GOLD: $1386.10 DOWN $24.70 (COMEX TO COMEX CLOSING)

Silver: $15,16 DOWN 16 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1383.50

silver: $15.14

This is a holiday week with many taking off as July 4 in the USA is their independence day. As always, this is an excuse for the crooks to raid as many are away. The fun will begin on Monday July 8.

YOUR DATA…

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 84/193

EXCHANGE: COMEX

CONTRACT: JULY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,409.700000000 USD

INTENT DATE: 06/28/2019 DELIVERY DATE: 07/02/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

167 H MAREX 6

624 C BOFA SECURITIES 3

657 C MORGAN STANLEY 14

661 C JP MORGAN 74

661 H JP MORGAN 10

690 C ABN AMRO 13 17

737 C ADVANTAGE 73 63

800 C MAREX SPEC 101

905 C ADM 12

____________________________________________________________________________________________

TOTAL: 193 193

MONTH TO DATE: 564

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 193 NOTICE(S) FOR 19,300 OZ (0.2674 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 564 NOTICES FOR 56,400 OZ (1.754 TONNES)

SILVER

FOR JULY

515 NOTICE(S) FILED TODAY FOR 2,575,000 OZ/

total number of notices filed so far this month: 3135 for 15,675,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

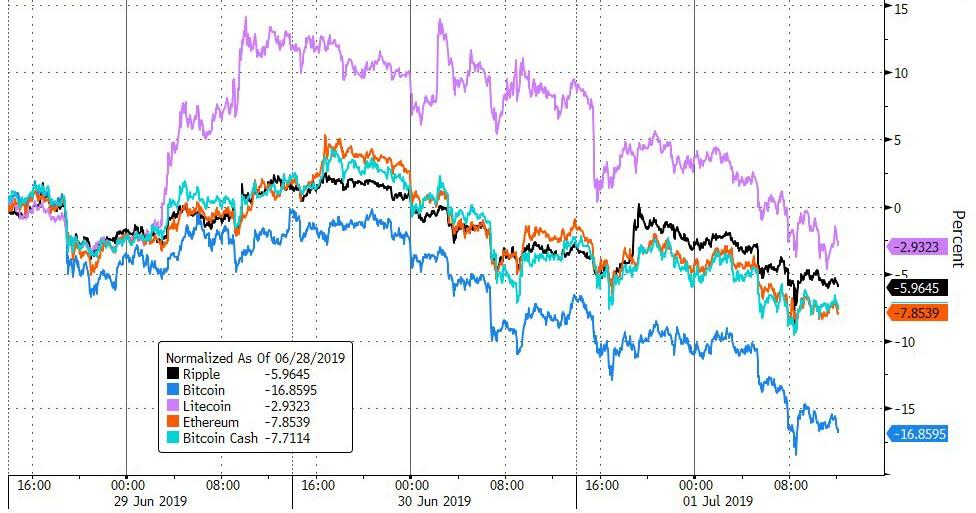

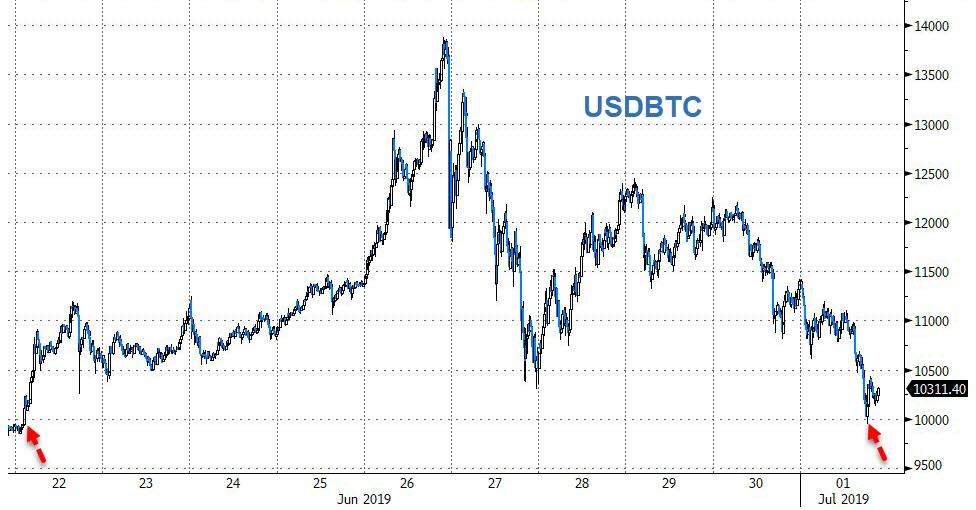

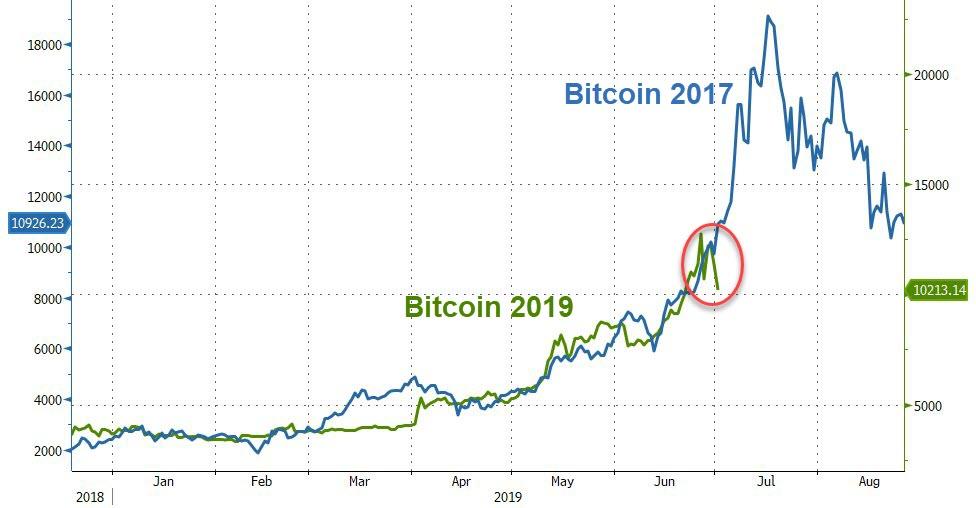

Bitcoin: OPENING MORNING TRADE : $ 10,933 DOWN 527

Bitcoin: FINAL EVENING TRADE: $ 10,157 DOWN 675

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL A CONSIDERABLE SIZED 2257 CONTRACTS FROM 220,612 DOWN TO 218,355 DESPITE THE 6 CENT GAIN IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JULY. 0 FOR AUGUST, 1816 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1816 CONTRACTS. WITH THE TRANSFER OF 1816 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1816 EFP CONTRACTS TRANSLATES INTO 9.08 MILLION OZ ACCOMPANYING:

1.THE 6 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

20.150 MILLION OZ INITIAL STANDING FOR JULY

WE HAD CONSIDERABLE SHORT COVERING AT THE SILVER COMEX FRIDAY ..AND ZERO SPREADING ACCUMULATION SO FAR.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

1816 CONTRACTS (FOR 1 TRADING DAY TOTAL 1816 CONTRACTS) OR 9.08 MILLION OZ: (AVERAGE PER DAY: 1816 CONTRACTS OR 9.08 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 9.08 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 1.29% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1166.57 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2257, DESPITE THE 6 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1816 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A SMALL SIZED: 441 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1816 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 2257 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 6 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.32 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.187 BILLION OZ TO BE EXACT or 169% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 515 NOTICE(S) FOR 2,575,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 20.150 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

WITH RESPECT TO SPREADING: WE WILL WITNESS THE MORPHING OF OUR SPREADERS OUT OF SILVER AND INTO GOLD AS THE JULY MONTH PROCEEDS INTO THE ACTIVE DELIVERY MONTH OF AUGUST.

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF AUGUST.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JULY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE OPEN INTEREST FELL BY A SMALL 1341 CONTRACTS, TO 580,855 ACCOMPANYING THE TINY $0.90 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING LIQUIDATION WILL NOW COMMENCE FOR GOLD….

FOR THE 6TH TIME IN THE LAST 7 TRADING DAYS WE HAVE WITNESSED A HUGE REDUCTION FORM THE PRELIMINARY GOLD OPEN INTEREST TO THE FINAL OI NUMBER. THE ONLY ANSWER TO THIS IS MASSIVE FRAUD TO WHICH THE CFTC REFUSED TO ANSWER…

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5397 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 5397 CONTRACTS, DEC> 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 580,855. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6738 CONTRACTS: 1341 CONTRACTS INCREASED AT THE COMEX AND 5397 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 6738 CONTRACTS OR 673,800 OZ OR 20.95 TONNES. FRIDAY WE HAD A TINY GAIN OF $0.90 IN GOLD TRADING.…AND WITH THAT TINY GAIN IN PRICE, WE HAD A STRONG GAIN IN GOLD TONNAGE OF 20.95 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY : 5397 CONTRACTS OR 539,700 oz OR 16.786 TONNES (1 TRADING DAY AND THUS AVERAGING: 5397 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY IN TONNES: 16.786 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 16.786/3550 x 100% TONNES =0.47% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2,936.92 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIR SIZED INCREASE IN OI AT THE COMEX OF 1341 WITH THE TINY PRICING GAIN THAT GOLD UNDERTOOK ON FRIDAY($0.90)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5397 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5397 EFP CONTRACTS ISSUED, WE HAD A GOOD SIZED GAIN OF 6738 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5397 CONTRACTS MOVE TO LONDON AND 1341 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 20.95 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED ACCOMPANYING THE TINY GAIN IN PRICE OF $0.90 WITH RESPECT TO FRIDAY’S TRADING AT THE COMEX. WE WILL COMMENCE WITH SPREADING ACCUMULATION IN GOLD AS THE MONTH PROCEEDS/

we had: 193 notice(s) filed upon for 19300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $24.70 TODAY//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 1.76 TONNES

WHICH WAS UTILIZED IN THE RAID TODAY.

