GOLD: $1339.40 DOWN $1.65 (COMEX TO COMEX CLOSING)

Silver: $14.83 UP 1 CENT (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1340.00

silver: $14.84

YOUR DATA…

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 93/119

EXCHANGE: COMEX

CONTRACT: JUNE 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,340.100000000 USD

INTENT DATE: 06/14/2019 DELIVERY DATE: 06/18/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 H HSBC 1

661 C JP MORGAN 93

686 C INTL FCSTONE 18

737 C ADVANTAGE 73 24

800 C MAREX SPEC 1

905 C ADM 28

____________________________________________________________________________________________

TOTAL: 119 119

MONTH TO DATE: 1,813

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 119 NOTICE(S) FOR 11900 OZ (0.3701 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1813 NOTICES FOR 181300 OZ (5.6391 TONNES)

SILVER

FOR JUNE

40 NOTICE(S) FILED TODAY FOR 200,000 OZ/

total number of notices filed so far this month: 340 for 1750,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 8715 UP 326

Bitcoin: FINAL EVENING TRADE: $ 9296 UP 344

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL A TINY SIZED 643 CONTRACTS FROM 233,302 DOWN TO 232,913 ACCOMPANYING THE 9 CENT LOSS IN SILVER PRICING AT THE COMEX.( LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR GOLD . HOWEVER WE ARE WITNESSING A RISE IN SPREADING ACCUMULATION BY THE BANKERS IN SILVER)..TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

200 FOR JUNE, 4350 FOR JULY. 0 FOR AUGUST, 0 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 4350 CONTRACTS.( IT IS NEWSWORTHY THAT SOMEBODY NEEDED SILVER IN A HURRY AS THEY USED THE EXCHANGE FOR PHYSICAL FORMAT TO OBTAIN SILVER HAVING EXERCISED 200 EFP’S IN JUNE) WITH THE TRANSFER OF 4350 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 4350 EFP CONTRACTS TRANSLATES INTO 22.75 MILLION OZ ACCOMPANYING:

1.THE 9 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

1.560 MILLION OZ STANDING FOR SILVER IN JUNE//

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

32,123 CONTRACTS (FOR 11 TRADING DAYS TOTAL 32,123 CONTRACTS) OR 160.62 MILLION OZ: (AVERAGE PER DAY: 2920 CONTRACTS OR 14.60 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JUNE: 160.62 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 22.94% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1031.37 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 643, WITH THE 9 CENT FALL IN SILVER PRICING AT THE COMEX /FRIDAY... THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 4550 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS WILL RESUME THEIR LIQUIDATION OF THE SPREAD TRADES FOR SILVER ONCE THE JUNE CONTRACT COMMENCES IN EARNEST….

TODAY WE GAINED A STRONG SIZED: 3907 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 4550 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 643 OI COMEX CONTRACTS. AND ALL OF THIS HUGE DEMAND HAPPENED WITH A 9 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $14.82 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.082 BILLION OZ TO BE EXACT or 152% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 40 NOTICE(S) FOR 200,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 1.560 MILLION OZ//

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

WITH RESPECT TO SPREADING: WE NO DOUBT HAD VERY STRONG ACTIVITY OF SPREADING ACCUMULATION IN SILVER TODAY AS TOTAL OI ROSE SHARPLY WITH THE SMALLISH GAIN OF 4 CENTS.

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JUNE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE OPEN INTEREST ROSE BY A STRONG 10,907 CONTRACTS, TO 522,378 DESPITE THE TINY $1.05 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING LIQUIDATION HAS STOPPED AND THESE SPREADERS HAVE ALREADY MORPHED INTO SILVER AND THEY ARE INTO THE ACCUMULATION PHASE OF THEIR OPERATION. THUS THE GAIN IN OI IS REAL AS INVESTORS ARE POURING INTO THE GOLD SECTOR

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7659 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 7659 CONTRACTS, DEC> 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 522,378. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 18,565 CONTRACTS: 10,907 CONTRACTS INCREASED AT THE COMEX AND 7659 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 18,566 CONTRACTS OR 1,856,600 OZ OR 57.74 TONNES. YESTERDAY WE HAD A TINY GAIN OF $1.05 IN GOLD TRADING.…AND WITH THAT SMALL GAIN IN PRICE, WE HAD A HUMONGOUS GAIN IN GOLD TONNAGE OF 57.74 TONNES!!!!!! THE BANKERS WERE SUPPLYING COPIOUS SUPPLIES OF SHORT GOLD COMEX PAPER.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 109,283 CONTRACTS OR 10,928,300 oz OR 339.92 TONNES (11 TRADING DAYS AND THUS AVERAGING: 9935 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAYS IN TONNES: 339.92 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 339.32/3550 x 100% TONNES =9.55% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2,617.81 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 10,907 WITH THE PRICING GAIN THAT GOLD UNDERTOOK ON FRIDAY($1.05)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7659 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7659 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC SIZED GAIN OF 18,566 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7659 CONTRACTS MOVE TO LONDON AND 10,907 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 57.74 TONNES). ..AND THIS INCREASE OF DEMAND OCCURRED WITH A TINY GAIN IN PRICE OF $1.05 WITH RESPECT TO FRIDAY’S TRADING AT THE COMEX. WE HAD ZERO PRESENCE OF SPREADING ACCUMULATION IN GOLD ///TODAY/

we had: 119 notice(s) filed upon for 11,900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $1.65 TODAY//

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 764.10 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 1 CENT TODAY:

A HUGE CHANGES WITH RESPECT TO SILVER INVENTORY AT THE SILVER SLV: A MASSIVE PAPER DEPOSIT OF 2.295 MILLION OZ

/INVENTORY RESTS AT 319.070 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TINY SIZED 643 CONTRACTS from 233,556 UP TO 232,913 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JUNE 200 CONTRACTS (SOMEBODY WAS IN NEED OF SILVER, BADLY) AND JULY: 4350 CONTRACTS FOR AUGUST: 0, FOR SEPT. 0 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 4550 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 254 CONTRACTS TO THE 4550 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A VERY STRONG GAIN OF 3907 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 21.48MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY AND NOW 1.570 MILLION OZ FOR JUNE.

RESULT: A TINY SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 9 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// FRIDAY. WE ALSO HAD A STRONG SIZED 4550 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 5.65 POINTS OR 0.20% //Hang Sang CLOSED UP 108.81 POINTS OR 0.40% /The Nikkei closed UP 7.11 POINTS OR 0.03%//Australia’s all ordinaires CLOSED DOWN .36%

/Chinese yuan (ONSHORE) closed DOWN at 6.9270 /Oil DOWN TO 52.12 dollars per barrel for WTI and 61.21 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9270 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9328 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

Simon Black outlines the horrifying situation with Japan’s pension system whereby there are only two workers to one pensioner. The USA is at 2.7 workers per pensioner and the entire world is deficient as there is just not enough money to pay pensions.For a young workers, they will be paying into the plan with no hope of receiving anything.

