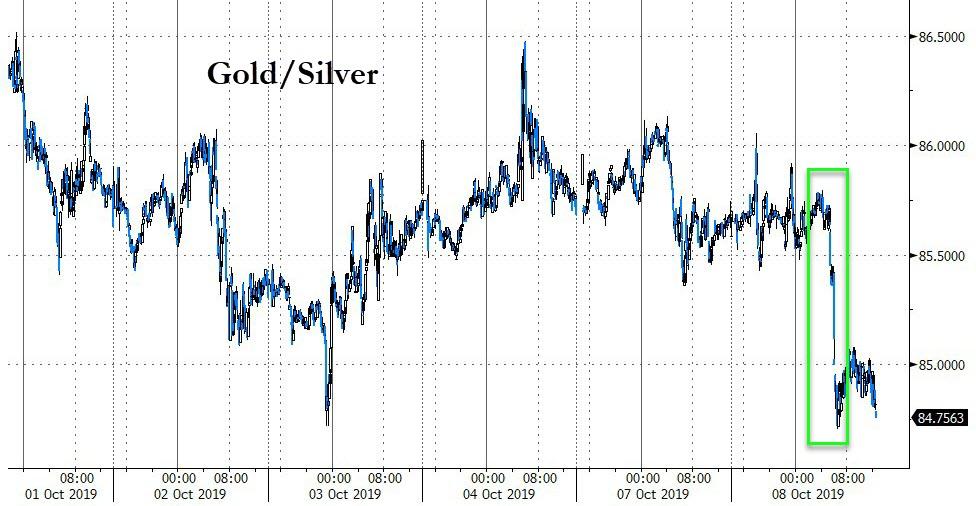

GOLD:$1499.00 DOWN $0.35(COMEX TO COMEX CLOSING

Silver:

$17.64 up 15 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1506.40

silver: $17.71

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 5/13

EXCHANGE: COMEX

CONTRACT: OCTOBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,497.700000000 USD

INTENT DATE: 10/07/2019 DELIVERY DATE: 10/09/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

118 H MACQUARIE FUT 1

661 C JP MORGAN 5

737 C ADVANTAGE 13 4

800 C MAREX SPEC 1

905 C ADM 2

____________________________________________________________________________________________

TOTAL: 13 13

MONTH TO DATE: 10,403

NUMBER OF NOTICES FILED TODAY FOR OCT CONTRACT: 13 NOTICE(S) FOR 1300 OZ (0.0404 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 10,403 NOTICES FOR 1,040,300 OZ (32.357 TONNES)

SILVER

FOR 0CT

7 NOTICE(S) FILED TODAY FOR 35,000 OZ/

total number of notices filed so far this month: 921for 4,605,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

we are coming very close to a commercial failure!!

Bitcoin: OPENING MORNING TRADE : $ 8184 DOWN 2

Bitcoin: FINAL EVENING TRADE: $ 8163 DOWN 3

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A CONSIDERABLE SIZED 554 CONTRACTS FROM 212,647 DOWN TO 211,282 WITH THE 6 CENT LOSS IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR SEPT 0,; DEC 813 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 813 CONTRACTS. WITH THE TRANSFER OF 813 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 813 EFP CONTRACTS TRANSLATES INTO 4.06 MILLION OZ ACCOMPANYING:

1.THE 6 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

6.275 MILLION OZ INITIALLY STANDING IN OCT

yESTERDAY, ANOTHER MAJOR ATTEMPT BY THE BANKERS TO COVER THEIR MASSIVE SHORTFALL AT THE SILVER COMEX WHICH FAILED MISERABLY. OUR BANKER /OFFICIAL SECTOR SAW THE WRITING ON THE WALL AS THEY TRIED TO COVER SOME OF THE HUGE SHORTS BUT NO NO AVAIL. THE TOTAL ON THE TWO EXCHANGES ROSE AND THAT DOOMED OUR BANKER-OFFICIAL SECTOR INITIATIVE. WE ARE NOW BACK FROM GOLDEN WEEK AND THE CHINESE HAVE STARTED THEIR MASSIVE PURCHASE OF THE PRECIOUS METALS.

