GOLD:

$1482.65 UP $15.25 (COMEX TO COMEX CLOSING)

Silver:$17.28 UP 30 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1480.50

silver: $17.26

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 120/283

EXCHANGE: COMEX

CONTRACT: OCTOBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,465.700000000 USD

INTENT DATE: 09/30/2019 DELIVERY DATE: 10/02/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 H GOLDMAN 48

092 C DEUTSCHE BANK 11

118 H MACQUARIE FUT 58

657 C MORGAN STANLEY 1

661 C JP MORGAN 29

661 H JP MORGAN 120

686 C INTL FCSTONE 9

690 C ABN AMRO 141 5

737 C ADVANTAGE 49 10

800 C MAREX SPEC 41 5

880 H CITIGROUP 33

905 C ADM 3 3

____________________________________________________________________________________________

TOTAL: 283 283

MONTH TO DATE: 7,497

NUMBER OF NOTICES FILED TODAY FOR OCT CONTRACT: 283 NOTICE(S) FOR 28,300 OZ (0.8802 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 7497 NOTICES FOR 749700 OZ (23.32 TONNES)

SILVER

FOR 0CT

585 NOTICE(S) FILED TODAY FOR 2,925,000 OZ/

total number of notices filed so far this month: 706 for 3,530,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 8312 UP 22

Bitcoin: FINAL EVENING TRADE: $ 10640 UP 823

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A TINY SIZED 255 CONTRACTS FROM 213,543 DOWN TO 213,288 DESPITE THE HUGE 58 CENT LOSS IN SILVER PRICING AT THE COMEX. AGAIN IN SILVER NOBODY LEFT THE SILVER COMEX ARENA

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR OCT 0,; DEC 1726 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1726 CONTRACTS. WITH THE TRANSFER OF 1726 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1726 EFP CONTRACTS TRANSLATES INTO 8.63 MILLION OZ ACCOMPANYING:

1.THE 58 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ STANDING IN AUGUST.

43.030 MILLION OZ STANDING IN SEPT. (HUGE)

5.925 MILLION OZ INITIALLY STANDING IN OCT.

YESTERDAY, ANOTHER MAJOR ATTEMPT BY THE BANKERS TO COVER THEIR MASSIVE SHORTFALL AT THE SILVER COMEX AS ANOTHER RAID WAS INITIATED. OUR OFFICIAL SECTOR//BANKERS AGAIN USED HUGE COPIOUS NON BACKED PAPER IN THEIR SUCCESSFUL ENDEAVOUR TO WHACK SILVER’S PRICE (58 CENTS). HOWEVER TO THEIR SHOCKING SURPRISE, AGAIN AND AGAIN NOBODY LEAVES THE SILVER COMEX ARENA AS THE TOTAL OF OUR TWO EXCHANGES ROSE BY 1575 CONTRACTS MAKING THEIR RAID TOTALLY USELESS TO THEM AS THEIR PRIMARY AIM IS TO FLEECE LONGS. THE MAJORITY EITHER MORPHED INTO LONDON FORWARDS OR THEY ARE STANDING FOR DELIVERY HERE AS THEY SEEK OUT PHYSICAL METAL ON BOTH SIDES OF THE POND

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF OCT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF OCT:

1726 CONTRACTS (FOR 1 TRADING DAY TOTAL 1726 CONTRACTS) OR 8.630 MILLION OZ: (AVERAGE PER DAY: 1726 CONTRACTS OR 8.630 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 8.630 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 1.23% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1680.73 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

SEPT 2019 TOTAL EFP ISSUANCE 174.900 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 255, DESPITE THE HUGE 58 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 1726 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 1471 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1726 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 255 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 58 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $16.98 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.067 BILLION OZ TO BE EXACT or 153% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 585 NOTICE(S) FOR 2925,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ// OCT: 5.925 MILLION OZ/

- THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

IN GOLD, THE COMEX OPEN INTEREST FELL BY A HUMONGOUS SIZED 19,123 CONTRACTS, TO 610,343 ACCOMPANYING THE HUGE $32.50 PRICING LOSS WITH RESPECT TO COMEX GOLD PRICING// YESTERDAY// /

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 10,382 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 10,382 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 610,343,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A CONSIDERABLE LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8741 CONTRACTS: 19,123 CONTRACTS DECREASED AT THE COMEX AND 10,382 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 8741 CONTRACTS OR 874,100 OZ OR 27.188 TONNES. YESTERDAY WE HAD A HUGE LOSS OF $32.50 IN GOLD TRADING….AND WITH THAT LOSS IN PRICE, WE HAD A STRONG LOSS IN GOLD TONNAGE OF 27.188 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON AS ANOTHER RAID WAS INITIATED. THE BANKERS WERE VERY SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE WHICH MEANT THAT NO UNDERWRITTEN CONTRACT WOULD BE EXERCISED. THEY WERE MILDLY SUCCESSFUL IN FLEECING SOME GOLD LONGS FROM THE GOLD ARENA.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT : 10,382 CONTRACTS OR 1,038,200 oz OR 32.29 TONNES (1 TRADING DAY AND THUS AVERAGING: 10,382 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAYS IN TONNES: 32.29 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 32.29/3550 x 100% TONNES =0.909% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4439.92 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

SEPT. 2019 TOTAL ISSUANCE: 509.57 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED DECREASE IN OI AT THE COMEX OF 19,123 WITH THE HUGE PRICING LOSS THAT GOLD UNDERTOOK YESTERDAY($32.50)) //.WE ALSO HAD A HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 10,382 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 10,382 EFP CONTRACTS ISSUED, WE HAD A CONSIDERABLE AND CRIMINALLY SIZED LOSS OF 8,741 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

10,382 CONTRACTS MOVE TO LONDON AND 19,123 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE LOSS IN TOTAL OI EQUATES TO 27.188 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED WITH THE LOSS IN PRICE OF $32.50 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 283 notice(s) filed upon for 28,300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP$15.25 TODAY//(COMEX-TO COMEX)

A HUGE PAPER WITHDRAWAL OF 2.05 TONNES

INVENTORY RESTS AT 920.83 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 30 CENTS TODAY:

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//

A PAPER DEPOSIT OF 1.87 MILLION OZ INTO THE SLV

/INVENTORY RESTS AT 383.656 MILLION OZ.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TINY SIZED 255 CONTRACTS from 213,543 DOWN TO 213,288 AND FURTHER FROM A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR OCT. 0; FOR DEC 1726: AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1726 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 255 CONTRACTS TO THE 1726 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 1471 OPEN INTEREST CONTRACTS DESPITE THE RAID. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 7.355 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ// SEPT: 43.030 MILLION OZ//AND FINALLY OCT: 5.925 MILLION OZ//

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 58 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1726 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN //Hang Sang CLOSED /The Nikkei closed UP 129.40 POINTS OR 0.59%//Australia’s all ordinaires CLOSED UP .77%