( Simon Black)

3 China/Chinese affairs

i)China/HONG KONG/

Hong Kong indefinitely suspends extradition bill. Hong Kong citizens still very angry

( zerohedge)

Wilbur Ross warns us not to expect any deal at the next G 20 meeting

( zerohedge)

iii/ Huawei/Globe

With the 90 day grace period coming to an end, expect trouble for Huawei as it braces for a huge 60 million smartphone unit sales plunge as these units can no longer use the Google android app

( zerohedge)

4/EUROPEAN AFFAIRS

i)UK

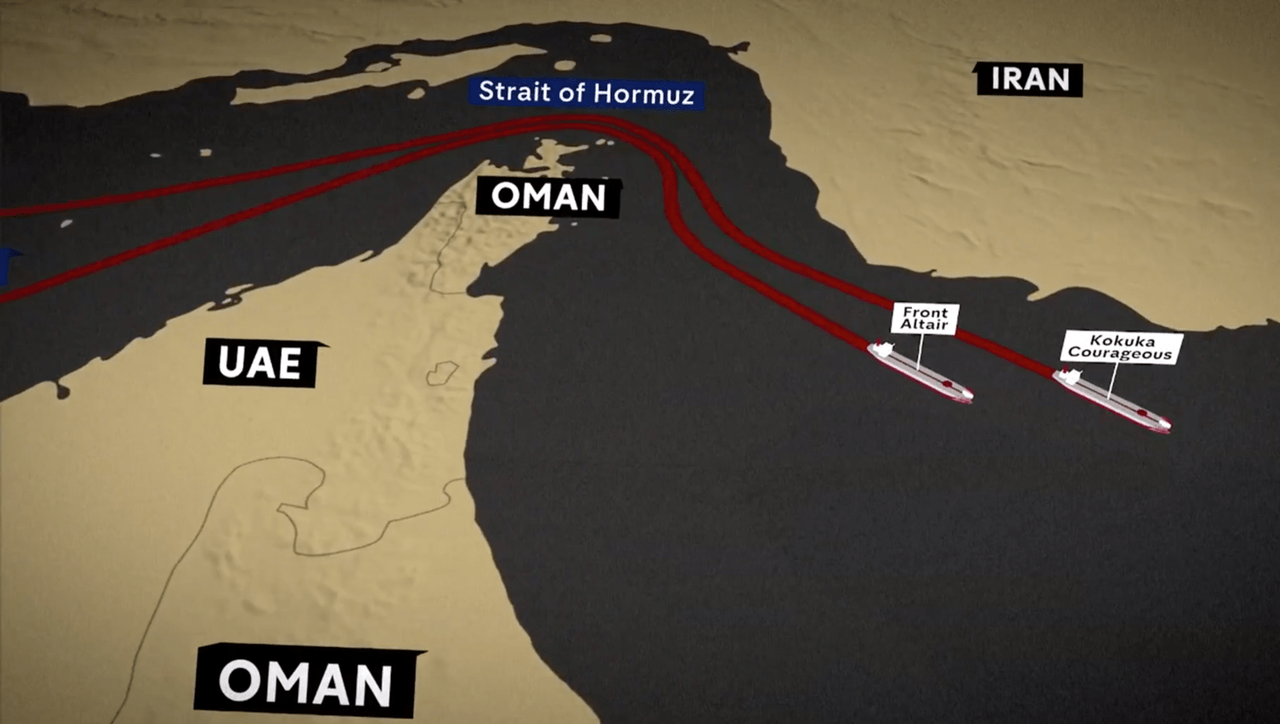

The UK are now siding with the USA as the evidence certainly points that the attacks in the Gulf were caused by the Iranians. The UK is deploying 100 elite royal mines to be stationed in Bahrain and these guys along with the Americans will try and guarantee safety of ships crossing through the Strait of Hormuz.

(courtesy zerohedge)

i b)

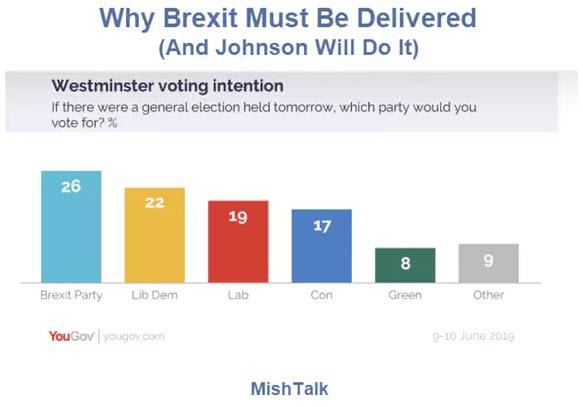

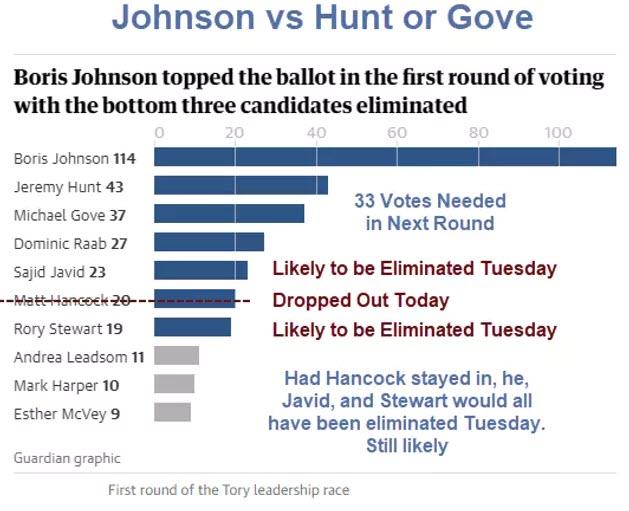

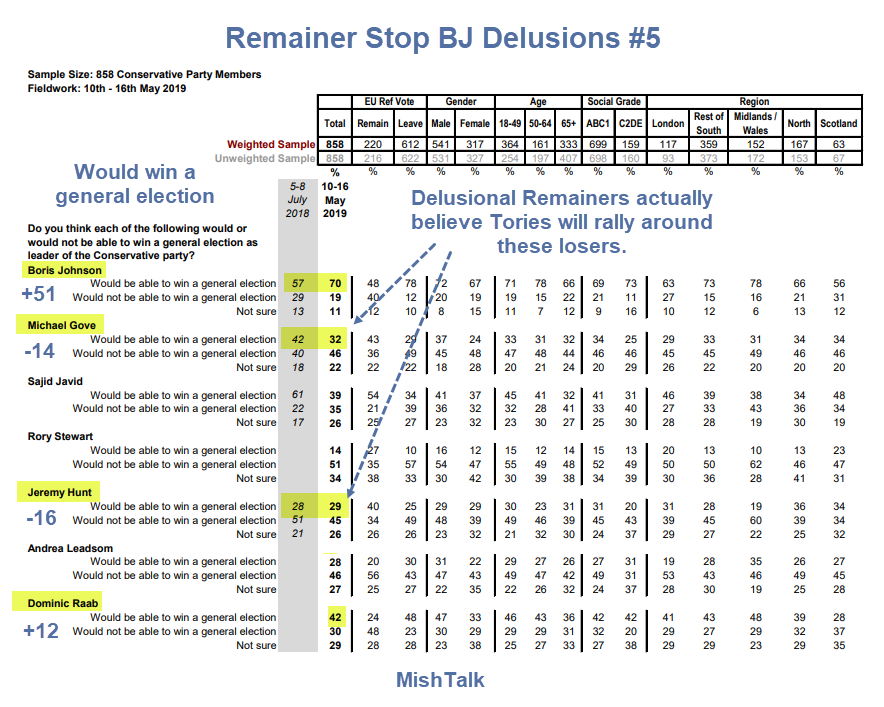

Mish explains how Boris Johnson will become the next Prime Minister and probably lead them to a no deal Brexit.(courtesy Mish Shedlock)

