FINALIZED

GOLD: $1281.70 UP $3.90 (COMEX TO COMEX CLOSING)

Silver: $14.34 UP 11 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1280.20

silver: $14.43

COMEX EXPIRY FOR GOLD/SILVER: TUES MAY 28/2019

LBMA/OTC EXPIRY: MAY 31.2019

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 0/0

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 0 NOTICE(S) FOR NIL OZ (0.0000 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 306 NOTICES FOR 3060000 OZ (.9517 TONNES)

SILVER

FOR MAY

77 NOTICE(S) FILED TODAY FOR 385,000 OZ/

total number of notices filed so far this month: 3651 for 18,255,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $8708 DOWN $51

Bitcoin: FINAL EVENING TRADE: $ 8653 DOWN $73

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY AN UNBELIEVABLE SIZED 6027 CONTRACTS FROM 211,578 UP TO 217,605 DESPITE THE 23 CENT LOSS IN SILVER PRICING AT THE COMEX. LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR SILVER BUT IT NOW IN FULL FORCE FOR GOLD. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR MAY, 0 FOR JUNE, 2294 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 2294 CONTRACTS. WITH THE TRANSFER OF 2294 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2294 EFP CONTRACTS TRANSLATES INTO 11.47 MILLION OZ ACCOMPANYING:

1.THE 23 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

AND NOW 18.765 MILLION OZ STANDING FOR SILVER IN MAY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MAY:

24,941 CONTRACTS (FOR 20 TRADING DAYS TOTAL 24,941 CONTRACTS) OR 124.71 MILLION OZ: (AVERAGE PER DAY: 1247 CONTRACTS OR 6.235 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF MAY: 124.71 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 17.81% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 865.80 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

RESULT: WE HAD AN UNBELIEVABLE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 6027 DESPITE THE 23 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A VERY STRONG SIZED EFP ISSUANCE OF 2294 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS RESUMED THEIR LIQUIDATION OF THE SPREAD TRADES TODAY.

TODAY WE GAINED A HUMONGOUS SIZED: 8,321 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2294 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 6027 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 23 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $14.34 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.536 BILLION OZ TO BE EXACT or 158% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 77 NOTICE(S) FOR 385,000, OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ AND NOW MAY: 18.765 MILLION OZ ..

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A HUGE SIZED 12,153 CONTRACTS, TO 505,126 WITH THE $6.40 PRICE FALL WITH RESPECT TO COMEX GOLD PRICING YESTERDAY/THERE WAS HUGE LIQUIDATION OF SPREADERS YESTERDAY

WE ARE NOW 2 TRADING DAYS PRIOR TO FIRST DAY NOTICE. THE SIGNAL WAS GIVEN TO START THE LIQUIDATION PROCESS OF OUR SPREADERS ON MAY 21.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7587 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 5411 CONTRACTS, AUGUST 2019: 2176 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 505,126. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4566 CONTRACTS: 12,153 OI CONTRACTS DECREASED AT THE COMEX AND 7387 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 4566 CONTRACTS OR 456,600 OZ OR 14.20 TONNES. YESTERDAY WE HAD A LARGE PRICE FALL OF $6.40 IN GOLD TRADING ….AND WITH THAT FALL IN PRICE, WE HAD A CONSIDERABLE LOSS OF GOLD TONNAGE OF 14.20 TONNES!!!!!!

WITH RESPECT TO SPREADING: WE HAD HUGE ACTIVITY YESTERDAY

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS HAVE NOW SWITCHED TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF MAY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 129,209 CONTRACTS OR 12,920,900 OR 401.89 TONNES (20 TRADING DAYS AND THUS AVERAGING: 6460 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAYS IN TONNES: 401,89 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 401.89/3550 x 100% TONNES =11.32% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2217.41 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 12,153 DESPITE WITH LARGE PRICING LOSS THAT GOLD UNDERTOOK YESTERDAY(6.40)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7587 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7587 EFP CONTRACTS ISSUED, WE HAD A HUGE SIZED LOSS OF 4566 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7587 CONTRACTS MOVE TO LONDON AND 12,153 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE LOSS IN TOTAL OI EQUATES TO 14.20 TONNES). ..AND THIS LOSS OF DEMAND OCCURRED WITH THE LARGE FALL IN PRICE OF $6.40 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAD A HUGE PRESENCE OF SPREADING LIQUIDATION YESTERDAY/

we had: 0 notice(s) filed upon for NIL oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $3.90 TODAY

NO CHANGS IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 737,34 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 11 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV:

/INVENTORY RESTS AT 311.616 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY AN ATMOSPHERIC SIZED 6027 CONTRACTS from 211,578 UP TO 217,605 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE STOPPED THEIR LIQUIDATION IN SILVER BUT HAVE NOW MORPHED INTO GOLD..

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 0 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 2294 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2294 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 6027 CONTRACTS TO THE 2294 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GIGANTIC GAIN OF 8,321 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 41.605 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL AND NOW 18.765 MILLION OZ FOR MAY

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 23 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// FRIDAY. WE ALSO HAD A STRONG SIZED 2294 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 43.77 POINTS OR 0.67% //Hang Sang CLOSED DOWN 155.10 POINTS OR 0.57% /The Nikkei closed DOWN 256.77 POINTS OR 1.21%//Australia’s all ordinaires CLOSED DOWN 0.67%

/Chinese yuan (ONSHORE) closed DOWN at 6.9091 /Oil DOWN TO 57,28 dollars per barrel for WTI and 68.41 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9091 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9273 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/USA

An excellent commentary on the” 3 Trump cards” that China holds on the USA, namely their rare earth supply, their huge treasury hoard and the fact that China can block USA access to the Chinese markets

( Oriental Review)

ii)Funny stuff: Huawei is to ask a USA court to declare Trump’s “national Security” ban unconstitutional even though Huawei used stolen technology. The hearing will be in September.

iii)China presses the panic button with huge liquidity as interbank funding freezes up after the Baoshang seizure(courtesy zerohedge)

4/EUROPEAN AFFAIRS

i)GERMANY

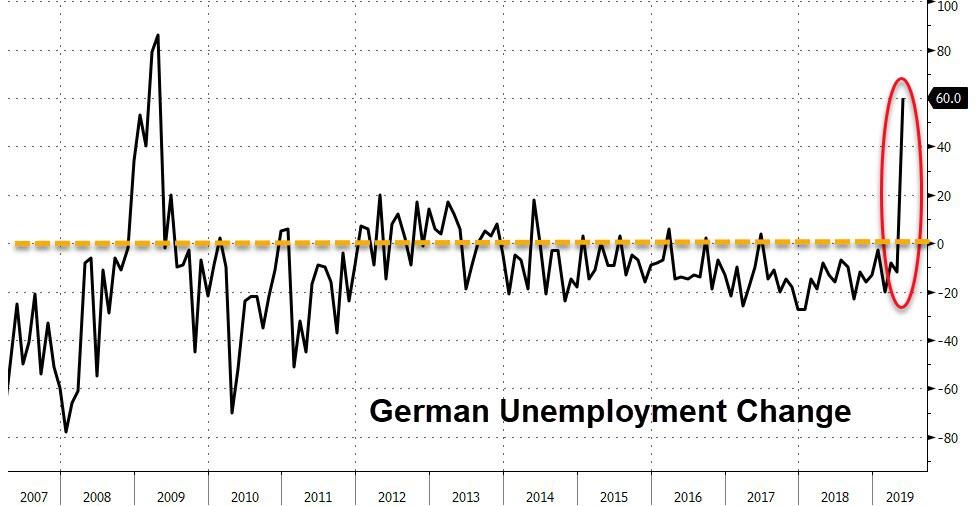

My goodness, that escalated fast…German unemployed exploded to 5.0% from 4.6% as their economy is faltering fast.

