GOLD: $1398.10 DOWN $0.35 (COMEX TO COMEX CLOSING)

Silver: $15.05 UP 7 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1395.50

silver: $15.03

YOUR DATA…

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 2/6

EXCHANGE: COMEX

CONTRACT: JULY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,396.700000000 USD

INTENT DATE: 07/05/2019 DELIVERY DATE: 07/09/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 1 2

737 C ADVANTAGE 5 4

____________________________________________________________________________________________

TOTAL: 6 6

MONTH TO DATE: 706

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 6 NOTICE(S) FOR 600 OZ (0.0186 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 706 NOTICES FOR 70600 OZ (2.1959 TONNES)

SILVER

FOR JULY

30 NOTICE(S) FILED TODAY FOR 150,000 OZ/

total number of notices filed so far this month: 3425 for 17,125,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ n/a

Bitcoin: FINAL EVENING TRADE: $ n/a

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL A SMALL SIZED 120 CONTRACTS FROM 222,167 DOWN TO 222,047 DESPITE THE HUGE 32 CENT LOSS IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JULY. 0 FOR AUGUST, 3107 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 3107 CONTRACTS. WITH THE TRANSFER OF 3107 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3107 EFP CONTRACTS TRANSLATES INTO 15.54 MILLION OZ ACCOMPANYING:

1.THE 32 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

20.600 MILLION OZ INITIAL STANDING FOR JULY

WE HAD CONSIDERABLE SHORT COVERING AT THE SILVER COMEX LAST NIGHT..AND ZERO SPREADING ACCUMULATION.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

8308 CONTRACTS (FOR 5 TRADING DAY TOTAL 8308 CONTRACTS) OR 41.54 MILLION OZ: (AVERAGE PER DAY: 1661 CONTRACTS OR 8.305 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 41.54 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 5.93% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1199.14 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 120 DESPITE THE 32 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 3885 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A HUGE SIZED: 2987 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 3107 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 120 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 32 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $14.98 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.187 BILLION OZ TO BE EXACT or 169% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 30 NOTICE(S) FOR 150,000, OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 20.600 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

WITH RESPECT TO SPREADING: WE WILL WITNESS THE MORPHING OF OUR SPREADERS OUT OF SILVER AND INTO GOLD AS THE JULY MONTH PROCEEDS INTO THE ACTIVE DELIVERY MONTH OF AUGUST.

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF AUGUST.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JULY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE OPEN INTEREST FELL BY A GOOD 5285 CONTRACTS, TO 5994,55 WITH THE HUGE $19.15 LOSS WITH RESPECT TO COMEX GOLD PRICING FRIDAY// /THE SPREADING LIQUIDATION WILL NOW COMMENCE FOR GOLD….

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUMONGOUS SIZED 17,683 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 17,683 CONTRACTS, DEC> 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 599,455. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,452 CONTRACTS: 5232 CONTRACTS DECREASED AT THE COMEX AND 17,683 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 12,452 CONTRACTS OR 1,245,200 OR 38.72 TONNES. YESTERDAY WE HAD A HUGE LOSS OF $19.10 IN GOLD TRADING.…AND WITH THAT HUGE LOSS IN PRICE, WE HAD A HUMONGOUS GAIN IN GOLD TONNAGE OF 38.72 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER AND I SURE LOOKS LIKE SOMEBODY BIG WAS PICKING UP THAT PAPER. IT IS QUITE CONCEIVABLE THEY ARE TAKING ON THE BANKERS BY TURNING THAT PAPER INTO PHYSICAL GOLD .

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY : 43,927 CONTRACTS OR 4,392,700 oz OR 136.63 TONNES (5 TRADING DAY AND THUS AVERAGING: 8786 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY IN TONNES: 136.63 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 136.63/3550 x 100% TONNES =3.84% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 3056.5 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GOOD SIZED DECREASE IN OI AT THE COMEX OF 5232 WITH THE HUGE PRICING LOSS THAT GOLD UNDERTOOK ON FRIDAY($19.10)) //.WE ALSO HAD A HUMONGOUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 17,683 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 17,683 EFP CONTRACTS ISSUED, WE HAD A STRONG AND CRIMINALLY SIZED GAIN OF 12,452 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

17,683 CONTRACTS MOVE TO LONDON AND 5232 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 38.72TONNES). ..AND THIS GIGANTIC INCREASE OF DEMAND OCCURRED DESPITE THE HUGE LOSS IN PRICE OF $19.15 WITH RESPECT TO FRIDAY’S TRADING AT THE COMEX. WE WILL HAVE INCREASE SPREADING ACCUMULATION IN GOLD AS THE MONTH PROCEEDS/

THE IS BECOMING QUITE ALARMING: FOR THE PAST 10 TRADING DAYS, WE HAVE WITNESSED AT LEAST A 6,000 CONTRACT DIFFERENTIAL BETWEEN THE PRELIMINARY OI NUMBER AND THE FINAL OI NUMBER OF GOLD. TODAY IT WAS IN EXCESS OF 8,000 CONTRACTS. ALL OF THE DIFFERENCE OCCURS IN THE FRONT MONTH OF AUGUST . THIS IS HIGHLY MANIPULATIVE AND FRAUDULENT. THE CFC REFUSES TO SUPPLY ANY ANSWER TO THIS.

we had: 6 notice(s) filed upon for 600 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $0.35 TODAY//

A HUGE CHANGE SIN GOLD INVENTORY AT THE GLD:

A WITHDRAWAL OF 1.47 TONNES FROM THE GLD

INVENTORY RESTS AT 796.97 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 7 CENTS TODAY:

A HUGE DEPOSIT OF 2,341 MILLION OZ?????????

/INVENTORY RESTS AT 328.482 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TINY SIZED 120 CONTRACTS from 222,167 DOWN TO 222,047 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JULY: 0 CONTRACTS FOR AUGUST: 0, FOR SEPT. 3107 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3107 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 120 CONTRACTS TO THE 3107 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUGE GAIN OF 2987 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 14.44 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 20.760 MILLION OZ STANDING SO FAR.

RESULT: A TINY SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 32 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// FRIDAY. WE ALSO HAD A STRONG SIZED 3107 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED DOWN 77.70 POINTS OR 0250% //Hang Sang CLOSED DOWN 443.19 POINTS OR 1.59% /The Nikkei closed DOWN 212.03 POINTS OR 0.98%//Australia’s all ordinaires CLOSED DOWN 1.04%

/Chinese yuan (ONSHORE) closed DOWN at 6.8827 /Oil UP TO 57.82 dollars per barrel for WTI and 64.53 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8827 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8859 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/

4/EUROPEAN AFFAIRS

i)UK

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)IRAN/USA

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

II)MARKET TRADING/USA

ii)Market data/USA

iii)USA ECONOMIC/GENERAL STORIES

SWAMP STORIES

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; 5,373.958 oz

FOR THE JULY 2019 CONTRACT MONTH)Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 6 contract(s) of which 2 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account and 0 notices by the squid (Goldman Sachs)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JULY /2019. contract month, we take the total number of notices filed so far for the month (706) x 100 oz , to which we add the difference between the open interest for the front month of JULY. (80 contract) minus the number of notices served upon today (6 x 100 oz per contract) equals 78,000 OZ OR 2.426 TONNES) the number of ounces standing in this NON active month of JULY

Thus the INITIAL standings for gold for the JULY/2019 contract month:

No of notices served (706 x 100 oz) + (80 OI for the front month minus the number of notices served upon today (6 x 100 oz )which equals 78,000 oz standing OR 2.426 TONNES in this active delivery month of JUNE.

We GAINED 13 contracts or an additional 1300 oz will stand as these guys refused to morph into London based forwards as well as negating a fiat bonus. Somebody was in need of physical gold badly on this side of the pond…VERY UNUSUAL TO SEE QUEUE JUMPING CONTINUE THIS EARLY IN THE UP FRONT JULY GOLD CONTRACT MONTH.

SURPRISINGLY LITTLE TO NO GOLD HAS BEEN ENTERING THE COMEX VAULTS AND WE HAVE WITNESSED THIS FOR THE PAST YEAR!! WE HAVE ONLY 10.043 TONNES OF REGISTERED ( GOLD OFFERED FOR SALE) VS 2.426 TONNES OF GOLD STANDING// THEY SEEM TO BE USING CONSIDERABLE GOLD VAPOUR TO SETTLE UPON UNSUSPECTING LONGS.

total dealer silver: 87.119 million

total dealer + customer silver: 304.604 million oz

The total number of notices filed today for the JULY 2019. contract month is represented by 30 contract(s) FOR 150,000 oz

To calculate the number of silver ounces that will stand for delivery in JULY, we take the total number of notices filed for the month so far at 3425 x 5,000 oz = 17,125,000 oz to which we add the difference between the open interest for the front month of JULY. (757) and the number of notices served upon today (30 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JULY/2019 contract month: 3425(notices served so far)x 5000 oz + OI for front month of JULY( 757) number of notices served upon today (30)x 5000 oz equals 20,760,000 oz of silver standing for the JULY contract month.