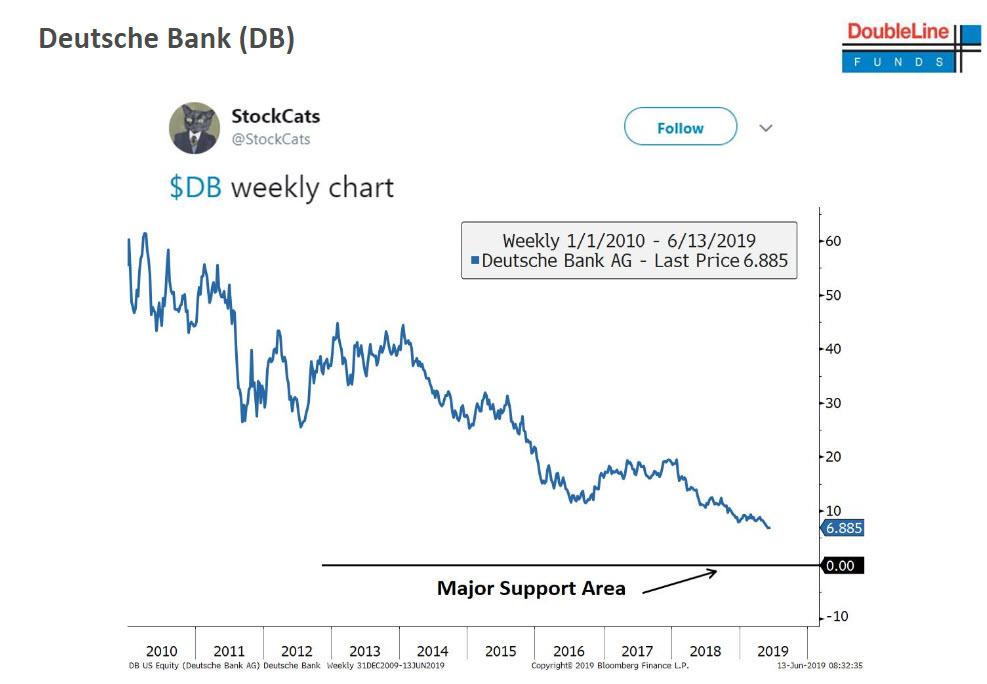

ii)/DEUTSCHE BANK/GERMANY

This should be interesting: Deutsche bank will try and launch a 50 billion euro bad bank as it puts a huge amount of toxic assets into it. What will become of DB’s huge derivative loss portfolio is anybody’s guess. Nobody in the right frame of mine will buy this garbage.

(zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)IRAN

very weird and very fluid…

(zerohedge)

ib)The countdown has begun: Iran warns that it will breach its uranium stockpile limits in 10 days. The Germans are now looking at the evidence that it was the Iranians who fired upon those two tankers. The situation is very fluid..

(courtesy zerohedge)

ii)Elijah Magnier comments on middle eastern affairs. He states that Iran is hurt really badly economically and they were the probable instigators of the attack on our two tankers. He main theme is the fact that if more strikes occur, then insurance rates skyrocket and it will be impossible for any oil to enter and exit the Gulf

a good read..

(courtesy Magnier)

iv)ISRAEL

ISRAEL honours Donald Trump with a new Israel settlement in the former occupied Golan Heights named Trump Heights after the USA recognized Israeli sovereignty over the territory.

(courtesy zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

a)Market trading/LAST NIGHT/

II)MARKET TRADING

ii)Market data

a)My goodness did this escalate fast. The New York Mgf Survey posted a 10 sigma move southbound as the manufacturing sector in this area splummeded to -11

Although a soft data entry point, it surely tells where we are heading

(courtesy zerohedge)

iii)USA ECONOMIC/GENERAL STORIES

a)Corporate tax receipts are plunging far more than expected and many believe it was due to the tariff situation where firms costs have now risen

(courtesy zerohedge)

SWAMP STORIES

a)A terrific commentary from Daniel Lacalle as he outlines why didn’t the Mueller team investigate the murder of Seth Rich

( Lacalle)

b)This is really amazing: the USA’s entire government narrative is based on a redacted draft of Crowdstrike and also that report has never been finalized.

(zerohedge)

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; nil oz

FOR THE JUNE 2019 CONTRACT MONTH)Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 119 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 93 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account and 0 notices by the squid (Goldman Sachs)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JUNE /2019. contract month, we take the total number of notices filed so far for the month (1813) x 100 oz , to which we add the difference between the open interest for the front month of JUNE. (590 contract) minus the number of notices served upon today (119 x 100 oz per contract) equals 228,400 OZ OR 7.104 TONNES) the number of ounces standing in this active month of JUNE

Thus the INITIAL standings for gold for the JUNE/2019 contract month:

No of notices served (1813 x 100 oz) + (590)OI for the front month minus the number of notices served upon today (119 x 100 oz )which equals 228,400 oz standing OR 7,104 TONNES in this active delivery month of JUNE.

We GAINED 392 contracts or an additional 39200 oz will stand as these guys refused to morph into London based forwards as well as negating a fiat bonus. Somebody was in need of physical gold badly.!!

SURPRISINGLY LITTLE TO NO GOLD HAS BEEN ENTERING THE COMEX VAULTS AND WE HAVE WITNESSED THIS FOR THE PAST YEAR!! WE HAVE ONLY 10.08 TONNES OF REGISTERED ( GOLD OFFERED FOR SALE) VS 7.104 TONNES OF GOLD STANDING// THEY SEEM TO BE USING CONSIDERABLE GOLD VAPOUR TO SETTLE UPON UNSUSPECTING LONGS.

total dealer silver: 87.119 million

total dealer + customer silver: 303.151 million oz

The total number of notices filed today for the JUNE 2019. contract month is represented by 40 contract(s) FOR 200,000 oz

To calculate the number of silver ounces that will stand for delivery in JUNE, we take the total number of notices filed for the month so far at 350 x 5,000 oz = 1,750,000 oz to which we add the difference between the open interest for the front month of JUNE. (241) and the number of notices served upon today (40 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JUNE/2019 contract month: 350(notices served so far)x 5000 oz + OI for front month of JUNE( 241) -number of notices served upon today (40)x 5000 oz equals 2,755,000 oz of silver standing for the JN contract month.

WE GAINED A WHOPPING 240 CONTRACTS OR AN ADDITIONAL 1,200,000 OZ WILL STAND AT THE COMEX AS THESE GUYS REFUSED TO MORPH INTO A LONDON BASED FORWARDS AND AS WELL THEY ALSO NEGATED A FIAT BONUS. IT SEEMS THAT SOMEBODY WAS BADLY IN NEED OF PHYSICAL SILVER ON THIS SIDE OF THE POND.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 72,841 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 134,033 CONTRACTS..(we no doubt had considerable spreading activity as they are now starting to accumulate in silver)

YESTERDAY’S CONFIRMED VOLUME OF 134,033 CONTRACTS EQUATES to 670 million OZ 95.7% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.26% June 17/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.53% to NAV (june 17/2019 )

Note: Sprott silver trust back into NEGATIVE territory at -1.26%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 13.20 TRADING 12.63/DISCOUNT 4.93

END

And now the Gold inventory at the GLD/

JUNE 17/WITH GOLD DOWN $1.65 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 764.10 TONNES

