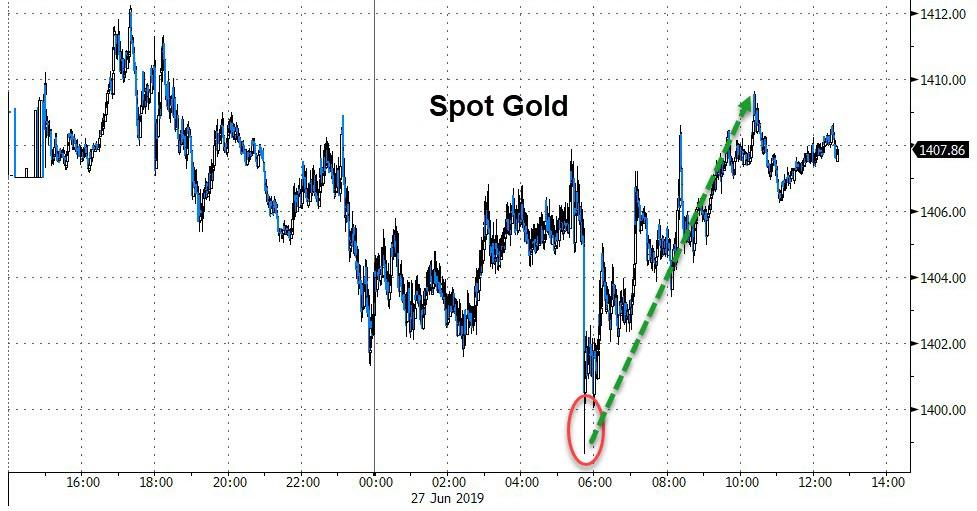

GOLD: $1408.90 DOWN $6.10 (COMEX TO COMEX CLOSING)

Silver: $15,25 DOWN 7 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1409.20

silver: $15.27

YOUR DATA…

FOR THE 5TH CONSECUTIVE DAY, A HUGE DISCREPANCY BETWEEN THE PRELIMINARY OI NUMBERS IN GOLD VS THE FINAL NUMBERS. TODAY OVER 6,000 CONTRACTS..AND THE CFTC STATES THAT THIS IS NOT MANIPULATIVE??

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 0/119

EXCHANGE: COMEX

CONTRACT: JUNE 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,411.600000000 USD

INTENT DATE: 06/26/2019 DELIVERY DATE: 06/28/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 H HSBC 109

657 C MORGAN STANLEY 15

905 C ADM 10 7

991 H CME 97

____________________________________________________________________________________________

TOTAL: 119 119

MONTH TO DATE: 2,522

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 119 NOTICE(S) FOR 11900 OZ (0.3701 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 2522 NOTICES FOR 252,200 OZ (7.8444 TONNES)

SILVER

FOR JUNE

0 NOTICE(S) FILED TODAY FOR NIL OZ/

total number of notices filed so far this month: 532 for 2,660,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

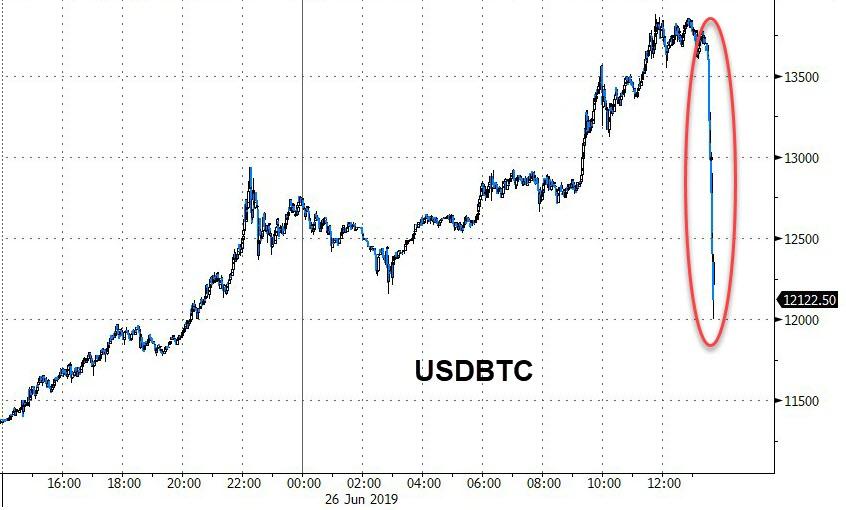

Bitcoin: OPENING MORNING TRADE : $ 12,014 DOWN 1054

Bitcoin: FINAL EVENING TRADE: $ 10,892 DOWN 2270 (bankers did a good job of fleecing bitcoin owners)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL A CONSIDERABLE SIZED 5869 CONTRACTS FROM 229,007 DOWN TO 223,138 DESPITE THE 17 CENT GAIN IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JUNE, 2371 FOR JULY. 0 FOR AUGUST, 1163 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 3523 CONTRACTS. WITH THE TRANSFER OF 3534 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3534 EFP CONTRACTS TRANSLATES INTO 17.67 MILLION OZ ACCOMPANYING:

1.THE 17 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

WE HAD CONSIDERABLE SHORT COVERING AT THE SILVER COMEX LAST NIGHT..AND MAJOR SPREADING LIQUIDATION.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

51,889 CONTRACTS (FOR 19 TRADING DAYS TOTAL 51,889 CONTRACTS) OR 259.445 MILLION OZ: (AVERAGE PER DAY: 2731 CONTRACTS OR 13.65 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JUNE: 259.445 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 37.05% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1140.22 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 5869, DESPITE THE 17 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 3534 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS WILL RESUME THEIR LIQUIDATION OF THE SPREAD TRADES FOR SILVER ONCE THE JUNE CONTRACT COMMENCES IN EARNEST….

TODAY WE LOST A CONSIDERABLE SIZED: 5869 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 3534 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 5869 OI COMEX CONTRACTS. AND ALL OF THIS LACK OF DEMAND HAPPENED WITH A 17 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.32 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.115 BILLION OZ TO BE EXACT or 159% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR 0 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

WITH RESPECT TO SPREADING: CONSIDERABLE LIQUIDATION OF OUR SPREADERS

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JUNE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE OPEN INTEREST DWLL BY A FAIR SIZED 3145 CONTRACTS, TO 574,460 WITH THE $3.00 PRICING LOSS WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING LIQUIDATION HAS STOPPED, THESE SPREADERS HAVE ALREADY MORPHED INTO SILVER AND THEY ARE INTO THE LIQUIDATION PHASE OF THEIR OPERATION.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 8481 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 8481 CONTRACTS, DEC> 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 574460. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A HUGE SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5336 CONTRACTS: 3145 CONTRACTS DECREASED AT THE COMEX AND 8481 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 5336 CONTRACTS OR 533600 OZ OR 16.59 TONNES. YESTERDAY WE HAD A LOSS OF $3.00 IN GOLD TRADING.…AND WITH THAT SMALL LOSS IN PRICE, WE HAD A STRONG GAIN IN GOLD TONNAGE OF 16.59 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 197,629 CONTRACTS OR 19,762,900 oz OR 614.70 TONNES (19 TRADING DAYS AND THUS AVERAGING: 10,401 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAYS IN TONNES: 614.70 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 614.70/3550 x 100% TONNES =17.31% OF GLOBAL ANNUAL PRODUCTION

PLEASE NOTE THE HUGE INCREASE IN THE USE OF THE EXCHANGE FOR PHYSICALS THIS MONTH COMPARED TO ALL OF DETHE OTHER MONTHS.

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2,869.59 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GOOD SIZED DECREASE IN OI AT THE COMEX OF 3145 WITH THE PRICING LOSS THAT GOLD UNDERTOOK ON YESTERDAY($3.00)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8481 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 8481 EFP CONTRACTS ISSUED, WE HAD AN GOOD SIZED GAIN OF 5336 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

8481 CONTRACTS MOVE TO LONDON AND 3145 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 16.59 TONNES). ..AND THIS INCREASE OF DEMAND OCCURRED DESPITE THE LOSS IN PRICE OF $3.00 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAD ZERO PRESENCE OF SPREADING ACCUMULATION IN GOLD ///TODAY/

we had: 119 notice(s) filed upon for 11900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $6.10 TODAY//

ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 1.76 TONNES

INVENTORY RESTS AT 797.85 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 7 CENTS TODAY:

A HUGE CHANGE WITH RESPECT TO SILVER INVENTORY AT THE SILVER SLV: A “PAPER” DEPOSIT OF: 2.575 MILLION OZ INT THE SLV

/INVENTORY RESTS AT 322.394 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A CONSIDERABLE SIZED 5869 CONTRACTS from 229,007 DOWN TO 223,138 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JUNE 0 CONTRACTS AND JULY: 2371 CONTRACTS FOR AUGUST: 0, FOR SEPT. 1163 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3534 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 5869 CONTRACTS TO THE 3534 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A FAIR LOSS OF 2335 OPEN INTEREST CONTRACTS BUT WE ALSO WITNESSED HUGE LIQUIDATION OF COMEX SPREADING CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 11.68 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY AND NOW 2.660 MILLION OZ FOR JUNE.

