GOLD: $1277.50 UP $0.05 (COMEX TO COMEX CLOSING)

Silver: $14.93 DOWN 4 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1277.50

silver: $14.95

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 249//295

EXCHANGE: COMEX

CONTRACT: APRIL 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,275.500000000 USD

INTENT DATE: 04/24/2019 DELIVERY DATE: 04/26/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 1

661 C JP MORGAN 249

686 C INTL FCSTONE 3

737 C ADVANTAGE 85 45

880 H CITIGROUP 200

905 C ADM 7

____________________________________________________________________________________________

TOTAL: 295 295

MONTH TO DATE: 6,902

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 295 NOTICE(S) FOR 29500 OZ (0.9175 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 6607 NOTICES FOR 660700 OZ (20.550 TONNES)

SILVER

FOR APRIL

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 775 for 3,875,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE :$5409 DOWN $6

Bitcoin: FINAL EVENING TRADE: $5465 UP 48

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL A STRONG SIZED 4851 CONTRACTS FROM 219,113 DOWN TO 214,262 DESPITE YESTERDAY’S 15 CENT RISE IN SILVER PRICING AT THE COMEX. AS I PROMISED YOU, WE DID HAVE OUR CUSTOMARY LIQUIDATION OF SPREADERS WITH TODAY READING. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR MARCH, 0 FOR APRIL, 2218 FOR MAY, 0 FOR JUNE 240 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 2458 CONTRACTS. WITH THE TRANSFER OF 2458 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2458 EFP CONTRACTS TRANSLATES INTO 12.29 MILLION OZ ACCOMPANYING:

1.THE 15 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

AND NOW 3.880 MILLION OZ STANDING FOR SILVER IN APRIL.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

33,048 CONTRACTS (FOR 18 TRADING DAYS TOTAL 33,048 CONTRACTS) OR 165.24 MILLION OZ: (AVERAGE PER DAY: 1836 CONTRACTS OR 9.180 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAR: 165.24 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 23.60% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 733.04 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4851 DESPITE THE 15 CENT FALL IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2458 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS RESUMED THEIR LIQUIDATION OF THE SPREAD TRADES TODAY.

TODAY WE LOST A CONSIDERABLE SIZED: 2393 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2458 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 4851 OI COMEX CONTRACTS. AND ALL OF THIS LOSS OF DEMAND HAPPENED WITH A 15 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $14.97 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.095 BILLION OZ TO BE EXACT or 157% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR nil OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ AND NOW APRIL AT 3.880 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 1811 CONTRACTS, TO 441,859 WITH THE RISE IN THE COMEX GOLD PRICE/(A GAIN IN PRICE OF $6.00//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY STRONG SIZED 8646 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 8648 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 441,736. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,457 CONTRACTS: 1811 OI CONTRACTS INCREASED AT THE COMEX AND 8648 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 10,457 CONTRACTS OR 1,045,700 OZ OR 32.52TONNES. YESTERDAY WE HAD A GAIN IN THE PRICE OF GOLD TO THE TUNE OF $6.00.…AND YET WITH THAT RISE, WE HAD A VERY STRONG GAIN IN TONNAGE OF 32.52 TONNES!!!!!!.??????????????????????????????????????????

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 126,328 CONTRACTS OR 12,632,800 OR 392.93 TONNES (18 TRADING DAYS AND THUS AVERAGING: 6922 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAYS IN TONNES: 392.93 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 392.93/3550 x 100% TONNES =10.31% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1766.32 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 1811 WITH THE GAIN IN PRICING ($6.00) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8646 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 8646 EFP CONTRACTS ISSUED, WE HAD A VERY STRONG GAIN OF 11,334 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

8646 CONTRACTS MOVE TO LONDON AND 1811 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 32.52 TONNES). ..AND THIS STRONG DEMAND OCCURRED WITH A RISE IN PRICE OF $6.00 IN YESTERDAY’S TRADING AT THE COMEX.

we had: 295 notice(s) filed upon for 29,500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $0.05 TODAY

WE HAD NO INVENTORY CHANGES AT THE GLD//

INVENTORY RESTS AT 747.87 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 4 CENTS TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLSV//

/INVENTORY RESTS AT 311.979 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A STRONG SIZED 4851 CONTRACTS from 219,113 DOWNTO 214,262 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..TODAY,IT LOOKS LIKE OUR SPREADERS RESUMED ITS LIQUIDATION WHERE THEY LEFT OFF THE DAY BEFORE.

HERE IS HOW THE CROOKS USED SPREADING AS WE ENTER AN ACTIVE DELIVERY MONTH. THUS SILVER HAS THE ACTIVE MONTH OF MAY COMING UP AND THUS SPREADERS DO THE FOLLOWING:

“YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF APRIL BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 2218 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 240 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2458 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 4851 CONTRACTS TO THE 2458 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG SIZED LOSS OF 2393 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 11.965MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH. AND NOW 3.880 MILLION OZ FOR APRIL.

RESULT: A STRONG SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 15 CENT RISE IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 2458 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 77.79 POINTS OR 2/43% //Hang Sang CLOSED DOWN 256.03 POINTS OR 0.86% /The Nikkei closed UP 107.78POINTS OR 0.48%/ Australia’s all ordinaires CLOSED HOLIDAY

/Chinese yuan (ONSHORE) closed DOWN at 6.7449 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 66/11 dollars per barrel for WTI and 5.19 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.7449 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7537/ TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA/ SOUTH KOREA

SOUTH KOREA

Export dynamo sees their economy unexpectedly plunge by the most in a decade. Its GDP unexpectedly shank in Q1 dropping .3% Q/Q

( zerohedge)

b) REPORT ON JAPAN

Japan

3 China/Chinese affairs

i)China/

4/EUROPEAN AFFAIRS

i)Deutsche bank/Commerzbank

ii)FRANCE//CHRISTIANITY

The burning of Notre Dame and how France is leading in the destruction of Christian Europe. Mosques on the rise..churches are empty and their buildings are falling apart

( Guy Milliere/Gatestone)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

iii)Iran/uSA

Iran warns the USA not to engage with Iran at the Straits of Hormuz. That will never happen. This is going to flare up

( zerohedge)

6. GLOBAL ISSUES

i)SWEDEN

QE will continue in Sweden and that sent the Krona crashing. The central bank has now delayed rate hikes

(courtesy zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

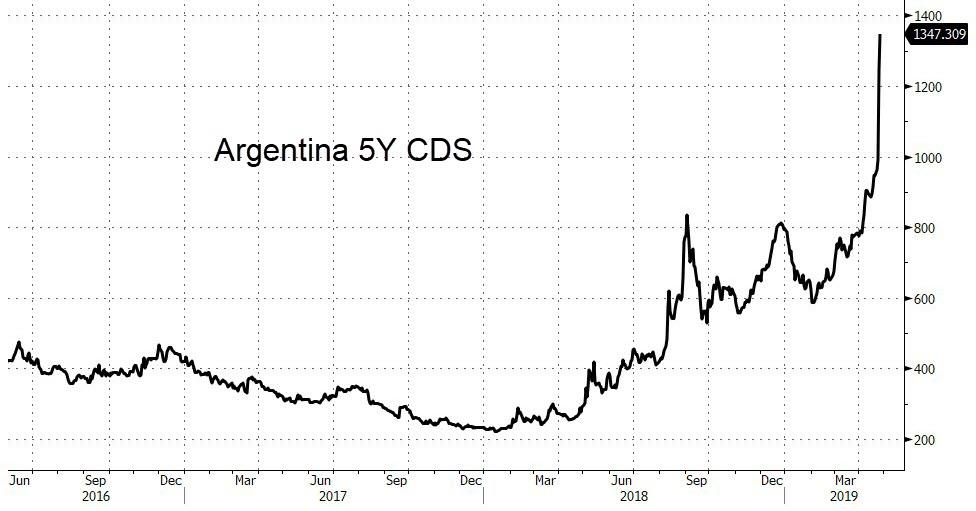

Argentina

(courtesy zerohedge)

9. PHYSICAL MARKETS

i

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning/TRADING

ii)Market data

i)Durable goods orders still weak

( zerohedge)

ii)The initial jobless claims turned on a dime: it surged the most in 18 months.

( zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

A good look at the deteriorating conditions inside one of the richest cities in the USA: San Francisco

( zerohedge)

SWAMP STORIES

I)Barr to give testimony to the senate on the Mueller report next Wednesday.

( zerohedge)

ii)Joe DiGenova is one of the smartest lawyers around. He explains where the Russian hoax is headed

Let us head over to the comex:

AFTER APRIL, WE HAVE THE ACTIVE DELIVERY MONTH OF MAY AND HERE THE OI FELL BY 15,264 CONTRACTS DOWN TO 44,613. CONTRACTS.. THE NEXT MONTH OF JUNE GAINED 5 CONTRACTS TO 336. AFTER JUNE, THE VERY BIG DELIVERY MONTH OF JULY HAD A GAIN OF 9736 CONTRACTS UP TO 126,942 CONTRACTS.

Gold withdrawals;

i) we had one withdrawal from HSBC and it was a biggy: 88,023.03 oz

Venezuela Sells $400 Million Worth Of Gold Bullion

Strengths

- The best performing metal this week was palladium, up 3.52 percent as CPM Group noted that the price could climb to $1,800 on supply constraints. Gold traders and analysts switched from bullish to mostly neutral or bearish on the yellow metal this week, according to the weekly Bloomberg survey.

- Turkey’s gold reserves reversed this week by rising $227 million from the previous week. The central bank’s holdings are now worth $20.9 billion as of April 12, according to official figures. Kazakhstan also increased its gold holdings to 11.63 million ounces in March, up from 11.46 million in February. Mexico, too, raised gold reserves by 3.86 million ounces last month.

- Bloomberg’s Cormac Mullen writes that currency traders should get ready for a big move in the dollar, if past periods of low volatility are a guide. Over the last 25 years, there have been three previous troughs in the JPMorgan Global FX Volatility Index, and each time the U.S. Dollar Index has moved around 10 percent over the subsequent six months, according to Bloomberg data. A weaker U.S. dollar has historically been positive for the gold price as the two trade inversely.

Weaknesses

- The worst performing metal this week was gold, down 1.13 percent. The yellow metal tumbled to its lowest since January on Tuesday morning just as the market opened after someone dumped 11,000 gold futures contracts, worth around $1.5 billion, into the market. Traders were said to be using the F-word—“fiduciary.” Who recklessly dumps so many contracts unless their motive is to drive the price down?

- Gold is headed for its fourth weekly drop – the longest run of weekly declines in eight months – amid speculation that the U.S. and China are nearing a trade deal. Bloomberg writes that better-than-expected first quarter growth and March industrial production for China weighed on gold prices. The data eased concerns about a slowdown in global growth that rattled investors.

- Holdings in the SPDR Gold Shares fund fell to its lowest since October on Tuesday, which also happens to be the same day that gold gave up all its 2019 gains. Unexpectedly strong data from emerging markets, and China in particular, helps explain gold’s slip as investors are turning away from safe haven assets. Japan’s largest bullion retailer, Tanaka Kikinzoku Kogyo K.K., said that first quarter sales of gold bars fell 33 percent year-over-year and platinum bars also fell 34 percent.

Opportunities

- Federal Reserve Chairman Jerome Powell has made an important shift in strategy for dealing with inflation, in a prelude to what could be a more radical change next year, writes Bloomberg’s Rich Miller and Craig Torres. “The Fed is evolving to a ‘white-of-the-eyes’ approach in terms of inflation” under which it won’t hike rates until price rises accelerate, said Stephen Stanley, chief economist at Amherst Pierpont Securities. Higher inflation is typically good for gold.

- Rio Tinto, the world’s second biggest miner, released a statement last week saying that it will only work with groups aligned with its own climate principals and pledged to become a “greener” miner. Mining.com writes that “Rio Tinto has effectively put mining industry lobby groups on notice that they need to adapt to a world in which the challenge of climate change is recognized and that mining should be a positive force for change.”

- According to a joint statement, ICBC and the World Gold Council are partnering to develop the Chinese gold market. The two groups will leverage online technology and ICBC’s platform advantages to design and develop new gold products and services for millennials in particular.

Threats

- Venezuela managed to sell as much as $400 million, or nearly 9 tons, in gold with sanctions in force, somehow skirting international sanctions. The sale not only means President Maduro has found a way to sidestep the economic blockage, but it also may have contributed to the drop in gold price this week, according to some analysts. “Of course [the sale] impacts the gold price,” RBC Wealth Management managing director George Gero told Kitco News. “Anytime you have a large supply overhanging the market, it impacts trading. It did not help attract buyers.”

- Gold demand has been supported lately by the idea that global output could begin to roll over on higher operating costs and the lack of large discoveries. However, it doesn’t look as if “peak gold” has arrived just yet. Output is expected to rise to 109.6 million ounces this year, an increase of 2.1 percent more than in 2018, according to S&P Global Market Intelligence. This will be “the strongest growth in the past three years, debunking commentary calling for peak gold,” analyst Christopher Galbraith told Bloomberg. Galbraith added that more than half of the increase “is projected to come from new mines that are expected to come on stream this year or have recently commissioned.”

- For the past two decades, U.S. corporate profits have widened on average, but this is unlikely to last much longer. According to a note by Bridgewater Associates’ Greg Jensen, “some of the forces that supported margins over the last 20 years are unlikely to provide a continued boost.” This could lead to a major valuation problem, Jensen says, adding that incentives for offshore production have been reduced “as global labor costs have moved closed to equilibrium, with domestic costs and rising trade conflict increasing the risk of offshoring, while the potential tax rate arbitrage from moving abroad is now much smaller.” As a result, it could be challenging for companies to maintain profitability levels over the next several years, let alone widen margins further.

