GOLD: $1410.80 UP $0.90 (COMEX TO COMEX CLOSING)

Silver: $15,31 UP 6 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1410.10

silver: $15.33

YOUR DATA…

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING

____________________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 371 NOTICE(S) FOR 37100 OZ (1.1539 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 371 NOTICES FOR 37,100 OZ (1.1539 TONNES)

SILVER

FOR JULY

2620 NOTICE(S) FILED TODAY FOR 13,100,000 OZ/

total number of notices filed so far this month: 2620 for 13,100,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

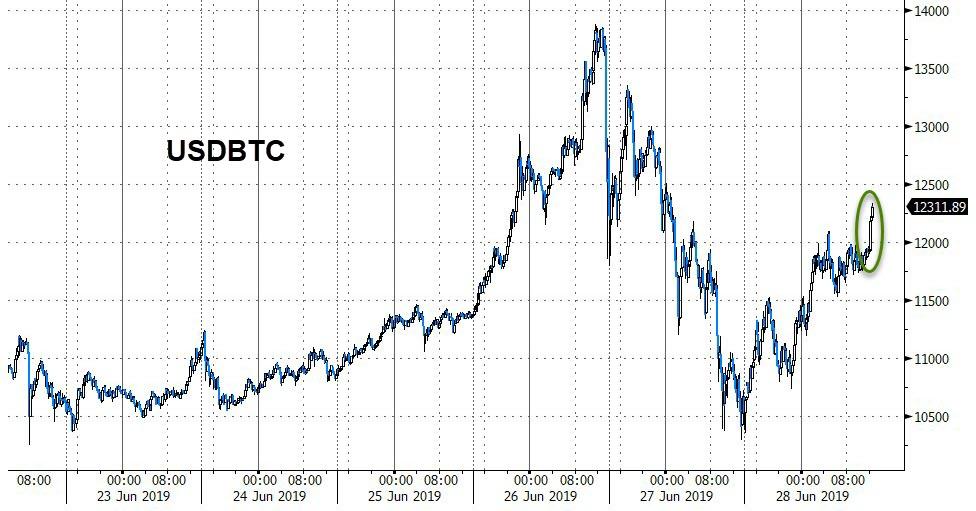

Bitcoin: OPENING MORNING TRADE : $ 12,010 UP 680

Bitcoin: FINAL EVENING TRADE: $ 11975 UP 1048

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL A CONSIDERABLE SIZED 2526 CONTRACTS FROM 223,138 DOWN TO 220,612 WITH THE 7 CENT LOSS IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JUNE, 1188 FOR JULY. 0 FOR AUGUST, 0 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1188 CONTRACTS. WITH THE TRANSFER OF 1188 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1188 EFP CONTRACTS TRANSLATES INTO 5.94 MILLION OZ ACCOMPANYING:

1.THE 7 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

NOTE: THE HUGE INCREASE IN EFP ISSUANCE FOR JUNE!!

WE HAD CONSIDERABLE SHORT COVERING AT THE SILVER COMEX LAST NIGHT..AND MAJOR SPREADING LIQUIDATION.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

53,077 CONTRACTS (FOR 20 TRADING DAYS TOTAL 53077 CONTRACTS) OR 265.38 MILLION OZ: (AVERAGE PER DAY: 2653 CONTRACTS OR 13.26 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JUNE: 265.38 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 37.91% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1157.49 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2526, WITH THE 7 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1188 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS WILL RESUME THEIR LIQUIDATION OF THE SPREAD TRADES FOR SILVER ONCE THE JUNE CONTRACT COMMENCES IN EARNEST….

TODAY WE LOST A GOOD SIZED: 1341 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1188 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 2526 OI COMEX CONTRACTS. AND ALL OF THIS HUGE DEMAND HAPPENED WITH A 7 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.25 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.187 BILLION OZ TO BE EXACT or 169% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JULY MONTH/ THEY FILED AT THE COMEX: 2620 NOTICE(S) FOR 13,100,100 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY:19.365 MILLION OZ//

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

WITH RESPECT TO SPREADING: WE NO DOUBT HAD CONSIDERABLE ACTIVITY OF SPREADING LIQUIDATION IN SILVER TODAY/IT WILL END AT THE CONCLUSION OF FIRST DAY NOTICE

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JUNE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE OPEN INTEREST ROSE BY A STRONG 5054 CONTRACTS, TO 579,514 ACCOMPANYING THE $6.10 PRICING DROP WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING LIQUIDATION HAS STOPPED IN GOLD,..HOWEVER THESE SPREADERS HAVE ALREADY MORPHED INTO SILVER AND THEY ARE NOW INTO THEIR CONCLUDING PHASE OF THEIR LIQUIDATION OPERATION WHICH ENDS AT 1:30 TODAY.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN STRONG SIZED 8844 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 8844 CONTRACTS, DEC> 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 579,514. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 163,898 CONTRACTS: 5054 CONTRACTS INCREASED AT THE COMEX AND 8844 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 13,898 CONTRACTS OR 1,389,800 OZ OR 43.22 TONNES. YESTERDAY WE HAD A LOSS OF $6.10 IN GOLD TRADING.…AND WITH THAT LOSS IN PRICE, WE HAD A HUMONGOUS GAIN IN GOLD TONNAGE OF 43.22 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 206,473 CONTRACTS OR 20,647,300 oz OR 642.22 TONNES (20 TRADING DAYS AND THUS AVERAGING: 10,323 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAYS IN TONNES: 642.22 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 642.22/3550 x 100% TONNES =18.09% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2,920.14 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

NOTE: THE HUGE INCREASE IN EFP ISSUANCE FOR GOLD

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 8844 DESPITE THE PRICING LOSS THAT GOLD UNDERTOOK ON YESTERDAY($6.10)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8844 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 8844 EFP CONTRACTS ISSUED, WE HAD A HUMONGOUS SIZED GAIN OF 13,898 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

8844 CONTRACTS MOVE TO LONDON AND 5054 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 43.22 TONNES). ..AND THIS INCREASE OF DEMAND OCCURRED DESPITE THE LOSS IN PRICE OF $6.10 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAD ZERO PRESENCE OF SPREADING ACCUMULATION/LIQUIDATION IN GOLD ///TODAY/

we had: 371 notice(s) filed upon for 37,100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $90 TODAY//

ANOTHER CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 2.05 TONNES

WHICH WAS USED IN ATTACKING GOLD.

INVENTORY RESTS AT 795.80 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 6 CENTS TODAY:

NO CHANGES WITH RESPECT TO SILVER INVENTORY AT THE SILVER SLV:

/INVENTORY RESTS AT 322.394 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A CONSIDERABLE SIZED 2526 CONTRACTS from 223,138 DOWN TO 220,612 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JUNE 0 CONTRACTS AND JULY: 1188 CONTRACTS FOR AUGUST: 0, FOR SEPT. 0 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1188 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 2526 CONTRACTS TO THE 1188 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD LOSS OF 1341 OPEN INTEREST CONTRACTS BUT ALSO SOME LIQUIDATION OF THOSE SPREADERS- COMEX CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 6.705 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY, NOW 2.660 MILLION OZ FOR JUNE…AND NOW 19.365 MILLION OZ FOR JULY.

