GOLD: $1280.15 UP $9.35 (COMEX TO COMEX CLOSING)

Silver: $14.95 UP 34 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1279.05

silver: $14.94

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 18/27

EXCHANGE: COMEX

CONTRACT: MAY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,269.700000000 USD

INTENT DATE: 05/02/2019 DELIVERY DATE: 05/06/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 18

690 C ABN AMRO 1

737 C ADVANTAGE 8 8

800 C MAREX SPEC 4

905 C ADM 15

____________________________________________________________________________________________

TOTAL: 27 27

MONTH TO DATE: 145

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 27 NOTICE(S) FOR 2700 OZ (0.0839 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 145 NOTICES FOR 14500 OZ (.4510 TONNES)

SILVER

FOR MAY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

362 NOTICE(S) FILED TODAY FOR 1,810,000 OZ/

total number of notices filed so far this month: 2901 for 14,505,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

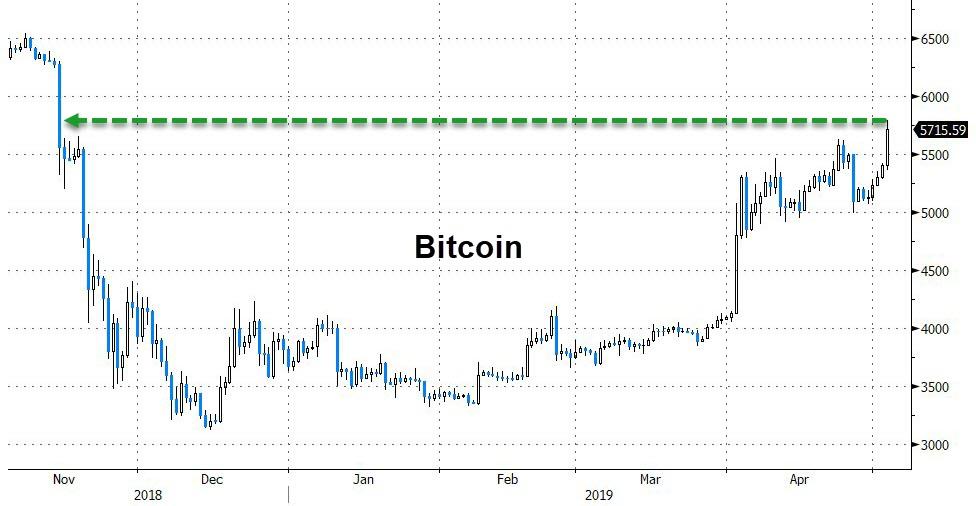

Bitcoin: OPENING MORNING TRADE :$5747 UP $237

Bitcoin: FINAL EVENING TRADE: $5756 UP 264

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A FAIR SIZED 762 CONTRACTS FROM 201,540 UP TO 202,302 DESPITE YESTERDAY’S 13 CENT FALL IN SILVER PRICING AT THE COMEX. ,LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR SILVER BUT IT NOW COMMENCES FOR GOLD. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR MAY, 0 FOR JUNE, 1157 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1157 CONTRACTS. WITH THE TRANSFER OF 1157 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1157 EFP CONTRACTS TRANSLATES INTO 5.79 MILLION OZ ACCOMPANYING:

1.THE 13 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

AND NOW 17.750 MILLION OZ STANDING FOR SILVER IN MAY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MAY:

6824 CONTRACTS (FOR 3 TRADING DAYS TOTAL 6824 CONTRACTS) OR 34.12 MILLION OZ: (AVERAGE PER DAY: 2274 CONTRACTS OR 11.37 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 34.12 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 4.87% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 775.97 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

RESULT: WE HAD A FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 965 DESPITE THE 13 CENT FALL IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1157 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS RESUMED THEIR LIQUIDATION OF THE SPREAD TRADES TODAY.

TODAY WE GAINED A STRONG SIZED: 1919 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1157 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 762 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 13 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.61 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

here is the COT up to April 30 and it is clear that we witnessed the liquidation of spreaders in silver

| Silver COT Report – Futures | |||||||

| Large Speculators | Commercial | Total | |||||

| Long | Short | Spreading | Long | Short | Long | Short | |

| 77,120 | 74,984 | 13,585 | 75,855 | 97,215 | 166,560 | 185,784 | |

| 1,231 | -1,015 | –4,530 | -14,545 | -13,177 | -17,844 | -18,722 | |

| Traders | |||||||

| 108 | 58 | 48 | 41 | 35 | 171 | 121 | |

| Small Speculators | |||||||

| Long | Short | Open Interest | |||||

| 30,050 | 10,826 | 196,610 | |||||

| -4,659 | -3,781 | -22,503 | |||||

| non reportable positions | Change from the previous reporting period | ||||||

| COT Silver Report – Positions as of | Tuesday, April 30, 2019 | ||||||

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.008 BILLION OZ TO BE EXACT or 144% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 362 NOTICE(S) FOR 1,810,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ AND NOW MAY: 17,750,000 OZ..

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A VERY STRONG SIZED 9,118 CONTRACTS, TO 442,992 DESPITE THE FALL IN THE COMEX GOLD PRICE/(A DROP IN PRICE OF $1.20//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6848 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 6848 CONTRACTS DECEMBER: 0 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 442,992. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A HUMONGOUS SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 15,966 CONTRACTS: 9118 OI CONTRACTS INCREASED AT THE COMEX AND 6848 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 15,966 CONTRACTS OR 1,599,600 OZ OR 49.66 TONNES. YESTERDAY WE HAD A LOSS IN THE PRICE OF GOLD TO THE TUNE OF $12.30….AND DESPITE THAT FALL, WE HAD A STRONG GAIN IN TONNAGE OF 49.66 TONNES!!!!!!.??????????????????????????????????????????

AS YOU WILL SEE, THE CROOKS HAVE NOW SWITCHED TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ENTER A NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

“YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF MAY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 18,261 CONTRACTS OR 1,826,100 OR 56.79 TONNES (3 TRADING DAYS AND THUS AVERAGING: 6087 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAYS IN TONNES: 56.79 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 56.79/3550 x 100% TONNES =0.627% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 1872.38 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUGE SIZED INCREASE IN OI AT THE COMEX OF 9118 DESPITE THE FALL IN PRICING ($12.30) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6848 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6848 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC GAIN OF 15,966 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6848 CONTRACTS MOVE TO LONDON AND 9118 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 49.66 TONNES). ..AND THIS STRONG DEMAND OCCURRED WITH A FALL IN PRICE OF $12.30 IN YESTERDAY’S TRADING AT THE COMEX. HOWEVER A HUGE PERCENTAGE OF THE GAIN IN OI WAS DUE TO THE COMMENCEMENT OF THE SPREADING OPERATION AS I HAVE OUTLINED ABOVE.

we had: 27 notice(s) filed upon for 2700 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $9.35 TODAY

STRANGE!!

ANOTHER BIG CHANGE IN GOLD INVENTORY AT THE GLD

A WITHDRAWAL OF 1.17 TONNES

INVENTORY RESTS AT 745.52 TONNES

IT LOOKS LIKE WE HAVE REACHED THE BOTTOM OF THE BARREL FOR PHYSICAL GOLD BEING SUPPLIED TO THE CROOKS.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 34 CENTS TODAY:

A BIG CHANGE IN SILVER INVENTORY AT THE SLV/

A DEPOSIT OF 843,000

/INVENTORY RESTS AT 315.691 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A FAIR SIZED 762 CONTRACTS from 201,540 UPTO 202,302 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE STOPPED THEIR LIQUIDATION IN SILVER BUT HAVE NOW MORPHED INTO GOLD..

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 0 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 1157 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1157 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 965 CONTRACTS TO THE 1157 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 1919 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 9.595 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL AND NOW 17.750 MILLION OZ FOR MAY

RESULT: A FAIR SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 13 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1157 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 15.84 POINTS OR .52% //Hang Sang CLOSED UP 137.37 POINTS OR .46% /The Nikkei closed //Australia’s all ordinaires CLOSED DOWN .04%

/Chinese yuan (ONSHORE) closed UP at 6.7345 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 63.26 dollars per barrel for WTI and 71.38 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.7345 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.74756/ TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A//NORTH KOREA/ SOUTH KOREA

NORTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/USA

Now it is Beijing that warns the uSA to compromise or else trade talks will collapse.

