GOLD:$1521.00 DOWN $7.00 (COMEX TO COMEX CLOSING

Silver: $18.22 DOWN 2 CENTS (COMEX TO COMEX CLOSING)

Gold : $1523.50

silver: $18.36

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 859/1279

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,526.500000000 USD

INTENT DATE: 08/29/2019 DELIVERY DATE: 09/03/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

118 H MACQUARIE FUT 677

132 C SG AMERICAS 2

152 C DORMAN TRADING 13

323 H HSBC 295

435 H SCOTIA CAPITAL 261

657 C MORGAN STANLEY 3

661 C JP MORGAN 366

661 H JP MORGAN 523

686 C INTL FCSTONE 85

690 C ABN AMRO 100

737 C ADVANTAGE 36 69

800 C MAREX SPEC 121

905 C ADM 7

____________________________________________________________________________________________

TOTAL: 1,279 1,279

MONTH TO DATE: 1,279

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 1279 NOTICE(S) FOR 127,900 OZ (3.978 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1279 NOTICES FOR 127900 OZ (3.978 TONNES)

SILVER

FOR SEPT

4862 NOTICE(S) FILED TODAY FOR 24,310,000 OZ/

total number of notices filed so far this month: 4862 for 24,310,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 9581 UP 89

Bitcoin: FINAL EVENING TRADE: $ 9536 UP 44

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A CONSIDERABLE SIZED 3150 CONTRACTS FROM 227,327 DOWN TO 224,177… WITH THE 13 CENT LOSS IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR AUGUST, 0 FOR SEPT: 2444 , AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 2444 CONTRACTS. WITH THE TRANSFER OF 2444 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2444 EFP CONTRACTS TRANSLATES INTO 12.22 MILLION OZ ACCOMPANYING:

1.THE 13 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ FINAL STANDING IN AUGUST.

33.715 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

WE HAD ATTEMPTED COVERING OF SHORTS AT THE SILVER COMEX YESTERDAY WITH SOME SUCCESS..BUT WE HAD HUGE SPREADING LIQUIDATION. THE PROCESS SHOULD END TODAY AND THEN WE START THE ACCUMULATION PROCESS FOR GOLD ON TUESDAY.

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF SEPTEMBER FOR SILVER.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF AUGUST BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF AUGUST:

43,294 CONTRACTS (FOR 22 TRADING DAYS TOTAL 43,294 CONTRACTS) OR 216.47 MILLION OZ: (AVERAGE PER DAY: 1967 CONTRACTS OR 9.839 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 216.47 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 30.92% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1549.71 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3150, WITH THE 13 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 2444 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED AN ATMOSPHERIC SIZED: 7237 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2444 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 3150 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 13 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $18.24 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.121 BILLION OZ TO BE EXACT or 160% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 4862 NOTICE(S) FOR 24,310,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

AND NOW WE ARE WITHIN A WHISKER OF ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,169 BUT THIS TIME THE PRICE OF SILVER YESTERDAY WAS $17.18 AND HIGHER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/AND NOW SEPT: 33.715 MILLION OZ//

- CLOSE TO THE RECORD OPEN INTEREST IN SILVER 244,169 CONTRACTS (OR 1.228 BILLION OZ/, THE PREVIOUS RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

THE SPREADING LIQUIDATION OPERATION IS NOW IN FULL SWING AND UNDERGOING ITS FINAL LIQUIDATION..THIS IS ONLY FOR SILVER ALMOST ALL OF THE LOSS IN TOTAL OPEN INTEREST WAS DUE TO THE LIQUIDATION OF THE SPREADERS……. THE LIQUIDATION( AND ACCUMULATION) PHASE FOR COMEX OI GOLD STOPS FOR THE AUGUST CONTRACT MONTH BUT WILL START IN EARNEST ONCE WE ENTER THE MONTH OF SEPTEMBER. AS I STATED ON TUESDAY AND WEDNESDAY: “IN SILVER WE WOULD NORMALLY WITNESS A HUGE COLLAPSE IN TOTAL OPEN INTEREST AS WE PROCEED TO THE ACTIVE DELIVERY MONTH OF SEPTEMBER”…AND TRUE TO FORM THAT PLAYED OUT PERFECTLY THESE PAST FEW DAYS

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 10,783 CONTRACTS, TO 618,946 ACCOMPANYING THE $11.65 PRICING LOSS WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// //THE SPREADING LIQUIDATION OPERATION BY THE BANKERS WILL FINISH TONIGHT FOR SILVER …. THE ACCUMULATION PHASE FOR COMEX OI GOLD WILL COMMENCE STARTING SEPT 3 AS THEY WILL CONTINUE ADDING TO THEIR STACK UNTIL ONE WEEK BEFORE FIRST DAY NOTICE FOR THE OCTOBER CONTRACT MONTH

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 12,782 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 12,782 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 618,946,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1999 CONTRACTS: 10,783 CONTRACTS DECREASED AT THE COMEX AND 12,782 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 1999 CONTRACTS OR 199,900 OZ OR 6.217 TONNES. YESTERDAY WE HAD A STRONG LOSS OF $11.65 IN GOLD TRADING….AND WITH THAT LOSS IN PRICE, WE HAD A GOOD GAIN IN GOLD TONNAGE OF 6.217 TONNES!!!!!!. THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON .

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST : 205,641 CONTRACTS OR 20,564,100 oz OR 639.62 TONNES (22 TRADING DAY AND THUS AVERAGING: 9347 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 22 TRADING DAY IN TONNES: 639.62 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 639.62/3550 x 100% TONNES =18.01% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4151.32 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED DECREASE IN OI AT THE COMEX OF 8,083 WITH THE PRICING LOSS THAT GOLD UNDERTOOK YESTERDAY($11.65)) //.WE ALSO HAD A HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 12,782 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 12,782 EFP CONTRACTS ISSUED, WE HAD A STRONG SIZED GAIN OF 1999 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

12,782 CONTRACTS MOVE TO LONDON AND 10,783 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 6.217 TONNES). ..AND THIS GOOD INCREASE OF DEMAND OCCURRED DESPITE THE LOSS IN PRICE OF $11.65 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX.

we had: 1279 notice(s) filed upon for 127,900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $7.00 TODAY//(COMEX-TO COMEX)

A CHANGES IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 2.05 TONNES

INVENTORY RESTS AT 880.36 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 2 CENTS TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV:

/INVENTORY RESTS AT 388.154 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A STRONG SIZED 3150 CONTRACTS from 227,327 DOWN TO 224,177 AND FURTHER FROM A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR DEC. 2444 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2444 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 3150 CONTRACTS TO THE 2444 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A LOSS OF 706 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 3.53 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ; AUGUST AT 10.025 MILLION OZ//SEPT 2019: 33.715 MILLION OZ/

RESULT: A STRONG SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 13 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 2444 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 4.68 POINTS OR 0.16% //Hang Sang CLOSED UP 21.23 POINTS OR 0.08% /The Nikkei closed UP 245.44 POINTS OR 1.19%//Australia’s all ordinaires CLOSED UP 1.40%

/Chinese yuan (ONSHORE) closed DOWN at 7.1494 /Oil DOWN TO 55.83 dollars per barrel for WTI and 59.97 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1494 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1473 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

i)Kyle Bass and others feel that Hong Kong is prepared for a mainland invasion

(zerohedge)

