GOLD:$1498.80 DOWN $6.80(COMEX TO COMEX CLOSING

Silver:$17.06 DOWN 11 CENTS (COMEX TO COMEX CLOSING)/

Closing access prices:

Gold : $1498.40

silver: $17.06

option trading silver:

We are now entering options expiry week for the comex which ends , August 27.2019

OTC/ LBMA expires on Friday, the 30th.

What is very interesting is the quantity of silver contracts that are in the money as silver has rise quite nicely over these past two months. There is going to be a lot of silver being exercised and we may see a silver squeeze

(read James Turk/Kingworldnews/yesterday)

You know something is up when you see huge paper advances in the GLD and SLV

(see below)

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 9/45

EXCHANGE: COMEX

CONTRACT: AUGUST 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,504.600000000 USD

INTENT DATE: 08/21/2019 DELIVERY DATE: 08/23/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

118 H MACQUARIE FUT 24

661 C JP MORGAN 9

685 C RJ OBRIEN 6

686 C INTL FCSTONE 16 3

737 C ADVANTAGE 15 9

800 C MAREX SPEC 2

905 C ADM 6

____________________________________________________________________________________________

TOTAL: 45 45

MONTH TO DATE: 6,330

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 45 NOTICE(S) FOR 4500 OZ (0.1399 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 6330 NOTICES FOR 633,000 OZ (19.688 TONNES)

SILVER

FOR AUGUST

0 NOTICE(S) FILED TODAY FOR NIL OZ/

total number of notices filed so far this month: 1996 for 9,980,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 9946 DOWN 195

Bitcoin: FINAL EVENING TRADE: $ 10171 UP 31

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A HUGE SIZED 3659 CONTRACTS FROM 238,086 DOWN TO 234,447 DESPITE THE 1 CENT GAIN IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR AUGUST, 2159 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 3342 CONTRACTS. WITH THE TRANSFER OF 2159 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2159 EFP CONTRACTS TRANSLATES INTO 10.795 MILLION OZ ACCOMPANYING:

1.THE 1 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

9.985 MILLION OZ INITIAL STANDING IN AUGUST.

WE HAD ATTEMPTED BANKER COVERING OF SHORTS AT THE SILVER COMEX YESTERDAY WITH CONSIDERABLE SUCCESS..WE ALSO HAD ZERO SPREADING ACCUMULATION. AGAIN SOMETHING IS SCARING OUR SILVER SHORTS TO NO END!!

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF SEPTEMBER FOR SILVER.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF AUGUST BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

29,348 CONTRACTS (FOR 16 TRADING DAYS TOTAL 29,348 CONTRACTS) OR 146.74 MILLION OZ: (AVERAGE PER DAY: 1834 CONTRACTS OR 9.171 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 146.74 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 20.95% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1459.26 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3659, DESPITE THE 1 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 2159 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A STRONG SIZED: 1480 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2159 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 3639 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 1 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $17.17 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

WE ALSO HAD NO SPREADING ACCUMULATION YESTERDAY. THE LIQUIDATION PHASE OF THEIR OPERATION WILL PROBABLY COMMENCE ON FRIDAY AUGUST 23.

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.172 BILLION OZ TO BE EXACT or 167% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 9.985 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 679 CONTRACTS, UP TO 595,486 DESPITE THE SMALL $0.30 PRICING LOSS WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /

THE SPREADING ACCUMULATION OPERATION IS NOW IN FULL SWING ONLY FOR SILVER AS ZERO WAS ACCOMPLISHED IN THAT ENDEAVOUR TODAY. LIQUIDATION OF SPREADING CONTRACTS WILL COMMENCE AROUND THE 23RD OF AUGUST….. THE LIQUIDATION( AND ACCUMULATION) PHASE FOR COMEX OI GOLD STOPS FOR THE AUGUST CONTRACT MONTH /(THE LOSS IN COMEX SILVER OI TODAY WAS DUE TO BANKER SHORT COVERING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 5201 CONTRACTS: AUGUST 2019: 0 CONTRACTS, OCTOBER: 283, DEC> 4918 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 595,486,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY STRONG GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5880 CONTRACTS: 679 CONTRACTS INCREASED AT THE COMEX AND 5201 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 5880 CONTRACTS OR 588,000 OZ OR 18.28 TONNES. YESTERDAY WE HAD A TINY LOSS OF $0.30 IN GOLD TRADING.…AND WITH THAT TINY LOSS IN PRICE, WE HAD A STRONG GAIN IN GOLD TONNAGE OF 18.22 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER TO CONTAIN THE PRICE OF GOLD.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST : 156,169 CONTRACTS OR 15,616,900 oz OR 485.72 TONNES (16 TRADING DAY AND THUS AVERAGING: 9,760 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY IN TONNES: 485.72 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 485.72/3550 x 100% TONNES =13.68% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 3996.427 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIR SIZED INCREASE IN OI AT THE COMEX OF 679 DESPITE THE TINY PRICING LOSS THAT GOLD UNDERTOOK YESTERDAY($0.30)) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5201 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5201 EFP CONTRACTS ISSUED, WE HAD A VERY STRONG CRIMINALLY SIZED GAIN OF 5880 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5201 CONTRACTS MOVE TO LONDON AND 679 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 18.28 TONNES). ..AND THIS GOOD INCREASE OF DEMAND OCCURRED DESPITE THE TINY LOSS IN PRICE OF $0.30 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 45 notice(s) filed upon for 4500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $6.80 TODAY//(COMEX-TO COMEX)

WOW!! TWO TRANSACTIONS: ONE LATE LAST NIGHT:

i)A STRONG PAPER DEPOSIT OF 6.74 TONNES INTO THE GLD

ii)ANOTHER STRONG PAPER DEPOSIT OF:2.93 TONNES INTO THE GLD/LATE THIS AFTERNOON

INVENTORY RESTS AT 854.84 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 11 CENTS TODAY:

A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.696 MILLION OZ.

/INVENTORY RESTS AT 383.850 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A HUGE SIZED 3639 CONTRACTS from 238,086 DOWN TO 234,447 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER THIS MONTH AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR AUGUST: 0, FOR SEPT. 2159 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2159 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 3639 CONTRACTS TO THE 2159 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG SIZED LOSS OF 1480 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 7.440 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ ;AUGUST AT 9.985 MILLION OZ//

RESULT: A GIGANTIC SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 1 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 2159 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL. WE HAD CONSIDERABLE BANKER SHORT COVERING IN SILVER YESTERDAY.

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 3.11 POINTS OR 0.11% //Hang Sang CLOSED DOWN 221.32 POINTS OR 0.84% /The Nikkei closed UP 9.44 POINTS OR 0.05%//Australia’s all ordinaires CLOSED UP .31%

/Chinese yuan (ONSHORE) closed DOWN at 7.0855 /Oil UP TO 56.11 dollars per barrel for WTI and 60.82 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0855 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0862 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

SOUTH Korea/JAPAN

South Korea surprisingly scraps an intelligence pact with Japan as we have rising trade tensions.

(courtesy zerohedge)

3b) REPORT ON JAPAN

3C CHINA

i)The Chinese economy is now slowing down dramatically..it is down to 4.6%

(zerohedge)

ii)Last week we reported that China was restricting the importation of gold to its citizens and commercial banks. This was to stem the outward flow of dollars. However it did not stop China sovereign form importing gold.\\Now China has again partially lifted the restrictions as they certainly want its citizens to buy gold.