( zerohedge)

4/EUROPEAN AFFAIRS

i)GERMANY

The hopeless attempt to get these two losers together…merger talks collapse again

( zerohedge)

ii)Bill Blain on the greed of people/corporations

(Bill Blain)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

i)A good one: The interview of Bart Chilton with Chris Marcus: is this a voice from the grave?

( Ted Butler/GATA)

ii)With Moore gone, we are now witnessing a huge fight at the Federal Reserve. The Wall Street Journal has a high regard for Moore and are very upset that tactics were used to make him unelectable by the Senate.

(courtesy New York Sun/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//Jobs report

( zerohedge)

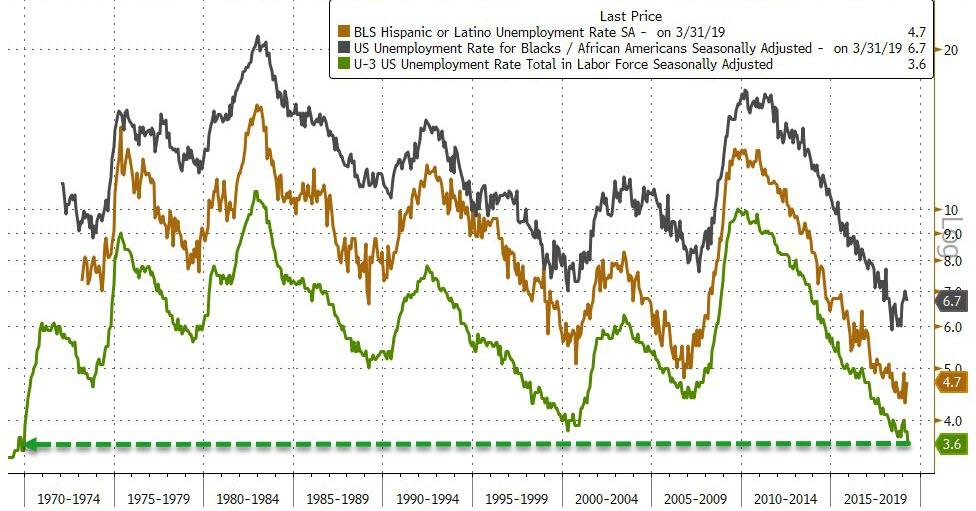

b)Trump will like this; Hispanic unemployment falls to record lows.

( zerohedge)

ii)Market data

The ISM data is much more reliable that Markit. Services sector is by far the better indicator for growth in the USA as the manufacturing sector has been falling for years. Today the ISM data shows that services has slumped to its weakest since 2017.

( zerohedge)

ii)USA ECONOMIC/GENERAL STORIES

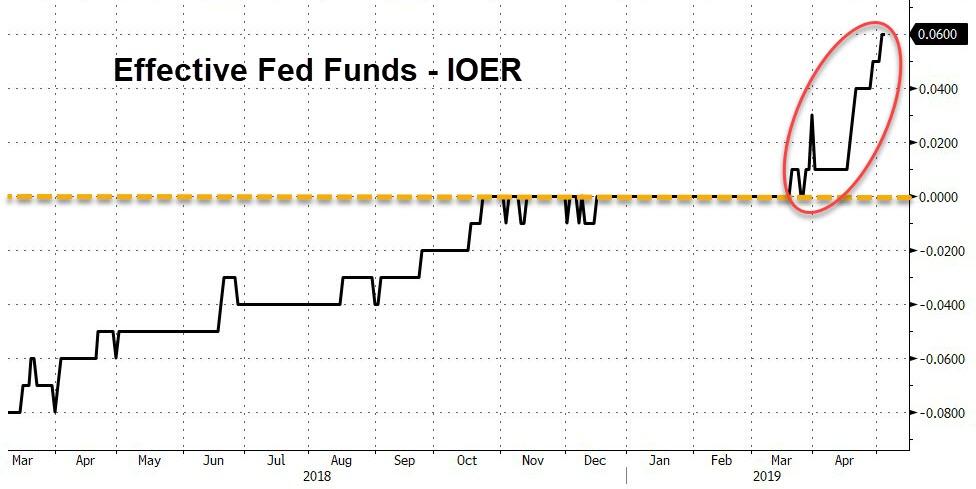

a)this is very technical but it is far more important to understand where this is heading. For years now the effective Fund rates have been in the middle of two rates: 1/ The IOER or the excess funds owned by the banks and which they loan back to the Fed and are paid a very high interest rates and 2. the lower floor Rep rate. If the Effective funds rate travels above the IOER it means that the Fed has a liquidity problem..the banks even though they have 1.5 trillion dollars in excess reserves….it is not enough and they need more liquidity. It generally means that the Fed is losing control.

( zerohedge)

SWAMP STORIES

As promised, Barr launches a wide ranging probe into the 2016 FBU spying and the genesis of the Trump Russian collusion hoax

( zerohedge)

Let us head over to the comex:

Gold withdrawals;

i) zero withdrawals.

Gold To Gain as Global Markets Brace for Turmoil: Reuters Poll

(Reuters) – A slowing global economy, stock market turmoil, delays to interest rate rises and potential U.S. dollar weakness are expected to boost average annual gold prices to their highest since 2013, a Reuters poll found.

Gold will average $1,322 an ounce this year and $1,369 in 2020, the median forecasts returned by the poll of 34 analysts and traders showed.

The forecasts were higher than those from a similar poll three months ago which saw averages of $1,305 this year and $1,350 in 2020.

Gold prices have slipped in recent weeks to around $1,280, under pressure from a stronger dollar, which makes bullion more expensive for buyers with other currencies, and rising stock markets which offered investors better returns.

Helping push gold lower, some investors have taken money out of gold-backed exchange-traded funds and speculators ramped up bets on lower prices on the Comex exchange, which now outnumber wagers on higher prices.

But analysts said slowing global economic growth, the increasing likelihood of stock market corrections, a pause in interest rate rises and a likely weakening of the dollar would bring money back to the metal.

Gold is traditionally seen as a safe place to invest during times of uncertainty, as it tends to retain its value while other assets slide.

“We expect falling risk appetite and a surge in safe-haven demand to be the key factor driving both gold and silver prices,” said Capital Economics analyst Ross Strachan.

Higher interest rates are bad for gold because they raise bond yields, making non-yielding bullion less attractive to investors.

A Reuters poll of 70 currency strategists showed they expected the U.S. dollar, which in April reached its strongest in almost two years, to slip over the coming year.

The gold forecast for this year is 4 percent higher than last year’s average price of $1,268 and would be the highest average since 2013.

But it suggests gold will struggle to break convincingly above recent peaks of $1,374.91 hit in 2016 and $1,366.07 last year – which together form strong technical resistance.

“We need a strong impetus to break that resistance,” said LBBW analyst Frank Schallenberger.

“(But) with central banks buying more and more gold … interest rates staying low and economic perspectives looking dull, gold will eventually go up,” he said.

For silver, poll respondents forecast an average price of $16.05 an ounce this year, up from $16 in the poll three months ago, and $17 in 2020, down from $17.20 in the previous poll.

Editors Note: We would prefer not to get into the forecasting and predictions business as “crystal ball gazing” is fraught with uncertainty at the best of times.

This is particularly the case in 2019 given the massive macroeconomic, geopolitical, monetary and systemic uncertainty and risk of today.

It is worth remembering that many, if not most, of the precious metal poll respondents (both Bloomberg and Reuters) were bearish in gold’s last bull market despite gold rising every year from 2003 to 2012.

We were one of the few respondents who were positive on gold in those years. Analysts who were bullish were only mildly so. Yet gold saw massive gains and was the best performing asset in those years, particularly during the global financial crisis from 2007 to 2011.

We expect gold and silver to again outperform stock and bond markets. U.S. equity markets, including the S&P 500, Nasdaq etc are back at all time record highs, while precious metal prices remain very undervalued. The record highs are largely due to the massive out-performance of the FAANG stocks, some of which saw serious selling pressure this week.

