GOLD:$1498.80. DOWN $4.20(COMEX TO COMEX CLOSING

Silver: $16.95 DOWN 23 CENTS (COMEX TO COMEX CLOSING)/

Closing access prices:

Gold : $1501.65

silver: $16.94

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 3/6

EXCHANGE: COMEX

CONTRACT: AUGUST 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,507.300000000 USD

INTENT DATE: 08/07/2019 DELIVERY DATE: 08/09/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

118 H MACQUARIE FUT 1

661 C JP MORGAN 3

686 C INTL FCSTONE 4

737 C ADVANTAGE 2

880 H CITIGROUP 2

____________________________________________________________________________________________

TOTAL: 6 6

MONTH TO DATE: 4,406

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 6 NOTICE(S) FOR 600 OZ (0.0186 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 4406 NOTICES FOR 440,600 OZ (13.704 TONNES)

SILVER

FOR JULY

326 NOTICE(S) FILED TODAY FOR 1,630,000 OZ/

total number of notices filed so far this month: 1458 for 7,290,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 11882 DOWN 89

Bitcoin: FINAL EVENING TRADE: $ 11613 DOWN 360

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A GIGANTIC SIZED 4879 CONTRACTS FROM 239,270 UP TO 244,169 AND WITHIN A HAIR OF A NEW COMEX OI RECORD, WITH THE 74 CENT GAIN IN SILVER PRICING AT THE COMEX.

TODAY WE ALMOST SURPASSED LAST YEAR’S AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR AUGUST, 2961 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 2961 CONTRACTS. WITH THE TRANSFER OF 2961 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2961 EFP CONTRACTS TRANSLATES INTO 14.805 MILLION OZ ACCOMPANYING:

1.THE 74 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

7.840 MILLION OZ INITIAL STANDING IN AUGUST.

WE HAD ATTEMPTED COVERING OF SHORTS AT THE SILVER COMEX YESTERDAY WITH ZERO SUCCESS..AND WE HAD CONSIDERABLE SPREADING ACCUMULATION.

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF SEPTEMBER FOR SILVER.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF AUGUST BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF AUGUST:

10,329 CONTRACTS (FOR 6 TRADING DAYS TOTAL 10,329 CONTRACTS) OR 51.65 MILLION OZ: (AVERAGE PER DAY: 1721 CONTRACTS OR 8.605 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 51.65 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 7.37% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1364.16 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4879, WITH THE 74 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A VERY STRONG SIZED EFP ISSUANCE OF 2961 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED AN ATMOSPHERIC AND CRIMINALLY SIZED: 7840 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2961 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 4879 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 74 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $17.18 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.220 BILLION OZ TO BE EXACT or 175% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 326 NOTICE(S) FOR 1,630,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

AND NOW WE ARE WITHIN A WHISKER OF ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,169 BUT THIS TIME THE PRICE OF SILVER YESTERDAY WAS $17.18 AND HIGHER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 7.840 MILLION OZ

- CLOSE TO THE RECORD OPEN INTEREST IN SILVER 244,169 CONTRACTS (OR 1.228 BILLION OZ/, THE PREVIOUS RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL 351 CONTRACTS, TO 599,965 ACCOMPANYING THE $31.00 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING ACCUMULATION HAS NOW COMMENCED IN EARNEST FOR SILVER..AS THE LIQUIDATION PHASE FOR COMEX OI GOLD HAS NOW STOPPED

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY STRONG SIZED 9883 CONTRACTS:

AUGUST 2019: 0 CONTRACTS, DEC> 9883 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 599,965,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 9532 CONTRACTS: 351 CONTRACTS DECREASED AT THE COMEX AND 9883 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 9532 CONTRACTS OR 953,200 OZ OR 29.647 TONNES. YESTERDAY WE HAD A STRONG GAIN OF $31.00 IN GOLD TRADING….AND WITH THAT STRONG GAIN IN PRICE, WE HAD A GIGANTIC GAIN IN GOLD TONNAGE OF 29.64 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER TRYING TO CONTAIN THE PRICE RISE TO NO AVAIL.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST : 75,503 CONTRACTS OR 7,550,300 oz OR 234.84 TONNES (6 TRADING DAY AND THUS AVERAGING: 12,583 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAY IN TONNES: 234.84 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 234.84/3550 x 100% TONNES =6.61% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 3746.09 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A SMALL SIZED DECREASE IN OI AT THE COMEX OF 351 DESPITE THE HUGE PRICING GAIN THAT GOLD UNDERTOOK YESTERDAY($31.00)) //.WE ALSO HAD A HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 9,883 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 9,883 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 9532 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

9883 CONTRACTS MOVE TO LONDON AND 351 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 29.64 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED WITH THE HUGE GAIN IN PRICE OF $31.00 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAVE NOW STOPPED WITH SPREADING LIQUIDATION OF GOLD OI CONTRACTS AND THIS HAS MORPHED INTO AN ACCUMULATION OF OI CONTRACTS IN SILVER.

we had: 6 notice(s) filed upon for 600 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $4.20 TODAY//(COMEX-TO COMEX)

two transactions!! what an absolute farce!

this morning

a)A MONSTROUS CHANGE IN GOLD INVENTORY AT THE GLD

A PAPER DEPOSIT OF 8.50 TONNES OF GOLD ADDED TO THE GLD

this evening:

b) A MONSTROUS WITHDRAWAL OF 5.57 TONNES FROM THE GLD

INVENTORY RESTS AT 839.85 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 23 CENTS TODAY:

A BIG CHANGE IN SILVER INVENTORY AT THE SLV

A DEPOSIT OF 1.409 MILLION OZ INTO THE SLV

/INVENTORY RESTS AT 363.311 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY AN ATMOSPHERIC AND CRIMINALLY SIZED 4879 CONTRACTS from 239,290 UP TO 244,169 AND WITHIN A WHISKER OF A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORDED HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET EXCEPT TODAY AS WE HAD A RISING PRICE..OUR SHORT DERIVATIVE BANKERS ARE NOW IN DEEP TROUBLE AS THEY ARE TERRIBLY OFFSIDE AND NEED ASSISTANCE FROM THE GOVERNMENT (FED) TO PROVIDE THE NECESSARY COLLATERAL TO CARRY THAT SHORT POSITION…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR AUGUST: 0, FOR SEPT. 2961 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2961 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 4879 CONTRACTS TO THE 2961 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 7840 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 29.64 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ ;AUGUST AT 7.840 MILLION OZ//

RESULT: A GIGANTIC SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 74 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 2961 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

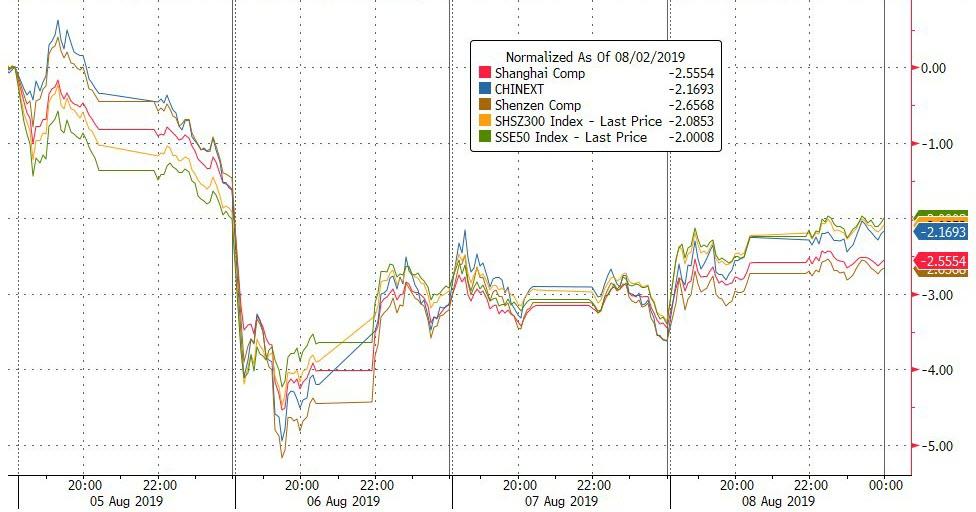

SHANGHAI CLOSED UP 25.87 POINTS OR 0.93% //Hang Sang CLOSED UP 123.74 POINTS OR 0.48% /The Nikkei closed UP 76.79 POINTS OR 0.37%//Australia’s all ordinaires CLOSED UP .82%

