GOLD: $1286.70 UP $9.20 (COMEX TO COMEX CLOSING)

Silver: $15.05 UP 12 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1286.10

silver: $15.07

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 46/46

DLV615-T CME CLEARING

BUSINESS DATE: 04/25/2019 DAILY DELIVERY NOTICES RUN DATE: 04/25/2019

PRODUCT GROUP: METALS RUN TIME: 20:13:07

EXCHANGE: COMEX

CONTRACT: APRIL 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,275.800000000 USD

INTENT DATE: 04/25/2019 DELIVERY DATE: 04/29/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 46

737 C ADVANTAGE 45

905 C ADM 1

____________________________________________________________________________________________

TOTAL: 46 46

MONTH TO DATE: 6,948

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 46 NOTICE(S) FOR 4600 OZ (0.1430 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 6948 NOTICES FOR 694800 OZ (21.611 TONNES)

SILVER

FOR APRIL

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1 NOTICE(S) FILED TODAY FOR 5,000 OZ/

total number of notices filed so far this month: 775 for 3,875,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE :$5350 UP $120

Bitcoin: FINAL EVENING TRADE: $5350 UP 65

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A CONSIDERABLE SIZED 1318 CONTRACTS FROM 214,262 DOWN TO 212,944 WITH YESTERDAY’S 4 CENT FALL IN SILVER PRICING AT THE COMEX. , WE DID HAVE CONSIDERABLE LIQUIDATION OF SPREADERS WITH TODAY READING. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 302 FOR MAY, 0 FOR JUNE 0 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 302 CONTRACTS. WITH THE TRANSFER OF 302 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 302 EFP CONTRACTS TRANSLATES INTO 1.510 MILLION OZ ACCOMPANYING:

1.THE 4 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

AND NOW 3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

33,350 CONTRACTS (FOR 19 TRADING DAYS TOTAL 33,350 CONTRACTS) OR 168.75 MILLION OZ: (AVERAGE PER DAY: 1755 CONTRACTS OR 8.776 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 168.75 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 24.10% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 734.55 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1318 WITH THE 4 CENT FALL IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 302 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS RESUMED THEIR LIQUIDATION OF THE SPREAD TRADES TODAY.

TODAY WE LOST A SMALL SIZED: 1016 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 302 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 1318 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 4 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.97 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.095 BILLION OZ TO BE EXACT or 157% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 1 NOTICE(S) FOR 5,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ AND NOW APRIL AT 3.875 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 6810 CONTRACTS, TO 435,049 DESPITE THE RISE IN THE COMEX GOLD PRICE/(A GAIN IN PRICE OF $0.05//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5146 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 5146 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 435,049. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1664 CONTRACTS: 6810 OI CONTRACTS DECREASED AT THE COMEX AND 5146 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 1664 CONTRACTS OR 166,400 OZ OR 5.175 TONNES. YESTERDAY WE HAD A GAIN IN THE PRICE OF GOLD TO THE TUNE OF $0.05.…AND YET WITH THAT RISE, WE HAD A GOOD LOSS IN TONNAGE OF 5.175 TONNES!!!!!!.??????????????????????????????????????????

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 131,474 CONTRACTS OR 13,147,400 OR 408.93 TONNES (19 TRADING DAYS AND THUS AVERAGING: 6919 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAYS IN TONNES: 408.93 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 408.93/3550 x 100% TONNES =11.52% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1782.32 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 6810 DESPITE THE GAIN IN PRICING ($0.05) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5146 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5146 EFP CONTRACTS ISSUED, WE HAD A STRONG GAIN OF 6812 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5146 CONTRACTS MOVE TO LONDON AND 6810 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE LOSS IN TOTAL OI EQUATES TO 5.175 TONNES). ..AND THIS STRONG DEMAND OCCURRED WITH A RISE IN PRICE OF $0.05 IN YESTERDAY’S TRADING AT THE COMEX.

we had: 46 notice(s) filed upon for 4600 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $9.20 TODAY

WE HAD A BIG INVENTORY CHANGES AT THE GLD//

ANOTHER WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD.

INVENTORY RESTS AT 746.69 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 12 CENTS TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV//

/INVENTORY RESTS AT 311.979 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A CONSIDERABLE SIZED 1318 CONTRACTS from 214.262 UP TO 212,944 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..TODAY,IT LOOKS LIKE OUR SPREADERS SAW GOOD ACTION WITH RESPECT TO THEIR USUAL AND CUSTOMARY LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ENTER AN ACTIVE DELIVERY MONTH. THUS SILVER HAS THE ACTIVE MONTH OF MAY COMING UP AND THUS SPREADERS DO THE FOLLOWING:

“YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF APRIL BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

We just had confirmation through the COT report just released at 3:30 pm

notice spreading has already started to liquify!!

in gold COT spreaders increased.!!

| Silver COT Report – Futures | |||||||

| Large Speculators | Commercial | Total | |||||

| Long | Short | Spreading | Long | Short | Long | Short | |

| 75,889 | 75,999 | 18,115 | 90,400 | 110,392 | 184,404 | 204,506 | |

| -144 | 5,851 | -2,757 | -3,836 | -7,516 | -6,737 | -4,422 | |

| Traders | |||||||

| 107 | 66 | 60 | 44 | 40 | 183 | 139 | |

| Small Speculators | |||||||

| Long | Short | Open Interest | |||||

| 34,709 | 14,607 | 219,113 | |||||

| 1,067 | -1,248 | -5,670 | |||||

| non reportable positions | Change from the previous reporting period | ||||||

| COT Silver Report – Positions as of | Tuesday, April 23, 2019 | ||||||

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 302 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 0 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 302 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 1318 CONTRACTS TO THE 302 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD LOSS OF 1016 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 10.32MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH. AND NOW 3.875 MILLION OZ FOR APRIL.

RESULT: A CONSIDERABLE SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE TINY 4 CENT FALL IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A SMALL SIZED 302 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 37.43 POINTS OR 1.20% //Hang Sang CLOSED UP 55.21 POINTS OR 0.19% /The Nikkei closed DOWN 48.85 POINTS OR 0.22%/ Australia’s all ordinaires CLOSED UP /04%

/Chinese yuan (ONSHORE) closed UP at 6.7359AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 64.03 dollars per barrel for WTI and 72.83 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 6.7359 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7446/ TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA/ SOUTH KOREA

NORTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/

4/EUROPEAN AFFAIRS

i)GERMANY/DAIMLER

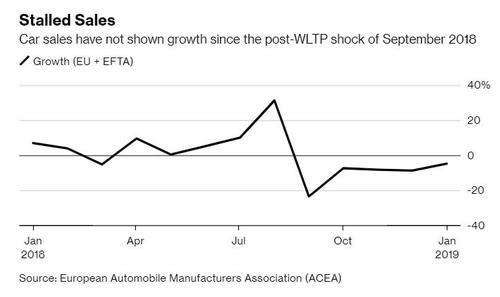

The automobile industry in Europe is in shambles led by Germany. Daimler is stung by falling Mercedes sales.

