GOLD:$1503.00 UP $31.00(COMEX TO COMEX CLOSING

Silver: $17.18 UP 74 CENTS (COMEX TO COMEX CLOSING)/

Closing access prices:

Gold : $1501.65

silver: $17.11

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 7/19

EXCHANGE: COMEX

CONTRACT: AUGUST 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,472.400000000 USD

INTENT DATE: 08/06/2019 DELIVERY DATE: 08/08/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

118 H MACQUARIE FUT 4

661 C JP MORGAN 3 7

686 C INTL FCSTONE 6

690 C ABN AMRO 3

737 C ADVANTAGE 6 2

800 C MAREX SPEC 1

880 H CITIGROUP 6

____________________________________________________________________________________________

TOTAL: 19 19

MONTH TO DATE: 4,400

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 19 NOTICE(S) FOR 1900 OZ (0.0590 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 4400 NOTICES FOR 440,000 OZ (13.688 TONNES)

SILVER

FOR JULY

54 NOTICE(S) FILED TODAY FOR 270,000 OZ/

total number of notices filed so far this month: 1132 for 5,660,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

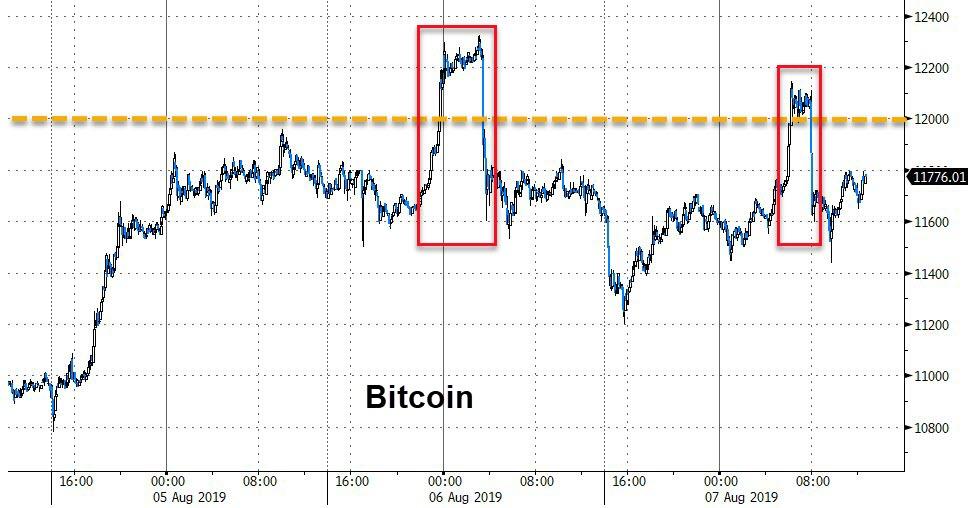

Bitcoin: OPENING MORNING TRADE : $ 11696 UP 216

Bitcoin: FINAL EVENING TRADE: $ 11799 UP 325

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A FAIR SIZED 856 CONTRACTS FROM 238,434 UP TO 239,290 WITH THE 5 CENT GAIN IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JULY. 0 FOR AUGUST, 1113 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1113 CONTRACTS. WITH THE TRANSFER OF 1113 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1113 EFP CONTRACTS TRANSLATES INTO 5.56 MILLION OZ ACCOMPANYING:

1.THE 5 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.425 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ INITIAL STANDING FOR JULY

7.425 MILLION OZ INITIAL STANDING IN AUGUST.

WE MUST HAVE HAD CONSIDERABLE COVERING OF SHORTS AT THE SILVER COMEX LAST NIGHT AND SOME SPREADING ACCUMULATION.

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF SEPTEMBER FOR SILVER.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF AUGUST BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

7368 CONTRACTS (FOR 5 TRADING DAYS TOTAL 7368 CONTRACTS) OR 36.84 MILLION OZ: (AVERAGE PER DAY: 1473 CONTRACTS OR 7.368 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 36.84 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 5.63% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1364.16 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

RESULT: WE HAD A FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 856, WITH THE 5 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1113 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A VERY STRONG SIZED: 1969 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1113 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 856 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 5 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $16.44 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.199 BILLION OZ TO BE EXACT or 171% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 54 NOTICE(S) FOR 270,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ;AUGUST 7.425 MILLION

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A TINY SIZED 485 CONTRACTS, TO 600,317 ACCOMPANYING THE $7.85 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING// YESTERDAY// /

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4966 CONTRACTS: AUGUST 2019: 0 CONTRACTS, DEC> 4966 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 600,317,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5451 CONTRACTS: 485 CONTRACTS INCREASED AT THE COMEX AND 4966 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 5451 CONTRACTS OR 545,100 OZ OR 5.620 TONNES. YESTERDAY WE HAD A GOOD GAIN OF $7.85 IN GOLD TRADING….AND WITH THAT GOOD GAIN IN PRICE, WE HAD A GOOD GAIN IN GOLD TONNAGE OF 5.62 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER DESPERATE TO CONTAIN THE PRICE RISE.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST : 65,620 CONTRACTS OR 6,562,000 oz OR 224.51 TONNES (5 TRADING DAY AND THUS AVERAGING: 13,124 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY IN TONNES: 224.51 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 224.51/3550 x 100% TONNES =6.32% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 3715.35 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A TINY SIZED INCREASE IN OI AT THE COMEX OF 485 WITH THE PRICING GAIN THAT GOLD UNDERTOOK YESTERDAY($7.85)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 4,966 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 4966 EFP CONTRACTS ISSUED, WE HAD A STRONG SIZED GAIN OF 5451 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

4966 CONTRACTS MOVE TO LONDON AND 485 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 5.620 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED WITH THE GAIN IN PRICE OF $7.85 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAVE NOW STOPPED WITH SPREADING LIQUIDATION OF GOLD OI CONTRACTS AND COMMENCED WITH SILVER SPREADER OI ACCUMULATION.

we had: 19 notice(s) filed upon for 1900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $31.00 TODAY//(COMEX-TO COMEX)

a deposit of: 1.86 tonnes

INVENTORY RESTS AT 836.92 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 74 CENTS TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 361.907 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A FAIR SIZED 856 CONTRACTS from 238,434 UP TO 239,290 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JULY: 0 CONTRACTS FOR AUGUST: 0, FOR SEPT. 1113 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1113 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 845 CONTRACTS TO THE 1113 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG SIZED GAIN OF 1969 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 9.845 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ STANDING AND AUGUST: .7.425 MILLION OZ/

RESULT: A FAIR SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 5 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1113 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 8.88 POINTS OR 0.32% //Hang Sang CLOSED UP 20.79 POINTS OR 0.08% /The Nikkei closed DOWN 68.75 POINTS OR 0.33%//Australia’s all ordinaires CLOSED UP .64%

/Chinese yuan (ONSHORE) closed DOWN at 7.0458 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0458 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0781 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

i)China/India

China threatens “reverse sanctions” if Huawei is excluded from India’s 5 G network plan. Dr Reddy, a huge Indian pharmaceutical manufacturing company makes a huge amount of global generics in China as labour is cheaper in China than India. Also the supply of raw pharmaceuticals is located in China. The Chinese may throw out Dr Reddy and others.

(courtesy zerohedge)

ii)Michael Snyder gives his assessment as to dangers facing us with respect to the tariff war with China and the USA

(Michael Snyder)

iii)The following is a terrific read from Tom Luongo. He talks about the huge pressure on China especially Hong Kong and how Trump is at war with the British Deep State

a must read…

(Tom Luongo)

4/EUROPEAN AFFAIRS

7. OIL ISSUES

Oil prices continue to plunge especially after a huge surprise crude build

(zerohedge)

8 EMERGING MARKET ISSUES

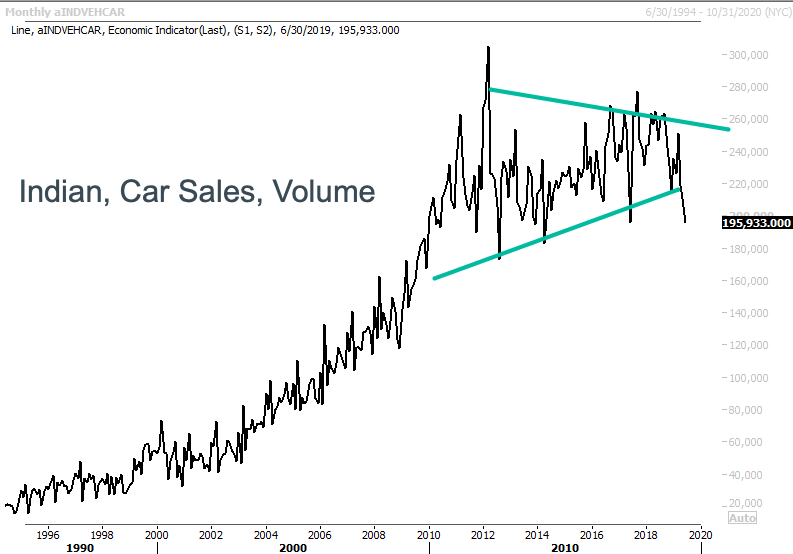

i)India

The global market continues to crash and this time it is India as we witness its auto market implode: 200,000 job losses in 3 months and another 1 million at risk

(zerohedge)

ii)War looks inevitable as Pakistan suspends bilateral trade with India and expels Indian envoy

(zerohedge)

9. PHYSICAL MARKETS

i)Negative interest rates at Swiss banks is forcing more citizens into gold

(Bloomberg//GATA)

ii)Gold which is just 2 atoms thick has been discovered in a lab..this will have tremendous use in medicine plus other areas

(zerohedge)

iii)Craig Hemke believes that there will be an assault on $1500 gold.

