GOLD: $1405.10 UP $18.90 (COMEX TO COMEX CLOSING)

Silver: $15.20 UP 4 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1414.00

silver: $15.28

YOUR DATA…

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 79/97

EXCHANGE: COMEX

CONTRACT: JULY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,385.600000000 USD

INTENT DATE: 07/01/2019 DELIVERY DATE: 07/03/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 1

661 C JP MORGAN 29 78

661 H JP MORGAN 1

685 C RJ OBRIEN 1

690 C ABN AMRO 26 1

737 C ADVANTAGE 36 13

905 C ADM 6 2

____________________________________________________________________________________________

TOTAL: 97 97

MONTH TO DATE: 661

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 97 NOTICE(S) FOR 9,700 OZ (0.2674 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 661 NOTICES FOR 66,100 OZ (2.0559 TONNES)

SILVER

FOR JULY

237 NOTICE(S) FILED TODAY FOR 1,185,000 OZ/

total number of notices filed so far this month: 3372 for 16,860,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 9924 down 801

Bitcoin: FINAL EVENING TRADE: $ 9768 UP 203

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE A TINY SIZED 164 CONTRACTS FROM 218,355 UP TO 218,519 DESPITE THE 16 CENT LOSS IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JULY. 0 FOR AUGUST, 961 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 961 CONTRACTS. WITH THE TRANSFER OF 961 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 961 EFP CONTRACTS TRANSLATES INTO 4.80 MILLION OZ ACCOMPANYING:

1.THE 16 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

20.430 MILLION OZ INITIAL STANDING FOR JULY

WE HAD CONSIDERABLE SHORT COVERING AT THE SILVER COMEX LAST NIGHT..AND ZERO SPREADING ACCUMULATION.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

2777 CONTRACTS (FOR 2 TRADING DAYS TOTAL 2777 CONTRACTS) OR 13.88 MILLION OZ: (AVERAGE PER DAY: 1388 CONTRACTS OR 6.94 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 13.88 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 1.98% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1171.38 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

RESULT: WE HAD A TINY SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 164, DESPITE THE 16 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE OF 961 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A FAIR SIZED: 1125 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 961 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 161 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 16 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.16 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.095 BILLION OZ TO BE EXACT or 156% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 237 NOTICE(S) FOR 1,185,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 20.43 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

WITH RESPECT TO SPREADING: WE WILL WITNESS THE MORPHING OF OUR SPREADERS OUT OF SILVER AND INTO GOLD AS THE JULY MONTH PROCEEDS INTO THE ACTIVE DELIVERY MONTH OF AUGUST.

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF AUGUST.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JULY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE OPEN INTEREST ROSE BY AN VERY STRONG 10,309 CONTRACTS, TO 591,164 DESPITE THE HUGE $24.70 PRICING LOSS WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING LIQUIDATION HAS NOW COMMENCED FOR GOLD….

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3485 CONTRACTS:

FOR AUGUST 2019: 7944 CONTRACTS, FOR OCT: 0 DEC> 0 CONTRACTS AND FEB 2020: 0 AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 591,164. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A HUMONGOUS AND CRIMINAL SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 18,253 CONTRACTS: 10,309 CONTRACTS INCREASED AT THE COMEX AND 7944 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 18,253 CONTRACTS OR 1,825,300 OZ OR 56.77. YESTERDAY WE HAD A HUGE LOSS OF $24.70 IN GOLD TRADING.…AND WITH THAT HUGE LOSS IN PRICE, WE HAD A HUGE GAIN IN GOLD TONNAGE OF 56.77 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER.THE NUMBERS ARE SURREAL!!

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY : 13,379 CONTRACTS OR 1,337,900 oz OR 41.61 TONNES (2 TRADING DAYS AND THUS AVERAGING: 6689 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAYS IN TONNES: 41.61 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 41.61/3550 x 100% TONNES =1.17% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2,961.74 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUGE SIZED INCREASE IN OI AT THE COMEX OF 10,309 DESPITE THE HUGE LOSS THAT GOLD UNDERTOOK YESTERDAY($24.70)) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7944 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7944 EFP CONTRACTS ISSUED, WE HAD A HUMONGOUS GAIN OF 18,253 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7944 CONTRACTS MOVE TO LONDON AND 10,309 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 56.77 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED DESPITE THE HUGE LOSS IN PRICE OF $24.70 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE COMMENCED WITH SPREADING ACCUMULATION IN GOLD STARTING TODAY/

we had: 97 notice(s) filed upon for 9700 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $18.90 TODAY//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 6,16 TONNES

INVENTORY RESTS AT 800.20 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 4 CENTS TODAY:

ANOTHER HUGE CHANGE WITH RESPECT TO SILVER INVENTORY AT THE SILVER SLV:

A DEPOSIT OF 2.821 MILLION OZ OF SILVER INTO THE SLV

/INVENTORY RESTS AT 326.151 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A TINY SIZED 164 CONTRACTS from 218,355 UP TO 218,519 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JULY: 0 CONTRACTS FOR AUGUST: 0, FOR SEPT. 961 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 961 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 2718 CONTRACTS TO THE 961 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A FAIR SIZED GAIN OF 1125 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 5.625 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 20.43 MILLION OZ STANDING SO FAR.

RESULT: A TINY SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 16 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A GOOD SIZED 961 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 0.96 POINTS OR 0.03% //Hang Sang CLOSED UP 332.94 POINTS OR 1.17% /The Nikkei closed UP 24.30 POINTS OR 0.11%//Australia’s all ordinaires CLOSED UP .14%

/Chinese yuan (ONSHORE) closed DOWN at 6.8763 /Oil UP TO 58.97 dollars per barrel for WTI and 64.92 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8763 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8793 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

NORTH KOREA/USA

A very good commentary by Tom Luongo as he analyzes Trump’s move on Kim. You do not want to miss this

( Tom Luongo)

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/USA

USA semi conductor Industry chipmakers lobbied Trump on the Huawei affair and suggested to him that long term they would be hurt as they would be blocked entry into the big Chinese market. Trump relented.