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

7. OIL ISSUES

Down goes oil after Trump called OPEC to tell them oil/gas prices are too high

( zerohedge)

8 EMERGING MARKET ISSUES

Argentina

9. PHYSICAL MARKETS

i)Sean Fieler notices many countries purchasing gold. He suggests there is a need for Americans to hold gold

ii)We brought you this story this week but it is worth repeating: China dollar bond defaults at China’s Minsheng Investment will test bank guarantees for the first time( Bloomberg/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning/TRADING

With the supposed strong GDP number: bond yields falter along with the dollar

( zerohedge)

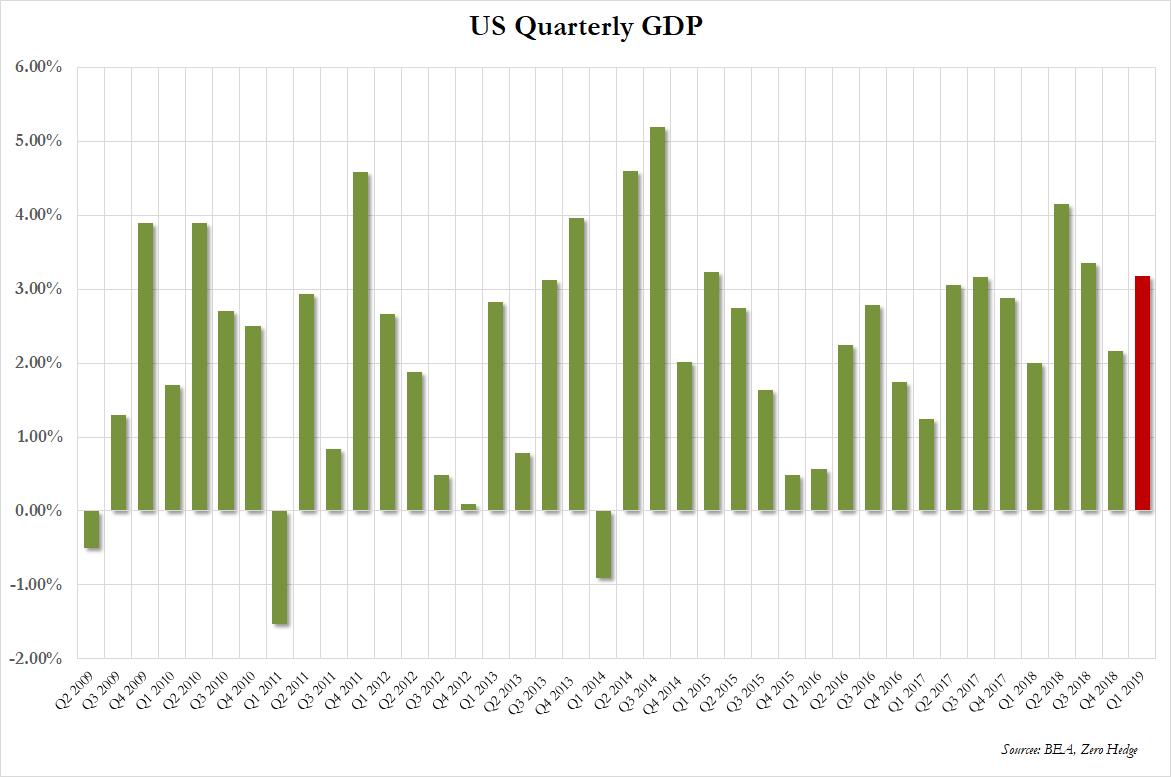

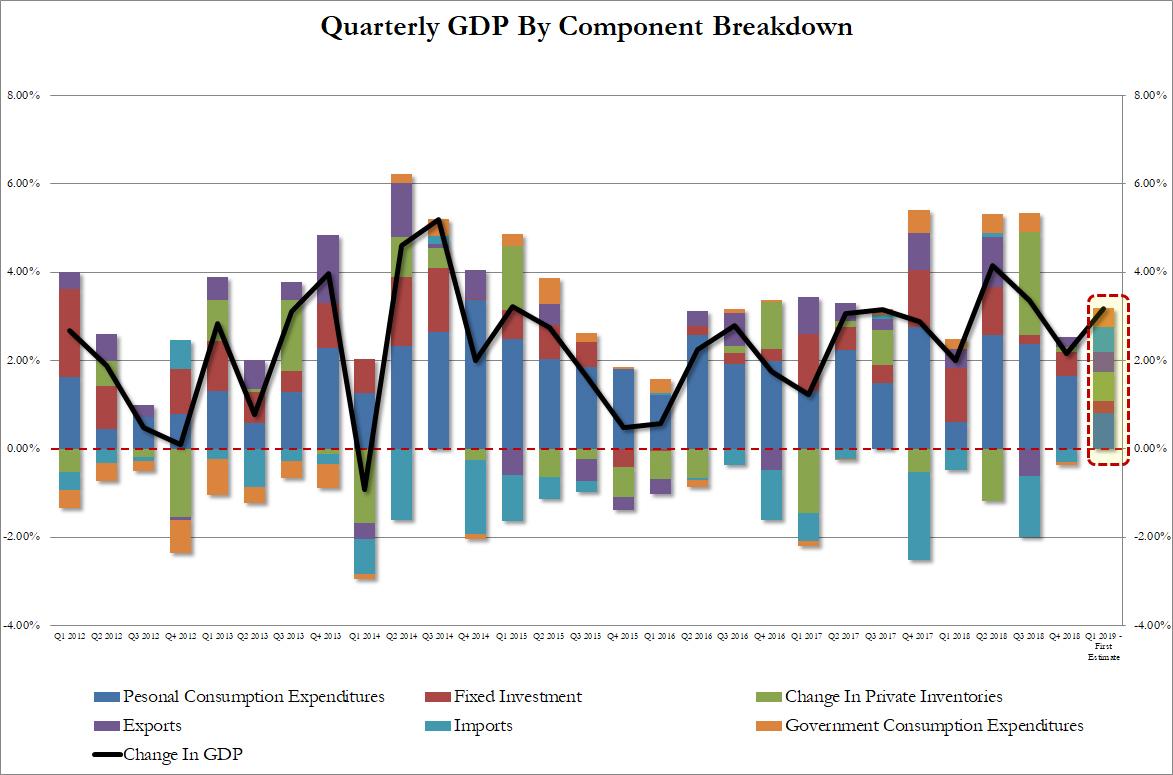

ii)Market data

Trump happy with first estimates for first quarter GDP soared to 3.2% but the gains were mostly one time items. You will find that this number will falter in the next few months

( zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

a)The total of all debt in the USA is now $72 trillion which works out to 220,000 per man woman and child.

( Michael Snyder)

b)First Volkswagen, then Daimler/Chrysler and now Ford. The Dept of Justice is launching a criminal probe over emissions irregularities

(zerohedge)

c)McDonald’s partners with AARP to recruit broke seniors to help fund the labour shortage which is worsening by the day

SWAMP STORIES

a)Amazing Strzok and Page discussed recruiting White HOuse sources for spying purposes.

( Sara Carter)

b)Rosenstein slams Obama for failing to call out the Russian election interference

c)We are getting close:

Trump makes a vow to release the “devastating FISA documents//and a good summary of the genesis

(courtesy zerohedge)

Let us head over to the comex:

AFTER APRIL, WE HAVE THE ACTIVE DELIVERY MONTH OF MAY AND HERE THE OI FELL BY 11,387 CONTRACTS DOWN TO 33,226. CONTRACTS.. THE NEXT MONTH OF JUNE GAINED 67 CONTRACTS TO 403. AFTER JUNE, THE VERY BIG DELIVERY MONTH OF JULY HAD A GAIN OF 8660 CONTRACTS UP TO 135,402 CONTRACTS.

Gold withdrawals;

i) we had zero withdrawal

Death of Inflation and the Death of Equities?

Is Inflation Dead? – Bloomberg Business Week

Inflation Is Here and Coming

From a contrarian perspective, the front page of Bloomberg Business Week this week is a classic contrarian sign that we may be on the verge of a serious bout of inflation or indeed stagflation as the global economy slows sharply and currencies are devalued again.

The online version of article, ‘Did Capitalism Kill Inflation?’ is well worth a read.

It ignores the fact that there has been massive increase in debt, inflation in asset markets and in particular in property markets – both to rent and to buy residential and commercial property.

It exonerates central bankers from creating very significant inflation in apartments, houses and property markets – the most important cost to most individuals, families and companies in the western world.

It ignores and exonerates central bankers for reigniting and recreating many property bubbles, stock market bubbles and other asset bubbles in the ‘Everything Bubble’ of 2019.