ii)China’s crackdown escalates with multiple arrests

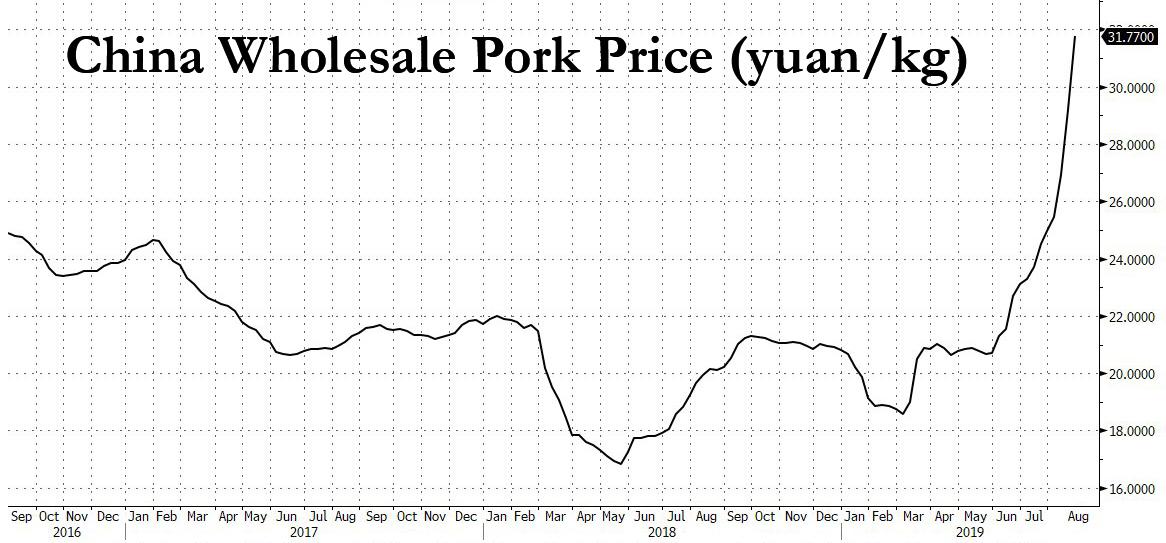

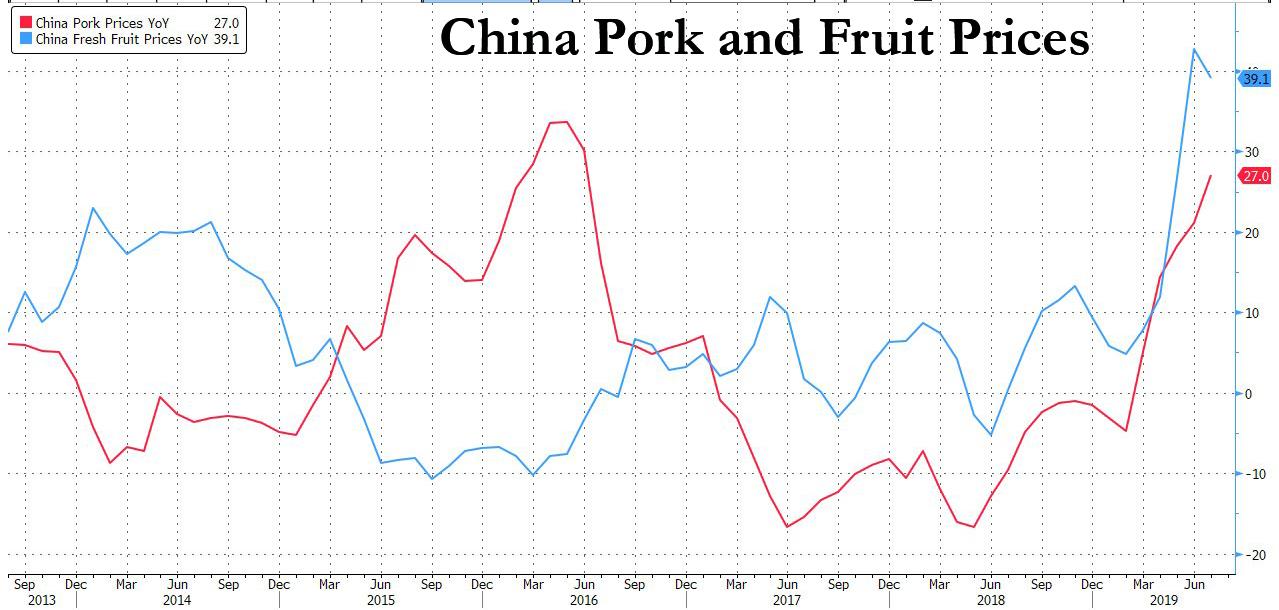

iii)We have been telling you on the ebola pig virus and postulated that pork prices would soon skyrocket. We were right China is now reeling as pork prices explode(zerohedge)

iv)China/USA

Seems that China shut out the USA for lobster as their exports to China crashed by 80%. No doubt that the big winner would be Canada.

(zerohedge)

v)China rejects Lam’s proposal to appease the protesters. The leaders who were arrested have been released and the march scheduled for tomorrow has been cancelled

4/EUROPEAN AFFAIRS

UK

Our resident expert on the Brexit, Mish Shedlock states that the Boris Johnson move was foolproff

(Mish Shedlock/Mishtalk)

ii)And now a Scottish judge rejects the bid to stop Bo.Jo from suspending parliament ahead of Brexit day

(zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

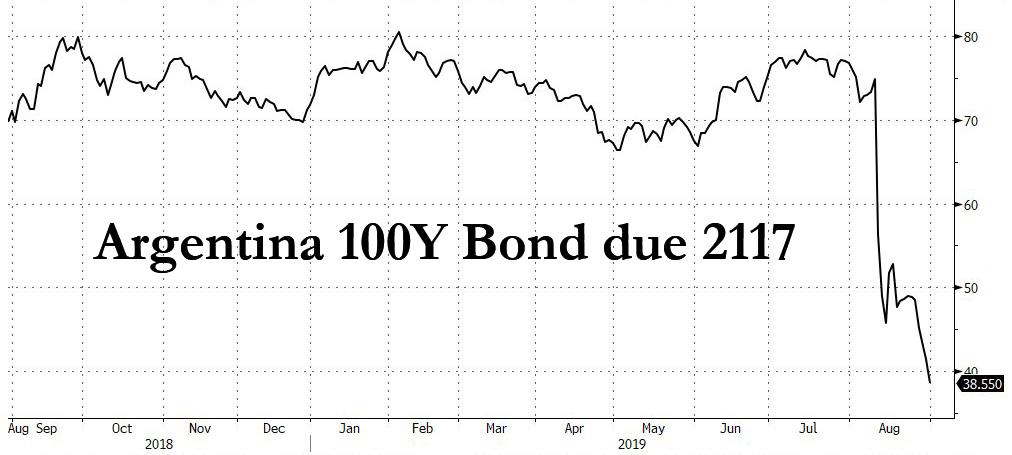

i)Argentina

Argentina is now officially in default as they delay payments on bonds. This also triggers credit default swaps. S and P now downgrades Argentina’s debt to what is called selective default

(zerohedge)

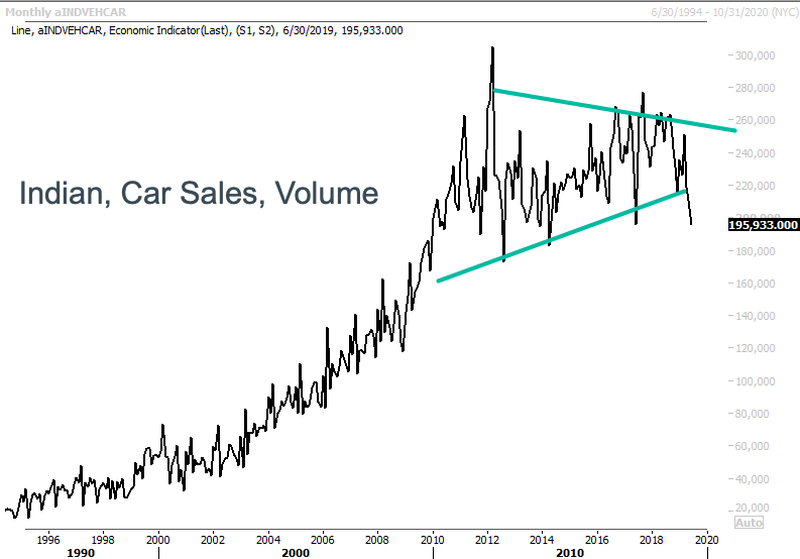

ii)India

The global slowdown is certainly having a huge effect on the economy in India. Now its car manufacturing sector has halted production

(zerohedge)

9. PHYSICAL MARKETS

i)Huge paper today from Alasdair Macleod:

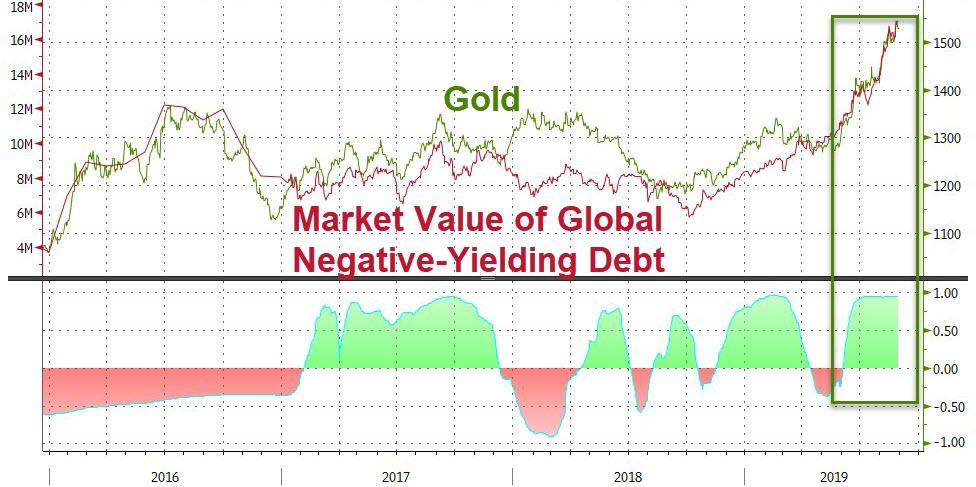

Negative interest rates drive people out of paper assets into gold. It also stops the gold carry trade as bankers cannot make any money loaning gold.