RESULT: A CONSIDERABLE SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 17 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 3534 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 20.51 POINTS OR 0.69% //Hang Sang CLOSED UP 399.44 POINTS OR 1.42% /The Nikkei closed UP 251.58 POINTS OR 1.19%//Australia’s all ordinaires CLOSED UP .40%

/Chinese yuan (ONSHORE) closed DOWN at 6.8785 /Oil UP TO 58.77 dollars per barrel for WTI and 65.91 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8785 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8782 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/USA

Pure nonsense! Why would the uSA agree to this deal with China offering nothing..this is going nowhere..there will be no deal

( zerohedge)

4/EUROPEAN AFFAIRS

i)UK

Mish Shedlock gives a terrific account on what is going on with Brexit. The key points he is making and I agree with Mish is that England will be far better off and the EU worse off. Germany as a big exporter will be damaged

a great read…

( Mish Shedlock/Mishtalk)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)IRAN/USA

6. GLOBAL ISSUES

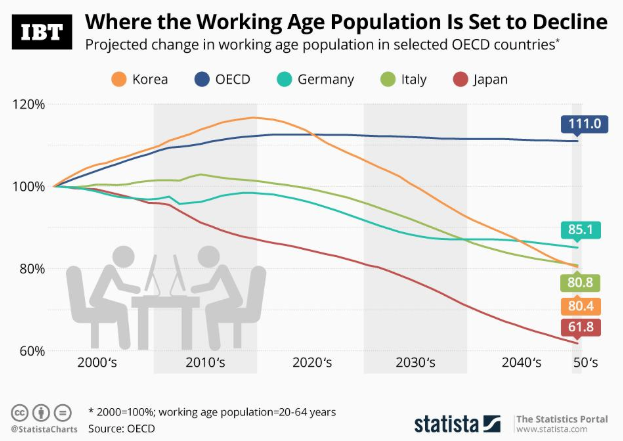

a)Not only is Japan facing a demographic doom but so is Germany, Italy, and South Korea as the total workforce in each of these countries will collapse by the year 2050

( zerohedge)

b)The global car industry is in big trouble as Ford is slashing 12,000 jobs across Europe

(courtesy zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

i)The bankers did it again to our crypto players..as bitcoin crashed last night, losing 1500 in minutes. This is why you do not invest in bitcoin.

( zerohedge)

ii)this will be good for the USA as Trump is ready to throw away the Obama era environmental restrictions that have stopped this huge project.

The owner of the mine is Northern Dynasty

( Bloomberg/GATA)

iii)The ECB gives the green light to Italy to claim that its gold held by the Bank of Italy belongs to the country and not the bank.

