GOLD: $1270.80 DOWN $12.30 (COMEX TO COMEX CLOSING)

Silver: $14.61 DOWN 13 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1271.50

silver: $14.64

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 16/30

EXCHANGE: COMEX

CONTRACT: MAY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,281.400000000 USD

INTENT DATE: 05/01/2019 DELIVERY DATE: 05/03/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 16

690 C ABN AMRO 5 2

737 C ADVANTAGE 17 8

800 C MAREX SPEC 8 4

____________________________________________________________________________________________

TOTAL: 30 30

MONTH TO DATE: 118

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 30 NOTICE(S) FOR 3000 OZ (0.0933 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 118 NOTICES FOR 11800 OZ (.3670 TONNES)

SILVER

FOR MAY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

386 NOTICE(S) FILED TODAY FOR 1,930,000 OZ/

total number of notices filed so far this month: 2539 for 12,695,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE :$5444 UP $62

Bitcoin: FINAL EVENING TRADE: $5504 UP 120

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A HUGE SIZED 4930 CONTRACTS FROM 196.610 UP TO 1201,540 DESPITE YESTERDAY’S 23 CENT FALL IN SILVER PRICING AT THE COMEX. ,LIQUIDATION OF THE SPREADERS HAVE STOPPED NOW THAT WE HAVE FINISHED WITH FIRST DAY NOTICE. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR MAY, 0 FOR JUNE, 2927 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 2927 CONTRACTS. WITH THE TRANSFER OF 2927 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2927 EFP CONTRACTS TRANSLATES INTO 14.63 MILLION OZ ACCOMPANYING:

1.THE 23 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

AND NOW 16.380 MILLION OZ STANDING FOR SILVER IN MAY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MAY:

5859 CONTRACTS (FOR 2 TRADING DAYS TOTAL 5859 CONTRACTS) OR 29,30 MILLION OZ: (AVERAGE PER DAY: 2929 CONTRACTS OR 14.64 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 14.64 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 2.09% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 770.19 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4930 DESPITE THE 23 CENT FALL IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2927 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS RESUMED THEIR LIQUIDATION OF THE SPREAD TRADES TODAY.

TODAY WE GAINED A HUMONGOUS SIZED: 7857 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2927 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 4997 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 23 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.74 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.008 BILLION OZ TO BE EXACT or 144% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 386 NOTICE(S) FOR 1,930,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ AND NOW MAY: 16,380,000 OZ..

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A GOOD SIZED 3863 CONTRACTS, TO 433,874 DESPITE THE FALL IN THE COMEX GOLD PRICE/(A DROP IN PRICE OF $1.20//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4084 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 4084 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 433,874. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7950 CONTRACTS: 3863 OI CONTRACTS INCREASED AT THE COMEX AND 4084 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 7950 CONTRACTS OR 795,000 OZ OR 24.72 TONNES. YESTERDAY WE HAD A LOSS IN THE PRICE OF GOLD TO THE TUNE OF $1.20….AND WITH THAT RISE, WE HAD A STRONG GAIN IN TONNAGE OF 24.72 TONNES!!!!!!.??????????????????????????????????????????

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 7157 CONTRACTS OR 715,700 OR 22.26 TONNES (2 TRADING DAYS AND THUS AVERAGING: 3579 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAYS IN TONNES: 22.26 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 22.26/3550 x 100% TONNES =0.627% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1851.08 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 53863 DESPITE THE FALL IN PRICING ($1.20) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A CONSIDERABLE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 4084 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 4084 EFP CONTRACTS ISSUED, WE HAD A STRONG GAIN OF 7950 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

4084 CONTRACTS MOVE TO LONDON AND 3863 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 24.72 TONNES). ..AND THIS STRONG DEMAND OCCURRED WITH A FALL IN PRICE OF $1.20 IN YESTERDAY’S TRADING AT THE COMEX.

we had: 30 notice(s) filed upon for 3000 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $12.30 TODAY

NO CHANGE IN GOLD INVENTORY AT THE GLD

INVENTORY RESTS AT 746.69 TONNES

IT LOOKS LIKE WE HAVE REACHED THE BOTTOM OF THE BARREL FOR PHYSICAL GOLD BEING SUPPLIED TO THE CROOKS.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 23 CENTS TODAY:

MY GOODNESS! THIS IS A HUGE SURPRISE!!

A BIG CHANGE IN SILVER INVENTORY AT THE SLV//

A DEPOSIT OF 2.869 MILLION OZ OF SILVER. IT IS YOUR GUESS IF IT IS PAPER SILVER OR THE REAL STUFF

I WILL PUT MONEY THAT THEY ARE “RETURNING” PAPER SILVER.

/INVENTORY RESTS AT 314.848 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A HUGE SIZED 4930 CONTRACTS from 1,6.610 UPTO 201,540 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE STOPPED THEIR LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ENTER AN ACTIVE DELIVERY MONTH. THUS SILVER HAS THE ACTIVE MONTH OF MAY COMING UP AND THUS SPREADERS DO THE FOLLOWING:

“YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF APRIL BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 0 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 2927 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2927 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 4930 CONTRACTS TO THE 2927 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUMONGOUS GAIN OF 7957 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 39.29 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL AND NOW 16.380 MILLION OZ FOR MAY

RESULT: A HUGE SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 23 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 2927 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED //Hang Sang CLOSED DOWN 48.85 POINTS OR .22% /The Nikkei closed Australia’s all ordinaires CLOSED DOWN 56%

/Chinese yuan (ONSHORE) closed UP at 6.7345 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 63.26 dollars per barrel for WTI and 71.38 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.7345 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7379/ TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA/ SOUTH KOREA

NORTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China

4/EUROPEAN AFFAIRS

i)The pound first rises and then dumps after the Bank of England signals that one more hike is needed. Then strangely they cut inflation forecasts.

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

i)This is a huge Bellwether for the USA economy. Semi conductor chip sales are a good indicator for growth in the USA economy and for that matter, the globe. Today we find that the entire global semiconductor sales have collapsed by a huge 15.5% in the first quarter of 2019:

( zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA

9. PHYSICAL MARKETS

ii)A very important commentary from Chris Marcus as he recalls Bart Chilton’s last interview

( Chris Marcus/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//early this morning/TRADING

ii)Market data

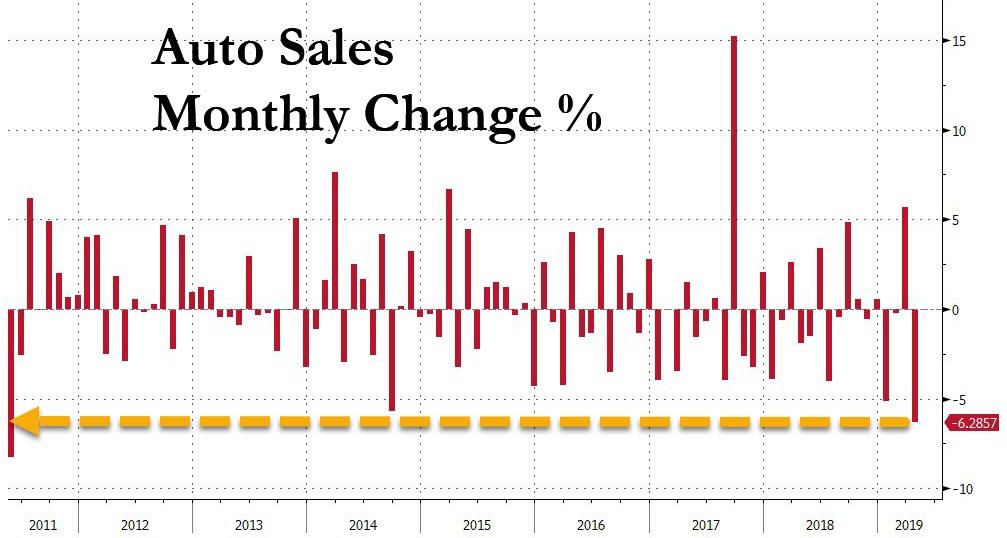

a)This does not look like a strong USA economy and a GDP growth rate of 3.2%: April USA auto sales crash by a huge 6.1%…it’s worst slide in 8 years. The USA economy has turned on a dime

( zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

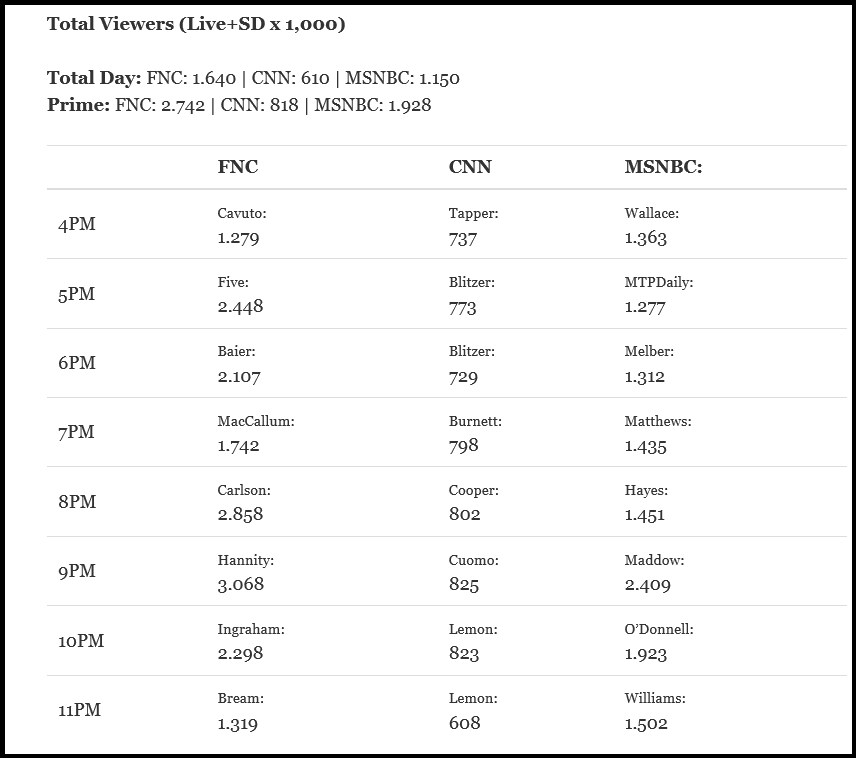

a)CNN rating plummet another 26% and for the first time viewership has dropped below the one million mark at b)767,000. It sure looks like the average person gets it with respect to the deep state activities in the uSA and they do not like it..they are refusing to watch CNN