4/EUROPEAN AFFAIRS

i)Italy

An excellent commentary on the challenges facing Salvini as he deals with the technocratic President of Italy and the Brussels picked Conte. Salvini’s next move is to isolate Conte and force elections. We will be watching this attentively

(Tom Luongo))

i b)Italy

Five star seeking an alliance with the Democrats. That has zero percent chance of working as these two parties are polar opposite. This would be a death wish for the 5 star movement.

(zerohedge)

ii)GERMANY

(zerohedge)

iii)GERMANY

(zerohedge)

iv)UK/FRANCE

7. OIL ISSUES

8 EMERGING MARKET ISSUES

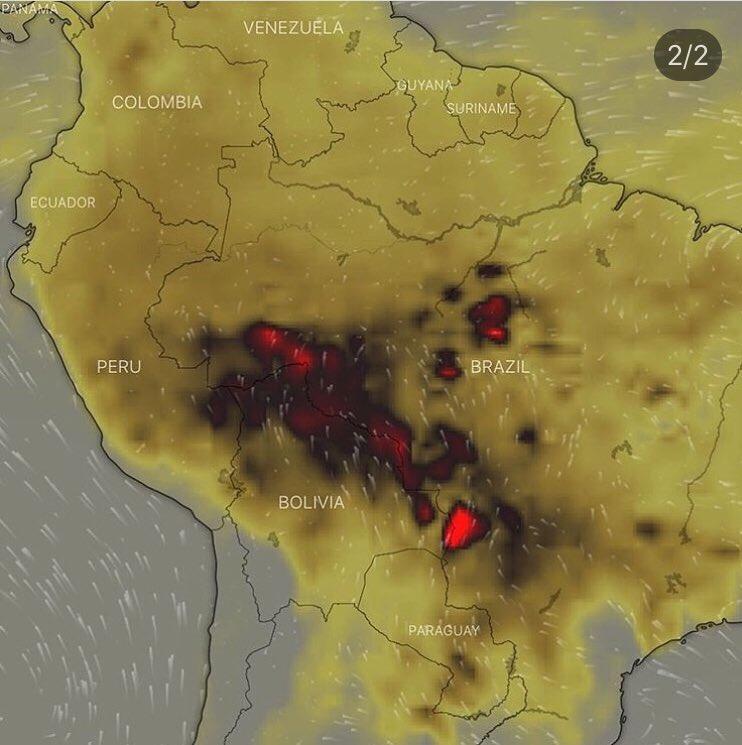

Brazil

Pay attention to this one! Wild fires are blazing throughout Brazil and destroying much of the rain forest. The rain forest produces 20% of our atmosphere’s oxygen

(Michael Snyder)

9. PHYSICAL MARKETS

i)The Iranian economy is in shambles. Parliament want to remove 4 zeros from the currency as hyperinflation is already started to rear its ugly head into this nation. The new currency will still be the rial and the toman, with one toman equal to 10 rials. In early days, one toman was equal to a sovereign in weight. As of this minute the riyal has traded at 116,500 per USA dollar and their inflation rate is around 40%

(Associated Press/GATA)

ii)Switzerland is doing everything they can to lower its value of the Swiss franc by continually lowering ints interest rate

(Bloomberg/GATA)

iii)Again the Indian government is toying with the idea of trying to convert citizens real gold into paper gold. It will never happen.

(London’s Financial Times/GATA)

iv)Simon Black outlines 4 reasons as to why you should hold gold

(Simon Black)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

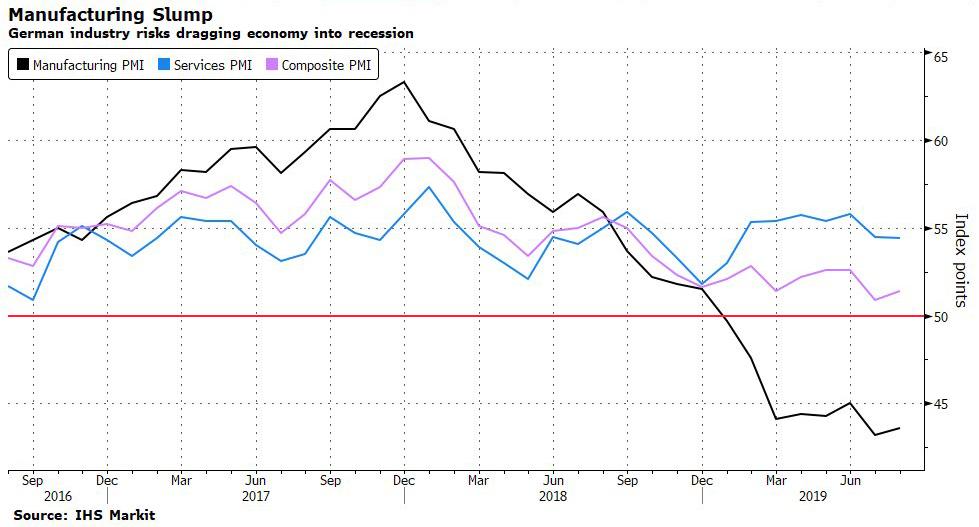

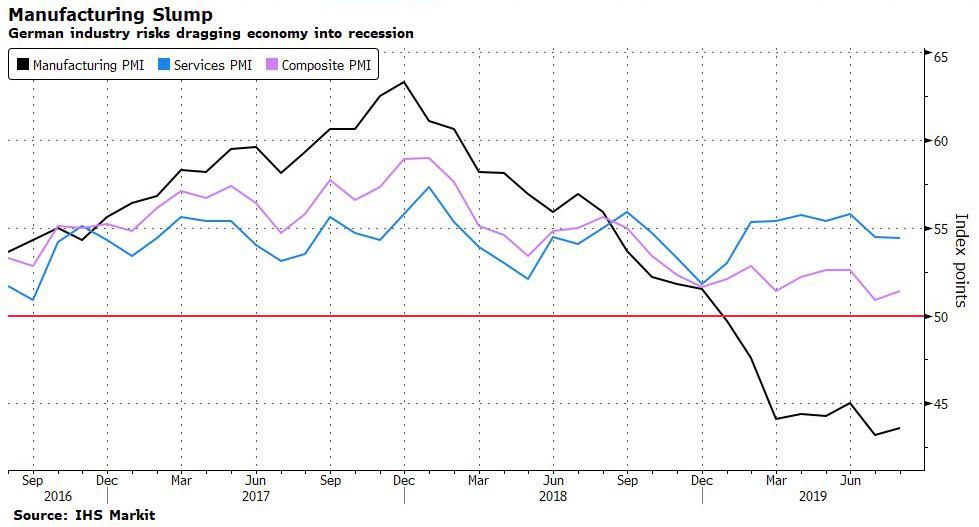

This is big news, Markit reports a huge downdraft in manufacturing PMi into contraction levels. It is the lowest print in 19 years, Not only that but the usually much stronger Service PMI also badly printed.

(zerohedge)

iii) Important USA Economic Stories

a)Huge number of Wall Street apartments is plaguing the Manhattan real estate market

(zerohedge)

b)If the American Justice system killed Jeffery Epstein is Julian Assange next

(Mac Slavo/SHFTPlan)

c)Dow goes into the green after Boeing jumps on news of record 737 Max production, if only the FCA would give them regulatory clearance.