That should have been obvious

( Reuters/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

II)MARKET TRADING/USA

ii)Market data/USA

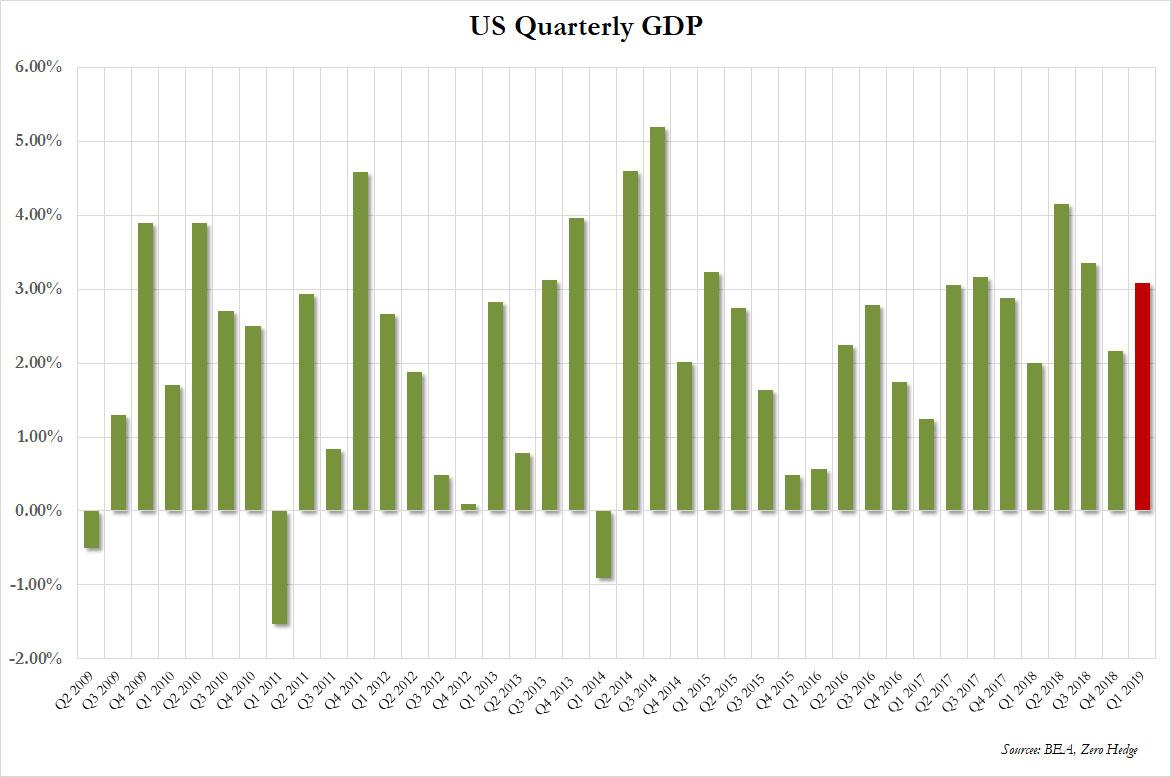

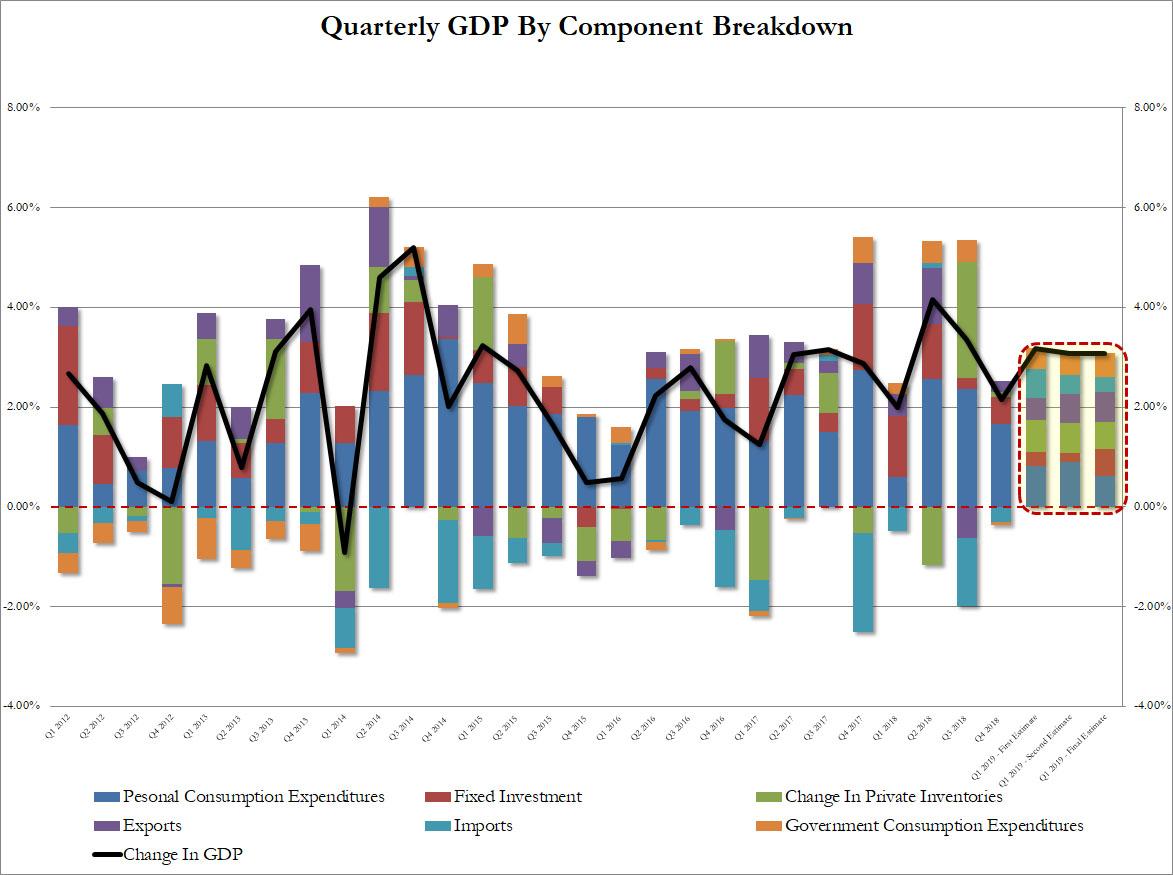

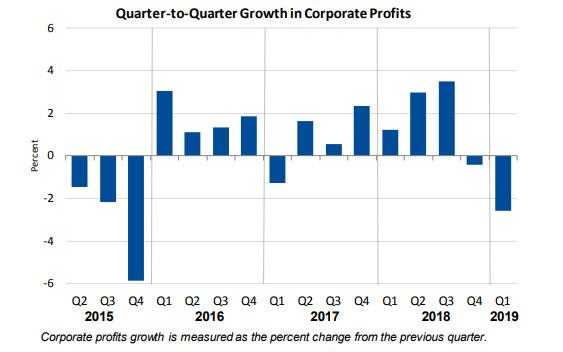

a)First quarter revised slightly lower as personal spending tumbles. Problem will be in core PCE which is heating up. This is the final reading for Q1 and it comes it at 3.1, falling from 3.2%

(courtesy zerohedge)

b)A good indicator of huge problems inside the uSA economy: pending home sales falter badly despite tubmling mortgage rates

iii)USA ECONOMIC/GENERAL STORIES

a)Last night, a new software glitch is found on the Boeing 737 Max and it results in “uncontrollable nosedives”

Does not look good for Boeing…

( zerohedge)

b)Shares of Boeing tumble on the news.

c)This has been the wettest year in many moons. It has decimated the corn crops! along with ancillary businesses(courtesy zerohedge)

SWAMP STORIES

a)Details on the first Democratic debate.

(courtesy zerohedge)

b)After closing the door on impeaching Trump, Pelosi also folds on the Senate emergency border bill and they will pass the $4.6 billion deal.

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; nil oz

FOR THE JUNE 2019 CONTRACT MONTH)Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 119 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account and 0 notices by the squid (Goldman Sachs)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JUNE /2019. contract month, we take the total number of notices filed so far for the month (2522) x 100 oz , to which we add the difference between the open interest for the front month of JUNE. (119 contract) minus the number of notices served upon today (119 x 100 oz per contract) equals 252,200 OZ OR 7.8444 TONNES) the number of ounces standing in this active month of JUNE

Thus the INITIAL standings for gold for the JUNE/2019 contract month:

No of notices served (2522 x 100 oz) + (119)OI for the front month minus the number of notices served upon today (119 x 100 oz )which equals 252,300 oz standing OR 7.8444 TONNES in this active delivery month of JUNE.

We GAINED 9 contracts or an additional 900 oz will stand as these guys refused to morph into London based forwards as well as negating a fiat bonus. Somebody was in need of physical gold badly on this side of the pond.

SURPRISINGLY LITTLE TO NO GOLD HAS BEEN ENTERING THE COMEX VAULTS AND WE HAVE WITNESSED THIS FOR THE PAST YEAR!! WE HAVE ONLY 10.043 TONNES OF REGISTERED ( GOLD OFFERED FOR SALE) VS 7.8444 TONNES OF GOLD STANDING// THEY SEEM TO BE USING CONSIDERABLE GOLD VAPOUR TO SETTLE UPON UNSUSPECTING LONGS.

total dealer silver: 86.515 million

total dealer + customer silver: 306.165 million oz

The total number of notices filed today for the JUNE 2019. contract month is represented by 0 contract(s) FOR NIL oz

To calculate the number of silver ounces that will stand for delivery in JUNE, we take the total number of notices filed for the month so far at 532 x 5,000 oz = 2,660,000 oz to which we add the difference between the open interest for the front month of JUNE. (0) and the number of notices served upon today (0 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JUNE/2019 contract month: 532(notices served so far)x 5000 oz + OI for front month of JUNE( 0) number of notices served upon today (0)x 5000 oz equals 2,630,000 oz of silver standing for the JN contract month.

WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND AT THE COMEX AS THESE GUYS REFUSED TO MORPH INTO A LONDON BASED FORWARDS AND AS WELL THEY ALSO NEGATED A FIAT BONUS. IT SEEMS THAT SOMEBODY WAS BADLY IN NEED OF PHYSICAL SILVER ON THIS SIDE OF THE POND.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 92,755 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 176,893 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 176,893 CONTRACTS EQUATES to .884 billion OZ 126%% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -0.70% June 27/2019)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.30% to NAV (JUNE 27/2019 )

Note: Sprott silver trust back into NEGATIVE territory at -0.70%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 13.76 TRADING 13.22/DISCOUNT 3.95

END

And now the Gold inventory at the GLD/

JUNE 27/WITH GOLD DOWN $6.10: ANOTHER HUGE WITHDRAWAL OF 1.76 PAPER TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 797.61 TONNES

JUNE 26/WITH GOLD DOWN $3.00: WE HAD A HUGE WITHDRAWAL OF 2.37 TONNES FROM THE GLD/INVENTORY RESTS AT 799.61 TONNES

JUNE 25/WITH GOLD UP $1.30 (AND WAY UP BEFORE THE BANKERS WHACKED) WE WITNESSED ANOTHER 1.95 TONNES OF PAPER GOLD ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 801.98 TONNES

JUNE 24/WITH GOLD UP $18.00 A MONSTROUS PAPER DEPOSIT OF 34.93 TONNES/INVENTORY RESTS AT 799.03 TONNES

JUNE 21/WITH GOLD UP $ 2.90, NO CHANGE IN GOLD INVENTORY: INVENTORY RESTS AT: 764.10 TONNES

June 20/WITH GOLD UP $47.95, NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 19 WITH GOLD DOWN $1.65: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONES

JUNE 18/JUNE 18/WITH GOLD UP $7.60: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 17/WITH GOLD DOWN $1.65 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 764.10 TONNES

JUNE 14/ WITH GOLD UP $1.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.40 TONNES OF PAPER GOLD INTO THE GLD///INVENTORY RESTS AT 764.10 TONNES

june 13/WITH GOLD UP $6.60 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 759.70 TONNES

JUNE 12/WITH GOLD UP $7.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 756.18 TONNES

JUNE 11/WITH GOLD UP $1.65 CENTS TODAY: A TINY CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .24 TONNES AND THIS IS TO PAY FOR FEES/INVENTORY RESTS AT 756.18 TONNES

JUNE 10/WITH GOLD DOWN $16.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES/INVENTORY RESTS AT 756.42 TONNES

june 7/WITH GOLD UP $3.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

jUNE 6/WITH GOLD UP $8.40 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 5 WITH GOLD UP $6.00 TODAY/STRANGE: A WITHDRAWAL OF 2.06 TONNES FROM THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 4/WITH GOLD UP 0.85 TODAY: A MONSTROUS PAPER GAIN OF 16.44 TONNES/GLD INVENTORY RESTS AT 759.65 TONNES

JUNE 3/WITH GOLD UP $17.50 TODAY: ANOTHER BIG CHANGE, A DEPOSIT OF 2.35 TONNES OF GOLD INTO THE GLD//

MAY 31/WITH GOLD UP $17.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GLD INVENTORY RESTS AT 740.86 TONNES

MAY 30: WI6H GOLD UP $6.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES/INVENTORY RESTS AT 740.86 TONNES

MAY 29/WITH GOLD UP $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 737.34 TONNES

MAY 28/WITH GOLD DOWN $6.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD> A WITHDRAWAL OF 1.47 TONNES/INVENTORY RESTS AT 737.34 TONNES

MAY 24/WITH GOLD DOWN $1.60 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 738.81 TONNES

