GOLD: $1271.45 DOWN $4.45 (COMEX TO COMEX CLOSING)

Silver: $14.82 DOWN 21 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1272.55

silver: $14.84

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 43/69

EXCHANGE: COMEX

CONTRACT: APRIL 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,273.500000000 USD

INTENT DATE: 04/22/2019 DELIVERY DATE: 04/24/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 1

661 C JP MORGAN 43

685 C RJ OBRIEN 4

737 C ADVANTAGE 65 25

____________________________________________________________________________________________

TOTAL: 69 69

MONTH TO DATE: 6,382

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 69 NOTICE(S) FOR 6900 OZ (0.3146 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 6382 NOTICES FOR 638,200 OZ (19.8506 TONNES)

SILVER

FOR APRIL

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 775 for 3,875,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE :$5507 UP $150

Bitcoin: FINAL EVENING TRADE: $5556 UP $207

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL A GOOD SIZED 3078 CONTRACTS FROM 220,936 DOWN TO 217,858 DESPITE YESTERDAY’S 4 CENT RISE IN SILVER PRICING AT THE COMEX AS WE HAVE A STARTED OUR CUSTOMARY LIQUIDATION OF SPREADERS ONE WEEK PRIOR TO FIRST DAY NOTICE WHICH IS APRIL 30. TODAY IS APRIL 23 AND ONE WEEK PRIOR TO FIRST DAY NOTICE…. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 403 FOR MAY, 120 FOR JUNE 278 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 681 CONTRACTS. WITH THE TRANSFER OF 681 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 681 EFP CONTRACTS TRANSLATES INTO 3.405 MILLION OZ ACCOMPANYING:

1.THE 4 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

AND NOW 3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

28,454 CONTRACTS (FOR 16 TRADING DAYS TOTAL 28,454 CONTRACTS) OR 142.27 MILLION OZ: (AVERAGE PER DAY: 1778 CONTRACTS OR 8.892 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 142.27 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 20.40% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 710.07 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3078 DESPITE THE 4 CENT RISE IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 681 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS HAVE NOT YET STARTED THEIR LIQUIDATION OF THE SPREAD TRADES.

TODAY WE LOST A CONSIDERABLE SIZED: 2397 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 681 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 3078 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 4 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $15.03 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.093 BILLION OZ TO BE EXACT or 156% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR nil OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ AND NOW APRIL AT 3.880 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 2437 CONTRACTS, TO 438,529 WITH THE RISE IN THE COMEX GOLD PRICE/(A GAIN IN PRICE OF $1.75//FRIDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 2318 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 2318 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 438,529. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4755 CONTRACTS: 2437 OI CONTRACTS INCREASED AT THE COMEX AND 2318 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 4755 CONTRACTS OR 475500 OZ OR 14.79 TONNES. YESTERDAY WE HAD A GAIN IN THE PRICE OF GOLD TO THE TUNE OF $1.75….AND YET WITH THAT SMALL RISE, WE STILL HAD A VERY STRONG GAIN IN TONNAGE OF 14.79 TONNES!!!!!!.??????????????????????????????????????????

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 110,837 CONTRACTS OR 11,083,700 OR 344.74 TONNES (16 TRADING DAYS AND THUS AVERAGING: 6297 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAYS IN TONNES: 344.74 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 344.74/3550 x 100% TONNES = 9.69% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1718.14 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIR SIZED INCREASE IN OI AT THE COMEX OF 2437 WITH THE GAIN IN PRICING ($1.75) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A SMALL SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 2318 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 2318 EFP CONTRACTS ISSUED, WE HAD A VERY GOOD GAIN OF 5580 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

2318 CONTRACTS MOVE TO LONDON AND 2437 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 14.79 TONNES). ..AND THIS GOOD DEMAND OCCURRED WITH A SMALL RISE IN PRICE OF $1,75 IN YESTERDAY’S TRADING AT THE COMEX.

we had: 69 notice(s) filed upon for 6900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $4.45 TODAY

NO CHANGES AT THE GLD//

INVENTORY RESTS AT 751.68 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 21 CENTS TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLSV//

/INVENTORY RESTS AT 311.979 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A STRONG SIZED 3078 CONTRACTS from 220,936 DOWN TO 217,858 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..IT LOOKS LIKE OUR SPREADERS HAVE COMMENCED THEIR RITUAL OF COMEX LIQUIDATION AS THEIR USUAL MODUS OPERANDI BEGINS ONE WEEK PRIOR TO FIRST DAY NOTICE (APRIL 30_ AND TODAY IS APRIL 23)

HERE IS HOW THE CROOKS USED SPREADING AS WE ENTER AN ACTIVE DELIVERY MONTH. THUS SILVER HAS THE ACTIVE MONTH OF MAY COMING UP AND THUS SPREADERS DO THE FOLLOWING:

“YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF APRIL BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 403 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 278 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 681 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 3078 CONTRACTS TO THE 681 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG SIZED LOSS OF 2397 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 11.11MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH. AND NOW 3.880 MILLION OZ FOR APRIL.

RESULT: A STRONG SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 4 CENT RISE IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A GOOD SIZED 681 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 16.45 POINTS OR 0.51% //Hang Sang CLOSED DOWN 0.02 POINTS OR 0.00% /The Nikkei closed UP 41.84 POINTS OR 0.19%/ Australia’s all ordinaires CLOSED UP .96%

/Chinese yuan (ONSHORE) closed DOWN at 6.7192 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 65.92 dollars per barrel for WTI and 74.23 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.7192 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7221 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

i

3A//NORTH KOREA

b) REPORT ON JAPAN

Japan

3 China/Chinese affairs

i)China/

4/EUROPEAN AFFAIRS

i)EU/USA

Fasten your seat belt: there is going to be a huge transatlantic trade war beginning in May and agriculture will be at the centre. The EU just does not let any agriculture into their sphere

(courtesy Mish Shedlock/Mishtalk)

ii)UK

Theresa May is now ready to bring back the Brexit legislation for the 4th time

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)ISIS/SRI LANKA

Isis states that they are the ones behind the bombings in Sri Lanka and it was in retaliation for the New Zealand mosque massacre

( zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)ARGENTINA

9. PHYSICAL MARKETS

i)there is no question on this: Judy Shelton, a true gold bug and strong money advocate, is the right nominee for the Fed

( New York Sun//GATA)

i b)This is why we need Judy Shelton at the Fed..she wants gold as the center piece of monetary reform.