(zerohedge)

iv) Swamp commentaries)

a)There is something sinister going on here; Patrick Byrne quits over his uproar on “deep state remarks” concerning the Clinton Foundaiton

(zerohedge)

b) this is big stuff!! I informed you that I thought Mifsud was a USA asset and that was the reason he hide from everyone. I guess that the Mueller team lied that Mifsud was a Russian asset.

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; nil oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 47,286 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 99,631 CONTRACTS.. we had some spreading accumulation and also banker short covering

YESTERDAY’S CONFIRMED VOLUME OF 99,631 CONTRACTS EQUATES to 498 million OZ 71.1% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -0.96% ((AUGUST 22/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.86% to NAV (AUGUST 22/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -/96%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 14.85 TRADING 14.38/DISCOUNT 3.18

END

And now the Gold inventory at the GLD/

AUGUST 22.WITH GOLD DOWN $6.80 TODAY: TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD: I)A PAPER DEPOSIT OF 6.74 TONNES INTO THE GLD (LATE YESTERDAY EVENING) AND 2) A PAPER DEPOSIT OF 2.93 TONNES LATE THIS AFTERNOON./INVENTORY RESTS AT 854.84 TONNES

AUGUST 21/WITH GOLD DOWN $.30 TODAY:A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.76 TONNES INTO THE GLD INVENTORY/GOLD INVENTORY RESTS AT 845.17 TONNES

AUGUST 20//WITH GOLD UP $2.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GOLD INVENTORY RESTS AT 843.41 TONNES

AUGUST 19/WITH GOLD DOWN $11.20//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .88 TONNES//INVENTORY RESTS AT 843.41 TONNES

AUGUST 16/WITH GOLD DOWN $7.35: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 844.29 TONNES

AUGUST 15/WITH GOLD UP $3.55 TODAY//WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: WE GOT BACK 7.63 TONNES OUT OF 11.11 TONNES LOST ON WEDNESDAY( A DEPOSIT OF 7.63 TONNES)/INVENTORY RESTS AT 844.29 TONNES

AUGUST 14/WITH GOLD UP $7.60 TODAY (AND DOWN $2.90 YESTERDAY) WE HAD A MONSTROUS WITHDRAWAL OF 11.11 TONNES OF GOLD FROM THE GLD/AND THIS WAS USED IN AN ABORTED RAID YESTERDAY: INVENTORY RESTS AT 836.66 TONNES

AUGUST 13.2019: WITH GOLD DOWN $2.60 TO DAY: A HUGE 7.92 PAPER GOLD TONNES WERE ADDED TO THE GLD/INVENTORY RESTS AT 747.77 TONNES

AUGUST 12.2019: WITH GOLD UP $7.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 839.85 TONNES

AUGUST 9/WITH GOLD DOWN $2.00//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REMAINS AT 839.85 TONNES OZ/

AUGUST 8: WITH GOLD DOWN $4.20: TWO TRANSACTIONS: A)A MONSTROUS PAPER DEPOSIT OF 8.50 TONNES WAS ADDED TO THE GLD/INVENTORY RESTS AT 845.42 TONNES b) A HUGE WITHDRAWAL OF 5.59 TONNES FROM THE GLD//INVENTORY RESTS AT 839.85 TONNES…ABSOLUTE FRAUD!

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 29/WITH GOLD UP $1.00: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 6.75 TONNES INTO THE GLD INVENTORY///INVENTORY RISES TO 824.89 TONNES

JULY 26/WITH GOLD UP $4.50: A HUGE INVENTORY WITHDRAWAL OF 4.09 TONNES OF PAPER GOLD LEAVES THE GLD/INVENTORY RESTS AT 818.14 TONNES

JULY 25.2019: WITH SILVER DOWN 19 CENTS: ANOTHER PAPER WITHDRAWAL OF 1.17 MILLION OZ/INVENTORY REST AT 358.213 MILLION OZ

JULY 24…A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A GAIN OF 1.685 MILLION OZ/INVENTORY RESTS AT 359.383 MILLION OZ

JULY 23/2019: WITH SILVER UP 5 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.221 MILLION PAPER OZ ADDED INTO THE GLD INVENTORY//INVENTORY RESTS AT 357.698 MILLION OZ////

JULY 22.2019/WITH SILVER UP 21 CENTS TODAY: A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 8.939 MILLION OZ ADDED TO THE SLV INVENTORY/INVENTORY RESTS AT 355.919 MILLION OZ//

JULY 19/WITH GOLD DOWN $1.00: A MASSIVE DEPOSIT OF 11.44 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 814.62

JULY 18/WITH GOLD UP $5.55 TODAY: A BIG PAPER DEPOSIT OF 3.81 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 803.18 TONNES

JULY 17/WITH GOLD UP $11.35 TODAY: A BIG WITHDRAWAL OF 1.17 TONNES FROM THE GLD//INVENTORY RESTS AT 799.37 TONNES

JULY 16: WITH GOLD DOWN $2.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 15: WITH GOLD UP $1.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 12/WITH GOLD UP $5.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 11.WITH GOLD DOWN $5.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 10//WITH GOLD UP $11.65 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER GOLD DEPOSIT OF 6.46 TONNES/INVENTORY RESTS AT 800.54 TONNES

JULY 9/WITH GOLD UP 70 CENTS, A HUGE PAPER WITHDRAWAL OF 2.89 TONNES WHICH WAS USED IN THE FUTILE RAID ON GOLD AND SILVER THIS MORNING//INVENTORY RESTS AT 794.08 TONNES

JULY 8/ WITH GOLD DOWN 35 CENTS A HUGE WITHDRAWAL OF 1.47 TONNES FROM THE GLD/INVENTORY FALLS TO 796.97 TONNES

JULY 5TH/WITH GOLD DOWN $19.50/NO CHANGES IN GOLD INVENTORY AT THE GLD//INV RESTS AT 798.44 TONNES

JULY 3// WITH GOLD UP $12.60 TODAY A SURPRISE WITHDRAWAL OF 1.76 TONNES FROM THE GLD//INVENTORY RESTS AT 798.44

JULY 2. WITH GOLD UP $18.90 A HUGE “PAPER” DEPOSIT OF 6.16 TONNES INTO THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 1: WITH GOLD DOWN $24.70 A HUGE “PAPER GOLD” WITHDRAWAL OF 1.76 TONNES FROM THE GLD/INVENTORY RESTS TONIGHT AT 794.04 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

AUGUST 22/2019/ Inventory rests tonight at 854.84 tonnes

*IN LAST 649 TRADING DAYS: 80.56 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 549- TRADING DAYS: A NET 86.11 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

AUGUST 22/WITH SILVER DOWN 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.696 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 21/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 20.WITH SILVER UP 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 19/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 16/: WITH SILVER DOWN 9 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 15/2019 WITH SILVER DOWN 2 CENTS: ANOTHER BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING 3.977 MILLION OZ PAPER DEPOSIT/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 14/2019 WITH SILVER UP 27 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 4.538 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 376.177 MILLION OZ//

AUGUST 13/2019: WITH SILVER DOWN 9 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 6.082 MILLION OZ///INVENTORY NOW RESTS AT 371.637 MILLION OZ

AUGUST 12/2019: WITH SILVER UP 11 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 365.557 MILLION OZ.

