GOLD: $1505.50 DOWN $26.90 (COMEX TO COMEX CLOSING)

Silver:$18.02 DOWN 56 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1504.50

silver: $17.90

today is options expiry for the comex contracts. With the extreme rise in the price of silver these past several days, the bankers with help from the official sector had to get silver below 18.00 dollars to make all of those underwritten contracts worthless. Gold held above 1500.00 dollars. We have until next Monday to deal with these crooks as the next expiry is the much bigger OTC /LBMA gold/silver options.

Definition of Rico

RICO is typically used to indict mobsters – which makes its use against employees of the largest bank in America a very disquieting event. But even more disquieting is that two trial lawyers compared JPMorgan Chase to the Gambino crime family five long years ago and recommended in their 2016 book that the bank’s officers be prosecuted under the RICO statute.” … Pam Martens and Russ Martens

Ted Butler….

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 0/5

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,532.100000000 USD

INTENT DATE: 09/24/2019 DELIVERY DATE: 09/26/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 3

737 C ADVANTAGE 2 2

905 C ADM 3

____________________________________________________________________________________________

TOTAL: 5 5

MONTH TO DATE: 1,751

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 5 NOTICE(S) FOR 500 OZ (0.0155 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1751 NOTICES FOR 175,100 OZ (5.4463 TONNES)

SILVER

FOR SEPT

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 8662 for 43,310,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 8320 DOWN 171

Bitcoin: FINAL EVENING TRADE: $ 8352 DOWN 155

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A SMALL SIZED 398 CONTRACTS FROM 215,615 DOWN TO 215,217 WITH THE 5 CENT LOSS IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR SEPT 0,; DEC 1169 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1169 CONTRACTS. WITH THE TRANSFER OF 1169 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1169 EFP CONTRACTS TRANSLATES INTO 5.845 MILLION OZ ACCOMPANYING:

1.THE 5 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.410 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE

YESTERDAY, THERE WAS A GOOD ATTEMPT AT COVERING OUR BANKER SHORTS AT THE SILVER COMEX. OUR OFFICIAL SECTOR AGAIN USED COPIOUS NON BACKED PAPER IN AN ATTEMPT TO CONTAIN SILVER’S PRICE RISE AND WERE SUCCESSFUL IN THAT DEPARTMENT BUT WERE UNSUCCESSFUL IN FLEECING LONGS, AS WE HAD A STRONG GAIN IN TOTAL OI ON BOTH EXCHANGES DESPITE THE TINY LOSS AT THE COMEX.

THE LIQUIDATION OF COMEX OI OF SPREADERS HAVE STOPPED AND WE WILL NOW COMMENCE WITH THE ACCUMULATION PHASE OF SPREADERS GOLD OPEN INTEREST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

29,356 CONTRACTS (FOR 17 TRADING DAYS TOTAL 29,356 CONTRACTS) OR 146.780 MILLION OZ: (AVERAGE PER DAY: 1726 CONTRACTS OR 8.634 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 146.78 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 20.96% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1696.38 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 398, WITH THE 5 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1169 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GOOD SIZED: 771 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1169 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 398 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 5 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $18.58 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.077 BILLION OZ TO BE EXACT or 154% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.410 MILLION OZ//

- THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE COMEX OPEN INTEREST ROSE BY AN ATMOSPHERIC AND CRIMINALLY SIZED 11,552 CONTRACTS, TO 658,944 ACCOMPANYING THE $8.65 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING// YESTERDAY// / AND NOW WE OBTAINED A NEW COMEX RECORD BREAKING THE LAST RECORD OF 652,919 CONTRACTS ESTABLISHED ON JULY 19/2016. THIS IS QUITE A FEAT BECAUSE 3 YEARS AGO EXCHANGE FOR PHYSICAL (EFP) USAGE WAS JUST IN ITS INFANCY. IF THEY WOULD HAVE BEEN OUTLAWED AS THEY SHOULD HAVE BEEN, THEN THE ENTIRE OPEN INTEREST AT THE COMEX WOULD BE IN THE STRATOSPHERE.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 11077 CONTRACTS:

OCT 2019: 980 CONTRACTS, DEC> 10,979 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 658,944,, AND THIS NOW STANDS AS THE NEW COMEX RECORD….. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 22,629 CONTRACTS: 11,552 CONTRACTS INCREASED AT THE COMEX AND 11,077 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 22,629 CONTRACTS OR 2,262,900 OZ OR 70.38 TONNES. YESTERDAY WE HAD A GOOD GAIN OF $8.65 IN GOLD TRADING….

AND WITH THAT GOOD GAIN IN PRICE, WE HAD A HUMONGOUS GAIN IN GOLD TONNAGE OF 70.38 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON AS THE COMEX GOLD VOLUME AND OPEN INTEREST ARE HUGE. THEY WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE LONGS AND AS YOU CAN SEE, THE TOTAL OPEN INTEREST IN BOTH EXCHANGES SKYROCKETED. THE COMEX IS ONE ABSOLUTE FRAUD!!

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 127,391 CONTRACTS OR 12,739,100 oz OR 396.24 TONNES (17 TRADING DAY AND THUS AVERAGING: 7493 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAYS IN TONNES: 396.24 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 396.24/3550 x 100% TONNES =11.16% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4548.33 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 11,552 WITH THE GOOD PRICING GAIN THAT GOLD UNDERTOOK YESTERDAY($8.65)) //.WE ALSO HAD A HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11,077 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11,077 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 22,629 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

11,077 CONTRACTS MOVE TO LONDON AND 11,552 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 70.38 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED WITH THE GAIN IN PRICE OF $8.65 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 5 notice(s) filed upon for 500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $26.90 TODAY//(COMEX-TO COMEX)

THESE GUYS ARE NOW OUT OF CONTROL

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF: 16.42 TONNES

INVENTORY RESTS AT 924.94 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 56 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV//

/INVENTORY RESTS AT 377.811 MILLION OZ.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TINY SIZED 398 CONTRACTS from 215,615 DOWN TO 225,452 AND FURTHER FROM FROM A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR SEPT. 0; FOR DEC 1169: AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1169 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 398 CONTRACTS TO THE 1169 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE STILL OBTAIN AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 771 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 3.855 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ// AND FINALLY SEPT: 43.401 MILLION OZ//

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 5 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1169 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 29.91 POINTS OR 1.00% //Hang Sang CLOSED DOWN 335.68 POINTS OR 1.28% /The Nikkei closed DOWN 78.69 POINTS OR 0.36%//Australia’s all ordinaires CLOSED DOWN .61%

/Chinese yuan (ONSHORE) closed DOWN at 7.1245 /Oil DOWN TO 56.47 dollars per barrel for WTI and 62.02 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1245 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1238 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

i)China/USA

Interesting: with all of the turmoil in Hong Kong plus trade wars etc, Chinese home buying plunges to an 8 yr low

(zerohedge)

ii)Ahead of the October talks, China is purchasing pork which it needs badly anyway

(zerohedge)

4/EUROPEAN AFFAIRS

i)UK

With the most likely calling for an election, Corbyn is the most unpopular opposition leader siunce 1977

(zerohedge)

ii)Europe

iii)DANSKE/ESTONIA//.NETHERLANDS

The body of former CEO of Danske Estonia, the centre of money laundering throughout Europe has been found,,apparent suicide

(zerohedge)

7. OIL ISSUES

There is a huge glut of natural gas as the price drops below 2.00. This is due to the huge production increase with our shale boys. This will crush them as their costs exceed what they are receiving

(zerohedge)

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

Pam and Russ Martens ask the same questions that we do. They are of the opinion (as do I) that the big bank in trouble that needs a huge 30 billion dollars in 14 day repo loans is none other than Deutsche bank. They explain why