INVENTORY RESTS AT 794.04 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 16 CENTS TODAY:

A BIG CHANGES WITH RESPECT TO SILVER INVENTORY AT THE SILVER SLV:

A SURPRISING PAPER DEPOSIT OF 936,000 OZ

/INVENTORY RESTS AT 323.330 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A CONSIDERABLE SIZED 2257 CONTRACTS from 220,612 DOWN TO 218,355 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JULY: 0 CONTRACTS FOR AUGUST: 0, FOR SEPT. 1816 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1816 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 2025 CONTRACTS TO THE 1816 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL LOSS OF 441 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 1.045 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY ; 2.660 MILLION OZ FOR JUNE AND NOW JULY AT 20.150 MILLION OZ STANDING SO FAR.

RESULT: A CONSIDERABLE SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 6 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1816 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 66.03 POINTS OR 2.22% //Hang Sang CLOSED DOWN 78.80 POINTS OR 0.28% /The Nikkei closed UP 454.05 POINTS OR 2.13%//Australia’s all ordinaires CLOSED UP .48%

/Chinese yuan (ONSHORE) closed UP at 6.8427 /Oil UP TO 60.02 dollars per barrel for WTI and 66.53 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.8427 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8421 TRADE TALKS RESUME//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/

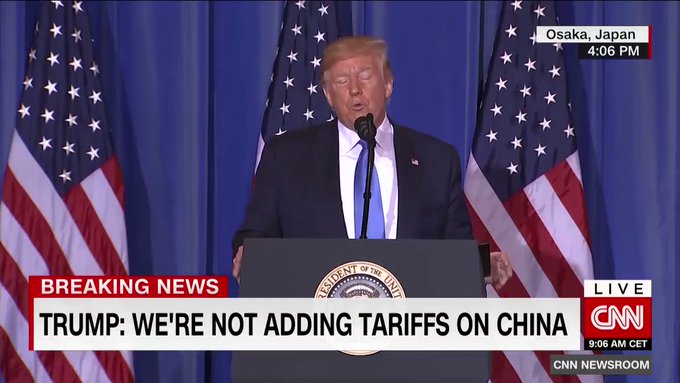

Early Saturday morning/Friday night: China and the USA agree to a ceasefire as their trade talks are back on. Trump concedes on Huawei and China agrees to purchase more goods. The problem is now with Powell as he will probably delay his interest rate cuts.

( zerohedge)

ii)Wall Street responds/Saturday morning

( zerohedge)

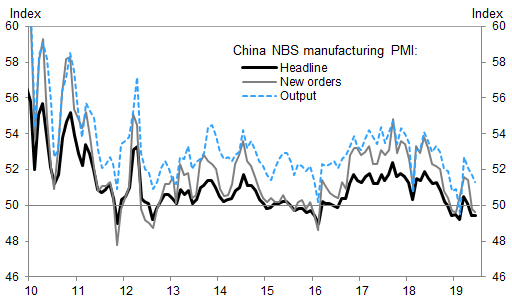

iii)This is not good for China. Last night they revealed with latest Mfg PMI and it was awful as it fell below 50 and thus contraction in their economy

( zerohedge)

iv)Hong Kong protests erupt again as thousands storm the legislature. The citizens will no way go for extradition to the Mainland.

( zerohedge)

4/EUROPEAN AFFAIRS

iItaly

A female captain of a Migrant NGO ship has been arrested after illegal docking in Italy

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Turkey

A wounded Erdogan is a dangerous person. From his purchase of Russian made S 400’s to his attack on ships trying to bring out natural gas in the Israeli-Cypriot-Greek waters.

( Hallinan//Counterpunch.org)

i b)Libya/Turkey/USA

Basically Hafter has declared war on Turkish planes flying over Libya and also boats off its shore. This proxy war is escalating fast. It certainly looks like Turkey will have to leave NATO as their policies are continuing to show their true colours as they face east.

(zerohedge)

i)IRAN

Iran enriches Uranium and the level has now surpasses 300 kg. Israel and the uSA are not happy.

( zerohedge)

6. GLOBAL ISSUES

i)Canada/Vancouver

China has long sought to get its money out of China and now Hong Kong is doing the same thing (the latest riots), Vancouver is one of the hot spots for the Chinese with Toronto coming in 2nd. It has made housing unaffordable now.

( zerohedge)

ii)Global warnings

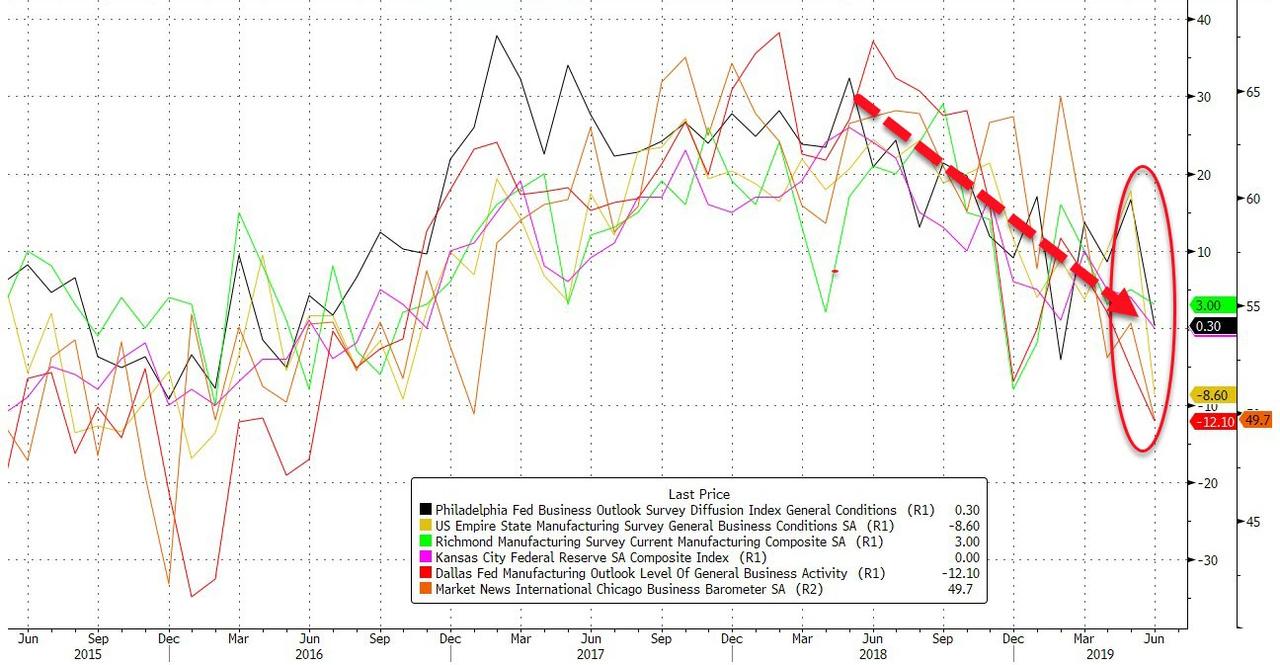

this is something that you must pay attention to: The BIS which is the central bank to the central banks warns of a worsening and spreading global slowdown as central banks are running out of ammo

(courtesy BIS/zerohedge)

iib)The latest manufacturing surveys: Japan’s Tankan mfg survey, China’s PMI and now the uSA all witnessing market declines

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

i)Dave is correct: the raid was well orchestrated by our crooks

(Dave Kranzler/IRD/GATA)

ii)Government debts are continually on the rise. So it is probably correct to assume that the only way to handle rising government debt is to lower all interest rates to zero or below

(Smith/Bloomberg/GATA)

iii)A must read…

James Turk states that the run up in gold has created losses of 2.2 billion dollars in gold. Who can withstand such losses other than central banks.

( Kingworldnews/James Turk/GATA)

iv)MbS has been very chummy with Trump who seems to have ignored the Khashoggi murder being orchestrated by the Prince. Now the Saudi’s are buying huge amounts of uSA treasuries.

(Bloomberg/GATA)

v)The following is continually happening in Europe as Swiss banks confiscate citizens allocated gold

( Von Greyerz/Kingworldnews)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