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF OCT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

5916 CONTRACTS (FOR 6 TRADING DAYS TOTAL 5916 CONTRACTS) OR 29.580 MILLION OZ: (AVERAGE PER DAY: 986 CONTRACTS OR 4.930 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 29.58 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 4.22% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1701.69 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 554, WITH THE 6 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 813 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A SMALL SIZED: 259 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 813 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 554 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 6 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $17.49 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.056 BILLION OZ TO BE EXACT or 151% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 24 NOTICE(S) FOR 120,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 6.275 MILLION OZ//

- THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

IN GOLD, THE COMEX OPEN INTEREST FELL BY A CONSIDERABLE SIZED 5435 CONTRACTS, TO 614,549 DESPITE THE $7.00 PRICING LOSS WITH RESPECT TO COMEX GOLD PRICING// YESTERDAY// /

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4107 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 4107 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 614,549,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A SMALL LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1328 CONTRACTS: 5435 CONTRACTS DECREASED AT THE COMEX AND 4107 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 1328 CONTRACTS OR 132,800OZ OR 4.13 TONNES. YESTERDAY WE HAD A LOSS OF $7.00 IN GOLD TRADING….

AND WITH THAT LOSS IN PRICE, WE HAD A SMALL LOSS IN GOLD TONNAGE OF 4.13 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON AS ANOTHER RAID WAS INITIATED. THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE BUT UNSUCCESSFUL IN FLEECING MANY GOLD COMEX LONGS FROM THE GOLD ARENA

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT : 18,399 CONTRACTS OR 1,839,900 oz OR 57.22 TONNES (6 TRADING DAYS AND THUS AVERAGING: 3066 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAYS IN TONNES: 57.22 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 57.22/3550 x 100% TONNES =1.61% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4720,94 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

SEPT. 2019 TOTAL ISSUANCE: 509.57 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GOOD SIZED DECREASE IN OI AT THE COMEX OF 5435 WITH THE PRICING LOSS THAT GOLD UNDERTOOK YESTERDAY($7.00)) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 4107 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 4107 EFP CONTRACTS ISSUED, WE HAD A SMALL SIZED LOSS OF 1328 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

4107 CONTRACTS MOVE TO LONDON AND 5435 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE LOSS IN TOTAL OI EQUATES TO 4.13 TONNES). ..AND THIS DECREASE OF DEMAND OCCURRED WITH THE LOSS IN PRICE OF $7.00 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 13 notice(s) filed upon for 1300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN 0.35 TODAY//(COMEX-TO COMEX)

INVENTORY RESTS AT 920.83 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 15 CENTS TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 383.656 MILLION OZ.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A GOOD SIZED 554 CONTRACTS from 212,647 DOWN TO 211,282 AND FURTHER FROM A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR OCT. 0; FOR DEC 813: AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 813 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 554 CONTRACTS TO THE 813 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL SIZED GAIN OF 259 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 1.295 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ// SEPT: 43.030 MILLION OZ//OCT: 6.275MILLION OZ//

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 6 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A GOOD SIZED 813 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 30.52 POINTS OR 1.04% //Hang Sang CLOSED DOWN 131.51 POINTS OR 0.46% /The Nikkei closed DOWN 422.94 POINTS OR 1.97%//Australia’s all ordinaires CLOSED DOWN .42%

/Chinese yuan (ONSHORE) closed DOWN at 6.8807 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8807 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8834 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

4/EUROPEAN AFFAIRS

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

iii) Important USA Economic Stories

iv) Swamp commentaries)

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

total gold withdrawals; nil oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 91,588 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 37,561 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 37,561 CONTRACTS EQUATES to 187 million OZ 26.7% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -1.50% ((SEPT 30/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.06% to NAV (SEPT 30/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -1.50%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 14.66 TRADING 14.17///DISCOUNT 3.34