(courtesy pam and Russ martens/Wall Street on Parade)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

a)A slight rise in the 30 yr rate was all that was needed to stop the refi business as the boom in housing crashes

b)Although the refis are finished it did not stop new home buyers from buying homes with lower mortgage rates

iii) Important USA Economic Stories

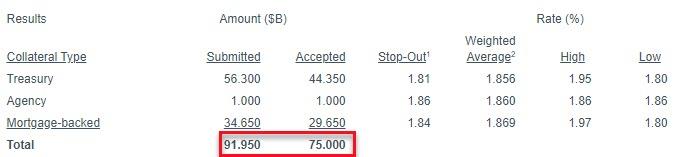

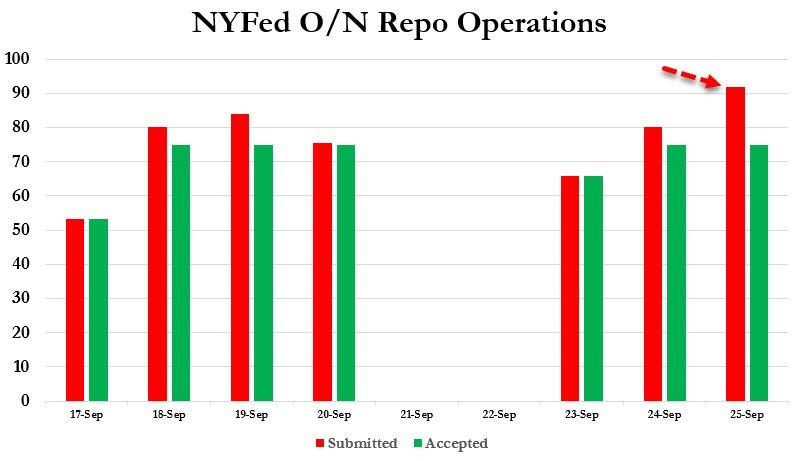

a)Your big story of the day. Each day we see record amounts of money needed in repo terms in order to unclog the money markets. Also remember we are coming close to the quarter end where the crooks put lipstick on their crooked balance sheets to make things looks better than it really is. Today a massive 92 billion dollars was needed and only 75 billion offered so again some could not get badly needed cash.

(zerohedge)

b)Philip Morris and Altria end the merger talks. The CEO of Juul quits

iv) Swamp commentaries)

a)An absolute joke: the IG states that the whistleblower has bias in favour of a rival candidate, The whistleblower retains the same lawyer for the Clintons and Schumer

(zerohedge)

b)Rudy G., lays out a pattern of corruption of the Bidens. He claims that China bought Biden

a must read and view

(zerohedge)

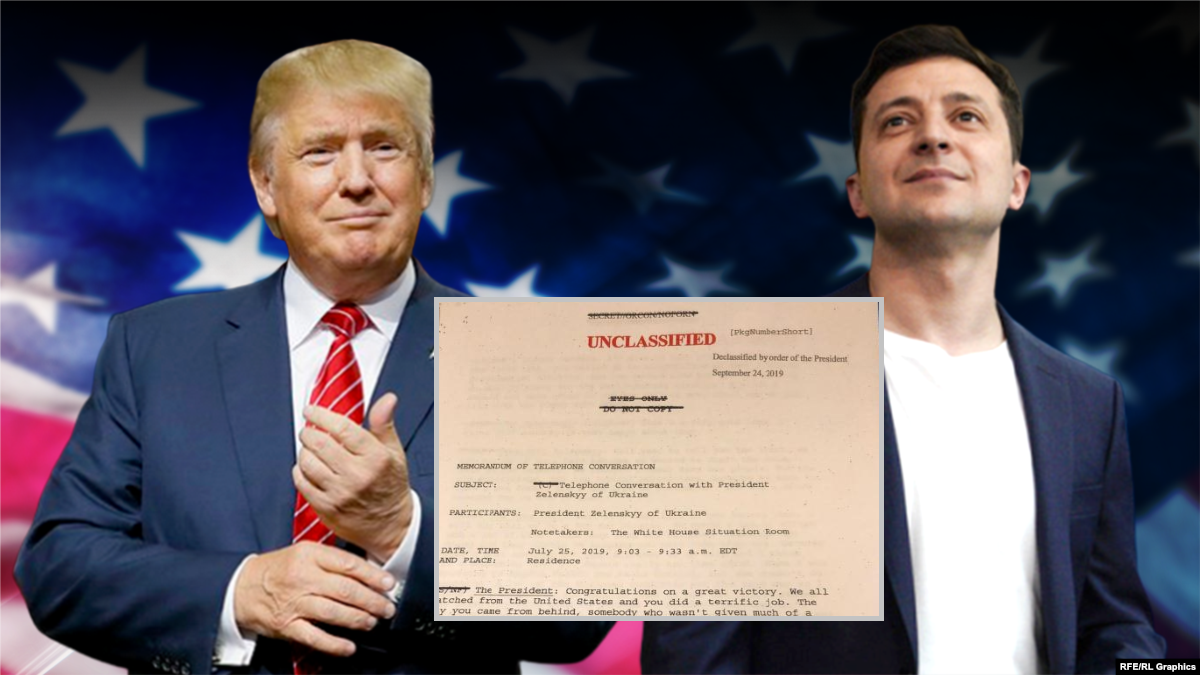

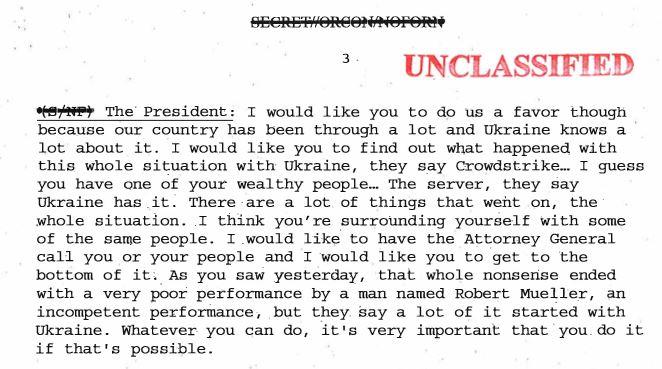

c)Trump releases the Ukraine transcript and it shows Trump asking the Ukraines to look into the Biden affair

d)The Wall Street Journal shreds the Democrat take out of a President after the release of the memorandum

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 1 kilobar entries

total gold withdrawals; 803.75 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 123,553 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 136,758 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 136,758 CONTRACTS EQUATES to 683 million OZ 97.6% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -1.76% ((SEPT 25/2019)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.93% to NAV (SEPT 25/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -1.76%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.14 TRADING 14.68/DISCOUNT 3.04

NAV 15.03 TRADING 14.53/DISCOUNT 3.32

END

And now the Gold inventory at the GLD/

SEPT 25/WITH GOLD DOWN $26.90 A HUGE PAPER DEPOSIT OF: 16.42 TONNES//INVENTORY RESTS AT 924/94 TONNES

SEPT 24/WITH GOLD UP $8.65 TODAY: A MONSTROUS CHANGE IN GOLD INVENTORY AT THE GLD: AN OUT OF THIS WORLD DEPOSIT OF 14.37 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 894.15 TONNES

SEPT 23/WITH GOLD UP $16.25 ON THE DAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER ADDITION OF 10.65 TONNES//INVENTORY RESTS AT 894.15 TONNES

SEPT 20/WITH GOLD UP $8.60 ON THE DAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 883.06 TONNES

SEPT 19/WITH GOLD DOWN $8.90 TODAY: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 3.23 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 883.60 TONNES

SEPT 18/WITH GOLD UP $2.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 5.86 TONNES/INVENTORY RESTS AT 880.37 TONNES

SEPT 17/WITH GOLD UP $1.50: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 874.51 TONNES

SEPT 16/WITH GOLD UP $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 5.86 TONNES FROM THE GLD///INVENTORY RESTS AT 874.51 TONNES

SEPT 13/WITH GOLD DOWN $7.75 TODAY: A BIG PAPER WITHDRAWAL OF 2.05 TONNES FROM THE GLD/INVENTORY RESTS AT 880.37 TONNES

SEPT 12//WITH GOLD UP $4.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 11/WITH GOLD UP $5.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 10/WITH GOLD DOWN $11.75 TODAY: A HUGE 7.33 PAPER TONNES OF GOLD WAS WITHDRAWN FROM THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 9/WITH GOLD DOWN $4.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 889.75 TONNES

SEPT 6//WITH GOLD DOWN $9.80: A BIG CHANGE IN GOLD INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 6.15 TONNES//INVENTORY RESTS AT 889.75 TONNES

