GOLD: $1341.15 UP $1.05 (COMEX TO COMEX CLOSING)

Silver: $14.82 DOWN 9 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1341.75

silver: $14.83

today was our first attempt at breaking the gold $1350 barrier for gold and $15.00 for silver. I know that many of you are discouraged dealing with the criminal bankers.

Lately it has been becoming increasing difficult for the bankers to whack because as they supply huge amounts of paper gold/silver, there are some on the other side

buying the paper but this time turning to the bankers and asking for physical delivery. The only time they did not have to worry about that is Friday as London is already put to bed

and only paper exists. Their nightmare returns on Monday…so do not be discouraged. Demand for physical is going through the roof!

YOUR DATA…

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 33/106

EXCHANGE: COMEX

CONTRACT: JUNE 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,339.200000000 USD

INTENT DATE: 06/13/2019 DELIVERY DATE: 06/17/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 H HSBC 4

657 C MORGAN STANLEY 1

661 C JP MORGAN 33

685 C RJ OBRIEN 1

686 C INTL FCSTONE 14 5

737 C ADVANTAGE 72 61

800 C MAREX SPEC 9

905 C ADM 11 1

____________________________________________________________________________________________

TOTAL: 106 106

MONTH TO DATE: 1,694

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 106 NOTICE(S) FOR 10600 OZ (0.3297 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1694 NOTICES FOR 169,400 OZ (5.2690 TONNES)

SILVER

FOR JUNE

0 NOTICE(S) FILED TODAY FOR NIL OZ/

total number of notices filed so far this month: 310 for 1550,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 8250 UP 33

Bitcoin: FINAL EVENING TRADE: $ 8217 UP 88

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE A STRONG SIZED 2976 CONTRACTS FROM 230,580 UP TO 233,556 ACCOMPANYING THE 11 CENT GAIN IN SILVER PRICING AT THE COMEX.( LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR GOLD . HOWEVER WE ARE WITNESSING A RISE IN SPREADING ACCUMULATION BY THE BANKERS IN SILVER)..TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JUNE, 1219 FOR JULY. 60 FOR AUGUST, 0 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1279 CONTRACTS. WITH THE TRANSFER OF 1279 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1279 EFP CONTRACTS TRANSLATES INTO 6.39 MILLION OZ ACCOMPANYING:

1.THE 11 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

1.560 MILLION OZ STANDING FOR SILVER IN JUNE//

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

27,573 CONTRACTS (FOR 10 TRADING DAYS TOTAL 27,573 CONTRACTS) OR 137.87 MILLION OZ: (AVERAGE PER DAY: 2757 CONTRACTS OR 13.78 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JUNE: 137.87 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 19.68% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1008.62 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2976 WITH THE 11 CENT FALL IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1279 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS WILL RESUME THEIR LIQUIDATION OF THE SPREAD TRADES FOR SILVER ONCE THE JUNE CONTRACT COMMENCES IN EARNEST….

TODAY WE GAINED A STRONG SIZED: 4255 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1279 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 2976 OI COMEX CONTRACTS. AND ALL OF THIS HUGE DEMAND HAPPENED WITH A 11 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $14.91 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.082 BILLION OZ TO BE EXACT or 152% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 1.560 MILLION OZ//

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

WITH RESPECT TO SPREADING: WE NO DOUBT HAD VERY STRONG ACTIVITY OF SPREADING ACCUMULATION IN SILVER TODAY AS TOTAL OI ROSE SHARPLY WITH THE SMALLISH GAIN OF 4 CENTS.

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JUNE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE OPEN INTEREST ROSE BY A STRONG 8931 CONTRACTS, TO 511,471 WITH THE $6.60 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING LIQUIDATION HAS STOPPED AND THESE SPREADERS HAVE ALREADY MORPHED INTO SILVER AND THEY ARE INTO THE ACCUMULATION PHASE OF THEIR OPERATION.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3812 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 3812 CONTRACTS, DEC> 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 511,471. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A HUGE SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,743 CONTRACTS: 8,931 CONTRACTS INCREASED AT THE COMEX AND 3812 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 12,743 CONTRACTS OR 1,274,300 OZ OR 39.63 TONNES. YESTERDAY WE HAD A GAIN OF $6.60 IN GOLD TRADING.…AND WITH THAT GAIN IN PRICE, WE HAD A HUGE GAIN IN GOLD TONNAGE OF 39.63 TONNES!!!!!! THE BANKERS WERE SUPPLYING COPIOUS SUPPLIES OF SHORT GOLD COMEX PAPER.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 101,624 CONTRACTS OR 10,162,400 OR 316.09 TONNES (10 TRADING DAYS AND THUS AVERAGING: 10,164 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAYS IN TONNES: 316.09 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 316.09/3550 x 100% TONNES =8.90% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2,593.99 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A VERY STRONG SIZED INCREASE IN OI AT THE COMEX OF 8,931 WITH THE PRICING GAIN THAT GOLD UNDERTOOK ON YESTERDAY($6.60)) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 3812 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 3812 EFP CONTRACTS ISSUED, WE HAD A HUGE SIZED GAIN OF 12,743CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

3812 CONTRACTS MOVE TO LONDON AND 10,176 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 39.63 TONNES). ..AND THIS INCREASE OF DEMAND OCCURRED WITH THE GAIN IN PRICE OF $6.60 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAD ZERO PRESENCE OF SPREADING ACCUMULATION IN GOLD ///TODAY/

we had: 106 notice(s) filed upon for 10,600 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $1.05 TODAY//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: ANOTHER DEPOSIT OF 4.40 TONNES OF GOLD INTO THE GLD

INVENTORY RESTS AT 764.10 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 9 CENTS TODAY:

NO CHANGES WITH RESPECT TO SILVER INVENTORY AT THE SILVER SLV:

/INVENTORY RESTS AT 316.775 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A STRONG SIZED 2976 CONTRACTS from 230,580 UP TO 233,556 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JUNE 0 CONTRACTS AND JULY: 1219 CONTRACTS FOR AUGUST: 60, FOR SEPT. 0 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1279 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 2976 CONTRACTS TO THE 1279 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A VERY STRONG GAIN OF 4490 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 21.28MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY AND NOW 1.570 MILLION OZ FOR JUNE.

RESULT: A HUGE SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 11 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A GOOD SIZED 1279 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 28.77 POINTS OR 0.99% //Hang Sang CLOSED DOWN 176.36 POINTS OR 0.65% /The Nikkei closed UP 84.89 POINTS OR 0.40%//Australia’s all ordinaires CLOSED UP .22%

/Chinese yuan (ONSHORE) closed DOWN at 6.9240 /Oil DOWN TO 52.20 dollars per barrel for WTI and 61.30 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9240 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9317 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

Beijing slams Washington to interfering into the extradition bill

(courtesy zerohedge)

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/USA/

This morning the Hong Kong interbank rate soars to a record high of 2.42%. Two reasons for this:

1. they wanted to crush the shorts

2 they want to prevent dollars from leaving their shores.

