GOLD:$1546.60 UP $25.60 (COMEX TO COMEX CLOSING

Silver:$19.15 UP 83 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1547.60

silver: $19.27

Gold and silver had stellar performances today with gold advancing by $25.60 and silver by 83 cents. I have been pointing out to you lately that the bankers are in serious trouble as they have a massive derivative shortage in both metals but a truly mammoth one in silver. Bankers get killed in derivatives with the speed to which our precious metal rises. Silver, in late June was trading around $14.75 so a gain of over 4.40 in 2 months fries our bankers. Deutsche bank with huge silver exposure will no doubt need the support of the Bundesbank to continue.

Many have asked how will gold perform in a negative yield environment especially if the USA undergoes the same route. The Alasdair Macleod paper answers that in detail and is your must read commentary for the day. I will refer to it in future commentaries as all nations go zero bound in interest rates.

we are getting very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 82/242

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,519.100000000 USD

INTENT DATE: 08/30/2019 DELIVERY DATE: 09/04/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

118 H MACQUARIE FUT 54

152 C DORMAN TRADING 13

657 C MORGAN STANLEY 17

661 C JP MORGAN 26

661 H JP MORGAN 56

686 C INTL FCSTONE 5

690 C ABN AMRO 38 6

737 C ADVANTAGE 70 37

800 C MAREX SPEC 121 38

905 C ADM 3

____________________________________________________________________________________________

TOTAL: 242 242

MONTH TO DATE: 1,521

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 242 NOTICE(S) FOR 24,200 OZ (0.7527 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1521 NOTICES FOR 152100 OZ (4.7309 TONNES)

SILVER

FOR SEPT

619 NOTICE(S) FILED TODAY FOR 3,095,000 OZ/

total number of notices filed so far this month: 5481 for 27,405,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 10,402 UP 70

Bitcoin: FINAL EVENING TRADE: $ 10659 UP 319

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A GIGANTIC SIZED 5390 CONTRACTS FROM 224,177 DOWN TO 218,787 DESPITE THE TINY 2 CENT LOSS IN SILVER PRICING AT THE COMEX.

TODAY WE ARE FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR SEPT,FOR DEC: 1270 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1270 CONTRACTS. WITH THE TRANSFER OF 1270 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1270 EFP CONTRACTS TRANSLATES INTO 6.35 MILLION OZ ACCOMPANYING:

1.THE TINY 2 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

35.405 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

WE HAD MASSIVE COVERING OF BANKER SHORTS AT THE SILVER COMEX ON FRIDAY AS THE BANKERS HAVE NOW COME TO REALIZE THAT THEY ARE IN SERIOUS TROUBLE. THE LIQUIDATION OF COMEX OI OF SPREADERS HAVE STOPPED AND WE WILL NOW COMMENCE WITH THE ACCUMULATION PHASE OF SPREADERS GOLD OPEN INTEREST.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

1270 CONTRACTS (FOR 1 TRADING DAYS TOTAL 1270 CONTRACTS) OR 6.35 MILLION OZ: (AVERAGE PER DAY: 1270 CONTRACTS OR X MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF SEPT: 6.35 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 0.907% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1556.06 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 5390, DESPITE THE TINY 2 CENT LOSS IN SILVER PRICING AT THE COMEX /FRIDAY... THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1270 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST AN ATMOSPHERIC SIZED: 4120 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1270 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 5305 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 2 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $18.22 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A VERY STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.094 BILLION OZ TO BE EXACT or 156% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 619 NOTICE(S) FOR 3,095,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/SEPT 35.404 MILLION OZ//

- THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 9474 CONTRACTS, TO 609,472 ACCOMPANYING THE $7,00 PRICING LOSS WITH RESPECT TO COMEX GOLD PRICING// FRIDAY// /

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 6946 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 6946 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 610,294,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A CONSIDERABLE LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1706 CONTRACTS: 8652 CONTRACTS DECREASED AT THE COMEX AND 6946 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 1706 CONTRACTS OR 170,600 OZ OR 5.306 TONNES. FRIDAY WE HAD A LOSS OF $7.00 IN GOLD TRADING….AND WITH THAT LOSS IN PRICE, WE HAD A SMALL LOSS IN GOLD TONNAGE OF 5.306 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER TRYING TO FLEECE GOLD LONGS ON OPTIONS EXPIRY WITH LIMITED SUCCESS…AND WITH THAT LOSS IN PRICE, WE HAD A SMALL LOSS IN GOLD TONNAGE OF 5.306 TONNES!!!!!!. IT ALSO LOOKS LIKE WE HAD SOME BANKER SHORT COVERING IN GOLD ACCOMPANYING THE HUGE SHORT COVERING IN SILVER.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 6946 CONTRACTS OR 694,600 oz OR 21.60 TONNES (1 TRADING DAY AND THUS AVERAGING: 6946 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY IN TONNES: 21.60 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 21.60/3550 x 100% TONNES =0.606% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4172.92 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED DECREASE IN OI AT THE COMEX OF 9474 DESPITE THE RATHER TIMID PRICING LOSS THAT GOLD UNDERTOOK FRIDAY($7.00)) //.WE ALSO HAD A HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6946 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6946 EFP CONTRACTS ISSUED, WE HAD A GOOD SIZED LOSS OF 2528 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6946 CONTRACTS MOVE TO LONDON AND 89474 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE LOSS IN TOTAL OI EQUATES TO 7.863 TONNES). ..AND ALL OF THIS LACK OF DEMAND OCCURRED DESPITE THE SMALLISH LOSS IN PRICE OF $7.00 WITH RESPECT TO FRIDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 242 notice(s) filed upon for 24,200 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $25.60 TODAY//(COMEX-TO COMEX)

VERY STRANGE INDEED!!

A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD..

INVENTORY RESTS AT 878.31 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 83 CENTS TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV:

/INVENTORY RESTS AT 388.154 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A GIGANTIC SIZED 5390 CONTRACTS from 227,327 DOWN TO 218,787 AND FURTHER FROM A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR SEPT. 0; FOR DEC 1270 OI CONTRACTS: AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1270 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 5305 CONTRACTS TO THE 1270 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN ATMOSPHERIC AND CRIMINALLY SIZED LOSS OF 4120 OPEN INTEREST CONTRACTS.THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 20.600 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ//SEPT 2019: 35.405 MILLION OZ/

RESULT: A GIGANTIC SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE TINY 2 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// FRIDAY. WE ALSO HAD A GOOD SIZED 1270 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE VERY STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL. IN SILVER WE ARE WITNESSING MASSIVE BANK SHORT COVERING AS THEY NOW REALIZE THAT THEY ARE IN DEEP TROUBLE.

