I WILL UPDATE LATER TONIGHT ON THE GLD/SLV IF ANY CHANGES

GLD UPDATED: 10 PM

YOUR DATA FOR TODAY:

GOLD: $1277.80 DOWN $6.40 (COMEX TO COMEX CLOSING)

Silver: $14.34 DOWN 23 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1279.90

silver: $14.36

COMEX EXPIRY FOR GOLD/SILVER: TUES MAY 28/2019

LBMA/OTC EXPIRY: MAY 31.2019

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 5/8

EXCHANGE: COMEX

CONTRACT: MAY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,283.000000000 USD

INTENT DATE: 05/24/2019 DELIVERY DATE: 05/29/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 5

737 C ADVANTAGE 4 3

905 C ADM 4

____________________________________________________________________________________________

TOTAL: 8 8

MONTH TO DATE: 314

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 8 NOTICE(S) FOR 800 OZ (0.0025 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 306 NOTICES FOR 3060000 OZ (.9517 TONNES)

SILVER

FOR MAY

40 NOTICE(S) FILED TODAY FOR 200,000 OZ/

total number of notices filed so far this month: 3574 for 17,870,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $8708 DOWN $51

Bitcoin: FINAL EVENING TRADE: $ 8653 DOWN $73

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A CONSIDERABLE SIZED 1429 CONTRACTS FROM 210,149 UP TO 211,578 DESPITE THE 6 CENT LOSS IN SILVER PRICING AT THE COMEX. LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR SILVER BUT IT NOW IN FULL FORCE FOR GOLD. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR MAY, 0 FOR JUNE, 715 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 715 CONTRACTS. WITH THE TRANSFER OF 715 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 715 EFP CONTRACTS TRANSLATES INTO 3.575 MILLION OZ ACCOMPANYING:

1.THE 6 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

AND NOW 18.765 MILLION OZ STANDING FOR SILVER IN MAY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MAY:

22,647 CONTRACTS (FOR 19 TRADING DAYS TOTAL 22,647 CONTRACTS) OR 113.23 MILLION OZ: (AVERAGE PER DAY: 1191 CONTRACTS OR 5.955 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 113.23 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 16.17% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 854.33 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

RESULT: WE HAD A CONSIDERABLE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1429 DESPITE THE 6 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A VERY FAIR SIZED EFP ISSUANCE OF 715 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS RESUMED THEIR LIQUIDATION OF THE SPREAD TRADES TODAY.

TODAY WE GAINED A FAIR SIZED: 715 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1715 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1429 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 6 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $14.57 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.058 BILLION OZ TO BE EXACT or 150% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 40 NOTICE(S) FOR 200,000, OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ AND NOW MAY: 18.765 MILLION OZ ..

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 2436 CONTRACTS, TO 517,279 WITH THE $1.30 PRICE FALL WITH RESPECT TO COMEX GOLD PRICING FRIDAY/THERE WAS SOME PROBABLE LIQUIDATION OF SPREADERS //FRIDAY BUT HUGE LIQUIDATION TODAY.

WE ARE NOW 3 TRADING DAYS PRIOR TO FIRST DAY NOTICE. THE SIGNAL WAS GIVEN TO START THE LIQUIDATION PROCESS OF OUR SPREADERS ON MAY 21.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1931 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 1441 CONTRACTS, AUGUST 2019: 490 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 517,279. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A FAIR SIZED LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 505 CONTRACTS: 2436 OI CONTRACTS DECREASED AT THE COMEX AND 1931 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 505 CONTRACTS OR 50500 OZ OR 1.57 TONNES. FRIDAY WE HAD A SMALL PRICE FALL OF $1.30 IN GOLD TRADING ….AND WITH THAT FALL IN PRICE, WE HAD A FAIR LOSS OF GOLD TONNAGE OF 1.57 TONNES!!!!!!

WITH RESPECT TO SPREADING: WE HAD SOME ACTIVITY FRIDAY/HUGE TODAY.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS HAVE NOW SWITCHED TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF MAY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 121,622 CONTRACTS OR 12,162,200 OR 378,29 TONNES (18 TRADING DAYS AND THUS AVERAGING: 6649 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAYS IN TONNES: 378.29 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 378.29/3550 x 100% TONNES =10.65% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2193.82 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 2436 WITH THE SMALL PRICING LOSS THAT GOLD UNDERTOOK FRIDAY($1.30)) //.WE ALSO HAD A FAIR SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 1931 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 1931 EFP CONTRACTS ISSUED, WE HAD A FAIR SIZED GAIN OF 1602 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

1931 CONTRACTS MOVE TO LONDON AND 2436 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE LOSS IN TOTAL OI EQUATES TO 1.57 TONNES). ..AND THIS LOSS OF DEMAND OCCURRED WITH THE SMALL FALL IN PRICE OF $1.30 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAD A SOME/NEGLIGIBLE PRESENCE OF SPREADING LIQUIDATION ON FRIDAY//HUGE AMOUNT OF LIQUIDATION TODAY AS OUTLINED ABOVE.

we had: 8 notice(s) filed upon for 800 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $6.50 TODAY

A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.47 TONNES

INVENTORY RESTS AT 737.34 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 23 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV:

/INVENTORY RESTS AT 311.616 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A CONSIDERABLE SIZED 1429 CONTRACTS from 210,149 UP TO 211,578 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE STOPPED THEIR LIQUIDATION IN SILVER BUT HAVE NOW MORPHED INTO GOLD..

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 0 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 715 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1715 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1429 CONTRACTS TO THE 715 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 2144 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 10.72 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL AND NOW 18.765 MILLION OZ FOR MAY

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 6 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// FRIDAY. WE ALSO HAD A GOOD SIZED 715 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 17.53 POINTS OR 0.61% //Hang Sang CLOSED UP 102.72 POINTS OR 0.38% /The Nikkei closed UP 77.56 POINTS OR 0.37%//Australia’s all ordinaires CLOSED UP 0.64%

/Chinese yuan (ONSHORE) closed DOWN at 6.9107 /Oil DOWN TO 59.07 dollars per barrel for WTI and 70,08 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9107 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9254 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/USA//Saturday

In the next trade war between China and the uSA, the commerce department is targeting more tariffs against China for currency manipulation. And not only that, they are targeting other countries as sell

( zerohedge)

ii)Saturday/China/Wall Street \journal

China’s jawboning is losing its major. Remember that there will be trouble ahead if the off shore yuan break 7 to one.

( zerohedge)

( zerohedge)

vi)The rhetoric intensifies as now Huawei accuses Fed ewx of diverting packages destined to it and saying that they are doing Trumps dirty work. It is now impossible to do a trade deal with China.