( Judy Shelton/Wall Street Journal)

ii)Gold trading:

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning/FOMC

ii)Market data

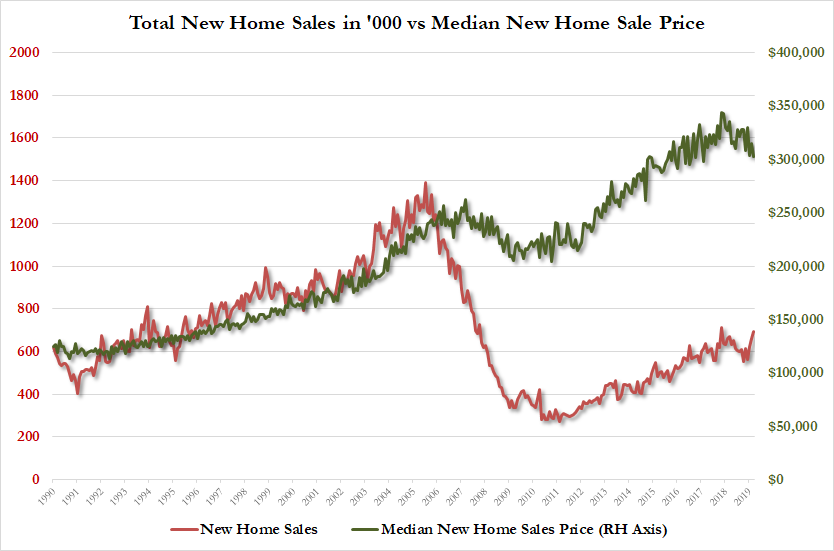

a)New home sales soar to 16 month highs but it is all due to prices plunging

( zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

a)An update on Social Security in the uSA. In earned a tiny 2.8% on its money last year and the reason for the poor return is that it is only invested in USA government bonds. Starting next year the fund will expend more money than it brings in. In 2026 it will be broke

( zerohedge)

b)Michael Snyder believes we are going to have a repeat of 1973 when oil skyrocketed because of the Yom Kippur war. We ended up with considerable stagflation

( Michael Snyder)

SWAMP STORIES

my goodness: Schiff is such a doorknob

( zerohedge)

Let us head over to the comex:

AFTER APRIL, WE HAVE THE ACTIVE DELIVERY MONTH OF MAY AND HERE THE OI FELL BY 11,953 CONTRACTS DOWN TO 69,050. CONTRACTS.. THE NEXT MONTH OF JUNE GAINED 40 CONTRACTS TO 267. AFTER JUNE, THE VERY BIG DELIVERY MONTH OF JULY HAD A GAIN OF 8579 CONTRACTS UP TO 108,837 CONTRACTS.

Gold Plunges Towards Key Technical Level After $1.5 Billion Notional Dump

Gold futures suddenly took a turn for the worse this morning as ‘someone’ once again decided that 0830ET was the perfect time to puke over $1.5 billion notional of the precious metal into the market…

Over 11,500 gold futures contracts suddenly dumped into the market…

…pushing it towards its 200DMA…

Silver is also getting hit…

As the London Fix looms…

Not Manipulated though.

Russia’s 2019 Gold Rush Continues: Buys 600,000 Ounces of Gold In March

– Russia buys 18.7 tonnes of gold bullion in March 2019

– Russia’s official gold holdings are now 2,150.5 tonnes which as a percent of foreign exchange reserves in gold is 19.1% (see table)

– Russia liquidated 85% of its US Treasury holdings in just two months in April and May 2018

– Russia dumped over $90 billion of Treasuries in April and May as holdings collapsed from near $100 billion to just $9 billion

– Russia sees gold’s role as independent currency and safe haven as is a “100% guarantee from legal and political risks”

– Russia and China’s gold buying is set to continue and may accelerate

Russia and it’s central bank added another 600,000 troy ounces or 18.7 tonnes of gold to its reserves in March according to the latest figures released in a press release by the Russian central bank on Good Friday.

Yesterday, the International Monetary Fund (IMF) published and released its Russian gold data which was different to the amount of gold announced by the Russian central bank. The IMF said that Russia raised its gold holdings by 19.4 tonnes in March as reported by Reuters. There was no clarification as to the discrepancy and we await an explanation for it.

Source: Wikipedia

Russia’s total foreign exchange reserves are $491 billion and their gold allocation has risen to 19% of their total reserves – even at these depressed gold prices.

Russia dumped some $90 billion of US Treasuries in April and May of 2018 – which is close to the current value of the entire Russian gold reserves, now worth c. $90 billion.

The Russian central bank, President Putin and senior politicians and policy makers have spoken about the importance of gold as a form of financial and monetary insurance. They believe gold provides valuable insurance against monetary and geopolitical risks. Manager of monetary policy at the central bank, Dmitry Tulin, recently said of gold:

“The price of it swings, but on the other hand it is a “100% guarantee from legal and political risks”.

Russia and China’s gold buying is set to continue and may even accelerate given the heightened financial and geopolitical risks and due to both increasingly powerful nations confidence in gold as a hedge and safe haven.

News & Commentary

PRECIOUS-Gold eases as strong equities check support from Iran sanctions (Reuters.com)

Gold ends higher after settling last week at 2019 low (MarketWatch.com)

Gold holds steady on softer dollar, U.S.-Iran tensions (Reuters.com)

U.S. to end all waivers Iran oil imports, crude price jumps (Reuters.com)

World’s Oldest Gold Object May Have Just Been Unearthed in Bulgaria (GoldReview.com)

London Home Prices Had Biggest Monthly Drop Since Lehman (ZeroHedge.com)

Australia Is On The Brink Of A Housing Collapse That Resembles 2008 (Forbes.com)

This is Bigger than Gold & Silver Manipulation – Chris Powell (USAWatchDog.com)

The case for monetary regime change – Shelton (WSJ.com)

Have a look inside the West Point Mint’s massive gold vaults and coin operations (Fox5NY.com)

Gold Prices (LBMA PM)

18 Apr: USD 1,276.50, GBP 981.12 & EUR 1,134.17 per ounce

17 Apr: USD 1,276.10, GBP 978.77 & EUR 1,127.82 per ounce

16 Apr: USD 1,283.75, GBP 981.30 & EUR 1,137.40 per ounce

15 Apr: USD 1,286.75, GBP 982.43 & EUR 1,137.23 per ounce

12 Apr: USD 1,296.15, GBP 991.68 & EUR 1,146.06 per ounce

Silver Prices (LBMA)

18 Apr: USD 15.00, GBP 11.49 & EUR 13.27 per ounce

17 Apr: USD 15.00, GBP 11.49 & EUR 13.27 per ounce

16 Apr: USD 14.94, GBP 11.42 & EUR 13.22 per ounce

15 Apr: USD 14.93, GBP 11.39 & EUR 13.20 per ounce

12 Apr: USD 15.06, GBP 11.51 & EUR 13.31 per ounce

Recent Market Updates

– When Should You Sell Your Gold and Silver? (GoldCore Video)

– Understanding Gold: A Step By Step Guide To Gold As An Asset Class

– World Trade Suffers Biggest Collapse Since Financial Crisis

– Exclusive Offer: Secure Gold and Silver Storage In Zurich For Free For Six Months

– There Is Too Much Debt In The World – World Bank

– How to Store Gold in an Uncertain World

– The ECB Is Struggling With Inflation, Interest Rates and The Outlook

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

This is why we need Judy Shelton at the Fed..she wants gold as the center piece of monetary reform.

