GOLD: $1277.45 UP $6.00 (COMEX TO COMEX CLOSING)

Silver: $14.97 UP 15 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1275.50

silver: $14.94

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 123/225

EXCHANGE: COMEX

CONTRACT: APRIL 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,269.300000000 USD

INTENT DATE: 04/23/2019 DELIVERY DATE: 04/25/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 12

661 C JP MORGAN 123

737 C ADVANTAGE 25 85

880 H CITIGROUP 200

905 C ADM 5

____________________________________________________________________________________________

TOTAL: 225 225

MONTH TO DATE: 6,607

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 225 NOTICE(S) FOR 22500 OZ (0.6998 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 6607 NOTICES FOR 660700 OZ (20.550 TONNES)

SILVER

FOR APRIL

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 775 for 3,875,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE :$5384 DOWN $102

Bitcoin: FINAL EVENING TRADE: $5502 DOWN 90

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE A GOOD SIZED 1255 CONTRACTS FROM 217,858 UP TO 219,113 DESPITE YESTERDAY’S 21 CENT FALL IN SILVER PRICING AT THE COMEX AS WE DID NOT HAVE OUR CUSTOMARY LIQUIDATION OF SPREADERS TODAY BUT IT SHOULD RESUME SHORTLY. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 1936 FOR MAY, 0 FOR JUNE 200 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 2136 CONTRACTS. WITH THE TRANSFER OF 2136 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2136 EFP CONTRACTS TRANSLATES INTO 10.68 MILLION OZ ACCOMPANYING:

1.THE 21 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

AND NOW 3.880 MILLION OZ STANDING FOR SILVER IN APRIL.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

30,590 CONTRACTS (FOR 17 TRADING DAYS TOTAL 30,590 CONTRACTS) OR 152.95 MILLION OZ: (AVERAGE PER DAY: 1799 CONTRACTS OR 8.997 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 152.95 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 21.85% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 720.75 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1255 DESPITE THE 21 CENT FALL IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 2136 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS HAVE NOT YET STARTED THEIR LIQUIDATION OF THE SPREAD TRADES.

TODAY WE GAINED A CONSIDERABLE SIZED: 3391 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2136 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1255 OI COMEX CONTRACTS. AND ALL OF THIS STRONG DEMAND HAPPENED WITH A 21 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.82 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.095 BILLION OZ TO BE EXACT or 157% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR nil OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ AND NOW APRIL AT 3.880 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 1519 CONTRACTS, TO 440,048 DESPITE THE FALL IN THE COMEX GOLD PRICE/(A DROP IN PRICE OF $4.40//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6845 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 6845 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 440,048. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8364 CONTRACTS: 1519 OI CONTRACTS INCREASED AT THE COMEX AND 6845 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 8364 CONTRACTS OR 836,400 OZ OR 26.01 TONNES. YESTERDAY WE HAD A LOSS IN THE PRICE OF GOLD TO THE TUNE OF $4.40.…AND YET WITH THAT FALL, WE STILL HAD A VERY STRONG GAIN IN TONNAGE OF 28.84 TONNES!!!!!!.??????????????????????????????????????????

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 117,682 CONTRACTS OR 11,768,200 OR 366.04 TONNES (17 TRADING DAYS AND THUS AVERAGING: 6922 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAYS IN TONNES: 366.04 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 366.04/3550 x 100% TONNES =10.31% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1739.43 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIR SIZED INCREASE IN OI AT THE COMEX OF 1519 DESPITE THE LOSS IN PRICING ($4.40) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6845 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6845 EFP CONTRACTS ISSUED, WE HAD A VERY STRONG GAIN OF 8364 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6845 CONTRACTS MOVE TO LONDON AND 1519 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 26.01 TONNES). ..AND THIS STRONG DEMAND OCCURRED WITH A FALL IN PRICE OF $4.40 IN YESTERDAY’S TRADING AT THE COMEX.

we had: 225 notice(s) filed upon for 22,500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $6.00 TODAY

TWO BIG TRANSACTIONS AT THE GLD.

mid afternoon:

i)A WITHDRAWAL OF 2.05 TONNES

late afternoon:

ii)a withdrawal of 1.76 tonnes

INVENTORY RESTS AT 747.87 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 15 CENTS TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLSV//

/INVENTORY RESTS AT 311.979 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A STRONG SIZED 1255 CONTRACTS from 217,858 UPTO 219,113 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..TODAY,IT LOOKS LIKE OUR SPREADERS TOOK THE DAY OFF AS IT SEEMS THAT NEW CONTRACTS WERE PROVIDED ON THE SHORT SIDE TO CAUSE THE CASCADING PRICE WITH RESPECT TO THE RAID YESTERDAY,

HERE IS HOW THE CROOKS USED SPREADING AS WE ENTER AN ACTIVE DELIVERY MONTH. THUS SILVER HAS THE ACTIVE MONTH OF MAY COMING UP AND THUS SPREADERS DO THE FOLLOWING:

“YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF APRIL BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 1936 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 200 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2136 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1255 CONTRACTS TO THE 2136 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A VERY STRONG SIZED GAIN OF 3391 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 16.96MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH. AND NOW 3.880 MILLION OZ FOR APRIL.

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 21 CENT FALL IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 2136 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 3.02 POINTS OR 0.09% //Hang Sang CLOSED DOWN 157.41 POINTS OR 0.53% /The Nikkei closed DOWN 59.74 POINTS OR 0.27%/ Australia’s all ordinaires CLOSED UP .93%

/Chinese yuan (ONSHORE) closed DOWN at 6.7182 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 65.92 dollars per barrel for WTI and 74.23 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.7182 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7238 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA

b) REPORT ON JAPAN

Japan

3 China/Chinese affairs

i)China/

China is running out of dollars as they try and fund their silk road project. However unlike Turkey they are still safe for now

(courtesy zerohedge)

4/EUROPEAN AFFAIRS

i)DEUTSCHE BANK/

Deutsche bank has no bank willing to take on the no 1 derivative player in the world. It is now again talking about a bad bank /good bank scenario as they wall off units that they want to close. The problem that they have is of course their huge losing derivative balloon

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

i)Canada

Looks like Canada is in a little trouble as Poloz states that growth in the first quarter was an anemic .3% and he projects growth for all of 2019 ( a stretch) at 1.2%. Down goes the Cdn dollar to 1.35 and bond yields plummet.

(zerohedge)

ii)Global FX crosses

Michael Every gives us a good look at ripple effects on our major currency crosses

i.e. the Euro, the pound, and the Turkish lira

a must read…

(courtesy Michael Every/Rabobank)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

Argentina

wow!! the Argentinian peso falters to almost 44 to the dollar. Traders are freaking out that we witness another default

(courtesy zerohedge)

9. PHYSICAL MARKETS

i)Kranzler states the obvious: yesterday’s raid was shear manipulation coupled with fake financial journalism which covers this crime

( Dave kranzler/IRD)

ii)I brought this story to you yesterday but it is worth repeating..the survey fails to address market manipulation

( Ted Butler/GATA)

iii)The best mining company in the world: Agnico Eagle

( Reuters)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning/TRADING

Treasury yields tumble and so does the German bund and other countries sovereign bond yields.