VII) Beijing is ready for the killer blow: banning exports of rare earths

viii)Apple braces for a backlash by China especially if citizens of China boycott Apple iphones plus other Apple products..and thus investors are warning of a profit plunge( zerohedge)

4/EUROPEAN AFFAIRS

i)UK

Tom Luongo discusses how Farge has taken down another Tory Government and what to expect next in this saga whereby Eurocrats have no interest in the will of the people

( Tom Luongo/)

i b) UK

This will probably be a first: The EU will tax a country over their excessive debt. Actually for the last 5 years Italy’s Debt to GDP has remained around 132 to 135%. You will recall that in December, Salvini wanted to kick start his moribund economy and spend his way out of their quagmire. The EU has resisted and now they are ready to fine that which the Italian populace will certainly revolt. Grab your popcorn on this:

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)IRAN/USA

Again the rhetoric increases as Iran is now touting “secret weapons” capable of sinking USA warships. This is in reaction to further troop deployment

( zerohedge)

( zerohedge

iv)TURKEY/SYRIA

6. GLOBAL ISSUES

i)The global auto industry

It sure looks like we have reached peak price for new autos. During May already a massive 38,000 jobs have been shed

( zerohedge)

ii)GLOBAL/FOOD SUPPLY/

This is surely a huge global problems the wettest in all of USA history strikes the USA plus other major hits to all parts of the globe

(courtesy Michael Snyder)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

VENEZUELA/

Maduro is very angry that inbound gas tankers are being “sabotaged” and not allowed to leave their ports heading to Caracas.

(zerohedge)

9. PHYSICAL MARKETS

i)Vietnam, is still a gold loving nation for its citizens and as you can see below, one person bought his house with gold. The government of course is not happy and would like citizens to use their own currency the Dong. It just has not caught on…

(courtesy Bloomberg/GATA)

ii)It now seems that the Tanzanian government will now only deal with Barrick in their dispute over a 190 billion dollar tax bill. Barrick, owns Acacia majority owned and in order to save the day as an informal plan to buy out Acacia’s minority shareholders.

(Bloomberg/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

MARKET TRADING/Europe Monday

Early morning//Election results showing a big gain for Eurosceptic parties but not enough to foil a majority for the dominant European parties and their policies. Trump states that he is not ready for a deal with China

( zerohedge)

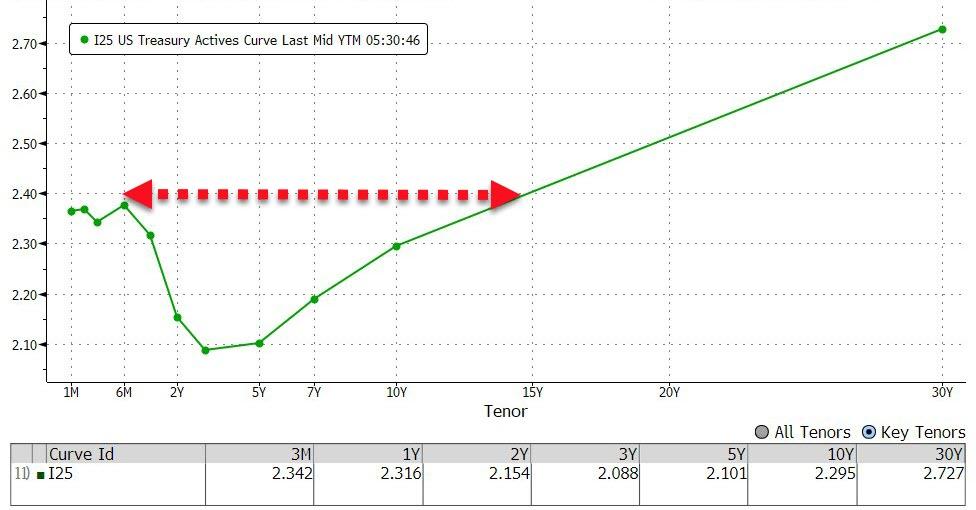

All is not well this morning with the USA 10 yr bond yield at 2.29

(zerohedge)

ii)Market data

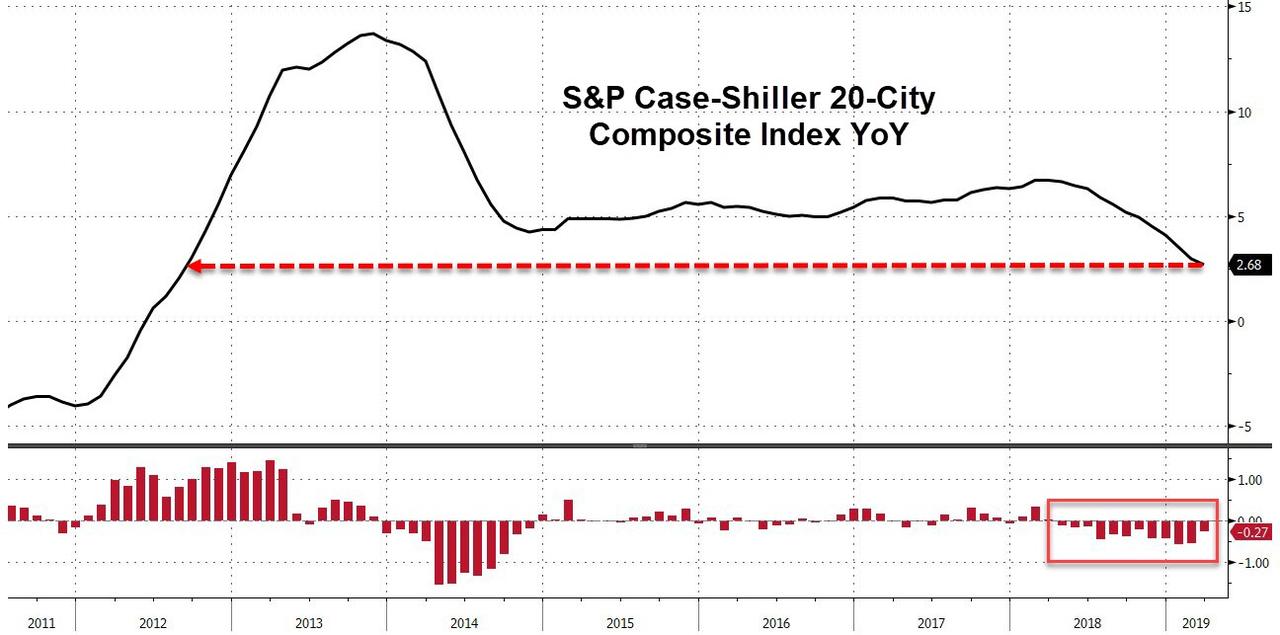

Good indicator that the uSA economy is faltering: home price gains have now slumped for the 12th straight month

( zerohedge)

iii)USA ECONOMIC/GENERAL STORIES

SWAMP STORIES

a)Trump targets the Genesis of the Russian collusion: how Mifsud fed PapaD. with the phony story in March of 2016 and this was fed to Downer who in turned fed this to the Australian government who in turn fed it back to the FBI. Trump also wants to learn about the Ukrainian government trying to influence the election as they were staunch supporters of Hillary

( zerohedge)

b)The real colluders…the real obstructionists and the real leakers…the Democrats.

a must read…

(courtesy Victor Davis Hanson/for the American Greatness Blog)

Let us head over to the comex:

Gold withdrawals;

i) We had 0 withdrawal:

.

The Best Way To Invest In Gold

Today we’re talking gold.

I’m not going to make projections about the price – whether it’s going to go up or down.

Instead we’re going to look at the cost of buying and selling gold.

How to buy gold on the cheap

What’s the easiest, cheapest way to buy gold?

Most would say via one of the gold exchange-traded funds (ETFs) such as the ETFS Physical Gold (LSE: PHAU), for more see a list of gold ETFs here. You buy the ETF through your broker, the same way you would buy a share. You pay a small premium to the spot price of gold, and a small annual percentage to cover storage and other related costs.