WE GAINED 29 CONTRACTS OR AN ADDITIONAL 145,000 OZ WILL STAND AT THE COMEX AS THESE GUYS REFUSED TO MORPH INTO A LONDON BASED FORWARDS AND AS WELL THEY ALSO NEGATED A FIAT BONUS. IT SEEMS THAT SOMEBODY WAS BADLY IN NEED OF PHYSICAL SILVER ON THIS SIDE OF THE POND JOINING GOLD!.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 179,985 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 236,657 CONTRACTS..(we no doubt had considerable spreading activity as they are now starting to accumulate in silver)

YESTERDAY’S CONFIRMED VOLUME OF 236,657 CONTRACTS EQUATES to 1,118 million OZ 169%% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -0.34% June 27/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.10% to NAV (JUNE 27/2019 )

Note: Sprott silver trust back into NEGATIVE territory at -0.34%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 13.77 TRADING 13.23/DISCOUNT 3.96

END

And now the Gold inventory at the GLD/

JULY 8/ WITH GOLD DOWN 35 CENTS A HUGE WITHDRAWAL OF 1.47 TONNES FROM THE GLD/INVENTORY FALLS TO 796.97 TONNES

JULY 5TH/WITH GOLD DOWN $19.50/NO CHANGES IN GOLD INVENTORY AT THE GLD//INV RESTS AT 798.44 TONNES

JULY 3// WITH GOLD UP $12.60 TODAY A SURPRISE WITHDRAWAL OF 1.76 TONNES FROM THE GLD//INVENTORY RESTS AT 798.44

JULY 2. WITH GOLD UP $18.90 A HUGE “PAPER” DEPOSIT OF 6.16 TONNES INTO THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 1: WITH GOLD DOWN $24.70 A HUGE “PAPER GOLD” WITHDRAWAL OF 1.76 TONNES FROM THE GLD/INVENTORY RESTS TONIGHT AT 794.04 TONNES

JUNE 28/WITH GOLD UP $.90 TODAY: ANOTHER 2.05 TONNES OF PAPER GOLD REMOVED AND THIS GOLD WAS USED IN ATTACKING GOLD AT THE COMEX/INVENTORY RESTS AT 795.80 TONNES

JUNE 27/WITH GOLD DOWN $6.10: ANOTHER HUGE WITHDRAWAL OF 1.76 PAPER TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 797.61 TONNES

JUNE 26/WITH GOLD DOWN $3.00: WE HAD A HUGE WITHDRAWAL OF 2.37 TONNES FROM THE GLD/INVENTORY RESTS AT 799.61 TONNES

JUNE 25/WITH GOLD UP $1.30 (AND WAY UP BEFORE THE BANKERS WHACKED) WE WITNESSED ANOTHER 1.95 TONNES OF PAPER GOLD ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 801.98 TONNES

JUNE 24/WITH GOLD UP $18.00 A MONSTROUS PAPER DEPOSIT OF 34.93 TONNES/INVENTORY RESTS AT 799.03 TONNES

JUNE 21/WITH GOLD UP $ 2.90, NO CHANGE IN GOLD INVENTORY: INVENTORY RESTS AT: 764.10 TONNES

June 20/WITH GOLD UP $47.95, NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 19 WITH GOLD DOWN $1.65: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONES

JUNE 18/JUNE 18/WITH GOLD UP $7.60: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 17/WITH GOLD DOWN $1.65 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 764.10 TONNES

JUNE 14/ WITH GOLD UP $1.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.40 TONNES OF PAPER GOLD INTO THE GLD///INVENTORY RESTS AT 764.10 TONNES

june 13/WITH GOLD UP $6.60 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 759.70 TONNES

JUNE 12/WITH GOLD UP $7.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 756.18 TONNES

JUNE 11/WITH GOLD UP $1.65 CENTS TODAY: A TINY CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .24 TONNES AND THIS IS TO PAY FOR FEES/INVENTORY RESTS AT 756.18 TONNES

JUNE 10/WITH GOLD DOWN $16.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES/INVENTORY RESTS AT 756.42 TONNES

june 7/WITH GOLD UP $3.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

jUNE 6/WITH GOLD UP $8.40 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 5 WITH GOLD UP $6.00 TODAY/STRANGE: A WITHDRAWAL OF 2.06 TONNES FROM THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 4/WITH GOLD UP 0.85 TODAY: A MONSTROUS PAPER GAIN OF 16.44 TONNES/GLD INVENTORY RESTS AT 759.65 TONNES

JUNE 3/WITH GOLD UP $17.50 TODAY: ANOTHER BIG CHANGE, A DEPOSIT OF 2.35 TONNES OF GOLD INTO THE GLD//

MAY 31/WITH GOLD UP $17.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GLD INVENTORY RESTS AT 740.86 TONNES

MAY 30: WI6H GOLD UP $6.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES/INVENTORY RESTS AT 740.86 TONNES

MAY 29/WITH GOLD UP $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 737.34 TONNES

MAY 28/WITH GOLD DOWN $6.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD> A WITHDRAWAL OF 1.47 TONNES/INVENTORY RESTS AT 737.34 TONNES

MAY 24/WITH GOLD DOWN $1.60 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 738.81 TONNES

MAY 23/WITH GOLD UP $11.10 TODAY: A STRANGE WITHDRAWAL OF .88 TONNES FORM THE GLD/INVENTORY RESTS AT 738,81 TONNES

MAY 22//WITH GOLD FLAT TODAY: WE HAD A GOOD 1.52 TONNES OF GOLD DEPOSIT INTO THE GLD/INVENTORY RESTS TONIGHT AT 739.69 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JULY 8/2019/ Inventory rests tonight at 796.97 tonnes

*IN LAST 620 TRADING DAYS: 137.79 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 520 TRADING DAYS: A NET 27.89 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JULY 8/WITH SILVER UP 7 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 328,492 MILLION OZ

JULY 5/WITH SILVER DOWN 32 CENTS WE STRANGELY HAD A HUGE INVENTORY GAIN OF 2,234 MILLION OZ//INVENTORY RESTS AT 328.492 MILLION OZ

JULY 3 WITH SILVER UP 10 CENTS A HUGE INCREASE IN INVENTORY..INVENTORY RESTS AT 326.151 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 323.330 MILLION OZ//

JULY 1/ WITH SILVER DOWN 16 CENTS: A SURPRISING DEPOSIT OF 936,000 OZ INTO THE SLV/INVENTORY RESTS TONIGHT AT 323.330 MILLION OZ/

JUNE 28/WITH SILVER UP 6 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.394 MILLION OZ//

JUNE 27/WITH SILVER DOWN 7 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.575 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.394 MILLION OZ//

JUNE 26/WITH SILVER UP 17 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 25/WITH SILVER DOWN 25 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ.

JUNE 24/WITH SILVER UP 11 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 21/WITH SILVER DOWN 22 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 20/WITH SILVER UP 53 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 19/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ/

JUNE 18 WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ

JUNE 17/WITH SILVER UP XXX CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ//

JUNE 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 12/WITH SILVER UP 4 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.413 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 11/WITH SILVER UP 10 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 10/WITH SILVER DOWN 38 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 7/WITH SILVER UP ANOTHER 12 CENTS, NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 6/WITH SILVER UP ANOTHER 9 CENTS TODAY: A FAIR SIZE DEPOSIT OF 630,087 OZ//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 5/WITH SILVER UP 4 CENTS TODAY: A HUGE PAPER DEPOSIT OF 2.396 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 314.434 MILLION OZ//

JUNE 4/WITH SILVER UP 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

JUNE 3/WITH SILVER UP 19 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

MAY 31/WITH SILVER UP 6 CENTS TODAY: A DEPOSIT OF 422,000 OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 312.038 MILLION OZ/

May 30/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ///

MAY 29/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 28/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 24/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ/

MAY 23/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 22/WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 311.616 MILLION OZ

MAY 21: WITH SILVER DOWN 3 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV; A WITHDRAWAL OF 750,000 OZ///INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 20/WITH SILVER UP 6 CENTS:NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.366 MILLION OZ

JULY 8/2019:

Inventory 328.492 MILLION OZ

Global Gold Alert: Is Your Gold S.A.F.E. ?