(courtesy Judy Shelton/Wall Street Journal)

Judy Shelton: The case for monetary regime change

Submitted by cpowell on Mon, 2019-04-22 21:01. Section: Daily Dispatches

By Judy Shelton

The Wall Street Journal

Monday, April 22, 2019

https://www.wsj.com/articles/the-case-for-monetary-regime-change-1155587…

Since President Trump announced his intention to nominate Herman Cain and Stephen Moore to serve on the Federal Reserve’s board of governors, mainstream commentators have made a point of dismissing anyone sympathetic to a gold standard as crankish or unqualified.

But it is wholly legitimate, and entirely prudent, to question the infallibility of the Federal Reserve in calibrating the money supply to the needs of the economy. No other government institution had more influence over the creation of money and credit in the lead-up to the devastating 2008 global meltdown. And the Fed’s response to the meltdown may have exacerbated the damage by lowering the incentive for banks to fund private-sector growth.

…

What began as an emergency decision in the wake of the financial crisis to pay interest to commercial banks on excess reserves has become the Fed’s main mechanism for conducting monetary policy. To raise interest rates, the Fed increases the rate it pays banks to keep their $1.5 trillion in excess reserves — eight times what is required—parked in accounts at Federal Reserve district banks. Rewarding banks for holding excess reserves in sterile depository accounts at the Fed rather than making loans to the public does not help create business or spur job creation.

Meanwhile, for all the talk of a “rules-based” system for international trade, there are no rules when it comes to ensuring a level monetary playing field. The classical gold standard established an international benchmark for currency values, consistent with free-trade principles. Today’s arrangements permit governments to manipulate their currencies to gain an export advantage.

No wonder advocates of pro-growth economic policies feel compelled to question the vaunted status of central bankers, even as currency speculators track their every utterance. Stable money is a prerequisite for genuine economic growth and shared prosperity. The increasing financialization of gross domestic product is unhealthy because the growing size and profitability of the finance sector come at the expense of the rest of the economy and increase income inequality. When the value of money is fixed, as under a gold standard, economic growth reflects higher levels of productive output.

Fed Gov. Lael Brainard, who was appointed by President Obama, told Bloomberg Television last week that new Trump administration nominees will be expected to put forward “fact-based, intellectually coherent arguments that are based on evidence, that are consistent over time” if they would participate meaningfully in the Fed’s deliberations.

She’s certainly right that the Fed should act based on the best studies and evidence. It could start with the 2011 paper “Reform of the International Monetary and Financial System,” published by the Bank of England, which analyzed the performance of the gold standard (1870-1913) and the Bretton Woods gold-exchange system (1948-72) relative to current monetary practices. The report concludes that today’s system has performed poorly relative to prior monetary regimes, “with the key failure being the system’s inability to maintain financial stability and minimise the incidence of disruptive sudden changes in global capital flows.” Trade and investment flows are distorted as the world’s major central banks engage in subtle exchange-rate competition.

Discussion might be further enriched by the Obama administration’s 2015 Economic Report of the President, which highlights the growth in middle-class incomes during the Bretton Woods system of fixed exchange rates. The report describes the period from 1948 to 1973 as the “Age of Shared Growth.” The period was characterized by accelerating labor productivity, falling income inequality, and increased workforce participation. What if post-1973 productivity growth had continued at its pace from the previous 25 years? The report posits that “incomes would have been 58 percent higher in 2013” and “the median household would have had an additional $30,000 in income.”

The kind of economic growth that increases living standards across all income levels occurs under conditions of monetary and financial stability. Money is meant to serve as a reliable unit of account and store of value across borders and through time. It’s entirely reasonable to ask whether this might be better assured by linking the supply of money and credit to gold or some other reference point as opposed to relying on the judgment of a dozen or so monetary officials meeting eight times a year to set interest rates. A linked system could allow currency convertibility by individuals (as under a gold standard) or foreign central banks (as under Bretton Woods). Either way, it could redress inflationary pressures.

Intellectually fair-minded people should be able to debate the pros and cons of alternative monetary approaches without rancor. What is most important is to avoid monetary mistakes that undermine otherwise positive economic developments. Inflation results when too much money is chasing too few goods. It is not caused by real economic growth, where wages increase to properly compensate people for their higher levels of output achieved through productivity gains.

The Fed’s newfound “patience” in appraising economic and financial developments is welcome—and suitably humble. Central bankers, and their defenders, have proven less than omniscient.

—–

Ms. Shelton, an economist, is author of “Money Meltdown: Restoring Order to the Global Currency System.”

* * *

Help keep GATA going

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

there is no question on this: Judy Shelton, a true gold bug and strong money advocate, is the right nominee for the Fed

(courtesy New York Sun//GATA)

New York Sun: Judy Shelton is the right nominee for the Fed

Submitted by cpowell on Mon, 2019-04-22 21:04. Section: Daily Dispatches

Judy Shelton Is the Right Nominee for the Fed

From the New York Sun

Monday, April 22, 2019

President Trump was understandably reluctant to accept Herman Cain’s request to drop out as a candidate for the Federal Reserve board. He faced the reality of senatorial spinelessness. Four Republicans had indicated they’d shrink from voting for the former chairman of the Kansas City Fed, at least in part over allegations of long-ago sexual improprieties. They didn’t even wait for a hearing.