News & Commentary

Gold ends higher as the U.S. stock market pauses its rally (ForexTv.com)

Gold prices inch up off 4-month low, still pressured by strong dollar (Reuters.com)

Bank of Canada cuts growth forecast, abandons talk of rate hikes (Reuters.com)

U.S. yields lower on soft global data, after strong auction (Reuters.com)

SWOT Analysis: Venezuela Liquidated $400 Million in Gold Last Week (GoldSeek.com)

Annual silver production surveys fail to address market manipulation – Butler (24HGold.com)

Gold futures smashes at odds with fundamentals – John Ing (KingWorldNews.com)

Paper gold raid and fake financial journalism (InvestmentResearchDynamics.com)

Gold Prices (LBMA PM)

24 Apr: USD 1,273.80, GBP 984.90 & EUR 1,135.34 per ounce

23 Apr: USD 1,273.45, GBP 979.67 & EUR 1,131.46 per ounce

18 Apr: USD 1,276.50, GBP 981.12 & EUR 1,134.17 per ounce

17 Apr: USD 1,276.10, GBP 978.77 & EUR 1,127.82 per ounce

16 Apr: USD 1,283.75, GBP 981.30 & EUR 1,137.40 per ounce

Silver Prices (LBMA)

24 Apr: USD 14.80, GBP 11.44 & EUR 13.21 per ounce

23 Apr: USD 14.97, GBP 11.51 & EUR 13.31 per ounce

18 Apr: USD 15.00, GBP 11.49 & EUR 13.27 per ounce

17 Apr: USD 15.00, GBP 11.49 & EUR 13.27 per ounce

16 Apr: USD 14.94, GBP 11.42 & EUR 13.22 per ounce

Recent Market Updates

– World’s Central Banks Want More Gold – India May Buy 1.5M Ounces In 2019

– Russia’s 2019 Gold Rush Continues: Buys 600,000 Ounces of Gold In March

– When Should You Sell Your Gold and Silver? (GoldCore Video)

– Understanding Gold: A Step By Step Guide To Gold As An Asset Class

– World Trade Suffers Biggest Collapse Since Financial Crisis

– Exclusive Offer: Secure Gold and Silver Storage In Zurich For Free For Six Months

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

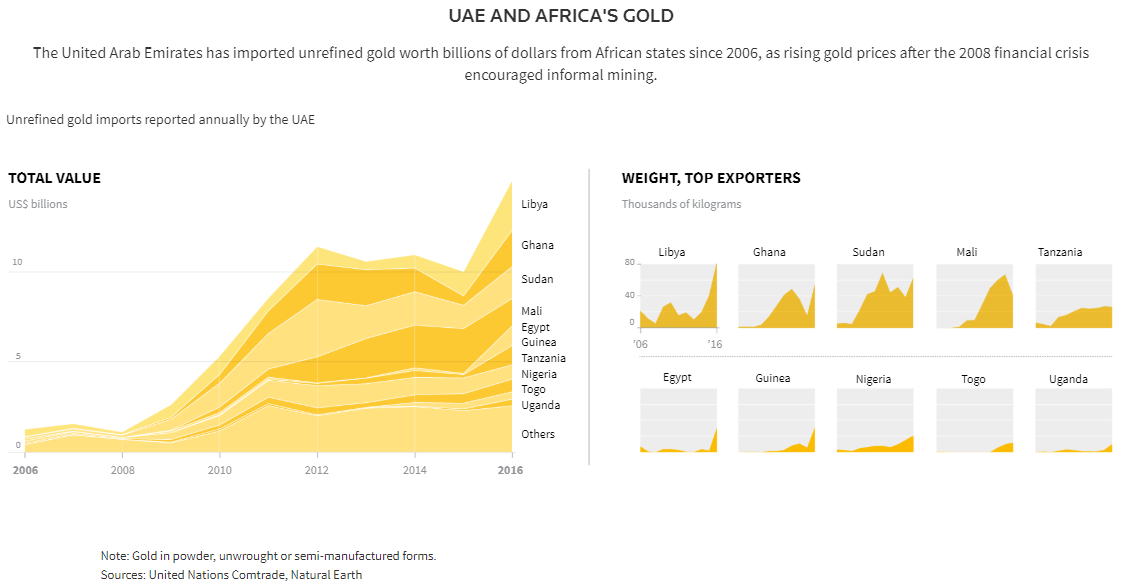

Reuters purports to be concerned that Africa is being cheated out of its gold

Submitted by cpowell on Wed, 2019-04-24 17:01. Section: Daily Dispatches

If Reuters is suddenly really so concerned about Africa’s being cheated out of its gold, why doesn’t the news agency investigate the international central bank gold price suppression scheme? Most of the work for such investigative journalism already has been done here:

http://gata.org/taxonomy/term/21

All the news agency would have to do is call a few central banks to collect their refusals to account for themselves.

* * *

Gold Worth Billions Is Smuggled Out of Africa

By David Lewis, Ryan McNeill, and Zandi Shabalala

Reuters

Wednesday, April 23, 2019

Billions of dollars’ worth of gold is being smuggled out of Africa every year through the United Arab Emirates in the Middle East — a gateway to markets in Europe, the United States, and beyond — a Reuters analysis has found.

Customs data shows that the UAE imported $15.1 billion worth of gold from Africa in 2016, more than any other country and up from $1.3 billion in 2006. The total weight was 446 tonnes, in varying degrees of purity, up from 67 tonnes in 2006.

…

Much of the gold was not recorded in the exports of African states. Five trade economists interviewed by Reuters said this indicates large amounts of gold are leaving Africa with no taxes being paid to the states that produce them.

Previous reports and studies have highlighted the black-market trade in gold mined by people, including children, who have no ties to big business, and dig or pan for it with little official oversight. No one can put an exact figure on the total value that is leaving Africa. But the Reuters analysis gives an estimate of the scale. …

… For the remainder of the report:

https://www.reuters.com/investigates/special-report/gold-africa-smugglin…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

This is something!! The Government of India is learning from its citizens..they are now acquiring gold

(Bloomberg/GATA)

Even the Reserve Bank of India is acquiring gold now

Submitted by cpowell on Wed, 2019-04-24 19:57. Section: Daily Dispatches

World’s Central Banks Want More Gold

By Ranjeetha Pakiam and Swansy Afonso

Bloomberg News

Wednesday, April 24, 2019

India’s central bank is likely to join counterparts in Russia and China scooping up gold this year, adding to its record holdings and lending support to worldwide bullion demand as top economies diversify their reserves.

The Reserve Bank of India’s purchases are part of a wider picture across developing economies that are looking at de-dollarizing their foreign-exchange reserves, according to Ross Strachan at Capital Economics Ltd. The RBI’s buying trend can be sustained for a number of years in relatively small quantities, as part of a long-term diversification, he said.

…

The RBI may purchase 1.5 million ounces in 2019, or about 46.7 tons, according to Howie Lee, an economist at Oversea-Chinese Banking Corp., with an outlook based on extrapolating amounts bought in the first two months of this year. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-04-23/central-bank-gold-buy…

END

John Ing believes (and so do I) that Basel III is the key catalyst that is causing central banks to purchase gold. No question that the leader in the purchasing dept. is China

(courtesy Kingworldnews/John Ing/GATA)

Gold futures smashes at odds with fundamentals, John Ing tells King World News

Submitted by cpowell on Wed, 2019-04-24 20:05. Section: Daily Dispatches

4p ET Wednesday, April 24, 2019

Dear Friend of GATA and Gold:

Recent smashes in the gold futures market don’t reflect the monetary metal’s fundamentals, gold market analyst John Ing tells King World News this week. With central banks aggressively buying, the Bank for International Settlements proclaiming gold as good as cash and government bonds, and gold miners acquiring each other, Ing says, the metal seems to be a bargain at the moment. Ing’s comments are posted at KWN here:

https://kingworldnews.com/legend-connected-in-china-at-the-highest-level…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Legend Connected In China At The Highest Levels Says Basel III Is Fueling Massive Central Bank Gold Buying//

Russia & China Buy As Gold Market Raids Continue

April 24 (King World News) – John Ing: “Gold is hitting some important technical levels after being hit in the last ten days by two dumps of 11,000 contracts on the downside. That has taken the steam out of a rally that I believe was going to test that $1,325 level…

Insiders Buying

Meanwhile, Russia and China have been buying gold. In fact, China has been buying gold four months in a row. So there has been this continued physical offtake, and this decline in the price of gold has nothing to do with fundamentals. And you see the continued merger and acquisition activity in the gold mining sector, which included Newmont and Barrick making peace by setting up a joint venture in Nevada. So when you see central bank buying — they are the biggest insiders — and then you see the gold industry themselves buying each other, that’s telling me that prices today are very attractive.

