GOLD: $1325.50 UP $1.65 (COMEX TO COMEX CLOSING)

Silver: $14.76 UP 10 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1327.00

silver: $14.75

YOUR DATA…

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 133/920

EXCHANGE: COMEX

CONTRACT: JUNE 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,324.700000000 USD

INTENT DATE: 06/10/2019 DELIVERY DATE: 06/12/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 H HSBC 499

657 C MORGAN STANLEY 50

661 C JP MORGAN 920 133

685 C RJ OBRIEN 3

686 C INTL FCSTONE 75

690 C ABN AMRO 6

737 C ADVANTAGE 96

800 C MAREX SPEC 20

905 C ADM 38

____________________________________________________________________________________________

TOTAL: 920 920

MONTH TO DATE: 1,459

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 920 NOTICE(S) FOR 92000 OZ (2.816 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1459 NOTICES FOR 14590000 OZ (4.538 TONNES)

SILVER

FOR JUNE

1 NOTICE(S) FILED TODAY FOR 5,000 OZ/

total number of notices filed so far this month: 310 for 1550,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 7926 UP 13

Bitcoin: FINAL EVENING TRADE: $ 7874 DOWN 40

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE A SMALL SIZED 263 CONTRACTS FROM 221,823 UP TO 222,086 DESPITE THE HUGE 38 CENT LOSS IN SILVER PRICING AT THE COMEX.( LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR SILVER AND IT STOPPED FOR GOLD AS WELL. WE WILL WITNESS A RISE IN THE SPREADERS IN SILVER ONCE WE START TRADING IN JUNE… READY FOR THE FIRST DAY NOTICE JULY CONTRACT.) TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A VERY HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR MAY, 0 FOR JUNE, 1313 FOR JULY. 180 FOR AUGUST, 24 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1517 CONTRACTS. WITH THE TRANSFER OF 1517 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1517 EFP CONTRACTS TRANSLATES INTO 7.585 MILLION OZ ACCOMPANYING:

1.THE 38 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

1.560 MILLION OZ STANDING FOR SILVER IN JUNE//

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

20,868 CONTRACTS (FOR 7 TRADING DAYS TOTAL 20,868 CONTRACTS) OR 104.340 MILLION OZ: (AVERAGE PER DAY: 2981 CONTRACTS OR 14.91 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JUNE: 104.230 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 11.09% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 993.06 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 263 DESPITE THE LARGE 38 CENT FALL IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A LARGE SIZED EFP ISSUANCE OF 1517 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS WILL RESUME THEIR LIQUIDATION OF THE SPREAD TRADES FOR SILVER ONCE THE JUNE CONTRACT COMMENCES IN EARNEST….

TODAY WE GAINED A GOOD SIZED: 1780 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1517 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 263 OI COMEX CONTRACTS. AND ALL OF THIS HUGE DEMAND HAPPENED WITH A 38 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $14.66 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.082 BILLION OZ TO BE EXACT or 152% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 1 NOTICE(S) FOR 5,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 1.560 MILLION OZ//

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

WITH RESPECT TO SPREADING: WE PROBABLY HAD VERY STRONG ACTIVITY OF SPREADING ACCUMULATION IN SILVER TODAY AS TOTAL OI ROSE DESPITE THE NASTY FALL IN PRICE

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JUNE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE OPEN INTEREST FELL BY A LESS THAN EXPECTED 2095 CONTRACTS, TO 499,227 DESPITE THE HUGE $16.40 PRICING FALL WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING LIQUIDATION HAS STOPPED AND THESE SPREADING FELLOWS HAVE ALREADY MORPHED INTO SILVER.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4389 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 4389 CONTRACTS, DEC> 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 5499,227. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN GOOD SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2294 CONTRACTS: 2095 CONTRACTS DECREASED AT THE COMEX AND 4447 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 2294 CONTRACTS OR 229,400 OZ OR 7.135 TONNES. YESTERDAY WE HAD A LARGE LOSS OF $16.40 IN GOLD TRADING.…AND DESPITE THAT LOSS IN PRICE, WE HAD A GOOD GAIN IN GOLD TONNAGE OF 7.135 TONNES!!!!!! THE BANKERS WERE SUPPLYING COPIOUS SUPPLIES OF SHORT GOLD COMEX PAPER.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 84,535 CONTRACTS OR 8,453,500 OR 262.293 TONNES (7 TRADING DAYS AND THUS AVERAGING: 12,076 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAYS IN TONNES: 262.293 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 262.293/3550 x 100% TONNES =7.38% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2,540.84 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A SMALL SIZED DECREASE IN OI AT THE COMEX OF 2095 DESPITE THE LARGE PRICING LOSS THAT GOLD UNDERTOOK ON YESTERDAY($16.40)) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 4389 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 4389 EFP CONTRACTS ISSUED, WE HAD AN GOOD SIZED GAIN OF 4447 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

4389 CONTRACTS MOVE TO LONDON AND 2095 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 7.13 TONNES). ..AND THIS GAIN OF DEMAND OCCURRED DESPITE THE FALL IN PRICE OF $16.40 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAD ZERO PRESENCE OF SPREADING ACCUMULATION IN GOLD ///TODAY/

we had: 920 notice(s) filed upon for 92,000 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $1.65 TODAY//

A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF .24 TONNES AND BECAUSE IT IS SMALL IT IS USUALLY FOR FEES ETC.

INVENTORY RESTS AT 756.18 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 10 CENTS TODAY:

NO CHANGE WITH RESPECT TO SILVER INVENTORY AT THE SILVER SLV

/INVENTORY RESTS AT 315.362 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A SMALL SIZED 263 CONTRACTS from 221,823 UP TO 222,086 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JUNE 0 CONTRACTS AND JULY: 1313 CONTRACTS FOR AUGUST: 180, FOR SEPT. 24 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1517 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 263 CONTRACTS TO THE 1517 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A VERY GOOD GAIN OF 1780 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 8.90MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY AND NOW 1.570 MILLION OZ FOR JUNE.