(Alasdair Macleod)

ii)Our good friend Jeff Christian is again spilling disinformation on silver

(Dave Kranzler/IRD)

iii)Jim Bianco explains why negative rates are toxic to the financial scene and like Alasdair Macleod he sees that gold will hit record highs this year

(Jim Bianco)

iv)Platinum prices jump on hope for stimulus in the car industry in China

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

Stocks Plunge, Dollar Spikes Into European Close As Tariff Delay Hopes Fade

Don’t show President Trump this chart…

Source: Bloomberg

On a broad trade-weighted basis, the dollar has never been stronger against the rest of the world’s fiat currencies.

And following this morning’s comments from European Central Bank policy maker Ewald Nowotny, that adding equity purchases to the ECB’s monetary-policy mix isn’t a realistic option,

“I would completely exclude it” as a tool because “for Europe it is inappropriate,” Nowotny told reporters in Alpbach, Austria.

“We can tweak the instruments we have to a certain extent, but I wouldn’t expect us to have new measures.”

“The central bank has to know what’s going on in the markets but it should not be following the markets,” said Nowotny, whose term as head of the Austrian central bank expires on Saturday.

“It should kind of steer the markets, and lead the markets, and there might be a certain danger that we’re too much following.”

And EURUSD is trading back to a 1.09 handle for the first time since May 2017.

Source: Bloomberg

This has sent the dollar surging to new highs…

Source: Bloomberg

Additionally, we note that Nowotny raised some graver concerns overnight, warning that three generations without war in western Europe have created a potentially dangerous imbalance in the economy.

“The fortune of a now 74-year period of peace has inevitably led to a tremendous accumulation of wealth on the one hand and debt on the other,” the Austrian central-bank governor said in an interview with Wiener Zeitung.

“In the past, wars or high inflation have effectively taken care of this problem. How we solve it without both these factors remains open.”

Can Lagarde save the world from this ominous future?

The US equity markets are reacting significantly to the surge in the dollar into the EU close…

Presumably we are running out of time for the tariffs to be delayed at the last minute.

ii)Market data/USA

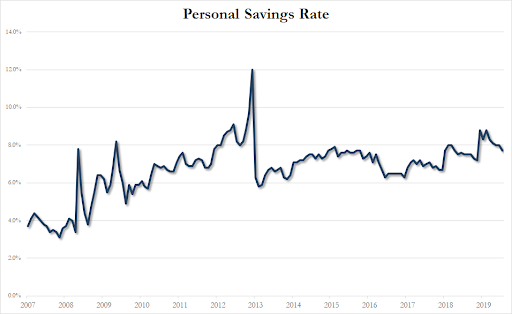

a)USA spending outpaces income by a wide margin. Thus the savings rate drops dramatically

(zerohedge)

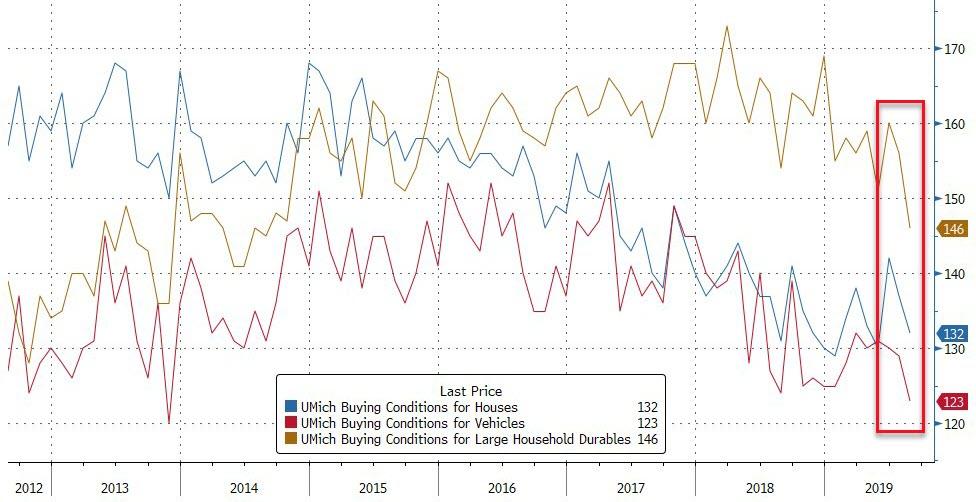

b)Univ. of Michigan confidence plummets as consumers face the tariff cliff

(zerohedge)

iii) Important USA Economic Stories

iv) Swamp commentaries)

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; nil oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 110,554 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 192,060 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 192,060 CONTRACTS EQUATES to 960 million OZ 137% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.35% ((AUGUST 30/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.06% to NAV (AUGUST 30/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -1.35%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.41 TRADING 14.93/DISCOUNT 3.10

END

And now the Gold inventory at the GLD/

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

AUGUST 22.WITH GOLD DOWN $6.80 TODAY: TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD: I)A PAPER DEPOSIT OF 6.74 TONNES INTO THE GLD (LATE YESTERDAY EVENING) AND 2) A PAPER DEPOSIT OF 2.93 TONNES LATE THIS AFTERNOON./INVENTORY RESTS AT 854.84 TONNES

AUGUST 21/WITH GOLD DOWN $.30 TODAY:A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.76 TONNES INTO THE GLD INVENTORY/GOLD INVENTORY RESTS AT 845.17 TONNES

AUGUST 20//WITH GOLD UP $2.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GOLD INVENTORY RESTS AT 843.41 TONNES

AUGUST 19/WITH GOLD DOWN $11.20//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .88 TONNES//INVENTORY RESTS AT 843.41 TONNES

AUGUST 16/WITH GOLD DOWN $7.35: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 844.29 TONNES

AUGUST 15/WITH GOLD UP $3.55 TODAY//WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: WE GOT BACK 7.63 TONNES OUT OF 11.11 TONNES LOST ON WEDNESDAY( A DEPOSIT OF 7.63 TONNES)/INVENTORY RESTS AT 844.29 TONNES

AUGUST 14/WITH GOLD UP $7.60 TODAY (AND DOWN $2.90 YESTERDAY) WE HAD A MONSTROUS WITHDRAWAL OF 11.11 TONNES OF GOLD FROM THE GLD/AND THIS WAS USED IN AN ABORTED RAID YESTERDAY: INVENTORY RESTS AT 836.66 TONNES

AUGUST 13.2019: WITH GOLD DOWN $2.60 TO DAY: A HUGE 7.92 PAPER GOLD TONNES WERE ADDED TO THE GLD/INVENTORY RESTS AT 747.77 TONNES

AUGUST 12.2019: WITH GOLD UP $7.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 839.85 TONNES

AUGUST 9/WITH GOLD DOWN $2.00//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REMAINS AT 839.85 TONNES OZ/

AUGUST 8: WITH GOLD DOWN $4.20: TWO TRANSACTIONS: A)A MONSTROUS PAPER DEPOSIT OF 8.50 TONNES WAS ADDED TO THE GLD/INVENTORY RESTS AT 845.42 TONNES b) A HUGE WITHDRAWAL OF 5.59 TONNES FROM THE GLD//INVENTORY RESTS AT 839.85 TONNES…ABSOLUTE FRAUD!

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

AUGUST 30/2019/ Inventory rests tonight at 880.36 tonnes

*IN LAST 654 TRADING DAYS: 55.02 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 554- TRADING DAYS: A NET 111.63 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 TONNES

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.696 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 21/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 20.WITH SILVER UP 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 19/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 16/: WITH SILVER DOWN 9 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 15/2019 WITH SILVER DOWN 2 CENTS: ANOTHER BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING 3.977 MILLION OZ PAPER DEPOSIT/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 14/2019 WITH SILVER UP 27 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 4.538 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 376.177 MILLION OZ//

AUGUST 13/2019: WITH SILVER DOWN 9 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 6.082 MILLION OZ///INVENTORY NOW RESTS AT 371.637 MILLION OZ

AUGUST 12/2019: WITH SILVER UP 11 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 365.557 MILLION OZ.

