GOLD:$1508.20 UP $2.70 (COMEX TO COMEX CLOSING)

Silver:$17.90 DOWN 12 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1505.50

silver: $17.84

Definition of Rico

RICO is typically used to indict mobsters – which makes its use against employees of the largest bank in America a very disquieting event. But even more disquieting is that two trial lawyers compared JPMorgan Chase to the Gambino crime family five long years ago and recommended in their 2016 book that the bank’s officers be prosecuted under the RICO statute.” … Pam Martens and Russ Martens

Ted Butler….

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 2/19

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,504.600000000 USD

INTENT DATE: 09/25/2019 DELIVERY DATE: 09/27/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 9

661 C JP MORGAN 2

685 C RJ OBRIEN 1

686 C INTL FCSTONE 1

690 C ABN AMRO 7 1

737 C ADVANTAGE 2 6

905 C ADM 9

____________________________________________________________________________________________

TOTAL: 19 19

MONTH TO DATE: 1,770

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 19 NOTICE(S) FOR 1900 OZ (0.0590 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1770 NOTICES FOR 177000 OZ (5.5054 TONNES)

SILVER

FOR SEPT

18 NOTICE(S) FILED TODAY FOR 90,000 OZ/

total number of notices filed so far this month: 8680 for 43,400,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

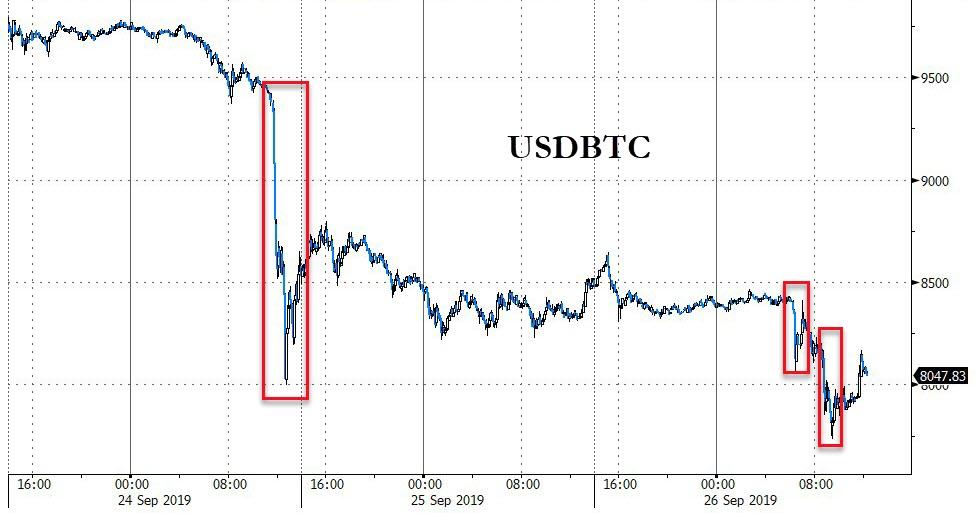

Bitcoin: OPENING MORNING TRADE : $ 8391 DOWN 41

Bitcoin: FINAL EVENING TRADE: $ 8104 DOWN 311

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A SHOCKING 1186 CONTRACTS FROM 215217 UP TO 216,403 DESPITE THE HUGE 56 CENT LOSS IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR SEPT 0,; DEC 1601 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1601 CONTRACTS. WITH THE TRANSFER OF 1601 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1601 EFP CONTRACTS TRANSLATES INTO 8.005 MILLION OZ ACCOMPANYING:

1.THE 56 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.400 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

YESTERDAY, THERE WAS A MAJOR ATTEMPT BY THE BANKERS TO COVER THEIR MASSIVE SHORTFALL AT THE SILVER COMEX. OUR OFFICIAL SECTOR//BANKERS AGAIN USED COPIOUS NON BACKED PAPER IN THEIR SUCCESSFUL ENDEAVOUR TO LOWER SILVER’S PRICE IN ORDER TO MAKE UNDERWRITTEN COMEX CONTRACTS NULL AND VOID. HOWEVER TO THEIR SHOCKING SURPRISE, NOBODY LEFT THE SILVER COMEX ARENA AS NOT ONLY DID THE COMEX OI RISE (1067 CONTRACTS) BUT ALSO A HUGE GAIN IN EFP ISSUANCE (1601 EFP’S). TOTAL GAIN A HUGE 2668 CONTRACTS WITH THAT MASSIVE PRICE HIT OF 56 CENTS. OUR OFFICIAL SECTOR/BANKER FRIENDS WERE NOT AMUSED WITH THIS.

THE LIQUIDATION OF COMEX OI OF SPREADERS HAVE STOPPED AND WE WILL NOW COMMENCE WITH THE ACCUMULATION PHASE OF SPREADERS GOLD OPEN INTEREST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

30,957 CONTRACTS (FOR 18 TRADING DAYS TOTAL 30,957 CONTRACTS) OR 154.78 MILLION OZ: (AVERAGE PER DAY: 1719 CONTRACTS OR 8.599 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 154.78 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 22.11% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1704.39 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

RESULT: WE HAD A SURPRISINGLY STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1186, DESPITE THE 56 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 1601 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED AN ATMOSPHERIC SIZED: 2787 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1601 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1186 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 56 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $18.02 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.082 BILLION OZ TO BE EXACT or 154% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 18 NOTICE(S) FOR 90,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.400 MILLION OZ//

- THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE . TODAY THE CROOKS STARTED THEIR LIQUIDATION OF SPREADING ACTIVITY

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE COMEX OPEN INTEREST FELL BY A HUGE 24997 CONTRACTS, TO 633,947 WITH THE HUGE $26.90 PRICING LOSS WITH RESPECT TO COMEX GOLD PRICING (RAID)// YESTERDAY// / HOWEVER THE MAJORITY OF THE LOSS IN COMEX OI CAME FROM THE LIQUIDATION OF SPREADERS. I WOULD ALSO LIKE TO POINT OUT THE HUGE DIFFERENCE BETWEEN THE PRELIMINARY NUMBERS AND FINAL NUMBERS SOMETHING THAT THE cftc REFUSES TO ADDRESS!!

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUMONGOUS SIZED 16,161 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 16,161 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 633,947,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC AND CRIMINALLY SIZED LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8836 CONTRACTS: 24947 CONTRACTS DECREASED AT THE COMEX (MOSTLY SPREADERS) AND 16161 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 8836 CONTRACTS OR 8836 OZ OR 27.48 TONNES. YESTERDAY WE HAD A LOSS OF $26.90 IN GOLD TRADING….

AND WITH THAT HUGE LOSS IN PRICE, WE HAD A HUMONGOUS LOSS IN GOLD TONNAGE OF 27.48 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON AS THE COMEX GOLD VOLUME AND OPEN INTEREST ARE HUGE. THEY WERE SUCCESSFUL IN THEIR ATTEMPT TO FLEECE SOME LONGS AS ONE OF THEIR FUNCTIONS WAS TO MAKE UNDERWRITTEN COMEX CONTRACTS NULL AND VOID. THE CME PRELIMINARY NUMBERS WERE A TINY LOSS AND THE FINAL NUMBER A HUGE 24,997 LOSS. THE DIFFERENTIAL WAS A GIGANTIC 20,662. THE MAJORITY OF THE LOSS WAS DUE TO THE SPREADERS ILLEGALLY LIQUIDATING THEIR CONTRACTS AT DIFFERENT TIMES OF THE DAY YESTERDAY MAGNIFYING THE ATTACK SOMETHING THAT THESE CROOKS DO AT EVERY UPCOMING ACTIVE DELIVERY MONTH WHETHER IT IS GOLD OR SILVER. THE CFTC REFUSE TO ANSWER ANY QUESTIONS ADDRESSED TO THEM ON THIS OBVIOUS CRIMINAL ACTIVITY (THIS ACTIVITY HAS BEEN ALSO HIGHLIGHTED IN BRIEFS SUBMITTED TO THE FCA IN LONDON.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 143,552 CONTRACTS OR 1,4355,200 oz OR 446.50 TONNES (18 TRADING DAY AND THUS AVERAGING: 7975 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAYS IN TONNES: 446.50 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 446.50/3550 x 100% TONNES =12.57% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4598.59 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A LARGER THAN EXPECTED DECREASE IN OI AT THE COMEX OF 24,997 WITH THE HUGE PRICING LOSS THAT GOLD UNDERTOOK YESTERDAY($26.90)) //.WE ALSO HAD A HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 16,161 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 16,161 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC AND CRIMINALLY SIZED LOSS OF 8836 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

16,161 CONTRACTS MOVE TO LONDON AND 24,997 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE LOSS IN TOTAL OI EQUATES TO 27.48 TONNES). ..AND THIS HUGE DECREASE OF DEMAND OCCURRED DESPITE THE HUGE LOSS IN PRICE OF $26.90 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 19 notice(s) filed upon for 1900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $2.70 TODAY//(COMEX-TO COMEX)

NO CHANGE IN GOLD INVENTORY AT THE GLD.