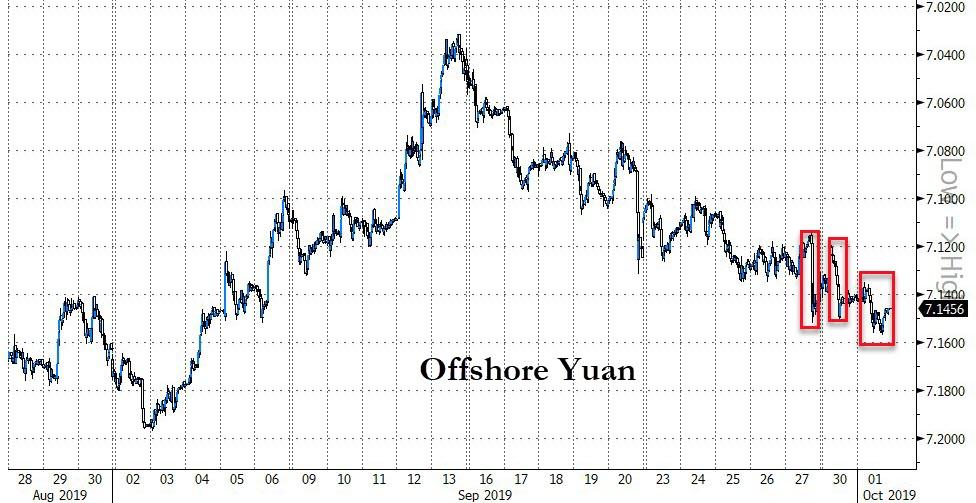

/Chinese yuan (ONSHORE) closed DOWN at 7.1483 /Oil UP TO 54.30 dollars per barrel for WTI and 59.77 for Brent. Stocks in Europe OPENED MOSTLY RED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1483 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1485 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

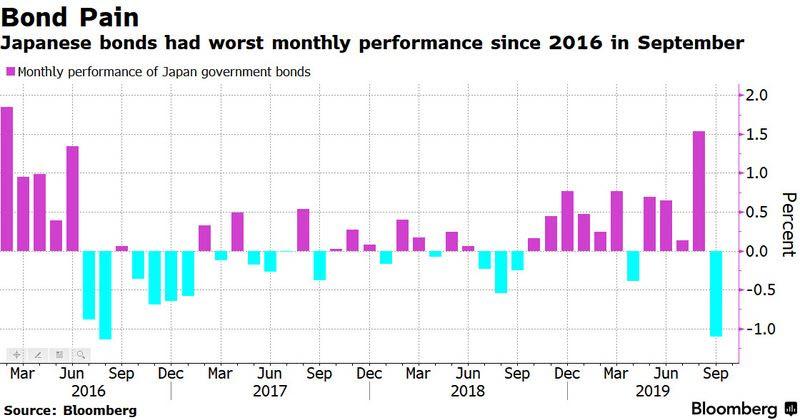

With the central bank of Japan stating that it may not buy Japanese bonds in October, investors ran for cover as bond prices collapsed. Yields rose around the globe as now it may not be safe to front run bond purchases anymore. Japan’s central bank owns just too many bonds.

(zerohedge)

3C CHINA

i)The Pig Ebola is killing China as over 140 billion dollars worth of pork meat has been destroyed. Pork prices are now at record levels.

(zerohedge)

ii)Hong Kong citizens protest again on Tuesday on a day coinciding with the 70th anniversary of Communist rule in China

(zerohedge)

4/EUROPEAN AFFAIRS

the EU is now ready to give a time limit on the Irish backstop

(zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

i)As more and more countries shift away from the dollar it’s share of global currency reserves falls. It is now at its lowest level since 2013

(Reuters/GATA)

ii)They are now beginning to understand that negative rates are having a devastating effect on markets because of the pricing of risk

(Bloomberg/GATA)

iii)No question about it, helicopter money or direct funding of government is only one step away

Rees/London Telegraph/GATA)

iv)We now hear that Deutsche bank’s headquarters were raided last week. It is Pam and Russ Martens contention that banks are refusing to loan any money to DB

(courtesy Russ and Pam Martens/Wall Street on Parade)

v)China will still import close to 1700 tonnes of gold this year.

(Lawrie Williams)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

iii) Important USA Economic Stories

(zero hedge)

b)Here is how billions of loans are exposed to a potential WeWork bankruptcy

c)USA manufacturing is the weakest in 10 years(zerohedge)

iv) Swamp commentaries)

a)Trump asked the Australian PM months ago to investigate the origins of the Mueller probe. And now guess what we have a new whistleblower

(zerohedge)

b)This is so true: Adam Schiff does epitomize the total collapse of the Democratic party’s integrity

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 1 kilobar entries

total gold withdrawals; 128.60 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 82,152 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 102,294 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 102,294 CONTRACTS EQUATES to 511 million OZ 73.0% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.47% ((OCT 1/2019)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.09% to NAV (OCT 1/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -1.47%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 14.77 TRADING 14.34///DISCOUNT 2.94

END

And now the Gold inventory at the GLD/

OCT 1/WITH GOLD UP $15.25 A HUGE PAPER WITHDRAWAL OF 2.05 TONNES FROM THE GLD///INVENTORY REST AT 920.83 TONNES

SEPT 30/WITH GOLD DOWN $32.50: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.06 TONNES FROM THE GLD /INVENTORY RESTS AT 922.88 TONNES

SEPT 27.WITH GOLD DOWN $8.20 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 924.94 TONNES

SEPT 26//WITH GOLD UP $2.70 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.94 TONNES

SEPT 25/WITH GOLD DOWN $26.90 A HUGE PAPER DEPOSIT OF: 16.42 TONNES//INVENTORY RESTS AT 924.94 TONNES

SEPT 24/WITH GOLD UP $8.65 TODAY: A MONSTROUS CHANGE IN GOLD INVENTORY AT THE GLD: AN OUT OF THIS WORLD DEPOSIT OF 14.37 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 894.15 TONNES

SEPT 23/WITH GOLD UP $16.25 ON THE DAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER ADDITION OF 10.65 TONNES//INVENTORY RESTS AT 894.15 TONNES

SEPT 20/WITH GOLD UP $8.60 ON THE DAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 883.06 TONNES

SEPT 19/WITH GOLD DOWN $8.90 TODAY: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 3.23 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 883.60 TONNES

SEPT 18/WITH GOLD UP $2.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 5.86 TONNES/INVENTORY RESTS AT 880.37 TONNES

SEPT 17/WITH GOLD UP $1.50: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 874.51 TONNES

SEPT 16/WITH GOLD UP $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 5.86 TONNES FROM THE GLD///INVENTORY RESTS AT 874.51 TONNES

SEPT 13/WITH GOLD DOWN $7.75 TODAY: A BIG PAPER WITHDRAWAL OF 2.05 TONNES FROM THE GLD/INVENTORY RESTS AT 880.37 TONNES

SEPT 12//WITH GOLD UP $4.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 11/WITH GOLD UP $5.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 10/WITH GOLD DOWN $11.75 TODAY: A HUGE 7.33 PAPER TONNES OF GOLD WAS WITHDRAWN FROM THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 9/WITH GOLD DOWN $4.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 889.75 TONNES

SEPT 6//WITH GOLD DOWN $9.80: A BIG CHANGE IN GOLD INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 6.15 TONNES//INVENTORY RESTS AT 889.75 TONNES

SEPT 5/WITH GOLD DOWN $33.80 TODAY: A BIG ADDITION (DEPOSIT) OF 5.86 OF PAPER GOLD TONNES PROBABLY ADDED BEFORE THE RAID/EXPECT A HUGE PAPER WITHDRAWAL TOMORROW: INVENTORY RESTS AT 895.90 TONNES

SEPT 4/WITH GOLD UP $5.00 TODAY: A BIG CHANGE: A HUGE PAPER DEPOSIT OF: 11.73 TONNES/INVENTORY RESTS AT ….890.04 TONNES

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

OCT 1/2019/ Inventory rests tonight at 920.83 tonnes

*IN LAST 672 TRADING DAYS: 28.33 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 572- TRADING DAYS: A NET 138.32 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

OCT 1.2019 //WITH SILVER UP 30 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 1.87 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.656 MILLION OZ//

SEPT 30/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 381.786 MILLION OZ/

SEPT 27/WITH SILVER DOWN 34 CENTS TODAY/ NO CHANGE IN SILVER INVENTORY AT THE SLV//.INVENTORY RESTS AT 381.786 MILLION OZ/

SEPT 26/WITH SILVER DOWN 12 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.975 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 381.786 MILLION OZ/

SEPT 25.//WITH SILVER DOWN 58 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 377.811 MILLION OZ//

SEPT 24/WITH SILVER DOWN 5 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.338 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 377.811 MILLION OZ//

SEPT 23.2019/WITH SILVER UP 80 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 375.473 MILLION OZ.