JUNE 14/ WITH GOLD UP $1.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.40 TONNES OF PAPER GOLD INTO THE GLD///INVENTORY RESTS AT 764.10 TONNES

june 13/WITH GOLD UP $6.60 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 759.70 TONNES

JUNE 12/WITH GOLD UP $7.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 756.18 TONNES

JUNE 11/WITH GOLD UP $1.65 CENTS TODAY: A TINY CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .24 TONNES AND THIS IS TO PAY FOR FEES/INVENTORY RESTS AT 756.18 TONNES

JUNE 10/WITH GOLD DOWN $16.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES/INVENTORY RESTS AT 756.42 TONNES

june 7/WITH GOLD UP $3.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

jUNE 6/WITH GOLD UP $8.40 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 5 WITH GOLD UP $6.00 TODAY/STRANGE: A WITHDRAWAL OF 2.06 TONNES FROM THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 4/WITH GOLD UP 0.85 TODAY: A MONSTROUS PAPER GAIN OF 16.44 TONNES/GLD INVENTORY RESTS AT 759.65 TONNES

JUNE 3/WITH GOLD UP $17.50 TODAY: ANOTHER BIG CHANGE, A DEPOSIT OF 2.35 TONNES OF GOLD INTO THE GLD//

MAY 31/WITH GOLD UP $17.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GLD INVENTORY RESTS AT 740.86 TONNES

MAY 30: WI6H GOLD UP $6.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES/INVENTORY RESTS AT 740.86 TONNES

MAY 29/WITH GOLD UP $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 737.34 TONNES

MAY 28/WITH GOLD DOWN $6.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD> A WITHDRAWAL OF 1.47 TONNES/INVENTORY RESTS AT 737.34 TONNES

MAY 24/WITH GOLD DOWN $1.60 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 738.81 TONNES

MAY 23/WITH GOLD UP $11.10 TODAY: A STRANGE WITHDRAWAL OF .88 TONNES FORM THE GLD/INVENTORY RESTS AT 738,81 TONNES

MAY 22//WITH GOLD FLAT TODAY: WE HAD A GOOD 1.52 TONNES OF GOLD DEPOSIT INTO THE GLD/INVENTORY RESTS TONIGHT AT 739.69 TONNES

MAY 21/WITH GOLD DOWN $3.65 TODAY: A SURPRISE 2.00 TONNES WERE ADDED TO THE GLD GOLD INVENTORY//INVENTORY RESTS AT 738.17 TONNES

MAY 20/WITH GOLD UP $1.00 A HUGE 2.96 TONNE DEPOSIT INTO THE GLD//INVENTORY RESTS AT 736.17 TONNES

MAY 17/WITH GOLD DOWN $9.70 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 733.23 TONNES

MAY 16/WITH GOLD DOWN $11.50: A WITHDRAWAL OF 3.23 TONNES FROM THE GLD//INVENTORY RESTS AT 733.23 TONNES

MAY 15/WITH GOLD UP $1.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 736.46 TONNES

MAY 14//WITH GOLD DOWN $5.45 TODAY: STRANGE!! THE CROOKS DECIDED TO DEPOSIT A HUGE 3.23 TONNES INTO THE GLD INVENTORY//INVENTORY RESTS AT 736.46 TONNES

MAY 13/ WITH GOLD UP ANOTHER $15.40 TODAY: STRANGE! A MASSIVE WITHDRAWAL OF 6.41 TONNES OF GOLD (TO TAME GOLD’S RISE TODAY)/INVENTORY RESTS AT 733.23 TONNES

MAY 10 WITH GOLD UP $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 739.64 TONNES

MAY 9//WITH GOLD UP $4.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 739.64 TONNES

MAY 8/WITH GOLD DOWN $3.70 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 739.64 TONNES

MAY 7/ WITH GOLD UP $1.80: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 739.64 TONNES

MAY 6/WITH GOLD UP $2.35: ANOTHER WITHDRAWAL OF 5.88 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 739.64 TONNES

MAY 3/WITH GOLD UP $9.35 TODAY: A WITHDRAWAL OF 1.17 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 745.52

MAY 2/WITH GOLD DOWN $12.30 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 746.69 TONNES

MAY 1/WITH GOLD DOWN $1.20 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 746.69 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JUNE 17/2019/ Inventory rests tonight at 764.10 tonnes

*IN LAST 611 TRADING DAYS: 169.66 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 511 TRADING DAYS: A NET 4.03 TONNES HAVE NOW BEEN REMOVED FROM THE GLD INVENTORY.

end

Now the SLV Inventory/

JUNE 17/WITH SILVER UP ONE CENT TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.295 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 319.070 MILLION OZ//

JUNE 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 12/WITH SILVER UP 4 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.413 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 11/WITH SILVER UP 10 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 10/WITH SILVER DOWN 38 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

june 7/WITH SILVER UP ANOTHER 12 CENTS, NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

jUNE 6/WITH SILVER UP ANOTHER 9 CENTS TODAY: A FAIR SIZE DEPOSIT OF 630,087 OZ//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 5/WITH SILVER UP 4 CENTS TODAY: A HUGE PAPER DEPOSIT OF 2.396 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 314.434 MILLION OZ//

JUNE 4/WITH SILVER UP 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

JUNE 3/WITH SILVER UP 19 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

MAY 31/WITH SILVER UP 6 CENTS TODAY: A DEPOSIT OF 422,000 OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 312.038 MILLION OZ/

May 30/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ///

MAY 29/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 28/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 24/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ/

MAY 23/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 22/WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 311.616 MILLION OZ

MAY 21: WITH SILVER DOWN 3 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV; A WITHDRAWAL OF 750,000 OZ///INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 20/WITH SILVER UP 6 CENTS:NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.366 MILLION OZ

MAY 17/WITH SILVER DOWN 13 CENTS TODAY: A BIG CHANGES IN SLV: A WITHDRAWAL OF 3.185 MILLION OZ FROM THE SLV INVENTORY VAULTS:/INVENTORY RESTS AT 312.366 MILLION OZ//

MAY 16/WITH SILVER DOWN 26 CENTS: NO CHANGES IN THE SLV INVENTORY//INVENTORY RESTS AT 315.551 MILLION OZ//

MAY 15/WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SLV INVENTORY: A WITHDRAWAL OF 1.031 MILLION OZ// THE SLV/INVENTORY RESTS AT 315.551 MILLION OZ.

MAY 14/WITH SILVER UP 2 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV. INVENTORY RESTS AT 316.582 MILLION OZ/

MAY 13//WITH SILVE5 DOWN 2 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.582 MILLION OZ…

MAY 10/WITH SILVER UP 2 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 316.582 MILLION OZ///

MAY 9/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 316.582 MILLION OZ//

MAY 8/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.582 MILLION OZ///

MAY 7/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.582 MILLION OZ//

MAY 6/WITH SILVER DOWN 3 CENTS WE HAD ANOTHER DEPOSIT OF 891,000 OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 316.582 MILLION OZ/

MAY 3//WITH SILVER UP 34 CENTS TODAY: A DEPOSIT OF 843,000 OZ INTO THE SLV/TOTAL INVENTORY RESTS AT 315.691 MILLION OZ//

MAY 2/WITH SILVER DOWN ANOTHER 13 CENTS, MIRACUOUSLY THE AUTHORITIES ADD 2.869 MILLION OZ OF SILVER BACK INTO THE SLV/INVENTORY RESTS AT 314.848 MILLION OZ//

MAY 1/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.979 MILLION OZ////

Gold Breaks Abov

end

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

The following two commentaries were sent our way.