/Chinese yuan (ONSHORE) closed DOWN at 7.0466 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0466 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0740 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

i)China

Although China fixes its yuan weaker than 7 for the first time it was a little better than expected and that was comforting to the markets

(zerohedge)

4/EUROPEAN AFFAIRS

i)Italy

Salvini is set to remove his coalition partner unless he gets his way. If he does not expect new elections and that will throw Italy in chaos

(zerohedge)

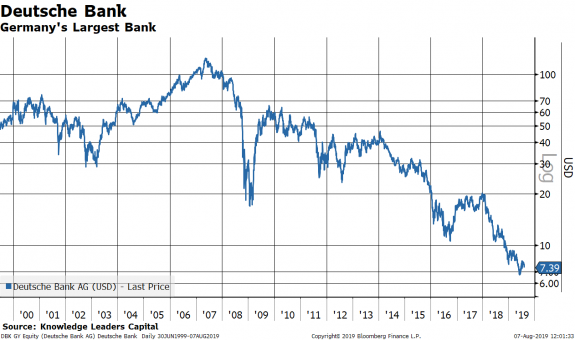

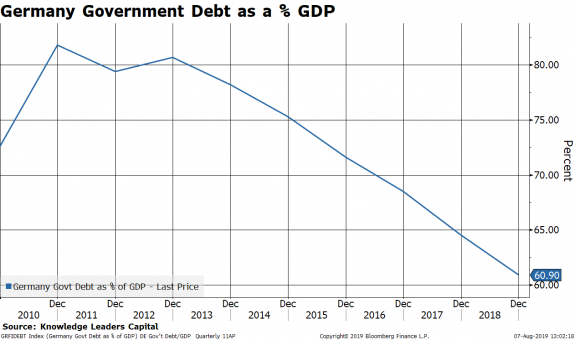

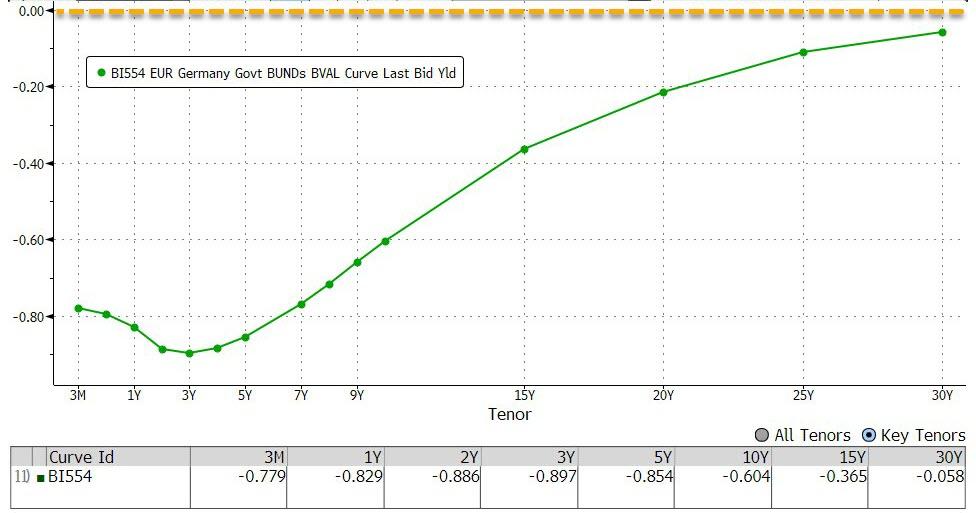

ii)Germany

A good looks at the GERMAN BANKING SYSTEM. German banks (the 3 major banks) has assets equal to 100% of German GDP. Germany’s debt to GDP is fallen from 80% down to 60% and this is making it harder for the ECB to purchase bonds to stimulate the European economy. This is why Draghi will try and lower rates again and this is a killer for the banks.

(zerohedge)

iii)Germany

7. OIL ISSUES

8 EMERGING MARKET ISSUES

a)It officially begins: Trump orders a blockade on food shipments coming from the Panama Canal to Venezuela

(zerohedge)

b)India/Pakistan

Heavy clashes erupt between these two nuclear powers

(zerohedge)

9. PHYSICAL MARKETS

i)China’s official holdings increase but this gold has already been mined and stored at banks. Gradually China takes that gold and it becomes official gold

(Bloomberg/GATA)

ii)Sprott has now done a deal to Tocqueville gold funds with its managers.

(Barrons/GATA)

iii)What has changed during these past six years?. Chris Powell comments on this

(Chris Powell/GATA)

iv)Bill Murphy of GATA interviewed by Kaiser of Reluctant Preppers

(GATA/Reluctant Preppers)

v)Chris Marcus interviews me

(Chris Marcus, Arcadia Economics/Harvey Organ)

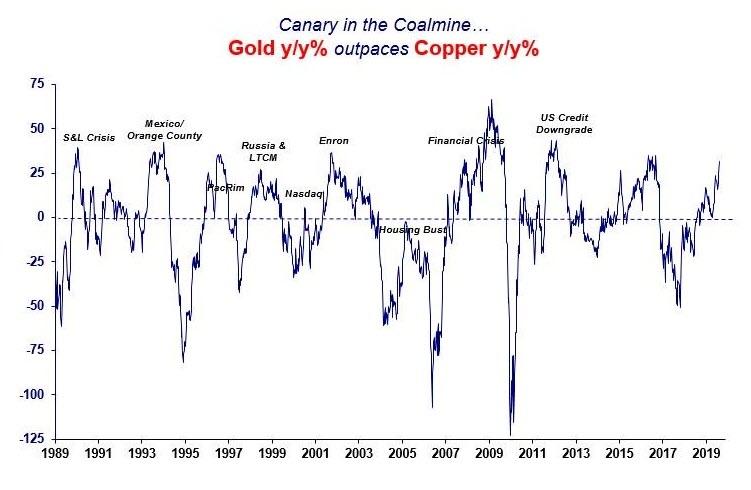

vi)A terrific commentary from Mish Shedlock on gold. He compares the percentage change of gold vs the %age change in the price of copper and the former is rising much faster than the latter. Gold is reacting to fears that central banks are out of control and do not know how to fix things

vii)China adds 10 tonnes of gold to its official levels which is quite laughable. They produce around 407 tonnes per year or 33 tonnes per year. Thus they have decided to add only 1/3 of their production to official levels and store the 2/3 with their state banks. The big question was Poland: they added 100 tonnes this week. Where did this amount come from? Poland produces only 3 tonnes of gold per year so this gold was acquired no doubt from London

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

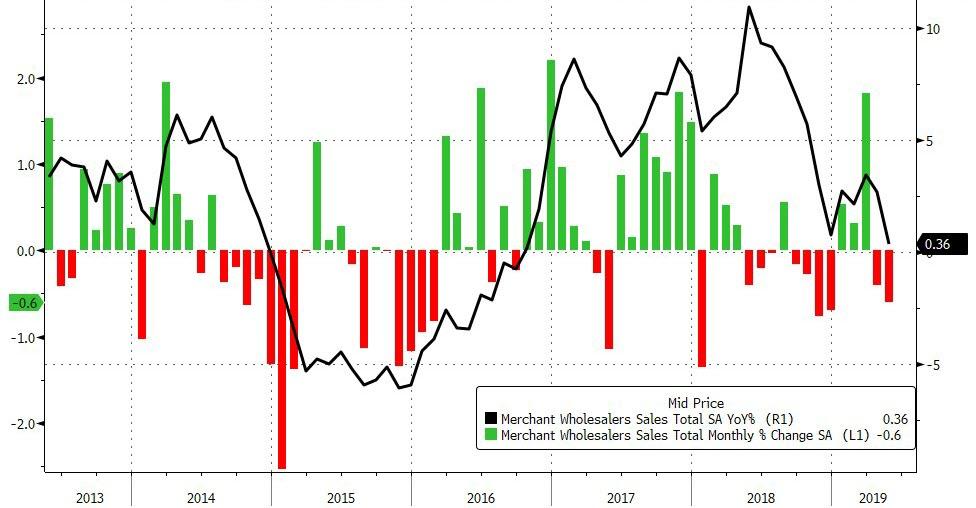

THIS IS A VERY IMPORTANT HARD DATA!! Wholesale inventories and wholesale sales growth both plunge and that will be a huge negative to GDP numbers.

(zerohedge)

iii) Important USA Economic Stories

a)Warren Buffet is badly bruised this morning as Kraft Heinz crashes are delayed results. It seems that many people are moving away from processed foods.

(zerohedge)

b)Trump bashing the Fed again on the strong dollar. He wants it lower so his manufacturing industries can compete

c)This is going to be interesting: Trump now readies an executive order cracking down hard on social media censorship of conservatives(Michael Snyder)

d)Full scale war has just erupted as Trump will hold off on a decision on licenses for USA companies doing business with Huawei. American companies need a special license to supply Huawei and Trump is just not going to give to them. The yuan tanks, the futures have just tanked..

iv) Swamp commentaries)

(Gates /Epoch Times)

b)One complete joke: Now McCabe sues the Dept of Justice and the FBI over his firing

(zerohedge)

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; nil oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 132,756 CONTRACTS (we had some spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 207,669 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 207,669 CONTRACTS EQUATES to 1,035 million OZ 147% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -.1.06% ((AUGUST 8/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.30% to NAV (AUGUST 5/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 14.85 TRADING 14.35/DISCOUNT 3.34

END

And now the Gold inventory at the GLD/

AUGUST 8: WITH GOLD DOWN $4.20: TWO TRANSACTIONS: A)A MONSTROUS PAPER DEPOSIT OF 8.50 TONNES WAS ADDED TO THE GLD/INVENTORY RESTS AT 845.42 TONNES b) A HUGE WITHDRAWAL OF 5.59 TONNES FROM THE GLD//INVENTORY RESTS AT 839.85 TONNES…ABSOLUTE FRAUD!

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 29/WITH GOLD UP $1.00: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 6.75 TONNES INTO THE GLD INVENTORY///INVENTORY RISES TO 824.89 TONNES

JULY 26/WITH GOLD UP $4.50: A HUGE INVENTORY WITHDRAWAL OF 4.09 TONNES OF PAPER GOLD LEAVES THE GLD/INVENTORY RESTS AT 818.14 TONNES

JULY 25.2019: WITH SILVER DOWN 19 CENTS: ANOTHER PAPER WITHDRAWAL OF 1.17 MILLION OZ/INVENTORY REST AT 358.213 MILLION OZ

JULY 24…A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A GAIN OF 1.685 MILLION OZ/INVENTORY RESTS AT 359.383 MILLION OZ

JULY 23/2019: WITH SILVER UP 5 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.221 MILLION PAPER OZ ADDED INTO THE GLD INVENTORY//INVENTORY RESTS AT 357.698 MILLION OZ////

JULY 22.2019/WITH SILVER UP 21 CENTS TODAY: A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 8.939 MILLION OZ ADDED TO THE SLV INVENTORY/INVENTORY RESTS AT 355.919 MILLION OZ//

JULY 19/WITH GOLD DOWN $1.00: A MASSIVE DEPOSIT OF 11.44 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 814.62

JULY 18/WITH GOLD UP $5.55 TODAY: A BIG PAPER DEPOSIT OF 3.81 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 803.18 TONNES

JULY 17/WITH GOLD UP $11.35 TODAY: A BIG WITHDRAWAL OF 1.17 TONNES FROM THE GLD//INVENTORY RESTS AT 799.37 TONNES

JULY 16: WITH GOLD DOWN $2.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 15: WITH GOLD UP $1.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 12/WITH GOLD UP $5.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 11.WITH GOLD DOWN $5.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 10//WITH GOLD UP $11.65 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER GOLD DEPOSIT OF 6.46 TONNES/INVENTORY RESTS AT 800.54 TONNES

JULY 9/WITH GOLD UP 70 CENTS, A HUGE PAPER WITHDRAWAL OF 2.89 TONNES WHICH WAS USED IN THE FUTILE RAID ON GOLD AND SILVER THIS MORNING//INVENTORY RESTS AT 794.08 TONNES

JULY 8/ WITH GOLD DOWN 35 CENTS A HUGE WITHDRAWAL OF 1.47 TONNES FROM THE GLD/INVENTORY FALLS TO 796.97 TONNES

JULY 5TH/WITH GOLD DOWN $19.50/NO CHANGES IN GOLD INVENTORY AT THE GLD//INV RESTS AT 798.44 TONNES

JULY 3// WITH GOLD UP $12.60 TODAY A SURPRISE WITHDRAWAL OF 1.76 TONNES FROM THE GLD//INVENTORY RESTS AT 798.44

JULY 2. WITH GOLD UP $18.90 A HUGE “PAPER” DEPOSIT OF 6.16 TONNES INTO THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 1: WITH GOLD DOWN $24.70 A HUGE “PAPER GOLD” WITHDRAWAL OF 1.76 TONNES FROM THE GLD/INVENTORY RESTS TONIGHT AT 794.04 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

AUGUST 8/2019/ Inventory rests tonight at 839.85 tonnes

*IN LAST 638 TRADING DAYS: 95.55 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 538 TRADING DAYS: A NET 70,99 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

AUGUST 8/WITH SILVER DOWN 23 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT: 1.409 MILLION OZ INTO INVENTORY///INVENTORY RESTS AT 363.311 MILLION OZ//

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 29/2019: WITH SILVER UP 4 CENTS TODAY: A SMALL WITHDRAWAL OF 468000 OZ FROM THE SLV/INVENTORY LOWERS TO 356.715 MILLION OZ//

JULY 26.2019: WITH SILVER DOWN 2 CENTS TODAY: A HUGE 1.03 MILLION OZ OF PAPER SILVER LEAVES THE SLV/INVENTORY LOWERS TO 357.183 MILLION OZ//

JULY 25.2019: WITH SILVER DOWN 19 CENTS: ANOTHER PAPER WITHDRAWAL OF 1.17 MILLION OZ/INVENTORY REST AT 358.213 MILLION OZ

JULY 24…A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A GAIN OF 1.685 MILLION OZ/INVENTORY RESTS AT 359.383 MILLION OZ

JULY 23/2019: WITH SILVER UP 5 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.221 MILLION PAPER OZ ADDED INTO THE GLD INVENTORY//INVENTORY RESTS AT 357.698 MILLION OZ////

JULY 22.2019/WITH SILVER UP 21 CENTS TODAY: A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 8.939 MILLION OZ ADDED TO THE SLV INVENTORY/INVENTORY RESTS AT 355.919 MILLION OZ//

JULY 19/WITH SILVER FLAT TODAY: ANOTHER MONSTROUS PAPER DEPOSIT OF 3.276 MILLION OZ ENTERS THE SLV//WHAT A MASSIVE FRAUD//INVENTORY RESTS AT 346.980 MILLION OZ

JULY 18/WITH SILVER UP 24 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.668 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 343.704 MILLION OZ//

JULY 17: WITH SILVER UP ANOTHER 29 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.518 MILLION OZ/INTO THE SLV INVENTORY///INVENTORY RESTS AT 341.036 MILLION OZ//

JULY 16: WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY: 15 WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY 12/WITH SILVER UP 10 CENTS: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 11/NO CHANGE IN SILVER INVENTORY

JULY 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 9/WITH SILVER UP A SMALL 7 CENTS A GIGANTIC INVENTORY GAIN OF 4.026 MILLION OZ/ INVENTORY RESTS AT 332.518 MILLION OZ AND NOW IT SHOULD BE QUITE CLEAR THAT THE SLV ( AND GLD ARE FRAUDS)

JULY 8/WITH SILVER UP 7 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 328,492 MILLION OZ

JULY 5/WITH SILVER DOWN 32 CENTS WE STRANGELY HAD A HUGE INVENTORY GAIN OF 2,234 MILLION OZ//INVENTORY RESTS AT 328.492 MILLION OZ

JULY 3 WITH SILVER UP 10 CENTS A HUGE INCREASE IN INVENTORY..INVENTORY RESTS AT 326.151 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 323.330 MILLION OZ//

JULY 1/ WITH SILVER DOWN 16 CENTS: A SURPRISING DEPOSIT OF 936,000 OZ INTO THE SLV/INVENTORY RESTS TONIGHT AT 323.330 MILLION OZ/

AUGUST 8/2019:

Inventory 363.311 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.12/ and libor 6 month duration 2.05

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .07

XXXXXXXX

12 Month MM GOFO

+ 1.94%

LIBOR FOR 12 MONTH DURATION: 1.98

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.04

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Jim Rogers Video Interview: Buy Gold Coins and Silver Coins as Global Crisis Is Coming

◆ “Get knowledgeable and get prepared as this crisis is going to be the worst in my life time”

◆ “I own physical gold and silver coins … everyone should own them”

◆ “I own Chinese, Russian, American, Australian, Austrian silver coins” and “I own UK and other gold coins”

◆ “Singapore has been and is a very safe location for storage, Switzerland is too, Austria is too, Liechtenstein is too, so far”

◆ “The Generals and “all the elites” have “their gold stored in Switzerland”

◆ The next crisis is going to happen so fast that people may not have time to react

◆ The fiat currency experiment of the last 50 years is coming to a brutal end

◆ “If you know a lot about silver and gold, you might allocate 90%”

◆ Gold and silver futures will be best in terms of returns, “if the financial and futures markets are still functioning”

◆ Gold and particularly silver are set to surge even more in the coming months and years

◆ The fiat currency experiment of the last 50 years is coming to a brutal end

◆ Gold and silver are not rising rather all fiat currencies are falling versus the precious metals

◆ This is seen in the surge of gold in all currencies to record nominal highs

◆ Gold’s record high in British pounds shows sterling is “falling apart” as people “are losing confidence in sterling”

◆ “Don’t sell your silver gold and silver now even though it may go down for a while”

◆ “If you do not know much about gold, please don’t invest too much in it”

◆ “I have made plenty of mistakes” …”all kinds” …”do you want to hear about my first wife!?”

◆ “Go out and have children … my children float my boat now more than anything else”

◆ Listen and Watch Jim Rogers Interview Here

NEWS & COMMENTARY

Silver prices book largest daily rise in 3 years as gold ends 2.4% higher

Gold touches 6-year high; Rush into US bonds sinks global stock markets

China Scoops Up More Gold for Reserves During Trade War

Growing fears of world recession haunt global markets

Fed’s Evans signals support for reducing borrowing costs further

Central banks around the world are surprising markets with aggressive rate cuts

Bonds and gold are sending danger signals to the stock market

Brexit: 8 Serious Risks To Germany and the EU

Gold hits highs in many currencies

Buy More Gold Now, Société Générale – 13% to 14% Allocation for a Balanced Portfolio

Gold Prices via LBMA (AM/ PM Fix – USD, GBP & EUR)

07-Aug-19 1487.65 1506.05, 1225.82 1239.33 & 1330.11 1341.44

06-Aug-19 1461.85 1465.25, 1199.59 1201.21 & 1304.85 1311.11

05-Aug-19 1457.45 1465.25, 1199.92 1203.85 & 1307.92 1310.23

02-Aug-19 1436.05 1441.75, 1184.17 1187.28 & 1294.02 1298.44

01-Aug-19 1406.40 1406.80, 1161.12 1161.74 & 1273.35 1273.29

31-Jul-19 1430.55 1427.55, 1175.48 1167.45 & 1283.20 1281.37

30-Jul-19 1428.45 1425.90, 1173.47 1171.95 & 1281.75 1279.60

29-Jul-19 1418.95 1419.05, 1150.91 1157.94 & 1275.78 1275.30

26-Jul-19 1418.25 1420.40, 1140.27 1144.70 & 1273.02 1275.95

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

China’s official holdings increase but this gold has already been mined and stored at banks. Gradually China takes that gold and it becomes official gold

(Bloomberg/GATA)

China scoops up more gold for reserves during trade war

Submitted by cpowell on Wed, 2019-08-07 13:49. Section: Daily Dispatches

By Ranjeetha Pakiam

Bloomberg News

Wednesday, August 7, 2019

There’s a powerful constant amid the to-and-fro of the U.S.-China trade war as currency policy gets dragged into the standoff between the world’s two top economies: Beijing wants more gold in its reserves.

China’s central bank expanded gold reserves again in July, pressing on with a run that stretches back to December. The People’s Bank of China raised holdings to 62.26 million ounces from 61.94 million a month earlier, according to data on its website. In tonnage terms, the inflow was close to 10 tons, following the addition of about 84 tons in the seven months to June. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-08-07/as-trade-war-runs-hot.

end

Sprott has now done a deal to Tocqueville gold funds with its managers.

(Barrons/GATA)

Sprott will acquire Tocqueville gold fund and its managers

Submitted by cpowell on Wed, 2019-08-07 16:28. Section: Daily Dispatches

As Gold Surges, a Gold Fund Manager Gets Acquired

By Ben Walsh

Barron’s, New York

Wednesday, August 7, 2019

https://www.barrons.com/articles/as-gold-surges-a-gold-fund-manager-gets…

Central banks around the world taking dovish turns, an intensifying U.S.-China trade war, and revved-up stock-market volatility have pushed gold over $1,500 an ounce for the first time since 2013.

And it isn’t just the precious commodity that;s getting a boost right now — gold funds seem to be feeling the optimism as well. Sprott, an alternative-asset manager with about $8 billion in assets, said today that it is acquiring Tocqueville Asset Management’s gold strategies business.

…

The companies said in a statement that Sprott would pay up to $50 million in cash and stock to acquire gold strategies and institutional accounts with $1.9 billion in assets under management based on Tuesday’s market prices, including the Tocqueville gold fund. The Tocqueville gold portfolio management team will join Sprott when the deal closes, which is expected in January 2020.

Sprott President Whitney George said that the Tocqueville team is “among the world’s most respected gold equities managers and we have enjoyed an excellent working relationship during the planning and launch of our joint venture over the past year.”

“Sprott has a globally recognized brand with a dedicated precious metals platform and a long history in the sector,” said John Hathaway, Tocqueville’s senior portfolio manager.

* * *

Join GATA here:

New Orleans Investment Conference

Hilton New Orleans Riverside Hotel

Friday-Monday, November 1-4, 2019

https://neworleansconference.com/noic-promo/powellgata/

* * *

Help keep GATA going

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

end

What has changed during these past six years?. Chris Powell comments on this

(Chris Powell/GATA)

Central banks change their policy on gold but not their madness

Submitted by cpowell on Wed, 2019-08-07 17:09. Section: Daily Dispatches

1:19p ET Wednesday, August 7, 2019

Dear Friend of GATA and Gold:

Over a weekend in April six years ago, without any corresponding news, the gold price was smashed out of the blue for nearly $200. For months before the smash analysts often said that China had put a floor under the gold price, buying whatever it could to hedge its U.S. dollar exposure without pushing gold’s price up too much.

That analysis made sense, since, with its estimated $3 trillion in foreign-exchange reserves, mostly in U.S. dollar instruments, China was in a position to control any market on the planet.

…

But over that weekend in April six years ago the supposed Chinese floor under gold disappeared. Regardless of how much gold China had been buying, no collapse of that size could have happened in any major international market without China’s cooperation or consent.

The gold smash was clearly a coordinated intervention by central banks. So soon there was speculation that the central banks had decided that the gold price was getting away from them too fast, particularly for China’s dollar-hedging purposes.

Now, over the last week, gold and silver prices have been spiking dramatically and unprecedentedly, and central bank intervention against gold seems to be diminishing. This is suggested by the gold-trading footnotes in the monthly reports of the Bank for International Settlements, as well as by the lapsing of the European Central Bank’s gold sales agreement with its members. The decline in intervention may result in part from the exhaustion of central bank gold available for intervention, just as the collapse of the London Gold Pool in 1968 was caused by exhaustion of the gold reserves of the participating Western central banks.

So who is buying the gold?

Central banks not so closely allied with the United States have announced substantial purchases in the last couple of years, and over the last eight months even most-secretive China has resumed announcing purchases, if small ones that may represent only a fraction of that nation’s purchases. Of course China still has a huge foreign-exchange reserve in dollars with which it can dominate any market, at least for a significant time.

So either central banks now are divided on policy toward gold or they no longer want or are able to suppress the price with sales, leases, swaps, and futures market intervention. Indeed, with even President Trump clamoring for a cheaper U.S. dollar, the gold policy of the U.S. government itself may have changed, though the government long has refused to say what its gold policy is.

* * *

All this will exhilarate long-suffering investors in the monetary metals, whose view of the world financial system has been correct but who have been defeated by comprehensive cheating. As the monetary metals strain and break their shackles, their investors deserve a triumphal march, maybe to Dick Powell’s rendition of “The Gold Diggers’ Song” from 1933:

http://www.gata.org/files/DickPowellSings.wma

Gone are my blues, and gone are my tears.

I’ve got good news to shout in your ears.

The silver dollar has returned to the fold.

With silver you can turn your dreams to gold.

All the same, it seems so long ago when Bobby Godsell, then chief executive of AngloGold, remarked that gold investors and the gold-mining industry aspired to “a good gold price in a good world.”

A good gold price — that is, a price determined by a free-market relationship to other currencies and financial assets — would always help insure a good world by safeguarding it against recklessness, stupidity, corruption, and tyranny in government. Of course to remove that safeguard is why over the last half century central banks intensified their largely surreptitious efforts to suppress the gold price. Gold impeded their power.

So now we may be on the way to a spectacular gold price in a terrible world, a world engaged in trade and currency wars and getting closer to more shooting wars, a world in which central banks frantically continue to destroy all market mechanisms, buying equities and bonds to support prices, secretly trading financial and commodity futures to dissuade investors out of alternative assets, pushing interest rates toward and even below zero, and rushing to devalue their currencies, virtually proclaiming the worthlessness of government-issued money.

* * *

Amid all this the monetary metals will protect people, but only to a certain extent. If people also come to need guns, ammunition, and large supplies of freeze-dried food and drinking water, the metals will not be quite the consolation their investors have hoped for.

Indeed, the world already seems to be going crazy. At least the well-dressed people running it have gone crazy, presiding somberly every day over the chaos they instigated with their decades of market rigging, conducting the most important affairs of humanity in secret while encouraging people to believe that there is something for nothing.

Far from creating a good world, the people running it are creating a world, in Norman Mailer’s words, “where orphans burn orphans and nothing is more difficult to discover than a simple fact.”

So the song today for everybody, not just monetary metals investors, may be Cole Porter’s “Anything Goes” from 1934. He performs it himself here:

https://www.youtube.com/watch?v=Wd1w5tn040g

The world has gone mad today

And good’s bad today

And black’s white today

And day’s night today

And that gent today

You gave a cent today

Once had several chateaus.

As long as anything goes, a good world will be a long way off.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Bill Murphy of GATA interviewed by Kaiser of Reluctant Preppers

(GATA/Reluctant Preppers)

Gold’s unprecedented trading hints at something big behind the scenes, GATA chairman says

Submitted by cpowell on Thu, 2019-08-08 00:51. Section: Daily Dispatches

8:51p ET Wednesday, August 7, 2019

Dear Friend of GATA and Gold:

In an interview with Dunagun Kaiser of Reluctant Preppers, GATA Chairman Bill Murphy says gold is trading like it has never traded before, signifying that something big is happening behind the scenes. Most likely, Murphy says, physical demand is starting to overcome the paper market.

The interview is 17 minutes long and can be viewed at You Tube here:

https://www.youtube.com/watch?v=BfTvQb2PZ-Y&feature=youtu.be

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Chris Marcus interviews me

(Chris Marcus, Arcadia Economics/Harvey Organ)

A government’s claims are probably driving silver up, GATA consultant Organ says

Submitted by cpowell on Thu, 2019-08-08 01:39. Section: Daily Dispatches

9:40p ET Wednesday, August 7, 2019

Dear Friend of GATA and Gold:

GATA consultant Harvey Organ, interviewed by Chris Marcus for Arcadia Economics, says he thinks silver is rising sharply because a government, probably that of China, is making claims for delivery of the metal. He adds that deliveries are taking longer and notes what he considers a key detail of tightness of supply — that shares of the Sprott physical silver fund have moved from their usual discount to net asset value to a premium over it.

The interview is 27 minutes long and can be heard at YouTube here:

https://www.youtube.com/watch?v=NBelIBvSxWg&feature=youtu.be

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

iii) Other physical stories:

FROM CHRIS MARCUS TO ME: (MY INTERVIEW WITH CHRIS MARCUS OF ARCADIAECONOMICS)

Gold’s Surge Is A Message: Central Banks Are Out Of Control, Not Inflation

Authored by Mike Shedlock via MishTalk,

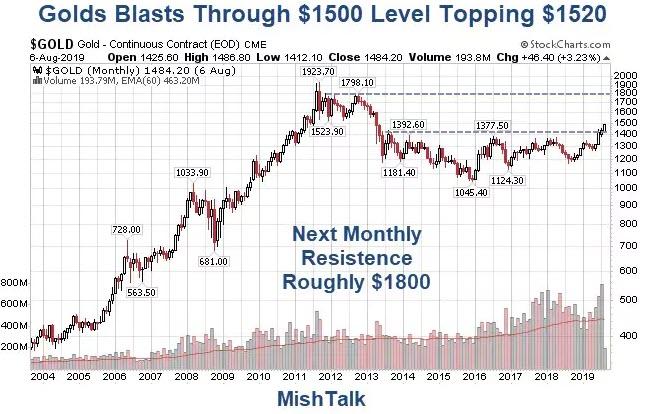

Gold blasted through the $1500 level this week. Let’s analyze the message. Here’s a hint: The message isn’t inflation.

The above chart is and end-of-day chart from yesterday. Gold closed at $1484.

At 11:30 AM Central, gold was at $1520, up $36 on the day.

Gold vs Copper

What’s the Message?

Stephanie Pomboy at Macro Mavens nails it.

steph pomboy@spomboyat the risk of piling-on,the canary in the financial crisis coalmine has been singing loudly. the relationship btw the metallic barometer of financial insecurity (gold) and the metallic barometer of economic activity (copper) has been a reliable predictor of trouble in the past.

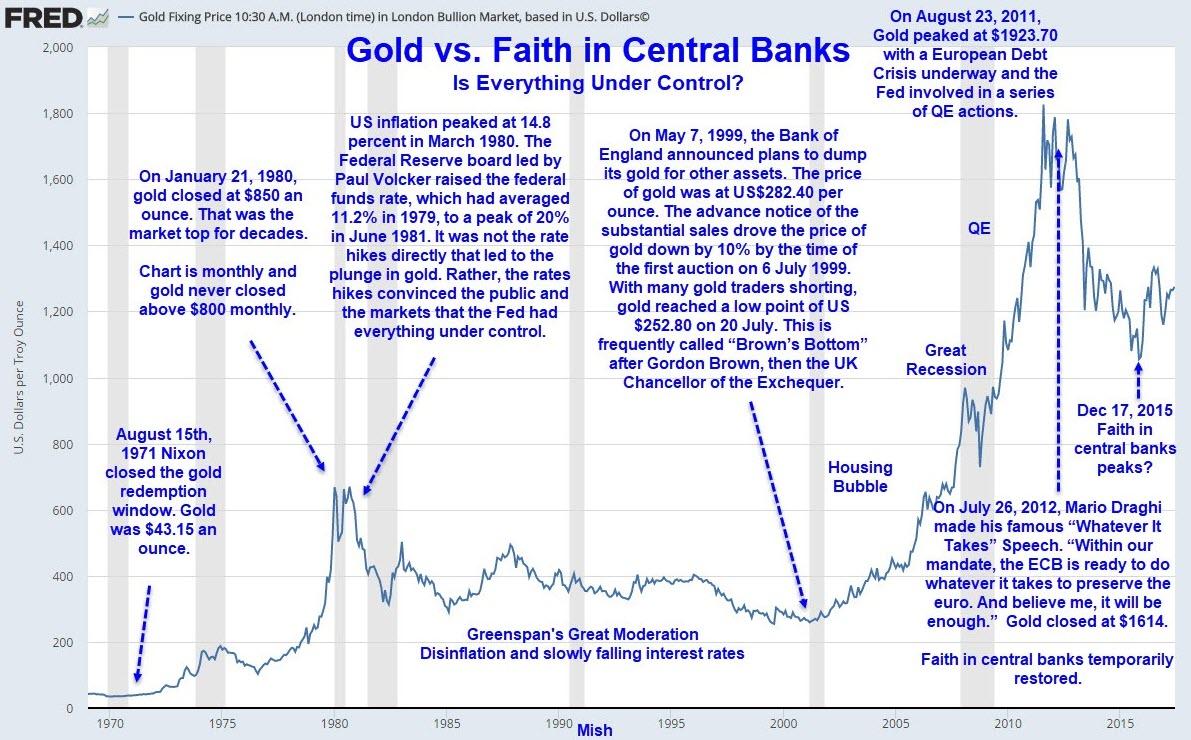

Gold Not an Inflation Hedge

As I have pointed out numerous times, and contrary to popular belief, gold is not an inflation hedge. Gold fell from $800 to $250 with inflation every step of the way.

Rather, gold is a measure of faith in central banks that everything is under control.

Gold vs Faith in Central Banks

Everything Under Control?

Clearly not, and I have easy-to-understand proof.

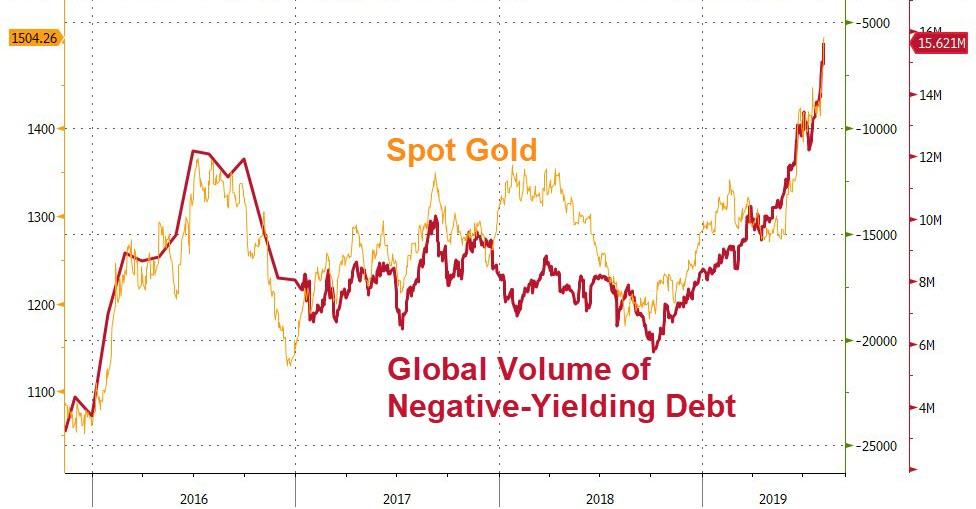

- Hello Treasury Bears: 10-Year Bond Yield Approaching Record Low Yield

- Negative Yield Debt Hits Record $15 Trillion, Up $1 Trillion in 2 Business Days

- US Treasury Declares China a Currency Manipulator Under Orders From Trump

If you believe gold tracks inflation or is some kind of inflation hedge, you need to think again.

Only in hyperinflation or its mild form, stagflation, is gold an inflation hedge. But even then, both are synonymous with central bank stress.

Hello Treasury Bears

Let me make it simple: It’s the debt, stupid!

The global economy is choking on debt as central banks are determined to have more of it.

Inflation? Forget about it. The bubbles are proof we “had” inflation.

The Bond markets says something else is coming up.

LAWRIE WILLIAMS: China says it added 10 tonnes to gold reserves in July

The People’s Bank of China (PBoC)- China’s central bank, says it added a further 9.96 tonnes of gold to its forex reserves in July – a seemingly particularly astute move given the strong recent advance in the gold price so far this month. This is just one of the world’s Central Banks adding regularly to its gold reserves this year. So far the PBoC says it has added a total of around 84 tonnes to its reserves over the first seven months of the year. However, the latest increase is yet another reduction in the level of its monthly reported reserve accumulations after adding 10.26 tonnes in June. China is thus tending to add rather less gold to its reserves than Russia which has announced additions of around 96.5 tonnes in the first half of the year. It won’t report any reserve increase for July for another couple of weeks (it usually announces any gold reserve increases on the 20th of the month).

Of course, as we have pointed out beforehand, the veracity of the actual reserve additions by China – or for any other central bank for that matter – is always open to question as reported figures are not independently audited. The PBoC has a track record of announcing what appear to be misleading statements regarding its gold reserves in the past in going for long periods of reporting zero increases and then announcing mega rises which must have been built up during the years and months of zero addition reporting. China has claimed in the past that this gold has been lodged in accounts it has not been required to report to the IMF and only reports this when it is merged into its forex figures at a time it feels appropriate to let the world know.

Overall though even the total amount of gold held by China in its reserves has been questioned by many analysts – some think it is actually considerably more than the total of a little under 2,000 tonnes currently reported to the IMF. The nation is thought to have a target of at least matching the U.S.’s reported holding of 8,133.5 tonnes (a figure which many also doubt given the resistance to it being audited). China is thought to believe that gold holdings may have an increasingly important role to play in any future global monetary re- alignment which may come about in the next few years.

While Russia, China and Kazakhstan are perhaps currently the most consistent purchasers of gold for their reserves, the overall level of Central Bank buying remains impressive According to World Gold Council figures Central Bank gold buying reached over 650 tonnes in 2018, while its latest quarterly Gold Demand Trends report puts first half 2019 gold purchases at 374.1 tonnes, suggesting that full year 2019 should at least match the 2018 figure. Deposits into gold ETFs remain strong too, which bodes well for gold demand in the current year, and although supply may also rise slightly due to higher gold prices enhancing scrap sales the overall balance is likely to be positive for gold.

In a survey of Central Bank buying intentions, 8% of central banks said they expected to increase their gold holdings in the next 12 months. Perhaps even more significantly a higher proportion of emerging markets and developing economy central banks (11%) expect to increase their gold holdings although the majority of central banks do not anticipate a change in their gold holding level. But this is as usual for the majority where reported gold holdings tend to remain unchanged year–in-year-out.

08 Aug 2019

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Global Markets Stabilize After China Fixes Yuan Stronger Than Expected

A quick case study on the power of expectations: On Monday, when the PBOC fixed the Yuan below 6.90 for the first time in 2019, well below consensus estimates, the offshore yuan collapsed, tumbling below 7.00 and as far as 7.10 for the first time since 2008, its biggest drop since the Aug 2015 devaluation and unleashing famine and pestilence across global capital markets. Then, on Thursday, one day after the comical fixing of 6.9996, the PBOC finally broke the seal, and set the daily reference rate of the yuan at 7.0039 per dollar, the first fixing weaker than 7.0000 in 11 years…

… but because the fix was a tad stronger than the 7.0156 rate estimated by analysts, the market took this as bullish and reacted with a relief rally sending S&P futures sharply higher from session lows.

And while China was quick to talk down the historic fix, and the market was clearly delighted by the fact that the fixing was not as worse as it could have been, the event was nonetheless momentous.

In a recent Bloomberg opinion piece, former UBS chief economist and China watcher George Magnus wrote “China allowing the yuan to slide below 7 to the dollar is a watershed moment for currency markets that’s symbolically equivalent to the U.S. and other countries abandoning the gold standard in the interwar period, or the collapse of the postwar Bretton Woods system of fixed exchange rates four decades ago. The implications for the global economy are equally significant.”

To be sure, the market has been eying the fix for insight on what constitutes a ‘comfortable’ level for the PBOC. UBS noted that although the PBOC has stepped up measures to slow the yuan’s pace of depreciation (including: introducing a larger counter cyclical factor, issuing central bank bills in Hong Kong to manage liquidity, pledging to keep the yuan stable) the market remains concerned about further weakening. “Today’s fixing is a clear message that China doesn’t mind letting its currency depreciate beyond any specific number, but would like to control the pace it weakens and mitigate market volatility as ‘stability’, which is PBoC governor Yi Gang’s main goal.” UBS believes that upward pressure on USDCNH is likely to persist in the near-term, as does Citi and SocGen, both of which expect the yuan to drift to 7.50 and lower against the USD.

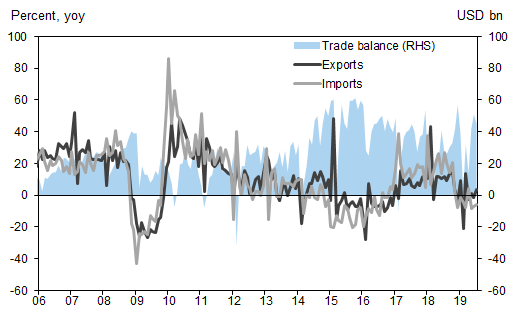

For now, however, China’s stronger than expected fix provided a brief comfort to markets, and global stock markets enjoyed a tentative recovery on Thursday after the PBOC print as well as better-than-expected Chinese export data. On the latter, China’s NBS reported that exports increased 3.3% yoy in July (USD terms), up from a decline of 1.3% yoy in June, and imports continued to soften, declining 5.6% yoy in July (v.s. -7.4% yoy in June). Both readings were above consensus expectations despite the Sino-U.S. tariff struggle.

In sequential terms, China’s exports rebounded 2.6% mom sa non-annualized in July, reversing a contraction of 0.9% in June. Imports went up by 2.6% mom sa non-annualized in July following two consecutive months of decrease. China’s trade surplus moderated to US$45.1bn in July from US$51.0bn in June. Exports to the US continued to contract by 6.5% yoy in July, and exports to Japan also declined 4.1% yoy. In contrast, exports to the EU rebounded 6.5% yoy in July from a decline of 3.0% yoy in June, and exports to ASEAN increased strongly by +15.6% yoy in July.

This was enough for the beaten down market to express some modest bullish sentiment overnight, and the MSCI world equity index rose 0.25%, led by Asia and Europe, even though it remains down more than 3% since the start of August.

Futures on all three of the main U.S. equity indexes advanced after the S&P 500 eked out a gain on Wednesday, although much of the gains have been pared as traders walk in to their desks.

The Stoxx Europe 600 also climbed for a second day, following Asia higher in early trade, led by tech and chemicals shares. European tech stocks lead gains, rising for a second day as investors bought into chip stocks and names which have lagged this year. The Stoxx Tech index rallied as much as 1.7%, led by chip maker AMS +3%, telecom carrier United Internet +2.5%, IT services co. Capgemini +1.9%, and Sweden’s Hexagon +2.1%. News that Japan has granted the first export license to South Korea also helped boost sentiment: “This is positive for the sector as this is one of the macro uncertainties (along with China-U.S.) with the potential to endanger a recovery,” Bankhaus Lampe analyst Veysel Taze said.

Earlier in the session, a gauge of Asia stocks increased as China’s Shanghai Composite rebounded from the lowest level since February. Asian stocks advanced for a second day, led by material firms, with most markets in the region up, led by Indonesia and Taiwan. Japan’s Topix slipped 0.1%, dragged by SoftBank Group and Takeda Pharmaceutical, after the yen extended gains against the dollar for a second day. The Shanghai Composite Index climbed 0.9%, driven by Kweichow Moutai and China Merchants Bank, as the nation’s July exports topped estimates. Chinese domestic equities are getting a boost in MSCI Inc.’s benchmark emerging-market indexes. India’s Sensex rose 0.8%, supported by HDFC Bank and Infosys, as investors weighed a bigger-than-expected rate cut against a less optimistic growth forecast by the central bank.

Emerging-market stocks headed for their first daily gain in 12 sessions, on track to end their longest losing streak in four years as investor concern over the yuan’s depreciation and the start of an all-out currency war faded. MSCI Inc.’s developing-nation equities index rose 0.9% after touching its lowest level since January earlier this week. “If the dovish pivot among global central banks manages to stay ahead of weaker growth data, risk and EM assets will likely find their feet even if USD/CNY stabilizes around a higher level,” Goldman Sachs strategists wrote in a client note.

Meanwhile, yields have continued to be volatile following the latest rate spasm which began when central banks in New Zealand, India and Thailand surprised markets on Wednesday with aggressive interest rate cuts. The Philippines followed suit and overnight the Monetary Board (MB) of Bangko Sentral ng Pilipinas (BSP) cut its key policy rates by 25bp, lowering the overnight borrowing rate, the overnight lending rate and the overnight deposit rate to 4.75%, 4.25% and 3.75%, respectively

“Financial markets are raising risks of recession,” said JPMorgan economist Joseph Lupton. “Equities continue to slide and volatility has spiked, but the alarm bell is loudest in rates markets, where the yield curve inverted the most since just before the start of the financial crisis.”

In response, markets ramped up their expectations for more easing by the U.S. Federal Reserve, but the question remains how fast Fed policymakers will move. Futures now price in a 100% probability of a Fed cut in September and a near 24% chance of a half-point cut. Some 75 basis points of easing is implied by January, with rates ultimately reaching 1%. Curiously, there is a non-trivial chance of an emergency, August rate cut.

In rates, U.S. government bond yields resumed their drop on Thursday, while in Europe German and French 10-year yields rose from record lows after a rally in recent sessions. The 10-year U.S. Treasury yield dropped to 1.7120%, although it reached a low of 1.595% on Wednesday.

Gold also benefited this week as investors scrambled to find somewhere safe to park their cash, rising above $1,500 for the first time since 2013. Spot gold was last at $1,498 per ounce, down from as much as $1,510 on Wednesday. Gold is up 16% since May.

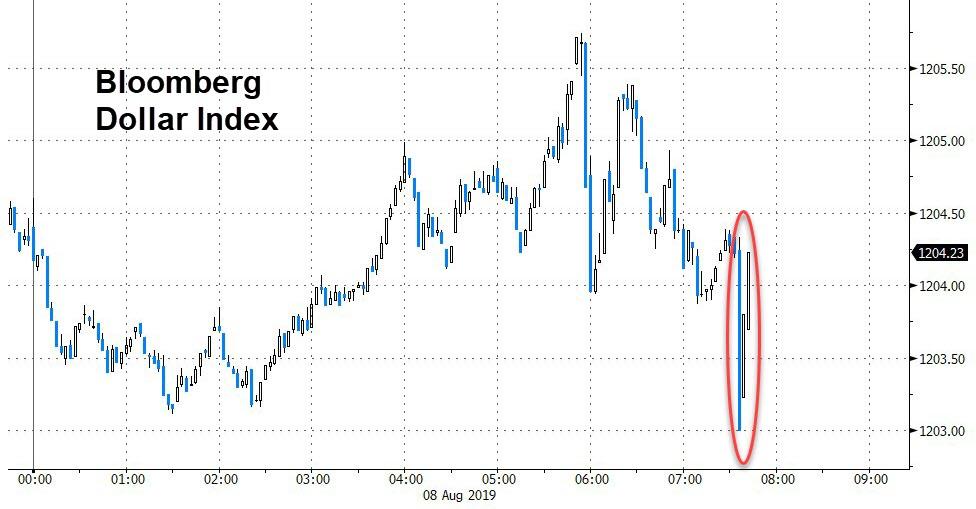

In foreign exchange markets, the Japanese yen rose again, gaining 0.2% to 106.04 yen per dollar. China’s yuan also gained. In the offshore market it rose 0.2% to 7.0734 yuan per dollar after touching as high as 7.14 yuan on Tuesday. The Bloomberg Dollar Spot Index inched lower Thursday as the greenback fell against all G-10 peers. The biggest overnight gains were seen in Australia’s dollar, which rose from a 10-year low as risk appetite stabilized.