ETFs really are brilliantly simple. It is because they’re so convenient that ETFs have become the means by which most investors and – perhaps more importantly in the financial scale of things – most institutions buy gold.

Almost as convenient is to open an account with one of the online bullion dealers – the likes of GoldMoney, GoldCore or Bullion Vault. You pay a small premium to the spot price of gold and storage costs are low.

The overall costs are usually marginally higher than ETFs (although in some cases they are lower), but many investors prefer the online bullion dealer route because they feel the gold that they buy is “theirs”. The gold bars are specifically allocated to them and they can take delivery, if they so choose. I should stress it is also possible to take delivery via some ETFs, but the process is more cumbersome.

I have used both methods, and they both have their advantages and disadvantages. Online bullion dealers are great – and this is a growth business – but the most gold bought and sold by investors is held with the ETFs, because institutions prefer them.

Competition between ETFs and bullion dealers has conspired to drive down prices, much to the benefit of the consumer. But there is one huge cost that neither of these methods is able to avoid – tax. This assumes you’re not buying your gold via an ISA or a SIPP, which it is, for the most part, possible to do via ETF or bullion dealer.

Capital gains tax (CGT) currently stands at 20% in the UK for higher rate taxpayers and 10% for lower. Funds don’t pay CGT. It is paid by the investor when they sell or redeem, assuming they made a profit. It kicks in once you have made profits of more than £12,000 in a year.

So over and above that level, you’re facing an unavoidable 10% or 20% cost for buying and selling gold at a profit. It used to be 18% or 28%, but even at current rates, it’s a considerable dent to profits.

There’s another method of buying gold (and silver), which, quite legally, avoids this cost altogether. There is a slightly higher premium to spot when you buy, there are slightly higher storage costs, and there is a slight discount to spot when you sell – but we are talking about a few per cent here, nothing like 20%.

Given the potential savings involved, it’s surprising that more UK investors don’t buy their gold and silver in this way. The method I’m describing, if you haven’t already figured it out, is to buy sovereigns and Britannias.

Gold sovereigns and Britannias – avoid paying capital gains tax on your gold profits

The gold sovereign used to be the pound coin. Imagine that – a pound coin made of solid gold. It was the pound coin from 1816, after the “Great Recoinage”, until 1932, when the UK finally abandoned its gold standard. Until then, the pound really was “as good as gold” – 22 carat gold to be precise (that’s about 92% purity).

A gold sovereign weighs about seven grammes, which is about a quarter of an ounce. Such is the devaluation of money that has taken place over the last three generations, it now takes about 250 pound coins to buy an old pound coin.

Despite the UK no longer being on the gold standard, the Royal Mint began producing sovereigns again in 1957 and continues to the present day. Many of them are minted in that well-known British heartland, Delhi (there is a huge market for them in India).

Technically these coins are legal tender, so they are exempt from CGT.

Aren’t sovereigns collectors’ items, and so more expensive than ordinary gold? Some are. For example the sovereigns struck in 1937 for Edward VIII were never circulated, because he abdicated. Thus the 1937 sovereign has considerable numismatic value. One sold in 2014 for over half a million pounds. That’s some premium.

Usually though, because sovereigns are so common, the numismatic value is zero. You can pick up 100-plus-year-old Victorian coins at a few per cent over spot. You get the history for nothing.

Gold Britannias – which are an ounce in weight – have only been issued since 1987. But they, too, are considered coins of the realm. Despite the fact that an ounce of gold is close to £1,000, the face value of a Britannia is £100. Don’t ask me how that works; I’m sure there’s a reason. But, as coins of the realm, they are exempt from CGT.

The Royal Mint began producing silver Britannias in 1997. They, too, weigh an ounce. They have a face value of £2 (an ounce of silver is about £12). They too are exempt from CGT.

For the quantities you would need to be buying to be liable for 20% CGT, you’re likely to be paying 4%-6% in premium above spot to buy any of these coins. You’ve then got to store them – that’s as little as a few hundred pounds a year if you go for a safety deposit box, but the simplest solution is to store them with the dealer you bought them from, which makes selling that much quicker when you come to do that. There will be a cost to this.

However, all in all, gold sovereigns and Britannias make for a considerable saving on cost because of the CGT exemption – assuming you have made a gain when you come to sell. And of course, there’s no guarantee of that.

So if you think the premium over the spot price is worth paying in order to avoid shelling out 20% CGT, there are a plethora of sovereign dealers out there.

Mark O’Byrne, one of the men behind GoldCore, is a buddy of mine. I like GoldCore. You can deal with them either over the phone or open an account online. You can buy sovereigns, Britannias, bars and probably even bells, and they’ll take care of the storage too.

Full article by Dominic Frisby on Money Week

Gold Hits 1-week High on Simmering U.S.-China Trade Spat

Gold To Tackle $1300, Watch For ‘Deteriorating Data’ — TD Securities

Bitcoin Hits One-year Intraday High, Nears $9,000 Level

Centrist Bloc Loses Majority in EU Vote as Greens and Euroskeptics Gain

U.S. Navy Pilots Reportedly Spotted Ufos Over East Coast

“The Most Destructive Breach in History”: Hackers Use NSA Code to Grind Baltimore to a Halt

Rare Earths Are Xi’s Ace Card in ‘long March’ of Trade War

Let’s Hope the Next Prime Minister Has a Sound Grasp of Economics

BIS Reduces Its Gold Swaps by Two-thirds Over Last Two Months

In Vietnam You Can Still Buy a House With Gold, and the Government Doesn’t Like It

Japanese Secret to a Longer and Happier Life is Gaining Attention from Millions Around the World

Baltimore Ransomware Attack: NSA Faces Questions

Click Here

LBMA Gold Prices (USD, GBP & EUR – AM/ PM Fix)

27-May-19 UK Bank Holiday

24-May-19 1281.50 1282.50, 1011.36 1011.89 & 1145.92 1145.40

23-May-19 1275.95 1283.65, 1009.79 1015.37 & 1146.19 1152.46

22-May-19 1274.00 1273.80, 1005.44 1008.09 & 1141.12 1141.20

21-May-19 1276.00 1271.15, 1004.85 998.62 & 1144.19 1139.84

20-May-19 1275.25 1276.85, 1000.05 1003.22 & 1142.63 1143.42

17-May-19 1285.80 1280.80, 1007.55 1005.17 & 1152.08 1146.70

16-May-19 1295.55 1291.70, 1009.62 1009.46 & 1155.76 1154.78

15-May-19 1298.90 1299.10, 1005.87 1011.87 & 1158.75 1161.53

14-May-19 1297.60 1298.40, 1002.14 1005.48 & 1154.34 1158.04

13-May-19 1282.95 1295.60, 985.95 994.89 & 1142.47 1151.27

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

* * *

Vietnam, is still a gold loving nation for its citizens and as you can see below, one person bought his house with gold. The government of course is not happy and would like citizens to use their own currency the Dong. It just has not caught on…

(courtesy Bloomberg/GATA)

In Vietnam you can still buy a house with gold, and the government doesn’t like it

Submitted by cpowell on Tue, 2019-05-28 01:11. Section: Daily Dispatches

By John Boudreau and Nguyen Dieu Tu Uyen

Bloomberg News

Monday, May 27, 2019

Vietnam may be one of the world’s fastest-growing economies, yet it’s still in the dark ages when it comes to joining the global trend toward cashless transactions. To understand why, look no further than to consumers like Tran Van Nhan, who recently bought his two-bedroom home in Hanoi with gold and a sack of cash.