RESULT: A CONSIDERABLE SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 7 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// FRIDAY. WE ALSO HAD A STRONG SIZED 1188 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 17.91 POINTS OR 0.60% //Hang Sang CLOSED DOWN 78.80 POINTS OR 0.28% /The Nikkei closed DOWN 62.65 POINTS OR 0.29%//Australia’s all ordinaires CLOSED DOWN .65%

/Chinese yuan (ONSHORE) closed UP at 6.8693 /Oil UP TO 59.57 dollars per barrel for WTI and 65.75 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.8693 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8740 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/

Two problem areas for China, the huge Pig Ebola that is wiping out the Chinese pig population and the “armyworm” caterpillar which has now invaded China from Burma and it is devastating the corn and other crops. China can no longer afford to tariff USA agriculture. If Trump stays solid he will win the trade war.

( Kyle Bass)

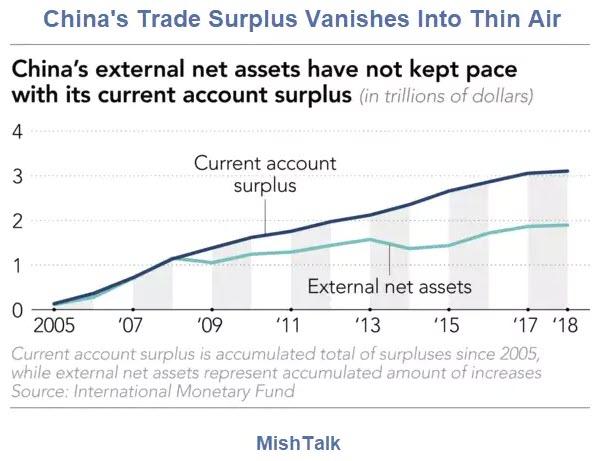

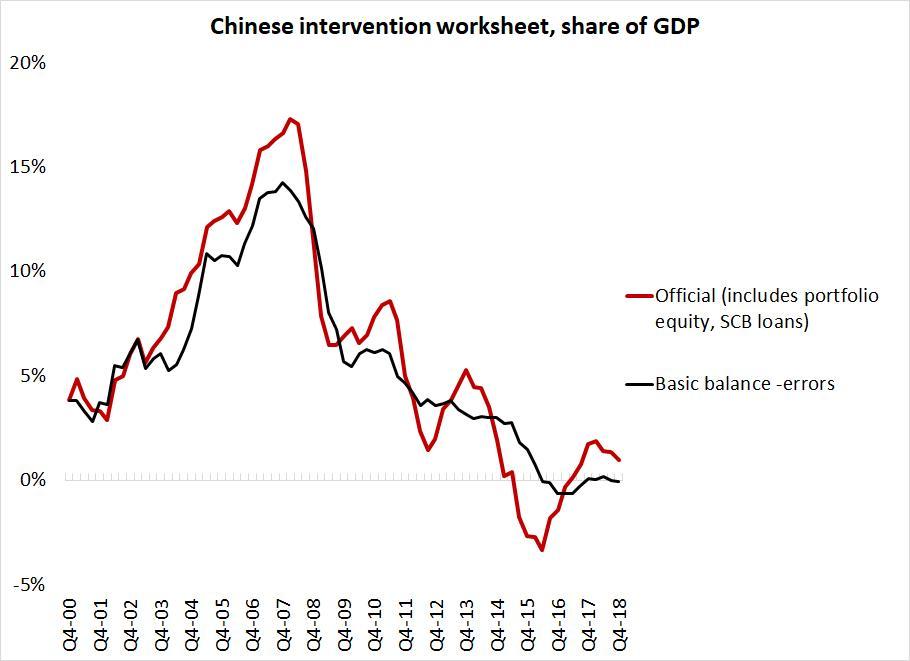

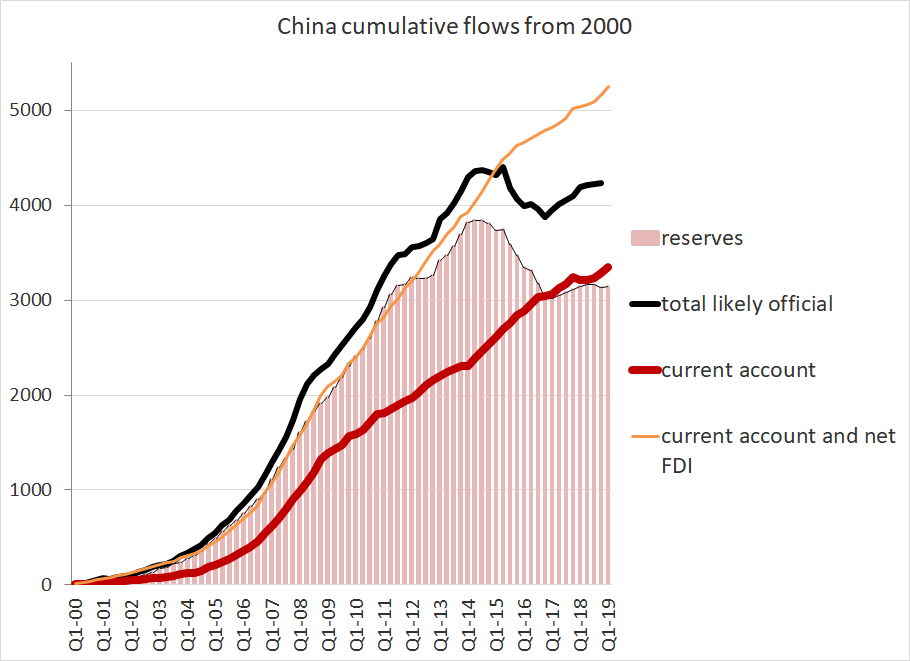

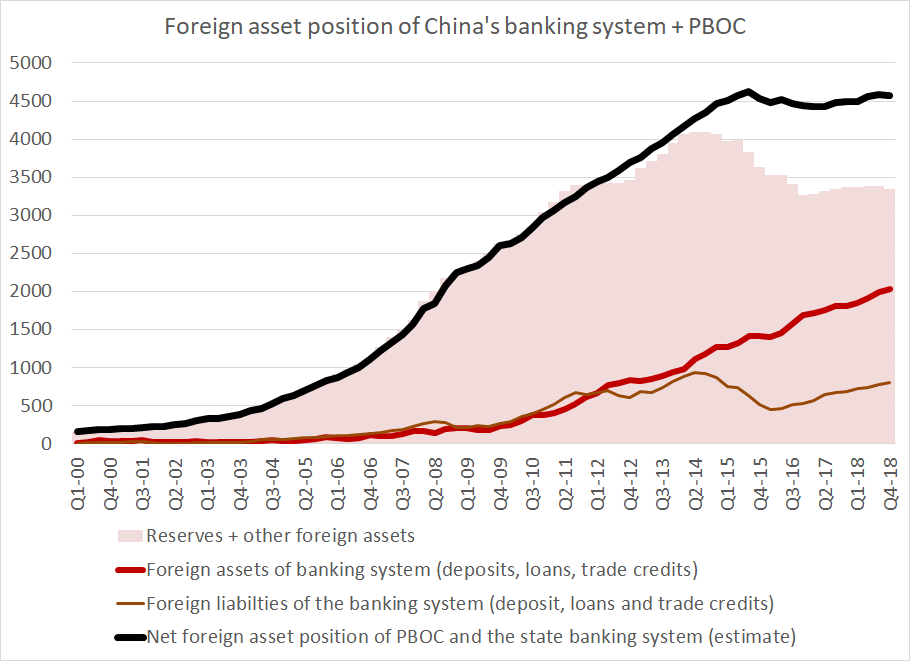

ii)THIS IS A HUGE PROBLEM!! China is witnessing a huge capital flight from its country