( zerohedge)

ii)Beijing slams Washington to interfering into the extradition bill

(courtesy zerohedge)

4/EUROPEAN AFFAIRS

i)EUROPE

Not good for global growth in Europe as Apple sales are crushed as Huawei outshines Apple

(zerohedge)

ii) ITALY

(courtesy Tom Luongo)

iii)UK

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)IRAN

The USA releases a ‘smoking gun” showing the Iran’s navy trying to remove mine fragments from the Tanker hull

( zerohedge)

ii)The Japanese owner denies the ship was hit by a mine and instead he claims that the crew saw “flying objects” before the attack..maybe a torpedo?

( zerohedge)

iii)Trump claims that the tanker attack has Iran written all over it..Tehran claims it is a false flag.

(courtesy zerohedge)

iv)Now with all of the above news, Michael Every puts it in proper prospective

v)TURKEY

The Turkish lira slides after Erdogan vows he will retaliate against uSA sanctions after Turkey receives its S 400 defense shield

( zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

A very important commentary on oil from Tom Luongo who correctly points out that our shale boys are bleeding badly. Their cash flows are negative. Thus, as the economy is slowing down, this will put a glut of oil remaining in the USA with no markets. Shale boys cannot discount as their costs are too high. Trump thinks he is winning by exporting oil..think again.

(courtesy Tom Luongo)

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

i)This is a fun story: Martin Armstrong who originally stated that he had no rare gold coins, strangely he is going to court to retrieve those gold coins stolen from his mother’s home. Te bankruptcy court is also involved as they want these rare coins.

(Bloomberg)

ii)I have been highlighting this to you on several occasions: India has been importing a massive amount of silver due to its low price

( Ted Butler/GATA)

iii)Both Schiff and Turk see a chance for gold to finally break the 1350 dollar barrier.

( Kingworldnews.Schiff/Turk/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

a)Market trading/LAST NIGHT/

II)MARKET TRADING

ii)Market data

a)Industrial production rebounds from last month’s decline

(zerohedge)

c)Retail sales recover a bit last month(zerohedge)

iii)USA ECONOMIC/GENERAL STORIES

a)Graham Summers asks: if everything is under control why is the Fed talking about permanent QE and Zirp/Nirp.. Find out why

(courtesy Graham Summers)

b)Wednesday night, saw riots in Memphis after a USA Marshall shot a robber. Thursday witnessed 24 officers wounded in gunfire

SWAMP STORIES

Let us head over to the comex:

Gold withdrawals;

i) We had 0 withdrawal:

.

Gold Breaks Above $1,350, €1,200 and £1,060 – Risk Of War In The Middle East

GoldCore Note

Gold prices jumped another 1% today, surpassing the key $1,350 level for the first time since April last year. Gold made strong gains in all currencies including the euro and the pound, rising above €1,200 and £1,060 per ounce respectively.

Poor economic data from China, the UK, the EU and the United States, and a significant escalation in tensions in the Middle East is seeing an increase in safe haven demand.

Spot gold climbed 1% to $1,356 per ounce by late morning in Europe. It reached its highest level since April 11, 2018 at $1,358.04 in early European trading.

Frequently, gold prices go lower as gold futures get sold in volume as U.S. markets open. However, as the drums of war with Iran bang louder and given the scale of the tensions in the Middle East, gold should see more hedging and safe haven demand today as we head into the weekend.

Gold bullion has gained another 1.2% so far this week and the precious metal is on track for its fourth consecutive weekly gain which bodes well technically.

Silver also gained 1% to $15.05, its highest in a week, while platinum gained 0.7% to $813.08.

Palladium has surged 7% this week and rose another 0.4% to $1,450/oz today. Palladium is on track for its best week in nearly 9 months.

LBMA Gold Prices (USD, GBP & EUR – AM/ PM Fix)

13-Jun-19 1335.80 1335.90, 1054.21 1052.69 & 1182.85 1184.81

12-Jun-19 1336.65 1332.35, 1049.27 1045.76 & 1179.99 1177.26

11-Jun-19 1322.65 1324.30, 1040.53 1041.30 & 1168.96 1170.42

10-Jun-19 1328.60 1328.60, 1046.94 1048.66 & 1175.41 1175.94

07-Jun-19 1334.30 1340.65, 1049.16 1052.14 & 1184.19 1184.60

06-Jun-19 1336.65 1335.50, 1053.15 1051.17 & 1189.62 1185.92

05-Jun-19 1337.75 1335.05, 1052.01 1049.22 & 1185.38 1184.99

04-Jun-19 1323.60 1324.25, 1045.51 1043.77 & 1177.47 1177.26

03-Jun-19 1313.95 1317.10, 1039.47 1042.35 & 1175.99 1175.38

News and Commentary

Gold Extends Advance to Third Straight Session on Fed Rate-cut View, Geopolitical Ripples

Gold Gains as Fed Rate Cut Expectations Provide Support

European Stocks Trade Lower Amid Middle East Tensions

Tanker Attacks Reignite Oil Fear Premium, Prices Could Spike to $80

U.S. Weekly Jobless Claims Rise; Imported Inflation Subdued

JEFFREY GUNDLACH : ‘I Am Certainly Long Gold’

Beijing May Face Consequences if Chinese President Refuses to Meet With Trump at G-20 Threatens Kudlow

The Fed Has No Choice But to Return to Ultra-Low Interest Rates

With Tariffs Trump is Destroying Dollar and U.S. Power – Salinas Price

A Morgan Stanley Economic Indicator Just Suffered a Record Collapse

end

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

This is a fun story: Martin Armstrong who originally stated that he had no rare gold coins, strangely he is going to court to retrieve those gold coins stolen from his mother’s home. Te bankruptcy court is also involved as they want these rare coins.

(Bloomberg)

Cult economist jailed for hiding rare coins says they’re his now

Submitted by cpowell on Thu, 2019-06-13 18:04. Section: Daily Dispatches

By Chris Dolmetsch and David Glovin

Bloomberg News

Thursday, June 13, 2019

The 58 rare coins at the center of two federal lawsuits are exceptionally valuable.

Now a bankrupt company’s receiver wants them.

An antique dealer wants them.

…

And so does Martin Armstrong, a self-taught economist with a cult following who spent years behind bars for what the U.S. said was a $700 million Ponzi scheme and for allegedly hiding assets, including what may be those very same coins.

Armstrong’s story is one of Wall Street’s more bizarre tales — and the newest chapter makes it even more absurd. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-06-13/cult-economist-jailed…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

I have been highlighting this to you on several occasions: India has been importing a massive amount of silver due to its low price

(courtesy Ted Butler/GATA)

Ted Butler: India provides more evidence of silver price manipulation

Submitted by cpowell on Fri, 2019-06-14 01:10. Section: Daily Dispatches

9p ET Thursday, June 13, 2019

Dear Friend of GATA and Gold:

Increasing demand for silver in India, silver market analyst Ted Butler writes today, is more evidence of price suppression and market manipulation in the West. For Indians are extremely price-sensitive about their monetary metals, Butler notes, and they wouldn’t be increasing their purchases of silver if they didn’t recognize that it is very underpriced now compared to gold.