MAY 23/WITH GOLD UP $11.10 TODAY: A STRANGE WITHDRAWAL OF .88 TONNES FORM THE GLD/INVENTORY RESTS AT 738,81 TONNES

MAY 22//WITH GOLD FLAT TODAY: WE HAD A GOOD 1.52 TONNES OF GOLD DEPOSIT INTO THE GLD/INVENTORY RESTS TONIGHT AT 739.69 TONNES

MAY 21/WITH GOLD DOWN $3.65 TODAY: A SURPRISE 2.00 TONNES WERE ADDED TO THE GLD GOLD INVENTORY//INVENTORY RESTS AT 738.17 TONNES

MAY 20/WITH GOLD UP $1.00 A HUGE 2.96 TONNE DEPOSIT INTO THE GLD//INVENTORY RESTS AT 736.17 TONNES

MAY 17/WITH GOLD DOWN $9.70 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 733.23 TONNES

MAY 16/WITH GOLD DOWN $11.50: A WITHDRAWAL OF 3.23 TONNES FROM THE GLD//INVENTORY RESTS AT 733.23 TONNES

MAY 15/WITH GOLD UP $1.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 736.46 TONNES

MAY 14//WITH GOLD DOWN $5.45 TODAY: STRANGE!! THE CROOKS DECIDED TO DEPOSIT A HUGE 3.23 TONNES INTO THE GLD INVENTORY//INVENTORY RESTS AT 736.46 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JUNE 27/2019/ Inventory rests tonight at 797.85 tonnes

*IN LAST 617 TRADING DAYS: 136.91 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 517 TRADING DAYS: A NET 28.72 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JUNE 27/WITH SILVER DOWN 7 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.575 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.394 MILLION OZ//

JUNE 26/WITH SILVER UP 17 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 25/WITH SILVER DOWN 25 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ.

JUNE 24/WITH SILVER UP 11 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 21/WITH SILVER DOWN 22 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 20/WITH SILVER UP 53 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 19/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ/

JUNE 18 WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ

JUNE 17/WITH SILVER UP XXX CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ//

JUNE 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 12/WITH SILVER UP 4 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.413 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 11/WITH SILVER UP 10 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 10/WITH SILVER DOWN 38 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

june 7/WITH SILVER UP ANOTHER 12 CENTS, NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

jUNE 6/WITH SILVER UP ANOTHER 9 CENTS TODAY: A FAIR SIZE DEPOSIT OF 630,087 OZ//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 5/WITH SILVER UP 4 CENTS TODAY: A HUGE PAPER DEPOSIT OF 2.396 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 314.434 MILLION OZ//

JUNE 4/WITH SILVER UP 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

JUNE 3/WITH SILVER UP 19 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

MAY 31/WITH SILVER UP 6 CENTS TODAY: A DEPOSIT OF 422,000 OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 312.038 MILLION OZ/

May 30/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ///

MAY 29/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 28/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 24/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ/

MAY 23/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 22/WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 311.616 MILLION OZ

MAY 21: WITH SILVER DOWN 3 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV; A WITHDRAWAL OF 750,000 OZ///INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 20/WITH SILVER UP 6 CENTS:NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.366 MILLION OZ

MAY 17/WITH SILVER DOWN 13 CENTS TODAY: A BIG CHANGES IN SLV: A WITHDRAWAL OF 3.185 MILLION OZ FROM THE SLV INVENTORY VAULTS:/INVENTORY RESTS AT 312.366 MILLION OZ//

MAY 16/WITH SILVER DOWN 26 CENTS: NO CHANGES IN THE SLV INVENTORY//INVENTORY RESTS AT 315.551 MILLION OZ//

MAY 15/WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SLV INVENTORY: A WITHDRAWAL OF 1.031 MILLION OZ// THE SLV/INVENTORY RESTS AT 315.551 MILLION OZ.

MAY 14/WITH SILVER UP 2 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV. INVENTORY RESTS AT 316.582 MILLION OZ/

Gold Standard Cometh In This The Multi Polar, Asian Century (Part I) – Jim Willie Interview

Gold Standard Cometh In This The Multi Polar, Asian Century (Part I) – Jim Willie Interview

-The Global Monetary RESET will see the “Third World” dollar sharply devalued and paper wealth and assets including stocks and bonds lose significant value

– The ‘Gold Standard’ jigsaw: the global monetary pieces are falling into place as China quietly moves to re-establish some form of Gold Standard

– The legs of the Gold Standard stool are here – gold trade notes, gold panda bonds (Italy) and central banks are buying gold as Basle III makes gold a “risk free asset”

– Trump may have become compromised by the Neo-Conservatives and their crazy and expensive dreams of maintaining Empire and a ‘New American Century’

– United States is bankrupt (with $22 trillion US debt and over $100 trillion of unfunded government liabilities) and “living on a maxed out credit card,” therefore U.S. Treasuries are no longer a risk free asset

– Global Financial Crisis II is “going to be much, much bigger” … Prepare now

Thanks for sharing and please click that ‘Like’ button.

Jim’s website is golden-jackass.com and the Gadfly channel is at thegadfly.vhx.tv

Receive our free daily or weekly updates by signing up here

LBMA Gold Prices (AM/ PM Fix – USD, GBP & EUR)

26-Jun-19 1406.75 1403.95, 1109.22 1106.73 & 1238.501236.32

25-Jun-19 1429.55 1431.40, 1120.62 1124.36 & 1255.72 1256.20

24-Jun-19 1405.45 1405.70, 1102.58 1105.30 & 1233.56 1235.05

21-Jun-19 1388.35 1397.15, 1095.96 1101.93 & 1228.55 1233.12

20-Jun-19 1381.65 1379.50, 1086.25 1087.74 & 1222.90 1221.27

19-Jun-19 1342.40 1344.05, 1066.67 1066.64 & 1198.36 1199.43

18-Jun-19 1344.55 1341.35, 1073.22 1070.67 & 1201.89 1198.09

17-Jun-19 1333.20 1341.30, 1059.49 1065.13 & 1188.81 1193.09

News and Commentary

ECB Cautious of Bank of Italy Law Which Declares Gold Reserves Are the States

Gold Settles Lower After 4-session Climb Lifted Prices Near a 6-year High

Gold Drops as Bets Fade for Big Fed Rate Cut Fade; Eyes on Trade Talks

Dollar Gains on Lower Rate Cut Expectations, Stocks Flat

NATO Says It Will Act Unless Russia Destroys Nuclear-ready Missile

Investors Should Buy Gold, Ignore G-20 and Brace for a Fresh Round of Trump Tariffs – Bass

ECB to Italian Government: Your Gold is Ours

Stablecoin Might Liberate the World From the U.S. Dollar

Warning: Federal Reserve Easing Ahead

Why Interest Rates Don’t Need to Rise Much to Cause Recessions Now

IRL +353 (0)1 632 5010

US +1 (302)635 1160

end

ii) Physical stories courtesy of GATA/Chris Powell

this will be good for the USA as Trump is ready to throw away the Obama era environmental restrictions that have stopped this huge project.

The owner of the mine is Northern Dynasty

(courtesy Bloomberg/GATA)

Alaska gold property with $100 billion lode to get lifeline from Trump EPA

Submitted by cpowell on Thu, 2019-06-27 01:42. Section: Daily Dispatches

By Jennifer A. Dlouhy

Bloomberg News

Wednesday, June 26, 2019

The Trump administration is throwing a lifeline to the massive Pebble Mine planned near Alaska’s Bristol Bay, as regulators move toward undoing Obama-era environmental restrictions that have thwarted the project.

The Environmental Protection Agency said today it was resuming consideration of the proposed water pollution restrictions that have effectively stalled the project since they were outlined in 2014. Reconsidering the issue — after a year-and-a-half hiatus — is a necessary prelude to the EPA officially lifting the restrictions later.

…

The EPA’s action is a significant boost for Northern Dynasty Minerals Ltd. and Pebble LP supporters, who have called on the EPA to lift the Clean Water Act restrictions and let the proposed gold, copper, and molybdenum mine move forward. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-06-26/pebble-gold-mine-in-a…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

end

The ECB gives the green light to Italy to claim that its gold held by the Bank of Italy belongs to the country and not the bank.

That should have been obvious

(courtesy Reuters/GATA)

ECB gives cautious approval to League’s bill on Bank of Italy gold reserves

Submitted by cpowell on Thu, 2019-06-27 01:58. Section: Daily Dispatches

By Gavin Jones and Giuseppe Fonte

Reuters

Tuesday, June 25, 2019

ROME — The European Central Bank on Tuesday gave a substantial green light to a bill by Italy’s ruling League party which seeks to spell out that gold reserves held by the Bank of Italy belong to the state, and not the bank itself.