It is a great time to re-balance portfolios. It makes sense and is prudent to take profits from stocks and bonds at these levels and acquire safe haven gold.

What is far more important than the price of gold is the value of gold as a hedge and safe haven asset. This has been seen throughout history including during the global financial crisis and indeed in the academic and independent research on gold in recent years.

News & Commentary

Central Banks Are Ditching the Dollar for Gold (Bloomberg)

Central bank binge buying fuels red-hot gold demand – WGC (Reuters)

Gold poised for gains as global markets brace for turmoil: Reuters poll (Reuters)

Societe Generale resigns as London gold and silver market maker – (Reuters)

Turkish central bank to set up lira-for-gold swap market (Reuters)

Markets Have Misread the Fed (Bloomberg)

When central banks don’t understand the markets, watch out (Marketwatch.com)

Australia Is On The Brink Of A Housing Collapse That Resembles 2008 (Forbes.com)

In Memory of Bart Chilton (ArcadiaEconomics.com)

Bart Chilton: A voice from the grave? (Silverseek.com)

OECD is a clear and present danger to Irish prospects (IrishTimes.com)

Recent Market Updates

– Global Gold Demand Gains In Q1, 2019: Central Banks Buy Gold Bullion and ETFs See Inflows

– Newstalk Interview: Investors Looking To Store Gold In Dublin Rather Than London

– Australia and Many Property Markets To Crash Like Ireland?

– Death of Inflation and the Death of Equities?

– SWOT Analysis: Venezuela Sells $400 Million Worth Of Gold Bullion

– World’s Central Banks Want More Gold – India May Buy 1.5M Ounces In 2019

– Russia’s 2019 Gold Rush Continues: Buys 600,000 Ounces of Gold In March

– When Should You Sell Your Gold and Silver? (GoldCore Video)

– Understanding Gold: A Step By Step Guide To Gold As An Asset Class

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

A good one: The interview of Bart Chilton with Chris Marcus: is this a voice from the grave?

(courtesy Ted Butler/GATA)

Ted Butler: A voice from the grave?

Submitted by cpowell on Thu, 2019-05-02 21:59. Section: Daily Dispatches

6p ET Thursday, May 2, 2019

Dear Friend of GATA and Gold:

Reflecting today on the career and death of former U.S. Commodity Futures Trading Commission member Bart Chilton, silver market analyst Ted Butler suggests that in his last days Chilton confirmed manipulation of the silver market by JPMorganChase to perform one last good deed for public service.

…

Butler wonders why other commissioners and former commissioners, who surely know what Chilton knew, won’t come forward and tell the truth.

Butler also discloses that JPMorgan Chase’s latest filing with the U.S. Securities and Exchange Commission acknowledges that the investment bank is under investigation by the U.S. Justice Department for manipulating the precious metals futures and options markets. But Butler is not convinced that the Justice Department is serious.

His commentary is headlined “A Voice from the Grave?” and it’s posted at GoldSeek’s companion site, SilverSeek, here —

http://silverseek.com/commentary/voice-grave-17645

— and at 24hGold here:

http://www.24hgold.com/english/news-gold-silver-a-voice-from-the-grave-….

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

A Voice From the Grave?

|

May 2, 2019 – 10:49am

The news that Bart Chilton, the former commissioner of the CFTC, suddenly passed away was truly sad but also shocking, so much so that some were given to fabricating conspiracy-type explanations. Chilton certainly had a larger than life persona and many came to appreciate his colorful pronouncements, enthusiasm and willingness to respond to just about everyone who contacted him – qualities quite rare in a regulator. I learned this first-hand very early on when I started communicating with Chilton shortly after he became commissioner in 2007, as I recounted not even a month ago in reaction to his last known interview, with Chris Marcus from Arcadia Economics –

http://silverseek.com/commentary/confirmation-outrage-and-disgust-17622

I stated in the first sentence of that article that Chilton’s interview nearly knocked me off my feet, but I didn’t fully explain why that was so, which I’d like to rectify today. Yes, I found the interview shocking because Chilton seemed to confirm much of what I had contended for more than a decade, but it was much more than that. I was confounded because I couldn’t quite fathom what prompted Chilton to “spill the beans” about the inner workings at the agency regarding JPMorgan’s manipulation of silver after so many years. After all, there was never any acknowledgement from the “inside” that the Commission was quite close to cracking down on JPMorgan – Chilton’s clear admission of this in his interview was the first ever. And perhaps the last.

With the revelation that Chilton was dying from pancreatic cancer, I was confounded no more – Bart Chilton was setting the record straight before his passing – perhaps the most noble act of a life that was more than notable. It is regretful that it would take such unfortunate circumstances – the immediacy of pending death – for the revelation to be made. While the burden on Chilton has been lifted, what does this say about all the other past and current officials at the agency and elsewhere who have chosen to remain silent about a matter of vital public interest?

The hundreds of meetings that Chilton had concerning JPMorgan’s excessive and manipulative short positions starting in 2008 featured other participants, not just Chilton. Most of these other participants have been quick to publicly lament his untimely passing, but still appear bound by some type of strict inner code not to admit to what Chilton admitted – the revelation that JPMorgan had been manipulating the price of silver (and gold) since it took over Bear Stearns in 2008. I thought all these officials took an oath of office to abide by the constitution and the rule of law – not to continue to conceal that JPMorgan was breaking the law in full view.

Bart Chilton set the record straight and for that he is to be commended and remembered. But what about those who have remained silent or worse, continue to deny that JPMorgan is at the heart of an ongoing manipulation? The most serious market crime of all is price manipulation and the fact that the CFTC refuses to deal with the silver manipulation openly and honestly is absolutely shameful.

Another matter that has continued to puzzle me is that lack of any public reaction or admission by JPMorgan that it has been openly accused of manipulating the silver and gold markets. I think I understand JPM not challenging my allegations over the past decade that it is manipulating these markets because it seeks to avoid a potential quagmire – although the thought of a major financial institution turning its back on open allegations of criminal activity without reaction is unprecedented.

But I’ve also been puzzled how JPMorgan could possibly avoid public acknowledgement that it is the subject of criminal investigation by the Justice Department as a result of the DOJ’s announcement on Nov 6 which unsealed a guilty plea by one of the bank’s former traders and an ongoing investigation into precious metals manipulation. It is, after all, a legal requirement that public companies disclosed material information – which being involved in a criminal investigation by the US Department of Justice would qualify. However, that particular puzzle has been solved with the following statement in the JPMorgan 10-K and annual reports.

Here’s the statement from JPMorgan’s recently released 10-K report, page 280 –

“Precious Metals Investigations and Litigation

Various authorities, including the Department of Justice’s Criminal Division, are conducting investigations relating to trading practices in the precious metals markets and related conduct. The Firm is responding to and cooperating with these investigations. Several putative class action complaints have been filed in the United States District Court for the Southern District of New York against the Firm and certain current and former employees, alleging a precious metals futures and options price manipulation scheme in violation of the Commodity Exchange Act. The Firm is also a defendant in a consolidated action filed in the United States District Court for the Southern District of New York alleging monopolization of silver futures in violation of the Sherman Act.”

Of course, it remains to be seen if the Justice Department will confine its investigation to the narrow issue of spoofing or will it open its eyes to the much more serious and pernicious overall manipulation by JPMorgan over the past eleven years; in which JPMorgan never once suffered a loss in trading COMEX silver and gold futures, only profits, and by which the crooked bank amassed 850 million physical silver oz and 20 million oz of gold on the down low.

It has now been exactly one year since I formally and privately complained to the Justice Department about JPMorgan’s manipulation of the silver market and the CFTC’s malfeasance in dealing with it. Initially, I did think that there might be a connection between my complaint and the DOJ’s announcement of the guilty plea and ongoing investigation six months later on Nov 6, but feel less so today. I hope I’m wrong and the Justice Department has a good sense of what’s really going on with JPMorgan in silver and gold, but I’d be lying if I told you my confidence was still high in that regard.

