GOLD: $1274.70 DOWN $13.60 (COMEX TO COMEX CLOSING)

Silver: $14.98 DOWN 3 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1276.75

silver: $15.01

Something To Ponder…

Remember what you’re told by The Fed – 2% inflation per annum is ‘stable prices’…

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING:1005/1143

EXCHANGE: COMEX

CONTRACT: APRIL 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,286.800000000 USD

INTENT DATE: 04/15/2019 DELIVERY DATE: 04/17/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 H HSBC 13

365 C ED&F MAN CAPITA 1

657 C MORGAN STANLEY 22

661 C JP MORGAN 1005

686 C INTL FCSTONE 1

737 C ADVANTAGE 1 91

773 C G.H. FINANCIALS 2

845 C GOLDMAN SACHS C 5

880 H CITIGROUP 1142

905 C ADM 3

____________________________________________________________________________________________

TOTAL: 1,143 1,143

MONTH TO DATE: 5,364

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 1143 NOTICE(S) FOR 114300 OZ (3.555 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 5364 NOTICES FOR 536400 OZ (16.684 TONNES)

SILVER

FOR APRIL

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 774 for 3,870,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE :$5042 UP $18

Bitcoin: FINAL EVENING TRADE: $5153 UP 130

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI AFTER A ONE DAY HIATUS, CONTINUED TO MARCH HIGHER TO THE TUNE OF A HUGE SIZED 4827 CONTRACTS FROM 218,290 UP TO 223,117 DESPITE YESTERDAY’S 1 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE MUST HAVE HAD CONSIDERABLE NEW SPREADS INITIATED BY OUR SPREADERS (BANKERS).

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A VERY STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 5969 FOR MAY, 0 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 5969 CONTRACTS. WITH THE TRANSFER OF 5969 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 5969 EFP CONTRACTS TRANSLATES INTO 29.84 MILLION OZ ACCOMPANYING:

1.THE 1 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

AND NOW 3.870 MILLION OZ STANDING FOR SILVER IN APRIL.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

21,336 CONTRACTS (FOR 12 TRADING DAYS TOTAL 21,336 CONTRACTS) OR 106.68 MILLION OZ: (AVERAGE PER DAY: 1778 CONTRACTS OR 8.890 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 106.68 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 15.24% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 674.85 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4827 DESPITE THE 1 CENT FALL IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A HUMONGOUS SIZED EFP ISSUANCE OF 5969 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED AN ATMOSPHERIC SIZED: 10,796 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 5969 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 4827 OI COMEX CONTRACTS. AND ALL OF THIS HUMONGOUS DEMAND HAPPENED WITH A 1 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $15.01 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.116 BILLION OZ TO BE EXACT or 160% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR nil OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ AND NOW APRIL AT 3.870 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL AND THIS TIME BY A CONSIDERABLE SIZED 4772 CONTRACTS, TO 439,508 WITH THE DROP IN THE COMEX GOLD PRICE/(A LOSS IN PRICE OF $3.70//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 9349 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 9349 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 439,508. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4577 CONTRACTS: 4772 OI CONTRACTS DECREASED AT THE COMEX AND 9349 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 4577 CONTRACTS OR 457,700 OZ OR 14.23 TONNES. YESTERDAY WE HAD A FALL IN THE PRICE OF GOLD TO THE TUNE OF $3.70.…AND YET WITH THAT, WE STILL HAD A STRONG GAIN IN TONNAGE OF 14.23 TONNES!!!!!!.???

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 72,387 CONTRACTS OR 7,238,700 OR 225.15 TONNES (12 TRADING DAYS AND THUS AVERAGING: 6032 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAYS IN TONNES: 225.15 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 225.15/3550 x 100% TONNES = 6.34% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1600.74 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 4772 WITH THE LOSS IN PRICING ($3.70) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 9349 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 9349 EFP CONTRACTS ISSUED, WE HAD A GOOD GAIN OF 5184 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

9349 CONTRACTS MOVE TO LONDON AND 4772 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 14.23 TONNES). ..AND ALL OF THIS GOOD DEMAND OCCURRED WITH A FALL IN PRICE OF $3.70 IN YESTERDAY’S TRADING AT THE COMEX.

we had: 1143 notice(s) filed upon for 114,300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $13.60 TODAY

A BIG CHANGE WITH RESPECT TO GOLD INVENTORIES AT THE GLD:

A HUGE WITHDRAWAL OF 3.82 TONNES OF GOLD WHICH WAS USED IN THE RAID TODAY

INVENTORY RESTS AT 754.03 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 3 CENT TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV//

/INVENTORY RESTS AT 309.167 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A HUMONGOUS SIZED 4827 CONTRACTS from 218.290 UPTO 223,117 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

HERE IS HOW THE CROOKS USED SPREADING AS WE ENTER AN ACTIVE DELIVERY MONTH. THUS SILVER HAS THE ACTIVE MONTH OF MAY COMING UP AND THUS SPREADERS DO THE FOLLOWING:

“YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF APRIL BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

THE CROOKS DID NOT DISAPPOINT US TODAY AS THE OI INCREASED BY A HUGE AMOUNT DESPITE THE SILVER LOSS.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 5959 FOR MAY AND JULY: 0 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 5969 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 4827 CONTRACTS TO THE 5969 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF 10,796 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 53.98MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH. AND NOW 3.870 MILLION OZ FOR APRIL.

RESULT: A HUMONGOUS INCREASE IN SILVER OI AT THE COMEX DESPITE THE 1 CENT FALL IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A HUGE SIZED 5969 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 75.81 POINTS OR 2.39% //Hang Sang CLOSED UP 319.15 POINTS OR 1.07% /The Nikkei closed UP 52.55 POINTS OR 0.24%/ Australia’s all ordinaires CLOSED UP .38%

/Chinese yuan (ONSHORE) closed UP at 6.7094 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 63.42 dollars per barrel for WTI and 71.11 for Brent. Stocks inEurope OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.7094 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7115 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/USA/VENEZUELA:

China lashes out at Mike pompeo for interference in its affairs with respect to Venezuela and other nations in Latin America

( zerohedge)

4/EUROPEAN AFFAIRS

i)Italy

Yesterday I brought to your attention the dire problems inside Turkey. Today I bring to you the other country with major problems: Italy

( Don Quijones/WolfStreet)

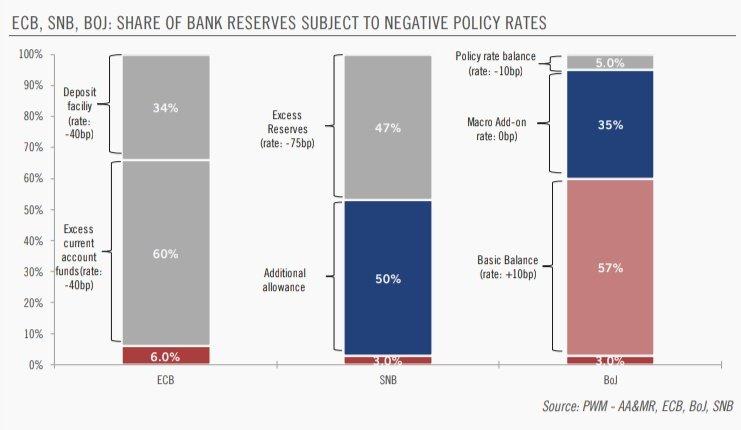

ii)ECB

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Turkey

A Turkish economist is arrested after insulting Erdogan on Twitter

( zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning/FOMC

Somebody dumps $1.5 billion dollars worth of paper gold at exactly 8:30 am this morning.