The bill, tabled in February by the League’s economics chief, Claudio Borghi, was strongly criticized by the opposition who said its aim was to allow the ruling coalition to potentially sell the gold to fix Italy’s public finance problems.

…

Borghi denied this, saying he wanted to clarify the legal ownership of the gold, establish a question of principle and bring Italy’s situation in line with those of other EU states.

In an official opinion published on the ECB’s website, the bank said EU treaties do not use the concept of ownership with regard to official gold reserves but deal only with the question of their “exclusive holding and management.”

The opinion, signed by ECB President Mario Draghi, asked the government to consult with the Bank of Italy if it planned to push ahead with the legislation, in order that the central bank’s independence be “fully respected.” …

… For the remainder of the report:

https://www.reuters.com/article/us-italy-cenbank-ecb/ecb-gives-cautious-…

* * *

iii) Other physical stories:

SILVER DOCTORS NEWS

I was interviewed on Tuesday by Silver Doctors

I hope you find this interview enlightening.

Hi Harvey,

The bankers did it again to our crypto players..as bitcoin crashed last night, losing 1500 in minutes. This is why you do not invest in bitcoin.

(courtesy zerohedge)

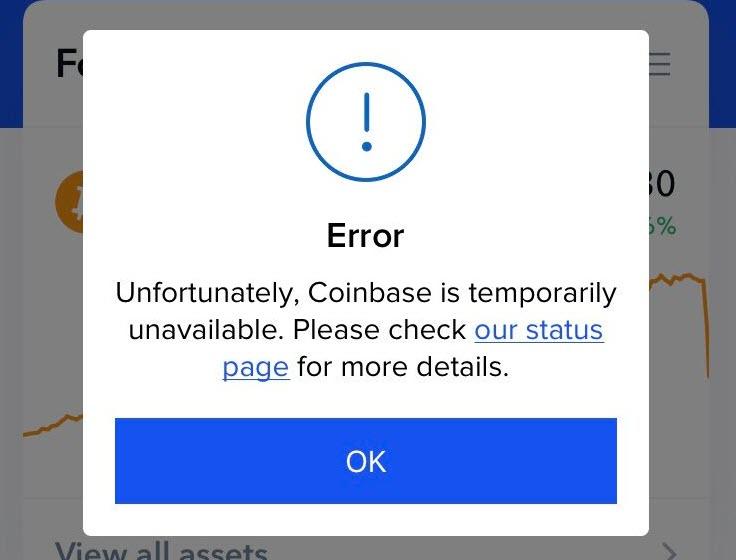

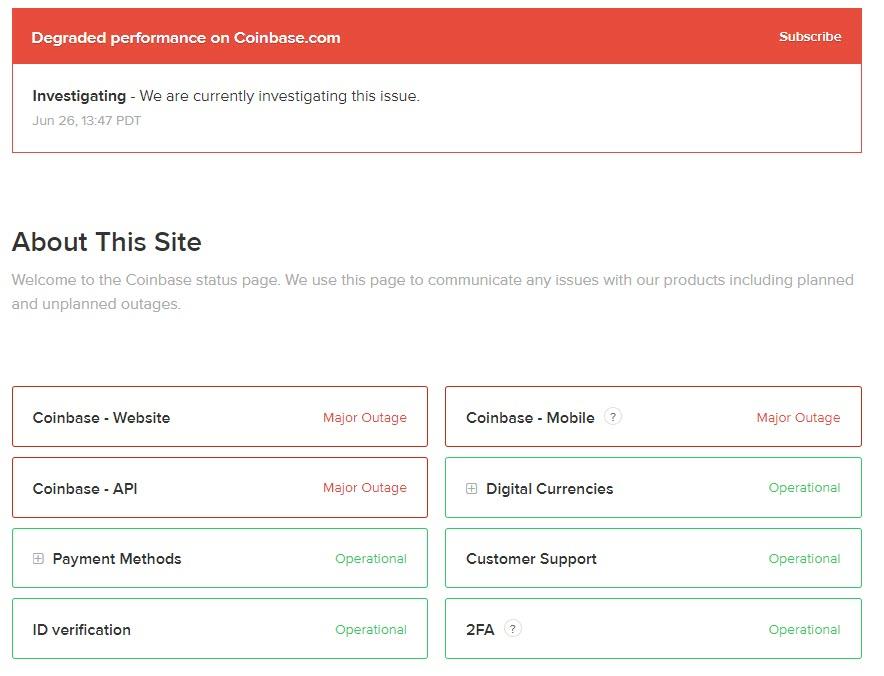

Coinbase Offline As Cryptos Collapse, Bitcoin Loses $1500 In Minutes

After the biggest day since December 2017, Bitcoin just crashed over $1500 in minutes, dragging the rest of the crypto space with it…

Erasing the day’s gains and then some..

And immediately Coinbase became unavailable…

As Tom Luongo warned earlier, this run up towards the end of this month into the end of Q2 may be morphing quickly into a FOMO rally that could see a blow-off top in the near future.

Markets that go vertical without really pausing to take a breather will always correct down. Hard.

When that happens given the expansion of Bitcoin’s dominance of the crypto market by market cap percentage in the past few weeks, I would expect to see some strong rotation into both cash and alt coins just clearing major technical hurdles on any correction.

And just so we’re clear as to what’s happening here. The mother of all safe haven trades is emerging. Trade Wars, Near Hot Ones, tariffs, sanctions, popular uprisings and political instability are all on the table.

While we’re all focused on whatever short-term idiocy comes out of Donald Trump’s mouth to secure his control over the Overton Window, we should be asking ourselves why the ECB is going looking at even more negative rates, LIBOR has inverted alongside Eurodollar and the U.S. Treasury market and stocks are at all-time highs.

The markets aren’t irrational. Our perceptions of what is driving this behavior is. Safe haven assets change with the times.

And when you step back from the insanity of the fiscal and political situation in the U.S. and Europe, the fall-out from their instability on emerging markets and the potential for major shifts in the geopolitical game board does it really seem all that odd that a simple electronic proxy for gold with thin supply, high trust and low holding risk would become a darling of the risk averse?

I don’t.

However, perhaps it is as simple as this chart…

Bitcoin is still protection from the idiocy of policymakers…

As an aside, US equity futures extended their losses after the close as Bitcoin got hit…

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.8785/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.8782 /shanghai bourse CLOSED UP 20.51 POINTS OR 0.69%

HANG SANG CLOSED UP 399.44 POINTS OR 1.42%

2. Nikkei closed DOWN 251.58 POINTS OR 1.19%

3. Europe stocks OPENED ALL RED EXCEPT ITALY

USA dollar index DOWN TO 96.16/Euro RISES TO 1.1376

3b Japan 10 year bond yield:RISES TO. –.14/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.84/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 58.77 and Brent: 65.91

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO -.30%/Italian 10 yr bond yield UP to 2.13% /SPAIN 10 YR BOND YIELD UP TO 0.41%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.43: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.45

3k Gold at $1405.50 silver at: 15.25 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 2/100 in roubles/dollar) 63.03

3m oil into the 58 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.84 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9770 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1144 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISING to –0.30%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.04% early this morning. Thirty year rate at 2.54%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.7736..

Global Stock Rally Ends With A Bang After WSJ Crushes Hope For Quick US-China Truce

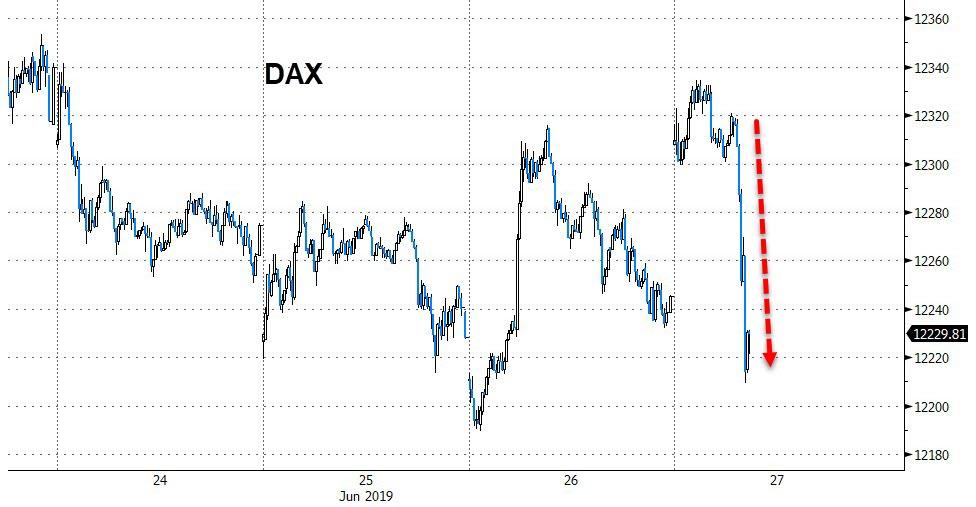

There has been a 180-degree reversal in market sentiment overnight, when at first US futures and global stocks ramped higher for much of the session following a SCMP report late on Thursday (US time) that US and China had agreed on a “truce” to avoid further tariffs, only for the WSJ to pour cold water on the report just before 6am EDT when it noted some of the key items the SCMP “missed” on purposes, namely that China had very specific demands to agree to a ceasefire, including the removal of the Huawei ban, something that Trump would almost certainly not agree to (and yet the Chinese publication made it seem like it was Beijing that was oh so generous, when in reality it was setting up Trump to be the guilty party when in reality it was China that once again held an untenable position going into the Trump-Xi talks).