“We paid almost half in gold bars and the rest in cash,” Nhan, a 47-year-old shopkeeper, said of his new $138,000 condo. “We did that because we and the flat’s owner didn’t want to do a bank transfer. We are so used to buying things with cash and gold.”

…

Prime Minister Nguyen Xuan Phuc is trying to drag his citizens into the modern era of digital payments, reduce the amount of U.S. dollars in circulation in the country and establish the dominance of the nation’s domestic currency, the Vietnamese dong. That also means introducing Vietnamese households to credit cards, bank transfers and digital payments rather than carrying around piles of cash and bullion for purchases.

Behind the push is growing frustration among Vietnamese officialdom about the cost of printing banknotes and the need for more transparent payment records in order to crack down on tax evasion and money laundering, a growing problem as the $237-billion economy continues to expand dramatically. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-05-27/vietnam-s-next-revolu…

* * *

Help keep GATA going

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please vi

https://www.bloomberg.com/news/articles/2019-05-15/bitcoin-rally-is-mas

end

It now seems that the Tanzanian government will now only deal with Barrick in their dispute over a 190 billion dollar tax bill. Barrick, owns Acacia majority owned and in order to save the day as an informal plan to buy out Acacia’s minority shareholders.

(Bloomberg/GATA)

Tanzania says it won’t deal with Acacia anymore, only Barrick

Submitted by cpowell on Tue, 2019-05-28 17:18. Section: Daily Dispatches

Tanzania Says Acacia Mining Won’t Be Allowed Any Role in Country

By Kenneth Karuri and Danielle Bochove

Bloomberg News

Tuesday, May 28, 2019

Tanzania will no longer allow Acacia Mining Plc to manage its mines in the country and will work only with the company’s parent, Barrick Gold Corp., to resolve the two-year impasse that has stymied operations, a government spokesman said.

“We will no longer work with Acacia,” Hassan Abbasi said today by phone. “Under no circumstances can Acacia be a party to the agreements, or have any role in the operation or management of the Barrick mining subsidiaries in Tanzania. The ball is now in Barrick’s court.”

…

Acacia has been at odds with Tanzania’s government since July 2017, when the state handed the London-listed gold producer a $190 billion tax bill, saying it under-declared bullion exports. Barrick has since led discussions with the government and, in an effort to solve the impasse, surprised the market last week with an informal plan to buy out Acacia’s minority shareholders. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-05-28/tanzania-says-acacia-…

A Short History of the Gold Cartel

James Turk

Goldmoney

Governments want a low gold price to make national currencies look good. Gold is recognizable the world over as the “canary in the coal mine” when it comes to money. A rising gold price blurts the unpleasant truth that a national currency is being poorly managed and that its purchasing power is being inflated.

This reality is made clear by former Federal Reserve Chairman Paul Volcker. Commenting in his memoirs about the soaring gold price in the years immediately following the end of the gold standard in 1971, he notes: “Joint intervention in gold sales to prevent a steep rise in the price of gold, however, was not undertaken. That was a mistake.” It was a “mistake” because a rising gold price undermines the thin reed upon which all fiat currency rests — confidence. But it was a mistake only from the perspective of a central banker, which is of course at odds with anyone who believes in free markets.

The U.S. government has learned from experience and has taken Volcker’s advice. Given the U.S. dollar’s role as the world’s reserve currency, the U.S. government has the most to lose if the market chooses gold over fiat currency and erodes the government’s stranglehold on the monopolistic privilege it has awarded to itself of creating “money.”

So the U.S. government intervenes in the gold market to make the dollar look worthy of being the world’s reserve currency when of course it is not equal to the demands of that esteemed role. The U.S. government does this by trying to keep the gold price low, but this is an impossible task. In the end, gold always wins — that is, its price inevitably climbs higher as fiat currency is debased, which is a reality understood and recognized by government policymakers.

So recognizing the futility of capping the gold price, they instead compromise by letting the gold price rise somewhat, say, 15 percent per year. In fact, against the dollar, gold is actually up 16.3 percent per year on average for the last eight years. In battlefield terms, the U.S. government is conducting a managed retreat for fiat currency in an attempt to control gold’s advance.

Though it has let the gold price rise, gold has risen by less than it would in a free market because the purchasing power of the dollar continues to be inflated and because gold remains so undervalued notwithstanding its annual appreciation this decade.

These gains started from gold’s historic low valuation in 1999. Gold may not be as good a value as it was in 1999 but it nevertheless remains extremely undervalued.

For example, until the end of the 19th century, approximately 40 percent of the world’s money supply consisted of gold, and the remaining 60 percent was national currency. As governments began to usurp the money-issuing privilege and intentionally diminish gold’s role, fiat currency’s role expanded by the mid-20th century to approximately 90 percent. The inflationary policies of the 1960s, particularly in the United States, further eroded gold’s role to 2 percent by the time the last remnants of the gold standard were abandoned in 1971.

Gold’s importance rebounded in the 1970s, which caused Volcker to lament the so-called mistakes of policymakers. Its percentage rose to nearly 10 percent by 1980. But gold’s share of the world money supply thereafter declined, reaching about 1 percent in 1999. Today it still remains below 2 percent.

From this analysis it is reasonable to conclude that gold should comprise at least 10 percent of the world’s money supply. Because it is nowhere near that level, gold is undervalued.

So given the ongoing dollar debasement being pursued by U.S. policymakers, keeping gold from exploding upward to a true free-market price is the first thing they gain from their interventions in the gold market. The other thing they gain is time. The time they gain enables them to keep their fiat scheme afloat so they can benefit from it, delaying until some future administration the scheme’s inevitable collapse.

So how does the U.S. government manage the gold price?

They recruit Goldman Sachs, JP Morgan Chase, and Deutsche Bank to do it, by executing trades to pursue the U.S. government’s aims. These banks are the gold cartel. I don’t believe that there are any other members of the cartel, with the possible exception of Citibank as a junior member.

The cartel acts with the implicit backing of the U.S. government, which absorbs all losses that may be taken by the cartel members as they manage the gold price and which further provides whatever physical metal is required to execute the cartel’s trading strategy.

How did the gold cartel come about?

There was an abrupt change in government policy around 1990. It was introduced by then-Federal Reserve Chairman Alan Greenspan to bail out the banks back then, which, as now, were insolvent. Taxpayers were already on the hook for hundreds of billions of dollars to bail out the collapsed “savings and loan” industry, so adding to this tax burden was untenable. Greenspan therefore came up with an alternative.

Greenspan saw the free market as a golden goose with essentially unlimited deep pockets, and more to the point, saw that these pockets could be picked by the U.S. government using its tremendous weight, namely, its financial resources for timed interventions in the free market, combined with its propaganda power by using the news media. In short, it was easier to bail out the insolvent banks back then by gouging ill-gained profits from the free markets instead of raising taxes.