( Mish Shedlock)

4/EUROPEAN AFFAIRS

i)UK

ii)Europe

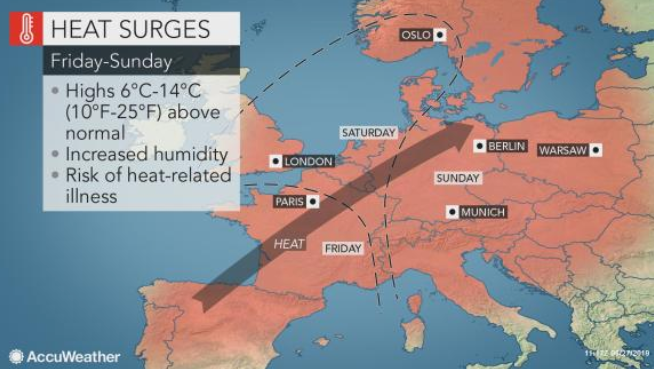

Huge heat wave hits Europe

(courtesy zerohedge)

iii) EU/USA/Iran

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)IRAN/USA

6. GLOBAL ISSUES

Famed Paul Singer is now warning of a huge 40% market crash..He tells you why.

(courtesy Paul Singer/Elliott Management/zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

( Chris Powell/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

II)MARKET TRADING/USA

ii)Market data/USA

Not good: Chicago’s National PMI plunges into contraction collapsing from 54.2 down to 49.7. A good indicator of problems in the Chicago mfg area

(courtesy zerohedge)

iii)USA ECONOMIC/GENERAL STORIES

a)This is terrifying: Bubonic plague in LA is becoming a reality…California is now on the verge of becoming a third world state

(courtesy Mac Slavo/SHFTPlan.com)

b)An extremely important read and this is in continuation of previous commentaries. Brandon Smith believes that Powell may not lower rates and he will continue to run off his balance sheet. Why? The Fed wants to implode the uSA economy. He explains why

SWAMP STORIES

Let us head over to the comex:

3873 X 5000 OZ PER CONTRACT = 19,330.000 OZ

we had 1 dealer entry:

i) Into Delaware: 1399.92 oz

total dealer deposits: 1399.92 oz

We had 0 kilobar entries

iii) Into Scotia: 3500.0000 oz ???

total gold withdrawals; nil oz

FOR THE JULY 2019 CONTRACT MONTH)Today, 0 notice(s) were issued from JPMorgan dealer account and 272 notices were issued from their client or customer account. The total of all issuance by all participants equates to 371 contract(s) of which 88 notices were stopped (received) by j.P. Morgan dealer and 26 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account and 0 notices by the squid (Goldman Sachs)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JULY /2019. contract month, we take the total number of notices filed so far for the month (371) x 100 oz , to which we add the difference between the open interest for the front month of JULY. (424 contract) minus the number of notices served upon today (371 x 100 oz per contract) equals 42,400 OZ OR 1.3188 TONNES) the number of ounces standing in this NON active month of JULY

Thus the INITIAL standings for gold for the JULY/2019 contract month:

No of notices served (371 x 100 oz) + (424)OI for the front month minus the number of notices served upon today (371 x 100 oz )which equals 42,400 oz standing OR 1.3188 TONNES in this NON active delivery month of JULY.

SURPRISINGLY LITTLE TO NO GOLD HAS BEEN ENTERING THE COMEX VAULTS AND WE HAVE WITNESSED THIS FOR THE PAST YEAR!! WE HAVE ONLY 10.0438 TONNES OF REGISTERED ( GOLD OFFERED FOR SALE) VS 1.3188 TONNES OF GOLD STANDING// THEY SEEM TO BE USING CONSIDERABLE GOLD VAPOUR TO SETTLE UPON UNSUSPECTING LONGS.

total dealer silver: 91.127 million

total dealer + customer silver: 306.313 million oz

The total number of notices filed today for the JULY 2019. contract month is represented by 2620 contract(s) FOR 13,100,000 oz

To calculate the number of silver ounces that will stand for delivery in JULY, we take the total number of notices filed for the month so far at 2620 x 5,000 oz = 13,100,000 oz to which we add the difference between the open interest for the front month of JULY. (3866) and the number of notices served upon today (2620 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JULY/2019 contract month: 2620 (notices served so far)x 5000 oz + OI for front month of JULY((3866) number of notices served upon today (2620)x 5000 oz equals 19,330,000 oz of silver standing for the JULY contract month.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 54,533 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 99,123 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 99,123 CONTRACTS EQUATES to 495 million OZ 70.8% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -0.34% June 28/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.10% to NAV (JUNE 28/2019 )

Note: Sprott silver trust back into NEGATIVE territory at -0.34%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 13.77 TRADING 13.23/DISCOUNT 3.96

END

And now the Gold inventory at the GLD/

JUNE 28/WITH GOLD UP $.90 TODAY: ANOTHER 2.05 TONNES OF PAPER GOLD REMOVED AND THIS GOLD WAS USED IN ATTACKING GOLD AT THE COMEX/INVENTORY RESTS AT 795.80 TONNES

JUNE 27/WITH GOLD DOWN $6.10: ANOTHER HUGE WITHDRAWAL OF 1.76 PAPER TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 797.61 TONNES

JUNE 26/WITH GOLD DOWN $3.00: WE HAD A HUGE WITHDRAWAL OF 2.37 TONNES FROM THE GLD/INVENTORY RESTS AT 799.61 TONNES

JUNE 25/WITH GOLD UP $1.30 (AND WAY UP BEFORE THE BANKERS WHACKED) WE WITNESSED ANOTHER 1.95 TONNES OF PAPER GOLD ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 801.98 TONNES

JUNE 24/WITH GOLD UP $18.00 A MONSTROUS PAPER DEPOSIT OF 34.93 TONNES/INVENTORY RESTS AT 799.03 TONNES

JUNE 21/WITH GOLD UP $ 2.90, NO CHANGE IN GOLD INVENTORY: INVENTORY RESTS AT: 764.10 TONNES

June 20/WITH GOLD UP $47.95, NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 19 WITH GOLD DOWN $1.65: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONES

JUNE 18/JUNE 18/WITH GOLD UP $7.60: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 17/WITH GOLD DOWN $1.65 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 764.10 TONNES

JUNE 14/ WITH GOLD UP $1.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.40 TONNES OF PAPER GOLD INTO THE GLD///INVENTORY RESTS AT 764.10 TONNES