( zerohedge)

SWAMP STORIES

a)Barr refuses to appear before the House panel today because the Democrats want to use lawyers to question him instead of the members themselves. Nadler threatens subpoena

( zerohedge)

( zerohedge)

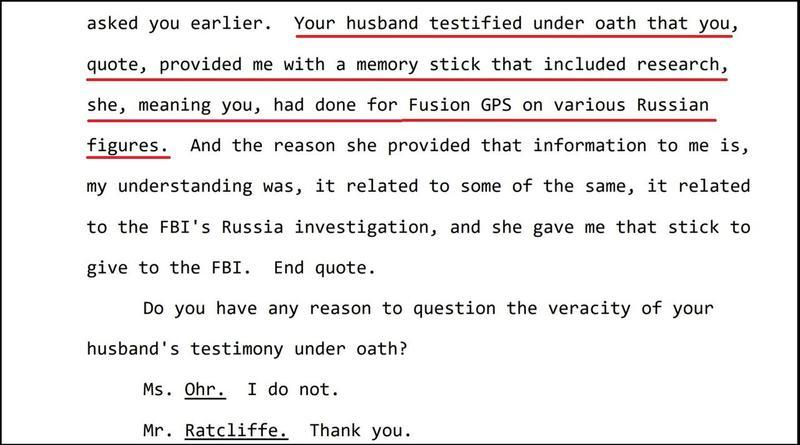

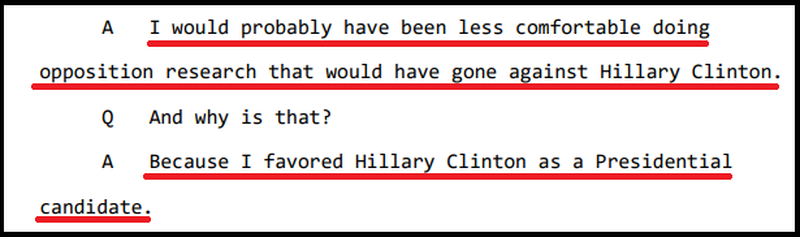

c)Nellie Ohr is to face a criminal referral for lying to Congress.

( zerohedge)

d)Seth Lipsky of the New York Post describes Leahy has a piece of garbage. The author describes the Bill Barr testimony yesterday

e)The Wall Street Journal sets the narrative straight that Barr has done nothing wrong. They expose the democrats hypocrisy with respect to Hillary Clinton and Attorney General Loretta Lynch vs Barr and Trump( Wall Street Journal/zerohedge)

f)My goodness, Hillary Clinton has now “asked” China to steal Trump’s tax returns. Obviously this is in retribution for Trump asking Russia to retrieve Hillary’s long lost emails.

( zerohedge)

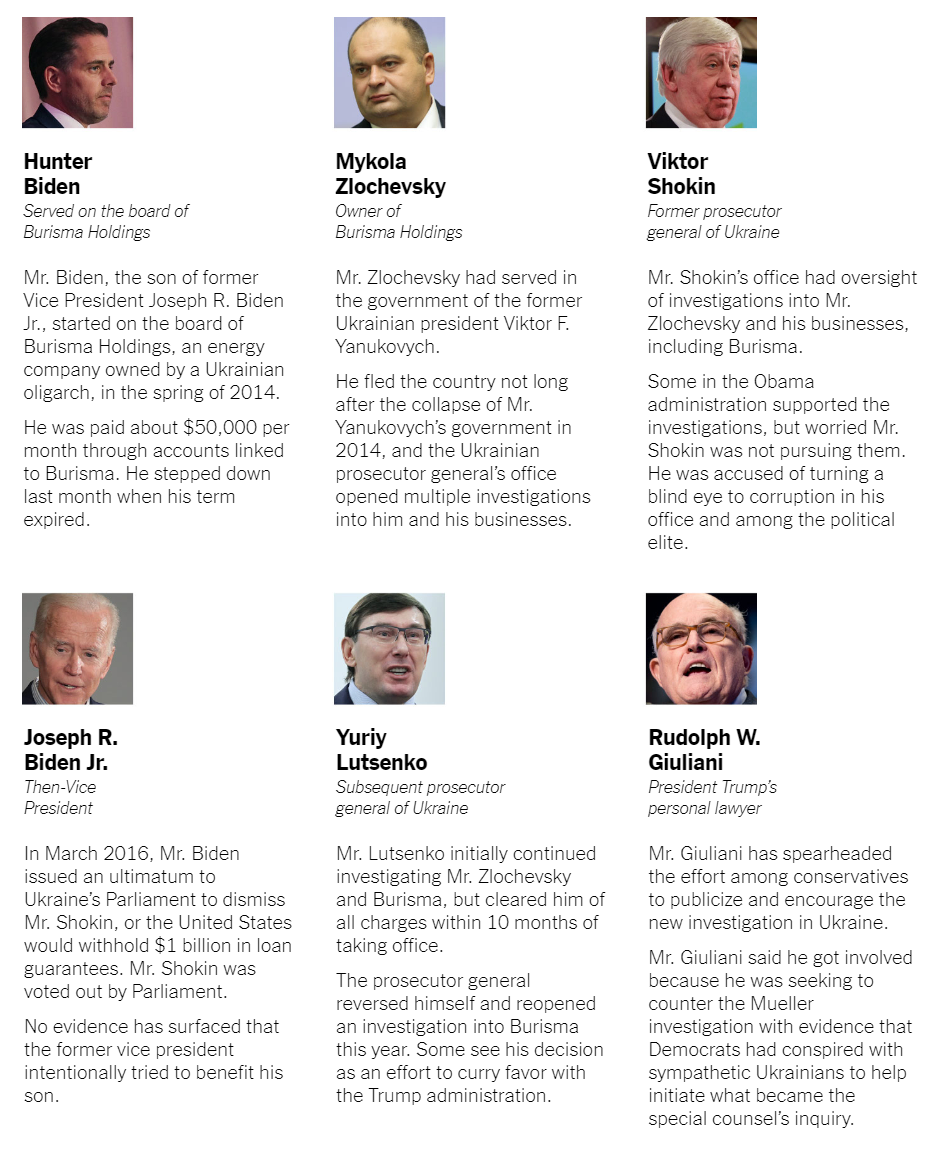

g)This is why Biden has little chance in the USA election as the New York Times publishes a scathing attack on their greed with respect to Biden son’s Hunter involvement in the Ukraine…graft at the highest levels.

( zerohedge)

h)Quite a story!! The FBI used a “honeypot” spy (Ms Turk) who accompanied Stefan Halper whose mission was to milk Papadopoulos on “dirt” that he picked up from Downer who received it from the Maltese Professor Mifsud. That is your genesis. The real story begins the 9th of March 2016.

Let us head over to the comex:

Gold withdrawals;

i) zero withdrawals.

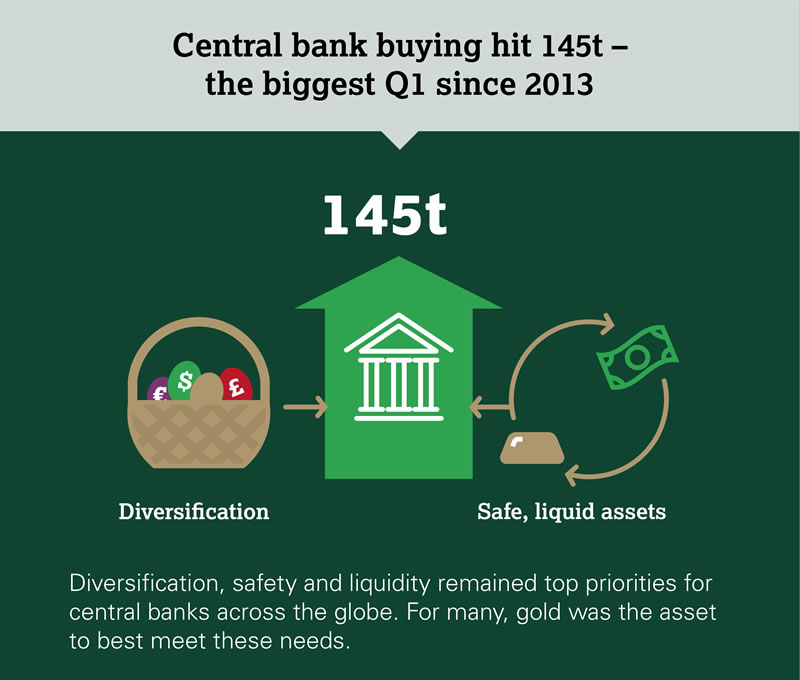

Global Gold Demand Gains In Q1, 2019: Central Banks Buy Gold Bullion and ETFs See Inflows

For many, gold was the asset to best meet these needs.