SEPT 5/WITH GOLD DOWN $33.80 TODAY: A BIG ADDITION (DEPOSIT) OF 5.86 OF PAPER GOLD TONNES PROBABLY ADDED BEFORE THE RAID/EXPECT A HUGE PAPER WITHDRAWAL TOMORROW: INVENTORY RESTS AT 895.90 TONNES

SEPT 4/WITH GOLD UP $5.00 TODAY: A BIG CHANGE: A HUGE PAPER DEPOSIT OF: 11.73 TONNES/INVENTORY RESTS AT ….890.04 TONNES

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

AUGUST 22.WITH GOLD DOWN $6.80 TODAY: TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD: I)A PAPER DEPOSIT OF 6.74 TONNES INTO THE GLD (LATE YESTERDAY EVENING) AND 2) A PAPER DEPOSIT OF 2.93 TONNES LATE THIS AFTERNOON./INVENTORY RESTS AT 854.84 TONNES

AUGUST 21/WITH GOLD DOWN $.30 TODAY:A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.76 TONNES INTO THE GLD INVENTORY/GOLD INVENTORY RESTS AT 845.17 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SEPT 25/2019/ Inventory rests tonight at 924.94 tonnes

*IN LAST 668 TRADING DAYS: 24.22 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 568- TRADING DAYS: A NET 142.43 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 25.//WITH SILVER DOWN 58 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 377.811 MILLION OZ//

SEPT 24/WITH SILVER DOWN 5 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.338 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 377.811 MILLION OZ//

SEPT 23.2019/WITH SILVER UP 80 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 375.473 MILLION OZ.

SEPT 20/ WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 375.473 MILLION OZ.

SEPT 19/WITH SILVER DOWN 4 CENTS TODAY; A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 1.029 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 375.473 MILLION OZ/

SEPT 18/WITH SILVER DOWN 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 17/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 16/WITH SILVER UP 41 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A PAPER WITHDRAWAL OF 2.899 MILLION OZ OF SILVER LEAVES THE SLV///INVENTORY RESTS AT 376.502 MILLION OZ/

SEPT 13/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 12/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 11/WITH SILVER DOWN ONE CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 10/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 1.778 MILLION PAPER OZ OF SILVER///INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 9/WITH SILVER DOWN 6 CENTS TODAY: A MAMMOTH CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 5.425 MILLION PAPER OZ/INVENTORY RESTS AT 381.179 MILLION OZ../

SEPT 6/WITH SILVER DOWN ANOTHER 60 CENTS TODAY: A RATHER TIMID CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 842,000 PAPER OZ FROM THE SLV///INVENTORY RESTS AT 386.604 MILLION OZ//

SEPT 5/WITH SILVER WHACKED 68 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 4/WITH SILVER UP 28 CENTS TODAY:STRANGE!! A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 708,000 OZ FROM SLV’S INVENTORY:/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 TONNES

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.696 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 21/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 20.WITH SILVER UP 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

SEPT 25/2019:

Inventory 377.811 MILLION OZ

Pam and Russ Martens ask the same questions that we do. They are of the opinion (as do I) that the big bank in trouble that needs a huge 30 billion dollars in 14 day repo loans is none other than Deutsche bank. They explain why

(courtesy pam and Russ martens/Wall Street on Parade)

Pam and Russ Martens: What has frightened Wall Street banks from lending in the repo market?

Submitted by cpowell on Tue, 2019-09-24 15:31. Section: Daily Dispatches

Is it the collapse of Deutsche Bank?

* * *

By Pam and Russ Martens

Wall Street on Parade

Tuesday, September 24, 2019

Last Friday the Federal Reserve Bank of New York made it clear that its interventions in the overnight repo lending market were going to be a longer-term action. Call it what you will, the Fed has effectively returned to quantitative easing, where it buys up Treasuries, federal agency debt, and agency mortgage-backed securities from financial institutions in exchange for loans.

…

According to the New York Fed, the program has now been extended to at least October 10 and likely thereafter in one form or another. The Fed will be pumping in $75 billion daily in overnight repo loans while infusing $30 billion in 14-day term loans three times this week for a total of $90 billion in term loans.

That there is one or more financial firms needing $30 billion on a two-week basis and can’t get it from anyone but the Fed isn’t confidence inspiring. …

… For the remainder of the commentary:

https://wallstreetonparade.com/2019/09/what-has-frightened-wall-street-b…

* * *

Join GATA here:

New Orleans Investment Conference

Hilton New Orleans Riverside Hotel

Friday-Monday, November 1-4, 2019

https://neworleansconference.com/noic-promo/powellgata/

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

What Has Frightened Wall Street Banks from Lending in the Repo Market?

By Pam Martens and Russ Martens: September 24, 2019 ~

Last Friday the Federal Reserve Bank of New York made it clear that its interventions in the overnight repo lending market were going to be a longer-term action. Call it what you will, the Fed has effectively returned to quantitative easing (QE) where it buys up Treasuries, Federal agency debt and agency mortgage-backed securities (MBS) from financial institutions in exchange for loans.

Last Friday the Federal Reserve Bank of New York made it clear that its interventions in the overnight repo lending market were going to be a longer-term action. Call it what you will, the Fed has effectively returned to quantitative easing (QE) where it buys up Treasuries, Federal agency debt and agency mortgage-backed securities (MBS) from financial institutions in exchange for loans.

According to the New York Fed, the program has now been extended to at least October 10 and likely thereafter in one form or another. The Fed will be pumping in $75 billion daily in overnight repo loans while infusing $30 billion in 14-day term loans three times this week for a total of $90 billion in term loans.

The fact that there is one or more financial firms needing $30 billion on a two-week basis and can’t get it from anyone but the Fed isn’t confidence inspiring.

The necessity of Fed interventions is being blamed on temporary forces like a loss of liquidity from corporations paying their taxes for the quarter and large Treasury auctions where primary dealers are forced to buy under contracts with the U.S. Treasury. But as we previously wrote, these explanations do not jive with the gargantuan deposit bases of four of the biggest banks in the world that call the United States home. As we reported last week:

“As of June 30 of this year, the four largest banks on Wall Street (which are allowed to own Federally insured commercial banks as well as stock, bond and derivative gambling casinos known as investment banks) held more than $5.45 trillion in deposits. The breakdown is as follows: JPMorgan Chase holds $1.6 trillion; Bank of America has $1.44 trillion; Wells Fargo has $1.35 trillion; and Citibank is home to just over $1 trillion.

“A number of excuses have been offered by the business press to explain why the New York Fed had to ride to the rescue yesterday but the very simple question is this: how can four banks with $5.45 trillion in deposits not be able to cough up $53 billion in overnight loans.”

The reference to $53 billion is the amount that was borrowed from the Fed during the first day of the intervention, Tuesday, September 17, from the $75 billion offered out by the Fed. Now that the Fed is offering $30 billion in additional two-week loans, the question is this: is one bank tapping the spigot more than others? Is a financial institution in distress? If so, shouldn’t the public know why?

As the Government Accountability Office (GAO) revealed belatedly in 2011 in an audit of the Fed’s loans to Wall Street during the financial crisis, the Fed’s Primary Dealer Credit Facility (PDCF) had secretly made revolving loans totaling $8.95 trillion but 63 percent of that amount went to just three Wall Street firms: Citigroup received $2 trillion; Morgan Stanley got $1.9 trillion; and Merrill Lynch was the privileged recipient of $1.775 trillion. The rationale from the Fed that it made these secret loans to help banks return to lending to businesses to help the economy is bogus. Morgan Stanley and Merrill Lynch were predominantly retail brokerage firms with millions of trading clients. These Fed loans thus looked suspiciously like a bailout of margin loans and trading accounts.

One big bank with a large footprint on Wall Street that has seen its share price evaporate over the past two years is the big German lender, Deutsche Bank. Prior to the financial crisis, this was a $120 stock. Deutsche Bank closed yesterday on the New York Stock Exchange at $7.79, down 2.50 percent on the day. That decline far exceeded the price decline for any other Wall Street bank yesterday.

Deutsche Bank tried to merge with Commerzbank earlier this year but that deal fell through in April. Its new plan is to fire 18,000 workers and create a good bank/bad bank, isolating off unwanted assets that it plans to sell.