(zerohedge)

ii)Market data

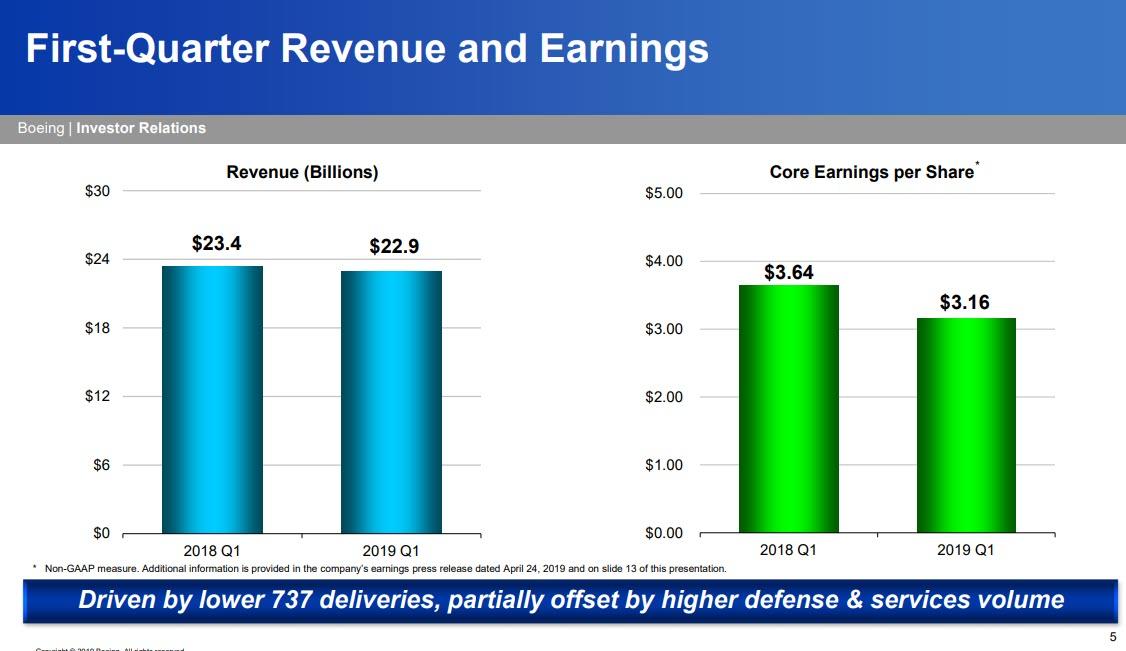

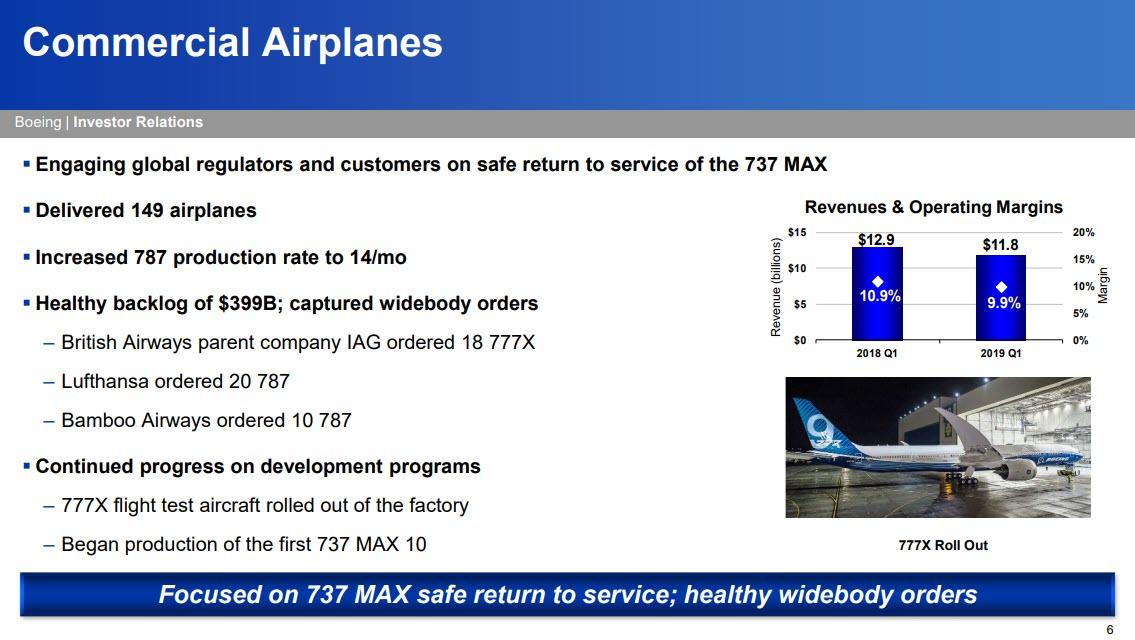

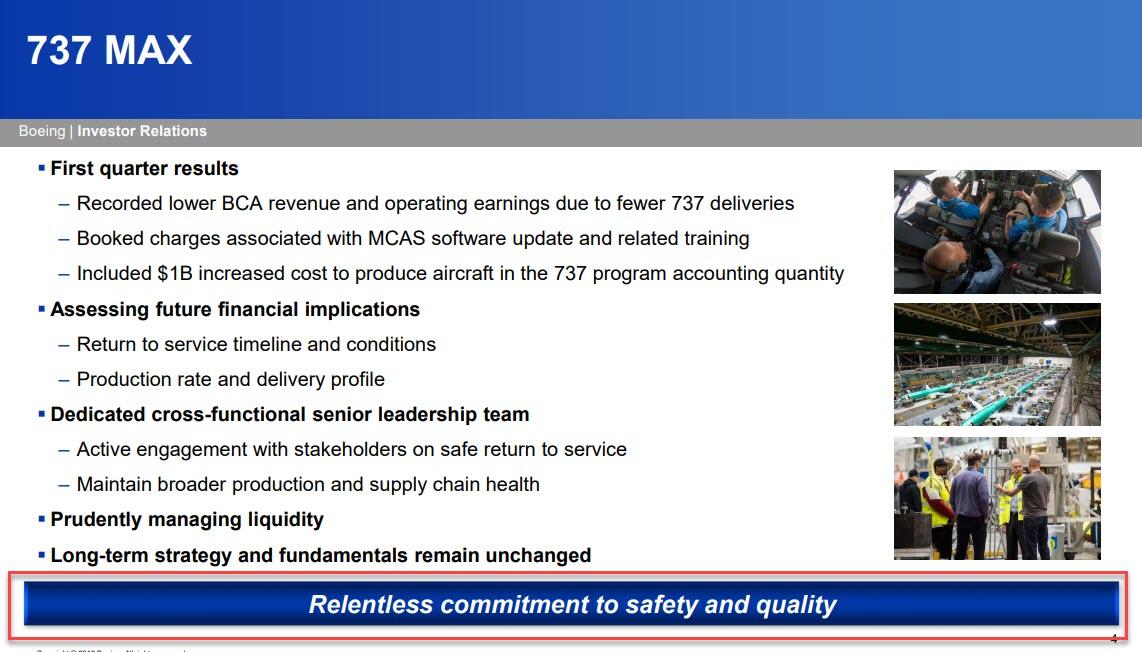

a)Earnings are down for Boeing but for the first time they suspend guidance and buybacks

( zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

( zerohedge)

b)Oh OH!!!~ this ought to be good. Our perennial crooks will not escape this one: the Dept of Justice demands a guilty plea on the iMDB case.