Global Gold Demand Trends Q1 2019: Global gold demand lifted by central banks and ETFs

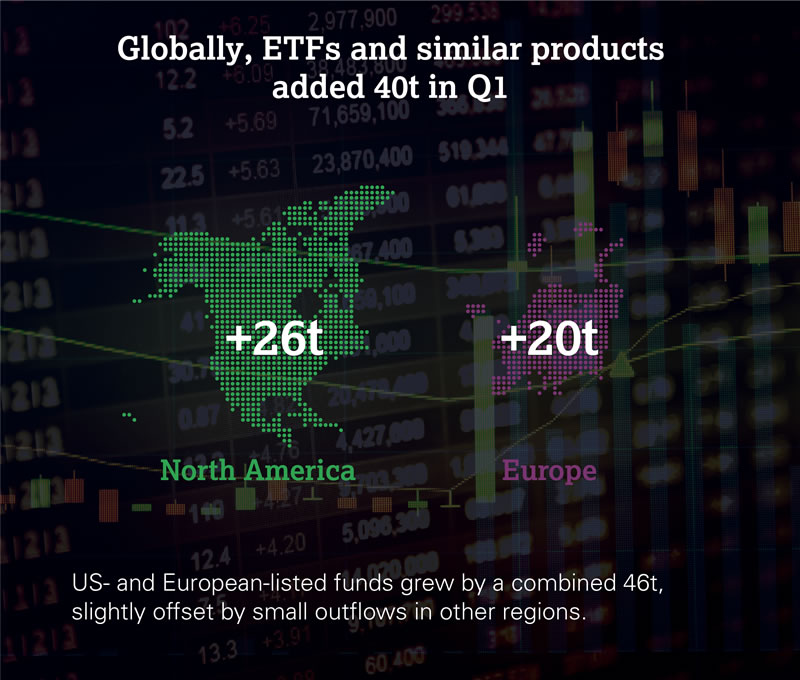

This compares with a relatively weak Q1 2018, when demand sank to a three-year low of just 984.2t. Central bank buying continued apace: global gold reserves grew by 145.5t. Gold-backed ETFs also saw growth: quarterly inflows into those products grew by 49% to 40.3t. Total bar and coin investment weakened a fraction to 257.8t (-1%), due to a fall in demand for gold bars; official gold coin buying grew 12% to 56.1t. Jewellery demand was a touch stronger y-o-y at 530.3t, chiefly due to improvement in India’s market. The volume of gold used in technology dipped to a two-year low of 79.3t, hit by slower economic growth. The supply of gold in Q1 was virtually unchanged, just 3t lower y-o-y at 1,150t.

Highlights

Central banks bought 145.5t of gold, the largest Q1 increase in global reserves since 2013. Diversification and a desire for safe, liquid assets were the main drivers of buying here. On a rolling four-quarter basis, gold buying reached a record high for our data series of 715.7t.

Q1 jewellery demand up 1%, boosted by India. A lower rupee gold price in late February/early March coincided with the traditional gold-buying wedding season, lifting jewellery demand in India to 125.4t (+5% y-o-y) – the highest Q1 since 2015.

ETFs and similar products added 40.3t in Q1. Funds listed in the US and Europe benefitted from inflows, although the former were relatively erratic, while the latter were underpinned by continued geopolitical instability.

Bar and coin investment softened a touch – 1% down to 257.8t. China and Japan were the main contributors to the decline. Japan saw net disinvestment, driven by profit-taking as the local price surged in February.

Gold used in applications such as electronics, wireless and LED lighting fell 3% to 79.3t.Trade frictions, sluggish sales of consumer electronics and global economic headwinds hit the technology sector.

Full Report From The World Gold Council – Download Here

News & Commentary

– Gold ends lower, then climbs after Fed policy update

– Fed holds rates steady, citing lack of inflation pressure

– Dow and S&P 500 erase gains after Powell dashes rate-cut hopes

– Russia warns U.S. over ‘aggressive’ moves in Venezuela

Recent Market Updates

– “The Gold Belongs To The Italians, Not The Bankers”

– Newstalk Interview: Investors Looking To Store Gold In Dublin Rather Than London

– Australia, UK & U.S. Should Learn Lessons From Irish Property Crash

– SWOT Analysis: Venezuela Sells $400 Million Worth Of Gold Bullion

– World’s Central Banks Want More Gold – India May Buy 1.5M Ounces In 2019

– Russia’s 2019 Gold Rush Continues: Buys 600,000 Ounces of Gold In March

– When Should You Sell Your Gold and Silver? (GoldCore Video)

– Understanding Gold: A Step By Step Guide To Gold As An Asset Class

– World Trade Suffers Biggest Collapse Since Financial Crisis

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

This is quite an operation and it took a few years of planning. Kinesis is launching the Kinesis mint where you can buy physical gold and silver on the blockchain format

(Kinesis/zerohedge)

Kinesis Launches the Kinesis Mint, physical gold and silver on the blockchain

Submitted by cpowell on Wed, 2019-05-01 16:56. Section: Daily Dispatches

Company Announcement

via PR Newswire, Chicago

Wednesday, May 1, 2019

LONDON — Today Kinesis Money is announcing the launch of its cutting-edge blockchain-based platform, the Kinesis Mint. The Kinesis Mint, which will cement Kinesis’ position in the market as a formidable global fintech player, is a platform that allows users to create Kinesis digital currencies, KAU (1 gram gold) and KAG (1 ounce silver), into existence.

…

Kinesis Money is an evolutionary monetary system using the real assets of gold and silver as the basis for digital currencies. These currencies provide a 1:1 allocation of physical bullion, with the transaction fees accumulated whenever the currencies are sent, spent, or traded and then proportionately redistributed to Kinesis currency and token holders as a velocity-based yield, incentivising use.

“Minting” is the process of creating Kinesis currencies by depositing fiat to purchase bullion or depositing existing bullion into the Kinesis Mint. The physical metal is then emitted to their bespoke fork of the stellar blockchain and represented in a user’s e-wallet; facilitating remittance over the stellar blockchain, which enables global transactions of over 3,000 transactions per second with a settlement time of 3 to 5 seconds at a flat fee of 0.45 percent. …

… For the remainder of the announcement:

https://www.prnewswire.com/news-releases/kinesis-launches-the-kinesis-mi…

END

A very important commentary from Chris Marcus as he recalls Bart Chilton’s last interview

(courtesy Chris Marcus/GATA)

Former CFTC Commissioner Bart Chilton’s last interview recalled

Submitted by cpowell on Wed, 2019-05-01 23:43. Section: Daily Dispatches

7:40p ET Wednesday, May 1, 2019

Dear Friend of GATA and Gold:

Chris Marcus of Arcadia Economics today recounts the interview he got from the former commissioner of the U.S. Commodity Futures Trading Commission, Bart Chilton, just before Chilton’s death. In that interview Chilton acknowledged that JPMorganChase assumed the big silver futures short position of Bear Stearns upon the latter’s collapse, that JPMorganChase exceeded the temporary exemption it was granted by the commission on silver position limits, and that he thought the CFTC compiled plenty of evidence of manipulation of the silver market, even as experts advised the commission that the evidence was not sufficient to prosecute.

Marcus’ commentary is headlined “In Memory of Bart Chilton” and it’s posted at Arcadia Economics here:

https://arcadiaeconomics.com/silver-manipulation/in-memory-of-bart-chilt…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

LBMA etc.

(courtesy Nicholas B)

-END-

Gold trading/yesterday and today.

Gold Tumbles To Critical Technical Support As Market ‘Tightens’ Fed Expectations

A “transitorily” hawkish Fed, which saw the market’s Fed rate change expectations tighten by 13bps, has prompted dollar gains and sparked selling in the precious metals.

And as the dollar rallied, gold sank…

Holding (for the second time in just over a week) at its 200DMA…

At the same time, Silver has dropped to its lowest since 12/3/18…

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7345/

//OFFSHORE YUAN: 6.7379 /shanghai bourse CLOSED

HANG SANG CLOSED UP 245.07 POINTS OR .83%

2. Nikkei closed DOWN 48.85 POINTS OR .22%

3. Europe stocks OPENED RED

USA dollar index FALLS TO 97.59/Euro RISES TO 1.1208

3b Japan 10 year bond yield: FALLS TO. –.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.49/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 63.57 and Brent: 72.06

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +01%/Italian 10 yr bond yield DOWN to 2.54% /SPAIN 10 YR BOND YIELD DOWN TO 1.00%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.53: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.34

3k Gold at $1271.80 silver at: 14.67 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 38/100 in roubles/dollar) 65.23

3m oil into the 63 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.49 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0189 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1421 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to +0.01%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.52% early this morning. Thirty year rate at 2.91%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.9613.. VERY DEADLY

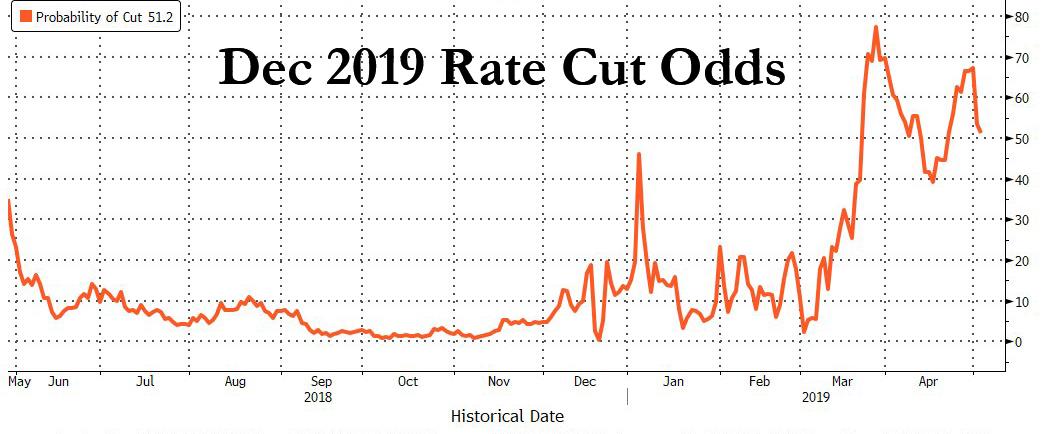

Stocks Drift Lower As Rate Cut Bets Slide On Hawkish Fed

With key Asian markets (China and Japan) closed for the second day in a row, Europe’s share markets struggled early on even as US equity futures levitated form session lows…

… after the Fed crushed hopes that it is preparing its first interest rate cut in years, as Powell said inflationary pressures were “transitory”, sending 2019 rate cut odds sliding.