Butler’s commentary is headlined “India Reacts to Depressed Silver Prices” and it’s posted at GoldSeek’s companion site, SilverSeek, here:

http://silverseek.com/commentary/india-reacts-depressed-silver-prices-17…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

India Reacts to Depressed Silver Prices

|

June 13, 2019 – 9:28am

Several recent articles have highlighted a surge of silver imports to India, prompting me to take a closer look. India has always been a big buyer of silver and gold, befitting the traditions and culture of the country with the world’s second largest population. The population of India, more than 1.3 billion citizens, is now only about 50 million less than that of China. Combined, both countries make up 35% of the total world population (7.7 billion) and have always been large buyers and holders of gold and silver. Together, India and China absorb close to 50% of total world gold and silver mine production.

One big difference between India and China is that the gold and silver buying in India is largely a grassroots phenomenon, emanating from the general population due to deep-rooted customs and traditions; where the buying from China is predominantly from official sources (similar to the gold buying by Russia). To me, this makes the gold and silver buying from India more “free market” and price-sensitive in nature because the more participants in any market, the freer the market is by definition. The many tens and even hundreds of millions of gold and silver buyers from India make the markets there the freest of all.

India has always played a vital role in gold and silver. I remember how my longtime friend and silver mentor, Izzy Friedman, more than 40 years ago, as he was deciding whether to make a major investment in silver in the mid-1970’s, actually flew to India to see for himself if the stories of great silver hoards about to flood the market should prices move higher (from $4 or $5) were true. Izzy saw plenty of silver, but none so closely held in large concentrated quantities to pose a market threat. I believe that’s still the case today.

Indian gold and silver buyers are quite price-sensitive and unlike the typical buyer in the West, Indians tend to buy more when prices are low and less when prices are high. Gold and silver flows into India are one-way affairs – what flows in stays there, never to leave the sub-continent. Gold prices are closer to the highest they have been over the past 5 or 6 years, while silver prices are closer to the lowest they have been over that period, resulting in the silver/gold price ratio widening out to the highest it has been in 25 years. I reviewed the import data from India over the past 15 years with that in mind. For silver, I relied on the Silver Institute’s World Survey and for gold, a straight Google search for Indian imports from 2004 to 2018.

Here’s what I found. The people of India, according to the import data, are buying more silver relative to gold than ever before. It’s not that gold imports are down sharply, it’s much more that silver imports are up sharply. I broke the data from the past 15 years into two segments – the 9 years from 2004 to 2012 and the six years from 2013 to 2018. As a reminder, by comparing the imports of gold and silver on a per ounce basis, all outside influences are neutralized, like currency and overall economic conditions. For instance, the great Indian demonetization of 2016, resulted in sharp declines in the imports of both gold and silver. That’s the objective beauty of making like-kind comparisons – it filters out peripheral issues.

For the 9 years 2004 to 2012, the silver/gold price ratio averaged 56 to 1 and India imported an average of 26.5 million ounces of gold and 85 million ounces of silver each year – or 3.2 times more ounces of silver than gold. Over the next 6 years 2013 to 2018, the silver/gold price ratio widened out to 73 to 1, with silver getting progressively cheaper relative to gold (except in 2016). Over the most recent six years, gold imports fell slightly to an average annual 25.2 million oz, while silver imports surged to 188 million oz annually, up 120% over the yearly average of the prior 9 years. Where imports of silver compared to gold in ounces were 3.2 times from 2004 to 2012, they jumped to 7.5 times from 2013 to 2018.

In the most recent full year of import data, 2018, India imported 24.4 million ounces of gold, the second lowest amount in 9 years, while silver imports were 224 million ounces, the second highest total in 15 years. The amount of silver ounces imported to India last year was more than 9 times the amount of gold imported, the highest level ever. The average silver/gold price ratio for 2018 was 82 to 1, the cheapest silver had been to gold in 15 years, so it’s not surprising that Indian buyers reacted as they did. Of course, while full year data is not available for 2019, the silver/gold price ratio has averaged 86 to 1 year to date, with very recent readings of 90 to 1.

Considering that the silver/gold price ratio has continued to widen out since 2018, exceeding 90 to 1, making silver even cheaper compared to gold, there is every reason to expect that India’s imports of silver have continued to grow, both on an absolute and relative basis compared to gold. What this means, aside from confirming the price-sensitivity (and good sense) of the Indian buyer, is that prices do have consequences. It’s often said that the cure for low prices is low prices because low prices discourage production and encourage demand. The record of India’s silver imports would seem to be clear confirmation of that.

The main price consequence of the surge in silver imports to India is as a direct result of the COMEX price suppression and manipulation of the price. The collective investment reaction in the US and West to the low price of silver (or any investment asset) is not to buy – that’s our investment culture, for better or worse. The collective reaction in India is markedly different and in a very real sense is the ultimate confirmation that silver prices have been manipulated; as what else could prove more conclusively that silver prices were artificially suppressed than the surge in demand from India?

In fact, had there been no surge in demand from India, that would be proof silver wasn’t manipulated in price. What else could possibly explain the surge in silver demand from tens of millions of Indian buyers if not that they felt prices were depressed – not just on an absolute basis, but relative to gold as well? I’m not suggesting that the many millions of Indian buyers are at all aware of the COMEX price manipulation; they just know that silver is unusually cheap and undervalued relative to gold.

So here we have compelling new proof that silver prices have been manipulated – not that more proof was needed. By depressing the price of silver, JPMorgan may have succeeded in discouraging western investment demand and cornering the physical market for its own accumulation, but has also inadvertently stimulated Indian demand. As a result, a brand new Catch-22 has emerged in silver. As and when JPMorgan decides to let silver prices fly to the upside, it is reasonable to assume that Indian demand would fall off, but as that demand falls off, the higher prices will jumpstart western demand. If the right hand doesn’t get you, then the left hand will. Should JPM choose to prolong the silver price suppression, the imports to India should continue to surge and with the concurrent decline in world silver mine production, a physical crunch becomes inevitable. Prices do have consequences.

Ted Butler

June 13, 2019

END

Both Schiff and Turk see a chance for gold to finally break the 1350 dollar barrier.

(courtesy Kingworldnews.Schiff/Turk/GATA)

At KWN, Schiff and Turk see chance for gold to break out

Submitted by cpowell on Fri, 2019-06-14 01:19. Section: Daily Dispatches

9:19p ET Thursday, June 13, 2019

Dear Friend of GATA and Gold:

King World News tonight publishes comments about the gold market from fund manager Peter Schiff and GoldMoney founder James Turk.

