GOLD: $1333.50 UP $7.50 (COMEX TO COMEX CLOSING)

Silver: $14.80 UP 4 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1333.20

silver: $14.78

YOUR DATA…

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 25/58

EXCHANGE: COMEX

CONTRACT: JUNE 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,326.400000000 USD

INTENT DATE: 06/11/2019 DELIVERY DATE: 06/13/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 H HSBC 7

657 C MORGAN STANLEY 2

661 C JP MORGAN 1 25

686 C INTL FCSTONE 20 3

737 C ADVANTAGE 18 13

800 C MAREX SPEC 19 8

____________________________________________________________________________________________

TOTAL: 58 58

MONTH TO DATE: 1,517

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 58 NOTICE(S) FOR 5800 OZ (0.1804 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1517 NOTICES FOR 151700 OZ (4.718 TONNES)

SILVER

FOR JUNE

0 NOTICE(S) FILED TODAY FOR NIL OZ/

total number of notices filed so far this month: 310 for 1550,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 7951 UP 69

Bitcoin: FINAL EVENING TRADE: $ 8089 UP 207

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE A HUGE SIZED 4427 CONTRACTS FROM 222,086 UP TO 226,513 WITH THE 10 CENT GAIN IN SILVER PRICING AT THE COMEX.( LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR SILVER AND IT STOPPED FOR GOLD AS WELL. WE WILL WITNESS A RISE IN THE SPREADERS IN SILVER ONCE WE START TRADING IN JUNE… READY FOR THE FIRST DAY NOTICE JULY CONTRACT.) TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A VERY HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JUNE, 1002 FOR JULY. 120 FOR AUGUST, 0 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1122 CONTRACTS. WITH THE TRANSFER OF 1517 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1122 EFP CONTRACTS TRANSLATES INTO 5.610 MILLION OZ ACCOMPANYING:

1.THE 10 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

1.560 MILLION OZ STANDING FOR SILVER IN JUNE//

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

25,583 CONTRACTS (FOR 8 TRADING DAYS TOTAL 25,583 CONTRACTS) OR 127.91 MILLION OZ: (AVERAGE PER DAY: 3198 CONTRACTS OR 15.99 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JUNE: 127.91 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 18.27% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 998.67 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4427 WITH THE 10 CENT FALL IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A LARGE SIZED EFP ISSUANCE OF 1122 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS WILL RESUME THEIR LIQUIDATION OF THE SPREAD TRADES FOR SILVER ONCE THE JUNE CONTRACT COMMENCES IN EARNEST….

TODAY WE GAINED A STRONG SIZED: 5549 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1122 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 4427 OI COMEX CONTRACTS. AND ALL OF THIS HUGE DEMAND HAPPENED WITH A 10 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $14.76 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.082 BILLION OZ TO BE EXACT or 152% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 1.560 MILLION OZ//

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

WITH RESPECT TO SPREADING: WE N DOUBT HAD VERY STRONG ACTIVITY OF SPREADING ACCUMULATION IN SILVER TODAY AS TOTAL OI ROSE SHARPLY WITH THE SMALLISH GAIN OF 10 CENTS.

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JUNE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE OPEN INTEREST FELL BY 2564 CONTRACTS, TO 496,663 DESPITE THE $1.65 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING LIQUIDATION HAS STOPPED AND THESE SPREADING FELLOWS HAVE ALREADY MORPHED INTO SILVER.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7042 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 7042 CONTRACTS, DEC> 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 496,663. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN GOOD SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4478 CONTRACTS: 2564 CONTRACTS DECREASED AT THE COMEX AND 7042 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 4478 CONTRACTS OR 447,800 OZ OR 13.93 TONNES. YESTERDAY WE HAD A GAIN OF $1.65 IN GOLD TRADING.…AND WITH THAT GAIN IN PRICE, WE HAD A GOOD GAIN IN GOLD TONNAGE OF 13.93 TONNES!!!!!! THE BANKERS WERE SUPPLYING COPIOUS SUPPLIES OF SHORT GOLD COMEX PAPER.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 91,577 CONTRACTS OR 9,157,700 OR 284.84 TONNES (8 TRADING DAYS AND THUS AVERAGING: 11,447 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAYS IN TONNES: 284.84 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 284.84/3550 x 100% TONNES =8.02% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2,562.74 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A SMALL SIZED DECREASE IN OI AT THE COMEX OF 2564 DESPITE THE PRICING GAIN THAT GOLD UNDERTOOK ON YESTERDAY($1.65)) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7042 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7042 EFP CONTRACTS ISSUED, WE HAD AN GOOD SIZED GAIN OF 4478 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7042 CONTRACTS MOVE TO LONDON AND 2564 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 13.93 TONNES). ..AND THIS INCREASE OF DEMAND OCCURRED WITH THE GAIN IN PRICE OF $1.65 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAD ZERO PRESENCE OF SPREADING ACCUMULATION IN GOLD ///TODAY/

we had: 58 notice(s) filed upon for 5,800 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $7.50 TODAY//

NO CHANGES IN THE GLD INVENTORY TONIGHT

INVENTORY RESTS AT 756.18 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 4 CENTS TODAY:

A HUGE CHANGE WITH RESPECT TO SILVER INVENTORY AT THE SILVER SLV: A DEPOSIT OF 1.413 MILLION OZ INTO THE SLV INVENTORY

/INVENTORY RESTS AT 316.775 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A HUGE SIZED 4427 CONTRACTS from 222,086 UP TO 226,513 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JUNE 0 CONTRACTS AND JULY: 1002 CONTRACTS FOR AUGUST: 120, FOR SEPT. 0 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1122 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 4715 CONTRACTS TO THE 1122 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A VERY STRONG GAIN OF 5549 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 27.755MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY AND NOW 1.570 MILLION OZ FOR JUNE.