As a result, stocks were mixed on Thursday as, in Bloomberg’s words “investors switched their focus from monetary policy back to company earnings and the outlook for global trade”. The dollar was little changed, while treasury yields continued their ascent.

Starting off the overnight session, Asian trading was thinned by holidays in Japan and China but Hong Kong and Korea’s stocks gained after CNBC reported the U.S. and China could announce a long-awaited trade deal by May 10, as Chinese Vice Premier Liu He heads to Washington. Though now expected by markets if confirmed, it would remove significant uncertainty that has weighed on markets and global data for a year now.

“I would still expect some relief rally once the deal gets done. The question is how big that move might be,” State Street GM’s Metcalfe added.

Following the subdued Asian action, Europe’s basic resource stocks led the downward shift in equities with a 1.4 percent drop to their lowest since late March. Continental Europe was also trying to get back up to speed having been shut for holidays on Wednesday. Oil and metals markets added to the pressure on stocks on Thursday with traders sending copper to a 2-month low while news of record US production sent the price of oil sliding after a 33% rise this year.

Elsewhere Turkey’s lira remained under pressure near the 6 per dollar mark after data there had showed manufacturing activity contracting for the 13th month in a row. Euro zone factory activity also contracted for a third straight month. “Demand shortages were again evident in the Turkish manufacturing sector in April, while currency weakness led to inflationary pressures building again,” said Andrew Harker, associate director of IHS Markit.

But the biggest driver of risk on Thursday was the reaction to the Fed, where for all the intense political pressure to ease policy and the mixed growth/inflation data, the central bank held the line on Wednesday and refused to signal anything other than it was still on pause as Reuters put it.

Although the Fed made the predicted 5 basis point cut to the interest it pays on banks’ excess reserves – a technical move to ease money market tightness as it runs down its balance sheet – chair Powell was unwavering on the rate outlook and said the recent relapse in inflation rates was likely temporary.

“The market has gotten perhaps ahead of itself in quite confidently pricing in (U.S) interest rate cuts,” said Michael Metcalfe, head of global macro strategy at State Street Global Markets. “Powell was quite dismissive of the latest downturn in inflation… which I think has caused the market to reassess that a little bit.”

Emerging markets steadied from Wednesday’s knee-jerk sell-off as the US spike slowed down, and investors weighed the Fed’s comments for clues on the global-growth outlook. The EM benchmark index rose for a second day, while an index developing-nation currencies was little changed, as the focus turned to the next big catalyst for risk sentiment – the U.S. jobs report due Friday.

In rates, most government bonds in Europe initially tracked the slide in Treasuries, though they reversed declines to edge higher after data showed the euro area’s manufacturing slump extended into a third month. Dollar bonds of shorter tenors from Ukraine to Turkey advanced, with money managers saying the asset class has received a new lease of life from the Fed’s pause on rate moves.

The Bloomberg Dollar Index was little changed after rising 0.1 percent on Wednesday; the dollar index drifted around 97.600 against its set of major currency peers after going as high as 97.728 and hovering around $1.1211 to the euro and $1.305 to Britain’s pound after the Bank of England kept its rates on hold. An increase in Treasury yields helped to narrow the premium on emerging-market sovereign bonds. Manufacturing data from Asia suggested the worst may be over for the region. “Emerging-market credit is holding up reasonably well,” BlueBay strategist Tim Ash told Bloomberg. “It is emerging as the asset of choice in the EM space as people feel nervous about investing in local currencies and local markets given enduring dollar strength and the U.S.-EM growth differential.”

In commodities, the drop in oil prices came after US crude production output set a new record, though the losses were capped by the intensifying crisis in Venezuela and the stopping of Iranian oil sanction waivers by Washington. US crude was last off 27 cents at $63.32 a barrel while Brent slipped 33 cents to $71.86. Copper was at a two month low after a heavy tumble on Wednesday, while spot gold was marginally weaker at $1,271.55 an ounce.

Looking at today’s calendar, durable goods orders, factory orders and initial jobless claims are due. Scheduled earnings include DowDuPont, Gilead Sciences and Cigna.

Market Snapshot

- S&P 500 futures up 0.2% to 2,927.25

- STOXX Europe 600 down 0.3% to 389.82

- MXAP down 0.02% to 162.64

- MXAPJ up 0.1% to 540.16

- Nikkei down 0.2% to 22,258.73

- Topix down 0.2% to 1,617.93

- Hang Seng Index up 0.8% to 29,944.18

- Shanghai Composite up 0.5% to 3,078.34

- Sensex up 0.2% to 39,093.26

- Australia S&P/ASX 200 down 0.6% to 6,338.41

- Kospi up 0.4% to 2,212.75

- German 10Y yield rose 1.9 bps to 0.032%

- Euro up 0.2% to $1.1215

- Brent Futures down 0.8% to $71.59/bbl

- Italian 10Y yield fell 2.9 bps to 2.184%

- Spanish 10Y yield rose 0.8 bps to 1.009%

- Brent Futures down 0.8% to $71.59/bbl

- Gold spot down 0.5% to $1,270.65

- U.S. Dollar Index down 0.1% to 97.55

Top Overnight Headlines from Bloomberg

- It’s possible for U.S. and China to announce a trade deal by May 10 as Chinese Vice Premier Liu heads to Washington for further talks next week, CNBC reported, citing people familiar with matter

- Theresa May and her arch political rival Jeremy Corbyn are both signaling they may be edging closer to a Brexit deal after a month of talks between their teams that seemed to be going nowhere

- U.K. Prime Minister May fired her defense secretary for revealing secret discussions about Huawei Technologies’s role in Britain, as she attempted to assert control over a government that has become dominated by the battle to succeed her

- BOC Governor Stephen Poloz said he still believes policy interest rates would likely need to rise if the slew of factors slowing the expansion vanish

- European Union warned about greater transatlantic political tensions after President Trump decided to let U.S. citizens file lawsuits over property confiscated in Cuba during the 1959 revolution

- Federal Reserve Chairman Jerome Powell pushed back against pressure for interest-rate cuts from traders and President Donald Trump, saying inflation will rebound and the economy will stay healthy without fresh help from the central bank

- The Federal Reserve’s message of patience this week further relieves pressure on “resilient” economies across Asia, said a regional body

- The euro area’s manufacturing slump showed tentative improvement in April as Italy’s contraction slowed markedly and French industry stopped shrinking

Asian equity markets were mixed as the region partially shrugged off the negative lead from US where all major indices were pressured, and the S&P 500 snapped a 3-day streak of record closes after Fed Chair Powell downplayed prospects for looser policy at the post-FOMC presser. ASX 200 (-0.6%) traded negative with the index led lower by financials after AMP Capital reported net cash outflows widened in Q1 and with ‘Big 4’ bank NAB also weighed after it lowered its interim dividend by 16%. Elsewhere, both KOSPI (+0.4%) and Hang Seng (+0.8%) recovered from early losses on return from Labour Day holidays amid US-China trade optimism as reports suggested a trade deal could be possible by the end of next week, while China also recently announced several measures to open up its financial sector to foreign companies in a concession to the US. As a reminder, Japan and mainland China remained closed for holidays.

Top Asian News

- Huawei is Said to Hold Fixed-Income Investor Meetings in Asia

- Naval Ships Deployed as India Braces for Worst Storm Since 2014

- AIA Hits High After China Plan to Open Up Financial Industry

Major European indices have traded indecisively this morning [Euro Stoxx 50 -0.3%], as the region struggles to find direction post-FOMC where US indices were subdued but Asia did manage to somewhat shrug off the negativity. It is also worth bearing in mind that markets are playing catchup due to yesterday Labour Day holiday for much of Europe which may account for some of the volatility. Sectors are subdued this morning, although there was some mild outperformance in Healthcare and utility names at the open. This morning’s notable earnings release came from Shell (+2.3%) who beat on their Q1 adj. profit and have begun the next tranche of their share buyback programme, with the heavyweight lifting energy names higher in-spite of lower oil prices. Separately, Volkswagen (+4.5%) are towards the top of the Stoxx 600 after beating on Q1 revenue and confirming their FY outlook for car sales. Also of note are Bayer (+3.3%) whose share prices are supported this morning by the US Environmental Protections agency stating that glyphosate is not a carcinogen. Elsewhere Lloyds (-1.0%) are in the red post-earnings as the Co’s Q1 statutory pre-tax profit missed on Co. complied estimates, Lloyds have also made an additional PPI provision of GBP 100mln.