GOLDNOMICS PODCAST (Episode 12)

Watch Podcast Here or Listen on Apple Podcasts, SoundCloud or Blubrry

- It is now time to move to own actual physical gold coins and bars

- Become your own central bank and avoid ETF and online gold

- Take delivery and own gold and silver bullion the S.A.F.E. way

- Gold ETFs, online gold and paper or electronic gold may not be liquid or cashed in or physically redeemed in a crisis

- Some 80% of gold and silver investments (our estimation) or proxy precious metals are not fit for purpose in a systemic or monetary crisis

Is Your Gold S.A.F.E. ?

Are your precious metals Segregated, Actionable, Flexible and what are the total Expenses?

- Are your precious metals FULLY SEGREGATED & Allocated?

- Are your gold and silver investments ACTIONABLE, accessible, portable & directional?

- Do you have real FLEXIBILITY, liquidity and competitive prices with your gold and silver bullion and the ability to take delivery, transfer to third parties and sell easily to the global market?

- What are the EXPENSES and total costs to buy, sell, fabricate, segregate, take delivery or move to another provider? Are the expenses clear and transparent or have the expenses changed over the years or are they hidden in the small print? Can the provider arbitrarily change the pricing to buy, sell, store and take deliver?

Test Your Gold Exit and Be Sure It Is SAFE

Test your provider by selling some of your holding for cash and by taking delivery of or transferring to a third party some of your gold and silver bars.

Call your provider today and test if you can take delivery or transfer some of your holding in a test transfer. Take note of all limitations, time delays and unexpected costs.

Watch Podcast Here or Listen on Apple Podcasts, SoundCloud or Blubrry

News and Commentary

Poland’s Central Bank Increases Gold Reserves by Over 125 Tonnes

Poland Central Bank Gold Reserves Rise Sharply in the Month of June

Gold Prices Drop, Log a Loss of 1% for the Week but Close Over $1,400

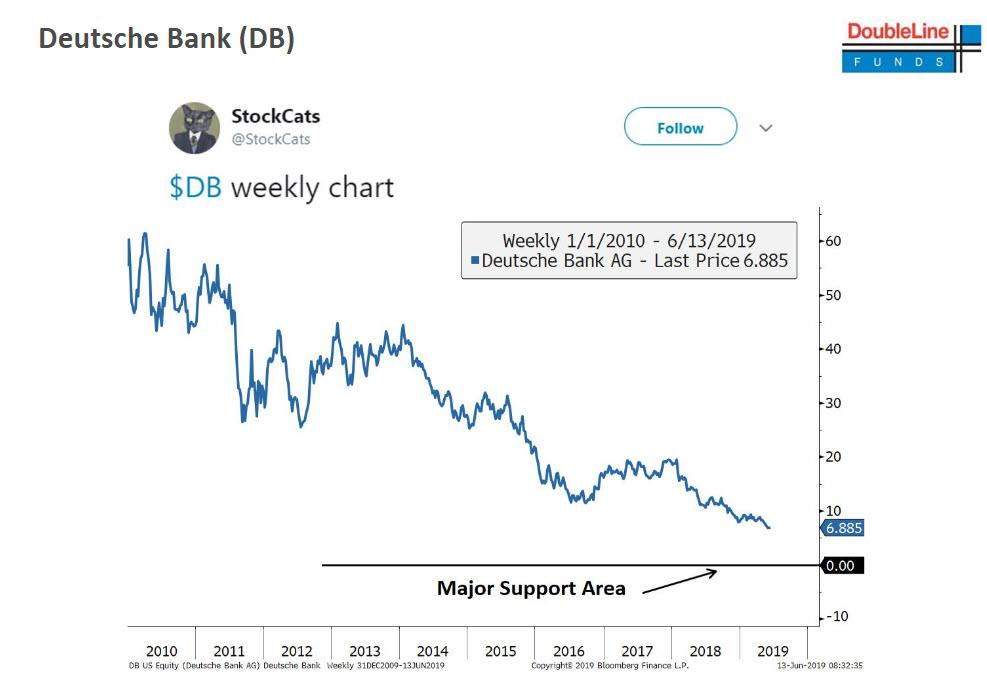

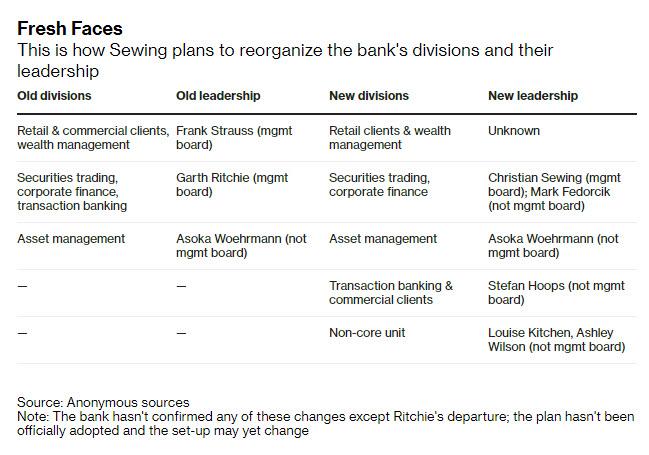

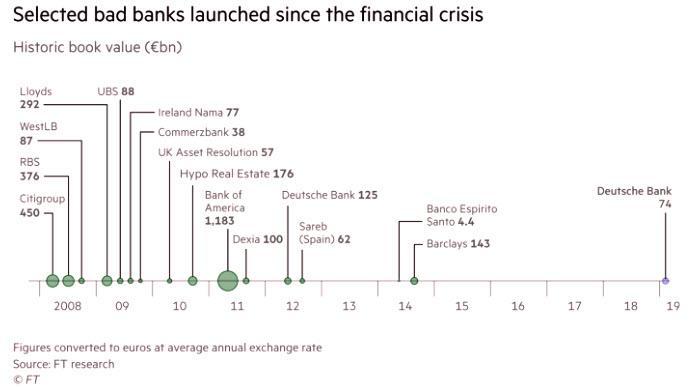

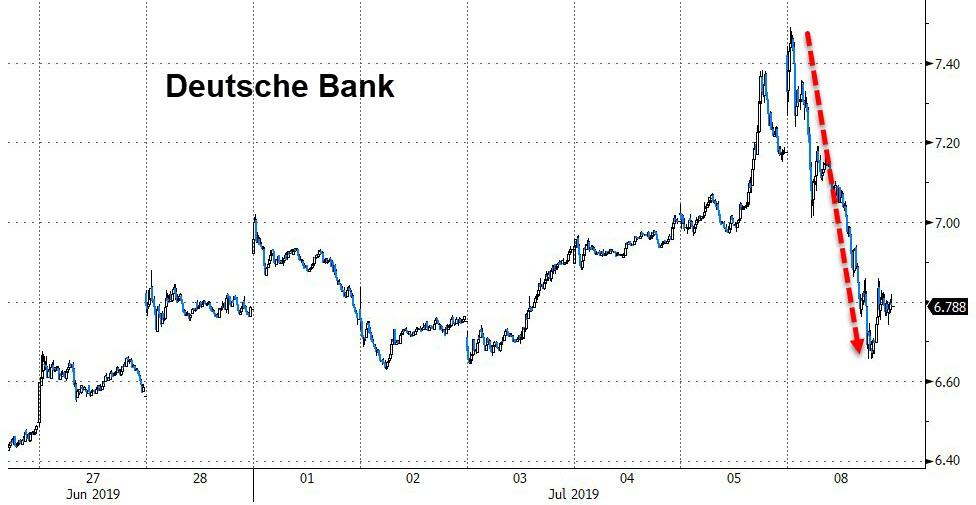

Deutsche Bank Will Exit Global Equities Business and Slash 18,000 Jobs in Sweeping Overhaul

Domestic Gold Discounts in India at Three-year Peak After Import Duty Increase

Why Gold Prices Have Climbed to Their Highest Since 2013

Traders “Used the Better-than-expected Jobs Number to Push Gold Prices Lower” – Goldcore

‘Never Has a Big Down Day Looked Better’ – GATA

This (Completely Reasonable) Change in Investor Behavior Would Send Gold to the Moon

LBMA Gold Prices (AM/ PM Fix – USD, GBP & EUR)

05-Jul-19 1414.40 1388.65, 1126.43 1110.92 & 1255.99 1237.70

04-Jul-19 1415.25 1414.90, 1125.41 1125.55 & 1254.19 1254.59

03-Jul-19 1425.10 1413.50, 1133.52 1123.31 & 1262.78 1251.65

02-Jul-19 1393.10 1391.05, 1105.01 1101.02 & 1233.59 1231.77

01-Jul-19 1390.05 1390.10, 1099.81 1099.99 & 1227.41 1227.74

28-Jun-19 1413.20 1409.00, 1114.87 1108.18 & 1241.07 1237.81

27-Jun-19 1402.25 1402.50, 1103.71 1105.87 & 1233.14 1234.76

26-Jun-19 1406.75 1403.95, 1109.22 1106.73 & 1238.501236.32

Receive Our Free Daily or Weekly Updates by Signing Up Here

ii) Physical stories courtesy of GATA/Chris Powell

At KWN von Greyerz notes that gold hasn’t kept up with inflation, so will anyone ever ask why?