In addition to the WSJ report, overnight China’s Commerce Ministry urged the US to immediately cancel sanctions on Chinese firms, including Huawei, and warned it would consider placing firms on a unreliable list if they implement discriminatory measures on Chinese entities, and firms that threaten the national security of China adding that the details are to be released soon.

In any case, the WSJ’s report immediately doused any positive market sentiment, with Bloomberg’s Heather Burke noting that “equities are waking up to the reality that this weekend’s meeting may not bring a shiny, happy trade solution”, which has sent S&P futures sharply lower, wiping out all overnight gains…

… and global markets lost much of their sparkle, with Europe turning sharply lower…

… led by the German Dax, which suffered a dramatic drop in minutes after the WSJ report refuted the SCMP.

“We should not expect too much from the Osaka meeting,” Christian Nolting, global chief investment officer at Deutsche Bank Wealth Management told Bloomberg TV. “To be overly optimistic could be on the wrong side for this weekend.”

Not helping US futures (or European stocks which slumped in the red) was the latest Boeing news, according to which the 737 MAX was prone to “uncontrolled nosedives” after new tests revealed a fresh software glitch, which in turn assured that the grounded Boeing planes would stay in parkling lots that much longer, and also sent Boeing stock plunging, which thanks to its biggest impact on the Dow has sent the “industrial” index into the red.

While both the US and Europe were scrambling to make sense of all the latest headlines, Asian stocks – which mostly closed ahead of the WSJ report – benefited from the earlier trade euphoria, and tech and material firms led Asian stocks higher. Almost all markets in the region rose, with Japan, Taiwan and Hong Kong leading gains. The Topix closed 1.2% higher, with SoftBank Group and Daikin Industries among the biggest boosts. Japan Display surged as much as 32% following a report that Apple is considering further financial support for the company. As noted above, Europe’s Stoxx 600 Index, which had gained led by retailers following H&M results, reversed.

Over in China, the Shanghai Composite Index rose 0.7%, driven by large banks and insurers, as investors cheered the probability of a China-U.S. trade deal (if only they had waited a few more hours, the cheering would have ended abruptly). Kweichow Moutai closed at a record high after climbing above the 1,000 yuan level for the first time on an intra-day basis. The outlier was Vietnam, whose stocks dropped 1.7%, bucking the regional trend, after Trump indicated that he might impose tariffs on the nation. The S&P BSE Sensex Index advanced 0.3%, rallying for a third day, with HDFC Bank and Housing Development Finance providing the biggest support to the gauge

In other assets, the dollar initially rose against the yen on hopes of a truce in U.S.-China trade war ahead of the Group of 20 summit, before losing traction amid quarter-end flows and the WSJ rejection. The euro rebounded on German regional inflation data even as a gauge of economic confidence in the region dropped to its lowest in nearly three years. Bunds dropped, Treasuries steadied and equities lost their bullish momentum as the London session progressed. European bonds were mixed after data showed economic confidence in the region declined more than forecast.

In other news overnight, Trump said he looks forward to speaking to India PM Modi about how India have placed very high tariffs on US for years and recently increased them further, while Trump added this is unacceptable and tariffs must be withdrawn. In response, Indian government sources noted that India’s tariffs on the US are well within the WTO bound rates.

And while the world is focused on the US-China meeting, President Trump will also meet with Russia President Putin on Friday at 1400 local time, ahead of Trump’s meeting with Chinese President Xi, which will take place on Saturday at 1130 local time in Osaka, according to a spokesman.

In other geopolitical news, Iran’s Parliament Speaker Larijani stated that the reaction from Tehran will be stronger in the event that the US repeats the mistake of violating Iran’s borders. Iran is still short of the nuclear deals limit on enriched uranium stocks, and are on course to reach the limit at the weekend., as according to diplomats citing IAEA data.

West Texas Intermediate crude declined 1% to $58.81 a barrel, the largest drop in more than a week. Gold dipped 0.2% to $1,405.64 an ounce.

Economic data include initial jobless claims, pending home sales and the third print of first-quarter GDP. Scheduled earnings include Nike, Accenture and Walgreens.

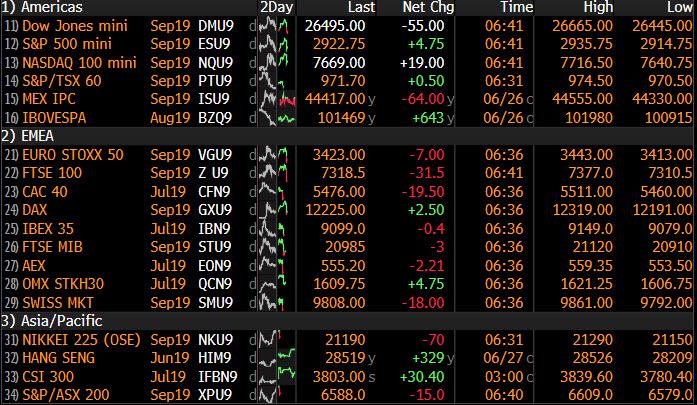

Market Snapshot

- S&P 500 futures up 0.2% to 2,923.00

- STOXX Europe 600 down 0.1% to 381.78

- MXAP up 0.9% to 160.15

- MXAPJ up 0.9% to 528.69

- Nikkei up 1.2% to 21,338.17

- Topix up 1.2% to 1,553.27

- Hang Seng Index up 1.4% to 28,621.42

- Shanghai Composite up 0.7% to 2,996.79

- Sensex up 0.3% to 39,709.40

- Australia S&P/ASX 200 up 0.4% to 6,666.31

- Kospi up 0.6% to 2,134.32

- German 10Y yield rose 1.3 bps to -0.29%

- Euro up 0.02% to $1.1371

- Brent Futures down 0.8% to $65.96/bbl

- Italian 10Y yield fell 1.8 bps to 1.779%

- Spanish 10Y yield rose 0.9 bps to 0.402%

- Brent Futures down 0.8% to $65.93/bbl

- Gold spot down 0.4% to $1,403.77

- U.S. Dollar Index up 0.03% to 96.24

Top overnight news from Bloomberg

- The first Democratic president debate in the U.S. exposed ideological fissures within the party over how to remake the economy, fix immigration and confront big companies — and whether the path to defeating Trump veers toward liberal solutions or hews to the middle

- Trump said India’s recent increase in tariffs on U.S. goods is “unacceptable” and should be withdrawn, ratcheting up tension before a planned meeting with Prime Minister Narendra Modi

- The European Central Bank will deliver a cut in September as policy makers step up their efforts to revive the euro-zone economy, economists predict

- Several Huawei Technologies Co. employees have collaborated with Chinese armed forces personnel on research projects, indicating closer ties to the country’s military than previously acknowledged by the smartphone and networking powerhouse

- Turkey is preparing a bill that would boost the Treasury’s cash flow through the use of central bank lira reserves, just weeks after policy makers refrained from proposing a similar measure for fear it could roil financial markets, Bloomberg HT reported on Thursday. The lira fell.