Top European News

- Volkswagen Gains After Profit Rises, Confirms Annual Targets

- Watches of Switzerland Considers IPO as Apollo Reduces Stake

- Deutsche Bank Said to Have Virtually No New Plan for What’s Next

In FX, although the Greenback has a lost a degree of its post-Powell recovery momentum, the index remains above 97.500 and on a more stable footing as the Fed chair refrained from flagging any shift towards a rate cut or even a hint that soft inflation could tip the policy balance from neutral to dovish. In fact, after the 5 bp IOER reduction he stressed that the move was technical rather than fundamental and repeatedly downplayed slowing price developments as transitory. Hence, the DXY has rebounded from sub-97.200 lows and just above a Fib support level (97.121), albeit with the Buck now mixed vs G10 peers.

- EUR – The single currency has drawn a bit more encouragement from the run of Eurozone manufacturing PMIs, as all bar Germany posted better than expected headlines, including Italy that rebounded relatively firmly following a return to GDP growth in Q1. Eur/Usd is back above 1.1200 as a result having probed a few pips below the 200 HMA at 1.1194, but the headline pair may be hampered by heavy option expiry interest stretching from 1.1200-10 through 1.1225-40 and up to 1.1250 (1.5 bn, 2 bn and 1.1 bn respectively). Moreover, chart resistance could cap the upside given the 30 DMA at 1.1236 and a Fib at 1.1242.

- NZD/AUD – The Kiwi and Aussie are marginally outperforming vs major counterparts amidst reports that a US-China trade accord may be in the offing as soon as next week and at the end of the next talks to take place in Washington, with Beijing said to be offering concessions in return for a recent olive branch from the US. Nzd/Usd is hovering between 0.6620-39 and Aud/Usd within a 0.7012-29 range as the Aud/Nzd cross sits just under 1.0600 and attention down under turns towards next week’s RBNZ and RBA policy meetings (notwithstanding NFP tomorrow of course). Both rate calls are seen tight with swap pricing not far from evens for easing, but as NAB contends that it may be to early for the RBA options are indicating higher break-evens as a result (circa 80 pips).

- GBP/CAD/CHF/JPY – All on a more even keel vs the Greenback, with Cable straddling 1.3050 and braced for BoE super Thursday after only deriving modest support from a return to growth in the UK construction sector. However, the Pound is consolidating gains relative to the Euro over 0.8600 amidst some talk that 1 MPC voter could break ranks and switch into hike mode – full preview on the headline feed and via the Research Suite. Conversely, the Loonie is struggling to hold above 1.3450 against the backdrop of ongoing weakness in oil prices, while the Franc is back down near 1.0200 and sub-1.1400 against the Euro in wake of weak Swiss retail sales and a contractionary manufacturing PMI. The Yen has also retreated from Wednesday’s pre-FOMC peaks through 111.50 and the 30 DMA (111.42) into decent option expiries (1.2 bn between 111.50-55).

- NOK/SEK – Disappointing Scandi manufacturing PMIs vs consensus and previous readings have soured sentiment to a degree, but Eur/Nok has also been driven higher by the aforementioned crude retracement, to 9.7400+ at one stage vs Eur/Sek topping out just shy of 10.7050.

In commodities, Brent (-1.0%) and WTI (-0.9%) prices are lower, with oil prices subdued as this week’s large crude stockpile builds overshadows Iranian waiver woes and Venezuela concerns, although some of downside in the complex could be attributed to a firmer post-FOMC Dollar. In terms of recent newsflow Russia’s April oil production stood at 11.23mln BPD vs. 11.3mln in March, with these levels being relatively in-fitting with recent IFX reports. Additionally, the Russian Energy Ministry have stated that they are to keep May’s production in-line with the prior agreements; which was agreed at a reduction of 228k BPD (from the October baselines of 11.4mln BPD) in the OPEC pact. Gold (-0.5%) was also afflicted by the surge in the Dollar, with the yellow metal unable to recover from this downside, in spite of the Buck easing off highs, and is currently trading firmly at the bottom of its USD 7/oz range. While copper prices are still around 2-month lows as the red metal is missing the support of its largest buyer China which is on Labour Day holiday for the remainder of the week.

US Event Calendar

- 7:30am: Challenger Job Cuts YoY, prior 0.4%

- 8:30am: Initial Jobless Claims, est. 215,000, prior 230,000; Continuing Claims, est. 1.66m, prior 1.66m

- 8:30am: Nonfarm Productivity, est. 2.2%, prior 1.9%; Unit Labor Costs, est. 1.5%, prior 2.0%

- 9:45am: Bloomberg Consumer Comfort, prior 60.8

- 10am: Factory Orders, est. 1.5%, prior -0.5%; Factory Orders Ex Trans, prior 0.3%

- 10am: Durable Goods Orders, prior 2.7%; Durables Ex Transportation, prior 0.4%

- 10am: Cap Goods Orders Nondef Ex Air, prior 1.3%; Cap Goods Ship Nondef Ex Air, prior -0.2%

DB’s Jim Reid concludes the overnight wrap

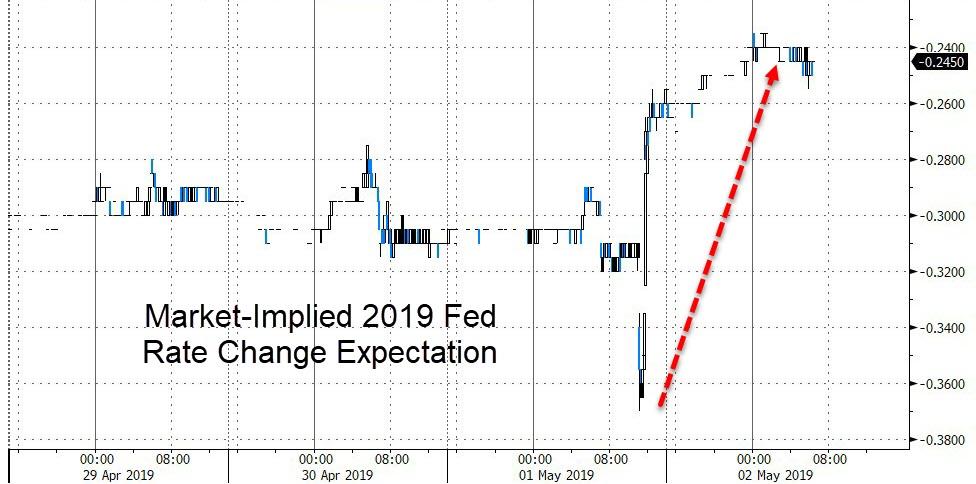

Needless to say, the focus yesterday in markets was on the Fed meeting, and though the eventual outcome was broadly in line with expectations, we did finally see a return of some volatility after the statement’s release and subsequent press conference. The only change in policy was a 5bps cut to the IOER, though that was just a technical adjustment and not a monetary policy signal. The S&P 500 initially rallied on dovish expectations, but then retraced to end the day -0.75% lower for the biggest decline since March as Powell spoke hawkishly about the inflation and growth outlook at his press conference.

Indeed, markets made a bit of a u-turn between the statement and press conference. First, Treasury yields fell as much as -4.9bps to touch 2.453% and the S&P 500 advanced as much as +0.29% to a new intraday all-time high. The reason for the rally was the initially dovish Fed statement, which contained few changes but did change the assessment on inflation from “near 2%” to “have declined and are running below 2%.” That was interpreted as a signal that the committee is more concerned about weak inflation data, which could be a catalyst to justify a rate cut in the near or medium term. However, in his press conference, Powell emphasized that recent inflation weakness is expected to be “transient or idiosyncratic” and that he doesn’t see a strong case for a move in either direction.Even when prompted about how he would respond to a downside surprise, he explicitly stopped short of endorsing a rate cut. He also spoke positively about the growth outlook in China and Europe, and said that financial conditions are accommodative. All in all, he sounded more optimistic about the economy than expected. Our US economists last night reiterated their view that they expect the Fed to remain patient and keep rates steady for the foreseeable future. See their note here .

Powell’s comments caused markets to promptly reprice, with bond yields completely reversing their moves. 10y yields ended the session flat at 2.501%, though they had already fallen earlier in the session after the weak ISM report – more on that below – so they ended net higher after all the Fed drama was done. 2y yields rose +3.8bps and the 2s10s curve, which had steepened over one basis point after the Fed’s statement, retraced to end -4.0bps flatter at 19.3bps. Along with the S&P 500’s retreat, the NASDAQ and DOW ended -0.56% and -0.61%, with losses fairly widespread. In fact, 83% of S&P 500 companies ended lower, the highest ratio in over five weeks and third worst day of the year. The dollar rallied +0.21%, which was +0.53% off its intraday lows, with losses spread evenly between the euro (-0.17%) and a basket of EM currencies (-0.17%). WTI oil prices mirrored the dollar’s move, falling -0.49%, though the big driver was data that showed another large build in US inventories.

This morning Asia has followed in a slightly more mixed fashion, however the various holidays in Japan and China have sapped some liquidity out of the market. Of those open, the Hang Seng (+0.63%) and Kospi (+0.41%) are both up, however the ASX (-0.67%) has retreated. US futures are also slightly positive. The gains in Hong Kong and Korea seem to have got a boost from news out of CNBC that a US-China trade deal is “possible” by next Friday. Politico is also reporting that the two sides are close to an agreement and that the plan being put forward is for the US to remove a 10% tariff on a portion of the $200bn of Chinese imports hit by tariffs, before lifting the rest not long after. However, the article also suggests that a 25% tariff on $50bn of Chinese goods would stay in place longer and possibly until after the 2020 election.