Schiff says: “The Fed’s balance sheet ticked up last week to $3.85 trillion. Perhaps it has already seen its lows. When the Fed goes back to quantitative easing, the balance sheet will balloon to $10 trillion even quicker than it did to $4.5 trillion. But next time the Fed’s exit-strategy bluff won’t work. Got gold?”

…

Turk says gold’s price likely will be capped next week because there is a meeting of the Federal Reserve’s Open Market Committee. But he adds, “There is a lot of money on the sidelines waiting to buy dips” and “the momentum guys are not even in there buying yet.”

The KWN report is headlined “Peter Schiff and James Turk — Possibility of a Major Breakout in the Gold Market” and it’s posted here:

https://kingworldnews.com/peter-schiff-and-james-turk-possibility-of-a-m…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

This morning, Ronan Manly reports that gold has broken records in multiple currencies, including the gold in Br. pounds and Cdn dollar

(courtesy Ronan Manly/Bullion star)

Ronan Manly: Gold price breakout in multiple currencies

Submitted by cpowell on Fri, 2019-06-14 02:19. Section: Daily Dispatches

10:10p ET Thursday, June 13, 2019

Dear

Friend of GATA and Gold:

Bullion Star’s Ronan Manly reports tonight that gold is performing spectacularly in many developed-nation currencies, including the euro, British pound, Australian dollar, Singapore dollar, and Swedish krona, and seems to be climbing steadily by the measure of its last obstacle, the U.S. dollar.

… Manly writes: “Only time will tell, but if the U.S. dollar gold price continues to take out ‘resistance’ and more up through the technically important area between $1,350 and $1,370, and then above $1,370, this would bring U.S. dollar gold to a three-year high. Thirty dollars or so above the $1,370 level would put gold at a five-year high above $1,400 and would bring in a lot of attention from the sidelines.”

As well, presumably, as a lot of attention from the U.S. Treasury Department, the Federal Reserve, the Bank for International Settlements, the People’s Bank of China, and the Central Bank of the Russian Federation. Where do they want the U.S. dollar gold price to go, and what will they do to push it there?

You can count on one thing: Mainstream financial news organizations will never ask.

Manly’s analysis is headlined “Gold Price Breakout in Multiple Currencies” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/gold-price-breakout-in-mul…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

end

* * *

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.9240/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.9317 /shanghai bourse CLOSED DOWN 28.77 POINTS OR 0.99%

HANG SANG CLOSED DOWN 176.36 POINTS OR 0.65%

2. Nikkei closed UP 84.89 POINTS OR 0.40%

3. Europe stocks OPENED ALL RED/

USA dollar index DOWN TO 97.15/Euro FALLS TO 1.1262

3b Japan 10 year bond yield: FALLS TO. –.13/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.23/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 52.85 and Brent: 62.24

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.26%/Italian 10 yr bond yield UP to 2.29% /SPAIN 10 YR BOND YIELD DOWN TO 0.49%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.55: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 2.70

3k Gold at $1354.00 silver at: 15.05 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 24/100 in roubles/dollar) 64.32

3m oil into the 52 dollar handle for WTI and 61 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.23 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9954 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1210 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.26%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.07% early this morning. Thirty year rate at 2.58%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.8917..

“Sea Of Red”: Global Stocks Tumble After Dismal Chinese Data, Broadcom Bust

Risk on, risk off.

One day after traders were greeted by a sea of green – on potential world war news – we are back to the sea of red as global stocks struggled and safe haven bets were back in play on Friday with German bond yields plumbing record lows after the latest dismal Chinese data dump sparked fears about the health of the global economy and concerns of a new U.S.-Iran confrontation intensified (which, by the way, was somehow bullish for risk yesterday).

Beijing May activity reported overnight was very weak and painted a fairly gloomy picture of the world’s second largest economy as the trade war with the United States starts to bite. May industrial output growth slowed to a more than 17-year low, the weakest since since 2002, and well below expectations, while fixed-asset investment also fell short of forecasts. Retail sales growth accelerated and surprised to the upside however.

The full breakdown:

- Industrial Output for May: 5.0%, est. +5.4% (range +5.1% to +6.4%, 35 economists), down from +5.4% last month.

- May retail sales +8.6% y/y; est. +8.1% April +7.2%

- Jan.-May fixed-asset investment excluding rural households +5.6% y/y; est. +6.1% (range +5.2% to +6.5%, 34 economists). Jan.-April +6.1%

Commenting on the data, Goldman said “May activity growth was very weak” noting that IP month-over-month annualized growth was around 2.6% based on our seasonal adjustment, which was higher than April but still at a weak level. The shifting Labor Day holiday distorted IP, and to a lesser extent FAI, data on the downside, but the impacts were limited as there was a difference of only one vacation day which could not fully explain the extent of the data weakness. The impacts of shifting holidays tend to be larger on retail sales data. April retail sales data was exceptionally weak and the reversal of the distortion was the main driver of the rebound in retail sales in May. The slowdown in property transactions year-over-year growth was partially due to an unfavorable base effect, but sequentially transactions also cooled in April-May as the government marginally tightened property policies in a few cities such as Changsha, Xi’an, Beijing etc.

As a result, expectations for more stimulus in China continue to grow as the Sino-U.S. trade dispute threatens to escalate into a full-blown trade war that many fear could push the global economy into recession.

“The Chinese data was disappointing, especially the industrial output numbers,” said Chris Scicluna, head of economic research at Daiwa Capital Markets. “That’s given bond markets additional momentum.”

The dismal Chinese data saw yields on German 10-year Bunds — one of the safest assets in the world — fall to fresh record lows, the yield dropping as low as -0.27%.

U.S. Treasury yields were also grinding lower, last seen just above 2.06%, the same level they hit one week ago when the dismal jobs print virtually assured a rate cut by the Fed. Safe-haven bond yields have already fallen in recent days amid rising speculation about monetary easing by major central banks. Meanwhile, Spain bond yields have fallen for the first time below 0.5%.

Speaking of Europe, the Stoxx 600 Index fell as much as 0.8%, hitting a session low, with 18 out of 19 sectors dropping, led lower by tech and banks. The Tech sector index was biggest drag on the Stoxx 600, down 1.9%, on contagion from U.S. chip giant Broadcom, which cut guidance and warned of a slowdown in demand due to trade tensions and the U.S. ban on Chinese tech and mobile phone company Huawei Technologies. European tech shares led the indexes lower, with semiconductor companies Infineon, AMS, STMicroelectronics, Siltronic and Dialog Semiconductor all dropping between 2%-3% after Broadcom outlined the impact of a total halt in sales to Huawei.

“The sales warning from Broadcom is also weighing on markets this morning as it suggests that both semiconductor and auto sectors are under pressure worldwide,” said Market Securities strategist Christophe Barraud in Paris, adding that expectations for a rebound were now shifting from the second half of this year to 2020. “Given both these sectors are key for world trade, it’s not good news for trade.”