RESULT: A TINY SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 38 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A GOOD SIZED 1517 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN UP 73.59 POINTS OR 2.58% //Hang Sang CLOSED UP 210.70 POINTS OR 0.76% /The Nikkei closed UP 69.86 POINTS OR 0.33%//Australia’s all ordinaires CLOSED UP 1.52%

/Chinese yuan (ONSHORE) closed UP at 6.9123 /Oil UP TO 53.76 dollars per barrel for WTI and 62/33 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.9123 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9274 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/Globe

China still produces 70% of the world’s rare earths but it is diminishing. Many countries have started to compete with China. However mining of rare earths are costly as these earths are locked up in oxides or other compounds making extraction difficult

( zerohedge)

4/EUROPEAN AFFAIRS

i) UK/

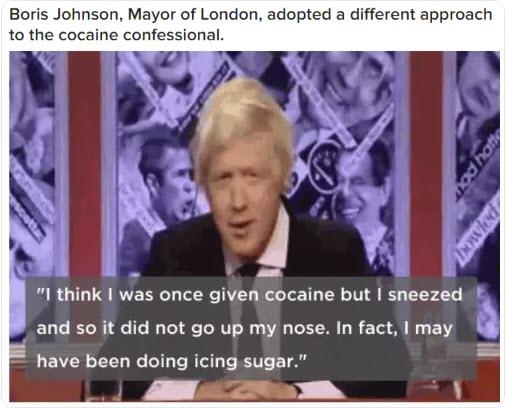

Boris Johnson’s seems to have solidified his lead as Gove is reported to have taken cocaine. He has pledged tax cuts which appeal to the conservative base. Boris Johnson wants to leave the EU and not to pay anything. He will renege on European debt owed. This should be very interesting if he wins

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)TURKEY

Turkey is helping enemies of Hafter. They still have large sections inside Tripoli and fighting is house to house.

A good look at the situation inside Libya today and how Turkey is destabilizing the situation.

( Miniter/HumanEvents.com)

ii)Iran

There is now no question that a permanent military presence in the Persian Gulf is the only way to counter Iran’s threats

( zerohedge)

6. GLOBAL ISSUES

Mexico/USA

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

a)Market trading/LAST NIGHT/

II)MARKET TRADING

ii)Market data

This is not what the Fed wants: producer price growth slumps the weakest in a 1 1/2 years. PPI is a forerunner for inflation growth.

( zerohedge)

iii)USA ECONOMIC/GENERAL STORIES

a)Illinois does not have a balanced budget: it still owes billions on its pension plans

( Dabroski)

b)This is something that we should pay attention to:

SWAMP STORIES

Let us head over to the comex:

Gold withdrawals;

i) We had 1 withdrawal:

out of Scotia: 798.54 oz

.

Gold To Reach 6 Y

end

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

GATA) Obviousness of gold market rigging helps central banks but there’s a limit

Submitted by cpowell on 02:25PM ET Tuesday, June 11, 2019. Section: Daily Dispatches

10:29a ET Tuesday, June 11, 2019

>Dear Friend of GATA and Gold:

Responding to your secretary/treasurer’s observation Sunday that central bank and government interventions against gold have been becoming more obvious —

http://www.gata.org/node/19134

— our friend C.W. writes that the more obvious interventions against gold become, the more effective they are.

“As more investors see that the gold market is relentlessly and successfully suppressed,” C.W. writes, “they (to quote Sam Goldwyn) ‘stay away in droves.’ The suppressors have found that there are no sanctions against their activities and so have concluded that the more widespread the belief that they are controlling the gold price, the better. That is why the rigging is so obvious.

“Although Stein’s Law (“If something can’t go on forever, it will eventually stop”) applies here, I am not sure I will live long enough to see it, and such a feeling also depresses sentiment.”

* * *

C.W. is right, but only to an extent. For central banks and governments long have concealed their interventions against gold —

http://www.gata.org/node/12016

— and even now refuse to acknowledge them formally —

— and still refuse to acknowledge them because they realize that acknowledging them would cause bigger problems, demolishing the myth of free markets generally and, by informing ignorant market participants, of whom there are still many, drive them out of rigged markets and impair the necessary publicity for the prices that discourage other investors.

The increasing obviousness of government and central banks interventions is less a strategy than a consequence of the increasing difficulty of market rigging. Gold price suppression is discouraging production and causing tightness in the physical market that “paper gold” cannot relieve as easily as it used to.

Indeed, the manipulation and suppression of the gold price depend on a certain number market participants being deceived all the time. If manipulation and suppression did not depend on this deception, governments and central banks would proclaim their gold price suppression every day.

This manipulation and suppression also depend — perhaps most of all — on the dignity of mainstream financial news organizations. They can overlook market rigging by governments and central banks and maintain their dignity only if it is not officially acknowledged. Mainstream financial news organizations will never pose to governments and central banks any critical questions about market rigging or anything else, but if the rigging ever was officially acknowledged, the news organizations would lose too much face by not reporting it. Word would get around among journalists themselves and market participants and before too long and what remains of the credibility of the news organizations would be shot.

So with their gold market rigging governments and central banks now are enjoying the benefits of both suspicion and ignorance. Market participants who are suspicious of intervention stay out of the gold market, and market participants who are not suspicious stay in it, get fleeced, and in getting fleeced help governments and central banks publicize the manipulated and suppressed prices.

That’s why exposure of government and central bank intervention in the gold market and other markets remains the prerequisite of ending imperialism and restoring limited and accountable government, free markets, fair dealing among nations, and democracy.

That exposure is GATA’s work and the basis of our appeal for financial support:

\Please consider helping us.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

USAGold’s ‘News & Views’ letter for June

Submitted by cpowell on Mon, 2019-06-10 18:23. Section: Daily Dispatches

2:25p ET Monday, June 10, 2019

Dear Friend of GATA and Gold:

USAGold’s June “News & Views” newsletter has commentary about gold’s upward breakout, billionaires who see virtue in the monetary metal as an investment, a new book by Jim Rickards, the Malaysian prime minister’s musings about a gold-backed east Asian currency, and more. The June issue is posted at USAGold here:

https://www.usagold.com/cpmforum/newsviewsjune19/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Demand for silver jewelry in India and the uSA increases dramatically and this is the reason we are witnessing hug importing of silver into India.

(courtesy Ghosal/Economic Times)

Premium on silver doubles due to weak supply

The current gold:silver ratio is expected to give a push to silver prices in the coming weeks.

By Sutanuka Ghosal, ET Bureau Jun 11, 2019, 10.21 AM IST

Kolkata: Premium on silver has doubled in the Indian bullion market in the past one week as supply has fallen due to aggressive buying by China, which is buying the metal for industrial usage. Also, the demand for silver jewellery from the US has pushed up the demand for the metal in India, which has witnessed a massive 186.23 per cent jump in silver jewellery exports in April 2019, compared with the same month last year.

The current gold:silver ratio, which stands at 90, is expected to give a push to silver prices in the coming weeks, feel analysts. The ratio measures how many ounces of silver it takes to buy an ounce of gold. On Monday, gold was hovering around $1,328 per troy ounce, while silver was trading at $14.98 per troy ounce.