Submitted by cpowell on Mon, 2019-07-08 00:03. Section: Daily Dispatches

8p ET Sunday, July 7, 2019

Dear Friend of GATA and Gold:

At King World News tonight, Swiss gold fund manager Egon von Greyerz writes that adjusted for inflation the gold price high in 1980 would be more than $18,000 today. That gold has not come close to keeping up with inflation since then is both the powerful disparagement of gold and evidence of gold price suppression via the government-inspired and underwritten creation of a vast imaginary derivative supply, about which no one in mainstream financial journalism and even the gold mining industry itself dares to ask.

Von Greyerz’s commentary is headlined “The Road To $18,160 Gold and the Wisdom Of Jesse Livermore,” the renowned investor of the last century who in 1940 declared himself a failure and committed suicide long before the era of gold price suppression. Insofar as GATA has not yet defeated central banking’s comprehensive market rigging, we too can be considered a failure so far, but there’s still beer, wine, and spite, so we aim to press on in the morning anyway.

Von Greyerz’s commentary is posted at KWN here:

https://kingworldnews.com/greyerz-the-road-to-18160-gold-and-the-wisdom-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

New York Sun: The debate over the Fed begins

Submitted by cpowell on Sun, 2019-07-07 21:41. Section: Daily Dispatches

From the New York Sun

Sunday, July 7, 2019

It can’t be entirely a coincidence that the first move by a major newspaper against the confirmation of Judy Shelton as a governor of the Federal Reserve should come from the Washington Post. It is, after all, the only newspaper in America to have been launched to glory by, in Eugene Meyer, a just-retired chairman of our central bank. Yet the Post gets into none of that history in its editorial this morning in respect of Ms. Shelton:

https://www.washingtonpost.com/opinions/one-of-trumps-latest-fed-board-n…

It’s not hard to see why.

The Post’s beef against Ms. Shelton is not that she lacks for credentials. It calls her academic credentials “strong” and acknowledges that she has held public positions in what we would call two non-political agencies, the National Endowment for Democracy, which she chaired, and the European Bank for Reconstruction and Development, to which she is currently America’s representative. What the Post objects to, for starters, is that she’s had an “eminently political career.” …

… For the remainder of the commentary:

https://www.nysun.com/editorials/the-debate-over-the-fed-begins/90754/

END

Ronan Manly: Poland joins Hungary with huge gold purchase and repatriation

Submitted by cpowell on Mon, 2019-07-08 01:54. Section: Daily Dispatches

9:54p ET Sunday, July 7, 2019

Dear Friend of GATA and Gold:

Poland has vastly increased its gold reserves in the last year and is repatriating at least 100 tonnes of them from the Bank of England, Bullion Star gold researcher Ronan Manly reports tonight.

Of special interest, Manly writes, the Polish central bank’s explanation for repatriating its gold reserves from London included “political risk,” perhaps an acknowledgment that the Bank of England effectively confiscated Venezuela’s gold reserves this year.

Manly’s commentary is headlined “Poland joins Hungary with Huge Gold Purchase and Repatriation” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/poland-joins-hungary-with-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Never has a big down day looked better,’ but the mainstream media won’t tell you

Submitted by cpowell on Sat, 2019-07-06 03:27. Section: Daily Dispatches

10:23a ET Saturday, July 6, 2019

Dear Friend of GATA and Gold:

At mid-morning Friday your secretary/treasurer noticed that despite the market opening’s $30 pounding in the gold price, gold and the gold mining shares were turning upward, and by the end of the day your secretary/treasurer was nearly amazed that the gold price had clawed back to $1,400 and the shares had finished down only 1%.

It was almost like Tuesday’s remarkable recovery after Monday’s pounding.

A few years ago the gold price and the shares would have required months to recover from such poundings, even a pounding inflicted from such a distorted and misleading federal jobs report as was announced Friday.

But as far as your secretary/treasurer can tell, there was no commentary Friday night about the remarkable recovery of gold and the shares except in GATA Chairman Bill Murphy’s daily “Midas” commentary at LeMetropoleCafe.com.

Murphy concluded: “What a day — very positive in some regards. Gold has clawed its way back to $1,400, proving once again that major dips are to be bought. Even pitiful silver has recovered so close to $15.

“The best news was the shares, which stood their ground like champs. The XAU lost only 0.87 to 83.18 and the HUI fell only 1.69 to 193.01.

“We know the Gold Cartel is going to throw the kitchen sink at the gold and silver markets. This is what they do. Gold is very much rebelling against the totalitarians. Should the gold price take out $1,440, it is very likely to change the cabal’s game plan.

“Fingers crossed that they are in as much trouble as it appears, after all these revolting, manipulative years.

“Supporting the trouble the bums might be in is the share action of the HUI and how it has refused to close its distinguished gap several times.

“Never has a big down day looked better.”

In his Gold & Silver Digest letter for Saturday, GATA board member Ed Steer concurred: “That the precious metal equities came very close to finishing the Friday session unchanged, though their respective underlying metals were crushed, has to been seen as a huge positive. It certainly indicates, at least to me, that gold and silver stocks continue to be under serious accumulation by the strongest of hands, because everything that was sold in a panic at the 9:30 a.m. ET open was bought, plus a whole bunch more as the Friday trading session progressed.”

Your secretary/treasurer avoids making predictions, except for sometimes respecting Orwell’s vision of the future: “A boot stamping on a human face — forever.” That’s what GATA is working against.

Our work would be easier if most of the people in the monetary metals mining industry cared about anything besides their own salaries and if mainstream financial news organizations had any journalistic integrity. But they don’t, so, as Lee Strasburg’s Hyman Roth scolds Al Pacino’s Michael Corleone in “The Godfather, Part II”: “This is the business we’ve chosen”:

https://www.youtube.com/watch?v=VsbyvuO_AqM

As always one must play the hand one is dealt.

But while GATA, Murphy’s LeMetropoleCafe.com and Steer’s Gold & Silver Digest letter are separate operations, the latter two being proprietary to Murphy and Steer, it is simply a matter of fact for your secretary/treasurer to acknowledge that there is seldom much daily commentary on the gold “market” that comes as close to what is really happening as those publications do.

Murphy’s “cafe” offers a free two-week trial subscription here:

http://lemetropolecafe.com/Guests.cfm

Steer’s digest can be subscribed to here:

https://edsteergoldsilver.com/

If you haven’t checked them out already, please do it now. You’re not likely to approach the truth about the “markets” through The Wall Street Journal or the Financial Times. Those news organizations know the “markets” are rigged and have been given the most compelling documentation but won’t report it. They are bought and paid for by the people and institutions they purportedly are covering.

The real news is elsewhere.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

Join GATA here:

New Orleans Investment Conference

Hilton New Orleans Riverside Hotel

Friday-Monday, November 1-4, 2019

https://neworleansconference.com/

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

…

END

Alasdair Macleod: Broken markets and fragile currencies

Submitted by cpowell on Fri, 2019-07-05 15:53. Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, St. Helier, Jersey, Channel Islands

Friday, July 5, 2019

There are growing signs that the global economic slowdown is for real.

As was the case in 1929, the combination of the peak of the credit cycle coupled with trade protectionism in the Smoot-Hawley Tariff Act are similar conditions to those of today and potentially pose a serious economic challenge to the post-Bretton Woods fiat currency system.

Therefore, we must consider the consequences if monetary policy fails to contain the developing recession and it turns into a full-blown slump.