(courtesy zerohedge)

4/EUROPEAN AFFAIRS

i)Europe

Just as China and the uSA entered into a ceasefire on their trade war, the USA has just entered into a new one with Europe. Very upset with subsidies on airplane production in Europe, the USA were very upset and they are now ready to engage with their tariffs. This does not include the introduction of Europe’s own SWIFT system (INSTEX) which is already embroiling Trump

( zerohedge)

ii)A very important commentary from Mish Shedlock on Trumps threats to begin tariffs on European goods. As explained above the EU lost on the WTO hearing on illegal subsidies to Airbus and that allows new tariffs to be initiated. Trump wants to sell agriculture to the EU but it is difficult to get all 27 nations on board.

This is going to be quite a show..

( Mish Shedlock)

iii)EUROPE/ISIS FIGHTERS

Europe has no idea where returning ISIS fighters are located.

(courtesy Kern/Gatestone)

iv)ECB

It looks like the ECB will cut rates at the following meeting and not the meeting in July. The problem of course is that rates are already negative in Europe and this is going to send them further into NIRP

( zerohedge)

v)ECB

The ECB is staying quite clear away from German hawk Weidmann: they have selected uber dove Christine Lagarde to head the ECB. what a joke!!

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Iran/USA

A good look at what Trump will do next when dealing with Iran

(courtesy Tom Luongo)

6. GLOBAL ISSUES

MEXICO, GUADALAJARA

Global warming?

(zerohedge)

ii)Michael Every lays out comparisons of today and the 1930’s. He covers England, France, Iran and China/Hong Kong

7. OIL ISSUES

i)Take a look at the world’s largest solar farm

( Irina Slav/OilPrice.com)

ii)The economy is in a severe downturn and there is a glut of oil out there. OPEC fails to get a bigger production cut and thus down goes oil

( zerohedge)

8 EMERGING MARKET ISSUES

i)ZIMBABWE/

Zimbabwe stops issuing passports because they cannot pay the printer that makes them. The country is basically short of everything

( zerohedge)

9. PHYSICAL MARKETS

(Hugo Salinas Price)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

II)MARKET TRADING/USA

ii)Market data/USA

iii)USA ECONOMIC/GENERAL STORIES

This is totally nuts…Nike;s endorser Kaepernick complains to Nike that its new shows showing the original Betsy Ross flag with 13 colonies is offensive to him because it symbolizes slavery????. China is upset at Nike because the Japanese designer supports the Hong Kong protests.

The world is going totally bonkers

(courtesy zerohedge)

SWAMP STORIES

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; nil oz

FOR THE JULY 2019 CONTRACT MONTH)Today, 0 notice(s) were issued from JPMorgan dealer account and 29 notices were issued from their client or customer account. The total of all issuance by all participants equates to 97 contract(s) of which 78 notices were stopped (received) by j.P. Morgan dealer and 1 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account and 0 notices by the squid (Goldman Sachs)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JULY /2019. contract month, we take the total number of notices filed so far for the month (661) x 100 oz , to which we add the difference between the open interest for the front month of JULY. (155 contract) minus the number of notices served upon today (97 x 100 oz per contract) equals 71,900 OZ OR 2.236 TONNES) the number of ounces standing in this NON active month of JULY

Thus the INITIAL standings for gold for the JULY/2019 contract month:

No of notices served (661 x 100 oz) + (155)OI for the front month minus the number of notices served upon today (97 x 100 oz )which equals 71,900 oz standing OR 2.236 TONNES in this active delivery month of JUNE.

We GAINED 124 contracts or an additional 12,400 oz will stand as these guys refused to morph into London based forwards as well as negating a fiat bonus. Somebody was in need of physical gold badly on this side of the pond…VERY UNUSUAL TO SEE QUEUE JUMPING THIS EARLY IN THE UP FRONT JULY NON ACTIVE CONTRACT MONTH.

SURPRISINGLY LITTLE TO NO GOLD HAS BEEN ENTERING THE COMEX VAULTS AND WE HAVE WITNESSED THIS FOR THE PAST YEAR!! WE HAVE ONLY 10.047 TONNES OF REGISTERED ( GOLD OFFERED FOR SALE) VS 2.236 TONNES OF GOLD STANDING// THEY SEEM TO BE USING CONSIDERABLE GOLD VAPOUR TO SETTLE UPON UNSUSPECTING LONGS.

i) Into CNT: 596,982.800 oz

total dealer silver: 92.920 million

total dealer + customer silver: 305.978 million oz

The total number of notices filed today for the JULY 2019. contract month is represented by 237 contract(s) FOR 1,185,000 oz

To calculate the number of silver ounces that will stand for delivery in JULY, we take the total number of notices filed for the month so far at 3372 x 5,000 oz = 16,860,000 oz to which we add the difference between the open interest for the front month of JULY. (950) and the number of notices served upon today (237 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JULY/2019 contract month: 3372(notices served so far)x 5000 oz + OI for front month of JULY( 950) number of notices served upon today (237)x 5000 oz equals 20,415,000 oz of silver standing for the JULY contract month.

WE GAINED 55 CONTRACTS OR AN ADDITIONAL 275,000 OZ WILL STAND AT THE COMEX AS THESE GUYS REFUSED TO MORPH INTO A LONDON BASED FORWARDS AND AS WELL THEY ALSO NEGATED A FIAT BONUS. IT SEEMS THAT SOMEBODY WAS BADLY IN NEED OF PHYSICAL SILVER ON THIS SIDE OF THE POND JOINING GOLD!.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 71,291 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 73,683 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 73,683 CONTRACTS EQUATES to 386 million OZ 55.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -0.34% July 2/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.10% to NAV (July 2/2019 )

Note: Sprott silver trust back into NEGATIVE territory at -0.34%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 13.77 TRADING 13.23/DISCOUNT 3.96

END

And now the Gold inventory at the GLD/

JULY 2. WITH GOLD UP $18.90 A HUGE “PAPER” DEPOSIT OF 6.16 TONNES INTO THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 1: WITH GOLD DOWN $24.70 A HUGE “PAPER GOLD” WITHDRAWAL OF 1.76 TONNES FROM THE GLD/INVENTORY RESTS TONIGHT AT 794.04 TONNES

JUNE 28/WITH GOLD UP $.90 TODAY: ANOTHER 2.05 TONNES OF PAPER GOLD REMOVED AND THIS GOLD WAS USED IN ATTACKING GOLD AT THE COMEX/INVENTORY RESTS AT 795.80 TONNES