(courtesy zero hedge)

SWAMP STORIES

a)For those of you who want a true definition of the Hebrew then Yiddish term “chutzpah”…this is it. Hillary outlines a roadmap for Trump impeachment as she sights Trump engaged in clear obstruction, knowing full well that she was the queen of obstruction

( zerohedge)

good reading….

( zerohedge)

c)Trump warns our angry democrats that he will take the impeachment threats straight to the Supreme Court…that will be a first.

( zerohedge)

d)Cohen is a basket case; now in a phone call he admits to more lies and he is claiming he is not actually guilty of any crimes that he plead guilty to.He did not want to get his wife messed up in his crap.

Let us head over to the comex:

AFTER APRIL, WE HAVE THE ACTIVE DELIVERY MONTH OF MAY AND HERE THE OI FELL BY 9173 CONTRACTS DOWN TO 59,877. CONTRACTS.. THE NEXT MONTH OF JUNE GAINED 64 CONTRACTS TO 331. AFTER JUNE, THE VERY BIG DELIVERY MONTH OF JULY HAD A GAIN OF 8369 CONTRACTS UP TO 117,206 CONTRACTS.

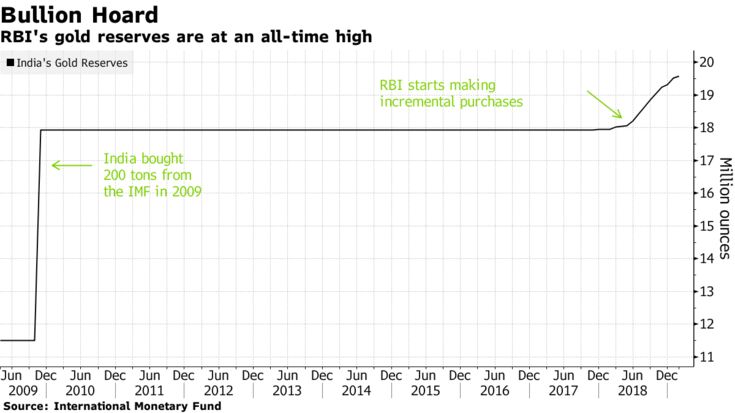

World’s Central Banks Want More Gold – India May Buy 1.5M Ounces In 2019

- Royal Bank of India (RBI) may buy another 1.5 million oz this year according to OCBC

- Many other central banks including large creditor nations Russia and China are also adding to gold holdings

India’s central bank is likely to join counterparts in Russia and China scooping up gold this year, adding to its record holdings and lending support to worldwide gold bullion demand as top economies diversify their reserves.

The Reserve Bank of India’s purchases are part of a wider picture across developing economies that are looking at de-dollarizing their foreign-exchange reserves, according to Ross Strachan at Capital Economics Ltd. The RBI’s buying trend can be sustained for a number of years in relatively small quantities, as part of a long-term diversification, he said.

The RBI may purchase 1.5 million ounces in 2019, or about 46.7 tons, according to Howie Lee, an economist at Oversea-Chinese Banking Corp., with an outlook based on extrapolating amounts bought in the first two months of this year.

The RBI increased its stash by about 42 tons last year, and after adding more in January and February, the country’s gold reserves now stand at a record high of almost 609 tons, according to data from the International Monetary Fund. Russia bought 274 tons in 2018 and has added more this year, while China’s central bank is on a renewed buying spree that began in December. Global official sector gold purchases could reach 700 tons in 2019 led by these countries as well as Kazakhstan, Iran, and Turkey, according to Citigroup Inc.

Heightened geopolitical and economic uncertainty pushed central banks to diversify their reserves and focus on investing in safe and liquid assets, with governments worldwide adding 651.5 tons of bullion last year — the second-highest total of purchases on record, according to the World Gold Council.

Further inflows — expected to run as high as 2018 as China, Russia, and Kazakhstan buy –should also be supportive sof prices, according to Goldman Sachs Group Inc. Spot gold has lost almost 6 percent since a peak in February as equities rallied.

“There seems to be some form of pattern, not just the RBI, that central banks tend to increase gold reserves when the global macroeconomic environment is uncertain,” OCBC’s Lee said. “It’s no coincidence that one of the biggest buyers of gold in recent months was China, which is in the midst of trade tensions with the U.S. and may have been seeking to diversify its trillions of dollar reserves.” India may be following a similar tactic of diversification, he said.

The trade war between the U.S. and China has disrupted supply chains, whipsawed markets and weighed on the world economy. In March, Donald Trump announced he plans to end key trade preferences for India and Turkey, and notified Congress of his “intent to terminate” benefits, starting a 60-day countdown before the president can take the action on his own authority.

While the RBI didn’t respond to a request for a comment, its annual report for 2017-2018 released in August said diversification of foreign currency assets continued during the year and that the “gold portfolio has also been activated.”

Diversification

The rising U.S. deficit and the Federal Reserve signaling a pause on interest rate hikes could be factors that may potentially compel the RBI to add more to its gold holdings, according to Shekhar Bhandari, the Mumbai-based business head of global transaction banking and precious metals at Kotak Mahindra Bank Ltd.

India’s foreign-exchange reserves are improving steadily and foreign fund inflows “are strong, hence buying U.S. Treasuries and gold will help keep the rupee on the weaker side and give a boost to exports,” he said.

The Indian rupee, which was Asia’s worst-performingmajor currency in 2018, has been strengthening in recent months due to strong foreign inflows into the equity and debt markets. Investors, though, remain wary of risks in the form of an increase in oil prices, a swing in global risk appetite and federal elections in the country.

There’s room for more diversification — while India’s gold holdings are the 10th-largest by country, they account for only 6.4 percent of its reserves, compared with more than 70 percent in Germany and the U.S., WGC data show.

“This is an argument for further buying,” said Carsten Fritsch, senior commodity analyst at Commerzbank AG in Frankfurt.

“It is too speculative to say how much gold the RBI will buy this year. It could be more than last year, though.”

News & Commentary

Gold slips towards 4-month low as robust dollar dents appeal (Reuters.com)

Asian shares fall despite strong Wall Street; oil retreats (Reuters.com)

Australia shares end at over 11-year high on rate cut hopes; NZ rises (Reuters.com)

Gold worth billions smuggled out of Africa (Reuters.com)

Worsening Mood in Germany, France Damps Euro-Area Rebound Hopes (Bloomberg.com)

World’s Central Banks Including India Want More Gold (Bloomberg.com)

You Are Here – Hussman (HussManFunds.com)

Seeds Sewn For Major Transatlantic Trade War Starting In May (ZeroHedge.com)

Chicago’s Pension Funds Looking More Like A Collapsing Ponzi Scheme (ZeroHedge.com)

Time for a True Global Currency – IMF (Project-Syndicate.org)

Total Identifiable Silver Investment Rose 5% to 161 Moz in 2018 (Twitter.com)

Gold Prices (LBMA PM)

23 Apr: USD 1,273.45, GBP 979.67 & EUR 1,131.46 per ounce

18 Apr: USD 1,276.50, GBP 981.12 & EUR 1,134.17 per ounce

17 Apr: USD 1,276.10, GBP 978.77 & EUR 1,127.82 per ounce

16 Apr: USD 1,283.75, GBP 981.30 & EUR 1,137.40 per ounce

15 Apr: USD 1,286.75, GBP 982.43 & EUR 1,137.23 per ounce

Silver Prices (LBMA)