AUGUST 9/2019//WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.245 MILLION OZ INTO THE SLV INVENTORY/INVENTORY ADVANCES 365.557 MILLION OZ

AUGUST 8/WITH SILVER DOWN 23 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT: 1.409 MILLION OZ INTO INVENTORY///INVENTORY RESTS AT 363.311 MILLION OZ//

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 29/2019: WITH SILVER UP 4 CENTS TODAY: A SMALL WITHDRAWAL OF 468000 OZ FROM THE SLV/INVENTORY LOWERS TO 356.715 MILLION OZ//

JULY 26.2019: WITH SILVER DOWN 2 CENTS TODAY: A HUGE 1.03 MILLION OZ OF PAPER SILVER LEAVES THE SLV/INVENTORY LOWERS TO 357.183 MILLION OZ//

JULY 25.2019: WITH SILVER DOWN 19 CENTS: ANOTHER PAPER WITHDRAWAL OF 1.17 MILLION OZ/INVENTORY REST AT 358.213 MILLION OZ

JULY 24…A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A GAIN OF 1.685 MILLION OZ/INVENTORY RESTS AT 359.383 MILLION OZ

JULY 23/2019: WITH SILVER UP 5 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.221 MILLION PAPER OZ ADDED INTO THE GLD INVENTORY//INVENTORY RESTS AT 357.698 MILLION OZ////

JULY 22.2019/WITH SILVER UP 21 CENTS TODAY: A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 8.939 MILLION OZ ADDED TO THE SLV INVENTORY/INVENTORY RESTS AT 355.919 MILLION OZ//

JULY 19/WITH SILVER FLAT TODAY: ANOTHER MONSTROUS PAPER DEPOSIT OF 3.276 MILLION OZ ENTERS THE SLV//WHAT A MASSIVE FRAUD//INVENTORY RESTS AT 346.980 MILLION OZ

JULY 18/WITH SILVER UP 24 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.668 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 343.704 MILLION OZ//

JULY 17: WITH SILVER UP ANOTHER 29 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.518 MILLION OZ/INTO THE SLV INVENTORY///INVENTORY RESTS AT 341.036 MILLION OZ//

JULY 16: WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY: 15 WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY 12/WITH SILVER UP 10 CENTS: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 11/NO CHANGE IN SILVER INVENTORY

JULY 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 9/WITH SILVER UP A SMALL 7 CENTS A GIGANTIC INVENTORY GAIN OF 4.026 MILLION OZ/ INVENTORY RESTS AT 332.518 MILLION OZ AND NOW IT SHOULD BE QUITE CLEAR THAT THE SLV ( AND GLD ARE FRAUDS)

JULY 8/WITH SILVER UP 7 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 328,492 MILLION OZ

JULY 5/WITH SILVER DOWN 32 CENTS WE STRANGELY HAD A HUGE INVENTORY GAIN OF 2,234 MILLION OZ//INVENTORY RESTS AT 328.492 MILLION OZ

JULY 3 WITH SILVER UP 10 CENTS A HUGE INCREASE IN INVENTORY..INVENTORY RESTS AT 326.151 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 323.330 MILLION OZ//

JULY 1/ WITH SILVER DOWN 16 CENTS: A SURPRISING DEPOSIT OF 936,000 OZ INTO THE SLV/INVENTORY RESTS TONIGHT AT 323.330 MILLION OZ/

AUGUST 22/2019:

Inventory 383.850 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.02/ and libor 6 month duration 2.03

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: + .01

XXXXXXXX

12 Month MM GOFO

+ 1.91%

LIBOR FOR 12 MONTH DURATION: 1.95

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.04

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Gold Steady At $1,500 As Russia Buys Another 300,000 Ounces Of Gold In July

- Russia increased it’s gold reserves by another 300,000 ounces in July and its gold reserves are now worth $101.9 billion

- Total amount of Russian gold reserves rose 0.4% in July, reaching 71.3 million ounces or 2,218 tons as of August 1

- Official figures show gold now accounts for 19.6% of the total reserves of the Russian Federation

- Russia was the world’s largest gold buyer last year and bought nearly 275 tons, the largest amount ever purchased in a single year, according to the World Gold Council

- Russia is en route to become the world’s fourth largest foreign exchange holder after China, Japan, and Switzerland

News and Commentary

Gold steady, focus on Jackson Hole summit for rate-cut direction

Fed debated bigger rate cut, wanted to avoid appearing on path for more cuts

Fed members affirm ‘mid-cycle adjustment,’ see no ‘pre-set course’ for cuts, minutes show

Surge in corporate debt with negative yields poses risk ‘unlike anything’ investors have ever seen

Russia Buys More Gold in July, Taking Reserves Well Above $100bn

Going for gold: Russia boosts bullion stockpile by 9 tons in July

Ira Epstein Precious Metals Update Video: Gold consolidating

Gold Prices (LBMA – USD, GBP & EUR – AM/ PM Fix)

21-Aug-19 1499.65 1503.25, 1235.41 1238.53 & 1351.48 1354.43

20-Aug-19 1502.65 1504.55, 1242.69 1239.60 & 1356.44 1357.86

19-Aug-19 1499.35 1496.60, 1236.66 1235.29 & 1350.76 1348.89

16-Aug-19 1509.05 1515.25, 1242.55 1246.14 & 1361.46 1367.82

15-Aug-19 1517.65 1515.65, 1254.49 1250.26 & 1361.48 1363.78

14-Aug-19 1500.35 1513.25, 1241.69 1253.73 & 1341.61 1356.17

13-Aug-19 1527.20 1498.40, 1265.90 1240.38 & 1363.48 1338.67

12-Aug-19 1501.95 1504.70, 1244.82 1243.63 & 1343.64 1341.74

09-Aug-19 1503.50 1497.70, 1242.19 1240.99 & 1342.02 1338.05

08-Aug-19 1497.40 1495.75, 1230.26 1234.14 & 1335.08 1335.70

07-Aug-19 1487.65 1506.05, 1225.82 1239.33 & 1330.11 1341.44

06-Aug-19 1461.85 1465.25, 1199.59 1201.21 & 1304.85 1311.11

05-Aug-19 1457.45 1465.25, 1199.92 1203.85 & 1307.92 1310.23

02-Aug-19 1436.05 1441.75, 1184.17 1187.28 & 1294.02 1298.44

Listen and Watch Jim Rogers Interview Here

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

The Iranian economy is in shambles. Parliament want to remove 4 zeros from the currency as hyperinflation is already started to rear its ugly head into this nation. The new currency will still be the rial and the toman, with one toman equal to 10 rials. In early days, one toman was equal to a sovereign in weight. As of this minute the riyal has traded at 116,500 per USA dollar and their inflation rate is around 40%

(Associated Press/GATA)

iii) Other physical stories:

Simon Black outlines 4 reasons as to why you should hold gold

(simon Black)

4 Compelling Reasons To Be Thinking About Gold

Authored by Simon Black via SovereignMan.com,

From time to time it’s important to take a giant step back and take a fresh look at everything that’s going on with a big picture perspective.

The last few weeks has been nothing short of incredible… so many important things happening that have never happened before ever.Let’s take a step back together:

1) $50 billion to “elevate your consciousness”

As we discussed on Monday, WeWork filed its formal IPO paperwork in the United States last week, indicating that the company will be worth nearly $50 BILLION when it goes public.

WeWork has never turned a profit. It doesn’t expect to turn a profit. It doesn’t have a plan to turn a profit. And it claims its mission is to ‘elevate the world’s consciousness’.