AUGUST 9/2019//WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.245 MILLION OZ INTO THE SLV INVENTORY/INVENTORY ADVANCES 365.557 MILLION OZ

AUGUST 8/WITH SILVER DOWN 23 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT: 1.409 MILLION OZ INTO INVENTORY///INVENTORY RESTS AT 363.311 MILLION OZ//

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

AUGUST 29/2019:

Inventory 388.154 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.07/ and libor 6 month duration 2.03

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .04

XXXXXXXX

12 Month MM GOFO

+ 1.90%

LIBOR FOR 12 MONTH DURATION: 1.96

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.06

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

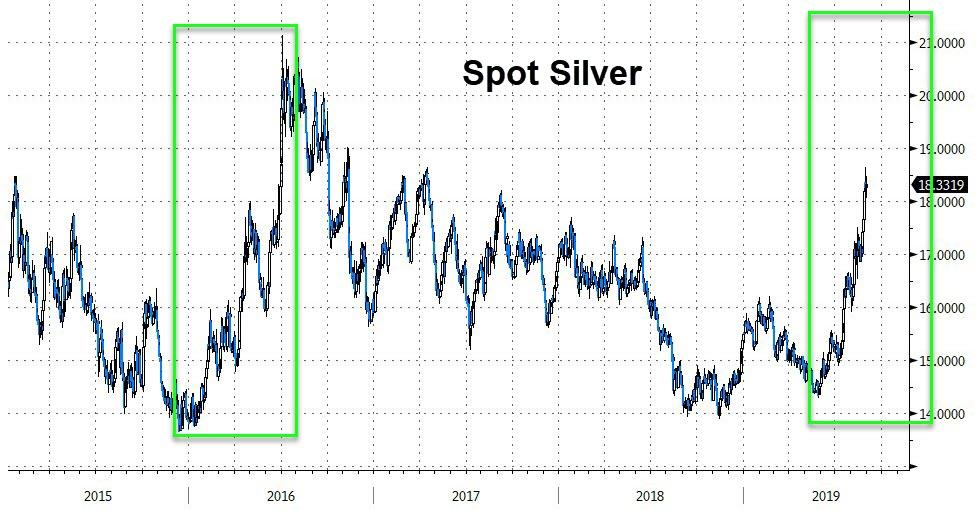

Silver Gains 6% To $18.40/oz and Gold Consolidates Over $1,500/oz This Week

News and Commentary

Gold steadies near six-year high, silver jumps as growth risks persist

Silver rally is stealing the show even as gold surges to 6-year high

Around 1,000 fake-branded bars likely from China slip dirty gold into Asian gold markets

Trump says US and China resume trade talks Thursday ‘at a different level’

China sends fresh troops into Hong Kong as military pledges to protect ‘national sovereignty’

Japan-South Korea dispute is a sign that the world order is ‘collapsing’

JP Morgan: Is the dollar’s “exorbitant privilege” coming to an end?

Gold Prices (LBMA – USD, GBP & EUR – AM/ PM Fix)

29-Aug-19 1536.65 1540.20, 1260.51 1262.96 & 1387.29 1392.03

28-Aug-19 1541.75 1537.15, 1263.31 1258.77 & 1389.89 1387.43

27-Aug-19 1531.85 1532.95, 1250.91 1247.51 & 1378.97 1380.88

26-Aug-19 UK Bank Holiday

23-Aug-19 1495.50 1503.80, 1224.37 1228.91 & 1351.48 1357.63

22-Aug-19 1498.70 1502.05, 1234.63 1225.97 & 1351.98 1354.10

21-Aug-19 1499.65 1503.25, 1235.41 1238.53 & 1351.48 1354.43

20-Aug-19 1502.65 1504.55, 1242.69 1239.60 & 1356.44 1357.86

Listen and Watch Jim Rogers Interview Here

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

Huge paper today from Alasdair Macleod:

Negative interest rates drive people out of paper assets into gold. It also stops the gold carry trade as bankers cannot make any money loaning gold.

(Alasdair Macleod)

iii) Other physical stories:

Jim Bianco explains why negative rates are toxic to the financial scene and like Alasdair Macleod he sees that gold will hit record highs this year

(Jim Bianco)

Bianco Warns “Negative Rates Are Extremely Toxic”, Sees Gold At Record Highs By Year-End

Authored by Christoph Gisiger via TheMarket.ch,

Jim Bianco, President of Bianco Research, cautions against evermore unconventional monetary policy interventions. He fears that the global slowdown is going to get worse and he spots opportunities in long-term bonds and gold.

The global economy is on the brink: Europe is headed for recession, Japan as well and China’s growth rate is the slowest in almost thirty years. Only the economy in the United States seems to hold up. But for how long?

«We live in a global world and if Japan and Europe are struggling and the world has a problem it’s going to come to the US eventually», says Jim Bianco.

According to the internationally renowned macro strategist, the biggest threat to the US economy is the inverted yield curve.

«This is the market’s way of saying the Federal Funds Rate is too high and must come down», Mr. Bianco is convinced.

Against this backdrop, the founder and President of Chicago based Bianco Research argues that the Federal Reserve should cut its target rate by 50 basis points at the next FOMC meeting. He also cautious against introducing negative interest rates in the United States during the next recession because in his view that would cripple the global financial system.

In this at-length interview with The Market, the profound financial market observer explains where he spots opportunities for investors in today’s challenging economic environment.

Mr. Bianco, the summer is basically over and we are heading into the final stretch of the year. What’s ahead for the financial markets in the coming months?

There are two issues at play: First, the trade and currency wars where the situation reminds me somewhat of «This Is Spinal Tap». It’s a cult satire movie from the eighties about a rock band and they coined the phrase «up to eleven» because that’s how high their amplifier went. So the expression «turning it up to eleven» refers to the act of taking something to an extreme. I’m saying this because I think Trump is “going to eleven” on trade: He’s going to turn it up so high that there is going to have to be a deal. That’s the way he wants to do this. He will just make it intolerable so everybody has to sit down and cut a deal.

What’s the other issue?

The inverted yield curve. The three-month/ten-year curve has been inverted since May and this is the market’s way of saying the Federal Funds Rate is too high and must come down. It is interesting how hard everyone is standing on their head to dismiss the yield curve and tell me why it’s different this time. This is not surprising, as it tends to happen every time the curve inverts until the recession hits. It might be different this time, but I still think that the yield curve is telling us that the Federal Reserve has to cut rates and it has to cut them aggressively.

Why is the inverted yield curve such a problem?

An inverted curve damages the economy. Accumulate enough damage and the economy sinks into recession. So, the curve does not predict a recession, it causes it. What is not known is how much damage the economy can withstand. Currently, the three-month/ten-year curve is at -49 basis points. It hit -52 Sunday night and it’s getting close to the 2007 extreme of -60, which is the most inverted reading of the last two decades.

You were interviewed by the White House in May for one of the open positions on the Board of Fed Governors. What should the Fed do at the next FOMC meeting on September 18?

The late economist Rudi Dornbusch coined the phrase that the Fed murders the economy by holding policy too tight for too long. Well, take careful note because that seems to be what the Fed might be doing yet again. The market is screaming to cut rates aggressively and the Fed is fighting it. So the question is how much it takes to un-invert the yield curve. At -49 basis points, that means a 25 basis point rate cut at the FOMC meeting next month is not going to un-invert the curve. You are going to need to cut 50 basis points or something along those lines.

At 2 to 2.25%, the Federal Funds Target Rate is already quite low. Shouldn’t the Fed be more careful than usual with its ammunition?

The “running out of bullets” argument is dangerous: either Fed cuts work or they do not. If cutting rates do not stimulate now, they will definitely not work if you save them until things get worse. Holding them back does nothing. So go hard now, cut hard now. If it works, great. If it does not work, saving the bullets for a rainy day would not have made a difference anyhow.

Then again, at the Jackson Hole conference last week Fed Chair Powell reinforced his view that the US economy is in good shape. Where do you see trouble brewing?