‘Rhody” is accurateiin his assessment

G B S G] FRIDAY’S MIDAS LETTER SIGNALLED THE END OF THE DOLLAR SYSTEM

Mon, Jun 17, 2019 at 9:49 AM

I commented on the Midas Letter yesterday. This Letter printed the trading volumes for gold and silver futures on Friday. The selling volumes in paper gold and silver were ludicrous and predictably the prices fell under an onslaught of selling at a time when the fundamentals were very bullish. Rising gold and silver prices are a very visible sign of decline in the viability of the American Dollar. Below is a quote in red about the selling data described in the Letter that illustrates how massive the selling was to repress prices. Rhody

Those ‘trading volumes’ mean 22.5 MILLION OUNCES of paper gold were dumped on CRIMEX in the first hour and a half of trading. In silver, 400 million ounces of paper silver were dumped on the market over the same time period. Total world above ground stockpiles of silver bullion are a mere 1 billion ounces, so these clowns dumped 40% of that on the silver ‘market’ in just over an hour. 22 million ounces of gold represents over 20% of total world ANNUAL gold production sold in just an hour and a half. These ounces in gold and silver do not exist, but the market assumes they do and down the price goes.

Don’t the managed funds see this? Don’t they realize that there is UNLIMITED selling being allowed by the CME and CFTC and that NO LONG POSITION STANDS A CHANCE OF EVER BEING LIQUIDATED AT A PROFIT? Are the managed funds THAT STUPID, or is this all a completely synthetic market with the commercials controlling both long and short sides of the market? These high selling volumes have been in place for some years now, but recently they have entered the realm of the ridiculous. Keep in mind that the above figures are just form ONE derivative market. London’s market is even bigger and there is parallel selling of equal volumes there as well. This is insanity, but welcome to Western economics.

Rhody

It seems almost impossible to see how the cartel can lose control of this market…..”Are the funds stupid” or just don’t care. I think you said some time ago that they don’t care about the losses since they can charge commissions and earn income for buying and selling the paper……This would be more dangerous for the funds if their investors started noticing. We sometimes forget that while the general investor at street level may be gone from the stock markets, the funds are where they now reside. I forget who said it (a little hyperbole perhaps) but “the average investor is the dumbest animal on the planet”.

So we watch (try to) any sign that physical buyers are rocking the boat at the COMEX. But would the data be published? The physical market exists, but is separate and follows the paper price generated on COMEX and London markets. This is allowed because those who want to accumulate physical gold and silver want to do so as cheaply as possible. The spot price of gold and silver is fake, but it allows participants to acquire physical gold and silver at small fractions of fair value. As long as a trickle of real metal reaches the market at the fake COMEX price, the physical market buys it in at the spot price plus a small premium. So it is not in the interests of the Russians or Chinese to disturb the synthetic market on COMEX or London. Nobody wants high gold or silver prices…..YET. Rising gold and silver prices are a very visible DEVALUATION of the Dollar. So far, the rise is slow and controlled by the hyper-selling of gold and silver derivatives by Western banks. At some point, the Russians, Chinese et al will have accumulated enough gold for their purposes or the West will run out of stockpiled metal that is being sent east and this whole sham will collapse. When this happens is unknown. Gold stockpiles are state secrets, so we won’t know when the East has enough or the West is about to run out of gold supplies. My guess is that the East will wait until the present fiat system collapses from its own debt load so that the East appears blameless. The east is blameless because fiat systems have finite life expectancies defined by the accumulation of toxic debt. You will know when the debt level has become toxic when interest rates here in the west drop to zero or below. That signals the end. Rates are already zero in Europe and Japan. They are low single digits in the U.S. and Canada and are about to drop here as well. Zero or even negative interest rates are coming to Canada and the United States. That will signal the end of the Dollar system.

It is amazing that this slow decay of the Dollar system occurs right under everybody’s nose and people don’t seem to notice or comment. That’s because no comment is allowed to reach the public through Main Stream Media. You are reading this only because this information comes via the internet and is personally directed. Joe Six Pack is clueless. World War two lasted less than 6 years. There has been war in the middle east since 1991. THAT’S 28 YEARS AND MILLIONS OF DEAD. War is a characteristic of monetary crisis and death of empire.

Rhody

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

end

* * *

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.9278/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.9328 /shanghai bourse CLOSED UP 5.65 POINTS OR 0.20%

HANG SANG CLOSED UP 108.81 POINTS OR 0.40%

2. Nikkei closed UP 7.11 POINTS OR 0.03%

3. Europe stocks OPENED ALL MIXED/

USA dollar index UP TO 97.52/Euro RISES TO 1.1219

3b Japan 10 year bond yield: RISES TO. –.12/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.68/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 52.12 and Brent: 61.21

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO -.24%/Italian 10 yr bond yield UP to 2.31% /SPAIN 10 YR BOND YIELD UP TO 0.51%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.55: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 2.72

3k Gold at $1334.70 silver at: 14.81 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 1/100 in roubles/dollar) 64.31

3m oil into the 52 dollar handle for WTI and 61 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.68 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9989 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1207 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISING to –0.24%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.11% early this morning. Thirty year rate at 2.61%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.8723..

Slow Start As Traders Brace For Huge Week For Global Markets

With the most important 2 weeks of the year looming dead ahead, on Monday U.S. equity futures drifted without conviction along with European stocks following a mixed session in Asia as a huge week for central-bank decisions and policy gets underway, to be followed by the highly anticipated G-20 meeting in Osaka at the end of the month. Treasuries and gold dropped, the dollar was steady and cryptos surged to new 2019 highs.

As the Federal Reserve prepares to signal on Wednesday whether it is readying its first interest rate cut since the financial crisis (or isn’t, and sends stocks plunging as the gap between market expectations and Fed signalling is the widest it has ever been…

… and oil still choppy after last week’s Gulf tanker attacks, most markets are in a holding pattern.

The Fed’s “overall tone will be dovish but there’s a fair bit priced into the market already,” Sally Auld, senior interest-rate strategist at JPMorgan Chase & Co., told Bloomberg TV in Sydney. “It’s probably going to be hard for the Fed to exceed what is already priced in.”

For now, traders are focusing on the dollar’s surge on Friday after above-forecast U.S. industrial output and sharp upward retail sales revisions, as well as upbeat consumer confidence, pushed back futures markets expectations of any quick Fed rate cut.

“A (U.S.) rate cut this week seems extremely premature,” said Royal Bank of Canada’s Global Head of FX Strategy Elsa Lignos. “But the Fed can make some communications tweaks that at least open up the possibility for a cut in July. The question is how flexible that messaging will be.” Traders are pricing a high probability of a July rate cut, despite there being unusually high uncertainty, particularly around trade, Lignos added. She said a G20 meeting late this month could also change the narrative again.

Futures on the S&P 500 were unchanged, while Europe’s Stoxx 600 Index was little changed even as a profit warning from Germany’s Lufthansa hit airlines and canceled out a 0.8% rise in banking stocks. Deutsche Bank stock rose and boosted lenders on reports that it’s considering creating a “bad bank” to wind down legacy assets as part of a broader overhaul.