Primarily, my confidence in the DOJ doing the right thing has sagged because the manipulation is continuing while the investigation is supposedly in force. In other words, the serial killer (JPM) is still littering the countryside with bodies, while the Justice Department appears to be contemplating its belly button. I’m not aware of any legitimate law enforcement process that allows for new crimes of the very same type to be committed continuously in the course of an investigation. I just hope the DOJ handles allegations of terrorism with more care than it appears to handle allegations of serious market crimes. As I said, I hope I’m wrong.

Ted Butler

May 2, 2019

With Moore gone, we are now witnessing a huge fight at the Federal Reserve. The Wall Street Journal has a high regard for Moore and are very upset that tactics were used to make him unelectable by the Senate.

(courtesy New York Sun/GATA)

New York Sun: The Federal Reserve fight

Submitted by cpowell on Fri, 2019-05-03 01:48. Section: Daily Dispatches

From the New York Sun

Thursday, May 2, 2019

The defeat of Steve Moore’s candidacy for a governorship of the Federal Reserve invites a strategic look at the fight over our central bank. This fight has, after all, been brewing a long time — since, in our view, 1971, when President Nixon closed the gold window and ended the era of Bretton Woods, when the dollar was redeemable by foreign governments for a 35th of an ounce of gold. (Since which the value of the dollar has plunged more than 97 percent.)

We share the Wall Street Journal’s admiration for Mr. Moore. It is denouncing, in tomorrow’s edition, the low tactics used against Mr. Moore. It notes that Democrats will never forgive Mr. Moore for being right on taxes. We’ve admired his preparedness to ask “basic, even radical questions about our monetary system, such as whether we need the Federal Reserve in the first place.” …

… For the remainder of the commentary:

https://www.nysun.com/editorials/the-federal-reserve-fight/90670/

-END-

Gold trading/

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7345/

//OFFSHORE YUAN: 6.7476 /shanghai bourse CLOSED UP 15.84 POINTS OR .52%

HANG SANG CLOSED UP 137.37 POINTS OR .46%

2. Nikkei closed

3. Europe stocks OPENED GREEN

USA dollar index RISES TO 97.99/Euro RISES TO 1.1152

3b Japan 10 year bond yield: FALLS TO. –.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.52/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

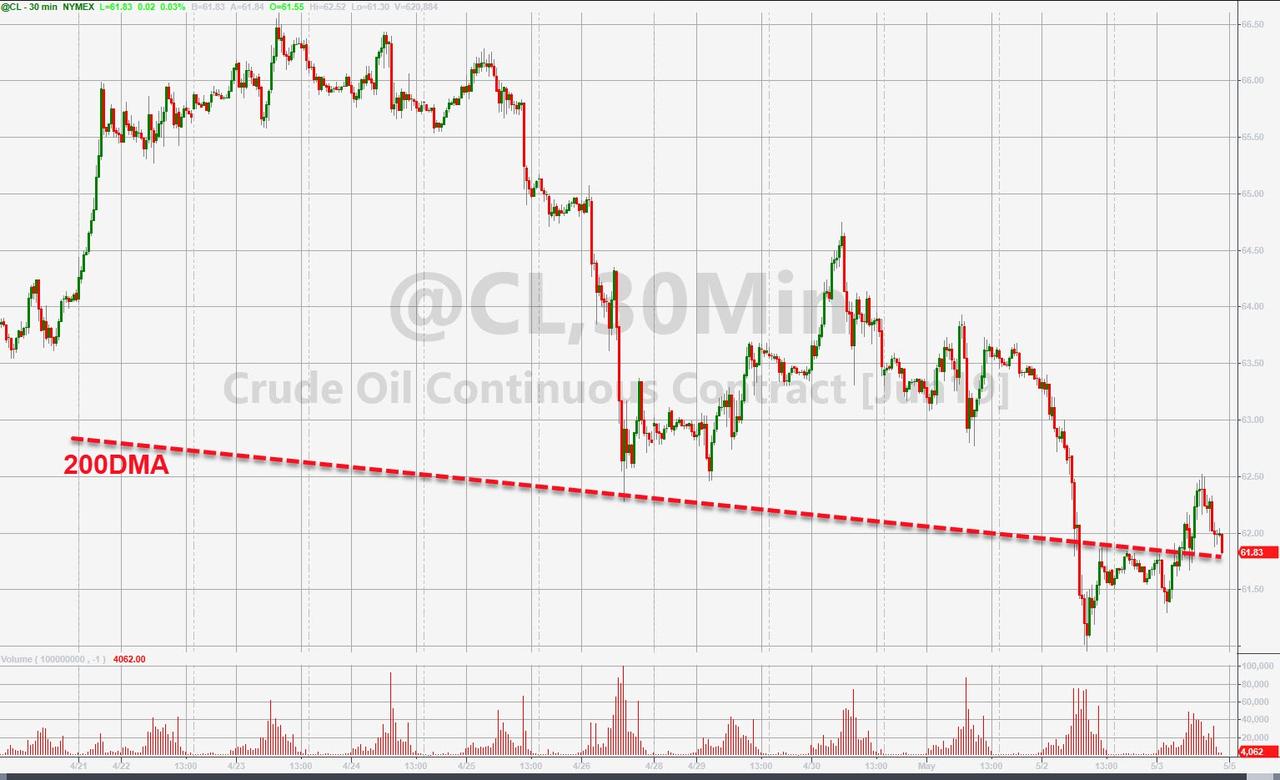

3e WTI:: 61.70 and Brent: 70.45

3f Gold DOWN/JAPANESE Yen UP CHINESE YUAN: ON -SHORE UP/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +04%/Italian 10 yr bond yield DOWN to 2.51% /SPAIN 10 YR BOND YIELD DOWN TO 0.99%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.51: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.35

3k Gold at $1270.15 silver at: 14.67 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 1/100 in roubles/dollar) 65.38

3m oil into the 61 dollar handle for WTI and 70 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.49 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0200 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1376 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISING to +0.04%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.56% early this morning. Thirty year rate at 2.94%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.9749.. VERY DEADLY

Global Markets, S&P Futures A Sea Of Green Ahead Of Payrolls

Global stocks were higher, with European markets and US equity futures a sea of green on the last day of the week, as China and Japan remained closed for holidays, as world stocks battled to avoid their first weekly fall in six weeks on Friday while investors waited to see if April US jobs data would give the Federal Reserve another reason to dismiss rate cut calls.

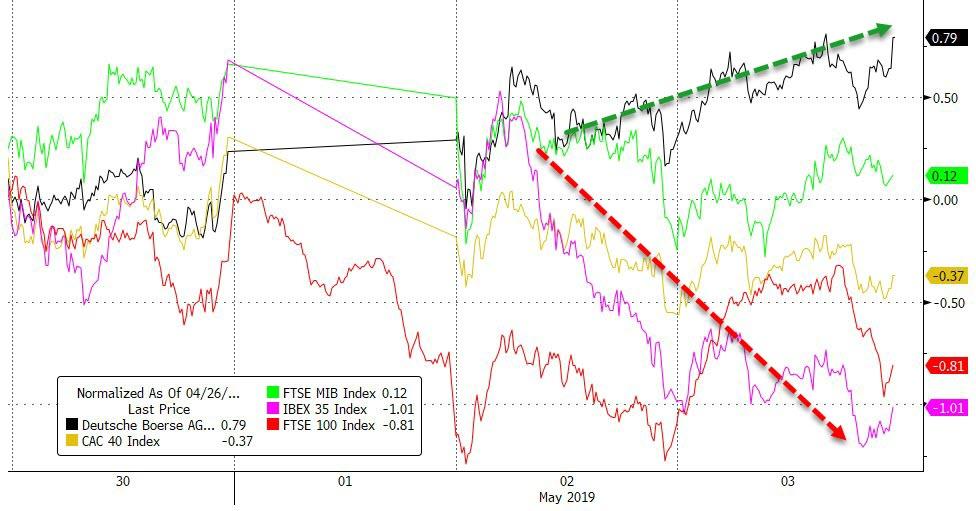

While Asian stocks were broadly flat, mostly due to subdued volumes as China and Japan remain closed, and the MSCI Index of Asian stocks closing just 0.02% higher, it appears that Asia once again was instrumental in pushing US futures higher as the Emini rebounded as Hong Kong shares rose 0.4 percent, while Australia gained 0.1%, while Korea’s KOSPI dipped 0.5 percent.