The Stoxx banks index slumped 1.1% as European curves continue to flatten; defensive utilities sector is the only sector that posts gains, up 0.3%

Earlier in the session, Asian stocks swung between gains and losses, with markets in the region mixed. While Japan’s Topix Index gained 0.3%, shares in Hong Kong and China dropped. In its third-day of losses, the Hang Sang Index fell another 0.7% as calls increased for the city’s leader to delay an extradition bill. China was the the region’s worst-performer, with the benchmark Shanghai Composite falling 1% after the above mentioned ugly economic data dump hit overnight. India’s S&P BSE Sensex Index declined 0.5% amid cash-crunch woes.

Over in the US, index futures were in line for a lower open, with the S&P e-mini pointing to a 0.2% fall.

With the week ending, all eyes now turn to the Fed’s June 18-19 meeting which will show investors if the U.S. central bank’s monetary policy stance matches market expectations for a near-term rate cut. A Reuters poll showed a growing number of economists expect the Fed to cut interest rates this year although the majority still expect it to stay on hold.

“There is a large degree of uncertainty going into next week’s FOMC (Federal Reserve Open Committee) meeting as market reaction will differ significantly depending on whether the Fed hints toward easing policy,” said Shusuke Yamada, chief Japan FX and equity strategist at Bank Of America Merrill Lynch. “A wait-and-see mood is likely to begin prevailing in the markets ahead of the FOMC.”

Elsewhere, growing worries about a new U.S.-Iranian confrontation after two attacks on two oil tankers in the Gulf of Oman on Thursday added to the unhappy mood, resulting in an oil price surge. Washington blamed Iran, but Tehran bluntly denied the allegation. But U.S. and European security officials as well as regional analysts left open the possibility that Iranian proxies, or someone else entirely, might have been responsible. The attacks set crude prices on a roller coaster ride, with Brent futures slipping 0.2% to $61.18 per barrel. Brent surged 2.3% on Thursday after the Norwegian- and Japanese-owned tankers both experienced explosions.

In the latest development, the US Navy Destroyer USS Mason was en route to the area where the 2 oil tankers were attacked, while it added it has no interest in engaging in new conflict in the Middle East and that it is ready to defend US interests as well as freedom of navigation. Furthermore, the US released video footage of Iranian military removing an unexploded mine from the Japanese tanker that was attacked in the Gulf of Oman. Iran categorically rejected the US unfounded claim regarding tanker attacks according to Iranian mission to the UN, while there were also comments from Iran Foreign Minister Zarif that US allegations against Iran without evidence shows the B team is moving to Plan B of sabotaging diplomacy.

In FX, the safe haven yen advanced after data showed China industrial output slowed in May to its weakest pace since 2002. The dollar’s index against a basket of six major currencies was little changed initially, but spiked to session highs after China warned the US not to get involved in Hong Kong matters. The Swedish krona led gains in the Group-of-10 currencies after Swedish inflation rose faster than expected, while the euro stayed close to $1.13 where hefty expiries rollover Friday. The euro was steady at $1.1282 while the greenback inched down 0.2% to 108.19 yen. The Australian and New Zealand dollars fell on Friday as bets on interest rate cuts undermined demand and Group of 20 meeting later this month sidelined investors.

Expected data include retail sales, industrial production and University of Michigan Consumer Sentiment Index. No major company is scheduled to report earnings.

Market Snapshot

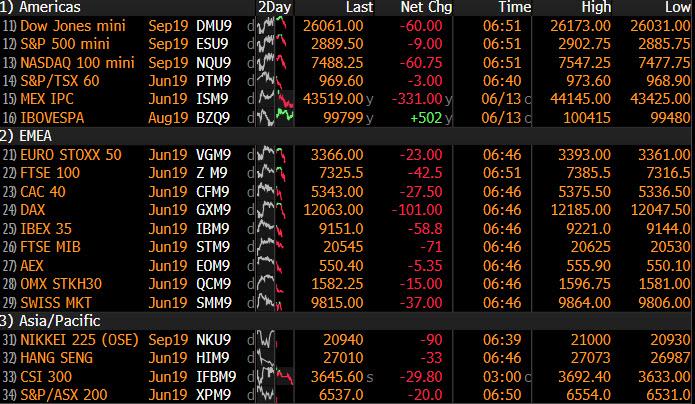

- S&P 500 futures down 0.3% to 2,891.25

- STOXX Europe 600 down 0.5% to 378.55

- MXAP down 0.07% to 155.50

- MXAPJ down 0.5% to 507.16

- Nikkei up 0.4% to 21,116.89

- Topix up 0.3% to 1,546.71

- Hang Seng Index down 0.7% to 27,118.35

- Shanghai Composite down 1% to 2,881.97

- Sensex down 0.5% to 39,551.96

- Australia S&P/ASX 200 up 0.2% to 6,554.00

- Kospi down 0.4% to 2,095.41

- German 10Y yield fell 2.1 bps to -0.262%

- Euro up 0.04% to $1.1280

- Italian 10Y yield fell 7.6 bps to 1.989%

- Spanish 10Y yield fell 4.6 bps to 0.497%

- Brent futures down 0.2% to $61.22/bbl

- Gold spot up 0.8% to $1,352.75

- U.S. Dollar Index up 0.1% to 97.13

Top Overnight News from Bloomberg

- President Donald Trump is still waiting for a response from Chinese President Xi Jinping about meeting to restart trade talks, economic adviser Larry Kudlow said while warning Beijing may face consequences it if refuses the invitation

- The Trump administration blamed Iran for attacks on two oil tankers near the entrance to the Persian Gulf, escalating tensions between the two rivals despite denials from officials in Tehran and a lack of public evidence for the U.S. claim. U.S. releases video it says is of Iran removing mine from ship

- Rivals to be Britain’s next prime minister are holding private talks over joining forces in an attempt to stop the pro-Brexit favorite, Boris Johnson, running away with the contest, people familiar with the matter said

- China’s industrial output growth slowed to the weakest pace since 2002, highlighting the headwinds the economy is facing as it grapples with the tariff war with the U.S.

- Hong Kong girded for another mass march against a China- backed extradition bill Sunday, as the city’s leader, Carrie Lam, faced new calls to withdraw the legislation after clashes between protesters and police

- Allies of Hong Kong leader Carrie Lam began questioning her tactics as lingering tensions prompted lawmakers to postpone debate on a controversial extradition bill until at least next week

- White House Press Secretary Sarah Huckabee Sanders is leaving the Trump administration after a turbulent tenure marked by attacks on the media, dissemination of false information and the near-disappearance of the daily press briefing

Asia equity markets traded mixed as they awaited Chinese Industrial Production and Retail Sales data, where retails sales beat on expectations, nevertheless Asia-Pac indices remained mixed as risk-off sentiment prevailed. ASX 200 (+0.2%) was lifted by strength in commodity-related stocks but with gains capped due to weakness in the largest weighted financials sector amid anticipation of a lower rate environment and with AMP shares heavily pressured after it received compliance orders from the financial regulator APRA. Nikkei 225 (+0.4%) was also underpinned by the mining sectors which saw Chiyoda as the biggest gainer, while Sony shares were also bolstered after activist investor Loeb called on the Co. to spin off its semiconductor business. Elsewhere, Hang Seng (-0.7%) was subdued and Shanghai Comp. (-1.0%) was indecisive amid trade uncertainty and after the PBoC’s efforts resulted to a net weekly injection of CNY 65bln vs. last week’s CNY 320bln net drain. Finally, 10yr JGBs followed suit to the recent upside in T-notes, while the BoJ was also present in the market with today’s Rinban operation heavily concentrated in the belly of the curve.