END

And now the Gold inventory at the GLD/

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

OCT 8/WITH GOLD DOWN 35 CENTS//NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY 923,76 TONNNES

0CT 7 WITH GOLD DOWN 7 DOLLARS//A BIG CHANGE //A DEPOSIT OF 2.93 TONNES//

INVENTORY RISES TO 923.76 TONNES

OCT 1/WITH GOLD UP $15.25 A HUGE PAPER WITHDRAWAL OF 2.05 TONNES FROM THE GLD///INVENTORY REST AT 920.83 TONNES

SEPT 30/WITH GOLD DOWN $32.50: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.06 TONNES FROM THE GLD /INVENTORY RESTS AT 922.88 TONNES

SEPT 27.WITH GOLD DOWN $8.20 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 924.94 TONNES

SEPT 26//WITH GOLD UP $2.70 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.94 TONNES

SEPT 25/WITH GOLD DOWN $26.90 A HUGE PAPER DEPOSIT OF: 16.42 TONNES//INVENTORY RESTS AT 924.94 TONNES

SEPT 24/WITH GOLD UP $8.65 TODAY: A MONSTROUS CHANGE IN GOLD INVENTORY AT THE GLD: AN OUT OF THIS WORLD DEPOSIT OF 14.37 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 894.15 TONNES

SEPT 23/WITH GOLD UP $16.25 ON THE DAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER ADDITION OF 10.65 TONNES//INVENTORY RESTS AT 894.15 TONNES

SEPT 20/WITH GOLD UP $8.60 ON THE DAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 883.06 TONNES

SEPT 19/WITH GOLD DOWN $8.90 TODAY: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 3.23 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 883.60 TONNES

SEPT 18/WITH GOLD UP $2.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 5.86 TONNES/INVENTORY RESTS AT 880.37 TONNES

SEPT 17/WITH GOLD UP $1.50: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 874.51 TONNES

SEPT 16/WITH GOLD UP $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 5.86 TONNES FROM THE GLD///INVENTORY RESTS AT 874.51 TONNES

SEPT 13/WITH GOLD DOWN $7.75 TODAY: A BIG PAPER WITHDRAWAL OF 2.05 TONNES FROM THE GLD/INVENTORY RESTS AT 880.37 TONNES

SEPT 12//WITH GOLD UP $4.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 11/WITH GOLD UP $5.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 10/WITH GOLD DOWN $11.75 TODAY: A HUGE 7.33 PAPER TONNES OF GOLD WAS WITHDRAWN FROM THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 9/WITH GOLD DOWN $4.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 889.75 TONNES

SEPT 6//WITH GOLD DOWN $9.80: A BIG CHANGE IN GOLD INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 6.15 TONNES//INVENTORY RESTS AT 889.75 TONNES

SEPT 5/WITH GOLD DOWN $33.80 TODAY: A BIG ADDITION (DEPOSIT) OF 5.86 OF PAPER GOLD TONNES PROBABLY ADDED BEFORE THE RAID/EXPECT A HUGE PAPER WITHDRAWAL TOMORROW: INVENTORY RESTS AT 895.90 TONNES

SEPT 4/WITH GOLD UP $5.00 TODAY: A BIG CHANGE: A HUGE PAPER DEPOSIT OF: 11.73 TONNES/INVENTORY RESTS AT ….890.04 TONNES

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

OCT 8/2019/ Inventory rests tonight at 923.76 tonnes

*IN LAST 675 TRADING DAYS: 25.44 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 575- TRADING DAYS: A NET 141.25 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

OCT 8.WITH SILVER UP 15 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV//SLV INTORY 383,496 MILLIONOZ

OCT 7/WITH SILVER DOWN 6 CENTS A SMALL WITHDRAWAL OF 166,000 OZ/INVENTORY LOWERS TO 383.496 MILLION OZ

OCT 1.2019 //WITH SILVER UP 30 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 1.87 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.656 MILLION OZ//

SEPT 30/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 381.786 MILLION OZ/