JUNE 27/WITH GOLD DOWN $6.10: ANOTHER HUGE WITHDRAWAL OF 1.76 PAPER TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 797.61 TONNES

JUNE 26/WITH GOLD DOWN $3.00: WE HAD A HUGE WITHDRAWAL OF 2.37 TONNES FROM THE GLD/INVENTORY RESTS AT 799.61 TONNES

JUNE 25/WITH GOLD UP $1.30 (AND WAY UP BEFORE THE BANKERS WHACKED) WE WITNESSED ANOTHER 1.95 TONNES OF PAPER GOLD ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 801.98 TONNES

JUNE 24/WITH GOLD UP $18.00 A MONSTROUS PAPER DEPOSIT OF 34.93 TONNES/INVENTORY RESTS AT 799.03 TONNES

JUNE 21/WITH GOLD UP $ 2.90, NO CHANGE IN GOLD INVENTORY: INVENTORY RESTS AT: 764.10 TONNES

June 20/WITH GOLD UP $47.95, NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 19 WITH GOLD DOWN $1.65: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONES

JUNE 18/JUNE 18/WITH GOLD UP $7.60: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 17/WITH GOLD DOWN $1.65 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 764.10 TONNES

JUNE 14/ WITH GOLD UP $1.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.40 TONNES OF PAPER GOLD INTO THE GLD///INVENTORY RESTS AT 764.10 TONNES

june 13/WITH GOLD UP $6.60 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 759.70 TONNES

JUNE 12/WITH GOLD UP $7.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 756.18 TONNES

JUNE 11/WITH GOLD UP $1.65 CENTS TODAY: A TINY CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .24 TONNES AND THIS IS TO PAY FOR FEES/INVENTORY RESTS AT 756.18 TONNES

JUNE 10/WITH GOLD DOWN $16.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES/INVENTORY RESTS AT 756.42 TONNES

JUNE 7/WITH GOLD UP $3.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 6/WITH GOLD UP $8.40 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 5 WITH GOLD UP $6.00 TODAY/STRANGE: A WITHDRAWAL OF 2.06 TONNES FROM THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 4/WITH GOLD UP 0.85 TODAY: A MONSTROUS PAPER GAIN OF 16.44 TONNES/GLD INVENTORY RESTS AT 759.65 TONNES

JUNE 3/WITH GOLD UP $17.50 TODAY: ANOTHER BIG CHANGE, A DEPOSIT OF 2.35 TONNES OF GOLD INTO THE GLD//

MAY 31/WITH GOLD UP $17.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GLD INVENTORY RESTS AT 740.86 TONNES

MAY 30: WITH GOLD UP $6.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES/INVENTORY RESTS AT 740.86 TONNES

MAY 29/WITH GOLD UP $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 737.34 TONNES

MAY 28/WITH GOLD DOWN $6.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD> A WITHDRAWAL OF 1.47 TONNES/INVENTORY RESTS AT 737.34 TONNES

MAY 24/WITH GOLD DOWN $1.60 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 738.81 TONNES

MAY 23/WITH GOLD UP $11.10 TODAY: A STRANGE WITHDRAWAL OF .88 TONNES FORM THE GLD/INVENTORY RESTS AT 738,81 TONNES

MAY 22//WITH GOLD FLAT TODAY: WE HAD A GOOD 1.52 TONNES OF GOLD DEPOSIT INTO THE GLD/INVENTORY RESTS TONIGHT AT 739.69 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JULY 2/2019/ Inventory rests tonight at 800.20 tonnes

*IN LAST 617 TRADING DAYS: 134.56 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 517 TRADING DAYS: A NET 31.12 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JULY 2/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 323.330 MILLION OZ//

JULY 1/ WITH SILVER DOWN 16 CENTS: A SURPRISING DEPOSIT OF 936,000 OZ INTO THE SLV/INVENTORY RESTS TONIGHT AT 323.330 MILLION OZ/

JUNE 28/WITH SILVER UP 6 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.394 MILLION OZ//

JUNE 27/WITH SILVER DOWN 7 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.575 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.394 MILLION OZ//

JUNE 26/WITH SILVER UP 17 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 25/WITH SILVER DOWN 25 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ.

JUNE 24/WITH SILVER UP 11 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 21/WITH SILVER DOWN 22 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 20/WITH SILVER UP 53 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 19/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ/

JUNE 18 WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ

JUNE 17/WITH SILVER UP XXX CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ//

JUNE 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 12/WITH SILVER UP 4 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.413 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 11/WITH SILVER UP 10 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 10/WITH SILVER DOWN 38 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 7/WITH SILVER UP ANOTHER 12 CENTS, NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 6/WITH SILVER UP ANOTHER 9 CENTS TODAY: A FAIR SIZE DEPOSIT OF 630,087 OZ//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 5/WITH SILVER UP 4 CENTS TODAY: A HUGE PAPER DEPOSIT OF 2.396 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 314.434 MILLION OZ//

JUNE 4/WITH SILVER UP 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

JUNE 3/WITH SILVER UP 19 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

MAY 31/WITH SILVER UP 6 CENTS TODAY: A DEPOSIT OF 422,000 OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 312.038 MILLION OZ/

May 30/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ///

MAY 29/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 28/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 24/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ/

MAY 23/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 22/WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 311.616 MILLION OZ

MAY 21: WITH SILVER DOWN 3 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV; A WITHDRAWAL OF 750,000 OZ///INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 20/WITH SILVER UP 6 CENTS:NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.366 MILLION OZ

If Gold

ii) Physical stories courtesy of GATA/Chris Powell

A good commentary from our good friend Hugo Salinas Price on how the monetary metal prices are suppressed by the bankers because it is true money and the bankers are supporting false money

(Hugo Salinas Price)

Hugo Salinas Price: Monetary metals prices are suppressed by the international banking cabal

Submitted by cpowell on Tue, 2019-07-02 03:39. Section: Daily Dispatches

By Hugo Salinas Price

Plata.com.mx

Monday, July 1, 2019

The prices of the precious metals — gold and silver — are under strict control by the syndicate of the international bankers. (Incidentally, I speak of the real power exercised by the International Bankers in a rather long article on my website, www.plata.com.mx. I do hope you will read it. Mr. Trump is finding out from Jay Powell of the Federal Reserve that the real power in this world is in the hands of the international bankers.)