(Craig Hemke/Sprott/GATA)

iv)China has been seen supporting the yuan.

(Reuters/GATA)

v)Boy are Mexicans brazen: they just stole a couple of million dollars worth of gold coins form the Mexican mint.

(zerohedge)

vi)Bill Murphy interviewed

(Bill Murphy,GATA)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

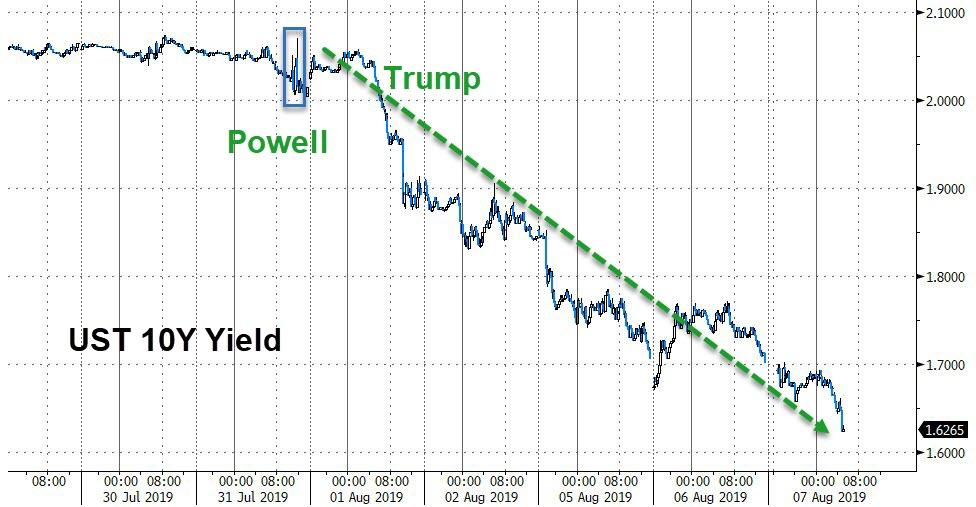

i) Treasury yields crashing!!

ii)Entire USA yield curves inverts

(zerohedge)

iii)Three areas of discussion:

- the panic in junk bonds. Even though yields are plummeting in sovereigns, the junk yields are rising indicating lack of liquidity and huge risks

- The Kashmir saga. The partition into3 areas is now basically over as India takes over its Indian Kashmir section. Pakistan is furious and worried about ethnic cleansing. War is coming in this area.

(courtesy Bill Blain)

ii)Market data/USA

iii) Important USA Economic Stories

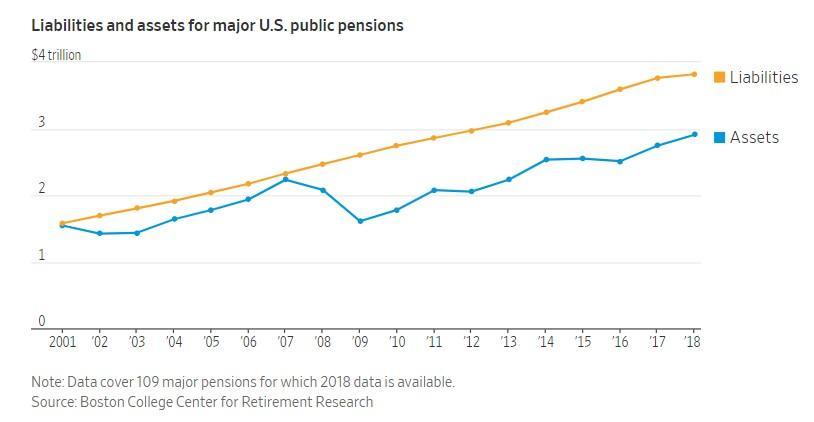

a)American Pension funds continue to miss their targets in 2019. They are terribly offside

(zerohedge)

b)After seeing three nations lower their interest rates, Trump pesters Powell to cut the Fed rate

(zerohedge)

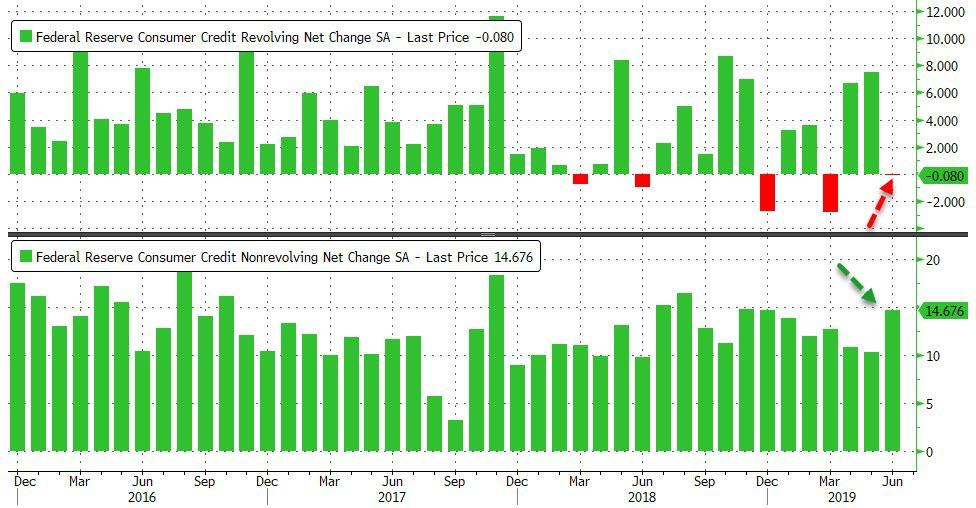

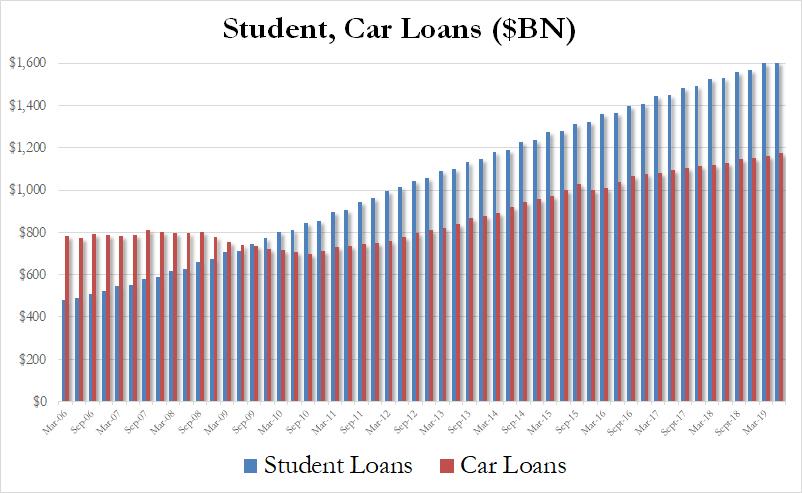

c)Total student and auto loans rise by close to 15 billion dollars: 2.77 trillion.

Revolving Credit: drops by 80 million

the only place the consume is getting money is through the auto loans and student loan sector

(COURTESY ZEROHEDGE)

iv) Swamp commentaries)

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 1 kilobar entries

total gold withdrawals; 321.50 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 179,558 CONTRACTS (we must have had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 84,366 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 84366 CONTRACTS EQUATES to 421 million OZ 60.3% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.35% ((AUGUST 7/2019)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.97% to NAV (AUGUST 7/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 14.90 TRADING 14.40/DISCOUNT 3.34

END

And now the Gold inventory at the GLD/

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 29/WITH GOLD UP $1.00: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 6.75 TONNES INTO THE GLD INVENTORY///INVENTORY RISES TO 824.89 TONNES

JULY 26/WITH GOLD UP $4.50: A HUGE INVENTORY WITHDRAWAL OF 4.09 TONNES OF PAPER GOLD LEAVES THE GLD/INVENTORY RESTS AT 818.14 TONNES

JULY 25.2019: WITH SILVER DOWN 19 CENTS: ANOTHER PAPER WITHDRAWAL OF 1.17 MILLION OZ/INVENTORY REST AT 358.213 MILLION OZ

JULY 24…A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A GAIN OF 1.685 MILLION OZ/INVENTORY RESTS AT 359.383 MILLION OZ

JULY 23/2019: WITH SILVER UP 5 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.221 MILLION PAPER OZ ADDED INTO THE GLD INVENTORY//INVENTORY RESTS AT 357.698 MILLION OZ////

JULY 22.2019/WITH SILVER UP 21 CENTS TODAY: A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 8.939 MILLION OZ ADDED TO THE SLV INVENTORY/INVENTORY RESTS AT 355.919 MILLION OZ//

JULY 19/WITH GOLD DOWN $1.00: A MASSIVE DEPOSIT OF 11.44 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 814.62

JULY 18/WITH GOLD UP $5.55 TODAY: A BIG PAPER DEPOSIT OF 3.81 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 803.18 TONNES

JULY 17/WITH GOLD UP $11.35 TODAY: A BIG WITHDRAWAL OF 1.17 TONNES FROM THE GLD//INVENTORY RESTS AT 799.37 TONNES

JULY 16: WITH GOLD DOWN $2.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 15: WITH GOLD UP $1.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 12/WITH GOLD UP $5.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 11.WITH GOLD DOWN $5.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 10//WITH GOLD UP $11.65 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER GOLD DEPOSIT OF 6.46 TONNES/INVENTORY RESTS AT 800.54 TONNES

JULY 9/WITH GOLD UP 70 CENTS, A HUGE PAPER WITHDRAWAL OF 2.89 TONNES WHICH WAS USED IN THE FUTILE RAID ON GOLD AND SILVER THIS MORNING//INVENTORY RESTS AT 794.08 TONNES

JULY 8/ WITH GOLD DOWN 35 CENTS A HUGE WITHDRAWAL OF 1.47 TONNES FROM THE GLD/INVENTORY FALLS TO 796.97 TONNES

JULY 5TH/WITH GOLD DOWN $19.50/NO CHANGES IN GOLD INVENTORY AT THE GLD//INV RESTS AT 798.44 TONNES

JULY 3// WITH GOLD UP $12.60 TODAY A SURPRISE WITHDRAWAL OF 1.76 TONNES FROM THE GLD//INVENTORY RESTS AT 798.44

JULY 2. WITH GOLD UP $18.90 A HUGE “PAPER” DEPOSIT OF 6.16 TONNES INTO THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 1: WITH GOLD DOWN $24.70 A HUGE “PAPER GOLD” WITHDRAWAL OF 1.76 TONNES FROM THE GLD/INVENTORY RESTS TONIGHT AT 794.04 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

AUGUST 7/2019/ Inventory rests tonight at 836.92 tonnes

*IN LAST 637 TRADING DAYS: 98.48 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 537 TRADING DAYS: A NET 68.06 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ//

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 29/2019: WITH SILVER UP 4 CENTS TODAY: A SMALL WITHDRAWAL OF 468000 OZ FROM THE SLV/INVENTORY LOWERS TO 356.715 MILLION OZ//

JULY 26.2019: WITH SILVER DOWN 2 CENTS TODAY: A HUGE 1.03 MILLION OZ OF PAPER SILVER LEAVES THE SLV/INVENTORY LOWERS TO 357.183 MILLION OZ//

JULY 25.2019: WITH SILVER DOWN 19 CENTS: ANOTHER PAPER WITHDRAWAL OF 1.17 MILLION OZ/INVENTORY REST AT 358.213 MILLION OZ

JULY 24…A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A GAIN OF 1.685 MILLION OZ/INVENTORY RESTS AT 359.383 MILLION OZ

JULY 23/2019: WITH SILVER UP 5 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.221 MILLION PAPER OZ ADDED INTO THE GLD INVENTORY//INVENTORY RESTS AT 357.698 MILLION OZ////

JULY 22.2019/WITH SILVER UP 21 CENTS TODAY: A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 8.939 MILLION OZ ADDED TO THE SLV INVENTORY/INVENTORY RESTS AT 355.919 MILLION OZ//

JULY 19/WITH SILVER FLAT TODAY: ANOTHER MONSTROUS PAPER DEPOSIT OF 3.276 MILLION OZ ENTERS THE SLV//WHAT A MASSIVE FRAUD//INVENTORY RESTS AT 346.980 MILLION OZ

JULY 18/WITH SILVER UP 24 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.668 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 343.704 MILLION OZ//

JULY 17: WITH SILVER UP ANOTHER 29 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.518 MILLION OZ/INTO THE SLV INVENTORY///INVENTORY RESTS AT 341.036 MILLION OZ//

JULY 16: WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY: 15 WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY 12/WITH SILVER UP 10 CENTS: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 11/NO CHANGE IN SILVER INVENTORY

JULY 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 9/WITH SILVER UP A SMALL 7 CENTS A GIGANTIC INVENTORY GAIN OF 4.026 MILLION OZ/ INVENTORY RESTS AT 332.518 MILLION OZ AND NOW IT SHOULD BE QUITE CLEAR THAT THE SLV ( AND GLD ARE FRAUDS)

JULY 8/WITH SILVER UP 7 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 328,492 MILLION OZ

JULY 5/WITH SILVER DOWN 32 CENTS WE STRANGELY HAD A HUGE INVENTORY GAIN OF 2,234 MILLION OZ//INVENTORY RESTS AT 328.492 MILLION OZ

JULY 3 WITH SILVER UP 10 CENTS A HUGE INCREASE IN INVENTORY..INVENTORY RESTS AT 326.151 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 323.330 MILLION OZ//

JULY 1/ WITH SILVER DOWN 16 CENTS: A SURPRISING DEPOSIT OF 936,000 OZ INTO THE SLV/INVENTORY RESTS TONIGHT AT 323.330 MILLION OZ/

AUGUST 7/2019:

Inventory 361.907 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.15/ and libor 6 month duration 2.05

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .10

XXXXXXXX

12 Month MM GOFO

+ 1.98%

LIBOR FOR 12 MONTH DURATION: 1.99

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.01

end

GOLD TRADING/LAST NIGHT:

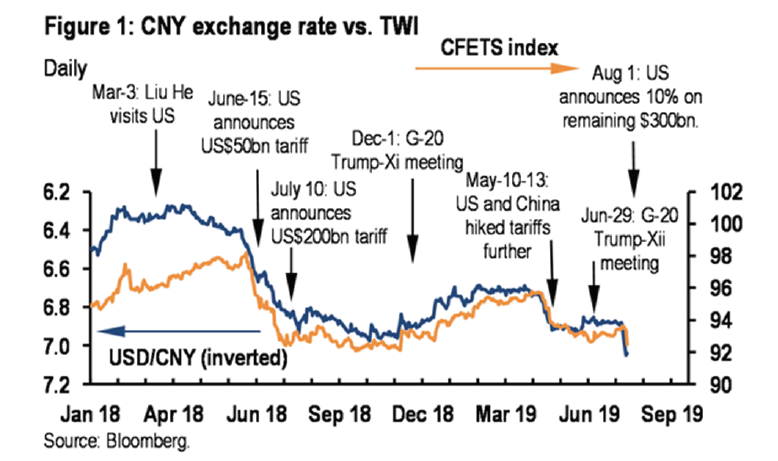

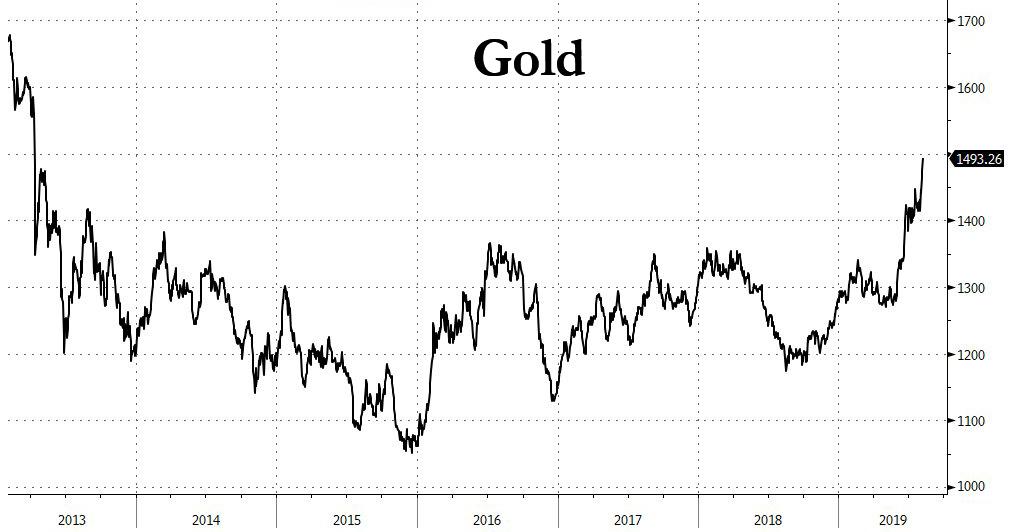

Gold Futures Top $1500 After China Weakens Fix More Than Expected

Update: In what appears to be China’s last warning (to push Trump to offer an olive branch before all hell breaks loose), PBOC fixed the yuan weaker than expected but just firmer than the critical 7.00 level.

The fixing was seen at 6.9977, according to the average projection of 22 traders and analysts surveyed by Bloomberg, but PBOC weakened the fixing by 0.45% to 6.9996 per dollar.

Offshore yuan slipped lower on the fix…

Gold futures topped $1500 (for the first time since 2013) – retracing 50% of the 2011 high to 2015 low plunge.

And Dow futures are leaking on the print…

* * *

With expectations for another weaker fix (at around 6.9994) tonight, it appears investors are seeking safe-havens (bonds and bullion bid) as equity futures slide.

Gold is bid…

Dow Futures are leaking lower…

But Treasury yields have plunged back to yesterday’s lows (1.67%), dramatically decoupled from stocks…

Smashing the yield curve to new cycle lows (-36bps is the most inverted since 2008)…

So all eyes will once again be on the CNY Fix…

Is China going to unleash hell again tonight?

If you ask JPMorgan, the answer is a definite maybe as they slashed their forecast for USDCNY to 7.35 by year-end.