Complacency over broken markets is no longer an option, with rising prices for gold and bitcoin signalling the prospect of a new round of currency debasement to avoid market distortions unwinding. This article shows why this outcome could undermine fiat currencies entirely and looks at the alternatives of bitcoin and gold in this context. …

… For the remainder of the commentary:

https://www.goldmoney.com/research/goldmoney-insights/broken-markets-and…

END

Trump tweet puts him at odds with his Fed nominee, Judy Shelton

Submitted by cpowell on Wed, 2019-07-03 21:46. Section: Daily Dispatches

By Victoria Guida

Politico, Washington, D.C.

Wednesday, July 3, 2019

President Donald Trump’s call today for the United States to manipulate its currency to boost exports is in direct conflict with the long-held view of at least one key scholar: his newest pick for the Federal Reserve board, Judy Shelton.

Shelton, who advised Trump’s presidential campaign and is now U.S. executive director for the European Bank for Reconstruction and Development, has spent decades calling for a more stable, predictable dollar value.

…

She wants central banks to do as little as possible to interfere with markets. As part of that, she thinks the Fed should more aggressively reduce the massive portfolio of bonds that it purchased to prop up the economy after the financial crisis.

But Trump wants the Fed to buy more bonds to inject additional cash into the economy.

… For the remainder of the report:

https://www.politico.com/story/2019/07/03/federal-reserve-judy-shelton-1…

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.8827/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.8859 /shanghai bourse CLOSED DOWN 77.70 POINTS OR 2.50%

HANG SANG CLOSED DOWN 443.19 POINTS OR 1.54%

2. Nikkei closed DOWN 212.03 POINTS OR 0.98%

3. Europe stocks OPENED ALL RED

USA dollar index UP TO 97.17/Euro RISES TO 1.1203

3b Japan 10 year bond yield: RISES TO. –.15/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107/51/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 57.82 and Brent: 64.53

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.38%/Italian 10 yr bond yield DOWN to 1.74% /SPAIN 10 YR BOND YIELD UP TO 0.39%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.12: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

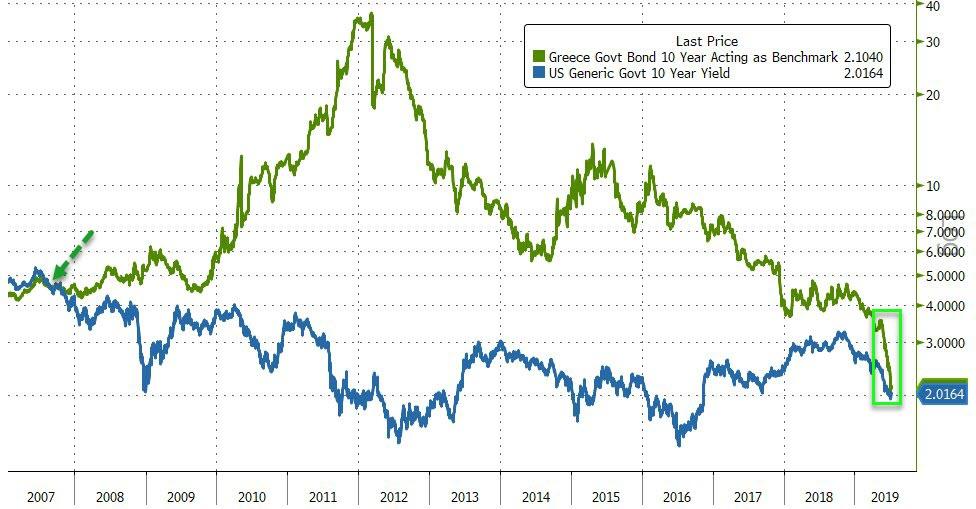

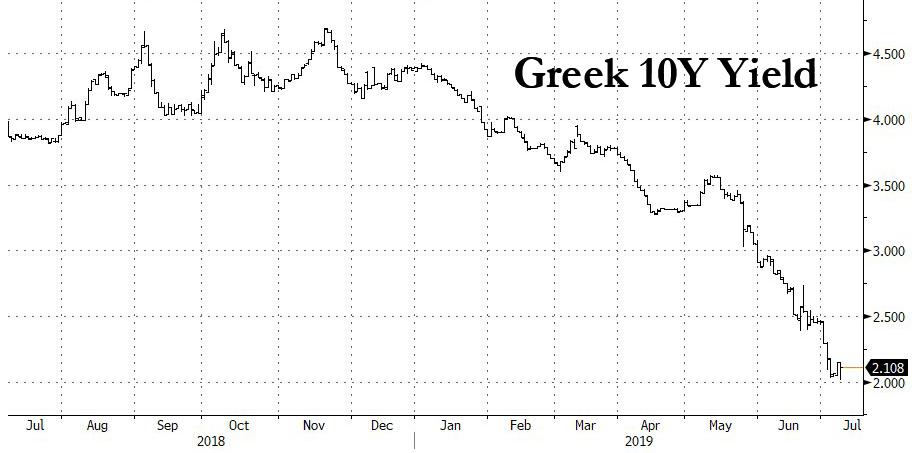

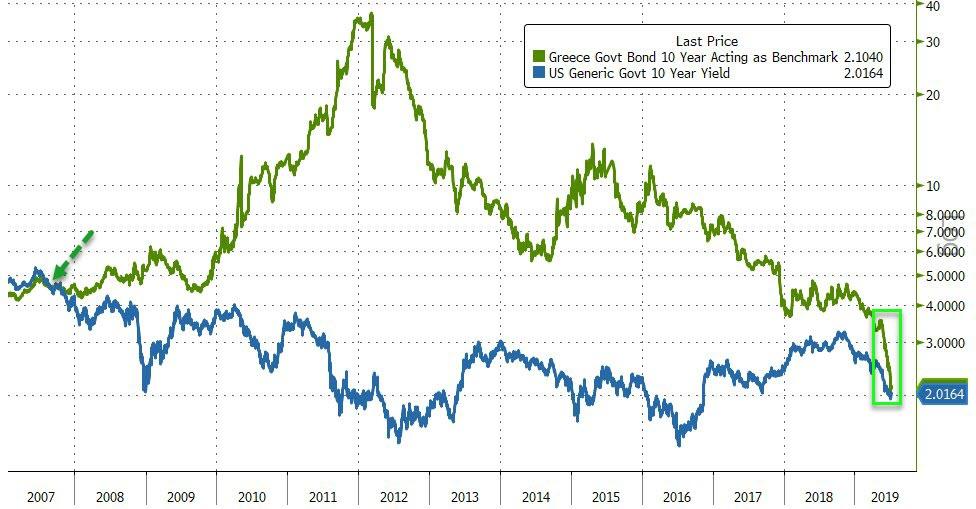

3j Greek 10 year bond yield FALLS TO : 2.11

3k Gold at $1405.50 silver at: 14.06 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 1/100 in roubles/dollar) 63.82

3m oil into the 57 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.37 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9910 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1127 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.38%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.02% early this morning. Thirty year rate at 2.53%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.7383..

US Futures Slide, Asia Tumbles In Post-Payroll Revulsion As Powell Looms

In delayed response to Friday’s stellar June payrolls report which saw rate cut odds slashed across the board, with a 50bps cut by the FOMC in three weeks no longer a possibility, global shares slumped on Monday, with Asian shares tumbling the most in two months, European stocks broadly lower and US equity index futures well in the red.

The overnight weakness in equity markets can be explained simply: since the start of 2019, global equities have been bolstered by expectations that central banks will keep interest rates at or near record lows to boost economic growth. Those expectations were hammered Friday’s payrolls report which showed that nonfarm payrolls jumped 224,000 in June, beating forecasts for 160,000, in a sign the world’s largest economy still had some fire. Given the strength shown in that data, investors now expect U.S. Federal Reserve Chairman Jerome Powell to go slow on rate cuts this year.

“The re-adjustment in expectations did push the dollar higher and had a negative effect on Asia but Europe has been supported by investors saying ‘whatever the Fed does, the ECB [European Central Bank] will still cut’,” said Andrew Milligan, head of global strategy at Aberdeen Standard Investments.

Sentiment was also hit by Morgan Stanley’s decision – first reported here – to cut its exposure to global equities to “Underweight” due to growing doubt about the ability of policy easing to offset weaker economic data. “We are lowering our exposure to global equities to the range we consider ‘underweight’,” Morgan Stanley’s London-based strategist Andrew Sheets said in a note. The previous range was ‘neutral’.

Expensive valuations and pressure on earnings were among the reasons for the downgrade, Sheets said, while the bank increased its exposure to emerging markets sovereign credit and safe haven Japanese government bonds.