The time when it was necessary to prove the existence of this control was over long ago. Today it is an unquestioned fact. However, most analysts of the precious metals market continue to bury their heads in the sand of falsity, for various personal reasons. Thus, they comment only on “market behavior.”

…

Why do international bankers wish to control the prices of the precious metals?

Because their power is based on the false money they issue, and true market prices of the precious metals would clearly reveal the steady loss of purchasing power of the false money they issue and thus erode their power significantly, or even destroy it. …

… For the remainder of the commentary:

END

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.8763/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.8793 /shanghai bourse CLOSED UP 0.96 POINTS OR 0.03%

HANG SANG CLOSED UP 332.94 POINTS OR 1.13%

2. Nikkei closed UP 24.30 POINTS OR 0.11%

3. Europe stocks OPENED ALL GREEN

USA dollar index UP TO 96.75/Euro RISES TO 1.1299

3b Japan 10 year bond yield: FALLS TO. –.15/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.26/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 58.97 and Brent: 64.92

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.36%/Italian 10 yr bond yield DOWN to 1.90% /SPAIN 10 YR BOND YIELD DOWN TO 0.32%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.26: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.19

3k Gold at $1392.50 silver at: 15.16 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 40/100 in roubles/dollar) 63.28

3m oil into the 58 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.28 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9888 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1168 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISING to –0.36%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.01% early this morning. Thirty year rate at 2.54%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.6618..

Trade Truce Euphoria Fizzles As Markets Hit A Wall, Futures Slide

This may be the shortest post-G-20 “trade truce rally” yet, because one day after global markets jumped, with the S&P hitting record highs even though nothing material was announced in the aftermath of US-China trade talks, the rally fizzled and global stocks eked out only meager gains, while US equity futures dropped in the red, following a fresh escalation in the US trade conflict with the EU, and amid renewed worries the global economy was faltering after data showed manufacturing activity slowed last month, snuffing appetite for risk.

The MSCI All Country World Index was barely higher in early trading, up for a fourth straight day, although should the US open in the red, the rally will likely end. On Monday, stocks rallied enthusiastically after the US postponed imposing another round of tariffs on Chinese products and the two countries agreed to continue negotiations on trade.

But just one day later, skepticism of further gains emerged after discouraging manufacturing surveys in the past 24 hours and a threat of additional US tariffs on European goods. “It’s clear that the tariffs already in place will continue to take a toll on global and domestic growth and with Trump now turning his attention on Europe, the early bullish bias seems to ease again,” said Konstantinos Anthis, head of research at ADSS.

As reported last night, the U.S. Trade Rep’s office released a list of additional products –including olives, Italian cheese and Scotch whiskey – that could be subject to tariffs, on top of products worth $21 billion that were announced in April. The new U.S. tariff threats against Europe also point to a worrisome prospect of a broadening trade dispute, said Michael McCarthy, chief markets strategist at CMC Markets in Sydney, in a note to clients.

“The problem is the widening of the dispute. Europe, the U.S. and China account for almost two thirds of global GDP,” he said. “An ongoing disruption to trade between these three major economies, prosecuted for domestic political purposes, could sink global growth.”

Despite being the subject of Lightlizer’s latest wrath, the European Stoxx 600 index managed a modest 0.2% advance, although Airbus dropped 1% as the United States stepped up pressure in the long-running dispute over aircraft subsidies. The euro climbed after Bloomberg reported ECB policy makers don’t see a need to rush into a July rate cut.

European bonds advanced alongside U.S. notes, and the yield on two-year Italian debt dropped below zero for the first time since the coalition government was formed in May 2018.

Earlier in the session Asian shares gained for a second day led by communications and utilities, as Washington and Beijing prepare for a new round of trade negotiations, with the MSCI index of Asia-Pacific shares ex-Japan adding 0.28%, helped by a 1.23% gain in Hong Kong shares as investors caught up to Monday’s global rally. Markets in Hong Kong had been closed on for a holiday. Most markets in the region edged higher after Trump said new trade talks with China is underway, ending a stalemate between the two countries amid escalating tariffs. The Topix gauge rose 0.3% for its best two-day advance since February, with technology firms among the biggest boosts; Japan’s Nikkei finished up 0.11%. The Shanghai Composite Index fluctuated and closed flat, as China Shipbuilding Industry jumped on restructuring talks, countering declines in Kweichow Moutai. The S&P/ASX 200 index pared earlier gains to close 0.1% higher after Australia executed its first back-to-back rate cuts in seven years. The S&P BSE Sensex Index edged up 0.1%, driven by Housing Development Finance and Infosys

Australian shares were flat, pulling back from earlier gains after the Reserve Bank of Australia cut its benchmark interest rate by 25 basis points to a record low 1.0%, as expected, which curiously sent the AUD sharply higher. However, the RBA left limited room for more cuts, raising the possibility of unconventional policy easing.

In FX, the dollar fell against most G-10 peers, paring Monday’s rally, which was the best in more than two months. The Australian dollar led gains, climbing after the central bank cut rates as expected – its first back-to-back rate cuts in seven years – and said further policy adjustments depended on growth and inflation data. The euro rose above $1.13 after ECB policy makers were said to be not ready to rush into additional monetary stimulus at this month’s meeting. The safe-haven yen strengthened against the dollar, which fell 0.2% to 108.24 yen per dollar, and the euro was flat at $1.1288. Most Asian currencies dropped, with the won leading declines.

In debt markets, Italian government bonds rallied after Italy cut its 2019 budget deficit target to avoid European Union disciplinary action, potentially easing another major concern for markets.