Large Investors Also Buying

And, Eric, when I talk to large investors, they have not been selling. In fact, they have been buying on these pullbacks in the high-quality names in the mining sector. Rob McEwen has been talking about how attractive the valuations are in the mining sector right now, so that tells you how undervalued the space is at this time.”

Eric King: “What about all of this central bank buying of gold that you mentioned?”

John Ing: “China is the largest producer of gold in the world and yet they keep importing gold. On top of that the world is facing peak gold production, where production will be declining dramatically for many years to come. And countries are watching the dollar constantly being debased, which is why China, Russia, and many other countries continue to buy gold…

Russia has dumped US Treasuries and they have now become the 5th largest holder of gold in the world. China is following suit, becoming the 6th largest holder of gold in the world. This is after four consecutive months of buying. Every month China seems to be buying significant quantities of gold in London. And we know that the Shanghai Gold Exchange is the largest physical gold market in the world. So China is well on its way to rivaling the United States with its 8,000 tonnes of gold.

Basel III Fueling Massive Central Bank Gold Purchases

And of course with Basel III, which was just enacted, gold can now be margined at 100%. This will serve to continue to drive physical demand for gold by central banks. This central bank buying is not only very real, it’s very aggressive. It’s the highest pace of buying in 50 years, since the US essentially went off the gold standard.”

end

The following story is quite interesting..a new startup back is being refused the free money of central bank reserves and they are taking them to court

(courtesy Bloomberg./GATA)

Fed wants to restrict premium interest rate to its pals

Submitted by cpowell on Wed, 2019-04-24 20:14. Section: Daily Dispatches

The Fed Fights a New Bank It Fears, While the Startup Sees Nothing to Worry About

By Alex Harris and Liz McCormick

Bloomberg News

Wednesday, April 24, 2019

The Federal Reserve is trying to kill a fledgling bank before the newfangled business takes root, arguing it’s a dangerous idea. The nascent company says there’s no reason to fret about its plan to give big investors access to the central bank’s highest interest rates.

Figuring out who’s right is no easy task.

…

James McAndrews, once the New York Fed’s director of research, created the bank in 2016, hoping to give pensions, insurers, and other large institutional investors higher yields on their cash by parking money at the Fed. Currently only a select few banks can receive that top-tier rate, now at 2.4 percent. The best that money-market funds — a popular cash receptacle for the firms McAndrews is targeting — can get from the Fed is 2.25 percent.

The New York Fed has prevented his company, TNB USA Inc., from opening the type of account it needs to make the business model work. That prompted the firm to sue the central bank last year, saying it was obstructing the project. The Fed found another way to fight back as the case continues to unfold. Last month it proposed rewriting its rules so TNB or any other potential “narrow banks” — so named because they are focused solely on taking deposits — could get only lower interest rates, sabotaging their raison d’être. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-04-24/fed-fights-a-new-bank…

* * *

Billions In African Gold Being Smuggled Through UAE By Crime Syndicates: Report

A bombshell investigative report by Reuters has blown open a hitherto under-reported massive black market trade which has seen billions of dollars worth of gold smuggled out of Africa and sold to Europe via “middle man” countries like the United Arab Emirates and others in the Middle East.

The investigation found the Middle East to be the illicit gold “gateway to markets in Europe, the United States and beyond” based on new analysis of customs data, showing tons of off-the-books non-taxed gold pouring out of countries like Ghana, Ivory Coast, Tanzania, Nigeria, and war-torn Libya and Sudan, with no official oversight by the states in which the gold is mined.

The numbers are staggering in terms of the newly revealed whopping unaccounted for increase in Middle East imports for the past decade and more:

Customs data shows that the UAE imported $15.1 billion worth of gold from Africa in 2016, more than any other country and up from $1.3 billion in 2006. The total weight was 446 tonnes, in varying degrees of purity – up from 67 tonnes in 2006.

Much of the gold was not recorded in the exports of African states. Five trade economists interviewed by Reuters said this indicates large amounts of gold are leaving Africa with no taxes being paid to the states that produce them.

Though small scale and individual mining which has long fueled Africa’s black market trade, often involving children and impoverished families, already known and understood, analysts interviewed by Reuters say the newly unearthed figures reveal illegal exporting on a much larger scale than was previously thought is taking place.

Charts via Reuters

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7449/

//OFFSHORE YUAN: 6.7537 /shanghai bourse CLOSED DOWN 77.79 POINTS OR 2.43%

HANG SANG CLOSED DOWN 256.03 points or 0.86%

2. Nikkei closed UP 107.78 POINTS OR 0.48%

3. Europe stocks OPENED RED EXCEPT SPAIN

USA dollar index RISES TO 98.28/Euro FALLS TO 1.1185

3b Japan 10 year bond yield: RISES TO. –.03/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.85/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 66.11 and Brent: 75/19

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO –01%/Italian 10 yr bond yield UP to 2.67% /SPAIN 10 YR BOND YIELD UP TO 1.09%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.68: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.29

3k Gold at $1276.25 silver at: 14.87 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 41/100 in roubles/dollar) 64.82

3m oil into the 66 dollar handle for WTI and 75 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.85 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0227 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1375 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.01%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.53% early this morning. Thirty year rate at 2.95%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.9347.. VERY DEADLY

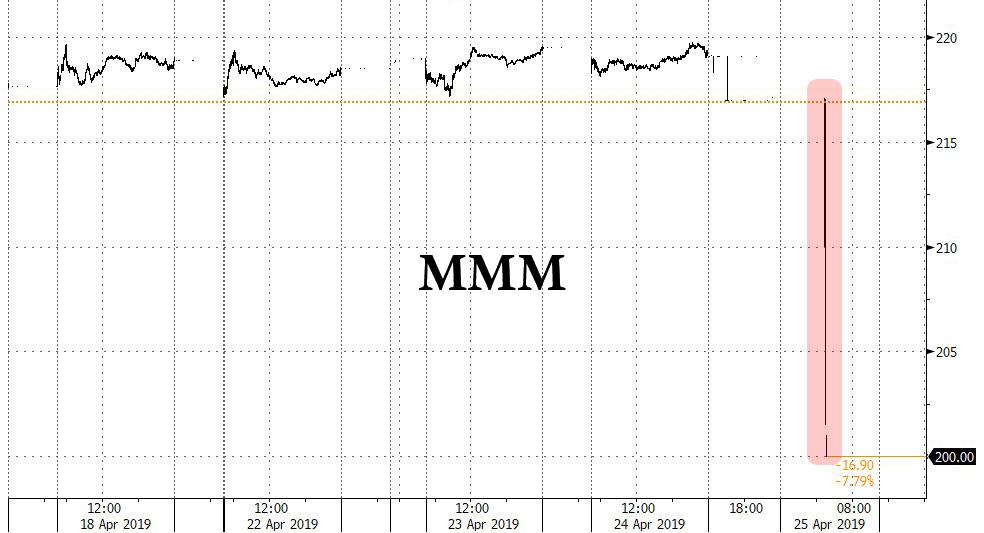

Dow Futures Plunge After 3M Plummets; Dollar Soars On Global Currency Carnage

It was shaping up as a relatively quiet session, with world equity markets slipping modestly on Thursday – despite blowout beats by Facebook and Microsoft which sent the latter’s stock 5% higher, sending its market cap above $1 trillion and making it the most valuable company in the world – amid worries on global growth and as investors digested European earnings, while the Swedish crown slumped to its lowest in 17 years and the euro suffered after German data.