The good news is that there is an ideal candidate, the economist Judy Shelton. We had no quarrel with Mr. Trump’s choice of either Stephen Moore or Mr. Cain; they both would be fine governors. Mr. Moore still faces a revolt from the economists’ guild, the geshrai from which, John Tamney has argued, underscores the logic of Mr. Moore, who seems to still be in the running. …

…

The kind of thing that makes us think of Ms. Shelton as so particularly ideal is an op-ed the Wall Street Journal issued arguing that currency manipulation is, just as Mr. Trump warned during the campaign, a real problem. She suggested that defenders of our current “global rules-based trading system” should be “wary of thinking their views are more informed than President Trump’s.” …

Ms. Shelton argues that “intellectually fair-minded people should be able to debate the pros and cons of alternative monetary approaches without rancor.” No less a figure than Paul Volcker has argued that “the absence of an official, rules-based, cooperatively managed monetary system has not been a great success.” Now’s the time to elevate to the Fed those like Ms. Shelton with the vision to chart the road to reform.

… For the complete commentary:

https://www.nysun.com/editorials/the-right-nominee-for-the-fed/90659/

* * *

Hi Bill/Harvey

New Developments and War Drums

The announcement by Pompeo yesterday that the USA is now going for the jugular vein of Iran’s economy with an express mission to completely halt Iran’s only export, oil, presumably embodies many objectives, including those of the warmonger Bolton, and certainly what the world needs right now is an Iranian humanitarian catastrophe to compound those already created in Iraq, Syria, Lebanon and Yemen. From the perspective of alleviating reported extreme tightness in the physical gold market, I have tried to unravel the approximate value of Iranian physical gold reserves, which the USA may be hoping will be disgorged as a consequence of very little alternative foreign exchange flowing into Iran. The total of Iran’s foreign exchange reserves is generally reported as about $130 billion but the isolation of the gold component is no easy matter. After considerable searching, the most information that I could unravel is the following extract taken from Wikipedia.

‘’In January 2012, the head of Tehran’s Chamber of Commerce reported that Iran had 907 tons of gold, purchased at an average of $600 per ounce and worth $54 billion at today’s price. The CBI governor however reports only 500 tons (i.e. above ground gold reserves). The discrepancy is unexplained but the 907 tons could (mistakenly) include below-ground gold reserves (320 metric tons as of 2012) and possibly the gold in Iranian private hands (~100 tons in coins or bullion. In 2014, reports from the Central Bank put its gold stores at 90 tons only, the rest possibly used in barter trade following sanctions.’’

Who knows if China and Russia and others will meekly cease trading Iranian oil merely because USA decrees that they mustnot. The total value of turnover of petro yuan futures on the Shanghai Exchange has recently more than halved since a monthly peak of Yuan 4.7 trillion achieved in January 2019. It will be interesting to observe the direction of future volumes in this market .I would hope that Iran will not dump its physical gold at midnight on a Sunday in one fell swoop but we must ,as usual, just wait .I have come to the believe (guided by Jim Willie) that China ,in conjunction with Russia and Iran and scores of other countries would merely be content gradually to consign the USA to oblivion/irrelevance as the old silk trading bloc is revived and gold is once again reintroduced into the terms of settling the trading obligations as generated by about two thirds of the world’s population. Pompeo/Bolton desperately need a new war in an attempt to thwart this planned orderly consignment of the USA to irrelevance and oblivion.

Regards

Nicholas

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7192/

//OFFSHORE YUAN: 6.7221 /shanghai bourse CLOSED DOWN 16.45 or 0.51%

HANG SANG CLOSED DOWN 0.02 points or 0.00%

2. Nikkei closed UP 41.84 POINTS OR 0.19%

3. Europe stocks OPENED MIXED/

USA dollar index RISES TO 97.37/Euro RISES TO 1.1249

3b Japan 10 year bond yield: FALLS TO. –.03/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.89/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 65.92 and Brent: 7423

3f Gold DOWN/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +05%/Italian 10 yr bond yield DOWN to 2.68% /SPAIN 10 YR BOND YIELD UP TO 1.11%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.63: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.32

3k Gold at $1272.45 silver at: 14.96 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 21/100 in roubles/dollar) 63.81

3m oil into the 65 dollar handle for WTI and 71 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.93 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0199 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1423 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.05%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.59% early this morning. Thirty year rate at 3.00%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.8366..DEADLY

Stocks Sputter As Oil Surge Continues

In another quiet overnight session following Monday’s lowest trading volume in nearly a year, stocks have been rangebound, with US equity futures trading in a narrow range (although solid beats by UTX and Coke will likely push stocks higher into the open), while the oil rampage continued, as Brent jumped to near six-month highs on Tuesday after the US tightened sanctions on Iran, sending shares of energy companies higher but failing to help the currencies of the main crude-oil producers.

Confirmation that the US had told buyers of Iranian oil to stop purchases by May 1 or face sanctions pushed Brent toward $75 a barrel, nearly $10 higher in the past month, and up 50% since December, and as Reuters put it, “made for a lively return from the four-day Easter break for Europe’s markets.”

While oil and gas shares jumped nearly 2% for their best start in six weeks, almost every other sector suffered. So did bonds, as higher energy costs hung over profits and nudged up inflation expectations.

Overnight, MSCI’s index of Asia-Pacific shares ended 0.1% higher and Japan’s Nikkei closed up 0.2% as oil and gas gains were offset by losses for airlines and other transport shares facing higher fuel costs. China’s Shanghai Composite slumped in the last hour of trading, closing near session lows amid growing concerns that the PBOC will end its aggressive easing after China reported some impressive economic numbers. Asian volumes were below average ahead of Japan’s Golden Week extended holiday which will see Japanese markets closed for nearly 2 weeks.

China’s blue-chip stocks have surged over 30% so far this year on expectations of more stimulus and hopes Beijing and Washington will reach an agreement to end their nine-month trade dispute.

“We’ve had a fantastic run in Chinese equities year-to-date. Some profit taking is completely normal. I don’t think China is changing its policy that quickly,” said Stefan Hofer, chief investment strategist at LGT Bank Asia in Hong Kong.

Following a muted Asian session, European stocks slipped as many markets reopened after a long weekend and as the earnings season ramps up. Banks led a drop across many sectors for the Stoxx Europe 600 Index, though energy companies outperformed thanks to the bounce in oil.

With little of note in equity markets, traders remained focused on oil prices which are up nearly 50 percent since late December, and before the re-imposition of sanctions last year Iran was the fourth-largest producer among the OPEC at around 3 million barrels per day. Oil prices are “not so high that it crushes manufacturing by putting energy-price inputs up, but it is producing a nice boost to oil-producing nations,” said ING economist Robert Carnell, although a few more dollars of oil upside and oil prices may get “too high.”