( zerohedge)

ii)Italy

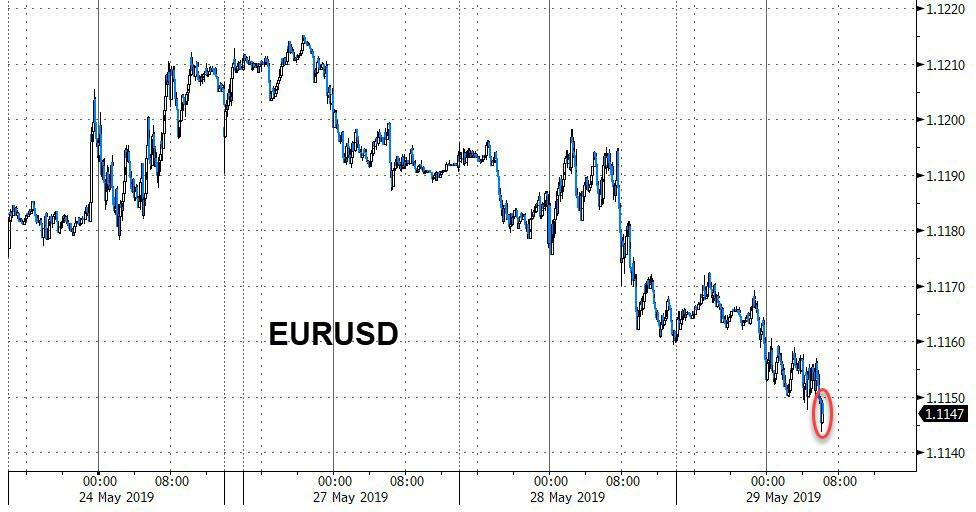

The EU confirms that Italy is now risking a massive fine over its huge deficit. It sent the Euro to session lows\\(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)IRAN/USA

(courtesy zerohedge)

ii)ISRAEL/PALESTINE/RUSSIA AND CHINA

It now seems that China and Russia will be against any USA initiative. Today they are against Trump’s Middle east proposal

( zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

VENEZUELA/

9. PHYSICAL MARKETS

Craig Hemke discusses what the bond market is telling us:

( Sprott/Hemke/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

MARKET TRADING/Europe Monday

ii)Market data

iii)USA ECONOMIC/GENERAL STORIES

SWAMP STORIES

i)Comey is one big nut job: here he states that there was no coup and Trump and his supporters are stating nothing but lies on him and his upper echelon of cohorts

( zerohedge)

ii)Full scale war in the intelligence community as Christopher Steel refuses to cooperate with AG Barr and Durham

( zerohedge)

iii a) We will be following this: Mueller is to make an unexpected statement on the Russian probe at 11 am

THE INTERVIEW AT 11 AM WAS A “NOTHING BURGER”

( zerohedge)

iii b)Democrats are now put into a tough spot after Mueller is goading them into the impeachment process

(courtesy zerohedge)

iii)c And then this; Pelosi and Schumer refuse to endorse impeachment procedures after the Mueller statement

( zerohedge)

Let us head over to the comex:

Gold withdrawals;

i) We had 1 withdrawal:

out of Brinks: 2170.88 leaves brinks

.

In Gold We Trust 2019 – Gold in the Age of Eroding Trust

In Gold We Trust 2019 –The Annual Gold Report from Incrementum is Here

We are happy to report that the new In Gold We Trust Report (2019) has been released today and the download link can be found at the end of this post.

Ronnie Stoeferle and Mark Valek of Incrementum and numerous guest authors once again bring you what has become the reference work for anyone interested in the gold market.

They are honoured that some of the thought leaders of the gold market read and support their annual In Gold we Trust report! #IGWT19

Mark O’Byrne @MarkTOByrne comments on the @IGWTreport:

“Put not your trust in money, but put your money in trust.”

Oliver Wendell Holmes

Key Takeaways

• Trust is the basic value of interpersonal cooperation and the cement of our social order. The erosion of our “trust capital” can be observed in many areas of society.

• The breakdown of trust in the international monetary order is manifesting itself in the highest gold purchases by central banks since 1971 and the ongoing trend to repatriate gold reserves.

• Gold reaffirmed its portfolio position as a good diversifier as trust in the “Everything Bubble” was tested in Q4/2018. While equity markets suffered doubledigit percentage losses, gold gained 8.1% and gold mining stocks 13.7%.

• The normalization of monetary policy was abruptly halted by the stock market slump in Q4/2018. The “monetary U-turn” that we already forecasted last year has begun.

• Recession risks are significantly higher than discounted by the market. In the event of a downturn, negative interest rates, a new round of QE, and the implementation of even more extreme monetary policy ideas (e.g. MMT) are to be expected.

• When it comes to trust in investments, our vote is clear. Trust looks to the future, forms itself in the present, and feeds itself from the past. Gold can look back on a successful five-thousand-year history as sound money.

And here is the download link to the 2019 IGWT Report – Enjoy!

In Gold We Trust 2019 – Gold in the Age of Eroding Trust (PDF)

LBMA Gold Prices (USD, GBP & EUR – AM/ PM Fix)

28-May-19 1283.90 1278.30, 1012.87 1008.20 & 1146.91 1142.29

27-May-19 UK Bank Holiday

24-May-19 1281.50 1282.50, 1011.36 1011.89 & 1145.92 1145.40

23-May-19 1275.95 1283.65, 1009.79 1015.37 & 1146.19 1152.46

22-May-19 1274.00 1273.80, 1005.44 1008.09 & 1141.12 1141.20

21-May-19 1276.00 1271.15, 1004.85 998.62 & 1144.19 1139.84

20-May-19 1275.25 1276.85, 1000.05 1003.22 & 1142.63 1143.42

17-May-19 1285.80 1280.80, 1007.55 1005.17 & 1152.08 1146.70

16-May-19 1295.55 1291.70, 1009.62 1009.46 & 1155.76 1154.78

15-May-19 1298.90 1299.10, 1005.87 1011.87 & 1158.75 1161.53

14-May-19 1297.60 1298.40, 1002.14 1005.48 & 1154.34 1158.04

13-May-19 1282.95 1295.60, 985.95 994.89 & 1142.47 1151.27

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

Craig Hemke discusses what the bond market is telling us:

(courtesy Sprott/Hemke/GATA)

* * *

Craig Hemke at Sprott Money: What is the bond market telling you?

Submitted by cpowell on Tue, 2019-05-28 21:17. Section: Daily Dispatches

5:15p ET Tuesday, May 28, 2019

Dear Friend of GATA and Gold:

Interest rates, Craig Hemke of the TF Metals Report writes today at Sprott Money, are inverting as they often do just before a recession and economic contraction, which may already be underway. Whereupon, he adds, the Federal Reserve will intervene massively with interest rate cuts and purchases of financial assets in another round of “quantitative easing.” Hemke predicts this will be good for gold. His analysis is headlined “What Is the Bond Market Telling You?” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/what-is-the-bond-market-telling-you-cra…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

-END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

* * *

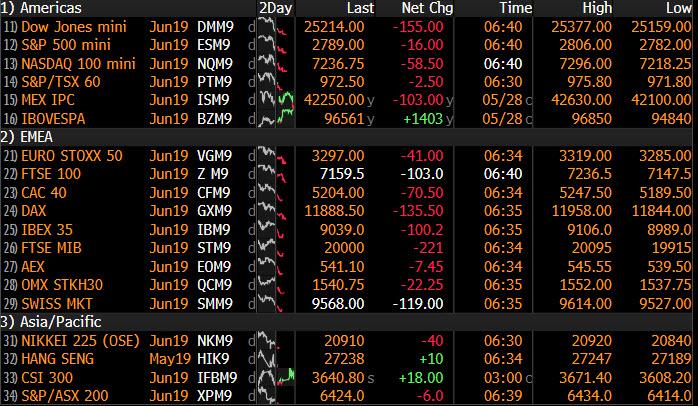

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.9094/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.9273 /shanghai bourse CLOSED DOWN 43.77 POINTS OR 0.67%