II)MARKET TRADING/USA

ii)Market data/USA

iii)USA ECONOMIC/GENERAL STORIES

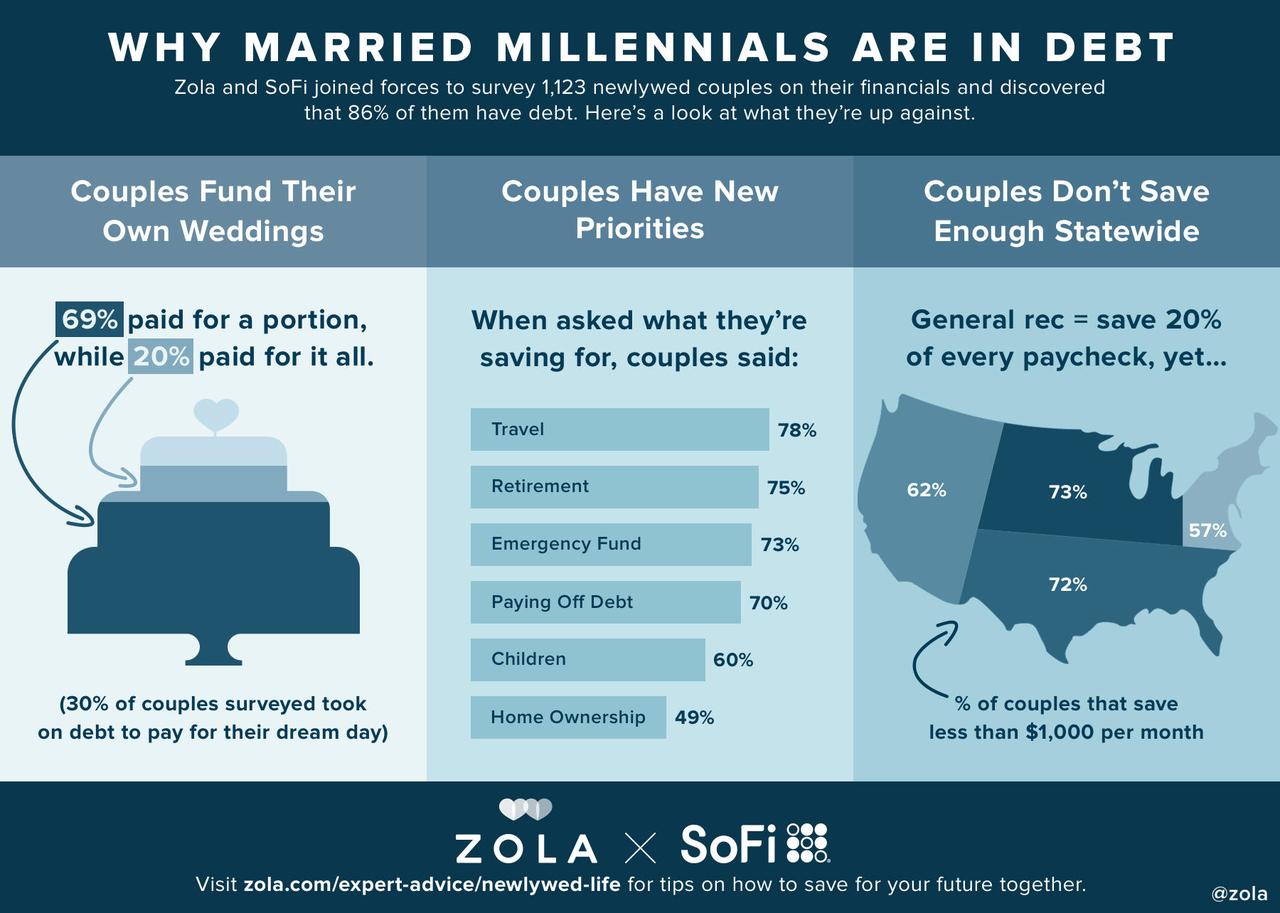

a)A good look at how millennials are thinking of marriage..how they use high interest loans to pay for their weeddings

etc

( zerohedge)

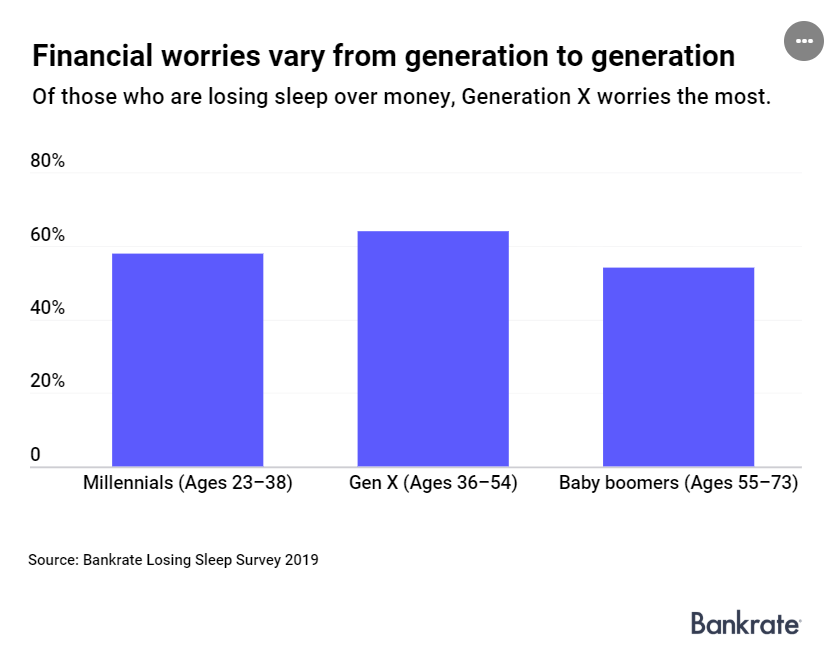

b)Inflation is ripping apart American way of life…

now more than half of Americans are lying awake at night worrying about how they are going to pay for necessities of life

(courtesy zerohedge)

c)Quite a story…Boeing outsourced its 737 Max software to low paying engineers ( after laying off higher cost engineers)

d)How the USA pension system is on a death spiral and it is reaching crisis mode

e)It is not just the USA that has devastating crop losses. It is happening all over the globe( Michael Snyder)

SWAMP STORIES

Let us head over to the comex:

we had 0 dealer entry:

We had 1 kilobar entries

total gold withdrawals; 32.15 oz

FOR THE JULY 2019 CONTRACT MONTH)Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 193 contract(s) of which 74 notices were stopped (received) by j.P. Morgan dealer and 10 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account and 0 notices by the squid (Goldman Sachs)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JULY /2019. contract month, we take the total number of notices filed so far for the month (564) x 100 oz , to which we add the difference between the open interest for the front month of JULY. (226 contract) minus the number of notices served upon today (193 x 100 oz per contract) equals 59,700 OZ OR 1.8569 TONNES) the number of ounces standing in this NON active month of JULY

Thus the INITIAL standings for gold for the JULY/2019 contract month:

No of notices served (564 x 100 oz) + (226)OI for the front month minus the number of notices served upon today (193 x 100 oz )which equals 59,700 oz standing OR 1.8569 TONNES in this active delivery month of JUNE.

We GAINED 173 contracts or an additional 17,300 oz will stand as these guys refused to morph into London based forwards as well as negating a fiat bonus. Somebody was in need of physical gold badly on this side of the pond…VERY UNUSUAL TO SEE QUEUE JUMPING THIS EARLY IN THE UP FRONT JULY CONTRACT MONTH.

SURPRISINGLY LITTLE TO NO GOLD HAS BEEN ENTERING THE COMEX VAULTS AND WE HAVE WITNESSED THIS FOR THE PAST YEAR!! WE HAVE ONLY 10.043 TONNES OF REGISTERED ( GOLD OFFERED FOR SALE) VS 1.8569 TONNES OF GOLD STANDING// THEY SEEM TO BE USING CONSIDERABLE GOLD VAPOUR TO SETTLE UPON UNSUSPECTING LONGS.

total dealer silver: 92.323 million

total dealer + customer silver: 305.683 million oz

The total number of notices filed today for the JULY 2019. contract month is represented by 515 contract(s) FOR 2,575,000 oz

To calculate the number of silver ounces that will stand for delivery in JULY, we take the total number of notices filed for the month so far at 3135 x 5,000 oz = 15,675,000 oz to which we add the difference between the open interest for the front month of JULY. (1410) and the number of notices served upon today (515 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JULY/2019 contract month: 3135(notices served so far)x 5000 oz + OI for front month of JULY( 1410) number of notices served upon today (515)x 5000 oz equals 20,150,000 oz of silver standing for the JULY contract month.

WE GAINED 164 CONTRACTS OR AN ADDITIONAL 820,000 OZ WILL STAND AT THE COMEX AS THESE GUYS REFUSED TO MORPH INTO A LONDON BASED FORWARDS AND AS WELL THEY ALSO NEGATED A FIAT BONUS. IT SEEMS THAT SOMEBODY WAS BADLY IN NEED OF PHYSICAL SILVER ON THIS SIDE OF THE POND JOINING GOLD!.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 69,221 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 60,949 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 260,949 CONTRACTS EQUATES to 304.7 million OZ 43.5% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -0.34% June 27/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.10% to NAV (JUNE 27/2019 )

Note: Sprott silver trust back into NEGATIVE territory at -0.34%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 13.77 TRADING 13.23/DISCOUNT 3.96

END

And now the Gold inventory at the GLD/

JULY 1: WITH GOLD DOWN $24.70 A HUGE “PAPER GOLD” WITHDRAWAL OF 1.76 TONNES FROM THE GLD/INVENTORY RESTS TONIGHT AT 794.04 TONNES

JUNE 28/WITH GOLD UP $.90 TODAY: ANOTHER 2.05 TONNES OF PAPER GOLD REMOVED AND THIS GOLD WAS USED IN ATTACKING GOLD AT THE COMEX/INVENTORY RESTS AT 795.80 TONNES

JUNE 27/WITH GOLD DOWN $6.10: ANOTHER HUGE WITHDRAWAL OF 1.76 PAPER TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 797.61 TONNES

JUNE 26/WITH GOLD DOWN $3.00: WE HAD A HUGE WITHDRAWAL OF 2.37 TONNES FROM THE GLD/INVENTORY RESTS AT 799.61 TONNES

JUNE 25/WITH GOLD UP $1.30 (AND WAY UP BEFORE THE BANKERS WHACKED) WE WITNESSED ANOTHER 1.95 TONNES OF PAPER GOLD ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 801.98 TONNES

JUNE 24/WITH GOLD UP $18.00 A MONSTROUS PAPER DEPOSIT OF 34.93 TONNES/INVENTORY RESTS AT 799.03 TONNES

JUNE 21/WITH GOLD UP $ 2.90, NO CHANGE IN GOLD INVENTORY: INVENTORY RESTS AT: 764.10 TONNES

June 20/WITH GOLD UP $47.95, NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 19 WITH GOLD DOWN $1.65: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONES

JUNE 18/JUNE 18/WITH GOLD UP $7.60: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 17/WITH GOLD DOWN $1.65 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 764.10 TONNES

JUNE 14/ WITH GOLD UP $1.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.40 TONNES OF PAPER GOLD INTO THE GLD///INVENTORY RESTS AT 764.10 TONNES

june 13/WITH GOLD UP $6.60 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 759.70 TONNES