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 6.05 POINTS OR 0.21% //Hang Sang CLOSED DOWN 98.70 POINTS OR 0.39% /The Nikkei closed UP 4.97 POINTS OR 0-.02%//Australia’s all ordinaires CLOSED DOWN .06%

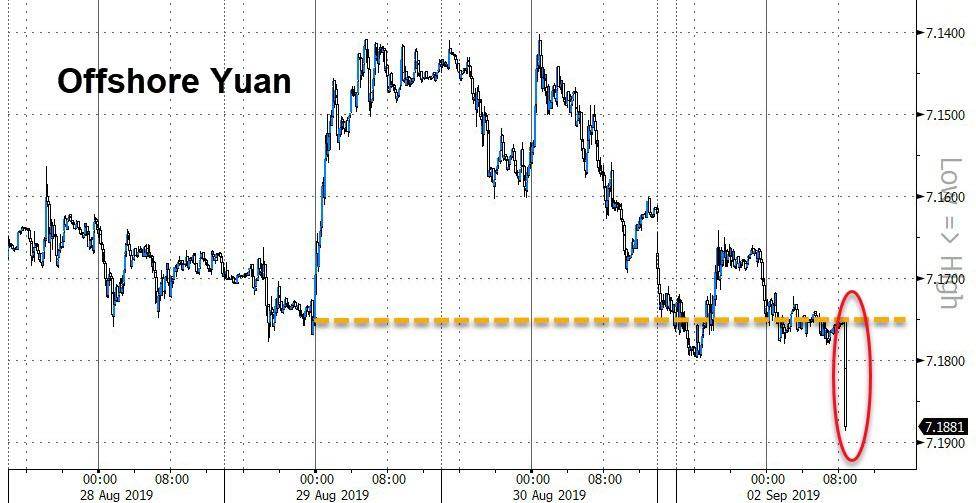

/Chinese yuan (ONSHORE) closed DOWN at 7.1771 /Oil UP TO 54.06 dollars per barrel for WTI and 57.68 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1771 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1815 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

i)Gatestone’s Lawrence Franklin discusses the options facing Mainland China in their dealings with the Hong Kong protests. It is a very important commentary and a must read. The real reason for the protests: What will happen in 2047 when Hong Kong must give up their 2 systems..two governments formula set up in the handover of the city in 1997.

ii)Hong Kong

iii)Sunday/Hong Kong

Protests continue on Sunday with the protesters occupying the Hong Kong Airport. There was a surge of violeance reported.

(zerohedge)

iv)CHINA/USA/SUNDAY

v)HONG KONG/CHINA/MONDAY

Hong Kong issued its ultimatum to not only protesters but also the West (not to infringe on Chinese sovereignty)

(zerohedge)

vi)MONDAY/CHINA/USA

vii)Tuesday

4/EUROPEAN AFFAIRS

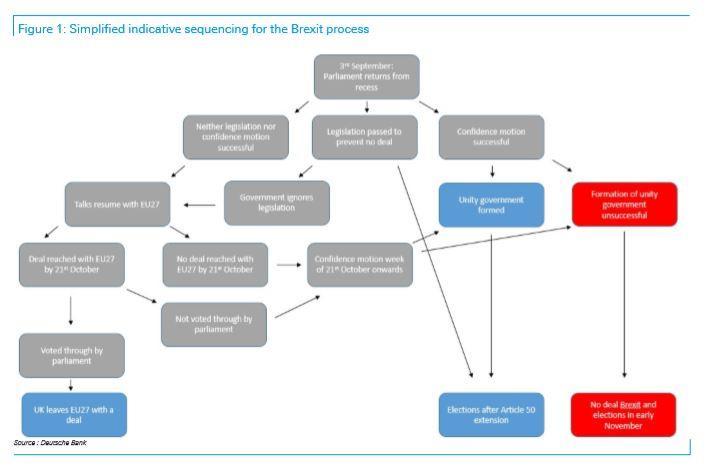

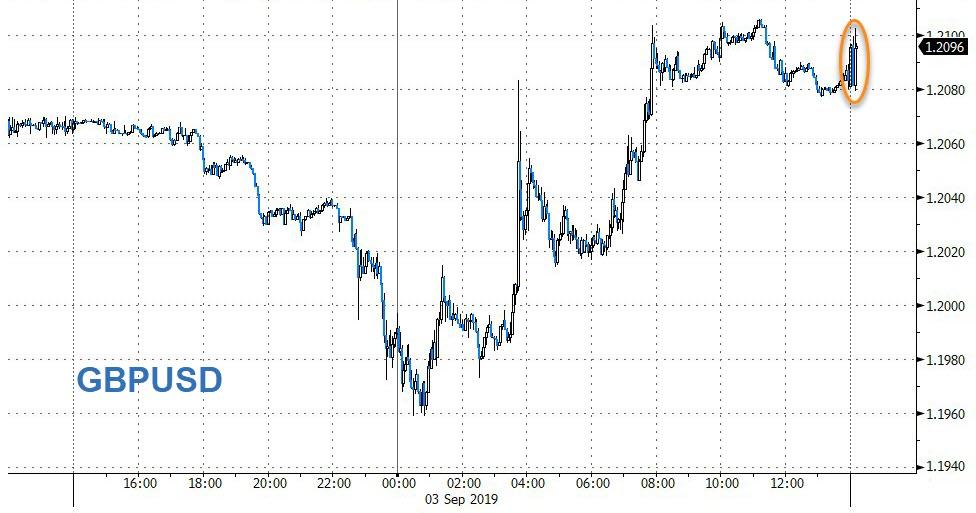

i)Mish Shedlock is terrific on his understanding of Brexit. He is now under the opinion that there is no way that the remainers can stop Brexit.

(Mish Shedlock/Mishtalk)

ii)According to Mish Shedlock this has no chance of stopping a hard Brexit

(zerohedge)

iii)In a stunning turn of events a Conservative crosses the floor and joins the Liberal Democrats. He was going to lose in the next election anyway as his riding is furious at him. However this lessens the chance of the hard Brexit

iiib)OH oh!! this does not look good as stupid rebel MP’s successfully seize control of the uK parliament. However on a general election they will be thrown out.chances for a Hard Brexit has been diminished and the UK is still handcuffed to the crooked EU

(zerohedge)

iv)ECB

Seem that we have a Mutiny of the Bounty with respect to the ECB as many hawks do not want any more bond purchases which of course would bankrupt Italy in a heartbeat. The hawks are still in favour of lowering the negative interest rates even more and consensus is that on the Sept 12 meeting they will lower the rates by 16 basis points.

(zerohedge)

7. OIL ISSUES

As promised to you on several occasions, the shale industry is in big trouble not so much because of low oil prices but because of huge debt. Companies are having trouble rolling over their debt and we have already major bankruptcies filed last month

(zerohedge)