There was more action in Europe, whose bourses were higher across the board as earnings from banks HSBC and Societe Generale cheered traders and encouraging Adidas profits sent the German sportswear firm’s shares surging 7% to a record high.

On Thursday, the S&P dropped on concerns about the US-China trade deal, giving up an initial attempt to regain their record highs and closed in the red, weighed down by energy shares. Oil prices had plunged again after U.S. crude production output set a new record, though the losses were capped by the intensifying political crisis in Venezuela and the stopping of Iranian oil sanction waivers by Washington.

Yet while stocks were broadly higher, bond and commodity markets remained firmly on the backfoot with most benchmark government bond yields up and Brent sliding back toward $70 a barrel again for what will be its worst week in over two months.

Quoted by Reuters, UBP strategist Koon Chow said it all pointed to a little bit of the steam coming out of the markets after a flying start to the year: “For the last four months it has been the unwinding the extreme pessimism that had built up (last year)” he said, referring to trade war nerves and the slowdown in many of the world’s largest economies. “So here we are now in search of the next big thing, and I think today, and for the last few weeks, it is a views and portfolio repositioning exercise.”

Some of the overnight bullishness was attributed to trader expectations for today’s jobs report. The only problem is that nobody knows if it’s better for the report to show bad or good news: since the recent surge in markets has been due to a dovish Fed, any unexpected overheating in job or wage gains, will likely further pressure risk. April payrolls, due at 830am ET, are forecast to show 185,000 net new jobs were added in April and the unemployment rate at a steady 3.8%. Average hourly earnings are expected to rise 3.3%, just shy of the post-crisis highs.

Over in the UK, the latest local council elections results show Labour Party councillors dropped by 53 councillors to 601 and Conservative party councillors dropped by 117 to 512 in England. Instead, voters turned to alternative parties which saw a significant swell in support for the Liberal Democrats, the Greens and independent candidates.

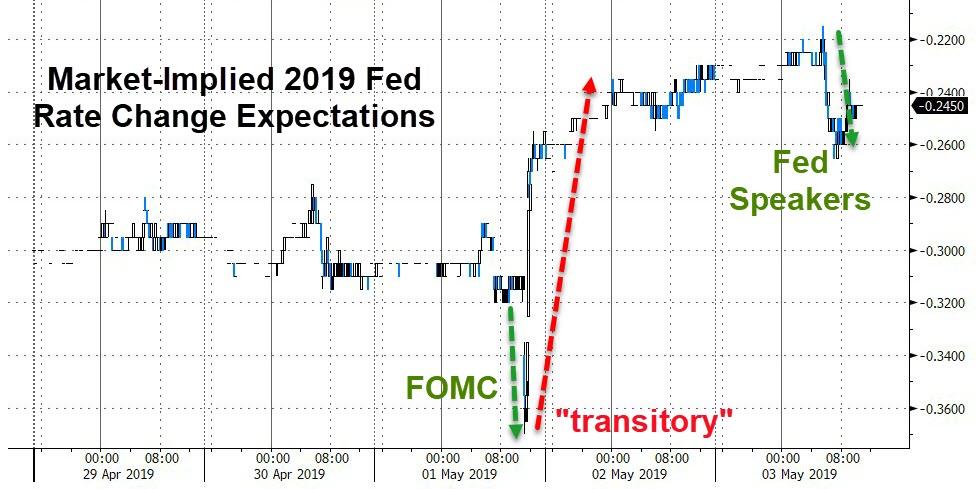

In the currency markets, the dollar strengthened, and the BBDXY rose to session highs ahead of the payrolls report although it may dip soon as an army of Fed doves hits the microphones: there are no less than eight Federal Reserve policymakers due to speak on Friday.The euro stayed lower even as inflation data beat estimates. The pound led G-10 losses but was still set for its biggest weekly gain in almost two months amid optimism a compromise Brexit deal may be struck next week. Australian and New Zealand dollars both fell as speculators wagered both countries could see interest cuts next week. The Aussie slipped below psychological support of $0.7000 overnight to the lowest since early January while the kiwi dollar drifted closer to a recent five-month trough of $0.6581. The weakness in the antipodean currencies also came as the U.S. dollar gained on remarks by U.S. Federal Reserve Chair Jerome Powell earlier this week that a recent weakness in inflation owed to “transitory” factors. That led traders to start paring expectations for a Fed rate cut. Futures now imply about a 49 percent probability of an easing at year-end, down from 61 percent late on Wednesday, according to CME Group’s FedWatch program.

In commodities, West Texas crude steadied, but was in the red in early London trade down 0.3% at $61.65 a barrel, while Brent slipped 0.5 percent to $70.42. Copper fluctuated, still on course for the biggest weekly drop since August. Bitcoin climbed to its highest level since November, advancing toward $6,000.

Other economic releases include wholesale inventories, Markit services PMI. American Tower, Dominion Energy are among companies reporting earnings. There is an avalanche of Fed speakers today including Williams, Bowman, Bullard, Daly, Kaplan and Mester.

Market Snapshot

- S&P 500 futures up 0.4% to 2,928.00

- STOXX Europe 600 up 0.3% to 390.15

- MXAP up 0.02% to 162.61

- MXAPJ up 0.02% to 540.03

- Nikkei down 0.2% to 22,258.73

- Topix down 0.2% to 1,617.93

- Hang Seng Index up 0.5% to 30,081.55

- Shanghai Composite up 0.5% to 3,078.34

- Sensex up 0.4% to 39,153.64

- Australia S&P/ASX 200 down 0.04% to 6,335.80

- Kospi down 0.7% to 2,196.32

- German 10Y yield rose 1.3 bps to 0.043%

- Euro down 0.07% to $1.1164

- Brent Futures down 1% to $70.06/bbl

- Italian 10Y yield fell 0.3 bps to 2.181%

- Spanish 10Y yield rose 0.2 bps to 0.999%

- Brent Futures down 1% to $70.06/bbl

- Gold spot down 0.05% to $1,270.07

- U.S. Dollar Index up 0.06% to 97.89

Top Headline News from Bloomberg

- Temporary federal government hiring for the U.S. Census Bureau’s 2020 count may give nonfarm payrolls a boost starting with the April jobs report due Friday, economists say

- A Brexit backlash hit both main parties in U.K. local elections, with smaller parties gaining seats. The news increases hopes that a compromise Brexit deal could be struck next week as both Labour and the Conservatives attempt to bring an end to the divisive issue

- ECB’s Weidmann sees signs of pickup in Germany economy, with the current weak phase only “temporary”. Urges the ECB to press ahead with its exit from unconventional monetary policy if inflation allows

- ECB’s Rehn also sees evidence of a recovery, but warns not to ‘jump the gun’ on first green shoots

- Oil tumbled as much as 4% in New York, lowest levels in a month, as American crude inventories hit highest level in two years and Russia missed targets for production cuts in April

- PIMCO Chief U.S. Economist Tiffany Wilding says many on the Fed may favor preemptively cutting rates if they see risks as to the downside, even if a recession is not expected

- European Commission president Jean-Claude Juncker is reported to have said that Bundesbank chief Jens Weidmann is a suitable candidate to take over from Mario Draghi as ECB president

- Global Times said in analysis that many observers are wondering if China-U.S. trade talks have hit an impasse as there were few details revealed after the latest meetings on Wednesday

- Billionaire investor Warren Buffett told CNBC in an interview that Berkshire Hathaway Inc. has been buying Amazon.com Inc. shares and the purchases will show up in a regulatory filing later this month

- Inflation in the euro area accelerated more than expected and a core measure jumped the most in nearly a year, capping a week of encouraging data for the European Central Bank

- Donald Trump doesn’t want anyone to see his tax returns. Not the public. Not Congress. But at least one group has peered into the carefully guarded trove and could provide some insight — a team from Deutsche Bank AG

Asian equity markets were mixed with the region cautious ahead of the looming US NFP data and after losses on Wall St where the fallout from the FOMC disappointment persisted and the energy sector underperformed on weaker oil prices. ASX 200 (U/C) swung between gains and losses with notable weakness seen in energy names after WTI crude declined by more than 3% and with financials subdued after Macquarie’s full-year results which improved from the prior year although it flagged a decline for FY20. KOSPI (-0.7%) and Hang Seng (+0.4%%) were negative with South Korea heavily focused on earnings and with risk appetite in Hong Kong sapped by poor GDP data which showed its economy grew at the slowest pace in nearly a decade. However, the Hang Seng is well off intraday lows as trade related news provided a glimmer of optimism with Chinese Foreign Minister Wang to travel to the US on Tuesday and is expected to close the trade deal next week, while US Commerce Secretary Ross suggested they are in the end-game of trade negotiations. As a reminder, mainland China and Japan remained closed for holidays.