23 Apr: USD 14.97, GBP 11.51 & EUR 13.31 per ounce

18 Apr: USD 15.00, GBP 11.49 & EUR 13.27 per ounce

17 Apr: USD 15.00, GBP 11.49 & EUR 13.27 per ounce

16 Apr: USD 14.94, GBP 11.42 & EUR 13.22 per ounce

15 Apr: USD 14.93, GBP 11.39 & EUR 13.20 per ounce

12 Apr: USD 15.06, GBP 11.51 & EUR 13.31 per ounce

Recent Market Updates

– Russia’s 2019 Gold Rush Continues: Buys 600,000 Ounces of Gold In March

– When Should You Sell Your Gold and Silver? (GoldCore Video)

– Understanding Gold: A Step By Step Guide To Gold As An Asset Class

– World Trade Suffers Biggest Collapse Since Financial Crisis

– Exclusive Offer: Secure Gold and Silver Storage In Zurich For Free For Six Months

– There Is Too Much Debt In The World – World Bank

– How to Store Gold in an Uncertain World

– The ECB Is Struggling With Inflation, Interest Rates and The Outlook

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

Kranzler states the obvious: yesterday’s raid was shear manipulation coupled with fake financial journalism which covers this crime

(courtesy Dave kranzler/IRD)

Dave Kranzler: Today’s paper gold raid and fake financial journalism

Submitted by cpowell on Tue, 2019-04-23 18:39. Section: Daily Dispatches

2:37p ET Tuesday, April 23, 2019

Dear Friend of GATA and Gold:

Today’s paper-market raid on gold was another instance of market manipulation, Dave Kranzler of Investment Research Dynamics in Denver notes, as the seller unloaded his mammoth position all at once rather than gradually, which would have enabled him to obtain better prices.

Of course we’ve seen such manipulative smashes a thousand times before, so Kranzler’s commentary today may be more welcome for taking a crack at another oblivious market analyst at Kitco, Jim Wycoff, for his trying to contrive an explanation for the smashdown that fits with ordinary market action. Fairness to Wycoff requires noting that nearly all monetary metals market analysts are just as willfully blind lest they impugn their “technical analysis.”

Kranzler’s commentary is headlined “Tuesday’s Paper Gold Raid and Fake Journalism” and it’s posted at the IRD internet site here:

http://investmentresearchdynamics.com/tuesdays-paper-gold-raid-and-fake-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

END

I brought this story to you yesterday but it is worth repeating..the survey fails to address market manipulation

(courtesy Ted Butler/GATA)

Ted Butler: Annual silver production surveys fail to address market manipulation

Submitted by cpowell on Tue, 2019-04-23 22:29. Section: Daily Dispatches

6:28p ET Wednesday, April 23, 2019

Dear Friend of GATA and Gold:

Silver market analyst Ted Butler this week examines the annual silver production reports by GFMS and CPM Group and wonders how they can be considered honest when they never mention the evidence of manipulation of the silver market. Butler’s commentary is headlined “The Annual Silver Surveys” and its posted at GoldSeek’s companion site, SilverSeek, here —

http://silverseek.com/commentary/annual-silver-surveys-17634

— and at 24hGold here:

http://www.24hgold.com/english/news-gold-silver-the-annual-silver-survey…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

The best mining company in the world: Agnico Eagle

(courtesy Reuters)

Agnico bets on high-grade gold as it digs in Canada’s remote north

Submitted by cpowell on Tue, 2019-04-23 22:55. Section: Daily Dispatches

By Nicholas Saminather

Reuters

Tuesday, April 23, 2019

TORONTO — Agnico Eagle Mines is doubling down this year on Nunavut, Canada’s least developed territory, betting that the high-grade gold ores and slim competition there will offset the risks of digging in the remote location in the far north.

For miners desperate to shore up reserves, the choice is often between safer jurisdictions with inhospitable geographies and easier-to-reach ores in politically challenging locations.

…

Investors have been rewarded for backing Agnico’s strategy.

The company’s shares have surged 71 percent over the past five years, trouncing the 0.3 percent gain in the benchmark S&P/TSX Global Gold Index. Investors believe the company is making the right move again, thanks to high-grade ores in Nunavut and Agnico’s 12 years of experience in the Arctic territory. …

… For the remainder of the report:

https://ca.reuters.com/article/businessNews/idCAKCN1RZ1PO-OCABS

END

If one offered investors a fat tail put option that never decays or expires, costs about -1% pa to carry, has no counter party risk & no chance of ever becoming worthless, there would be a line out the door. But when one explains that this option is physical gold… no interest.

– S. Mikhailovich

The above quote has been atop www.jsmineset.com for over 6 months now. Recently, several readers have asked “what does it mean and why has the quote remained for so long”? With financial markets bloated and ready to implode without notice, let’s look at this very important concept and then expand on it as you will see.

First, what is a “fat tailed put”? A put option is something speculators use to bet on downward movement, or hedgers use to protect long positions. In this instance, the “put” happens to be against the financial system as a whole. In other words, a put, or a bet/hedge against a systemic implosion. A “fat tail” refers to something that begins to move exponentially the higher the sigma event becomes. The worse the event, the greater the move higher of a fat tailed put in far greater magnitude. Ultimately in a credit meltdown, owning gold will be the equivalent of owning “all the marbles”!

If you have any understanding of options, you know they have final expiration dates and whatever “time premium” that exists will continually decay until expiration day when the premium vanishes as no more time exists. This is typically the problem with puts or calls, they have a final expiration date, you might be correct in your thought a market may move one way or the other but it may not happen within your timeframe. If this is the case and your option expires, your speculation or your hedge is gone when the event takes place. It is for this reason (premium decay into expiration) that the “writers” (issuers) of put and call options generally win something like 90% of the time. Conversely, buyers of options normally lose 90% of the time because of the premium decay due to the passage of time.

Getting to the meat of this quote, the author is trying to tell you gold is THE ultimate put option to protect against a credit meltdown as well as many other possible negative scenarios which could affect the entire credit edifice. Gold costs less than 1% per year to carry (store), it has no expiration date and it can never ever become worthless. Most importantly it has no counterparty risk. In today’s world where literally everything has liability (or promise) attached, gold has none. No government or institution needs to guarantee gold. For instance, when you purchase a bond, any bond, if the borrower fails to pay either interest or principal …you as the lender suffers. Gold promises nothing. Rather, it is “proof” labor, capital and equipment have already been employed to create the bar or coin in your hand.

The author finally points out, this type of put option with no time decay or expiration, AND no liability is the ultimate in protection …but because it is “called” gold, no one has interest. Bluntly, governments and their central banks have psyop’d the populace for many years that gold is “risky” and bad, only their currency is safe …! They have done a fabulous job from a psychological standpoint, though not so much from the standpoint of the actual performance of their currency as ALL have been debased and lost purchasing power over the years. The fact that investors/savers have seen with their own eyes currencies continually debase versus real goods (and of course gold), yet still think of gold as “risky”, is proof positive how thorough government negative campaigns against gold have been!