8 EMERGING MARKET ISSUES

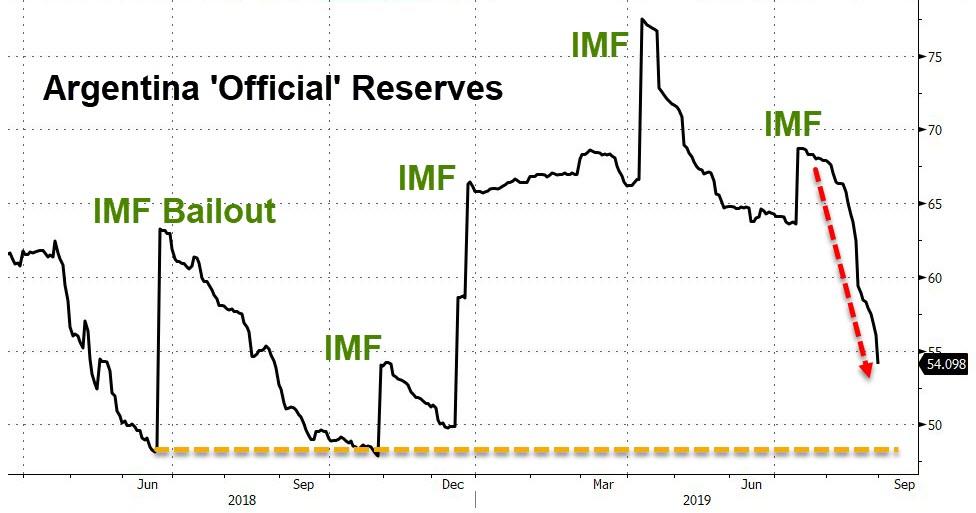

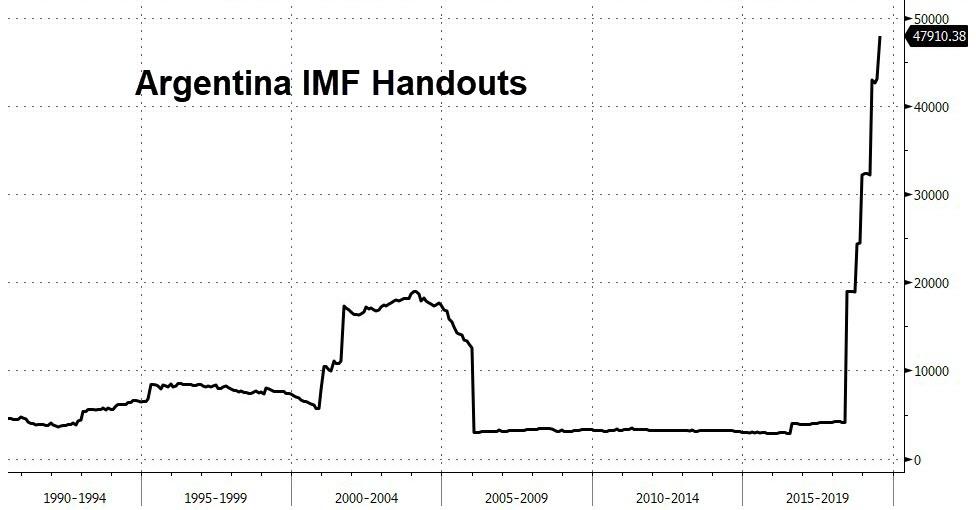

i)Saturday/Argentina

Argentina has been losing foreign exchange dollars by the bucketful. The government is now imposing currency controls trying to stem the losses of dollars which are badly need in the country. No matter which way you look at it, the Peso is doomed

(courtesy zerohedge)

ii)Monday Argentina

Strange The Argentina Peso temporarily rises amid zero liquidity. We have real problems in Argentina as they are finding it difficult to find dollars

(zerohedge)

9. PHYSICAL MARKETS

i)I pointed this commentary to you on Friday and I have gone over it myself several times and I finally understand it fully.

Each day, I report to you the following:

Libor rates

GOFO rates (time preference not to have gold in your possession)

and Gold Lease rates which is the Libor rate (generally the rate to which banks give you money on loan/money cost) – GOFO rate(gold cost time preference)

For the past few months, one can see that the lease rate is zero (or approaching zero) with the 12 month GOFO rates (today 1.96%) and the 12 month Libor rate (1.90%) being almost identical and a tiny positive lease rate of .06%. The 6 month rate which is the only that is most widely used in determining lease rates is negative .04%

here is the numbers from Friday

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.07/ and libor 6 month duration 2.03

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .04

XXXXXXXX

12 Month MM GOFO

+ 1.90%

LIBOR FOR 12 MONTH DURATION: 1.96

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.06

For years central banks were leasing out gold as it had a positive cost and the USA dollar reward was quite high. That is the time preference for gold averaged around 2% and the 6 month yield was around 6% and thus a tidy profit. Thus central banks dishoarded a huge 10,000 to 15,000 tonnes of gold and thus the huge mushrooming of derivatives on the previous metals was born. When gold costs are positive we are in contango.

However now we see Europe, Switzerland, Sweden and Japan has negative money rates and it is inevitable that the USA will go down this path as economies falter badly. As Alasdair Macleod states that once USA interest rates go negative (also Time Preference negative) then we will witness the reverse of the huge mushrooming of derivatives as banks try and cover their huge shortfall mess.

At this point in time, the dollar become time preference negative or goes into backwardation and this will lead to all commodities including gold and silver going into backwardation as well as a huge rise in the spot rise for our precious metals.

This is an important read..

ii)A good commentary today from Manly: he notes that the considerable decline in Chinese imports may be to mask the rise in official reserves as our sovereign is the one who is buying the precious metals.

iii)We have been highlighting this to you on a daily basis through the biggest of all EFT’s: the GLD/SLV(Pakiam/Bloomberg/GATA)

iv)At least somebody is paying attention to these chat room discussion where 5 banks collude. We have the evidence that they have also fixed the price of gold/silver. Judge Rakoff is one smart individual and he states that these discussions are a “rare smoking gun” of price fixing.

(zerohedge)

v)Platinum is coming to the party although late

(courtesy Lawrie Williams)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

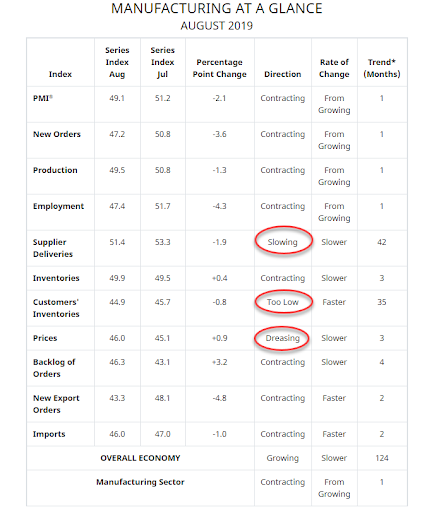

This is huge! After China and Europe reported huge contractions in their mfg PMI, the USA reported its weakest Mfg PMI in 10 years..new exports orders collapse

(zerohedge)

iii) Important USA Economic Stories

a)Dorian will cause havoc to our insurers as the storm may face losses to top 40 billion dollars

(zerohedge)

b)Floridians brace for Dorian as it weakens to a category 3. It was devastating to the Bahamas

(zerohedge)

iv) Swamp commentaries)

(zerohedge)

b)For those of you who think that Comey is out of the woods, think again. A great commentary from Larry Johnson

(courtesy Larry Johnson Sic Sempter Tyrannis blog)

c)McCarthy is one smart cookie. He gives a thorough analysis of the Trump and Clinton mess outlining how Clinton and her entourage gets a free pass and some of Trump’s people get charged. At the end he gives his reasoning for going after McCabe

(Andrew McCarthy)

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; nil oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 193,659 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 134,145 CONTRACTS.