Instead, evil “capitalism” and “globalisation” is again blamed for all economic ills. Ignoring the fact that there is no capitalism today, rather we have a ugly mongrel form of crony globalisation and corrupt capitalism or corporatism which continually puts the interests of elites, corporations and banks over the interests of families, small businesses and society.

The front page brings to mind the classic Business Week front page in August 1979 entitled ‘The Death of Equities’ which we considered in our recent video update looking at where we are at in the market cycle.

‘The Death of Equities’ front page and article showed how mass psychology was very negative towards stocks after a long bear market. But in fact, stocks were in the process of bottoming and the article heralded, within a few short months, a bull market in U.S. shares which saw massive gains over the next 20 years (with some significant blips in 1987 and 1998 along the way).

The article is very complacent about inflation and terms inflation a “bogey man.” The huge complacency about the risk of inflation today is a classic contrarian signal and strongly suggests that inflation, stagflation (and in a worst case scenario hyperinflation) will rear its ugly head in the coming months.

News & Commentary

Gold firms as weak data puts focus back on growth risks (Reuters.com)

Gold prices tally a second straight gain but hover near lows of the year (MorningStar.com)

Euro stung by German growth fears, political uncertainty (Reuters.com)

Romanian parliament votes to bring gold reserves back from Bank of England (Reuters.com)

World Trade Volumes Are Plunging at the Fastest Pace in a Decade (Bloomberg.com)

Central Banks’ Club of Caution Grows as Bad News Piles Up (Bloomberg.com)

World Trade Volumes Are Plunging at the Fastest Pace in a Decade (Bloomberg.com)

Flash Crash Fears Haunt Traders Ahead of 10-Day Japan Break (Bloomberg.com)

China dollar bond default tests bank guarantees for first time (SCMP.com)

Suddenly Something Is Wrong (ZeroHedge.com)

Who Says They Don’t Ring a Bell at the Top? (321Gold.com)

Why the U.S. needs to encourage Americans to hold gold (Gata.org)

Gold Prices (LBMA PM)

25 Apr: USD 1,277.85, GBP 991.87 & EUR 1,146.87 per ounce

24 Apr: USD 1,273.80, GBP 984.90 & EUR 1,135.34 per ounce

23 Apr: USD 1,273.45, GBP 979.67 & EUR 1,131.46 per ounce

18 Apr: USD 1,276.50, GBP 981.12 & EUR 1,134.17 per ounce

17 Apr: USD 1,276.10, GBP 978.77 & EUR 1,127.82 per ounce

Silver Prices (LBMA)

25 Apr: USD 14.86, GBP 11.55 & EUR 13.36 per ounce

24 Apr: USD 14.80, GBP 11.44 & EUR 13.21 per ounce

23 Apr: USD 14.97, GBP 11.51 & EUR 13.31 per ounce

18 Apr: USD 15.00, GBP 11.49 & EUR 13.27 per ounce

17 Apr: USD 15.00, GBP 11.49 & EUR 13.27 per ounce

Recent Market Updates

– SWOT Analysis: Venezuela Sells $400 Million Worth Of Gold Bullion

– World’s Central Banks Want More Gold – India May Buy 1.5M Ounces In 2019

– Russia’s 2019 Gold Rush Continues: Buys 600,000 Ounces of Gold In March

– When Should You Sell Your Gold and Silver? (GoldCore Video)

– Understanding Gold: A Step By Step Guide To Gold As An Asset Class

– World Trade Suffers Biggest Collapse Since Financial Crisis

– Exclusive Offer: Secure Gold and Silver Storage In Zurich For Free For Six Months

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

Sean Fieler: Why the U.S. needs to encourage Americans to hold gold

Submitted by cpowell on Thu, 2019-04-25 14:52. Section: Daily Dispatches

By Sean Fieler

The Federalist, Washington

Thursday, April 25, 2019

Foreign central banks are acquiring gold at the fastest pace in 50 years, and their purchases are not driven by investment considerations alone. The Central Bank of Russia, 2018’s largest official-sector buyer of gold, wants to reduce Russia’s dependence on the dollar, while the Hungarian National Bank noted gold’s increasing strategic importance as underlying their recent purchases.

…

America cannot stop foreign central banks from buying gold or reintroducing gold into the international monetary order. We can, however, adopt policies that will attract more of the world’s gold to the United States and position ourselves to deal with the remonetization of gold from a position of strength.

At the end of the Second World War, the U.S. Treasury owned more than 30 percent of the world’s gold. Today that same figure is less than 5 percent. America’s diminished share of the world’s gold is a result of our defense of the Bretton Woods System prior to its collapse in 1971 and subsequent failure to increase our gold reserves. The U.S. Treasury has not added to its gold reserves since 1969, and the Federal Reserve has not owned physical gold since the passage of the Gold Reserve Act in 1934. …

… For the remainder of the commentary:

https://thefederalist.com/2019/04/25/united-states-needs-start-encouragi…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

We brought you this story this week but it is worth repeating: China dollar bond defaults at China’s Minsheng Investment will test bank guarantees for the first time

(courtesy Bloomberg/GATA)

China dollar bond default tests bank guarantees for first time

Submitted by cpowell on Fri, 2019-04-26 02:57. Section: Daily Dispatches

By Carrie Hong and Carol Zhong

Bloomberg News

Thursday, April 25, 2019

Investor faith in Chinese dollar bonds backed by banks is about to be tested after a default by one of the country’s best-known private conglomerates.

China Minsheng Investment Group Corp. said last week cross-default clauses have been triggered on dollar bonds worth $800 million. These include $300 million of debt that carries a standby letter of credit from China Construction Bank Corp. — effectively a pledge to repay if the borrower can’t.

…

So far investor confidence that banks will honor such an agreement is unshaken. While CMIG’s dollar bonds due in August — which aren’t backed by a letter of credit — traded at around 58 cents on the dollar, bonds with CCB’s backing due in 2020 were indicated at about 99 cents on the dollar today. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-04-24/untested-china-bond-s…

end

* * *

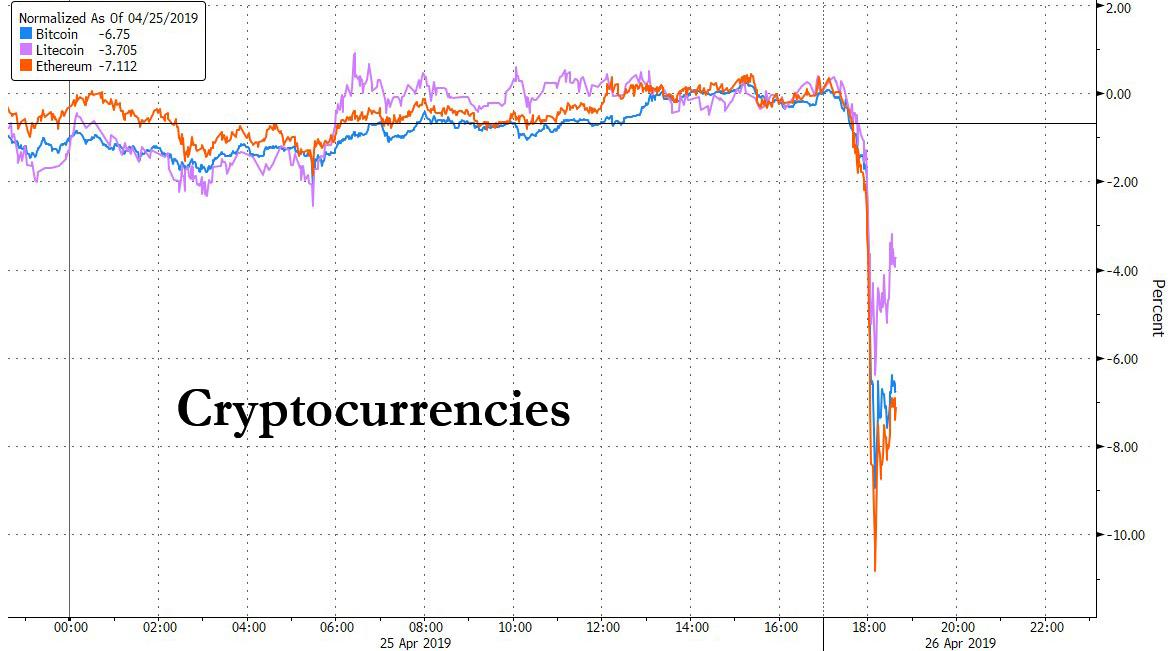

Cryptos Tumble After NY AG Accuses Bitfinex Of Massive Fraud, “Loss” Of $850 Million