“There is every possibility of silver prices going up any moment. The metal is underpriced and it can rally in the coming weeks,” said Gnanasekar Thiagarajan, director, Commtrendz Research.

“The metal is hovering between Rs 36,500 per kg and Rs 37,000 per kg. There is more or less stability in price movement which is attracting investors,” said Mukesh Kothari, director, RiddiSiddhi Bullion.

Washington-based The Silver Institute has predicted sentiment to be more supportive of the silver market this year. Silver demand for industrial fabrication, responsible for approximately 60 per cent of the total demand, is forecast to rise modestly this year.

Silver demand from brazing alloys and solders as well as electrical and electric applications is expected to rise again this year. This is on the back of continued demand from the automotive sector.

The photovoltaic demand is expected to rise too, the institute said. Even with legislative changes in China, coupled with global overstocking and continued attempts at thrifting, photovoltaic demand will still be very supportive of silver usage, as many governments will continue to install more solar power. The institute said India is expected to continue to be one of the largest silver consumers in 2019. Silver import reached nearly 225 million ounces (around 700 tonnes) in 2018, which is 35 percent higher than 2017.

Jewellery demand is expected to record a solid year of growth in 2019, according to the Silver Institute’s report. In the US, silver jewellery will remain a popular alternative to lower cart gold, driven by many issues. Globally, silver jewellery is expected to continue to expand due to its diversity of design, fine quality and excellent retail margins.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

end

* * *

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.9123/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.9274 /shanghai bourse CLOSED UP 73.59 POINTS OR 2.58%

HANG SANG CLOSED UP 210.70 POINTS OR 0.76%

2. Nikkei closed UP 69.86 POINTS OR 0.33%

3. Europe stocks OPENED ALL GREEN/

USA dollar index UP TO 96.78/Euro FALLS TO 1.1317

3b Japan 10 year bond yield: RISES TO. –.11/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.71/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 5376 and Brent: 62.33

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO -.22%/Italian 10 yr bond yield DOWN to 2.35% /SPAIN 10 YR BOND YIELD DOWN TO 0.57%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.57: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.78

3k Gold at $1321.80silver at: 14.67 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 18/100 in roubles/dollar) 64.54

3m oil into the 53 dollar handle for WTI and 62 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.71 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9916 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1222 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISING to –0.22%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.17% early this morning. Thirty year rate at 2.65%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

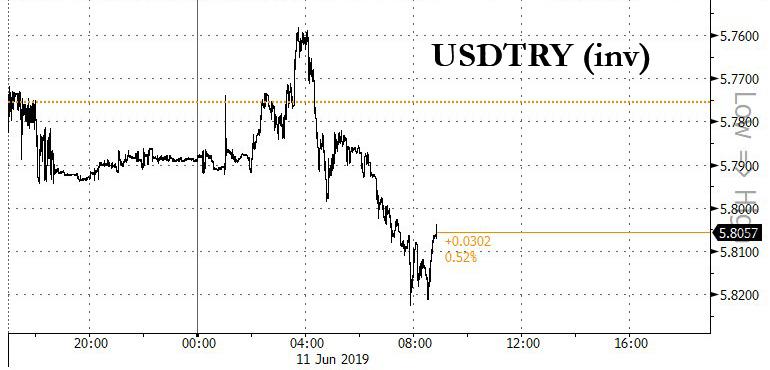

6. TURKISH LIRA: UP TO 5.8011..

Stock Buying Frenzy Accelerates, Sending S&P Above 2,900 As China, Yuan Soar

It is a sea of green in global markets today, with European stocks rallying as Germany’s carmakers outperformed, following a torrid session in Asia where the Shanghai Composite soared by 2.6%, as risk appetite refuses to go away after the United States stepped back from imposing tariffs on Mexico, while losses in treasuries and gold accelerated.

Advances in European miners and carmakers pushed Europe’s Stoxx 600 Index almost 1% higher, on course for a sixth day of gains in the last seven, with Frankfurt’s DAX racing up 1.2% as German investors returned from a one-day holiday, even as investor confidence in its economy fell to the lowest since 2010. BMW, Daimler and VW – seen as sensitive to trade tariffs – all gained between 1.8%-2%, mirroring a 1.9% gain for the auto sector.

Emini futures also continued their relentless June surge, with the S&P set to open above 2,900 for the first time in over a month.

“It looks like we will have to wait to see at the end of the month, to see what the next move will be,” said David Madden, an analyst at CMC Markets. “In that time, if nothing is said, stocks could press on higher – the belief that the Fed will all of a sudden become dovish is really driving markets.”

The MSCI world equity index, which tracks shares in 47 countries, advanced 0.24%. Wall Street futures were also seen opening higher, with S&P500 mini futures up 0.26%.

Earlier in the session, in Asia, MSCI’s broadest index of Asia-Pacific shares outside Japan gained 0.9% hitting the highest level since May 8, with Shanghai’s bourse climbing 2.6% after news that the country’s finance ministry said that it would loosen restrictions on how local governments spend money on infrastructure raised from selling special bonds helping offset the threat by President Donald Trump to raise tariffs again if President Xi Jinping doesn’t meet with him at the Group of 20 summit at month’s end. As a result, Asian stocks were set to post their biggest three-day gain since January as the risk-on mood spread across the region. Australian stocks also contributed to today’s strong climb. The S&P/ASX 200 Index closed 1.6% higher and reached fresh high for this year, as Vocus Group Ltd. soared after AGL Energy Ltd. offered to buy the company for about $2 billion. India’s S&P BSE Sensex also extended its gains into the third day. In emerging markets, stocks gained and currencies strengthened the most in a week. Oil edged up near $54 a barrel in New York.

Iron ore futures surged on the China spending plan, and the onshore yuan recovered after closing at its weakest level of the year. In emerging markets, stocks gained and currencies strengthened the most in a week. Oil edged up near $54 a barrel in New York.

After hitting its lowest level for 2019, with the “redline” level of 7.00 looming, China’s yuan jumped as much as 0.27%, the most in three weeks, as the central bank set its daily fixing at a stronger-than-expected level. The onshore currency was headed for its first gain in five sessions after the People’s Bank of China fixed its reference rate at 6.8930 per dollar, stronger than the average forecast of 6.9089 in Bloomberg’s survey of 21 traders and analysts. The central bank also said it plans to sell bills in Hong Kong in late June to improve the yield curve of yuan bonds. This comes after the yuan weakened to its weakest level since November on Monday, bringing it closer to 7 per dollar, a level it hasn’t breached since the financial crisis.