YESTERDAY’S CONFIRMED VOLUME OF 134,145 CONTRACTS EQUATES to 673 million OZ 96.07% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -1.57% ((SEPT 3/2019)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -2.62% to NAV (AUGUST 30/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -1.57%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.83 TRADING 15.39/DISCOUNT 2.77

END

And now the Gold inventory at the GLD/

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

AUGUST 22.WITH GOLD DOWN $6.80 TODAY: TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD: I)A PAPER DEPOSIT OF 6.74 TONNES INTO THE GLD (LATE YESTERDAY EVENING) AND 2) A PAPER DEPOSIT OF 2.93 TONNES LATE THIS AFTERNOON./INVENTORY RESTS AT 854.84 TONNES

AUGUST 21/WITH GOLD DOWN $.30 TODAY:A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.76 TONNES INTO THE GLD INVENTORY/GOLD INVENTORY RESTS AT 845.17 TONNES

AUGUST 20//WITH GOLD UP $2.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GOLD INVENTORY RESTS AT 843.41 TONNES

AUGUST 19/WITH GOLD DOWN $11.20//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .88 TONNES//INVENTORY RESTS AT 843.41 TONNES

AUGUST 16/WITH GOLD DOWN $7.35: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 844.29 TONNES

AUGUST 15/WITH GOLD UP $3.55 TODAY//WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: WE GOT BACK 7.63 TONNES OUT OF 11.11 TONNES LOST ON WEDNESDAY( A DEPOSIT OF 7.63 TONNES)/INVENTORY RESTS AT 844.29 TONNES

AUGUST 14/WITH GOLD UP $7.60 TODAY (AND DOWN $2.90 YESTERDAY) WE HAD A MONSTROUS WITHDRAWAL OF 11.11 TONNES OF GOLD FROM THE GLD/AND THIS WAS USED IN AN ABORTED RAID YESTERDAY: INVENTORY RESTS AT 836.66 TONNES

AUGUST 13.2019: WITH GOLD DOWN $2.60 TO DAY: A HUGE 7.92 PAPER GOLD TONNES WERE ADDED TO THE GLD/INVENTORY RESTS AT 747.77 TONNES

AUGUST 12.2019: WITH GOLD UP $7.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 839.85 TONNES

AUGUST 9/WITH GOLD DOWN $2.00//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REMAINS AT 839.85 TONNES OZ/

AUGUST 8: WITH GOLD DOWN $4.20: TWO TRANSACTIONS: A)A MONSTROUS PAPER DEPOSIT OF 8.50 TONNES WAS ADDED TO THE GLD/INVENTORY RESTS AT 845.42 TONNES b) A HUGE WITHDRAWAL OF 5.59 TONNES FROM THE GLD//INVENTORY RESTS AT 839.85 TONNES…ABSOLUTE FRAUD!

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SEPT 30/2019/ Inventory rests tonight at 878.31 tonnes

*IN LAST 655 TRADING DAYS: 57.07 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 555- TRADING DAYS: A NET 109.58 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.696 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 21/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 20.WITH SILVER UP 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 19/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 16/: WITH SILVER DOWN 9 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 15/2019 WITH SILVER DOWN 2 CENTS: ANOTHER BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING 3.977 MILLION OZ PAPER DEPOSIT/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 14/2019 WITH SILVER UP 27 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 4.538 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 376.177 MILLION OZ//

AUGUST 13/2019: WITH SILVER DOWN 9 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 6.082 MILLION OZ///INVENTORY NOW RESTS AT 371.637 MILLION OZ

AUGUST 12/2019: WITH SILVER UP 11 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 365.557 MILLION OZ.

AUGUST 9/2019//WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.245 MILLION OZ INTO THE SLV INVENTORY/INVENTORY ADVANCES 365.557 MILLION OZ

AUGUST 8/WITH SILVER DOWN 23 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT: 1.409 MILLION OZ INTO INVENTORY///INVENTORY RESTS AT 363.311 MILLION OZ//

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

SEPT 3/2019:

Inventory 388.154 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES/GOLD LENDING RATES:

YOUR DATA…..

6 Month MM GOFO 2.07/ and libor 6 month duration 2.02

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .05

XXXXXXXX

12 Month MM GOFO

+ 1.94%

LIBOR FOR 12 MONTH DURATION: 1.95

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.01

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Gold At New Record Highs In Pounds and Euros – £1,280/oz and €1,400/oz – On Brexit and Economic Concerns

* Gold in sterling and euros have reached new record nominal highs of £1,279.46/oz and €1,401.60/oz respectively this morning (see charts below)

* Gold priced in sterling and euros soared to record highs due to political turmoil in the UK, increasing concerns about a disorderly UK exit from the EU and the slowing UK and European economies

* Sterling has lost a third of its value in the last 12 months with gold priced in sterling having gained 35% in 12 months

* Silver continues to eke out gains in all currencies as it plays catch up to gold

News and Commentary

Gold rises as U.S., China begin new round of tariffs

Pound tumbles as British factory output hits seven-year low ahead of Brexit showdown

British Prime Minister Boris Johnson says Brexit deal chances are rising

India’s seizures of smuggled gold jumps in June quarter

Investors Rush Into Gold ETF’s, 101.9 tons in August (most monthly inflows since 2013)

Cazenove Capital Favors Gold Over Bonds as Uncertainty Hedge

Gold Rally May Cool Briefly – Greg Bender

What caused Britain’s blackouts?

Gold Prices (LBMA – USD, GBP & EUR – AM/ PM Fix)

02-Sep-19 1523.35 1525.95, 1260.42 1265.01 & 1388.69 1391.51

30-Aug-19 1526.55 1528.40, 1253.14 1251.15 & 1382.75 1383.51

29-Aug-19 1536.65 1540.20, 1260.51 1262.96 & 1387.29 1392.03

28-Aug-19 1541.75 1537.15, 1263.31 1258.77 & 1389.89 1387.43

27-Aug-19 1531.85 1532.95, 1250.91 1247.51 & 1378.97 1380.88

26-Aug-19 UK Bank Holiday

23-Aug-19 1495.50 1503.80, 1224.37 1228.91 & 1351.48 1357.63

22-Aug-19 1498.70 1502.05, 1234.63 1225.97 & 1351.98 1354.10

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

I pointed this commentary to you on Friday and I have gone over it myself several times and I finally understand it fully.

The commentary is basically what happens to gold when you go to USA zero bound interest rates.

Each day, I report to you the following:

Libor rates

GOFO rates (time preference not to have gold in your possession)

and Gold Lease rates which is the Libor rate (generally the rate to which banks give you money on loan/money cost) – GOFO rate(gold cost time preference)

For the past few months, one can see that the lease rate is zero (or approaching zero) with the 12 month GOFO rates (today 1.96%) and the 12 month Libor rate (1.90%) being almost identical and a tiny positive lease rate of .06%. The 6 month rate which is the only that is most widely used in determining lease rates is negative .04%

here is the numbers from Friday

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.07/ and libor 6 month duration 2.03

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .04

XXXXXXXX

12 Month MM GOFO

+ 1.90%

LIBOR FOR 12 MONTH DURATION: 1.96

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.06

For years central banks were leasing out gold as it had a positive cost and the USA dollar reward was quite high. That is the time preference for gold averaged around 2% and the 6 month yield was around 6% and thus a tidy profit. Thus central banks dishoarded a huge 10,000 to 15,000 tonnes of gold and thus the huge mushrooming of derivatives on the previous metals was born. When gold costs are positive we are in contango.

However now we see Europe, Switzerland, Sweden and Japan has negative money rates and it is inevitable that the USA will go down this path as economies falter badly. As Alasdair Macleod states that once USA interest rates go negative (also Time Preference negative) then we will witness the reverse of the huge mushrooming of derivatives as banks try and cover their huge shortfall mess.

