GOLD:$1467.40 DOWN $32.50 (COMEX TO COMEX CLOSING)

Silver:$16.98 DOWN 58 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1472.50

silver: $17.02

Definition of Rico

RICO is typically used to indict mobsters – which makes its use against employees of the largest bank in America a very disquieting event. But even more disquieting is that two trial lawyers compared JPMorgan Chase to the Gambino crime family five long years ago and recommended in their 2016 book that the bank’s officers be prosecuted under the RICO statute.” … Pam Martens and Russ Martens

Ted Butler….

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 839/7214

EXCHANGE: COMEX

CONTRACT: OCTOBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,499.100000000 USD

INTENT DATE: 09/27/2019 DELIVERY DATE: 10/01/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 H GOLDMAN 1248

092 C DEUTSCHE BANK 11

118 H MACQUARIE FUT 1156

323 H HSBC 4000

555 H BNP PARIBAS SEC 9

657 C MORGAN STANLEY 37

661 C JP MORGAN 3121 524

661 H JP MORGAN 3157

685 C RJ OBRIEN 1 3

686 C INTL FCSTONE 42 9

690 C ABN AMRO 137

737 C ADVANTAGE 6 49

800 C MAREX SPEC 41

880 H CITIGROUP 869

905 C ADM 7 1

____________________________________________________________________________________________

TOTAL: 7,214 7,214

MONTH TO DATE: 7,214

NUMBER OF NOTICES FILED TODAY FOR OCT CONTRACT: 7214 NOTICE(S) FOR 721,400 OZ (22.43 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 7214 NOTICES FOR 721,400 OZ (22.43 TONNES)

SILVER

FOR OCT

42 NOTICE(S) FILED TODAY FOR 210,000 OZ/

total number of notices filed so far this month 42 NOTICES FOR: 210,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 8017 DOWN 121

Bitcoin: FINAL EVENING TRADE: $ 8193 UP 150

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A SMALL SIZED 937 CONTRACTS FROM 214,480 DOWN TO 213,543 WITH THE 34 CENT LOSS IN SILVER PRICING AT THE COMEX. WE ALSO HAD A HUGE DISCREPANCY OF 5,315 CONTRACTS FROM PRELIMINARY TO FINAL NUMBERS //OBVIOUS MASSIVE FRAUD//

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR OCT 0,; DEC 1809 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1809 CONTRACTS. WITH THE TRANSFER OF 1809 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1809 EFP CONTRACTS TRANSLATES INTO 9.045 MILLION OZ ACCOMPANYING:

1.THE 34 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.610 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

YESTERDAY, ANOTHER MAJOR ATTEMPT BY THE BANKERS TO COVER THEIR MASSIVE SHORTFALL AT THE SILVER COMEX. OUR OFFICIAL SECTOR//BANKERS AGAIN USED HUGE COPIOUS NON BACKED PAPER IN THEIR SUCCESSFUL ENDEAVOUR TO LOWER SILVER’S PRICE (34 CENTS). HOWEVER TO THEIR SHOCKING SURPRISE, AGAIN AND AGAIN NOBODY LEAVES THE SILVER COMEX ARENA AS THE TOTAL OF OUR TWO EXCHANGES ROSE BY 872 CONTRACTS MAKING THEIR RAID TOTALLY USELESS TO THEM AS THEIR PRIMARY AIM IS TO FLEECE LONGS. THE MAJORITY EITHER MORPHED INTO LONDON FORWARDS OR THEY ARE STANDING FOR DELIVERY HERE AS THEY SEEK OUT PHYSICAL METAL ON BOTH SIDES OF THE POND

.

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF OCT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

34,980 CONTRACTS (FOR 20 TRADING DAYS TOTAL 34,980 CONTRACTS) OR 174.900 MILLION OZ: (AVERAGE PER DAY: 1749 CONTRACTS OR 8.745 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 174.900 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 24.98% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1,724.60 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

SEPT 2019 TOTAL EFP ISSUANCE 174.900 MILLION OZ

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4348 DESPITE THE 34 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 1809 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED AN ATMOSPHERIC AND CRIMINALLY SIZED: 872 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1809 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 937 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 34 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $17.56 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.067 BILLION OZ TO BE EXACT or 153% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT OCT MONTH/ THEY FILED AT THE COMEX: 121 NOTICE(S) FOR 605,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.610 MILLION OZ//

- THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALLISH 2225 CONTRACTS, TO 629,466 DESPITE THE STRONG $8.20 PRICING LOSS WITH RESPECT TO COMEX GOLD PRICING// FRIDAY// /

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUMONGOUS SIZED 12,838 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 12,838 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 629,466,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,613 CONTRACTS: 2225 CONTRACTS DECREASED AT THE COMEX AND 12,838 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 10,613 CONTRACTS OR 1,061,300 OZ OR 33.01 TONNES. YESTERDAY WE HAD A LOSS OF $8.20 IN GOLD TRADING….

AND WITH THAT LOSS IN PRICE, WE HAD A STRONG GAIN IN GOLD TONNAGE OF 33.01 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON AS THE COMEX GOLD VOLUME AND OPEN INTEREST ARE HUGE. THEY WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER THE PRICE OF GOLD BUT UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE LONGS WHICH IS THEIR PRIMARY FUNCTION. THE BANKER/OFFICIAL SECTOR ON FRIDAY CALLED FOR A RAID ON OUR GOLD AS THE SPREADERS ILLEGALLY LIQUIDATED THEIR CONTRACTS AT DIFFERENT TIMES OF THE DAY MAGNIFYING THE ATTACK AND LOSS OF OPEN INTEREST. HOWEVER, THEIR PLAN SOMEHOW WENT ARRAY AS AGAIN NOBODY LEFT THE GOLD COMEX ARENA. THESE CROOKS USE THE SAME MODUS OPERANDI AT EVERY UPCOMING ACTIVE DELIVERY MONTH WHETHER IT IS GOLD OR SILVER ( THAT IS SPREADING LIQUIDATION). THE CFTC REFUSE TO ANSWER ANY QUESTIONS ADDRESSED TO THEM ON THIS OBVIOUS CRIMINAL ACTIVITY (THIS ACTIVITY HAS BEEN ALSO HIGHLIGHTED IN BRIEFS SUBMITTED TO THE F.C.A.{FINANCIAL CONDUCT AUTHORITY}. IN LONDON).

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 163,828 CONTRACTS OR 16,382,800 oz OR 509.57 TONNES (20 TRADING DAY AND THUS AVERAGING: 8191 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAYS IN TONNES: 509.57 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 509.57/3550 x 100% TONNES =14.35% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4660.89 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

SEPT. 2019 TOTAL ISSUANCE: 509.57 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A SMALL SIZED DECREASE IN OI AT THE COMEX OF 2225 DESPITE THE STRONG PRICING LOSS THAT GOLD UNDERTOOK FRIDAY($8.20)) //.WE ALSO HAD A HUMONGOUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 12,838 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 12,838 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 10,613 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

12,838 CONTRACTS MOVE TO LONDON AND 2225 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 33.01 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED DESPITE THE LOSS IN PRICE OF $8.20 WITH RESPECT TO FRIDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had a monstrous: 7,214 notice(s) filed upon for 721,400 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $32.50 TODAY//(COMEX-TO COMEX)

A SMALL 2.06 TONNES OF PAPER GOLD IS WITHDRAWN FROM THE GLD

INVENTORY RESTS AT 922.88 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 58 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV//

/INVENTORY RESTS AT 381.786 MILLION OZ.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A SMALL SIZED 937 CONTRACTS from 214,480 DOWN TO 213,543 AND FURTHER FROM A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR SEPT. 0; FOR DEC 1809: AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1809 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 4378 CONTRACTS TO THE 1809 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 6,187 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 4.36 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ// AND FINALLY SEPT: 43.610 MILLION OZ//

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 34 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1809 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED DOWN 16.98 POINTS OR 0.92% //Hang Sang CLOSED UP 137.46 POINTS OR 0.53% /The Nikkei closed DOWN 123.06 POINTS OR 0.56%//Australia’s all ordinaires CLOSED DOWN .34%