The risk profile of our China and global growth forecast has shifted to the downside alongside the global inflation forecast – as indirect demand depressing channels are likely to prove more powerful than the direct effect of cost increases from trade restrictions. We have already added fiscal policy and monetary policy easing in China and there is likely to be more monetary policy easing than forecast elsewhere in the world.

Pressure on the USD is likely to be upward in this environment, particularly against the EM. While USD/CNY will not likely move in a straight line, we have revised downward the CNY forecast profile. We are now forecasting USD/CNY to reach 7.35 by end 2019 and 7.40 by the middle of 2020.

In terms of the CFETS CNY basket, we are now expecting an 88.70 level move by year end, which would bring the basket change to 4.6% versus end 2018 levels.

As a reminder, the last time China devalued on that scale, VIX exploded to 40, and we all know what happened last Q3/Q4…

Deja vu all over again?

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Gold Surges Over $1,500/oz as Investors Seek Shelter From Gathering Storm

via Bloomberg

Gold futures rallied above $1,500 an ounce on sustained demand for the traditional haven as the U.S.-China trade war festers, global growth slows and central banks around the world ease monetary policy.

The metal advanced as much as 1.3% to $1,503.30 an ounce on the Comex, the highest since 2013. The move extends this year’s climb to 17%, with gains underpinned by inflows into exchange-traded funds. Central banks in India and New Zealand both surprised markets on Wednesday with bigger-than-expected interest rate cuts, boosting speculation others will follow.

Silver, gold’s cheaper cousin, also surged. Spot prices rallied as much as 2.2% to $16.8082 an ounce, the highest in more than a year.

Gold has been one of the chief beneficiaries of the turmoil in global financial markets as Washington and Beijing spar over trade. In recent days, the Trump administration threatened fresh tariffs against Chinese goods, the yuan was allowed to sink, and the U.S. branded China as a currency manipulator. The stand-off has boosted the odds of more easing from the Federal Reserve.

“Gold is serving its traditional role as a safe-haven asset,” said Wayne Gordon, executive director for commodities and foreign exchange at UBS Group AG’s wealth management unit. Under the bank’s risk case, marked by a further escalation of the trade fight, prices could go as high as $1,600, he said.

Futures traded at $1,497.80 an ounce at 7:55 a.m. in London, gaining for a fourth day.

NEWS & COMMENTARY

Gold Tops $1,500 as Investors Seek Shelter From Gathering Storm

Gold Hits Over 6-year High as Trade Jitters Spark Safe-haven Rush

Gold Holds Near Six-year Peak as Trade Tensions Simmer

Asian Stocks Turn Lower on Lingering Trade War Fears, Yuan Slips

Scientists Just Created the World’s Thinnest Gold and It’s Two Atoms Thick

Yield Curve Blares Loudest U.s. Recession Warning Since 2007

Silver/Gold Ratio About to Send Multi-year Bullish Breakout Message

China’s Exit From US Agriculture is a Devastating Blow to an Already Struggling Sector

Pentagon Warns It Will Prevent “Unacceptable” Turkish Invasion of Northern Syria

Scientists Create the World’s Thinnest Gold

Gold Prices via LBMA (AM/ PM Fix – USD, GBP & EUR)

06-Aug-19 1461.85 1465.25, 1199.59 1201.21 & 1304.85 1311.11

05-Aug-19 1457.45 1465.25, 1199.92 1203.85 & 1307.92 1310.23

02-Aug-19 1436.05 1441.75, 1184.17 1187.28 & 1294.02 1298.44

01-Aug-19 1406.40 1406.80, 1161.12 1161.74 & 1273.35 1273.29

31-Jul-19 1430.55 1427.55, 1175.48 1167.45 & 1283.20 1281.37

30-Jul-19 1428.45 1425.90, 1173.47 1171.95 & 1281.75 1279.60

29-Jul-19 1418.95 1419.05, 1150.91 1157.94 & 1275.78 1275.30

26-Jul-19 1418.25 1420.40, 1140.27 1144.70 & 1273.02 1275.95

25-Jul-19 1426.35 1416.10, 1143.08 1132.88 & 1281.86 1265.85

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

Negative interest rates at Swiss banks is forcing more citizens into gold

(Bloomberg//GATA)

iii) Other physical stories:

Goldman Sees Gold Rising To $1,600 “Or Even Higher” On Escalating Trade War” 1

Gold just hit the highest level in 6 years and according to Goldman it is set to go much higher.

In a report by Goldman’s Sabine Schels, the commodity strategist looks at the consequences of the ever-escalating trade war between the US and China, and sees nothing but upside for gold, if not the other industrial metals. As she notes overnight, “the metals complex has weakened significantly, with iron ore down 18% and copper down 4% since the latest US tariff proposal. While there was a softening in iron ore fundamentals, the vast majority of the move was macro related, with copper positioning making fresh lows. Underscoring that, gold prices surpassed our target of $1475/toz.”

And with the yuan continuing to sink, as the PBOC is likely to deliver its first ever fixing below 7.00 tonight after the laughable 6.9996 on Tuesday, Goldman warns that a sharp CNY depreciation “could be highly disruptive, with the first order effect likely more dominant while the 2nd order effects may be much slower to take hold.”

Goldman then estimates that a 10% depreciation in the broad-based CNY could spell as much as 13% downside to the industrial metals complex, but of course, that would be good news for gold prices, which have increased further as a weaker CNY sparked substantial US and global growth fears. And with growth worries likely to persist, gold is expected to rise sharply. As a result, Goldman has hiked its 3, 6, 12-month gold price forecasts from $1450, $1475, $1475/toz to $1575, $1600 and $1600/toz, respectively.

Therefore, Goldman upgrades its gold ETF forecast for 2019 from 300 tonnes to 600 tonnes. While Goldman does not expect a global recession, for now, “until DM growth improves and worries ease gold should continue to move higher.” As such, it is upgrading its 3, 6, 12 month gold price forecasts from $1450, $1475, $/1475/toz to $1575, $1600 and $1600/toz, respectively. “At the same time, we see more upside in silver prices, too. When the push into gold is as strong as it now interest in silver tends to get reignited, too” and so Goldman upgrades its silver forecast from $15.4, $16, $/16/toz to $17.6, $18 and $18/toz, respectively.

Of course, gold could go even higher: as the Goldman analyst notes, “if growth worries persist, possibly due to a trade war escalation, gold could go even higher driven by a larger ETF gold allocation from portfolio managers, who still continue to under-own gold. Specifically we argued that 2019 gold ETFs build could reach the pace similar to Jan- Oct 2016, which is the last time DM growth was so low.” Fast forward to today, when with the DM CAI persistently low, the trade war escalating, global equities selling off and volatility spiking, “it looks our risk scenario is playing out” Goldman admits. Indeed, “gold ETFs have recently built momentum almost as strong as in 2016 and we believe that can be maintained in the short term.”

As Bloomberg calculates, bullion holdings in ETF climbed to the highest since April 2013. The precious metal climbed as much as 1.8% on Wednesday to $1,511.60 an ounce, the highest since April 2013.

To all this we would just add the following usual disclaimer: any time Goldman predicts one thing, the opposite happens…

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

3 Central Bank Shocks Unleash Overnight Yield Crash, With Yuan On Verge Of Collapse

There is just one way to describe the plunge in bond yields overnight and the events behind it: the global race to the currency bottom is rapidly accelerating in its final lap with a global deflationary Ice Age(take a bow Albert Edwards) waiting on the other side.

The main event, of course, was the latest yuan fixing with the PBOC showing a clear sense of humor when it set the currency at 6.9996, laughably not to be confused with 7.0000 (for at least another 24 hours that is), but just a fraction of a percent away from the critical threshold, and weaker than the 6.9977 expected. The result was a resumption in the offshore yuan selloff, a hit to US equity futures and a drop in Treasury yields. Of course, once the PBOC does finally fix the yuan on the wrong side of 7, all bets are off and watch as the CNH crashes… as far as 7.70 according to SocGen, especially once Trump hikes tariffs to 25%.

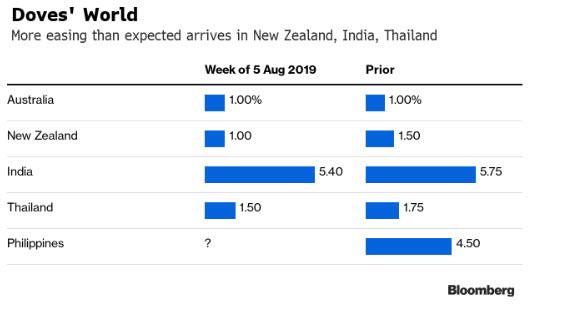

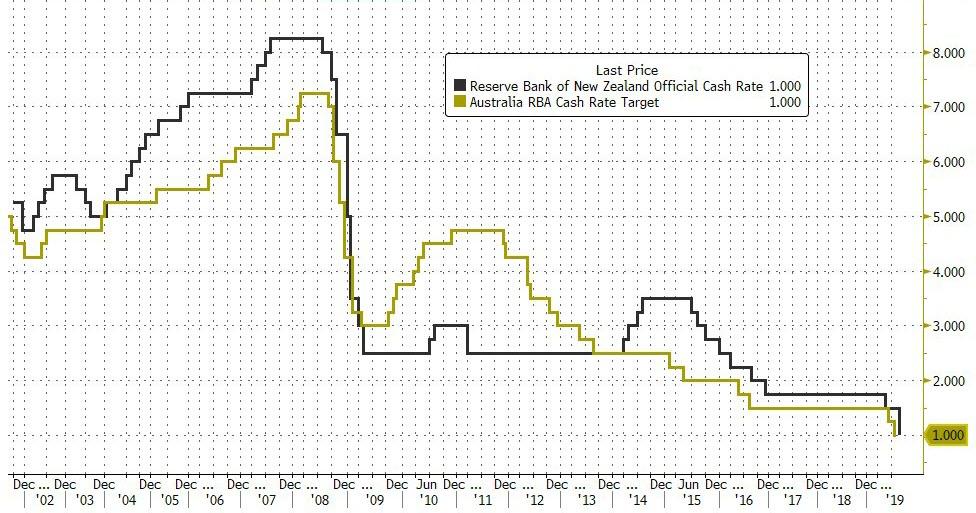

But there was much more in today’s iteration of the global race to the currency bottom, when first New Zealand, then India and finally Thailand shocked investors by being far more dovish than analysts expected. Indeed, the three Asian central banks delivered surprise interest-rate decisions on Wednesday as central bankers not only took aggressive action to counter a worsening global economy, but are now frontrunning each other – and the Fed – in doing so.

As noted last night, New Zealand’s central bank on Wednesday stunned investors by dropping its benchmark rate by 50 basis points, double the expected reduction and sending the kiwi tumbling. Thailand also surprised all but two in a survey of economists, cutting by 25 basis points. Finally, India’s central bank lowered its rate by an unconventional 35 basis points.

The response in the kiwi said it all, while the Australian dollar plunged to a ten year low in sympathy and on expectations that the OZ central bank would be next.

Some more details: the Reserve Bank of India lowered its benchmark rate by an unconventional 35 basis points to 5.4%, its fourth cut this year. New Zealand reduced its rate by 50 basis points to 1%; economists had forecast a 25 basis-point reduction. The Bank of Thailand’s rate cut was the first in more than four years. And it’s not over: the Philippines is set to decide monetary policy Thursday, with 24 of 26 economists predicting a 25-point cut. Bangko Sentral ng Pilipinas Governor Benjamin Diokno this week said there’s space for 50 basis points of easing before year’s end. The question is when will Australia join the party and cut to zero or below.

Traders and economists were shocked by the dovish three-peat:

- On New Zealand: “This was not what the market was expecting at all, it’s a shock to many. Considering the data isn’t terrible for New Zealand at all, this is an example of a central bank that’s looking beyond current data and trying to get ahead of the global slowdown.” – Kyle Rodda, analyst at IG Markets in Melbourne.

- On Thailand: “With the U.S.-China trade war spilling into currencies, more Bank of Thailand rate cuts may be forthcoming, especially as Bloomberg Economics expects the People’s Bank of China to cut rates later this year” – Tamara Mast Henderson, Bloomberg Asean economist

- On India: “The dovish tone in its policy statement signals further easingmight be in the pipeline to get the economy back on its feet” – Abhishek Gupta, Bloomberg India economist

A big picture recap from Chang Wei Liang, macro strategist of DBS, said it all: “Demand is easing globally, and inflation pressures look set to remain highly restrained. The dovish bias could remain somewhat entrenched, until there are signs of green shoots in Europe/China, and some meaningful reduction in trade anxiety.”

Still, the dovish moves by three Asian central banks showed that policy makers still have some power to surprise, and underscore the global shift toward easier policy even after the Federal Reserve‘s unexpectedly hawkish stance last week. Disappointing data may push the European Central Bank to turn toward easier monetary policies when it meets next month.

In short, a race to the bottom, and the US is badly lagging so expect either more rate cuts, more QE or direct currency intervention as Trump gets impatient with the ongoing dollar strength.

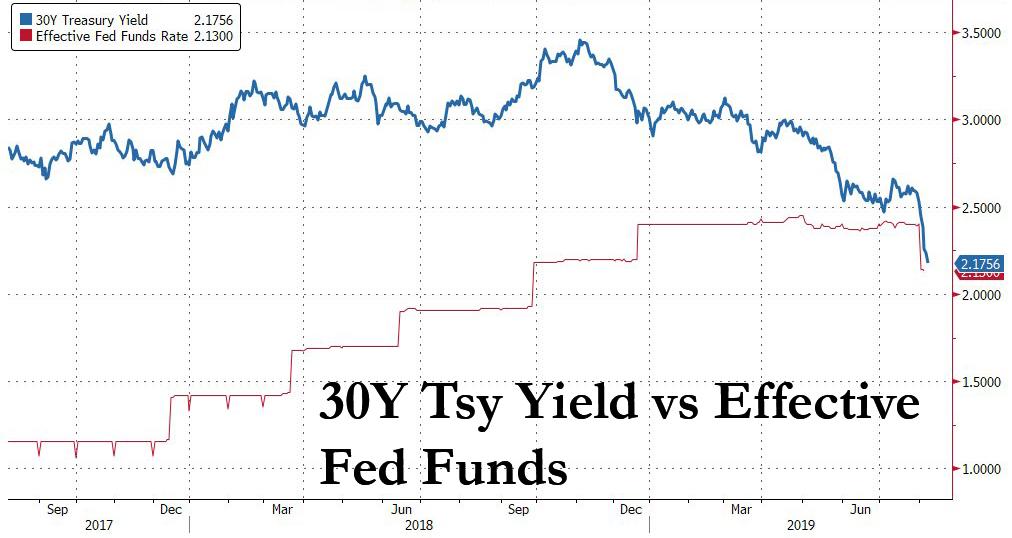

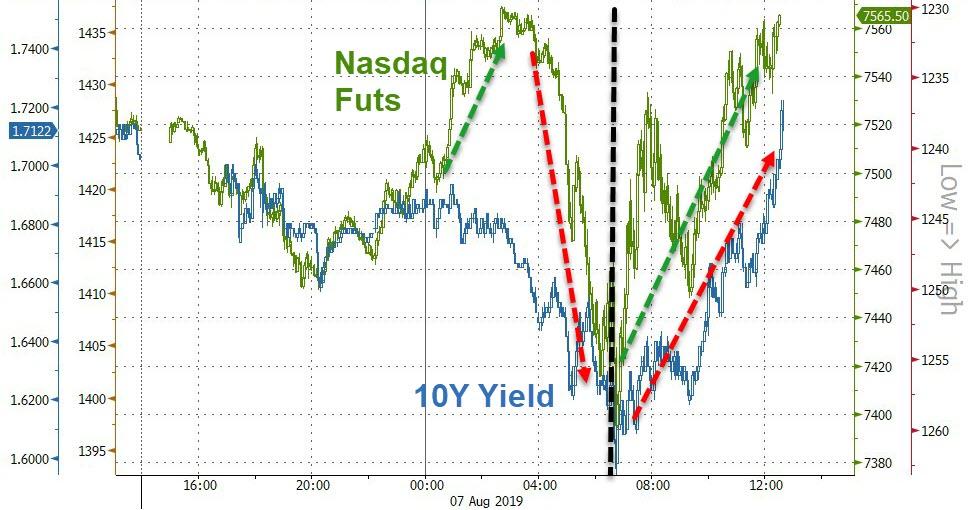

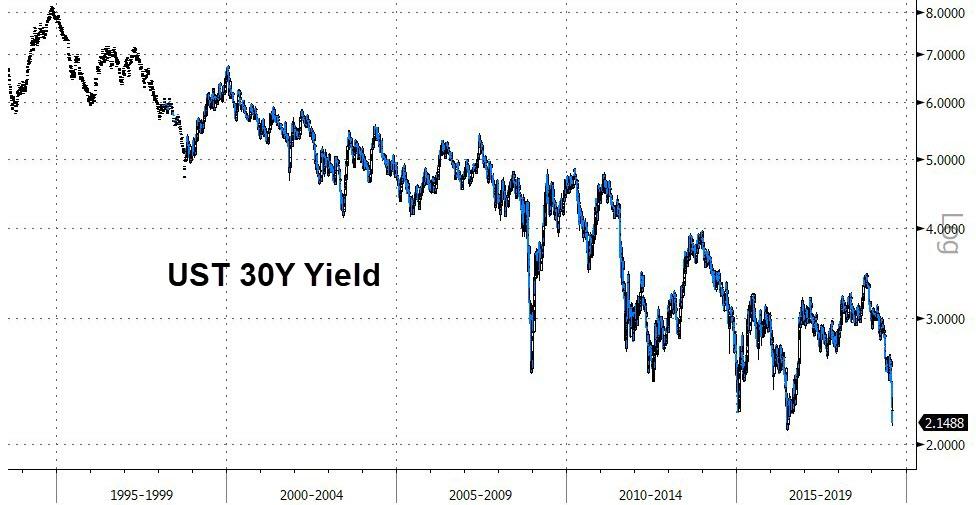

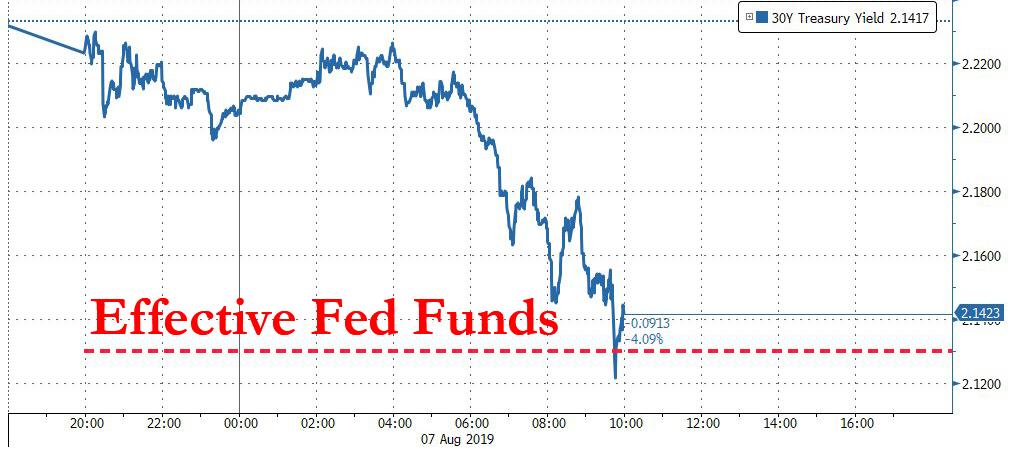

The central bank action, coupled with the ongoing currency war, roiled currencies and pushed bond yields to fresh record lows. The New Zealand dollar dropped more than 1% against the U.S. currency and the Thai baht slid 0.2%. But nowhere was the plunge in yield more visible than in the US where the 10Y dropped as low as 1.65%, while the 30Y Treasury tumbled to 2.16%, just 3 basis points above the effective Fed Funds rate, meaning the entire US curve is about to be inverted today.

Away from crashing yields, an eerie calm returned to stock markets on Wednesday as the dovish central bank overtures offset fears of an escalating currency war, thanks to some softer rhetoric from Washington. U.S. equity futures extended a rebound and European stocks rallied as markets continued to recover from a brutal selloff at the start of the week.

Caution was on display, however, as noted above with bonds soaring while currencies were roiled by a series of dovish central-bank moves in Asia.

U.S. equity futures turned higher following the dovish central bank three-peat in Asia, after slumping earlier following the PBOC fix.

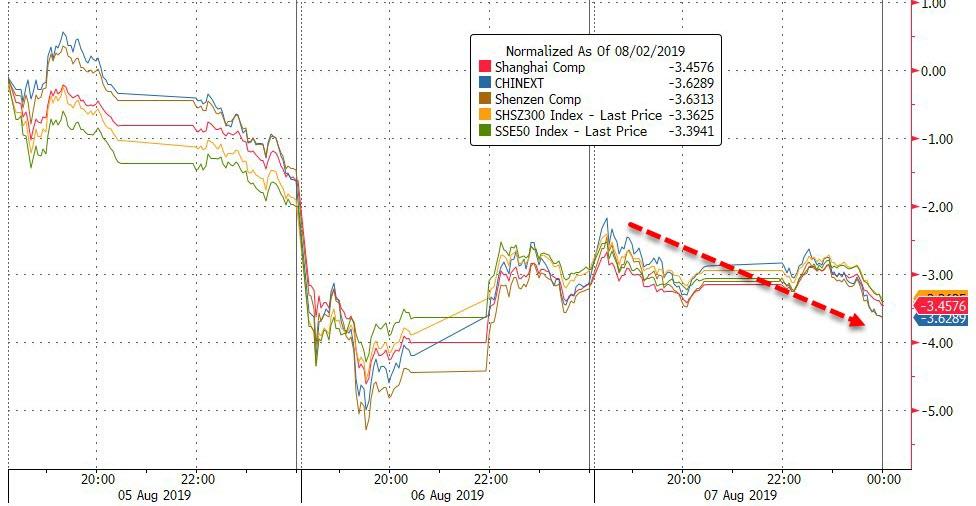

The MSCI world equity index rose 0.2%. The Stoxx Europe 600 index rose for the first time in four days, led by technology stocks after Microchip’s upbeat demand outlook. Chemicals producers advanced after Bayer and Lanxess agreed to sell their stakes in Currenta, while Glencore fell after its profits missed estimates. Shares were mixed but calmer in Asia, with Japanese stocks closing barely changed while equities in Shanghai declined.

But gold, the Japanese yen and government debt remained in high demand as investors remained wary of riskier assets.

Earlier in the session, Asian stocks inched higher, halting a five-day losing streak, after three central banks in the region delivered surprise rate cuts. Markets however were mixed, with Indonesia climbing and India retreating despite the bigger than expected rate cut. The Topix closed 0.1% higher, supported by Toyota Motor, Sony and Kao. The Shanghai Composite Index declined 0.3%, sliding for a sixth day, as the yuan weakened. Shanghai International Port and large financial firms were among the biggest drags. China’s central bank officials reassured foreign firms that the yuan won’t continue to drop significantly. New Zealand shares jumped in mid-afternoon trading after the central bank cut interest rates by more than economists had forecast. The Sensex fell 0.3% in a choppy session, as the Reserve Bank of India cut the annual economic growth forecast while reducing its benchmark interest rate by more than analysts had expected.

In FX, the star once again was the yuan, which dropped 0.3% to 7.0801 in offshore markets after China’s central bank set the daily fixing just a fraction stronger than the key level of 7 per dollar. The People’s Bank of China lowered the reference rate to 6.9996, an 11 year low. That leaves very little room for it to continue tracking the currency lower while setting the rate stronger than 7, a level that if breached could set the stage for further depreciation. “We had a little bit of recovery yesterday, but this morning we are seeing that stalling due to the PBOC fixing the dollar-yen higher again,” said Thu Lan Nguyen, FX strategist at Commerzbank. “It has caused markets to again be in a bit of a risk-off mode.”

Societe Generale SA said the yuan may fall to 7.7 per dollar if the U.S. ramps up tariffs on the nation’s goods, potentially bad news for other emerging markets that have been moving increasingly in lockstep with the currency. “There will be an inflection point for investors to dip their toes in and position for a tactical rally or to monetize carry in high yielders, but not now,” said Jason Daw, the head of emerging market strategy at Societe Generale in Singapore.

The kiwi slumped after the RBNZ surprised the market with a bigger-than-forecast cut. The Australian dollar fell to a 10 year low in sympathy as traders bet the RBA may follow suit. The yen led gains in the Group-of-10 currencies as the PBOC set fixing close to 7 per dollar. India’s rupee fluctuated and the Thai baht slipped after policy makers in both countries lowered borrowing costs. The euro declined with the pound and the U.S. dollar was steady.

Meanwhile, in rates yields were plunging across the board, with the 10-year Treasury yield falling through 1.7% and German rates dropping to a record after industrial production in the euro-region’s biggest economy registered the biggest annual decline in almost a decade. Semi-core bonds and most peripheral notes lead euro-area gains while curves flattened amid relentless search for yield. Money markets now price in more ECB rate cuts after weaker-than-forecast German data, while China fixes the yuan weaker, stoking trade tensions. Bunds rise as industrial production missed the median estimate; core debt underperforms as Germany’s sale of EU4b five-year sees oversubscription fall to 1.2x versus 1.5x prior and undersubcription of 0.78x after accounting for retentions. German 2s30s curve narrows 8bps to 69bps, the flattest since 2008. Money markets price 30bps of ECB rate cuts in June 2020 versus 28bps on Tuesday. Gilts outperform bunds by 1bp and short sterling strip bull flattens.

Traders remain on tenterhooks after Monday’s moves, which included the biggest one-day plunge in global equities since February 2018. An escalation in the trade war between the world’s two biggest economies continues to unnerve investors, even after China said recent yuan depreciation was decided by the market, not Beijing. “We’re likely to see perhaps another shoe drop as the week progresses because this is not getting fixed,” Kristina Hooper, the Atlanta-based chief global market strategist at Invesco Ltd., told Bloomberg TV. “There really is the potential for it to get worse from here.”

Meanwhile, Gold continued to soar and reached a six-year high of $1,489.76 per ounce. The Japanese yen rose 0.2% to 106.27, although that was still some way from levels seen on Monday when the trade war’s escalation panicked investors.

Finally, in commodity markets, oil prices slipped, with the potential for damage to the global economy and to fuel demand from the Sino-U.S. trade dispute casting a shadow over the market. Brent crude futures were at $58.79 a barrel by 0759 GMT, down 14 cents, or 0.05%, and trading near seven-month lows.

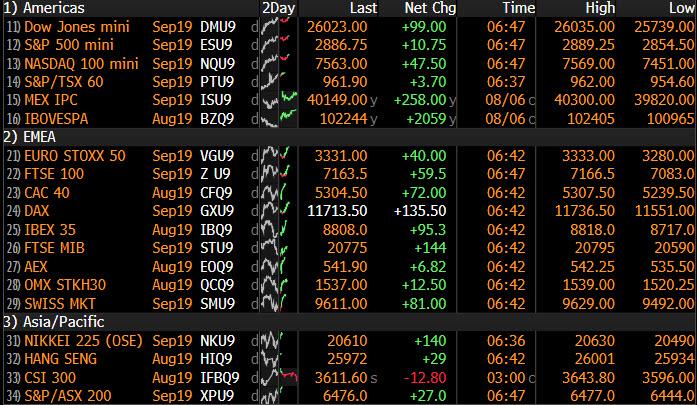

Market Snapshot

- S&P 500 futures up 0.3% to 2,884.25

- STOXX Europe 600 up 0.6% to 369.96

- MXAP up 0.08% to 150.96

- MXAPJ unchanged at 485.95

- Nikkei down 0.3% to 20,516.56

- Topix up 0.05% to 1,499.93

- Hang Seng Index up 0.08% to 25,997.03

- Shanghai Composite down 0.3% to 2,768.68

- Sensex down 0.3% to 36,874.41

- Australia S&P/ASX 200 up 0.6% to 6,519.46

- Kospi down 0.4% to 1,909.71

- German 10Y yield fell 2.9 bps to -0.565%

- Euro down 0.04% to $1.1194

- 10Y yield fell 5.3 bps to 1.162%

- Spanish 10Y yield fell 6.7 bps to 0.164%

- Brent futures down 0.4% to $58.68/bbl

- Gold spot up 0.9% to $1,487.18

- U.S. Dollar Index little changed at 97.72

Top Overnight News from Bloomberg

- Three central banks across Asia Pacific delivered surprise interest-rate decisions Wednesday as policy makers take aggressive action to counter a worsening global economy. New Zealand and India led with bigger-than-expected interest rate cuts, while Thailand’s 25-point reduction was a surprise to all but two in a Bloomberg survey of economists

- The escalating trade war between the U.S. and China is nudging the world economy toward its first recession in a decade with investors demanding politicians and central bankers act fast to change course

- U.S. is still expecting China to visit in September, says Larry Kudlow, the White House’s economic adviser. Things could change in respect to China tariffs, he adds. The U.S. will also take a “careful look” at whether China took steps to reverse the decline in the yuan. In Trump-Xi fight, both leaders make big bets that may backfire

- German industrial production registered its biggest annual decline in almost a decade, highlighting the severity of the trade- inflicted manufacturing slump in Europe’s largest economy

- U.K. house prices fell for a second month in July as the market continued to “tread water” amid economic uncertainty, mortgage lender Halifax said.

- Top European banks, such as Commerzbank, UniCredit, warned of weaker earnings as escalating trade tensions take a toll on their clients and the prospect of lower interest rates erodes their main source of income

- Michael Gove, the minister in charge of planning for a no-deal Brexit, blamed the European Union for failing to engage on a new agreement, deepening the diplomatic standoff between the two sides less than three months before the U.K. is due to leave the bloc

- Italy’s government won’t be able to contain the budget deficit below 2% if it’s going to deliver promised investments and tax cuts, Deputy Prime Minister Matteo Salvini said.

- North Korean leader Kim Jong Un oversaw the test- firing of a “new type” of guided missile Tuesday and the weapon should serve as a warning to the U.S. and South Korea as they conduct joint military drills, the state’s media said

- Gold futures rallied above $1,500 an ounce on sustained demand for the traditional haven as the U.S.-China trade war festers, global growth slows and central banks around the world ease monetary policy.

- Brent crude held losses after falling into bear market as lingering U.S.-China trade concerns dent the outlook for global demand

- The dovish turn sweeping the global economy gathered pace Wednesday as New Zealand shocked markets with a half-percentage point interest-rate cut, sending its currency tumbling

Asian equity markets traded mixed as the region observed caution despite the gains on Wall St. where stocks rebounded from their worst performance of 2019. ASX 200 (+0.6%) was initially indecisive as early gains were nearly wiped out by weakness in energy following a 2% drop in oil and with financials subdued after its largest lender CBA reported a decline in FY profits. However, Australia stocks were then boosted in late trade alongside outperformance in NZX 50 (+1.8%) after the RBNZ over-delivered with a surprise 50bps cut, while Nikkei 225 (-0.4%) was pressured as exporters digested a firmer currency and earnings updates. Hang Seng (U/C) and Shanghai Comp. (-0.3%) were lacklustre as trade concerns lingered and after the PBoC weakened the CNY reference rate to within a whisker of the 7.0000 ‘line in the sand’ level, although losses in the mainland were contained amid reports that China is to revise quota rules for farm product import tariffs in which it will remove soybean oil, rapeseed oil and palm oil import quotas. Finally, 10yr JGBs were underpinned as cautiousness spurred safe-haven demand and with global yields declining amid what some view as an ongoing race to the bottom among some of the world’s major central banks.

Top Asian News

- Singapore Air Picks Crucial Fight Against Emirates in India

- Aussie Dollar Slides to 10-Year Low as Traders Bet on Rate Cuts

- Papua New Guinea Asks for China’s Help to Ease Debt Burden

- Asia Surprises With Cuts in Global Race to the Monetary Bottom

- China Summons Hong Kong Officials to Shenzhen to Discuss Unrest

European equities have extended on opening gains [Eurostoxx 50 +1.3%] following on from a cautious Asia-Pac handover in which the antipodean indices cheered a deeper-than-forecast RBNZ OCR cut whilst upside Japan and China were capped by a firmer JPY and ongoing trade concerns. Major EU bourses are retracing recent losses with gains led by the DAX (+1.2%) as heavyweight Bayer (+7.0%) rallies on the back of its 60% stake sale in Currenta for EUR 1.17bln. The transaction also includes the minority shareholder Lanxess (+5.5%) who is poised to sell its 40% share for around EUR 700mln. Sector wise, healthcare names are lagging with the sector pressured by Novartis (-0.1%) after the US FDA stated that some data from early testing of its Zolgensma treatment was manipulated. Novartis opened lower by 2% before trimming losses. Other individual movers include UniCredit (-3.1%), Commerzbank (-3.1%) and ABN AMRO (-1.9%) post-earnings, in which the former cut its FY 19 revenue forecast and the latter stated it sees a bleaker margin ahead.

Top European News

- Commerzbank, UniCredit See Targets Under Threat From Low Rates

- Ex-HSBC Banker Pleads Guilty in $1.8 Billion French Tax Probe

- Muddy Waters’ Latest Short Is Woodford Holding Burford Capital

- Nordea’s Main Owner Opts to Cut Stake to Ease Capital Burden

In FX, NZD/AUD/INR/THB – The Kiwi is trying to claw back some lost ground, but remains the outright G10 underperformer in wake of the RBNZ’s shock decision to slash the OCR by 50 bp overnight against forecasts for -25 bp, and with Governor Orr indicating that there is more to come in post-policy meeting commentary. In fact, NIRP is not out of the realms of possibility as the Bank strives to hit its dual inflation and jobs target. Nzd/Usd slumped to lows around 0.6379 at one stage, but has subsequently reclaimed 0.6400+ status with key Fib support (0.6367) holding for now, while Aud/Nzd has rebounded further from sub-1.0300 levels to almost 1.0500 as Aud/Usd contains knock-on losses to circa 0.6678 even though RBA easing probability for September has risen in response to the more aggressive/pre-emptive RBNZ action. On that note, remarks from RBA’s Bullock later today may be pertinent. Conversely, the Rupee has strengthened in wake of an above consensus 35 bp reduction in benchmark rates from the RBI, and perhaps the vote split with 2 dissents for -25 bp plus the fact that the Bank has already administered 75 bp worth easing via 3 successive moves is being deemed as enough for now, even though the bias remains accommodative. Usd/Inr now circa 70.8000 within 71.000-70.5910 parameters in contrast to Usd/Thb nearer the top of a 30.9200-6900 range after a surprise ¼ point BoT rate cut and pledge to use other measures to curb Baht strength.

- JPY – Bucking broader trends again, and back on a firmer footing against the Dollar, as US Treasury yields retreat sharply from Tuesday’s fleeting retracement highs and the PBoC nudged the official Usd/CNY nearer 7.0000 to rekindle US-China trade concerns that seemed to abate a tad yesterday. Usd/Jpy is slipping back from just shy of 106.50 as the DXY continues to pivot 97.500 by virtue of greater gains vs riskier currency counterparts more than anything else as GOLD looks poised to breach Usd1500/oz amidst the escalation of trade wars and transition to conflicts of FX interests.

- CHF/GBP/EUR/CAD – All weaker vs the Greenback, or handing back recent gains, with the Franc approaching 0.9800 vs nearly 0.9700 and underlying safe-haven demand offset by prospects of SNB intervention at any time if the Chf appreciates too much. Indeed, Eur/Chf has also bounced further from recent lows between 1.0925-50 confines even though Eur/Usd remains top heavy on the 1.1200 handle amidst increasingly soft/negative Eurozone bond yields. Elsewhere, Cable is also struggling to maintain recovery momentum through 1.2200 and 0.9200 in Eur/Gbp cross terms amidst ongoing Brexit no deal/UK political risk, while the Loonie is straddling 1.3300 ahead of Canadian Ivey PMI prints.

- EM – Notwithstanding the wider swings in risk sentiment and specific factors impacting individual currencies and assets, the Lira revival continues, and the latest reversal in Usd/Try looks rather technical as key support ahead of 5.5000 has now given way.