SEPT 27/WITH SILVER DOWN 34 CENTS TODAY/ NO CHANGE IN SILVER INVENTORY AT THE SLV//.INVENTORY RESTS AT 381.786 MILLION OZ/

SEPT 26/WITH SILVER DOWN 12 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.975 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 381.786 MILLION OZ/

SEPT 25.//WITH SILVER DOWN 58 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 377.811 MILLION OZ//

SEPT 24/WITH SILVER DOWN 5 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.338 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 377.811 MILLION OZ//

SEPT 23.2019/WITH SILVER UP 80 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 375.473 MILLION OZ.

SEPT 20/ WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 375.473 MILLION OZ.

SEPT 19/WITH SILVER DOWN 4 CENTS TODAY; A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 1.029 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 375.473 MILLION OZ/

SEPT 18/WITH SILVER DOWN 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 17/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 16/WITH SILVER UP 41 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A PAPER WITHDRAWAL OF 2.899 MILLION OZ OF SILVER LEAVES THE SLV///INVENTORY RESTS AT 376.502 MILLION OZ/

SEPT 13/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 12/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 11/WITH SILVER DOWN ONE CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 10/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 1.778 MILLION PAPER OZ OF SILVER///INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 9/WITH SILVER DOWN 6 CENTS TODAY: A MAMMOTH CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 5.425 MILLION PAPER OZ/INVENTORY RESTS AT 381.179 MILLION OZ../

SEPT 6/WITH SILVER DOWN ANOTHER 60 CENTS TODAY: A RATHER TIMID CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 842,000 PAPER OZ FROM THE SLV///INVENTORY RESTS AT 386.604 MILLION OZ//

SEPT 5/WITH SILVER WHACKED 68 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 4/WITH SILVER UP 28 CENTS TODAY:STRANGE!! A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 708,000 OZ FROM SLV’S INVENTORY:/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 TONNES

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

OCT 8/2019:

Inventory 383.496 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.24/ and libor 6 month duration 2.20

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .04

XXXXXXXX

12 Month MM GOFO

+ 2.21%

LIBOR FOR 12 MONTH DURATION: 2.22

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.01

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

Pam and Russ Martens: There’s nothing normal about the Fed pumping hundreds of billions weekly to Wall Street banks

Submitted by cpowell on Fri, 2019-10-04 16:03. Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Friday, October 4, 2019

Yesterday the House Financial Services Committee released its hearing schedule for October. There is not a peep about holding a hearing on the unprecedented hundreds of billions of dollars that the Federal Reserve Bank of New York is pumping into unnamed banks on Wall Street at a time when there is no public acknowledgement of any kind of financial crisis taking place.

…

Congressional committees should have been instantly on top of the Fed’s actions when they started on September 17 because the Fed had gone completely rogue from 2007 to 2010 in funneling an unfathomable $29 trillion in revolving loans to Wall Street and global banks without authority or even awareness from Congress. The Fed also fought a multi-year court battle with the media in an effort to keep its giant money funnel a secret. …

… For the remainder of the report:

https://wallstreetonparade.com/2019/10/theres-nothing-normal-about-the-f…

* * *

There’s Nothing Normal About the Fed Pumping Hundreds of Billions Weekly to Unnamed Banks on Wall Street: “Somebody’s Got a Problem”

By Pam Martens and Russ Martens: October 4, 2019 ~

John Williams, President of the Federal Reserve Bank of New York

Yesterday, the House Financial Services Committee released its hearing schedule for October. There is not a peep about holding a hearing on the unprecedented hundreds of billions of dollars that the Federal Reserve Bank of New York is pumping into unnamed banks on Wall Street at a time when there is no public acknowledgement of any kind of financial crisis taking place.

Congressional committees should have been instantly on top of the Fed’s actions when they first started on September 17 because the Fed had gone completely rogue from 2007 to 2010 in funneling an unfathomable $29 trillion in revolving loans to Wall Street and global banks without authority or even awareness from Congress. The Fed also fought a multi-year court battle with the media in an effort to keep its giant money funnel a secret.