So that pretty much explains the quote. If you understand nothing else, knowing gold will be your life boat under nearly all possible negative systemic scenarios is critical. Inflation/hyperinflation? Gold. Depression/deflation? Gold Negative currency or credit events? Gold. War/civil war? Gold. Simply, when anything of real substance occurs that is systemically bad financially or economically, because of gold’s characteristics (especially the non liability aspect), GOLD is THE safe haven. This has been true for thousand’s of years and as you will see when the current credit bubble of historic proportions bursts …IS STILL TRUE TODAY!

OK, so the quote has been explained, “gold is the ultimate put option against a negative systemic event”. If this is the case and I assure you it is, then what form of gold is best? In this case, what gives you the most exposure to gold for your capital expended. In plain English, what is the ultimate call option? When TSHTF, what form of gold will give you the most exposure to gold’s “fat tail put” characteristic? Let’s call it a FAT TAILED CALL OPTION!

This is actually quite easy and has been in front of you all along. The greatest call option on gold is the mining company that has the most PROVEN gold ounces in the ground per share outstanding. I thought about saying “economically feasible to mine” but this is slightly incorrect. If cost to produce is currently $1,500 per ounce, then it’s not economically feasible today …but what happens when gold trades to $2,000 or many multiples? It is this concept that explains the operating leverage of mining companies and why they are historically far more volatile than the price of gold itself. Generally speaking, mining companies in production have 3 times the leverage or volatility to gold’s price.

But there is another sector of the mining industry with FAR MORE leverage than the producing miners …the juniors …and especially the exploration companies! For example, there are many juniors/explorers out there that are valued at $20 (or less) for every ounce of proven gold they currently sit on. These companies currently trade at a huge discount to the value of the proven gold their properties contain. Let’s look at these from the standpoint of a “call option”?

The ultimate call option is a situation that gives you THE most exposure to gold for your capital expended. Gold exposure that can be purchased at a discount (thus no premium) and does not expire unless the company bankrupts. In essence, you are looking for companies with the most proven gold ounces per common share. In this instance, you have the most gold exposure for your capital expended.

To wrap this up, gold itself is a fat tailed put that offers outsized financial protection the worse things get. Proven ounces in the ground, (owned by companies whose stocks are currently almost free) offers maximum leverage to gold. Thus you have massive leverage upon the asset which offers the most protection to the financial meltdown mathematically certain to occur! Call this the fat tailed call option on gold …which happens to be the fat tailed put option to a systemically bankrupt global Ponzi scheme. …And without expiration!

Standing watch,

Bill Holter

Holter-Sinclair collaboration

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7182/

//OFFSHORE YUAN: 6.7238 /shanghai bourse CLOSED UP 3.02 POINTS OR 09%

HANG SANG CLOSED DOWN 157.44 points or 0.53%

2. Nikkei closed down 59.74 POINTS OR 0.27%

3. Europe stocks OPENED MIXED/red

USA dollar index RISES TO 97.65/Euro RISES TO 1.1208

3b Japan 10 year bond yield: FALLS TO. –.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.84/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 66.09 and Brent: 74.47

3f Gold DOWN/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +00%/Italian 10 yr bond yield DOWN to 2.66% /SPAIN 10 YR BOND YIELD DOWN TO 1.08%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.66: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.30

3k Gold at $1271.45 silver at: 14.84 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 47/100 in roubles/dollar) 64.17

3m oil into the 66 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.84 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0182 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1412 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.00%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.54% early this morning. Thirty year rate at 2.96%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.8760.. VERY DEADLY

Stocks Struggle With S&P At All Time High; Global Stocks, Yields Slide On China Stimulus Fears

Global markets took a step back on Wednesday, with US index futures and Asian stocks struggling to push higher following Tuesday’s record S&P close amid clear signals that China has put broader monetary stimulus on hold. The MSCI world equity index, edged down 0.1 percent in early European trade, as Treasuries continued to climb alongside European sovereign bonds and the dollar extended its rally to a six-week high, defying the signal from the fresh all time highs in US stocks as bond traders refuse to “rotate greatly” into stocks, and instead see even more economic weakness (or just more QE) in the future.

European shares followed Asia lower, pulling back from eight-month highs, with Europe’s Stoxx 600 index slipping 0.4% in early trading, although subsequent gains in technology companies and builders as the ETF bid came in, helped push the the Stoxx 600 into positive territory, and looking to extend the longest run of gains since 2017, boosted by positive earnings reports from companies including Credit Suisse.

Germany’s DAX was in the green despite the latest confirmation that Europe was still not out of the woods, after the German Ifo business survey showed German business morale deteriorated in April. The Ifo index measuring Germany’s business climate fell 0.5pt to 99.2 in April, below consensus expectations, driven by the manufacturing sector, while the services and construction sectors showed improvements. The decline reflects both a negative assessment of future economic conditions in the next 6 months (down 0.4pt to 95.2) and of current conditions, which fell 0.6pt (to 103.3). The March print was revised up from the first estimate (driven by a 0.1pt upward revision in the current conditions subindex).

The first major European bank to report, Credit Suisse’s shares rose 3.9% after the bank posted an unexpected rise in earnings and said it was cautiously optimistic about the second quarter following a challenging start to the year. It posted a net profit of 749 million Swiss francs ($734 million) for the first quarter of 2019 as larger-than-expected wealth management gains offset investment banking declines. Results from UBS Group AG and Barclays follow on Thursday and Deutsche Bank on Friday.

The top performers on the STOXX 600 were payments company Wirecard and business software company SAP, which also boosted the DAX. As reported earlier, the battered Wirecard soared 8% after Bloomberg reported that Japan’s SoftBank was looking to invest about 900 million euros ($1 billion) for a minority stake in the company, forcing a violent short squeeze. Meanwhile, SAP climbed 6% as the company set new medium-term profit targets after reporting a first-quarter operating loss that chiefly resulted from a restructuring charge according to Reuters.

Elsewhere, payments firm Ingenico rose +5% after reporting 1Q sales and raising FY organic growth guidance; chip stocks quickly reversed opening losses to trade higher, shaking off cautious management comments from U.S. peer Texas Instruments which weighed on expectations of industry recovery in second half of this year. STMicro also rose +3.6% after cutting spending plans and keeping its forecast for sales growth to improve this quarter as well as in 2H.

Earlier in the session, the MSCI Index of Asian shares ex Japan dropped 0.2%, where the biggest regional loser was South Korea’s KOSPI, which fell 0.9%, with Samsung Electronics down 1%. Korean investors shrugged off the government’s proposed supplementary budget aimed in part at supporting exports from the country and focused instead on a warning from chipmaker Texas Instruments, which said it expects a slowdown in demand for microchips to last a few more quarters.

Chinese equities flitted between gains and losses as investors debated whether Beijing would slow its pace of policy easing following stronger-than-expected first-quarter economic growth.

“The big picture is the tussle between Asia, which has pulled back, and America, where the markets made new highs, so Europe is probably going to be a bit torn between the two,” said Andrew Milligan, head of global strategy at Aberdeen Standard Investments. “The positive for Europe is Credit Suisse’s earnings, which could reignite upbeat sentiment and show that some financials are doing well despite weak European economic sentiment and the problems from very low interest rates.”

The muted euphoria that took U.S. stocks to record highs on abysmal volume appears to have triggered some “soul-searching” among investors, with Bloomberg noting that positive earnings surprises in Europe failing to erase lingering concerns about the region’s economic outlook. To date, almost 80% of S&P 500 companies reporting results have exceeded estimates. Looking ahead we get some key economic news, with US Q1 GDP data due on Friday, while emerging market investors will be nervously watching the dollar’s climb.