New York’s Attorney General alleged the operator of the Bitfinex cryptocurrency trading platform and the issuer of the Tether “stablecoin” lost $850 million and subsequently used funds from affiliated stablecoin operator Tether – i.e., engaged in co-mingling of client and corporate funds – to secretly cover the shortfall; the news sparked a sharp selloff in the cryptocurrency space where Bitfinex has long been rumored to be a mechanism to prop up various virtual currencies.

A judge in Manhattan issued an order barring iFinex Inc., which operates the infamous Bitfinex cryptocurrency exchange and owns Tether Ltd. from money money from Tether’s reserves to Bitfinex’s bank accounts, halt any dividends or other distributions to executives and turn over documents and information, New York Attorney General Letitia James said Thursday in a statement. Tether is one of the world’s most valuable cryptocurrencies and is used in a significant share of trades involving Bitcoin. The NY AG said iFinex had been commingling client and corporate funds to cover up the missing funds, which occurred in mid-2018 and hadn’t been disclosed publicly.

“New York state has led the way in requiring virtual currency businesses to operate according to the law,” James said. “We will continue to stand-up for investors and seek justice on their behalf when misled or cheated by any of these companies.”

According to the WSJ, the AG’s findings emerged from an investigation into cryptocurrency exchanges that it launched in 2018 and is continuing. A report in September warned that many exchanges lacked basic safeguards and left consumers vulnerable to exploitation by market manipulators.

The attorney general said Bitfinex’s problems began in 2018, when it handed over $850 million to third-party payments processor Crypto Capital Corp. to handle customers-withdrawal requests. Over the months that followed, Panama-based Crypto Capital failed to process the orders, the attorney general said.

By November of that year, according to people close to the attorney general’s investigation, Bitfinex determined that it had permanently lost access to the $850 million. To hide the missing funds, Bitfinex and Tether engaged in a series of maneuvers that drained Tether’s reserves, the people said.

Tether has frequently been accused of facilitating cryptocurrency price manipulation; it is allegedly backed one-to-one by U.S. dollars, yet the firm has never released a public audit showing it has the reserves to back the coins in circulation, leading many to question whether the funds even exist.

As the WSJ notes, Tether has marketed the coin as a way to get both the safety of the dollar and the speed and anonymity of a digital currency. Its market value has risen steadily over the past two years, to $2.8 billion from about $10 million at the beginning of 2017. Since then it has become a major source of liquidity in the cryptocurrency market, and about 80% of all bitcoin trading is done via Tether, according to data from research site CryptoCompare. Some have speculated that tether is how various Asian accounts have been quietly laundering money into cryptocurrencies, which they then used to circumvent “firewalls” and deposit funds offshore.

Needless to say, $850 million would represent a major portion of Tether’s reserves. Tether currently claims on its website that the coins it issues are backed by reserves that include currency, cash equivalents and other assets and receivables. According to the WSJ’s Paul Vigna, the language was altered in March; it previously claimed the reserves were 100% in currency.

Many bitcoin advocates have repeatedly said that Tether represents a negative overhang over the cryptocurrency space and have been quietly hoping for a crackdown on both the exchange, and stablecoin, which would result in far more stability in the space which as seen in the chart above, tends to be greatly affected by any adverse report involving tether.

The full court NY AG court order can be found below (via CoinDesk):

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7359/

//OFFSHORE YUAN: 6.7446 /shanghai bourse CLOSED DOWN 37.43 POINTS OR 1.20%

HANG SANG CLOSED UP 55.21 points or 0.19%

2. Nikkei closed DOWN 48.85 POINTS OR 0.22%

3. Europe stocks OPENED GREEN EXCEPT LONDON

USA dollar index FALLS TO 98.13/Euro RISES TO 1.1137

3b Japan 10 year bond yield: FALLS TO. –.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.77/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 64.03 and Brent: 72.83

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO –01%/Italian 10 yr bond yield UP to 2.63% /SPAIN 10 YR BOND YIELD UP TO 1.07%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.64: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.27

3k Gold at $1280.95 silver at: 15.00 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 7/100 in roubles/dollar) 64.76

3m oil into the 64 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.85 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0213 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1374 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.01%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.52% early this morning. Thirty year rate at 2.94%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.9422.. VERY DEADLY

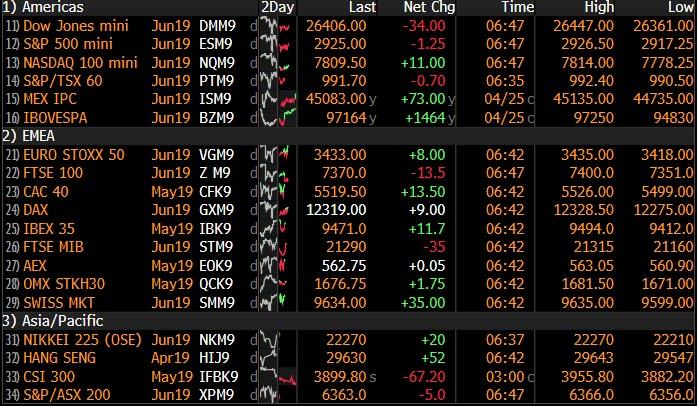

US Futures Drift Lower As China Suffers Worst Week Of 2019

US index futures, European stocks and Asian markets all drifted lower following an ugly report from Intel which hit chip stocks, offsetting a surge in Amazon’s Q1 profits as investors awaited the release of Q1 US GDP data and earnings season continued apace. Even so, global shares were on track for a fifth weekly gain in a row despite subdued trade, while the dollar retreated from 23-month highs.

Global stocks were largely flat on the day after subdued trading in Asia. MSCI’s All-Country World Index was down less than 0.1% as an unexpected tumble in Japanese industrial production underscored worries over the global expansion.

Looking at the key overnight earnings, another FAANG member showed their teeth after the Wednesday blowout number from FB, when Amazon beat EPS expectations by over $3 and didn’t sacrifice this gain in their revenue print, which came in marginally above expectations. This came as web services revenue increased by over 40% with the company reporting their most profitable quarter ever. Clouds remain on the horizon after the bright earnings, however, as the company warned of a slower Q2. In the pre-market AMZN are trading with gains of 1%.

On the flipside, Intel short-circuited and reported shockingly bad earnings guidance despite top and bottom line printing inline with expectations. The hardware maker cut their FY guidance and forecast a weak Q2 as Chinese data centre sales remain soft, as the region is consuming fewer microchips than expected, and follows on from a similar warning sign eschewed from Texas Instruments. As a result of the terrible results INTC is trading with losses of 7% in the pre-market.

Most European bourses opened lower, with Germany’s DAX and France’s CAC 40 being the only gainers. The pan-European STOXX 600 index was down 0.1 percent. The Stoxx 600 was little changed at press time as raw material producer losses were offset by gains in healthcare and media companies. In corporate news in the region, Deutsche Bank cut its revenue target and AstraZeneca posted an increase in cancer-drug sales.