HANG SANG CLOSED DOWN 155.10 POINTS OR 0.57%

2. Nikkei closed DOWN 256.77 POINTS OR 1.21%

3. Europe stocks OPENED RED /

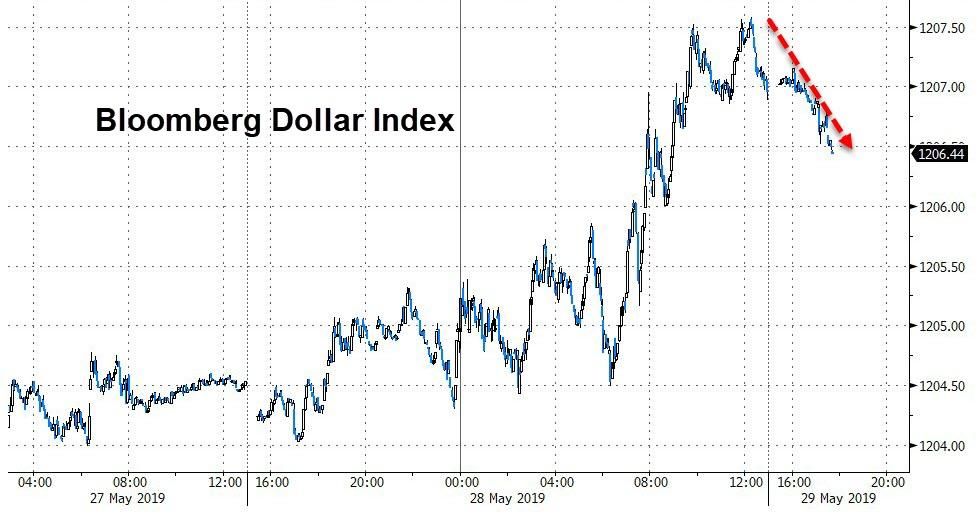

USA dollar index RISES TO 98.00/Euro FALLS TO 1.1154

3b Japan 10 year bond yield: FALLS TO. –.09/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.29/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

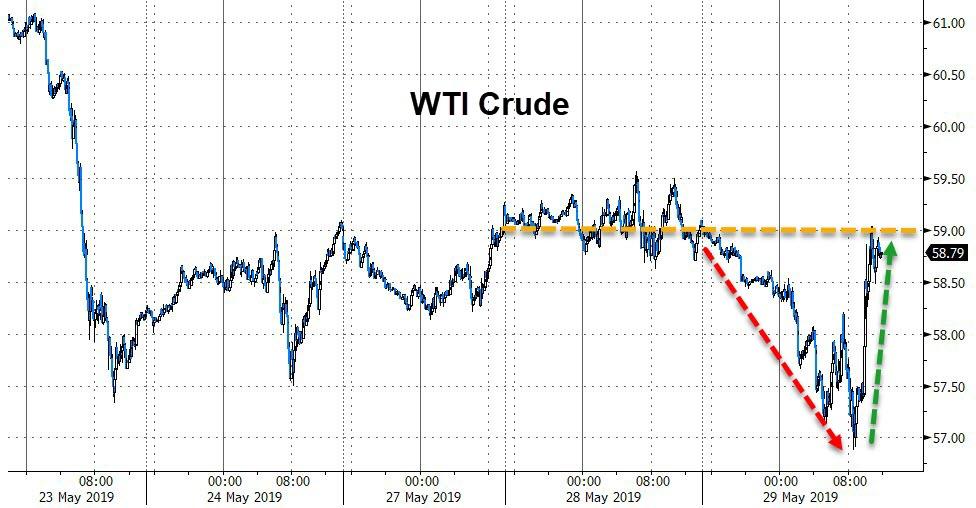

3e WTI:: 57.28 and Brent: 68.41

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

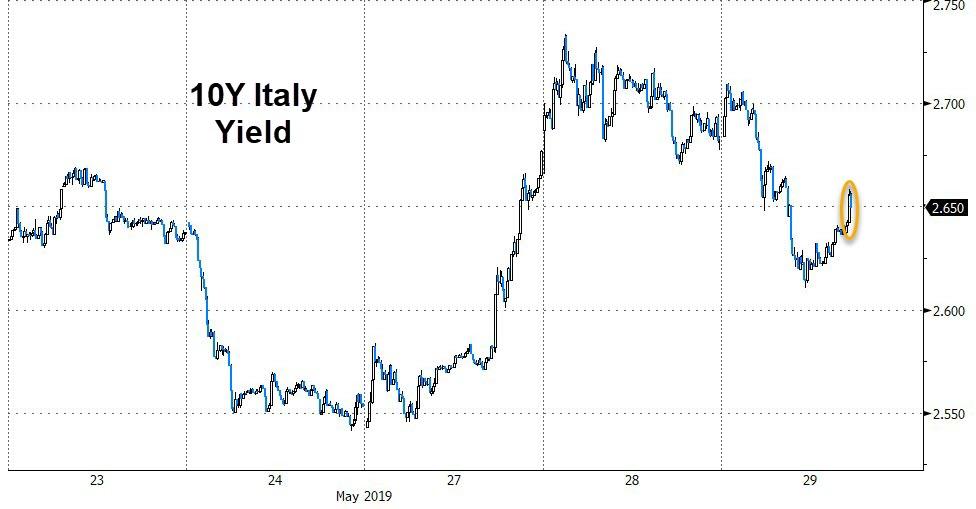

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.17%/Italian 10 yr bond yield DOWN to 2.64% /SPAIN 10 YR BOND YIELD DOWN TO 0.76%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.84: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.13

3k Gold at $1284.20 silver at: 14.46 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 48/100 in roubles/dollar) 65.17

3m oil into the 57 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.29 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0054 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1216 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.17%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.23% early this morning. Thirty year rate at 2.66%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 6.0107..they are toast

Markets Tumble, S&P Below 2,800, Bond Yields Crater As Traders Brace For Impact

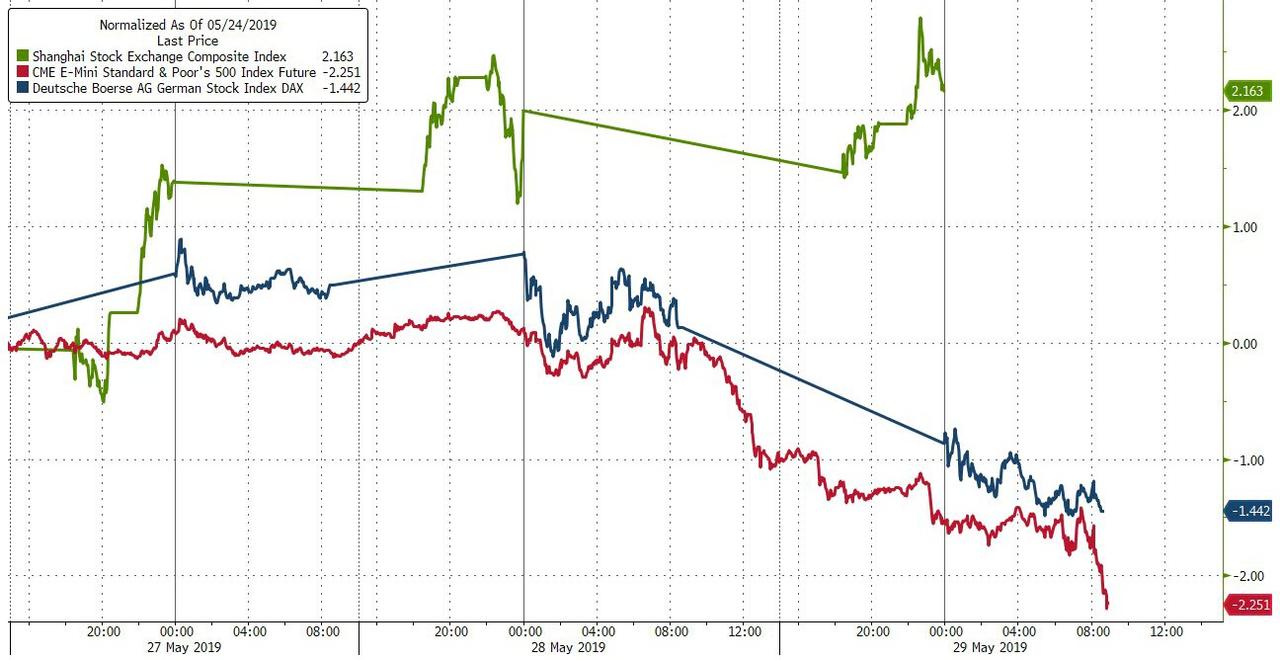

It’s going from bad to worse for global equity market and US stock futures, which again are a sea of red as Sino-U.S. trade tensions continue to escalate – with a rare earth boycott by China now virtually assured – while fears of an Italy-EU confrontation are growing again, accelerating a global bond rally on Wednesday, as investors dumped shares and scurried for the safety of government debt, the dollar and gold.

Amid the rush out of risk, German yields fell deeper into negative territory and inched toward record lows around minus 0.2%. In the US, 10Y Treasury bond yields reached 20-month lows, dropping as low as 2.20%, having fallen almost 30 basis points this month.

Benchmark yields slid to the lowest since 2016 in Japan, to a record in New Zealand and below the central bank’s policy rate in Australia. The 3M-10Y yield curve continued to slide deeper into negative territory, touching -13bps in the US, the lowest since 2007, and inverted in Australia and South Korea.