(zerohedge)

ii)Market data

Hard data Industrial output contracts badly in March led by auto production

( zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

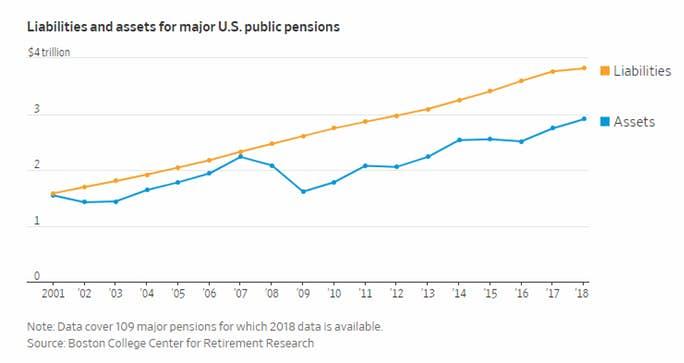

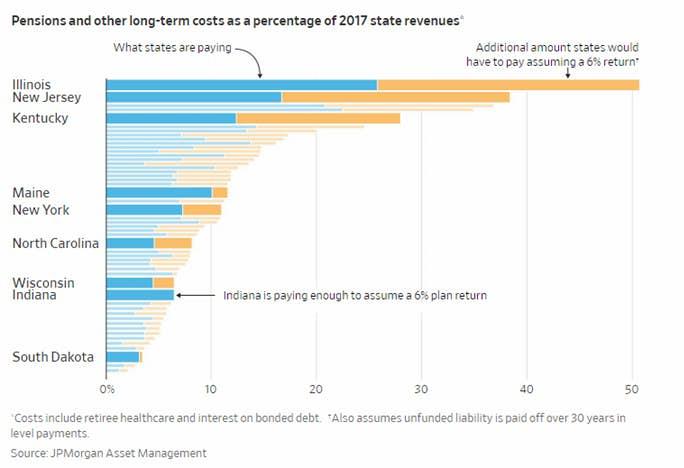

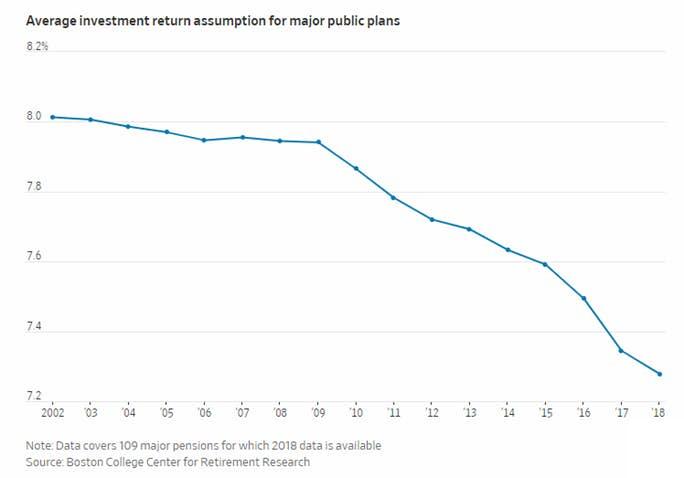

a)this is an accident waiting to happen: Pension plans are in the worst possible shape with Illinois at the top of the heap.

(Mish Shedlock/Mishtalk)

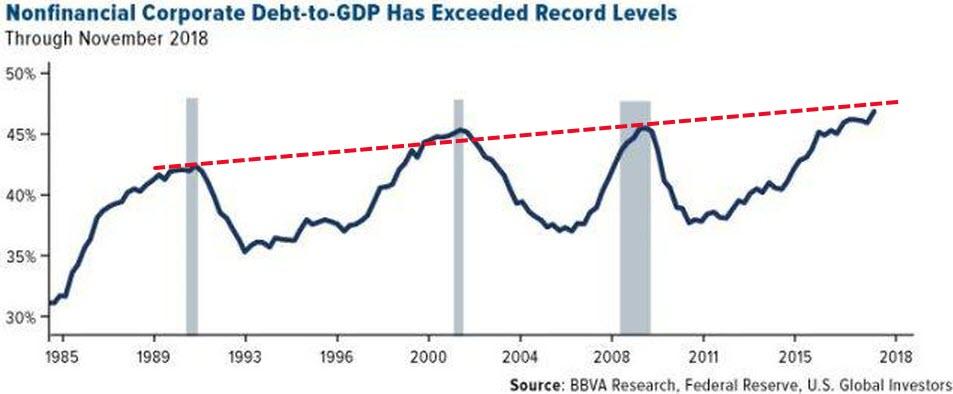

b)A good commentary tonight from Michael Snyder as he describes that corporate debt is now 50% of GDP. USA firms instead of investing in their infrastructure e.g. improving productivity in plants, they borrowed money to buy back in own stock. Now firms are drowning in debt.

iv)SWAMP STORIES

The House Democrats refuse to give up on Russian collusion in the USA election as they issue a friendly subpoena to multiple banks probing the issue as if they are now already willing not to accept the findings of Mueller

( zero hedge)

end

Let us head over to the comex:

AFTER APRIL, WE HAVE THE ACTIVE DELIVERY MONTH OF MAY AND HERE THE OI FELL BY 1082 CONTRACTS DOWN TO 102,471. CONTRACTS.. THE NEXT MONTH OF JUNE GAINED 42 CONTRACTS TO 121. AFTER JUNE, THE VERY BIG DELIVERY MONTH OF JULY HAD A GAIN OF 5432 CONTRACTS UP TO 82,344 CONTRACTS.

APRIL 16/2019:

Inventory 309.167 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

THE RISE IN LIBOR IS CREATING A SCARCITY OF DOLLARS BECAUSE FOREIGN EXCHANGE SWAPS (COSTS) ARE SIMPLY PROHIBITIVE

YOUR DATA…..

6 Month MM GOFO 2.12/ and libor 6 month duration 2.64

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: + .52

XXXXXXXX

12 Month MM GOFO

+ 2.50%

LIBOR FOR 12 MONTH DURATION: 2.75

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.25

end

PHYSICAL GOLD/SILVER STORIES

Early gold trading today:

Somebody dumps $1.5 billion dollars worth of paper gold at exactly 8:30 am this morning.

(zerohedge)

Gold Dumps As ‘Someone’ Decides 0830ET Is Perfect Time To Puke $1.5 Billion Notional

Precious metals traders are using the ‘f’ word a lot this morning – ‘Fiduciary’ – as they question the rationale for ‘someone’ deciding to puked over 11,000 gold futures contracts (around $1.5 billion notional) into the market, sending the price tumbling to its lowest since January…

Some have argued this is technically driven as Gold breaks below its 100DMA…

Silver was also hammered lower…

Exclusive Offer: Secure Gold and Silver Storage In Zurich For Free For Six Months

Own actual bullion coins and bars and avoid ETF and Digital or ‘.com’ gold and silver. Offers ends this Thursday, April 18

Given the many risks of today, we believe precious metal buyers should own gold and silver coins and bars in at least two jurisdictions and avoid digital and ETF gold. For three more days, we are providing exclusively to our clients a valuable storage offer in what we believe are the safest vaults in the safest and most liquid jurisdiction in the world – Zurich, Switzerland.