JUNE 13/WITH GOLD UP $6.60 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 759.70 TONNES

JUNE 12/WITH GOLD UP $7.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 756.18 TONNES

JUNE 11/WITH GOLD UP $1.65 CENTS TODAY: A TINY CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .24 TONNES AND THIS IS TO PAY FOR FEES/INVENTORY RESTS AT 756.18 TONNES

JUNE 10/WITH GOLD DOWN $16.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES/INVENTORY RESTS AT 756.42 TONNES

JUNE 7/WITH GOLD UP $3.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 6/WITH GOLD UP $8.40 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 5 WITH GOLD UP $6.00 TODAY/STRANGE: A WITHDRAWAL OF 2.06 TONNES FROM THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 4/WITH GOLD UP 0.85 TODAY: A MONSTROUS PAPER GAIN OF 16.44 TONNES/GLD INVENTORY RESTS AT 759.65 TONNES

JUNE 3/WITH GOLD UP $17.50 TODAY: ANOTHER BIG CHANGE, A DEPOSIT OF 2.35 TONNES OF GOLD INTO THE GLD//

MAY 31/WITH GOLD UP $17.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GLD INVENTORY RESTS AT 740.86 TONNES

MAY 30: WITH GOLD UP $6.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES/INVENTORY RESTS AT 740.86 TONNES

MAY 29/WITH GOLD UP $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 737.34 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JUNE 28/2019/ Inventory rests tonight at 795.80 tonnes

*IN LAST 617 TRADING DAYS: 138.96 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 517 TRADING DAYS: A NET 26.67 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JUNE 28/WITH SILVER UP 6 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.394 MILLION OZ//

JUNE 27/WITH SILVER DOWN 7 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.575 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.394 MILLION OZ//

JUNE 26/WITH SILVER UP 17 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 25/WITH SILVER DOWN 25 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ.

JUNE 24/WITH SILVER UP 11 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 21/WITH SILVER DOWN 22 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 20/WITH SILVER UP 53 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 19/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ/

JUNE 18 WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ

JUNE 17/WITH SILVER UP XXX CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ//

JUNE 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 12/WITH SILVER UP 4 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.413 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 11/WITH SILVER UP 10 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 10/WITH SILVER DOWN 38 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 7/WITH SILVER UP ANOTHER 12 CENTS, NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 6/WITH SILVER UP ANOTHER 9 CENTS TODAY: A FAIR SIZE DEPOSIT OF 630,087 OZ//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 5/WITH SILVER UP 4 CENTS TODAY: A HUGE PAPER DEPOSIT OF 2.396 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 314.434 MILLION OZ//

JUNE 4/WITH SILVER UP 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

JUNE 3/WITH SILVER UP 19 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

MAY 31/WITH SILVER UP 6 CENTS TODAY: A DEPOSIT OF 422,000 OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 312.038 MILLION OZ/

May 30/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ///

MAY 29/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 28/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 24/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ/

MAY 23/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 22/WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 311.616 MILLION OZ

MAY 21: WITH SILVER DOWN 3 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV; A WITHDRAWAL OF 750,000 OZ///INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 20/WITH SILVER UP 6 CENTS:NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.366 MILLION OZ

Credit Suisse: Gold May Retest Record High of $1,921

28, June

Gold prices are marginally higher today and look set to have their best monthly gain since June 2016.

Spot gold was up 0.2% at $1,413.60 per ounce in late morning trading in Europe. Gold has risen over 8% this month so far. A monthly close above $1,400/oz will be positive from a technical trading perspective.

Gold prices have surged to the highest since 2013 as the U.S. and global economy slows and due to the likelihood of a return to ultra loose monetary policies. Rising geopolitical tensions in the Middle East and between an aligned Iran, Russia and China versus the U.S. is also leading to safe haven demand. U.S.-Iran relations have deteriorated sharply whereby war has become a very real possibly alas.

Trade, economic and geopolitical uncertainty have seen safe haven demand return and pushed prices higher. There are real concerns ahead of the very important trade talks between China and the United States this weekend.

The meeting between Trump and Xi Jinping may determine the next phase in this dispute and whether the U.S.-China trade war deescalates or escalates.

Gold traders will be reluctant to go short today due to the scale of risks ahead of the likely Trump and Xi talks. Indeed some may move to cover their short positions as if there is no progress in ending the year-long trade dispute or indeed tensions escalate, gold will likely go higher.

Gold’s mood music has changed radically in the last month and banks, hedge funds and other institutions internationally have become much more bullish on gold. They are revising upwards their price forecasts for gold in 2019 and the coming years.

Credit Suisse and Morgan Stanley are two such institution and they see gold having strong gains in the second half of 2019.

Credit Suisse analysts, like us, see gold returning to it’s record nominal high of $1,921/oz.

“Bigger picture though, given the magnitude of the base, which has taken six years to form, we suspect we could even see a retest of the $1,921 record high,” according to David Sneddon, global head of technical analysis at Credit Suisse.

Gold has established a multiyear base that could provide the platform for a “significant and long- lasting rally” for gold, he said. We concur with this view and indeed are more bullish as we see gold going to well over $3,000/oz in the long term

-END-

ii) Physical stories courtesy of GATA/Chris Powell

Ted Butler in his latest piece wonders why the government is leaving JPMorgan alone. Maybe it is because JPMorgan is the real broker for the uSA government and anything the government does it legal?

(courtesy Chris Powell/GATA)

Ted Butler: Stranger than fiction

Submitted by cpowell on Thu, 2019-06-27 16:18. Section: Daily Dispatches

12:08p ET Thursday, June 27, 2019

Dear Friend of GATA and Gold:

In his new essay, “Stranger than Fiction,” silver market rigging whistleblower Ted Butler wonders why the U.S. Justice Department and Commodity Futures Trading Commission penalize some investment houses for rigging the monetary metals markets while leaving JPMorganChase free to rig them.

Here’s a possibility: JPMorganChase is acting as broker for the U.S. government, which, under the Gold Reserve Act of 1934, as amended since then, is fully authorized to rig any market in the world.

…

Indeed, JPMorganChase’s chief executive, Jamie Dimon, and the former chief of its commodity desk, Blythe Masters, replying a few years ago to complaints of rigging in the monetary metals markets, said the bank had no position of its own in those markets and traded them only for clients.

Here’s Masters saying so on CNBC in 2012, beginning at the 2:35 mark:

https://www.youtube.com/watch?v=gc9Me4qFZYo

Of course nobody but GATA has ever asked JPMorganChase if the clients for whom the bank trades the monetary metals markets include governments and central banks. The bank refused even to acknowledge GATA’s inquiry.

Now if CNBC or some other major financial news organization asked the question, was brushed off, and reported the brushoff, that might be the beginning of change. But the first rule of mainstream financial journalism these days is: Never put a critical question about market intervention to a government or central bank. It might spoil their party.