Banks generated these profits through the Federal Reserve’s steepening of the yield curve, which kept long- term interest rates relatively high while lowering short- term rates. To earn this wide spread, banks leveraged themselves to borrow short-term and use the proceeds to buy long-term paper. This mismatch of assets and liabilities became known as the carry trade.

The Japanese yen was a particular favorite to borrow. The Japanese stock market had crashed in 1990 and the Bank of Japan was pursuing a zero-interest-rate policy to try reviving the Japanese economy. A U.S. bank could borrow Japanese yen for 0.2 percent and buy U.S. T-notes yielding more than 8 percent, pocketing the spread, which did wonders for bank profits and rebuilding the bank capital base.

Gold also became a favorite vehicle to borrow because of its low interest rate. This gold came from central bank coffers, but central banks refused to disclose how much gold they were lending, making the gold market opaque and ripe for intervention by central bankers making decisions behind closed doors. The amount lent by central banks has been reliably estimated in various analyses published by GATA as between 12,000 and 15,000 tonnes, nearly half of total central bank gold holdings and four to six times annual gold mine production of 2,500 tonnes. The banks clearly jumped feet first into the gold carry trade.

The carry trade was a gift to the banks from the Federal Reserve, and all was well provided that the yen and gold did not rise against the dollar, because this mismatch of dollar assets and yen or gold liabilities was not hedged. Alas, both gold and the yen began to strengthen, which, if allowed to rise high enough, would force marked-to-market losses on those carry-trade positions in the banks. It was a major problem because the losses of the banks could be considerable, given the magnitude of the carry trade.

So the gold cartel was created to manage the gold price, and all went well at first, given the help it received from the Bank of England in 1999 to sell half of its gold holdings. Gold was driven to historic lows, as noted above, but this low gold price created its own problem. Gold became so unbelievably cheap that value hunters around the world recognized the exceptional opportunity it offered and demand for physical gold began to climb.

As demand rose, another more intractable and unforeseen problem arose for the gold cartel.

The gold borrowed from the central banks had been melted down and turned into coins, small bars, and monetary jewelry that were acquired by countless individuals around the world. This gold was now in “strong hands,” and these gold owners would part with it only at a much higher price. So where would the gold come from to repay the central banks?

While the yen is a fiat currency and can be created out of thin air by the Bank of Japan, gold is a tangible asset. How could the banks repay all the gold they borrowed without causing the gold price to soar, worsening the marked-to-market losses on their remaining positions?

In short, the banks were in a predicament. The Federal Reserve’s policies were debasing the dollar, and the “canary in the coal mine” was warning of the loss of purchasing power. So Greenspan’s policy of using interventions in the market to bail out banks morphed yet again.

The gold borrowed from central banks would not be repaid after all, because obtaining the physical gold to repay the loans would cause the gold price to soar. So beginning this decade, the gold cartel would conduct the government’s managed retreat, allowing the gold price to move generally higher in the hope that, basically, people wouldn’t notice. Given gold’s “canary in a coal mine” function, a rising gold price creates demand for gold, and a rapidly rising gold price would worsen the marked-to- market losses of the gold cartel.

So the objective is to allow the gold price to rise around 15 percent per year while enabling the gold cartel members to intervene in the gold market with implicit government backing in order to earn profits to offset the growing losses on their gold liabilities. The gold cartel’s trading strategy to accomplish this task is clear. The gold cartel reverse-engineers the black-box trend-following trading models.

Just look at the losses taken by some of the major commodity trading managers on their gold trading over the last decade. It is hundreds of millions of dollars of client money lost, and the same amount gained for the gold cartel to help offset their losses from the gold carry trade — all to make the dollar look good by keeping the gold price lower than it should be and would be if it were allowed to trade in a market unfettered by government intervention.

As I see it there are only two outcomes. Either the gold cartel will fail or the U.S. government will have destroyed what remains of the free market in America. I hope it is the former, but the flow of events from Washington and the actions of policymakers suggest it could be the latter.

-END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.9107/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.9254 /shanghai bourse CLOSED UP 17.53 POINTS OR 0.61%

HANG SANG CLOSED UP 102.72 POINTS OR 0.38%

2. Nikkei closed UP 77.56 POINTS OR 0.37%

3. Europe stocks OPENED MIXED /

USA dollar index RISES TO 97.77/Euro FALLS TO 1.1190

3b Japan 10 year bond yield: FALLS TO. –.07/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.37/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 59.07 and Brent: 70.08

3f Gold DOWN/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.15%/Italian 10 yr bond yield DOWN to 2.71% /SPAIN 10 YR BOND YIELD DOWN TO 0.83%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.86: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.19

3k Gold at $1284.20 silver at: 14.50 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 28/100 in roubles/dollar) 64.53

3m oil into the 59 dollar handle for WTI and 70 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.37 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0051 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1248 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.15%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.29% early this morning. Thirty year rate at 2.72%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 6.0371..they are toast

Treasury Yields Plunge To 19 Month Low As Italian Budget Crisis Returns With A Bang

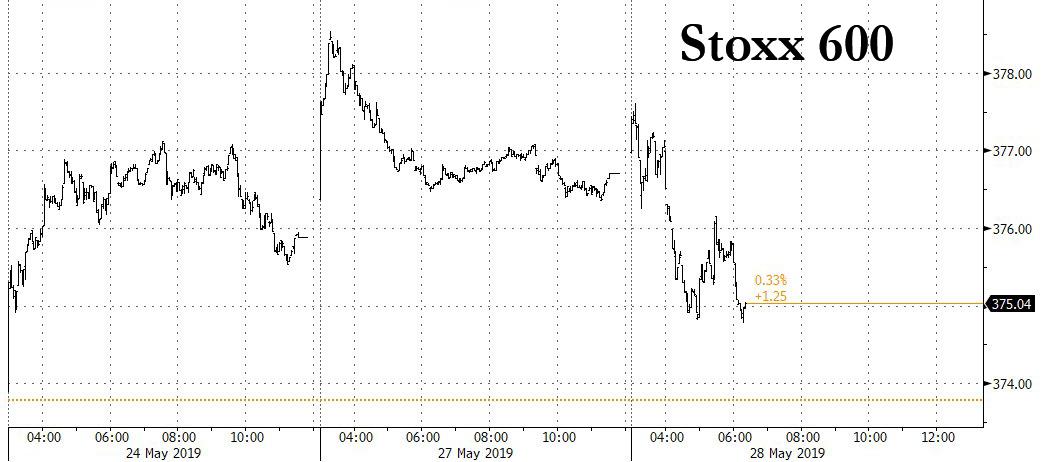

US equity futures, European stocks the the euro all fell on Tuesday as renewed concern about a fresh clash between Italy’s and Europe over the country’s budget overshadowed talks of a Fiat-Chrysler and Renault merger and EU parliamentary elections which failed to result in a worst-case scenario.

After gains in Asia, hopes that European stocks would open higher were dashed, with Italian shares falling more than half a percent, unwinding early gains in both the STOXX 600 and Germany’s DAX, as Italy’s dispute with the European Commission emerged to dominate European trading as markets opened. The Commission could fine Italy 3 billion euros for accumulating debt and deficits that break EU rules, Italian Deputy Prime Minister Matteo Salvini said on Tuesday.