Deutsche Bank has reported losses in three of the last four years; as of the close of trading yesterday, it had $16 billion in common equity value versus $49 trillion notional (face amount) in derivatives; and it’s had four different CEOs in four years. And that’s not the worst of it.

The worst of it is that regulators on neither side of the pond have seen fit to rein in the dangerous interconnections that Deutsche Bank has as a major derivatives counterparty with mega banks on Wall Street as well as other European banks. (See After a $354 Billion U.S. Bailout, Germany’s Deutsche Bank Still Has $49 Trillion in Derivatives.)

According to a 2016 report from the International Monetary Fund (IMF), Deutsche Bank is heavily interconnected as a financial counterparty to JPMorgan Chase, Citigroup, Goldman Sachs, Morgan Stanley and Bank of America as well as to big European banks. The IMF wrote that Deutsche Bank posed a greater threat to global financial stability than any other bank as a result of these interconnections. When the IMF made that assessment in 2016, Deutsche Bank had tens of billions of dollars more in market cap than it does today.

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

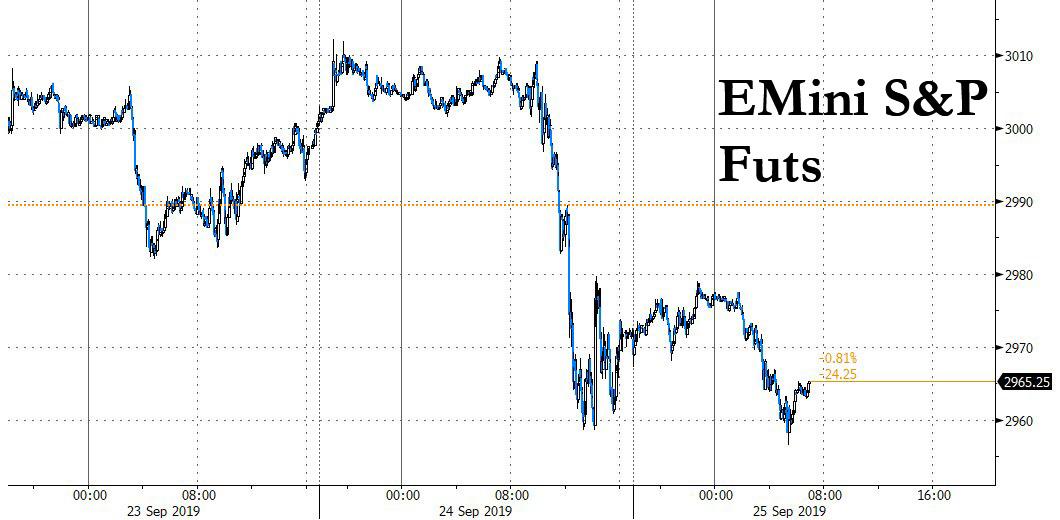

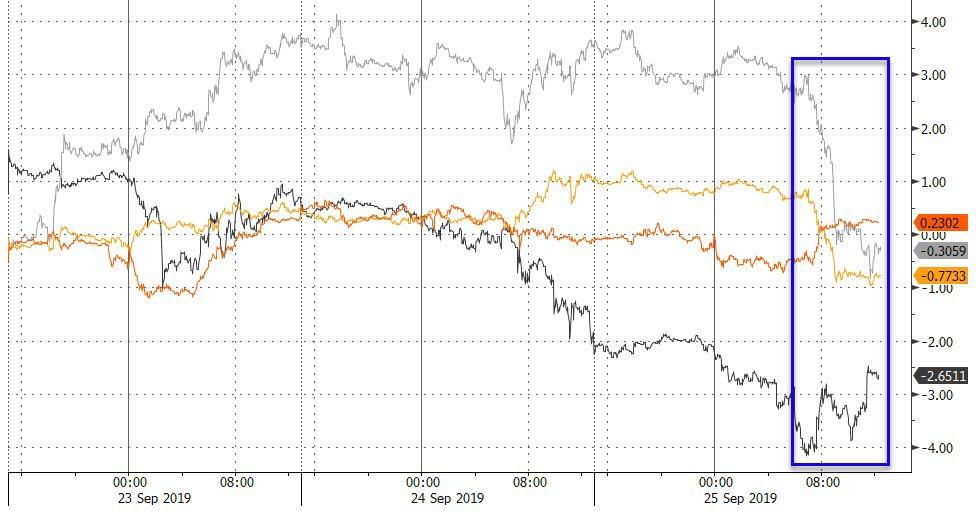

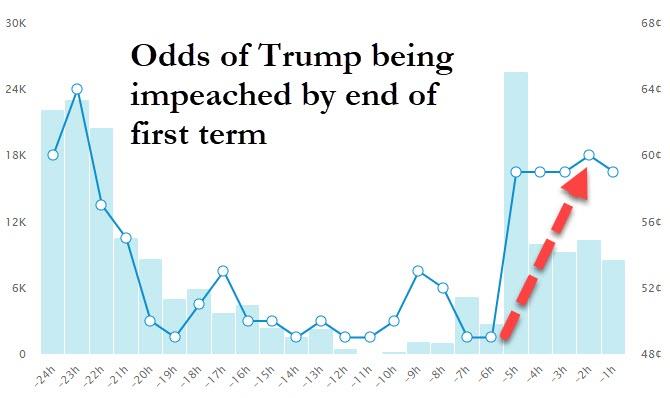

Global Stocks Tumble, Futures Sink As Traders Brace For Political Quake In Washington

World stocks fell to a two-week low, and US equity futures failed to sustain a modest bounce following a report of fresh “trade optimism” between America and China after U.S. lawmakers called for an impeachment inquiry into President Donald Trump, increasing the prospects of prolonged political uncertainty. The Dollar surged and interest rates were flat as traders braced for a “political quake” showdown between the president and democrats in Washington where Donald Trump is set to reveal both the transcript of his phone call with the Ukraine president as well as the full whistleblower complaint.

Despite a brief boost higher in the S&P EMmini future late on Tuesday night, when Bloomberg reported that China was preparing to purchase more U.S. pork – in what is supposedly another act of trade goodwill – as Beijing battles against domestic shortages and top trade negotiators from both nations plan to meet in Washington next month, the bearish mood prevailed and the “official” impeachment inequity launched by Democrats in the House of Representatives on Tuesday, exacerbated market anxieties running high over global recession risks. Of course, the impeachment inquiry will not actually lead to Trump’s removal from office: even if the Democratic-controlled House voted to impeach Trump, the Republican-majority Senate has said it will promptly kill the unprecedented motion.

Not helping sentiment was Trump stinging speech at the UN in which he delivered rebuke to China’s trade practices, adding to the pressure after more conciliatory tones in recent days.

Contracts for all three main equity gauges signaled more declines at the New York open as traders grappled with the impeachment investigation into President Donald Trump, seemingly getting little comfort from a Bloomberg report that China is preparing to buy more U.S. pork.

Meanwhile, adding to the China trade war concerns is the narrative that with impeachments proceedings now launched against Trump, China will delay its pursuit of any deal, hoping that either the president is removed or loses the 2020 presidential election. As such the next year will likely see no movement at all in the trade war between the two nations which has already sent Germany’s economy into a recession.

“It is hard to imagine how long can the truce with China remain on trade and that is adding to the general cautious environment for stocks,” said Neil Mellor at BNY Mellon in London. “As soon as markets start worrying about trade, they look at central banks for help but there is increasing pushback from them too.”

Also adding to geopolitical tensions is uncertainty over the outlook for Britain’s Brexit chaos after the Supreme Court ruled Prime Minister Boris Johnson had unlawfully suspended parliament.

MSCI’s global stock index dropped 0.4% in a fourth straight day in the red – the longest losing streak since the end of July rout.

European shares were broadly in the red, with Europe’s Stoxx 600 dropping 1.4% as technology stocks lead the losses, following Tuesday’s tumble in some of the biggest U.S. tech companies. France’s CAC tumbled 1.6% with export-reliant Germany falling 1.3%.

The downturn in Europe followed declines in Asia where Tokyo’s Nikkei suffered its largest loss in three weeks while China and Hong Kong dropped 1% or more. Nearly all markets in the region were down, with Hong Kong and South Korea leading declines. The Topix dropped 0.2%, snapping a three-day rising streak, with automakers and machinery firms among the biggest drags. The Shanghai Composite Index retreated 1%, driven by PetroChina and Kweichow Moutai. China’s economy in the third quarter was the weakest it has been this year, according to the China Beige Book, with manufacturing, property and the services sectors all worsening. India’s Sensex declined 1.2%, dragged by Housing Development Finance and HDFC Bank. Trump said he expects a trade deal with India very soon, while meeting Indian Prime Minister Narendra Modi at the United Nations General Assembly.

“Chinese shares were already exposed to downside risks. Trump’s comments likely increased those risks,” said Kiyoshi Ishigane, chief fund manager at Mitsubishi UFJ Kokusai Asset Management Co in Tokyo. “There are worries about U.S. consumer sentiment. There are also concerns that China’s economic slowdown hasn’t stopped.”

As risk assets took a beating, China’s offshore yuan fell.

China Foreign Minister Wang Yi said US and China need to take their bilateral relationship forward with wisdom and conviction, while he added that the relations have come to a crossroads and the trade war has inflicted losses on both sides. Wang further commented that neither US nor China can move ahead without the other and that opening up, as well as integration represent the way forward. However, Wang also stated US reverting to containment policy on China is a wrong idea which cannot possibly work, and that China will remain on its own path, while he added US should not try to change China and that trade negotiations cannot happen under threats.

In FX, the Bloomberg Dollar Spot Index erased much of its Tuesday drop as the greenback advanced versus all its peers amid political uncertainty in the U.S. and the U.K. The risk-sensitive Swedish krona led losses in the G-10; the pound reversed its Tuesday gain as U.K. Prime Minister Boris Johnson returned to the country after Britain’s Supreme Court ruled that he’d broken the law by suspending Parliament.

“Predicting the ultimate outcome of Brexit remains difficult,” said Mark Haefele, Chief Investment Officer, UBS Global Wealth Management. “As a result, the longer-term risk-return outlook for UK equities looks uncertain. We still advise being nimble on sterling.”

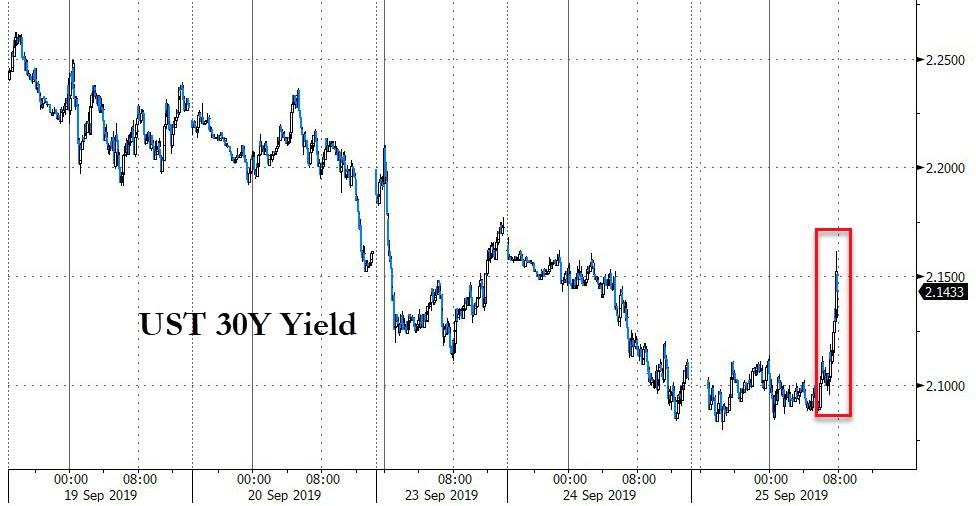

The yen weakened for the first time in five days against the dollar. Yields on 5-year Japanese government bonds slipped to a record low of minus 0.4% after comments from central bank Governor Haruhiko Kuroda added to speculation of an interest-rate cut in October while euro-area bonds gained to outperform Treasuries. Semi-core European debt led the advance in the region. The yield on 10- year U.S. Treasuries fell nearer to a two-week low with the the yield on benchmark 10-year Treasurys rising to 1.6387%, while the two-year yield stood at 1.6076%.

In commodities, crude futures declined after Saudi Aramco said it was ahead of schedule in restoring output that was reduced by a drone attack earlier in September.

In gepolitics, Iranian government spokesman says that President Rouhani will make important proposals in New York to build confidence and break the current deadlock, Limited amendments to nuclear deal could be accepted in exchange for Washington’s return to the agreement and Tehran is ready to reassure everyone that it is not seeking a nuclear weapon. US Secretary of State Pompeo tweeted that Iran must not be allowed to continue its destructive behaviour and suggested for the sake of the Iranian people and the world, the UNSC has a vital role to play in ensuring the UN arms embargo on the world’s top sponsor of terrorism

On today’s calendar, we got mortgage applications which crashed 10.1% in the past week as rates modestly picked up, and new home sales. HB Fuller is among companies reporting earnings.

Market Snapshot

- S&P 500 futures down 0.2% to 2,963.75

- STOXX Europe 600 down 1.3% to 384.87

- MXAP down 0.6% to 158.22

- MXAPJ down 0.9% to 503.19

- Nikkei down 0.4% to 22,020.15

- Topix down 0.2% to 1,620.08

- Hang Seng Index down 1.3% to 25,945.35

- Shanghai Composite down 1% to 2,955.43

- Sensex down 1.2% to 38,635.61

- Australia S&P/ASX 200 down 0.6% to 6,710.22

- Kospi down 1.3% to 2,073.39

- German 10Y yield fell 1.3 bps to -0.613%

- Euro down 0.2% to $1.1002

- Italian 10Y yield rose 0.2 bps to 0.494%

- Spanish 10Y yield fell 2.4 bps to 0.094%

- Brent futures down 1.5% to $62.13/bbl

- Gold spot little changed at $1,531.73

- U.S. Dollar Index up 0.2% to 98.53

Top Overnight News from Bloomberg

- Speaker Nancy Pelosi said the House is opening a formal impeachment inquiry of President Trump, saying he violated his oath of office and obligations under the Constitution. The U.S. Justice Department suggested it may defend Trump’s effort to block a subpoena to his accountant for tax records and other private documents

- Chinese companies are preparing to purchase more U.S. pork, according to people familiar with the situation, with top trade negotiators from both nations set to meet in Washington next month

- A defiant Boris Johnson hit back at the U.K.’s top judges and vowed to take the country out of the European Union next month, despite suffering an unprecedented legal defeat over his Brexit strategy in the highest court in the land. Labour rules out election until no-deal risk over

- China’s economy in the third quarter was the weakest it has been this year, according to the China Beige Book, with manufacturing, property and the services sectors all worsening, even as borrowing picked up

- Japan’s five-year government bond yield slipped to a record low after comments from central bank Governor Haruhiko Kuroda added to speculation of an interest-rate cut in October. BOJ’s Masai says FX could exert negative effects on Japan prices

- The leaders of France and the U.K. urged Iranian President Hassan Rouhani and President Trump to meet on the sidelines of the UN General Assembly in what appeared to be rapid-fire shuttle diplomacy aimed at easing tensions

Asian equity markets tracked the losses seen across global peers amid headwinds from the US where sentiment was dragged by weak Consumer Confidence data, increasing impeachment concerns and after President Trump kept a hardline tone on China and Iran. ASX 200 (-0.6%) and Nikkei 225 (-0.4%) were lower with Australia pressured by losses in the mining-related sectors and after optimistic comments on the economy from Governor Lowe placed some doubts regarding a rate cut next week, while Japan trade was dampened by recent flows into its currency and ongoing uncertainty regarding a trade deal with the US. Hang Seng (-1.2%) and Shanghai Comp. (-1.0%) were also negative after US President Trump kept a hawkish tone on China during his UN speech in which he alleged China has not adopted promised reforms, uses heavy state subsidies, steals intellectual property and manipulates its currency. This was later followed by comments from China’s Foreign Minister Wang who responded with a more conciliatory tone in which he suggested the sides need to take their bilateral relationship forward with wisdom as well as conviction and that neither countries can move ahead without the other, although he also added the US should not try to change China and that trade negotiations cannot happen under threats. Finally, 10yr JGBs were higher amid the negative risk tone and as the pressure on yields resumed with the 10yr yield below -0.25% and the 5yr yield touched a record low which has spurred speculation BoJ may be forced to reduce is regular purchases, while weaker results at the 40yr JGB auction did little to dent the rally in Japanese bonds.

Top Asian News

- BOJ’s Masai Offers New Reason for Sitting Tight Amid Easing Talk

- Kuroda Gets a Steeper Curve as Five-Year Yield Sets Record Low

- Thailand Holds Interest Rate as it Downgrades Growth Outlook

- Philippine Central Bank Cuts 2019 Inflation Forecast to 2.5%

Major European bourses (Euro Stoxx -1.3%) are lower, with sentiment weighed by a number of factors. Prior to the cash open, fresh concerns regarding US/EU trade relations were stoked; reportedly the US, in retaliation for illegal EU subsidies for Airbus (-0.5%) (as ruled recently by the US), is mulling hit EU imports with tariffs that randomly rotate, so as to hit as many industries as possible and create higher levels of uncertainty. 2) US President Trump impeachment. Additionally, the possibility of the impeachment of US President Trump adds further uncertainty to the macro backdrop. Further negative ticks were seen across equities (most pronounced in the DAX) on the reports that China is to accelerate the public listings of chip companies on Shanghai’s STAR stock market in the latest initiative by Beijing, as China counter US technology sanctions and speed the development of its semiconductor industry. Sectors are all in the red, with Tech (-2.0%) and Consumer Discretionary (-1.7%) leading the decline, while more defensive Utilities (-1.0%), Health Care (-1.1%) and Consumer Staples (-0.8) are lower but faring better. In terms of individual movers; Adidas (-0.8%) was higher at the open, in sympathy with Nike, who are higher in premarket trade after posting strong earnings, before succumbing to the broader market’s negative feel. Wirecard (-2.4%) is under pressure after a downgrade at UBS. EDF (-7.1%) sunk on the news of further delays to projects and a higher build up in associated costs that expected. Babcock (+4.3%) is higher, after posting a positive trading update.

Top European News

- TeamViewer Makes Drab Debut After IPO Priced at Upper End

- Did ECB Accidentally Tighten Policy? Analysts Won’t Let it Drop

- Europe’s Funds Are Hunkering Down in Bonds for Coming Recession

- Aston Martin Sells Bonds to Bridge Cash Gap Ahead of SUV Launch

In FX, the broad Dollar and Index is staging a recovery following yesterday’s losses after DXY briefly dipped below 98.30 due to a combination of further Fed repo operations, downbeat US consumer sentiment and strength in G10 peers. DXY now treads water just above 98.50 ahead of yesterday’s high of around 98.70 with participants keeping an eye on events State-side as the House is to open a formal impeachment inquiry into US President Trump (analysis on the RANsquawk headline feed) whilst Fed’s Evans (Voter, Dove) is due to speak at 1400BST on the economy and policy.

- GBP, EUR – Sterling is on the backfoot today ahead of Parliament’s return at 1130BST (analysis on the RANsquawk headlines) with initial downside in Cable coinciding with reiterations from Labour leader Corbyn, who stated that the earliest he would call a general election would be October 17th after the PM has requested a Brexit extension, although a firmer Buck somewhat influenced currency action. GBP/USD has reversed a bulk of yesterday’s gains with the pair back below the 1.2450 level after breaching its 10 DMA (1.2462) ahead of support between 1.2410-15. Meanwhile, EUR/USD remains around the 1.10 handle (where 740mln in options expire at today’s NY cut) , off its high of around 1.1023 (amid a firmer Buck) ahead of resistance and 1.1025, also where offers have been reported, whilst to the downside, EUR/USD sees resistance at 1.0980.

- NZD, AUD – The Kiwi has given up most a bulk of its post-RBNZ gains in which the Committee agreed that developments since the August Statement had not significantly changed the outlook for monetary policy. The RBNZ reached a consensus to keep the OCR at 1% and that, if necessary, there remains scope for more fiscal and monetary stimulus. CB also maintained a neutral stance despite some calls for an easing bias to be reintroduced. NZD/USD resides around 0.6325, having visited a high of 0.6350 (on the decision) and vs. a pre-announcement low of 0.6305. Meanwhile, the Aussie has faded yesterday’s Lowe-induced gains with some potential pressure from weaker copper prices and as the AUD/NZD cross falls further below 1.0750 having earlier tested 1.0700 to the downside.

- EM – The Lira continues to strengthen in European trade, this time amid comments from the CBRT Governor who reiterated the Central Bank’s “cautious” stance, in turn providing some relief to investors who fear that the Bank may be jumping the gun following two back-to-back deeper than forecast rate cuts. The Governor also acknowledged the continuing improvement in inflation whilst also noting an economic recovery in H2. USD/TRY is back below the 5.7000 level (low 5.6784) having declined from an intraday high of 5.7100.

- RBNZ maintained the Official Cash Rate at 1.00% as expected, while it stated the committee agreed new information did not warrant significant change to the policy outlook and that a steady OCR is needed to ensure inflation increases to the mid-point of its target range. RBNZ added there remains scope for fiscal and monetary stimulus, that domestic rates can be expected to remain low for longer but also noted that low rates and government spending is expected to support demand in the coming years. (Newswires)

In commodities, the crude complex is lower on Wednesday morning, seemingly in line with equities, although bearish supply side news doing the rounds is also likely a factor in the downside; reportedly, Saudi Aramco is recovering faster than expected form the recent attacks on its oil facilities, with total daily production capacity likely to be restored to over 11mln BPD roughly one week ahead of schedule. On the topic of bearish impulses; more reports focusing on the fact that the US drilled-but-uncompleted wells (DUCs) count is declining, possibly an indication that companies have started completing unfinished wells, which could foreshadow elevated US crude output, have been doing the rounds. Elsewhere, the complex has taken little impetus from geopolitics; Iranian President Rouhani has indicated a willingness to make some concession if the US eases sanctions (which remains a big if, especially given US President Trump’s slightly hawkish UNGA speech yesterday), and may unveil some proposals at the UN later today. WTI futures are again below the USD 56.50/bbl mark, consolidating for now around USD 56.50/bbl figure, meanwhile Brent remains near the USD 62/bbl level. Spot Gold futures are fairly flat, seemingly unable to take advantage of woes in the equity market, and is blanketed by support and resistance at USD 1520/oz and USD 1536/oz respectively. Elsewhere, copper is lower, in line with general sentiment.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -0.1%

- 8am: Fed’s Evans Discusses Economy and Monetary Policy

- 10am: New Home Sales, est. 658,000, prior 635,000; New Home Sales MoM, est. 3.62%, prior -12.8%

- 10am: Fed’s George Speaks to Senate Banking Panel on Payments System

- 10am: Fed’s Brainard Speaks Before House Panel on Financial Stabilit

- 7pm: Fed’s Kaplan Speaks in Moderated Q&A

DB’s Jim Reid concludes the overnight wrap

Although nothing seems that abnormal these days, yesterday was pretty remarkable as two of the most powerful leaders in the world faced serious misconduct/legal charges and accusations. After the US closing bell the day’s speculation that Mr Trump would face an impeachment inquiry materialised as Nancy Pelosi formally announced the start of the process in the US House of Representatives. This followed an unprecedented Supreme Court hearing in the U.K. which found that PM Johnson’s decision to prorogue Parliament was unlawful. They will reconvene today some three weeks ahead of the PM’s prior wishes.

The impeachment inquiry regards a phone call between President Trump and Ukrainian President Zelenskiy from July. An anonymous individual in the US intelligence community, who was apparently listening to the call as part of his job, issued a whistleblower complaint to his superiors alleging that a senior US administrator had improperly interacted with a foreign official, possibly by asking for political assistance in a US election. The Trump administration has refused to release the complaint to Congress, which Pelosi argues is illegal since the law requires all complaints to be forwarded to the legislature. Per Pelosi’s announcement, both the alleged misconduct on the call and the withholding of the complaint are two separate but parallel grounds for the impeachment inquiry.

Equity markets in the US and Europe had already pared earlier gains after slightly more negative trade comments from Mr Trump at the UN General Assembly (see below). The S&P 500 then took another leg lower after the European close as media outlets reported that the impeachment inquiry may happen. The S&P 500 traded as low as -1.14% after those unconfirmed press reports and the NASDAQ fell to -1.74%. However, both indexes pared part of their declines in mid-afternoon after Trump announced that he will release the full transcripts of the relevant phone call by later today. The S&P 500 and NASDAQ ended the session -0.84% and -1.46% lower, respectively.

Mr Trump’s earlier trade comments suggested that “hopefully we can reach an agreement that will be beneficial to both”, but that China hadn’t adopted the reforms they’d promised. He also spoke positively about the “massive tariffs on more than $500 billion worth of Chinese-made goods” and lauded that “supply chains are relocating back to America (…) and billions of dollars are being paid to our treasury.” Trump also pivoted directly from talking about trade to discussing the situation in Hong Kong, which would be a confrontational step if he starts to link the two topics.

Overnight Bloomberg has reported that Chinese companies are preparing to purchase more US pork. The story further added that the volume of the purchases hasn’t been finalised but may be around 100,000 tons, some of which will be for state reserves. This comes ahead of meeting between top trade negotiators from both nations next week and points to continued improvement in mood music ahead of the talks; however, one needs to be cautious given the uncertain nature of these talks and above mentioned comments from Trump at the UNGA. Elsewhere, Chinese Foreign Minister Wang Yi has said that both the US and China have shown good will with recent tariff moves while adding “Conflict and confrontation can lead nowhere and neither country can mould the other in its image.” He also said that China also expects the US to remove its own restrictions on Chinese trade and investment.

Asian markets are trading down this morning with the Nikkei (-0.47%), Hang Seng (-0.95%), Shanghai Comp (-0.57%) and Kopsi (-0.80%) all lower. However, most of the indices have pared deeper declines after the trade story above hit the wires. S&P futures which were flat after Pelosi’s announcement, are also up +0.22%. 5yr JGB yields are trading down -3.3bps this morning at a record low of -0.399%, surpassing the previous low reached in July 2016. 10y JGB yields are down a more limited -2.4bps to -0.271%. The moves comes after the BoJ Governor Kuroda said yesterday that he was closer to adding stimulus now than he had been earlier in the year while adding, “I don’t think we need to rule out cutting negative rates as a policy option at this point.” Overnight, the White House has also listed a 4pm press conference with President Trump in New York in the President’s daily schedule. So one to watch for. In terms of overnight data releases, Japan’s August services PPI came in one-tenth above consensus at +0.6% yoy while previous months read was also revised up by one tenths to +0.6% yoy.

The sharp US equity moves yesterday snapped the recent stretch of lower vol trading conditions. Indeed, on a closing basis, the S&P 500 had traded in a 0.59% range over the last 9 sessions, the tightest such range in just over a year. That had placed it within roughly +/-0.5% of the symbolic 3,000 level every session over that period, before snapping out to the downside last night. As mentioned above European equities closed below their earlier peaks but before the main part of the US’s afternoon selloff. The STOXX 600 ended flat while the DAX retreated -0.29%. The FTSE 100 (-0.46%) also fell thanks to sterling’s appreciation.

Indeed sterling rallied +0.50% yesterday as the UK Supreme Court ruled in a unanimous judgement that Prime Minister Johnson’s advice to the Queen to suspend Parliament “was unlawful, void and of no effect”, and that Parliament “has not been prorogued”. Furthermore, the President of the Supreme Court said that “The effect upon the fundamentals of our democracy was extreme”, and that “No justification for taking action with such an extreme effect has been put before the court.” The ruling is a massive setback for the government, who had planned that Parliament wouldn’t return until 14th October. After the ruling was announced, the Speaker of the House of Commons, John Bercow, said that Parliament would return this morning, and MPs would have further opportunities to scrutinise government ministers and apply for emergency debates.

In response to the decision Prime Minister Johnson, who had also been at the UN General Assembly in New York yesterday, changed his plans to fly back to the UK for Parliament’s resumption. He said he “strongly disagrees” with the ruling but that he’d respect the court’s decision. The developments from the Supreme Court rather upstaged the opposition Labour Party’s annual conference yesterday, with the resumption of Parliamentary proceedings leading Jeremy Corbyn to bring forward his speech by a day to be back in Parliament. Corbyn reiterated his stance in favour of a second referendum, pledging to implement whichever option the public decided. Notably, he said that he wouldn’t support another election until no-deal had been taken off the table, opposing Johnson’s attempts to call one for the time being. In terms of other proposals from the speech, which on another day would have been newsworthy in themselves, the highlights included proposals for: creating a state-owned drug manufacturer to produce low-cost generic drugs; nationalising rail, water, and postal companies; zero carbon emissions by 2030; and state-provided personal care for senior citizens. Perhaps most impressively, he promised to deliver the suite of new benefits without raising the national debt. This follows news from the previous day that we’ll all work 4-day weeks within a decade here in the U.K. under a new Labour administration.

Back to markets and in Europe the post ECB sell-off in bonds is becoming more of a distant memory as sovereign recovered from earlier losses to end the session higher, with bunds (-1.9bps) and OATs (-0.8bps) rallying following slightly disappointing US data (see below). We did have some European data releases yesterday, but following the previous day’s underwhelming PMIs, the releases weren’t quite so bad. In Germany, the Ifo business climate index rose three-tenths to 94.6 (vs. 94.5 expected), while the current assessment reading rose to 98.5 (vs. 96.9 expected). The dampener was the expectations reading however, which fell to its lowest in a decade at 90.8 (vs. 92.0 expected). Looking at the sector balances in the Ifo, services saw an uptick to 16.6 (from 13.0 in August), but both manufacturing (at -6.4) and trade (-3.7) slid deeper into negative territory. Data from France was more positive at the top level too, with the INSEE’s business climate composite indicator rising to 106.2 (vs. 105 expected), the joint highest over the last year.

A particular area that suffered in Europe yesterday were automobile stocks, with the STOXX Automobiles and Parts Index down –1.36% after Volkswagen’s CEO and Chairman, along with a former CEO, were charged by German prosecutors with market manipulation from failing to disclose knowledge of the emissions cheating scandal that has since cost the company billions of dollars in fines. Meanwhile Daimler was also fined €870m over vehicles that didn’t meet emissions regulations. Volkswagen and Daimler closed down -2.16% and -1.68% respectively.

Oil was a further casualty, with Brent Crude down -3.21% yesterday, as concerns about global energy demand following the US data releases coupled with hopes that Saudi output would be restored sent prices lower. Gold advanced +0.65% however as investors sought out safe havens, up for a 4th successive positive session.

As for the US data, the Conference Board’s consumer confidence indicator fell to 125.1 (vs. 133.0 expected), while the present situation (169.0) and the expectations readings (95.8) also lost ground on last month. Adding to the negative sentiment, the Richmond Fed’s manufacturing index underwhelmed as well, falling to -9 (vs. 1 expected). Following the releases, the dollar slipped back while Treasuries rallied, with 10yr yields down -8.6bps, though the rally gained momentum amid the equity selloff during the NY afternoon session. The 2s10s curve flattened by -1.8bps to close at 2.3bps the lowest since September 6.

Turning to the day ahead, data highlights include French consumer confidence for September and the CBI’s September distributive trades survey from the UK, while from the US we have August new home sales figures and weekly MBA mortgage applications. In terms of central bank speakers, we’ll be hearing from the ECB’s Coeure and Lautenschlaeger, the Fed’s Evans, George and Brainard , and the BoE’s Governor Carney. And of course keep an eye out for further developments on Brexit as both houses of the UK Parliament will be sitting again.

3A/ASIAN AFFAIRS

I)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 29.91 POINTS OR 1.00% //Hang Sang CLOSED DOWN 335.68 POINTS OR 1.28% /The Nikkei closed DOWN 78.69 POINTS OR 0.36%//Australia’s all ordinaires CLOSED DOWN .61%

/Chinese yuan (ONSHORE) closed DOWN at 7.1245 /Oil DOWN TO 56.47 dollars per barrel for WTI and 62.02 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1245 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1238 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

China/USA

Interesting: with all of the turmoil in Hong Kong plus trade wars etc, Chinese home buying plunges to an 8 yr low

(zerohedge)

Chinese Home buying In US Plunges To 8 Year Low

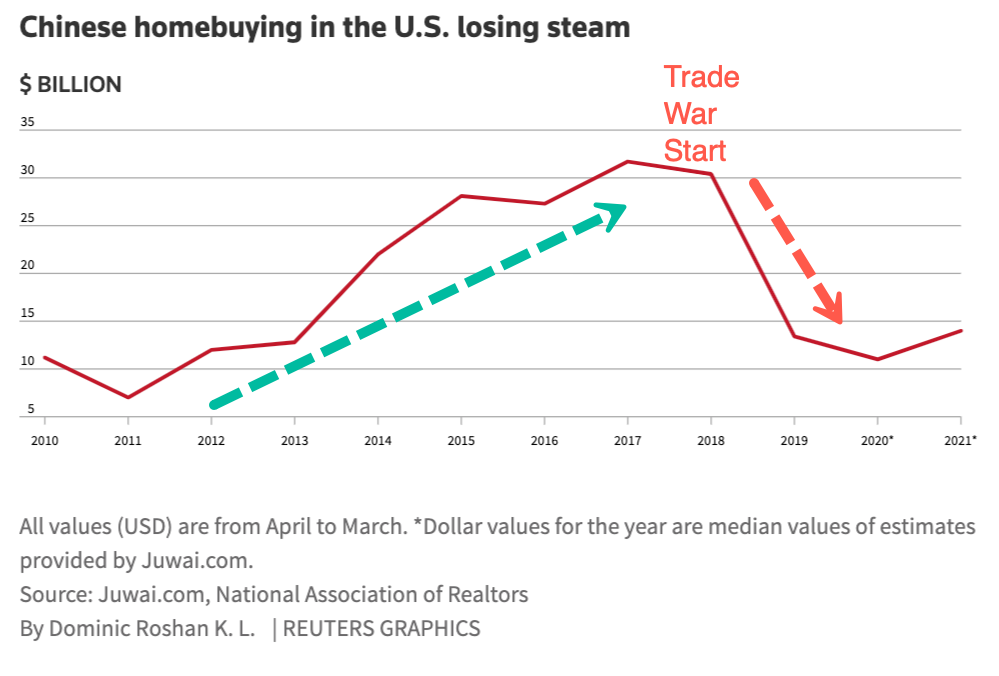

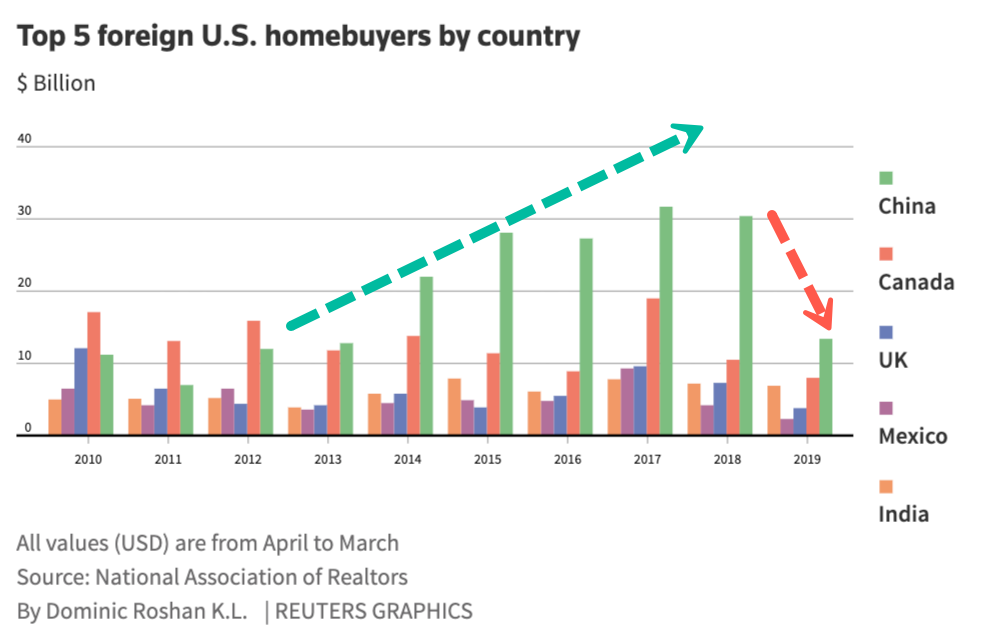

According to a new report from Reuters, leading Chinese real estate website, Juwai.com, estimates that Chinese buyers purchasing US homes will plunge to an eight-year low by the end of 1Q20.

Real estate data from Juwai estimates US home sales of Chinese buyers would drop to between $10 billion and $12 billion by the end of March 2020, is down from the $13.4 billion reported for the year ended in March 2019 via National Association of Realtors (NAR) and down from $30 billion seen in 2017 and 2018.

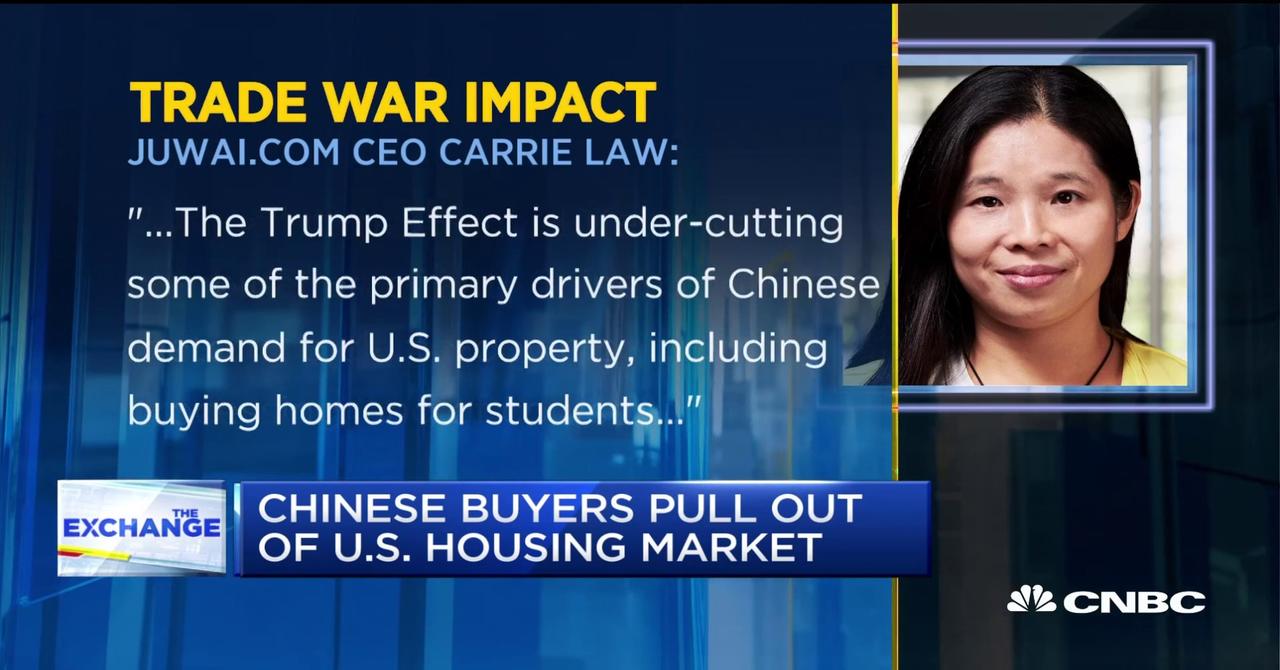

The site’s executive chairman, Georg Chmiel, told Reuters that the exodus of Chinese buyers comes at a time when many have worried about obtaining US visas, the weakening yuan, escalating trade tensions between the US and China, and overpriced real estate in the US, had spurred buyers to go elsewhere in the hunt for yield.

“The Trump administration’s tariffs, aggressive rhetoric, targeting of Chinese graduate students at US universities, and new visa red tape have all hurt Chinese demand,” Chmiel told Reuters.

He said Chinese buyers commonly use US real estate as investments and second or third homes.

“With the trade war going on, it’s easy to imagine a scenario in which you might be forced to sell or your investment might otherwise lose value,” he warned.

The removal of Chinese buyers has already started to weigh on luxury homebuilder Toll Brothers Inc, warning about slumping sales in California.