That story comes as US-China trade talks wrapped up in Beijing yesterday. Treasury Secretary Mnuchin confirmed in a tweet that the meetings had been “productive” and that talks between both sides will continue in Washington DC next week. So, we’re nearing the business end of talks at last it seems.

The other highlight for markets yesterday was the US data and most notably that much softer than expected ISM manufacturing report. The 52.8 reading for April came in well below expectations for 55.0 and represented a drop of 2.5pts from March. It was also the lowest reading since October 2016 and it means that the current level is now 8pts below the August 2018 peak. The breakdown was also soft with the employment component dropping over 5pts to 52.4, new orders also down over 5pts to 51.7 and most notably the prices paid component falling over 4pts to 50.0. The associated statement highlighted Mexico/US border crossing delays on numerous occasions as slowing supplier deliveries.

Prior to this and in contrast to the ISM data, we got a much stronger than expected April ADP employment change print (275k vs. 180k expected) which also included upward revisions to the March data. In fact, it was the strongest monthly reading since July 2018 and continues the theme of the labour market still being incredibly strong. A reminder that we’ve got the April employment report tomorrow. The only other notable US data yesterday was the April vehicle sales figures, which fell to 16.4mn, the lowest level since August 2017. That’s still higher than every month from mid-2007 through early 2014, so not a cause for alarm yet.

In Europe, it was only the UK that was open of the main markets, with the FTSE 100 closing -0.44% and Gilt yields falling -3.4bps. Sterling also ended +0.14%, despite the dollar’s broad strength, after the April manufacturing PMI was confirmed at 53.1 – matching the consensus – and therefore down 2pts from March. In addition, mortgage approvals in March were confirmed as declining to 62.3k and the least since 2017. Consumer credit was also the weakest since 2013 at just £0.5bn and therefore continues a declining trend for consumer lending in the UK. All-in-all this just means more confusing data to untangle for the BoE – which as a reminder meet today at lunchtime.

Staying with the UK, the Brexit newsflow is starting to slowly creep back onto our screens. The last couple of days have seen both the Conservatives and Labour talk up recent progress and especially compromise on a customs union, with PM May seen to be pushing for a deal being reached next week and ahead of the EU elections in just three weeks now. It’s worth flagging that the UK local elections are today, where an expected bad result for May will only increase pressure to a reach a deal sooner rather than later.

In other news, the ECB’s Guindos said yesterday that the ECB is “open-minded” to discussions around changing the inflation target, but haven’t yet discussed anything. This is similar to recent comments fellow policy maker Rehn made. This morning we’ve got the final April manufacturing PMIs in Europe where the consensus is for no change in the 47.8 flash reading for the Euro Area. A reminder that this included sub-50 readings for Germany (44.5) and France (49.6) while Italy is forecast to print at 47.8 which is only a marginal improvement on the very soft March reading. Spain is forecast to improve to 51.2. Those readings will be drip fed from 8am BST.

To the day ahead now, where this morning the focus is on those aforementioned final April PMIs in Europe. The focus after that turns to the BoE meeting where no policy change announcement is expected, however our UK economists expect the tone to be marginally hawkish given stronger than expected growth a tight labour market coupled with weaker rate expectations. This afternoon in the US we’ve got another busy slate of data releases with claims, preliminary Q1 nonfarm productivity and unit labour costs, and final March durable, capital and factory orders data all due. We’ve also got comments due from the ECB’s Hansson this morning and then Praet this evening, while from today US waivers on purchases of Iranian oil officially expire. The earnings highlights today include Shell, Volkswagen, DowDupont, BNP and Lloyds.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED //Hang Sang CLOSED DOWN 48.85 POINTS OR .22% /The Nikkei closed Australia’s all ordinaires CLOSED DOWN 56%

/Chinese yuan (ONSHORE) closed UP at 6.7345 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 63.26 dollars per barrel for WTI and 71.38 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.7345 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7379/ TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

i)China/USA

4/EUROPEAN AFFAIRS

The pound first rises and then dumps after the Bank of England signals that one more hike is needed. Then strangely they cut inflation forecasts.

(courtesy zerohedge)

Pound Jumps And Dump After BOE Signals More Than One Hike Needed, But Cuts Inflation Forecasts

There were no surprises in today’s BOE policy decision: the central bank held rates unchanged as expected, in a unanimous decision which gave today’s decision a less hawkish sentiment as some expected one policymaker may break ranks by voting for a hike.

Bank of England

✔@bankofengland

We have kept interest rates at 0.75%. Find out why in our visual summary: https://b-o-e.uk/2ITXIBB #InflationReport

Where there was some surprise was in the bank’s assessment of the monetary policy path and the BOE’s forecast of economic conditions. But first, here are the some of the highlights from today’s decision, courtesy of RanSquawk:

- Growth: the BOE has done a U-turn on its forecasts from the February meeting, raising the growth forecast for this year to 1.5% from 1.2% (BBG). However, the reasons for that rise might not be that encouraging, as part of it comes from companies stockpiling for Brexit. GDP is now expected to have grown by 0.5% in Q1 2019 vs. March view of 0.3%. This boost is expected to be temporary with Q2 growth expected to slow to 0.2%.

- Rates: Projections in the accompanying QIR are based on a path for the Bank rate that rises to around 1% by the end of the forecast horizon. (Lower than Feb assumption of 1.1%). Note, the MPC make reference to recent global developments as a factor behind this.

- Brexit: The MPC’s projections continue to assume a smooth adjustment to the average range of possible outcomes for the UK’s eventual trading relationship with the EU. The release doesn’t provide any major update on the MPC’s view on the latest extension to the Brexit deadline.

- Inflation: Headline CPI in March of 1.9% was was inline with the Feb QIR and expectations at the Bank immediately prior to the release. Over the coming months, CPI was expected to remain fairly close to the 2% target, picking up slightly in April before easing back to just below target.

- Investment: The marginally below potential growth in underlying growth is continuing to have a particularly pronounced impact on business investment. Investment is expected to pick-up at the end of the forecast period.

- Labor: The labor market remains tight, with the unemployment rate expected to fall to 3.5% by the end of the forecast period.

- Wages: Annual pay growth remains around 3.5% whilst unit labour costs have strengthened to rates that are above historical averages

On Brexit, via BBG:

- The BOE said that the delay to Brexit had, effectively, made no difference to their economic outlook, and continue to base their forecasts on a smooth outcome

- They also noted that the economy’s performance still depends significantly on the “nature and timing” of Brexit

- Officials also said that Brexit is causing more volatility in economic reports, particularly in private surveys, and noted data may be providing less of a signal than usual about the medium-term outlook

- They particularly highlighted the impact of Brexit-related stockpiling on the U.K.’s better-than-expected performance at the start of 2019, saying it likely pushed up growth in the first quarter by around 0.1 percentage point

- The BOE also flagged reports from its network of agents that said Brexit is pushing down already weak investment intentions, and that there could be some catch-up as clarity about the outcome emerges

In summary: on one hand, the central bank upgraded its growth outlook for this year to 1.5% from 1.2% and also raised its predictions for 2020 and 2021, while cutting the forecast for the unemployment rate and maintaining the limited, gradual rate hikes will be needed and noting that inflation may be above target in 2 years at current market rates, which sent cable spiking higher in kneejerk reaction.

However, cable then broadly sold off after the market noticed that the BOE cut its inflation forecasts for 2019, 2020, and kept it unchanged for 2021, while conceding that nobody really knows anything, and that economic indicators may be volatile in coming months.

One possible reason for the post-kneejerk reversal in cable: too much hawkishness had been priced in, as ahead of the meeting, banks including JPMorgan, Citigroup Inc. and Toronto Dominion Bank saw scope for a hawkish signal from the BOE ahead of the meeting. And the signal they got was not hawkish enough.

Separately, in the broader market reaction, gilts edged higher, paring underperformance versus bunds, as money markets now see 28% probability of a BOE hike this year versus 35% before the decision, in what ultimately appears to have been a dovish disappointment.

end

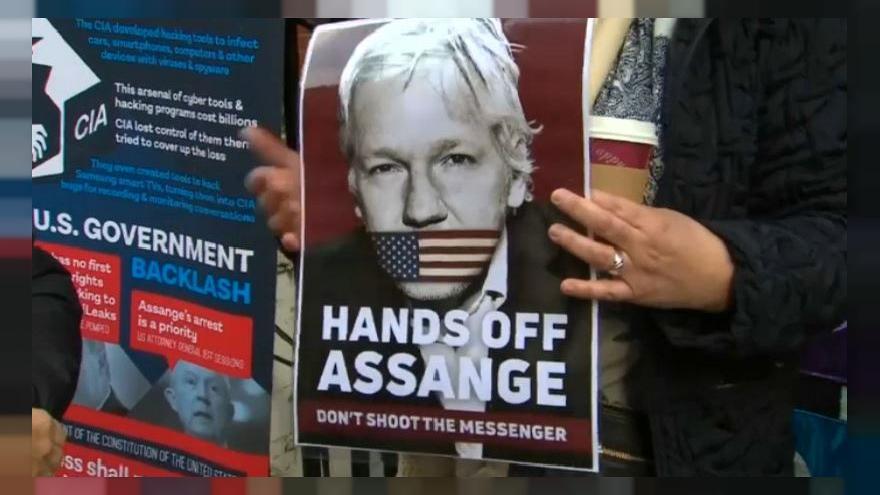

Today begins Assange’s extradition hearing

(courtesy zerohedge)

Thursday’s Extradition Hearing “Life & Death” For Assange And Journalism Itself

Following Julian Assange’s UK court sentencing early Wednesday where he was hit with 50 weeks in prison for skipping bail, which we noted earlier is close to the maximum sentence, WikiLeaks Editor-in-Chief Kristinn Hrafnsson slammed the “vindictive” punishment as having caused “shock and outrage” in statements to reporters.