“It reopens the whole agenda of whether Salvini wants to be part of the euro or not,” said Colin Harte, a portfolio manager and strategist at BNP Paribas Asset Management. “The danger is that the [dispute between Salvini and the EU] turns out to be more aggressive on both sides, then you will see people switch out of positions],” Harte said.

Renewed focus on Italy means that the spread between Italian and German 10-year debt, which reached around 100 bps between mid-October and mid-March, has blown out to 285 basis points. And as Italian 10Y yield slumped, Italian bank stocks have tumbled to 2018 lows, although on Tuesday they trimmed some losses after European Commissioner Pierre Moscovici said he didn’t favor sanctions for the country.

German government bond yields, deemed the region’s safest asset, fell four basis points to a two-and-a-half-year low. The euro weakened 0.11% against the dollar.

Meanwhile, the ongoing trade war between the US and China found no respite over the long weekend, with Trump saying on Monday that Washington was not ready to make a deal with China, but he expected one in the future. At the same time, he pressed Japanese Prime Minister Shinzo Abe to reduce Japan’s trade imbalance with the United States. The US president also warned that American tariffs on goods from China “could go up very, very substantially, very easily,” while over the weekend the Asian nation pushed back at the perception that the levies were hurting its economy. Escalating trade tensions have sent sovereign bonds higher and pushed global stocks toward their first monthly decline of 2019. In the US, 10Y Treasury Yields tumbled to 2.271%, the lowest level since October 2017 suggesting an accelerating flight to safety.

Hope for a US-China trade deal still underpins optimism in global markets, but ES futures were down almost 0.25%, taking out Monday’s holiday lows. “Markets are holding their nerve and will start to attach great hope to the meeting between Presidents Xi and Trump in June,” said BNP Paribas’s Harte. “But I’m not as convinced that Trump wants a deal. The big risk is that the U.S. starts being disruptive to supply chains … and the big problem is we don’t really understand how much damage this will do.”

“The Sino-U.S. tensions continue to weigh on equity markets,” said State Street strategist Benjamin Jones. “Thus far, there seems to be little sign of an easing in those pressures on either side of the fence.”

Earlier in the session, Asian stocks advanced for a third day, lifted by advances in China and gains by auto firms after Fiat Chrysler made a “transformative merger” proposal to French peer Renault. Auto stocks rose globally after Fiat Chrysler confirmed it had made proposed a merger with Renault, a deal that would create the world’s third-biggest carmaker. The rally spilled into Asia with Mitsubishi Motors in Japan adding 5.95% and Nissan Motor Co gaining 2.31%.

Otherwise, Asian markets were mixed, with China and Australia rising and Indonesia retreating. Japan’s Topix gauge climbed 0.3%, driven by Toyota Motor and Hitachi. The Shanghai Composite Index closed 0.6% higher, with Foshan Haitian Flavouring and SAIC Motor offering the biggest boosts. A planned increase in the weighting of Chinese A-shares in MSCI indexes after the market closes on Tuesday also boosted shares.

In FX, the dollar index which tracks the U.S. currency against a basket of six other major currencies, rose 0.15% higher at 97.747. The pound whipsawed on two-way flows as traders focused on the race for the next U.K. Prime Minister, while the euro slipped alongside Italian banks and bonds amid concerns of a renewed budget spat with the EU. The yen led gains among G-10 currencies.

The Yuan was largely unchanged after PBoC Governor Yi Gang said he is confident that China can keep the Yuan “basically stable”; the benchmark deposit rate will continue to play a important role in the promotion of market-based interest rate reform; the current benchmark lending and deposit rate is at an appropriate level. And the Chinese – US 10yr yield gap is within a relatively comfortable range. Separately, reported that the PBoC are to increase counter cyclical adjustments, Deputy Chief reiterates they are to maintain a prudent monetary policy.

In commodities, West Texas crude oil nudged above $59 a barrel. Oil prices extended gains after rising more than 1% on Monday, with prices rising on tensions in the Middle East and continuing Russian supply disruptions after a contamination problem discovered last month. Brent crude was 0.29% higher at $70.31 per barrel, having earlier dipped below the $70 mark. WTI crude gained 1.16% to $59.31 per barrel.

Economic data include S&P CoreLogic Case-Shiller home prices, Dallas Fed manufacturing and consumer confidence. Workday and Bank of Nova Scotia are due to report earnings.

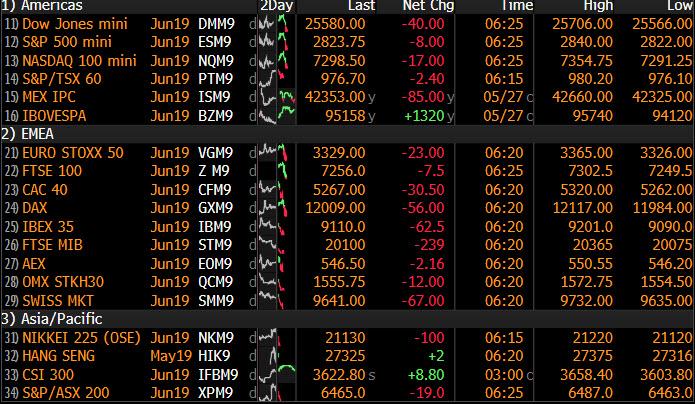

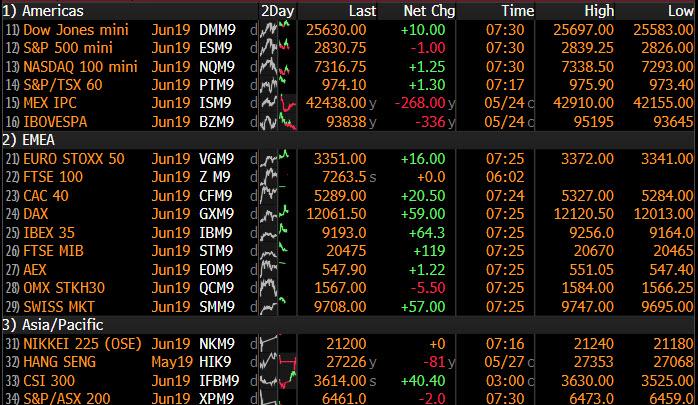

Market Snapshot

- S&P 500 futures down 0.2% to 2,826.25

- STOXX Europe 600 down 0.4% to 375.17

- MXAP up 0.3% to 153.81

- MXAPJ up 0.1% to 500.30

- Nikkei up 0.4% to 21,260.14

- Topix up 0.3% to 1,550.99

- Hang Seng Index up 0.4% to 27,390.81

- Shanghai Composite up 0.6% to 2,909.91

- Sensex down 0.2% to 39,618.71

- Australia S&P/ASX 200 up 0.5% to 6,484.84

- Kospi up 0.2% to 2,048.83

- German 10Y yield fell 1.5 bps to -0.159%

- Euro down 0.04% to $1.1189

- Brent Futures up 0.01% to $70.12/bbl

- Italian 10Y yield rose 12.1 bps to 2.304%

- Spanish 10Y yield fell 2.4 bps to 0.79%

- Brent Futures up 0.04% to $70.15/bbl

- Gold spot down 0.07% to $1,284.49

- U.S. Dollar Index up 0.1% to 97.75

Top Headlines from Bloomberg

- The Chinese government’s first seizure of a bank in more than two decades reverberated through markets for a second day, driving up funding costs for smaller lenders and adding pressure to shares that already trade at rock-bottom valuations