Top Asian News

- Chip Makers Lead Asia Gains on Hope of Better Earnings, Orders

- Foreign Fund Inflows Into Indonesian Bonds Surpass 2018 Level

Major European indices have been gradually grinding higher throughout the session [Euro Stoxx 50 +0.3%], diverging from the cautious trade seen overnight where sentiment was somewhat deterred by the upcoming US jobs report and mixed US-China trade reports. There is no real standout European bourse this morning with gains relatively broad based; although, the SMI (+0.2%) while positive is underperforming its peers, with the index weighed on by Swiss Re (-2.6%) after the Co. posted a miss on Q1 net. In a similar fashion sectors are predominantly in the green with the exception of the Technology sector which is weighed on by heavyweight Sap (-0.4%) in the red following on from reports yesterday that up to 50k companies which are using the Co’s software are at risk of a security breach; the Co. state that guidance on resolving these issues was published in both 2009 and 2013. Other notable movers this morning include banking giant HSBC (+2.4%) who are firmer post-earnings where they beat on both Q1 revenue and pre-tax profit. Separately, but also boosted by earnings are Adidas (+6.1%) with the Co. also topping the Dax (+0.3%) after confirming FY guidance and reporting strong net income & operating figures. Elsewhere, and at the other end of the Stoxx 600 are Intu Properties (-6.4%), after stating that they see FY19 LFL retail income falling by 4-6% and forecast the remainder of the year as being challenging.

Top European News

- Norway’s Wealth Fund Surges $84 Billion After Snapping Up Stocks

- Merkel Weighs German Carbon Prices to Speed Pollution Cuts

- U.K. Economy Seen Stagnating in April as Services Eek Out Growth

- Societe Generale Shares Gain on Surprise Strong Capital Beat

In FX, the Greenback remains on a firmer footing ahead of the monthly BLS jobs report, and the index has just notched a new post-FOMC peak at 97.971 amidst expectations that payrolls will post another solid gain, with average earnings forecast to tick up in m/m and y/y terms. The DXY has eclipsed Fib resistance at 97.881 in the process and is now eyeing another retracement level just above 98.000 at 98.059.

- CHF/EUR/GBP/JPY/AUD – All weaker, albeit marginally vs the Usd, with the Franc straddling 1.0200 after a further deterioration in Swiss consumer sentiment and in line/steady y/y CPI, but still well shy of the SNB’s 2% target. Meanwhile, the single currency is grinding down further having relinquished the 1.1200 handle on Thursday with Fibs marking out support and resistance at 1.1147 and 1.1186 respectively, and hefty option expiry interest also likely to influence trade/direction ahead of NFP if not the NY cut. Note, firmer than forecast Eurozone inflation has been largely shrugged off given national numbers indicating an upside bias vs consensus. Similarly, Cable failed to glean and positive momentum from confirmation that the UK services sector joined its construction counterpart back into expansion from contraction, with the pair having dipped below the 1.3000 level to circa 1.2990 (just shy of the 100DMA at 1.2983) while Usd/Jpy is pivoting 111.50 and the 30 DMA (111.47) in advance of the aforementioned US labour data and a 111.70 Fib. Last, but by no means least, the Aussie is trying to keep sight of the psychological 0.7000 mark following extended losses to a fractional 2019 low (0.6985) where decent expiry interest (877 mn) resides, but still wary about a potential RBA rate cut next week.

- CAD/NZD – Marginal G10 outperformers, or at least holding their own as the Loonie meanders between 1.3458-75 and Kiwi hovers above 0.6600, albeit also conscious that the RBNZ could ease policy at the May meet.

- EM – The Lira remains in the spotlight and under pressure in wake of weaker than anticipated Turkish CPI on perceived less hawkish CBRT policy implications, with Usd/Try at the upper end of 5.5800-9595 trading parameters.

In commodities, Brent (-0.5%) and WTI (-0.2%) prices are subdued this morning, as the general uptick in risk appetite this morning has not been able to outweigh the bearish pressure from the stronger dollar. WTI prices are still relatively secure above the USD 61/bbl level, currently trading around the USD 61.40 figure; however, the session lows for Brent did briefly breach the USD 70/bbl level. UBS note that of central concern for oil on the upside are the recent reports that US-China trade talks may have reached an impasse, ahead of next week’s negotiations in Washington. News flow this morning includes sources commenting that Saudi Arabia’s production may increase in June but will still be below the 10.3mln BPD quota under the OPEC+ agreement. For reference, surveys indicate that Saudi Arabia’s output as of April 30th is 9.85mln BPD. Gold (U/C) is relatively lacklustre this morning with the yellow metal torn between the firmer dollar, mixed US-China trade reports and the general improvement in risk sentiment; as such the metal is left pivoting the USD 1270/oz level. Elsewhere, copper is still suffering from the absence of China, although industrial metals in general have strengthened somewhat with some attributing this to recent comments from Tesla, stating that they foresee shortages of minerals which are used in electric vehicles.

US Event Calendar

- 8:30am: Change in Nonfarm Payrolls, est. 190,000, prior 196,000

- Unemployment Rate, est. 3.8%, prior 3.8%

- Average Hourly Earnings MoM, est. 0.3%, prior 0.1%

- Average Hourly Earnings YoY, est. 3.3%, prior 3.2%

- Underemployment Rate, prior 7.3%

- Wholesale Inventories MoM, est. 0.2%, prior 0.2%; Retail Inventories MoM, est. 0.1%, prior 0.3%

- 9:45am: Markit US Services PMI, est. 52.9, prior 52.9; Markit US Composite PMI, prior 52.8

- 10am: ISM Non-Manufacturing Index, est. 57, prior 56.1

- 10:15am: Fed’s Evans Speaks at NABE International Forum in Stockholm

- 11:30am: Fed’s Clarida Speaks at Hoover Institute Policy Conference

- 1:45pm: Fed’s Williams Speaks at Hoover Institute Policy Conference

- 3pm: Fed’s Bowman Speaks at Hoover Institute Policy Conference

- 7:45pm: Fed’s Bullard, Daly, Kaplan and Mester Speak at Hoover Event

DB’s Craig Nicol concludes the overnight wrap

The last 24 hours was always going to be a little bit of a no man’s land for markets given that it fell in-between the Fed meeting and a payrolls Friday. That said, the Fed-inspired plunge for equities continued, albeit at a much more moderate pace, with the S&P 500 ending -0.21% lower by the time the closing bell rung last night. That was admittedly 0.59% off the intraday lows, with the NASDAQ also bouncing off its low of -0.91% to end the session only -0.16% lower. The DOW fell -0.46%, dragged lower by poor earnings from Dow Chemicals, whose management said they see “discrete” headwinds in the second quarter, and by Caterpillar after investors were unimpressed with its latest dividend announcement.