Secure Storage In Zurich For Free For Six Months

Until this Thursday (April 18), when you invest the minimum amount of $€£ 10,000 (no maximum) in physical gold and or silver for storage in our Loomis vaults in Zurich, Switzerland, you will pay zero storage fees for the first six months from the date of your purchases. This applies to all investments for Secure Storage in Zurich.

All gold and silver is stored in professionally managed, specialist, high security precious metals vaults. In addition to this gold and silver stored in GoldCore Secure Storage is stored on a fully allocated and fully segregated basis – the safest way to store precious metals – ensuring liquidity, competitive pricing and ownership.

Complimentary Silver Bullion Coin

In addition to the 6 months’ worth of free Secure Storage we also appreciate that our clients enjoy seeing and holding their precious metals and that’s why we will also be delivering to you fully insured, a freshly minted, 2019, one ounce, legal tender, silver bullion coin. You can choose between two of the world’s most popular silver coins: the 2019 American Silver Eagle or the beautifully minted 2019 British Silver Britannia.

Complimentary Book

Because our mission is to ensure that our clients and community are kept informed and protected, each order also comes with a copy of “The New Case for Gold”, the fascinating and insightful book by gold expert and New York Times Best Selling author Jim Rickards.

More information about the offer can be accessed here and if you wish to avail of the offer simply wire funds and transact online or on the phone by close of business this Thursday (1700, April 18). Mention the Exclusive Offer code ‘offermarch2019’ on the phone or by email – support@goldcore.com

News and Commentary

Gold prices drop as trade hopes stoke risk appetite (Reuters.com)

Gold logs lowest finish in over a week (MarketWatch.com)

Asia stocks cling to 9 month high on China hopes, Wall Street hit by earnings (Reuters.com)

Notre-Dame smolders as investigation begins (Reuters.com)

Fed should ‘communicate comfort’ with slightly higher inflation: Evans (Reuters.com)

Germans hoard more gold than the Bundesbank has in its vaults (Twitter.com)

Why Japan’s 10-Day Break Has Markets Worried (Bloomberg.com)

How can anyone still deny gold is manipulated? Kranzler and Hemke (InvestmentResearchDynamics.com)

Will Gold Rally to $1,500 This Year? (GoldSeek.com)

Gold Prices (LBMA PM)

15 Apr: USD 1,286.75, GBP 982.43 & EUR 1,137.23 per ounce

12 Apr: USD 1,296.15, GBP 991.68 & EUR 1,146.06 per ounce

11 Apr: USD 1,304.65, GBP 997.01 & EUR 1,152.43 per ounce

10 Apr1: USD 1,304.80, GBP 998.04 & EUR 1,157.44 per ounce

09 Apr: USD 1,303.00, GBP 995.13 & EUR 1,155.00 per ounce

Silver Prices (LBMA)

15 Apr: USD 14.93, GBP 11.39 & EUR 13.20 per ounce

12 Apr: USD 15.06, GBP 11.51 & EUR 13.31 per ounce

11 Apr: USD 15.25, GBP 11.66 & EUR 13.53 per ounce

10 Apr: USD 15.25, GBP 11.66 & EUR 13.53 per ounce

09 Apr: USD 15.25, GBP 11.66 & EUR 13.53 per ounce

Recent Market Updates

– There Is Too Much Debt In The World – World Bank

– How to Store Gold in an Uncertain World

– The ECB Is Struggling With Inflation, Interest Rates and The Outlook

– Russia Dumps U.S. Dollars and Buys Gold As “Safety Metal”

– How A ‘No Deal’ Brexit Could Lead To The “Lehmanization” Of Europe

– Silver Bullion Set to Soar to $50 an Ounce (GoldCore Video)

– Perth Mint’s Gold Bullion Sales Surge 68% In March

Until April 18, when you purchase the minimum amount of 10,000 ($€£) in physical gold and or silver, you receive complimentary Storage In Zurich For 6 Months

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7094/

//OFFSHORE YUAN: 6.7105 /shanghai bourse CLOSED UP 75.81 or 2.39%

HANG SANG CLOSED DOWN 319.15 points or 1.07%

2. Nikkei closed UP 52.55 POINTS OR 0.24%

3. Europe stocks OPENED GREEN/MIXED

USA dollar index FALLS TO 96.99/Euro FALLS TO 1.1302

3b Japan 10 year bond yield: RISES TO. –.02/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.88/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 63.42 and Brent: 71.11

3f Gold DOWN/JAPANESE Yen UP CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +06%/Italian 10 yr bond yield UP to 2.61% /SPAIN 10 YR BOND YIELD UP TO 1.10%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.55: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.31

3k Gold at $1283.90 silver at:14.95 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 6/100 in roubles/dollar) 64.36

3m oil into the 63 dollar handle for WTI and 71 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.88 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0058 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1367 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.06%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.56% early this morning. Thirty year rate at 2.98%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.8076..GETTING VERY DANGEROUS

Stocks Jumps On Fresh China, Earnings Optimism As Volatility Disappears

Despite no reports of “China trade deal optimism” overnight, global markets are a sea of green this morning on optimism this time about China’s economy itself, which is set to report its GDP tomorrow, coupled with renewed confidence that the equity rally will be supported by stronger than expected corporate earnings. The dollar edged up while Treasuries fluctuated around unchanged.

The MSCI world equity index, which tracks shares in 47 countries, edged up 0.1 percent in early European trade. Europe’s Stoxx 600 Index rose for a fifth day, now within inches of 8 month highs, driven higher by banks and retail shares. Germany’s DAX gained over half a percent, while Britain’s FTSE 100 also strengthened. The recent rally comes as a blanket of calm has descended across financial markets, with European stock volatility falling to its lowest since January 2018.

Across the Atlantic, S&P 500 futures pointed to a sharply higher open, one which puts the S&P’s all time high within reach as better than expected earnings coming from both Bank of America and BlackRock. In Asia, shares in China and Hong Kong outperformed markets in Japan and South Korea. Emerging-market stocks climbed, though the currencies weakened. The yen inched higher.

While there was no immediate catalyst for the overnight optimism, Bloomberg notes that investors are spending the holiday-shortened week “assessing the chances that stocks will sustain their rally even as similar gains in investment-grade bonds have ebbed since late March. Optimism over earnings appears to be boosting bullish sentiment in equities, though volumes this week have been muted.”

Natixis Cross Asset Strategist Florent Pochon echoes this take, saying that investors were mainly focused on U.S. earnings, especially after the first flurry of bank results made for mixed reading: “After the strong rally we have seen in equities, people are now waiting for the next catalyst,” Pochan said. “We do expect some more positive data from Europe which should give a bit of fresh air (to European assets)”

All eyes are now on a slew of Chinese data due on Wednesday, including industrial production and retail sales data but most important will be the latest quarterly GDP data which is expected to post another decline to 6.3% Y/Y. After a worrying start to the year, Chinese data have been more positive as authorities ramped up stimulus measures, soothing investor fears about a slowdown in the world’s second-biggest economy.