You don’t see it in the economic data but you will find it when you look at interest rates in the developed world. Today, the highest interest rates in the developed world are the 30-year Italy government bond and the Fed Funds Rate at around 2.1%. The Fed Fund Rates has never been that big of an outlier before. So the market is saying: We live in a global world, relative interest rates matter and the Fed Funds Rate is out of line with everything else.

Why do relative interest rates matter?

There was a paper delivered on Saturday in Jackson Hole about the effects that globalization has on monetary policy. It pretty much said the same thing: The reality is that we live in a global world. So you have Draghi at the ECB being at -40 basis points and Kuroda at the Bank of Japan being at -10 basis points. They’re dragging their rates to negative which is forcing the rates in the US down as well. The global economy is going to be perceived as weak and on top of that, you have the whole trade situation. That’s why the bond market is going to continue to send messages that there are problems and I think the stock market is going to continue to churn sideways to lower until there is some kind of resolution.

How serious is this threat to the global recession?

All those low global rates are signaling a big problem in the world. I think Europe is in a recession. Italy has negative GDP and Germany had three of the last four quarters either zero or negative GDP. Industrial production numbers out of Germany are terrible, and Japan is very close to being in recession, too. At the same time, economic data in China is at thirty years lows. That’s what’s holding interest rates in Europe down all the way to negative and is forcing the rates in the US down as well. We live in a global world and if Japan and Europe are struggling and the world has a problem it’s going to come to the US eventually, too. That’s why the market is telling us the Fed has to cut rates.

So why isn’t there a greater sense of urgency at the Fed? At the last FOMC meeting, Powell characterized the first rate since 2008 as a «mid-cycle adjustment,» not «the beginning of a lengthy cutting cycle.»

The problem is that nobody knows what mid-cycle adjustment means. As we speak, the market is pricing in four more rate cuts in the next year. That means a total of five rate cuts, including the July 31 rate cut. So the market is pricing in something that the consensus of economists is nowhere near. If you look at a recent Bloomberg survey, only seven of sixty economists had the Fed cutting rates five times. The other 53 had the Fed cutting less than five times. What’s unusual about this cycle is that the market is an outlier right now. Again: it comes back to the fact, that consensus economists are looking at US domestic economic data and they don’t see trouble whereas the market is looking at global data and it sees trouble.

But there’s also the well-known line that the market predicted nine of the last five recessions.

Economists can only wish they were this good! They have predicted none of the recessions in the last 50 years. What economists usually do is that they give you a 30% chance of recession. That means a 70% chance that there isn’t one. And then, when the recession hits, they stay at 30% because they think it’s going to end soon. The old joke about stock salesmen used to be that they never see a bear market and when there actually is one, they’re screaming it’s over. That’s kind of what economists do in terms of predicting a recession: they never ever predict one.

So what’s going to happen next?

This story has played out many times in the past during similar economic turning points: The market is ahead of the Fed and economists and is calling for rate cuts. The next month or two will prove critically important in determining which opinion prevails.

Should the Fed follow other Central Banks and introduce negative interest rates in the United States if a recession can’t be averted?

I believe that negative interest rates are extremely toxic for the financial system. Economists and the Fed make the mistake that they look at negative rates from the lens of borrowers, and when you are a borrower of money lower is better, zero is better, negative is better. That linear relationship holds up all the way through and I agree with that.

What’s the problem with negative rates then?

The problem is that they’re not looking at it from the perspective of the financial system. Where are borrowers going to get the money from? They are going to get it from the financial system and that’s where the lender is. The financial system has been built on the idea of positive interest rates. So negative interest rates in the US would become a big problem for the financial system. The banking system cannot function properly with negative interest rates and neither can the pension system. Also, all the valuation measures that we’ve invented – whether it’s the Fed model, the capital asset pricing model or even the Black-Scholes options model – don’t work with negative interest rates. That’s because when these models were developed no one had thought of the possibility that we would see zero or even negative interest rates.

Are negative interest rates already damaging the financial system?

I see it happening in Europe. There are cracks appearing in the financial system. The German banks are screaming and yelling about it to the ECB. The only thing that might be holding them together is that they have the option of positive interest rates in the US, in the UK and some other countries. Today, 94% of all interest earned income in the developed world comes from U.S. debt. That’s also the reason why UBS and Credit Suisse can survive despite what’s going on with deeply negative interest rates in Switzerland. They are global banks with a big footprint in the US where they get positive rates. Once they lose that option, they’re in big trouble as well, like all the other banks. So if the US sinks into economic weakness and decides to go negative it will really cripple the banking system.

What’s your take on the Dollar against this backdrop?

I’m only a mild Dollar bull at this point. Last Friday, there was some speculation about a direct intervention in the Dollar exchange rate by the Treasury for the first time in over twenty years. I think that would be a giant mistake. I suspect that as long as the rates in the US are going to stay up and the Fed is going to be slow in cutting them there will be underlying support for the Dollar. I don’t see it really weakening much. So the path of least resistance will probably continue to be sideways to up in the Dollar.

What should investors do with their money in this market environment?

Investors should be recognizing that with the economic slowdown there will be a further rally in bonds and that would probably mean deeper negative yields in Europe. Keep in mind, going to negative interest rates in Europe has led to some eye-popping total returns: The total return on 15+ year government bonds in Switzerland is 30% this year versus 16% on the S&P 500. In the US, the thirty-year treasury bond is reporting a 20% total return.

These government bonds trade almost like the FAANG stocks. Isn’t that a reason for caution?

I think rates will continue to go lower as a perception of economic weakness and more Fed cuts to come. So you are going to have good total returns in safe assets and risk assets are going to struggle. But once we get a sense that there is a bottom in the global economy, or some kind of resolution in trade, or the Fed decides to get aggressive and starts talking about a 50 basis point rate cut, then you can maybe review the option of moving back to more risk assets. But right now, risk assets are going to be problematic and safe assets like long term government bonds will provide you a great capital return.

Do you think the yield on ten-year US treasuries will take out the all-time low of July 2016?

Yes. Right now, we’re at about ten basis points away. So it’s not a hard call at this point to say that the ten-year yield will take out the 2016 low. The thirty-year yield already has.

Where else do you spot opportunities?

Gold has a nearly perfect correlation to the amount of negative debt in the world.

So if rates continue to move lower and negative debt continues to grow, that will be a positive factor for gold and gold will continue to catch a bid. For 5000 years, the problem with gold was that it yields nothing. Today, gold is the high yielding alternative in a world with negative interest rates. As long as we don’t see a bottom in the global economy, no immediate resolution to trade, and the Fed doesn’t get aggressive, I could see the gold price hitting $1700 or $1800 in the fourth quarter and maybe even making a run at the all-time high of $1900 before the end of the year.

end

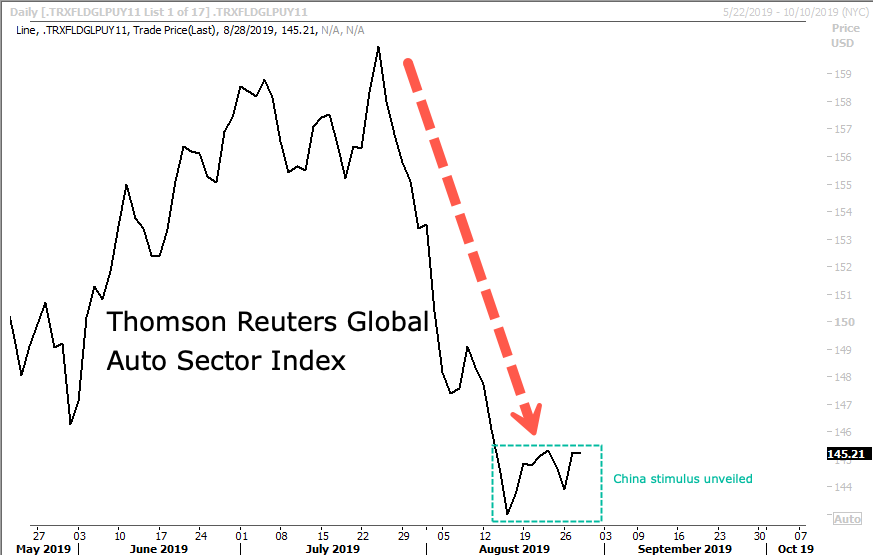

Platinum Prices Jump On China Stimulus Hopes; Seen As Catch-Up Trade To Gold & Silver

China is expected to dramatically ease restrictions on automobile purchases to help boost domestic consumption.

This includes new measures that will relax or lift restrictions and support the purchase of new cars, according to a new guideline that outlined 20 steps to spur economic growth issued by the State Council of the People’s Republic of China.