“What I see as more consistent is that typically when the yield curve inverts you get central bank easings. So the question about recession would be: would the U.S. Fed ease enough to avoid a recession?” said Nikko Asset Management PM Chris Rands. In relation to that, US. rates futures are pricing in two cuts by the Federal Reserve by the middle of next year to help prop up the country’s economy. “The fact that you have got a bit more noise around the trade war now at the same time as manufacturing is rolling over — it’s getting people to think that things are a little bit worse than they had expected,” he said.

Amid the global risk off, S&P500 futures slumped, with the Emini sliding below 2,800 for the first time since March after a bout of overnight selling, indicating a weak opening in New York.

Sentiment soured after President Trump’s comment that he was “not yet ready” to make a deal with China over trade. Chinese newspapers responded on Wednesday with a warning Beijing could use rare earths to strike back at the United States, suggesting further tit-for-tat escalation is imminent.

Asian stocks dropped, led by health care and consumer staples companies, after rising in the previous three trading days. Most markets in the region were down, with South Korea’s Kospi losing its year-to-date gain. The Topix gauge fell 0.9%, driven by Takeda Pharmaceutical and Sony. The Shanghai Composite Index edged higher, though, rising 0.2%, as large insurers rallied on a tax deduction.

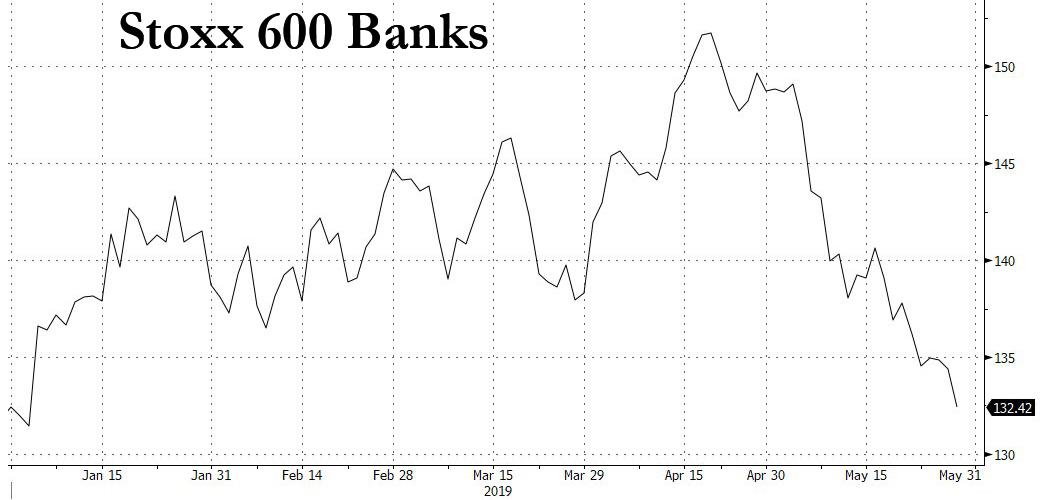

Later in the session, declines in European miners and tech companies pulled the Stoxx Europe 600 Index lower, after Japanese and South Korean equities bore the brunt of losses in Asia. European shares opened lower, with Germany’s exporter-heavy index down 1% and a pan-European share benchmark losing 1.3%. Europe’

Europe’s Stoxx 600 Banks Index falls as much as 1.7% on Wednesday, erasing all gains for the year 2019, to head for its worst month in three years. The decline was skewed by BNP Paribas down 7.9% as stock trades ex-dividend, however it was mostly bond yields hitting new lows that was once again weighing on the sector’s earnings outlook. Italian banks remain vulnerable as the political drama continues with EU Commission President Juncker confirming the EU is ready to open a disciplinary procedure concerning Italy’s debt, la Repubblica reported.

Italian Deputy Prime Minister Matteo Salvini, emboldened by his party’s strong EU election showing, has stepped up promises to slash taxes and is calling for new EU budget rules, raising fears his plans will drive up Italy’s huge public debt. Italian 10-year bond yields rose for the third day in a row to 2.73%.

A gauge of emerging-market stocks fell to the lowest since January and most developing-nation currencies declined versus the dollar.

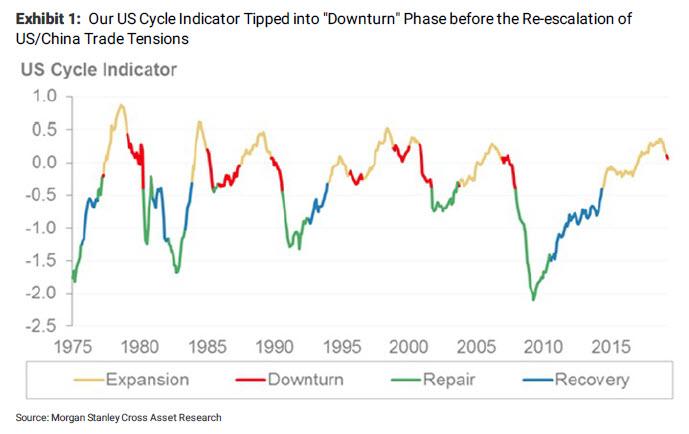

It’s not just trade war and renewed Italian tensions that are spooking markets: as Morgan Stanley noted overnight, the US economy was already sliding into a slowdown ahead of the May trade war return. Recent economic data, such as purchasing-manager surveys, have disappointed — U.S. manufacturing growth dropped to 10-year lows. A barrage of American data tomorrow and Friday will give traders more to chew on as they reassess the Federal Reserve’s policy path.

“Then we have a weaker growth outlook … so we have the negative shock of trade added to lower growth and the cushion of protection isn’t as good as it was eight to nine months ago.”

Another round of tariffs would sharply raise U.S. recession risk, said Justin Onuekwusi, a fund manager at Legal & General Investment Management. “The market is simply calculating what the impact will be of the next set of tariffs as it doesn’t look like the rhetoric is calming down. Then we have a weaker growth outlook … so we have the negative shock of trade added to lower growth and the cushion of protection isn’t as good as it was eight to nine months ago.”

As Reuters adds, the news was gloomy on the political front as well. Eurosceptic parties gained in recent EU elections, Austria and Greece face elections and Italy’s dispute with the European Commission over its budget may be escalating. In Britain, many speculate risks of a hard Brexit have risen, because candidates lining up to succeed Prime Minister Theresa May are mostly eurosceptic.

Currency activity was muted, with the dollar edging higher versus its major counterparts for a third day. The dollar is on track for its fourth straight month of gains, benefiting from flows away from markets such as Asia that are considered at greater risk from trade wars. The yuan steadied following news that the People’s Bank of China had injected the most in money-market operations since January. The euro was unchanged at $1.1159 after falling two straight days. The British pound slid to $1.2639.

On Tuesday, in its delayed report, the US Treasury said no major trading partner met currency manipulation list but added that China, Germany, Japan, Ireland, Italy, South Korea, Malaysia, Singapore and Vietnam warrant placement on its currency monitoring list (Switzerland and India were removed). Furthermore, it lowered 2 thresholds used to designate FX manipulators and urged China to take necessary steps to avoid a persistently weak currency

In commodities, West Texas oil futures dropped, losing all of their gains from Tuesday and more, dipping below $59 a barrel in New York. Gold recovered most of Tuesday’s losses as U.S.-China trade tensions climbed and global growth concerns escalated, as investors continue to seek haven assets. The metal has missed out on some haven buying in recent days, with investors favoring the dollar and bonds. Gold is on pace for its fourth monthly decline.