The session started on the back foot when Asian stocks suffered their biggest slide in two months, led by health care and communications firms as MSCI’s index of Asia-Pacific shares outside Japan tumbled 1.4%. Markets in China, South Korea and India led declines in the region. Strong U.S. payroll data weakened expectations for aggressive rate cuts, sending Japan’s Topix index 0.9% lower, with pharmaceutical companies among the biggest drags after news that the U.S. was devising a “favored nations” plan to buy drugs based on the lowest prices paid by other countries.

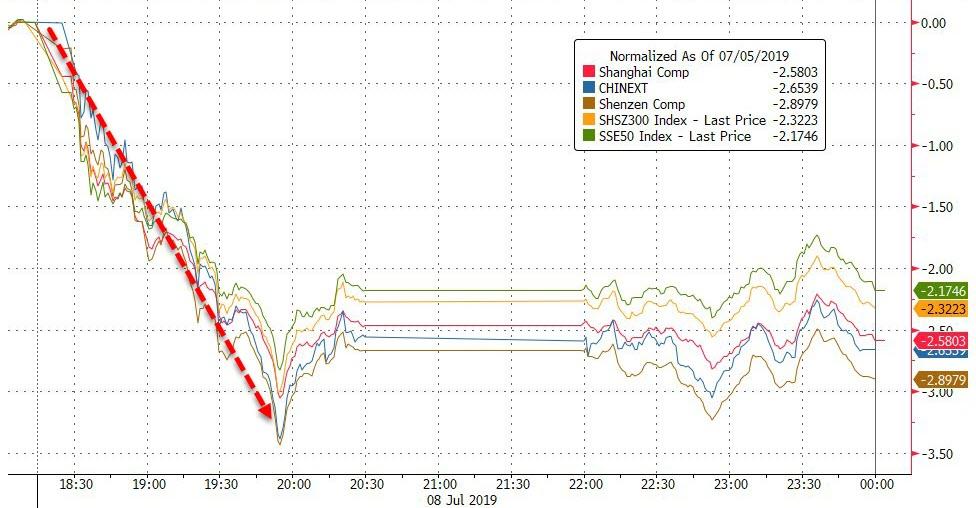

China’s Shanghai Composite Index slumped 2.6%, pulling back further away from 3,000, and its biggest drop since May 6, as traders fear a flood of new listings will overload the market and drain demand for existing stocks. Heavyweights China Shenhua Energy and Ping An Insurance helped drag the benchmark down. The S&P BSE Sensex Index fell as much as 2%, heading for its biggest loss in seven months, as disappointment over a lack of broad stimulus in India’s budget weighed on equities for a second day. In South Korea, the benchmark index was dragged lower by Samsung Electronics and SK Hynix as concerns mount over political tensions with Japan. The Kospi extended its loss in afternoon trading and closed 2.2% lower.

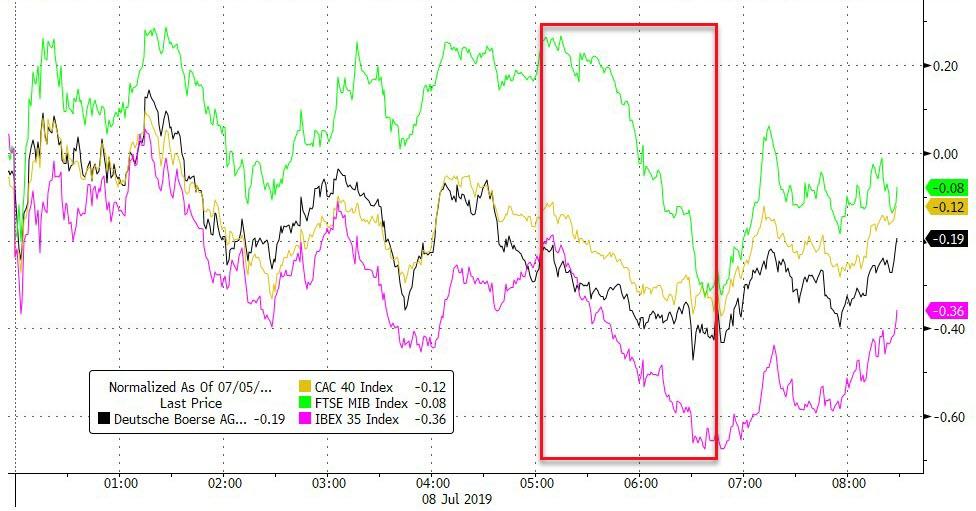

The drop in European stocks was more muted but still widespread as bonds were little changed; the Euro Stoxx 50 dropped -0.1%, tracking the 0.2% drop in the e-mini S&P futures. Deutsche Bank shares initially surged, rising to their highest level since early May as investors welcomed the bank’s move to cut 18,000 jobs around the world as part of a restructuring plan that will cost 7.4 billion euros; the surge helped lift shares in other European investment banks UBS, Credit Suisse and Societe Generale were up more than 1%, while Barclays is up 0.3% and HSBC is down around 1%.

However, it didn’t take long for traders to realize that amid the massive cuts, DBK will have problems boosting profits as it slashes revenue, and the shares quickly reversed their gain, sliding as much as 1.7% shortly after the open.

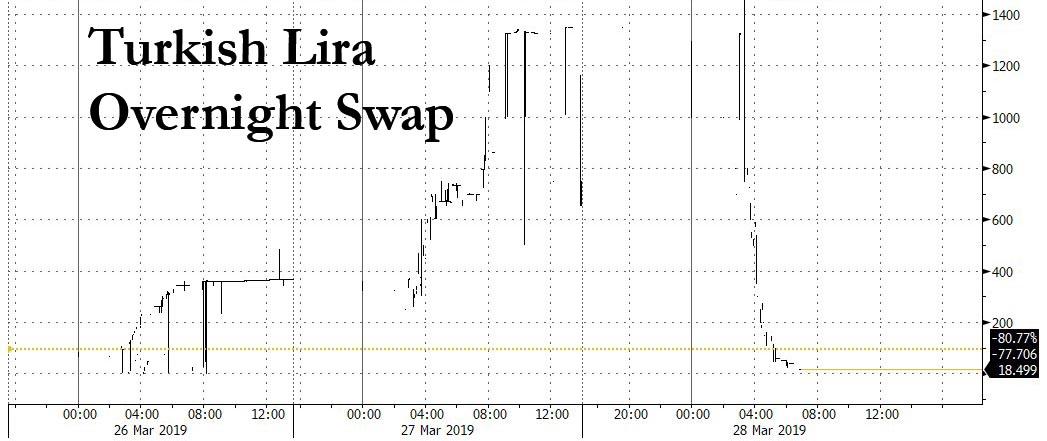

The big outlier in what has otherwise been a relatively quiet session was Turkey, where the lira, stocks and government dollar bonds all tumbled after President Erdogan dismissed the central bank governor, a move that fueled worries about monetary policy independence. Erdogan sacked Cetinkaya for refusing the government’s repeated demands for rate cuts, laying bare differences between them over the timing of interest rate cuts to revive the recession-hit economy. The turkish lira traded down 1.7% versus the dollar, off weakest levels in the session.

Not too far away, the Greek stock index rallied at first before erasing gains and slipping 1.2% after Greece’s opposition conservatives returned to power with a landslide victory in snap elections on Sunday.

European bonds mostly trade steady to 2bps lower, with 10-yr Greek yield -4bps to 2.11% after center-right party won election at the weekend. 10-yr BTP/bund spread 1bp wider at 212bps. UST yields 1bp lower in the 2-yr through 10-yr tenors. Greek 10-year bond yields fell by 14 basis points in early trade to hit new all-time lows of 2.016%, reversing the 12 basis point yield rise on Friday.

There was some positive news on the protracted China-U.S. trade war, with White House Economic adviser Larry Kudlow confirming that top representatives from the United States and China will meet in the coming week for trade talks.

“Whether the negotiators can find a solution to the difficult structural issues that remain between the two sides is another matter, and Kudlow cautioned there was ‘no timeline’ to reach an agreement,” National Australia Bank strategist Rodrigo Catril said.

In FX, the dollar index stood at 97.229 in early London trading, below the near three-week high of 97.443 it hit on Friday after last week’s strong U.S. jobs data lowered expectations for a sharp Federal Reserve interest rate cut. The euro, which dropped to $1.1208 EUR=EBS on Friday, traded at $1.1225, unchanged on the day. After hitting a six-month low to the dollar on Friday as a result of poor economic data and a rise in expectations that the Bank of England will cut interest rates, the British pound was last quoted at $1.2513 down 0.2% on the day.