“The outlook for Asia critically hinges on the outlook of China’s growth and the ongoing U.S.-China trade talks,” wrote strategists at Bank of America Merrill Lynch. “On both fronts, policymakers and investors believe that the outcome of these two issues is turning more positive.”

Currency markets were generally quiet, although the Australian dollar took a dive lower after the Reserve Bank of Australia signaled in policy minutes that an interest rate cut would be appropriate should inflation stay low and unemployment trend higher. The Aussie shed 0.4 percent to $0.7140.

Elsewhere, an otherwise lackluster European trading session saw a brief flurry of activity as news that some ECB policy makers remained doubtful about the region’s growth prospects sent the euro lower, only to rebound after a separate report indicated ECB officials are reportedly lacking enthusiasm for sub-zero tiering, whilst there has been no talks to cut the deposit rate.

The dollar gained for a second day amid thin volumes ahead of U.S. industrial production data. The Aussie slid after RBA minutes showed policy makers discussed cutting rates, while the Canadian dollar slipped alongside oil prices as equities rose.

In commodities, after a rally to five-month highs this month, crude oil paused on the prospect of Russia and OPEC boosting production to fight for market share with the United States. U.S. West Texas Intermediate was flat at $63.46 per barrel after losing nearly 0.8 percent the previous day. Oil has been surging on tightening global supplies, as output has fallen in Iran and Venezuela amid signs the United States will toughen sanctions on those two OPEC producers, and on the threat that renewed fighting could stop production in Libya.

Industrial production is among scheduled economic releases. Companies reporting earnings include Johnson & Johnson, Bank of America, UnitedHealth and Netflix.

Market Snapshot

- S&P 500 futures up 0.3% to 2,918.25

- STOXX Europe 600 up 0.3% to 389.38

- MXAP up 0.3% to 163.45

- MXAPJ up 0.4% to 544.55

- Nikkei up 0.2% to 22,221.66

- Topix down 0.09% to 1,626.46

- Hang Seng Index up 1.1% to 30,129.87

- Shanghai Composite up 2.4% to 3,253.60

- Sensex up 1.1% to 39,326.02

- Australia S&P/ASX 200 up 0.4% to 6,277.45

- Kospi up 0.3% to 2,248.63

- German 10Y yield rose 1.0 bps to 0.066%

- Euro up 0.04% to $1.1309

- Brent Futures down 0.5% to $70.83/bbl

- Italian 10Y yield rose 3.6 bps to 2.207%

- Spanish 10Y yield rose 1.3 bps to 1.097%

- Brent Futures down 0.5% to $70.83/bbl

- Gold spot down 0.3% to $1,284.72

- U.S. Dollar Index down 0.03% to 96.91

Top Overnight News from Bloomberg

- The U.K. labor market remained robust in the three months through February as employment jumped and wage growth far outpaced inflation. The number of people in work rose by 179,000 to a record high, keeping unemployment at 3.9%, the lowest rate since 1975, the Office for National Statistics said on Tuesday.

- German ZEW Expectations for April, a gauge of investor confidence, beat estimates.

- Congressional Democrats issued subpoenas to Deutsche Bank AG and other banks to obtain long- sought documents indicating whether foreign nations tried to influence U.S. politics, signaling an escalation of their probes into President Donald Trump’s finances and any dealings with Russians.

- Currency-only hedge funds were once a hot corner of the investment world. From 2000 to 2008 the tally of currency funds tracked by the BarclayHedge Currency Traders Index almost tripled, to 145. Now they’re looking more like an endangered species, with just 49 in operation.

- The People’s Bank of China shifted its tone on the economy, emphasizing that it will control excessive money supply amid signs of a recovery. It said it’ll keep good control of the money supply “floodgate” and not “flood” the economy with excessive liquidity, according to a statement released late Monday.

- Banco Santander SA has reassured investors in the riskiest type of bank debt with its decision to call $1.5 billion of its perpetual contingent convertible notes. Spain’s biggest lender said it will buy back the popular type of debt, known simply as CoCos.

Asian equity markets were mostly higher after the region eventually shrugged off the lacklustre lead from the US where mixed earnings from the large banks dampened risk appetite. ASX 200 (+0.4%) and Nikkei 225 (+0.2%) were initially cautious although sentiment gradually improved with Australia supported amid dovish views on the RBA and with Rio Tinto shares unfazed by weaker production numbers, while the Japanese benchmark just about remained afloat as several telecom names outperformed following reports NTT DoCoMo is to reduce mobile phone rates by as much as 40%. Hang Seng (+1.0%) and Shanghai Comp. (+2.4%) opened lower amid the early cautious tone across the region and tentativeness ahead of key Chinese data including GDP, Industrial Production and Retail Sales which are all due out tomorrow, although Chinese markets steadily improved to outperform their peers in the aftermath of the PBoC’s first liquidity injection in almost a month. Finally, 10yr JGBs were flat amid the indecisiveness in the region and uneventful price action in T-notes, while mixed results at the 20yr auction also failed to spur demand.

Top Asian News

- HNA Unit Defaults on Interest Payment, Faces Asset Seizures

- Citi Hails ‘Bullish Turn’ in China and Says Chase Metals Now

- China Traders Bet on Tight Liquidity as Interest-Rate Swaps Rise

European equities crept higher during early trade (Eurostoxx 50 +0.4%) following an upbeat tail-end to Asia-Pac session wherein the Shanghai Comp advanced in excess of 2% ahead of tomorrow’s China GDP release. Germany’s DAX (+0.7%) marginally outperforms its peers whilst broad-based gains are seen across other major bourses. Sectors are relatively mixed with outperformance seen in financials whilst energy names lag amid the price action in the complex. Notable movers include Lufthansa (-0.9%), after recouping from a 5.5% drop at the open amid a downgraded in EBIT guidance. Meanwhile Hays (-3.2%) shares tumbled to the foot of the Stoxx 600 amid disappointing earnings. Finally, UniCredit (+2.7%) shares felt some reprieve after the bank agreeing to pay USD 1.3bln to resolve investigations by US authorities regarding allegations that the bank violated multiple US sanction programmes. Looking ahead, markets will be looking out for earnings from UnitedHealth (at 10:55BST), Johnson & Johnson (11:45BST) and IBM (after-market), three DJIA components with the former accounting for 5.9% of the bellwether index. On a broader note, Morgan Stanley strategists believe that US stocks “sell off more than the rest of the world during a broad market sell-off”. This was measured by the S&P 500’s downside beta to the MSCI AC World Index (which the bank highlights is a measure of the US index’s performance when global shares decline), which is at a pre-financial crisis highs.