PBOC Governor Yi Gang said last week he was not wedded to defending the currency at a particular level. The fixing shows “China will still manage the pace of depreciation and the yuan will not break 7 so soon,” said Tommy Xie, an economist at Oversea-Chinese Banking Corp. “Even though the door has opened, China needs a proper catalyst.”

PBOC’s plan to sell bills in Hong Kong in late June and its stronger-than-expected fixings are a clear message it will defend the yuan at 7 per dollar, according to Standard Chartered. “The purpose is very very clear, that they just want to defend the currency regardless of the G-20 meeting” outcome, said Becky Liu, head of China macro strategy in Hong Kong. This new bill issuance is set to be around the G-20 meeting; if those talks are positive, the market will likely steady and the bill issuance size will be smaller; however, if the meeting disappoints, the PBOC can step up the amount and frequency of bill issuance in Hong Kong as “a very practical way to defend the currency.”

Elsewhere in FX, the dollar held steady above a 2-1/2 month low with rising expectations for a Fed rate cut tempered by a reluctance to close positions before the G20. “The markets are pricing in a 25-basis-point rate cut in July,” said Peter Schaffrik, head of European rates strategy at RBC Capital Markets, adding that expectations of looser policy would likely continue. “When you see the narrative that the market is painting, that it is all down to the negative implications from the trade war and the reduction of global trade,” he said. “It’s difficult to see how any one data point will change the entire picture.”

In rates, US Treasuries edged lower, with the 10 Yield rising to 2.17% after hitting a 2 year low of 2.05% on Friday. Amid the cautious optimism, a rally in longer-dated euro zone government bonds stalled as the pick-up in risk sentiment globally sparked a sell-off in the bloc. Germany’s 10-year bond yield, seen as a benchmark for government debt, was up 3 basis points at minus 0.23% – still a smidgeon away from last week’s record lows. Thirty-year bond yields in Germany and France were up as much as 8 basis points in early trade.

In commodities, oil prices rose, bolstered by firmer financial markets and expectations that producer group OPEC and its allies will keep withholding supply. Brent crude futures were at $62.67, up 0.4%. As noted above, gold (-0.4%) continues to fall at the whim of a firmer risk appetite, whilst in terms of base metals, copper (+0.9%) extends on its gains aided by the risk tone and Dalian iron ore surged 6% on supply woes amid expectations that miners will be unable to expand output to meet higher steel demand. Subsequently, JPM modestly upgraded its Chinese steel demand and iron ore price forecasts, noting that the peak disruption “is likely behind us”.

Today’s economic data include small business optimism. HD Supply, Wiley are due to report earnings

Market Snapshot

- S&P 500 futures up 0.4% to 2,901.75

- STOXX Europe 600 up 0.6% to 380.64

- MXAP up 0.7% to 157.13

- MXAPJ up 0.9% to 514.11

- Nikkei up 0.3% to 21,204.28

- Topix up 0.5% to 1,561.32

- Hang Seng Index up 0.8% to 27,789.34

- Shanghai Composite up 2.6% to 2,925.72

- Sensex up 0.5% to 39,990.92

- Australia S&P/ASX 200 up 1.6% to 6,546.29

- Kospi up 0.6% to 2,111.81

- German 10Y yield fell 0.2 bps to -0.221%

- Euro up 0.07% to $1.1320

- Brent Futures up 0.1% to $62.35/bbl

- Italian 10Y yield unchanged at 1.991%

- Spanish 10Y yield fell 2.1 bps to 0.583%

- Brent Futures up 0.1% to $62.35/bbl

- Gold spot down 0.4% to $1,322.97

- U.S. Dollar Index down 0.01% to 96.75

Top Overnight News from Bloomberg

- Chinese stocks posted their best gains in weeks on the news that local governments will have more room to spend on infrastructure, offsetting U.S. President Donald Trump’s latest threat to raise tariffs on China if President Xi Jinping doesn’t meet with him at the upcoming Group-of-20 summit in Japan

- China’s central bank moved to shore up the yuan with a stronger-than- expected fixing and a planned bond sale in Hong Kong

- Citigroup was suspended from the primary group of dealers that participate at certain Japanese government bond auctions after it was found to have manipulated futures prices

- The Bank of England doesn’t have to wait until all political uncertainty around Brexit is resolved to raise interest rates, according to policy maker Michael Saunders

- A record 10 British Conservatives will fight each other to replace Theresa May as prime minister. All agree that Britain has to leave the European Union, but most of them vow to renegotiate. Current favorite Boris Johnson says he will deliver Brexit in October with or without a deal

- The Bank of England doesn’t have to wait until all political uncertainty around Brexit is resolved to raise interest rates, according to policy maker Michael Saunders

- Australian business confidence surged after Prime Minister Scott Morrison’s shock election win, while conditions again deteriorated, providing further grist to the central bank’s decision to cut interest rates

- The U.S. expressed “grave concern” over Hong Kong legislation that would for the first time allow extraditions to mainland China, raising pressure on Beijing as the city braced for a potentially historic showdown over the proposal

- The Trump administration’s fight against China’s Huawei Technologies Co. justifies Russia’s decision to build a “sovereign internet” to protect its domestic network from external threats, according to Russian Deputy Prime Minister Maxim Akimov

Asian equity markets were higher across the board after a similar lead from US where sentiment was underpinned by the US-Mexico tariff relief which lifted the S&P 500 and DJIA to a 5-day and 6-day win streak respectively, although gains in the region were initially capped amid a lack of fresh catalysts. ASX 200 (+1.6%) and Nikkei 225 (+0.3%) traded positively with early outperformance in Australia as it played catch up on return from the extended weekend and with Vocus Group the largest gainer following a takeover offer from AGL Energy, while the Japanese benchmark was just about kept afloat by a weaker currency. Elsewhere, Hang Seng (+0.8%) and Shanghai Comp. (+2.6%) conformed to the upbeat tone despite another net liquidity drain by the PBoC and mixed comments by US President Trump who stated that a trade deal with China will work out because of tariffs but warned the next USD 300bln of tariffs will come into effect if Chinese President Xi does not come to the G20. Nonetheless, mainland China outperformed after China issued notice encouraging investment in local government special bonds issuance for project financing and amid reports that the PBoC may continue to support banks through various tools. Finally, 10yr JGBs were lower as yields tracked the rebound in their US counterparts and with demand for Japanese bonds also sapped by gains in stocks and after weaker demand in the enhanced liquidity auction for longer-dated bonds.