JUNE 12/WITH GOLD UP $7.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 756.18 TONNES

JUNE 11/WITH GOLD UP $1.65 CENTS TODAY: A TINY CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .24 TONNES AND THIS IS TO PAY FOR FEES/INVENTORY RESTS AT 756.18 TONNES

JUNE 10/WITH GOLD DOWN $16.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES/INVENTORY RESTS AT 756.42 TONNES

JUNE 7/WITH GOLD UP $3.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 6/WITH GOLD UP $8.40 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 5 WITH GOLD UP $6.00 TODAY/STRANGE: A WITHDRAWAL OF 2.06 TONNES FROM THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 4/WITH GOLD UP 0.85 TODAY: A MONSTROUS PAPER GAIN OF 16.44 TONNES/GLD INVENTORY RESTS AT 759.65 TONNES

JUNE 3/WITH GOLD UP $17.50 TODAY: ANOTHER BIG CHANGE, A DEPOSIT OF 2.35 TONNES OF GOLD INTO THE GLD//

MAY 31/WITH GOLD UP $17.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GLD INVENTORY RESTS AT 740.86 TONNES

MAY 30: WITH GOLD UP $6.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES/INVENTORY RESTS AT 740.86 TONNES

MAY 29/WITH GOLD UP $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 737.34 TONNES

MAY 28/WITH GOLD DOWN $6.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD> A WITHDRAWAL OF 1.47 TONNES/INVENTORY RESTS AT 737.34 TONNES

MAY 24/WITH GOLD DOWN $1.60 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 738.81 TONNES

MAY 23/WITH GOLD UP $11.10 TODAY: A STRANGE WITHDRAWAL OF .88 TONNES FORM THE GLD/INVENTORY RESTS AT 738,81 TONNES

MAY 22//WITH GOLD FLAT TODAY: WE HAD A GOOD 1.52 TONNES OF GOLD DEPOSIT INTO THE GLD/INVENTORY RESTS TONIGHT AT 739.69 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JULY 1/2019/ Inventory rests tonight at 794.04 tonnes

*IN LAST 617 TRADING DAYS: 140.72 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 517 TRADING DAYS: A NET 24.96 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JULY 1/ WITH SILVER DOWN 16 CENTS: A SURPRISING DEPOSIT OF 936,000 OZ INTO THE SLV/INVENTORY RESTS TONIGHT AT 323.330 MILLION OZ/

JUNE 28/WITH SILVER UP 6 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.394 MILLION OZ//

JUNE 27/WITH SILVER DOWN 7 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.575 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.394 MILLION OZ//

JUNE 26/WITH SILVER UP 17 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 25/WITH SILVER DOWN 25 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ.

JUNE 24/WITH SILVER UP 11 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 21/WITH SILVER DOWN 22 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 20/WITH SILVER UP 53 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 19/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ/

JUNE 18 WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ

JUNE 17/WITH SILVER UP XXX CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ//

JUNE 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 12/WITH SILVER UP 4 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.413 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 11/WITH SILVER UP 10 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 10/WITH SILVER DOWN 38 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 7/WITH SILVER UP ANOTHER 12 CENTS, NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 6/WITH SILVER UP ANOTHER 9 CENTS TODAY: A FAIR SIZE DEPOSIT OF 630,087 OZ//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 5/WITH SILVER UP 4 CENTS TODAY: A HUGE PAPER DEPOSIT OF 2.396 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 314.434 MILLION OZ//

JUNE 4/WITH SILVER UP 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

JUNE 3/WITH SILVER UP 19 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

MAY 31/WITH SILVER UP 6 CENTS TODAY: A DEPOSIT OF 422,000 OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 312.038 MILLION OZ/

May 30/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ///

MAY 29/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 28/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 24/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ/

MAY 23/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 22/WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 311.616 MILLION OZ

MAY 21: WITH SILVER DOWN 3 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV; A WITHDRAWAL OF 750,000 OZ///INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 20/WITH SILVER UP 6 CENTS:NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.366 MILLION OZ

Gold Falls 1.4% As Trade Truce Sees Gold Futures Sold Overnight

GoldCore Note

Gold fell 1.4% from a six year high to back below $1,400 at $1,390 an ounce today as traders took profits and sold gold futures after the U.S. and China agreed to a trade war truce.

Risk assets like stocks got a bounce higher while safe havens like gold and the Swiss franc came off as traders digested the better than expected news from the G20 summit. Gold prices fell after the leaders of the two largest economies, Trump and Xi Jinping, simply agreed to resume negotiations.

Markets and many investors are increasingly concerned about the outlook for the U.S. and the global economy. Participants will now focus on the U.S. jobs data which is due Friday.

Gold’s sell off may continue this week and a further correction is likely given the scale of the gains in the last month. Gold’s correction is likely to be temporary and will provide an attractive entry point for those seeking to take a position or buy gold. Dollar, pound and euro cost averaging and accumulating remains prudent.

The long-running and deepening trade, currency and geopolitical tensions will not disappear any time soon and looser monetary policies will also support gold.

LBMA Gold Prices (AM/ PM Fix – USD, GBP & EUR)

01-Jul-19 Prices not available from LBMA at time of publishing

27-Jun-19 1402.25 1402.50, 1103.71 1105.87 & 1233.14 1234.76

26-Jun-19 1406.75 1403.95, 1109.22 1106.73 & 1238.501236.32

25-Jun-19 1429.55 1431.40, 1120.62 1124.36 & 1255.72 1256.20

24-Jun-19 1405.45 1405.70, 1102.58 1105.30 & 1233.56 1235.05

21-Jun-19 1388.35 1397.15, 1095.96 1101.93 & 1228.55 1233.12

20-Jun-19 1381.65 1379.50, 1086.25 1087.74 & 1222.90 1221.27

19-Jun-19 1342.40 1344.05, 1066.67 1066.64 & 1198.36 1199.43

18-Jun-19 1344.55 1341.35, 1073.22 1070.67 & 1201.89 1198.09

News and Commentary

Gold tumbles nearly 1.5% as trade truce dents safe-haven demand

Trump says China trade talks ‘back on track,’ new tariffs on hold

Australia sees gold overtaking thermal coal as export earner

European shares hit 2-month high after U.S-China revive trade talks

UK current account gap hits highest since 2016, pushed up by gold

Facebook Should Link its Libra Cryptocurrency to Gold – Steve Forbes

BIS Warns “Slowdown Is Worsening And Spreading” As Central Banks Run Out Of Ammo

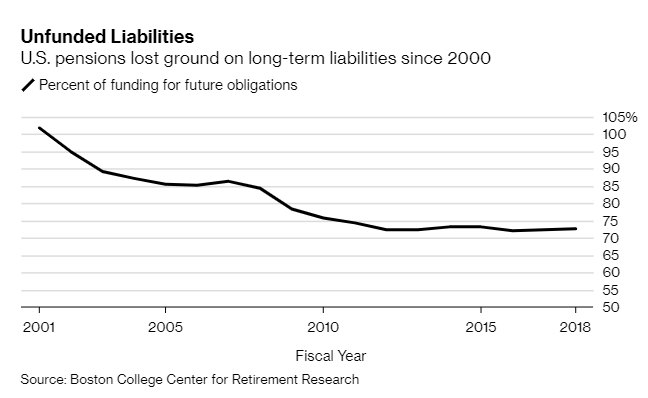

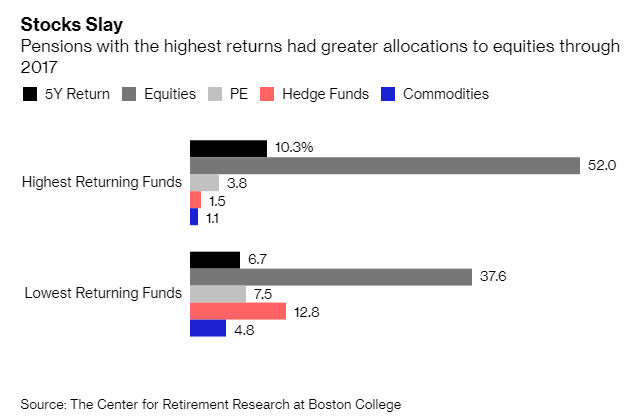

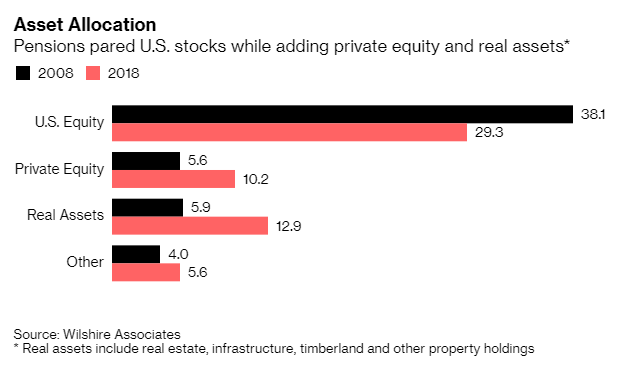

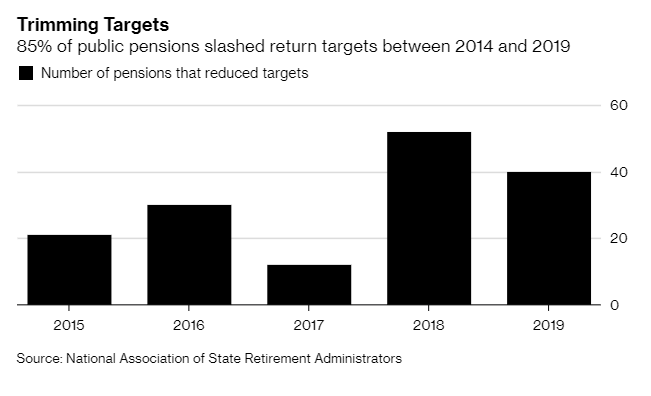

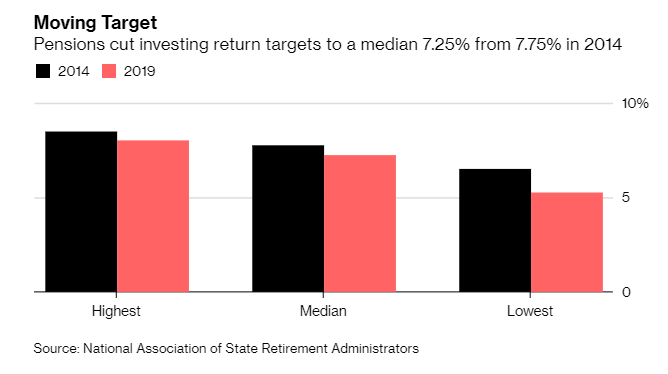

Pension Crisis Deepens in U.S. as Strategies Shift, Outlooks Dim

U.S. Is Heading to a Future of Zero Interest Rates

Highly Leveraged Zombie Companies Threaten the Global Economy

Receive Our Free Daily or Weekly Updates by Signing Up Here

ii) Physical stories courtesy of GATA/Chris Powell

Dave is correct: the raid was well orchestrated by our crooks

(Dave Kranzler/IRD/GATA)