Top Asian News

- Indonesia on Alert as Court Hears Prabowo’s Election Challenge

- As Trade War Hits, China Factories See Slowest Growth Since 2002

- Japan Display Is Likely to Miss Friday Deadline for Bailout

- Turkey Work Underway to Counter U.S. Sanctions, Official Says

Major European indices are mostly lower [Eurostoxx 50 -0.4%], with the exception of the SMI (+0.2%), as the region temporarily side-lines the prospect of Fed rate cuts and succumb to the risk-off sentiment as a result of rising US tensions with China, Russia, Germany, Iran, Turkey and India. Sectors are largely in the red with defensive stocks faring better, gains in the healthcare sector are keeping the SMI afloat. Meanwhile, IT names plumbed the depths with the sector heavily underperforming after a warning from Broadcom regarding a slowdown in global chip demand. As such, Infineon (-5.1%), STMicroelectronics (-4.0%), Dialog Semiconductor (-3.1%), ASML (-3.0%) and ASM (-2.7%) are all near the foot of the Stoxx 600. On the flipside, Scor (+2.6%) and Royal Mail (+2.0%) are in positive territory amid positive broker moves.

Top European News

- Kier Tumbles After Report Some Credit Insurers Withdraw Cover

- Buffett’s Berkshire, Engie Drive Europe’s Bond Sales Bonanza

- Finance Chiefs Agree on Euro-Area Budget But Skirt Funding

- Spain’s Sabadell Is Said to Weigh Sale of Consumer Finance Unit

In FX, the Dollar index continues respect resistance above the psychological 97.000 level (on a closing basis) and ahead of the recent range top at 97.370, as safer currency havens outperform amidst heightened geopolitical and global trade tensions. Moreover, the Dollar remains capped by growing expectations that the Fed will flag a rate cut next week following a run of macro data pointing to a more pronounced slowdown in the economy and benign inflation that that challenges the transitory theory put forward by Powell and other at the last FOMC gathering. On that note, impending retail sales and ip reports could cement an ease in July if not this month. DXY currently relatively contained within a 97.154-96.942 range.

- JPY/SEK – The Yen has nudged back up towards 108.00 vs the Buck, and is only really lagging behind Gold in the aforementioned risk-off climate plus the Swedish Krona in the G10 stakes due to firmer than forecast CPI and CPIF metrics that keeps the Riksbank on track to raise the repo. However, Usd/Jpy is still encountering underlying bids ahead of the big figure and may also be propped by decent option expiry interest between 108.00 and 108.15 (1 bn). Back to Scandinavia, Eur/Sek has extended post-inflation data declines through technical support at 10.6500 (10 DMA) and briefly below 10.6400 vs 10.7100+ at one stage.

- NZD/AUD – The major losers yet again, and with the Kiwi now underperforming after NZ manufacturing PMI only just held above the 50.0 threshold. Nzd/Usd has slipped under 0.6550 towards 0.6525 and Aud/Nzd is pivoting 1.0550 even though the Aussie has relinquished the 0.6900 handle and chart support a pip below amidst another round of more aggressive RBA policy easing calls (NAB now predicting 3 cuts in 2019 from 2 previously and RBC reckons the OCR will be lowered to 0.5% by May next year).

- EUR/CAD/CHF/GBP – All lower against the Greenback as well, albeit to a lesser extent compared to the Antipodean Dollars and to varying degrees. The single currency is retreating further from 1.1300 where massive expiries run off (4.4 bn) and the Loonie has reversed to test support ahead of 1.3350 having lost some of Thursday’s oil-powered momentum as crude prices simmer down after the post-tanker attack spike. Meanwhile, the Franc has pared gains across the board with Usd/Chf at the upper end of a 0.9966-26 band and Eur/Chf back above 1.1200 on SNB reflection (renewed and reemphasised convictions to keep NIRP or even cut deeper and continue intervention). Elsewhere, Cable has is now pivoting 1.2650 with independent bearish impulses from the ongoing UK political hiatus and resultant suspension of any real Brexit developments, but BoE Governor Carney may provide some additional impetus later.

- EM – No respite for the Lira it seems as Usd/Try rallies through 5.9000 to 5.9300+ and not far from chart resistance around 5.9500, including a 50% Fib of the retracement from last month’s highs to earlier June lows. The latest catalyst, warnings from Turkey’s Foreign Ministry that any US sanctions will be reciprocated.

The energy complex is poised for a weekly loss as the two tanker attacks off the coast of Oman only provided brief reprieve for the declining prices, with trade woes and rising US supply outweighing concerns in the Middle East. This morning also saw the release of the IEA monthly report in which the agency cut their outlook on oil demand growth by 100k BPD, which is in-fitting with the OPEC (70k BPD) and EIA (160k BPD) downgrades to oil demand growth for 2019 released earlier in the week. The report also noted that OPEC supply in May fell to the lowest since 2014 due to Iranian sanctions, in which Iranian oil production fell to the lowest since the 1980s. WTI and Brent are lower on the day and currently pressured by the continuation of the risk aversion. Elsewhere, gold has continued to advance as the yellow metal benefits from the risk-off sentiment, with prices now above the key USD 1350/oz ahead of strong trend-line resistance at USD 1358.50/oz. The rally in gold has spilled into other precious metals with silver hitting one-week highs and platinum gaining almost 1%. In terms of base metals, copper remains subdued amid the broad risk tone whilst Dalian iron ore touched new record highs as Chinese steel mills kept demand steady for the metal

US Event Calendaar

- 8:30am: Retail Sales Advance MoM, est. 0.6%, prior -0.2%; Retail Sales Ex Auto and Gas, est. 0.4%, prior -0.2%

- 9:15am: Industrial Production MoM, est. 0.2%, prior -0.5%; Manufacturing (SIC) Production, est. 0.1%, prior -0.5%

- 10am: U. of Mich. Sentiment, est. 98, prior 100; Current Conditions, est. 109, prior 110; Expectations, est. 92, prior 93.5

- 10am: Business Inventories, est. 0.5%, prior 0.0%

DB’s Jim Reid concludes the overnight wrap

Bloomberg have a competition on their terminals to predict every match in the Cricket World Cup. Unbeknown to me, my co-authors Craig and Quinn entered. I didn’t realise it was on until too late. Craig, like myself, is a cricket fan. Quinn is an American who knows nothing about cricket and a week or so ago made himself a laughing stock on our team by predicting that around half the games in this tournament would be ties. For those not familiar with one day cricket, a tie probably occurs every several hundred games. However two weeks into the tournament Quinn is near the top of the leaderboard as what we didn’t appreciate is that many of the games he marked as a tie would be rained off and giving him technically the correct answer. He has therefore had an uncanny knack of predicting our awful weather this past week. So for those that want a UK weather forecast, please have your umbrella to hand between these dates as Quinn has predicted another series of ties around then: June 22-26.