Top Asian News

- China Car Slump Extends to a Year With No Rebound In Sight

- China Sets Yuan Fixing Stronger Than Expected in Sign of Defense

- When This Chinese Newspaper Editor Tweets, Wall Street Listens

- India’s World-Beating Growth May Not Be so Fast After All

European equities are higher across the board [Eurostoxx 50 +0.9%] following on from a similar lead in Asia wherein Mainland China closed with gains in excess of 2.5%. Germany’s DAX (+1.3%) is outperforming its peers as the index plays catch-up following yesterday’s holiday. Sectors are broadly in the green with the exception of defensive sectors amid the current “risk on” mood, whilst material names are outperforming as Dalian iron ore futures spiked 6% higher on supply concerns and copper prices rose almost 1% on the firmer risk sentiment. In terms of in individual movers, Thyssenkrupp (+5.5%) sits near the top of the Stoxx 600 as the steel name benefits from the aforementioned iron ore spike. Elsewhere, German autos are supported (BMW +1.6%, Daimler +1.8%, Volkswagen +1.8%) as the stocks react to the weekend US-Mexico developments for the first time. Finally, Hugo Boss (+4.3%) shares were bolstered amid an upgrade at Morgan Stanley.

Top European News

- Lloyds Tests U.K. Utility Industry Exposure as Corbyn Risk Looms

- Alitalia Rescue Stalled as Govt Eyes New Deadline: Repubblica

- Novo Nordisk Climbs After Rival Lilly’s Disappointing Trial Data

- Danske Tells Debt Issuers to Act Fast as Orders Get Erratic

In FX, GBP rose on more hawkish leaning BoE rhetoric, as Saunders follows Haldane on the rate hike path has been validated to a degree by the latest UK labour report revealing firmer than forecast wages, and in particular an unexpected pick-up in ex-bonus earnings, in stark contrast to Monday’s dismal GDP and industrial output figures. Hence, the Pound has rebounded across the board with Cable back above 1.2700 and testing yesterday’s pre-data peaks ahead of resistance seen around 1.2740, while Eur/Gbp has reversed from fresh multi-week highs circa 0.8932 through 0.8900.

- NZD/JPY/CHF/AUD – In contrast to Sterling’s revival, the Kiwi has extended losses to 0.6588 vs its US counterpart and 1.0550+ against the Aussie, which is also weak compared to the Buck but holding up better around 0.6950 ahead of jobs data on Thursday. Nzd/Usd saw accelerated selling on a break of 0.6600 and market participants also noted stops in Nzd/Jpy when 71.81 failed to hold, with a variety of model and spec offers pushing the cross down to 71.54. Similarly, the Yen and Franc have weakened a bit further vs the Dollar as the DXY sits tight between 96.832-673, with Usd/Jpy hovering above 108.50 within a 108.36-73 range and Usd/Chf holding closer to the upper end of a 0.9923-0.9893 band. Note, however, Usd/Jpy may well be drawn towards decent option expiry interest at 108.50 in 1.1 bn.

- CAD/EUR – The Loonie continues to outperform, as technical impulses turn increasingly bullish and Usd/Cad trade below the 200 DMA (1.3273) towards 1.3250 and post-NA jobs data lows of 1.3225, while the single currency remains above 1.1300 where more expiries lie (1.1 bn) even though Eurozone Sentix sentiment soured significantly and ECB’s Rehn reiterated that all monetary stimulus options will be available if growth weakens further. On the flip-side, Eur/Usd is still butting up against resistance ahead of 1.1350 and the 200 DMA (1.1365), including option barriers and more expiries, like 2.3 bn from 1.1340 to 1.1350 and 2.8 bn at 1.1360.

- NOK – The Norwegian Crown slipped in wake of considerably sub-consensus CPI metrics that called into question firm Norges Bank guidance for a rate hike at this month’s policy meeting, but Eur/Nok reversed from a probe over resistance around 9.8300 to revisit pre-inflation data levels sub-9.7800 on the back of an upbeat regional survey that restored June tightening expectations. Conversely, Eur/Sek has seen more upside towards 10.6900 ahead of Sweden’s inflation update on Friday and potential pointers from Prospera’s expectations survey tomorrow.

In commodities, WTI (+0.8%) and Brent (-0.3%) futures are choppy as the benchmarks are benefitting from the improved risk tone,with the former around USD 62.50/bbl and the latter hitting a session peak just under USD 54.00/bbl. News flow has been light for the complex as participants eye tonight’s EIA Short term Energy Outlook report and API inventories release with the street looking for a headline draw of 1.25mln barrels. Elsewhere, Energy Intel’s Senior Correspondent notes that Russian Energy Minister Novak requested a delay to the OPEC/OPEC+ meeting (originally scheduled for June 25/26) as a later date would give key participants the chance to discuss the issue more at the G-20 summit on June 28. The correspondent also notes of that Iranian officials are yet to agree on the new proposed dates to move the OPEC meeting from June to early July, according to sources and the current secretariat is looking at the option of holding OPEC meet in June and the non-OPEC in July. Elsewhere, gold (-0.4%) continues to fall at the whim of a firmer risk appetite, whilst in terms of base metals, copper (+0.9%) extends on its gains aided by the risk tone and Dalian iron ore surged 6% on supply woes amid expectations that miners will be unable to expand output to meet higher steel demand. Subsequently, JPM modestly upgraded its Chinese steel demand and iron ore price forecasts, noting that the peak disruption “is likely behind us”.

US Event Calendar

- 6am: NFIB Small Business Optimism, est. 102, prior 103.5

- 8:30am: PPI Final Demand MoM, est. 0.1%, prior 0.2%; PPI Ex Food and Energy MoM, est. 0.2%, prior 0.1%

- 8:30am: PPI Final Demand YoY, est. 1.95%, prior 2.2%; PPI Ex Food and Energy YoY, est. 2.3%, prior 2.4%

DB’s Jim Reid concludes the overnight wrap

Since I moved out of London 9.5 years ago I’ve had a 1 to 3 mile commute to the station depending on whether I use the local or mainline station. I’m proud of the fact that outside of my leg being in a brace I’ve walked or cycled pretty much every day over that period. I’ve seen heavy rain, hail, lightening, snow and even Saharan sand fall from the skies whilst getting to and from the station. However I have to say that yesterday I took one look out the window first thing and also at the forecast and really didn’t fancy it so I drove. It proved to be one of the best decisions I’ve ever made as the rain was biblical in London and the surrounds yesterday with no real respite all day. I can’t remember a summer day like it. I’m back on my bike today and hopefully I’ll remember to change out of my Lycra in time to appear live on Bloomberg TV this morning at 10am. So catch me if you are able.