But it was Dow heavyweight 3M’s disastrous earnings report and guidance cut that sent Dow futures sharply lower as the industrial conglomerate became the first stock to validate investor fears about growth challenges for the rest of the year.

In a nutshell, this is what 3M reported as it lamented a “disappointing start” to 2019: Q1 adjusted EPS $2.23, missing the estimate of $2.48, and revenue of $7.86BN, Exp. $8.02BN. But most concerning of all was its guidance, which was slashed to an adjusted EPS of $9.25 to $9.75, down from its prior guidance of $10.45-$10.90, and far below the consensus estimate of $10.53, suggesting sharp weakness for the rest of the year. And the cherry on top: 3M announced it would fire about 2,000 jobs as the broad slowdown hits its operations.

Elsewhere, Europe’s STOXX 600 lost 0.3% in early trading, with concern over prospects for global growth underscored by weak economic data from South Korea which earlier in the session reported its weakest GDP print since the financial crisis.

Energy stocks and a 10% drop in Finnish telecoms equipment maker Nokia dragged down European shares, with a varied bag of earnings for the region’s banks.

Asian markets had fallen earlier in the day, losing 0.5% as South Korea’s economy unexpectedly contracted in the first quarter, a vivid reminder that the global economy continues to slowdown sharply. Chinese stocks also fell sharply late in the day, losing more than 2% following attempts by the central bank to temper expectations for further easing of monetary policy and another substantial liquidity withdrawal by the PBOC. Chinese officials also warned of protracted pressure on economic growth, casting a shadow over hopes for a sustained recovery in the world’s second biggest economy.

Those worries on growth also played out closer to home for European investors, with fears lingering over the state of the German economy after a survey on Wednesday showed German business morale falling.

As a result of this weakness in Asia and Europe, the MSCI world equity index also fell 0.3%.

Amid today’s renewed risk weakness, central banks continued to pivot dovishly, with the Bank of Japan on Thursday pledging to keep interest rates very low at least until early 2020, even as it retained main policy targets. However in stark reversal to the market’s prior response to central bank dovishness, Japan’s Nikkei barely responded, closing just 0.5% higher, while the Japanese yen also reacted little. The yen was last up about a third of a percent, at 111.85 yen per dollar.

Several hours later, the Swedish Krona plunged to its lowest since August 2002, after the central bank said weak inflationary pressures meant a forecast rate hike would come slightly later than planned, while the central bank announced it would resume QE until the end of 2020. The SEK sank 1.2 percent against the euro to 10.65 – on course for its biggest daily drop in more than six months.

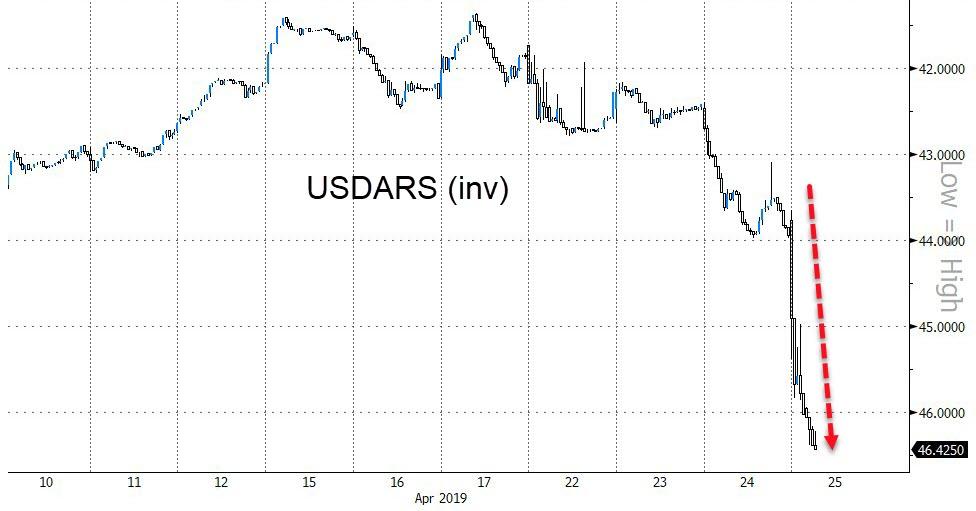

Turkey’s lira also crashed against the dollar, tumbling after the central bank announced it was removing its tightening pledge, and confirming that Turkey would no longer defend the lira after the nation’s reserves dropped to dangerously low levels.

“You certainly have a common response (from central banks) to a global growth slowdown in terms of monetary policy,” said Peter Schaffrik, head of European rates strategy at RBC Capital Markets. “We haven’t generally seen outright reduction, but it is easing relative to what was previously communicated to, and implied in, the markets.”

The currency carnage was not over, however, and the euro suffered its worst day in over six weeks, falling 0.6 percent to a 22-month following the further signs of flagging growth in Germany. It was last at $1.1141. Also on the agenda for the single currency were Spanish elections on Sunday and economic concerns out of Italy.

China’s yuan also declined to a two-month-low against the dollar later Thursday, while the Bloomberg replica of the CFETS RMB Index, which tracks the yuan versus a basket of 24 trading partners’ currencies, was at the highest in ten months. While the People’s Bank of China actually weakened the yuan’s reference rate, that wasn’t enough to keep the yuan index from rising so much. “Periods of broad dollar strength, as we have seen overnight, will result in a higher CFETS Index as the yuan fixing is normally not as weak as the moves in the basket currencies,” said Khoon Goh, head of Asia research at Australia and New Zealand Banking Group. Overnight, Chinese state media reported that the PBoC will set up policy framework to implement relatively low RRR for small and medium banks, in which the extra funds will be used to support private and small companies. However, there were later comments from the PBoC that China’s prudent monetary policy is overall appropriate and neither tight nor loose and that the use of repos and MLFs does not signal loosening bias.

With currencies around the globe tumbling, it’s not surprising that the dollar extended its gains, rising sharply and touching on fresh 2019 highs.

“The Fed isn’t keen to hike rates, but they are the strongest of the bunch so money will gravitate toward the U.S. dollar,” said David Madden, an analyst at CMC Markets in London.

Meanwhile, despite the dollar strength, oil continued to rise, Brent crude rose above $75 per barrel for the first time in 2019 in the wake of tightening sanctions on Iran, while gains in U.S. prices were crimped by a surge in U.S. supply.

Durable goods orders, initial jobless claims are due, while the afternoon sees scheduled earnings from Amazon and Intel.