Dave Kranzler: Expect raid on gold next week

Submitted by cpowell on Sun, 2019-06-30 03:34. Section: Daily Dispatches

11:35p ET Saturday, June 29, 2019

Dear Friend of GATA and Gold:

The week ahead probably will see attacks on the gold price by bullion banks because it includes the July 4 holiday in the United States and a financial crisis seems to be developing behind the scenes, Dave Kranzler of Investment Research Dynamics writes today.

“Low-volume holiday periods are the favorite time for the bullion banks to stage a raid on gold,” Kranzler writes. “The success of this raid is crucial to maintaining the illusion that obvious systemic problems are manageable.”

Kranzler’s commentary is headlined “Gold: Boom Goes the Dynamite” and it’s posted at IRD here:

http://investmentresearchdynamics.com/gold-boom-goes-the-dynamite-2/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Government debts are continually on the rise. So it is probably correct to assume that the only way to handle rising government debt is to lower all interest rates to zero or below

(Smith/Bloomberg/GATA)

Noah Smith: Zero interest rates forever may be only way to handle rising government debt

Submitted by cpowell on Sat, 2019-06-29 14:29. Section: Daily Dispatches

U.S. Is Heading to a Future of Zero Interest Rates Forever

By Noah Smith

Bloomberg News

Thursday, June 27, 2019

The Congressional Budget Office has just released its projections for the U.S. federal budget during the next 30 years. The picture is one of steadily rising deficits. Federal government borrowing now amounts to about 4.2% of gross domestic product each year. By 2049, the CBO predicts, that will more than double, to 8.7%:

Only a small portion of these deficits will be due to tax cuts; the CBO projection expects that individual income taxes rise substantially as a share of GDP. Nor will it be due to government profligacy; CBO predicts that discretionary spending will shrink substantially relative to the size of the economy.

…

Instead, the growth in deficits is mostly about two things. First, government health care spending is projected to grow, which is partly due to population aging and partly because the CBO predicts that medical costs will keep going up. Second, and even more importantly, the CBO predicts that interest rates will rise, forcing the government to spend much more on simply paying interest on its debt. The federal government now pays an average of 2.4 % to borrow; in three decades, the CBO predicts that this will rise to 4.2%.

If true, that will cause an exponential increase in the amount the government has to pay for debt service. …

… For the remainder of the commentary:

https://www.bloomberg.com/opinion/articles/2019-06-27/u-s-s-rising-debt-…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

end

A must read…

James Turk states that the run up in gold has created losses of 2.2 billion dollars in gold. Who can withstand such losses other than central banks.

(courtesy Kingworldnews/James Turk/GATA)

Only central banks could handle recent losses on gold futures sales, Turk says

Submitted by cpowell on Sun, 2019-06-30 19:39. Section: Daily Dispatches

3:39p ET Sunday, June 30, 2019

Dear Friend of GATA and Gold:

At King World News this weekend, GoldMoney founder James Turk says only central banks could accommodate the sort of losses — more than $2 billion — suffered by gold futures sellers since April:

https://kingworldnews.com/central-banks-see-massive-2-2-billion-in-losse…

And Swiss gold fund manager Egon von Greyerz says another Swiss bank seems to have misplaced its client’s gold, a reminder that no gold investor should store his gold with a bank:

https://kingworldnews.com/greyerz-another-swiss-bank-cant-find-their-cli…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Please join GATA from Nov. 1-4 at the New Orleans Investment Conference

Submitted by cpowell on Mon, 2019-07-01 01:49. Section: Daily Dispatches

9:48p ET Sunday, June 30, 2019

Dear Friend of GATA and Gold:

With four months to go, it’s time to start thinking about the biggest and most comprehensive financial conference in North America, the New Orleans Investment Conference, to be held Friday through Monday, November 1-4.

The conference’s speakers again will include GATA Chairman Bill Murphy and your secretary/treasurer. Also speaking will be GATA favorites including Gold Newsletter editor Brien Lundin, commodity newsletter editor Dennis Gartman, renowned contrarian Doug Casey of Casey Research, newsletter editors Mary Anne and Pamela Aden, Peter Boockvar of Bookmark Advisers, and Thom Calandra of The Calandra Report.

…

..The conference always is oriented toward sound money, free and transparent markets, and limited and accountable government and provides many prospective investment ideas, so GATA supporters always feel both comfortable and challenged there.

The conference continues to be held at the sensational Hilton New Orleans Riverside hotel downtown, on the banks of the Mississippi River at the northern entrance of the city’s famed RiverWalk shopping mall, just a few blocks from the historic French Quarter and across the street from Harrah’s casino.

Full of history, great restaurants, great music, fun, and romance, New Orleans competes mightily with the conference itself even as it much great value to the conference, so anyone considering attending the conference is well-advised to consider spending a few extra days in the city. November in New Orleans is usually balmy as winter descends on the rest of North America.

For more information about the conference and to register to attend, please visit:

https://neworleansconference.com/

We hope to see you there.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

MbS has been very chummy with Trump who seems to have ignored the Khashoggi murder being orchestrated by the Prince. Now the Saudi’s are buying huge amounts of uSA treasuries.

(Bloomberg/GATA)

Saudi buying of U.S. Treasuries has soared since Trump election

Submitted by cpowell on Mon, 2019-07-01 02:38. Section: Daily Dispatches

By Liz McCormick

Bloomberg News

Sunday, June 30, 2019

By now, President Donald Trump’s bromance with Mohammed bin Salman of Saudi Arabia is well documented. The platitudes and chummy photo-ops. The billions of dollars in U.S. arms sales. And, of course, the willingness to brush aside evidence implicating the crown prince in the murder of journalist Jamal Khashoggi.

But what’s gone largely unnoticed is just how enthusiastic the kingdom has been in snapping up America’s debt.

…

After aggressively culling its holdings of U.S. government debt for most of 2016, Saudi Arabia has amassed an even larger position since Trump’s election in November that year. Based on the latest reported figures, the nation nearly doubled its ownership of Treasuries to $177 billion. No major foreign creditor has ramped up its lending to the U.S. faster. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-06-30/saudi-buying-of-u-s-d…

iii) Other physical stories:

The following is continually happening in Europe as Swiss banks confiscate citizens allocated gold

(courtesy Von Greyerz/Kingworldnews)

BREAKING: Greyerz – Another Swiss Bank Can’t Find Their Client’s Gold

As the world edges closer to the next crisis, today the man who has become legendary for his predictions on QE and historic moves in currencies told King World News that another Swiss bank can’t find their client’s gold.

Another Swiss Bank Can’t Find Client’s Gold

June 30 (King World News) – Egon von Greyerz:“Don’t let your bank hold your gold. They might not find it. A gold investor told us recently that his Swiss bank had moved the client’s gold from the the bank’s safe to a private vault in the name of the bank, in Zurich. The client was aware of this move. But then the problems started…

Listen to the greatest Egon von Greyerz audio interview ever

by CLICKING HERE OR ON THE IMAGE BELOW.

Sponsored

Sponsored

The Gold Was Not To Be Found Anywhere

The gold was allocated and the client had the bar numbers. The client wanted to store the gold through our company and instructed the bank accordingly. But the gold wasn’t there any more. The gold was supposed to be segregated but the bank had stored it in the collective vault. And the client’s allocated, numbered bars were not to be found anywhere.

Presumably, the bank will accept liability and buy new bars for the client. But again this proves that it is not safe to keep your gold in a bank. We have regularly experienced similar problems with many different Swiss Banks, big or small.

In normal times when there is still physical gold available, the bank will clearly rectify the problem. But when there is a shortage of gold and the bank comes under pressure, they could easily “borrow” client gold. If at that point there is no gold available, the bank could have a liability that it wouldn’t be able to meet, especially if the gold price rises fast.

Do Not Store Gold In A Bank Vault Or Safety Deposit Box

So again I warn gold investors not to hold physical gold in a bank vault or in a bank safe deposit box. When the next financial crisis starts, you will not get your gold back from the bank’s vault and you will not get access to your safe deposit box. The bank will obviously tell you that the gold in the box is yours, but I wouldn’t trust them. Also, the bank doors could be closed for a very long time. So even if you did eventually got access, it might take years.Much better to store gold privately in secure vaults which you have physical access to at any time.

Total global government bond market is around $50 trillion. Out of that total, $13 trillion carries negative interest. To me it is totally incomprehensible that anyone can lend bankrupt governments money.First, since most currencies have lost 97-99% of their value in real terms after the Fed was created in 1913, you are guaranteed to get back less real money than you invested if you hold a sovereign bond for more than a few months.Second, no government will be in a position to pay back their debt in coming years. And soon they will reach a point when they can’t even pay the interest.