While US stocks continue to trade at all time highs, albeit with dismal volumes suggesting there is little enthusiasm to chase prices here, sentiment in China has turned decidedly for the worse, and Chinese stocks suffered their worst week since October, showing the influence that Beijing’s economic policies still hold over the bull market. As we previewed on Sunday, markets got a taste of how much equities are worth without the prospect of additional measures that had helped restore $2.3 trillion to share values since January. Shanghai stocks lost 5.6%, the most since October, after the Politburo signaled last Friday it will pare back support for the economy amid evidence of a recovery. China’s sovereign bonds, which are rapidly turning into Asia’s worst performers, also slumped.

Meanwhile, the yuan edged up after President Xi Jinping said his country won’t engage in currency depreciation. In overnight China news, President Trump suggested that Chinese President Xi will be visiting the White House soon. In other news, the US is considering concessions on drug protection in talks with China after the latter was said to offer 8 years of IP protections for biologics data vs. 12 years under current US law. SCMP subsequently reported that, Chinese President Xi could travel to the US to sign a trade deal as soon as June; if the two sides finalise a trade deal.

As Bloomberg notes, “it’s a pivotal moment for a world-beating rally in China that’s been underpinned by expectations of more stimulus and ample liquidity” noting that a barrage of earnings from the nation’s largest firms could swing sentiment either way, though the picture isn’t encouraging so far. Traders are also eyeing next week’s trade talks with the U.S., though the closure of China’s markets for a three-day holiday from Wednesday will likely dampen trading.

Meanwhile, back in the US, all eyes are on the U.S. GDP release which will be closely watched after a string of largely resilient data from an economy in its 10th year of expansion. A string of solid numbers has led analysts to revise up their forecasts for growth and the latest consensus estimate is for an annualized 2.3%, while the closely-watched GDP estimate of GDP from the Atlanta Federal Reserve is projecting an outcome of 2.7%, a huge turnaround from a few weeks ago when it was at 0.5%.

“A steady GDP reading will reinforce (stock) bulls’ appetite as worries over a recession will diminish but a potential miss may trigger some nervous profit-taking ahead of the weekend,” said Konstantinos Anthis, head of research at ADSS.

The GDP release will set the stage for the Fed interest rate decision next week, where investors will try to anticipate how the U.S. central bank will react to mostly resilient indicators of late. Yet the rebound has not been mirrored in inflation, which – according to the BLS – remains subdued across much of the developed world, prompting a host of central banks to turn dovish. Just this week central banks in Sweden and Canada have backed off plans to tighten, while the Bank of Japan tried to dispel doubts about its accommodative stance by pledging to keep rates at super-low levels for at least one more year. ECB Vice-President Luis de Guindos on Thursday opened the door to more money-printing if needed to boost inflation in the euro zone. Meanwhile, rate cuts look much likelier in Australia and New Zealand after recent disappointingly weak inflation reports.

In rates, Treasuries edged into the green alongside most European sovereign debt.

Elsewhere in currencies, the euro was off 1 percent for the week at $1.1136 as euro zone economic figures continued to disappoint, though it was 0.1 percent higher on the day. Against a basket of currencies, the dollar was 0.8 percent firmer for the week so far at 98.145 having touched its highest since May 2017.

In commodity markets, spot gold was 0.4 percent firmer at $1,281.81 per ounce. Oil prices dipped on Friday on expectations that producer club OPEC will soon raise output to make up for a decline in exports from Iran following a hardening of sanctions on Tehran by the United States.

. Expected data include 1Q GDP and University of Michigan Consumer Sentiment Index. American Airlines, AON, Chevron, Colgate-Palmolive, and Exxon are among companies reporting earnings

Market Snapshot

- S&P 500 futures down 0.2% to 2,922.00

- STOXX Europe 600 down 0.02% to 390.07

- MXAP down 0.08% to 162.00

- MXAPJ up 0.01% to 537.28

- Nikkei down 0.2% to 22,258.73

- Topix down 0.2% to 1,617.93

- Hang Seng Index up 0.2% to 29,605.01

- Shanghai Composite down 1.2% to 3,086.40

- Sensex up 0.6% to 38,977.58

- Australia S&P/ASX 200 up 0.05% to 6,385.65

- Kospi down 0.5% to 2,179.31

- German 10Y yield fell 1.3 bps to -0.022%

- Euro up 0.08% to $1.1141

- Italian 10Y yield rose 5.4 bps to 2.316%

- Spanish 10Y yield fell 0.9 bps to 1.082%

- Brent futures down 1.1% to $73.56/bbl

- Gold spot up 0.4% to $1,282.33

- U.S. Dollar Index down 0.1% to 98.11

Overnight Top News from Bloomberg

- Theresa May’s plan to stop Britain taking part in European elections in the middle of Brexit looks all but dead. The prime minister is unlikely to put her Brexit bill to Parliament next week, according to a government official

- Emmanuel Macron promised a new wave of tax cuts for France’s middle classes as he sought to placate Yellow Vest protesters and reinvigorate his flagging presidency.

- China won’t pursue yuan depreciation that harms others, President Xi Jinping says at Belt and Road forum in Beijing. Nation will keep yuan stable at reasonable and equilibrium level, he said

- The Trump administration may concede to a Chinese proposal that would give less protection for U.S. pharmaceutical products than they receive at home, according to people familiar with the matter, a move that could draw opposition from the American drug industry

- Japan’s factory output unexpectedly fell in March, raising the likelihood that gross domestic product shrank during the first quarter

- Oil is poised to notch an eighth weekly gain on the back of OPEC+ production cuts and as the U.S. moves to tighten sanctions against Iran

- Japan’s retail investors have propelled their net long yen positions against the dollar to near a record ahead of the nation’s extended Golden Week holidays

- North Korean leader Kim Jong Un used talks with Russian President Vladimir Putin to accuse the U.S. of “bad faith” in nuclear discussions, warning that the current detente on the Korean Peninsula was at risk

- Japan’s industrial production contracted by a surprisingly large amount in March as falling exports weigh on the world’s third- largest economy

- Chinese President Xi Jinping signaled his approval for Trump’s trade war demands in an address to some 40 world leaders where he pledged to address state subsidies, protect intellectual property rights, allow foreign investment in more sectors and avoid competitive devaluation of the yuan

- Wall Street is moving closer to modernizing the clubby $2 trillion market for new corporate bond issues while seeking to retain control of a lucrative business that’s being eyed by the tech sector

- The new Brexit Party started by anti-EU campaigner Nigel Farage is threatening the ruling Conservatives– and they aren’t even fighting back. Polls put the group on course to win the most votes in the EU elections next month

Asia-Pac risk sentiment was mostly downbeat as markets remained heavily focused on earnings releases and following the lacklustre performance of counterparts stateside. ASX 200 (Unch.) and Nikkei 225 (-0.2%) were both subdued with underperformance seen in Australia’s energy sector after a pullback in oil prices although losses in the broader market were only marginal and the index eventually recovered, while the Japanese benchmark was pressured amid a slew of earnings and following disappointing Industrial Production figures with participants also reducing exposure ahead of a 10-day closure for Golden Week. Elsewhere, Hang Seng (+0.2%) and Shanghai Comp. (-1.2%) opened lower as PBoC inaction resulted to a CNY 300bln liquidity drain for the week but with losses in Hong Kong later pared amid earnings including China Life Insurance which almost doubled its Q1 net from the prior year. Finally, 10yr JGBs are higher with prices underpinned by the mostly risk-averse tone and BoJ presence for JPY 480bln of JGBs in the belly.