In commodities, a day of respite thus far for the energy market following this month’s losses of almost 10%, pressured by the global oil demand outlook as the US-China saga intensifies. Yesterday saw the first of the monthly oil reports, the EIA STEO cut its 2019 global oil demand growth forecast by 70k BPD to a 1.0mln BPD Y/Y increase, albeit its 2020 forecast was raised slightly by 30k BPD. Investors will be keeping an eye on the IEA (Aug 6) and OPEC (Aug 16) Monthly reports for some harmony on the short-term global oil demand outlook. On the supply side, the weekly API crude stocks data showed a larger-than-forecast draw (-3.4mln vs. Exp. -2.8mln), the release did little to sway prices but may have underpinned the benchmarks in anticipation for today’s DoE data to confirm the drawdown (headline crude Exp. -2.845mln). Elsewhere, spot gold is inching closer to the key 1500/oz level with futures having already topped the level amid safe-haven inflows as US/China developments, global growth outlook and easing by global Central Banks. Spot gold printed a fresh 6yr peak at 1491/oz during early EU trade. Meanwhile, copper prices have rebounded off worst levels, albeit remain contained near 2yr lows with some support derived from news that Glencore is planning to shut its Mutanda cobalt and copper mine (which produced almost 200k tonnes of copper last year) by the end of 2019 due to lower cobalt prices impacting the economic viability of the project. Finally, Dalian iron ore prices extended its slide for a fifth session amid rising supply and weakening demand.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -1.4%

- 3pm: Consumer Credit, est. $16.1b, prior $17.1b

- 9:30am: Fed’s Evans Holds Media Breakfast in Chicago

DB’s Jim Reid concludes the overnight wrap

5 days after my accident and sitting down on a firm surface is starting to be a less harrowing experience again. Nevertheless my coccyx remains sore. I’m still waiting for the call from GAP who must surely want to use me in their advertising campaign as even with a few frays and tears, their trousers managed to hold together and keep my legs from having any external injuries even as I crash landed and skidded. All my cuts and scrapes were from my uncovered arms. I noticed that on Bloomberg’s MVP page, news of my accident has catapulted me several hundred hits ahead of Mr President for the week. So come on GAP, use the publicity and I’ll take a year’s supply of Baby GAP clothes in return.

Despite a fairly light day of newsflow, which might explain the order on Bloomberg’s MVP, markets staged an impressive rebound during the New York trading session yesterday, with the S&P 500 ultimately ending +1.30% higher. At the margin, comments from top Trump economic advisor Larry Kudlow helped to calm markets, with most of the gains coming after he spoke. Kudlow said that “The President and our team is planning for a Chinese visit in September” and “movement towards a good deal would be very positive and might change the tariff situation. But then again, it might not”. Despite the wide bid-offer in those remarks, it did seem that it represented a little shift in rhetoric from the White House. It will probably require something much more substantial to be sustainable though. In May/June markets recovered first because of a massive repricing of central banks expectations and then the news of the Trump/Xi meeting. It’s hard to believe that we could get the same impact from fresh central bank repricing which leaves us waiting for a trade de-escalation. This doesn’t feel that imminent but as ever we are a tweet away from a big shift in sentiment one way or another.

To put the recent moves in context, it’s worth highlighting a note DB’s Alan Ruskin did on Friday which looked at asset price performance through three previous periods where tariffs roiled financial markets (link here ). He found that the S&P 500 declined by a median of 10% and that Chinese equities were down less than the S&P. European equities held in a little better but were far from a great place to hide. As for bonds, in the past Bunds generally rallied more than Treasuries although clearly we’re now starting with the Bund curve mostly in negative territory. Growth sensitive commodities like Oil and Copper also struggled while interestingly the usual perceived safe haven assets like Gold and the Yen did not do as well as one might expect – although with the Fed expected to ease further, these assets might be more robust this time round. Food for thought in any case.

This morning in Asia markets are trading mixed with the Nikkei (-0.42%), Hang Seng (-0.37%) and Kospi (-0.15%) all lower while the CSI (+0.02%) and Shanghai Comp (-0.01%) are trading flat. The Japanese yen is up +0.368%, while the yield on 10yr JGBs in now trading below the lower end of the BoJ target range at -0.203% (-1.2bps). The PBoC has fixed the daily reference rate for the onshore yuan overnight at 6.9996 leading the currency to drop -0.34% to trade at 7.0434. Meanwhile, the RBNZ surprised the market by delivering a larger than expected rate cut of 50bps (market expectations were for a 25bps cut) thereby bringing the key policy rate to 1.0%. As a result, the New Zealand dollar (-1.92%, the largest daily decline in 4 months) and Australian dollar (-0.92%) are both trading weak this morning with the later sliding to a 10 year low. Elsewhere, futures on the S&P 500 are trading down -0.44%.

In other trade related news, the US Department of Commerce said yesterday that it will ask the US Customs and Border Protection to collect cash deposits from importers of wooden cabinets and vanities from China based on subsidy rates of as much as 229%. The preliminary response from the Commerce department came after a petition filed earlier this year by the American Kitchen Cabinet Alliance, alleging at least $2 billion in harm from Chinese shipments. The move is expected to affect $4.4bn in imported cabinets from China and while this is small numerically, the optics could weigh on the trade negotiations.

In addition Bloomberg has reported that the US is investigating hundreds of millions of dollars in financial transactions involving three big Chinese banks that allegedly helped finance North Korea’s nuclear weapons program, according to an appeals court opinion unsealed yesterday. Elsewhere, China’s Ministry of Commerce official said in an interview with MNI that regardless of the trade talks, China will gradually reduce its holdings of Treasuries, in order to diversify its foreign reserves while adding that “there are many options,” for China’s reserves, mentioning gold, other governments’ bonds, and other assets such as real estate and equities. The combination of this news and the uncertainty around escalating trade war has sent spot gold up this morning at 1485.15 (+0.72% ).

As for yesterday, the DOW and NASDAQ joined the S&P 500 rally, posting gains of +1.21% and +1.39% respectively, each bouncing off their morning lows amid higher-than-average trading volumes. That stemmed 6 consecutive daily losses for the S&P and NASDAQ and 5 for the DOW. Energy stocks (-0.06%) were the only sector to retreat, as Brent crude (-1.20%) slid into one definition of a bear market, as its level of $59.09 is now -20.76% off its April peak of $74.57. In Europe, equities actually traded fairly well through much of the session but a late dip saw bourses close in the red with STOXX 600 in particular down -0.47% and the trade sensitive DAX -0.78% after being up by a similar amount in the morning. The S&P 500 was only +0.38% higher at the European close so there is some catch-up likely. In bond markets, ten-year Treasuries rose as much as +6.4bps in line with the risk-on mood, but subsequently pared their gains to close near flat after a strong three-year auction. The 3y notes saw healthy demand and yielded the lowest in almost two years at 1.433%, ahead of today’s 10-year auction. The yield curve ended -1.1bps flatter at 12.1, which is just 1.1bps away from its cyclical low from December. In Europe, yields headed lower with Bunds (-2.0bps) hitting a new record low of -0.536%. Where will it all end!!

From negative yields to (relatively) High Yield. Overnight Nick has published a presentation based note looking at supply and demand trends in EUR HY. It includes the latest data and charts on issuance, redemptions, coupons and transitions between HY and IG (link here ).

Back to yesterday and it was a more typical summer day of light newsflow with the earlier slightly improved tone helped by a comment from the PBoC telling foreign firms that the CNY “won’t keep falling”. Our FX team have argued that some two-way and even a move potentially back below 7.0 in the near-term wouldn’t be a surprise even if the medium path might be further weakness. Indeed our strategists continue to expect additional weakness, forecasting a level of 7.3 versus the dollar for year-end 7.5 by end-2020. Deprecation on that scale would likely be a sticking point with the US, especially since White House trade advisor Peter Navarro took a victory lap on TV yesterday, crediting the stronger CNY fix as evidence that “they heard us.” He said “as soon as the president was firm – ‘You’re a currency manipulator’ – the Chinese announced that they’re stabilising.”

Meanwhile, two regional Fed presidents spoke and sent similar messages to Governor Brainard yesterday, that they are monitoring trade developments closely. St. Louis’s Bullard said that the Fed “cannot reasonably react to the day-to-day give-and-take of trade negotiations,” but he did also emphasize that the fall in rates over the last several months in anticipation of Fed rate cuts will take time to feed through to the economy. He stopped short of fully endorsing market pricing, however, saying that he has one more hike “pencilled in” for this year. Separately, San Francisco’s Daly noted that trade uncertainty has “re-emerged” and said that “I’m really focusing my attention (on) these headwinds.” Bullard is a voting FOMC member this year, though Daly does not vote until 2021.

Meanwhile, there wasn’t much to report in terms of data yesterday. Early on Germany factory orders surprised to the upside in June posting a +2.5% mom rise (vs. +0.5% expected) after a -2.0% fall the previous month (though that was revised up +0.2pp from the initial print). On the other hand, Swedish industrial production, sometimes viewed as a leading indicator for European manufacturing, fell -0.7% yoy, matching its slowest pace since 2016. In the US the sole release was the albeit outdated June JOLTS report which showed that the job opening report slipped to 4.6% from 4.7% in the month prior while the pace of hiring stood pat at 3.8%.

Looking at the day ahead, this morning data releases include June industrial production in Germany, June trade balance in France and July house prices data in the UK. In the US the sole data release is the June consumer credit release. Away from that earnings releases include CVS Health Corp and Glencore.

3A/ASIAN AFFAIRS

I)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 8.88 POINTS OR 0.32% //Hang Sang CLOSED UP 20.79 POINTS OR 0.08% /The Nikkei closed DOWN 68.75 POINTS OR 0.33%//Australia’s all ordinaires CLOSED UP .64%