Top European News

- Nexi Declines in Milan After Europe’s Biggest IPO This Year

- U.K. Labor Market Remains Robust as Employment Surges

- Everyone ‘Exhausted’ by Brexit as Talks Drag On, EU’s Tusk Says

- Takeover Target G4S Moves Ahead With Breakup as Sales Rise

- Zalando Gains on German Online Retailer’s Unexpected Profit

In currencies, once again it seems that the official RBA policy statement failed to reveal all, as alongside the neutral stance and guidance maintaining no need to change rates in the near term there was a relatively detailed discussion about easing, to the extent that criteria was laid out. Hence, Aud/Usd has retreated to retest sub-0.7150 levels and the Aud/Nzd cross is back under 1.0600 even though the Kiwi also took heed of RBNZ Governor Orr reaffirming an easy bias overnight, with Nzd/Usd pivoting 0.6750 and now looking to the latest GDT auction and NZ CPI for more direction.

- CAD/EUR/CHF – All weaker vs the Greenback as well, with the Loonie still suffering in wake of Monday’s somewhat cautious if not downbeat BoC business survey and extending losses to circa 1.3400 at one stage, while the single currency has lost grip of the 1.1300 handle after topping out around a Fib at 1.1316 yet again. The latest German/EZ ZEW survey was mixed, and the accompanying comments not exactly confident about economic developments, but the final straw for Eur/Usd came via sourced ECB comments suggesting that several members are concerned about forecasts for a growth rebound in H2 and the accuracy of the models used to formulate estimates. The headline pair is now just above another Fib (1.1284), while the Franc has also lost more ground vs the Buck towards 1.0060, but is pivoting 1.1350 vs the Euro.

- GBP/JPY – Cable largely shrugged off broadly in line UK jobs and earnings data, but the Pound has drifted away from hefty option expiries at 1.3100 (1.6 bn) amidst a broader Dollar upturn as the DXY reclaims the 97.000 handle, albeit just and to the detriment of the aforementioned weakness elsewhere. Indeed, Usd/Jpy has slipped through 112.00 following another fade ahead of the 2019 peak and amidst export offers layered above the big figure.

- EM – Only minor respite for the Lira via better than expected Turkish IP data as Usd/Try remains around 5.8000 and still eyeing recent highs on a mixture of negative domestic factors – political, fiscal and fundamental.

- RBA Minutes from April 2nd meeting stated the board saw no strong case for near term move in rates but added that a rate cut would be appropriate if inflation stayed low and unemployment trended up, while the likelihood of a near-term rate hike was low given subdued inflation. The board also agreed inflation likely to stay muted for some time and expects further gradual progress on unemployment and inflation. (Newswires)

In commodities, WTI and Brent are choppy amid a lack of catalysts ahead of tonight’s API inventory release. Markets expect US crude stocks to build by around 2mln barrels whilst gasoline and distillates are forecast to draw by 2.55mln and 1mln barrels respectively. Elsewhere, metals are mostly lower as the dollar recoups some recent losses. In terms of precious metals, gold losses more ground below the 1300/oz level ahead of support at 1281/oz. Meanwhile, base metals trade marginally in the red ahead of tomorrow’s China GDP release. On that note, Rio Tinto stated that Q1 Pilbara iron ore shipments were at 69.1mln tons (Prev. 80.3mln tons Y/Y), whilst iron ore production 76.0mln tons (Prev. 83.1mln tons Y/Y), and copper output 143.9k tons (Prev. 139.3k tons Y/Y).

Looking at the day ahead, we’ve got March industrial production and the April NAHB housing market index print. Away from that we’re due to hear from the ECB’s Nowotny this afternoon at an event in New York, before the Fed’s Kaplan speaks this evening at a community forum event in New Mexico. Meanwhile the earnings highlights include Bank of America, Johnson & Johnson, UnitedHealth, Netflix and IBM.

US Event Calendar

- 9:15am: Industrial Production MoM, est. 0.2%, prior 0.1%

- 9:15am: Manufacturing (SIC) Production, est. 0.1%, prior -0.4%; Capacity Utilization, est. 79.15%, prior 78.2%

- 10am: NAHB Housing Market Index, est. 63, prior 62

DB’s Jim Reid concludes the overnight wrap

Easter week has started relatively quietly but as a reminder by the time the EMR lands through your virtual letter box tomorrow we’ll have a slew of important China data to digest. Will it confirm our suspicions from Q1 that China has created a new mini growth cycle? We’ll have a better idea this time tomorrow. This morning sees the German ZEW survey which is always closely followed, especially with the Germany economy at its current inflection point. So all that to look forward to as well as Thursday’s flash PMIs before you can unravel and devour those Easter Eggs. As for yesterday, after a bright start in Asia and Europe, equity markets dipped as US equity markets opened before a late run nearly got US markets back to flat. Nevertheless after a very good recent run some softness crept in as markets digested the latest US bank earnings and trade news. The end result was the S&P 500 closing -0.06% (-0.38% at the lows) and weaker for only the second time in the last 13 sessions. The last time we had such a run was October 2017. The NASDAQ (-0.10%) and DOW (-0.10%) also dipped while in Europe the STOXX 600 (+0.15%) ended with a small gain but slightly off the session’s high of +0.27%.

Just on those earnings reports, while the GS and Citi results beat at a headline level for earnings, revenues did disappoint slightly. So JPM’s bumper results on Friday might be a bit more company specific than sector wide. It’s also worth noting that earnings expectations have been heavily slashed in recent months which is certainly helping the optics. For GS for example, EPS of $5.71 was a long way ahead of the $4.97 consensus however that is down from $5.50 at the end of March and closer to $6.00 at the start of the year. The talk was also that equity trading revenues disappointed at GS along with the outlook for the investment banking business. Their shares fell -3.84%. Citi shares pared losses to end the session close to flat. It’s worth noting that BofA results are out later today.

As for other markets yesterday, 10y Treasuries pulled back to 2.551% which was -1.4bps lower, while bunds closed flat at 0.056%. They did hit a vertigo inducing 0.079% at lunchtime though. Greek 10-year yields extended their recent rally, trading -0.9bps lower to 3.274%, within 7bps of the lowest yields based on bbg data going back to 1997. Later I’m going to dig through the archives to see if I have any longer history for Greek government bonds. WTI oil prices slid -0.59%, though there were limited catalysts yesterday. Investors were possibly reacting to Friday’s data showing a second weekly increase in the US rig count, as well as data showing that speculative long positioning in the commodity has risen to its highest level since last October. Credit markets were quiet with HY spreads -1bps and -4bps in the US and Europe respectively. Staying with credit it is worth highlighting that Michal Jezek from my team published a new report last week entitled “Value of high-grade corporate bonds in Japanified Europe” (click here ). The note examines the European IG market in light of recent developments on the data and policy fronts, and identifies the most attractive opportunities. It also assesses how much a restarting of CSPP is priced in.

This morning in Asia markets are largely moving higher with the Shanghai Comp (+1.11%), Hang Seng (+0.63%), Nikkei (+0.18%) and Kospi (+0.06%) all up. Elsewhere, futures on the S&P 500 are also up +0.11%. In other news, South Korea’s Yonhap News reported that Russia is preparing for North Korean leader Kim Jong Un’s first summit with President Vladimir Putin. Separately the South Korea’s Maeil Business Newspaper reported yesterday that Putin and Kim’s summit will likely take place on April 24 in Vladivostok. However Russian government spokesman Dmitry Peskov said that plans were being made for a summit but offered no details on a time or place.