According to Section 1101 of the Dodd-Frank financial reform legislation of 2010, both the House Financial Services Committee and the Senate Banking Committee are to be briefed on any emergency loans made by the Fed, including the names of the banks doing the borrowing. The section reads:

“The [Federal Reserve] Board shall provide to the Committee on Banking, Housing, and Urban Affairs of the Senate and the Committee on Financial Services of the House of Representatives, (i) not later than 7 days after the Board authorizes any loan or other financial assistance under this paragraph, a report that includes (I) the justification for the exercise of authority to provide such assistance; (II) the identity of the recipients of such assistance; (III) the date and amount of the assistance, and form in which the assistance was provided; and (IV) the material terms of the assistance, including — (aa) duration; (bb) collateral pledged and the value thereof; (cc) all interest, fees, and other revenue or items of value to be received in exchange for the assistance; (dd) any requirements imposed on the recipient with respect to employee compensation, distribution of dividends, or any other corporate decision in exchange for the assistance; and (ee) the expected costs to the taxpayers of such assistance…”

According to multiple sources we queried, the New York Fed has not made the names of these banks doing the borrowing available to either the Senate or House committees. And if there is pushback from the Committees, the public is not hearing about it. It was this exact kind of complacency and lack of leadership on the part of Congress in the early days of the financial crisis in 2007 that gave the Fed the guts to press a button and electronically create trillions of dollars to bail out the worst actors on Wall Street as they used large chunks of that money to reward themselves with tens of millions of dollars in bonuses and pay billions of dollars of the bailout money to lawyers to block their being prosecuted for fraud.

Journalists also failed to properly alert the public to the impending crisis – even when warning bells were loudly clanging.

More than a full year before the worst of the crisis, on August 23, 2007 the New York Times ran the headline “4 Major Banks Tap Fed for Financing.” The correct headline should have been: “Largest Banks in U.S. Take Unprecedented Step of Borrowing from the Fed’s Discount Window.” The article should have appeared on the front page but instead was buried on page C10 of the New York print edition.

Throughout the Fed’s history, a bank that is forced to borrow at the discount window because it can’t get loans elsewhere is seen as being in deep distress. That’s why banks don’t do it. The Times did acknowledge the stigma in the eighth paragraph, writing:

“ ‘Going to the discount window is like someone on the Upper East Side being seen in a Wal-Mart,’ said Charles R. Geisst, a financial historian at Manhattan College. ‘The T-shirts may be cheap, but why would you?’ ”

Geisst added: “ ‘The banks are circling the wagons. Somebody’s got a problem.’ ”

That was perhaps an underwhelming analogy for the situation. Being frugal when shopping for t-shirts is worlds apart from being on the cusp of the greatest banking crisis since the Great Depression.

The four mega banks that borrowed $500 million each at the Fed’s discount window were Citigroup, Bank of America, JPMorgan and Wachovia. Deutsche Bank, Germany’s biggest bank, whose U.S. unit still has a heavy footprint on Wall Street, had tapped the window the prior Friday for an undisclosed amount.

Making the media’s coverage of the early days of the financial crash look even more questionable, the day before the New York Times’ print edition ran the story, the wire service Reuters reported the action with this now infamous quote:

“ ‘The psychology is, if a bank needs to borrow from the discount window, and they think there’s a stigma attached to it, they can say, Citi has done it, too,’ said Robert Albertson, chief strategist at Sandler O’Neill in New York.”

In other words, the general public and even a top Wall Street strategist was under the impression that Citigroup was the strongest of the strong among the Wall Street mega banks at that point in time. In fact, its shakiness was a key source of the unwillingness of banks to lend to one another and why they had to rely on the Fed as a lender of last resort — because they did not know who had exposure to Citigroup. Before the crisis was over, Citigroup would have secretly tapped over $2.5 trillion in revolving loans from the Fed according to the Government Accountability Office (GAO) audit that was released in July 2011.