Elsewhere, Sri Lankan stocks slumped and bonds fell for a second day after terror attacks on Easter Sunday killed more than 300 people.

In rates, Treasuries were steady with yields marginally lower and within a basis point of Monday’s close; as Bloomberg notes, upside was capped as bunds lag on light cash volumes. Focus is on supply as Treasury auction cycle begins with $40b 2-year note sale, followed by $41b 5-year Wednesday and $32b 7-year Thursday. The 10-year TSY yielded around 2.583%, richer by half basis point; German 10s cheaper by 3bp vs. Treasuries with the spread hovering around 254bp

In FX, volatility was still largely absent. The dollar held near a three-week high, but the usual beneficiaries of higher oil prices, the Canadian dollar and Norwegian crown, dipped to $1.33 and $8.52 respectively; ironically the biggest losers from higher oil prices – India and Turkey – did not see their currencies dip materially either.

“Oil is interesting, but the interesting thing for FX is that we are not getting the usual feed-through in the petrocurrencies,” said Saxo bank’s head of FX strategy, John Hardy, adding that might be caused by questions about Chinese stimulus. Both the Canadian dollar and the crown had gained on Monday, and the Russian rouble, another petrocurrency, hit its highest against the euro in more than a year its highest against the dollar in a month.

Emerging-market currencies and shares were mostly steady. The pound advanced against major peers as Prime Minister Theresa May foughtto keep her job.

Investor attention remains focused on earnings season which is about to see an avalanche of Q1 filings as one third of the S&P is set to report: “Some of the world’s biggest technology companies are reporting earnings this week as well as a raft of the big European banks,” Rakuten’s Nick Twidale said in a note to clients Tuesday. “Investors will be hoping for some better-than-expected results from both groups to keep the topside momentum in global equities. If the data starts to show a significant slowing across these key industries then expect both stocks and risk trades to start to come under some heavy pressure.”

Expected data include new home sales. Coca-Cola, Harley-Davidson, Lockheed Martin, P&G, Twitter, Verizon, and Snap are among companies reporting earnings.

Market Snapshot

- S&P 500 futures little changed at 2,911.00

- STOXX Europe 600 down 0.2% to 389.76

- MXAP up 0.2% to 163.06

- MXAPJ up 0.1% to 542.39

- Nikkei up 0.2% to 22,259.74

- Topix up 0.3% to 1,622.97

- Hang Seng Index unchanged at 29,963.24

- Shanghai Composite down 0.5% to 3,198.59

- Sensex up 0.3% to 38,773.63

- Australia S&P/ASX 200 up 1% to 6,319.42

- Kospi up 0.2% to 2,220.51

- German 10Y yield rose 2.3 bps to 0.048%

- Euro down 0.05% to $1.1251

- Italian 10Y yield fell 1.0 bps to 2.231%

- Spanish 10Y yield rose 2.2 bps to 1.093%

- Brent futures up 0.5% to $74.42/bbl

- Gold spot down 0.1% to $1,273.76

- U.S. Dollar Index little changed at 97.32

Top Overnight News

- Oil extended gains after leaping to a six-month high on Monday after U.S. Secretary of State Mike Pompeo said any nation that continues to buy Iranian oil will face American sanctions. Futures in London added as much as 0.8 percent Tuesday.

- U.K. Prime Minister Theresa May is fighting to keep her job so she can complete her task of taking Britain out of the European Union — but her hopes of success now rest with her arch rival and opposition leader Jeremy Corbyn

- Benoit Coeure, the European Central Bank Executive Board member in charge of markets, said he doesn’t see any reason to dilute the effect of negative interest rates on banks and signaled a new long-term loan series may be less generous than the previous round

- China’s securities watchdog moved to curb cut-throat pricing competition among local debt arrangers looking to gain a bigger share in the world’s third-largest bond market

- The new indictment accusing Carlos Ghosn of redirecting $5 million from Nissan Motor Co. to his personal accounts not only may extend his time in detention, it also threatens to undermine his argument that he’s a victim of corporate intrigue

Asian equity markets traded mixed as sentiment somewhat deteriorated from the mostly positive close in the US, where the energy sector surged after the US decided to end Iranian oil sanction waivers but with gains in the broader market capped ahead of this week’s heavy slate of earnings. ASX 200 (+0.9%) was led higher by the energy sector after crude prices rallied around 3% to 6-month highs and NZX 50 (+0.5%) topped the 10K level for the first time ever, while Nikkei 225 (+0.2%) barely held on to early gains and stumbled from the weight of a firmer currency. Hang Seng (U/C) and Shanghai Comp. (-0.5%) were subdued after PBoC inaction resulted to a net liquidity drain of CNY 40bln which pushed the Overnight SHIBOR higher by over 27bps and with Hong Kong tentative amid resistance ahead of the 30K level and as its reflected on the recent mainland underperformance on return from its 4-day closure. Finally, 10yr JGBs were relatively flat after having recovered from earlier weakness as risk sentiment in Tokyo soured, while weaker results at today’s 2yr JGB auction also ensured price action was drab.

Top Asian News

- Maeda Says BOJ Will Consider Further Easing If Momentum Slows

- Singapore’s Pre-Election Cabinet Change Sets Heng Up for Top Job

- Fosun Could Only Buy Thomas Cook’s Tour Business: Citi

- Cash-Flow King for Templeton Seeing More Riches in China Stocks

Major European Indices are slightly subdued [Euro Stoxx 50 -0.2%], after being essentially unchanged for much of the session, with stocks largely following on from the indecisive sentiment seen overnight in Asia as participants return from the Easter weekend. Sectors are similarly mixed, although the significant outperformance in energy names continues following on from the lifting of Iranian waivers; as such Shell (+2.0%) are firmly in the green with the Co. also aided by the agreement to sell their 50% stake in SAREF to Saudi Aramco for USD 631mln. Due to the strong performance in Shell, alongside the Co. representing 11.3% of the FTSE 100 due to it having two listings in the form of A and B shares, the FTSE 100 (+0.4%) is outperforming its peers. Other notable movers this morning include Umicore (-15.4%) who are underperforming the Stoxx 600 following the Co. warning that 2020 revenue and earnings growth will be below expectations. Separately, Wirecard (-2.9%) are down after the expiration of BaFin’s short selling ban on Friday April 19th. Elsewhere, Thomas Cook (+16.3%) are soaring after reports that the Co. has received approaches for sections/entirety of the Co., with names such as Forsum International, KKR and EQT citied as potential bidders.