INVENTORY RESTS AT 924.94 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 12 CENTS TODAY: WOW!!!

SOMETHING MUST BE BREWING: WE HAD A HUGE PAPER DEPOSIT OF 3.975 MILLION OZ DESPITE TWO DAYS OF LOSSES IN PRICE

NO CHANGES IN SILVER INVENTORY AT THE SLV//

/INVENTORY RESTS AT 381.786 MILLION OZ.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A SURPRISINGLY STRONG SIZED 1186 CONTRACTS from 215,217 UP TO 216,403 AND CLOSER TO A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR SEPT. 0; FOR DEC 1601: AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1601 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1067 CONTRACTS TO THE 1601 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 2787 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 13.34 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ// AND FINALLY SEPT: 43.400 MILLION OZ//

RESULT: A SURPRISINGLY STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE HUGE 56 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1601 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 26.35 POINTS OR 0.89% //Hang Sang CLOSED UP 96.58 POINTS OR 0.37% /The Nikkei closed UP 28.09 POINTS OR 0.13%//Australia’s all ordinaires CLOSED DOWN .43%

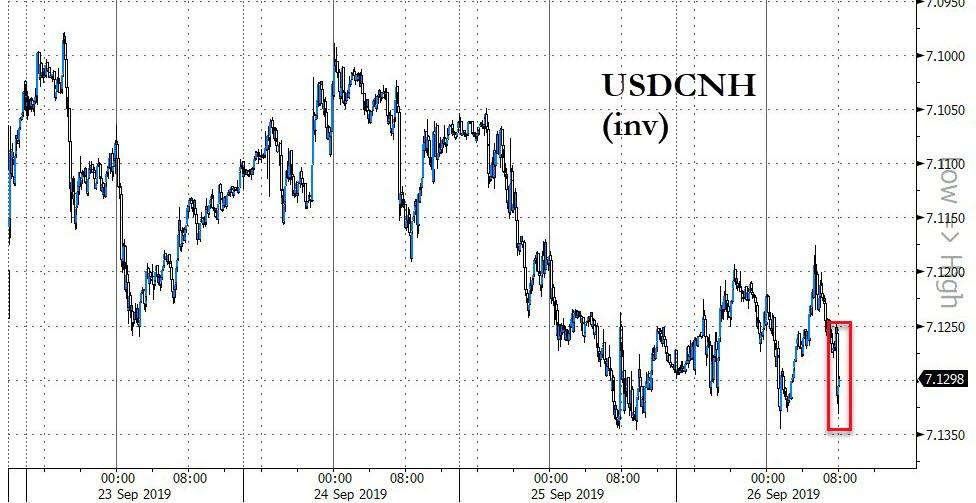

/Chinese yuan (ONSHORE) closed DOWN at 7.1300 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1300AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1238 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

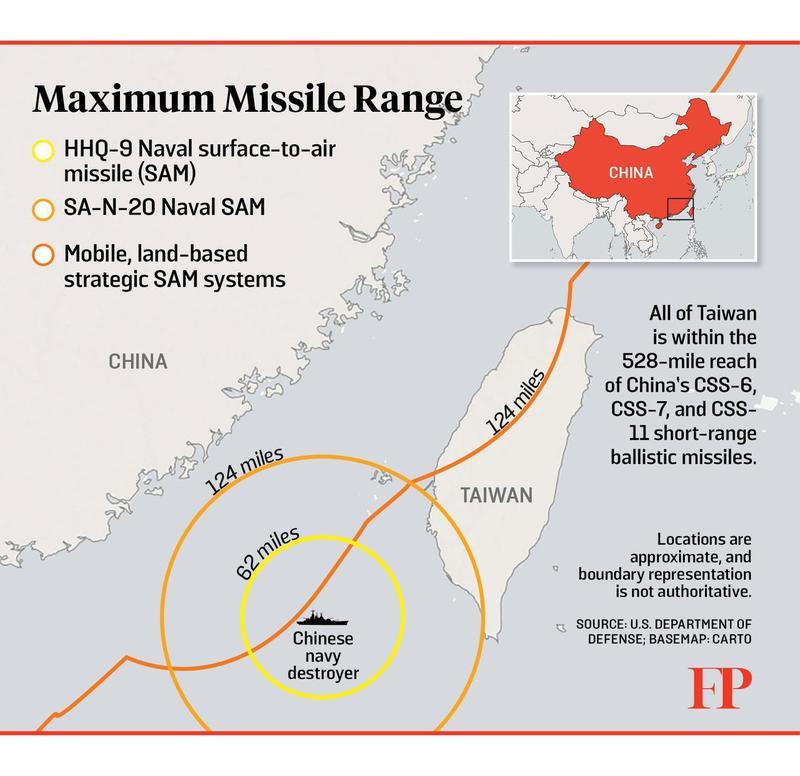

a(This is interesting: China launches a new attack ship which is capable of invading Taiwan

(zerohedge)

b)China/USA

4/EUROPEAN AFFAIRS

Netherlands/ABN Amro

Another Bank being investigated in Holland for money laundering and terrorism financing

(zerohedge)

7. OIL ISSUES

The oil and gas shale industry in deep anxiety due to a low price and losses on their balance sheet. A survey indicates a capex collapse is imminent.

(Nick Cunningham/OilPrice.com)

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

Yao and Sin, writing for Reuters believes that China has allowed its yuan to weaken and this is causing much anger with Trump