I suspect (and hope) the appearance won’t be as memorable as President Trump’s live phone interview with CNBC yesterday which drove much of the conversation around markets. To say that the interview was wide-ranging would be an understatement. While Trump proudly touted his weekend agreement with Mexico which averted higher tariffs, he also emphasised how his threats were key to reaching an agreement. He said “tariffs are a beautiful thing” and that “without tariffs, we would be captive to every country.” Trump did go on to say that China is “going to make a deal because they’re going to have to make a deal,” though he said that no bilateral meeting with President Xi was yet scheduled for the G-20 at the end of June. After US markets closed, headlines from the Chinese media broke suggesting that the two leaders will meet, but the details have yet to be hammered out. Meanwhile, Trump said to reporters outside the White House after the CNBC interview that he could impose tariffs of 25%, or “much higher than 25%” on $300 billion in Chinese goods, if Chinese President Xi Jinping doesn’t meet with him at the upcoming G-20 summit in Japan. Elsewhere, the US VP Pence said overnight that the US is going to stand firm on China while adding we are in a very strong position on the country.

Back to the CNBC interview, Trump also criticised the Federal Reserve, saying they have been “very disruptive to us,” and spoke admiringly of China’s system where President Xi has more direct influence on the PBoC. Two-year Treasury yields fell -2.8bps while Trump was speaking, but ultimately retraced to end the day +5.0bps higher at 1.90%.

Apart from the move in Treasuries, risk assets barely budged during his comments, as they were still being helped higher by the halo effect of no Mexican tariffs being imposed after the announcement late last Friday night. The +0.45% gain for the S&P 500 last night, although down from the +1.09% session highs, means that the index has risen for five consecutive days – the first time that has happened since April. It has now posted a +4.88% return for June to date so far which is the best start to a month since October 2011, taking the index to just 2.01% below its all-time peak. The NASDAQ also rallied +1.05% yesterday which means it’s up by an even larger amount this month (+4.96%), while semiconductors are the real standout after rising +2.54% yesterday (+9.08% in June). In Europe a +0.21% gain for the STOXX 600 means that index is up a solid +2.50% so far in June too. Meanwhile it’s been a much more sideways 10 days for rates following that fairly decent rally through May. For example, 10y yields are +2.0bps higher now following a +6.4bps climb yesterday, while the yield curve is +4.3bps steeper in June at 24.3bps following yesterday’s +1.6bps move. Bund yields rose +3.7bps to -0.219%, the first time in five sessions that they didn’t close at a new all-time low. Germany was on a public holiday though so trading was thin.

This morning in Asia markets are following Wall Street’s Lead with the Nikkei (+0.29%), Hang Seng (+0.76%) and Kospi (+0.31%) all up while Chinese bourses are up c.2% with the CSI 300 +2.33%, Shanghai Comp +1.87% and Shenzhen Comp +2.82%. Elsewhere, futures on the S&P 500 are up +0.17%.

In other overnight news, the PBoC fixed a higher reference rate for the yuan today at 6.8930 (vs. expectations of 6.9089). The move comes after the onshore yuan traded at weakest level of the year yesterday at 6.9311. The central bank has also said that it plans to sell bills in Hong Kong later this month, a move that will drain liquidity and support the currency. The onshore yuan is trading up +0.20% at 6.9170.

Moving on. Once again Italian assets traded to their own beat again yesterday with the FTSE MIB opening higher, then wiping out those gains by late morning before ultimately closing +0.61%. In bonds, 10y BTP yields closed flat, despite rising as much as +7.6bps earlier in the session. Italian PM Conte grabbed the early attention on the wires, telling Corriere della Sera that the Italian government would be effectively over if Italy can’t make a budget compromise with the EU. Deputy PM Salvini, who admittedly has regularly shifted his positions depending on circumstances, said that a confrontation with the EU “is the last thing we want to do.” Data in Italy also showed a big slump in industrial production in April of -0.7% mom (vs. 0.0% expected). It’s worth noting that despite the ongoing and justified concerns around Italy, 10y BTPs are still trading at around the lowest yield (2.358%) since the new government was elected last year.

Meanwhile, news from the UK economy was nearly as bleak as the weather yesterday following a weak April GDP reading of -0.4% mom (vs. -0.1% expected). While the extent of the drop was a surprise, the slump being led by a big drop in autos output was less so with car companies closing production plants preparing for a no deal Brexit last month. Sterling dropped -0.35% yesterday which helped the FTSE 100 to a +0.59% gain. It’s worth noting that we get the April and May employment stats in the UK today so that should be worth watching in light of yesterday’s data. After that attention will shift to Thursday’s first ballot for the Conservative leadership contest. The field is officially set with 10 contenders, with Boris Johnson leading according to the bookmakers, who give him around a 56% chance of winning the contest. Jeremy Hunt and Andrea Leadsom are next in line with roughly 17% and 10% chances, according to the betting markets. Elsewhere, the BoE MPC member Michael Saunders, a hawk, said in an overnight speech that “The MPC does not necessarily have to keep rates on hold until all Brexit uncertainties are resolved, the MPC has already raised rates twice since the Brexit vote. We will act again if needed to ensure a sustained return of inflation to target over time.” Our UK economists, however, changed their view last week forecasting that the BoE will no longer hike rates this year and see rising risks that the Bank rate has reached its terminal point, with the weak April GDP reading further reinforcing their view. To read their complete note click here .

Over in the US, the JOLTS report on the condition of the US labour market was released, showing still-robust conditions despite the disappointing nonfarm payrolls report. The quits rate, which has led wage growth fairly reliably, stayed at its cyclical high of 2.6%, while the hiring rate also stayed high at 4.3%. Separately, the New York Fed published its Survey of Consumer Expectations, which showed that 3-year inflation expectations have fallen to 2.59%, their lowest level since May 2017.

Looking at the day ahead, as well as the employment data in the UK this morning we’ll also get the May Bank of France industrial sentiment reading and Sentix investor confidence reading for the Euro Area. In the US we’ll get the May NFIB small business optimism reading, before the focus turns to the May PPI report. Away from that the ECB’s Nowotny and Rehn are due to speak this morning while over at the BoE we’re due to hear from Saunders, Tenreyro and Broadbent.