/Chinese yuan (ONSHORE) closed DOWN at 7.1426 /Oil DOWN TO 55.34 dollars per barrel for WTI and 60.35 for Brent. Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1426 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1414 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

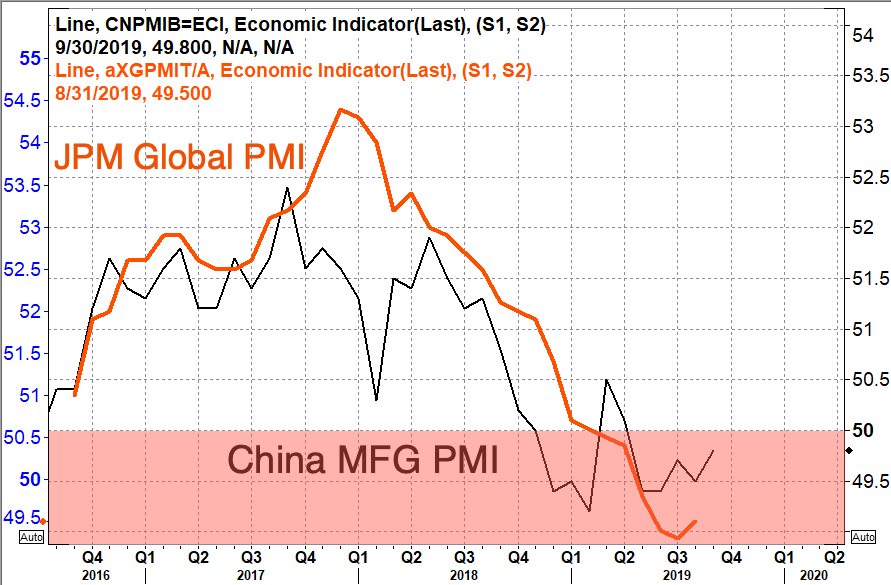

Green shoots in China’s mfg sector? Most likely the data is fudged

(zerohedge)

4/EUROPEAN AFFAIRS

i)Boris Johnson seems to be winning in this ugly Brexit war

a must read…

(Mish Shedlock/Mishtalk)

ii)Tom Luongo’s take on the Brexit affair. I would put my money on Mish Shedlock

iii)Metro bank teeters on bankruptcy after a failed bond sale. It shares collapsed by 95% from 4,000 pence down to a few pennies(Courbishley/WolfStreet)

IV)ITALY

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

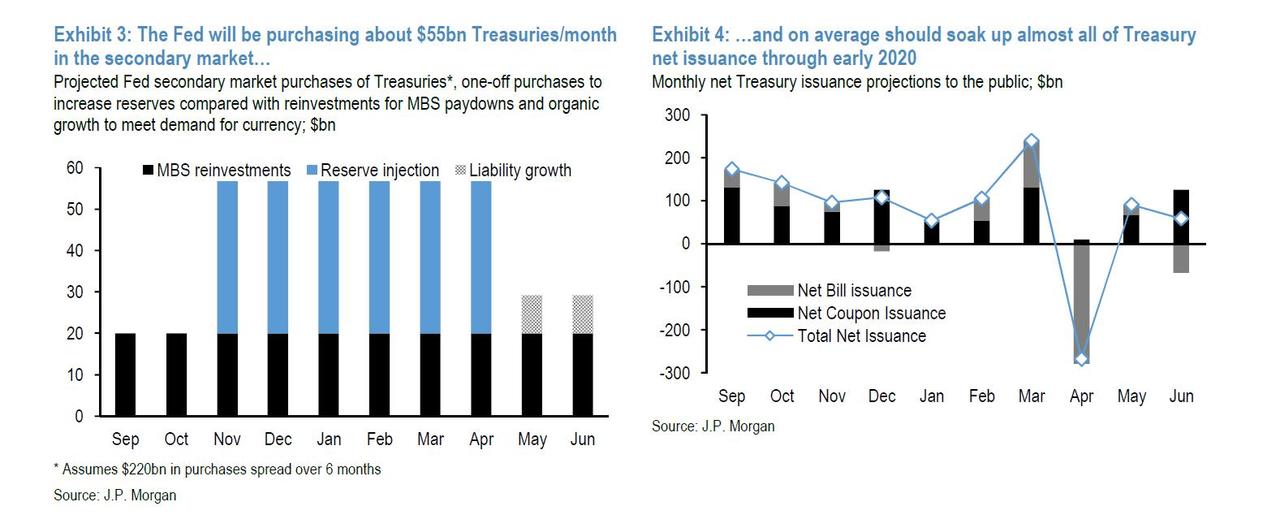

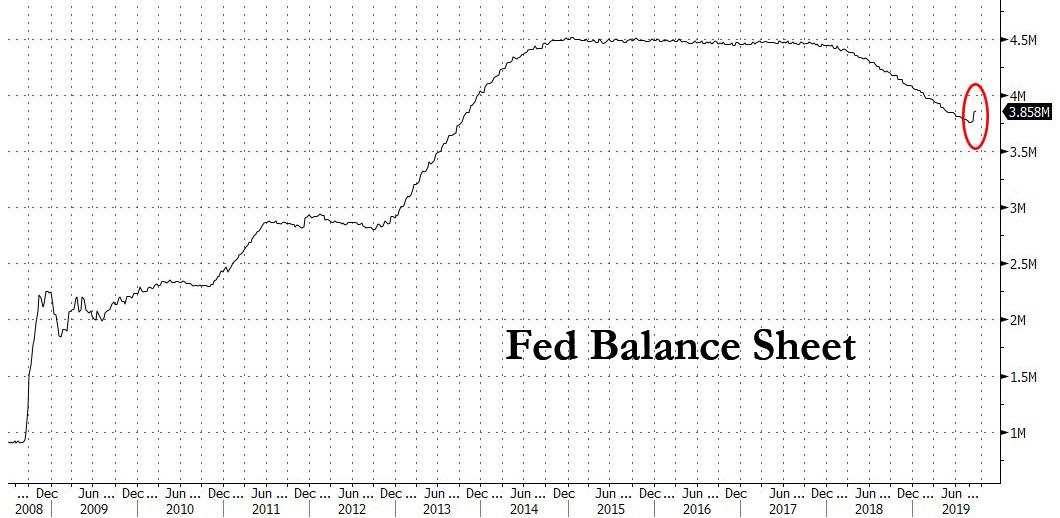

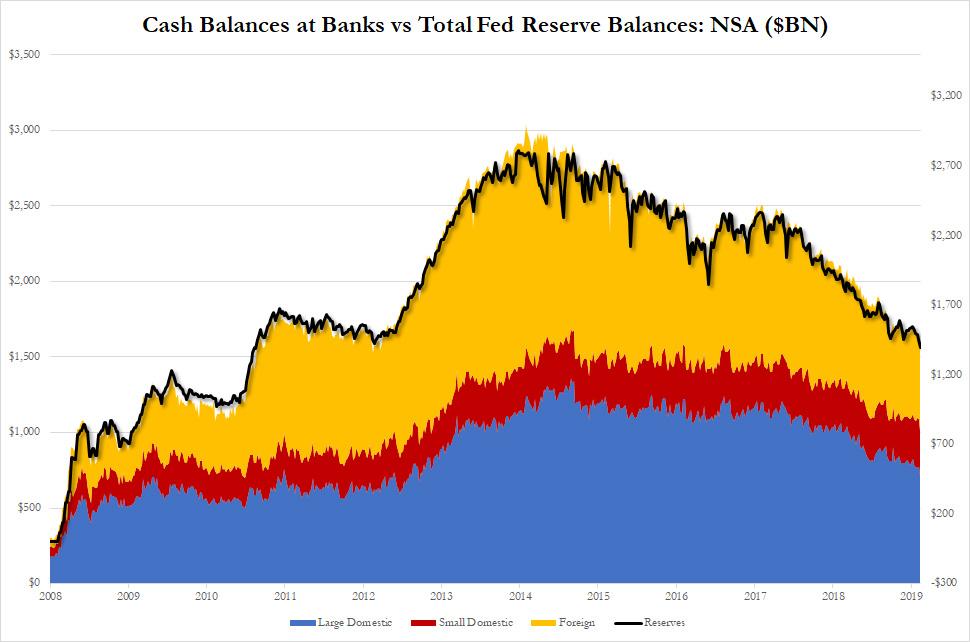

i)Avery Goodman like other analysts believe that QE4 has begun. First with the TOMO and then finally POMO will begin in earnest in November.

(Avery Goodman/GATA)

ii)Alasdair Macleod strongly believes that the failure in the repo market is due to the derivative busts of Deutsche bank

(Alasdair Macleod/GATA)

iii)Schiff still denies the massive intervention of governments in the gold/silver markets

(Chris Powell/GATA)

iv)Hugo Salinas Price on the damage caused by governments on the creation of infinite money

(Hugo/GATA)

v)Why you should join GATA in New Orleans

(Brien Lundin/GATA)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

Chicago area PMI back into contraction area for the 3rd month in the last 4 readings

(zerohedge)

iii) Important USA Economic Stories

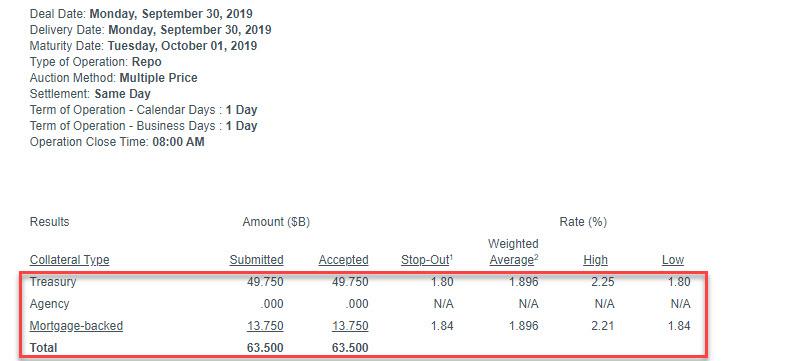

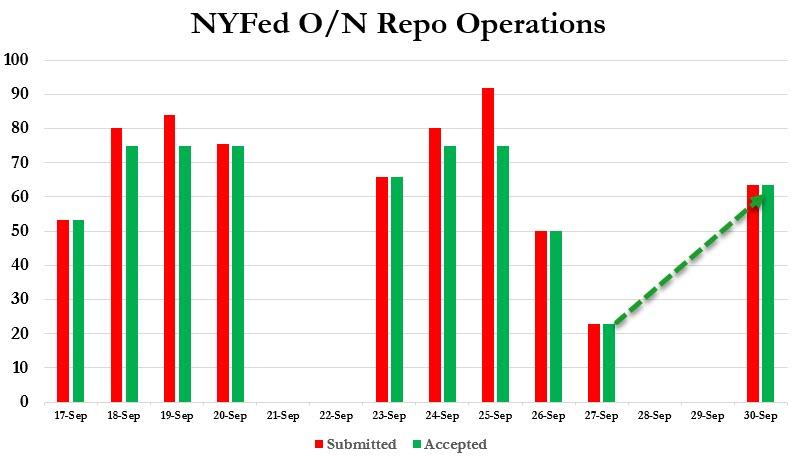

a)Many thought that it was our foreign banks that provided the repo problem last week. In the latest data release it was a few of the large USA banks that were short of liquidity. We await for the Monday numbers..

Third consecutive undersubscribed overnight repo operation/ $63.5 billion in collateral accepted on this last day of Q3. However the collateral rate charged rises by a huge 1% to 2.8%. However this rate should decrease as we enter the new quarter tomorrow and window dressing ceases.

(zerohedge)

c)Forever 21 finally succumbs as retail apocalypse continues. They believe 30,000 jobs is at risk

(zerohedge)

iv) Swamp commentaries)

a)An absolute joke; The Ukrainians reportedly had no idea about Trump withholding 400 million dollars until one month after the call

(zerohedge)

b)Russ Limbaugh has declared what I have been saying: we are in the middle of a cold civil war

c)In a letter to CBS, the attorney for the Whistleblower, states the obvious: that he is in obvious danger as Trump wants to expose him. However they did not say he is in Federal protection

d)This farce continues as House democrats subpoena Giulian over “scheme” to investigate Biden even though the Bidens are absolute crooks

v) King report/some major Swamp stories

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 2 kilobar entries

AND 3 PHONY ENTRIES

total gold withdrawals; 4924.53 oz

i) we had one adjustment from HSBC and this is a phony entry…there is no gold at the comex

i) Out of HSBC: 393,745.737 oz was adjusted out of the customer account and into the dealer account of HSBC

you will see that they will not settle upon this as it is nothing but paper.

i) into Brinks; 603,974.310 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 48,616 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 145,355 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 145,355 CONTRACTS EQUATES to 726 million OZ 104% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -1.50% ((SEPT 30/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.06% to NAV (SEPT 30/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -1.50%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 14.66 TRADING 14.17///DISCOUNT 3.34

END

And now the Gold inventory at the GLD/

SEPT 30/WITH GOLD DOWN $32.50: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.06 TONNES FROM THE GLD /INVENTORY RESTS AT 922.88 TONNES

SEPT 27.WITH GOLD DOWN $8.20 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 924.94 TONNES

SEPT 26//WITH GOLD UP $2.70 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.94 TONNES

SEPT 25/WITH GOLD DOWN $26.90 A HUGE PAPER DEPOSIT OF: 16.42 TONNES//INVENTORY RESTS AT 924.94 TONNES

SEPT 24/WITH GOLD UP $8.65 TODAY: A MONSTROUS CHANGE IN GOLD INVENTORY AT THE GLD: AN OUT OF THIS WORLD DEPOSIT OF 14.37 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 894.15 TONNES

SEPT 23/WITH GOLD UP $16.25 ON THE DAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER ADDITION OF 10.65 TONNES//INVENTORY RESTS AT 894.15 TONNES

SEPT 20/WITH GOLD UP $8.60 ON THE DAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 883.06 TONNES

SEPT 19/WITH GOLD DOWN $8.90 TODAY: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 3.23 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 883.60 TONNES

SEPT 18/WITH GOLD UP $2.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 5.86 TONNES/INVENTORY RESTS AT 880.37 TONNES

SEPT 17/WITH GOLD UP $1.50: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 874.51 TONNES

SEPT 16/WITH GOLD UP $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 5.86 TONNES FROM THE GLD///INVENTORY RESTS AT 874.51 TONNES

SEPT 13/WITH GOLD DOWN $7.75 TODAY: A BIG PAPER WITHDRAWAL OF 2.05 TONNES FROM THE GLD/INVENTORY RESTS AT 880.37 TONNES

SEPT 12//WITH GOLD UP $4.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 11/WITH GOLD UP $5.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 10/WITH GOLD DOWN $11.75 TODAY: A HUGE 7.33 PAPER TONNES OF GOLD WAS WITHDRAWN FROM THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 9/WITH GOLD DOWN $4.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 889.75 TONNES

SEPT 6//WITH GOLD DOWN $9.80: A BIG CHANGE IN GOLD INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 6.15 TONNES//INVENTORY RESTS AT 889.75 TONNES

SEPT 5/WITH GOLD DOWN $33.80 TODAY: A BIG ADDITION (DEPOSIT) OF 5.86 OF PAPER GOLD TONNES PROBABLY ADDED BEFORE THE RAID/EXPECT A HUGE PAPER WITHDRAWAL TOMORROW: INVENTORY RESTS AT 895.90 TONNES

SEPT 4/WITH GOLD UP $5.00 TODAY: A BIG CHANGE: A HUGE PAPER DEPOSIT OF: 11.73 TONNES/INVENTORY RESTS AT ….890.04 TONNES

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SEPT 30/2019/ Inventory rests tonight at 922.88 tonnes

*IN LAST 671 TRADING DAYS: 26.28 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 571- TRADING DAYS: A NET 140.37 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 30/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 381.786 MILLION OZ/

SEPT 27/WITH SILVER DOWN 34 CENTS TODAY/ NO CHANGE IN SILVER INVENTORY AT THE SLV//.INVENTORY RESTS AT 381.786 MILLION OZ/

SEPT 26/WITH SILVER DOWN 12 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.975 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 381.786 MILLION OZ/

SEPT 25.//WITH SILVER DOWN 58 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 377.811 MILLION OZ//

SEPT 24/WITH SILVER DOWN 5 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.338 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 377.811 MILLION OZ//

SEPT 23.2019/WITH SILVER UP 80 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 375.473 MILLION OZ.

SEPT 20/ WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 375.473 MILLION OZ.

SEPT 19/WITH SILVER DOWN 4 CENTS TODAY; A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 1.029 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 375.473 MILLION OZ/

SEPT 18/WITH SILVER DOWN 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 17/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 16/WITH SILVER UP 41 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A PAPER WITHDRAWAL OF 2.899 MILLION OZ OF SILVER LEAVES THE SLV///INVENTORY RESTS AT 376.502 MILLION OZ/

SEPT 13/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 12/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 11/WITH SILVER DOWN ONE CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 10/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 1.778 MILLION PAPER OZ OF SILVER///INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 9/WITH SILVER DOWN 6 CENTS TODAY: A MAMMOTH CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 5.425 MILLION PAPER OZ/INVENTORY RESTS AT 381.179 MILLION OZ../

SEPT 6/WITH SILVER DOWN ANOTHER 60 CENTS TODAY: A RATHER TIMID CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 842,000 PAPER OZ FROM THE SLV///INVENTORY RESTS AT 386.604 MILLION OZ//

SEPT 5/WITH SILVER WHACKED 68 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 4/WITH SILVER UP 28 CENTS TODAY:STRANGE!! A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 708,000 OZ FROM SLV’S INVENTORY:/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 TONNES

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

SEPT 30/2019:

Inventory 381.786 MILLION OZ

iii) Other physical stories:

A picture is worth a 1000 words: no other explanation necessary!!

One glance at the last few years and the gold price action should not be a huge surprise…

Source: Bloomberg

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

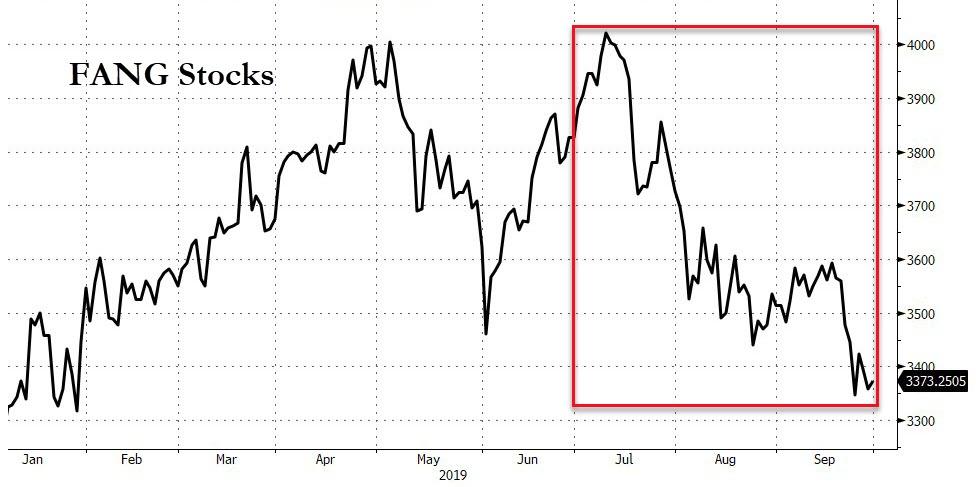

Futures Jump As Markets Downplay Risk Of US-China Trade War Escalation

Unlike last week, when every day was marked by either full-on trade deal euphoria or, as was the case on Friday afternoon, despair amid speculation of trade war escalation, overnight markets were relatively muted and fluctuated in Europe while US equity futures jumped as the lack of explicitly negative trade war news was interpreted as good news. Indeed, investors generally shrugged off reports that Washington is considering delisting Chinese companies from U.S. stock exchanges, with traders downplaying the likelihood of such radical escalation of the U.S.-China trade war.

Bloomberg reported that President Trump was looking at a broader effort to limit U.S. investment in Chinese companies, although Treasury officials denied that this was being considered “at this time“, and it remained unclear how any such delisiting would work. As a result, MSCI’s world equity index, was little changed, down 0.1%. MSCI’s broadest index of Asia-Pacific shares outside Japan also slipped just 0.1%. Some optimism crept into European markets with the Stoxx 600 turning positive, ekeing out a 0.1% gain after opening lower. Markets in Frankfurt, Paris and London were flat.

In the US, futures on all main indexes pointed to a green open, and the dollar spiked higher after the U.S. issued a partial denial that it was discussing new limits on Chinese access to American finance. The concern around the latest Sino-U.S. tensions had caused U.S. stocks to fall on Friday, with the Nasdaq losing 1%. The news also knocked Chinese shares listed on U.S. exchanges on Friday. Alibaba Group and JD.com both lost 5% to 6% on Friday.

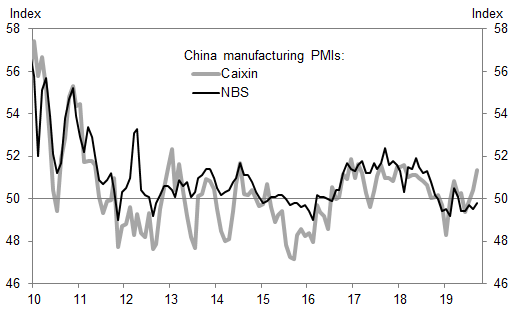

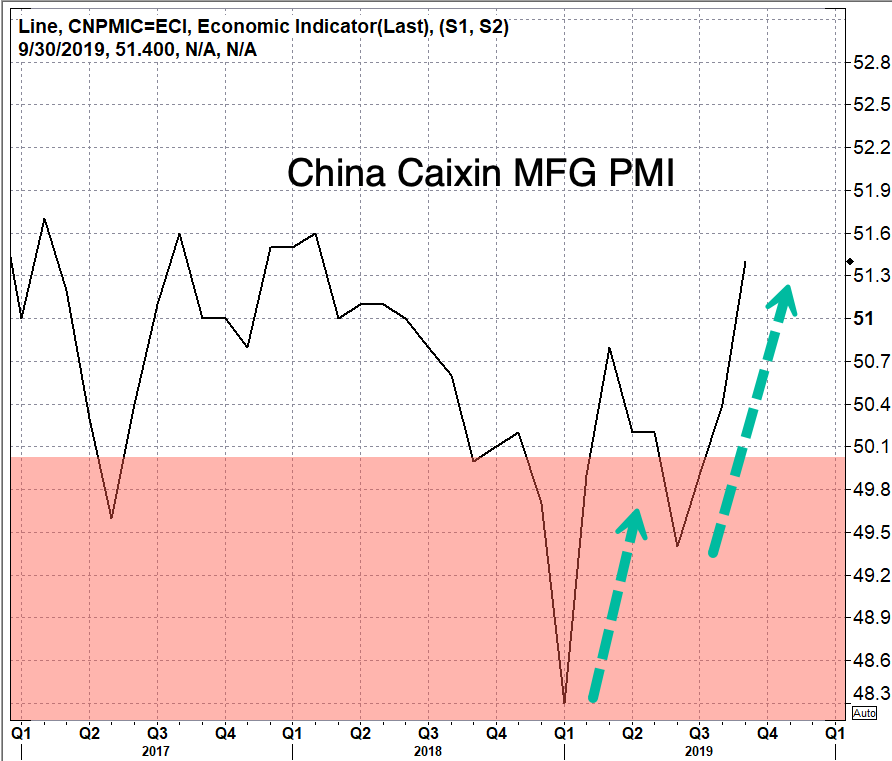

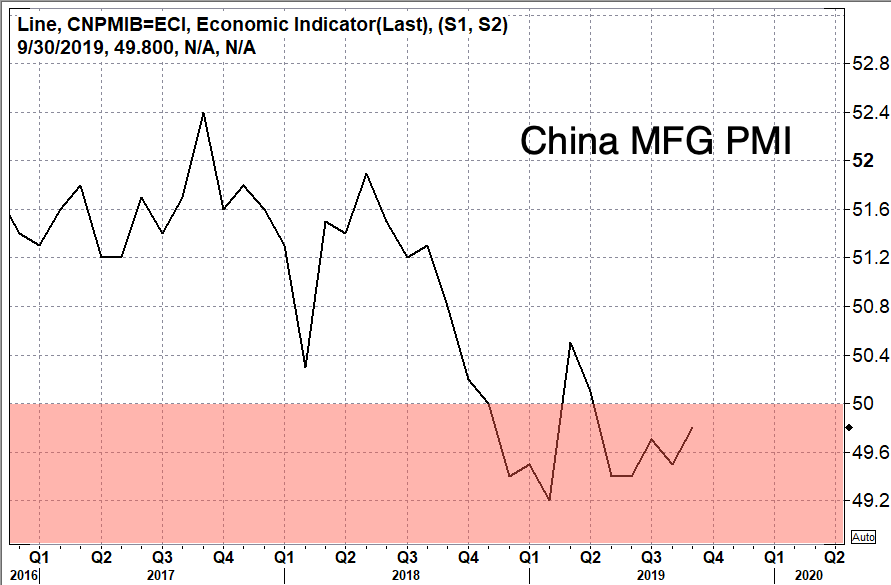

Earlier in the session, Chinese equities slumped almost 1% in the final session before a week-long holiday even though both the official and Caixin manufacturing PMIs beat expectations: the NBS manufacturing PMI increased to 49.8 in September and the Caixin manufacturing PMI rose to 51.4. Financial markets and offices in Taipei closed Monday due to the approach of Typhoon Mitag.

“This is better than what the market was expecting,” said Alessia Berardi, senior economist at Amundi Pioneer, adding that markets were downplaying the likelihood of a major escalation in the trade war by Washington. “The probability of implementing the (delisting) decision for the market is still quite low,” she said.

Overall Asian stocks dropped for a second day, led by utility and health care firms, as Washington’s potential move to restrict U.S. fund flows to Chinese firms dented risk sentiment. Most markets in the region were down, with Japan leading declines and South Korea advancing. The Topix fell 1%, with automakers and pharmaceutical firms among the biggest drags, as Japan’s factory production dropped in August amid a global slowdown. The Shanghai Composite Index retreated 0.9%, driven by Kweichow Moutai and Ping An Insurance Group. Chinese markets will trade only on Monday before a week-long holiday that marks the 70th anniversary of the founding of the People’s Republic of China.

China pledged to continue opening up its financial markets and encourage foreign investment ahead of trade talks with the U.S. India’s Sensex declined 0.5%, as ICICI Bank and Housing Development Finance weighed on the gauge. Indiabulls Housing Finance plunged as much as 38% after the Indian central bank placed curbs on a lender it plans to acquire.

China warned on Monday of instability in international markets from any “decoupling” of China and the United States following the reports, noting a U.S. Treasury response that said there were no immediate plans to block Chinese listings.

Most traders said equity markets thought the threat of delisting was just a tactic before U.S.-China trade talks resume next week. Investors are accustomed to belligerence from Trump before he dials down his rhetoric, said Luca Paolini, chief strategist at Pictet Asset Management.

“It’s a strategy that we have seen in the past – keeping the pressure very high and then settling for whatever deal is possible,” he said. Any progress in talks next month would probably fall short of a comprehensive deal, he added. “It’s more likely than not that there will some kind of agreement that would be more cosmetic in nature.”

Separately, Hong Kong protesters clashed with police for a 17th week with further protests planned for China’s 70th anniversary of Communist rule on Tuesday 1st October. Furthermore, Hong Kong police confirmed an officer fired a live round Sunday near Wan Chai MTR station, according to CNN International Correspondent Will Ripley. Subsequently, China Global Times says Police have received information about Hong Kong protest activity on 1 October creating a highly dangerous situation.

In rates, Treasuries were slightly cheaper across the curve, following wider losses across bunds after ECB President Draghi urged greater public spending in a Financial Times interview; Treasuries were choppy in Asia session while yields edged higher in poor volumes after solid China Caixin PMI print. Bond markets captured the early focus as 10y bund and USTs yields rise 3bp with 10y Aussie yields climbing 8bp to 1.02% ahead of the local session close with no fresh news flow cited for the move. Overall, yield curves bear steepened with the German long-end rising ~3.5bps. Core European bond futures remain around session lows after mixed CPIs readings from the German regions and softer peripheral European data although spreads tighten to core. Gilts and short sterling brush off domestic 2Q GDP data.

In geopolitics, Saudi Crown Prince Mohammed Bin Salman said the attacks on the Saudi oil facilities were an act of war by Iran, hopes military response will not be necessary as a political solution is “much better”. MBS also called on US President Trump to meet with Iranian President Rouhani to craft a new deal. Iranian Government Spokesman notes that they are prepared for a dialogue with Saudi Arabia if they alter their behavior and stop a war in Yemen; follows news of Iranian President Rouhani receiving a letter from Saudi Arabia.

In FX, the Kiwi was the stark underperformer, tumbling to its weakest level in four years Monday following dismal overnight confidence data, while GBPUSD edged back above 1.2300. The Bloomberg Dollar Spot Index was set to end this quarter stronger than all of its G-10 peers, with the Japanese yen seeing the smallest declines and the New Zealand dollar the largest.

In commodities, crude futures drift lower, Iron ore and nickel lead gains in the metals complex while Palladium rises above a record $1,700 an ounce

Expected data include MNI Chicago Business Barometer. Thor Industries is reporting earnings.

Market Snapshot

- S&P 500 futures up 0.4% to 2,974.25

- STOXX Europe 600 up 0.01% to 391.81

- MXAP down 0.4% to 156.37

- MXAPJ down 0.1% to 501.35

- Nikkei down 0.6% to 21,755.84

- Topix down 1% to 1,587.80

- Hang Seng Index up 0.5% to 26,092.27

- Shanghai Composite down 0.9% to 2,905.19

- Sensex down 0.8% to 38,529.84

- Australia S&P/ASX 200 down 0.4% to 6,688.35

- Kospi up 0.6% to 2,063.05

- German 10Y yield rose 1.7 bps to -0.556%

- Euro down 0.05% to $1.0934

- Italian 10Y yield unchanged at 0.486%

- Spanish 10Y yield rose 1.3 bps to 0.163%

- Brent futures down 1.6% to $60.94/bbl

- Gold spot down 0.6% to $1,487.53

- U.S. Dollar Index up 0.1% to 99.21

Top Overnight News from Bloomberg

- The Trump administration has issued a partial — and qualified – – denial to the revelation that it is discussing imposing limits on U.S. investments in Chinese companies and financial markets as China vowed to continue opening its markets to foreign investment

- Johnson hoped to use his Conservative Party’s annual convention to launch his campaign to win the next British general election. Instead, he is fighting for his credibility as prime minister as he faces allegations of sexual impropriety and plots to oust him. To add to that the opposition Labour Party has demanded an investigation into alleged potential conflicts of interest

- The U.K. economy experienced major distortions in the second quarter after firms stockpiled goods in the run-up to the original March 29 Brexit deadline, figures published Monday show. The Office for National Statistics confirmed the economy shrank 0.2% between April and June. It was the first quarterly contraction for seven years

- British businesses are getting increasingly gloomy about the economy as Brexit approaches, according to the Lloyds Business Barometer. A measure of optimism in September fell to its lowest since the immediate aftermath of the 2016 referendum, and concerns about Brexit intensified. A negative impact from Brexit is expected by 43% of businesses now, up from 39%

- Germany’s labor market unexpectedly improved this month, easing concerns that the economy is sliding into recession. The number of people out of work decreased by 10,000 to 2.276 million in September, the first drop in five months. The unemployment rate was at 5%, near a record low.

Asian equities showed a mixed performance after a negative lead from Wall Street in which major bourses fell deeper into the red amid reports which suggested that the White House is mulling limits on portfolio flows into China, albeit a US Treasury official later noted that there are no current plans regarding market access. ASX 200 (-0.4%) turned green as Nufarm shares rose in excess of 25% after the Co. reported an increase in revenue alongside the sale of its South American unit to Sumitomo. Meanwhile, Nikkei 225 (-0.6%) was subdued throughout the session as heavyweight Softbank fell over 2% amid the ongoing concerns surrounding WeWork after CEO Neumann left his position following the failed IPO. Elsewhere, Hang Seng (+0.5%) nursed the initial losses which emanated from continuing disarray in Hong Kong as protesters clash with police for yet another week, with further protests planned for China’s 70th anniversary of Communist rule tomorrow. Losses in Hong Kong later pared amid gains in large-cap energy names and as AB InBev’s Budweiser APAC soared over 5% at its debut today, which was seen as a litmus test for the IPO environment in Hong Kong. Meanwhile, Shanghai Comp (-0.9%) received a short-lived boost after the Chinese Caixin Manufacturing metric beat (see below from RANsquawk analysis). Furthermore, the PBoC skipped open market operations today which resulted in a modest net daily drain of CNY 20bln ahead of the Mainland’s absence for the remainder of the week due to the National Week Holiday.

Top Asian News

- China Factory Outlook Improves in September Ahead of U.S. Talks

- BOJ Paves Way to Buy Fewer Bonds in October to Steepen Curve

- Japan Nuclear Scandal Deepens as Payoff Timelines Widen

- ‘Frightening’ Thai Baht Surge Hurts Tourism, Industry Body Says

Major European bourses (Euro Stoxx 50 +0.3%) are mostly higher, but consolidating within recent ranges ahead of this week’s slate of important macroeconomic data releases, following a mixed AsiaPac session, in which sentiment was initially downbeat on recent negative US/China trade reports that the US was mulling China portfolio flows limits and the delisting of Chinese stocks from US exchanges; although there are no current plans to do so according to a Treasury Official. The sectors are mixed and unreflective of any definitive risk tone. In terms of individual movers; GlaxoSmithKline (+1.0%) are up on the news that the Co’s Phase 3 PRIMA trial for Zejula is the first study which illustrated a significant benefit, which, according to GSK, justifies the earlier acquisition of Tesaro for approximately USD 4.1bln. Saint Gobain (+2.4%) caught a bid on reports that the Co. announced the sale of their construction glass business in Korea. Separately, Ab InBev (-0.2%) are lower, despite the co’s APAC Budweiser unit opening at HKD 27.40/shr, which is above the initial IPO price of HKD 27.0/shr, before extending gains to over 28.0/shr. Elsewhere, BBVA (+1.0%) is higher on the news that the bank may sell EUR 5bln of bad loans to Deutsche Bank (+0.4%). Finally, Whitbread (-5.1%) is under pressure after being downgraded at Barclays.

Top European News

- Funcom Surges as Gaming Giant Tencent Purchases 29% Stake

- KPN Drops After It Cancels Hiring of Proximus’s Leroy as CEO

- Microsoft’s Largest Reseller SoftwareONE Plans Swiss IPO

- Lagarde Inherits ECB Tinged by Bitterness of Draghi Stimulus

In FX, NZD/GBP – Contrasting fortunes for the Kiwi and Pound at the start of the final session of September and Q3, as the former props up the G10 table in wake of a downbeat NBNZ business survey, but the latter shrugs off broadly soft UK data and outperforms in corrective trade following recent weakness. Nzd/Usd is hovering near the base of a 0.6303-0.6250 range, while Cable reclaims 1.2300+ status and Sterling also recoups losses vs the Euro after a test of resistance at 0.8900, but no clean break and a subsequent cross reversal down towards 0.8865. However, the Gbp is on tenterhooks awaiting further political developments and latest moves by opposition party Remainers to request another Brextension rather than risk a no deal departure on October 31.

- NOK/SEK – Marginal divergence between the Scandi Crowns as in line Norwegian retail sales keeps Eur/Nok rooted towards the bottom of 9.9450-9.9180 parameters in contrast to Eur/Sek that is nudging 10.7350 compared to lows of around 10.7060 following recent disappointing Swedish consumption and consumer sentiment reads.

- JPY/CAD/EUR/AUD/CHF – All weaker against a generally firm Greenback, as the DXY holds above 99.000 in a relatively narrow 99.047-216 range, with the Yen paring gains between 107.75-108.00 and flanked by decent option expiries at 107.50 (1.5 bn) and 108.00-05 (1.2 bn), while the Loonie meanders from 1.3225-47 ahead of Canadian PPI data. Elsewhere, the single currency has faded into 1.0950 amidst soft Eurozone inflation updates from Germany’s states and Spain, but Eur/Usd may derive underlying support from a hefty expiry at the 1.0900 strike (2.3 bn) and the fact that the big figure fended off several attempts to the downside last week. Similarly, the Aussie is keeping afloat around 0.6750 and within 1.0740-1.0800 extremes vs its Antipodean rival on the back of a better than expected Caixin Chinese manufacturing PMI and with the jury out on tomorrow’s RBA policy verdict (full preview available in the Research Suite), but the Franc is lagging across the board after a marked decline in the Swiss KOF indicator and downward revision to the previous print. Usd/Chf currently just shy of 0.9950 and Eur/Chf is straddling 1.0850 with latest weekly sight deposits suggesting more intervention.

- EM – Bucking the broad trend of losses vs the Dollar, Turkey’s Lira has climbed over 5.6500 after trade data showing a smaller deficit and typically upbeat comments/forecasts from the Finance Minister, bar a sharp downgrade to 2019 GDP.

In commodities, crude futures are lower, but well within recent ranges, as the market mostly shrugs off recent news flow; Russian oil output for the month of September is lower than in August, according to sources, at 11.24mln BDP (vs 11.29mln BDP). Additionally, following last Friday’s reports of Saudi Arabia agreeing to a partial ceasefire in Yemen, the Iran backed Yemeni Houthis reportedly offered to release 350 prisoners, 3 of whom are Saudis. Separately, an Iranian Government Spokesman said that they are prepared for a dialogue with Saudi Arabia if they alter their behaviour and stop the war in Yemen, following reports that Iranian President Rouhani had received a letter from Saudi Arabia. Spot Gold is lower, in line with the modestly better risk tone, and is back below the USD 1500/oz mark, an area which has been a solid base since mid-August. Separately, Copper prices are higher, after Chinese Caixin Manufacturing surprised to the upside, easing demand concerns in the red metals biggest market, although some of the forward-looking sub-components were more disappointing

US Event Calendar

- 9:45am: MNI Chicago PMI, est. 50, prior 50.4

- 10:30am: Dallas Fed Manf. Activity, est. 1, prior 2.7

DB’s Jim Reid concludes the overnight wrap

A happy wet Monday to you all. Last week we briefly mentioned how the Opposition party here in the U.K. outlined plans for a 4-day work week within a decade. To be honest after the weekend I’ve had ferrying children to parties and having to endure rolling crying tantrums between them, at the moment I would happily vote for a party who suggested a 7-day working week.

The first day of this working week, and the last of Q3, sees us go straight to Asia where Chinese markets have only today (due to holidays for the rest of the week) to digest Friday’s news that the US are considering limiting portfolio flows into China and their companies. The Bloomberg story suggested the options Mr Trump’s team are considering include delisting Chinese companies on US exchanges, limiting US government pension fund exposure to China and even limiting private US investment firm’s access. On Friday the US shares of Alibaba lost -5.2%, JD.com fell c.6% and Baidu down -3.7%. So a big story but the article didn’t suggest that the debate is particularly advanced so a difficult one to price at the moment. If you took it to it’s most negative you’d have to point out the amount of US Treasuries that China hold and the impact that any retaliation might have. A fair amount of water will need to flow under the bridge before we get there though.

Maybe conscious of the impact on the Asian open and follow through to the rest of global markets, a US Treasury spokesman made an emailed statement on Saturday that read that “The administration is not contemplating blocking Chinese companies from listing shares on US stock exchanges at this time”.

This statement has probably calmed the Asian session with bourses trading a lot better than feared on Friday night. The Nikkei (-0.55%) and Shanghai Comp (-0.40%) are still lower but the Hang Seng (+0.52%) and Kospi (+0.38) are up. Elsewhere futures on the S&P 500 are up +0.37% and 10y JGB yields are up +1.8bps to -0.230%.

Overnight, we’ve seen China’s official September PMIs with manufacturing PMI coming in at 49.8 (vs. 49.6 expected), marking the fifth continuous month of contraction while the services PMI came in at 53.7 (vs. 53.9 expected) bringing the composite PMI to 53.1 (vs. 53.0 last month). In terms of underlying details, the new orders component of the manufacturing reading printed at 50.5 (vs. 49.7 last month), marking the first above 50 reading since April while the new export orders component also improved to 48.2 from 47.2 last month. Separately, China’s September Caixin manufacturing PMI stood at 51.4 (vs. 50.2 expected), the highest reading since February 2018. In terms of other overnight data releases, Japan’s August retail sales came in at +2.0% yoy (vs. +0.7% yoy expected) and the preliminary August industrial production stood at -1.2% mom (vs. -0.5% mom expected).

Elsewhere the FT has an an exclusive interview with Mr Draghi this morning as he nears the end of his tenure. The key section is a direct quote where he says that “I (have) talked about fiscal policy as a necessary complement to monetary policy since 2014. Now the need is more urgent than before. Monetary policy will continue to do its job but the negative side effects as you move forward are more and more visible.” He then added, “Have we done enough? Yes, we have done enough — and we can do more. But more to the point what is missing? The answer is fiscal policy, that’s the big difference between Europe and the US.” He also said a long term commitment to a fiscal union was essential for Europe to compete.

Talking of fiscal, new Italian Finance Minister Roberto Gualtieri said that the government will use “all the flexibility available” with the country’s finances and plans “a slight expansion in order to reconcile the balance of public finances and the credibility of our commitment to cut debt,” while adding that any tightening “would have a negative effect on the economy.” On the deficit target, Gualtieri hinted that the number for 2020 would be between this year’s original goal of 2.4% and the revised target of 2.04%. Elsewhere, Ansa reported that the cabinet will present a framework for the budget after a meeting scheduled at 6:30 pm local time today. The deadline for submitting the draft budget to Brussels is October 15. So one to watch.

Market action on Friday was dominated by the US-China capital controls story. The negative impact of that news offset the earlier, positive impact of optimistic comments from President Trump and other officials on the scope for a near-term trade deal. The S&P 500 ultimately closed -1.01% lower on the week (-0.52% on Friday), while the DOW fell only -0.43% (-0.26% Friday) and the NASDAQ dropped -2.19% (-1.13% Friday). The former outperformed due to its greater exposure to bank stocks, which ended +0.26% higher on the week (+1.03% Friday), while the latter was dragged down by its exposure to China trade. Despite the seesawing moves, the VIX only rose +1.9pts on the week (+1.2pts Friday) to 17.3.

In Europe, the STOXX 600 fell a more modest -0.30% (+0.47% Friday), though it had already closed before the selloff in the US session. Bonds rallied across Europe, with the biggest driver being the poor PMI data last Monday which showed the German manufacturing sector reading falling to 41.4, its worst reading in around a decade. Bund yields fell -5.2bps (+0.9bps Friday), while OATs and BTPs rallied -5.9bps (+0.7bps Friday) and -9.8bps (flat on Friday), respectively. The five year-five year inflation swap rate fell below its pre-ECB level at 1.18%, down -6.7bps on the week (-1.2bps Friday) and is now just 5bps away from its all-time low just after Draghi’s Sintra speech in June. In the US, the curve steepened slightly as the front-end rallied more than the long-end, with 2- and 10-year yields down -5.4bps and -4.3bps (-2.6bps and -1.4bps Friday) respectively.

There’s plenty to look forward to this week with the rest of the global PMIs/ISM (manufacturing tomorrow, services Thursday) pretty important before US payrolls at the end of the week. The flash numbers showed a worrying deterioration in services in Europe after months of holding up well in the face of big declines in manufacturing so the final reading will help show more about this trend. Tomorrow sees China celebrate the 70th anniversary of the People’s Republic of China, which will see financial markets closed until October 7. The start of the event will also see a major speech from President Xi Jinping. It’ll be interesting to hear the tone and the substance. In the UK, the Conservative Party Conference is currently taking place until Wednesday, with PM Johnson giving his first conference speech as party leader on the final day unless it’s brought forward by events overtaking them in Parliament. On Friday the government suggested they would outline firm legal proposals for a Brexit deal in days after the conference. So we could know more about that by the end of the week. The PM may also face a vote of no confidence this week if press stories are to be believed. So a busy week in U.K. politics awaits.

Finally it’s a busy week for Fed-speak with all but three of the seventeen principals speaking, including all five Governors and nine of twelve regional Fed Presidents. For more on these see DB’s Brett Ryan’s preview of the US week ahead here.

3A/ASIAN AFFAIRS

I)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED DOWN 16.98 POINTS OR 0.92% //Hang Sang CLOSED UP 137.46 POINTS OR 0.53% /The Nikkei closed DOWN 123.06 POINTS OR 0.56%//Australia’s all ordinaires CLOSED DOWN .34%

/Chinese yuan (ONSHORE) closed DOWN at 7.1426 /Oil DOWN TO 55.34 dollars per barrel for WTI and 60.35 for Brent. Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1426 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1414 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

Green shoots in China’s mfg sector? Most likely the data is fudged

(zerohedge)

Green Shoots: China’s Caixin Mfg PMI Expands Fastest In 19 Months, But Doubts Remain

What a coincidence: economic green shoots appeared in China just in time for the start of the country’s National Day and Golden Week holidays, as both the official and Caixin manufacturing PMIs rose in September.

Specifically, the NBS manufacturing PMI increased to 49.8 in September and the Caixin manufacturing PMI rose to 51.4, with both readings coming in above expectations. Sub-indexes in the two surveys all pointed to stronger production, new orders and higher price pressures in the manufacturing sector. In contrast, the NBS non-manufacturing PMI edged down 0.1pp on the back of a weaker construction PMI.

China’s Caixin manufacturing Purchasing Managers’ Index, published on Monday, and which unlike the official PMI is a measurement of economic activity at smaller, privately-owned companies, showed China’s factory activity expanded at the fastest pace in 19 months in Sept., with a reading of 51.4, up from 50.4 in Aug., the highest level since early 2018.

And while China’s official manufacturing PMI contracted for a fifth month in Sept, amid the ongoing threats of a China-US trade war, it printed slightly higher to 49.8, from 49.5 in Aug., if still below the 50-level that separates it from contraction and expansion.

While there are conflicting signals of an economic rebound in China, and goalseeked number meant for political consumption will hardly change the narrative, manufacturers continue to deal with slowing domestic growth and an escalating trade war that has slowed global trade volumes. Trade talks between Washington and Beijing are expected to resume next week despite President Trump consideration to delist Chinese firms from US markets.

Meanwhile, economists don’t expect the slight manufacturing rebound in China to sustain into late year, but rather turn back down.

“We believe the official manufacturing PMI may decline again, the growth slowdown could gather pace and (financial)markets could become more volatile in coming months,” economists at Nomura said.

To be sure, Nomura revised its 3Q19 growth forecast for China to 5.9% and its 4Q19 view to 5.8%, decreasing from the 6.2% forecast in 2Q19. The note cited escalating trade war, slowing industrial production, waning real estate markets, and a construction slowdown.

Others were just as skeptical, with analysts at Citi saying that “even if there is a ceasefire, the damage is already partly done because of elevated business uncertainties. The government will certainly step up fiscal and monetary efforts to boost domestic demand, which we believe can help stabilize, probably not accelerate, economic growth.”

A look below the headline numbers showed that export demand remained weak, with orders sliding for the 16th straight month, an ominous sign for China’s export-heavy economy.

China’s manufacturing PMIs followed a weak industrial production print that hit 17.5-year lows last month, while factory deflation deepened.

Martin Lynge Rasmussen, a China economist at Capital Economics, said in a note that “China’s fiscal stance is unlikely to be loosened during the remainder of the year, we think the PBOC will find it an increasingly hard sell to refrain from more decisive monetary easing.”

To boost the economy, the PBOC lowered banks’ reserve requirements seven times since 2018 to spark more credit creation. China has cut its new benchmark lending rate for the second month in a row. However, economists warn that monetary policy easing in a downturn might not be as effective as before, considering China’s record debt levels, especially in the real estate market.

Furthermore, while Beijing was hoping that a strong services sector would counter the manufacturing slowdown, that appears to not be the case, with the non-manufacturing PMI in Sept. printed at 53.7, slightly down from August’s 53.8, although the convergence is so far weaker than in Europe where both the Manufacturing and Service PMIs are almost equal.

While oil dipped as China’s manufacturing, and non-manufacturing surveys remained weak, with no signs of a robust recovery but rather more slowing into the late year, futures rebounded and bond yields rose on the stronger than expected Caixin PMI. Ironically, stock in China traded lower on the PMIs, with the CSI 300 and Shanghai Composite both suffering a late session sell-off, and sliding down about 1%. Chinese shares only traded on Monday, ahead of the country’s National Day celebration that will last through Oct. 7.

China’s Yuan weakened from 7.12 to 7.14 after the PMI print. It jumped on Friday from 7.11 to 7.15 after President Trump announced new plans to delist Chinese companies from US stock exchanges.

Elsewhere, UST futures slipped on China PMI prints. The JGB curve moved higher ahead of BOJ’s Oct. buying plan announcement, while currencies were little change in the overnight session, with the USDJPY slightly firmer at 107.75.

4/EUROPEAN AFFAIRS

Boris Johnson seems to be winning in this ugly Brexit war

a must read…

(Mish Shedlock/Mishtalk)

Brexit “Surrender” Strategy: Winning Ugly

Authored by Michael Shedlock via MishTalk,

Boris Johnson and his political strategist Dominic Cummings have labeled the efforts by Parliament a “Surrender” act…

Surrender Act

Boris Johnson labels the acts of Parliament to stop No Deal a “Surrender Act”.

This is correct, of course.

If you take away the EU’s incentives to negotiate, they are less likely to do so.

It’s not a complete white flag as Johnson has other, albeit undisclosed options, in which he proclaims two seemingly contradictory ideas.

- He will abide by the Benn legislation seeking an extension

- He will not ask for an extension

Incite Violence

As noted by the Guardian Live blog, Amber Rudd says Boris Johnson’s language ‘Does Incite Violence’

The claim is preposterous.

The Labour MP Jess Phillips says she has received more threats after an incident outside her constituency office on Thursday when a man allegedly tried to smash her windows. She showed Sky News a message that said: “Unless you change your attitude, be afraid, be very afraid.”

The Labour MP David Lammy has criticised the columnist Brendan O’Neill after he said on BBC Politics Live that the delay to Brexit should have sparked riots. It came after the Times quoted an unnamed senior cabinet minister today who warned the country risked a “violent, popular uprising” if a second referendum overturned the result of the first.

Why Violence Picked Up

Violence has picked up, but “surrender” has little to do with it.

Rather, it’s the very nature of this heated campaign, fueled mostly by Remainers, commentators, and even official Labour Party policy that had led to violence.

Scrap Controls on Immigration

Please note Labour to Scrap Controls on Immigration and Hand Foreign Nationals the Right to Vote

Jeremy Corbyn will scrap controls on immigration and hand foreign nationals the right to vote in future elections and referendums if Labour wins power.

The Labour leader will head into the next election promising to extend freedom of movement to migrants around the world, along with abolishing detention centres, under plans approved on Wednesday.

Despite Mr Corbyn’s team being privately opposed to the plan, delegates at Labour’s annual conference in Brighton unanimously backed a motion which commits the party to “free movement, equality and rights for migrants”. The motion commits Labour to oppose any future immigration system which includes caps on numbers or targets, and which assesses a migrant’s suitability based on their income or usefulness to businesses.

And it requires Labour to commit to the proposals in its next election manifesto – meaning a complete reversal of its 2017 pledge to end free movement after Brexit.

No Immigration Controls and Voting Rights for Foreigners!

Might not that idea lead to violence?

Which Party Incites Violence?

spiked@spikedonlineJess Phillips once said she would knife Jeremy Corbyn ‘in the front’. Ed Davey said Remainers should unite to ‘decapitate’ Boris Johnson. John McDonnell still won’t apologise for repeating a joke about ‘lynching’ a Tory MP. These people are hypocrites: https://www.spiked-online.com/2019/09/26/four-times-remainers-used-toxic-language/ …

Four times Remainers used ‘toxic’ language

Leading Remainers have said far worse things than Boris Johnson has.

spiked-online.com

Surrender vs Decapitate

Big Girly Humbug@HumbugMcOutrageBoris saying “surrender act” encourages violence towards MPs, apparently. Lib-Dems don’t have a problem with an MP wanting to decapitate our Prime Minister, though.

Which side, if you had to pick one, is inciting violence?

This isn’t close. Let’s move on to Eurointelligence, emphasis mine.

Eurointelligence Comments

- Boris Johnson’s aggression and his use of the term surrender act are deliberate strategic choices, based on intensive polls;

- The latest polls show him widening the lead over Labour and managing to fend off the Brexit Party;

- We argue that the strategy is ugly, but it is working;

What is widely underestimated is the sheer unpopularity of the Brexit extensions. We recalled a Tory MP telling us in June that they had underestimated the electoral effect of the April extension, which resulted in the victory of the Brexit Party at the European elections.

Experience has taught not to predict elections, and certainly not elections that have not even been scheduled. But one micro prediction we are happy to make is that the person who extends will not be elected in a general election. That person might well be Jeremy Corbyn. If there ever were a government of national unity, it would be under his leadership. We don’t want to discount that possibility completely, but we don’t think that Labour would do itself any favours by forcing a Brexit extension followed immediately by an election. Just as we don’t think the Tories would do themselves any favours with a no-deal Brexit followed immediately by an election.

Boris Johnson’s bulldozing strategy is not pretty, but it is working. His repeated use of the term surrender bill strikes a cord not only with core Tory voters, but with many people in the country. Steven Swinford of the Times tells us that the Tories have done a lot of polling on this specific term, and they have come to the conclusion that it damages the Labour Party. We are reminded of the late 1980s, when it was Labour Party that used the damaging term of a poll tax to describe what was officially known as the community charge. It was the poll tax that sank Margaret Thatcher’s government – not her position on Europe.

The YouGov poll, with polling done on Sep 25, shows the Conservatives at 33% and LibDems and Labour both at 22%. This would translate into 348 seats for the Tories which is an absolute majority of 30, 163 for Labour and 77 for the LibDems. The Brexit Party scores 14% but does not get a single seat.What one needs to understand about this and other polls is the interplay of two conflicting dynamics. On the pro-Brexit side the Tories are competing with the Brexit Party. The pro-Remain vote is split between Labour and the LibDems. Johnson is managing to squeeze out the Brexit Party more than Labour is managing to squeeze out the LibDems.

It is best to understand the relation between percentage votes and seats in the UK in terms of thresholds. For the LibDems to get more seats than Labour, they would need to poll a lot more than 22%. At 14%, the Brexit Party’s potential to deprive the Tories of seats is limited only to a few marginals. But, once they get above 20%, they would become as dangerous to the Tories as the LibDems are to Labour.

Next week, the Tories will hold their party conference in Manchester despite the vote in the Commons against a customary recess. We expect another rabble-rousing performance by Johnson. Since he became leader, the party’s fundraising has skyrocketed. September was their best month ever. There is a lot of support for him from business.

Neither Careless Nor Casual

Similarly the Guardian reports PM’s divisive ‘surrender bill’ phrase is neither careless nor casual.

Part of the fury among MPs about Boris Johnson’s inflammatory rhetoric is that it appears to be a deliberate, election-driven strategy.

But the situation is made worse by the suspicion that it is neither careless nor casual – but rather a concerted effort to whip up anger in the country against MPs in order to motivate pro-Brexit voters to back him at the polls.

Johnson’s language about a “surrender bill” is calculated to cast his opponents as people colluding with foreign powers to block Brexit. It was not a flippant, one-off comment, as the prime minister has used the words at least eight times in the House of Commons. He also told Conservative MPs that he was determined to continue using those words.

This is the hallmark of Dominic Cummings, the former Vote Leave architect who is now Johnson’s most senior adviser. Jeremy Corbyn, the Labour leader, has also highlighted its similarities with the language of rightwing populist demagogues such as Donald Trump. “He is whipping up division with language that’s indistinguishable from the far right,” the Labour leader said in his conference speech this week.

Accurate Assessment

Indeed the language is neither careless, nor casual.

Rather, the language is an accurate assessment of the matter.

If you remove the strongest negotiation tactic someone has, the other side is less likely to negotiate.

Period.