RESULT: A HUGE SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 10 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A GOOD SIZED 1122 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN UP 16.34 POINTS OR 0.56% //Hang Sang CLOSED DOWN 480.58 POINTS OR 1.73% /The Nikkei closed DOWN 74.56 POINTS OR 0.35%//Australia’s all ordinaires CLOSED UP 0.04%

/Chinese yuan (ONSHORE) closed DOWN at 6.9195 /Oil UP TO 53.76 dollars per barrel for WTI and 62/33 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9195 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9298 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

Simon Black gives us a good look at Japan and what may go wrong in their country shortly

( Simon Black)

3 China/Chinese affairs

i)China/USA/Japan

Are we to have any Plaza Accord ii..Goldman Sachs gives 3 reasons why this will not happen

( zerohedge/Goldman Sachs//

ii)Many commentators are stating that the uSA-China trade war damage is irreversible by interrupting supply chains

(courtesy zerohedge)

iii)HONG KONG

Violent protests in Hong Kong on Mainland China’s extradition bill. There is no way that Hong Kong citizens would want to be tried in a Mainland court

just look at the angry crowds:

( zerohedge)

iv)China is not doing so good especially internally in the country. They just posted their worst auto monthly sales ever

( zerohedge)

4/EUROPEAN AFFAIRS

i) UK/

With Boris Johnson the supposed front runner and a hard Brexiteer, the EU has now found a way to deal with the Irish backstop problem and that is using technology. The EU are such crooks

(Mish Shedlock/Mishtalk)

ii)Bill blain discusses what he sees today with respect to England, the EU and China\\your morning porridge…

( Bill Blain)

iii)The fun begins: UK Parliament rejects a move to block a no deal Brexit. Our feelings on the matter is that the UK will do much better with a no deal brexit

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)TURKEY

TURKEY keeps its benchmark interest rate at 24% even though many expected them to lower its rate to stimulate Turkey’s moribund economy. This caused a slight rise in the Lira but it also dampens economic activity.

(courtesy zerohedge)

6. GLOBAL ISSUES

AUSTRALIA

Australia does good business with China and it see this nation in a recession speaks volume for world trade

(courtesy zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

Let us all stand up and cheer Venezuela for inflation has finally dropped below 1 million percent

(courtesy zerohedge

9. PHYSICAL MARKETS

b)We have pointed out to you on several occasions Trump’s displeasure at the high Fed interest rate and the higher value of the uSA dollar. He points out that the Europeans have a distinct advantage over the USA. Talking down the dollar may soon get a lot easier for Trump(Watts/.Market Watch/GATA)

c)James Rickards discusses the true value for gold.

( James Rickards)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

a)Market trading/LAST NIGHT/

II)MARKET TRADING

ii)Market data

iii)USA ECONOMIC/GENERAL STORIES

a)Graham Summers in simple language explains how the bond market blew up in December and why Mnuchin called an emergency meeting. The bond market is still broken and they must lower the rates at least 3 or 4 times during this year. Let us see what they are going to do

(courtesy GRAHAM SUMMERS)

b)The Fed is not happy with this: consumer inflation s slowing down badly in May and it has the weakest core inflation since Feb 2017

(courtesy zerohedge)

c)With the uSA engaging in a trade war one would think that their deficit would shrink. Guess again, it rose to an all time record 208 billion dollars. For 8 months of the year: 739 billion dollars. They are heading for a deficit of 1 trillion dollars and that does not include auto loans and student loans which are off balance sheet because they are an asset and a loan. The true deficit is north of 1.2 trillion dollars

SWAMP STORIES

a)A superb piece from Victor Davis Hansen on the evolution of the Trump collusion case

(courtesy Victor Davis Hansen)

Let us head over to the comex:

Gold withdrawals;

i) We had 0 withdrawal:

.

Gold Prices Move Higher Again As US-China Trade War Sees Stocks Fall

GoldCore Note

Gold prices have moved higher today after hitting a one-week low yesterday. Renewed worries over the U.S.-China trade war and its impact on the global economy are pushing gold higher.

Stocks globally have fallen as risk aversion creeps back in as the trade war escalates, increasing the appeal of gold bullion as a hedge and safe haven.

Spot gold was up 0.8% at $1,337.10 by mid morning (GMT), after falling to its weekly low at $1,319.35 in the previous session.

Stock markets moved lower as the warring factions in the China U.S. trade tussle engaged in another round of very heated exchanges. A new front in the deepening tensions between the superpowers is the new tech cold war and this does not bode well for an amicable resolution.

LBMA Gold Prices (USD, GBP & EUR – AM/ PM Fix)

11-Jun-19 1322.65 1324.30, 1040.53 1041.30 & 1168.96 1170.42

10-Jun-19 1328.60 1328.60, 1046.94 1048.66 & 1175.41 1175.94

07-Jun-19 1334.30 1340.65, 1049.16 1052.14 & 1184.19 1184.60

06-Jun-19 1336.65 1335.50, 1053.15 1051.17 & 1189.62 1185.92

05-Jun-19 1337.75 1335.05, 1052.01 1049.22 & 1185.38 1184.99

04-Jun-19 1323.60 1324.25, 1045.51 1043.77 & 1177.47 1177.26

03-Jun-19 1313.95 1317.10, 1039.47 1042.35 & 1175.99 1175.38

30-May-19 1276.45 1280.95, 1010.44 1015.92 & 1146.25 1151.70

News

Gold recovers as US-China trade jitters sour risk appetite

Gold finishes higher as U.S. stock market weakens

Equities fall with yields as trade optimism fades

Russian banks mull exporting more gold on new broader policy

China Extends Hand to India to Fend Off US Trade ‘Bullying’

Commentary

Why Trump’s Tweets about the Dollar Might Soon Pack a Lot More Punch

China’s loans to other countries are causing ‘hidden’ debt. That may be a problem

ECB’s Rehn: Rates cut, more QE all on the table

Gold is always shiny but US dollar is a ‘hyperinflated bubble’ ready to pop

Put Your Trust in Gold – Frank Holmes

end

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

Indian Gold Demand Surged In April And May

After a dip in demand in 2018, it appears Indians are buying gold again.

Anecdotal data seemed to indicate strong demand for the yellow metal in India during the Akshaya Tritiya holiday. Retailers reported sales were up by as much as 25%. As it turns out, demand was indeed strong. Gold imports into India were up 36% year-over-year in May, according to sources cited by Bloomberg.

India imported 105.8 tons of gold in May. That compares with just 77.6 tons a year earlier. Combined shipments of gold into the country during April and May came in at 226.6 tons. That was up about 74% from the same period in 2018.

According to Yahoo Finance, “Higher gold imports by India – the world’s second-biggest consumer of the yellow metal – could support global prices further.”

Gold imports into India dipped by about a fifth in 2018, primarily due to a weak rupee and high domestic gold prices.

“Sales were amazing last month, with huge demand seen during Akshaya Tritiya. The drop in prices has really complemented that trend,” said G.V. Sreedhar, managing director of Sree Rama Jewels and a former chairman of the All India Gem & Jewellery Domestic Council. Purchases for weddings were also good when compared to last year and sales are expected to be robust this month as well, he said.

Analysts say dynamics are in place to support continued strong demand through the end of the year. Gold-buying usually picks up in India in the last half of the year with wedding season and harvest time. Forecasters expect a normal monsoon season this year. A good monsoon season is good news for Indian farmers, as well as for the broader Indian economy. And when rural Indians have money in their pockets, they buy gold.

India ranks as second in the world in gold consumption behind China. According to Yahoo Finance, combined demand for gold from India and China has soared 71% in the last decade. A rising middle class and broad economic growth in both countries have spurred investment in the yellow metal.