Top Asian News

- Asian Chip Sector Shares Decline After Intel Cuts Outlook

- China Evergrande Is Said to Be Eyeing European Auto Acquisitions

- China’s Big Earnings Showdown Looms as Stocks Begin to Sink

- Sony Withdraws Some Profit Targets as Forecast Misses Estimates

- A Giant in China’s Equity Market Is Starting to Look Expensive

Major European indices are mixed but little changed overall [Euro Stoxx 50 +0.1%], with sectors portraying a similar scene; notably, the Oil & Gas sector is underperforming in-line with the recent downturn in oil prices and with sector heavyweights Total’s (-0.4%) broadly as expected earnings unable to counter the downward pressure. After an earning fuelled morning the FTSE 100 (-0.3%) is somewhat lagging its peers with the index weighed on predominantly by RBS (-4.4%) in-spite of the Co’s beat on Q1 profit before tax, as the Co. stated that the ongoing impact of Brexit uncertainty is likely to impact income growth in the near term. Glencore (-3.0%) and Just Eat (-3.2%) are also weighing on the FTSE 100 after the CFTC stated they are investigating if the Co’s units violated CFTC regulations and as UK Q1 orders increased by only 7.4% respectively. Other notable movers include Deutsche Bank (-3.0%) are lagging the Dax (+0.1%) after the Co. cut their FY19 sales outlook and they expect FY19 revenue to be flat. Elsewhere, Renault (+3.0%) posted Q1 revenue in-line with expectations and confirmed their guidance for FY19.

Top European News

- Continental Pushes Ahead With Powertrain Listing as Profit Drops

- Ferrexpo Slumps as Deloitte Resigns Amid Charity Probe

- Hydrogen as Replacement for Natural Gas Gets a Boost in U.K.

- Amundi Sees Investors Pull $7.7 Billion as DWS Stems Outflows

- Bayer’s CEO Faces Rebuke to Leadership as Shareholders Gather

In FX, the Kiwi and Swedish Krona are leading a comeback of sorts vs a still solid Greenback that is holding above the 98.000 handle in DXY terms and Fib support just shy of the big figure (97.961), with data providing respite for both G10 currencies in the form of NZ trade and Swedish retail sales. Nzd/Usd has subsequently extended its rebound through 0.6600 to just over 0.6650, with the added impetus of relatively upbeat rhetoric from RBNZ Orr overnight, while Eur/Sek has retreated further from post-Riksbank peaks and back below 10.6000 as the single currency lags amidst dovish remarks from ECB’s Rehn.

- AUD – Another major beneficiary of short covering and position paring in advance of US growth and PCE price gauges, as the Aussie recovers more ground from sub-0.7000 levels vs its US peer towards 0.7040, albeit still trading heavily on a Aud/Nzd cross basis under 1.0600 following weak Q1 CPI data earlier in the week that ramped up RBA easing expectations.

- EUR – As noted above, the Euro has been hampered to a degree by Rehn comments adding a bit more credence to sourced reports suggesting that some GC members are inclined towards shifting guidance on rate normalisation out further than the current end of 2019 or later to a BoJ-style next year. Hence, Eur/Usd’s bounce from yesterday’s new ytd low (circa 1.1116) has been stymied ahead of 1.1150 and decent option expiries stretching to 1.1160 (1.5 bn), while residual bids above 1.1100 may also be supplemented by hedging or buying interest linked to a total of 1 bn running off at the strike.

- GBP/CHF/CAD/JPY – All narrowly mixed vs the Usd as Cable pivots 1.2900 awaiting more Brexit developments and eyeing next week’s super BoE Thursday, while the Franc continues to straddle 1.0200 and meander between 1.1375-50 against the single currency in wake of yet another reminder from the SNB that NIRP and FX intervention are still warranted. The Loonie is still managing to hold above post-BoC lows and above 1.3500 even though crude prices are recoiling further from best levels in the run up to Canadian budget balances for February. Elsewhere, Usd/Jpy remains rangebound below 112.00 and just over chart support sub-111.40 in the form of the 30 DMA and a 61.8% Fib (at 111.37 to be precise), with the upside also capped by 1.1 bn option expiries from 112.00-20, and the impending long Japanese holiday still drawing attention as a potential hazard given the so called flash crash in currency and other markets when Japan was absent earlier this year.

- EM – A double-whammy for the Rouble on the aforementioned pronounced downturn in oil and with speculation that the CBR could take a lead from other Central Banks along a dovish policy path. Usd/Rub currently trading closer to the top of 64.8310-5630 parameters.

In commodities, Brent (-1.3%) and WTI (-1.3%) prices are firmly in the red with prices dropping below the USD 75/bbl and USD 65/bbl levels; notably, Brent had only reached the USD 75/bbl level yesterday for the first time this year. Iran’s crude oil exports from their Southern Ports have reportedly increased so far in April to 3.56mln BPD; specifically, regarding the Iranian oil waivers, Turkey are attempting to convince the US to allow Turpas to continue the purchase of oil from Iran. For reference, under the import waivers Turkey was permitted to import around 60kBPD of oil from Iran, and in December a total of around 54k BPD of oil was imported by Turkey from Iran. Elsewhere, following reports that a number of refineries had suspended the import of Russian oil from the Druzhba pipeline (1.2mln BPD) due to contamination issues, Russia has stated that the issues will be resolved from April 29th. However, reports indicate that some of the refineries that have suspended imports believe the problem will continue for another one or two weeks. Gold (+0.4%) prices have gradually moved higher across the session, benefitting from the cautious risk tone and concern ahead of Japan’s Golden Week holiday where markets will be closed for 10-days. Elsewhere, due to the softer dollar ahead of today’s GDP data, metal prices have retraced some of the prior session’s losses; and there were reports this morning of an explosion at Port Talbot, which is the UK’s largest steelworks. Tata Steel, who own the site, stated that there were no serious injuries and an investigation is ongoing.

US Event Calendar

- 8:30am: GDP Annualized QoQ, est. 2.3%, prior 2.2%

- 8:30am: Personal Consumption, est. 1.0%, prior 2.5%

- 8:30am: Core PCE QoQ, est. 1.4%, prior 1.8%

- 10am: U. of Mich. Sentiment, est. 97, prior 96.9; Current Conditions, prior 114.2; Expectations, prior 85.8

DB’s Craig Nicol concludes the overnight wrap

If the baton started with US equity markets hitting fresh record highs this week and then passed to the bond market on Wednesday, then it was the turn of EM to run the anchor leg yesterday following a day of relatively wild price action across assets.

Indeed broad EM FX slid as much as -0.59% before buyers stepped in during the New York session, arresting the broad declines and leaving the index close to flat by the end of play yesterday. A modest -0.04% decline was however still good for the fourth consecutive daily drop, with the index now down in 8 out of the last 10 sessions. Over that period, it has fallen -1.76%.Of the 24 most active EM currencies, 20 weakened versus the USD. This did however mask bigger declines for the likes of the Argentinian Peso (-2.43%) – which hit a new record low – and the Turkish Lira (-0.92%) which closed at 5.928 and the weakest since last October.In fact it was a rough day for assets in both of the countries. The Argentinian and Turkish equity markets dropped -0.64% and -1.71%, respectively, and 5y CDS spreads widened +26bps and +22bps. 10y hard currency bond yields rose 19.1bps in Turkey, but, somewhat puzzlingly and inconsistently with the action in other asset classes, 10y hard currency yields rallied off their intraday peaks to actually close -20.4bps lower in Argentina, completing an intraday swing of 72.3bps. More broadly the MSCI EM index closed -0.16% after trading down as much as -0.94% and this week has dropped -1.91%. That compares to a gain of +0.73% for the S&P 500. US HY spreads are a modest +3.3bps wider this week so there’s been little sign of the EM move spreading to credit so far.

That four-day move for the S&P 500 included a small -0.04% decline yesterday. In fairness there were some reasonable divergences on Wall Street yesterday with the NASDAQ (+0.21%) getting a boost from those Facebook and Microsoft results, while the DOW (-0.51%) got hit almost entirely due to a -12.95% drop for 3M following a disappointing set of results.Meanwhile the USD – which has been part of the reason for the weakness across EM recently – did at least ease off yesterday, closing flat. Treasuries also had a quieter day with 10y yields creeping up +1.4bps.

