China Passenger Car Association. This is after an 18.5% drop in February and a 4% drop in January, and follow the worst year for Chinese auto sales in decades.

As Bloomberg adds, it’s notoriously difficult to own a car in major Chinese cities because of quotas to tackle traffic congestion and air pollution. In Beijing, the annual new vehicle quota dropped to 100,000 in 2018, and each licensed gasoline-fueled car has to be idle one day a week. “That’s prompted the government to provide incentives for motorists to drive new-energy vehicles — including pure-battery electrics, plug-in hybrids and fuel-cell cars.”

The proposed stimulus would be the latest in a long series of attempts by the government to stimulate flagging growth: most recently China unveiled its most ambitious tax reduction in years, slashing the VAT, while a record credit injection has clearly had a favorable impact on industrial production, if not China’s all important real estate.

Needless to say, for a world desperate in need of its old, familiar, credit-fueled growth dynamo, China’s stabilization and the prospect of even more stimulus will come a relief. It’s also a sharp reversal from as recently as January when key readings were pointing to a pronounced downturn, a factor U.S. officials have touted as leverage in their push for a trade agreement. It is also a question as to whether the Fed will now be forced to once again reverse its tightening “pause” and resume rate hikes into the second half of 2019.

“President Trump and other U.S. officials spent much of the last year saying that China’s slowdown was making Beijing desperate for a deal,” said Michael Hirson, Practice Head, China and Northeast Asia at Eurasia Group and a former U.S. Treasury Department official. “Now that China’s growth is recovering, Trump and team will be getting more questions from pundits and the media about whether his leverage is slipping away.”

Justifying China’s ongoing desire to overstimulate the economy, Bloomberg economist Chang Shu and Qian Wan wrote that “we expect the economy to continue to stabilize in the second quarter, but believe continued policy support is warranted. Government-led infrastructure spending has kick started the recovery. What’s needed still — a turnaround in the private sector to drive self-sustaining growth.”

On the other hand, with China now on full tilt when it comes to stimulating the economy, the market will be especially attuned to the likelihood of China overheating in the near future, and as Bloomberg macro commentator Richard Breslow writes this morning, “we’ll get a good sense of whether rates can carry on from here by how they react to the latest, and not officially confirmed, report that the Chinese government is preparing new stimulus measures. It really matters in trying to understand the trading mindset.”

As for the overarching question of what this incremental stimulus means just as Beijing has, reportedly, stabilize the economy, Breslow also puts it bet: “Is additional stimulus a sign that things are about to get a lot better? Or a sign of renewed concern?”

Today’s stock market reaction should provide the answer.

end

China’s bond vigilantes are watching closely as data suggests a huge spike in their PMI due to the massive stimulus. However bond yields are also rising.

(courtesy zerohedge)

China’s Bond Vigilantes Loom As Economic Data Stabilizes

All hope-filled eyes are straining at tonight’s data deluge from China for signs that confirm the PMI spike (and exports rebound) that fueled the latest leg higher in global stocks and bond yields.

Remember, the official narrative is that after a rocky start to the year, the roll out of targeted stimulus has boosted investment, buoyed consumption and helped the manufacturing sector.

Or put another way, thanks to unprecedented injections of credit and endless fiscal and monetary largesse, Chinese stocks have tracked aggressively higher, following China’s world-leading credit impulse back from the abyss…

And thanks to that resurgence of China’s credit impulse (in the face of a Fed that has talked a lot but done nothing), the divergence between US and Chinese macro data performance is at an extreme…

And yet – amid all this exuberant indication – China GDP growth is expected to slow in Q1

end

4/EUROPEAN AFFAIRS

The British, Australian, Ecuadorian and US Governments have made an ad about Julian Assange’s arrest and it’s surprisingly honest and informative!

have fun with this:

end

UK

Tory support is faltering and Nigel Farage’s new Brexit party is picking up steam.

(courtesy Mish Shedlock/Mishtalk)

Tory Support Splinters, Nigel Farage’s Brexit Party Nearly Even In Polls

Authored by Mike Shedlock via MishTalk,

Theresa May, the worst negotiator in history, splintered the Tories so badly the Brexit Party is nearly even in polls.

Farage Forms New Party

The Guardian reports Tories Hit by New Defections and Slump in Opinion Polls as Party Divide Widens.