3. ASIAN AFFAIRS

I)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN UP 73.59 POINTS OR 2.58% //Hang Sang CLOSED UP 210.70 POINTS OR 0.76% /The Nikkei closed UP 69.86 POINTS OR 0.33%//Australia’s all ordinaires CLOSED UP 1.52%

/Chinese yuan (ONSHORE) closed UP at 6.9123 /Oil UP TO 53.76 dollars per barrel for WTI and 62/33 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.9123 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9274 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

China/Globe

China still produces 70% of the world’s rare earths but it is diminishing. Many countries have started to compete with China. However mining of rare earths are costly as these earths are locked up in oxides or other compounds making extraction difficult

(courtesy zerohedge)

4/EUROPEAN AFFAIRS

i) UK/

Boris Johnson’s seems to have solidified his lead as Gove is reported to have taken cocaine. He has pledged tax cuts which appeal to the conservative base. Boris Johnson wants to leave the EU and not to pay anything. He will renege on European debt owed. This should be very interesting if he wins

(courtesy zerohedge)

Boris Johnson Solidifies Lead: Pledges To Cut Taxes When Prime Minister

Authored by Mike Shedlock via MishTalk,

The 1922 Committee has certified 10 Tory candidates to battle to replace Theresa May. Boris Johnson solidified his lead.

BJ’s Campaign to Lose

The Sun reports Tory leadership Race is Now Boris Johnson’s to Lose as MPs Back Him Over Brexit.

What Happened?

- Pledge tax cuts appealing to the Tory base. The party is so fragmented that appealing to the base makes perfect sense.

- The court tossed out a private lawsuit against Johnson over alleged Referendum lies. The lawsuit was so absurd, it was guaranteed to help Johnson.

- Chances for rival Michael Gove, the best hope of Stop Boris Movement, are sinking fast over cocaine usage. Apparently it went up Gove’s nose but not Johnson’s.

Lewis Goodall

✔@lewis_goodall

Yesterday I observed that there is a stark set of double standards operating about the cocaine use of Michael Gove vs Boris Johnsson in this leadership contest. Johnson has now denied he ever took the drug. I have scoured the archives for everything we know about it. Here it is.

Lewis Goodall

✔@lewis_goodall

I’m sorry can someone explain something to me:we know Gove took cocaine and he’s getting deep flak for it; we know Johnson did the same (and was mayor in charge of the Met, enforcing anti drugs policies) but it seems to be no problem for him? Why? Because he told a joke about it?

Gove Q&A on Cocaine

In an afternoon speech, Gove tried to defend his cocaine position.

Q: You have a lot of supporters here. But you must know your campaign is in real trouble. When you were a prominent figure before you became an MP, you thought it was OK to snort cocaine. Then, as justice secretary, you were prepared to send poor people who did the same to jail. People do not like double standards.

A. Gove says he has reflected on this. He would ask people to judge him by what he did as justice secretary. He encouraged people to to accept that people should be given a second chance.

That defense was a flop.

Sneeze Defense

I Thought It Was Sugar

When ridiculous defenses work, it’s smacks of something far more fundamental: The party did not want Gove.

Gove did himself in, not cocaine. Gove was willing to ask for another Brexit extension.

That was political suicide.Cocaine hypocrisy obviously did not help.

Problem With Jeremy Hunt

Thanks to cocaine-gate, Jeremy Hunt is now the second favorite behind Johnson.

Like Gove, Hunt is willing to have another extension.

That will matter at some point.

Ten Candidates

Ten Candidates

The Guardian Live Blog reports 1922 Committee Confirms 10 Candidates on Ballot for First Vote.

Art of Not Doing

“Boris Johnson is dominating the campaign, despite being largely absent from it. The former foreign secretary is refusing to give broadcast interviews, and his campaigning consists of private talks with MPs, plus the odd intervention in friendly newspapers (mostly the Telegraph, which pays him handsomely for his column). Yet what has been striking today is how all the other contenders are defining themselves in opposition to him, by stressing the need for serious leadership or a fresh start etc.”

Johnson’s Shut Up and Dance With Me Campaign

Johnson may not be giving interviews but he did do one critical thing: appeal to the base with tax cuts.

Matt Hancock, Dominic Raab, and Michael Gove – criticized the tax cut directly.

“One thing I will never do as prime minister is to use our tax and benefits system to give the already wealthy another tax cut,” said Gove

Kiss them all goodbye as hopeless. Gove did himself in. The rest, other than Hunt, never had any real chance in the first place.

Via Eurointelligence

Over the weekend we got a glimpse of the Brexit dynamics we are likely to see under a new Tory leader. Boris Johnson proposed two fiscal measures likely to create significant new facts for the UK’s future relationship with the EU. One is a refusal to pay the £39bn, the negotiated total financial settlement included in the draft withdrawal agreement. The other is a massive Salvini-style income-tax cut, in the form of an increase in the upper threshold for the lower tax rate of 20% from the current £46000 to £80000.

Key Points

- Boris Johnson is building up his lead in the Tory leadership race with the promise of a dramatic income-tax cut.

- This is strategically a smart move, as it shifts the debate away from Brexit to a domain that is popular among Tory members.

- Tax cuts would make it harder for the UK and the EU to negotiate a future association agreement, as the EU could come to regard the UK as a tax haven.

Strategically Smart Move

- Shut up and dance. Johnson is not talking much with the media. The less you say to the media, the less likely you are to get trapped into offending someone.

- Does £46,000 (roughly $58,000) constitute being wealthy? Johnson’s tax cuts primarily benefits the middle class ($58,000 to $101,000). Gove ridiculously attacked the cuts as a benefit to the wealthy.

- Johnson also discussed not using the £39,000 Brexit breakup fee for other things.

- The EU does not like tax cuts and may view the UK as a tax haven. Via points 2 and 3, Johnson purposely gave the EU a strong reason not to deal. This increases the likelihood of no deal even if Johnson’s official stance is to negotiate.

- Being willing to deal but making it difficult or impossible to do so is brilliant.

Shut Up and Dance Musical Tribute to Johnson

Prepare for No Deal

This is likely to come down to Hunt vs Johnson.

Prepare for Johnson and No Deal.

END

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)TURKEY

Turkey is helping enemies of Hafter. They still have large sections inside Tripoli and fighting is house to house.

A good look at the situation inside Libya today and how Turkey is destabilizing the situation.

(courtesy Miniter/HumanEvents.com)

With Friends Like Turkey, Who Needs Enemies?

Authored by Richard Miniter via HumanEvents.com,

Turkey, America’s erstwhile NATO ally, is now arming America’s enemies in Libya, a flagrant violation of the 2011 United Nations arms embargo.

The clearest evidence of Turkey’s violation of U.N. embargoes came in the hold of a Turkish-crewed ship named “Amazon.” It delivered some 20 Turkish-made armored vehicles, known as “MRAPs,” the military news website South Front reported. A local blogger photographed the armored vehicles on the dock.