In Europe we had the PMIs to focus on – more on that below – however equities were playing catch up to the US moves from the day prior with the STOXX 600 ending -0.58%. Cash HY spreads widened by +4bps in Europe but tightened -1bp in the US. It was at least a bit more exciting in the rates market where 2y and 10y Treasury yields rose +4.0bps and +4.1bps respectively, and thus extending Wednesday’s move, while Bunds ended +1.7bps. Those moves were completely driven by real yields, as inflation expectations fell notably. That move was in turn driven by lower oil prices, as investors noted rising US stockpiles unconfirmed reports about increases to Russian and Saudi output. WTI ended -2.81% lower. The USD rose +0.15% which weighed on EM FX once again, as a basket of currencies retreated -0.40%. Oil exporting countries saw bigger falls, led by the Russian Ruble’s -1.24% retreat. In other commodities, Gold and Silver fell -0.48% and -0.32% to fresh year-to-date lows.

So before we can finally take a breather from what has felt like a fairly non-stop week, there’s the small matter of getting through this US employment report in about seven hours’ time. Our US economists expect nonfarm payrolls to slow to 160k versus 196k in March, while the consensus is for 190k. Our colleagues do note though that their forecast should be enough to keep the unemployment rate at 3.8%, while for earnings they forecast +0.2% mom, a tenth below what the market expects. That should still be enough to see the annual rate nudge up to +3.3% yoy though and just shy of its post-recession high.

It’s worth noting that as well as payrolls today we’ve got a number of Fed speakers due up this afternoon. Evans, speaking at 3.15pm BST, should be interesting given that Monday’s inflation data nudged closer to the 1.5% level that Evans said would make him “extremely nervous”. As you’ll see in the day ahead at the end we’ve also got Clarida, Williams, and Bowman speaking at the Hoover Institution Conference this afternoon.

This morning in Asia there isn’t a huge amount to report with markets fairly directionless. Thin trading volumes are still a factor however with Japan and China closed. The Hang Seng (-0.02%) is little changed while the Kospi (-0.69%) has struggled, in contrast to the ASX which is up +0.18%.

In other news, yesterday Stephen Moore withdraw his name from consideration for a Fed governorship, though he gave an interview 2 hours before that decision in which he said he was still “all in.” In China trade talks reportedly concluded positively between the US and China, though subsequent reporting in the Chinese press suggested that officials “may have hit an impasse” which seemed to be the trigger behind the mid-afternoon plunge for equities. The details were less negative than the headline suggested, but the story could nevertheless be a signal from Chinese officials about their willingness to walk away from talks if a satisfactory deal isn’t soon completed.

Meanwhile, the CBO released its latest budget forecasts which turned out to be uneventful. There were no major changes to the forecast for deficits to average -4.3% of GDP over the next 10 years, taking the public debt from its current 78% of GDP level to 92%. Roughly half of that rise is due to the CBO’s projections for higher interest rates, which are above DB’s and consensus forecasts, which suggests the rise will be less severe, but on the other hand the forecasts only include ‘current law’ so there is plenty of scope for things to get worse as tax cuts are renewed and spending caps are lifted moving forward.

Here in the UK it was the turn of the BoE to take the spotlight. As expected there were no policy surprises and the message was fairly neutral at best with growth projections revised up and inflation forecasts down. Our UK economists summarised that the overall communication from the BoE yesterday confirmed that policy remains almost exclusively conditional on a Brexit resolution. And with the ongoing tension between the Bank’s inflation projections and market pricing, Governor Carney reiterated the need for more hikes (than currently priced in) to keep inflation in check. Indeed, Carney’s push back against more dovish pricing at the front end of the UK rate curve was consistent with the MPC’s hawkish bias for gradual and limited tightening over the Bank’s forecast horizon. And given that our colleagues’ base case is for a Brexit resolution in May, they retain their call for an August rate hike. Sterling faded from the highs yesterday to close down -0.14% while the Gilt curve was a touch weaker with 10y yields ending +3.5bps.

As for the details of those PMIs in Europe, the manufacturing reading for the Euro Area was revised up 0.1pts to 47.9. That included better than expected readings for Italy (49.1 vs. 47.8 expected) and Spain (51.8 vs. 51.2 expected) and a +0.4pt upward revision for France to 50.0. The winner? Greece at 56.6 and the highest since 2000. Imagine thinking that four years ago. More significant for Europe, Germany was revised down 0.1pts to 44.4 which puts the increase over March at just +0.3pts. However, the good news was that new orders were up +1.4pts. As our economists noted, the improvement in the southern periphery is welcome and confirms that German contagion is more limited to its cyclical neighbours with falls in the manufacturing PMIs for Switzerland, Sweden, and the Czech Republic, possibly as collateral damage from Germany’s slide. The services readings are due on Monday so that’s the next focal point. Despite some green shoots of optimism then, the reality is that the manufacturing reading for the Euro Area is still the second lowest level in the current cycle and well into contractionary territory.

Over in the US, jobless claims stayed steady at 230k and the final print for March core capital goods orders were revised up +0.2pp to 0% mom. Factory orders rose +1.9% mom, better than the +1.6% expected, and the prior month was revised higher as well. This is likely to present upside risks for the first revision to Q1 US GDP growth later this month. Separately, Q1 productivity rose by +3.6% qoq, the fastest pace since 2014. On a yoy basis, that was the fastest pace since the financial crisis. Our US economists have published research previously showing that productivity tends to lag wage growth, as companies respond to wage pressures by finding new ways to boost output per hour. That underlies DB’s house view for US growth to remain strong over the next several quarters and years, as opposed to the consensus which envisions a gradual slowing.

Finally, the day ahead is unsurprisingly headlined by the April employment report in the US this afternoon, however prior to that we’ll get April CPI data out of Turkey this morning which will be worth a close eye, followed by the April services and composite PMIs in the UK and the April CPI report for the Euro Area. The core reading is expected to rise two-tenths to +1.0% yoy. The other data due in the US today includes the March advance goods trade balance, March wholesale inventories, the April services and composite PMIs and April ISM non-manufacturing. As mentioned earlier the other potentially interesting event to watch is the raft of Fedspeak this afternoon. It starts with Evans who is speaking at an event in Stockholm at 3.15pm BST, before Clarida (4.30pm BST), Williams (6.45pm BST) and Bowman (8pm BST) speak at the Hoover Institute Policy Conference. The Bundesbank’s Weidmann is also due to speak this morning.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 15.84 POINTS OR .52% //Hang Sang CLOSED UP 137.37 POINTS OR .46% /The Nikkei closed //Australia’s all ordinaires CLOSED DOWN .04%

/Chinese yuan (ONSHORE) closed UP at 6.7345 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 63.26 dollars per barrel for WTI and 71.38 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.7345 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.74756/ TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

i)China/USA

Now it is Beijing that warns the uSA to compromise or else trade talks will collapse.

(courtesy zerohedge)

Beijing Warns Trade Talks Will Collapse If White House Doesn’t Compromise

More cracks are forming in the White House’s carefully-constructed narrative that trade talks could be headed for a resolution next Friday following the 11th round of talks between US and Chinese trade negotiations in Washington. After Beijing floated a report on Thursday suggesting that talks had been an impasse, sending stocks hurtling toward session lows early Thursday afternoon, they have followed up on Friday with a statement casting doubt on Washington’s assertion that a deal is imminent.

According to the South China Morning Post, the Communist Party has published what appears to be a warning to Washington and the investing public. The Communist Party warned in a post on Taoran Notes, a venue for publishing trade-talk updates for the Chinese public, that reports about a deal being reached next Friday were part of a pressure campaign to get Beijing to acquiesce to a deal, adding that this “smoke and mirrors” ploy wouldn’t work.

“Taoran Notes, a social media account used by Beijing to release trade talk information and to manage domestic expectations, said the hints from the US side that next week’s 11th round of talks are a deadline is merely a trick “to increase tensions and generate pressure on the other side.”

“It’s the same tactic as the US threatening to raise tariffs, it is merely smoke and mirrors to exert extreme pressure [on China],” the post said. “You don’t have to take it seriously.”

Of even greater concern for stock market bulls: Beijing warned that “an unhappy departure” is still possible if the US fails to compromise.

It warned that there is still a possibility that the two sides will end up in “an unhappy departure” if one side wants the other to make compromises and neglects “fairness in negotiation.”

Exact details of the talks are shrouded in secrecy, although Beijing and Washington have hailed “progress” after every round of talks over the last five months, with Mnuchin calling this week’s talks in Beijing “productive.”