Moving on. In terms of the latest trade news, US Treasury Secretary Mnuchin said yesterday that US-China trade negotiations were “making a lot progress” but also that there “is more work to do…including enforcement”. That appeared to mirror a lot of what he had said over the weekend. Meanwhile, a separate Bloomberg story also suggested that China was considering a request from the US to shift certain tariffs on agricultural goods to other products “so the Trump administration can sell any eventual trade deals as a win for farmers ahead of the 2020 election”. Unconfirmed reports also circulated that President Trump may meet President Xi at the June 28-29 G20 summit, which could be an opportunity to finalize a trade agreement, though of course things can change over the next few weeks and months.

It wasn’t just US-China trade headlines yesterday though with Reuters also quoting the EU’s Malmstrom as saying that the EU is “ready to start trade talks” and that it is in the “US’ hands to see when talks start”. EU ministers yesterday gave the go ahead for formal talks to start and it’s worth noting that it’s just over a month until the S232 deadline for making a decision on auto tariffs, so we’re approaching a potentially important spell for trade talks.

In other news, it was a very quiet day for data yesterday with only the April empire manufacturing print in the US out. The headline reading was solid enough at 10.1, beating expectations for 8.0 and up from 3.7 in March however there was a big drop in the six-month outlook reading to 12.4 from 29.6 last month. That was in fact the lowest outlook reading since January 2016 so a fairly unusual dichotomy between the current conditions and the forward-looking readings.

Elsewhere Chicago Fed President Evans made some interesting public remarks. He is a voting member of the FOMC this year and has been near the centre of the committee on policy. He noted that economic data is “quite good” and that he expects to keep rates “flat and unchanged into the fall of 2020.” However, his more newsworthy remarks were in reference to the Fed’s policy review, as Evans said that “the Fed must be willing to embrace inflation modestly above 2 percent 50 percent of the time.” That would presumably suggest a preference for more dovish policy and higher inflation rates moving forward. Elsewhere, Boston Fed President Rosengren (voter) said in published remarks of a speech overnight that the US economy is doing quite well but inflation is “slightly below” the Fed’s 2% target and this is one of the reasons for the Fed to be patient. On policy review, he said that “My own preference is for the Federal Reserve to adopt an inflation range that explicitly recognizes the challenge of the effective lower bound,” while adding, “We might be forced to accept below-2% inflation during recessions, but we would commit to achieving above-2% inflation in good times, so as to provide more policy space to counteract the next recession.” Separately, the Bank of France Governor Villeroy said that economic growth is developing more weakly than he expected so far this year, though he expects a rebound later this year. He also said that the effects of negative rates are overall positive, but he did reiterate that he would be open to mitigating measures if necessary.

Finally to the day ahead which starts this morning in the UK with the February and March employment stats. Not long after that we get the April ZEW survey in Germany while this afternoon in the US we’ve got March industrial production and the April NAHB housing market index print. Away from that we’re due to hear from the ECB’s Nowotny this afternoon at an event in New York, before the Fed’s Kaplan speaks this evening at a community forum event in New Mexico. Meanwhile the earnings highlights include Bank of America, Johnson & Johnson, UnitedHealth, Netflix and IBM.

end

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 75.81 POINTS OR 2.39% //Hang Sang CLOSED UP 319.15 POINTS OR 1.07% /The Nikkei closed UP 52.55 POINTS OR 0.24%/ Australia’s all ordinaires CLOSED UP .38%

/Chinese yuan (ONSHORE) closed UP at 6.7094 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 63.42 dollars per barrel for WTI and 71.11 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.7094 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7115 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

China/USA/VENEZUELA:

China lashes out at Mike pompeo for interference in its affairs with respect to Venezuela and other nations in Latin America

(courtesy zerohedge)

“Pompeo Has Lost His Mind” – China Hits Back At Latin America Remarks

China has come out swinging after Mike Pompeo’s three-day Latin America tour in which the Secretary of State publicly called outChina for spreading “disorder” in Latin America alongside Russia. Pompeo identified the two countries, both of which have over the past two months condemned US efforts toward regime change in Venezuela, of backing failing investment projects that only fuel corruption and undermine democracy, especially in Venezuela.

China’s ambassador to Chile, Xu Bu, quickly lashed out in response to America’s top diplomat blaming China for Latin America’s economic woes which first came last Friday while standing alongside Chilean President Sebastian Pinera. Ambassador Xu told the Chilean newspaper La Tercera: “Mr Pompeo has lost his mind.”

Pompeo had asserted during his tour that Chinese investment and economic intervention in Venezuela, now facing financial and infrastructural collapse amidst political turmoil, had “helped destroy” the country and said Latin American leaders must therefore see who their “true friend” is.

“China’s bankrolling of the Maduro regime helped precipitate and prolong the crisis in that country,” Pompeo had stated, and further described Maduro as “a power-hungry tyrant who has brought ruin to his country and to his people”.

“I think there’s a lesson … to be learned for all of us: China and others are being hypocritical calling for non-intervention in Venezuela’s affairs. Their own financial interventions have helped destroy that country,” Pompeo added.

China is Venezuela’s biggest foreign creditor has provided up to $62bn in loans since 2007, according to estimates.

The Chinese foreign ministry didn’t hold back in its response: “For some time, some US politicians have been carrying the same version, the same script of slandering China all over the world, and fanning the flames and sowing discord everywhere,” Ministry spokesman Lu Kang said in a Monday statement.

“The words and deeds are despicable. But lies are lies, even if you say it a thousand times, they are still lies. Mr Pompeo, you can stop,” the spokesman said.

Hinting at Washington’s Cold War era record of overthrowing governments in Latin America — a longstanding tradition that can be traced all the way back to the Cold War, the statement added: “The Latin American countries have good judgment about who is their true friend and who is false, and who is breaking rules and making trouble,” Lu said.

The Chinese Ambassador to Chile’s remarks had also remotely invoked a continued Monroe Doctrine mentality on the part of US officials, saying “Pompeo’s body has entered the 21st century but his mind remains in the 20th century, full of thoughts about hegemony and the cold war,” Amb. Xu told La Tercera.

In addition to being the Maduro government’s single largest creditor, China has recently offered to help Venezuela with its failing power grid, after a series of devastating mass outages over the past month has resulted in “medieval” conditions amidst an already collapsing infrastructure. This as Pompeo and Bolton came close to positively celebrating the mass outages as proof of the ineptness of the Maduro regime.

Beijing also recently denied it has deployed troops to Venezuela after media reports a week ago cited online photos which appeared to show a Chinese military transport plane deployed to Caracas.

Given how boldly and directly Chinese officials’ Monday statements were, it appears Beijing’s patience with Pompeo is running thin, to the point of giving up on a positive avenue with the White House, also amidst a broader trade war. It appears the proverbial gloves are coming off.

A Global Rally Killer Has Emerged In China

Back in early October, the market catalyst that killed the US rally and sent stocks tumbling into a brief bear market after Powell warned that the neutral rate was a “long way away”, was the sudden spike in yields, which surged above 3.3%, breaking out above long-term resistance, and leading to renewed speculation that the 30 year long bull market in bonds is (again) officially over.

