GOLD: $1398.45 DOWN $19.15 (COMEX TO COMEX CLOSING)

Silver: $14.98 DOWN 32 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1399.40

silver: $14.98

YOUR DATA…

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 9/21

EXCHANGE: COMEX

CONTRACT: JULY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,417.700000000 USD

INTENT DATE: 07/03/2019 DELIVERY DATE: 07/08/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 9

737 C ADVANTAGE 21 11

905 C ADM 1

____________________________________________________________________________________________

TOTAL: 21 21

MONTH TO DATE: 700

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 21 NOTICE(S) FOR 2,100 OZ (0.0653 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 700 NOTICES FOR 7000 OZ (2.177 TONNES)

SILVER

FOR JULY

2 NOTICE(S) FILED TODAY FOR 10,000 OZ/

total number of notices filed so far this month: 3195 for 16,975,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ n/a

Bitcoin: FINAL EVENING TRADE: $ n/a

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE A CONSIDERABLE SIZED 943 CONTRACTS FROM 221,224 UP TO 222,167 WITH THE 10 CENT GAIN IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JULY. 0 FOR AUGUST, 1693 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1693 CONTRACTS. WITH THE TRANSFER OF 1693 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1693 EFP CONTRACTS TRANSLATES INTO 8.465 MILLION OZ ACCOMPANYING:

1.THE 10 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

20.600 MILLION OZ INITIAL STANDING FOR JULY

WE HAD CONSIDERABLE SHORT COVERING AT THE SILVER COMEX LAST NIGHT..AND ZERO SPREADING ACCUMULATION.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

5201 CONTRACTS (FOR 4 TRADING DAY TOTAL 5201 CONTRACTS) OR 26.005 MILLION OZ: (AVERAGE PER DAY: 1300 CONTRACTS OR 6.500 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 26.005 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 3.71% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1183,50 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 943, WITH THE 10 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1683 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 2636 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1693 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 943 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 10 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.30 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.111 BILLION OZ TO BE EXACT or 159% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 2NOTICE(S) FOR 10,000OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 20.600 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

WITH RESPECT TO SPREADING: WE WILL WITNESS THE MORPHING OF OUR SPREADERS OUT OF SILVER AND INTO GOLD AS THE JULY MONTH PROCEEDS INTO THE ACTIVE DELIVERY MONTH OF AUGUST.

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF AUGUST.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JULY BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE OPEN INTEREST FELL BY A FAIR 1262 CONTRACTS, TO 604,687 DESPITE THE strong $12.50 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING WEDNESDAY// /THE SPREADING ACCUMULATION WILL NOW COMMENCE FOR GOLD….

THIS IS THE 8TH OUT OF THE LAST 9 TRADING SESSIONS THAT THE PRELIMINARY OI CONTRACTED GREATER THAN 6,000 CONTRACTS FROM THE FINAL. TODAY IT IS OVER 8000 AND AS SUCH A MASSIVE FRAUD

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6564 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 6564 CONTRACTS, DEC> 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 604,687. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A SMALL SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5302 CONTRACTS: 1262 CONTRACTS DECREASED AT THE COMEX AND 6564 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 5302 CONTRACTS OR 530,200 OZ OR 16.49 TONNES. YESTERDAY WE HAD A STRONG GAIN OF $12.50 IN GOLD TRADING.…AND WITH THAT STRONG GAIN IN PRICE, WE HAD A GOOD GAIN IN GOLD TONNAGE OF 16.49 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY : 26244 CONTRACTS OR 2,624,400 oz OR 81.621 TONNES (4 TRADING DAY AND THUS AVERAGING: 2179 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAY IN TONNES: 81.62 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 81.621/3550 x 100% TONNES =2.81% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 3,001.49 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIR SIZED DECREASE IN OI AT THE COMEX OF 1262 DESPITE THE STRONG PRICING GAIN THAT GOLD UNDERTOOK ON YESTERDAY($12.500) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6564 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6564 EFP CONTRACTS ISSUED, WE HAD A GOOD SIZED GAIN OF 5302 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6564 CONTRACTS MOVE TO LONDON AND 1262 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 16.49 TONNES). ..AND THIS GOOD INCREASE OF DEMAND OCCURRED ACCOMPANYING THE STRONG GAIN IN PRICE OF $12.50 WITH RESPECT TO WEDNESDAY’S TRADING AT THE COMEX. WE WILL COMMENCE WITH SPREADING ACCUMULATION IN GOLD AS THE MONTH PROCEEDS/

we had: 21 notice(s) filed upon for 2100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $19.50 TODAY//

NO CHANGE SIN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 798.44 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 32 CENTS TODAY:

A HUGE DEPOSIT OF 2,341 MILLION OZ?????????

/INVENTORY RESTS AT 328.482 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A CONSIDERABLE SIZED 943 CONTRACTS from 221,224 UP TO 222,167 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JULY: 0 CONTRACTS FOR AUGUST: 0, FOR SEPT. 1693 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1693 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1168 CONTRACTS TO THE 1693 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 2636 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 14.18 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 20.600 MILLION OZ STANDING SO FAR.

RESULT: A CONSIDERABLE SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 10 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// WEDNESDAY. WE ALSO HAD A STRONG SIZED 1693 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 14.86 POINTS OR 0.50% //Hang Sang CLOSED DOWN 76.72 POINTS OR 0.27% /The Nikkei closed DOWN 204.22 POINTS OR 0.25%//Australia’s all ordinaires CLOSED DOWN .50%

/Chinese yuan (ONSHORE) closed DOWN at 6.8694 /Oil UP TO 57.82 dollars per barrel for WTI and 65.36 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.8694 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8759 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/

4/EUROPEAN AFFAIRS

i)UK

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)IRAN/USA

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

II)MARKET TRADING/USA

ii)Market data/USA

iii)USA ECONOMIC/GENERAL STORIES

SWAMP STORIES

Let us head over to the comex:

we had XX dealer entry:

We had XX kilobar entries

total gold withdrawals; XXX oz

FOR THE JULY 2019 CONTRACT MONTH)Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 21 contract(s) of which 11 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account and 0 notices by the squid (Goldman Sachs)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JULY /2019. contract month, we take the total number of notices filed so far for the month (700) x 100 oz , to which we add the difference between the open interest for the front month of JULY. (88 contract) minus the number of notices served upon today (21x 100 oz per contract) equals 74,200 OZ OR 2.308 TONNES) the number of ounces standing in this NON active month of JULY

Thus the INITIAL standings for gold for the JULY/2019 contract month:

No of notices served (700 x 100 oz) + (88)OI for the front month minus the number of notices served upon today (21 x 100 oz )which equals 76,700 oz standing OR 2.3856 TONNES in this active delivery month of JUNE.

We GAINED 25 contracts or an additional 2500 oz will stand as these guys refused to morph into London based forwards as well as negating a fiat bonus. Somebody was in need of physical gold badly on this side of the pond…VERY UNUSUAL TO SEE QUEUE JUMPING THIS EARLY IN THE UP FRONT JULY CONTRACT MONTH.

SURPRISINGLY LITTLE TO NO GOLD HAS BEEN ENTERING THE COMEX VAULTS AND WE HAVE WITNESSED THIS FOR THE PAST YEAR!! WE HAVE ONLY 10.043 TONNES OF REGISTERED ( GOLD OFFERED FOR SALE) VS 2.3856 TONNES OF GOLD STANDING// THEY SEEM TO BE USING CONSIDERABLE GOLD VAPOUR TO SETTLE UPON UNSUSPECTING LONGS.

total dealer silver: 87.119 million

total dealer + customer silver: 304.604 million oz

The total number of notices filed today for the JULY 2019. contract month is represented by 2 contract(s) FOR 10,000 oz

To calculate the number of silver ounces that will stand for delivery in JULY, we take the total number of notices filed for the month so far at 3395x 5,000 oz = 16,975,000 oz to which we add the difference between the open interest for the front month of JULY. (727) and the number of notices served upon today (2 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JULY/2019 contract month: 3395 notices served so far)x 5000 oz + OI for front month of JULY( 14727 number of notices served upon today (2)x 5000 oz equals 20,600,000 oz of silver standing for the JULY contract month.