WeWork owns no real estate. It has almost no assets. In fact, WeWork’s primary asset is the office space it currently leases (i.e. does not own).

And to be fair, they’re leasing a LOT of space. WeWork hopes to eventually lease 40 million square feet of office space.

But at $50 BILLION, investors are essentially paying $1,250 for each square foot of office space that WeWork is LEASING.

That’s almost as expensive as what it costs to BUY in New York City.

Talk about overpaying.

Then there’s are the ridiculous shenanigans of WeWork’s co-founder/CEO Adam Neumann, who has a history of unethical behavior.

Neumann charged his own company nearly $6 million for the “We” trademark earlier this year. He borrowed money from the company to buy real estate that he immediately leased back to WeWork.

And now he’s selling shares in this IPO to investors which have dramatically diminished voting rights… further cementing his power over the company.

So not only are investors dramatically overpaying for a company that has very few assets and burns cash with no end in sight, but they’re willingly giving up control to someone who has a history of enriching himself at their expense.

2) Yikes! Interest rates

But perhaps even more insane than WeWork (if that’s even possible) is what’s happening with interest rates.

Last week the yield on the 30-year US Treasury Bond hit an ALL-TIME LOW, breaking below 2% for the first time ever.

In other words, investors have essentially agreed to loan money to the US federal government for THREE DECADES at less than 2% per year.

That’s pure madness. That rate doesn’t even keep up with inflation… let alone take into consideration that the US government is totally insolvent.

But if you think that’s bad, Germany’s 30-year bond is presently at MINUS 0.12%! In fact, there is not a single German government bond that has a yield above zero right now.

(According to the Financial Times, there’s more than $15 TRILLION worth of bonds in the world right now that have negative yields!)

And next door in Austria, the government has issued a 100-year bond that yields just 1.1%.

100 years! Just think of everything that could happen over that period of time. It was barely a century ago, in fact, that the Austro-Hungarian Empire collapsed after World War I and the Austrian republic even came into existence!

And then of course there was the great hyperinflation of the 1920s, the German invasion of 1938, etc.

But I’m sure the next 100 years will be all rainbows and buttercups… more than justifying a 1.1% annualized return that doesn’t even keep up with inflation.

3) Stock market jitters

The past few weeks have seen the US stock market swooning, down 400 points, up 500 points, down 800 points. These are pretty wild swings, suggesting that investors are extremely uncertain and struggling to find anywhere sensible to put their money.

4) The Federal Reserve is extremely aggressive

It’s remarkable that the Federal Reserve (along with most of the world’s central bankers) is cutting interest rates.

By most measurements, the US economy is overheating. Unemployment is at a historic low. Yet the Fed is CUTTING interest rates (which are already WAY below historic averages).

Central banks typically only cut rates in a time of economic weakness, or rising unemployment. Cutting rates during ‘good times’ is incredibly unusual.

This leads me to gold…

None of this is supposed to be happening.

Investors aren’t supposed to overpay for shares of a real estate company that doesn’t actually own any real estate.

They’re not supposed to suffer NEGATIVE interest rates… or record low yields on long-term bonds.

The market isn’t supposed to constantly bounce around like a pinball. The Fed isn’t supposed to be aggressively slashing interest rates when the unemployment rate is near a record low.

The general theme here is chaos and uncertainty. The system is clearly broken. Again, none of this is supposed to be happening.

And that’s what makes gold such a sensible asset to own right now.

Gold is an asset with a 5,000+ year history of value and marketability. But it’s especially valuable in times of chaos and uncertainty.

I’ve been writing about this for quite some time, arguing back in December and January that it was a great time to buy gold.

Gold prices are up 20% since then. But they could still have more room to rise. (And silver could rise a LOT more.)

Stocks are still hovering near all-time highs. Bonds are at all-time highs. Property prices are near all-time highs.

Nearly every major asset class is near an all-time high. But not gold. Gold is still 30% from its all-time high. And silver would need to more than double to reach its all-time high.

Nothing goes up or down in a straight line… and gold has been rising for months. So it’s possible there may be a correction on the way.

But longer term, if this insanity, chaos, and uncertainty continue, gold is poised to do very well

END

For your interest..

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Rally Fizzles As Traders Digest FOMC Minutes, Brace For Jackson Hole

US equity futures drifted lower, tracking European and Asian stocks in the red as uncertainty over the outlook for interest rate cuts following the release of the FOMC minutes kept investors on edge, while few traders were willing to trade in size with the Jackson Hole meeting set to begin. The yen and dollar jumped as the euro dropped and the yuan tumbled, while Treasuries edged higher with oil, while gold dipped.

The euro and German yields initially nudged initially higher after better-than-expected PMI readings in the euro area helped offset some fears of an imminent European recession. The moves were modest, however, and gains quickly faded as the manufacturing readings remain challenging (especially in Germany).

Some details on the latest PMI report from Goldman:

- The Euro area Flash composite PMI was up three-tenths in August, against expectations of a decline. The gain only partially offset the decline in July. The breakdown of the Euro area PMI showed a small increase in the services PMI (+0.2pt to 53.4) and a larger one in the manufacturing PMI (+0.5pt to 47.0). Within the manufacturing PMI, employment, new orders and output were higher than their July levels, but remain in contractionary territory.

- At the country level, the French PMIs recorded gains across all subcomponents, helping to push the composite PMI up 0.8pt to 52.7. New orders increased in both the service and manufacturing sectors. In Germany, the composite PMI rose 0.5pt to 51.4, led by modest gains in the manufacturing output subcomponent. The German services PMI showed a marginal decline; however, the underlying indices were more subdued, with new orders and employment falling more. The press release also noted a sharp fall in business expectations in the services sector.

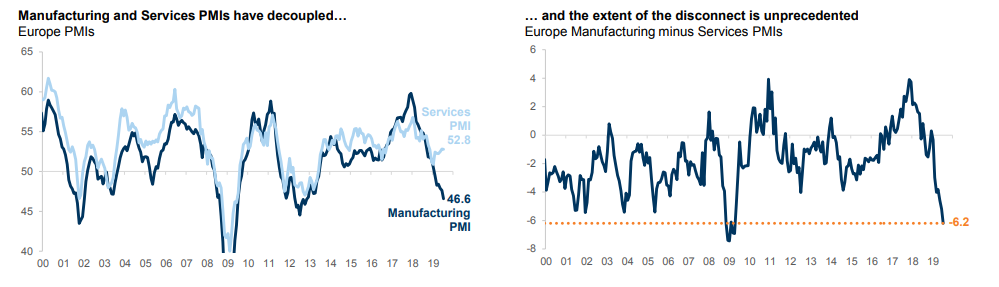

And visually:

As a result, after the glow faded from euro-area PMIs, investors again sought safer assets, pushing Treasuries higher while the yen hit a fresh daily high amid a flight to safe havens. The moves came after South Korea said it would withdraw from an intelligence-sharing agreement with Japan and a senior EU official says discussions with U.K. Prime Minister Boris Johnson suggest a no-deal Brexit is likely. Italy’s FTSE MIB (+0.4%) was kept afloat as Italian President Mattarella holds a barrage of talks with party leaders in search of a coalition to fill the country’s political void in order to pass the 2020 budget later this year. Meanwhile, UK’s FTSE 100 (-0.5%) marginally lags its peers as heavyweight tobacco stocks (Imperial Brands -1.0%, British American Tobacco -1.4%) weigh on the index amid news that the US House Energy and Commerce Committee launched a probe into four e-cigarette companies, British American Tobacco, Atria Group (MO), Japan Tobacco (2914 JT) and Reynolds American; seeking information on Cos’ research into public heath impacts, marketing practices and promotion of e-cigarette use by adolescents.