Indians traditionally buy and hold gold. The yellow metal is interwoven into the country’s marriage ceremonies and cultural rites. Indians also value gold as a store of wealth, especially in poor rural regions. Two-thirds of India’s gold demand comes from these areas, where the vast majority of people live outside the official tax system.

Gold is not just a luxury in India. Even poor people buy gold in the Asian nation. According to an ICE 360 survey last year, one in every two households in India purchased gold within the last five years. Overall, 87% of households in the country own some amount of the yellow metal. Even households at the lowest income levels in India own some gold. According to the survey, more than 75% of families in the bottom 10% had managed to buy gold.

While owning precious metals is part of India’s culture, the fundamental reasons Indians buy gold and silver are no different than those that motivate people over the world to invest in precious metals – they historically preserve wealth, they provide a safe haven, and most significantly, they are real money.

END

James Rickards discusses the true value for gold.

(courtesy James Rickards)

If Gold Was Just A Barbarous Relic…

Authored by James Rickards via The Daily Reckoning,

There’s nothing new about the Russian accumulation of gold bullion in their reserve position. It began in a material way in 2009 when Russia had about 600 metric tonnes of gold.

Today, Russia has 2,183 metric tonnes, a stunning 264% increase in less than 10 years. Russia is the sixth-largest gold power in the world after the U.S., Germany, IMF, Italy and France.

Russia’s gold hoard is over 25% of the U.S. hoard, but Russia’s economy is only 8% the size of the U.S. economy. This gives Russia a gold-to-GDP ratio over three times that of the U.S.

While these developments are well-known, the question of why Russia is accumulating so much gold has never been answered.

One reason is as a dollar hedge. Russia is the second-largest energy producer in the world. Most of that energy is sold for dollars. Russia can hedge potential dollar inflation by buying gold.

Another reason has to do with the avoidance of U.S. sanctions. Gold is nondigital and does not move through electronic payments systems, so it is impossible for the U.S. to freeze on interdict.

Yet a deeper reason is that Russia has a long-term plan to subvert the dollar’s role as the leading global reserve currency. The Russian ruble is not positioned to be a reserve currency, but a new cryptocurrency backed by gold would be a good candidate.

The Central Bank of Russia will consider a new study that suggests just such a gold-backed cryptocurrency to settle balance of payments among willing participants. This plan is in its preliminary stages and is a long way from reality at this point.

Still, the Russian endgame has now been revealed. The dollar’s days as the leading reserve currency are numbered.

Of course, Russia is not the only nation accumulating gold as a means to move away from the dollar. You can certainly add China to that list, and many others.

The latest move comes from Malaysian Prime Minister Mahathir Mohamad. He promoted the idea of a common trading currency for East Asia that would be pegged to gold.

“The currency that we propose should be based on gold because gold is much more stable,” he said.

I’ve actually advised Mahathir Mohamad in the past and he’s very familiar with my writings on gold. So I’m not surprised he’s issuing this call.

The global monetary regime has collapsed three times over the past 100 years, in 1914, 1939, and 1971. They seem to happen about every 30 to 40 years on average. It’s now been over 40 years since the last collapse, so we’re due.

Below, I show you why gold is heading for a powerful breakout. And yes, it involves the world’s central banks…

I read headlines all day and focus extensively, if not exclusively, on gold. If gold is the best form of money (it is), and if gold had unique properties as money (it does; it’s the only form of money that is not also debt), then gold is well worth the focus.

With that said, it’s hard to surprise me on the subject. After a while, you think you’ve seen it all. Yet, there are exceptions. This headline stopped me in my tracks: “Bank of Russia may consider gold-backed cryptocurrency.”

The idea itself is not exactly new. I first suggested that Russia might be acquiring gold with a view to a new gold-backed currency at a financial war game hosted by the Pentagon at a top-secret laboratory in 2009.

In my upcoming book, Aftermath, I describe a more sophisticated monetary arrangement among Russia, China, Iran and other nations to use a gold-backed cryptocurrency for international settlements.

Still, theory is one thing, reality is another. Here was a real central bank taking real steps toward a gold-backed cryptocurrency. Of course, the announcement came with lots of caveats about the need to stick to hard currencies. This gold initiative involves review of a report, not a live plan at this stage.

Still, it was a significant moment in the move away from the hegemony of the U.S. dollar as the dominant global reserve currency toward another system that included gold.

By itself, this announcement is not a reason to load up on gold. In fact, the spot price of gold barely budged on the news. Gold prices are far more likely to be affected by strength or weakness of the U.S. dollar, real interest rates, inflation prospects and geopolitical stress.

But, the announcement is highly significant in another way. It signals that the demand for physical gold by major central banks is here to stay. Whether a new gold-backed cryptocurrency emerges next year or five years from now does not alter the fact that you need gold to have a gold-backed currency.

Neither Russia nor China has all the gold it needs for that purpose yet. Therefore, demand for physical gold will remain strong even as supply has flatlined.

This creates an asymmetric trading pattern where gold has good potential to rise, but only limited prospects of a material fall. Those are the best kinds of markets for trading and investment. Taking into account both these fundamental and technical factors, what is the outlook for the dollar price of gold and gold mining stocks in the near term?

Right now, the evidence is telling us that the dollar price of gold is poised to breakout to the upside after a prolonged period of range-bound trading.

Chart 1 above illustrates recent price action in gold and shows why the prospects are good for near-term price appreciation.

After a rally from $1,215 per ounce in late November 2018 to $1,293 per ounce in early January 2019, gold remained in a tight trading range.

Over the past five months, gold has traded between about $1,270 and $1,345 per ounce (as of yesterday after gold’s big run over the past week).

That’s a range of about 2.8% above and below a mid-point of $1,305 per ounce. A 2.8% range is not unusual when governments try to peg two currencies to each other. In effect, gold has been pegged to the dollar at $1,305 per ounce.

However, this trading range exhibits another pattern called “lower highs.” Each spike at the high end of the range is slightly lower than the one before. Conversely, the bottom in each gyration has been more tightly bunched forming a kind of floor under gold prices.

The combination of a strong floor and declining highs results in a compression of the trading range. What this pattern presages is a breakout. Of course, the question is whether gold will breakout to the downside or the upside. This week we saw gold break higher, to $1,345.

The evidence is strong that gold is poised for a sustained upside breakout. The reason for the floor around $1,270 per ounce has to do with fundamental supply and demand. Russia and China continue to buy gold at a prodigious rate.

Russia has been buying between 15 and 25 metric tonnes per month, sometimes more, for over ten years. Russia’s gold reserves now stand at 2,183 metric tonnes, over 25% of the U.S. total with a far smaller economy. China is less transparent in its gold buying but also has over 2,000 metric tonnes, perhaps much more.