- Italian bonds declined and yields jumped for a second day as investors faced the prospect of a new budget standoff between the nation and the EU after the region’s elections strengthened the hand of Deputy Prime Minister Matteo Salvini. The bonds pared losses after EU Commissioner for Economic and Financial Affairs Pierre Moscovici played down talk of sanctions

- Labour leader Jeremy Corbyn grudgingly promised to support a referendum on any Brexit deal after his party sank to just 14% of the vote in the European election. Leading Conservatives competing to replace Theresa May as prime minister said their party’s near wipe-out in the poll showed voters wanted them to get on and leave the EU

- French President Emmanuel Macron will push chief Brexit negotiator Michel Barnier as his choice to lead the European Commission, as leaders meet Tuesday in Brussels to begin the jostling to fill the bloc’s leadership spots. Italy will seek a seat on the European Central Bank’s Executive Board, according to a senior lawmaker in the coalition government

- Alibaba Group Holding Ltd. is considering raising $20 billion via a second listing in Hong Kong after a record-breaking 2014 New York debut. The mega-deal will bring China’s largest company closer to investors at home as U.S. tensions escalate

- Euro-area economic confidence unexpectedly improved in May, snapping an almost yearlong streak of declines when the region was battling through a host of struggles

Asian equity markets were mostly higher but with gains capped as trade slowly picked up from the holiday lull in the US and UK. ASX 200 (+0.5%) was positive with the gains led by the tech sector and as miners cheered the recent upside in commodities including Chinese benchmark iron ore prices which hit record highs. Nikkei 225 (+0.4%) was underpinned by corporate news flow with Tokyo Electron lifted from a JPY 150bln buyback, while Nissan and Mitsubishi Motors gained following the recent merger proposal between alliance partner Renault and Fiat. Hang Seng (+0.4%) and Shanghai Comp. (+0.6%) gained following a substantial liquidity injection of CNY 150bln by the PBoC which placed the ongoing trade uncertainty on the back seat. 10yr JGBs were steady as they mirrored the sideways trade in T-note futures although saw mild support following the results from the 40yr JGB auction where the b/c was firmer than previous and as 40yr yields hit their lowest levels since September 2016.

Top Asian News

- China’s First Bank Seizure in 20 Years Spooks Investors

- Nomura Penalized by Regulator After Market Information Leaked

- India Has Political Space to Do Difficult Tasks to Spur Economy

- China Stock Surge Can Repeat as MSCI Boosts Weighting

A downbeat session thus far for European equities [Eurostoxx 50 -0.6%] as the region failed to capitalise on the positive momentum seen in Asia. Most major European bourses are experiencing broad-based losses although Italy’s FTSE MIB (-0.9%) underperforms as banking names are weighed on by the decline in BTPs, whilst the UK’s FTSE (Unch) is supported by heavyweight mining names (Rio Tinto +3.2%, BHP +1.8%, Antofagasta +2.2%) profiting from the surge in iron ore price. Thus, the sector is outperforming whilst most of the other sectors are posting broad-based losses. In terms of individual movers, Renault (+0.7%) shares are higher in a continuation of yesterday’s rise due to a potential Renault-Fiat Chrysler merger. Richemont (-0.6%) and Swatch (-0.8%) are subdued amid a Swiss watch export decline of 0.4% Y/Y. Finally, Thyssenkrupp (+3.2%) rose to the top of the DAX amid a rise in steel prices. In terms of some analysis from Nomura Quant, amongst major hedge funds, macro funds are tilting short equities, with overall sentiment on US-China trade discussions on a gradual downtrend. Whilst some short-lived rallies may yet come, little optimism is seen on the immediate horizon, and it is unlikely hedge funds and CTAs will be convinced to return to buying. “It also looks likely to us that CTAs will go back to closing out long positions in NASDAQ 100 futures and S&P 500 futures starting today” says Nomura.

Top European News

- Italy Risks $4 Billion EU Penalty Over Failure to Rein in Debt

- Italy Seeks ECB Board Seat as League Urges ‘Infrastructure QE’

- Swiss Economy Bounces Back With Growth Surge at Start of 2019

- Turkish Stocks Rally as Country Hints at Russian Missile Delay

In FX, the dollar remains off recent key day reversal or retracement lows, but the DXY is still struggling to regain sufficient momentum for an attempt to revisit 98.000 and 2019 peaks reached only last Thursday (98.373). However, in a twist to normal month end trends, equity rebalancing flows may be Dollar supportive this week as at least one preliminary model is signalling a net buy, and especially strong against Sterling vs relatively weak demand against the Yen.

- JPY/NOK/SEK – The clear G10 outperformers as Usd/Jpy retreats from 109.50+ highs to test support ahead of 109.00 at a 109.23 Fib amidst a broad downturn in risk sentiment, while the Scandi Crowns continue to derive encouragement from last week’s stellar unemployment developments rather than less upbeat sentiment indicators today. Indeed, Eur/Nok has had a look at 9.2000 ahead of a key downside technical level in the form of the 100 DMA (9.7190), with extra impetus from higher Norwegian oil investment forecasts, while Eur/Sek is back below 10.7000 and has been under 10.6750.

- NZD/AUD – The next best majors as the Kiwi holds above 0.6500 vs its US counterpart awaiting the latest RBNZ Financial Stability Report due tomorrow and the Aussie maintains 0.6900+ status ahead of next week’s RBA policy meeting with a 25 bp rate cut all but totally priced in. On that note, Aud/Usd may well be capped by macro offers

- CAD/GBP/CHF – All slightly softer vs the Greenback, as the Loonie pivots 1.3450 and trades cautiously into Wednesday’s BoC (full preview available on the Ransquawk Research Suite), while the Pound hovers closer to the base of a 1.2700-1.2655 range in the fall-out from last week’s formal notice of resignation from UK PM May and the weekend EU Parliamentary elections, and with the aforementioned end of May Cable signals hardly helping. In similar vein, the Franc has not been able to glean much, if any traction from much stronger than forecast Swiss GDP, as the Government was quick to caution that one-off factors impacted favourably in Q1 and it would not be raising its full year growth forecast on the back of a bumper first quarter, while April’s trade surplus was smaller than expected. Usd/Chf is firmly above recent lows within a tight 1.0050-35 band and Eur/Chf is also looking more solid on the 1.1200 handle between 1.1245-25 vs sub-big figure levels last week.

- EUR – As noted above, the single currency has rebounded off worst levels vs the Franc despite the return of Italian/EU fiscal tensions, and the Euro is also displaying a degree of resilience against the Dollar within 1.1176-1.1200 trading parameters, albeit not convincingly through 30 DMA resistance (1.1196) or beyond 1.1200 to challenge a Fib at 1.1215.

- EM – Another marginal move up in the Usd/Cny fix overnight still leaves the spread to Usd/Cnh on a wider trajectory, but the former could be set higher in wake of the PBoC’s move to raise its counter cyclical ‘adjustments’. Elsewhere, the Try has finally reaped some benefit from Monday’s CBRT hike in the RRR, but Turkey is still embroiled in geopolitical and diplomatic conflicts that could see the Lira lurch again.