“The risk is not massively balanced to the downside,” Jasper Lawler, head of research at London Capital Group, told Bloomberg. “We’ve had a big run higher, we’ve tested record highs in the U.S., and maybe this is time for consolidation. Everything has been baked into the market already.”

Elsewhere in global markets,

Sri Lanka’s main stock index traded at its lowest since December 2012 following the deadly Easter Sunday attacks that killed more than 350 people. Analysts have said the country’s economy might need IMF assistance to overcome the devastation from the incident.

The Turkish lira hit its weakest intraday level against the dollar since mid-October as investors worried about risks generated by challenges to Istanbul election results and strains in relations with the United States.

Market attention is also focused on the Turkish central bank’s rate-setting meeting on Thursday, when it is expected to keep its policy rate unchanged at 24 percent.

Also in FX, Australia’s dollar tumbled against all major peers after a very weak inflation print boosted bets for an interest-rate cut with Citi now expecting at least 2 rate cuts in the months ahead. The dollar climbed to the highest in almost 7 weeks, defying most bank predictions for a weaker greenback. The Euro stayed under pressure after German IFO data missed estimates, trying to hold above 1.12 before the European Central Bank releases its economic bulletin. The pound slipped as U.K. politics returned to center stage as Prime Minister Theresa May is said to be mulling a new plan to get her Brexit deal through Parliament

In commodities, after jumping to 2019 highs earlier this week, oil prices eased on Wednesday on signs that global markets remain adequately supplied. Brent traded down 0.34 percent at $74.26 per barrel, while U.S. crude dipped 0.39 to $66.04 a barrel. Gold prices dipped 0.1 percent to $1,270.60 per ounce, hovering around the four-month low touched in the previous session.

A busy earnings day lies ahead with Microsoft, Facebook, Visa, AT&T and Boeing among companies due to report.

Market Snapshot

- S&P 500 futures down 0.1% to 2,935.00

- STOXX Europe 600 down 0.2% to 390.67

- MXAP down 0.3% to 162.53

- MXAPJ down 0.2% to 541.57

- Nikkei down 0.3% to 22,200.00

- Topix down 0.7% to 1,612.05

- Hang Seng Index down 0.5% to 29,805.83

- Shanghai Composite up 0.09% to 3,201.61

- Sensex up 0.5% to 38,768.58

- Australia S&P/ASX 200 up 1% to 6,382.14

- Kospi down 0.9% to 2,201.03

- German 10Y yield fell 1.7 bps to 0.024%

- Euro down 0.1% to $1.1216

- Brent Futures down 0.4% to $74.21/bbl

- Italian 10Y yield rose 7.1 bps to 2.302%

- Spanish 10Y yield fell 1.4 bps to 1.102%

- Brent futures down 0.3% to $74.28/bbl

- Gold spot up 0.1% to $1,273.46

- U.S. Dollar Index up 0.01% to 97.65

Top Overnight News

- Key gauges of confidence in Germany and France, the euro area’s two largest economies, unexpectedly deteriorated, signaling that a long-expected rebound may still be some way off

- Trade negotiators led by U.S. Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin will travel to Beijing next week, the White House said, as both sides work to reach a draft agreement by next month

- The U.K. formally kick-started its search for Mark Carney’s successor as governor of the Bank of England, a role that’s been linked to both senior people within the institution and ex-central bankers around the world

- The People’s Bank of China offered 267.4 billion yuan ($40 billion) of targeted medium-term loans on Wednesday, a step that funnels money to some lenders while avoiding broad easing

- The death toll in the Easter massacre in Sri Lanka rose to 359, while internal tensions among the country’s dueling leaders have resurfaced in recent days over intelligence failures in the run-up to the blasts

Asian equity markets traded mixed after the region failed to sustain the tailwinds from Wall St where strong blue-chip earnings propelled the S&P 500 and Nasdaq to fresh record closes. ASX 200 (+0.9%) resumed this week’s outperformance as soft CPI data brought forward various expectations for a rate cut to as early as next month, while gains in the Nikkei 225 (-0.3%) were later pared on detrimental currency moves. Elsewhere, Hang Seng (-0.5%) and Shanghai Comp. (U/C) also failed to sustain opening gains as White House confirmation that US-China trade talks will resume next week and the PBoC announcement of CNY 267bln in targeted MLF, was overshadowed after the PBoC dismissed rumours related to a potential targeted RRR cut for rural banks and refrained from Reverse Repo operations. Finally, 10yr JGBs saw mild gains as sentiment in the region soured and after similar upside in T-notes amid bull-steepening in the US, while the BoJ were also active in the market today for a respectable JPY 950bln of JGBs and focus now shifts towards the conclusion of the central bank’s 2-day policy meeting tomorrow.

Top Asian News

- This Time Around, Asia Investors Aren’t Buying the Tech Euphoria

- Richest Family in Thailand Is Getting Richer by Helping China

- HKMA, SFC Inspect A China-Based Bank Over ‘Complex Transactions’

- China Stocks Fluctuate in Afternoon Trading as Small Caps Jump

Major European indices are mixed [Euro Stoxx 50 -0.1%] as sentiment continues to deteriorate from the Asia session which failed to sustain the momentum in US equities where the S&P and Nasdaq reached record closes. Sectors are similarly mixed, with Energy names underperforming in line with the oil complex’s positive momentum dissipating after the larger than expected API build. Also performing poorly is the auto sector, following Nissan cutting their FY guidance; which has weighed particularly heavily on Renault (-3.8%), with other auto names such as BMW (-0.8%) and Volkswagen (-1.0%) down in sympathy. Conversely, the Technology sector is significantly outperforming its peers led by the strong performance in sector heavyweight SAP (+6.8%) who represents 26% of the sector after the Co. reported strong earnings and raised 2019 operating profit guidance; subsequently, Co. shares have this morning printed a record high of EUR 109.3. Other notable movers this morning include Credit Suisse (+3.0%) and Novartis (+2.7%) following earnings with the SMI (+0.4%) outperforming on the back of this. In addition, Novartis strong performance, following the Co. raising guidance in-spite of the Q1 sales miss, has caused the Healthcare sector to perform strongly. Finally, in a turnaround from recent performance Wirecard (+7.1%) are the outperforming DAX constituent (+0.1%), after reports that the Co. and Softbank have signed an agreement for Softbank to purchase a 5.6% stake in the Co. for around USD 1bln.

Top European News

- U.K. Borrowing Hits 17-Year Low as Calls Grow to End Austerity

- London’s Unsold Homes Under Construction Increase to Record

- U.K. Said to Prepare Tougher Rules on Huawei, Avoid Full Ban

- Italy’s Coalition Reaches Accord on Rome Relief Amid Infighting

In FX, the Aussie has sharply extended losses in wake of weaker than expected Q1 CPI metrics overnight that have raised RBA rate cut expectations for the next policy meeting in May to circa 60% and heightened the probability of another 25 bp ease before year end. Aud/Usd collapsed from around 0.7102 to 0.7028 in response before finding some underlying bids ahead of big barriers at the psychological 0.7000 level and a couple of downside chart supports in very close proximity, like 0.7005 (50% Fib) and 0.7003 (March 7 low). Note also, more exporter bids are anticipated around the next big figure following similar interest at 0.7050 that were filled on the way down amidst all round selling from high frequency and leverage accounts along with macro funds when 0.7070 gave way. Similarly, Aud/Nzd saw leverage and momentum longs bail on a break through 1.0650 as the cross hit a low of 1.0618 from 1.0671 at one stage, while the Kiwi also fell in sympathy vs its US counterpart to 0.6614 from 0.6657 and Nzd/Usd is now hovering near 0.6625 ahead of NZ trade data on Thursday.