Neither Russia nor China have their targeted amount of gold yet, which would be 4,000 metric tonnes for Russia and 8,000 metric tonnes for China to achieve strategic gold parity with the U.S.

Iran and Turkey have also embarked on major gold accumulation efforts.

What all of these gold buying strategies have in common is a desire to escape from dollar hegemony and the imposition of dollar-based sanctions by the U.S. The practical implication for gold investors is a firm floor under gold prices since Russia and China can be relied upon to buy any dips.

The primary factor that has been keeping a lid on gold prices is the strong dollar. The dollar itself has been propped up by the Fed’s policy of raising interest rates and reducing money supply, so-called “quantitative tightening” or QT. These tight money policies have amplified disinflationary trends and pushed the Fed further away from its 2% inflation goal.

However, the Fed reversed course on rate hikes last December and has announced it will end QT next September. These actions will make gold more attractive to dollar investors and lead to a dollar devaluation when measured in gold.

The price of gold in euros, yen and yuan could go even higher since the ECB, Bank of Japan and People’s Bank of China will still be trying to devalue against the dollar as part of the ongoing currency wars. The only way all major currencies can devalue at the same time is against gold, since they cannot simultaneously devalue against each other.

A situation in which there is a solid floor on the dollar price of gold and a need to devalue the dollar means only one thing – higher dollar prices for gold. A breakout to the upside is the next move for gold.

END

We have pointed out to you on several occasions Trump’s displeasure at the high Fed interest rate and the higher value of the uSA dollar. He points out that the Europeans have a distinct advantage over the USA. Talking down the dollar may soon get a lot easier for Trump

(Watts/.Market Watch/GATA)

Could JPMorgan Chase Be Hit with a Fourth Felony Count for Rigging Precious Metals Markets?

By Pam Martens and Russ Martens: June 11, 2019 ~

The CFTC is a Federal regulator that oversees the U.S. commodities markets. The U.S. Department of Justice (DOJ) is also a Federal agency and the only one that can bring a criminal case against firms and individuals who commit conspiracy and fraud in commodity and securities markets. (The Securities and Exchange Commission can bring only civil, not criminal, cases.)

On September 25, 2013, after spending five years and 7,000 hours using taxpayers’ money investigating the potential rigging of the silver market, the Commodity Futures Trading Commission (CFTC) concluded that “there is not a viable basis to bring an enforcement action with respect to any firm or its employees related to our investigation of silver markets.” The investigation was provoked by multiple complaints asserting the market was rigged.

On October 9 of last year, the DOJ used its criminal powers and charged John Edmonds, a former long-time employee of JPMorgan Chase, with one count of commodities fraud and one count of conspiracy to commit wire fraud, commodities fraud, commodities price manipulation and spoofing.

The charges covered the period in which the CFTC had found no “viable basis to bring an enforcement action” for silver market manipulation.

Edmonds has pleaded guilty to the charges and admitted that “from approximately 2009 through 2015, he conspired with other precious metals traders at the Bank to manipulate the markets for gold, silver, platinum and palladium futures contracts traded on the New York Mercantile Exchange Inc. (NYMEX) and Commodity Exchange Inc. (COMEX)….”

In one specific example involving the silver market, Edmonds admitted to the following:

“As one example of this deceptive trading strategy, on or about October 12, 2012, at approximately 1:08:48.831 p.m. (Central Daylight Time), the defendant placed an order to sell 402 silver futures contracts at the per-contract price of $33.610 with the intent to cancel the order before execution. The purpose of this Spoof Order was to induce other market participants to trade against the defendant’s opposite side order to buy silver futures contracts, which order the defendant did want to execute. The defendant’s Spoof Order did, in fact, cause other market participants to react and trade at prices, quantities, and times that they otherwise would not have traded, but for the defendant’s Spoof Order, including a precious metals trader in Connecticut who sold a single silver futures contract at 1:08:48.837 p.m. at the price of $33.585.”

The CFTC’s fruitless 5-year investigation is all the more embarrassing because Edmonds was not some lone, rogue trader inside an otherwise pristine Wall Street bank. JPMorgan’s reputation is so soiled for rigging everything from electric markets to foreign exchange to wearing a self-imposed blindfold while Bernie Madoff carried out his decades-long Ponzi scheme that two trail attorneys have written a book comparing the bank to the Gambino crime family. (The reality is that it would take a 7,000-hour study just to chronicle this bank’s serial crimes. See our partial rap sheet here.)

Far from being a lone, rogue trader, Edmonds has now implicated other traders and supervisors within JPMorgan Chase. His plea agreement indicates the following:

“…the defendant and his fellow traders routinely placed bids and offers-in other words, orders-for precious metals futures contracts with the intent to cancel those bids and offers before execution (the ‘Spoof Orders’). This trading strategy was intended to, and did, transmit materially false and misleading liquidity and price information and otherwise deceive other market participants about the existence of supply and demand for the futures contracts at issue, and thus induce those other market participants to trade against orders that the defendant and his co-conspirators placed and did want to execute on the opposite side of the market from the Spoof Orders at prices, quantities, and times that the other market participants otherwise would not have traded. The Spoof Orders thus were designed to, and did, artificially move the price of precious metals futures contracts in a direction that was favorable to the defendant and his co-conspirators at the Bank, to the detriment of other market participants, including other market participants in Connecticut. The defendant placed the Spoof Orders in order to make money and avoid losses for himself, his co-conspirators, and the Bank. The defendant learned this deceptive trading strategy from more senior traders at the Bank, and he personally deployed this strategy hundreds of times with the knowledge and consent of his immediate supervisors.”

Making this case all the more interesting is the fact that JPMorgan Chase is still under probation in its own plea agreement for its role in rigging the foreign exchange market. It entered into that plea agreement on May 20, 2015 but a Federal District court did not approve the deal until 2017. This means that its three-year probation period does not end until January 2020. JPMorgan Chase agreed to one criminal felony count in that matter and agreed to two criminal felony counts in the Madoff matter in 2014.

JPMorgan Chase has acknowledged in its own 10-K filing with the SEC that it remains on probation, writing as follows:

“The Firm previously reported settlements with certain government authorities relating to its foreign exchange (‘FX’) sales and trading activities and controls related to those activities. FX-related investigations and inquiries by government authorities, including competition authorities, are ongoing, and the Firm is cooperating with and working to resolve those matters. In May 2015, the Firm pleaded guilty to a single violation of federal antitrust law. In January 2017, the Firm was sentenced, with judgment entered thereafter and a term of probation ending in January 2020.”