Asian equity markets traded higher after the region shrugged off the uninspiring lead from Wall St where participants were tentative heading into the G20 and amid mixed US-China trade commentary. ASX 200 (+0.4%) was positive in which outperformance in the energy sector just about kept the index afloat following the recent bullish oil inventory data, while Nikkei 225 (+1.2%) was underpinned by the JPY-risk dynamic and with Japan Display the front runner in Tokyo after reports that Apple will infuse USD 100mln into the Co. and also raise its orders. Elsewhere, Hang Seng (+1.4%) and Shanghai Comp. (+0.7%) inspired the turnaround in the region on several factors including the State Council’s recent announcement of measures to cut financing costs for smaller firms and with Industrial Profits back in the black, while the trade-related headlines were more constructive in which SCMP noted the US and China agreed a tentative truce before the G20 summit and that US President Trump’s decision to delay additional tariffs was Chinese President Xi’s price for holding this week’s meeting with him. Finally, 10yr JGBs were lower with demand dampened by the improved risk sentiment and after similar weakness in T-notes, but with downside limited amid a mixed 2yr auction in which most metrics improved despite a weaker bid to cover.

Top Asian News

- Trump Asks India to Reverse ‘Unacceptable’ Tariffs on U.S. Goods

- Trade-War Winner Vietnam Finds Itself in Trump’s Crosshairs

- Singapore to Review 2019 Growth Forecasts as Trade War Spreads

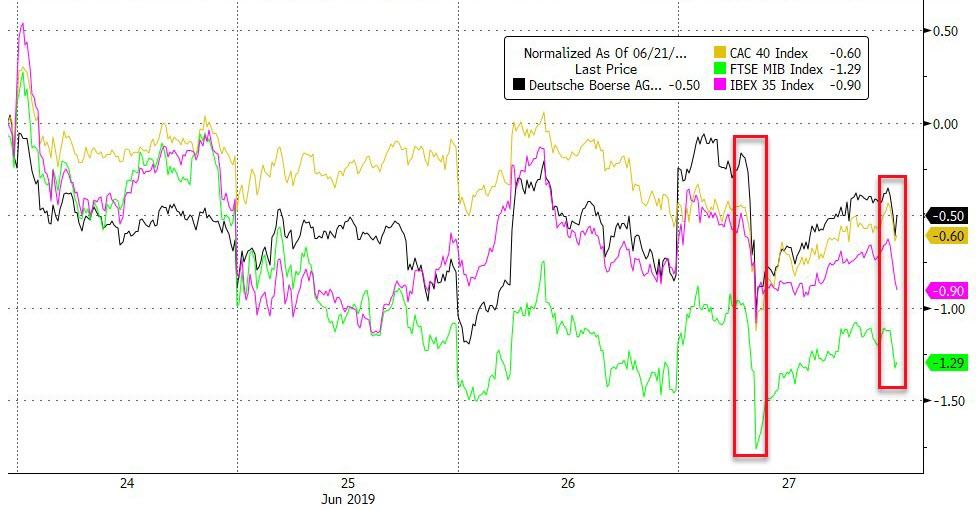

European equities have given up earlier gains [Eurostoxx 50 -0.3%] amid reports that Chinese President Xi is intending on presenting US President Trump with a set of terms that the US needs to meet before Beijing will be prepared to settle the trade dispute. Beijing is insisting that the U.S. removes its ban on the sale of U.S. technology to Huawei, according to a Chinese Official (which was noted earlier in the session by MOFCOM) whilst also asking for the removal of all punitive tariffs and for the US to drop its efforts to get China to buy more U.S. goods. Equity futures reacted negatively to the report as the conditions from China signal the gulf in demands between the two sides ahead of this weekend’s showdown. Germany’s DAX (-0.1%) is faring slightly better than its peers as the index heavyweight Bayer (+8.0%) surges amid reports of support from Elliott as the Co. reviews its legal strategy on weed killers. Sectors are mixed with some underperformance experienced in defensive sectors. In terms of individual movers, H&M (+9.3%) shares spiked higher at the open following results in which Q2 sales rose 11%. Meanwhile, CHR Hansen (-12.2%) fell to the foot of the Stoxx 600 after cutting its revenue guidance.

Top European News

- H&M Surges as Retailer Shows Early Progress Toward Turnaround

- European Car Market Forecast to Shrink 1%, Acea Says in Revision

- Johnson Zigzags Again, Says No-Deal Exit Unlikely: Brexit Update

- Macron’s G-20 Climate Threat Melts Away Just Like the Ice Caps

In FX, there has not been much deviation from established or recent ranges in major pairings, and the narrow DXY band (96.390-156) illustrates the subdued and cautious tone ahead of the eagerly awaited Summit in Osaka and US-China trade showdown. Indeed, there is still little sign of strong Dollar selling for month, quarter and half year end portfolio balancing purposes, although the Fed has intervened to an extent via Powell and Bullard’s efforts to manage dovish market expectations.

- AUD/NZD – The Aussie and Kiwi are still riding high on improved risk sentiment following some signs that relations between Washington and Beijing have cooled, albeit temporarily and conditionally pending the outcome of aforementioned G20 meeting where Presidents Trump and Xi will attempt to resolve issues that led to a breakdown in negotiations. Meanwhile, a welcome rebound in Chinese industrial profits has also lifted the mood down under, with Aud/Usd and Nzd/Usd both within a whisker of big figures at 0.7000 and 0.6700 respectively, and the latter not unduly ruffled by a deterioration in ANZ’s NZ activity outlook overnight.

- GBP – The Pound is looking perky again as Cable reclaims the 1.2700 handle that has been tested several times this week, but proved unsustainable. Encouraging comments from Japan on the prospect of a post-Brexit trade deal with the UK along TPP lines may be supporting Sterling that is also firmer vs the Euro (cross pivoting 0.8950), but a hefty 1bn option expiry at 1.2700 in Cable could still cap that pair.

- EUR/CAD/CHF/JPY/NOK – All narrowly mixed vs the Greenback and more confined, with the single currency remaining in a circa 1.1350-80 band and holding above key technical support in the form of the 200 DMA (1.1344) with the aid of firm-to-relatively frothy German state inflation data that puts an upside bias on the pan print consensus towards 1.6% from 1.4% and steady from the previous month. Conversely, the Loonie has lost some momentum ahead of 1.3100 due to a dip in oil prices, while the Franc pivots 0.9800 and Yen straddles 108.00 after dovish/downbeat remarks from BoJ’s Wakatabe. Elsewhere, the Norwegian Krona has retreated in wake of weaker than expected retail sales and the recoil in crude, with Eur/Nok back up around 9.6900.

- EM – Bucking the generally firmer regional trend, reports that Turkey is looking to syphon CBRT reserves have resurfaced and undermined the Lira alongside headlines about changes to tax policy, with Usd/Try up over 5.7900 at one stage.

In commodities, WTI and Brent futures are consolidating following this week’s geopolitics-inspired gains which were exacerbated by declining US stockpiles. WTI futures hovers around the USD 59/bbl level ahead of a cluster of DMA (50 DMA – 59.25, 100 DMA – 59.41 and 200 DMA 59.48) while its Brent counterpart trades just above the USD 65/bbl mark. On the OPEC+ front, Russia’s Energy Minister sounded somewhat upbeat in regard to reaching a consensus with Russia’s OPEC counterparts at next week’s meeting, adding that he will be meeting Saudi’s Energy Minister Al-Falih at the G20 this weekend. The energy producers will be heading into the meeting with full knowledge of the fallout from US-China talks. Market consensus is that a rollover of the current deal is the likely outlook (also mentioned by the Iraqi Oil Minister), although it is still not clear if any revisions will be made (Iraqi Oil Minister touted deeper cuts). Elsewhere, the gold rally has fizzled out as the DXY remains buoyed above 92.00, with the yellow metal now in close proximity to USD 1400/oz (vs. recent high of USD 1439/oz). Meanwhile, copper prices are little changed on the day ahead of the risk-packed weekend, with prices hovering just above USD 2.7/lb ahead of its 50 DMA at 2.73/lb. Finally, Dalian Iron ore has resumed its rally amid renewed concerns of tightening supply whilst Rebar steel continued its upwards trajectory amid pollution-related production curbs in China.

US Event Calendar

- 8:30am: GDP Annualized QoQ, est. 3.2%, prior 3.1%

- 8:30am: Initial Jobless Claims, est. 220,000, prior 216,000;Continuing Claims, est. 1.67m, prior 1.66m

- 9:45am: Bloomberg Consumer Comfort, prior 61.8

- 10am: Pending Home Sales MoM, est. 1.0%, prior -1.5%; YoY, est. 0.4%, prior 0.4%

- 11am: Kansas City Fed Manf. Activity, est. 1, prior 4

DB’s Jim Reid concludes the overnight wrap

As we await the G-20 none of us are any closer to knowing what the aftermath of the Trump/Xi meeting will be. If we weren’t confused enough, we had to try to decipher the following comments from Mr Trump yesterday, “my plan B’s maybe my plan A, my plan B is that if we don’t make a deal I will tariff, and maybe not at 25%, but maybe at 10%”. This certainly required a few re-reads but the ultimate takeaway from his interview was that the underlying threat of additional tariffs was still very much in place even if there were no greater insights into which way the upcoming talks will go. Trump also continued his now-customary attacks on the Fed and Chair Powell, saying he “should never have raised the rates to the level that he raised it” and that “we should have Draghi instead of our Fed person.”

