GOLD:$1445.70 UP $25.20(COMEX TO COMEX CLOSING)

Silver: $16.27 UP 10 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1440.00

silver: $16.32

YOUR DATA…

your data:

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 62/221

EXCHANGE: COMEX

CONTRACT: AUGUST 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,420.900000000 USD

INTENT DATE: 08/01/2019 DELIVERY DATE: 08/05/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 5

118 H MACQUARIE FUT 7

661 C JP MORGAN 62

686 C INTL FCSTONE 28 6

690 C ABN AMRO 88 21

737 C ADVANTAGE 59 11

800 C MAREX SPEC 25 2

880 H CITIGROUP 107

905 C ADM 21

____________________________________________________________________________________________

TOTAL: 221 221

MONTH TO DATE: 3,794

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 221 NOTICE(S) FOR 22100 OZ (0.6874 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 3794 NOTICES FOR 379400 OZ (11.800 TONNES)

SILVER

FOR AUGUST

66 NOTICE(S) FILED TODAY FOR 330,000 OZ/

total number of notices filed so far this month: 951 for 4,755,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

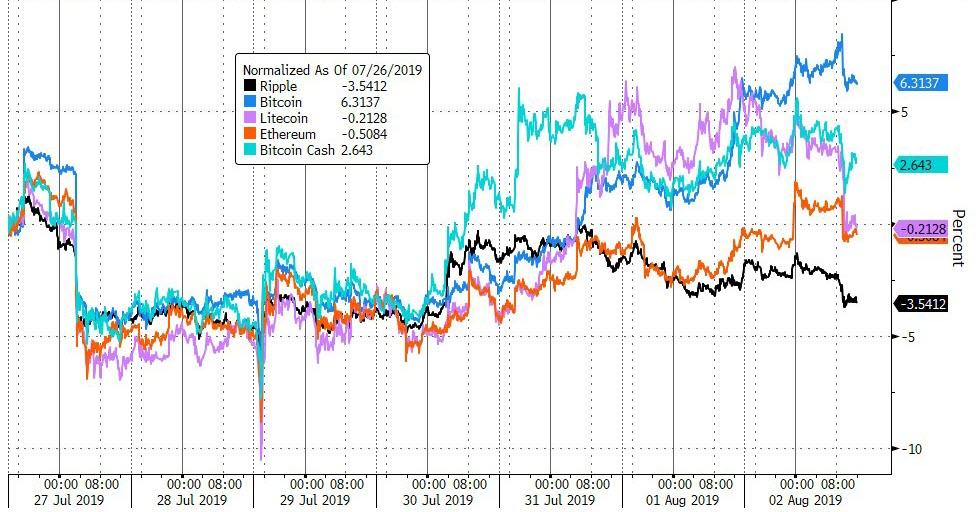

Bitcoin: OPENING MORNING TRADE : $ 10500 UP 129

Bitcoin: FINAL EVENING TRADE: $ 10500 UP 49

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A STRONG SIZED 1342 CONTRACTS FROM 236,226 UP TO 237,568 DESPITE THE 23 CENT LOSS IN SILVER PRICING AT THE COMEX. THE HUGE JUMP IN OI WILL OCCUR IN TOMORROW’S READING AS THE BIG PRICE GAIN OCCURRED AFTER THE COMEX HAD CLOSED.

TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JULY. 0 FOR AUGUST, 2487 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 2487 CONTRACTS. WITH THE TRANSFER OF 2487 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2487 EFP CONTRACTS TRANSLATES INTO 12.435 MILLION OZ ACCOMPANYING:

1.THE 23 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ INITIAL STANDING FOR JULY

WE HAD ATTEMPTED COVERING OF SHORTS AT THE SILVER COMEX LAST NIGHT WITH ZERO SUCCESS..AND ZERO SPREADING ACCUMULATION.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

3425 CONTRACTS (FOR 2 TRADING DAYS TOTAL 3425 CONTRACTS) OR 17.13 MILLION OZ: (AVERAGE PER DAY: 1713 CONTRACTS OR 8.565 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 17.13 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 2.447% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1350.36 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1342, DESPITE THE 23 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 2487 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A HUGE SIZED: 3829 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2487 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1342 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 23 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $16.33 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.181 BILLION OZ TO BE EXACT or 167% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 66 NOTICE(S) FOR 330,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ//AUGUST: 6.580 MILLION OZ//

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

IN GOLD, THE COMEX OPEN INTEREST ROSE BY AN ATMOSPHERIC AND CRIMINALLY SIZED 8,236 CONTRACTS, TO 572,320 DESPITE THE $4.90 PRICING LOSS WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING ACCUMULATION HAS NOW COMMENCED FOR SILVER..AS THE LIQUIDATION PHASE FOR COMEX OI GOLD HAS NOW STOPPED

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUMONGOUS SIZED 17,418 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 17,418 CONTRACTS, DEC> 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 572,320,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 25,654 CONTRACTS: 8,236 CONTRACTS INCREASED AT THE COMEX AND 17,418 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 25,654 CONTRACTS OR 2,565,400 OZ OR 79.79 TONNES. YESTERDAY WE HAD A LOSS OF $4.90 IN GOLD TRADING.…AND WITH THAT LOSS IN PRICE, WE HAD A GIGANTIC GAIN IN GOLD TONNAGE OF 79.79 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER. WE ARE NOW OUT OF THE LIQUIDATION PHASE IN GOLD AS WE MORPH INTO THE ACCUMULATION PHASE FOR SILVER. ALSO REMEMBER THAT WE DID NOT GET OUR BIG GAIN IN PRICE UNTIL AFTER THE COMEX CLOSED…SO EXPECT ANY HUGE GAIN IN TOTAL OI WITH MONDAY’S READING.

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF SEPTEMBER FOR SILVER.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF AUGUST BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST : 28,533 CONTRACTS OR 2,853,300 oz OR 88.74 TONNES (2 TRADING DAY AND THUS AVERAGING: 14,266 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY IN TONNES: 88.74 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 88.74/3550 x 100% TONNES =2.49% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 3600.01 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 58,236 DESPITE THE PRICING LOSS THAT GOLD UNDERTOOK YESTERDAY($4.90)) //.WE ALSO HAD A HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 17,418 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 17,418 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 25,654 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

17,418 CONTRACTS MOVE TO LONDON AND 8,236 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 79.79 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED DESPITE THE LOSS IN PRICE OF $4.90 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAVE NOW COMMENCED WITH SPREADING ACCUMULATION OF SILVER OI CONTRACTS AS WE HAVE ENTERED THE NON ACTIVE MONTH OF AUGUST.

we had: 221 notice(s) filed upon for 22,100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $25.20 TODAY//(COMEX-TO COMEX)

NO CHANGES IN GOLD INVENTORY AT THE GLD

INVENTORY RESTS AT 827.82 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 10 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV:

/INVENTORY RESTS AT 356.715 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A STRONG SIZED 1342 CONTRACTS from 236,266 UP TO 237,568 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF SPREADER OI IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JULY: 0 CONTRACTS FOR AUGUST: 0, FOR SEPT. 2487 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2487 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1342 CONTRACTS TO THE 2487 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUGE SIZED GAIN OF 3829 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 19.145 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.885 MILLION OZ AND AUGUST AT 6.580 MILLION OZ SO FAR.

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 23 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 2487 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 40.93 POINTS OR 1.041% //Hang Sang CLOSED DOWN 647.12 POINTS OR 2.35% /The Nikkei closed DOWN 647.12 POINTS OR 2.35%//Australia’s all ordinaires CLOSED DOWN .38%

/Chinese yuan (ONSHORE) closed DOWN at 6.9375 /Oil UP TO 55.31 dollars per barrel for WTI and 62.19 for Brent. Stocks in Europe OPENED ALL RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9375 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8636 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

Not good!! A trade war has opened up on a second front. This time it is powerhouse exporters Japan and South Korea going at it. Japan removes South Korea from its “white list” of preferential trade status

(zerohedge)

3C CHINA

i)Trump ignored Mnuchin’s advice to give China advance notice on the new tariffs to be implemented.

(zerohedge)

ii)The protests in Hong Kong… continue!! Citizens use lasers to disrupt facial recognition.

(zerohedge)

iii)CHINA/USA

4/EUROPEAN AFFAIRS

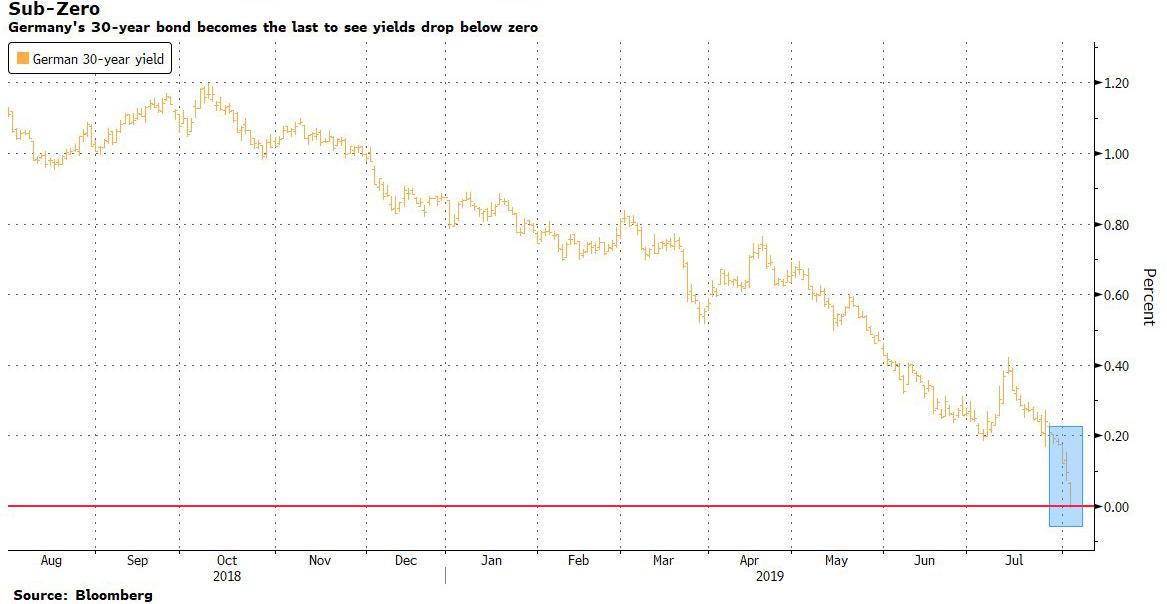

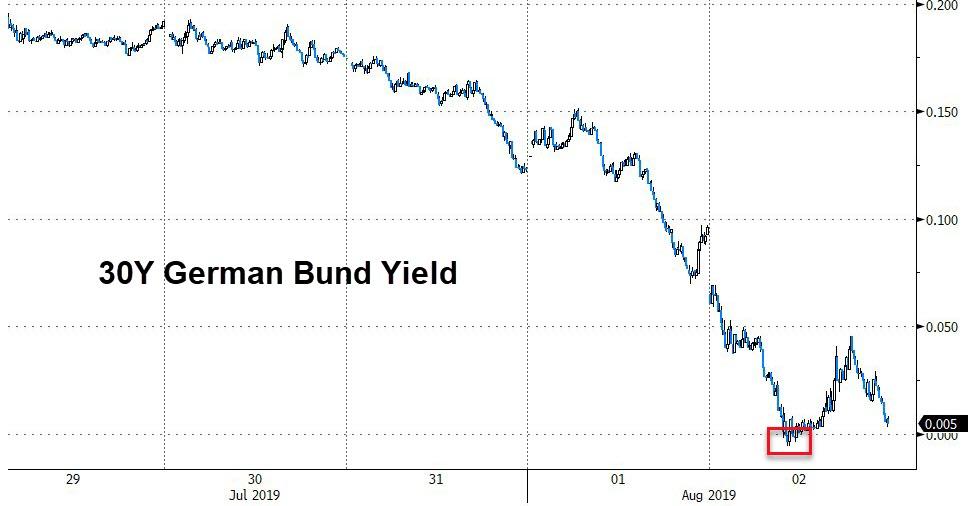

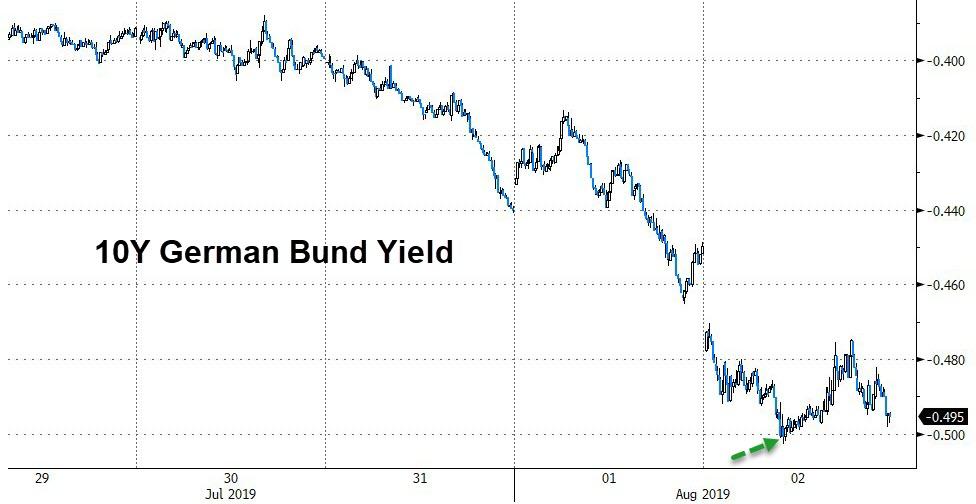

I)GERMANY

Deadly..the entire German curve is now below zero in interest rates. Draghi cannot buy any German debt

(zerohedge)

II)EU/USA

7. OIL ISSUES

8 EMERGING MARKET ISSUES

Venezuela/USA

This should be interesting: Trump proposing a complete naval blockade on Venezuela despite Russia and China’s presence in the country

9. PHYSICAL MARKETS

i)Central banks have loaded up in gold especially eastern nations

(Bloomberg.GATA)

ii)You do not want to miss any of Pam and Russ commentaries: today, JPMorgan is the New York fed.

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/THIS MORNING/USA/JOBS REPORT

Generally a poor report; only 164,000 jobs added..wage growth adds to .3% but hrs worked declined. The market will not be kind to this

(zerohedge)

b)The job numbers are a complete joke..multiple jobholder numbers soar to a record high. Remember that if you hold 3 jobs that counts as 3 job numbers in the non farm payrolls. Interestingly enough, the labour participation report for the 55 year olds and higher were significantly increased as old timers just do not have enough money to retire on

(zerohedge)

b)MARKET TRADING/USA/late morning

Stock loses accelerate as China warns that the USA will suffer more pain

(zerohedge)

c)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

(zero hedge)

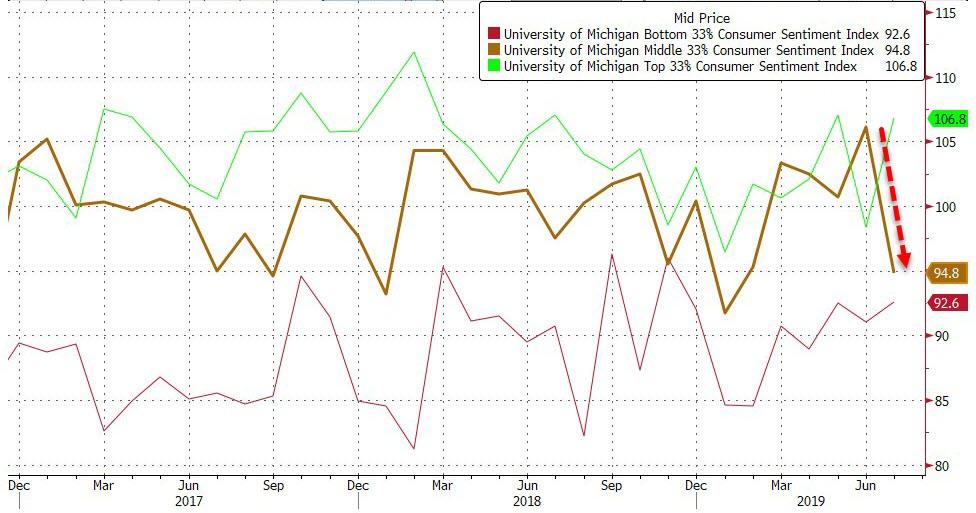

b)Another bad data point: U. of Michigan confidence falters as middle income American hopes plunge

c)USA factory orders contract for the 2nd month in a row

d)As we have predicted, the uSA total trade deficit hardly moves in June despite the tariffs. It slightly lowers to 55.2 billion dollars for the June month. This is a negative to GDP

iii) Important USA Economic Stories

An excellent commentary from Stefan Gleason. He wonders if Trump might engage in currency intervention to get the dollar down and help with the trade deficit.

a good read..

(courtesy Stefan Gleason)

iv) Swamp commentaries)

a)Ironic! Elijah Cummings Baltimore home is robbed

(zerohedge)

b)Looks like the UK is in trouble with this: many secret texts between the UK and FBI/CIA sources trying to undermine Trump

(zerohedge)

c)I have always stated that Tulsi Gabbard is the right candidate for President but wrong party. She is going after the Deep State

(Tom Luongo)

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 1 kilobar entries

total gold withdrawals; 32.15 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2019. contract month, we take the total number of notices filed so far for the month (3794) x 100 oz , to which we add the difference between the open interest for the front month of AUGUST. (3559 contract) minus the number of notices served upon today (221 x 100 oz per contract) equals 713,200 OZ OR 22.183 TONNES) the number of ounces standing in this active month of AUGUST

Thus the INITIAL standings for gold for the AUGUST/2019 contract month:

No of notices served (3794 x 100 oz) + (3559)OI for the front month minus the number of notices served upon today (221 x 100 oz )which equals 713,200 oz standing OR 22.183 TONNES in this active delivery month of AUGUST.

We LOST 219 contracts or an additional 21,900 oz will NOT stand as these guys morphed into London based forwards as well as accepting a fiat bonus.

SURPRISINGLY LITTLE TO NO GOLD HAS BEEN ENTERING THE COMEX VAULTS AND WE HAVE WITNESSED THIS FOR THE PAST YEAR!! WE HAVE ONLY 16.013 TONNES OF REGISTERED ( GOLD OFFERED FOR SALE) VS 22.183 TONNES OF GOLD STANDING// JUDGING BY THE HUGE SIZE OF THE COMEX NOTICES FILED TODAY, IT LOOKS LIKE SOMEBODY IS WILLING TO TAKE ON THE CROOKS AT THE COMEX.

REMEMBER THAT THE BIG GAIN IN PRICE FOR GOLD (AND SILVER) OCCURRED AFTER 1:30 ONCE THE COMEX WAS CLOSED. WE SHOULD SEE A HUGE OI GAIN WITH MONDAY’S READING.

At 3:30 they release the COT report and I highlight gold to show the liquidation of 10,499 spreading contracts.

| Gold COT Report – Futures | |||||||

| Large Speculators | Commercial | Total | |||||

| Long | Short | Spreading | Long | Short | Long | Short | |

| 312,214 | 57,826 | 45,699 | 141,164 | 429,131 | 499,077 | 532,656 | |

| Change from Prior Reporting Period | |||||||

| 333 | -2,805 | –10,499 | -34,621 | -34,493 | -44,787 | -47,797 | |

| Traders | |||||||

| 210 | 61 | 67 | 53 | 60 | 287 | 168 | |

| Small Speculators | |||||||

| Long | Short | Open Interest | |||||

| 64,221 | 30,642 | 563,298 | |||||

| -8,774 | -5,764 | -53,561 | |||||

| non reportable positions | Change from the previous reporting period | ||||||

| COT Gold Report – Positions as of | Tuesday, July 30, 2019 | ||||||

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 103,451 CONTRACTS (huge volume today)

CONFIRMED VOLUME FOR YESTERDAY: 134,751 CONTRACTS.. (monstrous volume yesterday

YESTERDAY’S CONFIRMED VOLUME OF 134,751 CONTRACTS EQUATES to 673 million OZ 96.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO +0.40.% ((AUGUST 2/2019)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.57% to NAV (AUGUST 1/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +0.40%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 14.23 TRADING 13.75/DISCOUNT 3.40

END

And now the Gold inventory at the GLD/

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 29/WITH GOLD UP $1.00: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 6.75 TONNES INTO THE GLD INVENTORY///INVENTORY RISES TO 824.89 TONNES

JULY 26/WITH GOLD UP $4.50: A HUGE INVENTORY WITHDRAWAL OF 4.09 TONNES OF PAPER GOLD LEAVES THE GLD/INVENTORY RESTS AT 818.14 TONNES

JULY 25.2019: WITH SILVER DOWN 19 CENTS: ANOTHER PAPER WITHDRAWAL OF 1.17 MILLION OZ/INVENTORY REST AT 358.213 MILLION OZ

JULY 24…A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A GAIN OF 1.685 MILLION OZ/INVENTORY RESTS AT 359.383 MILLION OZ

JULY 23/2019: WITH SILVER UP 5 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.221 MILLION PAPER OZ ADDED INTO THE GLD INVENTORY//INVENTORY RESTS AT 357.698 MILLION OZ////

JULY 22.2019/WITH SILVER UP 21 CENTS TODAY: A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 8.939 MILLION OZ ADDED TO THE SLV INVENTORY/INVENTORY RESTS AT 355.919 MILLION OZ/

JULY 19/WITH GOLD DOWN $1.00: A MASSIVE DEPOSIT OF 11.44 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 814.62

JULY 18/WITH GOLD UP $5.55 TODAY: A BIG PAPER DEPOSIT OF 3.81 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 803.18 TONNES

JULY 17/WITH GOLD UP $11.35 TODAY: A BIG WITHDRAWAL OF 1.17 TONNES FROM THE GLD//INVENTORY RESTS AT 799.37 TONNES

JULY 16: WITH GOLD DOWN $2.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 15: WITH GOLD UP $1.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 12/WITH GOLD UP $5.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 11.WITH GOLD DOWN $5.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 10//WITH GOLD UP $11.65 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER GOLD DEPOSIT OF 6.46 TONNES/INVENTORY RESTS AT 800.54 TONNES

JULY 9/WITH GOLD UP 70 CENTS, A HUGE PAPER WITHDRAWAL OF 2.89 TONNES WHICH WAS USED IN THE FUTILE RAID ON GOLD AND SILVER THIS MORNING//INVENTORY RESTS AT 794.08 TONNES

JULY 8/ WITH GOLD DOWN 35 CENTS A HUGE WITHDRAWAL OF 1.47 TONNES FROM THE GLD/INVENTORY FALLS TO 796.97 TONNES

JULY 5TH/WITH GOLD DOWN $19.50/NO CHANGES IN GOLD INVENTORY AT THE GLD//INV RESTS AT 798.44 TONNES

JULY 3// WITH GOLD UP $12.60 TODAY A SURPRISE WITHDRAWAL OF 1.76 TONNES FROM THE GLD//INVENTORY RESTS AT 798.44

JULY 2. WITH GOLD UP $18.90 A HUGE “PAPER” DEPOSIT OF 6.16 TONNES INTO THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 1: WITH GOLD DOWN $24.70 A HUGE “PAPER GOLD” WITHDRAWAL OF 1.76 TONNES FROM THE GLD/INVENTORY RESTS TONIGHT AT 794.04 TONNES

JUNE 28/WITH GOLD UP $.90 TODAY: ANOTHER 2.05 TONNES OF PAPER GOLD REMOVED AND THIS GOLD WAS USED IN ATTACKING GOLD AT THE COMEX/INVENTORY RESTS AT 795.80 TONNES

JUNE 27/WITH GOLD DOWN $6.10: ANOTHER HUGE WITHDRAWAL OF 1.76 PAPER TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 797.61 TONNES

JUNE 26/WITH GOLD DOWN $3.00: WE HAD A HUGE WITHDRAWAL OF 2.37 TONNES FROM THE GLD/INVENTORY RESTS AT 799.61 TONNES

JUNE 25/WITH GOLD UP $1.30 (AND WAY UP BEFORE THE BANKERS WHACKED) WE WITNESSED ANOTHER 1.95 TONNES OF PAPER GOLD ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 801.98 TONNES

JUNE 24/WITH GOLD UP $18.00 A MONSTROUS PAPER DEPOSIT OF 34.93 TONNES/INVENTORY RESTS AT 799.03 TONNES

JUNE 21/WITH GOLD UP $ 2.90, NO CHANGE IN GOLD INVENTORY: INVENTORY RESTS AT: 764.10 TONNES

June 20/WITH GOLD UP $47.95, NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 19 WITH GOLD DOWN $1.65: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONES

JUNE 18/JUNE 18/WITH GOLD UP $7.60: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 17/WITH GOLD DOWN $1.65 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 764.10 TONNES

JUNE 14/ WITH GOLD UP $1.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.40 TONNES OF PAPER GOLD INTO THE GLD///INVENTORY RESTS AT 764.10 TONNES

JUNE 13/WITH GOLD UP $6.60 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 759.70 TONNES

JUNE 12/WITH GOLD UP $7.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 756.18 TONNES

JUNE 11/WITH GOLD UP $1.65 CENTS TODAY: A TINY CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .24 TONNES AND THIS IS TO PAY FOR FEES/INVENTORY RESTS AT 756.18 TONNES

JUNE 10/WITH GOLD DOWN $16.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES/INVENTORY RESTS AT 756.42 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

AUGUST 2/2019/ Inventory rests tonight at 827.82 tonnes

*IN LAST 634 TRADING DAYS: 106.87 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 534 TRADING DAYS: A NET 58.76 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 29/2019: WITH SILVER UP 4 CENTS TODAY: A SMALL WITHDRAWAL OF 468000 OZ FROM THE SLV/INVENTORY LOWERS TO 356.715 MILLION OZ//

JULY 26.2019: WITH SILVER DOWN 2 CENTS TODAY: A HUGE 1.03 MILLION OZ OF PAPER SILVER LEAVES THE SLV/INVENTORY LOWERS TO 357.183 MILLION OZ//

JULY 25.2019: WITH SILVER DOWN 19 CENTS: ANOTHER PAPER WITHDRAWAL OF 1.17 MILLION OZ/INVENTORY REST AT 358.213 MILLION OZ

JULY 24…A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A GAIN OF 1.685 MILLION OZ/INVENTORY RESTS AT 359.383 MILLION OZ

JULY 23/2019: WITH SILVER UP 5 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.221 MILLION PAPER OZ ADDED INTO THE GLD INVENTORY//INVENTORY RESTS AT 357.698 MILLION OZ////

JULY 22.2019/WITH SILVER UP 21 CENTS TODAY: A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 8.939 MILLION OZ ADDED TO THE SLV INVENTORY/INVENTORY RESTS AT 355.919 MILLION OZ//

JULY 19/WITH SILVER FLAT TODAY: ANOTHER MONSTROUS PAPER DEPOSIT OF 3.276 MILLION OZ ENTERS THE SLV//WHAT A MASSIVE FRAUD//INVENTORY RESTS AT 346.980 MILLION OZ

JULY 18/WITH SILVER UP 24 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.668 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 343.704 MILLION OZ//

JULY 17: WITH SILVER UP ANOTHER 29 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.518 MILLION OZ/INTO THE SLV INVENTORY///INVENTORY RESTS AT 341.036 MILLION OZ//

JULY 16: WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY: 15 WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY 12/WITH SILVER UP 10 CENTS: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 11/NO CHANGE IN SILVER INVENTORY

JULY 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 9/WITH SILVER UP A SMALL 7 CENTS A GIGANTIC INVENTORY GAIN OF 4.026 MILLION OZ/ INVENTORY RESTS AT 332.518 MILLION OZ AND NOW IT SHOULD BE QUITE CLEAR THAT THE SLV ( AND GLD ARE FRAUDS)

JULY 8/WITH SILVER UP 7 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 328,492 MILLION OZ

JULY 5/WITH SILVER DOWN 32 CENTS WE STRANGELY HAD A HUGE INVENTORY GAIN OF 2,234 MILLION OZ//INVENTORY RESTS AT 328.492 MILLION OZ

JULY 3 WITH SILVER UP 10 CENTS A HUGE INCREASE IN INVENTORY..INVENTORY RESTS AT 326.151 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 323.330 MILLION OZ//

JULY 1/ WITH SILVER DOWN 16 CENTS: A SURPRISING DEPOSIT OF 936,000 OZ INTO THE SLV/INVENTORY RESTS TONIGHT AT 323.330 MILLION OZ/

JUNE 28/WITH SILVER UP 6 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.394 MILLION OZ//

JUNE 27/WITH SILVER DOWN 7 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.575 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.394 MILLION OZ//

JUNE 26/WITH SILVER UP 17 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

AUGUST 2/2019:

Inventory 356.715 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.17/ and libor 6 month duration 2.23

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: + .06

XXXXXXXX

12 Month MM GOFO

+ 2.19%

LIBOR FOR 12 MONTH DURATION: 2.24

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.05

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Fed’s Stock Bubble and Why Central Banks Blind Us To Risk

The Federal Reserve dropped interest rates by 0.25% and the U.S. stock markets fell from all time record new highs.

They also signaled to a surprised market that this is by no means an ongoing trend. The markets had to do a double take and were not enamored.

The Fed has turned dovish from a hawkish stance in just 6 months. They are rightly being mocked by some as now being in the pocket of Wall Street and the market which demands more and more accommodation to justify very lofty valuations.

This would be comical if it were not so serious. Our global markets are now addicted to official intervention and currency debasement to justify their ongoing flows and capital valuations.

This is happening 10 years after the emergency that was justified for adopting such extreme monetary measures began. They have become dumb and dumber with every accommodation, more demanding, more bold, and akin to a toddler having a tantrum.

Alas, every accommodation merely delays the inevitable correction, which threatens, with the passing of time, to become more systematically destructive. The time bought by cleansing the world’s financial balance sheets in 2009, by injecting liquidity, was not used to rebuild and restart the financial and monetary system.

Rather, it was used to bid up asset prices benefiting the chosen few.

The underlying structural issues are even more severe, risks more concentrated and the potential for lasting and permanent damage is very troubling.

No doubt the Fed see early warning signs that economic conditions are worsening and they feel they need to get ahead of the problem before it gets ahead of them.

Super Mario Draghi is signalling a “worse and worse” downturn in economic conditions. The US stock market has surged for 10 years now, posting a 4 fold increase.

In an excellent piece of research, Paban Raj Pandey explains that when the FED cuts, a recession follows (see chart above). The question is now does the cut trigger the recession with the public contracting spending or does the cut create exuberance by pumping the economy up to the point of derision and farce. It looks like the addict is now dictating to the dealer the price they are willing to pay.

ECB bond buying is in the dock in Germany by a number of patriotic and well informed members of the public. They are taking issue with the idea that the ECB can print euros and buy government bonds – known as monetary financing by officialdom or currency confiscation and theft by others.

It is illegal and rightfully so. The ECB’s defense is as idiotic as the original policy; they do not buy the bonds off the governments directly, rather they buy them off brokers who buy them off governments.

Here is the rub, if a central bank, mandated to control inflation, targeting 2% in most cases and keeping unemployment low can also then buy bonds issued by governments – we, collectively, become blinded to risks building in said economy.

Why, because the bond market is the largest capital market in the world. It is a de-facto measure of risk expectations now and into the future. If it does not like something, there tends to be good reason, because there is something not to like or some growing risk that needs to be considered and addressed.

If the price of a bond goes up and approaches par, then the yield is falling. This indicates that the market is happy with the risk in the world represented by that bond. Conversely if the bond falls out of favour, the price it commands falls and the yield rises, far above the initial interest rate coupon.

If country starts down a very risky and precarious path that has lots of risks you would expect that bond yields would rise. This shunning of the bonds by the market, would show up those in charge, cause strain in the public finances and force budgetary changes, thus raising the stakes for the government. Those in power would feel the heat, be removed or change course. The bond market is a sophisticated estimation of risk as voted by investors who have skin in the game. Central bankers do not have skin in the game.

We would argue that Brexit would have been debated more comprehensively and more rigorously from the initial announcement and that debate would have been reflected in a free bond market pricing in risk.

But because the world’s central banks are so active in our bond markets they have tempered debate, quashed decent and prudent policies and have led to political leaders who are wholly untested to govern nations.

Brexit may be the best long term, trajectory for the UK or it may not. But denying the collective wisdom of a free market is very, very dangerous.

Buying gold in this market gives personal sovereignty to investors and savers. It makes them less dependent on governments, banks and central banks. Why because gold and silver cannot be printed and electronically created at will and are universally liquid and exchangeable and proven stores of value.

NEWS & COMMENTARY

Gold surges nearly 2% after Trump says U.S. will impose new tariffs on Chinese imports

“We Expect This Selloff To Be Short and Relatively Shallow” – GoldCore via Blomberg

Central Bank Hunger for Gold Lifts Demand to Three-Year High

Gold demand leaps to 3-year high as prices surge – WGC

Ted Butler hails new CFTC chairman’s support for limiting derivatives positions

JPMorganChase is the New York Fed – GATA

Central bank buying and ETF inflows boosted H1 demand

Gold Prices via LBMA (AM/ PM Fix – USD, GBP & EUR)

01-Aug-19 1406.40 1406.80, 1161.12 1161.74 & 1273.35 1273.29

31-Jul-19 1430.55 1427.55, 1175.48 1167.45 & 1283.20 1281.37

30-Jul-19 1428.45 1425.90, 1173.47 1171.95 & 1281.75 1279.60

29-Jul-19 1418.95 1419.05, 1150.91 1157.94 & 1275.78 1275.30

26-Jul-19 1418.25 1420.40, 1140.27 1144.70 & 1273.02 1275.95

25-Jul-19 1426.35 1416.10, 1143.08 1132.88 & 1281.86 1265.85

24-Jul-19 1425.55 1426.95, 1142.29 1142.70 & 1279.86 1279.69

23-Jul-19 1417.55 1425.55, 1140.42 1145.29 & 1268.14 1277.01

22-Jul-19 1424.45 1427.75, 1142.69 1143.63 & 1270.04 1272.13

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

Central banks have loaded up in gold especially eastern nations

(Bloomberg.GATA)

iii) Other physical stories:

From Nicholas to Bill Murphy of GATA and me:

Hi Bill,Harvey,

It is that time of the month to once again visit the LBMA’s disseminated data to review this critical source of physical metal. Big yawn-as usual no material change. The profile of the loco London physical vault holdings of gold was as follows as at 30th April 2019.

| Total tonnes in loco London vaults | 7,650 |

| Less BOE | (5,019) |

| Less GLD as at 30th April 2019 | (747) |

| Net residual tonnes of vault gold | 1,884 |

These 1,884 tonnes must not only satisfy the claims of all allocated gold account holders, but also the counter parties to all those EFP contracts , now well above 10,000 tonnes. Unallocated gold accounts are mere claims to a fiat settlement (and probably all these opaque EFP contracts are in this same category of mere undeliverable promises) The main black hole would appear to be the claims of allocated gold account holders, who hold the title to a never ever disclosed quantity of numbered gold bars that have long ago been re-refined to .9999 finesse and shipped Eastwards. The above profile of LBMA physical vault gold as at 30th April 2019 has hardly changed since the LBMA embarked on this new policy of transparency of disclosure (90 days in arrears) as at 31st July 2016. If copious amounts of physical gold are indeed flowing out of London, it is axiomatic that, since the LBMA core vault holdings are just about constant, then all outflows must be matched by commensurate inflows from the LBMA’s list of nearly 70 accredited refineries. In other words, the only physical gold in play is fairly inelastic current mine supply.

It is of course possible that some of the physical gold, ostensibly reported as located in loco London ,has been swapped/loaned/leased, and the metronomically constant profile (as above) includes gold receivables of some description, instead of the real physical metal. (That would be naughty, naughty, but hardly a surprise).

The COMEX Open interest is currently elevated at about 564,000 contracts (about 1,754 tonnes) compared to only 16 tonnes of registered gold per the CME reports on metal depository statistics-5 tonnes of this amount was a 31stJuly 2019 internal transfer from the eligible to the registered category in the HSBC depository. I read some daily commentary relating to notices filed and contracts standing for delivery and contracts ‘stopped’, but I find this data to be a bit disparate. Beginning with the CME reports for 12th July 2019, I have started to download this data on a daily basis.(If you miss a day, bad luck because the reports are not archived and only the current daily report is accessible). Over time, my summary will provide an accurate profile of all the delivered/withdrawn physical precious metal as reported by the CME. Yesterday Jesse coined the term hyper-rehypothecation, so in these days when such hypothecation practices and fractional reserving of +100/1 are the new euphemistic descriptions for officially condoned rampant corruption and plundering, perhaps the distinction between COMEX registered and eligible gold is fairly meaningless. For the period from 12th July 2019 to 31st July 2019, here is the summary of physical precious withdrawn from the COMEX .(At least this data is current, unlike the totally useless historic LBMA data.)

| Metal Withdrawn from COMEX 12/07/2019 to 31/07/2019 | From Registered Holdings | From Eligible Accounts |

| Gold: NIL | Gold: 0.094 tonnes | |

| Silver: NIL | Silver: 2,357,813 troy ozs. |

No withdrawals at all from the COMEX registered category of either physical gold or silver in the last 20 days of July 2019 may not have much significance in isolation, but overtime the farcical nature of these undeliverable paper promises will be revealed in this alternative concise, unequivocal summary based on the CME’s own data, but stripped of the mystique, jargon and complexity that is designed to obfuscate the essentially undeliverable nature of physical metal that is alleged to be held in the virtually inaccessible COMEX depositories. Remember, however, that the COMEX seeks to distance itself from the chicanery of its constituency by issuing a disclaimer on each and every report which itemizes CME metal depository statistics.

This commentary was prepared primarily on Thursday morning as the headline paper prices of gold and silver were being trashed. Richard Quest on CNN was livid with rage at the apparent cause of the later stunning intraday reversals .Clearly we are near peak insanity in just about everything. Whilst the paper markets are acting in a slightly more robust fashion recently, before you jump to any hard conclusions, ask yourself whether it is possible for the COMEX Open Interest to jump to 2 million contracts and EFP transfers to exceed 30,000 tonnes? The only truly fatal impediment to decades of manipulation would be the hegemony of a market priced only by bid/offers for proven stocks of physical metal . Will the Comex deliver any physical gold at all in these coming days? It will be interesting to watch the forthcoming withdrawal data for hard evidence .The combined total of registered and eligible gold is only 242 tonnes, less than 14% of the open interest, so if there is ever a panic into ownership plus possession of physical gold, stripping the COMEX entirely will hardly alleviate the imminent crisis in an environment of fractional reserving fraud in the range of 100/1 (possibly even 500/1)

The Russia Today (RT) channel reports upon the increasing number of Sino-Russo collaborations as the new One Belt One Road trading bloc gathers momentum in respect of its roll out, eventually embracing more than 60% (70%?) of the global population. This massive accumulation of gold by China and Russia (possibly in excess of 30,000 tonnes each) has a definite purpose, which will be revealed in due course. When that purpose is revealed, the price of physical gold will be dictated by a physical market place. The magnitude of the conspiracy that GATA has sought to expose for two decades will be unraveled, and few, if any, will fail to be impressed by its ‘magnificence’ (magnificent in the sense that the ‘end of days’ will be magnificent to behold).

Regards

Nicholas

end

A good commentary showing the supply side of gold. I have been using 3500 tonnes which seems to be accurate.

Others use: global supply at 2800 tonnes – 700 tonnes (Russia and China)

as none of their gold ever gets out.

LAWRIE WILLIAMS: Peak gold continues to be elusive– WGC

While the latest quarterly Gold Demand Trends report from the World Gold Council (WGC) finds an encouraging pattern of gold demand growth in Q2 2019, largely due to seemingly ever-increasing Central Bank demand and some substantial inflows into gold ETFs over the quarter, along with a big pick-up in gold jewellery demand in India. What will be disturbing for some commentators/analysts on gold is that supply – far from plateauing or diminishing, as many have been suggesting, is actually continuing to rise making the ‘peak gold’ theory something of a gold bug’s myth – at least for the time being. We have ourselves suggested that supply may be peaking, but not according to the WGC’s latest research.

While global mine output continues to grow, albeit by only a small amount, the higher gold prices received in Q2 led to a 9% rise in recycled gold.

On the mining front, despite contractions – quite severe in some cases – in some major gold mining nations like China, South Africa and Indonesia, new mined gold output continued to grow from some others among the world’s biggest gold mining nations – notably Russia, the U.S. and Canada (all up around 9%), and Australia up around 6%. This led to overall new mined gold production growth of around 2% in Q2 2019 compared with the same quarter a year earlier. This follows on from a record Q1 too. Overall the WGC estimates H1 new mined gold production at 1,730.2 tonnes – up 1.1% on H1 2018. Kazakhstan – a mid-sized gold producer saw output rise by a massive 18% benefiting from the continued ramp-up of Polymetal’s Kyzyl project which is continuing towards full production by the end of the current year. In West Africa, Ghana – nowadays the continent’s largest producing nation – saw a 6% year-on-year increase in production, primarily from Ahafo and Akyem.

For comparison – Top 20 Gold Producing Nations 2017/2018 (Tonnes)

| Rank | Country | 20 18 Output | 2017 Output | % Change |

| 1 | China | 404 | 429 | -5.9% |

| 2 | Australia | 315 | 293 | +7.6% |

| 3 | Russia | 297 | 281 | +5.9% |

| 4 | USA | 222 | 236 | -6.3% |

| 5 | Canada | 189 | 171 | +10.4% |

| 6 | Peru | 158 | 167 | -4.9% |

| 7 | Indonesia | 137 | 114 | +20.0% |

| 8 | Ghana | 131 | 130 | +0.7% |

| 9 | South Africa | 130 | 154 | -15.7% |

| 10 | Mexico | 115 | 119 | -3.4% |

| 11 | Brazil | 97 | 96 | +1.3% |

| 12 | Uzbekistan | 92 | 89 | +3.9% |

| 13 | Sudan | 77 | 88 | -13.0% |

| 14 | Papua New Guinea | 69 | 64 | +7.4% |

| 15 | Kazakhstan | 68 | 56 | +22.1% |

| 16 | Mali | 61 | 50 | +21.3% |

| 17 | Argentina | 60 | 63 | -4.6%% |

| 18 | Burkina Faso | 59 | 53 | +12.8% |

| 19 | Tanzania | 48 | 55 | -12.7% |

| 20 | DR Congo | 45 | 37 | +22.8% |

| Others | 728 | 697 | +4.4% | |

| Total | 3,503 | 3,442 | +1.8% |

Source: Metals Focus, lawrieongold

On the downside, Chinese gold production registered another quarter of year-on-year declines. National output fell 4% as the stricter environmental regulations imposed in 2017 continued to impact the industry – albeit to a lesser degree. South African production fell 12%, disrupted by industrial action. Output from Beatrix, Kloof and Driefontein was cut significantly due to strikes that began in November 2018 and only drew to a close at the end of April. Hopefully there will be something of a pick-up in the second half of the year as the strikes appear to be over with union wage disputes transferring mostly to the platinum mining sector.

In Indonesia, national production fell by a massive 48%. At Freeport’s Grasberg operation – the world’s biggest gold producer in 2018 – the exhaustion of higher grades in the final phase of the open pit and the subsequent switch to underground mining continued to depress volumes relative to the prior year. The country’s other big gold mine. Batu Hijau, remains constrained by Phase 7 open pit expansion, as well as by copper concentration export limits and the lack of local smelting capacity.

In general, though, weaker currencies have been helping improve miners’ margins. Weaker producer currencies helped pushed relative non-US dollar costs down (or revenues up depending on which way you look at it), thereby boosting miners’ margins in key mining nations such as South Africa, Australia, Russia and Ghana. The WGC comments that this all puts the industry in a reasonably healthy position.

The other significant supply component is recycled gold which totalled 314.6 tonnes in Q2, 9% higher than the same period of 2018. The WGC puts this down primarily to the stronger gold price performance in Q2 when it broke through the psychological $1,350/oz level and then rapidly up through $1,400, thus encouraging a wave of selling as some consumers looked to lock in profits. This breakthrough though was all in the final month of the quarter, which suggests that such recycling supply increases may well have continued through the first part of Q3 as well and will likely be boosted further by yesterday’s sharp gold price rise. H1 recycled gold supply is put by the WGC at 602 tonnes, 7% higher than the same period in 2018 and the highest H1 since 2016 when a huge rally in the gold price prompted significant selling back.

While the rise in recycling may be unsurprising given the gold price performance in Q2, the WGC notes that the response was far from uniform. In Western markets – North America and Europe – higher recycling volumes in June were responsible for much of the increase over the quarter. The supply of recycled gold in April and May was relatively subdued (as was the gold price), which meant the boost in June helped achieve a modest overall increase in Q2.

In the Middle East, Iran again saw robust absolute levels of recycling, modestly higher year-on-year. The volatile USD/Rial exchange rate helped support local gold prices in May – as international prices fell – but then countered the gold price rally in June. Turkey, on the other hand, saw much more modest levels of recycling despite higher prices. The WGC puts the reason for this being price expectations amongst consumers, who generally believed that the rally had further to run and so waited to sell at higher prices. This may have occurred in July and thus be in Q3 figures.

In China, recycled gold supply in Q2 was noticeably higher year-on-year. While April and May were quiet, consumers were enticed to sell their gold through promotions offered by jewellers as the price rose in June. And, higher volumes may also have been helped by recent advances in China’s gold recycling market. India too saw more recycling as the gold price rose above Rs32,000/10g in June. Elsewhere in Asia, though, the response to the price increase was far more muted.

While the rise in the gold price perhaps won’t do much to arrest any potential downturn in new mined gold production – indeed it could enhance it by making previously uneconomic lower grade areas of a mine viable – it will also likely unlock some recycled gold which might not have become available at lower prices which may counterbalance any mine production shortfall. True peak gold thus could likely continue to remain elusive for a couple of years yet!

02 Aug 2019

-END-

(courtesy Dave Kranzler/IRD)

Gold / Silver May Be Breaking Free From Manipulation

Financial Markets, Gold, Market Manipulation, Precious Metals, U.S. Economy

The price of gold has rejected numerous attempts by the banks to hammer the gold price below $1400 using paper gold derivatives on the Comex and the LBMA. I have not seen gold behave with such resiliency in the last 19 years when the Comex banks have an extremely large short position in Comex paper.

The action in the price of gold is signalling that large buyers are accumulating a lot of physical gold. This is preventing the banks from using the Comex as a manipulative tool. Based on historical preferences, I highly doubt the buying is coming from the hedge funds, who have been content playing in the paper gold sandbox of the Comex.

Per the World Gold Council numbers, which are notoriously understated, Central Banks have purchased 374 tonnes of gold in the first half of 2019. This is the highest level of CB gold purchases in over 50 years. Note that western Central Banks – specifically the Fed, ECB, BoE and BoJ have been notably absent from the buying frenzy. The buying has been led by China, Poland and Russia.

“With governments everywhere itching to increase spending without raising taxes and as the global economy sinks into a trade and credit-cycle induced recession, budget deficits will fuel monetary inflation at a faster pace than seen before. Re-learning that gold is sound money is now the most urgent priority for all those charged with responsibility for other peoples’ investments.”

The quote above is from Alasdair Macleod’s must-read essay titled, “The Reasoning Behind Gold’s Breakout.” The article dispels the common “Fake news” myths about gold. It would be a great article to read for Warren Buffet, who believes that gold “just sits there doing nothing.” Of course, students of gold and history know that gold has outperformed the Dow since 1971. Macleod revisits the math behind this fact.

If you are looking for mining stock ideas to take advantage of the emerging bull market move in gold and silver, please consider my Mining Stock Journal. In the latest issue released last night I review a popular silver stock that I believe is overvalued and I present a high risk/high return junior exploration stock that is relatively unknown but has 10x potential. You can learn more about this newsletter here: Mining Stock Journal information.

***

When you know what is going on behind the scenes in the gold and silver markets, and are writing about it every day, it is hard not to gripe. For example, following the Trump tariff tweet yesterday…

*The DOW was hit hard, it is lower today.

*The dollar sold off, it is lower today.

*The yield on the 10 yr T note fell, it is lower today.

*And gold and silver rose, but at the moment both are now lower than their Access Market closes following the tweet. Gold is last at $1440. and silver at $16.18. THEY are going all out this afternoon to take gold back down below its key $1440/$1442 level.

There was natural follow-through in all but the precious metals.

That said, and despite the griping, it was one heckuva last 24 hours and the tone is set for a terrific last half of the year.

There has been a great deal of bullish power built up in gold over these past many weeks…

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

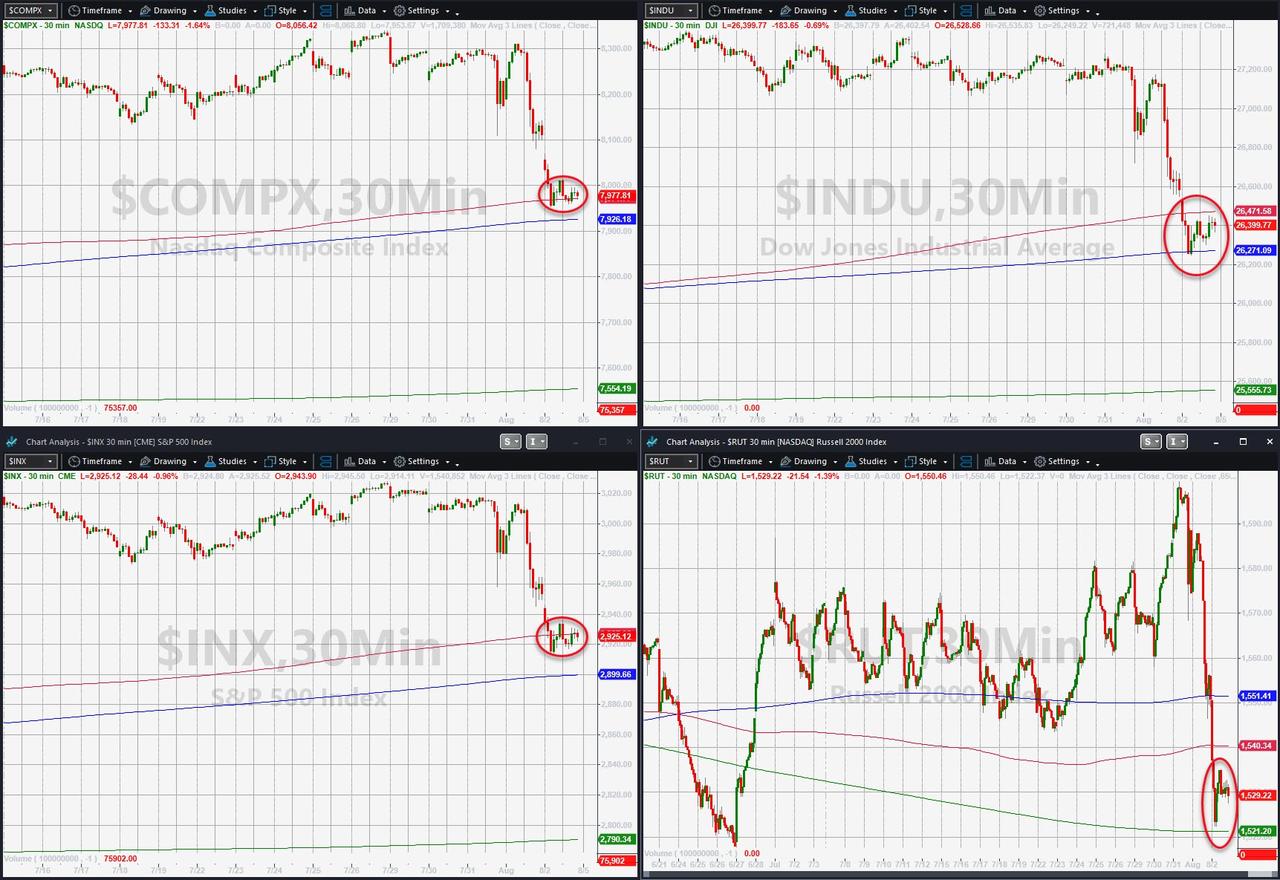

“Sea Of Red”: Global Markets Tumble In Post Trump Tariff Carnage

The Fed’s rate cut was supposed to boost markets and slam the dollar… it didn’t quite work out that way.

One day after stocks tumbled when Powell disappointed markets with his hawkish cut – the biggest plunge for stocks on a rate cut day since the memorable 1987 – global markets swooned as a wave of selling swept across the world, as panicked traders dumped stocks on fears that trade war between the US and China is about to escalate. Add to this a fresh trade war between Japan and South Korea, and a Trump announcement on EU trade at 1:45pm which will hang over markets, and it becomes obvious why world markets are a sea of red.

Meanwhile, safe havens such as bonds and the yen jumped in the wake of President Donald Trump’s move to escalate the trade war when he vowed to impose a 10% tariff on $300 billion of Chinese imports from Sept. 1, escalating a bruising and protracted trade war between the world’s two biggest economies, while China pledged “countermeasures” if the U.S. steps up tariffs on its goods.

“The question for investors is whether this is the first step in a series of escalations or a negotiating stance that will compel China to make concessions and the Fed to ease,” said Steve Englander, global head of FX research at Standard Chartered Bank. “If the president can elicit concessions from both China and the Fed, it would be a double win from his perspective.”

Trump’s announcement, which came a day after U.S. and Chinese negotiators concluded a meeting in Shanghai without much progress, marks an end to a trade truce struck in June and could further disrupt global supply chains.

“The combination of the Fed delivering a cut but not really what the market expected or wanted has tightened financial conditions, and may be partly the reason why Trump has gone for this escalation,” said Gerry Fowler, investment director at Aberdeen Standard Investments. “It is not good for what was already weak business sentiment.”

The carnage was focused on equities, with European stocks tumbling 2% led by automakers and miners, posting their biggest drop of 2019 on Friday …

… as the trade-sensitive DAX and France’s CAC 40 dropped 2.7%, the former hitting a fresh two-month lows.

German bond yields hitting record lows of -0.503% and the entire German curve now trading below 0% with the German 30Y dropping below zero for the first time ever.

MSCI’s index of world stocks dropped 0.6% as Asian bourses nursed heavy losses. The MSCI Asia Pacific Index dropped as much as 1.6%, extending its selloff to a third day. While Japan’s Topix Index fell 2.2% after the country decided to remove South Korea from a list of trusted export destinations, Korea’s benchmark pared earlier losses and closed 1% lower. The Hang Seng Index dropped to an almost two-month low as technology stocks tumbled. Materials and energy were the worst-performing sectors in the region, after crude prices had the steepest one-day drop in more than four years on Thursday.

The US was spared much of the brunt with S&P futures pointing to just a modest 0.3% lower open. On Thursday, the S&P 500 skidded 0.9% to hit one-month lows overnight.

Emerging-market stocks fell for an eighth day, the longest losing streak since December 2015, as new U.S. tariffs on Chinese imports raised the temperature in the trade war after the Federal Reserve’s hawkish cut already sapped demand for high-yielding assets.

Ahead of the July employment report to be released at 8:30am ET, Treasury yields are near multi-year lows reached Thursday after U.S. President Donald Trump announced additional tariffs on Chinese imports. Even before the latest declines, a survey by BMO found strong inclination to buy any dip in prices caused by the jobs report. The release of the June U.S. jobs report spurred a sell-off in Treasuries. Four of the previous five had a fleeting impact on the market. Median survey estimates for the July jobs report include nonfarm payrolls gain of 165k, 3.6% jobless rate and a 0.2% month-on-month increase in average hourly earnings

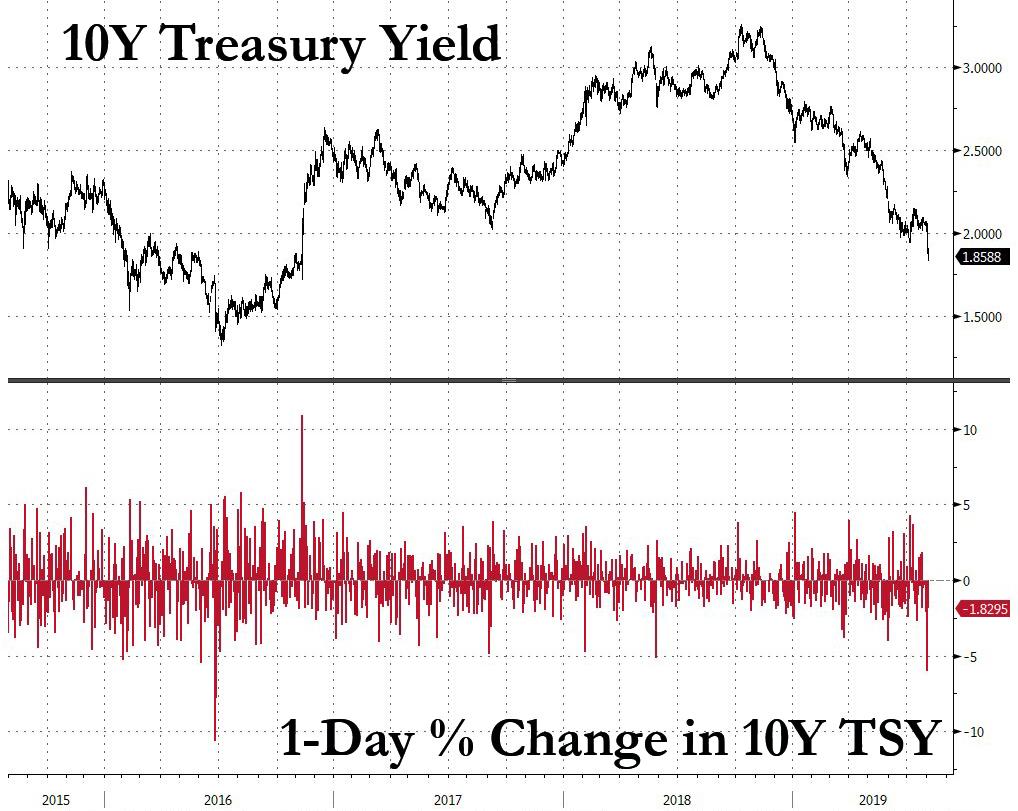

Not surprisingly, core euro zone bond yields tumbled, with German 10-year government bond yields dropping more than three basis points to an all-time low of -0.529% while the 30Y dropped below zero for the first time ever. That tracked the drop in 10-year U.S. Treasuries yields to 1.832% – the lowest since Nov. 8, 2016, the day Trump was elected president.

Trump’s strategic move may force the Federal Reserve to cut interest rates again – just as Trump intended – to protect the U.S. economy from trade-policy risks after its first rate cut in more than a decade on Wednesday. The October Fed funds rate futures have jumped to now fully price in a rate cut in September, compared with only around 60% before the tariff announcement. Another 25 basis point move is priced in by December.

“In the grand scheme of things, it will become clearer and clearer that the Federal Reserve has started an easing cycle and will have no choice but to cut rates further,” said Akira Takei, fund manager at Asset Management One.

While China has yet to offer details on what measures it would take, the sudden escalation of the trade war has put markets in a spin in an already action-packed week. The developments come after the Federal Reserve chief cast doubt about a long cycle of interest-rate cuts, provoking the president’s ire and disappointing many investors. The monthly U.S. jobs report will be the next big event later Friday, and while the market has priced in more trade cuts it is unprepared for an especially strong report, which will likely take place due to a surge in census hiring.

Meanwhile, as we wait for China to start dumping bonds, Japan’s cabinet approved removing South Korea from its export white list and Industry Minister Seko said they ready to talk only after South Korea corrects its statement regarding July meeting. It was also reported that BoK Governor Lee was to hold a meeting with officials and South Korean President Moon to chair a cabinet meeting following Japan’s decision to remove South Korea from its white list. Subsequently, South Korea have stated they will remove Japan from their White List as well. South Korea’s Deputy National Security Advisor states that Japan has generated obstacles in the way of achieving peace on the Korean peninsula, will review whether to maintain agreement on military intelligence sharing.

Oh, and just in case there wasn’t enough going on, the White House schedule for US President Trump showed that an announcement regarding EU trade is scheduled today at 1845BST, while reports later stated that US President Trump is to formally announce a deal to open up EU to more beef exports, according to sources familiar with the plans

In geopolitical news, North Korea conducted further short-range projectile launches early on Friday, which reports stated appeared to be a new type of missile.

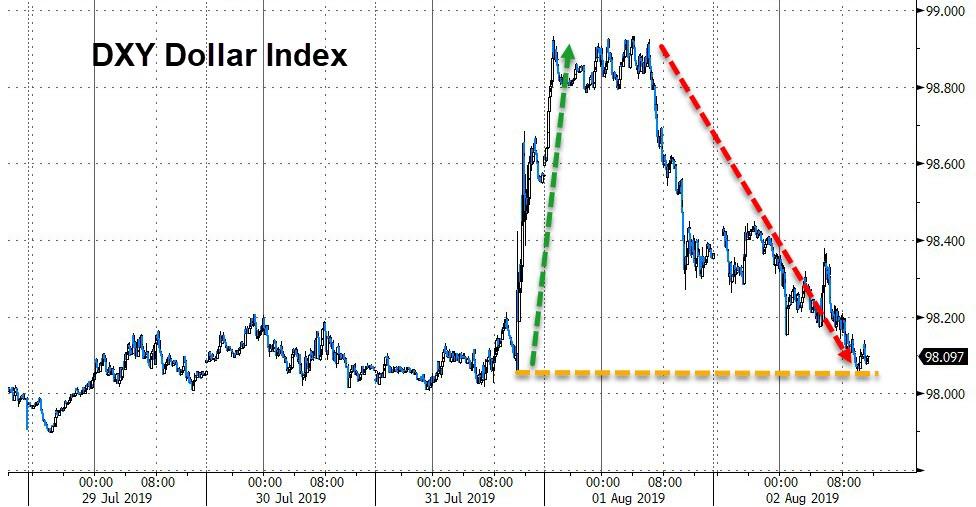

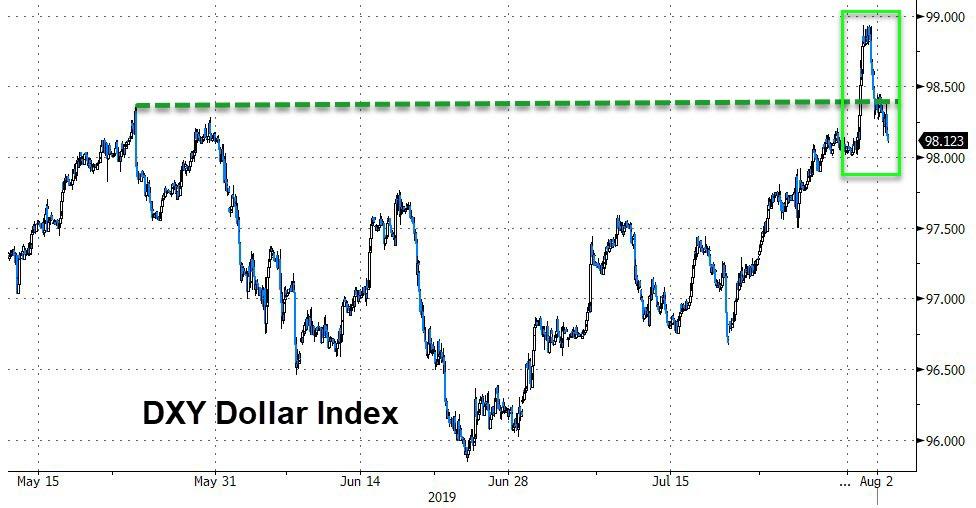

In currency markets, the Bloomberg Dollar Spot Index was up for a third week; the gauge reached a two-month high Thursday, having gained 1.3% since July 12. The safe-haven Japanese yen surged to a five-week high against the dollar and soared to a 2-1/2-year peak against the pound. The euro recovered to $1.1099, from a two-year low of $1.1027 hit in U.S. trade. The British pound held near a 30-month low versus the dollar as the ruling Conservatives’ majority in parliament was reduced to one seat, adding to concern over politics three months before the country is due to leave the European Union. Sterling was last 0.1% lower on the day at $1.2116. China’s onshore yuan slumped to its lowest since November 2018, falling some 0.7% to 6.9428 per dollar. In the offshore market, the yuan fell to as low as 6.9778.

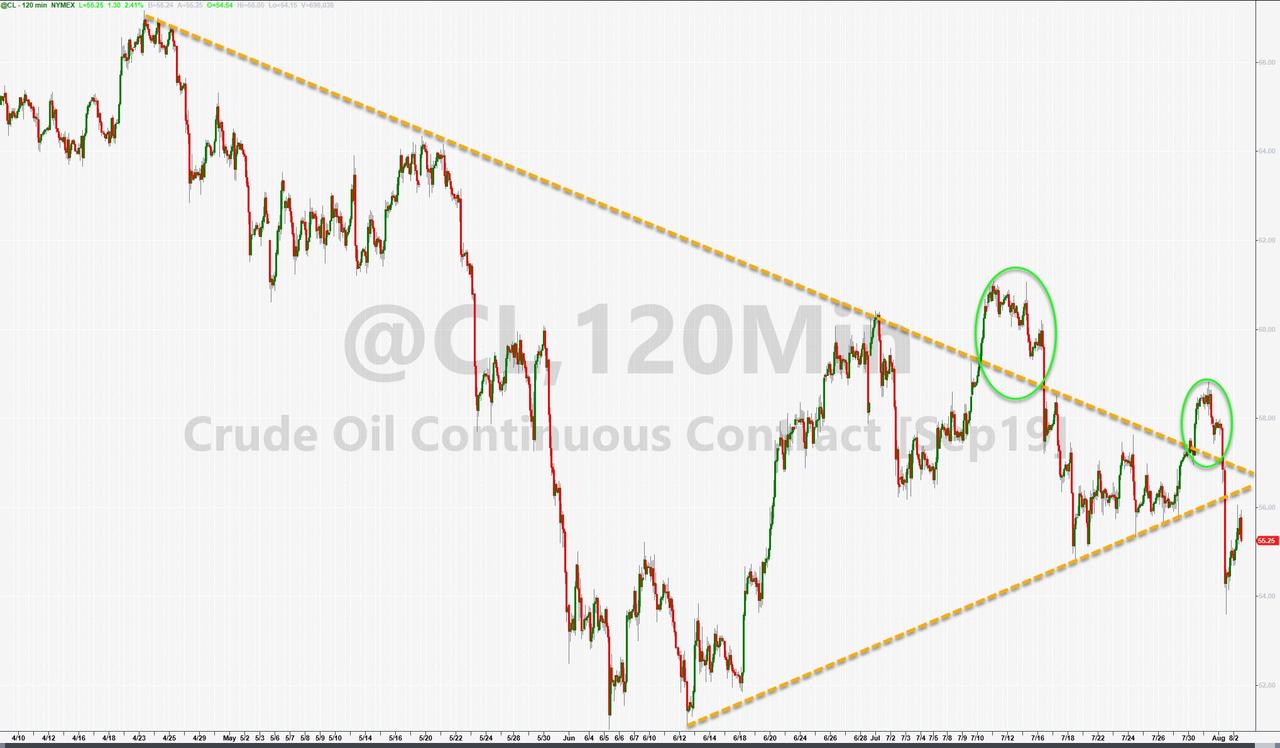

In commodity markets, gold dropped slightly to $1,435.46 per ounce after rising 2.3% on Thursday, near a six-year high of $1,453 touched two weeks ago. Oil prices bounced back after suffering a sharp, 7% selloff on Thursday, its biggest daily percentage drop since February 2016. U.S. West Texas Intermediate (WTI) crude rebounded 1.9% to $54.96, having shed 7.9% the previous day.

Exxon, Ferrari and Sprint are among companies reporting earnings

Market Snapshot

- S&P 500 futures down 0.5% to 2,938.50

- STOXX Europe 600 down 2% to 380.09

- MXAP down 1.4% to 155.50

- MXAPJ down 1.7% to 504.82

- Nikkei down 2.1% to 21,087.16

- Topix down 2.2% to 1,533.46

- Hang Seng Index down 2.4% to 26,918.58

- Shanghai Composite down 1.4% to 2,867.84

- Sensex up 0.4% to 37,178.95

- Australia S&P/ASX 200 down 0.3% to 6,768.57

- Kospi down 1% to 1,998.13

- German 10Y yield fell 3.5 bps to -0.485%

- Euro up 0.1% to $1.1100

- Italian 10Y yield rose 3.9 bps to 1.229%

- Spanish 10Y yield fell 2.3 bps to 0.271%

- Brent futures up 2% to $61.72/bbl

- Gold spot down 0.5% to $1,437.48

- U.S. Dollar Index down 0.1% to 98.24

Top Overnight News from Bloomberg

- Beijing pledged to respond if the U.S. insists on adding extra tariffs to the remainder of Chinese imports. Raw materials are reeling after President Trump abruptly threatened new tariffs on Chinese goods, casting doubt on negotiations to end the trade war that’s sapping global growth and demand for commodities.

- Trump announced that he would impose a 10% tariff on a further $300b in Chinese imports, and later said the levy could go “well beyond” 25% and will be implemented from Sept. 1. The U.S. President resisted advice to give Beijing advance notice of the tariffs

- Trump labeled recent protests in Hong Kong as “riots,” adopting the language used by Chinese authorities and suggesting the U.S. would stay out of an issue that was “between Hong Kong and China.”

- South Korea warned Japan it would be responsible for repercussions from its unprecedented decision to remove Seoul from a list of trusted export destinations, as escalating tensions between the two U.S. allies threaten to damage security ties and global supply lines

- U.K. Prime Minister Boris Johnson’s House of Commons majority was reduced to a single seat after the anti-Brexit Liberal Democrats won a by- election in Brecon and Radnorshire. This makes Johnson’s balancing act more difficult as he seeks to deliver Brexit by Oct. 31

- U.S. Trade Representative Robert Lighthizer and the European ambassador to the United States on Friday will sign an agreement to increase the amount of American beef that can be sold in the EU market, the people familiar said, speaking on condition of anonymity ahead of the announcement Friday.

- Ten-year Treasury yields plunged to the lowest since 2016 on news of new tariffs, and as traders slashed their inflation outlook. Trump told a campaign rally in Cincinnati that “until such time that there is a deal, we will be taxing the hell out of China”

- The anti-Brexit Liberal Democrats won a by-election in Brecon and Radnorshire, reducing PM Johnson’s majority in the House of Commons to just one and making his balancing act more difficult as he seeks to deliver Brexit by Oct. 31

- Oil is set for a weekly loss following the steepest one-day drop in more than four years after U.S.-China trade tensions worsened

Asian equity markets traded lower across the board with global risk sentiment spooked after US President Trump upped the pressure on China by announcing a 10% tariff on the remaining USD 300bln of Chinese goods to the US beginning September 1st. ASX 200 (-0.3%) was subdued with hefty losses seen in the energy sector after crude prices dropped over 7% the prior day and with broad weakness across mining names aside from gold stocks after the precious metal was boosted by safe-haven demand, while Nikkei 225 (-2.1%) was dragged lower by a firmer currency, soft earnings and as regional bilateral relations further deteriorated after Japan approved the removal of South Korea from its white list of preferred trading partners. Elsewhere, Hang Seng (-2.4%) and Shanghai Comp. (-1.4%) conformed to the washout across stocks following Trump’s tariff announcement in which he said he is taxing China until a deal can be reached and suggested that tariffs could be raised to 25%. Finally, 10yr JGBs were higher and notched their biggest gain since early January as they tracked the upside in global bonds due to safe-haven demand and with the BoJ present in the market for longer-dated bonds.

Top Asian News