Butler’s commentary is headlined “Stranger than Fiction” and it’s posted at GoldSeek’s companion site, SilverSeek, here —

http://silverseek.com/commentary/stranger-fiction-17678

— and at 24hGold here:

http://www.24hgold.com/english/news-gold-silver-stranger-than-fiction.as…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

Stranger Than Fiction

|

June 27, 2019 – 8:53am

Yesterday, the Department of Justice and the Commodity Futures Trading Commission announced yet another settlement, both criminal and civil, for “spoofing” and market manipulation in COMEX precious metals, this time against Merrill Lynch, a unit of Bank of America. The infractions occurred hundreds of times starting at least in 2008 and continuing through 2014. While Merrill Lynch and Bank America settled criminal charges via a deferred prosecution agreement and a $25 million fine, separate criminal charges are pending against a number of former individual traders.

https://www.cftc.gov/PressRoom/PressReleases/7946-19

Considering that a straight criminal charge and/or conviction could easily have resulted in, effectively, putting Merrill Lynch out of business (many cities, states and government entities are forbidden from doing business with convicted felons), Merrill and BAC got off easy. For the umpteenth time, price manipulation is the most serious market crime possible and Merrill just dodged a bullet that could have been fatal.

Not so lucky, of course, were the many victims of Merrill Lynch’s criminal activities who are unlikely to collect a penny for the long-running gold and silver price manipulation. Apparently, this is what comes of high-level corporate crime in the US – a wrist slap of a fine, a dubious trophy on some prosecutor’s mantle and an avoidance of the real issues.

What makes this all stranger than fiction is that the settlement covers nearly the exact time period that the CFTC (with DOJ involvement according to the late Bart Chilton) was involved in a formal five year investigation into a COMEX silver investigation which ended in 2013 with no findings of wrongdoing. Neither the CFTC nor the Justice Department could find anything wrong with silver (or gold) back then, but now each can recite chapter and verse about all the wrongdoing that took place at that time. What are the odds that the CFTC could have been inundated with more allegations of a silver manipulation than any other complaint in its history and for it to conclude repeatedly those allegations had no substance, only to come back years later saying plenty was wrong? Thanks for nothing.

Strangest of all is that the regulators are doing everything possible to avoid the 800 pound gorilla in the room – the real precious metals manipulation being run by JPMorgan since it acquired Bear Stearns in 2008. You know, the one by which JPM was the largest futures contract short seller on the COMEX and then used the resultant depressed prices to accumulate massive amounts of physical gold and silver. Next to what JPMorgan has done over the past decade, the spoofing charges are relatively child’s play.

I will admit that spoofing (the entering and immediate cancellation of large orders solely intended to manipulate prices in the short term) was so repetitive and serious enough to result in the complete surrender by Merrill Lynch and Bank of America to everything alleged by the DOJ in return for the prize of “only” a deferred criminal prosecution agreement. And it is good that spoofing has finally been cracked down on as those of us who complained about it for years would attest. But spoofing is only one of many tools used in the real price manipulation run by JPMorgan.

One thing is certain – the DOJ has the means, should it so choose, to truly crack down on anyone for spoofing or market manipulation, including JPMorgan (since it has an ongoing case on that aided by a criminal guilty plea by a former trader). Complicating matters for JPMorgan is that, unlike Merrill, it already has in place an outstanding criminal deferred prosecution agreement with the DOJ from the Madoff scandal (how many such agreements are allowed before you are considered a stone-cold crook?).

There can be no doubt that the Justice Department went light on Merrill and Bank America to avoid the consequences and aftermath of a straight criminal finding, as was possible under the law. How would it impact the financial system and serve the public good to, effectively, put either out of business? That goes in spades for JPMorgan. But whereas spoofing is largely a thing of the past, JPMorgan still looms large in the much more significant ongoing silver and gold manipulation – or at least it has until very recently.

The Nov 6 announcement by the Justice Department of a criminal guilty plea by an ex-trader from JPMorgan for spoofing and market manipulation, as well as there being an ongoing investigation of same did not immediately bring an end to JPM’s real manipulation (contrary to my hopes and expectations at the time). I say this because on the rally in gold and silver prices that commenced a week after the DOJ’s announcement and that lasted until the end of February, JPMorgan did as it always had done on every silver and gold rally over the past 11 years, namely, sold short enough in COMEX futures to cap both rallies. Gold and silver prices then declined into the end of May and JPMorgan bought back all of its added COMEX short sales at a profit – the same as it had done continuously since early 2008. And yes, JPMorgan continued to accumulate physical silver as well.

Over the past four weeks, there has been a very spirited rally in gold and a much less than impressive rally in silver. Since May 28, gold has surged by as much as $160 (12.5%), while silver has struggled to rise by as much as a dollar or so (7%). The only documented cause for the rise in the gold price has been massive managed money buying in COMEX gold futures, although the past few days has seen some significant net deposits in GLD, reflecting net investment buying due to the COMEX-induced price increase. While there has also been significant managed money buying in silver, that buying has not caused silver prices to rise as sharply as gold prices, either because it was not sufficient enough or because the sellers were much more aggressive in silver than they were in gold.

The great unknown at this point, particularly in silver, is the extent of short selling by JPMorgan into this rally. My sense is that JPM has been a moderate short seller in gold, but I am unsure about its short selling in silver. JPMorgan did go into the silver rally net long by about 6000 contracts or so, and while I believe it has sold out its longs (at profits), I’m not sure if it has added COMEX silver short positions. This Friday’s COT report might shed some light on this, as will the following COT and Bank Participation reports scheduled for Monday July 8.

As far as what to expect in Friday’s COT report, I’m going to stick with my previous guesses of 50,000 net contracts in gold and 15,000 net contracts in silver for managed money buying and commercial selling, although higher numbers in gold wouldn’t surprise me. My main concern is what JPMorgan may have done.

I’ve noticed a literal explosion of commentaries extolling the virtues of an impending silver price explosion, given how badly it has lagged the gold rally. I’m certainly not about to argue with an explosion in silver prices, although I do note with curiosity that few expecting such an explosion point to developments on the COMEX. If we do get an explosion in silver prices, it must be related to COMEX positioning and, more specifically, the positioning (or lack thereof) of JPMorgan.

With so many managed money contracts having been bought over the past four weeks, leading to what must be considered a bearish market structure in gold, it wouldn’t be surprising to witness a price setback. On the other hand, we are still miles above the key moving averages in gold (not so in silver), and if the managed money traders remain true to past form, they will be reluctant to sell until such averages are penetrated to the downside. The most comparable previous time in gold to now was the run up in 2016, when massive managed money buying wasn’t liquidated until much later in the year.

To be sure, if we do experience a sharp selloff in gold or silver (not something I’m predicting), it will be for the sole reason of managed money selling on the COMEX. Still lost in all the new talk of Justice Department findings of manipulation through spoofing is the recognition that the proof of a bigger ongoing manipulation is right in front of us. Why should a handful of large paper traders on the COMEX dictate to the rest of the world what prices should be? What is strangest of all is that the manipulation is so obvious and in your face that most can’t seem to focus on it. Speculative paper positioning should never set prices, yet it clearly does.