Market Snapshot

- S&P 500 futures down 0.03% to 2,929.75

- STOXX Europe 600 down 0.3% to 389.91

- MXAP down 0.4% to 161.83

- MXAPJ down 0.9% to 536.76

- Nikkei up 0.5% to 22,307.58

- Topix up 0.5% to 1,620.28

- Hang Seng Index down 0.9% to 29,549.80

- Shanghai Composite down 2.4% to 3,123.83

- Sensex down 0.2% to 38,970.94

- Australia S&P/ASX 200 up 1% to 6,382.14

- Kospi down 0.5% to 2,190.50

- German 10Y yield fell 0.3 bps to -0.015%

- Euro down 0.1% to $1.1142

- Brent Futures up 0.9% to $75.25/bbl

- Italian 10Y yield fell 4.0 bps to 2.262%

- Spanish 10Y yield rose 0.8 bps to 1.081%

- Brent Futures up 0.9% to $75.25/bbl

- Gold spot up 0.2% to $1,277.62

- U.S. Dollar Index up 0.01% to 98.18

Top Headlines from Bloomberg

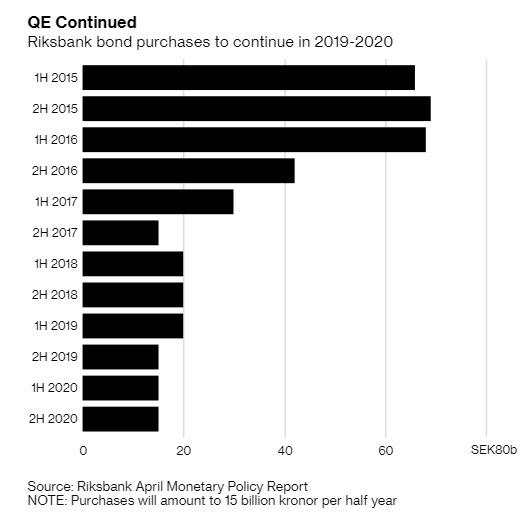

- The biggest currency driver in the European session was Sweden’s Riksbank which fell in line with the dovish tilt seen in other major central banks such as the European Central Bank. The Riksbank backtracked on plans to tighten monetary policy, as a less certain economic outlook meant negative Swedish rates may persist into next year — a shift from earlier where a rate hike was expected this September.

- The BOJ said it would keep interest rates extremely low through at least around spring 2020. A change to forward guidance was predicted by only 3 of 48 economists surveyed by Bloomberg. BOJ now projects it won’t hit its 2 percent inflation target at least through March 2022, which will be nine years since Governor Haruhiko.

- Deutsche Bank AG and Commerzbank AG ended talks on a historic tie-up, throwing the future of both lenders into question after failed turnaround plans. The two lenders decided that attempting to integrate would be too difficult to execute and also cited the restructuring costs and additional capital requirements.

- Bond traders are adding to Federal Reserve rate-cut bets in face of record stocks run. The futures market is moving back toward pricing in a full quarter-point cut this year, even as U.S. and Chinese economic data show signs of improvement.

- Rich Asians came to the rescue of UBS Group AG in the first quarter after Chief Executive Officer Sergio Ermotti’s dire outlook on market conditions sent investors into shock and investment banking revenue plummeted.

- South Korea, a bellwether for global trade and technology, cast doubt over hopes for a quick rebound in the world economy by reporting its biggest contraction of gross domestic product in a decade. Asia’s fourth-largest economy shrank by 0.3% in the first quarter from the previous three months, versus estimates for a 0.3% gain.

Asia equity markets traded cautious following an uninspiring lead from Wall St where the major indices consolidated albeit near record levels. In addition, holiday closures in Australia and New Zealand, the BoJ policy announcement, weak South Korean GDP and a slew of earnings provided much for participants to ponder over. Nikkei 225 (+0.5%) traded higher with newsflow and the biggest gaining stocks in Japan dominated by corporate results, while KOSPI (-0.5%) was subdued following abysmal growth data for Q1 in which GDP Q/Q unexpectedly contracted by 0.3% which was the worst reading since Q4 2008 and GDP Y/Y expanded at the slowest pace in almost a decade. Elsewhere, Hang Seng (-0.8%) and Shanghai Comp. (-2.5%) were downbeat as earnings season also started to pick up in the region and after the PBoC refrained again from liquidity operations which resulted to a net CNY 80bln drain. In addition, there were state media reports the PBoC will set up policy framework to implement relatively low RRR for small and medium banks, although this failed to spur a recovery given the absence of an actual RRR cut announcement and as PBoC officials reaffirmed a preference for prudent monetary policy. Finally, 10yr JGBs were choppy amid the cautious risk sentiment in the region and after the BoJ policy announcement which initially lifted 10yr JGBs at the open due to the dovish aspects from the statement and downgrades in the Outlook Report. However, prices then returned to pre-announcement levels as the lower projections were not much of a surprise given the recent data, while the BoJ slightly adjusted its modified forward guidance in which it stated that it will keep very low interest rate levels for an extended period of time at least through around Spring 2020.

Top Asian News

- BOJ Maintains Policy Rate, Adjusts Forward Guidance

- PBOC Has No Intention to Tighten or Loosen Policy, Liu Says

- South Korea Economy Unexpectedly Contracts as Investment Falters

- Axis, StanChart India CEOs Face Corp. Ministry Contempt Petition

- Global Steel Market Is Put on Notice as Top China Mill Warns

European Indices are trading with losses [Euro Stoxx 50 -0.5%] after having opened relatively flat, with markets initially taking the lead from the cautious performance in Asia. This morning’s downturn is on the back of significant underperformance in a number of Co’s after a morning driven by earnings with Nokia (-10.0%) leading the losses at the bottom of the Stoxx 600 after the Co. reported a EUR 50mln operating loss vs. Exp. profit of EUR 305mln. Separately, Sainsbury’s (-5.3%) are down after the CMA confirmed that they are to block merger discussions with Asda; as such the Co. are at the bottom of the FTSE 100 (-0.4%). The FTSE 100 is also weighed on by Barclays (-1.5%) post earnings where they reported a CIB total income which was lower than the prior, and Taylor Wimpey (-4.0%) after the Co. stated that increasing build costs are to push margins slightly lower. In recent reports Commerzbank (-2.0%) and Deutsche Bank (+3.0%) have confirmed that they have discontinued merger talks, as they believe that the merger would not result in sufficient benefits; which does follow earlier source reports that talks between the Co’s were on the verge of collapsing. Regarding this morning more positive earnings, ASM (+7.2%) lead the Stoxx 600 after beating on Q1 revenue and operating profit; while, Bayer (+3.5%) top the Stoxx 50 after confirming their FY guidance.

Top European News

- RBS Says Ross McEwan Has Resigned From Role as CEO

- Wirecard Addressing Auditing Quality Issues, CEO Braun Says

- Swedish Krona Tumbles as Riksbank Pushes Back Rate-Increase Plan

- SEB Says Riksbank Decisions Much More Dovish Than Expected

In FX, a technical break below support in Eur/Sek and brief look at the 10.5000 proved fundamentally flawed or just premature as the cross catapulted more than 15 big figures on a much more dovish than expected Riksbank policy meeting outturn, while Usd/Sek hit its highest levels in some 16 years. In short, the Swedish Central Bank pushed back the likely timing for further rate normalisation to year end or early 2020 from H2 this year and lowered its repo path over the forecast horizon, adding that the current -0.25% level will be maintained for longer than previously anticipated (ie as flagged in February). The Riksbank also predicted softer inflation in light of recent weaker than expected price developments and announced that Sek45 bn SGBs will be bought from July 2019 through December 2020 regardless of a couple of reservations. Eur/Sek has eased back from a circa 10.6655 peak, but remains relatively close to chart resistance around 10.6730 and Usd/Sek is now eyeing 9.6000 as the Dollar continues to rally across the board.