As part of its plea agreement, JPMorgan Chase agreed to “not commit another crime in violation of the federal laws of the United States” during the term of probation. It also agreed to the following:

“The defendant understands that during the term of probation it shall: (1) report to the Antitrust Division all credible information regarding criminal violations of U.S. antitrust laws by the defendant or any of its employees as to which the defendant’s Board of Directors, management (that is, all supervisors within the bank), or legal and compliance personnel are aware; and (2) report to the Criminal Division, Fraud Section all credible information regarding criminal violations of U.S. law concerning fraud, including securities or commodities fraud by the defendant or any of its employees as to which the defendant’s Board of Directors, management (that is, all supervisors within the bank), or legal and compliance personnel are aware.”

JPMorgan Chase has admitted in its February 10-K filing with the SEC that it’s under a criminal investigation by the DOJ relating to the precious metals market, writing that “Various authorities, including the Department of Justice’s Criminal Division, are conducting investigations relating to trading practices in the precious metals markets and related conduct.”

Raising suspicions that this investigation against the bank is serious is the fact that the DOJ has twice postponed the criminal sentencing of Edmonds, suggesting he continues to cooperate in providing evidence in the investigation. Sentencing is now scheduled for December. All motions pertaining to that matter are under seal.

Career prosecutors in the Department of Justice and Federal judges tend to take a dim view of recidivist Wall Street banks. It is also relevant that the same Chairman and CEO, Jamie Dimon, has been allowed by the Board of Directors to remain at the helm of the bank through two probation periods, two deferred prosecution agreements, three criminal felony counts and $36 billion in fines. And, by the way, those three criminal felony counts that occurred under Dimon are three more than the bank received during its prior 100 years of existence.

The case is 3:18-cr-00239-RNC, USA v. Edmonds, and is being conducted in the U.S. District Court for the District of Connecticut.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

end

* * *

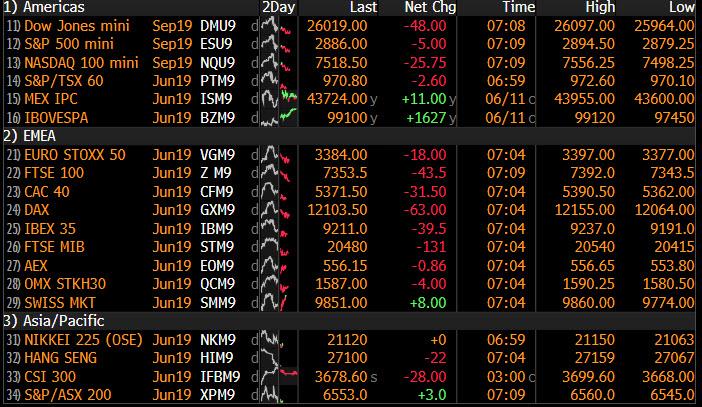

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.9195/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.9298 /shanghai bourse CLOSED DOWN 16.34 POINTS OR 0.56%

HANG SANG CLOSED DOWN 480.58 POINTS OR 1.73%

2. Nikkei closed DOWN 74.56 POINTS OR 0.35%

3. Europe stocks OPENED ALL RED/

USA dollar index UP TO 96.73/Euro FALLS TO 1.1319

3b Japan 10 year bond yield: RISES TO. –.11/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.35/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 51.92 and Brent: 60.91

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.24%/Italian 10 yr bond yield UP to 2.37% /SPAIN 10 YR BOND YIELD DOWN TO 0.57%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.61: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.75

3k Gold at $1335.95 silver at: 14.80 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 19/100 in roubles/dollar) 64.72

3m oil into the 51 dollar handle for WTI and 60 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.35 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9932 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1244 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.24%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.12% early this morning. Thirty year rate at 2.60%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.7918..

Futures Slide As Global Rally Ends 7-Day Streak; Hong Kong Riots, Trade War Eyed

The torrid June rally finally fizzled overnight as stocks slipped around the globe on Wednesday alongside S&P futures, after a six-day rally in the S&P ended yesterday with a whimper amid signs the June revival in risk appetite may have overshot, with trade concerns returning to the fore.

The market mood soured after a protest in Hong Kong turned violent as police were unleashed to contain a “riot”, compounding the negative sentiment, and Treasuries gained. An impending reading on U.S. CPI was set to further cement the Fed’s decision whether to cut rates in June/July.

“I think we are in for a very nervous wait until next week’s FOMC meeting,” Saxo Bank’s head of FX strategy, John Hardy, said.

Europe’s main markets followed Asia by declining early on. London’s FTSE, the DAX in Frankfurt and CAC40 Paris were down 0.2% to 0.4% as traders trimmed some of June’s 4% gains. The Stoxx Europe 600 index headed for its first drop in four sessions.

The rebound in Asia stocks paused on Wednesday as traders stayed cautious amid lingering U.S.-China trade tensions and an escalating protest in Hong Kong. The region’s benchmark declined 0.5% snapping a three-day gain. Hong Kong was the worst-performing market in the region, with the Hang Seng Index falling as much as 2%, after thousands of demonstrators converged on the city’s legislature Wednesday and blocked roads to protest a bill that would for the first time allow extraditions to China.

“The impact was short-lived in the past,” noted Alex Wong, director at Ample Finance Group in Hong Kong. “This time people will look at how the U.S. reacts to this kind of news. The U.S. attitude towards Hong Kong and China are also not the same.”

Japanese stocks halted their three-day advance as electronics makers were the heaviest drags on the index. Trading volume for the nation’s equities dropped almost 20%. Nintendo fell after delaying the release of Animal Crossing: New Horizons. Square Enix Holdings posted its worst two-day slump as investors took profits after the company announced new games at E3. Most of other major Asia markets also declined as the cautious sentiment spreading across the region. China’s Shanghai Composite Index retreated as much as 0.8%, and Jakarta Composite index fell 0.7%.

Then there was the ongoing trade war which has no resolution in sight: President Trump said on Tuesday he was holding up a trade deal with China and had no interest in moving ahead unless Beijing agrees to four or five “major points”, which he did not specify. He said interest rates were “way too high” and the Federal Reserve had “no clue”.

And speaking of the Fed, the FOMC will meet on June 18-19. With trade tensions rising, U.S. growth slowing and hiring in May declining, markets have priced in at least two rate cuts by the end of 2019. Futures imply around an 80% chance of an easing as soon as July. That may change depending on what U.S. consumer price data show later in the session. Headline inflation is expected to slow to 1.9%, with the core rate steady at 2.1%.

In FX, the euro rebounded initially to $1.1336, just short of the recent three-month high of $1.1347, despite Trump’s recent tweet slamming the Euro as “devalued.” The dollar fell against the yen to 108.36 and stalled on a basket of currencies at 96.608.