However, Hrafnsson said after the court that the “real battle” begins Thursday, which marks the start of US extradition hearings for Assange, set to begin at 10AM (UK) at the Westminster Magistrate Court. He called it a matter of “life and death” for Assange, and ultimately for the journalistic profession itself.

Hrafnsson noted that the outcome of the US extradition hearing could prove a watershed moment for the future of journalism: “Tomorrow is the first step in a long battle, so the fight will certainly continue. This is the fight for press freedom, primarily, as we’ve always stated.”

Hrafnsson stressed further: “That is a real battle, it’s not just for Julian Assange – even though for him it’s a question of life and death – it is most certainly a question of perseverance [over] a major journalistic principle,” in statements made after Assange’s sentencing stemming from the 2012 bail related charges.

Concerning Wednesday’s stiff sentence for skipping bail – close to one year in prison – WikiLeaks later issued the following statement:

WikiLeaks

✔@wikileaks

Julian Assange’s sentence, for seeking and receiving asylum, is twice as much as the sentencing guidelines. The so-called speedboat killer, convicted of manslaughter, was only sentenced to six months for failing to appear in court.

Reuters summarizes the specific charges the US will seek to extradite him on as follows:

The U.S. Justice Department said Assange was charged with conspiring with former Army intelligence analyst Chelsea Manning to gain access to a government computer as part of a 2010 leak by WikiLeaks of hundreds of thousands of U.S. military reports about the wars in Afghanistan and Iraq and American diplomatic communications.

Last week WikiLeaks and a German online magazine published the contents of a letter sent by the US Department of Justice (DOJ) to a former WikiLeaks staff member which suggests US officials are attempting to put together a case against Julian Assange based on the Espionage Act.

The DOJ letter addressed to former WikiLeaks spokesman Daniel Domscheit-Berg for the intent of requesting an interview outlined “possible violations of United States federal criminal law regarding the unauthorized receipt and dissemination of classified information,” according to a translation from the German, later published to WikiLeaks’ official social media.

Crucially, conviction under the 1917 law geared toward protecting the nation’s military secrets and most sensitive security matters could result in life in prison or even the death penalty for Assange.

But all of this is of course conditioned on whether or not the UK ultimately grants the Untied States’ extradition request, the first step in the process of which comes Thursday morning.

end

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

6.GLOBAL ISSUES

This is a huge Bellwether for the USA economy. Semi conductor chip sales are a good indicator for growth in the USA economy and for that matter, the globe. Today we find that the entire global semiconductor sales have collapsed by a huge 15.5% in the first quarter of 2019:

(courtesy zerohedge)

7 OIL ISSUES

8. EMERGING MARKETS

VENEZUELA

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:00 AM….

Euro/USA 1.1208 UP .0005 REACTING TO MERKEL’S FAILED COALITION/ REACTING TO +GERMAN ELECTION WHERE ALT RIGHT PARTY ENTERS THE BUNDESTAG/ huge Deutsche bank problems ///ITALIAN CHAOS /AND NOW ECB TAPERING BOND PURCHASES/JAPAN TAPERING BOND PURCHASES /USA RISING INTEREST RATES /FLOODING/EUROPE BOURSES /RED EXCEPT GERMANY

USA/JAPAN YEN 111.49 UP 0.045 (Abe’s new negative interest rate (NIRP), a total DISASTER/NOW TARGETS INTEREST RATE AT .11% AS IT WILL BUY UNLIMITED BONDS TO GETS TO THAT LEVEL…

GBP/USA 1.3054 UP 0.0007 (Brexit March 29/ 2019/ARTICLE 50 SIGNED/BREXIT FEES WILL BE CAPPED/BREXIT EXTENDED TO OCT 31/2019//

USA/CAN 1.3434 DOWN .0005 CANADA WORRIED ABOUT TRADE WITH THE USA WITH TRUMP ELECTION/ITALIAN EXIT AND GREXIT FROM EU/(TRUMP INITIATES LUMBER TARIFFS ON CANADA/CANADA HAS A HUGE HOUSEHOLD DEBT/GDP PROBLEM)

Early THIS THURSDAY morning in Europe, the Euro ROSE BY 5 basis points, trading now ABOVE the important 1.08 level RISING to 1.1208 Last night Shanghai COMPOSITE CLOSED HOLIDAY

//Hang Sang CLOSED UP 245.07 OR .53%

/AUSTRALIA CLOSED DOWN .56%// EUROPEAN BOURSES RED EXCEPT GERMAN DAX

The NIKKEI: this THURSDAY morning CLOSED DOWN 48.85 POINTS OR .22%

Trading from Europe and Asia

1/EUROPE OPENED RED EXCEPT GERMANY/

2/ CHINESE BOURSES / :Hang Sang CLOSED UP 245.07 POINTS OF .53%

/SHANGHAI CLOSED HOLIDAY

Australia BOURSE CLOSED DOWN 56%

Nikkei (Japan) CLOSED DOWN 48.85 POINTS OR .22%

INDIA’S SENSEX IN THE RED

Gold very early morning trading: 1271.80

silver:$14.67

Early THURSDAY morning USA 10 year bond yield: 2.52% !!! UP 2 IN POINTS from WEDNESDAY’S night in basis points and it is trading WELL ABOVE resistance at 2.27-2.32%.

The 30 yr bond yield 2.91 UP 2 IN BASIS POINTS from YESTERDAY night.

USA dollar index early THURSDAY morning: 97.59 DOWN 10 CENT(S) from WEDNESDAY’s close.

This ends early morning numbers THURSDAY MORNING

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now your closing THURSDAY NUMBERS \12: 00 PM

Portuguese 10 year bond yield: 1.11% DOWN 1 in basis point(s) yield from WEDNESDAY/

JAPANESE BOND YIELD: -.04% DOWN 0 BASIS POINTS from WEDNESDAY/JAPAN losing control of its yield curve/

SPANISH 10 YR BOND YIELD: 1.00% DOWN 0 IN basis point yield from WEDNESDAY

ITALIAN 10 YR BOND YIELD: 2.55 DOWN 1 POINTS in basis point yield from WEDNESDAY/

the Italian 10 yr bond yield is trading 155 points HIGHER than Spain.

GERMAN 10 YR BOND YIELD: RISES +.03% IN BASIS POINTS ON THE DAY//

THE IMPORTANT SPREAD BETWEEN ITALIAN 10 YR BOND AND GERMAN 10 YEAR BOND IS 2.52% AND NOW ABOVE THE THE 3.00% LEVEL WHICH WILL IMPLODE THE ENTIRE ITALIAN BANKING SYSTEM. AT 4% SPREAD THERE WILL BE A MASSIVE BANK RUN…

END

IMPORTANT CURRENCY CLOSES FOR THURSDAY

Closing currency crosses for THURSDAY night/USA DOLLAR INDEX/USA 10 YR BOND YIELD/1:00 PM

Euro/USA 1.118338OWN .0019 or 19 basis points

USA/Japan: 111.15 DOWN 0.065 OR YEN UP 7 basis points/

Great Britain/USA 1.3071 UP .0028 POUND UP 28 BASIS POINTS)

Canadian dollar DOWN 34 basis points to 1.3473

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The USA/Yuan,CNY closed AT 6.7345 0N SHORE (DOWN)

THE USA/YUAN OFFSHORE: 6.7471 (YUAN DOWN)

TURKISH LIRA: 5.9690 EXTREMELY DANGEROUS LEVEL.2

the 10 yr Japanese bond yield closed at -.04%

Your closing 10 yr USA bond yield UP 8 IN basis points from WEDNESDAY at 2.55 % //trading well ABOVE the resistance level of 2.27-2.32%) very problematic USA 30 yr bond yield: 2..94 UP 5 in basis points on the day

Your closing USA dollar index, 97.77 UP 8 CENT(S) ON THE DAY/1.00 PM/

Your closing bourses for Europe and the Dow along with the USA dollar index closing and interest rates for THURSDAY: 12:00 PM

London: CLOSED DOWN 33.95 0.46%

German Dax : CLOSED UP 1.34 POINTS OR .01%

Paris Cac CLOSED DOWN 47.55 POINTS OR .55%

Spain IBEX CLOSED DOWN 152.40 POINTS or 1.59%

Italian MIB: CLOSED DOWN 176.95 POINTS OR 0.78%

WTI Oil price; 61.21 1:00 pm

Brent Oil: 69.78 12:00 EST

USA /RUSSIAN / ROUBLE CROSS: 65.54 THE CROSS HIGHER BY 0.70 ROUBLES/DOLLAR (ROUBLE LOWER BY 70 BASIS PTS)

TODAY THE GERMAN YIELD RISES TO +.03 FOR THE 10 YR BOND 1.00 PM EST EST

END

This ends the stock indices, oil price, currency crosses and interest rate closes for today 4:30 PM

Closing Price for Oil, 4:00 pm/and 10 year USA interest rate:

WTI CRUDE OIL PRICE 4:30 PM : 61/59

BRENT : 70.44

USA 10 YR BOND YIELD: … 2.55… STILL DEADLY//

USA 30 YR BOND YIELD: 2.94..VERY DEADLY

EURO/USA 1.1173 ( DOWN 29 BASIS POINTS)

USA/JAPANESE YEN:111.50 UP .048 (YEN DOWN 5 BASIS POINTS/..