- USD – The Greenback is still outperforming or gaining at the expense of its currency counterparts, as the DXY consolidates and builds on advances through 98.000. In truth, aside from the Swedish Crown’s post-Riksbank collapse the Buck breached key levels late yesterday as resilience in several rivals finally gave way and the index cleared resistance ahead of the round number to register a new ytd best at 98.189, with only a relatively minor extension to 98.233 so far today. However, the DXY remains in the ascendency and 98.496 is the next bullish chart target.

- CAD/GBP/EUR/AUD – All weaker vs the Usd, albeit just off worst levels, as the Loonie continues to reflect on Wednesday’s shift from the BoC to a wait-and-see stance vs tightening previously and fails to derive much support from a rebound in oil prices. Meanwhile, Cable has fallen under 1.2900 to test Fib and MA supports, with Eur/Usd probing below its latest 2019 trough to 1.1135 and eyeing downside chart levels ahead of 1.1100 (1.1190-10), Aud/Usd pivoting 0.7000 where hefty option barriers lie and the Franc back to straddling 1.0200.

- JPY/NZD – The Yen has recovered well from new ytd lows vs the Usd around 112.40 to trade back above 112.00 amidst more speculation about positioning for the upcoming lengthy Golden Week holiday and not really reacting to the BoJ’s attempt to clarify policy guidance given Governor Kuroda’s admission that it is highly possible that ultra accommodation may continue beyond Spring 2020 as the 2% inflation target could well remain elusive even after FY 2021. Elsewhere, the Kiwi is trying to cling to 0.6600 vs its US peer ahead of NZ trade data and with some indirect help via the Aud/Nzd cross that is hovering near the base of a 1.0627-42 range at the tail end of ANZAC day.

In commodities, Brent (+1.0%) and WTI (+0.4%) prices are in the green as oil prices have now largely shrugged off yesterday’s larger than expected EIA build; which came in at 5.479M vs. Exp. 1.25mln, as this was below Tuesday’s API build of 6.86M. This morning Brent prices did surpass, and remain above, the USD 75/bbl level for the first time in 2019. In recent newsflow Iran’s Foreign Ministry have stated that Tehran will not allow any country to replace their oil sales within the market; which does come in the context of the Iranian oil waivers ending on May 2nd. Separately, Iraq’s Oil Minister states that they have the capacity to increase oil production to 6mln BPD, for reference Iraq currently have a production level of 4.5mln BPD; however, there will be no change in production and if markets need more oil this will be decided at the relevant time. Gold (+0.1%) has been relatively uneventful overnight, as the yellow metal remains subdued by the continuing dollar strength. Elsewhere, Anglo American reported Q1 copper production of 161k tonnes vs. Prev. 155k tonnes, and an increase in iron ore output from their Minas-Rio mine, 4.9mln tonnes vs. Prev. 3mln tonnes; with the mine having reopened in December after an 8-month closure due to a pipeline leak.

US Event Calendar

- 8:30am: Initial Jobless Claims, est. 200,000, prior 192,000; Continuing Claims, est. 1.68m, prior 1.65m

- 8:30am: Durable Goods Orders, est. 0.8%, prior -1.6%; Durables Ex Transportation, est. 0.2%, prior -0.1%

- 8:30am: Cap Goods Orders Nondef Ex Air, est. 0.2%, prior -0.1%; Cap Goods Ship Nondef Ex Air, est. 0.1%, prior -0.1%

- 9:45am: Bloomberg Consumer Comfort, prior 60.3

- 11am: Kansas City Fed Manf. Activity, est. 8, prior 10

DB’s Craig Nicol concludes the overnight wrap

With the US equity rally catching its breath yesterday, it was the bond market which instead took centre stage with yields sharply lower across the board. Indeed, having spent 8 consecutive sessions above 0%, Bunds succumbed to gravity once again and dropped back into negative territory following a -5.3bps decline taking 10y yields to -0.015%. There were moves of similar magnitude across the rest of Europe while Treasuries also rallied -4.7bps for the biggest move in over a month as curves broadly flattened.

There was a bit of head scratching as to what was driving the moves however in the end it appeared to be a bit of a compounding effect of various data releases and newsflow. Initially the well below market Aussie CPI release got the ball rolling this time yesterday, before Europe took the baton with Germany’s soft IFO survey doing the early damage – more on that further down. There was some commentary also about a decent Bund auction which kept yields anchored towards zero while the ECB’s latest Bulletin hammered home the implications of rising protectionism for the Euro Area, even if there wasn’t a huge amount of new information. Later in the afternoon we also got a dovish BoC meeting – which saw 10y Canadian yields fall -7.4bps to their lowest level since the start of the year after the bank’s statement removed its hiking bias – adding more fuel to the rates rally fire. Meanwhile, there was also some more chatter about the WSJ story from the weekend which was suggested as still hanging over the bond market, as it seemed to more seriously entertain the idea of a rate cut than previously. Our US economists dug into the underlying interview transcripts though, and they think the article is sensationalizing the actual, more measured argument from Fed officials. Finally, US oil inventory data showed another surprising build in stockpiles, which sent WTI prices -0.62% lower and weighed a bit on inflation expectations.

Holiday volumes are probably also exaggerating moves this week, however with central banks falling into the dovish line one-by-one and data outside of the US still faltering, it’s no great surprise to see yields really fail to break higher at the moment. The dollar has also perked up in response to those trends, advancing +0.55% to its strongest level in almost two years. It might have been boosted by breaking through some key technical levels, but the greenback has regardless gained against most currencies this week. Also interesting is the decoupling of bonds from equities at the moment. Whilst US equity markets gently eased on the breaks yesterday it still didn’t stop the S&P 500 and NASDAQ going above their record highs again intraday, before closing -0.22% and -0.23%, respectively. The energy sector underperformed and fell -1.85%, following the move in oil. Earnings played their part again but ultimately appeared to cancel each other out.

Indeed all eyes had been on Caterpillar (-3.03%), given its reputation as a macro bellwether. The company reported higher earnings than expected and worked down its backlog of orders, and left its guidance mostly unchanged.On the positive side, the CFO said that “strong” US demand will continue to grow this year, but investors focused on softer language about China. Management said that they expect to lose market share in China, because of aggressive competition and pricing pressure. Elsewhere, Boeing (+0.39%) advanced after management downplayed the impact of the 737 Max grounding, though the ultimate impact remains uncertain.

After the US close we also got the latest results from a couple of the tech juggernauts in Facebook and Microsoft, with both companies posting quite strong results. Microsoft traded as much as +4% higher after hours and Facebook +10% higher. Both companies saw revenues grow much stronger than consensus expectations, and Microsoft had particular strength in its cloud-computing sector. Facebook’s growth has slowed in developed markets, but the company has improved in emerging markets to compensate. US equity futures are posting small gains overnight led by the NASDAQ (+0.30%).