But while US yields have remained stubbornly low, perhaps in anticipation of rate cuts and/or QE4, perhaps due to increased buying from foreigners due to sliding FX hedging costs, there is one place where yields have recently soared much higher: the same place whose massive credit expansion in the past three months has led to renewed hopes for global “green shoots”, and speculation that the economic slump is now over – China.

After surging in the the first two weeks of April at the fastest pace in more than 2 years, on Monday Chinese ten-year yields rose to 3.38% Monday, extending their highest levels this year. And while for much of the recent advance Chinese equities were willing to ignore the spike in interest rates, in the past week Chinese stocks have been ominously toppy, and have continued to slide in Tuesday’s session.

As a result, and perhaps due to fears that Chinese liquidity is again getting too tight, on Tuesday the PBOC broke its streak of 18 consecutive days without open market interventions, and injected a net of 40 billion yuan via 7 day reverse repos. That plus concerns that the Chinese central bank will not cut rates as previously consensus had expected, stocks have topped out, even as 10Y yields have continued marching higher, and hit 3.40% in early Tuesday trading, the highest level since mid-December. In other words as Bloomberg’s Wes Goodman writes, while the PBOC says it will keep good control of the money supply, “yields may have more to rise even if the central bank is trying to temper the pace of the advance.”

The risk is that if yields rise even higher, the rally in Chinese stocks – which has outperformed all major markets in 2019 – is now officially over.

And, all else equal, it does appears that Chinese liquidity will shrink even more in the coming weeks, and local markets will face tighter credit conditions this quarter than in 1Q after the PBOC indicated the current pace had gone beyond its target. That, as Yinan Zhao cautions, is going to add to the pain for slumping sovereign bonds as investors face an uncertain economic outlook and reduced chances for stronger easing.

1Q credit growth at 10.7% was way above the PBOC’s goal to keep it “in line with the pace of nominal GDP,” a range it specifically emphasized in yesterday’s policy statement. It usually doesn’t go into that much detail on credit growth goals.

The PBOC emphasized a need for a balanced approach. Given 10-year yields are rising at the fastest pace in more than 2 years, that’s perhaps not the message fixed-income investors would have been hoping for.

But wait, there’s more: while US traders are casting a fearful eye on just how bad the EPS contraction in Q1 earnings season will be (and whether it will recover in Q2 and onward) in China it will be far worse. Indeed, the sharp Monday slump in Chinese small caps “underscores the dangers for mainland stock markets as what could be an ugly earnings season kicks off and steals the limelight from stimulus hopes”, as Bloomberg’s Kyoungwha Kim writes today.

Here’s the punchline: while US stocks are expected to post a roughly 4% drop Y/Y, China small cap earnings will be a massacre, with Q1 EPS on the ChiNext board forecast to slump 29% y/y, following a 12% drop in the prior quarter. That’s in line with China’s dour Jan.-Feb. economic data. Paradoxically, as earnings tumbled, the ChiNext index soared by over 35% during the same period, so any disappointment in earnings will lead traders to rush for the exits… especially if rates keep rising as liquidity shrinks. This will keep markets volatile in April, especially as the ChiNext’s double top formation sets the gauge up for a correction.

The silver lining in China, just like in the US, is that any earnings recession is expected to be brief: in Q2 earnings are already predicted to rebound, largely thanks to the recent VAT cut, with overall 2019 EPS growth for the ChiNext seen at 52%.

Whether or not that happens will ultimately depend on whether Chinese interest rates keep rising from here, and will also likely determine the fate of the global rally which, all else equals, is now entering extremely overbought territory.

4/EUROPEAN AFFAIRS

i)Italy

Yesterday I brought to your attention the dire problems inside Turkey. Today I bring to you the other country with major problems: Italy

(courtesy Don Quijones/WolfStreet)

A Big Old Problem Just Re-Erupted On Eurozone’s Southern Flank

Authored by Don Quijones via WolfStreet.com,

Italy’s fiscal health is once again in serious decline…

Last week, Italy’s coalition government slashed its growth forecast for the Italian economy in 2019 to 0.2% – the weakest forecast in the Eurozone – from a previous forecast of 1%. Italy is already in a technical recession after chalking up two straight quarters of negativeGDP growth in the second half of 2018.

The government’s budget for this year was based on the assumption that the economy would expand by 1% this year. Now, it seems the economy may not grow at all; it could even shrink.

One direct result of this is that Italy’s current account deficit for 2019 will be substantially higher than the 2.04% of GDP Italy’s government pledged to stick to late last year. And that can mean only thing: another standoff between Rome and Brussels over the direction of fiscal policy is in the offing.

Italy already boasts the largest public debt pile in Europe in nominal terms, clocking in at €2.14 trillion, as well as the second largest in relative terms after Greece’s twice bailed out economy. Rome just forecast that public debt would hit a new record high of 132.6% of GDP this year. That record is unlikely to last very long given Italy’s stagnating economy and the government’s determination to cut taxes, reduce the retirement age and introduce a citizens’ basic income.

The biggest problem with Italy’s economy is that many of its problems are chronic and deep seated. Many of them date back to the adoption of the euro, in 2000, or in the case of Rome’s massive addiction to public debt, to the 1980s. As the OECD points out, real GDP in Italy is still well below its pre-crisis peak. Italy is also the only OECD country where incomes (as measured by GDP per capita) are no higher than in 2000. By contrast, in France, Spain, the UK and Germany they have risen during the same period by 13%, 17%, 21% and 23 respectively.

The IMF now envisages Italy’s public debt ratio ratcheting up to 134.4% of GDP in 2020 to 138.5% in 2024. As the debt increases, so too will the interest payments on the debt. That is unsustainable, especially with much of that debt scheduled to fall due in the next few years. In 2019 alone, Italy has an eye-watering €250 billion of bond redemptions to fund, which is roughly the equivalent of all Eurozone bond maturities this year.

And now Rome doesn’t even have the ECB to rely on to buy up over half of the bonds it issues. Of course, in these yield-starved times investors will gobble up higher yielding Italian bonds, at least for a while. But a risk that those yields will climb too high, at which point bond vigilantes will take matters into their own hands, as happened in 2012 when the yields on Italy’s 10-year bonds soared to 7%.

Before that happens again, something will have to give. If Italy had its own currency and were in control of its own monetary policy, it could try to inflate the debt away — whatever that might do to its own currency. But it isn’t and it can’t. Alternatively, it could, like Greece, default on its debt, with dire consequences for holders of that debt, including Italian households and domestic and foreign banks.

The one other option open to Rome is one that has also already been tried, with limited success, by Greece — i.e., to slash public spending, hike taxes, privatize public assets, squeeze the informal economy, and impose a harsh austerity regime. This is the path recommended by the OECD, but it would virtually guarantee electoral suicide for Italy’s coalition government partners which will do whatever they can to avoid alienating the very voters who gave them their first real taste of power.

In other words, none of these classic solutions are realistic options for a country as big and as systemically important as Italy. That the country is now being run by two relatively nascent anti-austerity parties that are not wholly enamored with the European project and as such are willing to face down diktats from Brussels, at least up to a point, further heightens the risk of conditions spiraling out of control.