Earlier in the session, Asian equities fell 0.4% as a rebound in Hong Kong stocks failed to offset declines in Japan’s market. Japan’s Topix index dropped 0.5%, led by Ateam Inc. and Japan Communications Inc. Hong Kong’s Hang Sang Index pared earlier gains and closed 0.4% higher after the city’s chief executive suspended a controversial extradition bill. The Hang Seng fell for three sessions in a row through Friday, after the extradition bill triggered mass protests and some of the worst unrest seen in the territory since Britain handed it back to Chinese rule in 1997. Over in the Mainland, Chinese shares traded within a tight range, with the benchmark Shanghai Composite up 0.2% and the blue-chip CSI 300 barely budging. The region’s chipmakers declined as Broadcom triggered a global sell-off after it slashed its full-year revenue forecast Friday amid escalating trade tensions.

“Last week the issue looked as if it would become another thorny point between the United States and China. As the bill is now being postponed indefinitely, things will likely calm down, which is good for markets,” said Hiroyuki Ueno, senior strategist at Sumitomo Mitsui Trust Asset Management.

Emerging-market stocks and currencies declined for a fourth day as investors refrained from making any major judgement calls ahead of central bank meetings this week.

In rates, with long-term inflation expectations at an all-time low again, euro zone bond yields held close to their multi-year trough, despite inching fractionally higher early on. ECB board member Benoit Coeure said in an interview that the bank’s already sub-zero interest rates could be cut again if needed. It could also restart the quantitative easing program it wound down at the end of last year. In short: it can do everything – and more – that led to European inflation expectations hitting all time lows and leaving Deutsche Bank on the verge of insolvency.

“The question is not whether we have instruments; we do have instruments. We can change our guidance. We can cut rates. We can restart QE,” Coeure told the Financial Times. “The question is which instrument, or combination of instruments, would be best suited to the circumstances.”

No, the real question is when do the peasant finally rise up and put an and to the ECB. But we digress.

In FX, the dollar was steady after jumping on Friday, rising to the highest level in almost two weeks, after the U.S. retail sales data eased fears that the world’s largest economy is slowing sharply. Investors awaited clues from the Federal Reserve on the outlook for monetary policy, after solid U.S. economic data on Friday cast doubts about a more dovish position from the central bank. Asia’s currencies led declines after U.S. Commerce Secretary Wilbur Ross downplayed the prospect of a major trade deal emerging from a possible meeting between President Donald Trump and Chinese President Xi Jinping at the Group of 20 summit this month. “Weighing on investors’ collective mind is whether the Fed can live up the dovish expectations of the market, especially following firm U.S. data on Friday,” Credit Agricole SA strategists led by Valentin Marinov wrote in a report.

The Turkish lira added 0.4% to 5.87 per dollar, reversing losses of as much as 0.6%, after the Treasury and Finance Ministry said Moody’s decision to downgrade the nation’s credit rating is incompatible with fundamental indicators, adding that the country will never abandon free-market principles. The currency’s gain on Monday ends a four-day losing streak. Turkey central bank will provide Primary Dealer banks with a liquidity facility within the framework of open market operations. Russia’s ruble adds 0.1% to Friday’s gains after the central bank lowered interest rates and signaled more reductions to come.

In commodities, oil futures dipped as Saudi Arabia expressed hope that OPEC and its allies will agree to extend production cuts into the second half. Bitcoin jumped, heading toward its highest close in more than a year. Geopolitical tensions in the Middle East have added another layer of uncertainty after the United States blamed Iran for attacks on two oil tankers in the Gulf of Oman last week. U.S. Secretary of State Pompeo said Washington will take all actions necessary to guarantee safe navigation in the Middle East, though oil prices slipped again as worries about the broader slowdown in the global economy returned. Brent futures fell 25 cents, or 0.4%, to $61.76 a barrel by 0900 GMT, after gaining 1.1% on Friday while logging their fourth consecutive weekly fall. West Texas Intermediate crude futures were down 22 cents, or 0.4%, at $52.29, having firmed by 0.4% in the previous session.

“Today, oil markets will have to digest more demand concerns as India implemented retaliatory tariffs on a number of U.S. goods yesterday,” consultancy JBC Energy said in a note. Also sapping prices was the dim outlook for oil demand growth in 2019 projected by the International Energy Agency (IEA) on Friday, citing worsening prospects for global trade.

Finally, as reported over the weekend, Bitcoin jumped overnight to $9,391.85, its highest level in 13 months, as institutions are now buying the crypto according to JPM. It was last quoted at $9,195.62, up 2.4%.

Expected data include U.S. Empire State Manufacturing Survey. No major companies are scheduled to release earnings

Market Snapshot

- S&P 500 futures up 0.2% to 2,899.75

- STOXX Europe 600 up 0.06% to 379.05

- MXAP down 0.4% to 154.65

- MXAPJ down 0.3% to 504.84

- Nikkei up 0.03% to 21,124.00

- Topix down 0.5% to 1,539.74

- Hang Seng Index up 0.4% to 27,227.16

- Shanghai Composite up 0.2% to 2,887.62

- Sensex down 0.9% to 39,080.78

- Australia S&P/ASX 200 down 0.4% to 6,530.91

- Kospi down 0.2% to 2,090.73

- German 10Y yield rose 0.3 bps to -0.252%

- Euro up 0.06% to $1.1215

- Italian 10Y yield fell 0.8 bps to 1.981%

- Spanish 10Y yield fell 0.2 bps to 0.498%

- Brent futures down 0.3% to $61.83/bbl

- Gold spot down 0.6% to $1,333.45

- U.S. Dollar Index little changed at 97.53

Top Overnight News from Bloomberg

- ECB Executive Board member Benoit Coeure said the European Central Bank will act if needed to support the economy and could even be facing such a decision within months

- One of China’s biggest state-owned infrastructure companies excluded UBS Group AG from a bond deal after the bank’s global chief economist sparked a furor with his use of the phrase “Chinese pig”

- Iran’s atomic energy agency is expected to brief reporters Monday on the next phase of its retreat from obligations under the 2015 nuclear deal, the Iranian Students’ News Agency reported, as efforts to salvage the accord falter amid rising regional tensions

- Tory rivals battling to be the next U.K. prime minister traded insults over Brexit in the first TV debate of the party leadership contest, as front-runner Boris Johnson was mocked for refusing to take part

- Hong Kong rose up in defiance a day after leader Carrie Lam suspended a contentious extradition bill, jamming the streets with hundreds of thousands of people and drawing a formal apology from the embattled chief executive

- Commerce Secretary Wilbur Ross downplayed the prospect of a major trade deal emerging from a possible meeting between President Donald Trump and Chinese President Xi Jinping at the Group of 20 summit in Japan this month

- Tory rivals battling to be the next U.K. prime minister traded insults over Brexit in the first TV debate of the party leadership contest, as front- runner Boris Johnson was mocked for refusing to take part

- Turkey needs to work on a “new and fair” approach to managing the exchange rate that better suits the country’s economy and its people, according to a key ally of President Recep Tayyip Erdogan

- Financial markets are signaling investors see little risk of disruption from upcoming events, despite the potential for major shifts in the course of Fed policy and U.S.-China trade negotiations

Asian equity markets began mixed with the region cautious ahead of the upcoming slate of central bank activity and after last Friday’s losses on Wall St, where the tech sector underperformed as chipmakers suffered from losses in Broadcom. ASX 200 (-0.4%) and Nikkei 225 (Unch) were varied with Australia subdued by losses in telecoms, while Tokyo trade was underpinned as exporters benefitted from a weaker JPY. Hang Seng (+0.4%) and Shanghai Comp. (+0.2%) were both positive for most of early trade after the PBoC conducted a substantial liquidity injection and as the 2nd phase of its RRR cut took effect today which releases CNY 100bln of funds. However, momentum in the mainland eventually waned while Hong Kong outperformed after Chief Executive Lam postponed the extradition bill indefinitely. Finally, 10yr JGBs were lower amid the gains in Japanese stocks and following the bear flattening seen in US on Friday, with demand also dampened by the absence of BoJ Rinban operations in the market today.