It seems to me that the Justice Department sees the silver manipulation clearly, but is reluctant to drop the hammer on JPMorgan for fear of the consequences of finding JPM criminally culpable. It just demonstrated that in the case against Merrill Lynch. At the same time, however, neither can the DOJ address simple questions directed to it.

http://silverseek.com/commentary/questions-only-doj-can-get-answered-17543

Unfortunately for the DOJ, the case against JPMorgan is so straightforward so as to be inescapable. Being the largest paper short seller for more than a decade and then using the resultant depressed prices to accumulate more physical silver (and gold) than anyone in history is such a cut and dried market manipulation that a jury of 12 year olds could decide the matter in minutes. Yes, I understand that putting JPMorgan out of business works against the collective interest, but so does letting these crooks continue to manipulate.

The only practical alternative is for the Justice Department to force JPMorgan to end the silver (and gold) manipulation quietly and without the repercussions of straight criminal charges. Regardless of the precise format such an order would involve, the direct visible result would be an explosion in the price of silver, practically the minute JPM lifts its heavy hand off the price. I thinks most silver investors and producers could live with that.

Ted Butler

June 27, 2019

END

For your interest..

Gold’s naked shorts may have to rely on NASA’s asteroid exploration

Submitted by cpowell on Thu, 2019-06-27 20:49. Section: Daily Dispatches

Space Gold Rush: NASA to Explore Asteroid 16 Psyche, Which Is So Valuable It Could Crash the World’s Economy

By Margi Murphy

The Sun, London

January 18, 2018

NASA is planning a mission to an asteroid so valuable it could cause the world’s economy to collapse.

The mysterious “metal world” was formed during the turbulent birth of our solar system.

It is valued at L8,072 quadrillion ($10,000 quadrillion), according to Lindy Elkins-Tanton, the lead scientist on the NASA mission.

…

But bringing back an asteroid of this value could completely wipe out the economy.

Fortunately, Nasa doesn’t have the tech to lasso any soaring space rocks and drag them back to our planet. But the space agency is planning to visit it by 2023….

… For the remainder of the report:

https://www.thesun.co.uk/news/2642475/nasa-to-explore-asteroid-16-psyche…

* * *

END

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.8693/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.8740 /shanghai bourse CLOSED DOWN 17.91 POINTS OR 0.60%

HANG SANG CLOSED DOWN 78.80 POINTS OR 0.28%

2. Nikkei closed DOWN 62.75 POINTS OR 0.29%

3. Europe stocks OPENED ALL GREEN EXCEPT

USA dollar index UP TO 96.18/Euro RISES TO 1.1376

3b Japan 10 year bond yield: FALLS TO. –.16/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.73/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 59.57 and Brent: 65.75

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO -.33%/Italian 10 yr bond yield DOWN to 2.09% /SPAIN 10 YR BOND YIELD DOWN TO 0.41%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.42: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.44

3k Gold at $1412.60 silver at: 15.26 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 12/100 in roubles/dollar) 62.93

3m oil into the 59 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.51 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9754 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1103 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.33%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.01% early this morning. Thirty year rate at 2.53%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.7697..

Nervous Markets Coiled In Anticipation Ahead Of Critical Trump-Xi Meeting

US futures and European stocks edged higher albeit in a low-volume session, with bond markets trading sideways ahead of G-20 kickoff in Osaka, as markets took early comments from Xi and Trump broadly in stride even as growing uncertainty ahead of the critical meeting between the two world leaders deterred traders from making bold directional bets.

After Asian stock markets slipped, European shares were marginally higher, with the pan-European STOXX 600 index up 0.08%. Germany’s DAX index was the biggest gainer, up 0.36% percent on the day. Europe’s Stoxx 50 rose +0.3%, while the e-mini S&P future tracked Europe, and was up +0.2%.

In the day’s main event, Trump and Xi will meet on the sidelines of the G20 summit this weekend in Osaka, Japan, for talks that could help resolve a year-long trade war between China and the United States, as signs proliferate of rising risks to global growth. Of course, it is just as likely that nothing happens.

“Market participants are taking a cautious approach ahead of this high-level meeting as hopes for a material breakthrough are low,” said ADSS head of research, Konstantinos Anthis. “This is a stellar opportunity for the two leaders to find some common ground and unless they do so, equities will likely push lower as a prolonged period of tariffs on each other’s exports will take a heavier toll on both economies and global growth.”

Due to the uncertainty, the MSCI All Country World Index was up just 0.04% on the day; the index was set to break a three-week streak of gains but also on course for its best month since January, gaining nearly 6% in June as equities rallied globally on the back of a pivot towards easier monetary policy from major central banks. That shift came after a breakdown in trade negotiations between the United States and China earlier this year, and has markets betting on an interest rate cut from the U.S. Federal Reserve as early as the next policy meeting in July.

On Thursday, China’s central bank also joined the party when it pledged to support a slowing economy, ahead of the release of data that is expected to show China’s factory activity shrank for a second consecutive month in June.

That, however, was not enough to boost Asian markets as the MSCI Asia-Pacific index ex-Japan fell 0.1% with energy and material firms leading Asian shares lower. Japan’s Topix gauge slipped 0.1%, driven by Daikin Industries and Central Japan Railway, even as Japanese factory output beat estimates; the Nikkei stock index ended down 0.29%, while Chinese blue chips fell 0.24% on Friday and Hong Kong’s Hang Seng lost 0.32%. Australian shares shed 0.71%.

The Shanghai Composite Index retreated 0.6%, with PetroChina Co. and Kweichow Moutai among the biggest drags. The People’s Bank of China softened its tone on financial risk management, indicating an effort to allay fears for a possible funding squeeze. The S&P BSE Sensex Index dropped 0.3%, as traders gauged the scope of possible stimulus in a federal budget next week. Reliance Industries, Tata Consultancy Services and HDFC Bank dragged the Indian benchmark lower.

In Europe, stocks traded in proximity to unchanged, while euro zone government bond yields hovered near record lows in many cases ahead of the release of inflation data for the bloc. With the euro zone reporting inflation of 1.2% for the month of June — well short of the European Central Bank’s target of just below 2% — investors held on to government bonds in early trade. Core European yields steady to 1bp higher, with 10-yr BTP/bund spread 6bps tighter at 240bps. UST yields steady to 1bp higher in the 2-yr through 10-yr maturities.

Heading into the G-20, on Thursday White House economic adviser Larry Kudlow said that Trump had agreed to no preconditions for the meeting with Xi and is maintaining his threat to impose new tariffs on Chinese goods. Kudlow also dismissed a Wall Street Journal report that China was insisting on lifting sanctions on Chinese telecom equipment giant Huawei Technologies Co Ltd as part of a trade deal and that the Trump administration had tentatively agreed to delay new tariffs on Chinese goods.

“I’m not sure the Americans can deliver what the Chinese want and the Chinese don’t want to deliver what the Americans want,”said Greg McKenna, strategist at McKenna Macro, adding that he sees an “extend and pretend” outcome, in which Chinese and U.S. officials agree to continue talks, as the most likely outcome of the weekend meeting. Regardless of the outcome, McKenna said, “we will not be in a holding pattern on Monday morning.”