Expected data include mortgage applications. Canada Goose, Trulieve Cannabis and Palo Alto Networks are among companies reporting earnings

Market Snapshot

- S&P 500 futures down 0.5% to 2,790.25

- STOXX Europe 600 down 1.2% to 371.30

- MXAP down 0.7% to 152.67

- MXAPJ down 0.7% to 497.36

- Nikkei down 1.2% to 21,003.37

- Topix down 0.9% to 1,536.41

- Hang Seng Index down 0.6% to 27,235.71

- Shanghai Composite up 0.2% to 2,914.70

- Sensex down 0.4% to 39,606.99

- Australia S&P/ASX 200 down 0.7% to 6,440.03

- Kospi down 1.3% to 2,023.32

- Brent futures down 2.2% to $68.60/bbl

- German 10Y yield fell 0.2 bps to -0.163%

- Euro down 0.02% to $1.1158

- Italian 10Y yield rose 0.6 bps to 2.31%

- Spanish 10Y yield fell 4.9 bps to 0.738%

- Gold spot up 0.4% to $1,284.73

- U.S. Dollar Index up 0.1% to 99.04

Top Overnight News

- The Trump administration again refrained from labeling China a currency manipulator. The U.S. Treasury Department issued its semi-annual foreign-exchange report, expanding the number of countries it scrutinizes for currency manipulation to 21 from 12

- Traders are pricing in quicker and deeper rate cuts by the Federal Reserve as global macro risks ratchet higher. Swap markets now indicate expectations for three 25 basis point cuts by the end of 2020, a new dovish extreme for this cycle

- China accused the U.S. of abusing a national security exception at the WTO by cutting off Huawei Technologies to American suppliers and warned the move could have grave consequences

- Treasuries are in the vanguard of a bull run in global bonds, bringing into sight the prospect of benchmark 10-year yields dropping to 2% for the first time since late 2016

- Oil climbed for a second day as supply risks from the Middle East to the U.S. Great Plains overwhelmed concerns trade tensions will swamp energy demand

- Beijing is gearing up to use its dominance of rare earths as a counter in its trade battle with Washington, according to a salvo of media reports in China that included hints from the state planning agency

- Angela Merkel has decided that Annegret Kramp-Karrenbauer, who took over as leader of the Christian Democratic Union in December, is not up to the country’s top job, according to two officials with knowledge of her thinking

- Escalating U.S.-China trade tensions and faltering global growth have seen U.S. 10-year yields tumble and has brought into sight the prospect of benchmark yields dropping to 2% for the first time since late 2016

- German unemployment unexpectedly rose by 60,000 in May, compared with economists’ forecasts for a decline of 8,000. This was the first climb in almost two years as the economic slowdown finally started to take a toll on the labor market

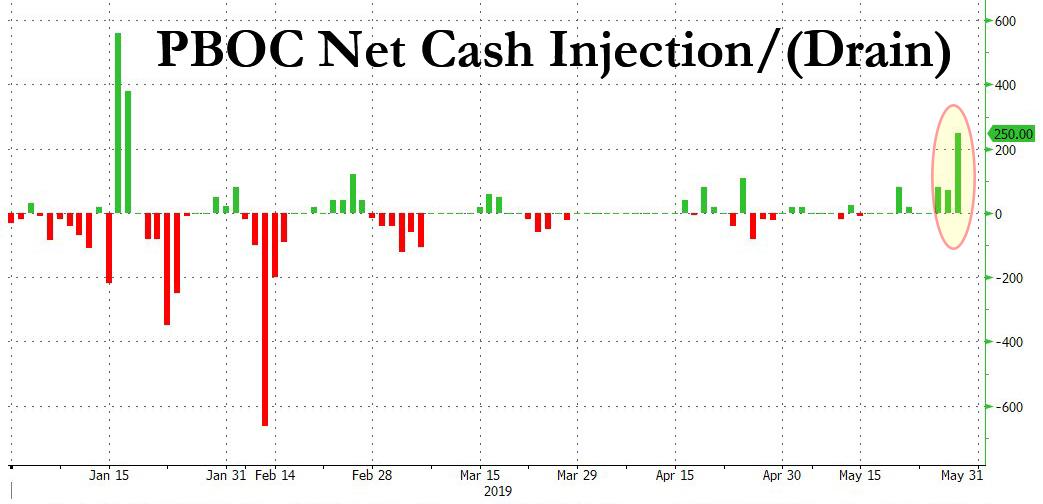

- China’s central bank moved to curb the risk of a funding squeeze on banks after the government’s surprise seizure of Baoshang Bank Co. sparked a jump in borrowing costs. The PBOC injected a net $36 billion Wednesday

Asian equity markets were mostly lower following the headwinds from US where all major indices declined on return from the extended weekend and in which the E-mini S&P eventually broke below the 2800 level. The weakness was attributed to lingering trade tensions after Chinese press pointed the blame on US for the recent breakdown in talks and as the outspoken Global Times Editor suggested China is seriously considering restricting rare earth exports to the US. ASX 200 (-0.7%) and Nikkei 225 (-1.2%) were negative with broad weakness seen across nearly all sectors in Australia and with financials subdued by the recent declines in global yields, while currency strength added to the pressures for Tokyo stocks. Hang Seng (-0.6%) and Shanghai Comp. (+0.1%) declined amid the trade uncertainty and as early data indicators reportedly suggested China’s economy weakened this month, although the losses were cushioned by a substantial liquidity operation of CNY 270bln which resulted to the PBoC’s largest daily net injection since mid-January. Finally, 10yr JGBs were higher as they tracked the upside in global counterparts amid declining yields and the negative risk sentiment, which lifted prices of the Japanese 10yr benchmark to above 153.00 and its best level since early April.

Top Asian News

- The Old Yen-as-Haven Trade Just Isn’t Panning Out as It Should

- Malaysia Weighs Bids for Return to Euro, Swiss Franc Bond Market

- Bank of Thailand MPC Member Expects Period of Key Rate Stability

European equities are lower across the board [Eurostoxx -1.6%] following on from a downbeat session in Asia as sentiment took the queue from Wall Street after the E-Mini S&P took out the 2800 level to the downside. Sectors are all in the red with IT names lagging after Huawei signalled that it is pressing ahead with its lawsuit against the US government as US-China tech tensions intensify. Defensive stocks such as utilities and healthcare names are somewhat faring better, albeit still in the red. In terms of individual movers, ProsiebentSat1 (+4.0%) spiked higher amid reports that Mediaset (-0.8%) are to purchase a 9.1% stake in the company, which would grant 9.9% of voting rights, although Mediaset noted that they do not seek board representation. Elsewhere, Casino (-4.6%) shares slid after the company announced that it will not pay an interim dividend this year, whilst S&P downgraded its credit after its parent company entered French safeguard procedures. Finally, ArcelorMittal (-4.0%) opened lower by as much as 7% after cutting production guidance in Europe amid weak market demand. In light of the recent sell-off in stocks amid trade woes, Nomura believe that the downside can be seen as orderly and sentiment is not out of control. The analysts state that the recent sell off in equities is being fuelled by transient stock selling via speculative players and a seasonal rise in volatility, as global equities pass through a predictable second wave of selling. Following the E-mini S&P’s declined below 2800, eyes turn to the cash market at the US open where Nomura warns that “CTAs have been pressed to close out long positions and cut their losses once the S&P 500 broke below 2,820”, but CTAs have already unwound over 80% of their longs, thus the risk of a chain reaction sell-off has diminished.

Top European News

- German Unemployment Rises as Weaker Economy Starts to Bite

- Berlusconi’s Mediaset Buys Stake in Germany’s ProSiebenSat.1

- Swiss Open Criminal Probe After Complaint Against Glencore

- Varta Acquires Varta Consumer Batteries Business From Energizer

In FX, we start with CHF/JPY/USD – The Franc’s resurgence or rebound from yesterday’s lows seems symptomatic of the wider safe-haven demand and deeper risk-off sentiment. Usd/Chf has retreated towards 1.0050 again vs a fraction shy of 1.0100 at one stage on Tuesday, while Eur/Chf is drifting back down to 1.1200 compared to almost 1.1280, albeit with the single currency under pressure independently on the back of latest bleak German data – see below. Usd/Jpy has also recoiled to retest key Fib support ahead of 109.00 at 109.23 (Fib retracement level) having bounced firmly to just over 109.60, but decent option expiry interest may prop up the headline pair (1 bn between 109.00-15) on top of anticipated buying interest at the big figure. Note also, the Buck has extended its recovery in wake of upbeat US consumer confidence and with the aid of gains vs riskier/high beta currencies, with the DXY back above 98.000, albeit just and eyeing last week’s 98.373 ytd best within a 98.043-97.861 range.