- CAD – The other non-US Dollar is also languishing and retreating further from recent highs as a downturn in crude prices adds to defensive positioning in the lead up to today’s BoC meeting and MPR that is expected to be cautious if not dovish, with downgrades to Canadian growth and inflation projections. The Loonie is currently near the bottom of 1.3461-18 parameters and not far from last month’s low of 1.3468, as Usd/Cad options predict a 67 pip break-event for the BoC.

- EUR – The single currency is holding rather precariously on to the 1.1200 handle after another dip below stopped just short of Wednesday’s 1.1192 base, with the latest German Ifo survey missing on all counts and softer than the previous month. Moreover, the institute noted that the April readings point to more slowing in the economy and industrial sector underperformance, chiming with underwhelming preliminary PMIs, and could translate to lower 2019 GDP growth overall compared to the 0.8% forecast that has only recently been revised down. However, Eur/Usd has recovered to retest a key Fib at 1.1216 within a 1.1195-1.1231 range.

- CHF/SEK – Relative G10 outperformers as the Franc rebounds through 1.0200 vs the Greenback and from 1.1450+ against the Euro, while the Swedish Krona is back above 10.5000 vs the single currency and braced for the Riksbank to reaffirm tightening guidance for H2 this year tomorrow. Conversely, Eur/Nok remains elevated over 9.6000 on the aforementioned retreat in oil.

- DXY – The Usd continues to proffer at the expense of others, in part if not the most part, but the index has not managed to build on Tuesday’s new 97.783 ytd peak as the JPY and GBP also display a degree of resilience and contain downside forays ahead of 112.00 and 1.2900 respectively. Cable has bounced off Fib support at 1.2911, albeit mildly amidst ongoing Brexit uncertainty, while Usd/Jpy is still encountering supply and the Yen retains underlying safe-haven support in the run up to the BoJ and US GDP data the day after. Note, detailed previews of all this week’s Central Bank policy convenes are available via the Research Suite and/or in the form of primers on the headline feed into each meeting.

In commodities, Brent (-0.2%) and WTI (-0.4%) prices have broken the Iran waiver induced positivity following last nights API’s, where crude stocks printed a significantly larger build than was expected; 6.9mln vs. Exp. 1.3mln; ahead of today’s EIA release which may result in some additional downward pressure on oil prices if a similar figure is reported. Newsflow for the complex has been relatively light, although Saudi Energy Minister Al Falih has reiterated that they remain focused on balancing the global oil market and global inventories will guide their actions. Adds that there will be little variance in May production levels from the previous months, as they will not pre-emptively increase production even though they expect increased demand following the conclusion of Iranian oil waivers. Gold (+0.1%) is little changed as the dollar remains firm with yellow metal remaining above the USD 1270/oz level and towards the top of the day’s relatively narrow range. Elsewhere, Copper has traded lacklustre in line with the general market sentiment and due to the underperformance seen in China for much of the overnight session; with China the largest buyer of the red metal.

US Event Calendar

- 7am: MBA Mortgage Applications -7.3%, prior -3.5%

DB’s Craid Nicol concludes the overnight wrap

Timing it with a holiday week doesn’t help, but you’d be hard pressed to find another occasion when there’s been a more subdued record-breaking day for US stock markets. Indeed the S&P 500 and NASDAQ waltzed to new all-time highs yesterday with both breaching their October peaks after advancing +0.88% and +1.32%, respectively. The DOW also gained +0.55% and remains just over 1% off its all-time peak. We had a quick glance back at this recent run and since the December trough, 82 trading sessions ago, the S&P 500 and NASDAQ are up a remarkable +24.78% and +31.13%, respectively. The last time they bounced as sharply and as quickly was after the financial crisis,after markets bottomed out in March 2009. Then, the S&P 500 took only 23 days to bounce over 25% off the trough, while it took the NASDAQ 36 days to rally 32%.

So this rebound has been the strongest in a decade, even if it feels less dramatic. Indeed, the VIX index slid -0.14pts yesterday to 12.28, back near its year-to-date lows. For comparison, during the aforementioned rebounds in 2009, the VIX averaged over 40pts over the rally period. In fact, we also looked back at the closing moves for the S&P 500 since April 2nd and the average in the 15 sessions up until and including then is just +0.15%. It doesn’t get any better if we look at ranges either with the average intraday range of just 0.59%. You have to go back to early January 2018 to find the last time we had a smaller average intraday range over 15 sessions. The good news is that the direction of travel is positive for now though and yesterday earnings played their part. We’ll go through the details on those below but with Microsoft and Facebook reporting today, positive earnings reports could provide a further tailwind for risk in the absence of any other drivers out there at the moment.

Speaking of earnings Caterpillar are also due to report their latest quarterly numbers today. Those results are always closely watched by both micro and macro investors given the company’s status as an economic bellwether.Remember that the stock tumbled -9.13% following its Q4 earnings release back in January when management flagged slowing demand in China. Caterpillar is expected to post Q1 EPS of $2.82 (Bloomberg consensus) which would be roughly flat on the same period last year. Like always though it’ll be the forward looking commentary which is most closely watched.

Back to markets yesterday where in Europe the STOXX 600 hit its highest level since last July after advancing +0.23%. The DAX and CAC posted fairly modest gains (+0.20% and +0.11% respectively), while Spain’s IBEX and Italy’s FTSE MIB lagged, falling -0.57% and -0.27%. More eye catching was European bank stocks falling -1.59%, possibly in response to comments from ECB Management Board member Benoit Coeure, playing down the possibility of deposit tiering. He told the Frankfurter Allgemeine Zeitung that “at the current juncture, I do not see the monetary policy argument for tiering” and sounded optimistic about the growth outlook.

The regional divergence was mirrored in fixed income markets, as 10y yields in Spain and Italy rose +5.2bps and +7.3bps respectively. Bund yields rose a more modest +1.7bps, while Treasury yields fell -2.4bps and also are down another -1.4bps overnight. A bit of catch up to the oil move seemed to play a part for European rates with WTI pushing above $66/bbl following another +0.91% jump yesterday. Il Sole also reported that Italy’s government could delay the approval of a growth pact until next week amidst feuding over corruption charges involving a League party lawmaker. On a related note it’s worth noting that S&P’s rating review for Italy is due this Friday with the sovereign currently rated BBB/Negative. While no change is expected it’ll be worth a watch all the same.

Meanwhile in FX there was a reasonable bid for the dollar yesterday which saw the Dollar index rise +0.36% and approach the top of a recent technical range. The euro (-0.27%) and sterling (-0.34%) suffered along with EM FX (-0.32%). There was some suggestion that a tweet from President Trump highlighting the impact of tariffs from the EU on Harley Davidson and the suggestion that the US would reciprocate as driving some of the price action however the reaction did appear to be somewhat delayed if so.