At this point in time, the dollar become time preference negative or goes into backwardation and this will lead to all commodities including gold and silver going into backwardation as well as a huge rise in the spot rise for our precious metals.

This is an important read..

take your time

h

Check-Mate For Central Banks: Negative Rates & Gold

Courtesy of ZeroHedge/GATA View original post here.

Authored by Alasdair Macleod via GoldMoney.com,

The reason for persistent strength in the price of gold can be found in the changing relationship between time preference for monetary gold, and a new round of interest rate suppression for the dollar. Evidence mounts that the forthcoming recession is likely to be significant, even turning into a deep slump. Bullion bank traders are waking up to the possibility that dollar interest rates are going to zero and that pressure is likely to be put on the Fed to introduce negative rates. The laws of time preference tell us bullion banks must urgently cover their short bullion positions in anticipation of a dollar rate-induced permanent backwardation for gold, silver and across all commodities.

This article dissects the moving parts in this fascinating story.

Introduction

For some time now, I have maintained the wheels are likely to fall off the global economic wagon by the year-end. Furthermore, for many of my interlocutors, the recent rise in the gold price is just evidence of an impending cyclical crisis, anticipating and discounting the certain inflationary response by central banks. But in this, we are describing only surface evidence, not the underlying market reality.

In the combination of trade protectionism and an emerging credit crisis we face a problem upon which almost no formal research has been done, so it is not something that even far-thinking analysts have considered. To my knowledge, no mainstream economist has pointed out the lethal mix these two dynamics together present. Very few even recognise the existence of a credit cycle, traditionally called a trade or business cycle. Not even the great von Mises called it a cycle of credit, having identified and described it with great accuracy in his The Theory of Money and Credit, first published in 1912. But a spade must be called a spade: it is in its fundament a credit cycle.

There are many Austrian economists who fully understand the credit cycle. But to it we must add the destructive synergy of American trade policy aimed at China. Much economic research has been conducted on the causes of a credit cycle, trade cycle, business cycle, whatever it may be called. Much research has also been conducted on the economic consequences of trade tariffs. But nowhere is there to be found any research or commentary on the destructive power of combining the two.

Yet, these were precisely the conditions in October 1929, when Wall Street awoke to the certainty that Congress would vote in favour of the Smoot-Hawley Tariff Act at the end of that month. The shock of a 35% top to bottom fall in the Dow in October 1929 was only a prelude to an extended collapse following President Hoover signing it into law the following year. The economic research that followed the subsequent depression was conducted almost entirely by inflationists promoting reflation, so the destructive synergy between a credit crisis and trade protectionism has been ignored.

We cannot know the future with certainty, but we can point to the empirical evidence following Smoot-Hawley and draw an alarming parallel with today’s events. Thus alerted, we can then develop a convincing theoretical case for its repeat. Every week, reports of the global economy stalling now hit the headlines, drawing the parallel even closer. Yet, with equity markets close to all-time highs, little more than a mild recession, easily batted away with a little more monetary inflation, is the general expectation.

But our knowledge tells us there is almost certainly a large unanticipated shock ahead of us, and we should proceed in any analysis with that expectation. This article postulates how early evidence from the rising price of gold suggests the shock is closer than even perennially bearish analysts expect. We shall now take the inflationary consequences of an unexpected slump as a given in order to predict the changes in the relationship between physical gold and fiat dollars; a relationship that has for the last four decades led to a massive expansion of gold derivatives. To understand that relationship, and why it now appears to be reversing requires a working knowledge of time preference, the basis of interest; and more specifically the changing relationship of gold’s time preference to that of dollars.

Interest and time preference

One’s own bookcase provides the perfect illustration of time preference, which is the greater value of possession over non possession. There will be books bought on a whim which just clutter a bookshelf and have no value. Next time there’s a clear-out, they are destined for the charity shop: there’s no difference in time value, being worthless to the owner today and in the future.

Then there are the first editions, which have a commercial value. Books in this category will have a high current value to you compared with their non-possession. But perhaps the books with the highest personal value are the ones that have little value to anyone else: that battered copy of Wren’s Beau Geste, or the translation of Hoffmann’s Struwwelpeter read to you when you were a child. You may have even visited the museum in Frankfurt dedicated to Hoffmann and his famous book of moral tales for children. The value of these books in possession is far greater than their absence, even though you rarely open their pages.

This is the basis of time preference: the greater value placed on possession than non-possession. The books with sentimental value will have very little value to anyone else, other booklovers having their own favourites. Everyone’s time preferences are different. In economic terms, we express these varying values in terms of the difference between a current value in possession and the value of non-possession, but the certainty of repossession at a future time. The discounted value of the future possession is normally expressed as an interest rate on the monetary value today.

Assuming free market prices, in theory nearly everything of value has a time preference, an interest rate. That is, anything people value more in their immediate possession than the promise of ownership at some stage in the future. A future value, with very few exceptions, is always less than that of current ownership, and it is the difference between the two that is given to a current owner in one form or another to part with possession for a defined period of time.

The only examples that go against time preference are special cases. For example, an individual might forgo a decent salary today, in order to study so that he or she can earn more after passing a professional exam. In this case, the value of a current earnings stream is rejected in favour of potentially better prospects later. Or the philanthropist, who lends artworks for free to a public gallery so that a wider audience can appreciate them (but perhaps he does have a reward – to be thought of as a generous philanthropist and pillar of society).

The proxy for valuing time preference on goods is money, and the way it is normally expressed is as a money-rate of interest, often termed the originary rate. The originary rate of interest can be specific, assessed and applied in a single transaction such as obtaining the temporary use of a machine for a defined time. It can be a consolidated rate through the application of savings, reflecting the time preferences of the many goods and services whose possession is temporarily deferred by the saver.

Time preference is just the core consideration behind an interest rate. There will be other interest elements in addition, such as the trustworthiness and financial record of the borrower. But for the individual who has sacrificed the immediate satisfaction of spending the money put aside as savings, the time preference element will reflect the discounted future values of the goods and services that otherwise would have been purchased.

As well as time preferences reflecting baskets of specific goods and services, individuals will personally have different time preferences as well, as illustrated with the example of a personal library. But as is the case with any value, it is the marginal rate which is usually accepted as the market rate of interest, and therefore indicates the overall value of time preference within it. In addition, an interest rate must be greater than the sum of the originary rate and the compensation for all perceived lending risks, in order to create savings flows to feed investment.

This being the case, why is it that in financial markets, the forward price of something at a future date is usually higher than the present? The answer is simple: forward prices are not for possession, but for extending non-possession. Instead of being obliged to pay for possession today, a futures or forward price allows an individual to hang on to money for longer, rather than part with it now. And, assuming free markets set interest rates, with money’s time preference being greater than that of the average consumer item (in order to create savings flows referred to above), plus the addition for financial risk compensation, it should always be higher than the pure time preference applied to the underlying commodity, item or even just a title to ownership.

Therefore, higher prices for future deliveries of commodities and titles to ownership in financial markets are principally a reflection of money’s time preference, plus the risks associated with change of its ownership.To this should be offset the specific time-preference for individual commodities, but so long as they are in adequate supply, they will not be relatively significant compared with that of money.