Who Buys This Stuff?

Then how can investors lend governments $13 trillion of money and pay for the privilege of the state holding your money.That is totally absurd. You give money to an insolvent country and you must pay them for that great honor. Take little Portugal as an example. They have a massive debt to GDP of 125% and they also have negative yields from 2-5 years. What would you do? Would you lend money to a country that will never repay it and also pay them for the pleasure or buy gold? I certainly wouldn’t.

Gold is the only money that has survived for 5,000 years and also the only money that has maintained its purchasing power. It is also no one else’s liability and totally unencumbered. In addition, it is totally liquid and can be used for barter. I doubt that anyone would accept a Portuguese bond as payment in 2025 when it will be totally worthless. But I am completely convinced that everybody will accept a gold coin or gold bar.

Using Gold To Buy A Condo In Vietnam

Many people in the Far East prefer to hold gold or foreign currency to cash. The Bangkok Post reported recently about using gold for house purchases in Vietnam. A shopkeeper in Hanoi bought a new $138,000 condo with half gold, half cash. He said:

“We did it because we and the the seller didn’t want to do a bank transfer. We are so used to buying things with gold and cash.”

Cue The Anti-Gold, Pro-Cashless Society Propaganda

The newspaper stated that Vietnam is one of the world’s fastest growing economies, yet “it is still in the dark ages when it comes to joining the global trend toward cashless transactions.”

Hmmm! It seems that the shopkeeper understands a lot more than the journalist. The shopkeeper understood and trusted the timeless value of gold rather than paper money that is likely to become worthless in the next few years. Seems like the journalist will be more likely to go back to the Dark Ages when paper money dies in the next few years.

The shopkeeper confirms the wisdom of the East that we often talk about. The people in India, China, Vietnam, Thailand and many more Eastern countries all put a major part of their savings in gold since they know that this is by far the best way to preserve wealth. Had the people in Zimbabwe, Argentina or Venezuela done this, it would have saved them from poverty and misery.

As asset prices collapse and gold appreciates, you will be able to buy a house for a fraction of the cost today, especially if you have your savings in gold, just like like the Vietnamese shopkeeper.

Let us look at the coming collapse of the price of a new house in the USA. Today the median price for a new house is $335,000. In 1963 it was $17,000 – a 20x increase.

As asset bubbles implode together with debt, a return to at least the 1985 level seems likely. That would mean a 75% fall in house prices. As credit dries up and interest rates surge, I would expect that this will be the minimum fall.

The Road To $10,000+ Gold

At the same time, let’s assume a very likely increase in the gold price to $5,000 in today’s money.In my view this is the very minimum and $10,000 or much higher is more likely.

235 Ounces Of Gold To Buy New Home Today But Only 17 Ounces Later

As the table above shows, a new home today costs $335,000 or 235oz of gold. In 2025, with the average price of houses down 75% to $84,000, and gold up 254% to $5,000, a house would cost only 17oz of gold. That is a 93% fall in gold terms. Sounds unrealistic today but it is very likely.

As the next global financial crisis unravels in the coming few years, we will see massive money printing, total debasement of most currencies and hyperinflation. The only way to protect yourself from the total destruction of paper assets is to hold physical gold and some silver.

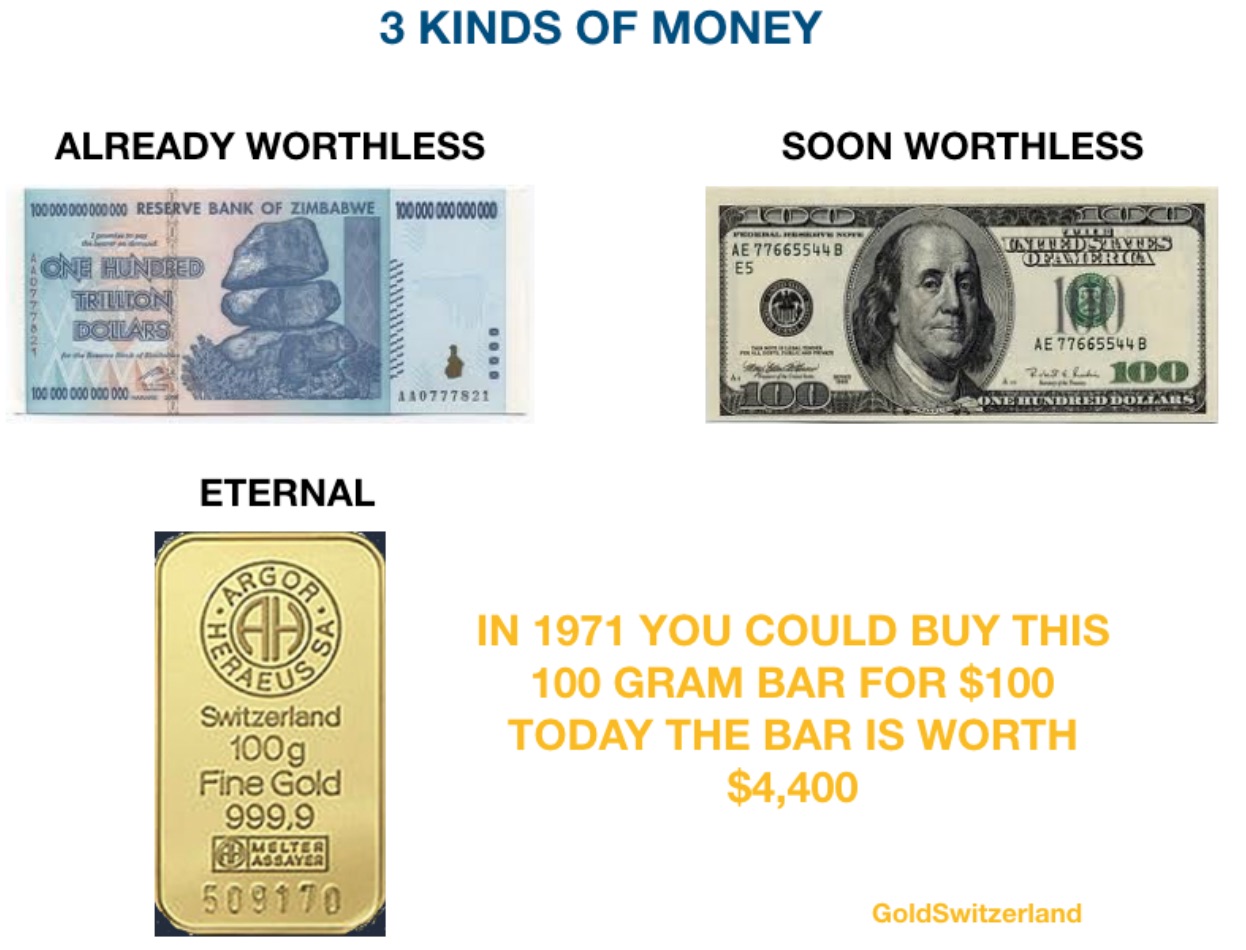

There are three kinds of money, Worthless, Soon Worthless, and Eternal. Since all fiat money has always gone to ZERO throughout history, the same will be the case for the dollar and all other currencies in coming years.

In 1971, you could buy 100 grams of gold (just over 3 oz) for the $100 bill in the picture above. Today the $100 gram bar costs $4,400 and for $100 you would only get a small corner of the gold bar. This is how central banks destroy the value of money with most people being totally unaware since they don’t understand that gold is constant purchasing power and eternal money.

The Gold Maginot Line Broken Decisively

Gold has moved $130 in a short time, decisively breaking the 6 year Maginot Line at $1,350. The current pause in the up-move can last around 2-10 days but thereafter gold will rise quickly toaround $1,650.

Crisis Will Return With A Vengeance

Very important changes will soon take place in markets with the 2007-9 crisis returning with a vengeance. The final phase up in US stocks could last a few weeks but most likely not more than 2 months. Thereafter a secular bear market will start that will be devastating for the world economy, the financial system and paper money. Wealth preservation today is more important than anytime in history…For those who would like to read more of Egon von Greyerz’s fantastic articles CLICK HERE.

$2.2 Billion In Losses For Gold Shorts

READ THIS NEXT! Central Banks See Massive $2.2 Billion In Losses On Gold Shorts, But Here Is Why It May Get Much Worse CLICK HERE TO READ

end

|

11:30 AM (4 minutes ago) |

|

||

|

||||

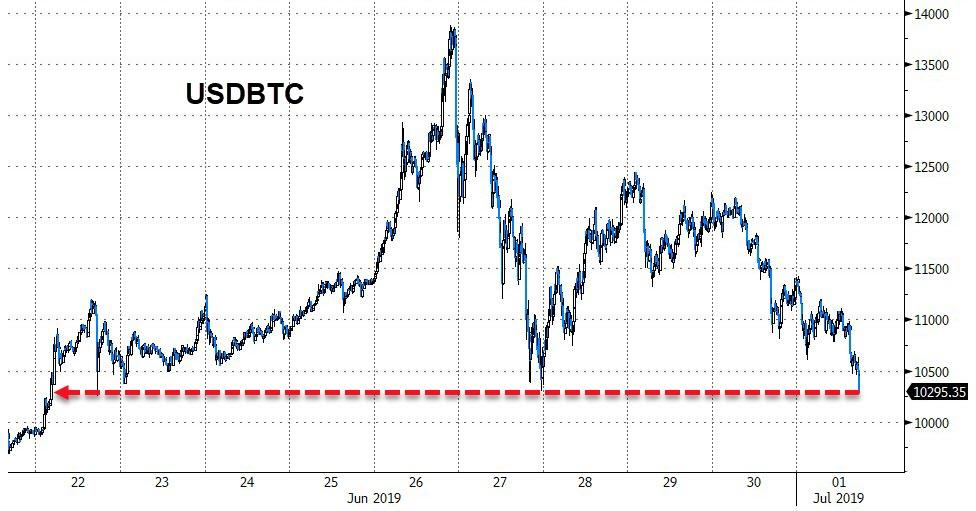

Bitcoin Tumbles To 10-Day Lows As Major Korean Bank Clamps Down On Crypto-Linked Accounts

Bitcoin prices have accelerated lower overnight, breaking below the $11,000 level and falling to 10-day lows.