Italy is home to an extremely fragile financial sector with the highest NPL ratio and lowest return on assets of any of the major European economies. The French government has already warned that an economic recession in Italy could pose as great a risk, if not greater, to the EU than Brexit.

And it makes sense for the French government to be worried. The economies of both Italy and France are tightly interwoven, with annual trade flows of around €90 billion. More important still, French banks are, by a long shot, the largest foreign owners of Italian public and private debt, with total holdings of €311 billion as of the 3rd quarter of 2018, according to the Bank for International Settlements.If Italy defaulted, French banks would take an almighty hit to their balance sheets.

ECB Credibility Crumbles As “Significant Minority” Of Governors Say Growth Projections “Overly Optimistic”

When the ECB slashed its growth forecast for 2019 from 1.7% to 1.1% of GDP back in March, some observers questioned the logic behind Mario Draghi’s insistence that the headwinds facing the eurozone economy would dissipate during the second half of the year, chalking it up to more of that signature European ‘magical thinking’.

Now it appears that several of Draghi’s fellow policy-setters would agree with these critics. To wit, according to Reuters, one of the ECB’s favorite trial balloon transmission mechanisms, a “significant minority” of Draghi’s fellow policymakers have thrown up all over the latest ECB forecast for 2019 – which was echoed by the IMF – claiming off the record that it was unjustifiably rosy, and seeing little chance that the second half rebound promised by Draghi would materialize.

Some policymakers went so far as to shoot what’s left of the central bank’s credibility in the foot, or any other bodily organ and/or appendage, and questioned whether the ECB’s projection models should be revisited. And while Draghi was reportedly open to discussing these concerns, he remains opposed to a revamp of the central bank’s methodology for obvious reasons as it would suggest that just like the Fed, the ECB is similarly just as clueless.

As Reuters reports, a “significant minority” of rate-setters in last week’s policy meeting “expressed doubt that a long projected growth recovery is coming in the second half of the year and some even questioned the accuracy of the ECB’s projection models, given their long history of downward revisions.”

With the ECB using the these projections as a key input into policy decision, more cuts in growth and inflation forecasts would raise the chance that the bank’s first post crisis rate, now seen next year, is delayed even longer.

[…]

Some governors went as far as saying that the ECB’s forecasting methodology may need to be reviewed since projections are persistently too optimistic and are regularly cut quarter after quarter, the sources said. The ECB now sees 2019 growth at 1.1 percent but projected 1.7 percent just three months ago.

While others are also prone to forecasting errors, the U.S. Federal Reserve does not publish a single projection, even if individual governors make their forecasts public. And while Fed governors also erred on growth recently, their projections on inflation have been relatively solid.

Some ECB policymakers thought there may be an inherent bias in the bank’s forecasts as they always show inflation on an upward slope, moving toward the ECB’s target and growth returning to trend.

Their concerns include the possibility that trade wars might be permanent, and that a one-off hit to the German auto sector might last longer than some have said.

While Germany’s vast car sector did take a one-off hit from an adjustment to new emissions-testing methods, more permanent factors could include shifting consumption habits, a move away from diesel and weak Chinese demand, some governors argued, according to the sources.

The policymakers added that weak global trade growth also appears to be more permanent, trade wars now look to be the norm rather than the exception and even if Chinese growth looks to be stabilizing, demand from Beijing is unlikely to surge.

Meanwhile, a second trial balloon released on Tuesday further undermined confidence in Draghi as the ECB chief prepares to step down, when his second term ends later this year.

According to a parallel report by Bloomberg,several board members are unenthusiastic about the prospect of adopting interest-rate “tiering”, which has been all the rage recently in terms of additional stimulus measures, and represents a policy that – just like in Japan and Switzerland – would alleviate pressure on European banks and contribute to the further ‘Japanification’ of Europe.

Though no proposals have been made on the matter yet, and the topic was conspicuously missing from last week’s ECB press conference, it had been reported that this option was explored as part of a review of the central bank’s policy of negative interest rates after Draghi surprised investors last month by calling on the bank to “reflect” on a policy revamp.

Draghi didn’t consult the Governing Council before his remarks last month, and while he didn’t mention rates tiering by name, the comments prompted speculation that the ECB could introduce a version of the policy, which is already being used in Japan, Switzerland and Denmark.

Given the central bank’s surprisingly dovish turn in March, where it communicated that rates would now be on hold at least through the end of the year and announced another round of TLTROs, we can’t help but wonder if there’s a mutiny brewing inside the central bank, and whether Draghi’s legacy as ECB chief could be seriously undermined during his last months at the helm.

The euro tumbled on the Reuters’ headline, but then it promptly rebounded higher when the BBG story hit:

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

Turkey

A Turkish economist is arrested after insulting Erdogan on Twitter

(courtesy zerohedge)

6.GLOBAL ISSUES

7 OIL ISSUES

8. EMERGING MARKETS

VENEZUELA

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:00 AM….

Euro/USA 1.13O2 DOWN .0003 REACTING TO MERKEL’S FAILED COALITION/ REACTING TO +GERMAN ELECTION WHERE ALT RIGHT PARTY ENTERS THE BUNDESTAG/ huge Deutsche bank problems ///ITALIAN CHAOS /AND NOW ECB TAPERING BOND PURCHASES/JAPAN TAPERING BOND PURCHASES /USA RISING INTEREST RATES /FLOODING/EUROPE BOURSES /MIXED

USA/JAPAN YEN 111.88 down .068 (Abe’s new negative interest rate (NIRP), a total DISASTER/NOW TARGETS INTEREST RATE AT .11% AS IT WILL BUY UNLIMITED BONDS TO GETS TO THAT LEVEL…

GBP/USA 1.3085 DOWN 0.0014 (Brexit March 29/ 2019/ARTICLE 50 SIGNED/BREXIT FEES WILL BE CAPPED/BREXIT EXTENDED TO OCT 31/2019//

USA/CAN 1.3383 UP .00015 CANADA WORRIED ABOUT TRADE WITH THE USA WITH TRUMP ELECTION/ITALIAN EXIT AND GREXIT FROM EU/(TRUMP INITIATES LUMBER TARIFFS ON CANADA/CANADA HAS A HUGE HOUSEHOLD DEBT/GDP PROBLEM)

Early THIS TUESDAY morning in Europe, the Euro FELL by 3 basis points, trading now ABOVE the important 1.08 level FALLING to 1.1302 Last night Shanghai COMPOSITE CLOSED UP 75.81 POINTS OR 2.39%.

//Hang Sang CLOSED UP 31.15 POINTS OR 1.07%

/AUSTRALIA CLOSED UP .38%// EUROPEAN BOURSES //MIXED

The NIKKEI: this TUESDAY morning CLOSED UP 52.55 POINTS OR 0.24%

Trading from Europe and Asia

1/EUROPE OPENED MIXED

2/ CHINESE BOURSES / :Hang Sang CLOSED UP 319.15 POINTS OR 1.07%

/SHANGHAI CLOSED UP 75.81 POINTS OR 2.39%

Australia BOURSE CLOSED UP .38%%

Nikkei (Japan) CLOSED UP 52.55 POINTS OR 0.24%

INDIA’S SENSEX IN THE GREEN

Gold very early morning trading: 1284.60

silver:$14.96