WE GAINED 5 CONTRACTS OR AN ADDITIONAL 25,000 OZ WILL STAND AT THE COMEX AS THESE GUYS REFUSED TO MORPH INTO A LONDON BASED FORWARDS AND AS WELL THEY ALSO NEGATED A FIAT BONUS. IT SEEMS THAT SOMEBODY WAS BADLY IN NEED OF PHYSICAL SILVER ON THIS SIDE OF THE POND JOINING GOLD!.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 179,985 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 236,657 CONTRACTS..(we no doubt had considerable spreading activity as they are now starting to accumulate in silver)

YESTERDAY’S CONFIRMED VOLUME OF 236,657 CONTRACTS EQUATES to 1,118 million OZ 169%% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -0.34% June 27/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.10% to NAV (JUNE 27/2019 )

Note: Sprott silver trust back into NEGATIVE territory at -0.34%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 13.77 TRADING 13.23/DISCOUNT 3.96

END

And now the Gold inventory at the GLD/

JULY 5TH/WITH GOLD DOWN $19.50/NO CHANGES IN GOLD INVENTORY AT THE GLD//INV RESTS AT 798.44 TONNES

JULY 3// WITH GOLD UP $12.60 TODAY A SURPRISE WITHDRAWAL OF 1.76 TONNES FROM THE GLD//INVENTORY RESTS AT 798.44

JULY 2. WITH GOLD UP $18.90 A HUGE “PAPER” DEPOSIT OF 6.16 TONNES INTO THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 1: WITH GOLD DOWN $24.70 A HUGE “PAPER GOLD” WITHDRAWAL OF 1.76 TONNES FROM THE GLD/INVENTORY RESTS TONIGHT AT 794.04 TONNES

JUNE 28/WITH GOLD UP $.90 TODAY: ANOTHER 2.05 TONNES OF PAPER GOLD REMOVED AND THIS GOLD WAS USED IN ATTACKING GOLD AT THE COMEX/INVENTORY RESTS AT 795.80 TONNES

JUNE 27/WITH GOLD DOWN $6.10: ANOTHER HUGE WITHDRAWAL OF 1.76 PAPER TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 797.61 TONNES

JUNE 26/WITH GOLD DOWN $3.00: WE HAD A HUGE WITHDRAWAL OF 2.37 TONNES FROM THE GLD/INVENTORY RESTS AT 799.61 TONNES

JUNE 25/WITH GOLD UP $1.30 (AND WAY UP BEFORE THE BANKERS WHACKED) WE WITNESSED ANOTHER 1.95 TONNES OF PAPER GOLD ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 801.98 TONNES

JUNE 24/WITH GOLD UP $18.00 A MONSTROUS PAPER DEPOSIT OF 34.93 TONNES/INVENTORY RESTS AT 799.03 TONNES

JUNE 21/WITH GOLD UP $ 2.90, NO CHANGE IN GOLD INVENTORY: INVENTORY RESTS AT: 764.10 TONNES

June 20/WITH GOLD UP $47.95, NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 19 WITH GOLD DOWN $1.65: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONES

JUNE 18/JUNE 18/WITH GOLD UP $7.60: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 17/WITH GOLD DOWN $1.65 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 764.10 TONNES

JUNE 14/ WITH GOLD UP $1.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.40 TONNES OF PAPER GOLD INTO THE GLD///INVENTORY RESTS AT 764.10 TONNES

june 13/WITH GOLD UP $6.60 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 759.70 TONNES

JUNE 12/WITH GOLD UP $7.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 756.18 TONNES

JUNE 11/WITH GOLD UP $1.65 CENTS TODAY: A TINY CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .24 TONNES AND THIS IS TO PAY FOR FEES/INVENTORY RESTS AT 756.18 TONNES

JUNE 10/WITH GOLD DOWN $16.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES/INVENTORY RESTS AT 756.42 TONNES

june 7/WITH GOLD UP $3.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

jUNE 6/WITH GOLD UP $8.40 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 5 WITH GOLD UP $6.00 TODAY/STRANGE: A WITHDRAWAL OF 2.06 TONNES FROM THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 4/WITH GOLD UP 0.85 TODAY: A MONSTROUS PAPER GAIN OF 16.44 TONNES/GLD INVENTORY RESTS AT 759.65 TONNES

JUNE 3/WITH GOLD UP $17.50 TODAY: ANOTHER BIG CHANGE, A DEPOSIT OF 2.35 TONNES OF GOLD INTO THE GLD//

MAY 31/WITH GOLD UP $17.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GLD INVENTORY RESTS AT 740.86 TONNES

MAY 30: WI6H GOLD UP $6.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES/INVENTORY RESTS AT 740.86 TONNES

MAY 29/WITH GOLD UP $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 737.34 TONNES

MAY 28/WITH GOLD DOWN $6.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD> A WITHDRAWAL OF 1.47 TONNES/INVENTORY RESTS AT 737.34 TONNES

MAY 24/WITH GOLD DOWN $1.60 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 738.81 TONNES

MAY 23/WITH GOLD UP $11.10 TODAY: A STRANGE WITHDRAWAL OF .88 TONNES FORM THE GLD/INVENTORY RESTS AT 738,81 TONNES

MAY 22//WITH GOLD FLAT TODAY: WE HAD A GOOD 1.52 TONNES OF GOLD DEPOSIT INTO THE GLD/INVENTORY RESTS TONIGHT AT 739.69 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JULY 5/2019/ Inventory rests tonight at 798.44 tonnes

*IN LAST 620 TRADING DAYS: 136.32 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 520 TRADING DAYS: A NET 29.36 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JULY 5/WITH SILVER DOWN 32 CENTS WE STRANGELY HAD A HUGE INVENTORY GAIN OF 2,234 MILLION OZ//INVENTORY RESTS AT 328.492 MILLION OZ

JULY 3 WITH SILVER UP 10 CENTS A HUGE INCREASE IN INVENTORY..INVENTORY RESTS AT 326.151 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 323.330 MILLION OZ//

JULY 1/ WITH SILVER DOWN 16 CENTS: A SURPRISING DEPOSIT OF 936,000 OZ INTO THE SLV/INVENTORY RESTS TONIGHT AT 323.330 MILLION OZ/

JUNE 28/WITH SILVER UP 6 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.394 MILLION OZ//

JUNE 27/WITH SILVER DOWN 7 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.575 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.394 MILLION OZ//

JUNE 26/WITH SILVER UP 17 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 25/WITH SILVER DOWN 25 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ.

JUNE 24/WITH SILVER UP 11 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 21/WITH SILVER DOWN 22 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 20/WITH SILVER UP 53 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 19/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ/

JUNE 18 WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ

JUNE 17/WITH SILVER UP XXX CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ//

JUNE 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 12/WITH SILVER UP 4 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.413 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 11/WITH SILVER UP 10 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 10/WITH SILVER DOWN 38 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 7/WITH SILVER UP ANOTHER 12 CENTS, NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 6/WITH SILVER UP ANOTHER 9 CENTS TODAY: A FAIR SIZE DEPOSIT OF 630,087 OZ//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 5/WITH SILVER UP 4 CENTS TODAY: A HUGE PAPER DEPOSIT OF 2.396 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 314.434 MILLION OZ//

JUNE 4/WITH SILVER UP 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

JUNE 3/WITH SILVER UP 19 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

MAY 31/WITH SILVER UP 6 CENTS TODAY: A DEPOSIT OF 422,000 OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 312.038 MILLION OZ/

May 30/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ///

MAY 29/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 28/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 24/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ/

MAY 23/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 22/WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 311.616 MILLION OZ

MAY 21: WITH SILVER DOWN 3 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV; A WITHDRAWAL OF 750,000 OZ///INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 20/WITH SILVER UP 6 CENTS:NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.366 MILLION OZ

JULY 5/2019:

Inventory 328.492 MILLION OZ

ii) Physical stories courtesy of GATA/Chris Powell

this will lead to increased smuggling

(courtesy India Express/GATA)

INDIA EXPRESS

India raises taxes on Gold for the first time in six years

The import tax on gold and other precious metals will be raised to 12.5% from 10%, Finance minister Nirmala Sitharaman said while presenting the federal budget for the year through March 31, 2020.