Predicting the daily swing in oil prices is proving to be one of the main challenges in markets at the moment. Indeed one day after Brent dipped -3.72% and to a five-month low, it recovered much of these losses in a single swing yesterday after bouncing back +2.37%. The catalyst was the attacks on tankers in the Gulf of Oman, the second attack in a month near the Strait of Hormuz chokepoint, which has led to fears that accelerated hostilities in the region are to return. The US Secretary of State blamed Iran for the attacks, in comments that President Trump subsequently retweeted, and overnight the US released a video demonstrating Iran’s involvement, saying an Iranian boat removed an unexploded mine from a US ship. US officials also suggested that a military response has not been ruled out. Separately, data from the US Energy Information Administration showed that in March, the US imported the lowest amount of crude oil from OPEC countries since March 1986, continuing a decade-long trend of lower US crude oil imports from the OPEC countries.

Unsurprisingly anything linked to oil benefited yesterday. The S&P energy sector rose +1.25% which carried the S&P 500 to a +0.41% gain, while the NASDAQ and DOW closed +0.57% and +0.39% respectively. The STOXX 600 finished +0.16%, with the DAX outperforming (+0.44%). Despite the geopolitical noise, the VIX traded fairly flat at 15.75. Interestingly, govies were actually better bid too with 2y and 10y Treasuries ending -4.7bps and -3.0bps lower respectively, sending the former to its lowest level since December 2017. So the simultaneous equity and rates rally was back in full force. In Europe 10y Bund (-0.5bps) and OAT (-0.2bps) yields edged lower, but the real action was in the periphery. Spanish 10y yields slid -3.1bps to a new all-time low of 0.537%, while BTPs rallied -7.7bps following strong demand at the 20-year auction. The latter move came despite increased political tension in Italy, where Deputy PM Salvini reportedly told his supporters to “be ready” for a possible early election.

One of the drivers for the rally in European bonds has been expectations for more accommodative policy from the ECB. DB’s Mark Wall has updated his forecasts in this note to reflect the latest macro information and the recent update to DB’s Fed call. In short, two trends are developing in ways that will push the ECB toward easing: escalation in the trade wars and a change in the relative monetary policy stance now that the Fed looks likely to cut rates this year. Mark now expects the ECB to cut its deposit facility rate at the September meeting, and anticipates 2020 growth to decelerate to 1.0% as a result of the anticipated slowdown in US growth. Similarly, DB’s China team has revised down their 2019 and 2020 growth forecasts by 0.1 and 0.2pp respectively, to 6.2% and 5.8%, also mostly as a function of lower expected US growth. If the trade war evolves as we expect, the PBoC is likely to ease rates policy and allow the yuan to weaken to as far as 7.3 versus the dollar. Zhiwei’s full China update is available here .

This morning in Asia equity markets are mostly trading lower. Although Japanese markets have pared back opening losses to trade higher, with the Nikkei +0.29%, elsewhere the story is less positive. The Hang Seng (-0.57%) is currently on track for a third consecutive move lower, while the Shanghai Comp (-0.26%) and the Kospi (-0.25%) have also lost ground. We should note that we’re still due to get China’s May activity indicators data. Bloomberg suggests that the data is out at 8am BST. For what it’s worth, fixed asset investment and industrial production are both expected to hold steady, however retail sales is expected to rise in year over year terms. This will probably dictate much of today’s mood. The other breaking news overnight that we’re just seeing is the AFP news agency reporting that French finance minister Le Maire has said that EU ministers have agreed to President Macron’s proposal for a Eurozone budget, although with no other information at present the question for markets will be how substantive this agreement actually is. President Macron has been previously disappointed by the reluctance of a number of northern European countries to set up a Eurozone budget as large as he’d like.