Top European News

- BlueMountain’s Europe CEO Church Is Said to Be Joining Och- Ziff

- Partners Group Buys Norwegian Gas Pipeline Owner CapeOmega

- Thomas Cook Up Most in 4 Months on Report of Buyout Interest

- Ahold Falls as Stop & Shop Strikes Will Cut Grocer’s Earnings

In FX, the dollar index remains firm and comfortably above the 97.000 handle within a 97.281-402 range amidst Greenback gains vs most major counterparts and EM rivals as the latest rally in oil prices continues to undermine crude importers and risk sentiment more broadly to the detriment of high beta currencies. However, the DXY still needs to overcome early April highs at 95.517 to expose ytd peaks posted in the previous month and virtually matching late 2018 levels just above 97.700.

- CHF/AUD/NZD/NOK/SEK – The G10 laggards and largest losers against the buoyant Buck, as the Franc extends its decline further towards 1.0200 and through 1.1450 vs a relatively resilient Euro, while the Aussie and Kiwi hover closer to the bottom of 0.7140-10 and 0.6685-57 ranges vs their US peer on more dovish RBA and RBNZ policy leanings compared to the Fed. On that note, the Aud will be eyeing Q1 inflation data overnight amidst the consensus for a slowdown in q/q and y/y CPI rates with caution given latest RBA minutes revealing discussions about the conditions that may warrant a lower OCR including weaker price developments along with any deterioration in the labour market. Elsewhere, even the Nok is underperforming alongside the Sek as the Scandi Crowns fall victim to overall aversion rather than gleaning more support from the aforementioned advance in oil, as the former retreats to circa 9.5900 and latter to around 10.5000 vs the Eur.

- GBP/JPY/EUR/CAD – All narrowly mixed vs the Usd, as Cable recovers from pre-Easter lows to retest the 1.3000 level after holding above the 200 DMA (1.2966) and shrugging off heightened pressure on UK PM May as Parliament returns from its recess. Meanwhile, Usd/Jpy remains capped just ahead of 112.00 within a 111.97-66 range and decent option expiry interest between 111.50-65 and 111.90-112.00 (1.1 bn either side). Note also, reported Japanese import and investor bids above 111.50 and the 200 DMA (111.51) may be curtailing a more concerted pull-back. Expiries could be impacting Eur/Usd as well given 2.3 bn rolling off from 1.1250 to 1.1260, while the Loonie is pivoting 1.3350 in the run up to Wednesday’s BoC policy meeting and press conference from Poloz and Wilkins – full preview of the event available on the Research Suite (along with a BoJ primer for Thursday).

- EM – Most regional currencies are on the back foot vs the Dollar, as noted above, but the Rand is also factoring in renewed concerns about SA’s Eskom in wake of reports that the Government had to bail out the company to the tune of Zar 5bn to avert non-payment and a call on state guarantees – Usd/Zar currently at 14.1900+ vs sub-14.1500 at one stage.

In commodities, Brent (+0.6%) and WTI (+0.8%) prices are in the green, as the oil complex extends on yesterdays gains following the US announcing that they are not going to extend waivers for Iranian oil, which expire on May 2nd. For reference, Iranian exports averaged 1.3mln BPD in March as such if the US are successful in their goal of reducing Iran’s exports to zero then this would result in a significant supply reduction; although, some analysts believe that the complete elimination of exports is unlikely. RBC state that they believe around 700-800K BPD to be removed from the market in the short term as a result of the waiver elimination. Saudi Energy Minister Al Falih stated that Saudi Arabia will cooperate with other oil suppliers in order to ensure that there is sufficient supply and that the market will not go out of balance. In light of the US’ announcement to not extend waivers Barclays sees upside risks of at a minimum USD 5/bbl for the USD 70/bbl Brent 2019 forecast if their exports drop to zero; however, Goldman Sachs state that the price impact will be limited and reiterates their 2019 Brent range of USD 70-75/bbl. Looking ahead, we have the API weekly crude release where the expectations are for crude stocks to build by around 0.5mln barrels. Gold (-0.1%) is largely unchanged and trading within a narrow USD 4/oz range, largely in line with major stock indices and the generally indecisive risk tone as markets return from the extended Easter weekend. Elsewhere, the majority of steel mills in China’s Tangshan, Hebei province have been asked to cut around 40% of their sintering capacity due to the expected increase in pollution levels over the coming week.

Looking at the day ahead, we get housing data in the form of the FHFA house price index reading for February and March new home sales. We’ve also got the April Richmond Fed manufacturing index print due out. Away from that we’re due to hear comments from Larry Kudlow in Washington while the earnings highlights are Proctor & Gamble, Verizon, Coca-Cola, eBay and United Technologies.

US Event Calendar

- 9am: FHFA House Price Index MoM, est. 0.5%, prior 0.6%

- 10am: Richmond Fed Manufact. Index, est. 10, prior 10

- 10am: New Home Sales, est. 649,000, prior 667,000; MoM, est. -2.7%, prior 4.9%

DB’s Craig Nicol concludes the overnight wrap

Hope you all enjoyed the long weekend. Here in the UK, we even managed to dust off the barbecues such was the unseasonably hot weather. Mind you Jim probably didn’t feel quite so thrilled with it given that he’s in box moving and unpacking mode right now. The good news for him is that the temperature is expected to drop over the rest of this week while for markets there’s probably just enough in the week ahead to keep us distracted.

Indeed, in all likelihood earnings will probably dictate the direction of travel for now especially with a number of tech heavyweights due to report including eBay, Amazon, Facebook, Twitter and Microsoft.Last week saw the NASDAQ 100 hit a fresh all-time high with the broader NASDAQ one decent session away from its own record high, so this week should be a reasonable test as to whether or not we can hold those levels. More broadly, in total we’ve got 148 more S&P 500 companies reporting this week and the stats after 86 companies having reported so far is 67 beating on earnings, which is above the five-year average, but just 41 on revenues, which is below the five-year average. Not to be left out, it’s worth noting that this week will also see a number of European Banks report their latest quarterlies.

Outside of that we’ve also got a few high-profile meetings between politicians over the next few days.Markets will likely be most fixated by Trump’s meeting with Abe at the White House from Friday with trade talks likely to be high up on the agenda list. Before that, Abe is due to meet Tusk and Juncker on Thursday while also on the cards this week is a possible meeting between Putin and Kim Jong Un tomorrow. Oh, and UK politicians return from their Easter recess today. So that only means one thing for the prospect of Brexit headlines. The last 10 days was fun while it lasted.