In commodities, WTI and Brent futures have been relatively resilient to the risk aversion around the market with the former hovering above USD 59/bbl and the latter around USD 70.50/bbl. Of note, there was no WTI settlement yesterday and thus there is a deviation in price change between the two benchmarks. Nevertheless, WTI’s discount to Brent has been gaining more focus, with the WTI/Brent Arb now almost USD -11/bbl. The widening spread is attributed to US stockpiles building keeping WTI subdued, whilst Brent is supported by the Russian oil contamination. Analysts at RBC highlight that physical markets are tight, and inventories are piling up despite the backwardated term structure. “We do not interpret the recent increases as entirely bearish given that the majority of builds from the US to consuming Asia have been deliberate and tactical which has, in turn, kept markets tight” RBC says. Meanwhile, gold (Unch) is flat on the day, but the yellow metal nursed some of its overnight losses as the risk tone deteriorated further, from a technical perspective; immediate levels to the upside include the 50 DMA at 1288.12/oz ahead of the psychological 1290/oz. Elsewhere, copper remains lacklustre amid the downbeat risk tone, as prices fluctuate on either side of USD 2.70/lb. Finally, Dalian iron ore prices spiked to record highs amid ongoing supply concerns and with stockpiles around 2yr lows.

US Event Calendar

- 9am: House Price Purchase Index QoQ, prior 1.1%

- 9am: FHFA House Price Index MoM, est. 0.2%, prior 0.3%

- 9am: S&P CoreLogic CS 20- City MoM SA, est. 0.5%, prior 0.2%; YoY NSA, est. 2.55%, prior 3.0%

- 10am: Conf. Board Consumer Confidence, est. 130, prior 129.2

- 10:30am: Dallas Fed Manf. Activity, est. 5.8, prior 2

DB’s Jim Reid concludes the overnight wrap

By the time you read this I’ll have just taken off for a work trip to Madrid precisely 4 days too early given this weekend’s Champions League final in this city. Unless I find a ticket lying on the floor whilst walking the streets I won’t be going on Saturday. Instead it’s nice to get away after a hard bank holiday weekend. My last google search of the long weekend was “are there pre-schools or nurseries that offer boarding?”. The twins are hard work and into everything but at least they seem to get into trouble together as they follow each other around everywhere. However 3.75 year old Maisie is so demanding. The long weekend basically involved her jumping all over me (often at speed), asking to be spun round all the time (often at speed), to be pushed on the swings (again at speed) and then clinging onto my leg or jumping on my back whenever I tried to do something else. I’m exhausted. To the younger readers please don’t have children in your 40s or beyond. You’ll be exhausted!!!

While I was being beaten up yesterday it was all about Europe with the US and UK on hols.Markets held up relatively well but there was lots to digest in terms of the European Parliament elections and also fresh worries about Italy/EU tensions. The main market highlight of the day was seeing 10yr BTPs rise 12bps to 2.67% while 10yr Bunds fell -2.8bps to -0.147% – the lowest for 3 years and only around 4bps off the all time closing lows. The EP elections in Italy were pretty much in line with forecasts but it was news from Bloomberg that the EU commission is considering a €3.5bn fine for Italy due to their ongoing debt issues that encouraged the bulk of the sell-off. The EU have a regular budgetary meeting next week and there was talk in the article that the next steps towards a fine could come at this meeting. The FTSE-MIB earlier greeted news that Salvini had extended his power base (34% vote vs. 17% in 2018 – with the M5S at 17% down from 33% in 2018) positively and was c.+1.5% just after the open. However it fell after the fine story and closed -0.06% lower with the Stoxx +0.22% as autos climbed after Fiat Chrysler’s proposed merger with Renault was announced over the weekend. Back to Italy and from listening to Salvini talk post elections it doesn’t seem he’s prepared to back down on his views and said taxes won’t be raised and that the EU has to listen to voters. He seems emboldened by a firmer mandate post the EP elections. Interesting times ahead for Italy vs the EU.

For DB’s take on the European wide elections see the piece here from Kevin Koerner. The results were broadly inline with expectations. Populists and anti-establishment parties are continuing to build support without landing knock-out blows. As Kevin writes, “the “grand coalition” of conservatives (EPP) and social democrats (S&D) has lost its traditional absolute majority in the next European Parliament. Together with the liberals and greens, pro-European groups will still hold a clear majority of two-thirds of the seats in the next EP. But policymaking for them will likely become more complex and require broader cross-party agreements and discipline.” A lot depends on the alliances formed over the next few weeks and months. As for the UK, the Brexit party – which is weeks old – stormed the polls with nearly 32%. The second referendum backing Liberals were second with around 20%. Labour were third with c.14%, the Greens fourth were c.12% with the ruling Tories in a shockingly bad 5th at c.9%. What it basically shows is that the UK in still split down the middle in terms of Brexit but the “leave” vote more focused to one party than the “remain” vote. In general election terms where its first past the post you can’t help thinking that it would be easier for the Tories to get to nearer 40% in moving to a harder Brexit policy than it would be for the Labour Party moving to a remain policy as the remain vote is a bit more spread out across parties. Again interesting times. Meanwhile, Labour leader Jeremy Corbyn promised yesterday to support a referendum on any Brexit deal after the results (per Bloomberg). Elsewhere, writing for the Telegraph, the UK Foreign Secretary Jeremy Hunt – who is standing for leader – warned that any Prime Minister who tries to take Britain out of the EU without a deal will likely trigger a general election first which risks the “extinction” of the Conservative Party. Sterling is trading relatively flat (-0.04% to 1.2674) this morning.

This morning in Asia markets are largely up with the Nikkei (+0.43%), Hang Seng (+0.50%), Shanghai Comp (+0.89%) and Kospi (+0.10%) all higher. China’s onshore yuan is down -0.17% to 6.9093. Elsewhere, futures on the S&P 500 are up +0.22% while 10y UST yields are down -1.4bps to 2.307%. In terms of overnight data releases, Japan’s April services PPI came in at +0.9% yoy (vs. +1.1%yoy expected).

As discussed at the top, at the end of last week we updated our credit spread forecasts after the team held a mid-week round table discussion which we wrote up. We’ve been tactically bullish on credit since November 2018 but previously expected this positive momentum to turn in H2. However US President Trump’s May 5th tweet has changed the landscape somewhat and as I’ve been discussing in the EMR since, risk off continues to be the most likely outcome now. We have conducted these round table exercises on numerous occasions over recent times and its fair to say that this was the meeting where there were perhaps the most divergent views within the team which perhaps speaks to the high level of uncertainty there is at the moment about the recent trade war escalation and also where we are in the cycle. I was probably most bearish as I think we bracing ourselves for a summer sell-off as both the US and China are now entrenched enough in their views that it would be difficult for them to back down without substantial external pressure. The war of words has been worse than it was in 2018 and national pride also seems to be at stake now.

The substantial pressure that might be needed to focus minds can likely only come from the markets or economic activity falling sharply. Given that the direct impact of the recent rise in US tariffs on Chinese imports is going to be minimal then the pressure is most likely to come from markets and financial conditions tightening. By the middle of June the public consultation on tariffs on the last $300bn of Chinese imports into the US will end. This final round of goods has the most potential to be damaging to the US and global economy and as such the subsequent decisions on whether to impose tariffs is going to be very important and lead us into a higher risk period for markets.