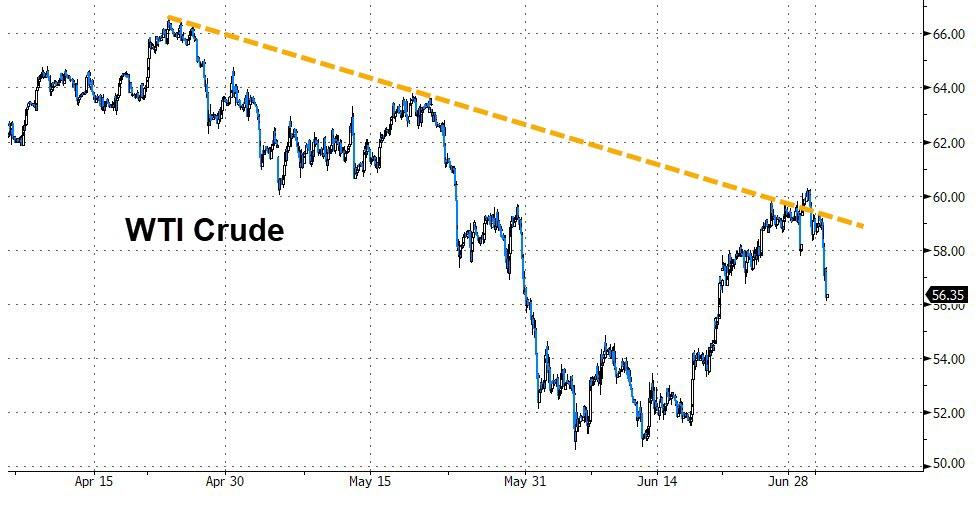

In commodity markets, oil gained as OPEC agreed to extend supply cuts until next March, although prices were pressured by worries demand may ease amid hints of a slowdown in the global economy. Treasuries climbed amid mixed trading in global stocks.

In commodities, oil fluctuated as investors weighed OPEC’s extension of output cuts into 2020. Spot gold added over half a percent to $1,392.11 per ounce. Bitcoin crashed, tumbling below $10,000 after rising to $13,000 less than a week ago.

No major economic data is expected today. Acuity Brands and Simply Good Foods are reporting earnings, while Ford, Tesla, and other carmakers release their U.S. monthly sales.

Market Snapshot

- S&P 500 futures down 0.1% to 2,963.50

- STOXX Europe 600 up 0.09% to 388.22

- MXAP up 0.3% to 162.04

- MXAPJ up 0.3% to 532.45

- Nikkei up 0.1% to 21,754.27

- Topix up 0.3% to 1,589.84

- Hang Seng Index up 1.2% to 28,875.56

- Shanghai Composite down 0.03% to 3,043.94

- Sensex up 0.2% to 39,778.57

- Australia S&P/ASX 200 up 0.08% to 6,653.21

- Kospi down 0.4% to 2,122.02

- German 10Y yield fell 0.3 bps to -0.36%

- Euro up 0.04% to $1.1291

- Italian 10Y yield fell 13.3 bps to 1.607%

- Spanish 10Y yield fell 1.9 bps to 0.317%

- Brent futures down 0.3% to $64.88/bbl

- Gold spot up 0.6% to $1,393.11

- U.S. Dollar Index down 0.1% to 96.79

Top Overnight News from Bloomberg

- While ECB Governing Council members agree that they could act on July 25 if the outlook deteriorates, they are said to be currently leaning toward the following meeting when they’ll have updated economic forecasts to back up their decision. The council might tweak its policy language this month to signal more stimulus is imminent

- The U.S. added more European Union products to a list of goods it could hit with retaliatory tariffs in a long-running trans-Atlantic subsidy dispute between Boeing Co. and Airbus SE. The Trade Representative’s office in Washington on Monday published a list of $4 billion worth of EU goods to target

- China will scrap ownership limit for securities, futures and life insurance companies by 2020, one year ahead of the original plan of 2021, Premier Li Keqiang says at the World Economic Forum in Dalian. China will keep yuan at a reasonable and equilibrium level and won’t resort to competitive depreciation

- Jeremy Hunt said he would “100% not” suspend Parliament to force through a no-deal Brexit, drawing a dividing line with Boris Johnson as the two men entered the last days of campaigning before Tory activists start voting for the U.K.’s next prime minister.

- OPEC will extend production cuts into 2020, attempting to buoy oil prices as the world’s leading exporters fret about the outlook for global demand growth and the relentless rise in output from America’s shale fields. Oil edged lower as investors weighed troubling economic data from around the world against OPEC’s extension of output cuts into 2020.

- Iran said it had exceeded limits set on its enriched-uranium stockpile, a move that risks the collapse of the 2015 nuclear accord and raises concerns that a standoff with the U.S. could lead to military action

- Italy’s populist government lowered its 2019 budget deficit goal to 2% in a bid to comply with European Union rules and avoid sanctions for failing to rein in debt. Market relief drove Italian bonds higher

- Australia’s central bank governor signaled he’ll stand pat in coming months to observe the impact of back-to-back interest rate cuts, while standing ready to resume easing should the outlook at home or abroad take a turn for the worse

- London bankers are bracing for thousands of job cuts. Nomura Holdings Inc., Japan’s biggest brokerage, let go of 30 people in April. HSBC Holdings Plc and Deutsche Bank AG are cutting jobs. In an atmosphere that may be the gloomiest since the financial crisis, some are jumping before they’re pushed

Asian equity markets traded indecisive as the euphoria from the US-China trade truce began to wane and with the region looking ahead to this week’s key risk events. ASX 200 (U/C) was underpinned by strength in mining names and amid a widely anticipated back-to-back rate cut from the RBA, while Nikkei 225 (+0.1%) was choppy and largely reflected the price action in the domestic currency. Elsewhere, Hang Seng (+1.2%) and Shanghai Comp. (U/C) were mixed with the mainland dampened after another liquidity drain by the PBoC, while Hong Kong outperformed as it played catch up on return from the extended weekend and amid declines in money market rates, with casino stocks among the biggest gainers following the strong growth in Macau gaming revenue. Finally, 10yr JGBs were subdued by the indecisive risk tone and after mixed results at the 10yr JGB auction failed to spur prices.

Top Asia News

- Credit Suisse Hires UBS Veteran as Asia Head of Equity Research

Major European indices are mixed and overall largely unchanged [Euro Stoxx 50 U/C] as sentiment deteriorated overnight with the notable development being that the US Trade Representative Office has proposed increasing tariffs on EU products as a result of the aircraft subsidies; with a proposed USD 4.0bln of additional tariffs being added. The tariffs would be on-top of the USD 21bln worth of tariffs announced by the USTR in April, with the products in question encompassing a vast range including whisky, iron tubes and cheese; a public hearing on these additions is scheduled for August 5th. Airbus (-0.9%) are afflicted on these additions as they are at the center of the European aircraft subsidies. Similarly, sectors are mixed with utilities and consumer staples outperforming on the day. In terms of this mornings notable movers, Adidas (-0.4%) opened lower after a downgrade at HSBC. Separately, but still within the Dax (-0.2%), Deutsche Bank (-0.7%) have slipped into negative territory as the broader index deteriorates on the back of negative comments from the VDMA this morning; however, the Co. did open around 1.1% higher on reports that they are considering lowering their capital buffer in order to fund the Co’s overhaul. Finally, Casino (+2.0%) are higher after selling 8 stores.