Which is surprising because over the past week, media reports have suggested that the US has done nothing but compromise. Not only have Mnuchin, Lighthizer & Co. reportedly backed down on US demands for a stable enforcement mechanism and – even more embarrassingly – demands that China promise to end its cyberespionage campaign, and the US Chamber of Commerce said Thursday that a final deal could fall short on addressing state industrial subsidies – another one of the Trump Administration’s key demands.

During a speech at the BRI Forum last week, President Xi spoke about promises to increase agricultural purchases, increase market access for foreign companies and prohibit forced technology transfers. Though Xi didn’t explicitly mention talks with the US, it’s looking increasingly likely that these concessions represent a ‘final offer’ from Beijing.

Whether the White House decides to take it, or leave it, next week could decide whether a deal is reached, or China walks away.

4/EUROPEAN AFFAIRS

GERMANY

The hopeless attempt to get these two losers together…merger talks collapse again

(courtesy zerohedge)

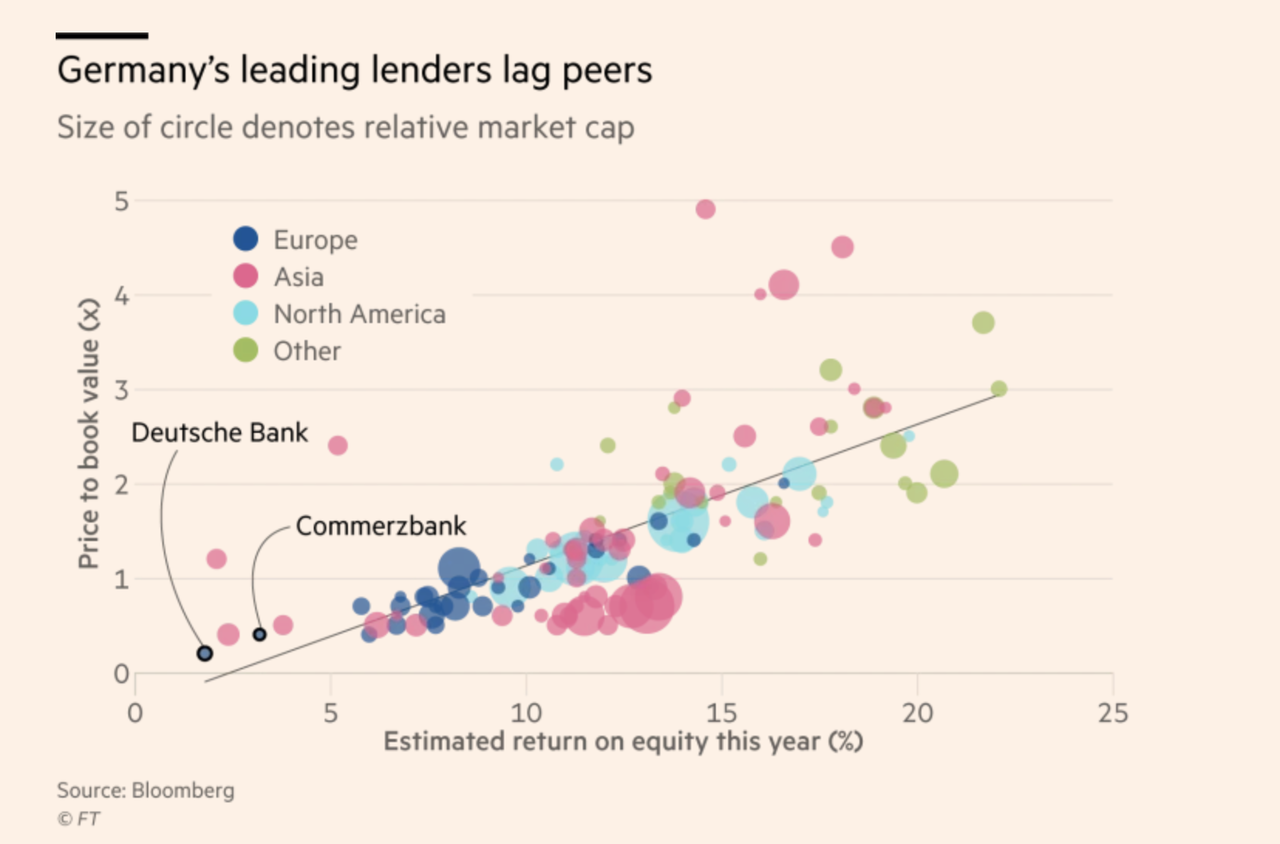

Deutsche Bank Back To ‘Square One’ As Commerzbank Merger Talks Collapse

Ever since it became apparent that the Deutsche Bank-Commerzbank tie-up wasn’t meant to be after all, despite incessant lobbying from the German Finance Ministry over the objections of pretty much every other stakeholder, both Deutsche Bank shareholders as well as the bank’s still-relatively-new CEO have probably been wondering: What’s next for Europe’s least-favorite perennially troubled megabank?

Well, as DB’s management team scrambles to close a deal with UBS to merge the Swiss bank’s once-storied asset-management business with DWS, the asset-management arm that functions as a separate corporate entity controlled by Deutsche, Bloomberg and the FT have effectively confirmed what most shareholders have been hoping for: Despite Sewing and Chairman Paul Achleitner’s insistence that the investment bank is vital to Deutsche’s future, it’s probably time for Deutsche to take an axe to its long-suffering investment bank (the bank has already reportedly been considering the ring-fencing of its most toxic businesses and assets in a shadow ‘bad bank’).

Specifically, the bank’s equities business (and more specifically, it’s US equities trading business) will likely be on the chopping block.

But even a restructuring would be difficult, coming with many up-front costs, according to analysts quoted by Bloomberg:

With a Commerzbank deal gone, Deutsche Bank’s only move is “a more radical investment bank restructure, with a potential exit from the U.S. region and the equities product line,” Citigroup Inc. analysts wrote in a note on April 29. Such a move would be difficult. Restructuring costs would hit upfront, and revenue would be squeezed at first, potentially exacerbating rather than fixing Deutsche Bank’s core problem. In any case, that option seems off the table. Achleitner and Sewing say the trading and corporate finance businesses are crucial. “Every executive has to constantly adjust to a changing market environment,” Achleitner told the Financial Times. “But in this regard, we are not talking about strategy, we are talking about execution” of the existing plan.

As if the bank needed another incentive, Reuters reported a few days back that Deutsche’s US operation – which would be greatly curtailed or shuttered entirely in a restructuring – is once again in danger of failing one of the Fed’s stress tests.

In a detailed insider account of the factors that inspired Sewing’s decision to walk away from merger talks (according to the FT, though it had been announced as a mutual decision, the idea to walk away was first broached by Sewing and his team, who argued that financing the deal would be too burdensome).

As one regulator put it:

“Calling the merger off wasn’t a strategic decision,” a top regulator said. “They could just not afford the deal.” “Without the one-off [accounting and tax] effects the transaction would have triggered, the deal stacked up,”the person said, adding it was “unsettling…[that] both banks do not have enough firepower to bring forward a merger that makes strategic sense.” Deutsche disputes that it lacked firepower to do the deal.

But while Commerzbank’s steady corporate business will make it an ideal acquisition target for another European lender (UniCredit and ING have reportedly been weighing bids), DB has no obvious path to finally shed the mantle of ‘most hated bank in Europe’.

end

Bill Blain on the greed of people/corporations

(Bill Blain)

Blain: “We’ve Hit Peak Greed”

Blain’s Morning Porridge submitted by Bill Blain

Thanks to all the Porridge Readers who have forwarded me the Bank of England Job, suggesting I apply. Not for me…

A few years ago I used to think I was being hilariously witty when I wrote about the Global Financial Crisis 2007-2027.

I fear I might not have joking! It doesn’t necessarily mean we’re in for 8 more years of austerity, doom and gloom. Fortunes will continue be won and lost. Markets will go up and down. There will be plenty more to write about in terms of extraordinary corporate madness – like Tesla’s new convertible issue (Please!) – and credulous markets. I’m not convinced there will be the global financial reset many fear.