It’s worth jumping straight to Asia now where this morning the EM pain has seemingly hit the Nikkei (-0.68%), Shanghai Comp (-0.78%) and Kospi (-0.52%),with only the Hang Seng (+0.11%) posting a gain. Weak March industrial production data in Japan (-0.9% mom vs. +0.0% expected) is also playing a role. Asian FX is hanging in a little better, while the CNY (+0.12%) is slightly stronger after following a stronger than expected fix. President Xi Jinping also reiterated China’s commitment to keeping the currency stable by saying that China won’t engage in currency depreciation that harms other countries. Generally it’s the PBoC that make comments like this so it’s perhaps significant to come directly from the President, especially as he is chairing a number of economic committees.

Overnight, Bloomberg has also reported that the White House might concede to a Chinese proposal that would give less protection for the US pharma products in China (proposed 8 years) than they receive at home (12 years and new NAFTA 10 years). Elsewhere, Japan’s Finance Minister Taro Aso met with the US Treasury Secretary Steven Mnuchin as part of the ongoing trade talks with the US and said that Japan can’t agree to any talk of linking currency and trade policy while a Japanese Finance Ministry official said that he believes that talks concerning currency will be secondary to the trade talks between Economy Minister Toshimitsu Motegi and Lighthizer. President Trump and Japanese Prime Minister Shinzo Abe are due to meet today and are expected to discuss trade amongst other issues.

Turning back to yesterday’s US earnings, the highlights were a strong report by Amazon and a weak one from Intel. Amazon – who’s shares traded up just over 1% in extended trading – showed first quarter profits far above expectations, at $7.09 per share versus Bloomberg consensus expectation for $4.67, while revenues also grew strongly including a +47% gain in sales by Amazon Web Services, their cloud computing business. Strength in the same business line had boosted Microsoft earlier this week, with the software giant floating above a $1 trillion market capitalization in intraday trading before retreating slightly below that level. Intel – who’s shares dropped over 7% in extended trading – reported a 2.3% beat on profits, but lowered their full-year guidance markedly. Management now expects 2019 revenues to be around $69 billion, below consensus expectations for $71 billion. NASDAQ futures are little changed overnight as a result.

Back to yesterday and specifically some of the idiosyncratic stories in Turkey and Argentina. The Turkish Lira really got moving post the Central Bank of Turkey meeting where, although policy was left unchanged, the Bank dropped a commitment to tighten policy further if needed, saying that the action “will be determined to keep inflation in line with the targeted path”. By the way, inflation in Turkey is running just below 20%. Meanwhile in Argentina the story appears to be one of a negative feedback look between political uncertainty, out of control inflation, and the weakening Peso.The closing level on Argentina’s 5y CDS yesterday now implies a 59% probability of default. Bonds maturing in 2 years were at one stage yielding over 20% yesterday. Back in February the same bonds were trading at ‘just’ 8%.

A reminder that it was declining EM growth expectations last year which eventually filtered through to weakness in broader DM markets, so it’s worth seeing if we get a continuation of this price action in the near term.

In the meantime it’s likely that today’s first look at Q1 GDP for the US will do nothing but highlight the DM/EM growth divergence. Our economists expect a +2.6% qoq/saar reading (full preview here ) which is above the market consensus of +2.3%. For what it’s worth the range of expectations for that consensus reading is from as low as +1.0% to as high at +2.9%, with the Atlanta Fed’s tracker at +2.7%. A reminder that Q4 came in at +2.2%. The last piece of data which could have helped fine-tune today’s growth expectations – the preliminary March durable and capital goods orders data – came in above market. Core capex orders printed at +1.3% mom versus expectations for +0.2% while durable orders ex transport rose +0.4% mom (vs. +0.2% expected). Both series were also revised higher in prior months as well.

The other data that was released yesterday included the latest weekly claims reading which revealed a surprisingly 37k uptick to 230k (vs. 200k expected).However, one-offs appeared to be in play again with strikes at New England supermarkets flagged as a reason behind the spike. Lastly the Kansas City Fed manufacturing survey for April fell to 5 from 10, remaining in positive territory for the 29thconsecutive month, the longest streak since February 2008.

In Europe there were no data releases with earnings still the main driver.Swedish industrial firm Atlas Copco (+5.01%) reported strong first quarter figures including surprisingly high new orders. Bank earnings were hit or miss, as UBS (+1.23%) gained but Barclays (-3.59%) lagged. The former attracted new inflows and announced the resumption of its buyback program, while the latter reported softer-than-expected figures for both its revenues and capital ratio. Spanish utilities firm Iberdrola (+4.30%) also outperformed after profits grew 12%, which explained just about all of the IBEX’s gain yesterday, as the index advanced +0.47% while the DAX and CAC slid -0.25% and -0.33%, respectively. Italy’s benchmark index traded flat, but BTP yields rose +5.5bps, possibly reflecting some anxieties ahead of today’s S&P ratings review.

Elsewhere in Europe, the Swedish Riksbank was the latest central bank to strike a surprisingly dovish tone, sending the krona to its weakest level versus the dollar since 2002.The central bank noted softer inflation and the weaker outlook for employment, and opened the door to the possibility that they do not hike rates at all this year, whereas the market had priced in one hike. Somewhat in parallel, ECB Vice President de Guindos said that he “cannot be super optimistic” about the European economy, which helped the euro to a -0.21% loss versus the dollar.

Over in the US, former Vice President Joe Biden officially launched his presidential campaign yesterday. He is viewed as more moderate than most of the rest of the Democratic field and has consistently polled at the top of the pack. It remains to be seen if he can maintain his initial strong position as the grind of the campaign accelerates.

Looking at the full day ahead, this morning the only data of note is more CBI survey data out of the UK. The focus then turns to that Q1 GDP print in the US while the final April University of Michigan consumer sentiment survey revisions follows. Away from that GDP print in the US the other potentially market sensitive event is a meeting between Japanese PM Abe and President Trump at the White House. Russian President Putin is also travelling to China to meet with President Xi Jinping while the earnings highlights include Exxon Mobil, Chevron, Total and Sanofi. Finally, S&P are due to complete their review of Italy’s BBB/Negative credit rating today.

end

3. ASIAN AFFAIRS

i)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 37.43 POINTS OR 1.20% //Hang Sang CLOSED UP 55.21 POINTS OR 0.19% /The Nikkei closed DOWN 48.85 POINTS OR 0.22%/ Australia’s all ordinaires CLOSED UP /04%

/Chinese yuan (ONSHORE) closed UP at 6.7359AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 64.03 dollars per barrel for WTI and 72.83 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 6.7359 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7446/ TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

China/

4/EUROPEAN AFFAIRS

GERMANY/DAIMLER

The automobile industry in Europe is in shambles led by Germany. Daimler is stung by falling Mercedes sales.

(courtesy zerohedge)

Daimler Stung By Falling Mercedes Sales Amid Continuing Global Auto Recession

The global auto industry, which has been grinding to a painful slowdown for the better part of the last two years, just claimed its latest victim. On Friday, German auto giant Daimler AG said that its guidance is going to be harder to achieve after a rough start to 2019, forcing it to try to cut costs, according to Bloomberg.

Daimler saw its first quarter profit tumble 16% due to a decline in deliveries mixed with the rising cost of developing new models. Even though earnings met analyst estimates, CEO Dieter Zetsche said the quarter fell short of the company’s expectations and had tempered outlook for the future.

“Achieving the financial targets for 2019 has not become easier since the first quarter,” Zetsche said Friday.

Like many car companies, Daimler is dealing with slower sales in the United States and Europe while maintaining significant costs associated with investing in electric vehicles. Other automakers saw similar rocky starts to the first quarter. Renault reported a 4.8% drop to Q1 revenue and Nissan Motor said earlier this week it would miss its annual profit goal.