The State Council said in a statement that local governments across 23 provinces should consider relaxing or removing restrictions on vehicle purchases and encourage purchases of new energy vehicles.

As a result, global auto stocks have stabilized this week on the news that Beijing is expected to loosen restrictions.

More importantly, platinum is up 10% in 68 trading hours on hopes China’s domestic automobile industry can be revived.

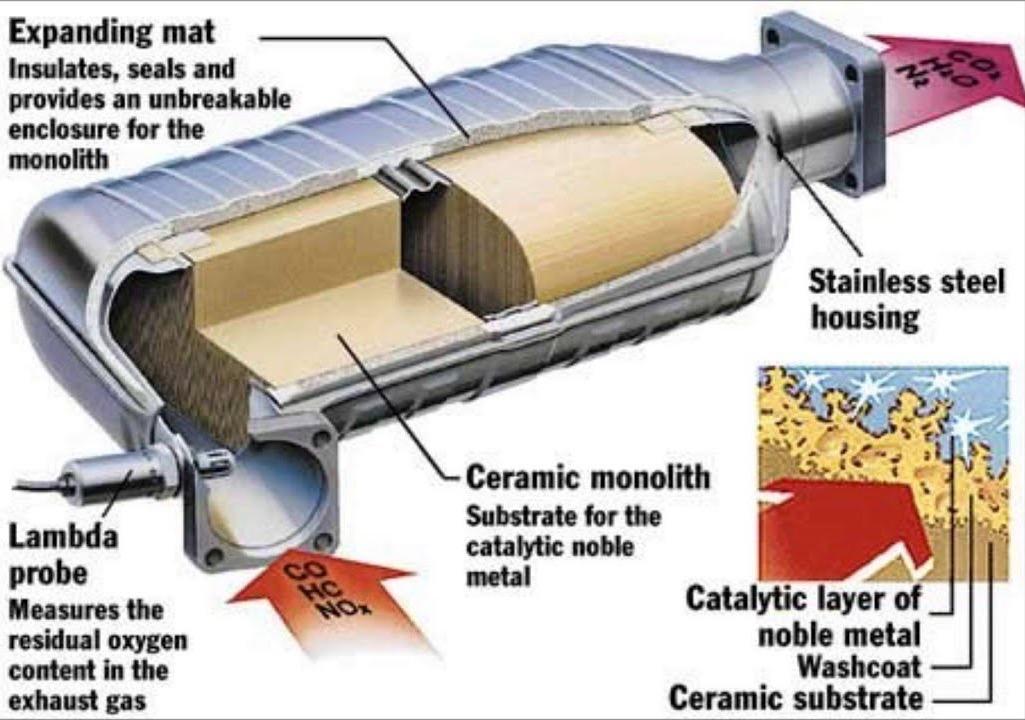

Platinum is used in making catalytic converters, which all modern automobiles are equipped with these devices that reduce emissions of harmful compounds found in car exhaust, including Carbon monoxide (a poisonous gas) and Nitrogen oxides (a cause of smog and acid rain).

On average, 3 to 7 grams of platinum is used in making a standard catalytic converter, but the amount varies on manufacturer and model.

Platinum has tumbled 60% in 46 quarters thanks to weaker demand and excess supply, whereas gold and silver have been accumulated in droves as per a hedge against a dovish Federal Reserve.

Trading at 2008 lows, platinum has been trying to base in the 1,000 to 750 level for 43 months.

Among the contributing factors mentioned above of why platinum prices are rising, it could be soon considered a catch-up trade to gold and silver, which have exploded over the course of this year thanks to dovish tilts by global central banks, an escalating trade war between the US and China, and macroeconomic risks pertaining to a worldwide synchronized slowdown.

The State Council is attempting to boost China’s domestic economy to weather an economic storm that started before the trade war but has undoubtedly been accelerated by trade disputes. It’s likely that a trade deal between the US and China isn’t expected until after 2020, that’s why China is implementing new measures to stimulate its economy.

Overall car sales in the country have declined for the 13th consecutive month in July. The government is hoping to trough the industry with the easing of restrictions.

Beijing is expected to roll out further stimulus measures to help boost its economy in the quarters ahead.

“China data weakness will likely be more visible in August and September, and policymakers will likely lean towards more intensive easing,” analysts at the Bank of America Merrill Lynch said in a note. “We expect policy loosening to resume in infrastructure investment, consumption stimulus, and monetary easing.”

Hard to say if platinum will erupt further, but it’s one precious metal that’s still trading on 2008 lows — something to watch for sure.

Blessings, ~ DK Dunagun Kaiser, founder ReluctantPreppers.com

Alasdair Macleod with Dunagun Kaiser

a must view..talks about Gold and Brexit

*Dennis Gartman…

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Global Stocks Surge On Trade Optimism, Ending Turbulent August With A Sea Of Green

For the second day in a row, global markets and US equity futures are a sea of green with stocks pushing higher as trade headlines bathe algos in a sea of trade optimism ahead of month end, even as the dollar ascent continued offsetting the weaker Chinese yuan which was on track for its weakest month in 2-1/2 decades.

On Thursday, the mood lifted after President Donald Trump said some trade discussions were taking place with China on Thursday, with more talks scheduled, even though there has been no subsequent news that any discussions did in fact take place suggesting this was yet another “fake call” report meant to boost stocks. China’s commerce ministry also said a September round of meetings was being discussed by the two sides, but added it was important for Washington to cancel a tariff increase.

There was more of the same on Friday, with US equity futures red ahead of the European open, when China’s Foreign Ministry spokesman Geng Shuang said that US and China “are maintaining effective communication,” during a regular briefing Friday in Beijing. He added that “we hope the U.S. can demonstrate good faith and take real action to work in concert with China and find solutions together on the basis of mutual respect.”

That little snippet was enough for algos to ignite momentum and lift the US some 20 points higher…

… even ignoring hawkish commentary from the ECB’s Executive Board member Sabine Lautenschlaeger who said in an interview with MNI that “I don’t see the need for a re-start of the asset purchase program”, adding that QE “should only be used if you have a deflation risk and a deflation risk is nowhere to be seen now.”

As a result, the MSCI All-Country World Index climbed 0.3% but is on track for a near 3% decline in August – only the second month the benchmark has spent in the red this year. It was set to be the weakest August for the index since 2015.

Taking their cue from US equity future optimism, European stocks on Friday extended the previous session’s gains, with the European STOXX 600 index up 0.3% to trade at a fresh one-month high. “The trade war seesaw has certainly moved back in favor of riskier assets for now, with Trump and China supposedly holding a call yesterday,” said Deutsche Bank strategist Jim Reid, although as noted above, there has yet to be confirmation of this. The DAX outperformed (+1%), with gains helped by a surge in German real estate firms which saw the country’s DAX index add 0.7%.

Earlier in the session, the picture was more mixed in Asia, where Chinese and Hong Kong stock markets dipped in and out of the red. Arrests or detentions of pro-democracy activists in Hong Kong added to investor jitters, with the Chinese-ruled territory facing its first recession in a decade. Most Asian stocks did advance, however, led by energy producers and technology firms, after Beijing took a softer tone on possible trade talks with Washington. Almost all markets in the region were up, with South Korea and Taiwan leading gains. The Topix added 1.5%, buoyed by SoftBank Group, Sony and Takeda Pharmaceutical. Japan’s industrial output rebounded in July following the worst decline in more than a year. The Shanghai Composite Index slipped 0.2%, dragged down by Shenzhen Goodix Technology and Industrial & Commercial Bank. China’s state-backed funds added positions in high-end manufacturing industries. India’s Sensex climbed 0.3%, with HDFC Bank and Housing Development Finance among the biggest boosts. Data due Friday is expected to show the nation’s gross domestic product growth slowed for a fifth straight quarter.

Also overnight, the global Times tweeted China is unswervingly tethered to its non-stop opening-up drive and reforming its economic system, even when the country is forced into a battle of tit-for-tat tariffs with the US on a massive, unprecedented magnitude.

Meanwhile, Hong Kong rejected the appeal against the protest ban on Saturday, while it was also reported that Hong Kong arrested prominent activists Joshua Wong, Andy Chan and Agnes Chow. Subsequent reports indicate that Wong and Chow have been released

Rates markets took a breather on Friday, at the end of a stellar month that has seen prices rally and borrowing costs push deeper and deeper into negative territory. U.S. Treasury yields nudged higher overnight, with the benchmark 10-year Treasury climbing to 1.5214% from a three-year low of 1.443% touched earlier this week. And despite the 2s10s curve briefly uninverted, the 10Y yield was once again below two-year yields at 1.538%.