Top Asian News

- Huawei Warns Trump’s Ban to Wipe Out $30 Billion of Sales Growth

- Adnoc, OCI to Form $1.7 Billion Middle East Fertilizer Giant

- Japan Opposition Prepares No-Confidence Vote in Finance Minister

European stocks are mixed in a continuation of the cautious tone seen in Asia, ahead of the central bank-packed week. Sectors are mixed with underperformance in the energy sector amid price action in the complex, whilst financial names lead the gains as banks benefit from the higher yields. In terms of movers, airline stocks took a hit after Lufthansa (-11.3%) cut its revenue and adj. EBIT margin guidance, citing increased competition in the market, and as such, Ryanair (-5.9%), easyJet (-5.3%) and Air France (-3.6%) all slipped in tandem. Elsewhere, Airbus (+1.0%) shares are buoyed as the Paris Air Show gets underway with reports noting the Co. has won a major 100-plane order over Boeing. Finally, Deutsche Bank (+2.2%) shares are feeling some reprieve after sources stated that the bank is mulling holding EUR 50bln of assets in a “bad bank” whilst also shrinking or shutting its US equity trading business.

Top European News

- H&M Sales Growth Decelerates in Gloomy Clothing Retail Market

- Kier Turns to ‘Self Help’ by Shedding 1,200 Jobs, Exiting Units

- Tories Spar Over ‘Dictator’ Brexit Plan With Johnson Absent

In FX, the Dollar has maintained its post-US data positivity and the DXY is pivoting 97.500 with resistance close by in the form of a 61.8% Fib retracement of the relatively pronounced pull-back from May 23 ytd highs of 97.373 to June 7 lows at 96.451, and support sitting around 97.457-6 where 21 and 55 DMAs converge. In terms of fundamentals, the looming FOMC will be paramount as markets widely if not unanimously anticipate another dovish shift from the Fed and signal that rates will be cut in July. However, ongoing global trade wars and geopolitical developments are propping up the Greenback and other safe-havens to varying degrees.

- NZD/AUD – Bucking the broad consolidative G10 trend and largely rangebound Usd/major trade, the Kiwi has bounced back to straddle 0.6500 and appears to be deriving some impetus from firmer NZ inflation metrics ahead of Westpac’s Q2 consumer survey tonight. Moreover, Aud/Nzd cross-flows may be supportive as the Aussie remains depressed around 1.0550 and 0.6875 vs its US counterpart amidst more dovish RBA calls (Macquarie now expecting the OCR to decline to 0.5% by year end) in advance of June policy meeting minutes in the early hours on Tuesday.

- EUR/CAD/JPY/GBP/CHF – As noted above, narrow parameters vs the Buck for the most part as the single currency holds within a 1.1205-25 band and just above decent option expiry interest at the 1.1200 strike (1 bn). Contacts also believe that reserve managers are lurking at the big figure on the buy-side, while nearest chart levels are seen at 1.1171 (76.4% Fib of the move from 1.1116 to 1.1348) and 1.1250 (latter more psychological than technical). Meanwhile, aside from the aforementioned Fed meet, the Euro may get some independent direction from the ECB’s annual Sintra conference that kicks off today with an opening speech from President Draghi. Elsewhere, the Loonie is also sitting tight between 1.3405-20 and awaiting a speech from BoC’s Schembri, but Deutsche Bank expects the headline pair to spike on FOMC disappointment given overly dovish expectations and some BoC catch up, targeting 1.3665 with a 1.3225 stop (recent low). The Yen is holding in a 108.43-70 range ahead of the BoJ on Friday and Cable is hovering just below 1.2600 pre-BoE, UK CPI and retail sales with Pound bears aware that 1.2560 is last month’s trend low. Finally, the Franc is holding just above parity post-last Thursday’s SNB and Eur/Chf remains confined either side of 1.1200.

- EM – The Lira has pared some losses from 5.9250+ lows vs the Dollar after Moody’s downgraded Turkey’s credit rating deeper into junk with the aid of a much needed improvement in unemployment, while the CBRT has enhanced liquidity provisions for primary banks via a facility discounted by 1% vs the 24% benchmark rate and based on government bond holdings.

In commodities, WTI and Brent futures continue to decline ahead of a risk-packed week with a number of bearish factors looming over the complex. 1) US crude stocks have been on the rise, with inventory reports via both API and EIA printing surprise builds for two straight weeks. Traders will now be wondering whether these increases will be enough for OPEC+ to possibly revise its output cut pact, with the meeting now seemingly taking place in the first week of July according to the Saudi Energy Minister. 2) Last week saw all three monthly oil reports (EIA, OPEC, IEA) cut their respective global oil growth demand forecasts amid rising threats of trade wars, whilst hopes for a deal between China and the US at the G20 summit seem slim. 3) Last week, speculators trimmed net long positions in Brent longs (-12.3k lots), but WTI saw a more significant reduction (-53.96k lots) as speculators try to balance rising US inventories with Middle-East tensions and potential OPEC+ reaction. WTI futures are hovering just above the USD 52/bbl mark (low USD 52.07/bbl) whiles Brent futures lost the USD 62/bbl handle, albeit remain off lows (USD 61.56/bbl). Elsewhere, precious metals are subdued, potentially on some profit taking ahead of this week’s key risk events including BoJ, BoE and Fed and a slew of ECB speakers. Gold has lost further ground below the USD 1350/oz level after a failed attempt at breaching long-term resistance at USD 1358.50/bbl last week. Meanwhile, copper is little changed amid the indecisive risk tone ahead of the aforementioned risk events.

US Event Calendar

- 8:30am: Empire Manufacturing, est. 11, prior 17.8

- 10am: NAHB Housing Market Index, est. 67, prior 66

- 4pm: Net Long-term TIC Flows, prior $28.4b deficit; Net TIC Flows, prior $8.1b deficit

DB’s Jim Reid concludes the overnight wrap

Morning from New York. As much as it’s tough to be away from the family I must admit it was lovely watching the final round of a US golf major in a better time zone last night rather than having to go to bed just before it gets to the final stretch. I was lucky enough to play Pebble Beach last month although to be fair I’ve played it around 200 times before. Yes it was my favourite course on Tiger Woods 2001 on the PlayStation 2. Lots of weekends wasted back then!!

Central banks will be getting their drivers out this week and will try to avoid the rough. The key drive will be that from the FOMC on Wednesday in what will likely be a very narrow fairway. The BoE and BoJ also meet on Thursday with the annual ECB get together in Sintra from tonight through to Wednesday. Data is a little second tier up to the flash global PMIs on Friday. Also by Thursday night we’ll know the final two in the UK Tory party leadership race ready for the ballot of 160,000 members with the winner known by July 22nd. In the background we also have the trade dispute and the political manoeuvrings ahead of the G-20 summit in less than 2 weeks. On that Commerce Secretary Wilbur Ross has again reiterated over the weekend that the most that will come out of the G-20 is “an agreement to actively resume talks”. Our guys in Washington believe there are negotiations occurring behind the scenes to try to set up a Trump/Xi meeting or dinner at the event. It’s possible we’ll hear more on this this week. This follows news that Mr Trump has stepped in again to delay VP Pence’s supposed hawkish speech on China. So it feels like Mr Trump is treading carefully with regards to the Chinese leadership and it’s also noticeable that he’s been quiet on the ongoing situation in Hong Kong.