Top European News

- Italy Cuts 2019 Deficit Goal to 2% in Bid to Avoid EU Procedure

- Salvini Seizes Economic Reins to Take on EU in Budget Battle

- U.K. Construction Posts Worst Month Since 2009 on Brexit Worries

- Polish Banks Warn of $16 Billion Risk From EU Ruling, Puls Says

In FX, the Aussie has staged another strong rebound from fleeting overnight lows as bears quickly seized the opportunity to book profits in wake of the RBA’s decision to cut the OCR by another 25 bp, and other short positions were covered/squeezed on the accompanying statement suggesting no rush to ease again at the next policy meeting. Subsequently, comments from Governor Lowe appear to affirm a wait-and-see stance given back-to-back moves and Aud/Usd is inching closer to 0.7000 from 0.6958 lows, while Aud/Nzd has rebounded from sub-1.0450 towards 1.0500, with the Kiwi independently hampered by a further deterioration in NZIER business sentiment and ASB’s call for 2 more RNBZ rate reductions. Consequently, Nzd/Usd is hovering closer to the bottom of a 0.6657-80 range and eyeing the latest GDT auction next.

- GBP/EUR – The Pound has tumbled to the base of the G10 pile on the back of June’s UK construction PMI that confounded expectations for a modest recovery and slumped even deeper into contraction at 43.1, much worse than the manufacturing miss on Monday. Moreover, components like housing and new orders were bleak, as the former fell below zero for the first time in 17 months and the latter weakened the most in over a decade. Cable is clinging to 1.2600 and Eur/Gbp is edging up towards 0.8960 as the single currency rebounds further from daily chart support vs the Dollar ahead of a Fib (circa 1.1277 and 1.1259 respectively) on ECB sourced reports downplaying July rate cut speculation. However, Eur/Usd faded around 1.1320 and could be drawn back towards decent option expiry interest between 1.1295-1.1300 (1 bn), especially after considerably weaker than forecast German retail sales data and some bleak numbers/outlooks from the likes of the DIHK and VDMA.

- JPY – The Yen retains a relatively firm underlying bid on safe-haven grounds as the initial post-G20 euphoria dissipates and attention shifts back to the global slowdown and geopolitical factors, like the ongoing US-Iran spat. Hence, Usd/Jpy remains capped around 108.50 and the 30 DMA (108.55), but also confined on the downside at 108.00 given a generally firm Greenback as the DXY has bounced further from recent lows and back over the 200 DMA (96.690) into a loftier 96.624-879 band.

- RBA lowered the Cash Rate by 25bps to a record low 1.00% as expected and stated that it cut rates to support employment growth, as well as provide greater confidence on inflation. RBA noted that the economy can sustain a lower rate of unemployment and that employment growth remains strong, while it added that the outlook for the global economy remains reasonable and that there are signs house prices are stabilizing in Sydney and Melbourne. (Newswires)

In commodities, the oil complex is somewhat subdued as the G20-driven positive sentiment waned. Brent (-0.4%) and WTI (-0.4%) have failed to find much support this morning on OPEC agreeing to extend the oil output cut by 9-months; with the OPEC+ meeting commencing today and the press conference expected at around 12:00 BST. In terms of recent commentary sources indicate that Russian Energy Minister Novak has given his support to the extension, with the deal to be signed soon. Nonetheless, markets will remain on guard for any dissent at today’s meeting from the non-OPEC members, with the joint verdict on an extension not expected until the OPEC+ press conference. From a technical perspective for WTI, PVM highlight that USD 59.07/bbl and USD 58.57/bbl are the two ‘pivot points’ to keep an eye on. Looking ahead, aside from the OPEC+ meeting we have the API report which last week posted a headline draw of -7.55mln BPD. Gold (+0.5%) has reverted back towards the USD 1400/oz level after yesterday’s G20-induced decline; with today’s reversion stemming from a decidedly less-positive market sentiment than yesterday. However, the USD 1400/oz level remains elusive for the yellow metal this morning, for reference session high is currently just over USD 1397/oz. In contrast to yesterday’s gains, copper has remained largely negative throughout the session as risk sentiment turning negative is weighing on the red metal.

US Event Calendar

- Wards Total Vehicle Sales, est. 17m, prior 17.3m

- 6:35am: Fed’s Williams Speaks on Global Economic and Policy Outlook

- 11am: Fed’s Mester to Speak on Economy in London

DB’s Jim Reid concludes the overnight wrap

Before the weekend we sent birthday party invites out to Maisie’s new classmates for September when she starts full time nursery. Yesterday we got over 10 acceptances from parents we don’t know yet and it makes me very worried that this is going to start an endless cycle of party invites that I’m going to increasingly find it hard to plan my weekends around. So my question to parents out there with more experience is what’s the best I can get away with in terms of party/round of golf ratio? Is 1:10 a bit optimistic? Maybe I’ll request to home school the twins to avoid the next round of this in a year or so’s time. My wife has promised a children’s entertainer but without booking one yet. So all recommendations as to what will go down well with 4 year olds are very welcome!

It wasn’t a full on risk party yesterday as markets shifted between optimism over the weekend developments on the trade war and renewed macro concerns yesterday, but ultimately the S&P 500 still closed +0.76% at a fresh all-time high. That was below its opening level of +1.23%, but is nevertheless just 35pts from the psychologically significant 3,000 level. Sentiment did fade from the early highs possibly as the aftermath of the Trump/Xi talks was light on details after deeper inspection. Indeed, China has not actually confirmed any details and markets are a little confused as to what happens next. Also the offshore yuan, a very trade war-exposed asset, has actually reversed all of its rally from Sunday night.