SEPT 20/ WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 375.473 MILLION OZ.

SEPT 19/WITH SILVER DOWN 4 CENTS TODAY; A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 1.029 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 375.473 MILLION OZ/

SEPT 18/WITH SILVER DOWN 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 17/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 16/WITH SILVER UP 41 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A PAPER WITHDRAWAL OF 2.899 MILLION OZ OF SILVER LEAVES THE SLV///INVENTORY RESTS AT 376.502 MILLION OZ/

SEPT 13/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 12/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 11/WITH SILVER DOWN ONE CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 10/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 1.778 MILLION PAPER OZ OF SILVER///INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 9/WITH SILVER DOWN 6 CENTS TODAY: A MAMMOTH CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 5.425 MILLION PAPER OZ/INVENTORY RESTS AT 381.179 MILLION OZ../

SEPT 6/WITH SILVER DOWN ANOTHER 60 CENTS TODAY: A RATHER TIMID CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 842,000 PAPER OZ FROM THE SLV///INVENTORY RESTS AT 386.604 MILLION OZ//

SEPT 5/WITH SILVER WHACKED 68 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 4/WITH SILVER UP 28 CENTS TODAY:STRANGE!! A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 708,000 OZ FROM SLV’S INVENTORY:/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 TONNES

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

OCT 1/2019:

Inventory 383.656 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.17/ and libor 6 month duration 2.06

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .11

XXXXXXXX

12 Month MM GOFO

+ 2.03%

LIBOR FOR 12 MONTH DURATION: 2.03

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.00

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Video: Gold $16,000 and Silver $770 Per Ounce? Focus On Safe Haven Value, Not Price

– “The possibility of gold over $16,000 per ounce and silver over $770 per ounce … I hear people gasp in dismay when I say those figures and I will qualify them”

– “There are a lot of important developments in the precious metals market … the outlook for gold and silver has never been more positive”

– “Price is what you pay; value is what you get” – Warren Buffett’s phrase regarding value stocks is very apt with regard to the safe have value of gold and silver today

– Most investors remain gold cynics, some of whom know the price of gold and silver but very few of whom know the real hedging and safe haven value as seen in the data, research and all of history including that of recent years

– Gold and silver’s fundamentals and the heady cocktail of macroeconomic monetary, geo-political and systemic risk have never been more bullish

– “Ignore the short term noise and focus on the long term value of gold and silver”

Watch Latest GoldCore Video Here

NEWS and COMMENTARY

Gold prices dip as fears of widening trade war ease

Sliver and Nickel Outshine Gold to Score Biggest Commodities Gains Since June

Gold app Glint collapses just months after fundraising

Asian shares, yuan off to calm start; focus on China

China Sept factory activity surprises, expands fastest in 19 mths

Dollar supported as fears of ramp up in Sino-U.S. trade war ease

September Container Shipping Rates Collapse 43% Forcing Carriers To Slash Capacity

“The Semmelweis Reflex” – Why Experts Don’t Understand Gold – Salinas Price

Gold Prices (LBMA – USD, GBP & EUR – AM/ PM Fix)

27-Sep-19 1496.15 1489.90, 1218.17 1209.05 & 1369.58 1362.51

26-Sep-19 1507.05 1506.40, 1223.72 1219.28 & 1378.50 1374.89

25-Sep-19 1530.85 1528.75, 1231.11 1234.62 & 1391.24 1391.77

24-Sep-19 1520.25 1520.65, 1220.76 1216.67 & 1382.36 1381.36

23-Sep-19 1519.50 1522.10, 1222.13 1225.90 & 1385.48 1385.11

20-Sep-19 1504.10 1501.90, 1199.07 1203.62 & 1361.06 1362.52

19-Sep-19 1498.40 1500.70, 1200.67 1201.76 & 1354.85 1357.08

18-Sep-19 1502.20 1503.50, 1206.27 1204.90 & 1360.39 1359.92

17-Sep-19 1499.30 1502.10, 1208.89 1207.24 & 1361.51 1360.45

16-Sep-19 1502.05 1497.20, 1207.35 1203.30 & 1357.25 1359.46

13-Sep-19 1506.30 1503.10, 1209.41 1208.19 & 1356.88 1358.35

12-Sep-19 1502.95 1515.20, 1219.94 1227.46 & 1362.88 1373.53

11-Sep-19 1493.65 1490.65, 1208.21 1209.07 & 1354.74 1355.90

ii) Important gold commentaries courtesy of GATA/Chris Powell

As more and more countries shift away from the dollar it’s share of global currency reserves falls. It is now at its lowest level since 2013

(Reuters/GATA)

U.S. dollar share of global currency reserves hits lowest since 2013

Submitted by cpowell on Mon, 2019-09-30 15:00. Section: Daily Dispatches

From Reuters

Monday, September 30, 2019

https://www.reuters.com/article/us-forex-reserves/u-s-dollar-share-of-gl…

The U.S. dollar’s share of currency reserves reported to the International Monetary Fund fell in the second quarter to its lowest level since the end of 2013, while the yen’s share of reserves grew to the largest in nearly two decades, data released on Monday showed.

…

..Reserves held in U.S. dollars totaled $6.79 trillion, or 61.63% of allocated reserves, in the second quarter, compared with $6.74 trillion, or 61.86%, in the first quarter.

This was the greenback’s smallest share of overall reserves since the fourth quarter of 2013 when it was 61.27%.

* * *

Join GATA here:

New Orleans Investment Conference

Hilton New Orleans Riverside Hotel

Friday-Monday, November 1-4, 2019

https://neworleansconference.com/noic-promo/powellgata/

* * *

.END

They are now beginning to understand that negative rates are having a devastating effect on markets because of the pricing of risk

(Bloomberg/GATA)

Negative rates are rewriting the rules of modern finance

Submitted by cpowell on Mon, 2019-09-30 15:12. Section: Daily Dispatches

By Brandon Kochkodin

Bloomberg News

Monday, September 30,2019

Negative interest rates have quite literally broken one of the pillars of modern finance.

As economists and central bankers weigh the pros and cons of sub-zero rates and their impact on the world, traders have been contending with a rather more mundane, but fundamental issue: How to price risk on trillions of dollars of financial instruments like interest-rate swaps when their complex mathematical models simply don’t work with negative numbers.

…

Out are certain variations of the Black-Scholes model, the framework that allowed derivatives to flourish in the past four decades. In are a hodgepodge of approximations and workarounds, including one dating to the 19th century.

Granted, the current state of affairs is more a nuisance than a serious problem. And it’s one that has been largely confined to Europe and Japan. But with sub-zero interest rates becoming a long-term economic feature and the number of negative-yielding bonds reaching $15 trillion, it’s an issue more and more traders, particularly in the U.S., are trying to wrap their heads around. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-09-30/how-negative-rates-br…

* * *

END

No question about it, helicopter money or direct funding of government is only one step away

Rees/London Telegraph/GATA)

‘Helicopter money’ may be only weapon to confront next recession

Submitted by cpowell on Mon, 2019-09-30 15:34. Section: Daily Dispatches

By Tom Rees

The Telegraph, London

Monday, September 30, 2019

A radical world of “helicopter money” – where central banks fund government spending – is “inevitable” as policymakers run out of ammunition ahead of the next recession, top economists have warned.

Central banks are likely to “explore more unconventional policies” in the next downturn and blur the lines between fiscal and monetary policy with radical new tools, such as monetary financing, Deutsche Bank argued.

…

Recession fears are mounting but central banks have very little firepower remaining with traditional monetary policy — the control of the money supply and interest rates — blunted.

Helicopter money to stimulate the economy therefore “seems inevitable over the medium to longer term,” said Jim Reid, a Deutsche analyst. He argued that central banks “effectively invited governments to experiment with more unconventional policies” with ultra-low interest rates on debt.

Helicopter money is when central banks finance government spending through money printing but can also refer to cash transfers into individuals’ bank accounts and haircuts to debt already held by central banks.

“If the post global financial crisis decade has all been about printing money to buy financial assets, we think the next decade will be more about printing money and injecting it into the real economy,” Mr. Reid said.

The German bank’s analysis found that the world is already drenched in debt in the wake of the financial crisis. Total debt has tripled since the turn of the century to $247 trillion while government debt as a percentage of GDP in advanced economies is at a record peacetime high. …

… Dispatch continues below …

https://www.telegraph.co.uk/business/2019/09/29/helicopter-money-may-wea…

* * *

END

We now hear that Deutsche bank’s headquarters were raided last week. It is Pam and Russ Martens contention that banks are refusing to loan any money to DB

(courtesy Russ and Pam Martens/Wall Street on Parade)

Pam and Russ Martens: The repo loan crisis, dead bankers, and Deutsche Bank

Submitted by cpowell on Mon, 2019-09-30 16:04. Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Monday, September 1, 2019

Last week, as the Fed was carrying out hundreds of billions of dollars in emergency loan operations on Wall Street for the second week in a row — the first such operations since the financial crisis — Deutsche Bank’s headquarters office in Frankfurt, Germany was being raided by police for the second time in less than a year. That’s not the sort of thing that inspires confidence among depositors to keep their money in your bank.

…

.Deutsche Bank has been a constant headache for the U.S. financial system because it is heavily intertwined via derivatives with the big banks on Wall Street, including JPMorgan Chase, Citigroup, Goldman Sachs, Morgan Stanley and Bank of America. It has become the dark cloud on the horizon in the same way Citigroup cast a negative pall in the early days of the financial crisis of 2008. (It’s not a good omen that Citigroup’s stock eventually went to 99 cents and the bank received the largest taxpayer and Federal Reserve bailout in U.S. history. The Fed alone secretly pumped $2.5 trillion in revolving loans into Citigroup from December 2007 to the middle of 2010.)

The latest raid at Deutsche Bank occurred on Tuesday and Wednesday of last week, September 24 and 25, and was related to the $220 billion money laundering probe of Danske Bank, Denmark’s largest lender. Deutsche Bank served as correspondent bank to Danske’s Estonia branch where the laundering is alleged to have occurred. On Wednesday, as the raid was proceeding, the body of Aivar Rehe who previously ran the Estonia business of Danske Bank, was discovered by police in Estonia. Rehe had been questioned by prosecutors and was considered a key witness in the probe. His death is being called an apparent suicide by European media.

On the day the police raid started at Deutsche Bank, Tuesday, September 24, the Federal Reserve Bank of New York offered $30 billion in 14-day emergency term loans and had demand for more than twice that amount. That led the New York Fed to increase its subsequent 14-day term loans from $30 billion to $60 billion later in the week. The Fed’s overnight repo loans that were offered every day last week were also increased from $75 billion per day to $100 billion per day.

As the timeline below illustrates, Deutsche Bank has been in a slow motion collapse as a result of its serial crime charges while international regulators have failed to address the fact that it is a counterparty to $49 trillion notional (face amount) in derivatives according to its 2018 annual report and thus presents systemic risk throughout the global financial system.

Wall Street On Parade believes that the repo crisis on Wall Street may, at least in part, relate to big Wall Street banks backing away from lending to Deutsche Bank. You can read the timeline below and make up your own mind. …

… For the remainder of the report:

https://wallstreetonparade.com/2019/09/the-repo-loan-crisis-dead-bankers…

* * *’

end

China’s golden week explains fully the whack on our precious metals yesterday.

(zerohedge)

China’s Golden Week holiday explains gold’s counterintuitive weakness, Zero Hedge says

Submitted by cpowell on Mon, 2019-09-30 16:13. Section: Daily Dispatches

Is This The Real Driver Of Gold’s Recent Weakness?

From Zero Hedge, New York

Sunday, September 29, 2019

Despite uber-dovish Fed jawboning (and a re-expansion of their balance sheet), a liquidity crisis prompting repo action by New York Fed, re-escalated trade tensions, a breakdown in talks with North Korea, and, of course, the Trump impeachment process, safe-haven precious metals were pummeled lower the last few days, breaking back down below $1,500.

The question on many investors’ minds is: Why?

The answer is surprisingly simple: China’s Golden Week holiday. …

… For the remainder of the commentary:

https://www.zerohedge.com/commodities/gold-prices-plunge-right-cue-china.

iii) Other physical stories:

LAWRIE WILLIAMS: China gold imports still hugely significant despite earlier cuts

China will still import close to 1700 tonnes of gold this year.

(Lawrie Williams)

Gold investors may have had their attention drawn to reports that China has been severely curtailing its gold imports earlier this year. This is true – at least in part – with significant cutbacks in May, June and July, but the Middle Kingdom nonetheless still remains a hugely important importer and consumer of gold – and the gold import numbers appear to have been beginning to pick up again.

So far this year (to end-August), according to Nick Laird; http://www.goldchartsrus.com figures, China has imported a shade under 700 tonnes of gold as against 1,126 tonnes to August 2018 and 864 tonnes in the first 8 months of 2017. It is still on track for imports over the full year to exceed 1,000 tonnes, which together with the country’s own domestic gold production, plus an allowance for gold scrap recycling, would probably still put China’s annual gold absorption at around 1,600 to 1,700 tonnes. This is well above the figures publicised by major consultancies like GFMS and Metals Focus, which seem to limit their consumption estimates to only some limited demand categories. This latest figure would still leave China as comfortably the world’s largest annual consumer of gold, despite the apparent slowdowns implemented earlier in the year and supported by lower Shanghai Gold Exchange withdrawal data so far this year.

But does this signify a global gold demand slowdown. We don’t think so because of the big pick up in gold inflows into the gold-based ETFs around the world which has happened at the same time, along with the overall gold price advance. Gold is up around 13% year to date and even silver, which has been underperforming gold so far, is up 9% this year, despite the latest sharp price falls. These are reasonably respectable performances vis-a-vis equities which have the overhanging ongoing likelihood of a major crash ahead according to many respected financial commentators.

According to the World Gold Council, Gold ETFs added some 292 net tonnes of gold up until end-August, and the figures have risen further since. The biggest gold ETF of all, GLD in the USA, has alone added 126 tonnes of gold to its holdings since the beginning of the year, and as a guide to global inflows in the past month, added around 31 tonnes in September alone. Assuming global totals rose at a similar rate to those of GLD, global ETF holdings will have risen by a total of around 360 tonnes of gold year to date – countering most of the fall-off in Chinese imports.

Total global gold production, while it may not have peaked quite yet – with continuing production growth in countries like Australia, Russia and Canada countering declines in many other gold producers like China and South Africa – is pretty well flat. Maybe it will rise between 0.5 and 2 percent this year depending on whose data one follows. Peak gold may not be with us yet, but it is close, so we are not expecting any big supply increases, National demand reductions, like that we are seeing this year in China, is the primary supply/demand balance factor – but as we have pointed out above, this is largely being counterbalanced by ETF gold inflows, plus continuing central bank purchases, so the actual supply/demand fundamentals are little changed by the Chinese gold import curtailment, big though it may be, which will thus have little direct impact on the gold price.

Ed Steer has published a graphic in his daily newsletter demonstrating that movements in the gold price correlate extremely closely to COMEX trades by Managed Money traders, which brings an interesting context into precious metals price movements in that the other precious metals are all influenced by the gold price. I quote Ed: “If they’re [the managed Money Traders] buying, the act of them doing that is what causes prices to rise — and if they’re selling, prices fall. It has nothing do with interest rates, the stock market, the Fed…or the price of tea in China.” Of course some of the factors that Ed notes as not being relevant will influence the aforesaid Managed Money traders’ decisions whether to buy or sell! Nevertheless it’s an important observation, and one which is well-supported by the graphic Ed supplies.

Overnight trade and early activity in Europe today saw a further sharp gold price downturn, although silver was less affected. It seems that every time gold looks as if it might approach the $1,550 mark, as it did early last week, it is brought back down very sharply driven by activity in the COMEX futures market. It is already picking up a little and we wouldn’t be surprised to see it regain the $1,500 level in the next few days – geopolitical events continue to create uncertainty, and the latest Chicago PMI data is far from encouraging for the U.S. markets, but perhaps positive for gold. However, beware if it gets to the $1,530s or 40s as it may well be brought back down heavily again, although we see this as a short to medium term temporary setback in an overall ongoing upwards movement in precious metals prices. The world remains an uncertain place and that tends to be positive for gold and silver in particular.

01 Oct 2019

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

US Stock Futures Levitate, Ignore Bond Market Blowout

In a session market by fireworks in the bond market, stocks were relatively tame and well-behaved as we officially entered the last quarter of the year.

S&P e-mini futures gained on Tuesday as trade talk optimism returned, and ahead of the release of key US manufacturing data as investors looked for fresh signs of domestic demand in the world’s largest economy amid softening global growth. The ISM’s PMI data is expected to show the manufacturing sector rebounded to 50.0 in September after contracting for the first time in 3-1/2 years to 49.1 in August. The US ISM data comes on the heels of euro zone data, which showed manufacturing activity in the bloc contracted at its steepest rate in almost seven years as the global economy flashed clearer warning signs as a wave of data showed manufacturing stuck in a slump, exports falling and sentiment sliding: as the trade war between the U.S. and China rages, industry executives from Japan and Russia to Germany and Italy complained of contracting business, while the World Trade Organization cut its forecast for commerce to the lowest in a decade.

The latest dismal European numbers only added to the gloom for investors facing a laundry list of threats just now, including everything from the drawn-out trade war and Brexit to protests in Hong Kong and an impeachment probe of President Trump; they even barely blinked at the news of the first shot protesters in Hong Kong. Nonetheless, stocks continue to ignore the looming threat in what has been yet another perplexing risk-on start to the week (propelled by more stock buybacks ahead of the blackout period), perhaps because the outcome of each risk seems impossible to predict and the safest assets are looking expensive.

The overnight session started with subdued Asian markets as Hong Kong and China were closed for holidays. Japanese shares rose about 1%, while Australia’s dollar slid after the central bank cut its benchmark interest rate to a record low.

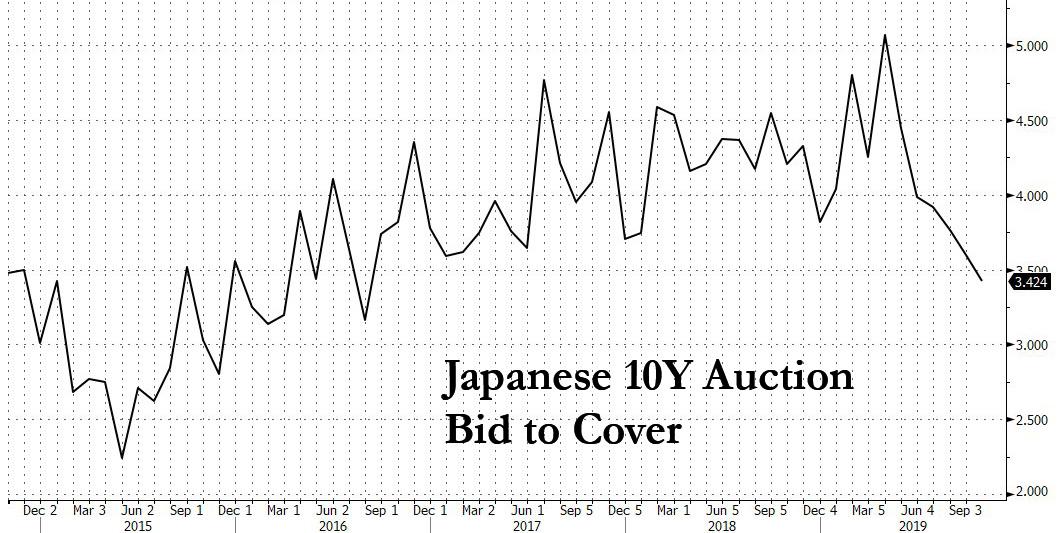

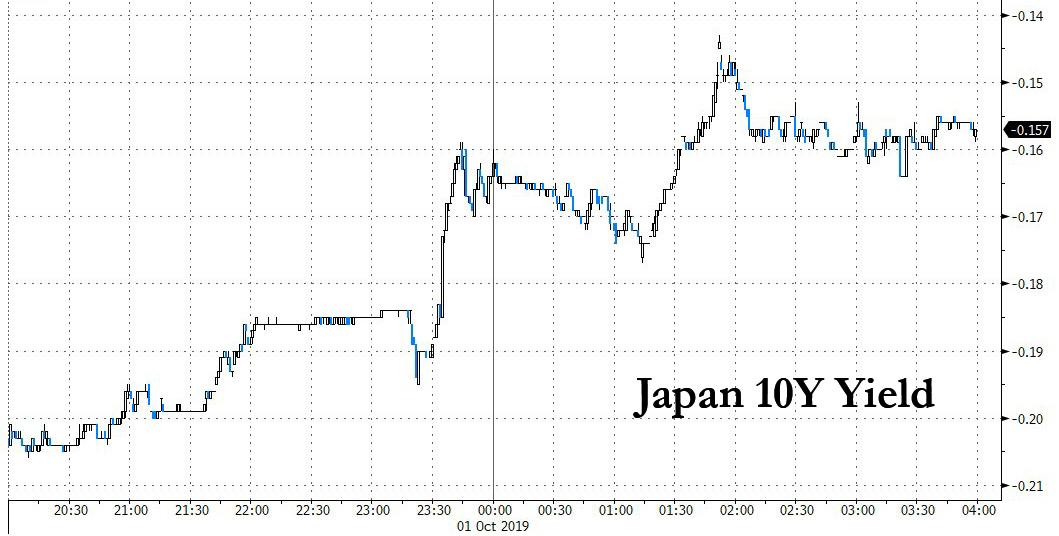

Yet while European stocks slipped amid the disappointing factory and inflation data, global stocks generally ignored the latest dismal manufacturing data, bonds were rather active, and as noted earlier, Japan’s 10Y JGBs suffered the biggest drop since August 2016 on a trifecta of negative developments, following a BOJ warning it would further trim its bond purchases, the GPIF saying it would shift to offshore bond purchases, and the ugliest 10Y bond auction in three years; the violent plunge set off a brief margin call which only made the selloff worse.

Treasuries and bunds then promptly joined the JGB selloff which gradually spread across the world.

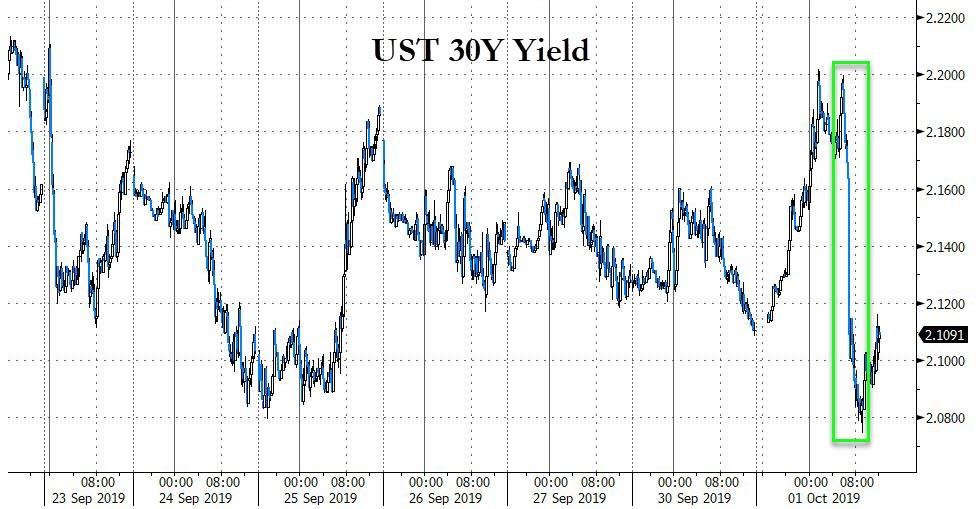

The yield on 10-year U.S. bonds headed for the first increase in four days in the wake of the Japanese fiasco.

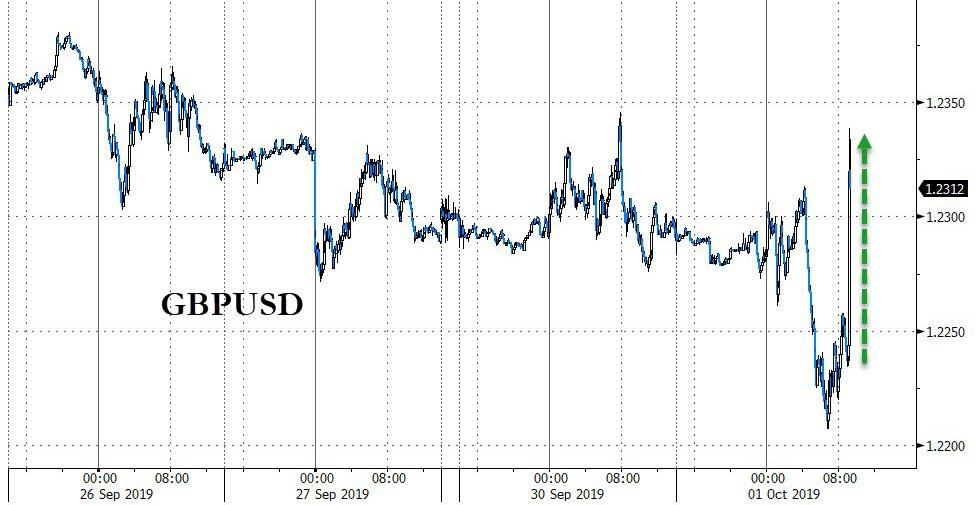

In FX, the Bloomberg dollar index rose for a second day, while the pound fluctuated as British Prime Minister Boris Johnson prepares to present his blueprint for a new Brexit deal to the European Union.

The Australia dollar tumbled as Australia’s central bank was dragged further into the global easing tide as it cut interest rates for the third time this year, to a new record low, even as it risks refueling excesses that Governor Philip Lowe warned against just weeks ago. The Reserve Bank reduced the cash rate by 25 basis points to a record-low 0.75% and said it may ease even further, venturing deeper into levels where unconventional measures may need to be adopted. The move is in part designed to prevent a rebound in the depreciating currency that might have been triggered if it stood pat while global counterparts eased. “The global race to the bottom is, in a sense, dragging the RBA along,” said Michael Blythe, chief economist at the Commonwealth Bank of Australia. “Failure to participate could see the Australian dollar move higher.”

In other geopolitical news, Chinese President Xi said no force can stop the Chinese people and the Chinese nation forging ahead, must uphold path of peaceful developments. Xi added that the central government would “maintain long-term prosperity and stability of Hong Kong and Macao.”

Gold extended recent declines and West Texas oil climbed.

On today’s calendar, expected data include PMIs and construction spending. McCormick and Stitch Fix are reporting earnings

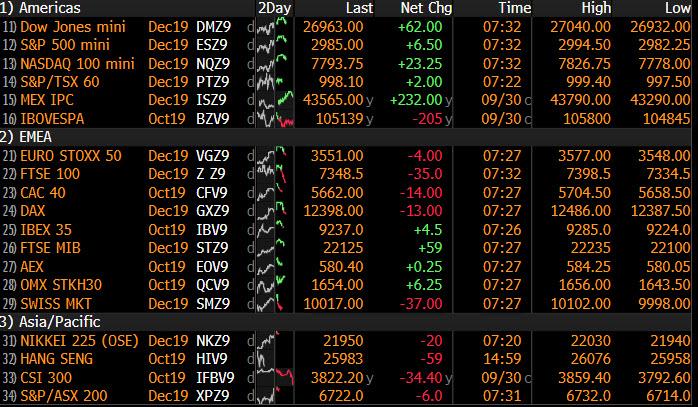

Market Snapshot

- S&P 500 futures up 0.3% to 2,987.25

- STOXX Europe 600 down 0.07% to 392.86

- MXAP up 0.2% to 156.70

- MXAPJ down 0.03% to 501.93

- Nikkei up 0.6% to 21,885.24

- Topix up 1% to 1,603.00

- Hang Seng Index up 0.5% to 26,092.27

- Shanghai Composite down 0.9% to 2,905.19

- Sensex down 1.6% to 38,050.80

- Australia S&P/ASX 200 up 0.8% to 6,742.85

- Kospi up 0.5% to 2,072.42

- German 10Y yield rose 4.5 bps to -0.526%

- Euro down 0.06% to $1.0893

- Italian 10Y yield fell 0.2 bps to 0.484%

- Spanish 10Y yield rose 4.4 bps to 0.189%

- Brent futures down 1.5% to $59.90/bbl

- Gold spot down 0.6% to $1,464.37

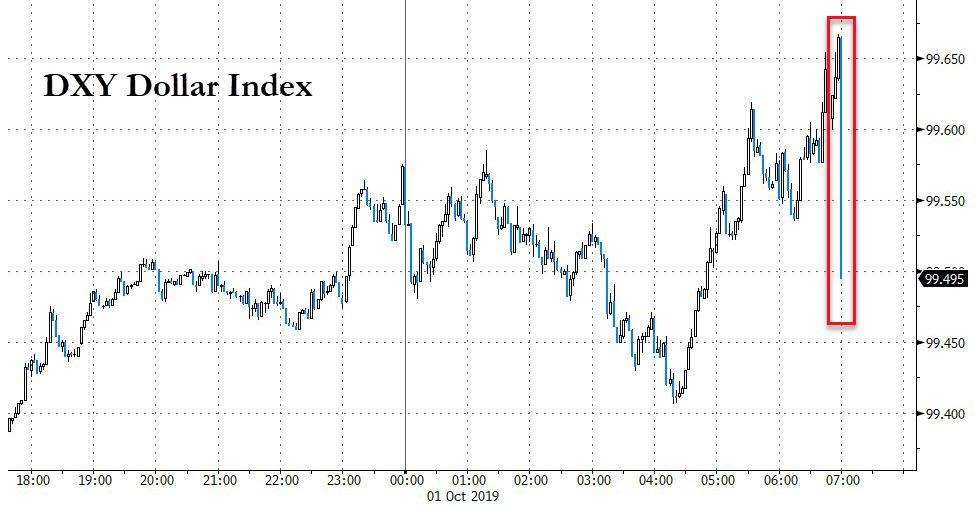

- U.S. Dollar Index up 0.1% to 99.50

Top Overnight News from Bloomberg

- British Prime Minister Boris Johnson will present a new plan for a Brexit deal to the European Union within days but there are signs that it may fail. While some purist euro-skeptics in Johnson’s ruling Conservative party are willing to compromise, the Irish government has said his proposals so far for resolving the Brexit impasse are a non-starter

- The euro area’s manufacturing sector slumped in September as German factories experienced their worst month since the depths of the financial crisis. IHS Markit’s index for manufacturing in the euro region came in at 45.7 last month, slightly higher than the initial estimate of 45.6, but still the lowest level since October 2012

- Police shot tear gas volleys at protesters as simultaneous rallies raged across Hong Kong, including a march through the city center, hours after celebrations for a holiday marking 70 years of Communist rule in China began in Beijing

- Gold sank to an eight-week low as investors weighed the impact of a stronger dollar — which traded near the highest level since 2017 — together with unfavorable chart patterns and prospects of renewed, high-level U.S.-China trade talks next week

- Japanese bond traders just had a taste of what it’s like when the nation’s central bank and pension fund aren’t there to support them. Bond futures tumbled by the most since 2016, triggering margin calls for investors, after the worst 10-year debt auction in three years. Yields across the curve climbed, while the sell- off also spilled into Treasuries and European debt.

Asian equities traded higher across the board after Wall Street wrapped up the third quarter with a session in the green ahead of principle-level US-Sino trade talks in Washington next week. In terms of Q3 performance, the S&P and DJIA both advanced for a third consecutive quarter, rising in excess of 1% each, whilst the Nasdaq dipped 0.1% Q/Q. Upside in the ASX 200 (+0.8%) was capped as base and precious metal miners bore the brunt of softer prices, whilst Nikkei 225 (+0.6%) cheered favourable currency moves and largely side-lined the planned sales tax hike which came into effect today. Elsewhere, the KOSPI (+0.5%) conformed to the risk appetite despite South Korean exports declining for the tenth straight month and semi-conductor exports slumping 31.5% Y/Y, albeit inflation metrics fell short of forecasts. As a reminder, Mainland China and Hong Kong markets were closed today due to National Day Holiday, although protests were underway in Hong Kong whilst China celebrated the 70th anniversary of the People’s Republic with a military parade. Finally, 10yr JGB futures were softer amid the risk-sentiment, however downside was more pronounced after the Japanese 10yr auction was received poorly as results showed a bid-to-cover at multi-year lows, which pressured UST and Bund futures in sympathy, Japan Securities Clearing Corporation then said an emergency margin call has been triggered on JGB futures.

Top Asian News

- Japan’s GPIF Positions Itself for More Foreign Debt Buying

- Marubeni Is Said to Sound Out Potential Buyers for Gavilon

- Taiwan Dollar Is a Surprise Winner From U.S.-China Trade War

- Japan Post Favors CLOs for U.S. Loan Purchases Over Mutual Funds

Major European bourses (Euro Stoxx 50 -0.1%) pared initial gains, following a positive AsiaPac lead, where stocks took impetus from a solid Wall Street session and better than expected Japanese Tankan manufacturing data. The FTSE 100 (-0.3%) is a marginal laggard, amid Sterling strength on renewed Brexit deal hopes and after the second reading of September’s Manufacturing PMI data proved not as grim as expected, while Switzerland’s SMI (-0.4%) is also lower amid weakness in some of its heavyweights. Negative ticks were seen across European bourses (although most pronounced in the DAX [-0.1%]) after the second reading of Germay’s Manufacturing PMI data, which although coming in better than expected, confirmed a deterioration in the sector in the month of September. Amid the initially firmer risk tone, defensives (Utilities (-0.3%), Health Care (-0.6%) and Consumer Staples (-0.9%)) are on the back foot while Tech (+0.3%) is in the lead. In terms of individual movers; MediaSet (+1.3%) was buoyed after posting decent earnings. PostNL (-2.7%) sunk on the news that the Co. is to combine its network with Sandd, in a deal worth EUR 105mln. ASML (+1.8%) advanced after the Co. was reiterated buy at UBS. Ryanair (+3.1%) and Air France (+2.7%) both moved higher after the Co’s were upgraded to buy at BAML. Atlantia (-2.3%) after Italy PM Conte said the process to revoke highway concessions is underway.

Top European News

- Euro-Area Manufacturing Slump Deepens in Worst Month Since 2012

- Euro-Area Inflation Slows, Adding to Case for ECB Stimulus Move

- U.K. Mulls Help-to-Buy Future to Avoid Shock End for Developers

- U.K. Factories Extend Slump Even as Brexit Preparations Resume

In FX, it has been a lively start to the new month and Q4 amidst ongoing Greenback strength, but with independent weights exacerbating declines and underperformance. The Aussie rebounded initially after the RBA cut rates by a further 25 bp and inserted a relatively upbeat line in the accompanying statement about a gentle turning point in the economy, but with guidance for further easing retained recovery gains were short-lived and Aud/Usd subsequently slipped below 0.6700, while Aud/Nzd retreated from another test of resistance around 1.0800 even though the Kiwi eventually succumbed to contagion and Nzd/Usd reversed through 0.6250 again to a 0.6220 low following another downbeat NZ business sentiment survey overnight. Meanwhile, the Swedish Krona slumped in wake of a significantly weaker than forecast sub-50 manufacturing PMI that was compounded by a downward revision to the previous month, and its Scandinavian counterpart has fallen in sympathy as Norway’s manufacturing sector only just escaped contraction and decelerated sharply from almost 54.0 in August. Eur/Sek has tested 10.8000 following a breach of technical resistance circa 10.7742 and Eur/Nok rallied beyond 9.9550 from lows of around 9.9080 and just below 9.8850 at one stage on Monday.

- USD – The Dollar continues to prosper, partly at the expense of others, but also as US Treasury yields rebound and curves re-steepen with some extra impetus via Fed’s Evans advocating a policy pause after the 2 insurance cuts administered in July and September. Accordingly, the DXY has forged a fresh ytd high and breached 99.500 in the process, at 99.590, eyeing the Markit PMI, ISM and more Fed speakers for further direction.

- CHF/CAD/JPY – The Franc has also bowed to disappointing Swiss macro news in the form of retail sales and deeper manufacturing PMI recession, with Usd/Chf up through parity and Eur/Chf crossing 1.0900 even though the single currency is struggling to cope with the aforementioned broad Buck advance and its own frailties. Elsewhere, the Loonie is still pivoting 1.3250 and awaiting Canadian GDP and/or Markit’s manufacturing PMI for extra inspiration, while the Yen appears more attuned to the latest gains in UST yields rather than a post-auction plunge in JGB futures that triggered emergency Japanese SCC margin calls. Indeed, Usd/Jpy has extended gains above 108.00 towards 108.50, with upside chart levels at 108.43 (Fib) and 108.48 (September’s peak) proving tough to break convincingly, thus far.

- GBP/EUR – Relative G10 outperformers, or at least putting up a fight against the Greenback with the aid of an unexpected bounce in the UK manufacturing PMI and a steady pan Eurozone final print thanks to a German upgrade from the dire preliminary reading. However, Cable is still not making much headway beyond 1.2300 and Eur/Usd has waned just above 1.0900, with the former down through the 55 DMA (1.2279), Fib support (1.2271) and a late September base before the Brexit re-stocking PMI recovery and latter having another close look at bids at 1.0880 that are protecting a deeper retracement to 1.0864 (strong Fib support).

- EM – Blanket losses vs the Greenback, and with sub-50 manufacturing PMIs across the region, bar Turkey, not helping, as the Lira loses more ground amidst rebounding oil prices and further investor disenchantment with the Finance Minister’s latest grand economic plan.

- The RBA cut its cash rate by 25bps to 0.75% as expected. RBA reiterated that it is reasonable to expect that an extended period of low interest rates will be required in Australia to reach full employment and achieve the inflation target. RBA added “A gentle turning point, however, appears to have been reached”. The Central Bank noted the low level of interest rates, recent tax cuts, ongoing spending on infrastructure, signs of stabilisation in some established housing markets and a brighter outlook for the resources sector should all support growth, but repeated that the Board will continue to monitor developments, including in the labour market, and is prepared to ease monetary policy further if needed to support sustainable growth in the economy, full employment and the achievement of the inflation target over time.

In commodities, the crude complex is consolidating, with both benchmarks having found support around their 12 September lows around USD 54.00/bbl for WTI and USD 59.00/bbl for Brent respectively, following yesterday’s steep declines which were exacerbated by bearish supply signals re. Saudi Aramco’s recovery to full output. News flow on the Middle Eastern geopolitical front has been light, although reports that Iran has sentenced one person to death for spying for the US could be providing some support to the complex. However, further details regarding who the person is and what the wider implications, if any, may be are scant. Elsewhere, amid continued constructive risk tone and possible technical selling after it convincingly lost its grip on the USD 1500/oz handle yesterday, Gold continues to move lower. The fall in Gold prices comes despite continued escalations in protestor/police tensions in Hong Kong, as markets more broadly remain seemingly unperturbed by developments for now. Meanwhile, Copper futures remain unable to derive support from the more constructive risk tone, and have extended on their overnight declines after broking below short-term resistance around USD 2.572/lbs.

US Event Calendar

- 8:50am: Fed’s Clarida Makes Brief Remarks at AI Conference

- 9:30am: Fed’s Bowman Speaks at Community Banking Conference

- 9:45am: Markit US Manufacturing PMI, est. 51, prior 51

- 10am: ISM Manufacturing, est. 50, prior 49.1

- 10am: Construction Spending MoM, est. 0.5%, prior 0.1%

- Wards Total Vehicle Sales, est. 17m, prior 17m

DB’s Jim Reid concludes the overnight wrap

Welcome to Q4 and only 85 days until Xmas. Craig has just published the Sept/Q3/YTD performance review. Q3 ended up being relatively positive for global assets with 29 of our 38 asset sample finishing with a positive total return although only 14 did so in dollar adjusted terms owing to the stronger greenback. September saw 23 out of 38 (22 in dollar terms) higher and reversed a tough August where only 18 of the 38 saw positive returns (14 in dollars). See Craig’s full review here .

I am on an advisory board for a research centre at the University of Warwick where I studied Economics (the no.1 place in the UK to study it according to last week’s Sunday Times). It’s called CAGE (Competitive Advantage in the Global Economy) and has published many interesting pieces over the years helping to shape policy and debate. However on a more fun theme it has very recently been associated with a report that debunked an old assertion that winning the lottery doesn’t make you happy. It’s been in a lot of newspapers over the last few days with the new research suggesting (using a much bigger sample than earlier work on this topic) that it absolutely does make you happier and the bigger the better. This made me smile as our new house was commissioned over a hundred years ago by someone that won a small lottery in the UK around the time of WWI. However much of the infrastructure (windows, plumbing, electrics, drainage etc.) hadn’t been touched since and as such I now feel like I’ve lost a lottery renovating it. However I’m blissfully happy living there so I can confirm that spending money you don’t have can also make you very happy – well at these interest rates it can.

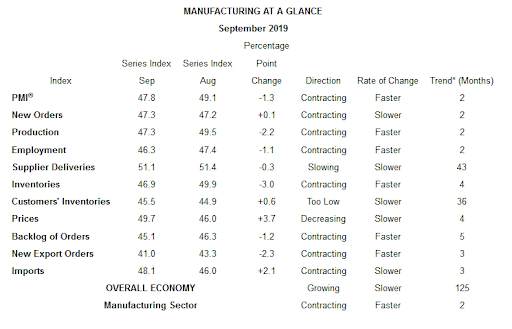

One part of the world that’s not very happy at the moment is the global manufacturing sector and today brings the final PMIs/US ISM on this front with Europe’s numbers the most important. Ahead of that, the Chicago PMI yesterday wasn’t indicative of strong activity. Indeed the 47.1 reading for September compared to expectations for an even 50.0 and the print represented a decline of 3.3pts from August. Yesterday’s number tied for the third worst reading in this cycle although it did hit as low as 44.4 in July, although that means the three-month average is just 47.3. More concerning were some of the details though with the employment component at 45.6 which means the quarterly average of 44.1 is the lowest since Q4 2009. Our US economists also made the point that the ISM adjusted for the Chicago PMI was 46.2 and the lowest since 2009.

This comes ahead of today’s September US ISM manufacturing report. A reminder that the August reading fell into contractionary territory at 49.1 for the first time since August 2016. The consensus today is for a slight rebound back to 50.0 and our US economists expect a 50.8 reading. The Chicago number is a worry though.

Ahead of the European PMIs remember that the flash Euro Area reading fell to just 45.6 while Germany hit 41.4. France also only just stayed in expansionary territory at 50.3. We’ll also get a look at the non-core with Italy expected to print at 48.1, while here in the UK the consensus expects a 47.0 reading.

So a rare chance to focus on the data following what feels like nothing but politics for the past few weeks. As for markets, the partial walk back over the weekend of the US restricting capital to China story helped the S&P 500 and NASDAQ to gains of +0.50% and +0.75% respectively last night. Markets got a further boost after Peter Navarro said that the reports about capital controls were “inaccurate.” He’s one of the biggest China hawks in the White House, so his denial carries more weight. On the impeachment front, there weren’t any major new developments, though President Trump’s personal lawyer Rudy Giuliani was subpoenaed by the House Intelligence Committee. Our economists did note, that amid the heightened political noise, the Baker, Bloom, Davis economic policy uncertainty index has risen to 6-year high. Meanwhile, overnight the New York Times reported that President Trump pushed the Australian prime minister during a recent telephone call to help Attorney General William P. Barr gather information for a Justice Department inquiry that Trump hopes will discredit the Mueller investigation.

This morning in Asia markets are largely up in thin trading as Chinese and Hong Kong markets are closed. The Nikkei (+0.76%), Kospi (+0.53%) and ASX (+0.09%) are all higher. Elsewhere, futures on the S&P 500 are up +0.41% while yields on 10yr JGBs are up +5.6bps to -0.170% as a 10yr note auction saw the weakest demand since 2016 in the wake of a steady cutback in bond purchases by the BoJ. Yields on 10Y USTs are also up +3.6bps this morning. As for overnight data releases, Japan’s final September manufacturing PMI came out in line with the initial read of 48.9 while the Q3 Tankan survey results were largely better than expected. Meanwhile, South Korea’s September manufacturing PMI came in at 48.0 (vs. 49.0 last month) while CPI came in at -0.4%yoy (vs. -0.3%yoy expected) and exports printed at -11.7%yoy (vs. -9.6%yoy expected) with imports standing at -5.6%yoy (vs. +0.8% yoy expected).

In terms of markets, Europe also had a good day yesterday with the STOXX 600 (+0.35%) rising to its highest closing level in more than 16 months. It was a quiet quarter end for bond markets with 10y Treasuries and Bunds little changed by the end of play although Treasuries did rally a couple of basis points after that Chicago PMI data. Meanwhile, the dollar rallied (+0.27%; up a further +0.11% this morning) to its strongest level in 29 months, to the disadvantage of both oil (-1.83%) and gold (-1.59%).