This means the financial representation of time in a futures or forward contract in a properly functioning market is normally a positive cost. This condition is termed contango.We must also allow for the relative demand and supply characteristics of the underlying security between Date 1 and Date 2, which may temporarily lift a commodity’s time preference above that of money. If demand characteristics are such that the value of an immediate delivery overrides money’s time preference, then we have a backwardation. For example, there may be an acute shortage currently but supplies of the commodity in question are expected to be more plentiful at a future date. Backwardation is a temporary condition, and not the normal situation in financial markets.

To summarise so far, time preference tells us, except in a few specific cases, that the underlying or originary interest rate on money, which represents the time preference in all goods and services, must always be positive and include an extra margin to ensure savings flows occur. Furthermore, this is the basis for all pricing in financial markets for deferring delivery or settlement, which is called contango. In normal markets, backwardations are always unnatural and temporary, reflecting an excess of demand over supply for an earlier date over a later, but is never a general condition.

Negative interest rates create permanent backwardations

The reason it is vital to grasp the meaning and implications of time preference is to show that negative interest rates are unnatural, and do not accord with human action. It might not be obviously disruptive to financial markets when a central bank, whose currency is not the reserve currency, imposes a relatively minor negative rate on its commercial banks’ reserves. After all, a commercial bank will still charge its borrowers a positive rate, even though it may have to be imaginative when it comes to keeping depositors happy. But this is beginning to change, with both governments and large corporates now being able to issue bonds at negative rates. As we have seen from our discourse on time preference, this is a significant distortion from normality, indicating bond markets expect yet deeper negative rates in the currencies concerned.

In managing interest rates, the assumption central bankers make is that interest is the price of money. This is wrong for the reasons argued above. But instead of realising that deeper negative rates will not promote economic recovery in accordance with a cost of money approach to economic management, central banks’ economic models predict deeper negative rates are necessary in the event that a significant recession materialises.

However, this is new territory for policy makers, and they are naturally cautious about the prospect of deeper negative rates. Deeper negative interest rate policies will almost certainly be preceded or accompanied by quantitative easing, which allows a central bank to anchor term rates and government bond yields at the zero bound or even in negative territory. If the world faces a global recession, monetary expansion is likely to be the only course of action open to central banks, and deeper negative rates will become central to monetary policy if a recession persists.

With the expansionary phase of the credit cycle demonstrably running out of steam, history tells us that not only are we overdue a crisis in bank credit, but the tariff war between China and America will probably synergise with the cyclical downturn in the credit cycle to trigger a slump on a scale not seen since the early 1930s.

That being the case, under our assumptions for economic prospects, deeper negative rates will become unavoidable.The first to explore this dangerous territory are likely to be the ECB, the Swiss National Bank and the Bank of Japan. So far, lending rates at the Fed and the Bank of England are still in positive territory, but faced with an economic slump, that may not persist. The Fed’s interest rate is particularly important, because international financial markets price everything in dollars. And unless the Fed is prepared to see a dollar being strengthened by deepening negative rates elsewhere, the Fed may have little option but to follow.

If the Fed introduces negative dollar rates, then distortions of time preference will take a catastrophic turn. All financial markets will move into backwardation, reflecting negative rates imposed on dollars. Remember, the only conditions where backwardation can theoretically exist in free markets are when there is a shortage of a commodity for earlier settlement than for a later one. Yet here are backwardation conditions being imposed from the money side. It leads us to one conclusion: if negative rates for the dollar are imposed on financial markets, they will almost certainly lead to a flight out of the dollar where deposits become taxed with negative rates, not into other currencies, but into all commodities and future claims upon them. The current situation, where since the 1980s derivatives have inflated commodity supply, thereby suppressing prices, will be reversed. The purchasing power of dollars will be undermined by an attempted flight out of money. And it is unlikely to be long before the difference between negative time preferences between dollars and mildly positive ones for everyday items promotes a similar flight out of retail bank deposits.

That is the black and white of it. But there is a grey area of close to zero rates, when they are less than the implied rate of interest on gold, because of its time preference. Here it should be noted that gold’s interest rate when sterling was on the gold standard generally varied between two and four per cent, using the yield on British Consols as proxy. The Fed fund rate is already testing the lower boundary for monetary gold’s historic time preference, and markets are now expecting the FFR to go lower still.

Negative dollar interest rates and gold

This leads us to consider how a negative dollar interest rate will affect the price of gold. Gold is different from other commodities, because it is also a medium of exchange. And while it may not be commonly used as such in capital markets, it is widely retained by central banks and diverse parties as a monetary store of value.

Gold has a monetary time preference of its own, in accordance with time preference theory. And when gold was money, expressed as such through money substitutes, we know from the British experience in the nineteenth century, gold’s time preference usually held above two per cent, and that was still roughly the case reflected in gold’s lease rate since the 1980s.

In the 1980s gold was increasingly used as the collateral for a carry trade, leading to an explosion in business for the London bullion market. The underlying position was that central banks had accumulated bullion as part of their monetary reserves, and the gold price was generally falling. As bullish conditions died, gold’s time preference fell. Central banks and government treasury departments added to this trend, being prepared to lease their gold in large quantities to specialist banks in the bullion market.

At that time, a bullion bank could lease gold from a central bank and use it as collateral to invest in US Treasury bills. Gold’s time preference was reflected in a lease rate of typically 1.5-2% (though there were some spikes to 3-5%). Lease rates rhymed with evidence of gold’s originary rate established in the nineteenth century.

Meanwhile, 6-month UST bills yielded about 6% or more, giving bullion banks a fat profit over the lease rate. While figures were never published, Frank Veneroso, at that time a leading independent gold analyst, gave a speech in Lima in 2002 estimating central bank gold leases and swaps were between 10,000 and 15,000 tonnes. In other words, up to half of all central bank gold was out on lease or swapped.

Since those days, the London forward market has continued to grow. Bullion banks extended their operations to offer bullion accounts for wealthier individuals around the world, almost entirely on an unallocated basis. Unallocated accounts allow a bullion bank to own the gold deposited with it and to leverage its use as collateral for carry trades and other opportunities of interest rate arbitrage. This market became so developed that insiders have postulated that for every ounce of physical bullion in the possession of bullion banks there could be a hundred of paper liabilities.

We have no way of knowing the true level of paper gold leverage today. A working assumption that actual gearing is closer to between ten or twenty times seems more realistic, given Bank for International Settlements statistics of OTC swaps and forwards and LBMA vaulting statistics, allowing for ETF and other custody holdings, segregated from bullion bank ownership. To this must be added the banks’ unallocated customer account liabilities which go unrecorded. In any event, we can be certain that in recent decades a positive gold lease rate led to a substantial systemic uncovered position, likely to be still institutionalised, given the evidence from the LBMA’s daily clearing statistics.

The dollar interest rate that matters today is the wholesale market rate, USD LIBOR of a term that matches a gold lease. At the time of writing, 12-month USD LIBOR shows at 1.949%. The gold 12-month forward rate is roughly the same, implying the lease rate is zero. Clearly, with gold lease rates reflecting no time preference for gold, its supply into wholesale markets is being severely restricted. Look at it from a central bank’s point of view: if a lease is coming due, there is no incentive to renew it, particularly given the unquantifiable counterparty and systemic risks that may arise in the current global economic climate.