Staying with Asia, the Hang Seng is the biggest mover this morning following the decision to suspend the extradition bill yesterday. After advancing +1.42% at the highs following the open the index has pulled back somewhat to be +0.60%. Elsewhere in Asia, other equity markets have also pulled back somewhat from the highs, with the Nikkei (+0.09%), the Shanghai Composite (-0.05%) and the KOSPI (-0.17%) all seeing modest movements in either direction. Meanwhile, S&P 500 futures are +0.26% overnight, while there’s not much to report in FX or bond markets.

Back to this week and the Fed have a very delicate balancing act to contend with as they have a choice of endorsing current dovish market pricing and keeping things calm, or to suggest it’s gone too far too quickly and give risk assets a sharp jolt. Friday’s strong retail sales data (more later) adds to the complexity. It’s hard not to feel that they are being driven into a corner at the moment as markets are now pricing in virtually a full rate cut at the July meeting and a further 2 cuts over the next 12 months. Expectations are much lower for a cut this week, with around an 18% chance. Our US economists recently changed their Fed call and expect 3 cuts of 25bps each at the July, September and December meetings. They also lowered their 2019 growth forecast by 40bps to 1.9%. So all eyes on Wednesday.

The BoE and BoJ meetings are not expected to be game changers but the ECB Sintra meetings have provided market moving events before. Two years ago it was used to highlight the paring back of stimulus and markets then started to price the winding down of QE. Could this forum mark a firm signalling that more stimulus is planned in the autumn? For the record, Draghi is making opening remarks tonight and introductory remarks tomorrow morning, while Guindos, Praet, Lane, Lautenschlaeger and Coeure are all due to take part. The BoE’s Carney also takes part in a policy panel with Draghi and former Fed Chair Yellen on Tuesday afternoon. Staying with the ECB we should note that EU leaders also gather in Luxembourg on Thursday for another round of talks about candidates for the European Commission and ECB.

As discussed it’s a fairly light week for top tier data until Friday’s global flash PMIs where we’ll get the latest chance to see how the trade war is impacting real time business sentiment and activity. The rest of the data/events/central bank activity is highlighted in the day by day week ahead at the end.

As for last week, most global equity markets ended in the red on Friday, but ultimately gained on the week, as economic data returned to focus. The S&P 500 ended +0.48% higher (-0.16% on Friday), with similar moves by the DOW and NASDAQ, which ended the week +0.41% and +0.70% (-0.07% and -0.52% Friday), respectively. In Europe, the STOXX 600 index advanced +0.35% (-0.40% Friday) with Italian equities outperforming, as the FTSE MIB gained +1.24% (-0.09% Friday). Banks underperformed in Europe, retreating -0.42% (-0.75% Friday) but outperformed in the US, gaining +1.26% (+0.43% Friday). Semiconductors lagged notably, falling -1.61% (-2.61% Friday) after Broadcom’s earnings report showed weaker than expected revenue guidance, with management citing the US-China trade war as a key headwind.

European banks were negatively impacted by sliding yields and heightened expectations for possible ECB easing, as the five year-five year inflation swap rate fell another -9.9bps (-4.8bps Friday) to a new all-time low of 1.134%. The drop in crude oil prices certainly didn’t help, as WTI crude ended the week -2.70% lower (+0.48% Friday), as continued US inventory increases drove a drop of over 6% early in the week, before geopolitical tensions near the Straits of Hormuz sparked a partial retracement. Collapsing inflation expectations also drove bunds to touch a fresh all-time low of -0.270% intraday on Friday, but they ultimately retraced a touch to end the week -2.3bps lower (-1.8bps Friday) at -0.255%. To see 5 year inflation swaps and 10 year bunds at these levels is not healthy. However can the ECB credibly persuade markets that they still have the tools to reverse these trends?

Over in the US, yields traded flat on the week (-1.2bps Friday), though under the surface there was a -10.9bps drop in the inflation breakeven rate (-4.2bps Friday) offset by a +10.4bps increase in real interest rates (+2.8bps Friday). The former was depressed by soft CPI data earlier in the week and the drop in oil prices, while the latter was supported by stronger real economic data, which turned more positive on Friday. The May retail sales report showed a 0.5% mom increase in activity, while the key “control group” reading which strips out volatile elements and is used to calculate GDP was 0.4% mom, double the 0.2% expected. The prior two months’ control group readings were revised up by 0.4pp and 0.1pp, making the positive signal even stronger. Indeed, the Atlanta Fed now forecasts second quarter real consumption growth at 3.9%, which would match the strongest print since 2014. A nice layer of complexity for the Fed to throw into the mix.

3. ASIAN AFFAIRS

I)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 5.65 POINTS OR 0.20% //Hang Sang CLOSED UP 108.81 POINTS OR 0.40% /The Nikkei closed UP 7.11 POINTS OR 0.03%//Australia’s all ordinaires CLOSED DOWN .36%

/Chinese yuan (ONSHORE) closed DOWN at 6.9270 /Oil DOWN TO 52.12 dollars per barrel for WTI and 61.21 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9270 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9328 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

Simon Black outlines the horrifying situation with Japan’s pension system whereby there are only two workers to one pensioner. The USA is at 2.7 workers per pensioner and the entire world is deficient as there is just not enough money to pay pensions.For a young workers, they will be paying into the plan with no hope of receiving anything.

(courtesy Simon Black)

Meanwhile, Over On Planet Japan…

Authored by Simon Black via SovereignMan.com,

It was only a few days ago that the Japanese government’s Financial Services Agency published its oddly-titled “Annual Report on Ageing Society”.

(Like everything in Japan, English translations often hilariously miss the mark…)

This is a report that the Ministry of Finance puts out every year. And as the name implies, the report discusses the state of Japan’s pension fund, and its future prospects for taking care of its senior citizens.

Bear in mind that Japan has the oldest population in the world; Japan ranks #2 in the world for average age (46.9, just behind Monaco), #1 in the world for the greatest percentage of citizens over the age of 70, and #1 in the world for life expectancy.

In a nutshell, this means that Planet Japan has more people collecting pension benefits, for more years, than anywhere else.

Yet at the same time, Japan’s pension fund is completely insolvent.There simply aren’t enough people paying into the system to make good on the promises that have been made.

At present there are only 2 workers paying into the pension program for every 1 retiree receiving benefits in Japan.

The math simply doesn’t add up, and it’s only getting worse. Planet Japan’s birth rate is infamously low, and the population here is actually DECLINING.

So, fast forward another 10-15 years, and there will be even MORE people collecting pension benefits, and even FEWER people paying into the system.

This year’s ‘Annual Report on Ageing Society’ plainly stated this reality; it was a brutally honest assessment of Japan’s underfunded pension program.

The report went on to tell people that they needed to save their own money for retirement because the pension fund wouldn’t be able to make ends meet.

This terrified a lot of Japanese workers and pensioners.

So the government stepped in to quickly solve the problem… by making the report disappear.

Prime Minister Shinzo Abe apologized for the report, calling it “inaccurate and misleading.”