July 5, 2019 3:19:00 pm

India raises taxes on Gold for the first time in six years

India, the world’s biggest consumer of gold after China, increased the import tax on the precious metal for the first time since 2013, spurring domestic prices to a record. Shares of jewelers slumped.

The import tax on gold and other precious metals will be raised to 12.5% from 10%, Finance minister Nirmala Sitharaman said while presenting the federal budget for the year through March 31, 2020. India, which imports almost all of its gold, raised the tax thrice in 2013 to control a record current-account deficit.

India’s consumption of gold has been affected by the government’s efforts to curb its trade deficit and measures to discourage investors who used the metal to evade taxes. The high duties have spurred a spate of smuggling, including attempts to bring in bullion via planes and trains. Domestic prices have tracked a surge in overseas spot gold and further increases would imperil demand during the festival and peak wedding season running from August to December.

Benchmark gold futures in Mumbai rose as much as 2.6% Friday to 35,100 rupees per 10 grams ($512), while overseas gold was little changed. Shares of Titan Co., India’s largest maker of branded jewelry by market value, slumped as much as 3.2%, while Tribhovandas Bhimji Zaveri Ltd. slid as much as 6.6%.

India’s Cash Crackdown Hits Gold Pawners

The high import tax has led to a thriving grey market for gold in India and it “needs to be obliterated” for broader reforms to take effect, P.R. Somasundaram, managing director for India at the World Gold Council, said last month.

The tax increase may discourage buyers and demand in the physical market may slide by 10% this year from 760 tons in 2018, according to the All India Gems & Jewellery Domestic Council. The association will request the government to roll back the duty, he said.

“This is very unfortunate and disappointing,” Chairman Anantha Padmanaban said by phone. “We were expecting a cut in customs duty and this came as a surprise and a shock. This is going to encourage a lot of smuggling.”

-END-

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

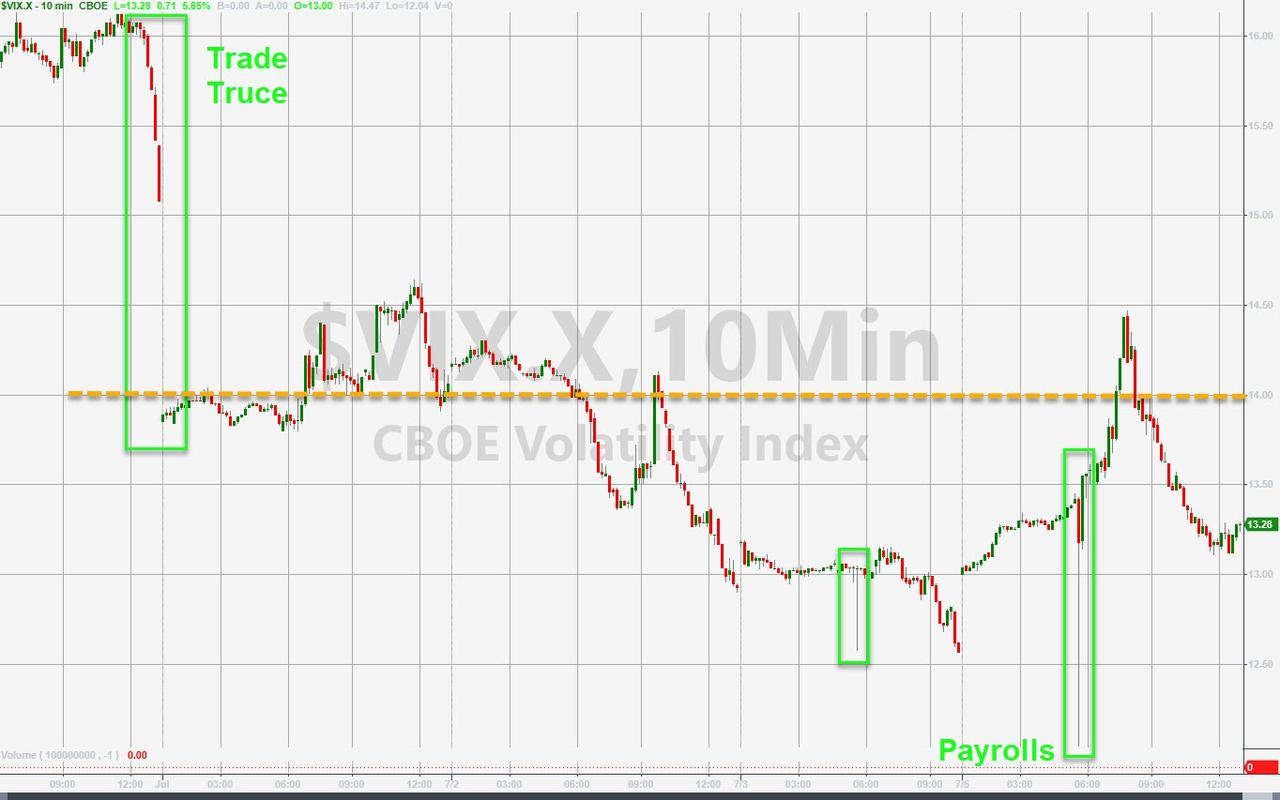

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.8694/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.8759 /shanghai bourse CLOSED UP 14.86 POINTS OR 0.50%

HANG SANG CLOSED DOWN 204.22 POINTS OR 0.95%

2. Nikkei closed DOWN 204.22 POINTS OR 0.95%

3. Europe stocks OPENED ALL GREEN EXCEPT GERMAN DAX/

USA dollar index UP TO 96.66/Euro RISES TO 1.1307

3b Japan 10 year bond yield: FALLS TO. –.16/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107/51/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 57.82 and Brent: 65/36