Turkey supports Libya’s Government of National Accord holed up in Tripoli. Qatar and, seemingly, Iran also back it. If it prevails, its government will impose Sharia law, corrupt the press, socialize the economy, and open a safe haven for terrorists.

America backs General Khalifa Haftar’s Libyan National Army, which commands a large swathe of eastern Libya. Gen. Haftar’s promises an Egypt-style government, if he wins. That means basic human rights, rule of law, a semi-free press, and regular elections that are usually won by the ruling party. And a new ally in the war on terror. America’s security is often strengthened by such hard compromises with its principles, leaving many Americans uneasy. This is an alliance that makes sense. Mainly because all of the realistic alternatives are far worse.

Sirte, Libya, 23/01/12. Photo: ECHO Jan 2012, Flickr

Gen. Haftar was once a high-ranking official in Muammar Gadhafi’s regime. He defected, worked with the CIA, and spent the better part of two decades living in the northern Virginian suburbs before returning to his homeland a few years ago. His forces are large, broadly disciplined, and well equipped.

So far Haftar’s army has easily swept away all opposition in their path.

Yet Tripoli may be beyond its grasp. Urban warfare is the opposite of fast-moving desert campaigns. It is usually a house-to-house proposition in which defenders make invaders pay for yards gained… in lives lost.

Civilians are often murdered, maimed, or raped by one side or the other. Some join the resistance, becoming human bombs or amateur snipers. Even corpses are boobytrapped with explosives. Tripoli is a humid Stalingrad.

Haftar’s forces arrived in April. Almost two months later, it controls less than half of the city.

In this urban battleground, Turkish-supplied armor makes a big impact. America used similar vehicles to clear the Baghdad airport road of dug-in insurgents in 2005. Turkish armor will either lengthen the war and widen the death toll or, worse, prevent the war’s end by enforcing a murderous stalemate. Without aircraft or armor of its own there is little Haftar’s soldiers can do.

(Kabul, Afghanistan) Two Turkish soldiers salute. (U.S. Navy photo by MC2 (SW) Christopher Hall)

Ignoring or withdrawing from Libya is not a realistic option. A failed state on the Mediterranean would soon become a transit point of millions of refugees onward to Europe. As the Syrian refugee wave taught us, Europe can quickly be destabilized, both economically and politically, by migrants.

The new “nationalist” or nativist parties would surge, while crime and poverty climb. Landing one million more North Africans would also boost Europe’s unemployment rates, which are at double digits in some places. The cultural chasm between secular Europeans and observant Muslims would provoke riots, as we have already seen in Germany. Even if the U.S. wanted to sit Libya out, the Europeans would not agree.

What is Turkey’s future as part of America’s most important military alliance, NATO?

Long governed by the Islamist AKP, Turkey has broken its longtime alliance with Israel, helped Iran evade U.S. sanctions by trading with it, and now, in Syria and Libya, aids America’s battlefield enemies.

President Donald J. Trump and President Recep Tayyip Erdoğan of Turkey at the United Nations General Assembly (Official White House Photo by Shealah Craighead)

There is no treaty mechanism to painlessly expel Turkey from NATO. Besides, it supplies the second-largest contingent of ground troops in the alliance – more than Britain and France combined. Asking the Turks to leave may not be wise.

Yet neither would be ignoring Turkish antagonism.

President Trump’s willingness to use tariffs could play a helpful role. He imposed onerous tariffs on Turkey before, to spring a U.S.-born pastor from Turkish prison. Using that tool again may dissuade the Turks from arming America’s enemies – before such behavior hardens into habit.

end

Turkey Lashes Out At US Pressure Over Russian Missile Deal, Lira Slides

After two weeks of torrid gains with the market now expecting a dip in the country’s double-digit inflation, the Turkish lira is again lower on Tuesday, after Ankara lashed out at Washington, saying a U.S. House of Representatives’ resolution condemning Turkey’s purchase of Russian defense systems and urging potential sanctions was “unacceptably threatening.”

The resolution, introduced in May and entitled “Expressing concern for the United States-Turkey alliance”, was agreed in the House on Monday according to Reuters. It urges Turkey to cancel the S-400 purchase and calls for sanctions if it accepts their delivery, which may come as soon as July. That would undermine the U.S.-led transatlantic defense alliance, according to the resolution.

In response, Turkey’s Foreign Ministry said in a statement that its foreign policy and judicial system were being maligned by “unfair” and “unfounded” allegations in the resolution.

“It is unacceptable to take decisions which do not serve to increase mutual trust, to continue to keep the language of threats and sanctions on the agenda and to set various artificial deadlines,” it added.

On Monday, U.S. officials said the training of Turkish pilots on F-35 fighter jets had come to a faster-than-expected halt at an air base in Arizona, as Ankara’s involvement was wound down over the S-400 controversy.

President Erdogan’s government faces a balancing act in its ties with the West and Russia, with which it has close energy ties and is also cooperating in neighboring Syria. The United States has also been pressuring Turkey and other nations to isolate Iran, including blocking oil exports.

As has been thoroughly documented here and elsewhere, relations between the two NATO members have been strained on several fronts including Ankara’s plans to buy Russia’s S-400 air defense systems, the detention of U.S. consular staff in Turkey, and conflicting strategy over Syria and Iran which precipitated a crisis in Turkey’s economy in the summer of 2018, sparking runaway inflation and a crash in the lira.

The United States has claimed that Turkey’s acquisition of Russia’s S-400 air defenses poses a threat to Lockheed Martin Corp’s F-35 stealth fighters, which Turkey also plans to buy.

“We rarely see it in foreign affairs, but this is a black and white issue. There is no middle ground. Either Mr. Erdogan cancels the Russian deal, or he doesn’t,” Eliot Engel, chairman of the House Committee on Foreign Affairs, said on the House floor on Monday. “There is no future for Turkey having both Russian weapons and American F-35s. There’s no third option.”

Regardless of the U.S. warnings, Turkey appeared to be moving ahead with the S-400 purchase. Erdogan said last week it was “out of the question” for Turkey to back away from its deal with Moscow. And so, with the two nations set on collision course in a repeat of last summer, the selling in the lira appears to have resumed, with the USdTRY jumping from 5.76 to as high as 5.82…

… amid trader concerns Trump may flex his tariff muscles again, this time in the direction of Ankara.

Iran

There is now no question that a permanent military presence in the Persian Gulf is the only way to counter Iran’s threats

(courtesy zerohedge)

Is A Permanent Military Presence In The Persian Gulf The Only Way To Counter Iran?