“The President’s tweets on the USD have the potential to have much more lasting impact in the coming election year,” said Alan Ruskin, global head of G10 FX strategy at Deutsche Bank. “Global conditions are nicely set for what has colorfully been described as a ‘currency war’ or a currency race to ‘the bottom’.”

China’s yuan weakened against the dollar, a day after it climbed the most in two months following the central bank’s moves to shore up the currency. The PBOC set a slightly stronger-than-expected reference rate Wednesday, after showing the largest strong bias in its fix on Tuesday since Bloomberg began releasing fixing forecasts in 2017. The central bank on Wednesday resumed 28-day reverse repurchase agreements for the first time since January, a signal that it seeks to ensure market stability amid seasonal tightness and the aftermath of the Baoshang seizure, according to Qi Sheng, chief fixed-income analyst from Zhongtai Securities Co. In Hong Kong, stocks tumbled and the currency soared in its biggest gain in six months, as interbank interest rates jumped amid protests that closed roads in the city’s financial district.

Benchmark government bond yields fell as caution grew, with the 10Y Treasury down to 2.12%.

In commodities, oil prices dropped over 2% as concern about a global economic slowdown offset expectations that OPEC and its allies will extend their supply curbs. Hedge fund managers have been liquidating bullish oil positions at the fastest rate since late 2018 amid growing economic fears.

Economic data include mortgage applications and CPI, while Lululemon is among companies reporting earning

Market Snapshot

- S&P 500 futures down 0.3% to 2,879.75

- STOXX Europe 600 down 0.5% to 379.06

- MXAP down 0.5% to 156.57

- MXAPJ down 0.6% to 511.71

- Nikkei down 0.4% to 21,129.72

- Topix down 0.5% to 1,554.22

- Hang Seng Index down 1.7% to 27,308.46

- Shanghai Composite down 0.6% to 2,909.38

- Sensex down 0.6% to 39,713.77

- Australia S&P/ASX 200 down 0.04% to 6,543.74

- Kospi down 0.1% to 2,108.75

- German 10Y yield fell 0.2 bps to -0.234%

- Euro up 0.09% to $1.1336

- Brent Futures down 2.2% to $60.94/bbl

- Italian 10Y yield rose 3.4 bps to 2.025%

- Spanish 10Y yield rose 0.4 bps to 0.583%

- Brent Futures down 2.2% to $60.94/bbl

- Gold spot up 0.8% to $1,337.41

- U.S. Dollar Index down 0.05% to 96.63

Top Overnight Highlights from Bloomberg

- The dollar touched an eight-week low before U.S. inflation data that may back the case for Fed interest-rate cuts. The greenback is weaker against all its G-10 peers so far this month as markets have boosted pricing on Fed easing amid concern trade frictions will sap global growth.

- The yen led gains on Wednesday, strengthening for the first time in three days against the dollar

- The euro was little changed after Tuesday’s advance; the common currency was pressured after comments from ECB Governing Council member Francois Villeroy de Galhau who said the central bank could increase stimulus if needed

- European bond markets traded flat ahead of a large supply slate from Germany, Portugal, Italy and Spain; U.S. Treasuries advanced for a second day, the 10-year yield dropped 2bps to 2.12%

- U.S. index futures slipped, the Stoxx Europe 600 index opened lower for the first time in four sessions

Asian equity markets traded mostly subdued after the flat lead from Wall St where the relief rally stalled, and the major indices finished flat to snap a 5 and 6-day win streak for the S&P 500 and DJIA respectively. ASX 200 (U/C) and Nikkei 225 (-0.4%) were mixed with Australia kept afloat by mining names as iron prices in China surged to fresh record highs, while the Japanese benchmark mirrored the indecisiveness of its US peers amid a firmer JPY and with SoftBank among the laggards as a group of US states attempt to block the Sprint and T-Mobile merger. Elsewhere, Hang Seng (-1.7%) and Shanghai Comp. (-0.6%) were negative following another net liquidity drain by the PBoC and pessimism regarding the ability to reach a US-China trade deal at the G20, with underperformance in Hong Kong amid increases in money market rates and mass protests outside government buildings in opposition against the controversial extradition bill. Finally, 10yr JGBs kept rangebound with price action hampered by the indecisiveness in the region and amid a lack of BoJ presence in the market today.

Top Asia News

- Nintendo Moves Some Switch Production Out of China: WSJ

- Indonesia’s Jokowi Open to Gerindra Joining His New Cabinet

- Japan to Propose TPP-Level Tariff Cut on U.S. Farm Goods: Kyodo

- Rumors About China Military Going to HK Are Misinformation: Geng

European equities are mostly lower [Eurostoxx 50 -0.5%] in a continuation of the subdued lead from Asia in which Hong Kong’s stock index suffered heavy losses due to the mass protests against the controversial extradition bill. Sectors are mixed, with heavy underperformance across energy names (sector -1.2%) amid the slide in oil prices. Meanwhile, defensive sectors (utilities +0.3%, healthcare +0.4%) are in the green as investors flock to the ‘safer’ and more stable stocks. In terms of individual movers, shares in British American Tobacco (-6.0%) fell to the foot of the Stoxx 600 index as the cigarette maker expects global industry volume to fall by around 3.5%, although the Co. reiterated guidance despite its peer Imperial Brands (-1.8%) cutting guidance for their tobacco business yesterday. Elsewhere, shares in Axel Springer (+11.8%) rocketed after KKR’s Traviata confirmed that it is to make a takeover offer for the company for EUR 63/shr (vs. yesterday’s close at EUR 55.85/shr). Meanwhile, SMI’s LafargeHolcim (-3.1%) fell to the bottom of the index after a major shareholder cut his stake in the company.

Top European News

- Brexit Britain Contemplates Another Foreign Central Bank Boss

- Reckitt Benckiser Names Laxman Narasimhan as CEO From Sept. 1

- Britain’s Banking Upstarts Vulnerable to a Downturn, BOE Finds

- Drug to Replace Chemotherapy May Reshape Cancer Care

In FX, the Dollar is on the defensive ahead of US headline inflation data that could provide more justification for the Fed to consider a rate cut, with the index only just holding above chart support ahead of 96.500 in the form of the 200 DMA within a 96.578-722 range.