USA DOLLAR INDEX: 97.83 UP 15 cent(s)/

The British pound at 4 pm: Great Britain Pound/USA:1.3034 DOWN 19 POINTS

the Turkish lira close: 5.9637

the Russian rouble 65.42 DOWN 58 Roubles against the uSA dollar.( DOWN 58 BASIS POINTS)

Canadian dollar: 1.3470 DOWN 32 BASIS pts

USA/CHINESE YUAN (CNY) : 6.7343 (ONSHORE)/

USA/CHINESE YUAN(CNH): 6.7472 (OFFSHORE)

German 10 yr bond yield at 5 pm: ,+0.03%

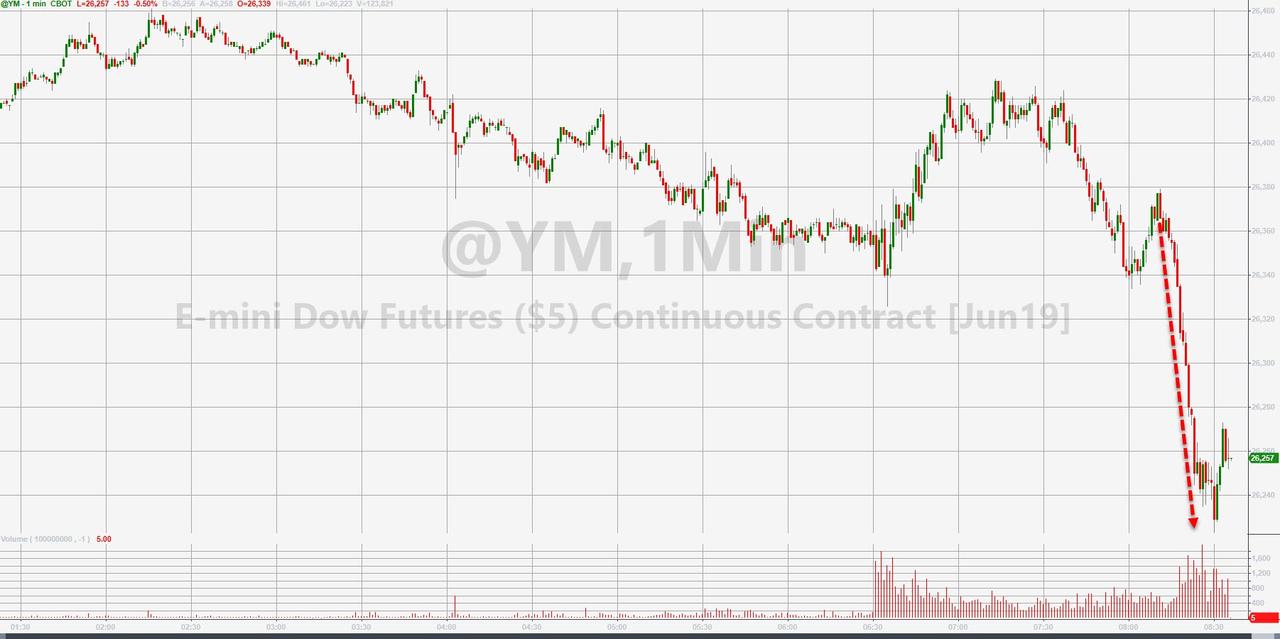

The Dow closed DOWN 122.35 POINTS OR 0.35%

NASDAQ closed DOWN 12.87 POINTS OR 0.16%

VOLATILITY INDEX: 14.45 CLOSED DOWN .35

LIBOR 3 MONTH DURATION: 2.575%//

FROM 2.575

And now your more important USA stories which will influence the price of gold/silver

TRADING IN GRAPH FORM FOR THE DAY/WEEKLY SUMMARY/FOLLOWED BY TODAY

The Last Time This Happened, Stocks Slumped 20%

The market asked Powell, “where’s the ‘dovish’ meat?” and he had no answer…and the market suddenly tightened its rate-cut expectations by 14bps!!

Powell translated:

Oh and in case you wondered where the meat was – it was here! Beyond Meat soars over 175% from its IPO price…

Chinese markets were closed overnight but European markets reopened weaker after US ended lower…

US markets tried to rebound from Powell’s mishap but headlines from China that the trade deal had reached an “impasse” sparked selling as Europe closed…

Nasdaq is suffering the most on the week for now.

The Dow is heading for its second down week in a row (the first consecutive loss since Dec 21st) – a terrifying thought – and as Nomura’s Charlie McElligott noted, CTAs have just flipped to 100% short…

NOTE – The cash Dow filled its gap from the 4/12 open

VIX spiked to almost 16 intraday before ramping back, but remains decoupled from stocks…

And bear in mind that VIX specs are at a record short…

Which, given VVIX’s surge today, makes us wonder if all those VIX shorts are buying VIX protection…

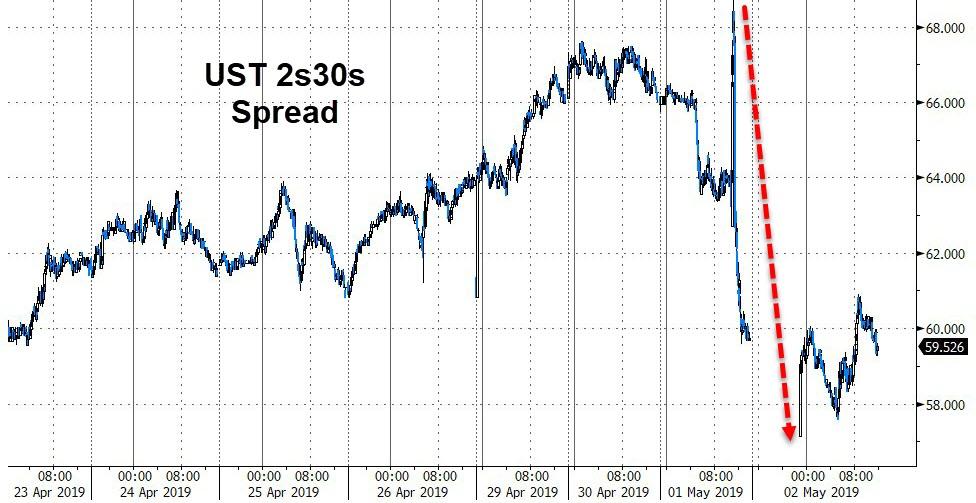

Treasury yields were higher across the curve today as Powell’s “transitory” hawkishness rippled up the curve… (the belly slightly underperformed +5bps vs the wings at +3.5bps)

The yield curve has flattened quite notably after an initially exuberant steepening…

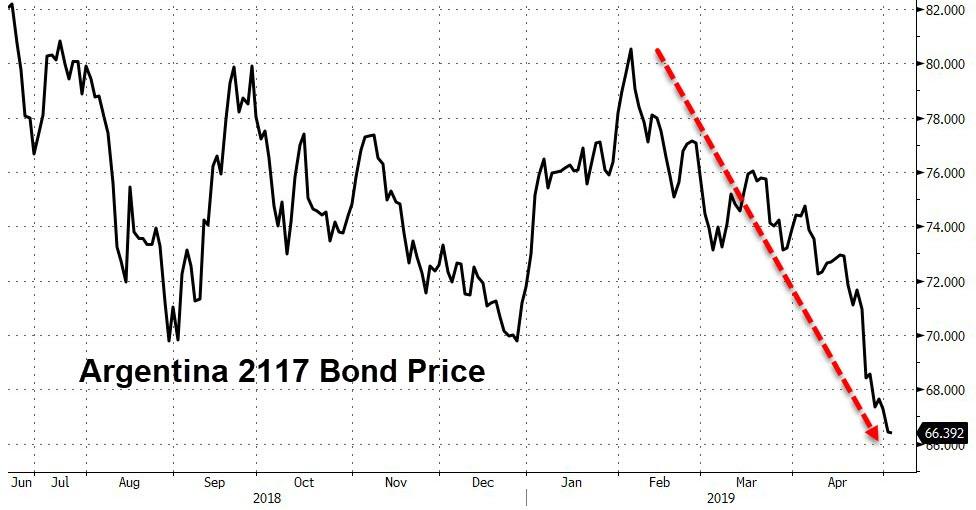

Still could be worse – could be Argentina’s Century Bonds (which just hit a new record low)…

Inflation breakevens continued to slide (along with crude prices)…

The Dollar extended yesterday’s gains post-Powell…

Yuan was pressured on the back of China trade deal “impasse” headlines…

Cryptos held on to gains today with Bitcoin best on the week…

WTI was the worst performer among the commodity complex but all drifted lower…

WTI traded very technically, breaking down to its 50DMA after breaking below its 200DMA, only to rebound back up to the 200DMA

Gold was smacked lower again, testing its 200DMA and bouncing hard once again…

Silver was also slapped to five-month lows…

And Dr.Copper collapsed through key technical levels to its lowest since mid Feb…

And finally, as BMO’s Brad Wishak highlighted, the world’s favorite (and also largest) index to completely ignore is flashing another negative divergence here…the exact same divergence that kicked off the the fall equity slide lower.

Back in SEP the SPX pushed to new all time highs while the NYSE did not, flagging the initial divergence. Y’day the SPX again made fresh all time highs with the NYSE again NOT confirming.

Is it different this time?

END

Market trading:/

Here’s Why Stocks Suddenly Tumbled