- NZD/CAD/GBP/AUD/EUR – All softer vs the Greenback, and with the Kiwi underperforming after the latest RBNZ FSR and NBNZ business survey showing that expectations remain weak. Nzd/Usd has slipped back below 0.6550 to around 0.6515, with the Aud/Nzd cross climbing over 1.0600 again even though the Aussie is also struggling to retain 0.6900+ status following yet another uber dovish RBA call overnight as JPM is now predicting a total of 100 bp worth of easing by mid-2020. Elsewhere, the Loonie is really trading on the defensive as the clock ticks down to a potentially dovish BoC with Usd/Cad not far from 1.3520+ late April peaks and options pricing a circa 53 pip break-even over the event – see our policy meeting preview on the Research Suite. Meanwhile, Cable is slipping further from 1.2700 towards the big figure below as another Tory leadership hopeful joins the list and the EU stresses no renegotiation of the WA, and Eur/Usd is hovering just above 1.1150 stops having failed to hold above the 30 DMA (1.1191) again. Note, a shock jump in German unemployment and uptick in the jobless rate that was only partly mitigated by a reclassification of the labour force also weighed on the Euro as noted above.

- NOK/SEK – Divergence between the Scandi Crowns as Eur/Nok rebounds through 9.7500 amidst another retreat in oil prices (that may also be niggling the Cad), but Eur/Sek is capped around 10.7000 after significantly stronger than forecast Swedish Q1 GDP data (largely due to a healthy export contribution vs depressed domestic consumption however).

- EM – Contrasting fortunes for the Lira and Rand as well, like yesterday, as Usd/Try revisits 6.0000, but Usd/Zar pivots 14.8000 within 14.8900-7000 parameters on a further fall-out from SA political developments and the return of Mabuza to Ramaphosa’s fold.

In commodities, WTI (-2.3%) and Brent (-2.0%) futures continue to free-fall amidst the risk-off tone in the market, with the former extending loses below the psychological USD 58.00/bbl and under its 100 DMA at USD 58.46/bbl. Similarly, its Brent counterpart trades south of the USD 69/bbl level and closer to the USD 68.50/bbl mark. News flows has been relatively light in the complex although the Druzhba pipeline will be pumping clean oil to Hungary as of 1700BST following the halt in operations amid contaminated oil from Russia in mid-April. Turning to OPEC, ahead the upcoming meeting of the cartel (date yet to be confirmed), Kazakhstan’s Energy Minister noted that it stands ready to join the extension of the global oil cut deal if the decision in taken. On that front, Russia’s First Deputy PM noted that they will consider an extension to the deal but have arguments in favour and against an extension, adding that Moscow will continue to weight the arguments. Finally, as a reminder, the API crude inventory data will be released tonight due to US’ market absence on Monday, and thus the EIA release has been delayed until tomorrow.

Over in the metal complex, gold (+0.4%) continues to rise despite a firmer USD as investors flee to the safe haven amid the current risk aversion; meanwhile, copper (-0.8%) falls in tandem with the risk tone. Further for the red metal, workers at the Chilean Chuquicamata copper mine of have been voting on a potential strike after labour unions rejected management’s final offer on wages. The results of the vote are expected this evening.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 2.4%

- 10am: Richmond Fed Manufact. Index, est. 7, prior 3

DB’s Jim Reid concludes the overnight wrap

If like me you are looking to fill the Game of Thrones void you can do worse than to watch “Chernobyl” if it’s available in your region. I got home late from Madrid last night and didn’t even say hello to my wife but instead rushed in and sat down next to her to watch the gripping penultimate episode after binge watching the previous three over the last week. Obviously the subject matter and scenes are not for the faint hearted but it really is very good. I looked at the definitive big screen database IMDb last night and remarkably it’s already become the highest ranked TV show in history. For those interested, the full top 10 are Chernobyl, Planet Earth II, Band of Brothers, Planet Earth I, Breaking Bad, Game of Thrones, Our Planet, The Wire, Cosmos and Blue Planet. Obviously a lot of natural history fans on this site. The only problem about getting hooked on the five episodes of Chernobyl is that I’m pretty sure that it’s not going to have a season 2!!

It feels like the trade war still has a number of episodes left with the option of being renewed for a new season. The stand-off continues to dominate proceedings in markets with yesterday’s highlight being a fresh new low for 10y Treasuries after they closed at 2.266%, down -5.4bps (a further -2.4bps this morning) and to the lowest for over 20 months. Though equities opened higher and held up well for most of the day, they ended up selling off in the last two hours of NY trading. The S&P 500 fell -0.84%, with the DOW and NASDAQ down -0.93% and -0.39%, respectively. The utilities sector fell -1.61%, retracing some of its recent outperformance, while the NYFANG index was the rare bright spot after a +0.05% advance.

Earlier comments from President Trump about the US not being ready to reach a trade deal with China and that tariffs could go up “very very substantially”, as well as the not-so-insignificant news that the Chinese government had taken control of Baoshang Bank – the first Chinese bank seized in 20 years – and also that China is “seriously considering” restricting rare earth exports to the US according to the Global Times Editor, all contributed to the negative sentiment even if the full sell off only occurred late in the day. In fairness a surprisingly upbeat consumer confidence reading (more on that below) was reason for some earlier optimism.

A flight to quality dominated though and not only did yields fall but the US curve flattened with 2s10s -1.5bps at +13.9bs and to the lowest since March. It has reversed this move this morning though as 2yr yields are over 4bps lower. Bunds ticked down another -1.7bps yesterday to close at -0.161%. I must admit that after they sold off from their all time record low of -0.189% in July 2016, I was pretty confident that we may not see these lows again for perhaps a thousand years given where yields have traded over the last millennium. I’m 2.7bps from being 997 years wrong.

Meanwhile the STOXX 600 closed -0.22% with Italian assets remaining choppy yesterday. They initially opened much weaker although they did at least attempt to bounce back late afternoon. The FTSE MIB closed -0.50% after being down -1.33% in the morning session and 10y BTPs finished flat after rallying back 5bps from the earlier wides. The partial recovery appeared to be supported by the EU’s Moscovici stating that he didn’t support sanctions for Italy. A reminder that this followed stories of the European Commission proposing a disciplinary procedure for Italy as soon as next week following failure to reduce its debt. Regardless, Northern League leader Salvini said he plans to push ahead with his tax cut plan by submitting it to the cabinet, so this issue will continue to fester for many more months.

After US markets had closed, the US Treasury released their latest FX Report, which refrained from labeling any countries as “currency manipulators,” but expanded the list of countries under review and added Italy, Ireland, Singapore, Malaysia, and Vietnam to the “watch list.” Notably, they did not designate China as a manipulator, which would have automatically triggered a new bilateral negotiation process and possible additional sanctions, though the language criticised the “misalignment and undervaluation of the RMB relative to the dollar.” The new countries join China, Japan, Korea, and Germany on the watch list, while India and Switzerland were removed. The criteria used to evaluate countries were also modified, with stricter definitions for a material current account surplus and persistent one-sided intervention.

Turing to trade war related news, most of China’s news dailies are carrying articles today signifying that China could use rare earth exports as a bargaining chip in the ongoing trade war with the US. The Global Times carried an editorial today saying that “sooner or later” China will use “the weapon of rare earth” if the US keeps escalating the trade war while adding that although this weapon is powerful, it will only be used as a tool for defence to convey a message that China won’t bow to US pressure. The People’s Daily, a flagship newspaper of the ruling Communist Party, also carried an editorial today stating that the US shouldn’t underestimate China’s ability to fight the trade war while using some historically significant language on the weight of China’s intent, like the phrase “don’t say I didn’t warn you.” The specific wording was used by the paper in 1962 before China went to war with India and in 1979 before conflict broke out between China and Vietnam. The Global Times had said in an article in April that “those familiar with Chinese diplomatic language know the weight of this phrase.” Meanwhile, an official at the China’s National Development & Reform Commission told CCTV that people in the country won’t be happy to see products made with exported rare earths from China being used to suppress China’s development. Elsewhere, at a meeting of the WTO’s Committee on Market Access in Geneva yesterday, China said that the US had violated WTO rules and urged the Trump administration to “immediately lift all unilateral sanction measures against Chinese companies” while warning that the move could have grave consequences for the global trading system. So lots of more negative rhetoric.

This morning in Asia markets are mostly trading down with the Nikkei (-1.17%), Hang Seng (-0.40%), Shanghai Comp (-0.11%) and Kospi (-1.47%) all lower. The South Korean won is down -0.631% this morning while the onshore Chinese yuan is trading flattish (-0.06% to 6.9142). Meanwhile, yields on 10yr JGBs are down -0.4bps to -0.09% and crude oil prices (WTI -1.03% and Brent -0.68%) are heading lower. Elsewhere, futures on the S&P 500 are down -0.32%. In commodities, base and ferrous metals are heading lower with iron ore futures (down c.3%) leading the declines.