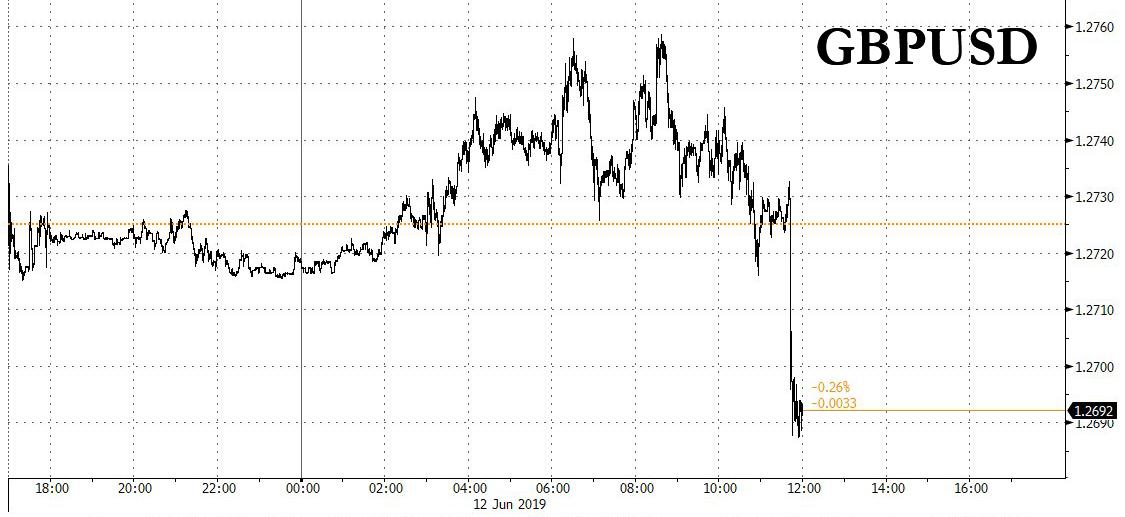

- JPY/GBP/EUR/CHF – All taking advantage of the softer Greenback, as the Yen rebounds towards 108.00 and into decent option expiry territory with 1 bn sitting between 108.40-25 before a further 1.2 bn from 108.10 down to the big figure. Note, Usd/Jpy has also pared gains on a partial retracement in global stocks as improving risk sentiment wanes, but the Franc has not regained as much safe-haven allure given Thursday’s SNB quarterly policy review and the likelihood of more NIRP and intervention iterations – check out the headline feed or Research Suite for a detailed preview. Usd/Chf and Eur/Chf remain above 0.9900 and 1.1200 respectively, with the single currency also consolidating above 1.1300 vs the Dollar and inching closer towards last Friday’s post-NFP highs circa 1.1348 where stops are anticipated, but could be countered by hedges for a 1.2 bn expiry at the 1.1350 strike. Meanwhile, Cable has retested yesterday’s post-UK data/BoE commentary peaks just shy of 1.2750 and Eur/Gbp is pivoting 0.8900 awaiting Tory leadership front-runner BoJo’s official campaign launch.

- NZD/CAD/AUD – Ongoing global trade concerns are undermining the non-US Dollars, as the Kiwi remains capped below 0.6600 and Loonie retreats further from best levels towards 1.3300, and perhaps takes heed of the more pronounced recoil in crude prices having decoupled somewhat in wake of supportive Canadian jobs data and the fillip from the US and Mexico clinching a deal to avert tariffs. However, the Aussie is underperforming in the run up to tomorrow’s labour report and probing key Fib support circa 0.6945.

- EM – Usd/Try is back above 5.8000 amidst latest Turkish remonstrations about the US not adhering to the spirit of alliance on the missile front and reports that an official response to a letter from Washington is being prepared. Meanwhile, the Lira is also looking pressured ahead of the looming CBRT that could turn more dovish given recent inflation data showing a slowdown in CPI, weaker oil and Try appreciation from worst levels – for more see Ransquawk’s headline feed and/or Research Suite.

In commodities, another day of losses for the energy complex with WTI (-2.7%) and Brent (-2.8%) futures heavily pressured amid the latest surprise build in API crude stocks (+4.9mln vs. Exp. -0.5mln) coupled with risk aversion around the market, whilst the EIA’s downgrade in global oil demand forecast only adds to the bearish sentiment. WTI futures currently hover just above the USD 51.50/bbl level, having dipped below its 200 WMA (52.59) whilst its Brent counterpart briefly fell under the USD 60.50/bbl mark. News flow for the complex has been light thus far with participants now gearing up for the weekly DoEs to potentially reinforce the build in stockpiles seen in the APIs. Elsewhere, gold (+0.8%) resumes its climb as the recent relief rally dissipated. The yellow metal is comfortably above the USD 1325/oz level ahead of US CPI data. Turning to base metals, copper prices are sliding despite a weaker Buck amid the absence of risk appetite in the market, although it is worth noting from a supply point of view that Labour unions at Codelco’s Chuquicamata mine are set to reject the latest wage offer in a vote tomorrow, which could see a operations come to a halt at the largest open pit copper mine. Finally, given the recent supply-driven surge in iron ore prices, Chinese steel mills are facing a slump in profit margins and are reportedly seeking lower grade iron ore to cut costs, thus the spread between medium and low grade iron ore in China has narrowed to two-and-half year lows.

US Event Calendar

- 7am: MBA Mortgage Applications +26.8%, prior 1.5%

- 8:30am: US CPI MoM, est. 0.1%, prior 0.3%; CPI YoY, est. 1.9%, prior 2.0%

- CPI Ex Food and Energy MoM, est. 0.2%, prior 0.1%; US CPI Ex Food and Energy YoY, est. 2.1%, prior 2.1%

- Real Avg Hourly Earning YoY, prior 1.2%; Real Avg Weekly Earnings YoY, prior 0.92%

- 2pm: Monthly Budget Statement, est. $199.5b deficit, prior $146.8b deficit

DB’s Jim Reid concludes the overnight wrap

According to the Oxford English Dictionary, today I venture into middle age as I turn 45. In some ways that’s quite a relief as I just assumed I had been there for some time. I’ll find out later if my dreams have been realised and I’ll be getting an eyebrow comb for my birthday (see last week’s EMRs for an explanation) and also what the children will be buying me with my own money. Wikipedia has this entry for middle age which makes me feel great. “The body may slow down and the middle aged might become more sensitive to diet, substance abuse, stress, and rest. Chronic health problems can become an issue along with disability or disease. Approximately one centimeter of height may be lost per decade. Emotional responses and retrospection vary from person to person. Experiencing a sense of mortality, sadness, or loss is common at this age.” To commiserate my wife and I are having our first night out alone this year. Let’s hope my sensitivity to champagne hasn’t suddenly changed overnight.