Currency markets also reflected caution, with the Japanese yen reversing a three-day losing streak against the dollar. Bloomberg dollar index traded lower again by 0.1%, set to turn in its worst monthly performance since the start of 2018. Bets on interest rate cuts from the Fed have pushed the dollar index down 1.7% this month. All G-10 currencies ex-NOK gaining versus the greenback. In commodities, gold trades +0.3% at $1414, with both Brent ($66.24) and WTI ($59.20) lower.

In commodity markets, trade worries continued to weigh on oil, with U.S. crude losing 0.3% to $59.26 a barrel and global benchmark Brent crude down 0.36% to $66.31 per barrel. The weak dollar and uncertainty over global trade saw gold rebound after dipping below $1,400 per ounce on Thursday. Spot gold was last traded at $1,414.15 per ounce, up 0.35%, but down from earlier highs.

Expected data include personal income and spending, as well as University of Michigan Sentiment. Constellation Brands is reporting earnings.

Market Snapshot

- S&P 500 futures up 0.3% to 2,938.50

- STOXX Europe 600 up 0.3% to 383.23

- MXAP down 0.09% to 160.21

- MXAPJ down 0.1% to 528.48

- Nikkei down 0.3% to 21,275.92

- Topix down 0.1% to 1,551.14

- Hang Seng Index down 0.3% to 28,542.62

- Shanghai Composite down 0.6% to 2,978.88

- Sensex down 0.2% to 39,499.81

- Australia S&P/ASX 200 down 0.7% to 6,618.77

- Kospi down 0.2% to 2,130.62

- German 10Y yield rose 0.7 bps to -0.313%

- Euro up 0.2% to $1.1390

- Italian 10Y yield fell 0.7 bps to 1.772%

- Spanish 10Y yield fell 0.7 bps to 0.389%

- Brent futures down 0.4% to $66.32/bbl

- Gold spot up 0.3% to $1,413.71

- U.S. Dollar Index down 0.1% to 96.07

Top Overnight News from Bloomberg

- President Trump wants a weaker dollar to help boost exports, and is counting on the Federal Reserve to help make that happen. But Fed Chair Jerome Powell has made clear it’s not his job

- Euro-area inflation was unchanged well below the European Central Bank’s goal in June, despite a faster-than-expected pickup in underlying prices. The rate of growth was 1.2%, in line with economists’ estimates

- Trump lightheartedly asked Russian President Vladimir Putin not to interfere in the upcoming U.S. election during a meeting at the G-20 summit, their first since Special Counsel Robert Mueller documented alleged Kremlin efforts to manipulate the 2016 vote

- With speculation still bubbling that the Bank of Japan’s next move will be further stimulus, a BOJ board member tried to rule out a lowering of Japanese interest rates, saying they were already close to an unfavorable tipping point

- Hedge funds have turned bullish on the yen for the first time in a year amid rising global tensions, even as Japanese retail investors have boosted shorts on the currency to the most in 15 months betting sinking bond yields will spur outflows

- Policy makers in Beijing are trying to funnel cash into the economy while warding off a re-inflation of the property market bubble, a task made doubly hard by the uncertainty generated by the intensifying trade war

Asian equity markets were subdued amid book squaring heading into the end of H1 and ahead of the upcoming Trump-Xi meeting at the G20. ASX 200 (-0.7%) was led lower by mining names with BHP pressured as it is expected to pay AUD 250mln as settlement in the royalty dispute with Western Australia, although downside for the broader market was limited by outperformance in tech and financials, while Nikkei 225 (-0.3%) also suffered losses in the commodity-related sectors and with exporters weighed by detrimental flows into the currency. Hang Seng (-0.3%) and Shanghai Comp. (-0.6%) weakened amid continued PBoC inaction and as trade uncertainty remained rife heading into the US-China showdown at the G20. Finally, 10yr JGBs tracked the upside in their US counterparts with prices lifted by safe-haven flows and amid the BoJ presence in the market for JPY 720bln of government bonds in the belly to super-long end.

Top Asia News

- Australia Pension Managers in Talks to Create A$22 Billion Fund

Major European indices are just into positive territory after a tentative and mixed/flat open [Euro Stoxx 50 +0.3%] as the G20 summit gets underway and markets move into month, quarter and half end. Within the bourses the SMI (-0.2%) is the modest underperformer as we approach the Sunday expiry of temporary measures introduced by the EU which allow Swiss Co’s to be traded on EU exchanges; most recently the Swiss Government stated they will block trading of Swiss shares in the EU following the Commission stating they do not see reason to extend the measures beyond June. In terms of this morning notable movers, significantly outperforming at the top of the Stoxx 600 are Merlin Entertainment (+14.0%) after reports that the Co. had received a GBP 6bln offer from the Lego Family, Blackstone & a Canadian fund. On the back of yesterday’s Fed stress tests where all banks capital plans were approved Deutsche Bank (+3.7%) are the outperforming financial name; however, Credit Suisse (-1.0%) are lagging their peers after receiving only conditional approval and being the Co. must now address the relevant weaknesses.

Top European News

- Rutte Says the EU Must Intervene Over Italy’s Public Finances

- Italy May Nominate ECB Chief Draghi for Top EU Job, Stampa Says

- Volkswagen’s Truck Unit Opens Flat in Frankfurt Trading Debut

- Berlin Scares Off Banks Targeting the Rich as Fintechs Boom

In FX, the broad Dollar and Index remain in a relatively confined 96.05-25 range as markets gear up for tomorrow’s US-Sino showdown. US President Trump said that he believes the meeting with his Chinese counterpart (at 0330BST tomorrow) will be “productive at minimum”. The comments somewhat reaffirmed market expectations for a restart in talks, but no breakthrough. The index currently hovers closer to the bottom of the intraday range ahead of the psychological 96.00 and its 200 WMA at 95.97, while to the upside, technicians will be eyeing resistance at 96.37 (50 WMA). Meanwhile, US Core PCE and comments from Fed’s Daly are unlikely to sway the Buck ahead of the weekend’s risk event. In a similar vein, CNH is caged within a tight 6.86-88 range vs Greenback but is ultimately flat, having briefly dipped below its 50 DMA at 6.8675.

- EUR, GBP, NZD, AUD, JPY, CHF – All largely benefitting from a marginally softer USD, albeit the EUR also feels tailwind from touted month-end EUR/GBP buying, which aided the pair climb to levels last seen in January. EUR was little moved by the release of overall encouraging inflation data in which the core and super-core figures topped estimates while the headline matched expectations. EUR/USD remains near the top of a 1.1360-90 intraday band with around 1bln in options scattered around strikes 1.1375-85. Meanwhile, the GBP is benefiting slightly less from a softer USD amid the aforementioned EUR/GBP buying as Cable remains within a tight band under 1.2700. Elsewhere the AUD and NZD have similarly jumped on the back of a softer Buck and over close to HODs of 0.7017 and 0.6710 respectively, albeit off best levels. Finally, the safe heaven FX follow suit from the tentative tone in the FX market, although positioning before the end of the trading day may sway the currencies. USD/JPY hovers just above the near the bottom of a 107.57-83 range with 2.1bln in options expiring at 107.50 at today’s NY cut.