Also worth flagging this week is the BoJ meeting on Thursday where no change in policy is expected, however the meeting does include the BoJ’s latest quarterly report. Finally, it’s fairly quiet for data releases however the Q1 advance GDP reading for the US is by some distance the highlight. In terms of what to expect, at the expense of Q2 growth and the recent strong retail sales data, our US economists recently revised up their forecast to 2.6% for Q1 which is ahead of the market consensus for 2.2%. That data is due out on Friday.

Ahead of all that Wall Street was open for business yesterday however it wasn’t a particularly exciting session with the S&P 500 and NASDAQ advancing +0.10% and +0.22% respectively, while the DOW retreated -0.18%. With volumes also 25% below average, the range on the S&P 500 was in fact just 0.45%. That makes 14 straight sessions with no intraday ranges of +/-1%, the longest streak since October.

The good news is that there was one big mover and shaker yesterday and that was oil where WTI rose +2.31% to a fresh 6-month high of $65.55/bbl. The catalyst was the surprise move by the US to end their waivers on Iran sanctions.These waivers had allowed eight countries to continue importing oil from Iran despite the Trump administration’s withdrawal from the nuclear accord last year, and their termination will likely result in further reductions to Iran’s exports. The US said that other countries would compensate for the fall in Iranian supply to leave the global market balanced. However, the risk of disruptions injected a risk premium into oil markets. In an immediate response, an Iranian military official said that they would close the Strait of Hormuz in retaliation if the US completely blocks their exports. The 5y Treasury breakeven was +1.5bps higher off the back of that move while 10y Treasuries more broadly speaking were +2.9bps higher. The energy sector also led gains for the S&P, closing up +2.05%, while HY energy spreads were -3bps tighter, in contrast to a moderate widening for the broader HY index. The currencies that gained the most included oil-exporters like the Russian Ruble (+0.40%) and Canadian Dollar (+0.33%), while oil importing EMs were hit negatively, with the Indian rupee (-0.46%) and South Korean won pacing losses (-0.41%).

This morning in Asia it’s been just as muted for equity markets with the Nikkei (-0.06%), Hang Seng (-0.08%), CSI 300 (-0.03%) and Kospi (+0.06%) all struggling for direction in thin trading conditions once again. Oil has held onto the gains from yesterday while US equity futures are flat.

As for other news yesterday, the data calendar was light with only a few releases in the US. The Chicago Fed’s National Activity Index rose to -0.15 from -0.31, though lower than the expected -0.10. A negative reading points to lower-than-average growth, not necessarily economic contraction. Existing home sales fell more than expected, at 5.21 million versus consensus expectations for 5.30 million, a -4.9% mom drop. That’s the sharpest monthly percentage drop since 2015 and the second sharpest since 2011. US homebuilder stocks fell -1.39% in response.

Elsewhere, President Trump announced via twitter that he will not proceed with nominating Herman Cain to the Federal Reserve Board.That came as media outlets reported fresh scrutiny of his other pick, Stephen Moore. His nomination is still reportedly on track though not officially submitted.

Finally, in terms of the day ahead, the only data release due out in Europe is the April consumer confidence reading for the Euro Area this afternoon. In the US we’ve got more housing data in the form of the FHFA house price index reading for February and March new home sales. We’ve also got the April Richmond Fed manufacturing index print due out. Away from that we’re due to hear comments from Larry Kudlow in Washington while the earnings highlights are Proctor & Gamble, Verizon, Coca-Cola, eBay and United Technologies.

end

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 16.45 POINTS OR 0.51% //Hang Sang CLOSED DOWN 0.02 POINTS OR 0.00% /The Nikkei closed UP 41.84 POINTS OR 0.19%/ Australia’s all ordinaires CLOSED UP .96%

/Chinese yuan (ONSHORE) closed DOWN at 6.7192 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 65.92 dollars per barrel for WTI and 74.23 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.7192 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7221 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

China/

4/EUROPEAN AFFAIRS

EU/USA

Fasten your seat belt: there is going to be a huge transatlantic trade war beginning in May and agriculture will be at the centre. The EU just does not let any agriculture into their sphere

(courtesy Mish Shedlock/Mishtalk)

Seeds Sewn For Major Transatlantic Trade War Starting In May

Authored by Mike Shedlock via MishTalk,

Trump wants a trade treaty with the EU to include agriculture. France says no. It only takes one.

Trump has made a considerable number of trade threats only to eventually back down. Will it play out that way again?

For a number of reasons, I think Trump will act this time. First, let’s look at the threats.

Severe Pain

On February 25, Trump told the EU Play Ball or ‘We’re Going to Tariff the Hell Out of You’

“The European Union is very, very tough. Very, very tough. They don’t allow our products in. They don’t allow our farming goods in,” Trump said at a meeting with U.S. governors, according to a transcript from the White House. He added that “maybe, in certain ways,” the EU is “tougher than China.”

On March 14, Trump Warned EU of ‘Severe’ Economic Pain if No Progress On Trade Talks.

Partial Agreement Won’t Fly

On April 15, Reuters reported EU Ready to Launch U.S. Trade Talks, but Without Agriculture.

The EU approved two areas for negotiation, opposed by France with an abstention from Belgium. But agriculture was not included, leaving the 28-country bloc at odds with Washington, which has insisted on including farm products in the talks.

EU trade agreement are unanimous. Tiny countries can and have influenced outcomes. It took over a decade to get an agreement with Canada over concerns of tiny nations.

Even if US-EU trade talks take place, nothing will come of them and Trump will quickly get frustrated.

Climate Change Now in the Picture

On April 18, France has signaled it will not cooperate with Trump in any way.

Please consider the new French demand: No EU-US Trade Talks Unless Trump Supports Climate Deal.

Earlier this week, the European Union agreed to start trade talks with the United States on industrial goods. France, however, has objected to the decision while Belgium abstained. In Paris, the concern is that there cannot be any agreement over trade while the U.S. refuses to commit to key environmental targets.

“France is opposed to the initiation of any trade negotiations with countries outside the Paris climate agreement,” a French official said Monday, explaining why the second largest euro country said no to trade negotiations with Washington.

“It is a question of values. Europe must be exemplary and firm in its defense of the climate,” the same official said.

Uri Dadush, a Washington-based scholar for the think tank Bruegel, told CNBC: “I believe France and others less prominently visible than France and which are net beneficiaries of the Common Agricultural Policy (Italy, Spain, for example) will veto discussion of agriculture trade reforms.”

“This will make it even tougher for the U.S. to accept a deal, and I suspect that President Trump was not adequately briefed or ignored his brief when he agreed with (European Commission) President Juncker to omit agriculture,” he added.