Earlier in the day there appeared to be a bit of excitement about slightly more upbeat trade comments from Trump’s Treasury Secretary Mnuchin suggesting that a trade deal was 90% complete. However, after some initial giddiness, the market reappraised the remarks to appreciate that Mnuchin said the two sides “were” 90% of the way there. In other words, Mnuchin was referencing where talks were before they broke down. His remarks were live direct to CNBC immediately after I was a guest speaker in the London studio. Indeed I couldn’t help think that I was a filler as the studio was a whirl of activity, stress, and anticipation that they had Mnuchin on live at any moment. Earpieces were a constant stream of noise. Indeed I was told I could be booted off if he came through early. So I was the support act to the main event.

Anyway, the end result for equities was a small retreat for the S&P 500 (-0.12%) and DOW (-0.04%) after sliding steadily throughout the session, notably below the +0.58% and +1.18% peaks that futures hit after the misinterpreted Mnuchin comments. The NASDAQ (+0.32%) posted bigger gains, but the real standout was the Semi-Conductor Index (+3.21%). Two notable laggards were Google (-0.60%) and Facebook (-0.62%), possibly as a result of President Trump’s statement that ” we should be suing Google and Facebook.” European markets faded from earlier highs with the STOXX 600 ending -0.31% while in rates Treasuries continued their post Bullard and Powell move higher with 10y yields up +6.4bps (a further +1bps this morning). At the short end 2y yields rose ‘only’ +3.9bps (+1.7bps this morning) which caused the curve to steepen +2.66bps to 27.5bps (26.8bps this morning).

Breakevens assisted the move higher for rates with oil rallying hard again. WTI closed up +2.42% and has now posted 5 daily moves of at least 2% up or down in the last 11 sessions. Brent also rose +1.84% and is now +10.5% off the recent lows. The spike yesterday appeared to be triggered by the latest EIA inventories data, which showed a 12.8 million barrel drawdown in inventories, the biggest since 2016 and 5th biggest on record going back to 1982. There have been some concerns lately about oversupply, so the initial strong start to the summer driving season sends a bullish signal for oil prices.

Bond markets were a bit less exciting in Europe where 10y Bund yields in particular edged up +2.9bps, similar to the rest of the continent with the exception of BTPs (-1.9bps). Part of that outperformance may well have reflected the Reuters story which hit just after midday suggesting that the ECB was looking at ways to circumvent the issuer limit constraint, potentially by stripping central banks of their voting rights through a clause known as “disenfranchisement”. Clearly there are policy and legal arguments to both sides of this and therefore it’s unlikely to be a decision that is made overnight. There has been more chatter on it recently, especially since Draghi signalled his potential willingness to change the program’s parameters, so it’s a topic worth following closely.

Gold prices slipped -0.99%, their first decline after six straight sessions of gains, though they remain near recent highs. We had highlighted earlier this week how gold and bitcoin were both rising in unison, perhaps as speculators retreated from fiat currencies ahead of expected rate cuts, but that correlation snapped yesterday. While gold fell, bitcoin prices rocketed up another +21.87% at one point to $13,852 before collapsing most of the way back into the close but then spiking again to be +12.03% higher. In Asia it’s gone through a sizeable range again. It feels to H2 2017 all over again.

Elsewhere in Asia this morning markets are heading higher on optimism that a temporary truce might be the most likely outcome of the Trump/Xi meeting at G20. The Nikkei (+0.98%), Hang Seng (+1.13%), Shanghai Comp (+0.89%) and Kospi (+0.83%) are all up c. 1%. The Japanese yen is down -0.287% this morning Elsewhere, futures on the S&P 500 are up +0.28%.

We got confirmation overnight that the Trump/Xi meeting will start at 11:30am (Japan time) on Saturday, with a 90mins slot provided after which Trump is scheduled to meet Turkish President Erdogan. Meanwhile, the Washington Post has reported that President Trump’s top China critic, senior adviser Peter Navarro, is also part of the US delegation visiting G20. He was a last minute addition to the team which includes the U.S. Trade Representative Robert E. Lighthizer, Treasury Secretary Steven Mnuchin and Commerce Secretary Wilbur Ross. Navarro’s inclusion reduces the possibility of any quick deal between the presidents, which was never the base case anyway. Meanwhile, Reuters has reported that Lighthizer and Mnuchin are expected to meet with China’s Liu He ahead of the meeting between Trump and Xi. Staying with trade, Bloomberg reported (citing EU officials) that if talks at the G20 meeting and in the coming weeks fail to head off US tariffs on Europe’s car industry, then they are confident that their response will be sharp enough to “hit the president where it hurts”.

Back to yesterday now. As for the data, in the US headline durable goods orders slumped a lot more than expected in May based on the preliminary reading. The headline was -1.3% mom compared to expectations for -0.3%. However the ex-transportation number was a lot more positive (+0.3% mom vs. +0.1% expected) while core capex orders also rose more than expected (+0.4% mom vs. +0.1% expected). Elsewhere, the advance goods trade deficit widened to $74.5bn in May and more than expected to a five-month high. Finally wholesale inventories rose +0.4% mom in May and a little less than expected. In aggregate, the data should signal a modest increase in second quarter growth expectations.

In the UK, Bank of England Governor Carney generated some headlines when testifying to a Parliamentary committee. On the policy front, he emphasised that Brexit is the key risk, with “the degree of uncertainty high” and was sanguine about the disconnect between markets and the BoE’s own forecasts. Markets are resistant to pricing hikes, he said because investors ascribe “some possibility to no deal,” in which case there would be easing. Carney seemed to ratify this view, but cautioned that “we would do what we could to support the transition to no deal, but there’s no guarantee on that.” Relatedly, he pushed back on the view – recently espoused by Boris Johnson among others – that the UK could retreat to the relationship under article 24 of the GATT, which would maintain existing rules while negotiations continue. Carney said such an arrangement would need to be multilaterally agreed and the EU has showed no signs of interest. Boris Johnson said last night that he thought the chances of a no deal Brexit were a “million to one” but that he was prepared for one. He is going to have some tough times squaring this if and when he gets elected!

Across the pond, the Fedspeak calendar was light, with the only major remarks coming from San Francisco Fed President Mary Daly, who leans toward to dovish side of the committee but is relatively centrist. She said that “the labour market is strong. I believe it’s tighter than it’s been in a while, but there might be more room to run.” She also said she is “uncomfortable with not only the level of inflation currently but the direction.” So her comments would be consistent with her support for a July cut, but didn’t really offer any new info.

Looking at the day ahead, this morning we’re due to get June confidence indicators for the Euro Area before the preliminary June CPI report is out in Germany. Also out this afternoon in the US is the third and final Q1 GDP reading (which is expected to be revised up one-tenth to +3.2%) and Q1 core PCE, jobless claims, May pending home sales and the June Kansas Fed manufacturing survey. Elsewhere, the ECB’s Nowotny is due to speak this evening while the Fed will release part two of its bank stress test results.

3A/ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 20.51 POINTS OR 0.69% //Hang Sang CLOSED UP 399.44 POINTS OR 1.42% /The Nikkei closed UP 251.58 POINTS OR 1.19%//Australia’s all ordinaires CLOSED UP .40%

/Chinese yuan (ONSHORE) closed DOWN at 6.8785 /Oil UP TO 58.77 dollars per barrel for WTI and 65.91 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8785 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8782 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3c China/Chinese affairs

Pure nonsense! Why would the uSA agree to this deal with China offering nothing..this is going nowhere..there will be no deal

(courtesy zerohedge)

Futures Tumble After Beijing Reveals Demands To Agree To Trade War “Truce”, Including Lift Of Huawei Ban

The big news overnight came from the South China Morning Post, which echoed what Bloomberg reported earlier this week, namely that the US and China have “tentatively” agreed to another truce in their trade war in order to resume talks aimed at resolving the dispute, with details of the agreement being laid out in press releases in advance of the meeting between Chinese President Xi Jinping and US President Donald Trump at the G-20 leaders summit in Osaka.