Japanese yields popped higher early in the session, after the BOJ trimmed the amount of debt it would purchase in the 5-10 year bucket for the second time in 2 weeks, this time reducing the purchase amount from 450BN to 400BN.

Euro zone government bond yields were steady near record lows as data showed the bloc’s inflation remained low at 1.0% in August, well below the ECB’s target and bolstering expectations for European Central Bank stimulus in September. Bunds reversed early losses to trade little changed below 179.00, brushing off hawkish commentary and preliminary Eurozone inflation data that remains stuck below ECB’s target. German and US curves are marginally steeper however overall activity is muted in European hours. Italy bucks the spread-widening trend in Europe to tighten ~1bp against German 10y.

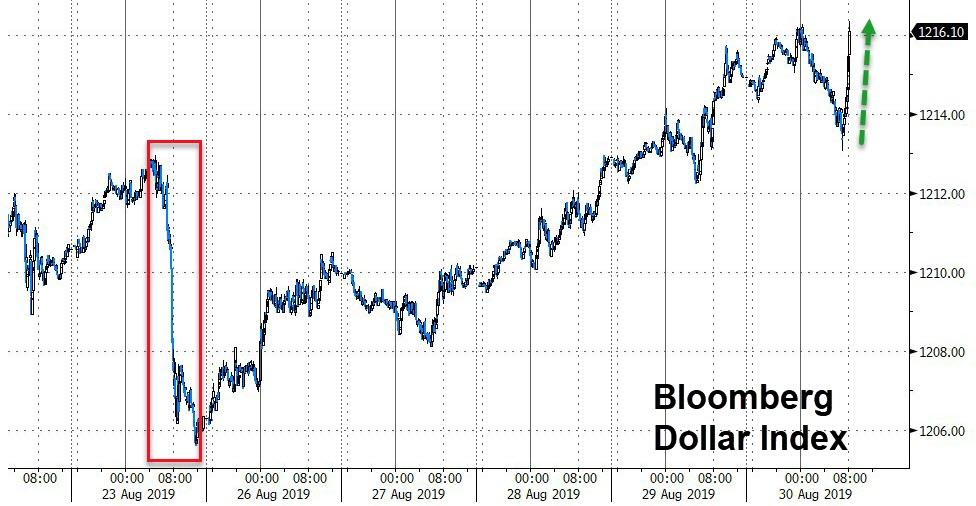

In FX, the Bloomberg dollar index was initially stronger for a fifth straight day although gains fizzled and it has since dipped into the red; SEK lags G-10 peers; ZAR leads in EM FX. The pound struggled for direction as lawmakers lost a bid to block Prime Minister Boris Johnson’s plan to suspend parliament. Elsewhere, the euro plunged to a one-month low against the dollar, as investors looked for aggressive easing by the European Central Bank and ignored doubts by some policymakers about the need for more stimulus.

Fresh trade optimism failed to inspire China’s yuan, which resumed its decline with spot yuan at 7.1462 against the dollar. The currency is on track for its weakest month since Beijing’s currency reform in 1994 after it broke through the key 7 to the dollar level earlier in August. Curiously, while both the yuan and US stocks got hit last Friday when Trump re-escalated the trade war, since then the CNH has remained deeply underwater, while the S&P has managed to recover all losses.

“The yuan move back to 7 and beyond has been a distinct possibility for months. It is clearly down due to the tariffs,” said Neil Mellor, senior FX strategist at BNY Mellon in London. “It does help them to some extent to absorb the tariff costs – it is one of the few options they have. The fiscal option is limited after years of excess, and the monetary stimulus has already been unprecedented this year.”

The Australian dollar, often seen as a proxy bet on the Chinese economy, slipped towards a 10-year trough.

In commodities, WTI slipped 57 cents to $56.14 a barrel while Brent fell 30 cents to $60.78 a barrel. Iron ore futures rally about 5% to conclude a torrid month, nickel rallies on supply concerns. Spot gold came off recent highs to trade at $1,526 an ounce. Silver was at $18.37 an ounce after hitting its highest level in more than two years.

Investors were focused on a string of economic releases due over the weekend including China’s official manufacturing survey, which would provide a good gauge of the real impact from the Sino-U.S. trade war.

Economic data include personal income and spending, MNI Chicago business barometer

Market Snapshot

- S&P 500 futures up 0.6% to 2,942.50

- STOXX Europe 600 up 0.7% to 379.37

- MXAP up 1.2% to 152.79

- MXAPJ up 1.1% to 493.71

- Nikkei up 1.2% to 20,704.37

- Topix up 1.5% to 1,511.86

- Hang Seng Index up 0.08% to 25,724.73

- Shanghai Composite down 0.2% to 2,886.24

- Sensex up 0.4% to 37,208.51

- Australia S&P/ASX 200 up 1.5% to 6,604.22

- Kospi up 1.8% to 1,967.79

- German 10Y yield fell 0.5 bps to -0.697%

- Euro down 0.1% to $1.1042

- Brent Futures down 0.5% to $60.78/bbl

- Italian 10Y yield fell 6.0 bps to 0.642%

- Spanish 10Y yield rose 0.9 bps to 0.112%

- Brent Futures down 0.5% to $60.78/bbl

- Gold spot down 0.2% to $1,524.85

- U.S. Dollar Index up 0.05% to 98.55

Top Headline News from Bloomberg

- European Central Bank policy makers wary of ever-more monetary stimulus have fired the first warning shots two weeks before they meet to discuss bolstering the economy

- A Scottish judge refused to block Boris Johnson’s plan to suspend Parliament, dealing a blow to lawmakers who argued that there isn’t enough time to thwart a no-deal Brexit; Johnson’s Brexit team will meet with EU officials at least twice a week in September as he seeks to break the current impasse and ward off a rebellion in his own party

- President Donald Trump said Thursday that the U.S. and China are scheduled to have a conversation about trade today without giving details. His comments followed signs from China that it wouldn’t immediately retaliate against the latest U.S. tariff increase

- Hong Kong police arrested prominent opposition figures including Joshua Wong a day after banning a mass protest planned for this weekend as authorities seek to quell pro- democracy demonstrations that have raged for nearly three months; China rejected HK’s Chief Executive Carrie Lam’s plan to appease protesters, Reuters reported on Friday

- Argentina’s bonds extended declines as S&P Global Ratings cut the South American nation’s foreign- and local-currency credit ratings to “selective default” after it said it would delay payments on as much as $101 billion of debt.

Asian equity markets headed into month-end higher across the board after the tumultuous US-China trade saga took a positive turn following comments from Mofcom spurred that hopes regarding talks in September and indicated that China doesn’t plan to immediately retaliate against President Trump’s latest tariff hikes. ASX 200 (+1.5%) and Nikkei 225 (+1.2%) advanced from the open with notable strength seen in Australia’s trade-sensitive sectors and as earnings continued to trickle in, while Tokyo trade was buoyant with focus on a slew of mixed data in which Industrial Production significantly topped estimates and amid reports that Japan permitted the first exports of hydrogen fluoride to South Korea since curbs were enacted. Hang Seng (+0.1%) and Shanghai Comp. (-0.1%) were underpinned by the trade hopes after Mofcom stated that both sides are discussing the September talks and that the sides have been in touch, while it also suggested that China wants to settle the dispute calmly and avoid further escalation. Furthermore, earnings have also been a driving force with firm gains in China’s largest bank ICBC, as well as oil majors CNOOC and PetroChina following their results, although upside in the broader market was contained given the looming additional tariffs and after continued PBoC inaction resulted to a consecutive weekly net liquidity drain. Finally, 10yr JGBs were lower with safe-haven demand sapped by the positive risk tone and after the BoJ reduced its purchases in 5yr-10yr JGBs to JPY 400bln from JPY 450bln for today’s Rinban operation.

Top Asian News

- China Had Rejected Lam Plan to Appease H.K. Protesters: Reuters

- BOJ Paves Way to Buy Fewer Bonds in September as Yields Slide

- China, U.S. Maintaining Effective Trade Communication: Geng

- Samsung Heir’s Retrial Spotlights Moon’s Coddling of Korea Inc.