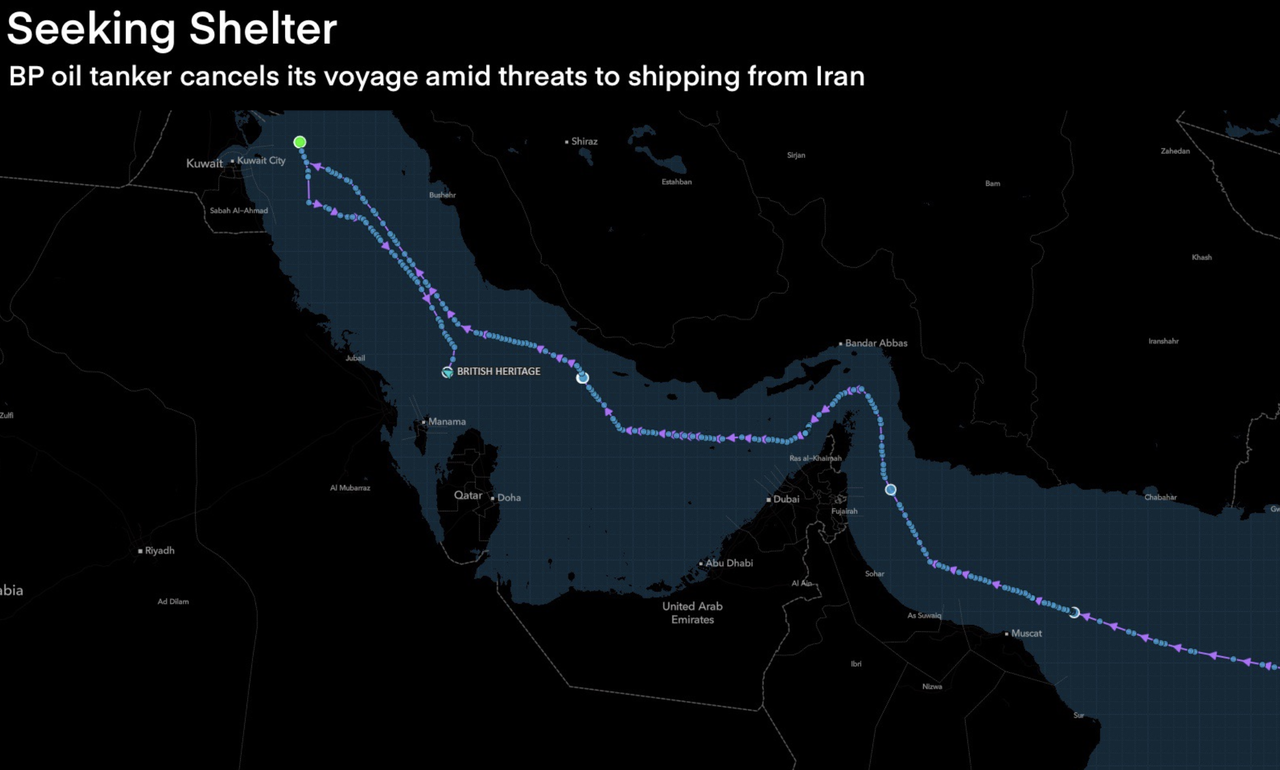

Geopolitics will also be in focus this week following news on Sunday that Iran will boost its uranium enrichment, in breach of a cap set by a landmark 2015 nuclear deal. “So far U.S.-Iran tensions have not had a material impact on markets, but if tensions escalate it could be a different story,” said NAB’s Catril.

In commodity markets, oil prices rose with Brent crude futures LCOc1 up 8 cents at $64.31. U.S. West Texas Intermediate was up 6 cents at $57.57 a barrel.

In other geopol news, President Trump said the Fed does not have a clue and that the most difficult problem for the US is the Fed and not the nation’s competitors, while he separately commented that the Fed would lower rates if it knew what it was doing. Furthermore, Trump said that China is devaluing its currency and that the UK Ambassador to the US has not served the UK well.

Iran announced that it has surpassed the 3.67% uranium enrichment cap, according to a Iran Nuclear Energy Spokesman; additionally, enriching uranium above 20% has been discussed at the Supreme National Security Council but no decision has been taken as of yet; Iran’s 3rd step in reducing commitments under the 2015 nuclear deal will be stronger. Follows earlier reports that Iran is to lift uranium enrichment to over 3.67%, while an Iranian official confirmed they will scale back commitment to the 2015 nuclear deal and will keep reducing its commitments every 60 days unless signatories move to protect it from US sanctions and signal room for diplomacy

Trading is expected to be subdued ahead of Powell’s semi-annual testimony to the U.S. Congress on Wednesday, which will provide further clues on the near-term outlook for monetary policy. The only economic data on the calendar is the latest Consumer Credit report at 3pm ET.

Market Snapshot

- S&P 500 futures down 0.2% to 2,985.25

- STOXX Europe 600 up 0.09% to 390.48

- MXAP down 1.2% to 159.82

- MXAPJ down 1.4% to 523.74

- Nikkei down 1% to 21,534.35

- Topix down 0.9% to 1,578.40

- Hang Seng Index down 1.5% to 28,331.69

- Shanghai Composite down 2.6% to 2,933.36

- Sensex down 1.9% to 38,746.13

- Australia S&P/ASX 200 down 1.2% to 6,672.20

- Kospi down 2.2% to 2,064.17

- German 10Y yield fell 0.9 bps to -0.372%

- Euro up 0.06% to $1.1232

- Italian 10Y yield rose 6.8 bps to 1.39%

- Spanish 10Y yield rose 6.1 bps to 0.384%

- Brent futures up 0.6% to $64.60/bbl

- Gold spot up 0.4% to $1,405.53

- U.S. Dollar Index down 0.1% to 97.18

Top Overnight News from Bloomberg

- The Turkish lira declined by the most since March after President Recep Tayyip Erdogan dismissed central bank governor Murat Cetinkaya, undermining the institution’s independence weeks before it’s scheduled to decide on policy and fueling concerns that borrowing costs will be lowered faster than expected

- Deutsche Bank announced a radical overhaul of its business — it is cutting a fifth of its 91,000-person work force and closing it’s equity trading. Analysts said that while the restructuring was broader than expected, the newly announced targets will be tough to achieve

- Kyriakos Mitsotakis will have to move swiftly to tackle a raft of lingering economic problems when he’s sworn in as Greek prime minister on Monday. Investors expect the 51-year-old New Democracy leader, whose conservatives secured a healthy parliamentary majority in Sunday’s election, to prove his business-friendly reputation is deserved

- British Conservatives plotting to thwart a no-deal Brexit will make another attempt this week to stop the next prime minister from forcing a chaotic break with the European Union without Parliament’s consent. BOE has a forecast problem in market’s bets on Brexit rate cuts

- President Donald Trump wrapped up the weekend as he started it, jawboning the Federal Reserve to lower interest rates at a time when he may be sizing up his two latest picks for Fed governor as successors to Chairman Jerome Powell.

- The European Central Bank has the determination and capacity to act as needed to support the euro-area economy, Bank of France Governor Francois Villeroy de Galhau said

- Bank of Japan Governor Haruhiko Kuroda says extremely low interest rates will be kept in place until at least around next spring while the bank will keep an eye on risks for price momentum.

- China’s foreign-currency holdings rose for a second month amid potential capital inflows and positive valuation effects to the highest level in more than a year

- Oil edged higher as rising tension in the Middle East kept investors wary, while expectations the U.S. and China can make a quick breakthrough following the resumption of trade talks are low

- German industrial production saw a slight pick-up in May — a rare sign of resilience as manufacturers in Europe’s largest economy struggle with global trade tensions and subdued demand. Output gained 0.3% on the month, just short of economists’ estimates for a 0.4% gain. While the increase is welcome, it claws back only a fraction of the 2% drop recorded in April

- The U.K. plans to fine British Airways 183.4 million pounds ($230 million) over computer attacks that exposed customer data, marking the first major application of far-reaching European Union rules requiring companies to tighten anti-hacking measures

Asian equity markets began the week with firm losses as the region reacted to the weakness last Friday on Wall St. ASX 200 (-1.1%) and Nikkei 225 (-1.0%) were lower in which the commodity-related sectors led the broad declines in Australia, especially gold miners after the precious metal slipped below the USD 1400/oz level as a function of a stronger USD and tempered rate cut calls, while Tokyo sentiment was also downbeat as participants digested data releases including a contraction in Machinery Orders. Hang Seng (-1.5%) and Shanghai Comp. (-2.6%) were the laggards after continued PBoC liquidity inaction and further clashes between police and protesters who have now targeted tourist areas in Kowloon. In addition, there were suggestions the US-China trade truce at the G20 has done little to bring the sides closer to an actual trade agreement and it is also expected that China could use its plan to name foreign companies a national security risk, as a bargaining chip in trade discussions. Finally, 10yr JGBs were lower as they tracked the decline in T-notes and rebound in yields in the aftermath of the strong US jobs data, with the absence of the BoJ in the market also contributing to the lack of demand for bonds.