- NOK, SEK – The Swedish Crown has pared back recent losses vs. the EUR after dismal retail sales extended the pair’s intraday upper bound to 10.5850, albeit the SEK has since pared back those losses and trades flat on the day thus far. Meanwhile, the NOK was little fazed by the regional unemployment figures and fares slightly worse but ultimately on the back of softer energy prices.

In commodities, WTI and Brent futures are cautious ahead talks between US President Trump and his Chinese counterpart. The benchmarks found supports USD 59/bbl and USD 66/bbl respectively but remain subdued on the day. Post-G20, the energy market will be looking forward to the delayed OPEC+ meeting in which the oil producers are expected to roll over the output curbs but still seem split on potential revisions to the pact. Russia still remains the unknown, despite Energy Minister Novak stating that consensus will be found in July, however “the potential downside risk in the market in the event of a no deal will likely be enough to persuade Russia to continue” ING says. Back to G20, analysts remind us that talks between Russian President Putin and Saudi Crown Prince Mohammed Bin Salman will also be monitored as it may influence the cartel’s decision. Elsewhere, gold is marginally firmer on the day as a function of a weaker Dollar. In light of the recent gold rally, UBS has raised its 3-month gold forecast to USD 1430/oz from USD 1380/oz. Meanwhile, Copper remains above the USD 2.7/lb as the softer USD outweighs the supply resumptions from the end of strikes at the Coldeco Chuquicamata mine. The workers, after 14 days, have accepted the latest offer and miners returned to work today.

US Event Calendar

- 8:30am: Personal Income, est. 0.3%, prior 0.5%; Personal Spending, est. 0.5%, prior 0.3%

- 8:30am: PCE Deflator MoM, est. 0.2%, prior 0.3%; PCE Deflator YoY, est. 1.5%, prior 1.5%

- 9:45am: MNI Chicago PMI, est. 53.5, prior 54.2

- 10am: U. of Mich. Sentiment, est. 97.9, prior 97.9; Current Conditions, prior 112.5; Expectations, prior 88.6

DB’s Jim Reid concludes the overnight wrap

I’m at a big 2-day macro DB hosted conference at the moment with investors representing over 25 trillion of investable capital attending. There were a few shows of hands through day one to gauge the mood and a couple of the interesting takeaways from me was that about 90% expected 10yr US yields to go to 1.70% next versus 2.30%, and around a similar percentage expected the Euro construct to look similar in 10 years time than it does today (in terms of countries in it) – so relatively sanguine about Italy. On the second question I was one of the 10%! The conference was held in beautiful 30 degree London sunshine but that seems to have been near Arctic like conditions compared to what was the hottest June day on record in mainland Europe. My wife has gone away on her own for a long weekend to Scotland to cool down and is away from the children overnight for the first time since they started to come along like buses nearly four years ago. The problem with that is I’m petrified as I now take sole charge of them all for the longest period of time so far in my brief (and sometimes chaotic) parenting career. Given the weather, immediately after I type this I’m going to search for blow up paddling pools on Amazon Prime! What could possibly go wrong?

The same might be said about the G-20 that starts today. A resolution might be highly unlikely, but will markets have any greater clarity as to which path trade talks travel down next in a little under 24 hours’ time? Presidents Trump and Xi are scheduled to meet at 11.30am local time tomorrow morning. That is 3.30am in London and 10.30pm tonight in New York for those who want to base their whole weekend around it. Hopefully it won’t interfere with my solo parenting. Unsurprisingly, the headlines second-guessing what may or may not happen have picked up in recent days with the latest being the WSJ story yesterday suggesting that Xi will insist on any trade truce including the US lifting the Huawei ban, though he will also reportedly offer new support for the US vis-à-vis Iran and North Korea. Given the rhetoric that surrounded the Huawei ban when it was announced, plus the fact that law enforcement is theoretically separate from trade policy, the bar for progress on that front feels high. That said, Larry Kudlow did say that “we may change our views” if “China is willing to offer us a good deal,” so maybe there is scope for some movement.

We should note that by the time we hit send on this Trump is due to meet with Russia’s Putin so that could be one to watch for markets. The early headlines out of the summit are unsurprisingly about trade with Trump saying that he expects to announce “very big” trade deals with both Japan and India while Xi in a meeting with African leaders ahead of the summit condemned protectionism and “bullying practices,” saying, “any attempt to put one’s own interests first and undermine others’ will not win any popularity”. At the BRICS nations gathering, Xi said that protectionism is “destroying the global trade order… This also impacts common interests of our countries, overshadows the peace and stability world wide.” On Iran, Trump said that there was “absolutely no time pressure” to deal with the country. Meanwhile on the WTO, Indian PM Modi called for its reform while Russian President Putin said that “We consider counter-productive any attempts to destroy WTO or to lower its role”. Separately, a White House official said Trump wanted to promote to Abe and Modi “a resilient quality secure infrastructure” – a reference to the US push with allies to keep Huawei out of next generation telecoms networks.

Asian markets are heading lower ahead of the anticipated meeting between Trump and Xi tomorrow amidst lower than average volumes. The Nikkei (-0.39%), Hang Seng (-0.56%), Shanghai Comp (-0.88%) and Kospi (-0.16%) are all down thereby partly erasing yesterday’s gains. Elsewhere, futures on the S&P 500 are up +0.10%. In terms of overnight data releases, Japan’s preliminary May industrial production came in at +2.3% mom (vs. +0.7% expected).

Also overnight and after the US market close, all 18 banks passed the qualitative US Fed stress test which was a positive surprise. The results for the US banks gave them the green light to proceed with their capital plans. The major firms all announced enhanced buyback and dividend programs and their share prices gained further in after-hours trading. Bank of America (+1.77% after hours) will buy back $30.9bn in stock, JP Morgan (+1.63%) will buy $29.4bn, and Wells Fargo (+1.21%) will buy $23.1bn. Goldman Sachs (+2.46%) and Morgan Stanley (+1.61%) announced buybacks of $7bn and $6bn, respectively. All the major firms boosted their dividends as well.

This followed a healthier day in US equities yesterday which culminated in the S&P 500 (+0.38%) halting a four-day slide. The NASDAQ (+0.73%) also closed higher while banks (+0.78%) led at a sector level even before the stress test results. The DOW (-0.04%) underperformed as Boeing slid -2.93% after US regulators found new safety risks in the troubled 737 Max aircraft after fresh tests. In Europe, the STOXX 600 ebbed and flowed in another fairly tight range before ultimately ending flat. Bond markets weren’t a lot more interesting, though treasuries resumed their recent rally, with 10y yields down -3.3bps and 2-year yields a more modest -2.6bps. Bunds traded down -1.8bps while peripheral bonds were near flat on the day. Oil (-0.15%) and Gold (flat) also had quiet sessions, but Bitcoin’s selloff went into overdrive (-16.09%) making it -22.85% lower from the peak just before the close the previous night. However, this morning in Asia the crypto currency is back up +3.64 taking month-to-date gains to +30.11%, which is still quite impressive but feels somewhat flat after reaching gain of +62.90% on the month late on Wednesday. In other currency markets, the dollar traded flat yesterday and EM currencies advanced +0.13%.