The market’s champagne was put on ice last night though as a five day party that had looked likely to extend into a sixth session started to fade. Despite opening as much as +0.83% and +1.09% higher, the S&P 500 and NASDAQ both faded throughout the day to end marginally lower at -0.04% and -0.01% respectively. The trade-related rhetoric from the White House continued to be somewhat negative, as President Trump said that “it’s me right now that’s holding up the deal” and suggested that he will not back down unless China makes new concessions. Two of his main lieutenants, Commerce Secretary Ross and Acting Chief of Staff Mulvaney, both separately downplayed the odds of an agreement at this month’s G-20, though they did say that talks could get back on track if Trump and President Xi can make positive progress. Despite the continued uncertainty, some of the most trade-exposed equity sectors performed well yesterday, with autos gaining +0.56% and Apple up +1.16%, as headlines circulated indicating that they are prepared to completely adjust their supply chain to avoid manufacturing iPhones in China for the US market.

President Trump complemented his trade remarks with a fresh broadside against the Fed, saying “they don’t have a clue” and that rates are too high. He also called “very low inflation” a “beautiful thing” so we’ll see if today’s CPI report changes that dynamic at all. The PPI data – which we’ll run through below – was at the margin slightly hawkish and helped push 2y Treasury yields higher. Indeed 2y Treasuries closed +2.6bps higher at 1.93% while 10y Treasuries ended -0.5bps lower, meaning the curve flattened-3.13bps to 22.1bps, albeit still above the range for much of the year. The DOW shed -0.05%.

Apart from the political noise, there wasn’t a great deal of new news with markets initially reacting to the China infrastructure spend headlines from this time yesterday. This helped Europe with the STOXX 600 finishing +0.69%. The DAX (+0.92%) was the big out-performer having been closed on Monday, while the FTSE 100 gained +0.31% despite the pound’s +0.30% rally on strong wage data.

This morning in Asia markets are largely heading lower with the Hang Seng (-1.50%) leading the declines as locals protest ahead of a legislative council debate on a controversial bill that would allow extraditions to mainland China. The Shanghai Comp (-0.57%) and Kospi (-0.13%) are also lower while the Nikkei (+0.04%) is trading flattish. Elsewhere, futures on the S&P 500 are trading a touch lower. Crude oil prices (WTI -1.52% and Brent -1.40%) are also falling this morning as a report from the American Petroleum Institute reported that the US crude stockpiles increased by a further 4.85mn barrels last week. In terms of overnight data releases, China’s May CPI and PPI both came in line with consensus at +2.7% yoy and +0.6% yoy, respectively. We also saw Japan’s April core machine orders come in at +5.2% mom (vs. -0.8% expected), the third consecutive monthly rise thereby marking the longest sequence of such gains in the past four years, while May PPI came out in line with expectations at +0.7% yoy.

Back to the UK and yesterday saw the Labour Party table a cross-party motion to prevent a no deal Brexit. If such a bill were to pass, the tensions within Parliament would likely escalate towards a general election. On that theme, the Conservative party leadership contest kicks off with its first ballot tomorrow, where a hard Brexit-supporting candidate is likely to emerge victorious at the end of the process. This dysfunctional setup is outlined in more detail in Oliver Harvey’s latest note ( here ), which also updates his indicative probabilities of likely outcomes moving forward. He thinks the odds that a deal is successfully ratified by end-October are now 25%, while the odds of a no-deal Brexit are 25% as well. The remaining 50% is covered by his modal case for a general election, with 20% chance of a Conservative no-deal platform winning, 20% chance of a Labour/Liberal Democrat soft-Brexit platform winning, and 10% chance of no clear winner. The Brexit story and its consequences still have an enormous amount of runway to go but we are currently in the eye of the storm. This fresh parliamentary vote in a couple of weeks could shake things up again leaving a new PM little choice but to go to the country. ComRes published the first opinion poll overnight that I have seen with all the different potential Conservative leaders vs all the other parties. On this poll Boris Johnson is only one of the candidates that give the Tory’s a majority (140 seats) at the next election alongside a substantial 14% lead. He is the only candidate that reduces the Brexit party’s support enough (below 20%) to do this.

In other news from yesterday, the US May PPI report was at the margin slightly hawkish as we mentioned earlier with the ex food and energy reading printing in line at +0.2% mom but ex trade at +0.4% mom (vs. +0.2% expected). In addition, the healthcare component rose +0.25% mom which, when combined with a bounce back for the portfolio management component, suggests a stronger read-through for core PCE when we get the data at the end of this month. Holding everything else steady, today’s print implies around +7bps to the core PCE number due toward the end of this month.

That data dovetails nicely into today’s data highlight which is the CPI report in the US which should act as the next test for markets. The consensus expects a +0.2% mom core reading which would be enough to keep the annual rate at +2.1% yoy. Our US economists also expect a +0.2% mom reading and note that core goods should rebound slightly from the plunge in April which was the biggest monthly decline since 2006. That said, there are some downside risks from negative payback from shelter inflation. The data is due out at 1.30pm BST.

As for the other data yesterday, there was a decent jump in the May NFIB small business optimism reading of 1.5pts to 105.0 (vs. 102.0 expected). That reading had got as low as 101.2 back in January but has since risen every month. Meanwhile, here in the UK the latest employment data was mostly upbeat – in stark contrast to the April growth data we saw on Monday. The unemployment rate was confirmed as holding steady at 3.8% in April as expected, while 32k jobs were added which exceeded expectations. Regular wage growth also ticked up one-tenth to 3.4% compared to expectations for a small deceleration. So that keeps the hawkish labour market data versus BoE’s supply side narrative still very much intact. It’s worth noting that we heard from a couple of different BoE policy makers yesterday. Vleighe – seen as a centrist – said that “news since May has been disappointing in data and downside risks have intensified” while Broadbent said that “I am not particularly exercised that the future path of interest rates in the market should be exactly the one that is in our forecasts,” and thus made little conscious attempt to try and reprice the market.

In other news, yesterday EU officials confirmed their endorsement of the EC’s decision that Italy had failed to take the necessary steps to reduce its debt load in line with the bloc’s fiscal rules. The EU therefore confirmed that a disciplinary process is warranted. BTPs were +3.4bps higher yesterday, lagging the broader European fixed income rally. Italian politicians continued to speak positively, with Finance Minister Tria saying Italy is committed to a dialogue with the EU over the debt censure and Prime Minister Conte announcing that the leaders of the Five Star Movement and the Northern League will meet over the next few days to decide on a plan that will satisfy the Commission since “we are all determined” to avoid an EDP. That said, the market seems to be at a place where actions will speak louder than words.

To the day ahead now, which is headlined by that May CPI report in the US this afternoon. Other than that we’ll get the May monthly budget statement in the US while the European diary is particularly sparse this morning with nothing of note. Away from the data the ECB’s Draghi is due to speak this morning in Frankfurt where he is due to make welcome comments at a conference. The ECB’s Guindos will also speak.

3. ASIAN AFFAIRS

I)WEDNESDAY MORNING/ TUESDAY NIGHT: