GOLD:$1498.80. DOWN $2.00(COMEX TO COMEX CLOSING

Silver: $16.97 UP 2 CENTS (COMEX TO COMEX CLOSING)/

Closing access prices:

Gold : $16.97

silver: $16.97

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 7/18

EXCHANGE: COMEX

CONTRACT: AUGUST 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,497.700000000 USD

INTENT DATE: 08/08/2019 DELIVERY DATE: 08/12/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

118 H MACQUARIE FUT 3

661 C JP MORGAN 7

686 C INTL FCSTONE 16

737 C ADVANTAGE 2

880 H CITIGROUP 6

905 C ADM 2

____________________________________________________________________________________________

TOTAL: 18 18

MONTH TO DATE: 4,424

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 18 NOTICE(S) FOR 1800 OZ (0.0559 tonnes

TOTAL NUMBER OF NOTICES FILED SO FAR: 4424 NOTICES FOR 44240000 OZ (13.7604 TONNES)

SILVER

FOR AUGUST

147 NOTICE(S) FILED TODAY FOR 735,000 OZ/

total number of notices filed so far this month: 1605 for 8,025,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

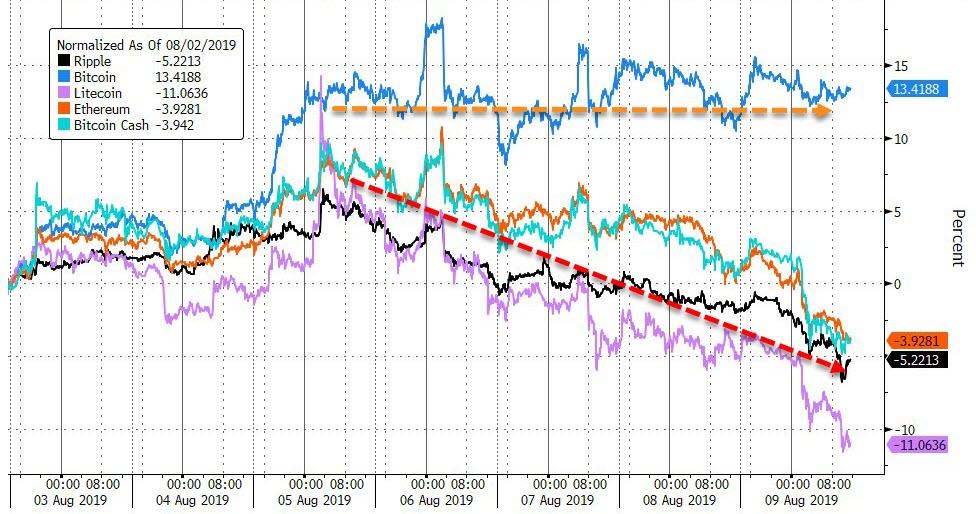

Bitcoin: OPENING MORNING TRADE : $ 11735 DOWN 266

Bitcoin: FINAL EVENING TRADE: $ 11878 down 113

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A FAIR SIZED 1063 CONTRACTS FROM 244,169 DOWN TO 243,775… DESPITE THE STRONG 23 CENT LOSS IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR AUGUST, 0 FOR SEPT 2019, AND DEC: 37 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 2056 CONTRACTS. WITH THE TRANSFER OF 2056 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 4245 EFP CONTRACTS TRANSLATES INTO 10.28 MILLION OZ ACCOMPANYING:

1.THE 23 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

8.570 MILLION OZ INITIAL STANDING IN AUGUST.

WE HAD ATTEMPTED COVERING OF SHORTS AT THE SILVER COMEX YESTERDAY WITH MINOR SUCCESS..AND WE HAD SOME SPREADING ACCUMULATION.

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF SEPTEMBER FOR SILVER.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF AUGUST BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF AUGUST:

12,385 CONTRACTS (FOR 7 TRADING DAYS TOTAL 12,385 CONTRACTS) OR 61.93 MILLION OZ: (AVERAGE PER DAY: 1769 CONTRACTS OR 8.846 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 61.93 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 8.841% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1374.44 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

RESULT: WE HAD A FAIR SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1063, WITH THE 23 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2056 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A VERY GOOD SIZED: 993 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2056 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 1056 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 23 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $16.95 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.215 BILLION OZ TO BE EXACT or 174% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 147 NOTICE(S) FOR 735,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

AND NOW WE ARE WITHIN A WHISKER OF ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 243,795 BUT THIS TIME THE PRICE OF SILVER YESTERDAY WAS $16.95

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 8.570 MILLION OZ

- CLOSE TO THE RECORD OPEN INTEREST IN SILVER 244,169 CONTRACTS (OR 1.228 BILLION OZ/, THE PREVIOUS RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2,457 CONTRACTS, TO 602,423 DESPITE THE $4.90 PRICING LOSS WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING ACCUMULATION HAS NOW COMMENCED FOR SILVER..AS THE LIQUIDATION PHASE FOR COMEX OI GOLD HAS NOW STOPPED

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUMONGOUS SIZED 13,196 CONTRACTS:

AUGUST 2019: 0 CONTRACTS, DEC> 13196 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 602,423,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 15,653 CONTRACTS: 2,457 CONTRACTS INCREASED AT THE COMEX AND 13,196 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 15,653 CONTRACTS OR 1,565,300 OZ OR 48.69 TONNES. YESTERDAY WE HAD A STRONG LOSS OF $4.20 IN GOLD TRADING….AND WITH THAT STRONG LOSS IN PRICE, WE HAD A GIGANTIC GAIN IN GOLD TONNAGE OF 48.69 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER AND MANY GOLD LONGS JUST PILED ON WITHOUT ANY REGARD TO THAT LOSS IN PRICE.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST : 88,699 CONTRACTS OR 8,869,900 oz OR 275.89 TONNES (7 TRADING DAY AND THUS AVERAGING: 12,671 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY IN TONNES: 275.89 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 275.89/3550 x 100% TONNES =7.77% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 3787,13 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 2457 DESPITE THE PRICING LOSS THAT GOLD UNDERTOOK YESTERDAY($4.20)) //.WE ALSO HAD A HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 13,196 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 13,196 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 15,653 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

13,196 CONTRACTS MOVE TO LONDON AND 2,457 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 48.69 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED DESPITE THE LOSS IN PRICE OF $4.20 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. THE COMEX IS NOW UNDER FULL ASSAULT FOR OUR TWO PHYSICAL METALS, GOLD AND SILVER

we had: 6 notice(s) filed upon for 600 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $2.00 TODAY//(COMEX-TO COMEX)

NO CHANGE IN GOLD INVENTORY AT THE GLD

INVENTORY RESTS AT 839.85 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 2 CENTS TODAY:

A HUGE CHANGE IN INVENTORY AT THE SLV:

A DEPOSIT OF 2.246 MILLION OZ INTO THE SLV

/INVENTORY RESTS AT 365.557 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A FAIR SIZED 1063 CONTRACTS from 244169 DOWN TO 243,106 AND WITHIN A WHISKER OF A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORDED HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET EXCEPT TODAY AS WE HAVE A RISING PRICE..OUR SHORT DERIVATIVE BANKERS ARE NOW IN DEEP TROUBLE AS THEY ARE TERRIBLY OFFSIDE AND NEED ASSISTANCE FROM THE GOVERNMENT (FED) TO PROVIDE THE NECESSARY COLLATERAL TO CARRY THAT SHORT POSITION…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR AUGUST: 0, FOR SEPT. 2019; DEC 37 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2056 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 1056 CONTRACTS TO THE 2056 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD SIZED GAIN OF 993 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 4.965 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ ;AUGUST AT 8.570 MILLION OZ//

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE STRONG 23 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 2056 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 19.80 POINTS OR 0.71% //Hang Sang CLOSED DOWN 181.47 POINTS OR 0.69% /The Nikkei closed UP 91.47 POINTS OR 0.44%//Australia’s all ordinaires CLOSED UP .32%

/Chinese yuan (ONSHORE) closed DOWN at 7.0595 /Oil UP TO 53.27 dollars per barrel for WTI and 58.20 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0505 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0858 TRADE TALKS STALL//YUAN LEVELS PAST THE DANGEROUS 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

i)Last night: USA futures extend their losses after a weaker yuan fix

(zerohedge)

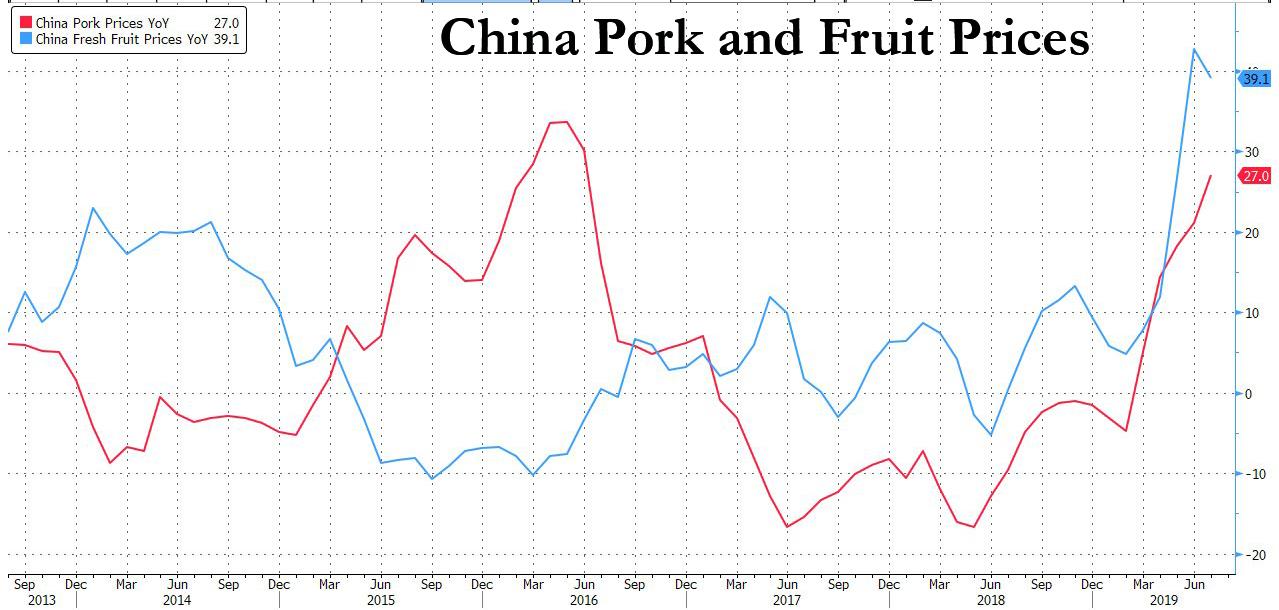

ii)This is why China has huge problems ahead. Its PPI indicates huge deflation has now become the norm in China as commodity prices tumble which in turn causes factory prices to fall. However food prices are on the rise caused by the Pig Ebola. Fruit prices are also on the rise. Thus China has a twofold problem:

iii)Heng Feng bank has now been nationalized. They have over 200 billion dollars in assets(zerohedge)

4/EUROPEAN AFFAIRS

i)UK

For the first time since 2012, the UK contracted as a no deal Brexit looms. The pound collapses on this news

(zerohedge)

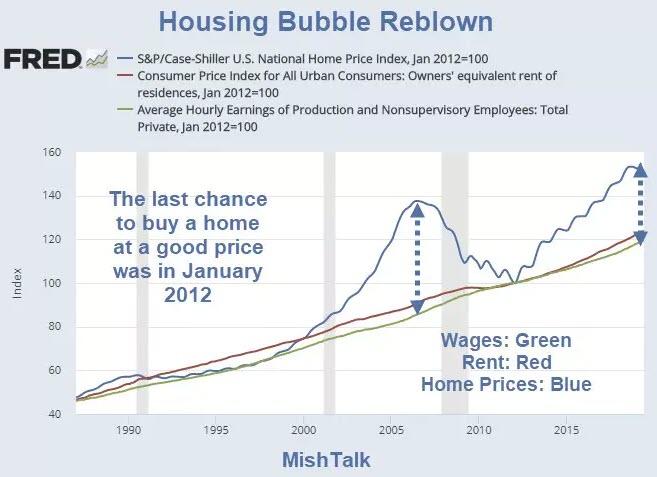

ii)The truth behind the EU negotiations with the UK on its Brexit.

(Mish Shedlock)

iii) The CEO of HSBC was fired a few days ago. These guys are massively short the precious metals.

v)ITALY

7. OIL ISSUES

China continues to defy USA sanctions by purchasing Iranian oil. If China stops buying oil from Iran the price could plummet by 30 dollar per barrel

(zerohedge)

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

i)Any new GATA supporter will receive a Thomas Callendra subscription for one year free.

(Gata/Thom Callandra)

ii)Alasdair \macleod is in my camp one this one: expect deeply negative interest rates to the entire globe

(Alasdair Macleod)

iii)Chris Powell comments on whether central banks have lost control or are they in a “controlled retreat:

Find out if you agree with Chris Powell

(GATA)

iv)Craig Roberts asks: Is the Federal Reserve losing control of the gold price?

an excellent commentary

( Craig Roberts/GATA)

v)Will a 1985 Plaza Accord work (cheapening the dollar vs everybody else) work? I think not

(Watt/MarketWatch/GATA)

vi)Peter Schiff on gold’s strength lately

(Peter Schiff)

vii)Who would have thought that this might happen… hi grade Nickel may have severe supply problems in the next few years

(Lesage/Oil Price.com)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LATE MORNING/USA

This triggered a sell off in the Dow, Nasdaq and the yuan

(zerohedge)

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

(zerohedge)

iii) Important USA Economic Stories

(zerohedge)

b)Another great commentary from Mish Shedlock as he states that we must expect a huge debt deflation as the central bankers are losing control

(Mish Shedlock/Mishtalk)

iv) Swamp commentaries)

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; nil oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 111,868 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 151,839 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 151,839 CONTRACTS EQUATES to 759 million OZ 108% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -.1.06% ((AUGUST 8/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.30% to NAV (AUGUST 5/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 14.85 TRADING 14.35/DISCOUNT 3.34

END

And now the Gold inventory at the GLD/

AUGUST 9/WITH GOLD DOWN $2.00//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REMAINS AT 839.85 TONNES OZ/

AUGUST 8: WITH GOLD DOWN $4.20: TWO TRANSACTIONS: A)A MONSTROUS PAPER DEPOSIT OF 8.50 TONNES WAS ADDED TO THE GLD/INVENTORY RESTS AT 845.42 TONNES b) A HUGE WITHDRAWAL OF 5.59 TONNES FROM THE GLD//INVENTORY RESTS AT 839.85 TONNES…ABSOLUTE FRAUD!

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 29/WITH GOLD UP $1.00: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 6.75 TONNES INTO THE GLD INVENTORY///INVENTORY RISES TO 824.89 TONNES

JULY 26/WITH GOLD UP $4.50: A HUGE INVENTORY WITHDRAWAL OF 4.09 TONNES OF PAPER GOLD LEAVES THE GLD/INVENTORY RESTS AT 818.14 TONNES

JULY 25.2019: WITH SILVER DOWN 19 CENTS: ANOTHER PAPER WITHDRAWAL OF 1.17 MILLION OZ/INVENTORY REST AT 358.213 MILLION OZ

JULY 24…A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A GAIN OF 1.685 MILLION OZ/INVENTORY RESTS AT 359.383 MILLION OZ

JULY 23/2019: WITH SILVER UP 5 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.221 MILLION PAPER OZ ADDED INTO THE GLD INVENTORY//INVENTORY RESTS AT 357.698 MILLION OZ////

JULY 22.2019/WITH SILVER UP 21 CENTS TODAY: A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 8.939 MILLION OZ ADDED TO THE SLV INVENTORY/INVENTORY RESTS AT 355.919 MILLION OZ//

JULY 19/WITH GOLD DOWN $1.00: A MASSIVE DEPOSIT OF 11.44 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 814.62

JULY 18/WITH GOLD UP $5.55 TODAY: A BIG PAPER DEPOSIT OF 3.81 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 803.18 TONNES

JULY 17/WITH GOLD UP $11.35 TODAY: A BIG WITHDRAWAL OF 1.17 TONNES FROM THE GLD//INVENTORY RESTS AT 799.37 TONNES

JULY 16: WITH GOLD DOWN $2.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 15: WITH GOLD UP $1.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 12/WITH GOLD UP $5.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 11.WITH GOLD DOWN $5.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 10//WITH GOLD UP $11.65 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER GOLD DEPOSIT OF 6.46 TONNES/INVENTORY RESTS AT 800.54 TONNES

JULY 9/WITH GOLD UP 70 CENTS, A HUGE PAPER WITHDRAWAL OF 2.89 TONNES WHICH WAS USED IN THE FUTILE RAID ON GOLD AND SILVER THIS MORNING//INVENTORY RESTS AT 794.08 TONNES

JULY 8/ WITH GOLD DOWN 35 CENTS A HUGE WITHDRAWAL OF 1.47 TONNES FROM THE GLD/INVENTORY FALLS TO 796.97 TONNES

JULY 5TH/WITH GOLD DOWN $19.50/NO CHANGES IN GOLD INVENTORY AT THE GLD//INV RESTS AT 798.44 TONNES

JULY 3// WITH GOLD UP $12.60 TODAY A SURPRISE WITHDRAWAL OF 1.76 TONNES FROM THE GLD//INVENTORY RESTS AT 798.44

JULY 2. WITH GOLD UP $18.90 A HUGE “PAPER” DEPOSIT OF 6.16 TONNES INTO THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 1: WITH GOLD DOWN $24.70 A HUGE “PAPER GOLD” WITHDRAWAL OF 1.76 TONNES FROM THE GLD/INVENTORY RESTS TONIGHT AT 794.04 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

AUGUST 9/2019/ Inventory rests tonight at 839.85 tonnes

*IN LAST 639 TRADING DAYS: 95.55 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 539 TRADING DAYS: A NET 70,99 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

AUGUST 9/2019//WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.245 MILLION OZ INTO THE SLV INVENTORY/INVENTORY ADVANCES 365.557 MILLION OZ

AUGUST 8/WITH SILVER DOWN 23 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT: 1.409 MILLION OZ INTO INVENTORY///INVENTORY RESTS AT 363.311 MILLION OZ//

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 29/2019: WITH SILVER UP 4 CENTS TODAY: A SMALL WITHDRAWAL OF 468000 OZ FROM THE SLV/INVENTORY LOWERS TO 356.715 MILLION OZ//

JULY 26.2019: WITH SILVER DOWN 2 CENTS TODAY: A HUGE 1.03 MILLION OZ OF PAPER SILVER LEAVES THE SLV/INVENTORY LOWERS TO 357.183 MILLION OZ//

JULY 25.2019: WITH SILVER DOWN 19 CENTS: ANOTHER PAPER WITHDRAWAL OF 1.17 MILLION OZ/INVENTORY REST AT 358.213 MILLION OZ

JULY 24…A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A GAIN OF 1.685 MILLION OZ/INVENTORY RESTS AT 359.383 MILLION OZ

JULY 23/2019: WITH SILVER UP 5 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.221 MILLION PAPER OZ ADDED INTO THE GLD INVENTORY//INVENTORY RESTS AT 357.698 MILLION OZ////

JULY 22.2019/WITH SILVER UP 21 CENTS TODAY: A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 8.939 MILLION OZ ADDED TO THE SLV INVENTORY/INVENTORY RESTS AT 355.919 MILLION OZ//

JULY 19/WITH SILVER FLAT TODAY: ANOTHER MONSTROUS PAPER DEPOSIT OF 3.276 MILLION OZ ENTERS THE SLV//WHAT A MASSIVE FRAUD//INVENTORY RESTS AT 346.980 MILLION OZ

JULY 18/WITH SILVER UP 24 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.668 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 343.704 MILLION OZ//

JULY 17: WITH SILVER UP ANOTHER 29 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.518 MILLION OZ/INTO THE SLV INVENTORY///INVENTORY RESTS AT 341.036 MILLION OZ//

JULY 16: WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY: 15 WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY 12/WITH SILVER UP 10 CENTS: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 11/NO CHANGE IN SILVER INVENTORY

JULY 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 9/WITH SILVER UP A SMALL 7 CENTS A GIGANTIC INVENTORY GAIN OF 4.026 MILLION OZ/ INVENTORY RESTS AT 332.518 MILLION OZ AND NOW IT SHOULD BE QUITE CLEAR THAT THE SLV ( AND GLD ARE FRAUDS)

JULY 8/WITH SILVER UP 7 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 328,492 MILLION OZ

JULY 5/WITH SILVER DOWN 32 CENTS WE STRANGELY HAD A HUGE INVENTORY GAIN OF 2,234 MILLION OZ//INVENTORY RESTS AT 328.492 MILLION OZ

JULY 3 WITH SILVER UP 10 CENTS A HUGE INCREASE IN INVENTORY..INVENTORY RESTS AT 326.151 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 323.330 MILLION OZ//

JULY 1/ WITH SILVER DOWN 16 CENTS: A SURPRISING DEPOSIT OF 936,000 OZ INTO THE SLV/INVENTORY RESTS TONIGHT AT 323.330 MILLION OZ/

AUGUST 9/2019:

Inventory 365.557 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.11/ and libor 6 month duration 2.05

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .06

XXXXXXXX

12 Month MM GOFO

+ 1.93%

LIBOR FOR 12 MONTH DURATION: 1.99

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.06

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

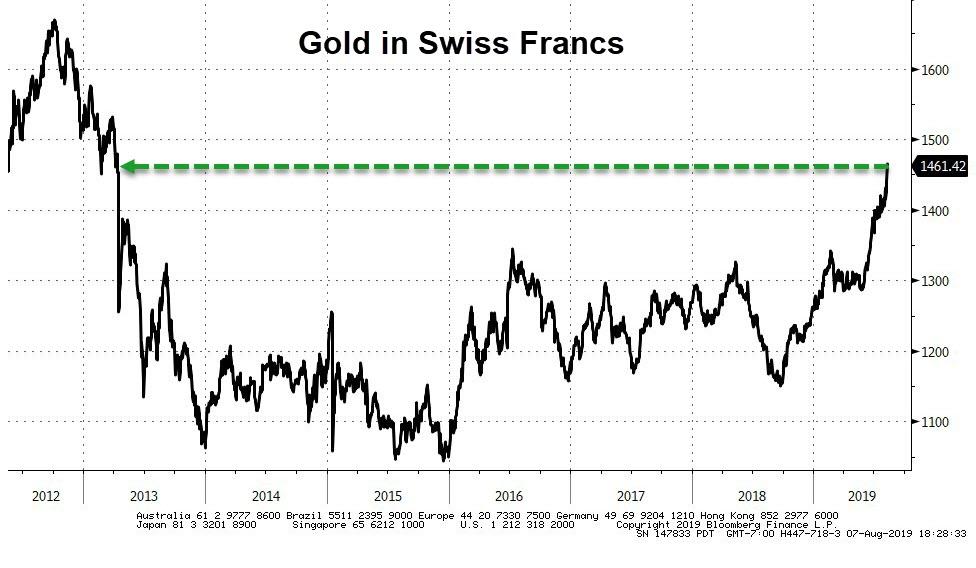

Gold Holds Above $1,500 As Central Banks Lose Control and China Continues to Buy Gold Bullion

NEWS & COMMENTARY

Gold and silver are 4% and 4.7% higher respectively for the week so far

Gold ends lower but holds firmly above $1,500; Silver loses grip on $17

Gold dips, taking a breather after surpassing key $1,500 level

China Increases Gold Reserves & Diversifies From The Dollar

European stocks seen lower on trade worries and political turmoil in Italy

Carl Icahn is not sure rate cuts can fix problems facing the economy

Bonds, Gold Bid As Italian Political Crisis Re-Emerges: Salvini Demands Fresh Elections

Paul Craig Roberts: Is the Federal Reserve losing control of the gold price?

Is Silver Demand Overwhelming Supply? with Harvey Organ

Gold Blasts Through $1500: Message? Central Banks Out of Control, Not Inflation

Gold Prices via LBMA (AM/ PM Fix – USD, GBP & EUR)

08-Aug-19 1497.40 1495.75, 1230.26 1234.14 & 1335.08 1335.70

07-Aug-19 1487.65 1506.05, 1225.82 1239.33 & 1330.11 1341.44

06-Aug-19 1461.85 1465.25, 1199.59 1201.21 & 1304.85 1311.11

05-Aug-19 1457.45 1465.25, 1199.92 1203.85 & 1307.92 1310.23

02-Aug-19 1436.05 1441.75, 1184.17 1187.28 & 1294.02 1298.44

01-Aug-19 1406.40 1406.80, 1161.12 1161.74 & 1273.35 1273.29

31-Jul-19 1430.55 1427.55, 1175.48 1167.45 & 1283.20 1281.37

30-Jul-19 1428.45 1425.90, 1173.47 1171.95 & 1281.75 1279.60

29-Jul-19 1418.95 1419.05, 1150.91 1157.94 & 1275.78 1275.30

26-Jul-19 1418.25 1420.40, 1140.27 1144.70 & 1273.02 1275.95

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

Any new GATA supporter will receive a Thomas Callendra subscription for one year free.

(Gata/Thom Callandra)

iii) Other physical stories:

Peter Schiff on gold’s strength lately

(Peter Schiff)

Peter Schiff: We Have Global Currency Weakness; They’re All Losing Value Against Gold

Several currencies have been strong against the dollar over the last couple of days, but as Peter Schiff said in his podcast, the biggest gainer wasn’t a currency at all. It was real money – gold.

Source: Bloomberg

Gold hit six-year highs on Monday and set records in a number of currencies. It continued to move upward the rest of the week, pushing above $1,500.

Any talk you hear in the media about the strong dollar simply by measuring it against some currencies… You don’t have a strong dollar when the price of gold is rising the way it is. We have a weak dollar. It’s just that we also have a weak yuan and we have a weak euro and we have a weak yen, because all these currencies are falling against gold.”

Peter noted the all-time record highs for gold in countries like Australia and Canada – countries that mine a lot of gold.

It’s only a question of time now, and I don’t think it’s going to be that much time, before gold starts making an all-time record high in terms of US dollars as well, because we are now in a period of global currency weakness. All currencies are losing value when priced in gold.”

Source: Bloomberg

Peter said that currencies sink at different levels and currently the dollar is sinking more slowly than a lot of other currencies.

But it’s about to pick up the pace. The dollar is going to be sinking faster as the economic reality sets in.”

There has been a lot of concern about the drop in the yuan against the dollar. Peter said the real problem isn’t that the Chinese yuan is dropping. The problem is going to come when the Chinese currency begins to rise. And Peter said it’s going to rise a lot.

And he said the recent fall in the yuan wasn’t because the Chinese are manipulating their currency. It fell do to market forces. Most investors believe the trade war is going to hurt the Chinese economy and they are selling off the yuan. Trump is upset that the Chinese government did not intervene — that they actually refrained from manipulating the yuan higher than the market wanted to set it.

Peter said he does think the Chinese have manipulated their currency in the past, but said they aren’t really doing that anymore.

Which means the currency is going to appreciate when market forces start to move it in that direction.”

Peter went on to reiterate that the Fed is going to keep cutting rates, noting that Goldman Sachs has projected 75 basis points in cuts by the end of the year.

They’re looking for 75 basis points. We’re going to get 200 basis points. And the reason it’s 200 is because that’s how many we got. Because once they cut 200, now we’re at zero. And the fact of the matter is 200 basis points is not a lot of cutting when you’ve got a bubble this big, and when you’re going to try to reflate an even bigger bubble, you’re going to have to have a lot more ammunition than that, which is why the Fed is going to be going back to quantitative easing. But even that is not going to be enough because it’s going to produce an overdose.”

Also in this podcast, Peter analyzes the bear market rally in the US stock markets and makes the case that the US economy was stronger before we had a bunch of economic advisors – highlighting some of the absurdity coming from Larry Kudlow.

END

Who would have thought that this might happen… hi grade Nickel may have severe supply problems in the next few years

(Lesage/Oil Price.com)

Tightening Nickel Supply Threatens Electric Vehicle Boom

Authored by Jon LeSage via Oilprice.com,

For Tesla and its chief competitors in the race for global domination of electric vehicle sales, it ain’t all about lithium ion.

There are other valuable metals needed to make the battery packs do what’s asked of them, with nickel being essential. Tesla and its battery producer partners, and other automakers and their suppliers, are worried about the longer-term supply of nickel according to a new study by BloombergNEF.

The study predicts that EV makers will be driving demand for nickel about 16 times to 1.8 million tons in the next years.

Class-one nickel, a high-purity material used in batteries, is expected to see demand greatly outstrip supply in the next few years. That will be fueled by meeting the large Chinese EV market, and other global markets where demand is expected to grow.

That need for class-one nickel will outstrip supply within five years, according to the study.

One problem has been a lack of real investment in new mines for materials including nickel, Tesla’s global supply manager of battery metals, Sarah Maryssael, said at a Washington meeting in May. That could drive up prices as battery demand increases greatly.

Tesla CEO Elon Musk is concerned about having enough economically viable — and available — metal to continue meeting its growing electric car demand. That will take off even more as the company taps into China’s booming markets.

“They are getting ready to have the new factory in China, and are at full capacity in North America,’’ Peter Bradford, chief executive officer of nickel producer Independence Group NL, said.

“They recognize the biggest risk from a strategic supply point of view is nickel.’’

Bradford last week met with one of Tesla’s battery metals supply chain team. His company, Perth-based Independence, last year increased nickel output from its Nova mine in Western Australia. Independence will be spending as much as A$75 million ($51 million) on exploration in an effort to extend the asset’s life and find new deposits.

Bradford’s industry had been focused mainly on supplying the metal to stainless steel. By 2030, the BloombergNEF study expects that batteries will account for more than half of demand for the valuable class-one nickel.

Metal suppliers have been scrambling to find the right metal to fill that demand. Australian firm BHP, the biggest maker, is betting on bright-turquoise colored nickel sulphate. That will be taking place at its nickel refinery south of Perth, with plans to potentially carry out the industry’s largest expansion.

The mining company had been seeking a buyer for its Nickel West facility, but reversed course recently after reviewing growth forecasts in lithium-ion batteries and a scarcity of high-quality nickel supply.

The challenge will be there to mass produce more affordable EVs and meet consumer demand in China and other key markets; battery costs have been the biggest stumbling block to reaching that sales volume. Increasing government mandates to bring in more EVs is part of the forecast, with incentives being offered and alliances being forged to increase public charging stations.

Tesla is seeing car buyers impatiently waiting for delivery of their Model 3 electric cars. The company is betting that its upcoming Model Y will be in strong demand, and is already preparing to have production capacity in place more in line with the popular Model 3.

The Model 3 looks like a smaller version of the Model S, and the Model Y will be available to car shoppers interested in the crossover SUV functionally of the Model X, but also want to have a more affordable and smaller alternative. Musk is also promising that the Model Y will have 300 miles of range, which would address a critical concern for buyers ready to leave their gasoline-powered cars behind for the first time ever.

A new Wood Mackenzie study sees the metals problem much broader, with lithium, cobalt, and nickel supplies to be worst hit over the next few years.

Supply for the three metals is fine for now, said Gavin Montgomery, research director at Wood Mackenzie. Short-term market prices have fallen, and that will deter producers from increasing supply to meet future demand, he said.

But long-term that will change. Demand is expected to grow so rapidly with car makers taking on their ambitious goals to mass produce EVs, that metal suppliers won’t be able to keep up, Montgomery said.

Automakers and their battery partners need to start planning for it now.

“Getting the quantity of nickel that (electric vehicles) will need by the mid-2020s will be a challenge … with lead times often up to 10 years, investment needs to happen now,” Montgomery said.

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

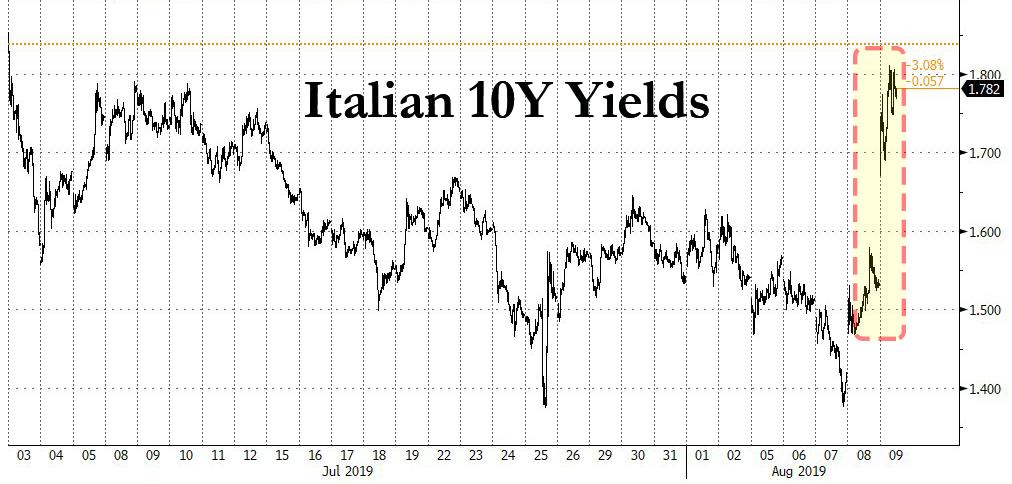

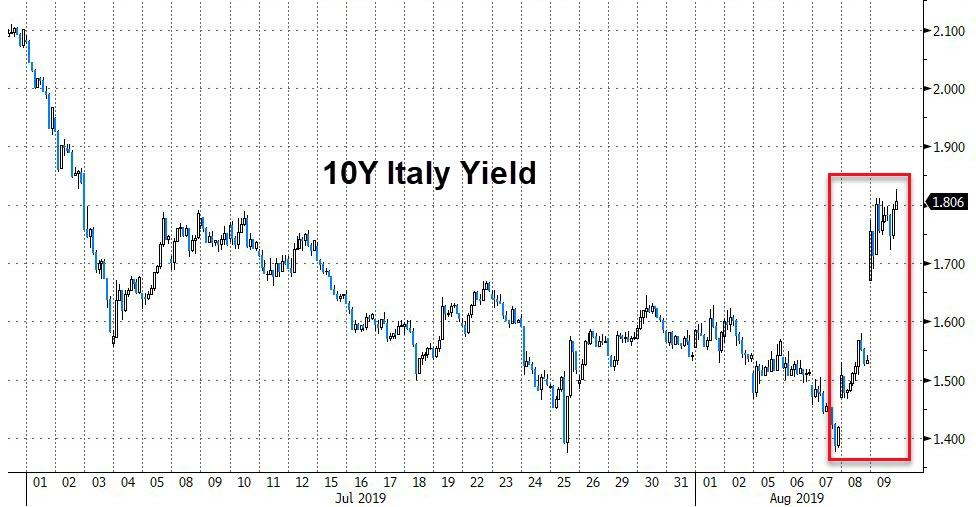

Global Markets Tumble On Trade War Fears, Italian Bonds Plunge As Crisis Returns

Global stocks and US equity futures were set to end the week in a sea of red as trade war tensions resurfaced after the US was said to hold off on Huawei licenses in retaliation for China’s halting of US crop imports…

… while fears of a government crisis in Italy sent the country’s bond plunging, after Deputy PM Salvini called for a snap election, fanning political uncertainty and prompting a haven bid in bunds. Italy’s BTPs tumbled led by the belly, with the 5-year yield rising 30bps to 1.14% and the 10-year yield up 25bps to 1.78%, widening the BTP-bund spread by 29bps to 238bps, amid a violent selloff as 10-year futures volumes surge to 250% of the 10-day average.

The fresh risk-off episode left gold on course for its best week in three years, Japan’s yen near an eight-month high and bonds surging. Meanwhile, US stock futures were down as much as 0.5%, while MSCI’s broadest index of world shareswas headed for its second straight week of declines, after one of its worst days in years on Monday.

With one day left until the weekend after a historically turbulent week, dominated by a symbolic drop in China’s currency was not finished yet: a Bloomberg report that Washington was delaying a decision about allowing some trade between U.S. companies and Huawei again spooked Asia. Markets in the region slumped with the MSCI Asia ex-Japan index ending down 2.3% for the week after data showed China’s first decline in producer prices in three years, compounding the Huawei disappointment, with South Korea advancing amid oversold signs for Kospi stocks and Hong Kong sliding. Japan’s Topix, meanwhile, rose 0.4%, boosted by technology shares, as Japan’s economy grew more than expected in the second quarter. The Shanghai Composite Index retreated 0.7%, capping a second week of losses, with Kweichow Moutai and China Merchants Bank among the biggest drags, after Beijing reported the first negative PPI print in 3 years even as food inflation soared, pushing CPI to the highest in 16 months, and leaving the PBOC in a bind, unable to cut rates to stimulate the economy.

As Bloomberg reported after the close on Thursday, Washington held off on a decision about licenses for U.S. companies to restart business with Huawei, while Beijing halted purchases of U.S. farming goods. India’s Sensex rose 0.8%, buoyed by HDFC Bank and Housing Development Finance, amid optimism the government may drop an increased surcharge on foreign investors registered as trusts.

The European session was uglier, and was led lower by a 2.4% slump in Italian stocks after Matteo Salvini, the leader of one of the country’s ruling parties, the League, pulled his support for the governing coalition on Thursday. The Stoxx Europe 600 index’s decline was led by automaker shares.

While Italian snap elections have been likely for months, markets were jarred when Salvini, who’s publicly insisted the government would last its full five years before, pushed for a new poll as deja vu moments of bidless Italian bonds filled traders with dread. The result was a plunge in Italian government debt, which pushed yields on 10-year Italian bonds up 26 basis points to 1.8%, the biggest daily increase in over a year.

“Those who waste time hurt the country,” the League said in a statement as it presented a no-confidence motion to the Senate in Rome.

Meanwhile, London’s FTSE and the pound were under strain, too, with Gilt yields sliding and cable tumbling to 1.2080, the lowest since the start of 2017, after the UK reported its economy unexpectedly shrank in the second quarter, the first contraction in seven years.That followed reports on Thursday that the new UK Prime Minister, Boris Johnson, was planning for an election after an Oct. 31 Brexit. Those reports had shoved sterling to a two-year low against the euro.

“It has been a very volatile week,” said Elwin de Groot, Rabobank’s head of macro strategy. “Until recently, the markets’ view was that this trade war will be resolved, but clearly now the thinking is that maybe this is not the case and it could be accelerating from here,” and Italy and Brexit worries are now adding to that, he said.

As a result, treasuries ticked higher alongside gold, which extended above $1,500 per ounce. While most of Europe’s debt inched higher, Italy’s bonds plunged with benchmark 10-year yields heading for the biggest increase since 2018 (see more above).

In FX, a turbulent week for the yuan ended on a calmer note, reflecting the central bank’s efforts to sooth nerves after the currency dropped below 7 per dollar. Volume in the onshore rate has fallen every day since Monday, with the PBOC on Friday setting its daily reference rate for the onshore yuan at a level that was in line with expectations. A gauge of expected volatility in the offshore yuan fell for a fourth day. Recent fixings reinforced the message that the PBOC seeks stability, said Ken Cheung, senior FX analyst at Mizuho Bank. “Recent onshore yuan fixings with counter cyclical factor in place to slow down depreciation flagged PBOC’s policy to guide a gradual depreciation rather than one-off sharp yuan depreciation,” he said. Still, the currency continued to weaken against a basket of trading partners’ currencies, hitting a new low after dropping to its lowest level since at least 2015 on Thursday.

Emerging-market equities and currencies headed for third week of declines as escalating trade tensions and concerns of a global slowdown shattered a recent calm, even as central banks pushed through rate cuts to limit the damage. The MSCI stocks gauge for developing nations extended its August slump to 5.1% after Thursday’s rebound proved short-lived. The currency index erased its 2019 gains, with the South African rand leading this week’s retreat. Peru joined peers from India to Brazil in cutting interest rates amid a deteriorating growth outlook as the intensifying conflict between China and the U.S. takes its toll on trade and investment flows. China’

China’s pledge to keep the yuan steady gave markets a brief respite Thursday, but the bearish outlook returned to sour sentiment on Friday. “We are in a slight risk-off mode today,” said Guillaume Tresca, senior emerging-market strategist at Credit Agricole in Paris. “The decline of growth prospects, the yuan’s weakening and the trade war concerns are behind the emerging-market currencies’ depreciation.”

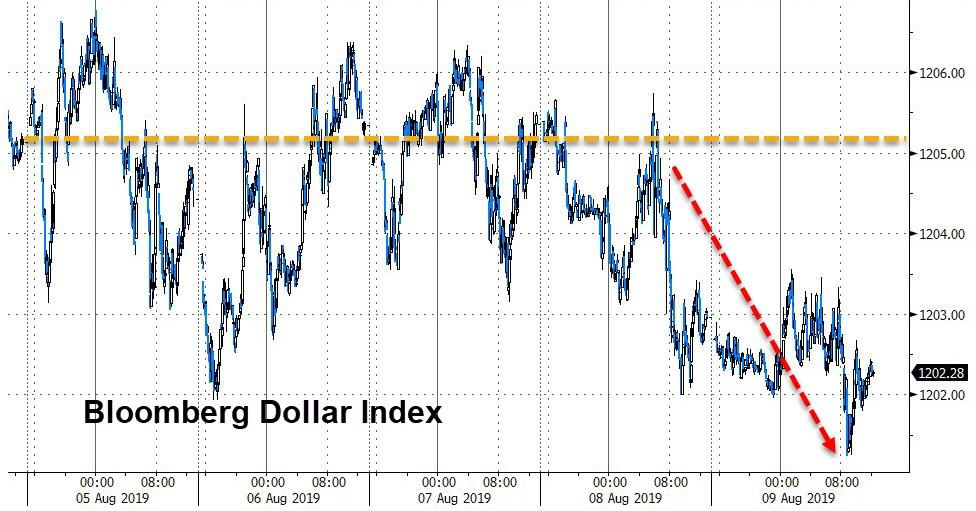

Elsewhere in FX, the dollar was weighed down by renewed complaints by Trump about the U.S. currency’s strength; the greenback weakened against all of its G-10 peers except the pound, while the Bloomberg Dollar Spot Index was set for its first weekly decline in four. Meanwhile, sterling was set for its fourth weekly decline against the dollar after poor growth data added to Brexit-related political uncertainty. The yen gained for a third day and Treasuries advanced as investors sought shelter in haven assets with no signs of a let-up in the U.S.-China trade war.

“The news about Huawei triggered the rise in the yen,” said Junichi Ishikawa, senior foreign exchange strategist at IG Securities. “This is a reminder that the U.S.-China trade dispute remains a risk, and this risk is not receding.”

Other safe havens also gained. Gold rose back above $1,500 on Friday, its highest in more than six years, en route to its best week since April 2016. Oil prices held most of the previous day’s gains as well, on expectations of more production cuts by OPEC. Brent crude hovered at $57.32 per barrel. U.S. West Texas Intermediate crude fell 0.1% to $52.50. Worries about the global economy meant Brent was down over 6% for the week and WTI more than 5%.

“The trade spat is driving the market crazy,” said Jigar Trivedi, commodities analyst at Mumbai-based Anand Rathi Shares & Stock Brokers. “$1,500 (for gold) is now the new normal unless trade relations take a turn in a right direction.”

On today’s calendar expected data include PPIs. Cambrex, Hydro One, TransAlta and Tribune Media are among companies reporting earnings.

Market Snapshot

- S&P 500 futures down 0.5% to 2,926.50

- STOXX Europe 600 down 0.5% to 372.82

- MXAP up 0.3% to 152.33

- MXAPJ unchanged at 491.50

- Nikkei up 0.4% to 20,684.82

- Topix up 0.4% to 1,503.84

- Hang Seng Index down 0.7% to 25,939.30

- Shanghai Composite down 0.7% to 2,774.75

- Sensex up 1% to 37,700.04

- Australia S&P/ASX 200 up 0.3% to 6,584.43

- Kospi up 0.9% to 1,937.75

- German 10Y yield fell 2.6 bps to -0.586%

- Euro up 0.1% to $1.1191

- Italian 10Y yield rose 11.3 bps to 1.182%

- Spanish 10Y yield unchanged at 0.224%

- Brent futures up 0.7% to $57.79/bbl

- Gold spot up 0.1% to $1,502.89

- U.S. Dollar Index down 0.1% to 97.54

Top Overnight News from Bloomberg

- U.S. was said to decide to hold off on a decision about licenses for American firms to restart business with Huawei Technologies

- The U.K. economy shrank in the second quarter, delivering a blow to newly installed Prime Minister Boris Johnson. GDP fell 0.2% following a solid 0.5% advance in the previous three months while economists had expected output to be unchanged

- German exports registered their steepest annual decline in three years, highlighting the plight of a manufacturing sector suffering from global trade conflicts.

- Bayer AG is proposing to pay as much as $8 billion to settle more than 18,000 U.S. lawsuits alleging its Roundup herbicide causes cancer, according to people familiar with the negotiations.

- Italy’s PM Giuseppe Conte signaled he won’t leave office without a fight as his deputy, Matteo Salvini, took steps toward bringing the government down and forcing snap elections. The nation’s bonds plunged.

- UBS Group AG’s investment bank co-heads are working on their first shake- up of the business – plans which could entail plans could entail hundreds of job cuts

- U.K.’s Johnson says ‘Bags of Time’ to renegotiate Brexit with EU

- Oil Recovers From Seven-Month Low as Saudis Signal Export Curbs

- U.S. Warns of Shipping Interference in Strait of Hormuz

- RBA Governor Philip Lowe said he’s prepared to reduce Australia’s record-low interest rates further, though he signaled that the economy could in fact be through the worst of its slowdown

- Too much too soon on rates better than too little too late, Reserve Bank of New Zealand Governor Adrian Orr said to business audience

Asian equity markets traded mostly higher as the region got a mild tailwind from the strong performance on Wall St where stocks extended their rebound, helped by the recent better than expected Chinese trade data and continued PBoC restraint on the CNY. As such, ASX 200 (+0.3%) and Nikkei 225 (+0.5%) were higher with notable strength seen in tech stocks after similar gains in the sector stateside and with investors in Tokyo cheering better than expected GDP data, although weakness in real estate and profit taking in gold miners has limited the upside for Australia. Elsewhere, Hang Seng (-0.7%) and Shanghai Comp. (-0.7%) were choppy with initial support seen after the PBoC once again set a firmer than expected reference rate but with gains later pared after participants digested mixed inflation data in which CPI topped estimates but PPI contracted, while reports the US held off on the decision regarding Huawei licences after China stopped agricultural purchases, added to the cautiousness. Finally, 10yr JGBs were higher as they track upside in T-notes and as prices broke through prior at 154.50/55, with the BoJ also present in the market under its bond buying program in which it upped purchases in 1-3yr JGBs but lowered purchases of 3-5yr and 10-25yr maturities.

Top Asian News

- Huawei Suppliers Fall After U.S. Is Said to Hold Off on Licenses

- Philippines’ Diokno Sees Further Rate, Reserve Ratio Cuts

- Thailand Says Policy Panel Won’t Interfere With Central Bank

- China Mobile Jumps the Most in Two Years on Dividend Pledge

Major European indices have diverted from their Asia-Pac counterparts largely positive performance and opened and remain in negative territory [Euro Stoxx 50 -1.0%]. The FTSE MIB (-2.2%) is the notable underperformer this morning as the Italian political turmoil has escalated following comments from League’s Salvini that there is no longer a majority of support for the government and elections are necessary (a summary of the situation is available on the headline feed). The MIB’s underperformance is most significantly driven by banking names with the likes of UniCredit (-6.0%), UBI Banca (-6.0%) and Banco BPM (-8.3%) experiencing significant losses; as such, the FTSE MIB Banking Index is lagging (-4.4%) with the largest weighted bank in the Stoxx 600 Bank index (-1.5%), Intesa Sanpaolo (-4.5%), with a 3.8% weighting likely the most significant laggard out of Italy in terms of index points. Elsewhere, the DAX (-0.6%) did get a short-lived boost from a Bayer (+3.2%) update, where reported indicate the Co. are to propose up to a USD 8bln roundup settlement; which generated a significant spike in Co. shares from around EUR 63.50 to EUR 70.00 at best. DAX aside, this morning’s notable movers to the upside largely reside in the FTSE 100 (-0.2%), with WPP (+7.3%) topping the index higher post earnings where the Co. proposed an interim dividend of GBP 0.0266 and H1 net revenue came in above the prior. Sticking with the UK, but outside of the 100 are Hikma Pharmaceuticals (+6.8%) as the Co’s H1 revenue also came in above prior and additionally the Co. increased some FY guidance components.

Top European News

- Italy Early Election Might Be Set for Oct. 23: Repubblica

- Ukraine Eyes New IMF Deal Worth Up To $10B: Deputy C.Bank Chief

- Faith in Woodford Plummets as Fund Trades at Record Discount

In FX, GBP/EUR – The Pound has come under renewed pressure on the back of an unexpected, but not exactly shocking negative UK GDP print for Q2, while monthly IP and output data also missed expectations. However, Cable has dipped below the 1.2080 multi-year base and Eur/Gbp has just crossed yesterday’s 2 year high at 0.9265. given the single currency’s separate struggles in wake of more Italian political instability. Indeed, Eur/Usd remains capped around 1.1200 after the collapse of Rome’s 2-party coalition, and ahead of a confidence vote before fresh elections potentially in October or November, while circa 1 bn option expiries at the big figure and from 1.1175-60 may also keep the headline pair in check into Friday’s NY cut.

- JPY/CHF/NZD/AUD/CAD – All mildly firmer against the Greenback, albeit well within this week’s ranges and for the Yen that means largely anchored on 106.00 as Fib resistance just above (106.06) continues to be respected on a closing basis, while decent expiry interest between 105.90-106.00 could stall pull-backs towards 105.50. Meanwhile, the Franc has rebounded through 0.9750 and 1.0900 vs the Euro on the aforementioned renewed political uncertainty in Italy and the Antipodean Dollars are still clawing back post-RBNZ declines vs their US counterpart even though RBA comments and the SOMP overnight have underscored clear downside economic risks that will likely require further monetary, or perhaps even unconventional easing. Hence, Aud/Usd looks vulnerable above 0.6800 and Nzd/Usd just shy of 0.6500 as the Aussie/Kiwi cross pivots 1.0500. Turning to the Loonie, looming Canadian jobs and to a lesser extent perhaps housing data should provide some independent impetus as crude prices essentially tread water approaching the end of a volatile week and the DXY stays close to 97.5000. Usd/Cad currently trading towards the base of 1.3245-15 parameters.

- NOK/SEK – The Scandi Crowns are flat-lining against the Euro after some relatively big swings so far this week, with Eur/Nok and Eur/Sek meandering between 9.9955-9665 and 10.7475-7070 respectively and neither really reacting to data as Norwegian inflation metrics and Swedish household consumption updates were both somewhat mixed.

- EM – Broad losses vs the Buck as the overall risk tone sours again and specific bearish factors persist, while the Lira has also been subject to fresh reports about more Government interference at the CBRT (at least 9 senior personnel ‘given’ new roles, according to the FT). Elsewhere, the Yuan continues to weaken after another seemingly off-radar incrementally higher PBoC Usd/Cny mid-point fix (at 7.0136).

In commodities, WTI and Brent futures are firmer in early EU trade, albeit the benchmarks have far to go to retrace this week’s losses. The ramp up of US-China trade tensions saw the global benchmark slump to a current weekly low of 55.90/bbl (vs. 61.40/bbl weekly open), whilst WTI found a weekly base at 50.55/bbl (vs. 55.29/bbl weekly open). The former currently eyes 53/bbl (200 WMA 53.05/bbl) to the upside whilst the latter climbs closer towards 58/bbl (200 WMA at 57.76/bbl) . The oil demand outlook has been deteriorating with IEA the latest agency to cut its global demand growth forecast, by 100k BPD to 1.1mln BPD and 2020 by 50k BPD to 1.3mln BPD. The release is relatively in-fitting with EIA’s STEO earlier in the week, where it cut 2019 world oil demand growth forecast by 70k BPD to 1.0mln BPD, but raised its 2020 forecast by 30k BPD to 1.43mln BPD. Prices may also see support from the Saudi’s intention for intervention to stem the decline in the market, although official measures have not been announced. Elsewhere, a stellar week for gold as the yellow metal was bolstered as investors flocked to the safe-haven amid the aforementioned ramp up in protectionism. Spot gold has a current weekly (and 6-year) high of 1510/oz (vs. 1440/oz at the weekly open). BAML Flow Show notes that precious metals have reaped inflows of USD 2.3bln, its fourth largest weekly inflows to date. Meanwhile, copper prices are flat around the USD 2.6/lb level amid the cautious risk tone ahead of US’ market entrance. Sticking with base metals, iron ore prices continue to decline with the metal down 18% thus far this month amid a bleaker short-term demand outlook with steel mills potentially reducing operations on low profitability, whilst exports from Brazil and Australia continue to rise. The Reserve Bank of Australia, at its SoMP, also noted that iron ore prices are “expected to decline further” as supply gradually comes back online and China demand moderates. Finally, nickel prices continue to be supported by the speculation that Indonesia could reel in an export ban on nickel ore in a regulatory move. Indonesia initially planned to ban exporting nickel ore by 2022 in an attempt to build up its manufacturing base by using its raw resources. The country said that no decision has been made on the mineral ore export ban timing but bringing the deadline forward from 2022 will disrupt USD 4bln in ore exports.

US Event Calendar

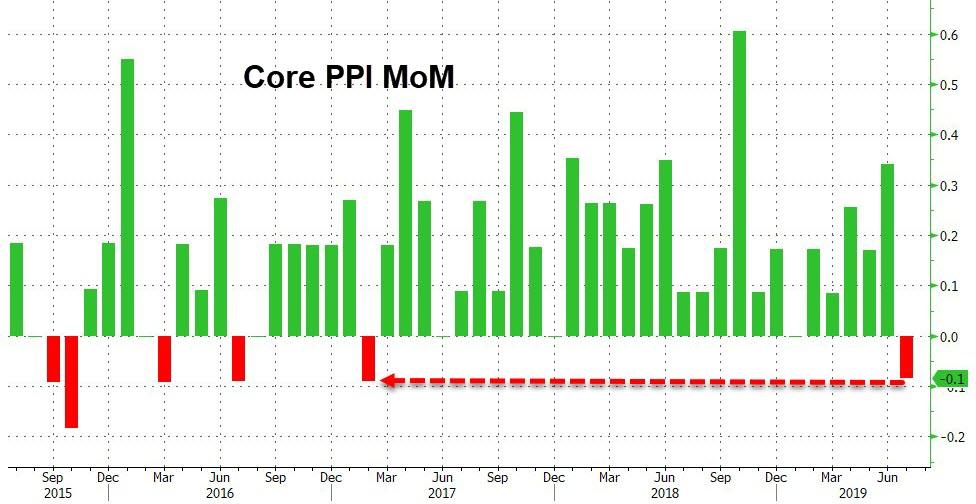

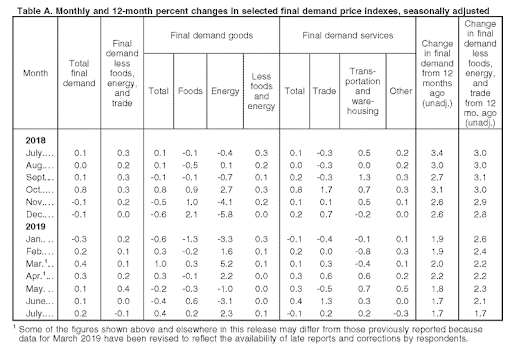

- 8:30am: PPI Final Demand MoM, est. 0.2%, prior 0.1%

- 8:30am: PPI Ex Food and Energy MoM, est. 0.11%, prior 0.3%

- 8:30am: PPI Ex Food, Energy, Trade MoM, est. 0.2%, prior 0.0%

- 8:30am: PPI Final Demand YoY, est. 1.7%, prior 1.7%

- 8:30am: PPI Ex Food and Energy YoY, est. 2.3%, prior 2.3%

- 8:30am: PPI Ex Food, Energy, Trade YoY, prior 2.1%

DB’s Jim Reid, off to vacation, concludes the overnight wrap

Right. At the end of today I’m going to put down my quill and ink pot and have a 2-week break. You’ll find me in the French Alps. One of my favourite bits of being in the Alps in summer is walking Bronte up and down the mountain across rolling Alpine meadows. At this time of the year it’s swarming with grasshoppers, who are slightly annoying to the ankles of a human, however they give Bronte the right hump. They jump all over her and flap in and out of her ears and face. She must burn three times the calories of a normal walk just by fighting them off. To be fair she gulps at them and I suspect she catches and eats about 50 on the average hourly walk. I’m hoping to get back on my bike for the first time since the accident a week ago but my derrière is still sore from the fall and my confidence might be a bit low for those steep mountain descents. So we’ll see. See you on the other side and you’ll be left in the very capable hands of Craig and Quinn.

The moves in the last couple of days means markets are going into my two-week break in a bit of a happier state with last night’s closing gains of +1.89% and +2.24% for the S&P 500 and NASDAQ, respectively, limiting the damage done since Trump’s tweet to ‘only’ -2.07% and -3.07% from intra-day lows of -5.95% and -7.61% on Monday. Yesterday’s rally was the best in two months, since Fed Chair Powell gave a dovish speech at the Chicago Fed conference on June 4. The recent rally hasn’t been accompanied by big swings in Fed expectations though with the market still pricing around 64bps of additional cuts this year. It remains to be seen if monetary policy can act as a shock absorber for markets moving forward. The reality is that the outcome is probably more binary than that. Monetary policy is unlikely to help much in a full blown trade escalation.

The good news is that the main talking point in markets yesterday was away from trade and instead reserved for a Reuters story which broke in the afternoon suggesting that Germany was mulling a “fiscal U-turn” by issuing new debt to finance a climate protection programme according to a senior government official. A bit of scepticism surrounded the news not least because this isn’t the first such story to emerge about a change of fiscal policy in Germany and also because there may be an element of political posturing behind the headlines. That being said, there is still a very significant and interesting side to the story if true. Our economists showed last week in their report ( here ) that Germany is the member state with room for manoeuvre within current fiscal rules and limits. DB’s Chief Economist Mark Wall made the point that the story (if true) signalled a political reset of domestic rules – not because of fears of where the economic cycle is going – but structurally because of climate change, which in itself is an increasingly viable policy route to fiscal spending, providing cover to those naturally opposed to higher spending. So a potentially very interesting development to follow.

The immediate response in bond markets was a sudden move higher in yields (a near 5bps rise in 5 minutes), however, that quickly faded as the market debated the story and Germany’s finance ministry played it down, saying there has not been a decision to give up the balanced budget. By the end of play, 10y Bunds finished just +2.1bps higher at -0.560% and close to where they were before the story hit. The big mover though were BTPs, which sold off +11.5bps and as much as +16.1bps at one point as news filtered through that PM Conte was meeting President Mattarella and thus raising fears over new elections. After European markets had closed, Deputy PM Salvini did confirm that his Northern League party wants new elections and will aim to dissolve the government. His party have nearly 40% support in recent opinion polls, nearly double that of his coalition partner. It’s not immediately clear if Mattarella will agree to new elections, or if he will ask other parties to try to form a new government. In theory, the Five Star Movement could join with the centre-left PD in a new coalition. If elections are called, they likely won’t be held for at least another 60 days after parliament is actually dissolved.

Back to fixed income and Treasuries ended up rallying -1.9bps (a further -1.7bps this morning) to 1.716%, paring a mid-session selloff of +5.4bps, with the reversal coming after a mixed 30-year auction. While demand wasn’t great in absolute terms, with the issuance tailing 1.3bps, that was better than Wednesday’s 10-year auction and much improved from last month’s 30-year issuance, which tailed 2.6bps. The improvement helped spark a rally in the long-end treasuries, taking the yield curve (2s10s) -2.9bps tighter to around 10bps.

As for other markets, the STOXX 600 (+1.66%) was buoyed by the fiscal story while HY spreads in the US and Europe were also -7.4bps and -3.2bps tighter respectively. Oil bounced back +3.43% after its recent selloff, while Gold again flirted with the $1500 level without firmly breaking out. It’s nudged back above this morning. EM assets performed well, with equities up +1.23% and Latin American currencies leading FX gains, especially the Brazilian real (+1.27%) and the Mexican peso (+0.92%).

Overnight, we have fresh trade headlines with Bloomberg reporting that the White House is holding off on a decision about licenses for US companies to restart business with Huawei after China said that it was halting purchases of US farming goods. Huawei suppliers Micron Technology (-1.34% ), Western Digital (-1.0% ), Qualcomm (-1.36% ), Xilinx (-0.82%) and NeoPhotonics (-6.31%) all fell in after-hours trading after news of the delay in license approvals.

The above news has poured a little cold water on the risk-on sentiment from yesterday as Asian equity markets are trading mixed with the Shanghai Comp (-0.37%) and Hang Seng (-0.18%) down while the Nikkei (+0.60%) and Kospi (+1.13%) are up. Meanwhile, all G10 currencies are trading higher this morning (c. +0.1% – +0.2% range) and the Chinese onshore yuan is trading at 7.0512 (-0.09%) after another slightly stronger fixing than expected. Elsewhere, futures on the S&P 500 are down -0.43%. We should also note that we’ve had the latest inflation data out of China where June CPI and PPI came in at +2.8% yoy (vs. +2.7% yoy expected) and -0.3% yoy (vs. -0.1% expected) respectively. The yoy decline in PPI is the first since September 2016. Meanwhile, the preliminary Q2 GDP data in Japan surprised on the upside at an annualized +1.8% qoq (vs +0.5% qoq expected and +2.8% qoq last quarter). Business spending (at +1.5% qoq vs. +0.8% qoq expected) and consumer spending (+0.6% qoq vs. +0.7% qoq expected) helped, with the latter getting lift from a 10-day public holiday and shoppers making purchases ahead of a planned sales-tax hike in October. This suggests that we should be a bit wary of reading too much into this surprise. Government spending also supported the expansion, contributing a surprisingly strong 0.7 pp to the annualized GDP growth figure.

In other news, the BoJ made changes to its bond purchase amounts in three different maturity zones at its regular operation today, which seems like an attempt to limit yield curve flattening. They cut the purchases of 3-5yr bonds (at JPY 360b vs. 380bn in previous auction) and increased buying of 1-3yr debt (at JPY 400bn vs. 380bn). Purchases of 10-25yr bonds was also reduced to JPY 160bn from JPY 180bn. Despite the reduction in purchases at the longer end, the yield on 10yr JGBs are down -1.5bps this morning to -0.217%. Elsewhere, Bloomberg reported that Turkey’s central bank removed at least nine high-ranking officials, including chief economist Hakan Kara, yesterday. Other officials removed from duty include the bank’s head of research, banking department chief, risk management chief and the institutional transformation manager.

On yesterday’s data front, the only noteworthy releases were in the US, where jobless claims fell by 8k to 209k. That’s right around their recent lows. Wholesale inventories were flat, compared to expectations for a 0.2% mom increase. That means that inventories, which had dragged around -0.9pp on the first estimate of US second quarter GDP growth, will likely provide an even bigger drag in the second estimate.

To the day ahead now, which this morning includes June trade data in Germany and June industrial production in France and the UK. We’ll also get the preliminary Q2 and June GDP readings in the UK along with June manufacturing production and trade data. In the afternoon the big release in the US is the July PPI report.

3A/ASIAN AFFAIRS

I)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 19.80 POINTS OR 0.71% //Hang Sang CLOSED DOWN 181.47 POINTS OR 0.69% /The Nikkei closed UP 91.47 POINTS OR 0.44%//Australia’s all ordinaires CLOSED UP .32%

/Chinese yuan (ONSHORE) closed DOWN at 7.0595 /Oil UP TO 53.27 dollars per barrel for WTI and 58.20 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0505 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0858 TRADE TALKS STALL//YUAN LEVELS PAST THE DANGEROUS 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

Last night: USA futures extend their losses after a weaker yuan fix

(zerohedge)

US Equity Futures Extend Losses After Weak Yuan Fix

Equity futures and bond yields traded lower ahead of the yuan fix following reports that Washington will not grant any licenses for deals with Huawei (in response to China not buying US ag products). But a weaker than expected fix by the PBOC sparked further selling pressure in US equity futures.