Sheila Bair, the head of the Federal Deposit Insurance Corporation (FDIC) at the time, wrote this in her subsequent memoir (see Sheila Bair’s Book Gores Citigroup’s Bull):

“By November [2008], the supposedly solvent Citi was back on the ropes, in need of another government handout. The market didn’t buy the OCC’s and NY Fed’s strategy of making it look as though Citi was as healthy as the other commercial banks. Citi had not had a profitable quarter since the second quarter of 2007. Its losses were not attributable to uncontrollable ‘market conditions’; they were attributable to weak management, high levels of leverage, and excessive risk taking. It had major losses driven by their exposures to a virtual hit list of high-risk lending; subprime mortgages, ‘Alt-A’ mortgages, ‘designer’ credit cards, leveraged loans, and poorly underwritten commercial real estate. It had loaded up on exotic CDOs and auction-rate securities. It was taking losses on credit default swaps entered into with weak counterparties, and it had relied on unstable volatile funding – a lot of short-term loans and foreign deposits. If you wanted to make a definitive list of all the bad practices that had led to the crisis, all you had to do was look at Citi’s financial strategies…What’s more, virtually no meaningful supervisory measures had been taken against the bank by either the OCC or the NY Fed…Instead, the OCC and the NY Fed stood by as that sick bank continued to pay major dividends and pretended that it was healthy.”

New York Times’ writers like Andrew Ross Sorkin and Paul Krugman have for years been pushing the narrative that it was not universal banks like Citigroup (where risky securities and derivatives trading are under the same bank holding company roof as the Federally-insured commercial bank) that caused the financial crash of 2008 but rather the investment bank Lehman Brothers and the insurer AIG. In reality, Lehman and AIG were symptoms while Citigroup was the disease. The underlying agenda of Sorkin and Krugman appears to be to thwart Elizabeth Warren’s multi-year efforts to restore the Glass-Steagall Act which prevented these kinds of mergers.

Under the Glass-Steagall legislation of 1933, the U.S. financial system remained safe for 66 years until its repeal in 1999. It took just nine years after the repeal for the U.S. financial system to blow up in a replay of 1929, a time when there had also been no separation between securities speculation and deposit taking.

There are only two ways to look at what is happening today. It starts with basic math. As of June 30 of this year, the four largest commercial banks held more than $5.45 trillion in deposits. The breakdown is as follows: JPMorgan Chase has $1.6 trillion; Bank of America clocks in at $1.44 trillion; Wells Fargo has $1.35 trillion; and Citibank is home to just over $1 trillion.

With $5.45 trillion in deposits, why isn’t there enough liquidity to make loans in the billions. Either the big banks are backing away because of something they see on the horizon or something very troubling has happened to their liquidity.

The New York Fed has trimmed its daily $100 billion in loan offers to just $75 billion per day. This morning, just $38.55 billion of the $75 billion in overnight loans offered by the Fed was taken. But when the New York Fed offered $60 billion in 14-day loans on September 26, there were bids to borrow all of that plus $12.75 billion more or a total of $72.75 billion. (The New York Fed only loaned out the $60 billion.) In other words, one or more banks needed longer-term financing that they could not get elsewhere. As of today, the Fed has made 14-day loans on three different occasions with a total of $139 billion being borrowed by financial institutions that remain anonymous to the American people.

And it is not confidence building that Wall Street players are pointing the finger at JPMorgan Chase, the largest bank in the U.S. with three felony counts which just last month had its precious metals desk named a criminal enterprise and three of its traders criminally charged under the RICO statute that is typically reserved for organized crime.

On October 1, Reuters’ David Henry reported the following:

“Publicly-filed data shows JPMorgan reduced the cash it has on deposit at the Federal Reserve, from which it might have lent, by $158 billion in the year through June, a 57% decline.”

Why isn’t Congress curious about why the country’s largest bank needs to get its hands in a six-month period on $158 billion when it’s supposed to already have $1.6 trillion in deposits and a “fortress balance sheet,” according to its Chairman and CEO, Jamie Dimon.