In other news, the PBOC stepped up its efforts to bridge the funding gap in China’s financial system after the surprise seizure of Baoshang Bank Co. led to a jump in borrowing costs by injecting c. CNY 250bn into the financial system via open-market operations today. So lots of moving parts at the moment.

In terms of data yesterday, US consumer confidence in May surprisingly jumped +4.9pts to 134.1, exceeding expectations for a 130.0 reading. In fact the headline reading is now back to being at the highest level since last November. Both the present situations and expectations components rose also with the data collected through the 18th of this month, and thus capturing some of the recent risk off. So a surprisingly positive set of data given the recent trade escalation. It’s worth noting that within that survey, the jobs plentiful/hard-to-get differential hit the highest since 2000 which points to a still healthy labour market. Elsewhere, we also got plenty of house price data yesterday including the FHFA house price index (+0.1% mom vs. +0.2% expected) and S&P CoreLogic index (+0.09% vs. +0.46% expected) – both of which disappointed in March and confirmed that home price appreciation has slowed meaningfully in recent months. Finally, the Dallas Fed’s manufacturing activity survey dropped to -5.3 from 2.0, close to its multi-year low.

As for Europe, the most significant release was the ECB’s M3/credit report for April. Our economists in Europe noted that in summary the monthly credit data were positive in aggregate with net bank loan flows, after recent soft prints, recovering to EUR +43bn, the highest monthly print in the current cycle. As a result, the euro area credit impulse rebounded from negative levels in recent months to its strongest reading since summer 2018, with credit growth picking up to +3.7% yoy. However, the team also flagged that country details show signs of concern due to underperformance in the periphery. Though the credit impulse rebounded in Italy and Spain, it was boosted by base effects and it is set to turn negative again if the current pace of loan flows, with negative corporate credit growth, continues. For the ECB, the credit data continue to favour generous TLTRO3 terms but less so deposit tiering in the view of the team. On that topic of deposit tiering and the adverse impact of negative interest rates, Bank of France Governor Villeroy said yesterday that “the issue should certainly not be ignored, but we also need to avoid blowing it out of proportion.”

As for the other data yesterday, the May economic confidence reading for the Euro Area improved 1.2pts to 105.1, far exceeding expectations for a broadly flat print. In addition industrial and service sector confidence was higher however industrial order books, and especially export orders, were down once again. On a country level, Germany’s consumer confidence ticked down slightly while France’s rose. Over in Turkey, consumer confidence fell to 55.5, its lowest level on record going back to 2004, though the lira nevertheless strengthened +0.50%.

To the day ahead now, which is another quiet one for data with the preliminary May CPI and final Q1 GDP reports in France this morning, May unemployment data in Germany and then the May Richmond Fed manufacturing survey in the US being the only releases due. Away from, that we’re due to hear from the ECB’s Mersch and Rehn this morning before we get the release of the ECB’s financial stability review. The BoC rate decision is also due this afternoon.

end

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 43.77 POINTS OR 0.67% //Hang Sang CLOSED DOWN 155.10 POINTS OR 0.57% /The Nikkei closed DOWN 256.77 POINTS OR 1.21%//Australia’s all ordinaires CLOSED DOWN 0.67%

/Chinese yuan (ONSHORE) closed DOWN at 6.9091 /Oil DOWN TO 57,28 dollars per barrel for WTI and 68.41 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9091 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9273 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

i)China/USA

An excellent commentary on the” 3 Trump cards” that China holds on the USA, namely their rare earth supply, their huge treasury hoard and the fact that China can block USA access to the Chinese markets

(courtesy Oriental Review)

Global Times: China Holds Three Trump Cards In War Against US

Amid the escalating economic war between the US and China, discussions have intensified on how Beijing might stand up to the economic power of America, especially given that the global economy is increasingly dependent on the US dollar as the main currency for international trade, and the closing of US markets could do some serious damage to China’s export-oriented companies. China’s main foreign-policy publication, the Global Times, points to three trump cards that Beijing could use to at least level the playing field in its fight with the Trump administration and cause appreciable harm to the US economy, possibly forcing its opponent to temporarily scale back its ambitions.

According to an article in the Global Times by a professor at the Renmin University of China, the three trump cards are:

1) banning the export of rare earths to the US;

2) blocking US companies’ access to Chinese markets; and

3) using China’s portfolio of US Treasury bonds to bring down the US government debt market.

Each of these trump cards are worth looking at in detail, both in terms of their impact on the US economy and also in terms of any possible retaliation from the US and the repercussions for the global economy as a whole.

Banning the export of rare earths to the US would actually be a pretty serious blow for US electronics manufacturers and, indeed, US high-tech manufacturers generally. This is because rare earths are a key raw material for the production of smartphones, various chips, and other high-value-added products that are the biggest cash cows of US companies such as Apple and Boeing.

President Donald Trump during a meeting with Chinese Vice Premier Liu He over trade talks in the Oval Office, February 22, 2019

Reuters, an agency one could hardly accuse of sympathising with Beijing, reports: “The United States has again decided not to impose tariffs on rare earths and other critical minerals from China, underscoring its reliance on the Asian nation for a group of materials used in everything from consumer electronics to military equipment.”

China does not exactly have a monopoly on such materials, but the market would definitely be in short supply without Chinese exports, with all the price implications that would bring. Moreover, it is likely that some deficit positions will be impossible to close no matter how much money is involved.

Not everything is that simple, however. Should such a ban be introduced, then Beijing will encounter certain technical difficulties. If sanctions are only imposed on US companies, then they will still be able to purchase the necessary materials through Japanese or European straw buyers, making the embargo pointless. But if China imposes a total export ban, then it won’t just be US companies that suffer but European ones as well, leading to EU reprisals against Chinese exporters to Europe. This would be very painful for China, especially given the economic war with the US that is making access to European markets invaluable to the Chinese economy.

It appears that a ban on rare earth exports is a powerful weapon, but its use will require the utmost delicacy and serious diplomatic efforts to avoid any extremely unpleasant side effects.

The second trump card mentioned by the Global Times is blocking US companies’ access to the fast-growing and extensive Chinese market. This should be looked at from a political, rather than economic, point of view (although the latter may seem logical). The aim of such restrictive measures is not to inflict unacceptable damage on the US economy, but to make the full might of America’s corporate lobbying machine work against Donald Trump and support his political opponents.

According to the S&P Dow Jones Indices, Asia only accounts for around 14 per cent of the sales of S&P 500 companies. If we assume that China makes up the majority of this, then not even a complete closure of the Chinese markets would be a disaster. There are a few important details, however.

- First, China is the only (and final) market for sales growth for many US companies. So if China closes, the graphs at business presentations won’t be showing any kind of growth.

- Second, China plays a key role in many production chains that end with sales in the US and other markets. A loss of access to Chinese production would therefore severely damage the competitiveness of American companies on the world (and even on the US) market, especially if their European and Japanese competitors retain complete access to China’s production facilities.

As a result, the profits of US companies and the future of the American stock market (which is a key political barometer given that many Americans have invested their savings in shares) would be at risk. It might be possible to offset these problems by transferring production to other Asian countries with cheap labour and favourable terms, but this couldn’t be done quickly and it would be risky, given that Trump is waging trade wars with everyone from the European Union to loyal US allies such as Japan and India. In light of this, US companies will have a huge incentive to prevent Trump from being elected for a second term, and the lobbying and political capabilities of that part of the US corporate sector that will suffer the most from this trump card could really play a key role in the political victory of Trump’s opponents.

The third trump card involves China dumping its portfolio of US Treasury bonds. The Global Times writes: “China holds more than $1 trillion of US Treasury bonds. China made a great contribution to stabilizing the US economy by buying US debt during the financial crisis in 2008. The US would be miserable if China hits it when it is down.” One can conclude from this that Beijing will most probably save dumping its portfolio of US treasury bonds for dessert – in that it will have the biggest impact when the US stock market is experiencing its next crisis.

China’s Vice Premier Liu He (left) speaks during a meeting with President Donald Trump (right) in the Oval Office of the White House on February 22, 2019

The move is not likely to cause catastrophic damage in and of itself (although the value of US bonds will definitely fall), but if it is done at the moment when America is most vulnerable, then China’s portfolio may well end up being the straw that breaks the camel’s back.