As a result, Europe’s STOXX 600 index fell 0.1% in choppy trade, following a 0.5% drop in MSCI’s broadest index of Asia-Pacific shares outside Japan. The MSCI world equity index was down 0.1%.

Earlier in the session, Asian stocks dropped for a second day, led by energy and utility firms, as traders awaited a Friday address by Federal Reserve Chairman Jerome Powell. Markets in the region were mixed, with India retreating and Malaysia climbing. The Topix closed little changed, as chemical producers advanced and electronic companies slipped. The Shanghai Composite Index edged up 0.1%, supported by Kweichow Moutai Co. and China International Travel Service Corp. The Hang Seng Index fell 0.8%, with Hong Kong-listed stocks facing their worst earnings decline since 2008. India’s Sensex fell for a third day, dragged down by Reliance Industries Ltd. and HDFC Bank Ltd. The country needs a “significant” fiscal package, a gradual decline in the rupee and more liquidity for the shadow-banking system to ease tight financial conditions, according to Bank of America Merrill Lynch.

While it didn’t impact markets on Wednesday, when US equities posted notable gains, minutes of the Fed’s July meeting showed deep splits among policymakers over whether to cut interest rates last month, though there was some unity in wanting to signal it was not on a preset path to looser policy. The Fed cut rates by 0.25% in July. While a “couple” of Fed members supported a deeper cut of half a percentage point, “several” favored no change at all. That reluctance to loosen policy seems at odds with the expectations for a cut of over 100 basis points by the end of 2020 that are already priced into markets.

Strategists said that the minutes reflected a dissonance between expectations for cuts – fueled by geopolitical concerns such as U.S.-China trade tensions and economic weakness in major economies such as Germany – and the apparently solid fundamentals of the U.S. economy.

“The update last night was a bit of a reality check – maybe don’t get ahead of yourself on what the Fed is going to do,” said David Madden, market analyst at CMC Markets. “If you forget about the geopolitical headlines, forget about what the bond markets are doing, and look at the underlying indicators of the U.S. … people are in jobs, earning decent money, and more importantly spending money.”

But beyond the United States, worries about the fragility of the global economy were evident in data from Europe on Thursday. Germany’s private sector continued to struggle in August, suggesting further that Europe’s largest economy is heading for a recession after its economy shrunk between April-June. Euro zone business growth expectations also fell to their weakest in more than six years on trade war fears, even as the expansion picked up a touch in August.

In FX, the slump in the yuan dragged it to an 11-year low, which also sapped appetite for risk, with dealers saying state-owned banks were seen selling dollars to support the yuan.

The Fed minutes also raised the stakes for Chairman Jerome Powell’s speech on Friday at the Fed’s annual policy retreat in Jackson Hole, Wyoming – an event that investors are waiting for with bated breath hoping for some clarity on the Fed’s intentions. U.S. President Donald Trump has been urging larger rate reductions, with proponents of looser policy pointing to the need to lift inflation toward the Fed’s target and thwart fallout from global trade tensions. And those trade worries played out again in currency markets, where the fall in onshore China’s yuan to 7.0752 per dollar, its lowest since March 2008, promoted a rush to perceived safe-haven assets such as the Japanese yen. The yen advanced by 0.2% to 106.41 yen, nearing last week’s eight-month low of 105.05 yen. The euro slipped to a daily lows as commodity and Scandinavian currencies deepened losses.

Currency traders said that while the Chinese economy’s slowing growth meant pressure had been building on the renminbi from long before, the new fall suggested Beijing was prepared to use the currency as leverage as trade tensions simmer.

“This indicates that this is an instrument of the Chinese government in the trade war. It is allowing for renminbi weaknesses,” said Thu Lan Nguyen, FX strategist with Commerzbank in Frankfurt. “It is an indication that they are expecting the trade war to continue, to last longer than they anticipated last year.”

In geopolitics, North Korea carried out live fire drills by bombing replicas of South Korea’s F-15K fighter jets, surface to air missiles and a radar. Across the border, South Korea stated they will not be renewing their intelligence accord with Japan, according to the Blue House. Iran displayed a new locally built mobile missile defence system, reported via Iranian news agencies. Iranian Foreign Minister Zarif says he is prepared to work on France’s proposals regarding a nuclear deal.

In commodities, oil prices dipped on worries about the global economy and bigger-than-expected buildups in oil product inventories in the United States, the world’s biggest oil consumer. Brent crude futures rose 0.3%, or 18 cents, to $60.48, while U.S. crude gained 23 cents to $55.91 a barrel.

Expected data include jobless claims and PMIs. Gap, Intuit, Salesforce, and VMware are among companies reporting earnings.

Market Snapshot

- S&P 500 futures unchanged at 2,929

- STOXX Europe 600 down 0.4% to 374.24

- MXAP down 0.3% to 152.02

- MXAPJ down 0.5% to 492.13

- Nikkei up 0.05% to 20,628.01

- Topix up 0.04% to 1,498.06

- Hang Seng Index down 0.8% to 26,048.72

- Shanghai Composite up 0.1% to 2,883.44

- Sensex down 1.1% to 36,660.18

- Australia S&P/ASX 200 up 0.3% to 6,501.81

- Kospi down 0.7% to 1,951.01

- German 10Y yield rose 1.3 bps to -0.657%

- Euro up 0.2% to $1.1102

- Italian 10Y yield fell 3.9 bps to 0.985%

- Spanish 10Y yield rose 1.2 bps to 0.109%

- Brent futures up 0.2% to $60.44/bbl

- Gold spot down 0.2% to $1,499.52

- U.S. Dollar Index little changed at 98.24

Top Overnight News

- German manufacturers are reinforcing concern that Europe’s largest economy is headed into a recession. A nationwide gauge showed orders at factories and services companies dropping at the fastest pace in six years, and more companies now expect output to fall than rise over the next 12 months. That’s the first time that’s happened since 2014, according to the Purchasing Managers’ Index from IHS Markit

- Federal Reserve officials viewed their interest-rate cut last month as insurance against too-low inflation and the risk of a deeper slump in business investment stemming from uncertainty over President Donald Trump’s trade war.

- Angela Merkel’s challenge to Boris Johnson to find a Brexit solution in the next 30 days sounds impossible. But while both sides are talking tough, officials in private say there’s still time to salvage a deal

- The prospects for forming a new coalition in Italy improved after the first day of consultations as most of the smaller parties and independent lawmakers told Mattarella they’re against a snap election and would eventually favor a new government.

- The French government expects the U.K. to leave the European Union without a withdrawal agreement, an official in President Emmanuel Macron’s office said, meaning the immediate imposition of border controls after Brexit at the end of October

- The IMF executive board recommended removing the age- limit for the fund’s managing director, paving the way for Kristalina Georgieva the European Union-backed candidate to replace Christine Lagarde

- Oil climbed as attention turned from expanding American fuel stockpiles to the prospects for monetary easing as the world’s top central bankers gather in Jackson Hole, Wyoming

- South Korea said it would withdraw from an intelligence-sharing agreement with Japan, extending their feud over trade measures and historical grievances into security cooperation.