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

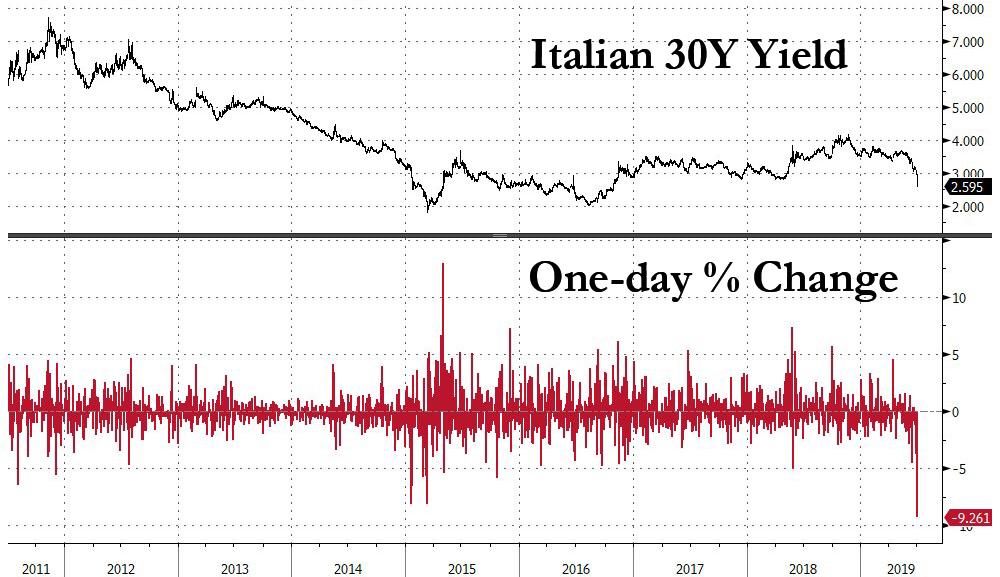

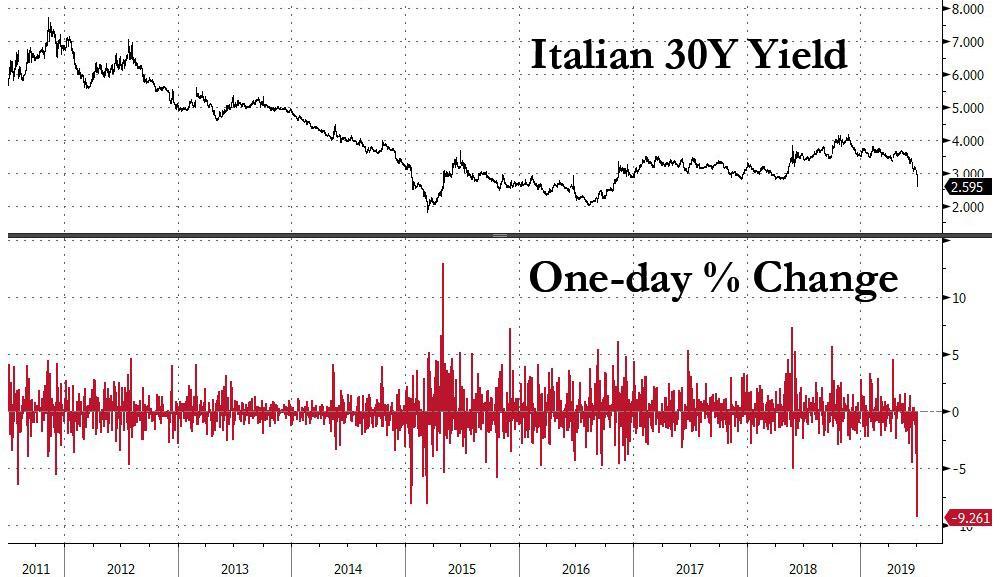

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO -.30%/Italian 10 yr bond yield UP to 2.12% /SPAIN 10 YR BOND YIELD UP TO 0.42%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.52: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.55

3k Gold at $1393.90 silver at: 14.32 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 51/100 in roubles/dollar) 63.37

3m oil into the 57 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.51 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9824 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1108 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISING to –0.30%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

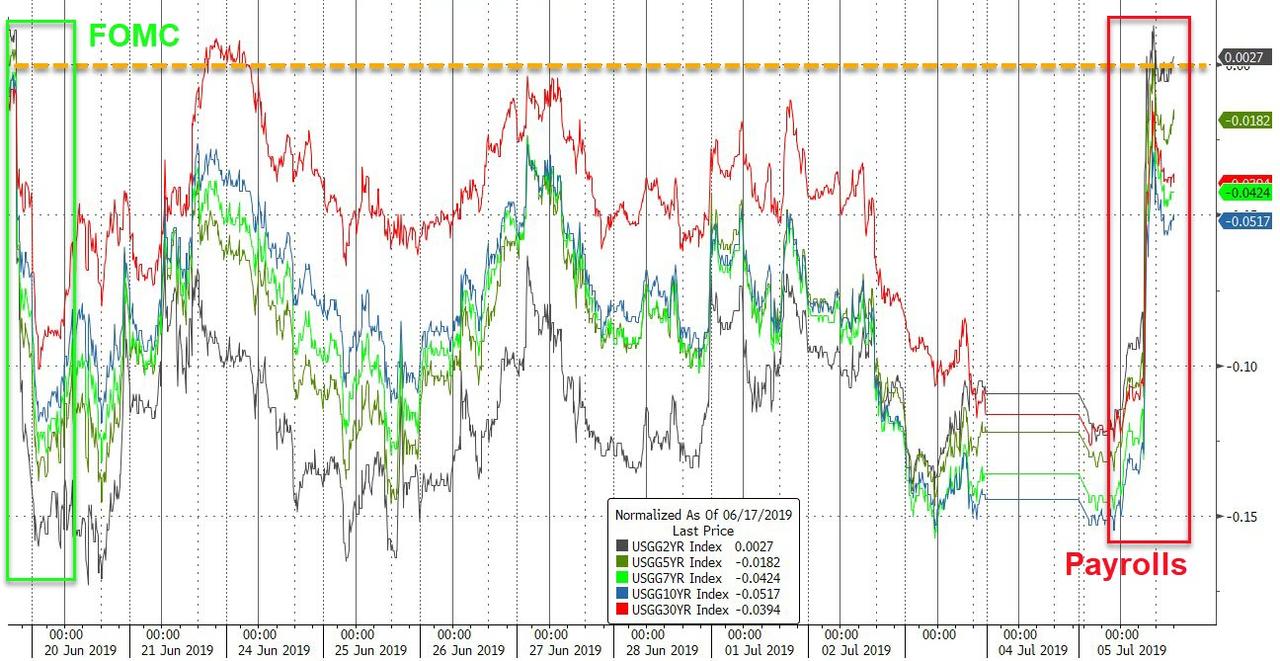

4. USA 10 year treasury bond at 2.03% early this morning. Thirty year rate at 2.54%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.8080..

Futures Slide Ahead Of Payrolls, Europe Red After “Devastating” German New Orders

Amid non-existent volumes as many US traders are taking an extended holiday weekend, this week’s rally fizzled with global markets and US equity futures drifting into the red ahead of today’s U.S. jobs data which could either boost or temper market expectations about aggressive policy easing by the Federal Reserve.

European bourses suffered with the pan-region STOXX 600 slipping 0.3%, dragged lower by the basic resource and industrial goods & services sectors which both fell more than 1.5%. A sharp drop in China iron ore futures hit miners. Tech shares retreated 0.9% after Samsung’s dour forecast showed the impact of U.S.-China trade war on global chip and smartphone markets, sending Infineon, STMicroelectronics and Siltronic as much as 1.5% lower.

Losses accelerated after the latest German data showed Europe’s largest economy was still stuck in pre-recessionary limbo with industrial orders falling far more than expected in May, and a warning from the economy ministry this sector of Europe’s largest economy was likely to remain weak in the coming months.

“Devastating new orders data just undermined any hopes for an industrial rebound. We are starting to lose our optimism,” said Carsten Brzeski, chief economist at ING Germany. “Combined with the weakest June performance of the labour market since 2002 and disappointing retail sales, today’s new orders wrap up a week to forget for the German economy. The fear factor is back.”

Europe’s losses followed gains in Asia, where MSCI’s index of Asia-Pacific shares ex-Japan was set for its fifth straight weekly rise. S&P futures and Shanghai Composite index both hovered near 3,000-mark in muted post-holiday trade. Asian stocks traded sideways, heading for the fifth week of gains, their longest winning streak since January 2018, as traders assessed India’s federal budget and awaited U.S. payroll data. Consumer staples companies rallied, countering declines in material firms. Markets in the region were mixed, with Australia climbing and India dropping. The Topix gauge closed 0.2% higher, capping its best week since January, as electronics makers offered the biggest boost. The Shanghai Composite Index gained 0.2%, driven by Kweichow Moutai and China Life Insurance. Chinese equities should post gains this quarter despite uncertainty over trade disputes, according to a Bloomberg survey of analysts and fund managers.

The S&P BSE Sensex Index fell 1% as a lack of stimulus from the government in its annual spending plan unveiled Friday and additional tax on high income spooked investors. Meanwhile, jewelers tumbled after the government announced a proposal to raise import tax on gold to 12.5% from 10%. Shares of Indian shadow lenders rose after Finance Minister Nirmala Sitharaman proposed to provide a partial guarantee to state-run banks with exposure to pooled assets of financially-sound non-bank lenders.

A rebound in emerging-market stocks and currencies paused as ahead of the June payrolls report. The MSCI Emerging Markets Index fell on Friday, still heading for its sixth week of gains, the longest winning streak in five months. The currency gauge was little changed for the week, with currencies in Latin America largely outperforming those in eastern Europe and Asia. The risk premium on sovereign dollar bonds narrowed.

“Following the strong performance more recently, markets are looking for what next,” said Trieu Pham, a London-based strategist at ING Bank NV. “U.S. job market data will certainly be closely watched in view of the July 31 Fed meeting. Lastly, a bit of caution as well as the trade truce is holding but the matter is far from resolved.”

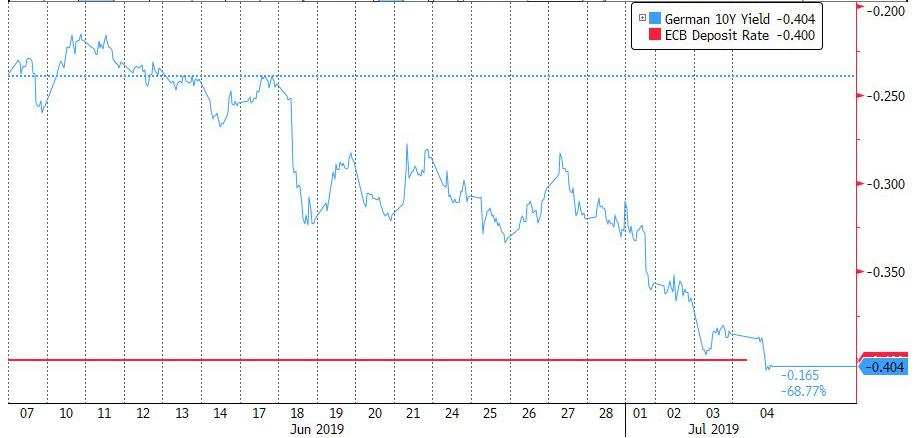

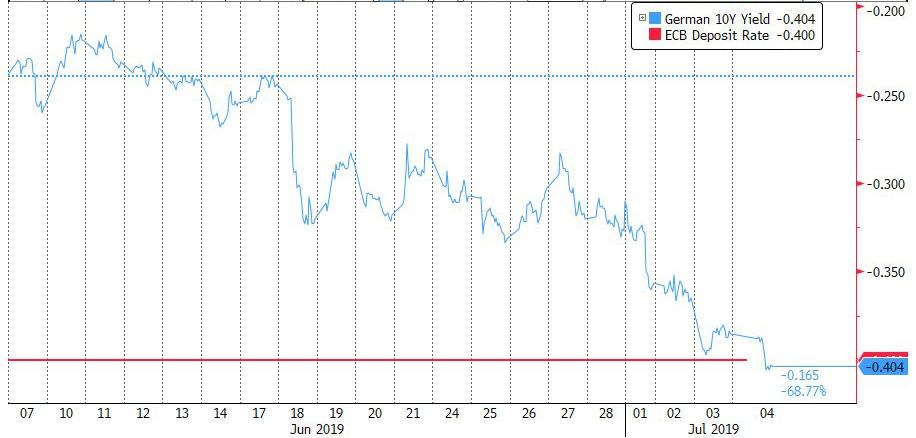

In rates, Treasury futures dipped, lifting the 10-year yield fractionally to 1.958% after hitting the lowest since November 2016 at 1.941%; Aussie curve little changed. JGB futures edge higher, supported by buying in ultra long-end, despite strongest Japanese spending pace in four years. Germany’s 10-year government bund yield, fell to minus 0.4% and breached the European Central Bank’s deposit rate for the first time – a level analysts say acts as a psychological barrier even though shorter-dated German bond yields trade well below it.

World stocks and bonds have rallied at a feverish pace since the start of June on hopes global central banks will keep policy easy to support growth. A ceasefire in the protracted Sino-U.S. trade war has also bolstered sentiment.

All eyes were now on U.S. non-farm payrolls – which we previewed earlier – due later in the day, and which are expected to have jumped by 160,000 in June compared with 75,000 in May.

“This will be the last employment report before the FOMC meeting at the end of this month for which markets are pricing in 33 basis points of cuts as of this morning,” Deutsche Bank’s Craig Nicol wrote in a note to clients. Fed futures are fully pricing in a 25-basis-point cut when the Fed meets on July 30-31. Investors also see a 25% chance of a 50-basis-point reduction.

“What today’s report says about the trends in hiring and income growth could meaningfully impact market expectations so expect there to be just as much focus on hours and wages as the headline payrolls reading.”

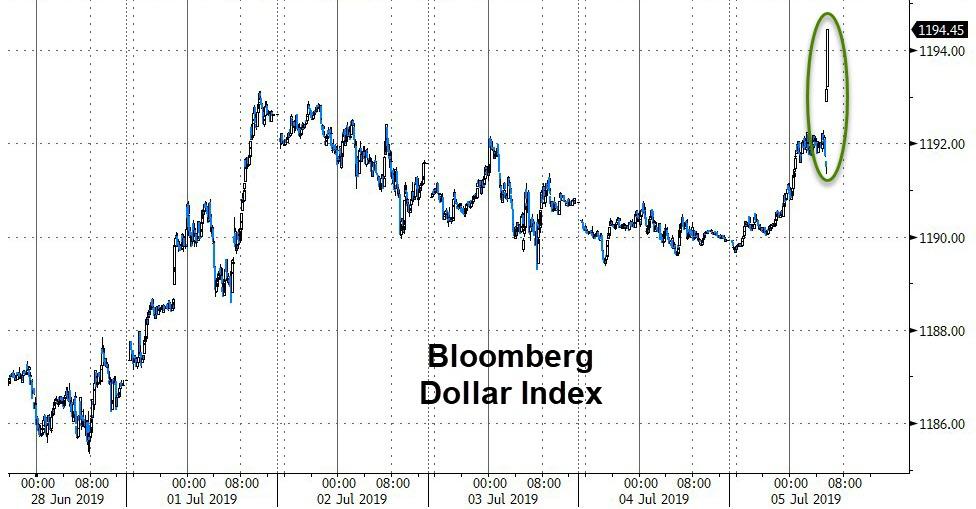

In FX, the easing bund yields dragged the euro lower to $1.1273 with the common currency on track for the biggest weekly drop in three weeks. The Bloomberg dollar index beat its Group-of-10 peers amid thin flows ahead of Friday’s U.S. labor data, which could signal whether the Fed will cut interest rates this month; it was on track for a ~1% gain this week. Against the Japanese yen the dollar gained 0.2% to 108.04.

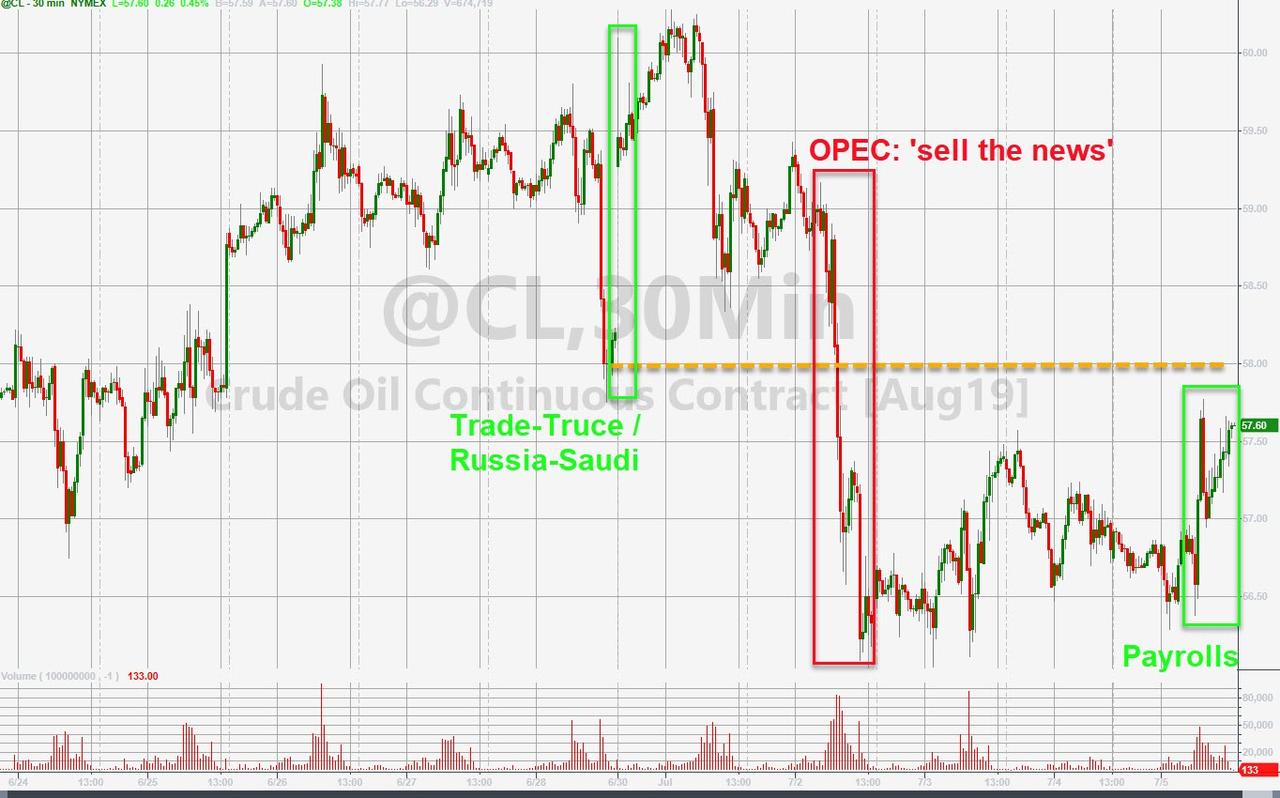

Worries about the health of the global economy also weighed on commodity markets. Oil prices eased with Brent crude futures , the international benchmark for oil prices, off 30 cents at $63.00 per barrel while U.S. crude slipped 85 cents to $56.49. Crude markets shrugging off tensions around Iran and a decision by OPEC and its allies to extend a supply cut deal until next year was an ominous sign to market watchers.

“When bullish signals fail to lift the oil market’s spirits, we should be very concerned this downtrend could run much further than expected,” said Stephen Innes, managing partner at Vanguard Markets.

Bitcoin rebounded from a loss on Thursday, while China iron ore futures racked up sharp losses after hitting a record on Wednesday. China’s most-active September iron ore contract on the Dalian Commodity Exchange fell as much as 4.9% to 838 yuan ($121.89) a tonne.

Market Snapshot

- S&P 500 futures down 0.09% to 2,997.50

- STOXX Europe 600 down 0.3% to 391.97

- MXAP down 0.04% to 162.18

- MXAPJ down 0.08% to 532.39

- Nikkei up 0.2% to 21,746.38

- Topix up 0.2% to 1,592.58

- Hang Seng Index down 0.07% to 28,774.83

- Shanghai Composite up 0.2% to 3,011.06

- Sensex down 0.6% to 39,666.60

- Australia S&P/ASX 200 up 0.5% to 6,751.28

- Kospi up 0.09% to 2,110.59

- German 10Y yield rose 0.3 bps to -0.396%

- Euro down 0.2% to $1.1265

- Brent Futures up 0.1% to $63.38/bbl

- Italian 10Y yield rose 9.0 bps to 1.322%

- Spanish 10Y yield rose 0.5 bps to 0.253%

- Brent Futures up 0.1% to $63.38/bbl

- Gold spot down 0.1% to $1,414.14

- U.S. Dollar Index up 0.1% to 96.91

Top Overnight News from Bloomberg

- China continues to stress that the U.S. must remove all the tariffs placed on Chinese goods as a condition for reaching a trade deal. On Friday, an influential blog connected to state media said the talks will “go backward again” without that step, echoing the line from Ministry of Commerce’s weekly briefing on Thursday

- German factory orders slumped in May as trade uncertainty continued to weigh on global manufacturers and drive a slowdown in Europe’s largest economy. The continued gloom is pushing a growing number of economists to predict the ECB will add more monetary stimulus as soon as this month

- Deutsche Bank AG’s job cuts across the U.S. will probably go far beyond equities and interest-rate derivatives trading, which have been marked as major targets, according to people with knowledge of the matter

- Investors are so keen to find a safe home for their cash that they’re paying the German government to take it, and that makes the nation’s reluctance to borrow increasingly puzzling. Yields are now below zero for 85% of German sovereign debt, right out to bonds that don’t mature for another 20 years

- Boris Johnson, the front-runner to replace Theresa May as British prime minister, said delivering Brexit would be key to keeping the U.K. together, just hours after May warned her successor not to put the union at risk with a no-deal Brexit

Asian equity markets were mixed following the non-existent lead from Wall Street where markets were shut due to Independence Day and with the region tentative heading into the key US Non-Farm Payrolls data. ASX 200 (+0.5%) was positive with the index led higher by strength in financials and real estate after APRA effectively relaxed guidance on mortgage lending in which banks will be able to review and set their own minimum rate floor in assessing serviceability, although gains were capped for most the session by weakness in the commodity-related sectors. Elsewhere, Nikkei 225 (+0.2%) was choppy as it failed to find inspiration from the highest growth in Household Spending since 2015, due to a humdrum tone in the currency and the KOSPI (+0.1%) traded cautious amid losses in index heavyweight Samsung Electronics which beat expectations in its preliminary earnings for Q2 but still showed oper. profit slipped by 56% Y/Y. Elsewhere, Hang Seng (U/C) and Shanghai Comp. (+0.2%) were initially subdued after further PBoC inaction resulted to a net weekly liquidity drain of CNY 340bln, while there were also recent mixed comments from China’s MOFCOM which confirmed US-China trade teams are in communication but also suggested that tariffs must be removed for a trade deal to occur. Finally, 10yr JGBs were marginally higher and briefly reclaimed the 154.00 level with mild support seen amid the lacklustre risk tone in Japan and BoJ’s presence in the market for JPY 555bln of JGBs.

Top Asian News

- India to Narrow Budget Gap Target, Sell First Global Bond

- India Sees Economy Rebounding This Year as Growth Risks Balanced

- India to Inject Another $10.2 Billion Into State-Run Banks

- Call Center Nation to Lose Shine on Duterte’s Manila Ecozone Ban

European indices are little changed/modestly into negative territory this morning [Euro Stoxx 50 -0.2%] as bourses lack any firm direction due to the US market holiday and the relatively quiet newsflow ahead of the US Jobs Report later on in the session. Sectors are largely negative, with some underperformance seen in tech names as Samsung Electronics reported earnings last night where Q2 operating profit fell by 56% Y/Y. Separately, mining names are suffering on the pullback in iron ore prices and amidst reports that Chinese regulators are to examine the drivers behind the metal’s recent price surge; as such, Rio Tinto (-2.4%) and Anglo American (-2.6%) are towards the bottom of the Stoxx 600. Elsewhere, at the bottom of the Stoxx 600 are Hexagon (-14.0%) after the Co. stated that they have been impacted due to a China slowdown in July, stemming from the ongoing US-China trade dispute. Finally, Osram Licht (+1.8%) are firmer this morning after confirming that they support the Bain & Carlyle takeover for EUR 35.00 per share.

Top European News

- Brevan Howard Main Hedge Fund Posts Best First Half in a Decade

- German Factory Orders Slump as Europe Economic Slowdown Worsens

- South African Stocks Fall as Iron Ore Producers, Aspen Slump

- Euro Hopeful Croatia Sets Sights on Adoption as Early as 2023

- Saudi Arabia, Kuwait Make Breakthrough in Neutral Zone Oil Talks

In FX, the Dollar is edging higher ahead of US jobs data, albeit not independently or directly as G10 and EM rivals weaken further or retreat in advance of the big release. The DXY has inched back up towards 97.000 and into a marginally firmer range, but may be capped by resistance seen between the big figure and 97.010 awaiting the latest BLS report and return of US markets after yesterday’s market holiday.

- CHF/NZD – The major underperformers, though not by much, as the Franc and Kiwi hover around 0.9875 and 0.6670 respectively vs the Greenback and both still within recent trading parameters awaiting further direction from the aforementioned NFP metrics.

- JPY/EUR/SEK – The Yen has slipped back to around 108.00 from safe-haven highs circa 107.50 earlier this week, but may derive some support from decent option expiry interest at the 108.00 strike (1 bn), or heavy supply said to be stacked from 108.50 if the US labour data is strong. Meanwhile, the single currency is testing key downside technical levels in wake of yet more poor German data, like converged DMAs and a Fib in the 1.1259-62 region, but outpacing the Swedish Krona amidst a sharp slide in Hexagon shares (due to the IT firm flagging weakness in China). Indeed, Eur/Sek has rebounded firmly from sub-10.5000 levels towards 10.5500.

- AUD/CAD/GBP – The Aussie is holding up better than its G10 peers and forming base above 0.7000/1.0500 vs the Usd and Nzd as post-RBA short covering continues, while the Loonie has lost some ground after a trade data-related boost as the focus switches to Canadian jobs data alongside NFP. However, Usd/Cad remains closer to weekly lows between 1.3045-70, and Cable is also nearer the bottom end of a 1.2550-87 range after this week’s bleak UK PMIs and further survey evidence of Brexit uncertainty weighing on the economy (BDO retail activity weak and IoD business morale worse).

In commodities, WTI and Brent futures have lost some ground in early trade, but have recently picked back up with the former just below the USD 57.00/bbl mark whilst the latter is around the USD 63.50/bbl mark. While newsflow remains light, it’s worth keeping in mind that WTI prices did not settle yesterday amid the US Independence Day holiday, thus a divergence in prices is observed. Elsewhere, gold is tentative, as usually the case in the run-up to NFP data with the yellow metal still above the USD 1300/oz level, having traded in a wide weekly 1382-1437 range. Meanwhile, copper prices are heading for the first weekly drop in a month as the red metal is pressured by a sluggish demand outlook and an increase in supplies. Finally, Dalian iron ore futures fell over 7% after China Iron & Steel Association urged the government to maintain order amid rising iron ore prices and wants prices to return to a reasonable level, while it was also reported that China regulators are to examine the drivers for the increase in iron ore prices. China Iron & Steel Association urged the government to maintain order amid rising iron ore prices and wants prices to return to a reasonable level, while it was also reported that China regulators are to examine the drivers for the increase in iron ore prices.

US Event Calendar

- 8:30am: Change in Nonfarm Payrolls, est. 160,000, prior 75,000

- 8:30am: Change in Private Payrolls, est. 150,000, prior 90,000

- 8:30am: Change in Manufact. Payrolls, est. 3,000, prior 3,000

- 8:30am: Unemployment Rate, est. 3.6%, prior 3.6%

- 8:30am: Average Hourly Earnings MoM, est. 0.3%, prior 0.2%; YoY, est. 3.2%, prior 3.1%

- 8:30am: Average Weekly Hours All Employees, est. 34.4, prior 34.4

- 8:30am: Underemployment Rate, prior 7.1%

DB’s Jim Reid concludes the overnight wrap

It may have lost some steam but no prizes for guessing what happened to core bond yields yesterday. On an unsurprisingly light day for news it was yet another move lower for yields outside of the periphery which was the only real talking point here in Europe however before we get to that let’s look forward as we’ve got a much anticipated US employment report due out this afternoon.

Indeed, this will be the last employment report before the FOMC meeting at the end of this month for which markets are pricing in 33bps of cuts as of this morning. As our economists noted in their preview, what today’s report says about the trends in hiring and income growth could meaningfully impact market expectations so expect there to be just as much focus on hours and wages as the headline payrolls reading.

In terms of expectations both our economists and the consensus peg payrolls at 160k. As a reminder, the May print was a much softer than expected 75k which dragged down the three-month trailing average to 151k. Our colleagues note that from the Fed’s perspective, the year-over-year trend in private employment is more important as this needs to outpace the trend in labor force growth in order to keep downward pressure on the unemployment rate. As Cleveland Fed President Mester reminded us recently, monthly payroll gains in the 75k – 120k range would still be consistent with the underlying trend in overall output growth. As for the rest of the report, the consensus expects the unemployment rate to hold steady at 3.6%, earnings to rise +0.3% mom and hours to hold at 34.4. Our economists also expect earnings to rise +0.3% which should result in a one-tenth increase in the year-over-year rate to +3.2%, however they do expect hours to tick up to 34.5. All that to look forward to at 1.30pm BST.

Back to markets where, as mentioned at the top, it was the move lower for bond yields which got the most attention on an otherwise quiet day. The headline grabber was 10y Bunds falling below the ECB deposit rate for the first time ever. They eventually closed at -0.402% which was -1.3bps on the day and the sixth successive day that yields have dropped. In fact, out of the 45 trading days back to May 3rd, 10y Bund yields have fallen on 32 of those days. The most that we can find over 45 days based on data back to 1991 is 34 days that yields have dropped so this is up there with the most days ever over a 45-day run. Similar maturity yields in France (-2.9bps) and Netherlands (-1.8bps) also nudged lower while Gilts fell -1.5bps. The exception was the periphery where BTPs rose +9.0bps. There wasn’t any specific news and instead it just appeared to be a bit of profit taking following a six-day rally which had seen yields fall -57.6bps. Also tentatively bucking the trend was the EUR 5y5y inflation swap which rose 1.9bps to 1.160%. Meanwhile, equity markets were open however there really wasn’t much to report with the STOXX 600 rising +0.09% in an intraday range of just 0.25%.

Anyway, yesterday’s bond moves mean the Bund curve is now negative at all maturities out to 2040. In fact, we count 49 outstanding Bunds with a maturity of at least 12 months and all but 4 now have a negative yield. That’s around 90% by market value which is fairly staggering. Across Europe we’ve now got negative 2y and 5y yields in 17 different countries. At the 10y maturity we’ve got negative yields in 9 different countries including Switzerland, Germany, Denmark, Netherlands, Austria, Finland, France, Belgium and Sweden. To be fair Slovakia, Ireland, Slovenia and Latvia are within a sneeze of dropping into negative territory too. For 30y bonds it’s still only Switzerland which has a negative yield with Germany (0.194%) and Netherlands (0.204%) the closest after that. If you were also wondering what the longest dated government bond was yielding in Europe, well the Austrian 2117 bond – with 98 years to maturity – is now down to 1.061%. The duration on that is fairly eye watering at 52.7 and at a cash price now of 163.2, the bond is up nearly 47pts this year alone. Anyway, when it was all said and done the global stack of negative yielding debt held at the record high of $13.4tn yesterday.

Of course, JGBs are a big part of the global negative yielding debt stack too with yields negative at all maturities out to 2033. This morning 10y JGBs are little changed at -0.165% and the Treasury market has reopened with 10y yields down a modest -0.7bps to 1.943%. There’s not much movement in equity markets this morning either with the Nikkei flat and Hang Seng (+0.08%), Kospi (-0.04%) and Shanghai Comp (-0.18%) all failing to move with much conviction. That said futures on the S&P 500 have crept over the 3,000 level this morning which suggests we could be in for a record start on Wall Street. Elsewhere, news that British military forces had seized a supertanker near Gibraltar carrying Iranian oil to Syria in violation of sanctions against the country hasn’t caused much of a reaction in the oil market with WTI actually down -1.01% as we go to print.

In other news, the South China Morning Post reported last night that US trade negotiators will be in China next week to restart trade discussions. The report also suggested that China has still not confirmed to the US that it would immediately restart soybean purchases with China wanting clarity on how President Trump would ease sanctions on Huawei. It goes on to say that US officials are still debating between extending a 90-day reprieve on the export ban beyond August 13 or establishing a special approval process for Huawei and that the White House may elaborate in “next couple of days” on conditions for lifting export restrictions.

In other news, while it was a very quiet session yesterday we did hear from one of the ECB Governing Council members. Indeed Rehn told Boersen-Zeitung that “growth in the euro area has slowed significantly recently” and that “we cannot deny that there are doubts among market participants and the public about the ability of the central bank to achieve the price stability target”. He added “we have a number of instruments which are very effective and which, as a package, have even greater effects than isolated”. Perhaps most significant was his reference “if we really want to live up to our mandate, further monetary stimulus is now needed until there is improvement in economic and inflation prospects”. All-in-all the tone leant dovish and followed a similar rhetoric from Lane earlier this week.

As for data, it was very quiet with weak May retail sales numbers for the Euro Area (-0.3% mom vs. +0.3% expected) and a further decline in new car registrations in the UK in June (-4.9% yoy) the only readings of any substance.

Finally, the day ahead will be dominated by the aforementioned June employment report in the US this afternoon. Prior to that the only data due out this morning in Europe is the May factory orders reading in Germany and May trade balance reading in France. Away from that the ECB’s Guindos is due to make comments at a conference in Madrid.

3A/ASIAN AFFAIRS

I)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 14.86 POINTS OR 0.50% //Hang Sang CLOSED DOWN 76.72 POINTS OR 0.27% /The Nikkei closed DOWN 204.22 POINTS OR 0.25%//Australia’s all ordinaires CLOSED DOWN .50%

/Chinese yuan (ONSHORE) closed DOWN at 6.8694 /Oil UP TO 57.82 dollars per barrel for WTI and 65.36 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.8694 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8759 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

SOUTH KOREA/JAPAN

A new feud is breaking out between South Korea and Japan. South Korea wants to be compensated for war time labour

(zerohedge)

Global Chip Supply In Jeopardy As New Trade Feud Erupts Between Japan And South Korea

The US trade war with China may have entered a tentative truce period, but a brand new, emerging trade feud threatens to jeopardize an entirely new universe of technological supply chains.