Bitcoin is leading the charge lower but the rest of crypto is also sliding…

While potentially some relief from the China-US trade truce could be driving some selling in cryptos, some market participants noted that fears of further crackdowns in Asia also sparked some unwinds.

As CoinTelegraph’s Thomas Simms reports, one of South Korea’s biggest banks is planning to intensify regulations on accounts linked tocrypto exchanges, BEI News reported on July 1.

image courtesy of CoinTelegraph

The “special measures” Shinhan Bank are proposing would reportedly involve dedicating staff to analyzing account transactions.

It is believed the bank is hoping to distance itself from claims that it is helping financial criminals, amid a rise in the number of fraud cases involving exchanges.

Later in July, the bank is also hoping to launch an artificial intelligence monitoring system that uses deep learning to identify fraudulent transactions more quickly and accurately.

BEI News quoted a Shinhan Bank spokesperson as saying:

“We have set up a comprehensive plan for the elimination of telecommunication and financial fraud… We will continue to implement preventive measures so that customers will not be harmed in the future.”

The clampdown comes as crypto exchanges continue to fall victim to hacks — including the South Korean platform Bithumb.

Bithumb has suffered several major hacks. In March, more than three million eos (worth $17.5 million at press time) was stolen from a hot wallet.

A bigger attack last summer saw $17 million stolen across 11 cryptocurrencies, predominantly bitcoin (BTC) and ether (ETH.)

end

Interesting report: Reuters believes that world gold demand (consumption) will grow by 3.7% to 4,728 tonnes this year lead by central bank buying. Jewelry demand rises by 5.7% up to 2,257 tonnes. The total world production including China and Russia is 3500 tonnes. If you remove both of these countries gold available to the world is around 2850 tonnes and demand is 4728 tonnes.

(courtesy Reuters)

World Gold consumption to rise in 2019 to 2020, before falling in 2021: report

CANBERRA (Scrap Register): World gold consumption is likely to grow at an average annual rate of 3.7% in 2019 and 2020 – reaching a peak of 4,728 tonnes in 2020 – and then decrease by 4.9% in 2021, to 4,497 tonnes, Australia’s Department of Industry, Innovation and Science said in its Resources and Energy Quarterly report.

The growth is expected to be largely driven by central banks’ gold buying, with a forecast increase of 4.3% a year in 2019 and 2020, to over 700 tonnes by 2020. The official sector is expected to remain a net buyer throughout the forecast period. The need to diversify central bank reserves is the key driver of many central banks’ growing appetite towards gold. After reaching a peak of 711 tonnes in 2020, the pace of central bank purchases is expected to decrease by 10% in 2021, to 640 tonnes, as geopolitical risks moderate, the report said.

Retail investment is expected to drive up global gold consumption, as the demand for gold bars and coins rises in 2019 and 2020. The report estimates retail investment to rise by 13 and 12 per cent in 2019 and 2020, to 1,244 and 1,392 tonnes, respectively.

This is being supported by trade tensions, the economic slowdown across advanced and developing economies, and political uncertainty in Europe, Venezuela and the Middle East. In China, ongoing trade tensions with the US are likely to boost gold demand, as retail investors seek to buy gold as a hedge against the depreciation of the Renminbi. However, gold retail investment is expected to slow down after 2020, as global economic slowdown and trade tensions are expected to ease, the report said.

Jewellery demand is forecast to rise by 5.7% in 2020 and 4.6% (to 2,357 tonnes) in 2021. Demand from China – the world’s largest jewellery consumer – is expected to remain strong, supported by the Chinese Government’s monetary and fiscal stimulus.

In India – the world’s second largest gold jewellery consumer – a strong demand growth forecast is propelled by robust economic growth, ongoing urbanisation, rising farm incomes, and improved consumer sentiment.

-END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.8427/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.8421 /shanghai bourse CLOSED UP 66,03 POINTS OR 2.22%

HANG SANG CLOSED DOWN 78,80 POINTS OR 0.28%

2. Nikkei closed UP 454.05 POINTS OR 2.13%

3. Europe stocks OPENED ALL GREEN EXCEPT /

USA dollar index UP TO 96.42/Euro FALLS TO 1.1348

3b Japan 10 year bond yield: RISES TO. –.15/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.49/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 60.02 and Brent: 66.53

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.33%/Italian 10 yr bond yield DOWN to 2.02% /SPAIN 10 YR BOND YIELD DOWN TO 0.02%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.45: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.34

3k Gold at $1392.55 silver at: 14.28 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 21/100 in roubles/dollar) 63.01

3m oil into the 60 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.31 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9816 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1142 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.33%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.02% early this morning. Thirty year rate at 2.54%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.6631..

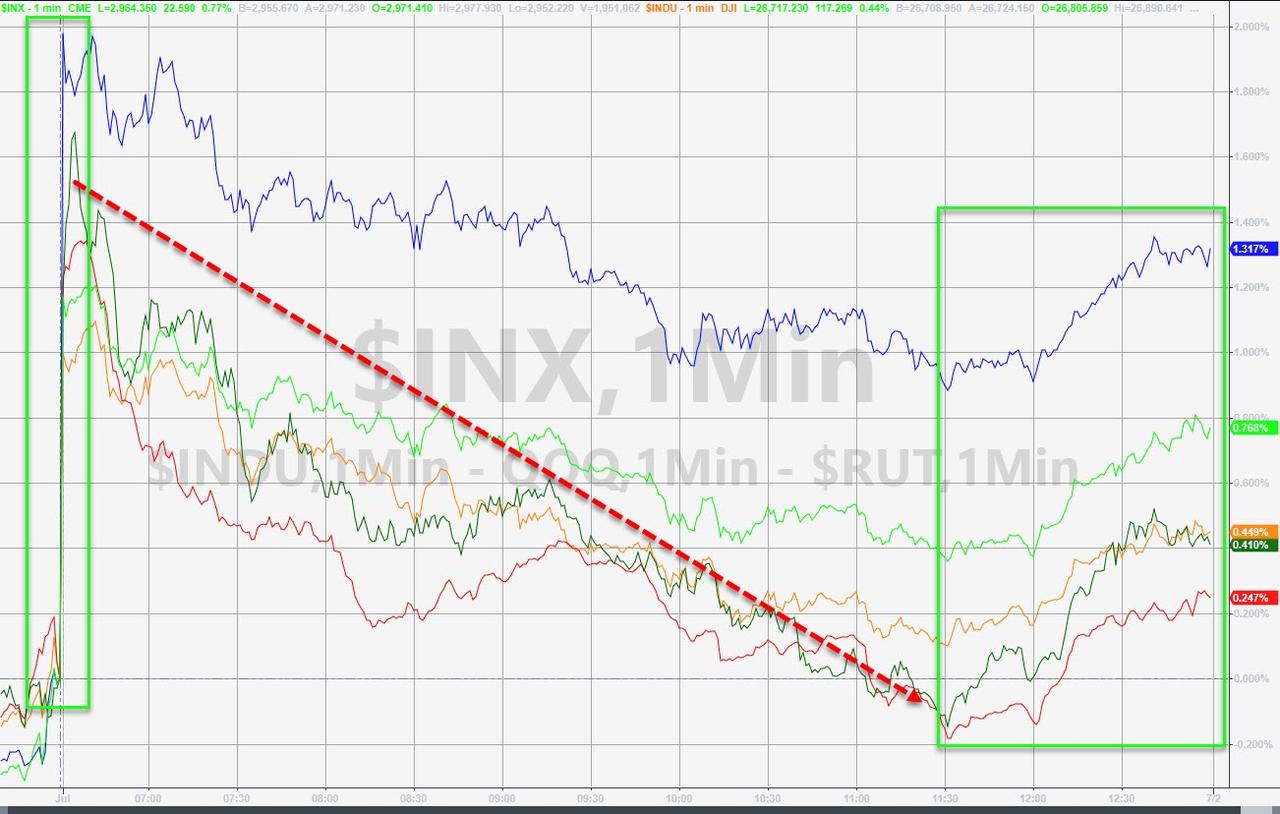

Global Stocks Soar On Trade Truce, As Other Assets Get Cold Feet

Global bonds retreated on Monday (although losses were pared) as the U.S. and China agreed to restart trade talks, leading investors to pare wagers on aggressive policy easing by the major central banks.

That, however, did not prevent stocks from surging out of the gate, with S&P futures set to open at new all time highs just 20 or so point below 3,000 even though as Bloomberg points out, the outcome of the G-20, or rather G-2, meeting was just as consensus expected.

Stocks are jumping even as none of the market Gremlins have left, with Hong Kong protests turning violent again on Monday (incidentally, there was zero mention of China’s growing pains in Hong Kong, just as Beijing wanted),while global PMI continued plumbing new cycle lows, and after both Chinese manufacturing surveys missed expectations, printing in contraction just below 50…

… the picture turned even uglier in Europe, where the UK PMI missed expectations, sliding to a three year low of 48, while Spain’s mfg PMI printed in contraction, or 47.9, for the first time in five and a half years.

Surveys from Japan and South Korea showed similar slowdowns as did the 19-country euro zone’s reading which contracted for fifth month running and at a faster pace than previously thought.

“Euro zone manufacturing remained stuck firmly in a steep downturn in June, continuing to contract at one of the steepest rates seen for over six years,” said Chris Williamson, chief business economist at IHS Markit. “The disappointing survey rounds off a second quarter in which the average PMI reading was the lowest since the opening months of 2013.”