Beijing is not displaying a particularly cocksure attitude. As the Global Times’ editor-in-chief quite rightly notes on Twitter:

“Most Chinese agree that the US is more powerful than China and Washington holds initiative in the trade war. But we just don’t want to cave in and we believe there is no way the US can crush China. We are willing to bear some pain to give the US a lesson.”

As China lays its trump cards on the table, the world’s globalised economy will creak and collapse. Globalisation is going backwards, and chances are we’ll end up with a completely different economic system that has more protectionism. Instead of a global market, there will be several large regional markets with their own rules, dominant currencies, technical standards, and financial systems.

Huawei Asks US Court To Declare ‘National Security’ Ban Unconstitutional

It’s a testament to the American legal system that even companies like Huawei, which built an empire on stolen technologyand shady anti-competitive practices, have a right to seek redress of grievances in US courts.

Song Liuping

The Chinese telecoms firm on Wednesday filed a motion in a Texas court seeking a summary judgment on the constitutionality of the Trump Administration’s decision to prohibit US companies and government agencies from using Huawei equipment due to ‘national security’ concerns. The motion is the latest development in a lawsuit that Huawei first filed back in March challenging Section 889 of the National Defence Authorisation Act (NDAA) – signed into law back in August – which barred federal agencies and their contractors from buying Huawei equipment.

That prohibition has since been expanded by executive order to cover most American companies.

The lawsuit was filed in the US District Court for the Eastern District of Texas, which covers the headquarters of Huawei’s American subsidiary in Plano, according to the Australian Broadcasting Corporation.

Huawei’s chief legal officer Song Liuping argued that the “state sanctioned” campaign wouldn’t improve national security, and accused the White House of using “the strength of an entire nation” to “come after a private company.”

“That is not normal,” he added.

Trump’s executive order invoked the Emergency Economic Powers Act, which grants the president the authority to regulate commerce in response to perceived national security threats. Trump administration officials have insisted the order is “company and country agnostic.”

The legal challenge is Huawei’s “last line of defense for justice,” Song said, adding that the security objections were a “ruse” designed to “gain support for other goals” – presumably a reference to the Trump Administration’s trade war with China.

“We believe that US politicians are using cybersecurity as an excuse to gain public support for actions that are designed to achieve other goals,” he said. “These actions will do nothing to make networks more secure.”

On Wednesday, the FT reported – citing unnamed senior Huawei officials – that Washington’s decision to blacklist Huawei will impact roughly 1,200 American suppliers, including chipmakers and software companies, including companies that – ironically enough – produce cybersecurity software, once the ban takes effect in August.

The decision is a ‘distraction’, he added, even as the company has so far failed to provide any evidence contradicting claims that it’s a security threat.

“They provide a false sense of security and distract attention from the real challenges we face.”

“There is no gun, no smoke – only speculation,” he said.

A hearing on Huawei’s motion won’t be held until September.

end

China presses the panic button with huge liquidity as interbank funding freezes up after the Baoshang seizure

(courtesy zerohedge)

PBOC Panics, Floods Market With Liquidity As Interbank Funding Freezes After Baoshang Seizure

With China’s bond market continues to be hammered in the aftermath of the government’s surprise seizure of Baoshang Bank (see “A Big Wake Up Call”: Chinese Bond Market Roiled By First Ever Bank Failure“), the PBOC – whose open market operations had been in dormancy for much of 2019 – finally panicked and on Wednesday injected a whopping net 250 billion yuan ($36 billion) into the financial system via open-market operations, as it fills what traders have dubbed a growing funding gap following the Baoshang failure.

The consequences of this liquidity flood were instant: China’s overnight repurchase rate, a measure of interbank liquidity, tumbled the most in three weeks, while the benchmark 7-day repo rate also declined.

“The operations so far this week send a strong signal that the PBOC is ready to ensure ample liquidity for the market, amid fragile sentiment in the credit and bond market,” said Westpac strategist Frances Cheung. The central bank also set the daily yuan fixing at a stronger-than-expected level to prevent even a hint of speculation that China will be have no choice but to devalue the yuan as part of the “reliquification” of the market.

The PBOC’s massive liquidity injection, which was the largest since January when the S&P was still close to a bear market and started the tremendous Chinese stock market rally, also helped the Shanghai Composite be one of the few markets that closed in the green overnight.

However, while the near-term reaction was favorable to Chinese risk, the paradox is that this only became a viable option as a result of a far greater problem: China’s interbank funding market is starting to freeze.

As we reported on Tuesday, the bank has – or rather had – more than 60 billion yuan of negotiable certificates of deposit (NCDs) and 6.5 billion yuan of subordinated bonds outstanding. Trading in the the company’s NCDs and other bonds was promptly suspended on Monday, with traders fearing that a self-fulfillling prophecy would emerge as contagion spreads to other troubled banks’ NCDs and/or bonds.

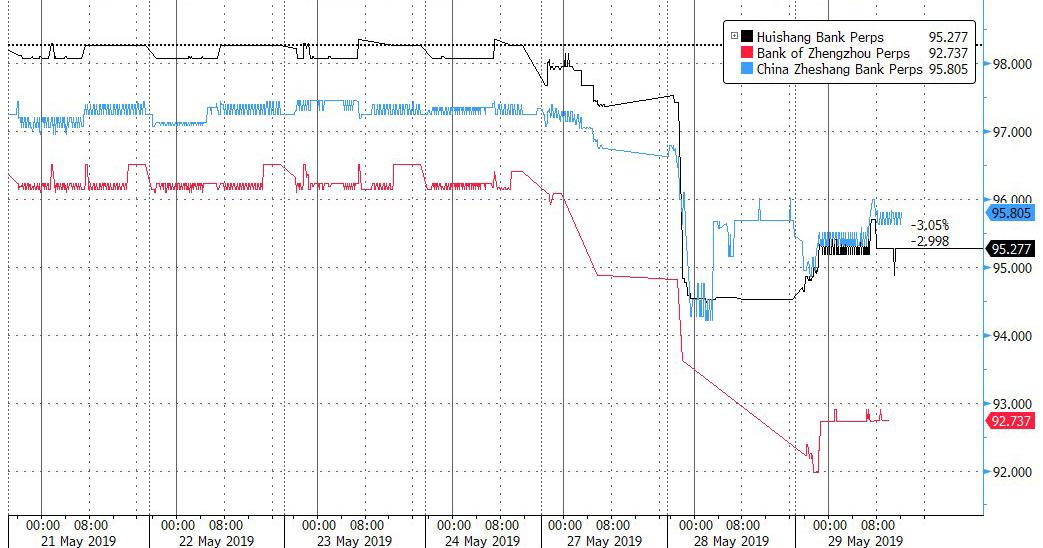

As noted previously, the contingent convertible/perpetual debt issued by some of the more troubled banks such as Huishang, Bank of Zhengzhou and China Zheshang Bank, was hammered over the past three days and has yet to recover.

As an aside, for those asking why NCD’s matter, the answer is because as we explained as far back as two years ago, numerous smaller banks had become acutely reliant on such shadow banking funding mechanisms as Certificates of Deposit, which had become the primary source of short-term funding for many of China’s banks mid-size and smaller banks.

As Deutsche Bank further explained, the banks most exposed to a shut down in this “shadow funding” pathway are medium-sized and small banks, for whom wholesale funding made up 31% and 23%, a number that has risen substantially in the interim period.

The issue of NCD funding is especially troublesome, because as Bloomberg reported overnight, in the aftermath of the Baoshang seizure, some Chinese banks and securities firms “tightened requirements for negotiable certificates of deposits that are used as collateral for funding.” In some cases, private NCDs were shunned altogether, and some financial institutions now only accept NCDs sold by state-owned and joint stock banks as collateral while some have refused to lend money to investors pledging NCDs issued by lenders rated AA+ and below for now.

While the lock up in the NCD market is concerning, it is only partial so far, even as yields on Chinese banks’ NCDs spiked in the past 48 hours after only 44% of the planned amount was issued. Putting this in context, banks typically issue an average of 82% of the planned amount.

“The Baoshang incident is pressuring short-term liquidity,” said a trader at a Chinese bank. “Along with month-end seasonal factors, cash conditions are becoming tighter and pushing up the near-date swap points higher. And that has led the swap curve moving upward.”

Ji Tianhe, China rates and FX strategist at BNP Paribas in Beijing, said that the takeover of Baoshang could be interpreted as a “marginal targeted deleveraging” campaign, and could change the ecosystem of the interbank market.