In commodities, oil prices regained some ground amid talk that Saudi Arabia was weighing options to halt its decline, offsetting an increase in stockpiles and fears of slowing demand. Brent crude futures climbed $1.25 to $57.48, though that followed steep losses on Wednesday, U.S. crude rose $1.46 to $52.53 a barrel.

Market Snapshot

- S&P 500 futures up 0.2% to 2,885.75

- MXAP up 0.3% to 151.68

- MXAPJ up 0.8% to 489.77

- Nikkei up 0.4% to 20,593.35

- Topix down 0.08% to 1,498.66

- Hang Seng Index up 0.5% to 26,120.77

- Shanghai Composite up 0.9% to 2,794.55

- Sensex up 0.7% to 36,927.55

- Australia S&P/ASX 200 up 0.8% to 6,568.15

- Kospi up 0.6% to 1,920.61

- STOXX Europe 600 up 0.7% to 371.14

- German 10Y yield rose 2.0 bps to -0.561%

- Euro up 0.2% to $1.1223

- Italian 10Y yield fell 9.3 bps to 1.069%

- Spanish 10Y yield rose 1.2 bps to 0.183%

- Brent futures up 2.2% to $57.48/bbl

- Gold spot down 0.2% to $1,497.66

- U.S. Dollar Index little changed at 97.49

Top Overnight News from Bloomberg

- The yuan steadied after China’s central bank set the daily fixing stronger than analysts expected, providing some reassurance to traders rattled by a tumultuous week in markets.

- China’s export growth rebounded in July, and imports shrank less than forecast, signaling some recovery in trade just as companies brace for the arrival of new tariffs from the U.S.

- The Trump administration is rushing to finalize a list of $300b in Chinese imports it plans to hit with tariffs in a few weeks’ time, as U.S. companies make a last-ditch appeal to be spared from the latest round of duties

- China is mulling the biggest changes to its futures market since 2015, an overhaul that would give global investors unprecedented access, make it easier to execute bearish trades, and lay the groundwork for wagers on stock-market volatility

- The global trade storm battering manufacturing in Europe’s largest economy is about to reach the labor market. German joblessness, which declined from one record low to the next for much of the past decade, is no longer falling and risks a reversal as workers endure the repercussions of the country’s factory slump

- Deputy Premier Matteo Salvini increased pressure on Italy’s ruling coalition, reportedly giving Prime Minister Giuseppe Conte a Monday deadline to shake up the cabinet and indicating that if his partners in the Five Star Movement don’t yield to his demands he’ll dissolve the government.

- The exodus from active funds has sent fees inexorably lower, led to the loss of thousands of jobs, forced large-scale consolidation among firms and pushed the industry to the brink of a shakeout that only the strongest will survive. Now, the $74 trillion industry, as measured by the Boston Consulting Group, is on the brink of a shakeout that only the strongest will survive

- Large fluctuations in currency and stock markets are not good for the economy, Japanese Finance Minister Taro Aso said

- Oil rebounded from the lowest level since January after Saudi Arabia contacted other producers to discuss options to stem a rout that’s been driven by the worsening U.S.-China trade war

Asian equity markets gained as a firmer than expected PBoC reference rate setting and Chinese trade data helped the region shake off the initial tentativeness following the tumultuous day on Wall St, where stocks staged a dramatic intraday recovery and although the DJIA closed in the red, it posted its largest rebound YTD. ASX 200 (+0.7%) was initially subdued amid losses in its top weighted financials sector following earnings from AMP Capital and Insurance Australia Group but then conformed to the improved risk tone led by gold miners after the precious metal rallied above USD 1500/oz for the first time since 2013, while Nikkei 225 (+0.4%) was underpinned by currency flows and KOSPI (+0.6%) outperformed after Japan approved some exports of tech materials to South Korea for the first time since curbs were imposed last month. Hang Seng (+0.5%) and Shanghai Comp. (+0.9%) were positive with sentiment underpinned by relief after the PBoC announced the reference rate which was set beyond the 7.0000 level for the first time since 2008 but not as weak as expected, while participants also digested Chinese trade data which topped estimates across the board and still showed a significant, albeit narrower imbalance in US-China trade. Finally, 10yr JGBs were initially lower with mild pressure seen amid the improved risk tone in the region, although prices then returned flat with support seen amid firmer demand at the 10yr inflation-indexed auction.

Top Asian News

- China Plans Biggest Futures Market Overhaul Since 2015 Clampdown

- Philippine Central Bank Cuts Interest Rate as Economy Slows

- Shady Japan Bond Sale Practice Returning as Yields Fall

Major European stocks are higher across the board [Eurostoxx 50 +1.1%], following on from a positive Asia-Pac handover after optimistic Chinese trade data lifted sentiment in the region. Indices are posting broad-based gains, although UK’s FTSE 100 (+0.1%) lags its peers amid a slew of large cap ex-divs. Sectors are also in positive territory, although defensive sectors are somewhat lagging. Looking at individual movers, Adidas (-1.3%) shares opened lower by over 2% as investors for weeks sought an upgrade to guidance, particularly after its rival Puma (+2.5%) raised its sales and profit forecasts recently. Sticking with the DAX, Thyssenkrupp (+3.3%) shares rose despite an EBIT guidance cut as investors shifted focus to its elevator division IPO (expected in FY19/20) and expression of interests for other divisions. Finally, Osram Licht (-6.6%) slumped to the foot of the Stoxx 600 after the Co’s largest shareholder rejected the EUR 3.4bln takeover offer form Bain & Carlyle. It’s also worth noting that Goldman Sachs has downgraded trade sensitive sectors (EU autos and basic resources) in light of the recent developments between US and China, although individual stocks are little swayed by the broker update.

Top European News

- Thyssenkrupp Open to Selling Divisions, Cuts Profit Outlook

- The Inside Men Who Johnson May Tap for a More Understated BOE

- Aviva Reviews Asia Unit as New CEO Tulloch Starts Turnaround

- Novozymes Finance Chief Makes Sudden Exit as Outlook Darkens

In FX, the Dollar is on a softer footing against its G10 rivals, and most EMs amidst another revival in broad risk appetite, prompted in part by Chinese trade data that beat consensus across all key components and offset or appeased concerns over the ongoing incline in the Usd/Cny reference rate. However, the index is still straddling 97.500 and from a technical perspective holding above key Fib support at 97.392 on a closing basis, if not intraday, and it remains to be seen if the latest upturn in sentiment proves more sustainable or transitory like on Tuesday.

- AUD/NZD/GBP/CAD – In keeping with the improved risk tone noted above, Aud/Usd has turned full circle and a bit more from midweek session lows towards 0.6800, but unlikely at this stage to reach hefty expiry options residing between 0.6840-50 (1.2 bn), while Nzd/Usd is still underperforming within 0.6468-35 parameters following more dovish RBNZ rhetoric on balance after yesterday’s double-barrelled ½ point OCR cut. Elsewhere, Cable is back around 1.2150 and the Loonie has rebounded through 1.3300 along side crude prices ahead of Canadian house price data.

- JPY/EUR/CHF/XAU – The safer-havens are off best levels, but interestingly and perhaps tellingly still relatively bid as the Yen contains losses below 106.00 to circa 106.30 with decent option expiry interest likely to cap further upside in Usd/Jpy given 1 bn running off from 106.45-55. Similarly, the single currency is holding above 1.1200, but also likely to be stymied by expiries as 2.4 bn awaits between 1.1230-40, while the latest ECB monthly bulletin is far from Euro supportive given a downbeat assessment of the Eurozone economy and outlook, albeit largely a repetition of President Draghi’s post-policy meeting text. Elsewhere, the Franc is pivoting 0.9750 and Gold is rangebound either side of Usd1500/oz.

- EM – The Rand continues to underperform with Usd/Zar mostly above 15.0000 after recent technical breaks to the upside and with weaker than forecast SA mining data not helping.

- RBNZ Assistant Governor Hawkesby said outlook for rates is more balanced after 50bps cut but added there is still some probability OCR will need to be reduced further, while Hawkesby also stated the central bank are watching inflation expectations closely and that unconventional tools are a contingency in the event inflation tanks although they would need to exhaust conventional policy tools first. (Newswires)