(Yao//Sin///Reuters/Gata/

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

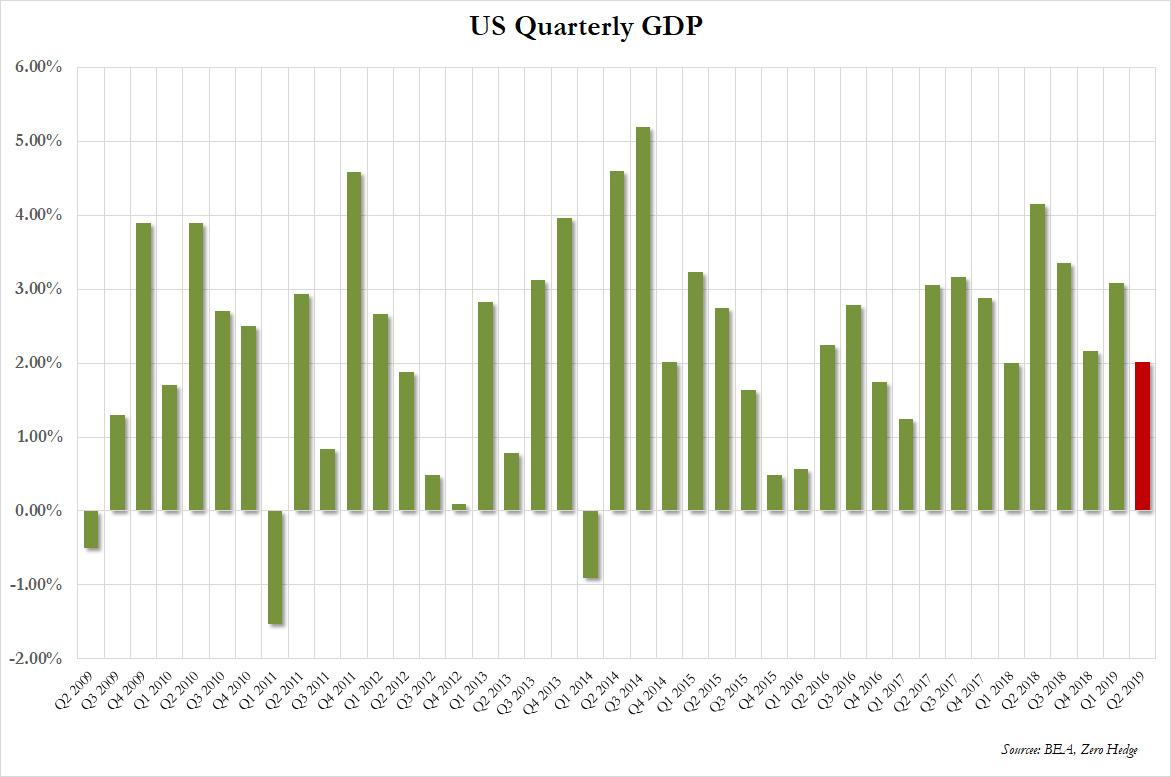

i)Final Q2 GDP revision is unchanged at 2% despite profit growth shrinking

(zerohedge)

ii)Final Q2 GDP revision is unchanged at 2% despite profit growth shrinking

(zerohedge)

iii)Trump still not getting anywhere with his tariffs. The trade deficit actually widened

iii) Important USA Economic Stories

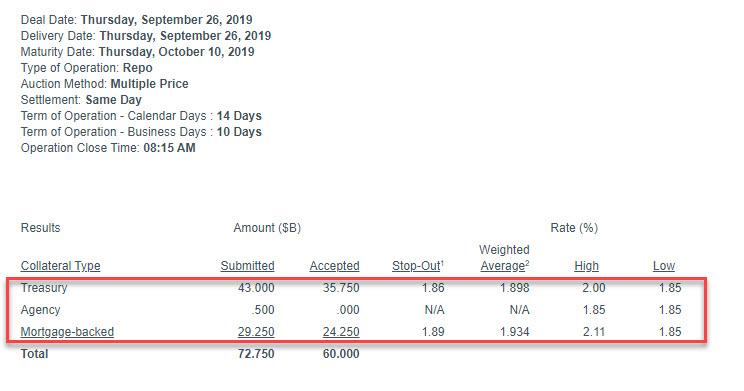

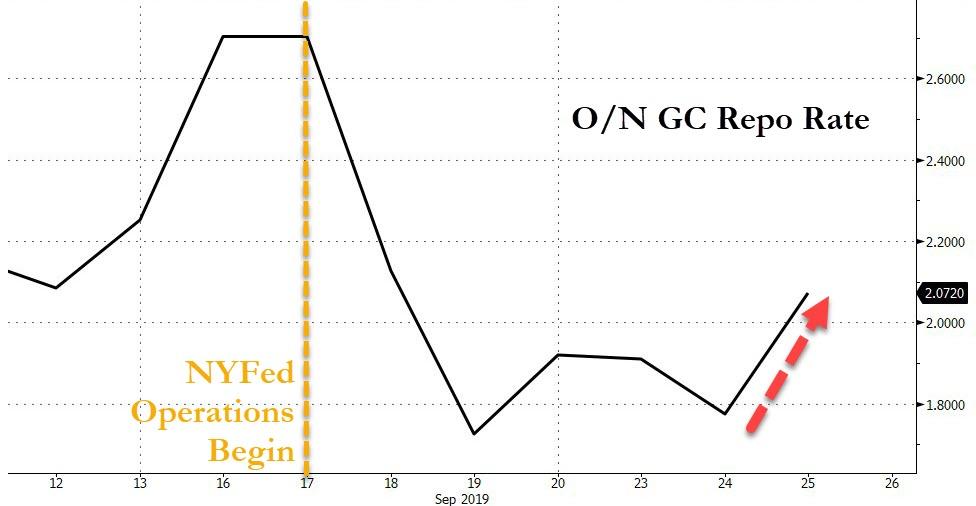

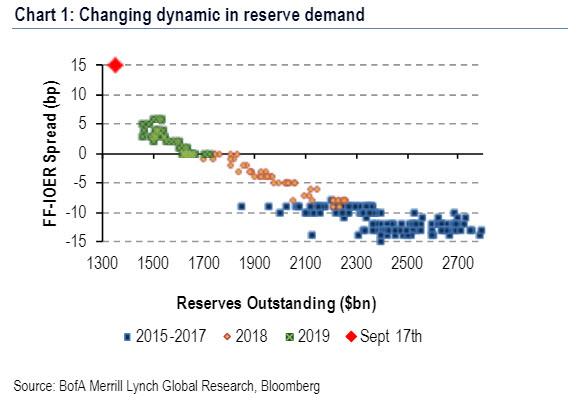

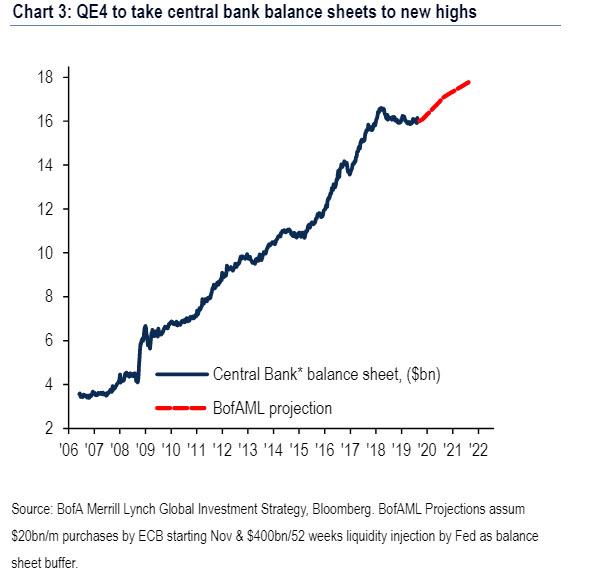

a)We now have results of the 2nd Term Rep and it was terribly oversubscribed as the funding shortage keeps getting worse. knows why..Pam and Russ Martens are pounding the table that Deutsche bank plus two other banks have a severe funding shortage. We know that Deutsche bank is massively short silver and that may be the reason for the continual repo money thrown at the bank.