Major European indices are firmer this morning [Euro Stoxx 50 +0.8%] as markets look to round a volatile week and month off on a positive tone, ahead of next month’s Central Bank infused slate. European bourses positivity follows on from the relatively strong performance seen in the Asia-Pac session, as sentiment received a boost on US-China updates; although, trade newsflow has been light in European hours. In terms of sectors the STXX Housing Sector (+2.2%) is outperforming on the back of reports that the rent freeze in Berlin may not be as strict as was initially feared/reported. Reports which have led to Deutsche Wohnen (+12.9%) topping the Stoxx 600, with Vonovia (+5.8%) not far behind. Elsewhere, other notable movers include Daimler (+2.3%) after being upgraded to buy at Kepler Chevreux, which has helped the auto sector more broadly (+1.7%). Separately, Deutsche Bank (+0.1%) are lagging the DAX (+0.6%) after reports that the Co. are examining the closure of local branches and are likely to begin an equity derivatives book auction in September. More broadly, the Banking index (+0.7%) remains in positive territory but is towards the bottom of the index pile, which may be partially explained by S&P downgrading Argentina’s credit rating to ‘Selective Default’ from ‘B-‘ after the country stated it would be delaying debt payments.

Top European News

- EU Concerned on U.K. Democracy After ‘Strange’ Parliament Move

- Merkel Might Be in Real Trouble If German Populists Win Sunday

- Equinor Signals Potential Early Start for Oil Giant Sverdrup

In FX, the Euro is edging closer to ytd lows vs the Dollar at 1.1027 following more dire German data (retail sales), and despite ECB’s Lautenschlaeger adding her hawkish views to those of Knot and Weidmann ahead of September’s policy meeting. Month end rebalancing flows are not providing traction/support this time as light Usd sales are touted against all G10s bar the Euro, while even the usual RHS flows/orders in Eur/Gbp seem to be conspicuously absent or relatively small given that the cross remains capped ahead of 0.9100 and the Pound is hardly firm in its own right. In terms of fundamentals, the ECB is still widely expected to deliver some form of stimulus next month even if not the big bazooka favoured by Rehn and other doves perhaps. However, hefty option expiry interest at 1.1050 (1.9 bn) could be cushioning Eur/Usd vs smaller size at the 1.1000 strike (1 bn), albeit amply backed up by barrier defences.

- USD – Notwithstanding the mostly bearish portfolio models noted above, the Greenback is only really softer vs the Yen in major markets, and the DXY has probed above resistance ahead of the 2019 peak, though remains some way below at 98.609 vs 98.932. Looming US data/surveys could give the index further impetus, but direction looks more contingent on broader risk sentiment and US-China trade developments with repercussions for Treasury yields and the curve alongside the Euro’s ability to evade further weakness.

- JPY – Bucking the overall trend, but marginally the Yen is holding a tight line around 106.50 vs the Buck following a raft of mixed Japanese data overnight and with plenty flanking the headline pair either side of the range. 1.4 bn expiries reside between 106.00-15 and the 21 DMA is only a fraction above at 106.17, while exporter supply is said to be layered from 106.70 right up to and through 107.00 at 107.10.

- CHF – In contrast to its fellow safe-haven, the Franc has retreated towards 0.9900 vs the Dollar and below 1.0900 against the Euro even though Switzerland’s KOF index was better than expected, and it appears evident that latest SNB warnings about action to curb excessive Chf demand are being heeded.

- GBP/CAD/NZD/AUD – All narrowly mixed against the Greenback, with Cable deriving some traction above 1.2150 and the 21 DMA (1.2154) to retest offers/resistance around 1.2200, while the Loonie continues to straddle 1.3300, but could finally break out of its shackles if Canadian GDP is outside consensus. Elsewhere, the Kiwi and Aussie are still top heavy on a mixture of dovish RBNZ/RBA and downbeat economic indicators not to mention negative input from RBA’s Debelle, with Aud/Usd only just hovering above 0.6700 and Nzd/Usd struggling to keep tabs on 0.6300.

- SEK/NOK – The Scandi Crowns are mixed vs the Euro, but both looking technically weak as the crosses trade above 10.8000 and 10.0000 respectively. However, the Sek is underperforming ahead of next week’s Riksbank policy meeting that could culminate in a dovish tweak to forward guidance via the timing of the likely next rate hike and/or a flatter repo path.

In commodities, WTI and Brent are in negative in territory and failing to benefit from the strong performance in stocks thus far; with WTI retreating somewhat from yesterday’s weekly high of USD 56.86/bbl and Brent painting a similar picture. In terms of catalysts there have been no fundamental updates for the complex, though its worth nothing that today is Brent’s Oct’19 future expiry which, alongside month-end flows, may be playing a role in today’s price action. Turning to metals, where spot gold has slipped somewhat on the strength in stocks and the USD’s strength this morning; as such the yellow metal looks set to finish the week just a few dollars away from its Monday open at USD 1527/oz. Separately, UBS note that iron ore prices have had a very volatile H1, and the metal is now being afflicted by slower production and supply lifts which may push it below the USD 80.0/t mark.

US Event Calendar

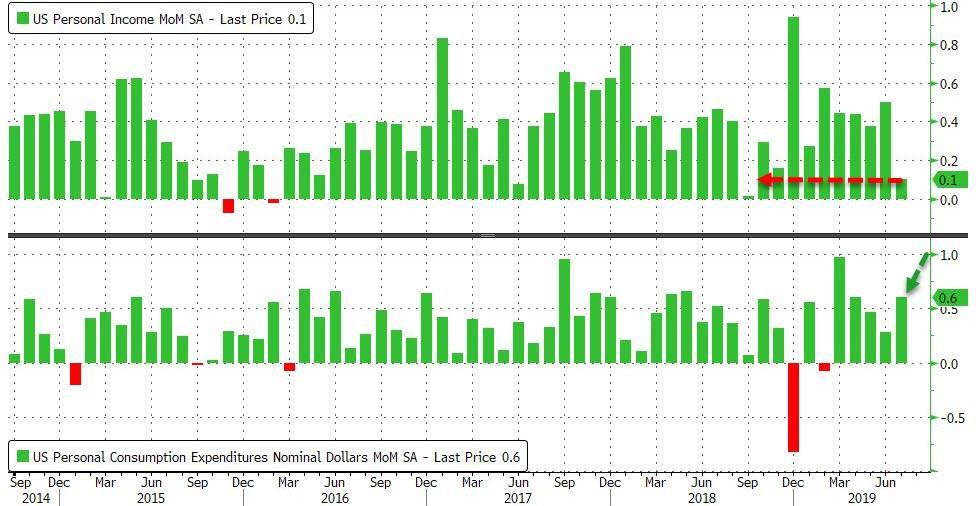

- 8:30am: Personal Income, est. 0.3%, prior 0.4%; Personal Spending, est. 0.5%, prior 0.3%

- 8:30am: PCE Deflator MoM, est. 0.2%, prior 0.1%; PCE Deflator YoY, est. 1.4%, prior 1.4%; PCE Core Deflator YoY, est. 1.6%, prior 1.6%;

- 9:45am: MNI Chicago PMI, est. 47.5, prior 44.4

- 10am: U. of Mich. Sentiment, est. 92.3, prior 92.1; Current Conditions, prior 107.4; Expectations, prior 82.3

DB’s Jim Reid concludes the overnight wrap

elcome to the last business day of August and with it the last of the meteorological Summer (or Winter depending on where you’re reading this). Since I’ve got back from holiday it’s been dark writing the EMR again which is a little depressing! Roll on next April. We’ll do our usual full performance review on Monday but August has been a trying month for markets. However the reality is that the full range for the S&P 500 was put in place in the first 5 days of the month and although we’ve got to the bottom of that range a couple of times since we haven’t broken through and markets have bounced back off the ropes three times this month now.

Indeed that’s what’s happened this week as we’ve now had three out of four strong days since Monday including a +1.27% gain yesterday meaning that the S&P 500 is back above last Friday’s closing level which is impressive given that all the talk over the weekend was about how bad Monday’s open would be after renewed trade escalations. The trade-war seesaw has certainly moved back in favour of riskier assets for now, with Trump and China supposedly holding a call yesterday, at least according to Trump earlier in the day. However, neither side had confirmed this as we go to print. Meanwhile, risk assets were already getting a boost from the news that China doesn’t intend to immediately retaliate on tariffs, following comments out of the Ministry of Commerce just as European markets were opening. The NASDAQ (+1.48%) and DOW (+1.25%) also closed higher along with the STOXX 600 (+1.04%) as cyclical sectors led the advance. After lagging earlier this week, large-cap tech stocks outperformed, with the NYFANG index +2.15% higher.