- Italy’s President Sergio Mattarella will meet with the country’s main political leaders on Thursday in an effort to carve out a viable governing coalition after Rome’s government – – an alliance between the hard-right League and the anti- establishment Five Star Movement — collapsed earlier this week

Asian equity markets traded mixed as the region failed to sustain the early momentum from Wall St where sentiment was underpinned by strong retailer earnings and after the FOMC minutes did little to alter the landscape as they showed a divide among officials on rate cuts. ASX 200 (+0.3%) and Nikkei 225 (U/C) were both higher at the open with tech and energy the outperformers on the busiest day of the earnings season in Australia, while Tokyo trade was less decisive as price action eventually reflected a choppy currency and after a lack of progress in talks between Japanese and South Korean Foreign Ministers to resolve the ongoing spat. Hang Seng (-0.8%) and Shanghai Comp. (+0.1%) were subdued amid CNY weakness and as Hong Kong’s property sector suffered the brunt of the Hong Kong protests with developers said to be reducing prices to support sales, although losses in the mainland have been cushioned by the PBoC’s liquidity efforts. Finally, 10yr JGBs were initially unchanged amid similar uneventful trade in T-notes, but later saw mild support after firmer demand at the enhanced liquidity auction for long end JGBs and as risk tone began to deteriorate.

Top Asian News

- Hong Kong Faces Worst Earnings Recession Since 2008 Crisis

- Indonesia Surprises With Second Rate Cut to Support Growth

- Hedge Fund Outflows of $55.9 Billion Make Dismal 2018 Look Good

European stocks have given up the earlier PMI-induced gains [Eurostoxx 50 -0.1%] as the sentiment seen from firmer EZ metrics across the board failed to persist, and amid little follow-through from FOMC Minutes. Italy’s FTSE MIB (+0.4%) is kept afloat as Italian President Mattarella holds a barrage of talks with party leaders in search of a coalition to fill the country’s political void in order to pass the 2020 budget later this year. Meanwhile, UK’s FTSE 100 (-0.5%) marginally lags its peers as heavyweight tobacco stocks (Imperial Brands -1.0%, British American Tobacco -1.4%) weigh on the index amid news that the US House Energy and Commerce Committee launched a probe into four e-cigarette companies, British American Tobacco, Atria Group (MO), Japan Tobacco (2914 JT) and Reynolds American; seeking information on Cos’ research into public heath impacts, marketing practices and promotion of e-cigarette use by adolescents. Moreover, broker downgrades for BHP (-1.7%), Anglo American (-2.0%) and Rio Tinto (-0.4%) adds further pressure on the index. Sectors are almost all in the red with cyclical stocks faring worse than defensives, in-fitting with the current risk tone. In terms of individual movers, Thyssenkrupp (+5.4%) shares jumped to the top of the Stoxx 600 amid reports that parties interested in Co’s elevator unit include Advent, Apollo, CVC, Carlyle, KKR and possibly EQT, according to Manager Magazin. Meanwhile, BBVA (+1.3%) and Caixabank (+1.7%) benefit from broker upgrades at HSBC

Top European News

- Italy’s President Enters High-Stakes Talks in Bid to End Crisis

- Osram Board Agrees AMS Can Make Offer to Rival Bain- Carlyle

- Distressed-Debt Hedge Fund Mudrick Starts Expanding Into Europe

In FX, the euro was Not the strongest G10 currency, but the Euro perked up in wake of the flash Eurozone PMI surveys that were firmer than forecast across the board. Eur/Usd started to climb after the French preliminary prints and then crossed 1.1100 and beyond when German and pan headlines maintained the recovery trend, but faded again before testing offers reportedly waiting at 1.1120. Note also, hefty option expiries between 1.1095 and the big figure may be exerting a gravitational pull given 1.65 bn rolling off at the NY cut.

- GBP/JPY – The other major outperformers as the Dollar continues to drift post-FOMC minutes that failed to provide any further or clearer insight on guidance for the September policy meeting. Indeed, the DXY remains tightly bound just above the 98.000 handle and inside relatively narrow confines for the week so far (between 98.451-115), awaiting Fed chair Powell for clearer pointers (hopefully) at Jackson Hole on Friday. Meanwhile, Sterling is still seemingly taking the positive view that there is time left (albeit limited and decaying) to resolve the Irish backstop stalemate and reach some sort of Brexit deal before October 31, with Cable keeping its head above 1.2100, but capped by the 21 DMA circa 1.2154 and Eur/Gbp pivoting 0.9150 even though the single currency is underpinned as noted above. Elsewhere, the safe-haven Yen retains an underlying bid around 106.50 amidst ongoing global trade and geopolitical tensions after tough talks between the US and Japan failed to produce a breakthrough and SK not renewing its intelligence sharing agreement with Japan.

- NZD/AUD/CAD – All on the backfoot vs their US counterpart as the Kiwi loses more ground after failing to sustain recovery momentum above 0.6400 and the Aussie likewise following fleeting bounces over 0.6800, but also undermined by CBA PMIs overnight showing sub-50 manufacturing and composite readings. The Loonie is holding up a bit better after Wednesday’s frothy Canadian CPI, but unable to rally too far beyond 1.3300 ahead of wholesale trade data later today.

- SEK/NOK – Also weaker, partly on fundamentals and technically as Swedish unemployed jumped in SA terms and Norway trimmed its Q3 oil investment estimate, with Eur/Sek back up above 10.7000 and Eur/Nok hovering nearer the top of 9.9550-9145 trading parameters against the backdrop of faltering risk appetite.

- EM – Widespread losses against the Greenback, but Cnh and Try depreciation looks particularly eye-catching as the offshore Yuan teeters around 7.1000 amidst more warnings from China that retaliation is in the pipeline if the US presses ahead with extra tariffs on September 1st. Meanwhile, the Lira continues to list and tested 100 DMA support circa 5.7922 even though Turkish consumer sentiment picked up in August.

In commodities, WTI and Brent futures are modestly firmer on the day with the former around the 56/bbl mark, whilst the latter remains near the 60.50/bbl level having found a base at 60/bbl. News flow has been light thus far for the complex with price action likely to be dictated by macro developments/sentiment heading into Fed Chair Powell’s speech tomorrow. Meanwhile, the WTI/Brent Arb widened to around USD 4.60/bbl vs. USD 3.60 earlier in the week. ING notes that “it does appear that the relative strength in WTI is starting to raise concerns over how it may impact demand for US oil from overseas buyers”. Elsewhere, gold is marginally softer and pivots on either side of 1500/oz ahead of ECB Minutes and as the Jackson Hole Symposium goes on underway, with Fed Chair Powell due to speak tomorrow. Copper prices declined further below the 2.6/lb mark as risk appetite somewhat waned.

US Event Calendar

- 8:30am: Initial Jobless Claims, est. 216,000, prior 220,000; Continuing Claims, est. 1.71m, prior 1.73m

- 9:45am: Bloomberg Consumer Comfort, prior 61.2; Bloomberg Economic Expectations, prior 55

- 9:45am: Markit US Manufacturing PMI, est. 50.5, prior 50.4; Markit US Services PMI, est. 52.8, prior 53

- 10am: Leading Index, est. 0.3%, prior -0.3%

- 11am: Kansas City Fed Manf. Activity, est. 1.2, prior -1

DB’s Craig Nicol concludes the overnight wrap

So there we have it, another one of those ‘where were you when…’ moments in the era of crazy low bond yields with the world’s first-ever zero coupon 30-year bond issued yesterday. Indeed, the 30y Bund ended up pricing at -0.11%; however, the big talking point was the anaemic demand at the auction with less than half of the offering being taken up by investors, meaning the Bundesbank had to retain the balance. The real subscription rate as a result was just 0.43x, which compares with 0.86x at the July auction. A lot was made of this being a very weak auction although it’s still hard to ignore the fact that €824m of the negative yielding ultra-long bonds were taken up by investors.