Top Asian News

- China’s June FX Reserves Rise to Highest Since April 2018

- SocGen’s Long Lira-Rand Call Proves Short-Lived on Erdogan Risk

- Kuroda: To Keep Rates Very Low Until at Least Around Spring 2020

- Anta Drops Most Since May as Second Short Seller Targets Firm

- Investors Dump Korean Chip Makers Amid Japan’s Export Curbs

Major European indices are little changed this morning [Euro Stoxx 50 -0.1%] though bourses have been somewhat choppy. Deutsche Bank (-0.1%) have announced a major restructuring programme (full details available in the EU Equity Opening News) which includes 18k job cuts by 2022 and the creation of a net capital release unit representing EUR 74bln of risk-weighted assets. In addition, no dividend is to be paid for the next two years and they anticipate a Q2 net loss of EUR 2.8bln. The bank opened firmer this morning by around 3.5%, as markets initially had positive expectations for the Co’s plan; notably the FT highlight that UBS’s share prices roughly doubled in the 3 years after they announced a very similar plan in 2012. However, Co. shares have since given up these gains as further comments have been released by the Co for instance that they see significant uncertainty in their forecast to at least break even in 2020. Unsurprisingly, the banking sector has moved largely in sympathy the German bank this morning, currently lower by around 0.2%. Elsewhere, Pirelli (+4.0%) reside at the top of the FTSE MIB after being upgraded to overweight from neutral at JP Morgan. Finally, Sodexo (-4.1%) are in the red this morning post-earnings, where the Co. indicated that FY19 operating profit is to towards the lower end of the previously announced range.

Top European News

- ECB Plan to Modernize Bond Sales Gets Cool Reception From Banks

- New Democracy Meets Old Greek Problems After Mitsotakis Win

- Tories Plotting to Thwart No-Deal Brexit Prepare New Attack

- Philipp Who? Julius Baer Stuns Market With Insider Pick for CEO

- Spanish Bulls Shrug Off Doubters as Economy Keeps on Booming

In FX, vastly contrasting starts to the new week for the Kiwi and Lira, as Nzd/Usd rebounds firmly from post-NFP lows to probe above 0.6650, but Usd/Try extends gains to just over 5.7930 at one stage on the back of further Government intervention aimed at forcing the Turkish CB to cut rates. In short, President Erdogan sacked CBRT chief Cetinkaya over the weekend by decree and put Deputy Governor Uysal in charge and it seems that the failure to cut rates at the June policy meeting and/or not signalling sufficiently aggressive easing for this month prompted the decree and change of leadership.

- USD – The Dollar has eased back from Friday’s headline payrolls peaks across the board, not just against the Kiwi as noted above, with the DXY unable to sustain momentum or breach 97.500 to expose the next upside technical objective. Another verbal lashing from US President Trump about the Fed not helping the economy, along the lines of his Turkish counterpart may be weighing on the index and Greenback generally, as markets brace for Powell’s semi-annual testimony to gauge whether easing is on the cards for the July FOMC, and more importantly if there is more than merely an insurance cut in the offing. On that note, markets are 97.5% certain that Funds will be lowered by 25 bp vs just 2.5% still looking for -50 bp.

- AUD – The next best major, but capped ahead of 0.7000 as the Aud/Nzd cross drifts back down to 1.0500 from rebound highs posted in wake of last week’s RBA rate cut and tweak in guidance to signal a pause after 2 in a row.

- GBP/JPY/CAD/EUR/CHF – All narrowly mixed against the Usd as Cable consolidates in a narrow range north of 1.2500 and the Yen pares some losses between 108.58-29 amidst weaker than forecast Japanese data (machinery orders) and with decent option expiry interest sitting just below (1.2 bn from 108.25-15 and 1 bn from 108.05-00). Meanwhile, the Loonie has also found its footing after underperforming on Friday when Canadian jobs data revealed an unexpected decline, but the breakdown was not as bleak, with Usd/Cad meandering in a 1.3062-83 range, and the single currency has shrugged off a surprise deterioration in Sentix sentiment to hold above 1.1200 in a 1.1219-34 band. Note, expiries could keep Eur/Usd in check given 2.5 bn sitting at 1.1250-55 and 1.1260-65, while the Franc is midway between 0.9900-19 and straddling 1.1125 vs the Euro in lacklustre mood overall.

In commodities, WTI and Brent have had a jittery start to the week and are trading within a relatively narrow USD 0.50/bbl range, with the complex continuing to garner some support from Friday’s price action where WTI reclaimed the USD 57.00/bbl level on Friday and is approaching the USD 58.00/bbl level; session high of USD 57.91. Recent commentary for the complex has been relatively light, Iranian Oil Minister Zanganeh said he is hopeful that Iran’s oil exports will improve and the main concern is Iran’s ability to export oil not the price of oil. Elsewhere, Ineos’ Forties Pipeline System’s (575k BPD) oil flows are to be continually reduced as a processing unit is in need of maintenance; flows are expected to be reduced to 150mln BPD until Tuesday. Separately, Goldman Sachs have reiterated their stance that they continue to see WTI between USD 50-60/bbl and Brent between USD 55-65/bbl. Looking ahead, this week we have the three main monthly oil market reports beginning with the EIA’s STE tomorrow at 17:00 BST which includes their expanded forecast discussion. Gold (+0.5%) is firmer this morning as the metal has once again surpassed the USD 1400/oz level to the upside after losing the handle last week post US jobs report. Of note for the yellow metal, PBoC added 0.33mln ounces of gold to their reserve stockpile in June, to a total of 61.94mln ounces; the PBoC’s seventh consecutive months of gold buying. Separately, copper has been largely resilient to the downside seen in Asia overnight, with the red metal firmer by jut shy of 1.0% this morning; though does trade within a narrow range on the day thus far.

US Event Calendar:

- 3pm: Consumer Credit, est. $17.0b, prior $17.5b

DB’s Jim Reid concludes the overnight wrap

Welcome to a new week where the main highlight for markets will likely be Fed Chair Powell’s testimony before the House Financial Services Committee (Wednesday) and the Senate (Thursday) on monetary policy and the state of the US economy. Friday’s strong payrolls report has thrown the cat amongst the pigeons to some degree with regards July’s rate cut options(0, 25bps or 50bps?) with 2yr yields up 10bps on Friday and markets moving from pricing in low 30bps of rate cuts earlier on Friday to around 27.5bps now. We’ll also see the last FOMC meeting minutes on Wednesday for a little extra detail on how that dovish get together played out. In addition it’s a very busy week for Fedspeak as tomorrow Bostic and Bullard address a conference in St Louis while Quarles will make a keynote address on stress testing with Powell due to make introductory remarks. On Wednesday we’re due to hear from Bullard again while on Thursday we’re expecting comments from Williams, Bostic, Barkin, Kashkari and Quarles. So plenty of potential for market moving headlines.

As for data, global inflation reports are the highlights. The June CPI report will be out in the US on Thursday followed by the June PPI report on Friday. The consensus for the former is a 0.0% mom headline reading and +0.2% core reading which should be enough to hold the annual rate at +2.0% yoy. We’ll also get June CPI and PPI data in China on Wednesday while in Europe we get final June CPI revisions for Germany and France on Thursday. In Europe the other key data are probably the May industrial production prints in Germany on Monday, the UK on Wednesday and the Euro Area on Friday. In the UK we also get May GDP on Wednesday which given the alarm over the recent deterioration in data will be closely watched. The rest of the day by day week ahead is at the end as usual.

Asian markets have started the week on a weaker footing after Friday’s strong US payroll report reduced expectations for the scale of imminent Fed rate cuts. The Nikkei (-0.98%), Hang Seng (-1.64%), Shanghai Comp (-2.46%) and Kospi (-1.84%) are all lower. Meanwhile, the Turkish lira is down c. -2.2% this morning as over the weekend Turkish President Erdogan removed the central bank chief Murat Cetinkaya and made it clear that he expects both the successor and the rest of the establishment to toe the government’s line on monetary policy. Deputy Governor Murat Uysalwas has been named as a replacement. Elsewhere, futures on the S&P 500 are down -0.21%.