The NASDAQ and DOW also traded down from their opening highs of +1.80% and +1.09% to end the day at +1.06% and +0.44%, respectively. Semiconductor stocks rallied +2.65%, boosted by the trade headlines and the apparent de-escalation against Huawei, while energy stocks lagged at +0.10% as oil prices declined after the OPEC meeting (more below). European bourses also peaked at their open but held onto decent gains by the close, with the STOXX 600 rising +0.78% and DAX +0.99%. The DAX is also up +20.61% from the December lows now which means it’s entered a bull market if that’s your definition of one!

Overnight one of the main stories has been the US Trade Representative’s office publishing a list of $4 bn worth of EU goods that the US could hit with duties as retaliation for European aircraft subsides, particularly to Airbus. It adds to a list of EU products valued at $21 bn that the USTR published in April, according to the release. The USTR said a public hearing on the proposed additional $4 billion worth of products will be held on August 5th and added that, “the final list will take into account the report of the WTO Arbitrator on the appropriate level of countermeasures to be authorized by the WTO.” As a reminder, the WTO has found that the EU subsidies violate international trade rules and it’s expected to decide this summer on the amount of countermeasures the US can impose. Staying with trade, President Trump said that a new round of trade talks with China is already underway as negotiators are speaking on the phone.

This morning in Asia markets are trading mixed with the Nikkei (+0.09%) up while the Shanghai Comp (-0.06%) and Kospi (-0.27%) are down. The Hang Seng is up +1.35% as Hong Kong’s market reopened after a holiday to catch up with yesterday’s move in markets. Elsewhere, futures on the S&P 500 are up +0.12%.

In other news, China’s Premier Li Keqiang said in a speech at the WEF this morning that China will scrap ownership limits for securities firms, futures businesses and life insurance companies by 2020, one year ahead of the original target of 2021. The rule change would mean foreign entities could wholly own firms in those sectors. Li also said that China is working on deeper tax cuts for businesses and it should reach CNY 2tn while adding that China remains concerned about prohibitive financing costs for smaller and medium sized businesses and will work towards the need for more monetary and fiscal support for these companies.

Back to yesterday and credit also had a good day with HY spreads 7bps tighter in the US and -6bps tighter in Europe. EM performed well with the MSCI EM equity index climbing +1.19% and EM FX +0.15%. In bonds, the big move was BTPs which rallied -13.5bps and closed at 1.967% after catching a bid with the wider risk on move, though they were also helped by unconfirmed reports that the European Commission will not recommend an excessive deficit procedure against the country as was possible as early as today (per Bloomberg). Clemente De Lucia has a writeup on the current state of play available here . The rally pushed BTP yields below 2% for the first time since May last year and with Bunds ‘only’ -3.0bps lower (albeit to a new low of -0.357%) – the BTP-Bund spread is now at 232bps and the lowest since last September. The global stock of negative yielding debt is now at $12.83tn with yesterday’s moves in rates and remains close to recent all time high of $13.01tn.

Meanwhile Treasuries were quiet all things considered, with 10y yields rising +2.4bps and back above Italian yields. Two-year yields rose +3.2bps, as markets continued to price out the odds of a 50bps cut at the Fed’s meeting later this month. The current odds are now just 20%, from 44% last week. That caused the 2st10s curve to flatten -0.7bps. In commodities, oil prices slipped -2.40% after OPEC announced an extension of its production cuts through next March but failed to reach an agreement on deeper cuts. There were also unconfirmed reports of disagreements within the cartel as well, which caused the meeting’s press conference to be delayed and sent a negative signal about future cooperation.

Moving onto the data, the general risk on came despite what was a pretty weak set of PMIs across the globe yesterday. In fact, over Sunday and Monday we counted 35 different manufacturing PMIs of which 19 came in below 50 and a worrying 27 dropped month on month. The hope will be that a trade truce can stabilise things but there’s obviously concern that the damage has already been done and will need firmer resolution to reverse it.

Notwithstanding these numbers it was the ISM manufacturing in the US which was most anticipated and to be fair the reading was better than expected at 51.7 (vs. 51.0 consensus) even if it was down -0.4pts from May. Less positive was the new orders component which dropped -2.7pts to 50.0 – the lowest since December 2015 – although employment rather encouragingly rose 0.8pts to 54.5. A few moving parts but it’s hard to ignore the fact that this was still the lowest headline ISM manufacturing reading since October 2016.

Just coming back to the final manufacturing PMIs in Europe, the Eurozone reading was revised down -0.2pts to 47.6 from the flash print and was -0.1pts lower than May. Germany (45.0 vs. 45.4 flash) and to a lesser extent France (51.9 vs. 52.0 flash) also saw downward revisions while the biggest miss was reserved for Spain (47.9 vs. 49.5 expected) which fell -2.2pts from May and also hit the lowest level since April 2013. Italy (48.4 vs. 48.7 expected) also disappointed with output and new orders falling for the eleventh consecutive month too. That also marks the ninth successive sub-50 reading. Of the 13 EU countries that reported manufacturing PMIs yesterday, only 5 posted a reading of greater than 50 with Hungary (54.4) leading the way.

Indeed the weakness includes the UK where the manufacturing PMI slumped to 48.0 last month versus expectations for a 49.5 reading. That is also a drop of-1.4pts from May and the lowest reading since February 2013. The details showed that output fell and new orders remained in negative territory too. In fact most of the sub-indices were lower with the associated text noting that “the stranglehold of sustained Brexit-related uncertainty and disruption also weighed heavily on business confidence and employment, as optimism ebbed to one of its lowest levels in the survey history”. Our UK economists noted that current levels are now consistent with prior BoE easing so this will likely increase the scrutiny of the BoE maintaining a tightening bias in the communication. We should also note that consumer credit data for May also slipped yesterday to £0.8bn. Sterling fell -0.46% yesterday while 10y Gilts ended -1.9bps lower.

As for the remaining US data, the final June manufacturing PMI was revised up +0.5pts to 50.6 which actually means it was up 0.1pts from May. Finally construction spending in May was confirmed as falling -0.8% mom, though the April figure was revised up 0.4pp.

In other news, the ECB’s new chief economists Lane made fairly dovish comments during a speech in Helsinki. This was notable as the market is still fairly new to Lane. He said that “the effectiveness of the policy toolkit means that we can add further monetary accommodation if it is required to deliver our objective” and that “it is essential that a central bank shows consistency in its monetary policy decisions by proactively responding to shocks that might delay convergence to the target or move inflation dynamics in an adverse direction”.

Meanwhile, the ECB’s Knot, one of the more hawkish members on the Governing Council, said that it is “indisputable” that inflation is too low in the euro area. He went on to say that it’s “important to underline the Governing Council stands ready to act decisively” if necessary. This contrasts with his remarks from earlier this year, where he said that price appreciation in the Dutch housing market was “exuberant” and advocated for “doing something about this.”

To the day ahead now, where this morning we’ll get the May retail sales data in Germany, June construction PMI in the UK and May PPI reading for the Euro Area. In the US the only data due is the June vehicle sales numbers. Away from the data we’ve also got scheduled comments due from the Fed’s Williams at 11.35am BST and the Fed’s Mester at 4pm BST. The ECB’s Knot and BoE’s Carney are also due to speak today. The other event is the OPEC+ meeting in Vienna where a press conference is expected at the end, however with output cuts being extended it’s unlikely that we’ll get much new news.

3A/ASIAN AFFAIRS

I)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 0.96 POINTS OR 0.03% //Hang Sang CLOSED UP 332.94 POINTS OR 1.17% /The Nikkei closed UP 24.30 POINTS OR 0.11%//Australia’s all ordinaires CLOSED UP .14%

/Chinese yuan (ONSHORE) closed DOWN at 6.8763 /Oil UP TO 58.97 dollars per barrel for WTI and 64.92 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8763 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8793 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

NORTH KOREA/USA

A very good commentary by Tom Luongo as he analyzes Trump’s move on Kim. You do not want to miss this

(courtesy Tom Luongo)

Luongo: It’s Time For All This Insanity To Stop

Donald Trump did the unthinkable. He went to North Korea. He stepped over the line in the sand demarked by Washington protocol for nearly seventy years.

And that Washington establishment, predictably, hates him for it. It can be felt from all sides of the political rotunda. They hate that Trump realizes their position, one of maximum pressure, isn’t working.

They despise that Russia and China will benefit from ending this frozen conflict not to mention Koreans on both sides of the DMZ.

The cynic in me thinks they are angry that the American people will benefit as well.

So this weekend was a good one for peaceniks around the world. Trump and Chinese Premier Xi Jinping agreed to back down on the worst of his trade war demands.

Trump presumably had a good meeting with Russian President Vladimir Putin which likely set the stage for his meeting with Chairman Kim Jong-un. Remember Kim met with Putin earlier this year and designated him as his go-between with Trump after the talks in Hanoi fell apart.

The Bile Belt

This event should not be downplayed. Trump showed great humility and generosity towards Kim at the moment of truth. We should be cheering this regardless of what we think of him personally.

Diplomacy is not groveling. It is the acknowledgment of the other person’s basic humanity, a fundamental point lost in the political cesspit that is D.C.

Because of his previous mistakes and belligerence, only Trump could have made the walk across the DMZ to meet Kim on his territory. Only someone as blunt as Trump could cut through the nonsense that North Korea isn’t capable of independent action.

And only people so full of bile and despite would not be happy about this. Only people so enthralled with the thought of war and their own political and social ambitions would look at this event and seek to tear it down.

These are the people who lost yesterday in Trump’s historic and brilliant bit of diplomacy. And they are complaining bitterly about it today.

Everyone else wins.

In the land of the Twitterati, after stripping away the snark masquerading as analysis, we are left with a bunch of malcontents bemoaning their lost relevance.

I’m not praising him today to get back on anyone’s good side. I’ve been very straight about this. When Trump does good I praise him. When he screws up or acts dangerously I lambaste him.

And that is exactly how we should treat, at all times, all politicians everywhere. The telling point today is that the whole of the Washington establishment, Democrats and Neocons, are aghast at the prospect of peace.

The Wrong Path to Peace

I’ve been a harsh critic of most of Trump’s foreign policy moves since April 2017, when he bombed the airbase at Khan Sheikoun in Syria. It was the first inkling that he didn’t understand the rules of the game he was playing.

And those initial bombings would cost him far more in the end then he could ever gain. Not only did he lose most of his first term in office but he lost the trust of most world leaders pandering to establishment forces within the U.S. Deep State and donor class.

We can trace each move since then as a continuum leading up to Iran shooting down a U.S. Global Hawk drone and see we were always going to end up right where we are.

Because the alternative is a world at war. And think what you want about Trump, I’ve never been convinced that he was interested in that. If anything his problem has been allowing his fundamental humanity to be twisted into something ugly, limbicly lashing out at ‘bad guys’ like at Khan Shiekoun and not seeing the lies around it for what they were.

In the past few weeks we’ve seen a smarter, savvier Trump avoid the traps his allies and advisors set for him. He’s showed immense restraint.

And now, Trump is climbing down off the immense mountain of entitlement he and his advisors placed him on. By stepping over the line into North Korea and meeting with Kim for nearly an hour he’s beginning to deliver on the promises he made during the 2016 campaign.

Why wouldn’t I or anyone else be cheering?

When Iran shot down that drone I said on Sputnik Radio that to solve Iran’s nuclear weapons problem Trump should be looking to North Korea. Getting Kim to agree to freezing warhead production, and presumably dissemination, ends the possibility of Iran achieving that goal anytime soon.

After meeting with most of his ‘enemies’ at the G-20, Trump did just that. He pivoted away from Iran, now a source of political pitfalls, back to North Korea which was the right thing to do.

If Iran wanted a bomb they would have one. If Russia and China wanted Iran to have one, they would have one.

So all of this talk is simply theater. Just like the strategic importance of North Korea in 2019 is still relevant with China fully capable of projecting its interests on its own.

It’s time for this insanity to end. Full stop.

The Koreans want it. The Russians want it. The Chinese want it. Japan wants it.

And we should want it too.

Free at Last?

From the moment he began to engage Kim directly Trump’s strategy was to acknowledge the reality that North Korea can stand on its own. That it is not a puppet state of China.

It has been a constant theme of his while his advisory team tells him otherwise.

Well, they were in Mongolia on Sunday, while the best proxy for his antiwar base was on Air Force One.

Jonathan Cheng

✔@JChengWSJ

In the room: N. Korean Foreign Minister Ri Yong Ho (left) and Tucker Carlson.