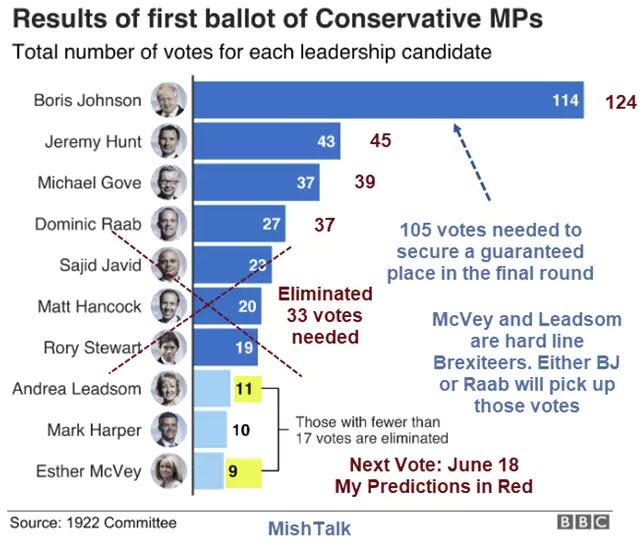

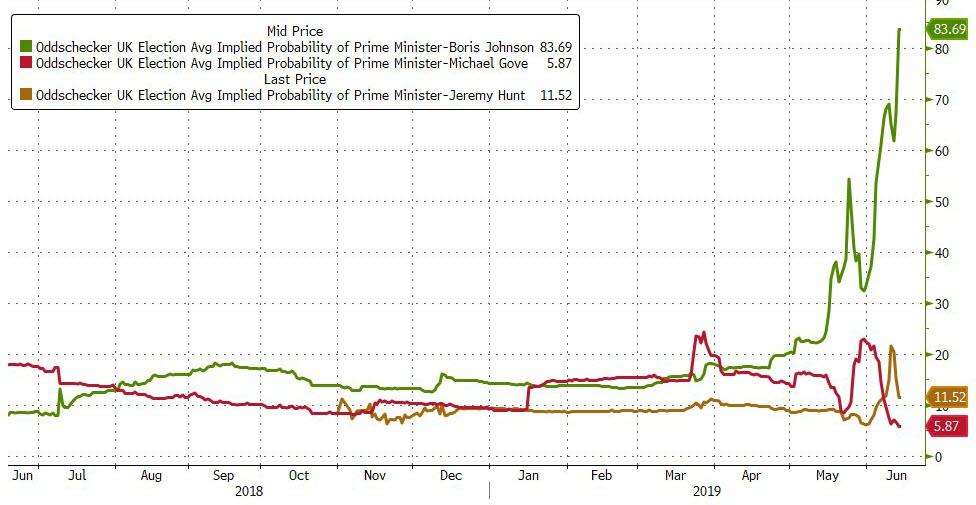

Back to yesterday and while there wasn’t a great deal of other news to digest for markets, we did have the first Conservative Party leadership contest which revealed overwhelming support for Boris Johnson in his bid to become the next PM. He took 114 votes with Jeremy Hunt a reasonable way back in second place at 43 votes. Gove, Raab, Javid, Hancock and Stewart all made it through to the next round which is due to take place next Tuesday, and where candidates will need to secure 33 votes (10% of the total). Brexiteers Leadsom and McVey were eliminated yesterday along with Harper. The BBC’s political editor Laura Kuenssberg tweeted last night that Health Secretary Hancock was “mulling over” whether to continue in the race, having come in 6th place with 20 votes. It’s clear from the first round that Johnson is the clear frontrunner and although history tells you frontrunners often don’t win the Tory leadership race it’s hard to see him being toppled outside of an “event” that derails his campaign. Sterling bounced a bit following the results before closing a touch weaker at -0.10%.

In US politics, no developments were immediately market-moving, but the White House did say that “we’re moving in that direction” with regards to a Trump-Xi meeting at the G20. Top economic advisor Larry Kudlow said that “President Trump has indicated his strong desire for a meeting (…) if the meeting doesn’t come to bear, there may be consequences.” So that event, set to start two weeks from today, will be key. Away from the China conflict, the passage of the USMCA deal (to replace NAFTA) still looks precarious, as Canadian Foreign Minister Freeland said that talks are “on the right track” but stopped short of giving a timeline for ratification.

As for the data, in the US the latest weekly claims reading ticked up to 222k and a little more than expected to a five-week high. The import price index meanwhile declined more than expected in May, by -0.3% mom at both the headline and core level. Previous dollar strength appeared to explain much of the weakness in non-petrol prices.

Prior to this, in Germany there were no final surprises in the May CPI report where the headline reading was confirmed at +0.3% mom and +1.3% yoy. Elsewhere, industrial production for the Euro Area in April was confirmed as declining -0.5% mom, as expected.

To the day ahead now, where this morning we’ll get the final May CPI revisions for France and Italy. Bisecting that data is the China May activity indicators while in the US this afternoon the main highlight should be the May retail sales report, while May industrial production, April business inventories and the preliminary June University of Michigan consumer sentiment survey are also due. Away from that we’re due to hear from the BoE’s Carney this afternoon.

3. ASIAN AFFAIRS

I)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 28.77 POINTS OR 0.99% //Hang Sang CLOSED DOWN 176.36 POINTS OR 0.65% /The Nikkei closed UP 84.89 POINTS OR 0.40%//Australia’s all ordinaires CLOSED UP .22%

/Chinese yuan (ONSHORE) closed DOWN at 6.9240 /Oil DOWN TO 52.20 dollars per barrel for WTI and 61.30 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9240 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9317 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

China/HONG KONG/

This morning the Hong Kong interbank rate soars to a record high of 2.42%. Two reasons for this:

1. they wanted to crush the shorts

2 they want to prevent dollars from leaving their shores.

(courtesy zerohedge)

4/EUROPEAN AFFAIRS

i)EUROPE

Not good for global growth in Europe as Apple sales are crushed as Huawei outshines Apple

(courtesy zerohedgE)

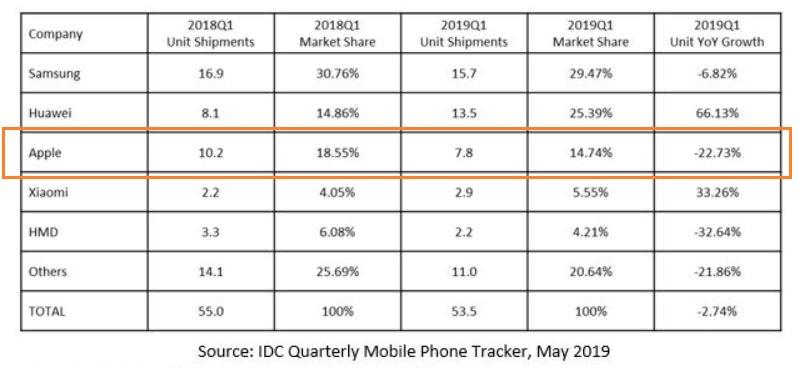

Apple Smartphone Sales Crash In Europe As Huawei Outshines Competition

A new report from the International Data Corporation’s (IDC) latest Quarterly Mobile Phone Tracker shows Chinese smartphone makers are solidly outperforming Apple and Samsung across European markets.

Huawei and Xiaomi, two of China’s top smartphone producers, recorded YoY unit sale increases for all regions across Europe in 1Q19, while all other major smartphone companies experienced declines.

Huawei’s unit shipment in Europe jumped 66% YoY in 1Q19, while Xiaomi increased 33% YoY. During the same period, Samsung’s unit shipments dropped 7%, while Apple’s unit sales plummeted by 23%.

“In brands, Huawei continued to make incremental advances, and so did Xiaomi, while Apple had a tough quarter, with its 23% market share across Europe the lowest Q1 result in five years,” said Marta Pinto, research manager at IDC EMEA.

“The market has been changing in the last few quarters in relatively predictable ways,” said Pinto. “Shipments have slowed as consumers hold on to devices for longer, Apple has been challenged with its latest devices, and Chinese manufacturers have been making strides each quarter.”

Simon Baker, program director at IDC EMEA, said, “Europe has been a global focus of vendor concentration in recent quarters, with some of the smaller players under a lot of pressure. Looking ahead, it is no longer possible to see clear trends as before. The blacklisting of Huawei in the U.S. on May 16 is creating so many unknowns, and uncertainty is the new keyword in the industry as global geopolitics — unconnected directly with Europe or EMEA — becomes the single most important factor in how the market will develop over the rest of the year.”

Overall EMEA shipments reached 83.7 million units in 1Q19, a 3% drop YoY — confirming the smartphone slowdown isn’t just gaining momentum as the world continues to cycle down through summer, but Chinese smartphone makers have displaced Apple and Samsung as the top players in Europe.

(courtesy Tom Luongo)

What Happens If Salvini Goes Mini-BOT On The EU?

Since the idea was first floated there has been rampant speculation about how/when Lega Leader Matteo Salvini would introduce the Mini-BOT parallel currency to assist Italy’s fiscal situation.

Mike Shedlock has a great post on the subject that brings up a number of points about this subject. Well worth the read. Let’s go back and start at the beginning.

The mini-BOT or Mini-Bill of Treasury, is a small denomination bond that the treasury can sell which can be used by businesses and people as an alternative domestic currency.

As Mike brings up, without mandating their usage Italy skirts the letter of EU law prohibiting any country from issuing its own currency.