Back in February, Daimler had already said it was looking to cut costs in order to offset falling profits. A 5.6% drop in Mercedes-Benz deliveries through March had been another negative headwind that the company has faced. The company offered little additional detail on Friday on its plans to reverse a profitability decline in its main cars unit. Despite Mercedes-Benz holding up in China, the country is mired in a broader slump that makes the environment for a profound turnaround difficult.

Investors are looking forward to incoming CEO Ola Kallenius taking over in May, according to Bloomberg Intelligence analyst Michael Dean. “We anticipate his new strategic plan will be unveiled this summer,” Dean said.

Daimler says it still expects its earnings to “rise slightly” this year. Shares were down about 1% trading in Frankfurt on the news on Friday. After a an ugly 2018, the stock is up 25% since the beginning of the year. Jefferies analyst Philippe Houchois said the outlook for the company “seems slightly optimistic given the weak start of the year.”

CFO Bodo Uebber said that business is expected to improve during the second half of the year. He added that currency headwinds have also worked against the company. These currency headwinds are forecast to cut between €500 million and €1 billion from earnings this year.

Restructuring moves and efficiency measures “will hopefully push the cars unit margin back to between 8% and 10% and trucks to between 7% and 9% by 2021,” according to the CFO. He declined to elaborate more on what cutbacks the company is making.

The company is reportedly also considering a reduction of about 10,000 jobs through voluntary measures as part of a €6 billion savings target. Outgoing CEO Zetsche said that a weak first quarter margin in the cars unit was due to the cost of upgrading the GLE sport utility vehicle and a joint venture in Mexico with Nissan. High inventory levels resulted in negative cash flow of €2 billion compared to a positive €1.8 billion in the first quarter of last year for the company.

Evercore ISI analyst Arndt Ellinghorst said:

“Daimler is blaming supplier bottlenecks and quality issues pretty much across all divisions for its poor financial performance. To be clear: it is management’s job to manage its supply chain and relationships with partners. Other companies do not complain about similar issues.”

Well, except Tesla of course…

Going forward, Daimler slashed its margin guidance for its vans unit, which swung to a loss in the first quarter, to between 0% and 2%. Previously, the company had targeted a return on sales between 5% and 7%, but expenses associated with cutting capacity in Argentina and Russia, as well as building a new U.S. factory, have weighed on these targets.

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

6.GLOBAL ISSUES

7 OIL ISSUES

Down goes oil after Trump called OPEC to tell them oil/gas prices are too high

(courtesy zerohedge)

Oil Tumbles After Trump Says “He Called OPEC, Gas Prices Are Coming Down”

WTI crude futures have tumbled back to a $63 handle, breaking a key technical support, following President Trump comments that he has called OPEC and “gasoline prices are coming down.”

The last 107 days have seen an almost unprecedented surge in gas prices in America…

And Trump’s comments seems to have taken some shine off the mega crude bull…

This has taken oil prices back below the key retracement level…

Additionally, ABN Amro Senior Energy Economist Hans van Cleef writes in a report today that crude oil looks “toppish around current levels” as there is enough supply growth from other nations to offset any drop in Iranian crude output.

end

8. EMERGING MARKETS

ARGENTINA

.

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:00 AM….

Euro/USA 1.1137 UP .0002 REACTING TO MERKEL’S FAILED COALITION/ REACTING TO +GERMAN ELECTION WHERE ALT RIGHT PARTY ENTERS THE BUNDESTAG/ huge Deutsche bank problems ///ITALIAN CHAOS /AND NOW ECB TAPERING BOND PURCHASES/JAPAN TAPERING BOND PURCHASES /USA RISING INTEREST RATES /FLOODING/EUROPE BOURSES /GREEN EXCEPT LONDON

USA/JAPAN YEN 111.77 UP .223 (Abe’s new negative interest rate (NIRP), a total DISASTER/NOW TARGETS INTEREST RATE AT .11% AS IT WILL BUY UNLIMITED BONDS TO GETS TO THAT LEVEL…

GBP/USA 1.2903 UP 0.0009 (Brexit March 29/ 2019/ARTICLE 50 SIGNED/BREXIT FEES WILL BE CAPPED/BREXIT EXTENDED TO OCT 31/2019//

USA/CAN 1.3485 UP .0006 CANADA WORRIED ABOUT TRADE WITH THE USA WITH TRUMP ELECTION/ITALIAN EXIT AND GREXIT FROM EU/(TRUMP INITIATES LUMBER TARIFFS ON CANADA/CANADA HAS A HUGE HOUSEHOLD DEBT/GDP PROBLEM)

Early THIS FRIDAY morning in Europe, the Euro FELL by 26 basis points, trading now ABOVE the important 1.08 level FALLING to 1.1128 Last night Shanghai COMPOSITE CLOSED DOWN 37.43 POINTS OR 1.20%.

//Hang Sang CLOSED UP 55.21 POINTS OR 0.19%

/AUSTRALIA CLOSED UP .04%// EUROPEAN BOURSES //MOSTLY /GREEN

The NIKKEI: this FRIDAY morning CLOSED DOWN 48,85 POINTS OR 0.22%

Trading from Europe and Asia

1/EUROPE OPENED MOSTLY GREEN/EXCEPT LONDON

2/ CHINESE BOURSES / :Hang Sang CLOSED UP 55.21 POINTS OR 0.19%

/SHANGHAI CLOSED DOWN 37,43 POINTS OR 1.20%

Australia BOURSE CLOSED UP .04%

Nikkei (Japan) CLOSED DOWN 48.85 POINTS OR 0.22%

INDIA’S SENSEX IN THE GREEN

Gold very early morning trading: 1280.95

silver:$15.00

Early FRIDAY morning USA 10 year bond yield: 2.52% !!! DOWN 1 IN POINTS from THURSDAY’S night in basis points and it is trading WELL ABOVE resistance at 2.27-2.32%.

The 30 yr bond yield 2.94 DOWN 1 IN BASIS POINTS from THURSDAY night.

USA dollar index early WEDNESDAY morning: 98.13 DOWN 7 CENT(S) from THURSDAY’s close.

This ends early morning numbers FRIDAY MORNING

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now your closing FRIDAY NUMBERS \12: 00 PM

Portuguese 10 year bond yield: 1.13% DOWN 6 in basis point(s) yield from THURSDAY/

JAPANESE BOND YIELD: -.04% DOWN 1 BASIS POINTS from THURSDAY/JAPAN losing control of its yield curve/

SPANISH 10 YR BOND YIELD: 1.03% DOWN 6 IN basis point yield from THURSDAY

ITALIAN 10 YR BOND YIELD: 2.58 DOWN 11 POINTS in basis point yield from THURSDAY/

the Italian 10 yr bond yield is trading 155 points HIGHER than Spain.

GERMAN 10 YR BOND YIELD: FALLS -.02% IN BASIS POINTS ON THE DAY//

THE IMPORTANT SPREAD BETWEEN ITALIAN 10 YR BOND AND GERMAN 10 YEAR BOND IS 2.60% AND NOW ABOVE THE THE 3.00% LEVEL WHICH WILL IMPLODE THE ENTIRE ITALIAN BANKING SYSTEM. AT 4% SPREAD THERE WILL BE A MASSIVE BANK RUN…

END

IMPORTANT CURRENCY CLOSES FOR FRIDAY

Closing currency crosses for FRIDAY night/USA DOLLAR INDEX/USA 10 YR BOND YIELD/1:00 PM

Euro/USA 1.1157 UP .0020 or 20 basis points

USA/Japan: 111.59 UP 0.045 OR YEN DOWN 5 basis points/

Great Britain/USA 1.2936 UP .0041 POUND UP 41 BASIS POINTS)

Canadian dollar UP 25 basis points to 1.3455

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx