GOLD: $1417.60 UP $12.50 (COMEX TO COMEX CLOSING)

Silver: $15.30 UP 10 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1417.90

silver: $15.31

YOUR DATA…

GOLD HAS A STELLAR DAY RISING $12,50 AND YET GLD DECLINES INVENTORY BY 1.76 TONNES//SILVER RISES BY 19 CENTS AND SLV INVENTORY RISES BY 2,37 MILLION OZ

UNTIL NEXT WEEK I WILL NOT PROVIDE INVENTORY LEVEL MOVEMENTS. SINCE NOTHING MOVES IN GOLD..YOU ARE NOT MISSING ANYTHING,

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 11\18

EXCHANGE: COMEX

CONTRACT: JULY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,404.600000000 USD

INTENT DATE: 07/02/2019 DELIVERY DATE: 07/05/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 11

737 C ADVANTAGE 15 7

905 C ADM 3

____________________________________________________________________________________________

TOTAL: 18 18

MONTH TO DATE: 679

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 18 NOTICE(S) FOR 1800 OZ (0.0559 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 679 NOTICES FOR 67900 OZ (2.112 TONNES)

SILVER

FOR JULY

21 NOTICE(S) FILED TODAY FOR 105,000 OZ/

total number of notices filed so far this month: 3393 for 16,965,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 11,398 UP 569

Bitcoin: FINAL EVENING TRADE: $ 11,373 UP 508

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE A CONSIDERABLE SIZED 2705 CONTRACTS FROM 218,519 UP TO 221,224 DESPITE THE TINY 4 CENT GAIN IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JULY. 0 FOR AUGUST, 731 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 731 CONTRACTS. WITH THE TRANSFER OF 731 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2731 EFP CONTRACTS TRANSLATES INTO 3.65 MILLION OZ ACCOMPANYING:

1.THE 4 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

20.415 MILLION OZ INITIAL STANDING FOR JULY

WE HAD CONSIDERABLE SHORT COVERING AT THE SILVER COMEX LAST NIGHT..AND ZERO SPREADING ACCUMULATION.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

3508 CONTRACTS (FOR 3 TRADING DAYS TOTAL 3508 CONTRACTS) OR 17,54 MILLION OZ: (AVERAGE PER DAY: 1169 CONTRACTS OR 5.84 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 17.54 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 2.50% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1175.03 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2705, DESPITE THE TINY 4 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 731 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 3036 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 731 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 2731 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 4 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.20 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.106 BILLION OZ TO BE EXACT or 158% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JULY MONTH/ THEY FILED AT THE COMEX: 21 NOTICE(S) FOR 105000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 20.415 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

WITH RESPECT TO SPREADING: WE WILL WITNESS THE MORPHING OF OUR SPREADERS OUT OF SILVER AND INTO GOLD AS THE JULY MONTH PROCEEDS INTO THE ACTIVE DELIVERY MONTH OF AUGUST.

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF AUGUST.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JULY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE OPEN INTEREST ROSE BY A HUMONGOUS 14,785 CONTRACTS, TO 605,949 ACCOMPANYING THE HUGE $18.90 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING LIQUIDATION WILL NOW COMMENCE FOR GOLD….

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6301 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 56301 CONTRACTS, DEC> 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 605,949 ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A HUMONGOUS SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 21,086 CONTRACTS: 14,785 CONTRACTS INCREASED AT THE COMEX AND 6301 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 21,086 CONTRACTS OR 2,108,600 OZ OR 65.58 TONNES. YESTERDAY WE HAD A HUGE GAIN OF $18.90 IN GOLD TRADING.…AND WITH THAT STRONG GAIN IN PRICE, WE HAD A HUGE GAIN IN GOLD TONNAGE OF 65.58 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY : 19,680 CONTRACTS OR 1,968,000 oz OR 61.21 TONNES (3 TRADING DAY AND THUS AVERAGING: 6560 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY IN TONNES: 61.21 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 61.21/3550 x 100% TONNES =2.179% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2,981.33 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUMONGOUS SIZED INCREASE IN OI AT THE COMEX OF 14,785 WITH THE HUGE PRICING GAIN THAT GOLD UNDERTOOK ON YESTERDAY($18.90)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6301 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6301 EFP CONTRACTS ISSUED, WE HAD A HUMONGOUS AND CRIMINALLY SIZED GAIN OF 21,086 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6301 CONTRACTS MOVE TO LONDON AND 14,785 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 65.58 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED ACCOMPANYING THE STRONG GAIN IN PRICE OF $18.90 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE WILL COMMENCE WITH SPREADING ACCUMULATION IN GOLD AS THE MONTH PROCEEDS/

we had: 18 notice(s) filed upon for 1800 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $12.50 TODAY//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 1.76 TONNES

INVENTORY RESTS AT 798.44 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 10 CENTS TODAY:

ANOTHER HUGE CHANGE WITH RESPECT TO SILVER INVENTORY AT THE SILVER SLV:

A DEPOSIT OF 2.341 MILLION OZ OF SILVER INTO THE SLV

/INVENTORY RESTS AT 328.482 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A CONSIDERABLE SIZED 2705 CONTRACTS from 218,519 UP TO 221,224 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JULY: 0 CONTRACTS FOR AUGUST: 0, FOR SEPT. 731 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 731 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 2025 CONTRACTS TO THE 731 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUGE GAIN OF 3036 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 15.18 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 20.415 MILLION OZ STANDING SO FAR.

RESULT: A CONSIDERABLE SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE TINY 4 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 731 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 14.86 POINTS OR 0.50% //Hang Sang CLOSED DOWN 76.72 POINTS OR 0.27% /The Nikkei closed DOWN 204.22 POINTS OR 0.25%//Australia’s all ordinaires CLOSED DOWN .50%

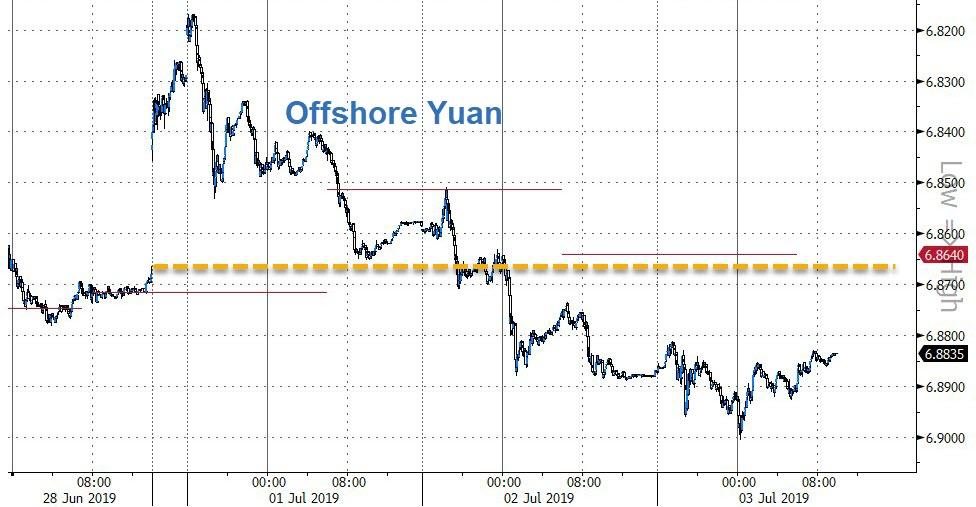

/Chinese yuan (ONSHORE) closed DOWN at 6.8694 /Oil UP TO 57.82 dollars per barrel for WTI and 65.36 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.8694 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8759 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/

4/EUROPEAN AFFAIRS

i)UK

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)IRAN/USA

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

II)MARKET TRADING/USA

ii)Market data/USA

iii)USA ECONOMIC/GENERAL STORIES

SWAMP STORIES

Let us head over to the comex:

we had XX dealer entry:

We had XX kilobar entries

total gold withdrawals; XXX oz

FOR THE JULY 2019 CONTRACT MONTH)Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 18 contract(s) of which 11 notices were stopped (received) by j.P. Morgan dealer and 10 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account and 0 notices by the squid (Goldman Sachs)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JULY /2019. contract month, we take the total number of notices filed so far for the month (679) x 100 oz , to which we add the difference between the open interest for the front month of JULY. (81 contract) minus the number of notices served upon today (18 x 100 oz per contract) equals 74,200 OZ OR 2.308 TONNES) the number of ounces standing in this NON active month of JULY

Thus the INITIAL standings for gold for the JULY/2019 contract month:

No of notices served (679 x 100 oz) + (81)OI for the front month minus the number of notices served upon today (18 x 100 oz )which equals 74,200 oz standing OR 2.308 TONNES in this active delivery month of JUNE.

We GAINED 23 contracts or an additional 2300 oz will stand as these guys refused to morph into London based forwards as well as negating a fiat bonus. Somebody was in need of physical gold badly on this side of the pond…VERY UNUSUAL TO SEE QUEUE JUMPING THIS EARLY IN THE UP FRONT JULY CONTRACT MONTH.

SURPRISINGLY LITTLE TO NO GOLD HAS BEEN ENTERING THE COMEX VAULTS AND WE HAVE WITNESSED THIS FOR THE PAST YEAR!! WE HAVE ONLY 10.047 TONNES OF REGISTERED ( GOLD OFFERED FOR SALE) VS 2.308 TONNES OF GOLD STANDING// THEY SEEM TO BE USING CONSIDERABLE GOLD VAPOUR TO SETTLE UPON UNSUSPECTING LONGS.

total dealer silver: 87.119 million

total dealer + customer silver: 304.604 million oz

The total number of notices filed today for the JULY 2019. contract month is represented by 21 contract(s) FOR 105,000 oz

To calculate the number of silver ounces that will stand for delivery in JULY, we take the total number of notices filed for the month so far at 3393 x 5,000 oz = 16,965,000 oz to which we add the difference between the open interest for the front month of JULY. (742) and the number of notices served upon today (21 x 5000 oz) equals the number of ounces standing.

.Thus the INITIAL standings for silver for the JULY/2019 contract month: 3393(notices served so far)x 5000 oz + OI for front month of JULY( 742) number of notices served upon today (21)x 5000 oz equals 20,570,000 oz of silver standing for the JULY contract month

WE GAINED 29 CONTRACTS OR AN ADDITIONAL 145,000 OZ WILL STAND AT THE COMEX AS THESE GUYS REFUSED TO MORPH INTO A LONDON BASED FORWARDS AND AS WELL THEY ALSO NEGATED A FIAT BONUS. IT SEEMS THAT SOMEBODY WAS BADLY IN NEED OF PHYSICAL SILVER ON THIS SIDE OF THE POND JOINING GOLD!.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 68,994 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 79,122 CONTRACTS..(we no doubt had considerable spreading activity as they are now starting to accumulate in silver)

YESTERDAY’S CONFIRMED VOLUME OF 79,122 CONTRACTS EQUATES to 395.0 million OZ 56.5%% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -0.34% June 27/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.10% to NAV (JUNE 27/2019 )

Note: Sprott silver trust back into NEGATIVE territory at -0.34%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 13.77 TRADING 13.23/DISCOUNT 3.96

END

And now the Gold inventory at the GLD/

JULY 3// WITH GOLD UP $12.60 TODAY A SURPRISE WITHDRAWAL OF 1.76 TONNES FROM THE GLD//INVENTORY RESTS AT 798.44

JULY 2. WITH GOLD UP $18.90 A HUGE “PAPER” DEPOSIT OF 6.16 TONNES INTO THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 1: WITH GOLD DOWN $24.70 A HUGE “PAPER GOLD” WITHDRAWAL OF 1.76 TONNES FROM THE GLD/INVENTORY RESTS TONIGHT AT 794.04 TONNES

JUNE 28/WITH GOLD UP $.90 TODAY: ANOTHER 2.05 TONNES OF PAPER GOLD REMOVED AND THIS GOLD WAS USED IN ATTACKING GOLD AT THE COMEX/INVENTORY RESTS AT 795.80 TONNES

JUNE 27/WITH GOLD DOWN $6.10: ANOTHER HUGE WITHDRAWAL OF 1.76 PAPER TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 797.61 TONNES

JUNE 26/WITH GOLD DOWN $3.00: WE HAD A HUGE WITHDRAWAL OF 2.37 TONNES FROM THE GLD/INVENTORY RESTS AT 799.61 TONNES

JUNE 25/WITH GOLD UP $1.30 (AND WAY UP BEFORE THE BANKERS WHACKED) WE WITNESSED ANOTHER 1.95 TONNES OF PAPER GOLD ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 801.98 TONNES

JUNE 24/WITH GOLD UP $18.00 A MONSTROUS PAPER DEPOSIT OF 34.93 TONNES/INVENTORY RESTS AT 799.03 TONNES

JUNE 21/WITH GOLD UP $ 2.90, NO CHANGE IN GOLD INVENTORY: INVENTORY RESTS AT: 764.10 TONNES

June 20/WITH GOLD UP $47.95, NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 19 WITH GOLD DOWN $1.65: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONES

JUNE 18/JUNE 18/WITH GOLD UP $7.60: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 17/WITH GOLD DOWN $1.65 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 764.10 TONNES

JUNE 14/ WITH GOLD UP $1.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.40 TONNES OF PAPER GOLD INTO THE GLD///INVENTORY RESTS AT 764.10 TONNES

june 13/WITH GOLD UP $6.60 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 759.70 TONNES

JUNE 12/WITH GOLD UP $7.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 756.18 TONNES

JUNE 11/WITH GOLD UP $1.65 CENTS TODAY: A TINY CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .24 TONNES AND THIS IS TO PAY FOR FEES/INVENTORY RESTS AT 756.18 TONNES

JUNE 10/WITH GOLD DOWN $16.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES/INVENTORY RESTS AT 756.42 TONNES

JULY 7/WITH GOLD UP $3.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 6/WITH GOLD UP $8.40 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 5 WITH GOLD UP $6.00 TODAY/STRANGE: A WITHDRAWAL OF 2.06 TONNES FROM THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 4/WITH GOLD UP 0.85 TODAY: A MONSTROUS PAPER GAIN OF 16.44 TONNES/GLD INVENTORY RESTS AT 759.65 TONNES

JUNE 3/WITH GOLD UP $17.50 TODAY: ANOTHER BIG CHANGE, A DEPOSIT OF 2.35 TONNES OF GOLD INTO THE GLD//

MAY 31/WITH GOLD UP $17.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GLD INVENTORY RESTS AT 740.86 TONNES

MAY 30: WITH GOLD UP $6.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES/INVENTORY RESTS AT 740.86 TONNES

MAY 29/WITH GOLD UP $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 737.34 TONNES

MAY 28/WITH GOLD DOWN $6.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD> A WITHDRAWAL OF 1.47 TONNES/INVENTORY RESTS AT 737.34 TONNES

MAY 24/WITH GOLD DOWN $1.60 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 738.81 TONNES

MAY 23/WITH GOLD UP $11.10 TODAY: A STRANGE WITHDRAWAL OF .88 TONNES FORM THE GLD/INVENTORY RESTS AT 738,81 TONNES

MAY 22//WITH GOLD FLAT TODAY: WE HAD A GOOD 1.52 TONNES OF GOLD DEPOSIT INTO THE GLD/INVENTORY RESTS TONIGHT AT 739.69 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JULY 3/2019/ Inventory rests tonight at 798.44 tonnes

*IN LAST 619 TRADING DAYS: 136.32 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 519TRADING DAYS: A NET 29.36 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JULY 2/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 323.330 MILLION OZ//

JULY 1/ WITH SILVER DOWN 16 CENTS: A SURPRISING DEPOSIT OF 936,000 OZ INTO THE SLV/INVENTORY RESTS TONIGHT AT 323.330 MILLION OZ/

JUNE 28/WITH SILVER UP 6 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.394 MILLION OZ//

JUNE 27/WITH SILVER DOWN 7 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.575 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.394 MILLION OZ//

JUNE 26/WITH SILVER UP 17 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 25/WITH SILVER DOWN 25 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ.

JUNE 24/WITH SILVER UP 11 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 21/WITH SILVER DOWN 22 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 20/WITH SILVER UP 53 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 19/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ/

JUNE 18 WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ

JUNE 17/WITH SILVER UP XXX CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ//

JUNE 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 12/WITH SILVER UP 4 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.413 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 11/WITH SILVER UP 10 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 10/WITH SILVER DOWN 38 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

JULY 7/WITH SILVER UP ANOTHER 12 CENTS, NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

JULY 6/WITH SILVER UP ANOTHER 9 CENTS TODAY: A FAIR SIZE DEPOSIT OF 630,087 OZ//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 5/WITH SILVER UP 4 CENTS TODAY: A HUGE PAPER DEPOSIT OF 2.396 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 314.434 MILLION OZ//

JUNE 4/WITH SILVER UP 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

JUNE 3/WITH SILVER UP 19 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

MAY 31/WITH SILVER UP 6 CENTS TODAY: A DEPOSIT OF 422,000 OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 312.038 MILLION OZ/

May 30/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ///

MAY 29/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 28/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 24/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ/

MAY 23/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 22/WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 311.616 MILLION OZ

MAY 21: WITH SILVER DOWN 3 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV; A WITHDRAWAL OF 750,000 OZ///INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 20/WITH SILVER UP 6 CENTS:NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.366 MILLION OZ

If Gold

ii) Physical stories courtesy of GATA/Chris Powell

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.8811/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.8833 /shanghai bourse CLOSED DOWN 28.68 POINTS OR 0.97%

HANG SANG CLOSED DOWN 20.42 POINTS OR 0.07%

2. Nikkei closed DOWN 116.11 POINTS OR 0.53%

3. Europe stocks OPENED ALL GREEN

USA dollar index UP TO 96.76/Euro FALLS TO 1.1278

3b Japan 10 year bond yield: FALLS TO. –.15/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107/51/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 56.78 and Brent: 63.25

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

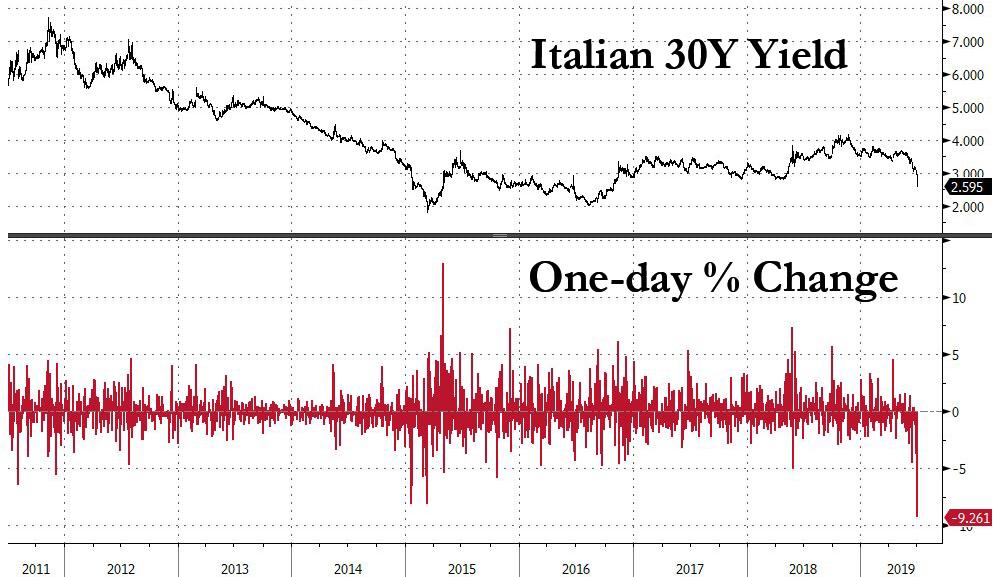

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO -.39%/Italian 10 yr bond yield DOWN to 1.59% /SPAIN 10 YR BOND YIELD DOWN TO 0.28%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.98: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.05

3k Gold at $1418.0 silver at: 14.30 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 51/100 in roubles/dollar) 63.34

3m oil into the 56 dollar handle for WTI and 63 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.83DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9824 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1108 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISING to –0.39%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.95% early this morning. Thirty year rate at 2.47%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.6560..

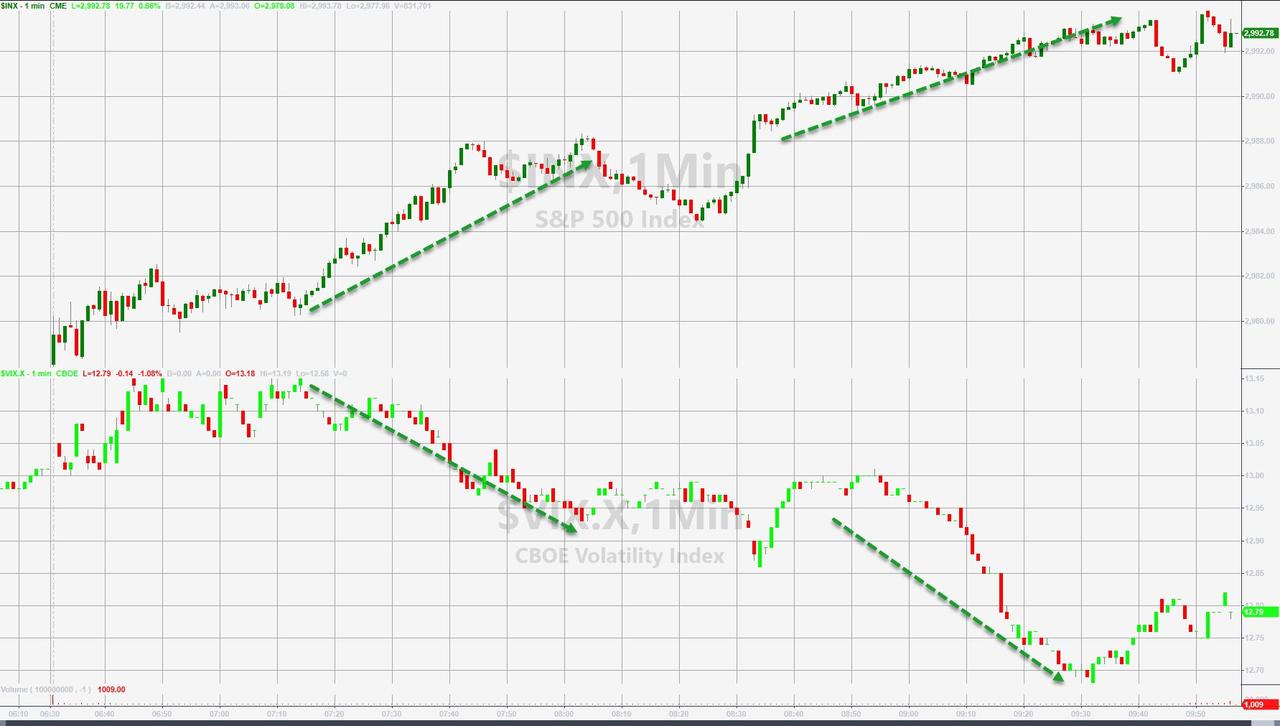

Global Bond Yields Tumble As Risk Rally Returns; S&P Inches Away From 3,000

With US traders eyeing a half-trading day today ahead of tomorrow’s July 4 holiday, and volumes even more abysmal than usual, the market’s confounding divergence accelerated overnight, with global bond yields tumbling to fresh multi-year lows, which pushed US equity futures higher amid expectations of even easier central banks, and on pace to hit 3,000 just ahead of the US holiday while European stocks were green across the board even as Asian markets were modestly lower.

Benchmark debt yields slumped to fresh lows as simmering global trade war and recession fears rose after the latest round of dismal service PMI data across the globe, which saw China’s Caixin Composite PMI tumble in June to one of the weakest prints since the financial crisis…

… however the latest catalyst for even lower rates were two particularly dovish developments, when the IMF’s Christine Lagarde was unveiled as the ECB’s next head ushering in a candidate analysts anticipate will take up departing President Mario Draghi’s mantle in providing stimulus, while Trump nominated two particularly dovish economists to the Fed’s board, St Louis Fed’s Christopher Waller, and Judy Shelton, an informal advisor to Trump who publicly said the central bank should reduce rates.

Europe’s nomination of IMF chief Christine Lagarde as Mario Draghi’s ECB replacement reinforced expectations of monetary policy easing in the bloc. Traders greeted the decision by sinking German 10-year Bund yields to record lows of minus 39 basis points, threatening to drop below the European Central Bank’s deposit rate of -0.40% for the first time in history, and Italian two-year yields back into negative territory for first time in over a year.

Meanwhile, in the US 10Y Treasury yields also tumbled, dropping as low as 1.93%, or the lowest since November 2016.

“An absence of inflation, the shortages of ‘safe’ positive yielding bonds that is a legacy of QE, geopolitical concerns and a dovish monetary policy bias almost everywhere are seeing the bond rally go on, and on,” Kit Juckes, chief global FX strategist at Societe Generale, wrote in a note.

In the UK, 10Y UK gilts yield fell 4 basis points to 0.687, bringing the below the BoE’s main policy rate for the first time in a decade after Bank of England Governor Mark Carney warned overnight of damage from rising protectionism and a “widespread slowdown.”

“We have already seen some weak data in recent weeks so that is the backdrop (for the plunge in bond yields),” said Head of Macro Strategy at Rabobank Elwin de Groot. “And now have Christine Lagarde as the likely successor of Mr Draghi at the ECB, which for the market says that the dovish policies will continue.”

Finally, Italian bonds extended gains with the 2Y Italian yield dropping below zero and the 10Y sliding to 1.71%, the lowest since Dec 2017 and well below last May’s tantrum, after a report that Rome has approved legislation aimed at setting aside future savings to keep the fiscal shortfall in line with EU limits.

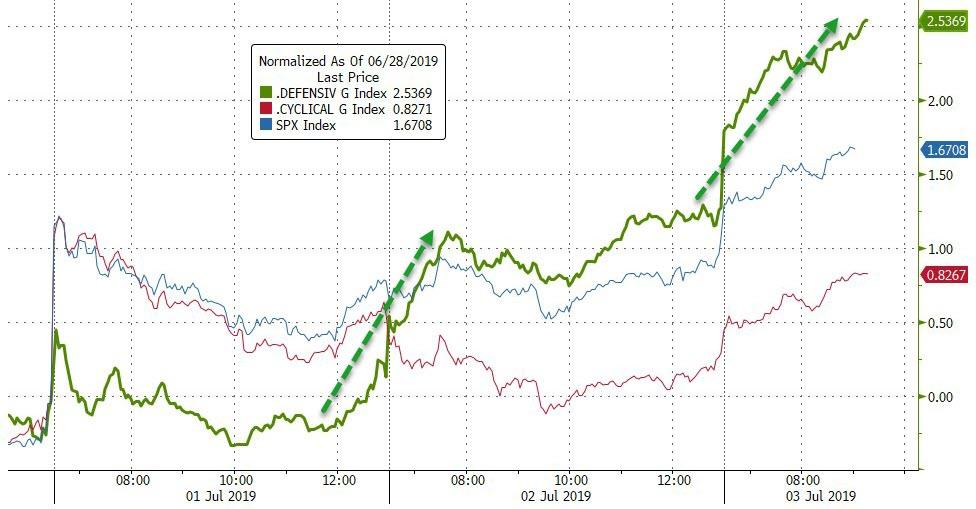

As yields dropped, stocks rose, perpetuating the divergence observed ever since the start of June when hopes of an all-in thrust by central banks unleashed a furious risk buying spree.

European shares took little notice of some sizeable overnight falls for Asia’s big bourses to push 0.6% higher. Gains were however led by an unusual pairing of traditionally defensive healthcare stocks and carmakers, which jumped 1.2%. There was plenty of data to digest too. Euro area business activity picked up slightly last month, figures showed, but it remained weak as a modest upturn in the services industry offset a continued deep downturn in factory output. Worse, forward-looking indicators did not point to a bounce back, and other data showed Britain’s economy appeared to have contracted in the second quarter against a backdrop of Brexit and global trade worries.

“The latest downturn has followed a gradual deterioration in demand over the past year as Brexit-related uncertainty has increasingly exacerbated the impact of a broader global economic slowdown,” Chris Williamson, chief business economist at IHS Markit, said of the UK reading.

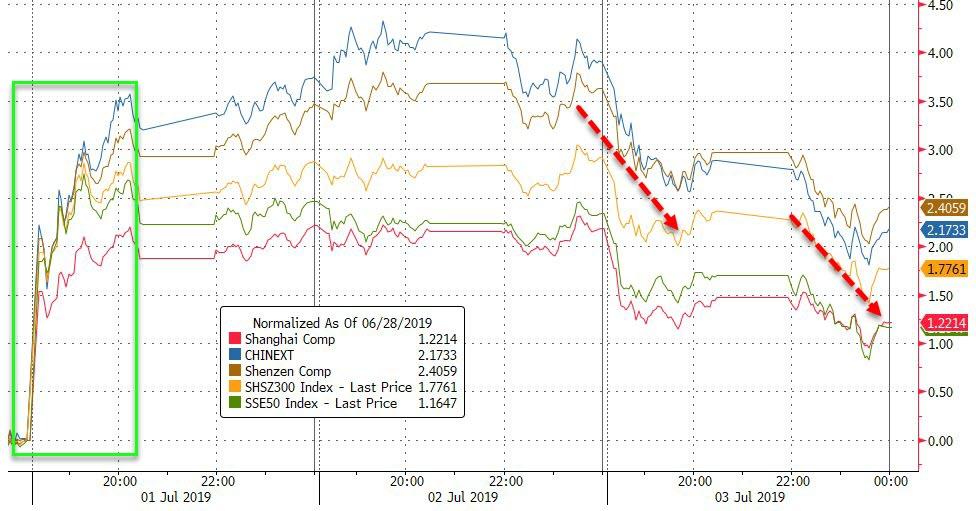

Earlier in the session, Asian traders were less excited by the prospect of negative rates across the globe as Asian stocks dropped, led by technology and energy firms, while buying Treasuries and gold amid a murky global growth outlook. Most markets in the region were down, with South Korea and China leading declines. Japan’s Topix gauge fell 0.9%, driven by Toyota Motor and Keyence, as the yen strengthened against the dollar. The Shanghai Composite Index declined 0.9%, led by Industrial & Commercial Bank and Kweichow Moutai. The S&P BSE Sensex Index advanced 0.3%, with IndusInd Bank and Reliance Industries among the biggest boosts, as traders looked toward possible government stimulus in a federal budget due Friday.

In the US, S&P futures rose 8 points just shy of 3,000 with Nasdaq 100 contracts advancing as Tesla climbed in premarket trading after a record quarter of deliveries for the electric-car maker.

In currency markets, the pound flirted with two-week lows after the PMI data and stood at $1.2568, on course for its fifth drop in the last six sessions. The euro was steadier at $1.1282 while the dollar traded down at 107.70 yen, off Monday’s high of 108.535 after the Bank of Japan made small tweaks to its bond buying program. The euro pared a small drop as purchasing manager data for the region was revised slightly higher. Gold extended gains.

Sweden’s crown meanwhile hit a 2-1/2 month high of 10.4890 versus the euro after the Riksbank bucked the global trend back towards cutting interest rates and said it remained on track to raise its by early 2020, albeit with some caveats.

Oil prices also rose a touch after data showed U.S. crude inventories fell more than expected last week but remained wobbly after a more than 4% dive on Tuesday, even after OPEC and allies including Russia agreed to extend supply cuts. Brent crude futures traded at $62.85 per barrel, up 0.7%, while U.S. West Texas Intermediate (WTI) crude futures rose 0.6% to %56.56 a barrel, following a 4.8% drop the previous day.Safe-haven gold was back on the rise too, up 0.5% at $1,425.64 per ounce having reached as high as $1,435.99

Data on U.S. private hiring, factory orders and the services sector will come on Wednesday before an early close. June’s government jobs report is due Friday, after the July 4 break.

Expected data include trade balance, jobless claims, and factory orders. International Speedway is reporting earnings.

Market Snapshot

- S&P 500 futures up 0.2% to 2,986.00

- STOXX Europe 600 up 0.5% to 391.41

- MXAP down 0.3% to 161.67

- MXAPJ down 0.4% to 531.26

- Nikkei down 0.5% to 21,638.16

- Topix down 0.7% to 1,579.54

- Hang Seng Index down 0.07% to 28,855.14

- Shanghai Composite down 0.9% to 3,015.26

- Sensex up 0.2% to 39,893.00

- Australia S&P/ASX 200 up 0.5% to 6,685.46

- Kospi down 1.2% to 2,096.02

- German 10Y yield fell 2.9 bps to -0.396%

- Euro down 0.06% to $1.1278

- Italian 10Y yield fell 12.5 bps to 1.482%

- Spanish 10Y yield fell 8.6 bps to 0.207%

- Brent futures up 0.5% to $62.73/bbl

- Gold spot up 0.5% to $1,425.43

- U.S. Dollar Index little changed at 96.75

Top News Highlights from Bloomberg

- Germany took a top EU job for the first time in more than half a century, after Ursula von der Leyen was nominated to be the bloc’s chief executive. While that’s a win for Chancellor Angela Merkel, the EU power politics involved in distributing the region’s top jobs also laid bare the cracks in her once unassailable power

- President Donald Trump said he’s planning to nominate economists Christopher Waller and Judy Shelton to serve on the Federal Reserve Board. Both are likely inclined to support the president’s call for lower interest rates

- Christine Lagarde is set to swap the helm of the International Monetary Fund for that of the European Central Bank, becoming the first woman to run euro-area monetary policy just as the bloc’s economy looks in need of fresh stimulus

- Germany’s 10-year bond yields are threatening to drop below the European Central Bank’s deposit rate for the first time

- Oil had its worst reaction to an OPEC meeting in more than four years, with prices sliding just after the cartel agreed to prolong production curbs as fears about the global economy mount

- Britain’s dominant services sector all but stagnated in June amid Brexit uncertainty and fears for the global economy. IHS Markit’s Purchasing Managers Index unexpectedly fell to 50.2. It followed weak readings for manufacturing and construction, suggesting the economy has slipped into contraction

- Boris Johnson, the favorite to be the next U.K. prime minister, has pledged he’ll launch a review of “sin taxes” on salt, fat and sugar, a signal that he wants to adopt an economically liberal approach after years in which government tried to clamp down on unhealthy behavior

- After a yearlong assault on the Federal Reserve and its chairman, President Donald Trump has tapped two wildly different economists to the central bank’s board who seemingly have one important thing in common. They’re both likely to support the president’s call for lower interest rates

Asian equity markets traded mostly subdued as the region digested another bout of substandard PMI data from China and following a lacklustre session on Wall St where trade was predominantly range-bound despite the late breakout which helped the S&P 500 notch a consecutive record closing high. ASX 200 (+0.5%) and Nikkei 225 (-0.5%) were mixed with Australia led higher by gold miners as the precious metal resumed its advances but with upside capped by financials amid concerns of tighter margins due to the lower rate environment and as energy names suffered the brunt of a near-5% drop in crude, while sentiment in Tokyo caved in from the weight of a firmer currency. Elsewhere, Hang Seng (U/C) and Shanghai Comp. (-1.0%) were downbeat with underperformance in the mainland after another PBoC liquidity drain and disappointing Chinese data in which Caixin Services PMI missed estimates to print a 4-month low and Composite PMI deteriorated to its weakest since October 2016. Finally, 10yr JGBs were higher as they tracked the gains in T-notes which saw the US 10yr Treasury yield drop to its lowest since 2016, with demand also underpinned by the downbeat risk sentiment and BoJ presence in the market.

Top Asian News

- Singapore Deal Forms Biggest Asia Pacific Hospitality REIT

- Turkish Inflation Respite Starts Countdown to First Rate Cut

- Teva Credit Investors Ramp Up Short Bets as Legal Costs Weigh

- Saudi Makeover Masks Same Old Habits When It Comes to Jobs

European Indices are firmer this morning [Euro Stoxx 50 +0.9%] diverting from the somewhat mixed performance seen overnight, where sentiment was afflicted by poor Chinese data and a PBoC liquidity drain; upside in European bourses so far has led to some chatter that the Stoxx 50 is on track to enter a bull market soon. This mornings stock strength follows on from the SPX setting a fresh record close of 2973 yesterday, in-spite of the backdrop of increasing global growth concerns. Sectors are broadly in positive territory, with the exception of the Energy sector; which is lagging on the back of yesterday’s near-5% oil complex decline. In terms of notable movers this morning, Vonovia (+3.0%) are towards the top of the Stoxx 600 on the back of a broker move where they were upgraded to buy from neutral. Alcohol and tobacco are faring better following reports that UK PM Candidate Johnson is to review ‘sin taxes’, thus upside is seen in related names such as British American Tobacco (+2.5%) and Fever Tree (+1.8%). At the other end of the index are Sainsbury’s (-1.4%) after reporting poor grocery sales and commenting that consumer outlook remains uncertain.

Top European News

- U.K. Services Stagnate, Pointing to an Economy in Contraction

- Euro-Zone Business Stays Somber as ECB Plans for More Stimulus

- Unite Buys Student Landlord Liberty Living for $1.8b

- How the Two Tory Rivals for PM Reckon They Can Fix Brexit

In FX, the Antipodean Dollars have both overcome overnight dips on the back of sub-forecast Chinese Caixin services and composite PMIs following reports that Beijing is considering purchasing a reduced amount of US agricultural products in acknowledgement of the agreement to resume trade talks. Aud/Usd has reclaimed 0.7000+ status, but remains capped below the pre-RBA high, while Nzd/Usd has not quite managed to revisit 0.6700 as the Aud/Nzd cross holds firmly above 1.0450. However, the Aussie may yet be hampered by decent expiry options sitting between 0.6985-0.7000 (1 bn) into the NY cut.

- JPY/SEK – The Yen and Swedish Crown are vying for position as the next best major, as Usd/Jpy consolidates within a 107.92-54 range after the latest safe-haven move through 108.00 and the headline pair now looks likely to remain contained by hefty expiry interest spanning 107.00-10 (3 bn) through 107.65-80 (1 bn) to 108.00 (2.2 bn). Meanwhile, Eur/Sek has pared some losses after a test of Fib support under 10.5000 in wake of the Riksbank policy meeting that stuck rigidly to previous (April) guidance in terms of the rate path and likely timing of the next hike, as growth and inflation assessments were deemed to be unchanged in the interim period.

- EUR – Mostly better than expected Eurozone PMIs and an almost glowing review of Italy’s 2019 and 2020 finances, according to EU officials citing Government analysis have propped up the single currency to an extent, with Eur/Usd trading in a tight 1.1294-69 band. Moreover, option expiries appear influential given as much as 4.7 bn running off from 1.1290 to 1.1300 vs strong technical support in the form of the 100 DMA at 1.1260.

- GBP – The Pound remains rooted to the base of the G10 ranks and another dismal UK PMI has rattled Sterling sentiment, as the services sector only just escaped contraction and the composite fell through 50 to signal negative Q2 GDP, albeit very marginal. Cable held above 1.2550, but partly due to a lethargic Dollar as the DXY continues to straddle the 200 DMA in a confined 96.873-662 range, while Eur/Gbp edged back up towards 0.9000 and recent highs only a few pips shy of the round number.

- TRY – The Lira has maintained its recovery momentum in wake of broadly in line and softer Turkish CPI data that offset subsequent news that tax on retail FX transactions could be doubled to 0.2% and President Erdogan may be given the green light to hike levies further. Usd/Try currently around the middle of 5.6645-6090 bounds.

In commodities, WTI (+0.7%) and Brent (+0.8%) are higher this morning and at the top of the day’s range, although, both WTI and Brent did drop to within a few cents of the USD 56.00/bbl and USD 63.00/bbl handles to the downside earlier in the session. Last nights larger than expected headline API draw failed to provide much in the way of impetus for the complex, which was already heavily subdued having experienced around a 5% decline in prices; in-spite of the OPEC+ meeting concluding and resulting in a agreement to extend the output cuts, with analysts citing a “sell the fact” scenario. Looking ahead, we have the EIA release later in the session where markets will be looking for confirmation of the larger than expected draw and ahead of tomorrow’s US market holiday for Independence Day. Gold (+0.5%) is supported this morning as safe havens are benefiting from the ongoing concerns around global growth, which has most prominently been seen across Fixed Income. The yellow metal has is convincingly above the USD 1400/oz mark, and has printed session highs of USD 1437/oz. Separately, Copper is subdued due to the mixed overnight Asia-Pac performance and after Chinese data missed on expectations.

US Event Calendar

- 7:30am: Challenger Job Cuts YoY +12.8%, prior 85.9%

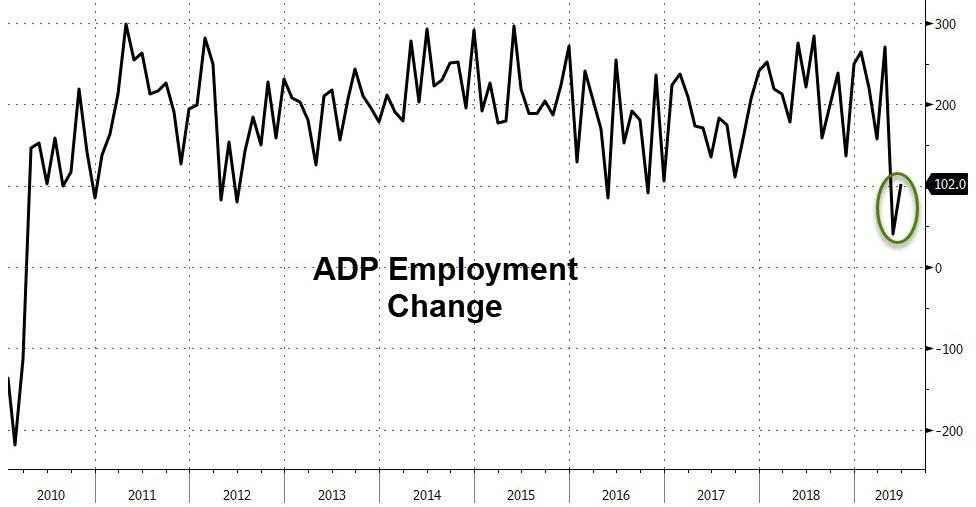

- 8:15am: ADP Employment Change, est. 140,000, prior 27,000

- 8:30am: Trade Balance, est. $54.0b deficit, prior $50.8b deficit

- 8:30am: Initial Jobless Claims, est. 222,500, prior 227,000; Continuing Claims, est. 1.68m, prior 1.69m

- 9:45am: Bloomberg Consumer Comfort, prior 63.6

- 9:45am: Markit US Services PMI, est. 50.7, prior 50.7; Markit US Composite PMI, prior 50.6

- 10am: Factory Orders, est. -0.6%, prior -0.8%; Factory Orders Ex Trans, prior 0.3%

- 10am: Durable Goods Orders, est. -1.3%, prior -1.3%; Durables Ex Transportation, prior 0.3%

- 10am: Cap Goods Ship Nondef Ex Air, prior 0.7%; Cap Goods Orders Nondef Ex Air, prior 0.4%

- 10am: ISM Non-Manufacturing Index, est. 56, prior 56.9

DB’s Jim Reid concludes the overnight wrap

A stray offside toe, VAR, a very bad penalty miss and a late sending off led to yet another World Cup semi-final heartache for England last night. Yes England’s women lost 2-1 to the USA in a very tense and dramatic last 25 minutes of football. Meanwhile over in cricket, England’s women lost the first game in the Ashes so the nations hopes roll back to the men who effectively have a World Cup quarter final in the cricket today. As someone who has followed England cricket round the world in my younger days I would be glued to this game except for the fact I’m in Milan today. I suspect the TV screens will not have it on!

It was a better day for females in the business/political world than English sportswomen yesterday as Ursula von der Leyen was nominated to be president of the European Commission with Christine Lagarde proposed as the President of the ECB. The former may face more nomination hurdles than the latter but the latter is the more important one for markets.

These nominees and the relentless march lower for bond yields were the main stories in markets yesterday. Interestingly, Lagarde will be the first ECB President who isn’t a professional economist. Given her relative inexperience with the ECB’s (complicated) policy toolkit, there is a credibility risk, especially if and when things get more complicated economically, but markets will like the fact that she is a skilled and well connected political operator.

The euro weakened a touch in response to the announcement, possibly reflecting the fact that a more hawkish individual was not chosen. It’s probable that the intellectual economic legwork will now need to be carried solely by Chief Economist Lane, the only trained economist at the top of the new leadership team (recently-appointed Vice President de Guindos is, like Lagarde, a lawyer by training). That said, a lawyer could prove to be useful in the current environment, with the focus on the legal limits of ECB asset purchases, “disenfranchisement,” the risk of debt restructurings, and the prohibition on monetary financing of governments.

Though not a central banker, Lagarde does have a catalogue of prior economic views that may provide clues of her likely policy preferences. Unsurprisingly, she is in favour of deeper European integration. She previously called for “truly integrated financial and capital markets that allow companies to raise financing across borders more easily and support investment” and also pushed for a “rainy day fund” of common EU money. More specifically, she has called for “agreement on a schedule for common deposit insurance, together with a roadmap for reducing vulnerabilities in the banking sector.” She has also cautioned against the risk of deflation, saying that “if inflation is the genie, then deflation is the ogre that must be fought decisively.” So the good intentions are likely there.

Not to be overshadowed, after US markets closed, President Trump announced two nominations to the Fed Board of Governors: Judy Shelton and Christopher Waller. Shelton is currently the US Executive Director at the European Bank for Reconstruction and Development, a role for which she was already confirmed by the Senate. Her confirmation for Governor may be more contentious, given her stated skepticism of the Fed’s legally mandated goals of maximum employment and stable prices. Waller is a more conventional candidate, currently serving as director of research at the St. Louis Fed. That means he currently works for James Bullard, the most dovish member of the FOMC. Both nominees are highly likely to support lowering interest rates.

Turning back to the move in yields yesterday now. They were driven by the combination of dovish comments out of the BoE, a big slide for oil, and holiday-impacted volumes. Indeed it was Gilts which really led the charge with 10yr yields dropping -9.2bps, equalling the biggest drop since last November. At 0.722%, yields are also now at the lowest since September 2016 and they now trade below the BoE’s Bank Rate for the first time since November 2008. The same phenomenon occurred earlier this year in the US and is just 3.3bps away from happening in Europe, using bunds and the ECB’s deposit facility.

Although shockingly poor construction data kick started the move (more on that below), it was comments from Carney which was the bigger story after the BoE Governor said that “intensification of trade tensions has increased the downside risks to global and UK growth” and that it’s “unsurprising” that the market views a lower bank rate in the future. Carney also said that the MPC will be addressing the global growth outlook in the August report. The overall feeling from the speech was that the MPC is preparing the ground to potentially drop the tightening bias (that has recently perplexed markets) when they meet next month.

Even greater was the move for BTPs where 10y yields rallied -12.8bps. That takes the two-day move to -26.3bps, the sharpest rally since last June. In fact yields are -32.1bps over the last 5 sessions. In what is perhaps less of a surprise now, 2y BTP yields also dropped into negative territory briefly yesterday however they eventually closed just above that at 0.022% (-8.0bps on the day). 10yr Bunds were a more modest -1.1bps lower albeit to a new low of -0.367%. 10yr Spain (-4.5bps) and Portugal (-4.8bps) are all of a sudden now just 30-35bps away from 0% which feels all a bit surreal.

Speaking of which, 10y Greek yields also rallied -12.4bps yesterday and are now at a new record low of 2.138%. Amazingly, the spread over Treasuries is just 16.2bps. The last time the spread was that low was all the way back in 2007. For context, the spread was above 1,600bps during 2015. That spread compression to Treasuries came despite Treasuries rallying -4.8bps to 1.976% yesterday. All this came with 5y5y inflation breakevens dropping -4.5bps in the US and -4.2bps in Europe – just 2.9bps off the pre-Sintra all-time lows. Lagarde will have her work cut out!

As mentioned, one of the drivers of lower yields and softer inflation expectations was the sharp fall in oil prices. WTI crude fell -4.65%(up +0.36% this morning), its steepest drop since May. While OPEC and its other partners reached a new output deal earlier this week, the newsflow since then has been consistently poor. The various parties are struggling to agree on the specifications of the next output cuts, with officials from Saudi Arabia and Russia both out in the press (Bloomberg) yesterday giving different methodologies for how to calculate the cuts. The former said that they would change their baseline to the 2010-14 average, rather than continuously updating it based on a five-year moving average. In response, Russian Energy Minister Novak said that “a final decision to switch hadn’t been made.” This is pretty technical, but a change would equal around 670,000 barrels per day difference in output over a year.

Given all of the above bubbling in the background, it was a much more holiday-like session for equity markets. The S&P 500 (+0.29%), NASDAQ (+0.22%) and DOW (+0.26%) all fluctuated in small ranges while the STOXX 600 also closed +0.37%. Volumes were around -20% lower in the US too with markets shutting early today ahead of the Independence Day holiday tomorrow.

This morning in Asia markets are largely heading lower with the Nikkei (-0.61%), Hang Seng (-0.18%), Shanghai Comp (-0.70%) and Kospi (-0.87%) all down. The Japanese yen is up +0.25% while gold is +0.57%. In terms of overnight data releases, we saw China’s Caixin June services PMI reading at 52.0 (vs. 52.6 expected) bringing the composite PMI down to 50.6 (vs. 51.5 last month), the lowest reading since October 2018. The Chinese yuan is trading -0.13% to 6.8806. Elsewhere, futures on the S&P 500 are down -0.13% and yields on 10y USTs are down -2.1bps this morning after declining -5.1bps yesterday to 1.954%, the lowest level since November 2016 while 2y USTs are down -2.5bps this morning (-2.5bps yesterday as well) to 1.738 bringing the 2s10s spread to +21.6bps.

In other overnight news, the US Commerce Department imposed duties of more than 400% on imports of steel products produced in Vietnam using material from South Korea and Taiwan. In three preliminary circumvention rulings on Vietnamese steel, the Commerce Department said certain products produced in South Korea and Taiwan were shipped to Vietnam for minor processing before being exported to U.S. as corrosion-resistant steel products and cold-rolled steel. Elsewhere, the BoJ reduced its bond purchases across three maturity zones. The moves, however, were somewhat expected after the central bank last week altered its monthly bond-buying plan for July, seeking to address a flattening yield curve. Yield on 10yr JGBs are down -0.6bp to -0.156%.

As for other newsflow yesterday, a Bloomberg story attracted a bit of attention, suggesting that ECB policy makers see “no need to rush into a July rate cut” and instead would prefer to wait for further data. That would better fit with the view of a September cut at which point we’ll also get the new staff forecasts and the benefit of knowing what the Fed will have done. The bigger takeaway from the story, rather than the exact timing, is that it further confirmed that a rate cut is likely.

Across the Atlantic, the only Fedspeak came from Cleveland Fed President Mester, who is a known hawk and is not a voter this year. That said, she did lay out her argument against a near-term rate cut. She said that she “prefers to gather more information before considering a change in our monetary policy stance.” She said she doesn’t want to “always react to the market” and does not support a proactive rate cut to boost inflation now. Mester was pretty specific about what would change her view: citing “a few weak job reports, further declines in manufacturing activity, indicators pointing to weaker business investment and consumption, and declines in readings of longer-term inflation expectations.” That heightens interest in this Friday’s jobs report for those who make it back after the holidays.

As for data, it was a very sparse calendar yesterday however the highlight was a spectacularly bad construction PMI here in the UK. The June reading printed at 43.1 which was well below expectations for 49.2 and also 5.5pts down from the May reading. In fact it was the lowest since the crisis. I can only think it’s because my building work finally came to an end that month. The details didn’t look much better and combined with the manufacturing reading on Monday, the data is now increasingly hinting towards a recession here in the UK or at least the rising probability of a negative growth quarter. The services reading is due out today and arguably this is the more important driver of growth so it’ll be well worth watching.

The remaining data yesterday included a weak May retail sales print in Germany (-0.6% mom vs. +0.5% expected) albeit offset to upward revisions to the prior month, and a softer than expected May PPI reading for the Euro Area (-0.1% mom vs. +0.1% expected). In the US, the only notable release was the June Wards total vehicle sales which came in at 17.3 million, matching May’s figure and exceeding the 3m, 6m, and 12m moving averages.

Looking at the day ahead, the main focus this morning in Europe will be on the remaining June PMIs with the services and composite prints due. As for the US, with markets expected to close early ahead of Thursday’s holiday we’ve got a fairly heavy slate of releases to get through including the June ADP employment change print, initial jobless claims, May trade balance, June services and composite PMIs, June ISM non-manufacturing and final May durable, capital and factory orders. Away from that the ECB’s Nowotny and Villeroy are scheduled to speak along with the BoE’s Cunliffe and Broadbent.

3A/ASIAN AFFAIRS

I)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 14.86 POINTS OR 0.50% //Hang Sang CLOSED DOWN 76.72 POINTS OR 0.27% /The Nikkei closed DOWN 204.22 POINTS OR 0.25%//Australia’s all ordinaires CLOSED DOWN .50%

/Chinese yuan (ONSHORE) closed DOWN at 6.8694 /Oil UP TO 57.82 dollars per barrel for WTI and 65.36 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.8694 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8759 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3c China/Chinese affairs

Commerce Department: Ignore Trump’s Promise To Remove Huawei From Blacklist

President Trump reportedly promised President Xi that he would ease restrictions on sales by US firms to Chinese telecoms giant Huawei when the two leaders met last weekend. But whether this was a serious offer, or just an expedient to guarantee fresh market highs for the Fourth of July, remained to be seen.

During an interview with CNBC on Tuesday, Peter Navarro, a Trump advisor and one of his administration’s most prominent trade hawks, tried to downplay the president’s promise, saying the US would allow “lower tech” chip sales to Huawei, but kept up the same wary stance that the administration has maintained for the past year.

Now, with just hours to go before the holiday and an early market close, Reuters has published details from an internal Commerce Department memo that laid the truth bare: Huawei should be treated like it’s still on the entities list, mostly because it still is.

Here’s more from Reuters:

In an email to enforcement staff on Monday that was seen by Reuters, John Sonderman, Deputy Director of the Office of Export Enforcement, in the Commerce Department’s Bureau of Industry and Security (BIS), sought to clarify how agents should approach license requests by firms seeking approval to sell to Huawei.

All such applications should be considered on merit and flagged with language noting that “This party is on the Entity List. Evaluate the associated license review policy under part 744,” he wrote, citing regulations that include the Entity List and the “presumption of denial” licensing policy that is applied to blacklisted companies.

He added that any further guidance from BIS should also be taken into account when evaluating Huawei-related license applications.

So far, at least, the memo is the only guidance that Commerce Department officials have received since Trump’s meeting with Xi in Osaka.

A person familiar with the matter said the letter was the only guidance that enforcement officials had received after Trump’s surprise announcement on Saturday. A presumption of denial implies strict review and most licenses reviewed under it are not approved.

It is unclear when the Commerce Department will provide its enforcement staff with additional guidance, based on Trump’s promises, and how that might alter the likelihood of obtaining licenses.

Approached for comment by Reuters, Huawei praised Trump’s statement over the weekend, but said little beyond that.

Huawei told Reuters earlier on Wednesday that founder and CEO Ren Zhengfei had said Trump’s statements over the weekend were “good for American companies”.

“Huawei is also willing to continue to buy products from American companies. But we don’t see much impact on what we are currently doing. We will still focus on doing our own job right,” a Huawei spokesman said in an email.

Though the news didn’t have much of an impact on their shares, chipmakers are apparently in for a rude awakening when they realize Trump’s promises re: Huawei are just more bluster.

end

4/EUROPEAN AFFAIRS

Deutsche Bank’s Restructuring Plan To Cost Staggering €5 Billion

After talks with Commerzbank collapsed, one of the key questions on the mind of most long-suffering DB shareholders has been ‘can Deutsche even afford the type of restructuring that CEO Christian Sewing has promised?’

It appears we now have an answer – and that answer is ‘no’.

According to the Financial Times, DB’s plan to drastically shrink its investment banking division will not only drive the perennially imperiled German banking giant to a net loss this year (after it barely squeaked out a profit last year) and cost as much as €5 billion ($5.65 billion), according to three sources.

That’s equivalent to roughly one-third of the bank’s market cap.

The FT report was published one day after WSJ reported that the bank is in talks with several US rivals, including Citigroup, to sell off much of its US investment-banking business. The bank has also said it plans to lower its common equity tier-one ratio to free up more cash – but whether regulators will tolerate this remains to be seen.

The restructuring plan, which will reportedly be put before the bank’s advisory board on Sunday, will involve shedding as many as 20,000 jobs, while dumping as many as €50 billion ($56.5 billion) in assets (remember all those ‘bad bank’ jokes?)

As a reminder, among the largest banks in the US and Europe, DB ranks dead last in terms of price to book, leaving its shareholders with little appetite to absorb more equity pain.

Here are some more details of the plan, courtesy of FT.

Under the plan, the 49-year-old chief executive is aiming to cut Deutsche’s annual costs by about €4bn by 2022, according to one of the people, a sharp increase from its current target of €1bn for this year. However, the bank is not preparing to raise more capital to foot the restructuring bill, one of the people said.

Raising fresh equity would be highly dilutive to existing investors, who have seen the stock sink to a record low. A decision not to raise more capital will see the Deutsche’s common equity tier one ratio fall below its current minimum target of 13 per cent of its risk-weighted assets. The bank is preparing to announce a new minimum ratio of 12.5 per cent, a person briefed on the matter said, although the actual ratio will stay above the new target even as the bulk of the restructuring costs are absorbed. A one percentage point reduction of the ratio unlocks €3.5bn in capital.

The ratio stood at 13.7 per cent at the end of the first quarter. The European Central Bank and other regulators were comfortable with Deutsche’s new target because the ratio will still be about one percentage point higher than the regulatory minimum, another person added. Deutsche, which has 91,500 employees and €347bn in risk-weighted assets, declined to comment.

The axe is expected to fall hardest on Deutsche’s Wall Street operations, with Mr Sewing preparing to shut the bank’s unprofitable US equities trading business and slim down its rates division, the people said. Garth Ritchie, head of the investment bank, is expected to depart in a change that will see Mr Sewing assume control of the ailing division, two people briefed on the matter said.