Looking out at screens this morning, despite the gains on Wall Street last night it’s a very different picture in Asia where most bourses are seeing decent losses.That’s the case for the Nikkei (-0.48%), Hang Seng (-0.85%), Shanghai Comp (-0.92%) and Kospi (-1.32%) in particular. Futures on the S&P 500 (-0.15%) are also slightly lower. The moves come despite confirmation from the White House that Lighthizer and Mnuchin will travel to China on April 30th for another round of trade talks while the Chinese Vice Premier Liu He will then lead a Chinese delegation to the US for subsequent trade talks on May 8th. Perhaps most significantly, Bloomberg is reporting that the US and China are aiming to announce during Liu’s visit that they have agreed to a deal and details of a signing summit.

Moving on. Back to the earnings releases that were out yesterday, the highlight was Twitter (+15.64%), which reported healthy gains in revenue and daily active users.Sales were up 18% yoy and the platform added 8 million new users over the first quarter. The other major mover was Hasbro (+14.23%) as sales surprisingly grew for the first time in six quarters and earnings were positive. Coca-Cola (+1.78%) also rallied on strong sales growth in Asia. On the other hand, Procter and Gamble (-2.69%) underperformed despite sales and profit growth, as guidance for the rest of the year was a touch soft, with the CEO citing higher input prices as a headwind.

In other news, you couldn’t really blame Brexit headlines for the Sterling move yesterday however we did see the return of some headlines yesterday. Bloomberg reported an official as saying that the withdrawal bill was planned to be put to parliament next week, although this would be the implementation legislation required to kick off the process, rather than the meaningful vote. A spokesman for PM May confirmed that all the focus is on getting the WA passed by Parliament and that talks with Labour are ongoing still.

Finally yesterday’s data was a sideshow once more, however for completeness the April Richmond Fed manufacturing index in the US dropped 7pts unexpectedly to +3 after expectations were for no change. The new orders component also dropped and turned negative for the first time since January however it’s worth noting that this data does tend to be fairly volatile. On the plus side March new home sales rose +4.5% versus expectations for a -2.7% mom decline while the February FHFA house price index rose +0.3% mom and slightly less than expected in February. In Europe the April consumer confidence reading slipped 0.7pts to -7.9.

In terms of the day ahead, this morning in Europe we’re due to get April confidence indicators out of France before focus turns to the April IFO survey in Germany and March public finances data in the UK. It’s quiet in the US with only the latest MBA mortgage applications data due. Away from that we’ve got the BoC decision this afternoon while UK Chancellor Hammond is due to testify on the Spring Statement. Russia President Putin may also meet North Korean leader Kim Jong Un. Expect earnings to be a big focus once more with Microsoft, Facebook, AT&T, Boeing and Caterpillar amongst the headliners.

end

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 3.02 POINTS OR 0.09% //Hang Sang CLOSED DOWN 157.41 POINTS OR 0.53% /The Nikkei closed DOWN 59.74 POINTS OR 0.27%/ Australia’s all ordinaires CLOSED UP .93%

/Chinese yuan (ONSHORE) closed DOWN at 6.7182 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 65.92 dollars per barrel for WTI and 74.23 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.7182 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7238 / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

China/

China is running out of dollars as they try and fund their silk road project. However unlike Turkey they are still safe for now

(courtesy zerohedge_

Why Chinese Banks Are Running Out Of Dollars

Following the biggest quarterly credit injection in Chinese history, it is safe to say that China’s banks are flush with yuan loans. However, when it comes to dollar-denominated assets, it’s a different story entirely. As the WSJ points out, in the past few years, a funding problem has emerged for China’s biggest commercial banks, one which is largely outside of Beijing’s control: they’re running low on US dollars so critical to fund operations both domestically and abroad.

As shown in the chart below, the combined dollar liabilities at China’s four biggest commercial banks exceeded their dollar assets at the end of 2018, a sharp reversal from just a few years ago. Back in 2013, the four together had around $125 billion more dollar assets than liabilities, but now they owe more dollars to creditors and customers than are owed to them.

The reversal is the result of just one bank: Bank of China, which for many years held more net assets in dollars than any other Chinese lender, ended 2018 owing $72 billion more in dollar liabilities than it booked in dollar assets. The other “top 3” lenders finished the year with more dollar assets than liabilities, even though their net dollar surplus has shrunk substantially in the past five years.

And yet, as everything else with China, there is more than meets the eye: as the WSJ reports looking at Bank of China’s annual report, the bank’s asset-liability imbalance is more than addressed by dollar funding that doesn’t sit on its balance sheet. Instruments like currency swaps and forwards are accounted for elsewhere.

This is reminiscent of the shady operations discussed recently involving Turkey’s FX reserves, where the central bank has been borrowing dollar assets from local banks via off balance sheet swaps, which it then used to prop up and boost the lira at a time of aggressive selling of the local currency. It is safe to assume that the PBOC has been engaging in a similar operation.

Additionally, as the WSJ observes, such off-balance-sheet lending “can be flighty”, and citing a recent BIS study, the vast majority of currency derivatives mature in under one year, meaning they are up for constant renewal and could evaporate during times of pressure.

Of course, as we noted last week, the Turkish central bank got the idea to manipulate its currency using swaps from China, where currency swaps, meant to protect banks from liquidity crises when they lend in currencies other than their own, have boomed in recent years…. even if it still does not have “the most crucial of all” swap line – one with the Federal Reserve.

The good news is that unlike Turkey, whose net foreign asset position may be as low as just $10 billion, the imbalance at Bank of China is small relative to its balance sheet, so it shouldn’t be seen as an imminent threat. As a reminder, China has roughly $3.1 trillion in foreign exchange reserves (gross of swaps), which remain a safety backstop in case of a crunch or funding crisis, but as the WSJ notes, it is unclear how bad things would have to get before Beijing would permit its use by major commercial banks; meanwhile, in a worst case scenario, “a heightened need to help the big four lenders also makes that hoard of reserves seem somewhat less formidable.”

As for who is soaking up all the local bank’s dollar assets, one culprit is China’s Belt-and-Road projects, which are overwhelmingly financed in the U.S. currency, and are sending dollars overseas in the form of Chinese loans. Additionally, Chinese property developers have a rapacious demand, too.

But at the heart of this funding mismatch there is a simple cause: as the WSJ’s Mike Bird notes, “Beijing would like to be a major financial player overseas, but few borrowers have any interest in the yuan. Most international trade is accounted for in dollars, the yuan is difficult to convert and foreign owners of Chinese assets have at best an uncertain relationship with the country’s legal system.”

Until that changes, expect to see the banks’ net dollar funding position continue to turn increasingly negative.

end

4/EUROPEAN AFFAIRS

DEUTSCHE BANK/

Deutsche bank has no bank willing to take on the no 1 derivative player in the world. It is now again talking about a bad bank /good bank scenario as they wall off units that they want to close. The problem that they have is of course their huge losing derivative balloon

(courtesy zerohedge)

Deutsche Considering ‘Bad Bank’ Unit As Merger Talks Falter

Thanks to the Wall Street Journal, investors won’t need to wait until later this week for a promised update on the status of merger talks between Deutsche Bank and Commerzbank. Based on reports about Deutsche’s continued contingency planning, we can surmise that the answer to the question ‘how are deal talks going?’ is clearly ‘not well’.