(zerohedge)

b)Yesterday after the close, the Fed doubles the allotment of Rep money. If fully subscribed it will pump in a huge 1/4 trillion dollars into the system. It sure looks like Deutsche bank is causing massive headaches for the global finances

(zerohedge)

c)Brandon Smith offers his view that the Fed is deliberately pricking the bubble and wants a crash.

iv) Swamp commentaries)

a)Acting DNI denies that he stated he would resign over the Trump phone call

(zerohedge)

b)This morning: an absolute joke… the whistleblower complainant only heard about the stuff through others

(zerohedge)

c)Michael Snyder delves into the phony Ukrainian hoax

d)Seems that this whistleblower had help and everything was contrived

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

THE BANKERS SUPPLIED THE NECESSARY AND INFINITE AMOUNT OF SHORT PAPER IN GOLD. THE BANKERS SUCCEEDED IN LOWERING GOLD’S PRICE BY A HUGE LOSS OF $26.90. THE ILLEGAL ACTIVITY OF THE SPREADING LIQUIDATION MAGNIFIED THE LOSSES AT THE COMEX. I CAN ASSURE YOU THAT THE LONGS THAT PICKED UP CHEAP CONTRACTS WILL TURN THAT PAPER INTO REAL METAL.

we had 0 dealer entry:

We had 1 kilobar entries

total gold withdrawals; 160.75 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 106,838 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 136,964 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 136,964 CONTRACTS EQUATES to 684 million OZ 97.7% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.25% ((SEPT 25/2019)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.15% to NAV (SEPT 25/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -1.25%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.12 TRADING 14.64///DISCOUNT 3.16

END

And now the Gold inventory at the GLD/

SEPT 26//WITH GOLD UP $2.70 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.94 TONNES

SEPT 25/WITH GOLD DOWN $26.90 A HUGE PAPER DEPOSIT OF: 16.42 TONNES//INVENTORY RESTS AT 924.94 TONNES

SEPT 24/WITH GOLD UP $8.65 TODAY: A MONSTROUS CHANGE IN GOLD INVENTORY AT THE GLD: AN OUT OF THIS WORLD DEPOSIT OF 14.37 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 894.15 TONNES

SEPT 23/WITH GOLD UP $16.25 ON THE DAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER ADDITION OF 10.65 TONNES//INVENTORY RESTS AT 894.15 TONNES

SEPT 20/WITH GOLD UP $8.60 ON THE DAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 883.06 TONNES

SEPT 19/WITH GOLD DOWN $8.90 TODAY: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 3.23 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 883.60 TONNES

SEPT 18/WITH GOLD UP $2.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 5.86 TONNES/INVENTORY RESTS AT 880.37 TONNES

SEPT 17/WITH GOLD UP $1.50: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 874.51 TONNES

SEPT 16/WITH GOLD UP $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 5.86 TONNES FROM THE GLD///INVENTORY RESTS AT 874.51 TONNES

SEPT 13/WITH GOLD DOWN $7.75 TODAY: A BIG PAPER WITHDRAWAL OF 2.05 TONNES FROM THE GLD/INVENTORY RESTS AT 880.37 TONNES

SEPT 12//WITH GOLD UP $4.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 11/WITH GOLD UP $5.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 10/WITH GOLD DOWN $11.75 TODAY: A HUGE 7.33 PAPER TONNES OF GOLD WAS WITHDRAWN FROM THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 9/WITH GOLD DOWN $4.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 889.75 TONNES

SEPT 6//WITH GOLD DOWN $9.80: A BIG CHANGE IN GOLD INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 6.15 TONNES//INVENTORY RESTS AT 889.75 TONNES

SEPT 5/WITH GOLD DOWN $33.80 TODAY: A BIG ADDITION (DEPOSIT) OF 5.86 OF PAPER GOLD TONNES PROBABLY ADDED BEFORE THE RAID/EXPECT A HUGE PAPER WITHDRAWAL TOMORROW: INVENTORY RESTS AT 895.90 TONNES

SEPT 4/WITH GOLD UP $5.00 TODAY: A BIG CHANGE: A HUGE PAPER DEPOSIT OF: 11.73 TONNES/INVENTORY RESTS AT ….890.04 TONNES

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

AUGUST 22.WITH GOLD DOWN $6.80 TODAY: TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD: I)A PAPER DEPOSIT OF 6.74 TONNES INTO THE GLD (LATE YESTERDAY EVENING) AND 2) A PAPER DEPOSIT OF 2.93 TONNES LATE THIS AFTERNOON./INVENTORY RESTS AT 854.84 TONNES

AUGUST 21/WITH GOLD DOWN $.30 TODAY:A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.76 TONNES INTO THE GLD INVENTORY/GOLD INVENTORY RESTS AT 845.17 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SEPT 26/2019/ Inventory rests tonight at 924.94 tonnes

*IN LAST 669 TRADING DAYS: 24.22 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 569- TRADING DAYS: A NET 142.43 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 26/WITH SILVER DOWN 12 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.975 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 381.786 MILLION OZ/

SEPT 25.//WITH SILVER DOWN 58 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 377.811 MILLION OZ//

SEPT 24/WITH SILVER DOWN 5 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.338 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 377.811 MILLION OZ//

SEPT 23.2019/WITH SILVER UP 80 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 375.473 MILLION OZ.

SEPT 20/ WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 375.473 MILLION OZ.

SEPT 19/WITH SILVER DOWN 4 CENTS TODAY; A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 1.029 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 375.473 MILLION OZ/

SEPT 18/WITH SILVER DOWN 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 17/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 16/WITH SILVER UP 41 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A PAPER WITHDRAWAL OF 2.899 MILLION OZ OF SILVER LEAVES THE SLV///INVENTORY RESTS AT 376.502 MILLION OZ/

SEPT 13/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 12/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 11/WITH SILVER DOWN ONE CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 10/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 1.778 MILLION PAPER OZ OF SILVER///INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 9/WITH SILVER DOWN 6 CENTS TODAY: A MAMMOTH CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 5.425 MILLION PAPER OZ/INVENTORY RESTS AT 381.179 MILLION OZ../

SEPT 6/WITH SILVER DOWN ANOTHER 60 CENTS TODAY: A RATHER TIMID CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 842,000 PAPER OZ FROM THE SLV///INVENTORY RESTS AT 386.604 MILLION OZ//

SEPT 5/WITH SILVER WHACKED 68 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 4/WITH SILVER UP 28 CENTS TODAY:STRANGE!! A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 708,000 OZ FROM SLV’S INVENTORY:/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 TONNES

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.696 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 21/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

SEPT 26/2019:

Inventory 381.786 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.15/ and libor 6 month duration 2.04

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .11

XXXXXXXX

12 Month MM GOFO

+ 2.01%

LIBOR FOR 12 MONTH DURATION: 1.99

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -.01

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

World’s Largest Gold ETF Sees Holdings Rise 1.8% to 924.94 Tonnes In One Day

◆ Gold prices have inched 0.3% higher today as a sharp drop of nearly 2% yesterday has attracted bargain hunters

◆ Gold tested support at $1,500/oz after another peculiar sell off in the futures market saw prices fall $30 in two hours on the COMEX yesterday with most of the selling coming after European and London markets had closed

◆ The sell off came despite robust demand for gold globally as seen in the world’s largest gold ETF seeing yesterday, in just one day, its holdings rise 1.81% to 924.94 tonnes

◆ The smart money continues to diversify into gold due to the concerns about the outlook for risk assets

◆ Prudent money is moving to the safety of fully segregated gold coin and bar ownership outside of large debtor nations and the vulnerable global banking system (see Jim Rogers interview below)

NEWS and COMMENTARY

Gold gains ground on bargain hunting, stronger dollar caps gains

Gold falls 1.8% on firmer dollar, U.S. stock gains

Asian stocks give up gains as U.S.-China optimism fades

Trump says trade deal with China could happen sooner than people think

Asian stocks gain as Trump says China trade deal could be ‘soon’

Trump says impeachment inquiry could derail trade deal, Mexico markets slump

Wall Street believes Trump is safe but worries impeachment inquiry could hinder trade deals

Eco ‘gold mine of the future’ has arrived in Canada

GOLD vs. PAPER MONEY: Production Cost Is A Good Indicator Of Real Value

Gold backing off, chart does not look overly bearish – Ira Epstein Update

Gold Prices (LBMA – USD, GBP & EUR – AM/ PM Fix)

25-Sep-19 1530.85 1528.75, 1231.11 1234.62 & 1391.24 1391.77

24-Sep-19 1520.25 1520.65, 1220.76 1216.67 & 1382.36 1381.36

23-Sep-19 1519.50 1522.10, 1222.13 1225.90 & 1385.48 1385.11

20-Sep-19 1504.10 1501.90, 1199.07 1203.62 & 1361.06 1362.52

19-Sep-19 1498.40 1500.70, 1200.67 1201.76 & 1354.85 1357.08

18-Sep-19 1502.20 1503.50, 1206.27 1204.90 & 1360.39 1359.92

17-Sep-19 1499.30 1502.10, 1208.89 1207.24 & 1361.51 1360.45

16-Sep-19 1502.05 1497.20, 1207.35 1203.30 & 1357.25 1359.46

13-Sep-19 1506.30 1503.10, 1209.41 1208.19 & 1356.88 1358.35

12-Sep-19 1502.95 1515.20, 1219.94 1227.46 & 1362.88 1373.53

11-Sep-19 1493.65 1490.65, 1208.21 1209.07 & 1354.74 1355.90

Source: Bloomberg via James Henry Anderson @jameshenryand

Jim Rogers: Buy Gold Coins and Silver Coins as Global Crisis Is Coming – Watch here

ii) Important gold commentaries courtesy of GATA/Chris Powell

Yao and Sin, writing for Reuters believes that China has allowed its yuan to weaken and this is causing much anger with Trump

(Yao//Sin///Reuters/Gata/

Its leash lengthened, China’s yuan flirts with trade war role

Submitted by cpowell on Thu, 2019-09-26 13:22. Section: Daily Dispatches

By Kevin Yao and Noah Sin

Reuters

Thursday, November 26, 2019

China, having let the yuan cross the once-sacred red line of 7 per dollar, will allow its currency to fall further and may even risk U.S. anger by using it as a bargaining chip in already thorny trade talks, market participants believe.

Beijing had kept the yuan on the strong side of 7 since 2008, so effectively abandoning that trading floor on Aug. 5 triggered intense investor activity.

The currency’s 3.8% decline in August as a whole was its sharpest monthly fall in 25 years, prompting U.S. President Donald Trump to launch a fresh salvo in the more than 15-month tariff war by labeling China a currency manipulator.

While the central bank denies that charge, its attempts this month to smooth the yuan’s weakening suggest the currency’s fluctuations are not entirely unsupervised. …

… For the remainder of the report:

https://www.reuters.com/article/us-china-markets-yuan/its-leash-lengthen…

* * *

Join GATA here:

New Orleans Investment Conference

Hilton New Orleans Riverside Hotel

Friday-Monday, November 1-4, 2019

end

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Futures Reverse Drop, Rise On Renewed “Trade Optimism”

Yesterday we predicted that looking to today’s overnight market wrap headline, it would be one of two choices:

zerohedge@zerohedgeTomorrow market open headline cointoss:

“Futures rise as trade deal hopes buoy risk”

Or

“Futures fade as trade deal hopes dim”

A few hours later, that’s exactly what happened because after an initial modest dip in S&P futures during a mixed Asian session where Trump’s impeachment process sparked some concerns, risk swiftly rebounded once Europe opened for trading, with Reuters chiming in this morning right on cue:

“U.S.-China trade optimism lifts stocks”…

… after China’s MOFCOM sounded constructive, saying the two sides are “closely communicating and preparing for making trade talk progress in October.” Commenting on this, Reuters said that “positive noises from China on U.S. trade talks lifted European stocks on Thursday and snuffed out a modest rally in safe-haven assets that had dominated in Asia.” Because almost a year and a half after the trade war started with no possibility of ending soon, all it takes to still fool the algos is hope, which in turn has pushed global market into a sea of green.

As a result, after some initial weakness, S&P 500 futures turned higher, pointing to more gains on Wall Street after Wednesday’s solid gains which trampled over any concerns over a Trump impeachment. The dollar was unchanged after soaring the most since March the previous day, while gold rebounded back over $1,500 after Wednesday plunge. The pound weakened amid rising acrimony among politicians as the U.K. limps toward Brexit.

Trading started off on the back foot, with Asian markets struggling for direction. MSCI’s broadest index of Asia-Pacific shares outside Japan and Japan’s Nikkei both ended fractionally higher after Japanese Prime Minister Shinzo Abe and Trump signed a limited trade deal on Wednesday, one which excluded autos. But major China tech stocks slumped more than 3% for the second day running after the PBOC drained a net 100bn in liquidity, and Australian shares fell 0.5% while gold tiptoed higher in a sign that some investors were still searching out safety.

This cautious mood reversed however once Europe opened: Europe’s main bourses initially stuttered but muscled 0.5% higher when China said it was in close communication with Washington and preparing to make progress in upcoming trade talks. President Trump had also stoked hopes when he told reporters the two sides were having “good conversations” and that an agreement “could happen sooner than you think”.

Europe’s Stoxx 600 jumped 0.7%, reversing much of yesterday’s sharp drop, with all but two industry groups in the green. Tech stocks, among the biggest losers on Wednesday, lead gains on Thursday. Industrial goods and auto shares also outperform, while banks are worst performers

As they bought stocks, investors dumped European government bond holdings, as the third German resignation from the European Central Bank’s board in recent years overnight also amplified doubts around the sustainability its stimulus measures; that said the move was not too dramatic and 10-year yields rose no more that 2 basis point across the region,, and the major currencies barely budged too, “having now got used to the constant tooing and froing of the year-long trade war” as Reuters put it.

Ironically just a day earlier, trade war odds seemed to spike after Trump sharply criticized China in a speech at the United Nations General Assembly, where he said he would not accept a “bad deal”.

“I think the trade talks will take years if it ever has a solution,” Makor Capital Markets strategist, Stéphane Barbier de la Serre, correctly concluded. “To me, what we see (today) is just market expectations, it is purely micro management of the market, nothing else. We have nearing a point where nobody cares about the discussions.”

Meanwhile, transcripts of a call showed Trump had nudged Ukraine’s president for possible information on presidential rival Joe Biden, but it was hardly the quid-pro-quo picture painted previously by Democrats who are frothing at the mouth to impeach Trump no matter the cost. Traders however remained skeptical about the likelihood of Trump being officially impeached.

In a late Wednesday report, an adviser to Ukraine’s President said President Trump’s insistence for the two leaders to discuss a possible investigation into Joe Biden was a precondition for their July 25 phone call, while it was also reported the Whistleblower’s complaint against US President Trump has been declassified and could be releases as early as Thursday morning according to sources.

In FX, the sidewinding dollar was still well within reach of a 2-year high having also shrugged off the latest controversy surrounding Trump. The Bloomberg Dollar spot index stabilized as the greenback was supported by month- and quarter-end flows, while Treasuries advanced. The yen rose amid persisting political turmoil in U.S. and the U.K. and as trade sentiment remained mixed. Sterling extended Wednesday’s drop, reversing an early gain, while the kiwi led gains among Group-of-10 currencies after RBNZ central bank Governor Adrian Orr said authorities are unlikely to need ‘unconventional’ monetary-policy tools.

Elsewhere in the region the Philippines joined the army of global central banks which have cut interest rates this month, with a 25 basis point trim to 4% Mexico could slice its 8% rates but a similar amount later too.

In other central bank news, Fed’s Kaplan (non-voter, dove) said he feels current policy setting is on the margin of being a little accommodative, while he is agnostic on whether or not more cuts are required and is keeping an open mind. Furthermore, Kaplan said the odds of a recession within next 12 months are relatively low and that repo problems last week show a need for more liquidity but are not sign of broader stress.

In commodities, oil prices swung in and out of the red meanwhile with Brent fetching $62.52 per barrel and U.S. crude at $56.50 a barrel.

Expected data include GDP and wholesale inventories. Carnival and Micron are among companies reporting earnings.

Market Snapshot

- S&P 500 futures up 0.2% to 2,991.75

- STOXX Europe 600 up 0.6% to 389.78

- MXAP up 0.1% to 158.34

- MXAPJ up 0.07% to 504.30

- Nikkei up 0.1% to 22,048.24

- Topix up 0.2% to 1,623.27

- Hang Seng Index up 0.4% to 26,041.93

- Shanghai Composite down 0.9% to 2,929.09

- Sensex up 0.8% to 38,911.86

- Australia S&P/ASX 200 down 0.5% to 6,677.58

- Kospi up 0.05% to 2,074.52

- Brent futures up 0.2% to $62.51/bbl

- German 10Y yield fell 0.6 bps to -0.581%

- Euro down 0.05% to $1.0937

- Italian 10Y yield rose 1.0 bps to 0.504%

- Spanish 10Y yield fell 1.5 bps to 0.118%

- Gold spot up 0.3% to $1,507.92

- U.S. Dollar Index up 0.1% to 99.10

Top Overnight News from Bloomberg

- Boris Johnson sparked uproar during angry exchanges in the House of Commons after he was dragged back to Parliament to explain why he broke the law and tried to suspend the legislature in the run-up to Brexit

- ABN Amro Bank NV fell the most in more than three years in Amsterdam trading after Dutch authorities opened a criminal investigation into the bank under anti-money laundering laws

- Trump tried to squelch the latest threat to his presidency with the release of a transcript of his call with Ukraine’s president. Democrats say transcript bolsters move for impeachment inquiry

- The Federal Reserve should consider increasing its balance sheet by $250 billion over the next two quarters through outright purchases of Treasury securities to help diminish the risk of future money market turmoil, two former U.S. central bank officials said

- A record pace of defaults hit China’s domestic bonds this year. In 2020, it could be the offshore market’s turn. That’s because of a looming wall of dollar debt, issued by now-stressed borrowers, that comes to maturity. There’s $8.6 billion of offshore bonds coming due next year that currently have at least 15% yields — classifying them as stressed, according to data compiled by Bloomberg

- London’s dominance of the derivatives market is under threat, with European firms at risk of being blocked from using clearinghouses in the British capital within six months

Asian equity markets traded somewhat mixed as the region struggled to maintain the momentum from the US where President Trump ignited trade hopes after he suggested a deal with China could happen ‘sooner than you think’, while the US and Japan also reached a first stage trade agreement. ASX 200 (-0.5%) and Nikkei 225 (+0.1%) were higher at the open although the optimism in Australia later faded amid losses in commodity related sectors especially gold miners after the precious metal slumped to test the USD 1500/oz level, while the Japanese benchmark was positive but with gains capped as participants reflected on the limited US-Japan trade pact which didn’t involve autos although the US was said to have agreed to not impose Section 232 tariffs on Japan while talks are underway. Hang Seng (+0.4%) and Shanghai Comp. (-0.9%) were both underpinned at the open following the encouraging trade rhetoric from US President Trump who also stated that China is making large agricultural purchases and that there is a good chance we’ll make a trade deal with China which is getting closer and closer. However, the advances in the region later waned considering Trump’s tendency to flip flop on trade discussions and as US impeachment concerns lingered, while the PBoC’s open market operations also resulted to a considerable CNY 100bln net drain in liquidity. Finally, 10yr JGBs were lower following the bear steepening in the US and after the BoJ reduced its purchase amounts of 5yr-10yr JGBs for today’s Rinban operations.

Top Asian News

- Chinese Economy Weakens Across the Board, Early Indicators Show

- ‘Massive Snowball’ Effect to Spur China Bond Defaults Overseas

- India’s Combined Fiscal Deficit Seen Rising to 7.5% by Fitch

- Hong Kong Protests Threaten Billionaires’ Ties With Beijing

Major European Indices (Euro Stoxx 50 +0.5%) are higher, following a more mixed AsiaPac lead, as the market digests the latest trade developments; China’s MOFCOM sounded constructive, saying the two sides are “closely communicating and preparing for making trade talk progress in October” (reminder; US President Trump yesterday hinted that a deal could come sooner than we think). Moreover, a stumbling block for the potential US/Japan trade deal seems to have been averted; USTR Lighthizer said it is not the intention of the US to put tariffs on Japanese auto exports. However, on the EU/US front, the WTO look set to rule that the US can sanction up to USD 8bln worth of EU goods over Airbus (AIR FP) aid, sources said. It is also worth noting that Eurozone broad money supply increased more than forecast. ING note that it considered one of the best leading indicators for the eurozone economy, and as such, could be lending some support to sentiment (though EURUSD is just off YTD lows). Sectors are mostly higher, lead by Tech (+1.3%), and Energy (+1.3%), with Telecoms and Financials (+0.2) the laggards for now. In terms of stock specific movers; ABN Amro (-10.0%) shares took a tumble, as the company joined the ranks of other notable European banks in that it is now being investigated by public prosecutors over potential money laundering violations. Imperial Brands (-10.6%) issued negative outlook, expressing concerns over its next generation of products. British American Tobacco (-1.3%) moved lower in sympathy, and US tobacco names may not escape the session unscathed, not least given Imperial Brands specifically names US action on vaping products as resulting in a notable slowdown of vapour product growth. Pearson (-18.1%) sunk after the co. provided disappointing guidance. Wirecard (+2.3%) was bid premarket, after SocGen initiated the company at a Buy premarket. Ericsson (-0.7%) managed to reverse the majority of what was initially substantial losses as the broader market advanced, on the co. provided guidance for Q3 provisions in relation to investigations State-side, and sees costs at SEK 12bln. Finally, airlines were under pressure after IAG (-3.5%) issued a profit warning.

Top European News

- IMF to Leave Ukraine Without Accord Amid Privatbank Uncertainty

- Ericsson Expects to Pay $1 Billion in U.S. Corruption Probes

- British Airways Owner Warns Industry Woes Spill Over Into 2020

- Barclays Names El-Erian and Fitzpatrick as New Board Members

In FX, the DXY is marginally firmer on the day thus far with the index topping yesterday’s high (99.06) in a continuation of recent strength, whilst an optimistic tone from China’s MOFCOM regarding October trade talks in Washington did little to stem the Buck’s rise. DXY has breached its 12 Sept high at 99.10 with its YTD high at 99.37. Next up on the docket State-side, the final metrics US GDP and PCE prices, weekly initial jobless claims and a slew of Fed speaks including Kaplan (non-voter), Bullard (voter, dissenter), Calrida (voter), Daly (non-voter), Kashkari (non-voter) and Barkin (non-voter). In terms of US politics, participants will also be eyeing the potential release of the whistleblower’s complaint against US President Trump in regard to the controversial phone call between Trump and his Ukrainian counterpart, which some members of congress described as “troubling”.

- NZD, AUD – All firmer, with outperformance in the Kiwi following comments from RBNZ Governor Orr who struck an optimistic tone on the domestic economy whilst highlighting that unconventional policy tools are not currently necessary. NZD/USD reached a 0.63+ status overnight, albeit remains off highs (0.6310) at around 0.6290 after kicking the session off at 0.6270. Meanwhile, its Aussie counterpart remains buoyed by the optimistic US/China trade tone after the US President said a deal with China could happen “sooner than you think”, whilst rhetoric from China was remained constructive ahead of trade talks in Washington next month. AUD/USD trades north of 0.6750 with little by way of immediate technical levels in play.

- GBP, EUR – Both softer on the day with Cable the underperformer amid a firmer Buck coupled with Brexit angst as the UK PM remains resilient to a Brexit extension, whilst rhetoric from the EU is also less optimistic as most diplomats believe another delay will only increase the chances of No Deal down the line, according to Sun’s Nick Gutteridge. GBP/USD has tested 1.2300 to the downside after breaching a barrage of support levels between 1.2346-50 with the next level to the downside touted at 1.2233 (9th Sept low). The Euro is marginally softer, down from highs of 1.0965 due to a firmer Dollar as the pair moves closer to its YTD low of 1.0924. In terms of levels to the downside, below the psychological 1.0900 mark, the pair sees a strong Fib level at 1.0864 ahead of support at 1.0850. Note: EUR/USD sees large option expiries at today’s NY cut with 2bln between 1.0925-50 and 6bln at 1.1000. On the docket, ECB’s de Guindos, and Villeroy are set to speak later in the session.

- JPY, CHF – Discrepancies seen in the safe-haven currencies, albeit marginal with USD/JPY within a narrow intraday parameter of 107.60-80 ahead of a slew of Fed speakers. CHF meanwhile remains modestly softer with USD/CHF at session highs of around 0.9940 ahead of its 50 WMA and 200 DMA both at 0.9948.

In commodities, crude is trading flat, albeit seeing some upside in recent trade alongside European equities, amid a lack of notable fresh supply side/geopolitical developments. OPEC Secretary General Barkindo said that Saudi Arabia has almost restored the bulk of its oil supply, in line with recent commentary from the Saudis. Barkindo added that OPEC will continue to do whatever it takes to insulate oil market from politics but took an extraordinary OPEC+ meeting off the table. Elsewhere, the Kazaks said that had no plans to up crude production in wake of the recent Saudi attacks. ING note the fall in crude prices that occurred yesterday, on reports that Saudi Aramco is ahead of schedule by about a week in bringing capacity back. However, “it still seems that the market is being complacent,” the bank says, “with less than a US$3/bbl risk premium priced into the market, despite the heightened geopolitical risk in the region”. WTI Nov’ 19 and Brent Nov’ 19 futures currently sit near the USD 56.50/bbl and USD 62.50/bbl levels respectively. Elsewhere, Gold prices are slightly higher, but have been coming off somewhat during the European session, as the precious metal consolidates following yesterday’s declines in which it lost the USD 1520/oz handle again. Elsewhere in the metal complex, Copper prices are similarly lacklustre.

US Event Calendar

- 8:30am: GDP Annualized QoQ, est. 2.0%, prior 2.0%; GDP Price Index, est. 2.4%, prior 2.4%

- 8:30am: Core PCE QoQ, est. 1.7%, prior 1.7%

- 8:30am: Advance Goods Trade Balance, est. $73.4b deficit, prior $72.3b deficit

- 8:30am: Personal Consumption, est. 4.7%, prior 4.7%

- 8:30am: Wholesale Inventories MoM, est. 0.1%, prior 0.2%

- 8:30am: Retail Inventories MoM, est. 0.1%, prior 0.8%, revised 0.8%

- 8:30am: Initial Jobless Claims, est. 211,500, prior 208,000; Continuing Claims, est. 1.67m, prior 1.66m

- 9:45am: Bloomberg Consumer Comfort, prior 62.7

- 10am: Pending Home Sales MoM, est. 1.0%, prior -2.5%; Pending Home Sales NSA YoY, est. 1.3%, prior 1.7%

- 11am: Kansas City Fed Manf. Activity, est. -4, prior -6

DB’s Jim Reid concludes the overnight wrap

The political drama surrounding President Trump and a possible impeachment inquiry was the main talking point again even if positive trade momentum won out in the end. Other than a slight dip, markets appeared fairly non-fussed over the impeachment risks which probably goes to show how complicated, long-winded, and uncertain this investigation is in reality, especially since the Republicans control the Senate. Yesterday’s late afternoon headlines (European time) instead from the President suggesting that a trade deal with China “could happen sooner than you think” in the end saw markets recover after the post impeachment inquiry losses from the previous day and the morning session.

Indeed the S&P 500 (+0.62%) finished on a firmer footing despite trading down nearly half a percent at the lows after a rough transcript was released of the call between Trump and Ukraine President Zelenskiy yesterday. It showed that Trump asked Zelenkskiy to look into political rival Joe Biden, with the specific reference in the statement saying that “there’s a lot of talk about Biden’s son, that Biden stopped the prosecution and a lot of people want to find out about that…so whatever you can do with the attorney general would be great” but fell short of an explicit link to his days-earlier decision to freeze more than $391 million in military aid to Ukraine. As mentioned above, equities took a leg up on the positive trade comment, and then rallied further in the afternoon when USTR Lighthizer said that it’s “not our intention” to impose tariffs on Japanese cars. Ultimately, the more trade-sensitive tech sector outperformed, with the NASDAQ and Philly semiconductors indices up +1.05% and +1.78% respectively.

As for treasuries, 10y yields rose +8.5bps while the 2s10s curve finished +3.7bps steeper at 5.3bps. That marked the third consecutive session with the 10y trading in an intra-day range of around 10bps, which hasn’t happened in six weeks. Yields kicked higher after the Fed’s Evans said that his rate forecast does not include another cut which was somewhat surprising, as our economists had previously believed he leaned somewhat dovishly on the committee. Since he is a voting member of the FOMC this year, his rate expectation is particularly important. On the other hand, there was some attention paid to new research from the Fed staff which introduced a new measure of the labour market, which shows the recent job growth trend to be at its weakest level since 2010, which would argue for more accommodative rate policy. Finally, St. Louis Fed President Bullard reiterated his stated view that he would’ve preferred to cut rates by 50bps last week. Overnight we also heard from Kaplan (non-voter) and he said that the message from debt markets around the world is that monetary policy isn’t going to be sufficient on its own to lift growth. He added, “The marginal return in lowering the fed funds here has got diminishing returns. QE in the future may well have diminishing returns.” These comments from him signals that there is need for the fiscal spending alongside monetary policy support.

On a similar vein the resignation of Sabine Lautenschläger, the German Executive Board member was a bit of a surprise last night and she becomes the third German ECB resignation in the QE era. Lautenschläger is a hawk and was clearly opposed to the restarting of QE. Given this and the relatively high dissent rate at the last meeting, it hints at very difficult meetings to come in order to rally around a consensus. Policy tensions are building across countries in the Euro-area.

Back to markets and the VIX ‘spiked’ to as high as 18.45 after the Trump transcript was released but settled down to close at 15.88, back lower than where it ended Tuesday and now just 2 points above the September lows, and well below the closing high of 25.45 back in August. Meanwhile in commodities the main mover yesterday was oil where WTI fell -1.40% after inventories data showed a 2.4 million barrel increase in stockpiles, compared to expectations for a slight drawdown. We are now only +2.99% above the levels before the Saudi attack and an impressive -10.78% below the intra-day highs immediately after.

Meanwhile, Mr Trump and Japanese PM Abe signed the “first stage” of an initial pact after meeting at the UNGA yesterday, with Trump saying that he expects “in the fairly near future” that the US will have “final comprehensive deals signed with Japan.” In terms of specifics, the trade deal will help US farmers by opening up Japan’s agricultural market as it will eliminate or reduce tariffs on $7.2bn of US food and agricultural products, helping US beef, corn, pork and other farmers. Trump also said that the deal, which also covers a $ 40bn digital trade agreement, would help reduce a “chronic” US trade deficit and both the countries’ goal is for the accord to go into force on January 1, 2020. The limited deal will also not require a vote from Congress according to Trump while Japanese PM Abe said that he received direct confirmation from President Trump that the US won’t slap tariffs on Japan’s auto exports. Markets will hope this eventually extends to European autos.

This morning in Asia markets are trading mixed with the Nikkei (+0.24%), Hang Seng (+0.16%) and Kospi (+0.12%) all up while the Shanghai Comp (-0.73%) is down. Meanwhile, the BoJ reduced purchases in the key 5-10yr segment by JPY 30bn at today’s regular operation thereby bringing the purchases to JPY 350bn (vs. JPY 380bn at previous operation). This marks the fourth reduction in this segment in six weeks and the move come after the yield on 5yr JGBs reached record lows yesterday. They are up +1.9bps to -0.379% with 10yrs +1.6bps at -0.252%. Elsewhere, futures on the S&P 500 are down -0.15% while yields on 10yr USTs are down -3.8bps this morning.

Back to yesterday, where the political drama playing out in the House of Commons saw MPs back in their seats following the return of parliament. PM Johnson spoke late in the day after a fraught session with the highlight being his fresh challenge to the opposition to join him in supporting an election. The Labour party declined to take the bait, and looks set to maintain their position that they will not support a fresh vote until after Article 50 is extended successfully or until the Benn bill can be made watertight.

In other news, the data didn’t add much to proceedings yesterday. In the US, August new home sales rose a better than expected +7.1% mom reading (vs. +3.8% expected) which continues the trend of some outperformance in the housing sector, even if this data tends be volatile and prone to revisions. Meanwhile in the UK CBI retail sales volume survey for September wasn’t quite as bad as feared, printing at -16 (vs. -25 expected).

To the day ahead now, which for data this morning includes August M3 money supply data for the Euro Area and October consumer confidence in Germany. In the US the focus will likely be on the third revision to Q2 GDP where no change from the +2.0% qoq estimate is expected. Along with that, we’ll also get the August advance goods trade balance, August wholesale inventories, latest weekly jobless claims print, August pending home sales and September Kansas Fed manufacturing survey. Away from that data it’s a busy day for central bank speak. Indeed over at the Fed we’re due to hear from Kaplan at 2.30pm BST, Bullard at 3pm BST, Clarida and Daly at 4.45pm BST, Kashkari at 7pm BST and Barkin at 9.30pm BST. Along with that, ECB President Draghi speaks at 2.30pm BST at a conference in Frankfurt. Finally the BoE’s Cunliffe is also due to speak. The Mexico policy meeting is also due today.

3A/ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 26.35 POINTS OR 0.89% //Hang Sang CLOSED UP 96.58 POINTS OR 0.37% /The Nikkei closed UP 28.09 POINTS OR 0.13%//Australia’s all ordinaires CLOSED DOWN .43%

/Chinese yuan (ONSHORE) closed DOWN at 7.1300 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1300 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1238 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

This is interesting: China launches a new attack ship which is capable of invading Taiwan

(zerohedge)

China Launches New Attack Ship With Capabilities Of Invading Taiwan

We have outlined that China represents one of the greatest long-term strategic threats to the Indo-Pacific region and the US military that operates with-in. President Trump made it extremely clear last week that the People’s Liberation Army Navy (PLAN) is a “threat to the world.”

New reports surfaced on Twitter indicating the PLAN has started the launch process of a new amphibious assault ship that could soon be capable of launching an attack on Taiwan.

East Pendulum@HenriKenhmannLe lancement tant attendu du navire de tête Type 075, 1er « Navire d’assaut amphibie » chinois, a eu lieu ce matin à 09h20 au chantier naval Hudong-Zhonghua à Shanghai. Le sister-ship de ce bâtiment de plus de 30000t est sur cale et une version plus grande serait en conception.

A statement from the PLAN Wednesday said the Type 075, a helicopter carrier displacing more than 30,000 tons, is undergoing launch preparations at China State Shipbuilding Corporation’s Hudong-Zhonghua shipyard, reported Naval News.

Mike Yeo 杨启铭@TheBaseLegPhoto of reportedly China’s first Type 075 LHD being built geolocated to CSSC’s Hudong-Zhonghua shipyard in Shanghai (31° 16’38″N 121°34’10″E). Of course the “CSSC 沪东中” (truncated 沪东中华) is also a dead giveaway. Artwork (not mine) shows how it will probably look like

Latest news from the first Type 075 LHD at Hudong–Zhonghua shipyard: The big red “lantern” – usually containing colour strips – has been attached to the bow, balloons are ready … seems as if launch is indeed scheduled for tomorrow.

(Image via cycy03666 via @horobeyo)

Probably the best set of images of the first Type 075 LHD so far from today … unfortunately the second ship as well as certain details like the hangar as still psed, but anyway an impressive ship.

(Images via @10969YUKIKAZE )

The statement said water is being pumped into the dry dock in which the ship’s hull was built.

PLAN officials said Type 075 is a new class of warship, entirely produced in China, will be able to carry out amphibious combat missions.

Development work on Type 075 started in 2011, and it will be a “vertical” amphibious assault vessel capable of launching attacks on the mountainous East Coast of Taiwan.

For comparison, the Type 075 is slightly smaller than the US Navy’s landing helicopter assault vessel and more comparable to ones that are currently deployed in the Australian Navy.

The expected launch of Type 075 could be during a massive military parade in Beijing next week (Oct. 01). The PLAN will show the world its advanced vessels, fifth-generation fighters, advanced combat drones, robots, main battle tanks, and a show of force that could result in a few angry tweets from President Trump.

China has declared Taiwan as its territory although it has never controlled it, and threatens to invade by military force if Taipei resists unification.

Chinese and foreign analysts don’t see China launching an amphibious attack on Taiwan in the near term, rather a conflict with the US could spiral out of control in the South/East China Sea.

“Looking at various flashpoints in Asia including the Korean peninsula and the South China Sea, I have come to the conclusion that Taiwan is the most dangerous one,” Brendan Taylor, a strategic studies professor at Australian National University, told the Financial Times.

China has a long term plan, and it’s by the year 2049, Taiwan will be under Beijing control, which means sometime in the coming decades, a war could break out between both countries.

The world is positioning for conflict, and the reports we bring you — detail how countries are actively preparing for that inevitable day.

Beijing Accuses Washington Of Spreading “Anti-China Sentiment” In Hong Kong As Protests Drag On

Beijing is less-than-thrilled about American and British politicians offering words of encouragement and sympathy to Hong Kong’s protesters. It has made no secret of this.

But as the Hong Kong Human Rights and Democracy Act of 2019 finds growing support in Washington, Beijing is doubling down on its criticism of the US.

Hedge Funder Kyle Bass, who has been closely monitoring the situation in China and HK and frequently comments on twitter, recently bet against the Hong Kong dollar, which has been pegged to the dollar for 36 years. Bass claimed in a letter to investors earlier this year that the loss of Hong Kong’s special economic privileges via a change in US law or an executive order from the president would be economically devastating for Hong Kong. The subsequent economic shock would likely be enough to force the HKMA to abandon its currency peg, he said.

Beijing likely understands this, and knows that without these special privileges, Hong Kong will be rendered useless as a pathway for capital flowing to and from the West.

With this animosity weighing on the US-China relationship, it’s difficult to imagine how a trade breakthrough might be reached next month. But setting the issue of trade aside, the deputy commissioner of China’s Ministry of Foreign Affairs has some more scathing comments about western interference in Hong Kong as Beijing doubles down on a narrative that’s at the center of state propaganda about the protests. (of course, that narrative is aided by protesters waving American flags and appealing to President Trump to save them from China).

This time, they went a step further, accusing ‘senior’ US officials of personally meeting with the “anti-China” forces (apparently a reference to protest leader Joshua Wong’s recent trip to Washington to testify at a Congressional hearing).

Song Ruan, deputy commissioner of China’s Ministry of Foreign Affairs in Hong Kong, told foreign media that the U.S. and other Western countries were playing a “negative and disgraceful role” in the demonstrations that have gripped Hong Kong for more than three months. He said some foreign politicians “have sided with anti-China forces” in order to “sow trouble in China as a whole, and hold back China’s development in every possible way.”

“American senior officials had high-profile meetings with and spared no effort to cheer the anti-China forces who intend to mess up Hong Kong,” Song said at the briefing, during which he also extolled China’s decades of economic accomplishments less than a week before the 70th anniversary of the People’s Republic of China on Oct. 1.

“They have distorted the truth, condoned the rioters and claimed support for the right to peaceful protests, but turned a blind eye to the crime of the rioters, who undermined law and order and assaulted the police and citizens,” he said.

Echoing President Trump’s own tactics, the deputy commission blamed the foreign press for writing stories that are “unfair to China.”

“The top priority is to stop violence, end the chaos and restore order,” Song said.

He also scolded journalists working for foreign media for what he described as unfair coverage of the political turmoil.

“Some foreign media have confounded right with wrong, applied double standards and acted selectively in reporting the Hong Kong situation,” he said. “Instead of telling the truth, they have fanned the flames and cheered the opposition and violent extremists by offering them a platform to spread rumor.”