Trade Talks Going Nowhere

Even without the absurd demand on climate change, trade talks with the EU are going nowhere.

Not Just Trump Holding Up Talks

One difference this time is that it isn’t just Trump threatening the EU.

Via Eurointelligence:

It would be rather silly to report the EU Council’s decision to open limited trade talks with the US without noting the immediate cool response on the other side of the Atlantic. The first reaction did not come from Donald Trump – who was busy giving technical advice to French firefighters – but from Chuck Grassley, the chair of the US Senate’s finance committee. He immediately dismissed the decision by the EU Council to open up trade negotiations with the US, making it clear that no deal would pass the Senate without including agriculture.

Trade policy with Europe is not a matter where Congress and the White House are divided. It is our understanding that Trump’s closest advisers are all expecting the president to slap tariffs on European auto imports.

The French opposition, together with that expressed earlier by the European Parliament, does bot bode well for future EU adoption of even a limited trade deal with the US. The trade talks need only a qualified majority to be launched, but unanimity of member states and a majority in the EP to be ratified.

We have been observing a definite hardening of French positions in a variety of issues, including trade and the Brexit extension. Last week France blocked an EU statement on Libya. It will be interesting to see whether Emmanuel Macron’s readiness to assert himself more strongly will survive the European elections.

Grassley

Chuck Grassley, head of the Senate Finance Committee is from Iowa, an huge farm-belt state. Grassley will insist agriculture be part of any trade deal.

Trump will listen to Grassley and the trade hawks.

Chlorinated Chicken

Major Transatlantic Trade War Coming Up

Trump’s position is somewhat logical (if you foolishly believe tariffs are an answer).

The EU runs a massive trade surplus with the US in industrial goods. Eliminating tariffs on industrial goods would likely increase that surplus.

There is one tried and true way to get Trump to back down: Give in on some minor point then agree to buy more soybeans.

However, the EU is not going to buy more soybeans, GMO products in general, or chlorinated chicken.

Instead, Macron taunted Trump with a huge red flag issue regarding climate change.

Trade War in May

The Commerce Department presented a report on auto imports in mid-January. Supposedly, auto imports are a threat to US national security. That’s absurd, but it allows “tariff man” to do whatever he wants.

The deadline for Trump to make a decision on EU tariffs is mid-May.

Trump is set to sign a trade deal with China in late May or early June. Expect Trump to finalize a meaningless deal with China, then start a major trade war with the EU.

end

Theresa May is now ready to bring back the Brexit legislation for the 4th time

(courtesy zerohedge)

May Ready To Bring Back Hated Brexit Plan For Unprecedented 4th Vote

Though the pound’s weakness against the dollar in the euro on Tuesday has been widely interpreted as a knock-on effect of the dollar’s strength, traders could be forgiven for assuming otherwise. Because after a brief Easter recess, Parliament is back in session, and Brexit-related news is back in the headlines.

Little has happened since Theresa May struck an 11th-hour agreement with the EU for a six-month extension of Article 50. Talks with Labour to find an alternative to May’s Brexit deal (talks that May clearly disdains) appear unlikely to succeed. Though the Tory and Labour delegations resumed talks on Tuesday, whispers suggest the talks could fall apart in the coming days.

Whatever happens with the talks is largely irrelevant anyway, since the EU has made it clear that the withdrawal agreement is the only deal that it would accept. That deal has already been rejected three times by Parliament, albeit by slightly more favorable margins in each successive vote, though as long as the Irish Backstop, the big sticking point in the deal, remains, it’s unlikely that May will be able to win over enough Brexiteers to push the deal through.

With few viable alternatives (apart from another can kick or, failing that, a second referendum), the Financial Times reported on Tuesday, surprising absolutely no one, that May is already preparing to bring the text of her withdrawal agreement back for a fourth vote.

Just like the third vote, May will need to embrace some procedural maneuvers to satisfy Speaker Bercow’s condition that the deal must be “substantially different” than prior votes if May wants to bring it back. This time, the withdrawal agreement will come packaged in a more far-reaching withdrawal agreement bill.

And a vote could come as soon as next week.

Downing Street sources said a fourth vote on May’s bill could be the last and best hope to avert Britain’s participation in the upcoming EU Parliamentary elections, something May had desperately sought to avoid.

If the bill is defeated, which is extremely likely, May would be prohibited from bringing it back for another vote until a new session of parliament begins. That wouldn’t happen until later this year, though we imagine May will find some kind of procedural loophole to keep bringing her deal back.

Even if it does manage to pass the Commons, it would still need to pass a few procedural hurdles before Brexit could be officially delivered.

The treaty the bill is intended to implement includes provisions such as the UK’s £39bn exit payment to the EU, protection of citizens’ rights, a transition period and the so-called backstop to avoid a hard border on the island of Ireland. If the legislation is rejected, as currently seems likely, the government could not reintroduce it again in this session of parliament.

“It would be quite a big thing,” admitted one ally of Mrs May. In those circumstances the bill could only be brought back if the current parliamentary session was ended.

Approval for the legislation would kick off a tortuous passage through parliament during which the bill could be amended. Attempts to add a customs union or a second referendum would be expected. Even if the bill did eventually become law, Downing Street said there would still have to be a separate “meaningful vote” on Mrs May’s deal under the terms of 2018 Brexit legislation. However, that would be expected to be a formality if MPs have already approved the bill to put the draft treaty into effect.

But whatever happens with the deal, it may soon become somebody else’s problem. That’s because, as the Telegraphreported, Graham Brady, the leader of the 1922 Committee of Tory backbenchers, is planning to confront May on Tuesday and demand that she either set a date for her departure, or Tories will change the leadership rules to allow her to be ousted (after surviving a no confidence vote late last year, May is immune from further challenges for a year under the current rules).

Other Tories, including Nigel Evans, another leading backbencher, have called on May to resign immediately. Though previous intra-party efforts to oust May have fizzled in the not-too-distant past, we seriously wonder how long the Tories can keep up with these threats to oust May before finding a way to actually get the job done. Brady will meet with the 1922 Committee later on Tuesday to vote on a possible rules change.

Either way, the Brexit impasse appears no closer to resolution. Which means a second referendum cannot yet be ruled out.

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

ISIS/SRI LANKA

Isis states that they are the ones behind the bombings in Sri Lanka and it was in retaliation for the New Zealand mosque massacre

(courtesy zerohedge)

ISIS Says Behind Sri Lanka Bombings; Was ‘Retaliation’ For New Zealand Mosque Massacre