None of this had an impact on stocks, however, with European markets rising over 1%, chasing the outperformance in Asia, as US equity futures ramped higher, even as the dollar firmed across the board, as traders reined in bets for a half-point rate cut from the U.S. Federal Reserve this month. And yet, the Fed’s dovishness which was responsible for the market’s gain in June (as a reminder PE multiple expansion accounted for 90% of the June surge), is being widely ignored on Monday, with the market’s attention focused on the G-20 outcome instead, where as we noted overnight (and this morning), nothing has been resolved.

To be sure, trader sentiment about the outcome was mixed: “It (Trump-Xi G20 meeting) played as well as possible,” said SEB Investment Management’s global head of asset allocation Hans Peterson. “So It gives us time to digest and get a bit better activity in the global economy.”

On the other hand, Bloomberg’s Cameron Crise was more skeptical, noting that “a truce is a long way from a deal, and it may be worth recalling that the sharp rally after the previous G-20 meeting between Trump and Xi lasted a mere 24 hours, albeit under a somewhat different backdrop. While there’s no guarantee that the rally fades by the end of the day, therefore, it wouldn’t come as a surprise to see a little late-session selling once the euphoria starts to cool off.”

For now, however, risk is certainly higher, with Europe’s STOXX 600 and Japan’s Nikkei climbed 1% and 2.1% respectively to hit two-month tops and MSCI’s global index added 0.2% having only just missed out on its best first half to a year.

In Asia, Chinese blue chips jumped 2.6% to their highest since late April, Germany’s export-heavy DAX sprang 1.5% to its highest since August, Wall Street futures were up over 1% while the combination of the Huawei hiatus and M&A activity hoisted Europe’s the tech sector to a one-year high.

In the US, E-Mini futures for the S&P and Nasdaq rose 1.1% and 1.7%, with the former breaking out above resistance, and just whispers away from 3,000 whereas in the bond market Treasury futures slid 10 ticks as yields on 10-year notes edged up 4 basis points to 2.04%.

Ironically, the S&P may hit 3,000 on the day the ISM dips below 50 (expectations for the Mfg ISM is for a 51.0 print).

As noted last night, Fed funds dropped over 5 ticks as the market scaled back the probability of a half-point rate cut this month to around 15%, from nearer 50% a week ago. “I think the Fed expectations in the market are very aggressive. Possibly a bit too aggressive,” SEB’s Peterson added.

The reaction in currency markets was to strip some recent gains from safe harbors like the yen and Swiss franc. The dollar crept up 0.4% on the yen to 108.26 and 0.7% on the franc to 0.9830. The dollar strengthened versus all its Group-of-10 peers, while haven currencies weakened. Weaker-than-forecast manufacturing PMIs from the euro zone weighed on the euro and capped losses in the region’s bonds. The pound slipped following disappointing U.K. manufacturing data and before Conservative leadership contender Jeremy Hunt is expected to detail contingency plans for a hard Brexit

In commodities, oil prices sprang higher on news OPEC and its allies look set to extend supply cuts at least until the end of 2019 as Iraq joined top producers Saudi Arabia and Russia in endorsing the policy. Brent crude futures rose $1.85 or 2.8% to $66.40, while U.S. crude gained $1.84 or 2.75% to $59.90 a barrel.

Expected data include manufacturing PMIs. No major company is scheduled to report earnings

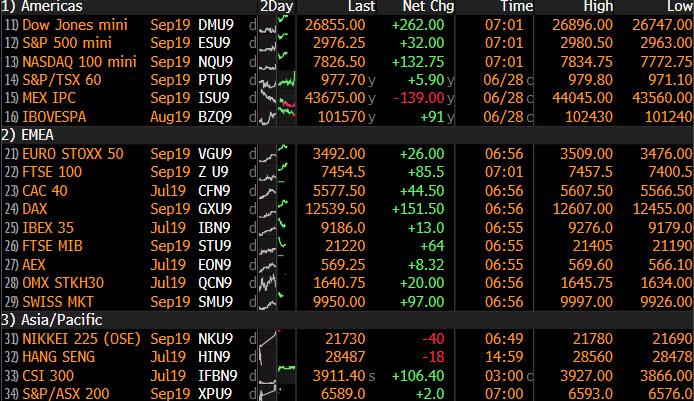

Market Snapshot

- S&P 500 futures up 1.1% to 2,976.25

- STOXX Europe 600 up 0.7% to 387.73

- MXAP up 0.8% to 161.38

- MXAPJ up 0.4% to 529.96

- Nikkei up 2.1% to 21,729.97

- Topix up 2.2% to 1,584.85

- Hang Seng Index down 0.3% to 28,542.62

- Shanghai Composite up 2.2% to 3,044.90

- Sensex up 0.8% to 39,716.91

- Australia S&P/ASX 200 up 0.4% to 6,648.10

- Kospi down 0.04% to 2,129.74

- German 10Y yield unchanged at -0.326%

- Euro down 0.4% to $1.1331

- Italian 10Y yield fell 3.2 bps to 1.74%

- Spanish 10Y yield fell 1.3 bps to 0.382%

- Brent futures up 2.8% to $66.53/bbl

- Gold spot down 1.5% to $1,388.10

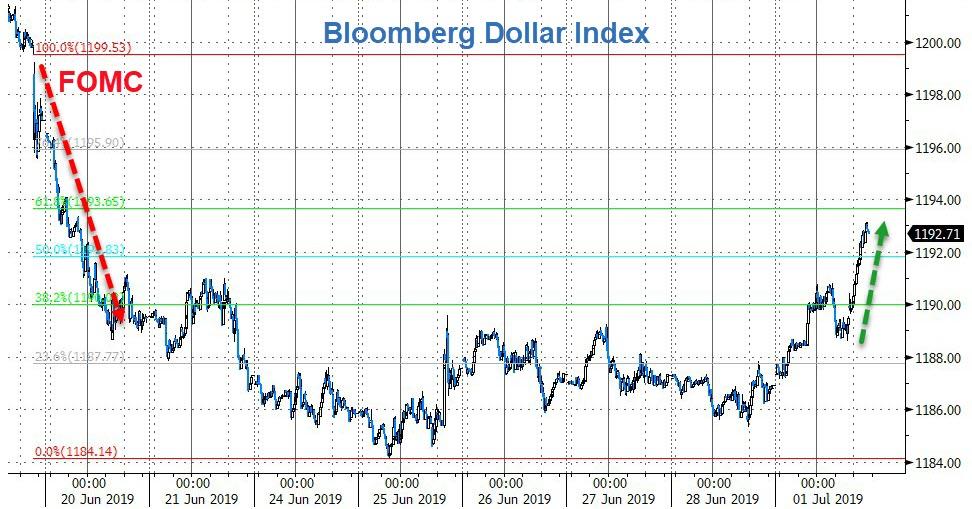

- U.S. Dollar Index up 0.4% to 96.51

Top Overnight News

- President Donald Trump declared the U.S. was “winning” the trade war a day after reaching a temporary truce with Chinese President Xi Jinping. Gauges of activity in China’s manufacturing sector showed the economy remains fragile, underlining the need for the truce with the U.S. forged at the weekend to be a lasting one

- Manufacturers in the euro area remained firmly stuck in a slump last month as new orders slid and business confidence remained subdued

- Tension returned to Hong Kong’s streets Monday as protesters attempted to break into the city’s legislature and thousands more began marching in opposition to the city’s China- backed government

- Sentiment among Japan’s large manufacturers deteriorated to the lowest level in almost three years amid trade tensions that are adding to uncertainties for the economic outlook

- Jeremy Hunt and Boris Johnson, the candidates competing to become U.K. prime minister, reiterated their willingness to take the nation out of the European Union without a deal if necessary, as both insisted they have the fiscal space to fund their spending plans

- The ECB presidency won’t be decided at the EU summit in Brussels, a high-ranking German official said, who declined to be identified because the matter is confidential. That decision will be postponed until September in an attempt to move it away from the highly political nominations for the commission and council presidencies

- Oil raced higher after Russian President Vladimir Putin struck a deal with Saudi Crown Prince Mohammed Bin Salman at the G-20 to extend output cuts for the rest of this year and potentially into early 2020, while the U.S. and China called a temporary truce in the trade war

- Factory sentiment across Asia became even more frigid in June, signaling a worsening in the region’s growth outlook as U.S.-China trade tensions continue to simmer

- The European Central Bank could be headed for its first-ever female president as European Union leaders haggle over top policy positions

Asian equity markets began H2 with gains across the board as global sentiment was buoyed following the US-China trade truce at the G20, while President Trump also met with North Korea leader Kim at the Demilitarized Zone and became the first sitting US President to step into North Korean territory. ASX 200 (+0.4%) was lifted by the trade sensitive sectors, as well as energy names after oil prices were buoyed by news of a Russia and Saudi agreement regarding the output cut deal. Advances in Nikkei 225 (+2.2%) were exacerbated by favourable currency moves and the KOSPI (U/C) was subdued by domestic tech weakness amid a dispute with Japan related to wartime forced labour in which the latter is to restrict chip material exports to South Korea. Elsewhere, the Shanghai Comp. (+2.2%) was buoyed by the US-China trade truce and after comments from President Trump which raised hopes of a potential U-turn on Huawei. This underpinned tech and telecom stocks with mainland Chinese markets the regional outperformers despite the miss in Chinese Manufacturing PMI data and absence of Hong Kong participants for holiday. Finally, 10yr JGBs were lower as they mirrored the slump seen in T-notes and heavy losses across safe-havens, while the BoJ also recently announced its bond buying intentions last week in which it reduced the amounts of JGBs with 3yr-5yr and 10yr-25yr maturities.

Top Asian News

- Applied Materials Said to Buy Kokusai Electric From KKR