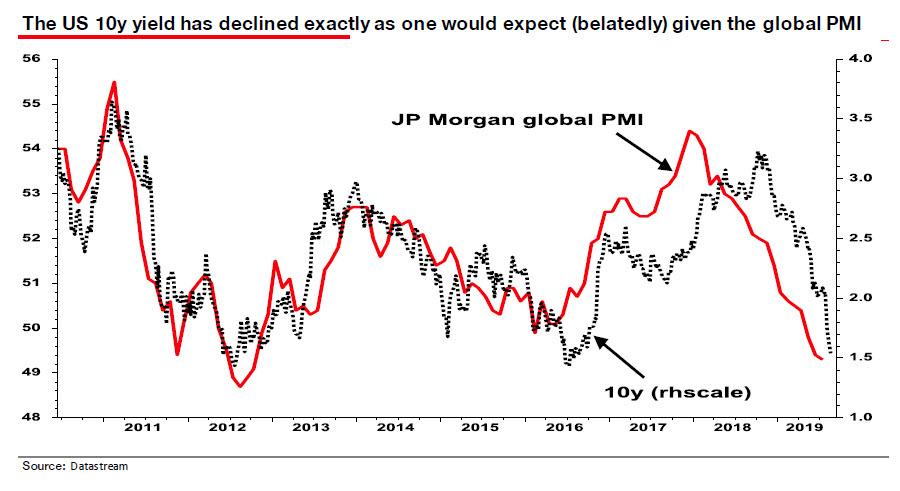

That auction came on a day when bond markets were a bit weaker. The whole Bund curve is still negative; however, yields were up a couple of basis points while Treasury yields also closed higher after the release of the FOMC minutes. Two-year yields rose +6.3bps, while 10-year yields rose +3.4bps.That sent the curve back down to just 1.0bp – a level it’s holding this morning – and dangerously close to inversion again.

The most immediately-relevant takeaway from the minutes was that there is minimal support for a 50bps cut in September, and markets moved to price in only a 12% chance of the bigger cut. That’s down from 20% before the minutes and from as high as 50% last week, though a 25bps cut remains fully priced. The minutes also suggested that policymakers were attentive to the trade war risks and were not caught off guard by the recent escalation, saying that “participants were mindful that trade tensions were far from settled.” As for the Fed’s longer-term policy review, there were several indications that the discussions are accelerating, as policymakers reportedly discussed using QE “more aggressively” and also analyzed “makeup strategies.” The latter “could be designed to promote a 2 percent inflation rate, on average, over some period,” which would have dovish implications for rates. While we’re on the Fed, President Trump continued his relentless attack on twitter, calling Powell “a golfer who can’t putt, has no touch”. To be fair, the same could be said for 99% of amateur golfers.

The moves in bond markets reflected a generally more upbeat tone across markets more broadly. That was certainly the case in equities where last night the S&P 500 closed +0.82%. The NASDAQ and DOW also finished +0.90% and +0.93%, respectively, with cyclical sectors generally leading gains. Favourably-viewed corporate earnings results in the retail sector from Target (+20.55%) and Lowe’s (+10.35%) helped. Nevertheless, the reality is that equities have just chopped around in a range since the plunge early in August and sit roughly where they were two weeks ago. HY credit spreads also had a strong day, with cash spreads trading -11bps and -10bps tighter in the US and Europe, respectively.

Overnight, Asian markets are quickly losing momentum although it’s not entirely obvious what’s driving the reversal from the highs. The Nikkei (-0.04%), Hang Seng (-0.87%), Shanghai Comp (-0.18%) and Kospi (-0.38%) are all lower having opened with decent gains. Futures on the S&P 500 (-0.03%) are also back to flat as we go to print.

Moving on. While markets have had very little to feed on the way of economic data this week, the good news is that we’ve got the global flash August PMIs today, which will give us a fresh opportunity to test the global growth pulse. We’ve already had the data out in Japan this morning where the composite rose half a point to 51.7, helped by a 1.6pt increase in the services reading to 53.4 while the manufacturing reading remained in contractionary territory at 49.5, albeit up 0.1pt from July. We’ll get the data for France, Germany and the Euro Area shortly and the consensus expects the composite reading for the Euro Area to have deteriorated slightly from 51.5 to 51.2, with the manufacturing and services readings expected to print at 46.2 and 53.0, respectively. A reminder that the July numbers confirmed a reversal of the improvement seen in June with the composite reading roughly consistent with a low +0.2% qoq rate of growth. This data of course will be the single biggest growth data point ahead of the ECB meeting in 3 weeks’ time. We should note that we’ll also get the data in the US where expectations are for a 50.5 manufacturing and 52.8 services print.

In other news, Italian assets continue to perform well despite persistent political uncertainty. Prime Minister Conte is scheduled to meet with leaders from the League and Five Star today, to see if he can find a prospective government and avoid fresh elections. Italian assets outperformed their European counterparts yesterday with the FTSE MIB finishing +1.77% versus +1.21% for the STOXX 600 while BTPs rallied -4.0bps and now sit at the lowest since October 2016.

Elsewhere, the CBO updated their US economic and budget forecasts. They now expect the fiscal deficit to widen to $960bn this year, up from their prior estimate of $896bn from May. That will be worth around 4.5% of GDP, worse than their prior forecast for 3.9%. The worse outlook will also result in trillion-dollar deficits beginning in 2020, two years earlier than before. On the bright side, the CBO raised their 2020 GDP growth forecast by 0.4pp to 2.1%, though they left 2019 at 2.3%.

Finally, the economic data didn’t add much but for completeness, US existing home sales rose to 5.42mn for July, marginally beating expectations for 5.40mn. That took the trend to 2.5% mom, and the prior month was revised upward slightly. Mortgage applications, a more forward-looking metric, fell -0.9%.

Looking at the day ahead now, outside of the PMIs the other data scheduled for release is August CBI survey data in the UK and August consumer confidence data for Euro Area, before jobless claims, July leading index and August Kansas Fed manufacturing survey is released in the US. We’ll also get the ECB minutes and of course the Fed’s Jackson Hole symposium kicks off tonight but with Powell not due to speak until tomorrow.

3A/ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 3.11 POINTS OR 0.11% //Hang Sang CLOSED DOWN 221.32 POINTS OR 0.84% /The Nikkei closed UP 9.44 POINTS OR 0.05%//Australia’s all ordinaires CLOSED UP .31%

/Chinese yuan (ONSHORE) closed DOWN at 7.0855 /Oil UP TO 56.11 dollars per barrel for WTI and 60.82 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0855 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0862 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

SOUTH Korea/JAPAN

South Korea surprisingly scraps an intelligence pact with Japan as we have rising trade tensions.

(courtesy zerohedge)

South Korea Scraps Intelligence Pact With Japan Amid Rising Trade Tensions