We can conclude that the basis for highly geared interest rate arbitrage by borrowing gold is running into a brick wall. Not only is there no incentive for lessors but also there is also a diminishing appetite for lessees, because the opportunities are vanishing. Synthetic gold liabilities are being gradually reduced, not only by ceasing the creation of new obligations, but by buying bullion to cover existing ones. This will have been particularly the case when the USD yield curve began to invert in recent months (itself a backwardation of time preference), and was the surface reason, therefore, that the gold price moved rapidly from under $1200 to over $1500.

Bullion banks are now faced with the prospect that the Fed will reduce interest rates to zero again, even without a systemic crisis such as Lehman. Traders, who are not often deeply analytical, will almost certainly link gold’s move in the wake of the Lehman crisis, once dollar liquidity concerns subsided, from under $750 to over $1900, with dollar rates being suppressed at the zero bound. If rates return there and LIBOR remains positive, that will be a reflection of systemic risk, not time preference. Meanwhile, gold’s time preference will almost certainly be increasing as markets attempt to discount a new wave of base money expansion when the Fed attempts to stabilise the US economy and manage government finances.

Bullion bank traders can see therefore, the day has arrived when gold’s time preference exceeds that of the dollar by an increasing margin. Furthermore, there is the growing threat of negative dollar rates, as economic conditions deteriorate. Putting other considerations aside, the switch in time preferences suggests a bullion bank’s future trading strategy should be the polar opposite of their current position. Instead of holding a small stock of gold to finance a large dollar position, logically they should maintain a small reserve of dollars to finance a larger position in physical gold.

It is for this reason that not only is the gold price rising, but is likely to continue to rise, appearing to defy all expectations. It is impossible to quantify the extent to which the gold price will rise as the bullion banks scramble to unwind or even reverse their habitual short positions, but if there is a surprise it is likely to be on the upside.

The consequences

As well as being modified by its specific supply and demand conditions, Gold’s time preference is essentially for its moneyness, represented by its use as a medium of exchange and store of value. The moneyness aspect links it to its exchange value for all commodities, and it is this aspect of gold’s qualities that should warn us that a backwardation in gold, emanating from negative dollar interest rates, will herald a general backwardation in commodities as well.

We must not forget that markets anticipate events where they can, so with a recession threatening to turn into a slump and with a looming credit crisis in the wings the prospect of negative rates will be increasingly priced into the relationship between commodities and fiat dollars. Assuming economic prospects darken because of the coincidence of American tariffs and the emerging crisis stage of the credit cycle, it will be check-mate for central banks. They were never appointed nor are they technically equipped to save the currency at the expense of widespread bankruptcies, not just in the private sector, but of their governments as well. And that is what markets will be faced with.

The current situation has striking similarities with the 1930s, and the prospects for the global economy are driven by the same broad factors. With the gold standard then and not now the price effects are already showing differences. Nor was there a bubble of hundreds of trillions of outstanding derivatives then as there are today. This time, the monetary sins since the ending of the Bretton Woods agreement seem set to come home to roost all of a sudden, even if dollar rates are lowered towards zero and only stay there. But if they go negative and the more below zero that they go, the greater the backwardation on the whole commodity complex. The more rapidly commodities will be bought so the dollar, taxed with negative rates can be sold, and the quicker market actors will devalue the currency.

With all other fiat currencies referenced to the dollar, it will mark the start of a process that is likely to collapse the entire fiat currency system. Bullion banks which are too slow to recognise the change and have not shut down their gold obligations will be forced to steal their customers allocated gold, or go to the wall, adding to the disruption. All commodity derivatives will face a period of rapid contraction of open interest, in lockstep or one pace behind those of gold.

Instead of central banks stabilising the system by monetary easing, the easing itself will guarantee the crisis. The development of a problem in gold markets, driving the gold price rapidly higher while some banks are caught napping, is likely to anticipate a wider financial and systemic crisis. Therefore, with gold’s sudden move higher coupled with its persistent strength we can reasonably certain that we are seeing the start of the dismantling of the dollar-based monetary system, and that gold has much further to go.

Ronan Manly: Supposed decline in China gold imports may mask rise in official reserves

Submitted by cpowell on Mon, 2019-09-02 13:51. Section: Daily Dispatches

9:52a ET Monday, September 2, 2019

Dear Friend of GATA and Gold:

Bullion Star gold researcher Ronan Manly today verifies the Chinese gold import data recently reported by Reuters, showing a substantial decline this year, but notes that monetary gold — the gold held in central bank reserves — is exempt from import reporting.

Manly writes: “By adjusting the gold import quotas lower, gold imports could be channeled to the the vault of the central bank, while providing the necessary cover to create the illusion that lower quotas are the culprit for the decline. Given that nobody much believes the official low-ball figures for China’s official gold reserves, stranger things have happened than the Chinese state temporarily diverting some of the country’s gold imports for the coffers of its gold vaults in Beijing.”

…

Indeed, Manly’s speculation is supported by the shallowness and exceedingly brief duration of the usual gold price smashes by government-connected bullion banks in recent months, which suggest that demand for physical has only risen, not declined, and the recent advocacy by a leading Chinese government newspaper of return to some sort of gold standard for currencies:

http://www.gata.org/node/19398

Besides, no financial market is bombarded by more disinformation from manipulators than the gold market, and this disinformation often comes from official sources, their lackeys, and mainstream financial news organizations that never put a critical question to an official source.

Manly’s analysis is headlined “Chinese Gold Imports — Better Data, Lower Inflows, Unanswered Questions” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/chinese-gold-imports-bette…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

Join GATA here:

New Orleans Investment Conference

Hilton New Orleans Riverside Hotel

Friday-Monday, November 1-4, 2019

https://neworleansconference.com/noic-promo/powellgata/

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

end

The rising price of gold is causing sellers to hold out for higher prices: it is squelching Merger and Acquisition activity

(McGee/Globe and Mail/GATA)

Rapidly rising gold price squelching M&A activity

Submitted by cpowell on Mon, 2019-09-02 14:15. Section: Daily Dispatches

By Niall McGee

The Globe and Mail, Toronto

Sunday, September 1, 2019

https://www.theglobeandmail.com/business/article-rapidly-rising-gold-pri…

The big run in gold bullion means potentially higher profits for miners, but investors say the same dynamic is stifling mergers and acquisitions activity, as both buyers and sellers struggle to come to grips with where the commodity price will eventually land.

“When the gold price is rising, it’s going to be hard to get deals done. But if you saw it settle at US$1,500 [an ounce] for five or six months, I think you’d start seeing deals again,” said Jonathan Goodman, chief executive of investment manager Dundee Corp., and chairman of gold-mining company Dundee Precious Metals Inc.

…

After trading sideways for the best part of three years, gold has risen by about 20% in 2019, as investors buy the precious metal as a hedge against macroeconomic troubles, including a global economic slowdown, and geopolitical tremors, such as the continuing trade war between the United States and China. On Friday gold futures traded at around US$1,520 an ounce.

Gold M&A started with a bang this year, with Barrick Gold Corp. closing its zero-premium, US$6-billion acquisition of Randgold Resources Ltd. in January, and Newmont Mining Corp. (now Newmont Goldcorp Corp.) announcing the same month it was scooping up Vancouver’s Goldcorp Inc. for US$10 billion.

However, since then, just a handful of deals have been announced, including Australia’s St. Barbara Ltd. buying Vancouver-based Atlantic Gold Corp. for $722 million in May, and Toronto-based Kinross Gold Corp. purchasing a Russian gold development project for US$283 million in July.

There is no shortage of large-scale gold deals waiting to happen. The world’s two largest gold companies, Barrick and Newmont, have indicated they are willing to sell around US$3 billion collectively in non-core mines over the next few years as they concentrate on whittling down their vast portfolios to the most profitable and longest-life mines.

Last month Barrick said it was starting a process to sell its 50% stake in its Kalgoorlie mine in Australia. Barrick CEO Mark Bristow also told The Globe and Mail he was prepared to sell its Massawa gold development project in Senegal.

Newmont’s management hasn’t been as explicit about naming assets, but analysts have pointed to the company’s Red Lake and Porcupine mines, both formerly Goldcorp assets, and both in Ontario, as likely to be sold.

The rising gold price means that sellers can likely demand more than they would have a few months ago.

“Everybody gets stars in their eyes,” Mr. Goodman said.

“The deals we saw earlier in the year were these low-premium deals. Now that we’ve got a [strong] gold market again, people are going to be looking for a premium.”

For the most part the Newmont and Barrick mines for sale are high cost with low reserves, but that doesn’t mean there won’t be willing buyers.

Benoit Gervais, precious-metals portfolio manager with MacKenzie Investments, says Australian miners Evolution Mining Ltd. and Northern Star Resources Ltd. have proven themselves to be deft turnaround artists in such scenarios, acquiring underperforming mines and eventually making them profitable again. As examples he points to Evolution’s 2015 acquisition of the Cowal mine from Barrick for US$550 milllion and Northern Star’s 2018 acquisition of the Pogo mine from Japan’s Sumitomo for US$260 million.

While Mr. Gervais sees the potential for many individual asset deals, he doesn’t foresee a lot of transactions involving gold companies buying their competitors outright. Those deals tend to be costlier, riskier, and much harder to nail down, with discussions often dragging on over who the management and board of the new company should be.

“Whether you are Australian or Canadian, before you go out and try to buy another company, it’s much simpler to buy an asset,” he said. “You can buy exactly what you want rather than the whole package.”

end

Grant Williams is one smart cookie and a good reason to go to New Orleans and here him talk

(GATA)

Another big reason to join GATA in New Orleans: Real Vision’s Grant Williams

Submitted by cpowell on Mon, 2019-09-02 14:40. Section: Daily Dispatches

10:40a ET Monday, September 2, 2019

Dear Friend of GATA and Gold:

Here’s another big reason to join GATA at the New Orleans Investment Conference during the first four days in November.

Market analyst, financial letter writer, fund manager, and Real Vision co-founder Grant Williams has just been added to the speaker lineup.

Williams’ work is often sensational, as it was with his presentation to the Stansberry Alliance Conference in Las Vegas last year, a presentation he titled “Cry Wolf,” which likened the ecology of nature to the ecology of the world economy. Meddling with one part of it, Williams showed, can have terrible effects throughout the whole of it.

In “Cry Wolf” Williams argued that the removal of the golden anchor of the world financial system in 1971 de-industrialized and financialized the economy of the United States and gave supreme power to bankers.

That presentation is still as compelling as ever and remains posted in the clear at Real Vision here:

https://www.realvision.com/grant-william-keynote-speech

GATA Chairman Bill Murphy and your secretary/treasurer again will be speaking at the conference as well, and in the letter below the conference’s organizer, Gold Newsletter Editor Brien Lundin, explains why you should join us there.

The New Orleans Investment Conference is probably the most serious financial conference in the United States, even as it is held in what may be the country’s most fun and interesting city. Because of the conference, your secretary/treasurer has been there many times and always looks forward to returning for the beauty, history, food, and atmosphere of the place.

…

Indeed, the city itself competes heavily with the conference for your attention, so if you’re able, it’s good to give yourself an extra couple of days there.

The New Orleans conference has a long history of concentration on the monetary metals, and now that infinite money and devaluation have broken out among central banks and the monetary metals are on the verge of regaining their rightful places in the world financial system, this year more than ever New Orleans will be where gold and silver investors will want to be.

Registration for the conference entails a substantial expense, but as Brien explains below, if you register quickly you’ll enjoy a serious discount along with extra services at no extra cost and a money-back guarantee in case you don’t profit from attending.

Additionally, if you register using the internet link at the bottom of Brien’s letter, the conference will kindly pay a commission to GATA, which will diminish our fundraising appeals in the future.

So please consider joining us in New Orleans.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

We have been highlighting this to you on a daily basis through the biggest of all EFT’s: the GLD/SLV

(Pakiam/Bloomberg/GATA)

Growth in gold ETFs in August was biggest since 2013

Submitted by cpowell on Mon, 2019-09-02 14:49. Section: Daily Dispatches

All those investors shooting themselves in the foot, facilitating the shorting of what they want to rise in price.

* * *

Investors Rush Into Gold

By Ranjeetha Pakiam

Bloomberg News

Monday, September 2, 2019

Investors are going for gold in a big way. Inflows into bullion-backed exchange-traded funds topped 100 tons in August to hit the highest since February 2013 as the trade war worsened, risk assets took a knock, and central banks signaled looser monetary policy.

Holdings rose 101.9 tons, bringing total known assets to 2,453.4 tons as of Friday, according to data compiled by Bloomberg. It was the third straight monthly increase after the addition of a combined 154.1 tons in June and July.

…

.Bullion has been on a tear, gaining 19% this year, as the global outlook worsened on the standoff between the U.S. and China. Central bank buying has provided another layer of support, and Goldman Sachs Group Inc. says prices are likely to advance further as official purchases continue and demand for ETFs rises. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-09-02/gold-etfs-surge-more-…

* * *

end

Two extra reasons to help GATA by subscribing to The Calandra Report

Submitted by cpowell on Mon, 2019-09-02 15:05. Section: Daily Dispatches

11:05a ET Monday, September 2, 2019

Dear Friend of GATA and Gold:

Two bonuses now await GATA supporters who help us by subscribing to Thom Calandra’s financial letter, The Calandra Report.

Those who subscribe by this Thursday will receive not only Thom’s basic report but also:

— His frequent TCR Collateral missives, which include material from his notebook about financial people, companies, and commodities.

— A special recent issue of The Calandra Report that identifies what Thom believes are substantially undervalued gold, silver, and copper mining companies and a rising biomedical company with a promising new drug.

…

Thom’s generous offer to GATA supporters is to split with GATA their one-year subscription fee of $169. That is, for each GATA supporter who subscribes, Thom will contribute $85 to GATA.

Now that the monetary metals seem to be breaking out of their central bank chains, companies that produce gold, silver, and other strategic resources are starting to draw investment again, making The Calandra Report of interest even to the most demoralized followers of the monetary metals.

A note from Thom explains below.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

Hello Alpha-GATAs. I have supported GATA since the early 2000s. Over the years GATA Chairman Bill Murphy, GATA Secretary/Treasurer Chris Powell, and I have shared ideas, panel appearances, and even a drink or three.

I’d like you to join The Calandra Report community. It’s been going since 2011, and since 1998 for MarketWatch.com, which I co-founded.

Here’s a small biography:

https://thomcalandra.com/about-thom-calandra/

Here’s a subscription offer exclusively for GATA supporters, like the offer we made last year.