Overnight we’ve also had the BoJ meeting. As expected, policy was left unchanged with the most notable statement changes including a mention to keep rates low through at least spring 2020. Previously the BoJ had suggested rates would stay low for an “extended period”. There were also modest downward revisions to growth and inflation while the BoJ is considering a facility to offer term-limited loans of its ETFs to investors. Kuroda is due to speak after we go to print.

Despite the Yen (+0.17%) advancing, the Nikkei (+0.30%) is also slightly higher post that news and leading gains in Asia with the Hang Seng (-0.07%), Shanghai Comp (-0.70%) and Kospi (-0.26%) all in the red. The latter has struggled after Q1 GDP printed at a well below market -0.3% qoq (vs. +0.3% expected) in South Korea – the weakest since 2008.

Back to yesterday, where as noted above the initial trigger for the rates rally appeared to be the soft German IFO survey. The headline reading came in at 99.2 which was both lower than the 99.9 consensus and also down half a point for March.The expectations component slid 0.4pts to 95.2, however that was almost a full point below consensus while the current assessment component dropped 0.6pts to 103.3. Like the PMIs, the manufacturing sector bore the brunt of the decline, dropping to the lowest since 2013.So little turnaround in sight for the sector. It’s worth noting that less followed confidence indicators in France were also softer for the manufacturing sector yesterday.

Interestingly, despite the Bund and broader rates move the DAX actually outperformed most other European equity markets, closing up +0.63% albeit entirely thanks to big moves for SAP and Wirecard.In contrast the STOXX 600 closed -0.09%, CAC -0.28% and FTSE MIB -0.79%. European Banks also got hit to the tune of -1.71% which was the biggest decline in a month. The rates move clearly overshadowing any positive read through from the Credit Suisse results.

Meanwhile, in EM the MSCI EM equity index fell -0.48%. It’s interesting to note that while US equities breached record highs two days ago, and European equities are not far off, EM has very much lagged the broader DM move with the index still -14.81% off its 2018 highs achieved last January.In FX a basket of EM currencies finished -0.69% with the Turkish Lira (-0.77%) again grabbing the spotlight, weakening for the fifth consecutive day, and to a new six month high. We’ve actually got the Central Bank of Turkey decision today where the market will no doubt be looking for some soothing words to stop the slide.

In other news, the latest on Brexit is that the 1922 Committee refused to approve any changes to the leadership rules, and thus taking the press of the PM.Staying with the UK, Chancellor Hammond confirmed yesterday that he hoped to make the appointment of Carney’s successor as BoE Governor by October. He also suggested that the new Governor wouldn’t necessarily have to serve a full eight-year term. Sterling closed -0.28% yesterday.

In terms of the day ahead,this morning in Europe we’re due to get CBI survey data for April in the UK. Also worth keeping an eye on given recent volatility is the Central Bank of Turkey decision at midday. This afternoon in the US we’ve got preliminary durable and capital goods orders data due which should be the last set of data to help sharpen Q1 GDP forecasts tomorrow. Also due up is the latest claims reading and Kansas City Fed manufacturing survey. Away from the data the ECB’s Guindos is due to speak this afternoon in New York. Japan’s PM Abe is also due meet Tusk and Juncker in Brussels while Japan’s Finance Minister Aro is due to meet with Mnuchin over provisions against currency manipulation. Finally the earnings highlights today are Amazon, Intel, ComCast, 3M, Ford, Bayer, and UBS.

end

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 77.79 POINTS OR 2/43% //Hang Sang CLOSED DOWN 256.03 POINTS OR 0.86% /The Nikkei closed UP 107.78POINTS OR 0.48%/ Australia’s all ordinaires CLOSED HOLIDAY

/Chinese yuan (ONSHORE) closed DOWN at 6.7449 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 66/11 dollars per barrel for WTI and 5.19 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.7449 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7537/ TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/SOUTH KOREA

SOUTH KOREA

Export dynamo sees their economy unexpectedly plunge by the most in a decade. Its GDP unexpectedly shank in Q1 dropping .3% Q/Q

(courtesy zerohedge)

Canary Meet Coalmine: South Korean Economy Unexpectedly Plunges Most In A Decade

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

China/

4/EUROPEAN AFFAIRS

FRANCE//CHRISTIANITY

The burning of Notre Dame and how France is leading in the destruction of Christian Europe. Mosques on the rise..churches are empty and their buildings are falling apart

(courtsy Guy Milliere/Gatestone)

The Burning Of Notre Dame And The Destruction Of Christian Europe

Authored by Guy Milliere via The Gatestone Institute,

- Barely an hour after the flames began to rise above Notre Dame — at a time when no explanation could be provided by anyone — the French authorities rushed to say that the fire was an “accident” and that “arson has been ruled out.” The remarks sounded like all the official statements made by the French government after attacks in France during the last decade.

- The Notre Dame fire also occurred at a time when attacks against churches in France and Europe have been multiplying. More than 800 churches were attacked in France during the year 2018 alone.

- Churches in France are empty. The number of priests is decreasing and the priests that are active in France are either very old or come from Africa or Latin America. The dominant religion in France is now Islam. Every year, churches are demolished to make way for parking lots or shopping centers. Mosques are being built all over, and they are full.

The fire that destroyed much of the Notre Dame Cathedral in the heart of Paris is a tragedy that is irreparable. Even if the cathedral is rebuilt, it will never be what it was before. (Photo by Veronique de Viguerie/Getty Images)

The fire that destroyed much of the Notre Dame Cathedral in the heart of Paris is a tragedy that is irreparable. Even if the cathedral is rebuilt, it will never be what it was before. Stained glass windows and major architectural elements have been severely damaged and the oak frame totally destroyed. The spire that rose from the cathedral was a unique piece of art. It was drawn by the architect who restored the edifice in the nineteenth century, Eugène Viollet-le-Duc, who had based his work on 12th century documents.

In addition to the fire, the water needed to extinguish the flames penetrated the limestone of the walls and façade, and weakened them, making them brittle. The roof is non-existent: the nave, the transept and the choir now lie in open air, vulnerable to bad weather. They cannot even be protected until the structure has been examined thoroughly, a task that will take weeks. Three major elements of the structure (the north transept pinion, the pinion located between the two towers and the vault) are also on the verge of collapse.

Notre Dame is more than 800 years old. It survived the turbulence of the Middle Ages, the Reign of Terror of the French Revolution, two World Wars and the Nazi occupation of Paris. It did not survive what France is becoming in the 21st century.

The cause of the fire has so far been attributed to “an accident,” “a short circuit,” and most recently “a computer glitch.”

If the fire really was an accident, it is almost impossible to explain how it started. Benjamin Mouton, Notre Dame’s former chief architect, explained that the rules were exceptionally strict and that no electric cable or appliance, and no source of heat, could be placed in the attic. He added that an extremely sophisticated alarm system was in place. The company that installed the scaffolding did not use any welding and specialized in this type of work. The fire broke out more than an hour after the workers’ departure and none of them was present. It spread so quickly that the firefighters who rushed to the spot as soon as they could get there were shocked. Remi Fromont, the chief architect of the French Historical Monuments said: “The fire could not start from any element present where it started. A real calorific load is necessary to launch such a disaster”.

A long, difficult and complex investigation will be conducted.