On Tuesday, Japan unexpectedly announced that it was considering imposing stricter export controls on more items bound for South Korea, in an apparent effort to raise pressure on Seoul to help resolve a bilateral dispute over compensation for wartime labor. The envisaged plan comes in response to what Tokyo views as Seoul’s failure to address the months-long dispute properly and prevent it from hurting mutual trust between the two neighbors.

Expanding the list of items, possibly to include electronic parts and related materials that can be diverted to military use, will likely exacerbate bilateral tensions, according to the Japan Times, and some within the government remain cautious about taking further steps, even though Japan has already announced that effective today, it will require manufacturers to file applications when they export to South Korea three materials used in the production of semiconductors and displays for smartphones and TVs.

Prime Minister Shinzo Abe on Wednesday defended the government’s export controls.

“We cannot give the preferential treatment that has been afforded until now, as the other country has not kept its promise,” he said during a nationally televised debate with leaders of other political parties, a day before official campaigning begins for the July 21 Upper House election. “This does not go against WTO agreements at all.”

Meanwhile, Seoul, which regards the move as conflicting with the spirit of free trade, has threatened to launch a complaint against Japan at the World Trade Organization.

Commenting on the latest trade feud, the Nikkei warned that Japan’s new export controls on South Korea, a country that produces the bulk of the world’s memory chips, threaten a ripple effect that spreads beyond the two wary neighbors to electronics manufacturing globally, and could result in another semiconductor shockwave across the globe.

The restrictions mark the latest setback in a bilateral relationship between the two Pacific Rim nations, fraught with colonial-era grievances. The move prompted Seoul to say it was considering retaliatory measures and left chipmakers to confront an immediate supply challenge.

Adding to the complications, Japan’s government expects export reviews to take about three months. But South Korean chipmakers typically keep only one to two months’ worth of parts and materials in stock.

A source at chipmaker SK Hynix told Nikkei the company does not have three months of inventory. The chipmaker would have to halt production if it cannot procure necessary materials from Japan for that long, the source said. Top memory chip maker Samsung Electronics said it was assessing the situation, without elaborating.

The impact could spread worldwide.

South Korean players control 70% of the global market for dynamic random access memory and 50% for NAND flash memory. Samsung leads the global chip market by revenue, with SK Hynix in third. These chips go into devices such as Apple’s iPhone, rival models from Huawei Technologies, personal computers made by HP and Lenovo Group as well as televisions from Sony and Panasonic.

A representative at a major Japanese electrical equipment maker expressed concern that the new controls could backfire.

“If supplies of things like memory from South Korea are delayed and production of Apple’s iPhone falls [as a result], there could be an impact on our provision of parts,” the representative said.

Lesser-known Japanese companies hold leading market shares in the three restricted materials. Polyimides are used to make flexible organic light-emitting diode displays. The others are used in forming circuit patterns: resist – a coating substance – and etching gas. These companies include JSR, Showa Denko and Shin-Etsu Chemical – all of which are a third or more owned by foreign investors.

Japan also plans to remove South Korea by August from an export “whitelist” of 27 friendly countries that includes the U.S., Germany and France, meaning that shipments of products with potential military applications will require government approval. No country has ever been dropped from the list.

* * *

Tokyo cited a deteriorating relationship with Seoul as the reason for the controls, seemingly referring to a long-running dispute over compensation from Japanese companies to South Koreans for wartime labor.

The move follows Tokyo’s increase in inspections of some South Korean seafood that began last month, reportedly in retaliation for continued curbs on imports of food from areas affected by Japan’s 2011 Fukushima Daiichi nuclear disaster.

“It’s become difficult to manage exports based on a relationship of trust with South Korea,” Japanese Deputy Chief Cabinet Secretary Yasutoshi Nishimura told reporters Monday.

* * *

In response to the sudden trade aggression, South Korean Vice Foreign Minister Cho Sei-young summoned Japanese Ambassador Yasumasa Nakamine to demand that the export controls be removed. He expressed concern about the impact on South Korean industry and bilateral relations, and argued that the restrictions directly contradict Japan’s advocacy for “free and fair trade” at the Group of 20 summit in Osaka last week.

Cho said that the government would work with businesses to prepare countermeasures. South Korea’s Ministry of Trade, Industry and Energy also said it would respond with “appropriate measures,” including filing a complaint with the World Trade Organization.

“We’ll make this an opportunity to enhance South Korea’s technological capabilities,” industry Minister Sung Yun-mo said.

Experts differed on whether the new regulations are valid under WTO rules. “This is an area where Japan can make decisions on its own, so it’s probably not a violation,” said Keisuke Hanyuda, partner at Japan-based Deloitte Tohmatsu Consulting. But Yuka Fukunaga, a professor at Waseda University in Tokyo, argued that the curbs may violate WTO agreements, as they fall into a “gray area.”

Whether a quick ceasefire follows in the coming weeks, and whether the US trade war with China ends up in a deal, remains unclear, but should trade relations collapse between Japan and South Korea, two nations at the cutting edge of global semi and tech manufacturing, the consequences not only for global trade but for corporate profitability would be disastrous. And case in point, this just hit:

Yonhap News Agency

✔@YonhapNews

(URGENT) Samsung Electronics Q2 operating profit dips 56.3 pct to W6.5tln http://yna.kr/AEN20190705000800320 …

(URGENT) Samsung Electronics Q2 operating profit dips 56.3 pct to W6.5tln | Yonhap News Agency

en.yna.co.kr

end

b) REPORT ON JAPAN

3c China/Chinese affairs

Ceasefire Crumbles? China Won’t Buy American Soybeans Until Washington Provides ‘More Clarity’ On Huawei

Markets greeted President Trump and President Xi’s decision to re-start trade talks with jubilation. But as we’ve been saying from the beginning, this doesn’t mean a trade deal is a given – quite the opposite, actually.

That’s because Beijing and Washington have already begun to parrot some of their demands from before talks collapsed. And with Washington still unwilling to roll back all of the trade war tariffs, something that Beijing sees as non-negotiable, it could be a long time before the market gets the trade deal is so desperately seeks.

In the latest sign that suspicions among senior Chinese officials continue to simmer, and that the hastily cobbled G-20 ceasefire is suddenly on the rocks (again), the South China Morning Post reported on statements from a government spokesman and state-run media claiming that the commentary on Taoran Notes, a popular economic news source on the mainland, said Beijing would reneg on its promise to buy tons of agricultural goods from the US if Washington “flip flops” again, and that talks would “go backward again” unless Washington is willing to remove all trade-war tariffs.

“If the US flip-flops again in the negotiations, the promises to buy American agriculture products will also be overturned,” Taoran Notes said.

It added that China would have to consider its domestic demand and the opinions of domestic companies before buying US agricultural products.

SCMP’s sources confirmed that American negotiators would return to Beijing next week for what would be the 11th round of talks between the two sides since the trade spat first erupted more than one year ago.

If the issue of the US lifting its tariffs on Chinese goods can’t be resolved (which it almost certainly won’t be), talks could “break down immediately,” one source warned, leaving Washington to slap tariffs on another $300 billion+ of Chinese goods

If the negotiators are unable to resolve the issues, the talks could “break down immediately,” with Washington going ahead with new tariffs on US$300 billion of Chinese products, the source warned.

A Chinese source also confirmed that American negotiators would return to Beijing next week to iron out the details of what was discussed.

In any event, before moving ahead with promised purchases of American soybeans and other ag products, Beijing has been playing coy, insisting that they want to see Washington formally remove Huawei from the ‘blacklist’ as Trump promised.

Then, Gao Feng, the influential spokesman for the Chinese Ministry of Commerce, said a trade deal would be “impossible” without the complete removal of US sanctions˜on China.

On Thursday, Chinese Ministry of Commerce spokesman Gao Feng said a trade deal would only be possible if the US called off all tariffs on Chinese imports.

Such a move would require the Trump administration to give up its insistence that some levies remained in place to ensure Beijing honoured the deal. The US had argued that these levies should be lifted only when China made progress on certain agreed-to goals/