If Senator Carl Levin were still in Congress and still Chair of the Senate Permanent Subcommittee on Investigations, there would certainly be hearings on this matter happening right now. It was Levin who led the investigation into how JPMorgan Chase had used its depositors’ money to make wild gambles in derivatives in London and lose $6.2 billion in the process. (See our reporting on the London Whale scandal here.)

According to the New York Fed’s annual reports for 2017 and 2018, at the end of 2017 it was holding $1.2 trillion in deposits for its depository institutions, which would have included JPMorgan Chase. But at the end of 2018 that amount had dropped by $314.8 billion or 26 percent.

Compare that drop at the New York Fed to what occurred in the same time frame at the San Francisco Fed. That Fed regional bank had $287.6 billion in deposits at the end of 2017 versus $250.4 billion at the end of 2018, a decline of just $37.2 billion or 12.9 percent.

Thus the question arises, why did the New York Fed allow JPMorgan to withdraw so much liquidity from the system? To help answer that question, Institutional Investor has a must-read article out on the crony operations between Wall Street’s banks and the New York Fed.

No fees with Barclays new gold and silver funds — and no gold and silver either

Submitted by cpowell on Mon, 2019-10-07 14:32. Section: Daily Dispatches

Barclays Launches First Zero-Fee Gold Investment Product

By Chris Flood

Financial Times, London

Monday, October 7, 2019

UK bank Barclays has muscled into the price war in the gold investment market with the launch of the world’s first zero-fee precious metals exchange traded products, which is due to launch in New York on Tuesday.

The aggressive move by Barclays will push competitors, including BlackRock and State Street, to respond with fee cuts at a time when demand for gold from investors is nearing an all-time high.

…

The Barclays iPath Gold exchange-traded note (ETN) and iPath Silver ETN, which will use the tickers GBUG and SBUG respectively, are structured as unsecured debt obligations issued by the UK-listed bank. Both ETNs will use derivatives to match the total return provided by three-month forward gold and silver prices. Most existing competing products track the spot price and are backed by physical holdings of gold and silver that sit in secure bank vaults. …

… For the remainder of the report:

https://www.ft.com/content/391d13fb-e263-3670-8af4-2e9fa862fd4a

end

Craig Hemke is perfectlyy correct..you cannot have any technical analysis in manipulated markets

(Craig Hemke.Stefan Gleeson)

At Money Metals, TF Metals Report’s Craig Hemke scorns technical analysis of manipulated markets

Submitted by cpowell on Mon, 2019-10-07 14:49. Section: Daily Dispatches

10:55a ET Monday, October 7, 2019

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report, interviewed by Mike Gleason of Money Metals Exchange, notes the irrelevance of much technical analysis in markets that are as manipulated as those for gold and silver.

The “spoofing” in the gold and futures markets that recently has yielded indictments and convictions of bullion bank traders in the United States is directly related to the strange “waterfall” smashes in gold and silver in recent years, Hemke says.

…

The gold and silver trading desk of JPMorganChase in New York, whose gold and silver traders have been indicted and convicted, worked closely with the bank’s physical desk in London, Hemke says.

Hemke explains: “Say the physical desk in London has an order that they took a few weeks back and they’ve got to fill. They’ve got to get a ton, 50,000 ounces, whatever. And they’ve got to fill that order and they don’t have it. So they’ve got to go buy it. First they’ve got to get that metal shook free, so they’ve got to convince somebody to sell, but at the same time they might want to save a few bucks when buying that metal and so they get the desk in New York to rig the price lower.

“The guy in London calls up [JPM gold trading desk chief] Michael Nowak and says, ‘Mike, I really could use the price down $10 from here. Could you take care of that for me?’

“Mike gets [confessed JPM gold-spoofing trader John] Edmonds on the phone. They start spoofing away — boom. And you get these waterfall declines where we all sit back and scratch ours head going, ‘Wait a second. Who in their right mind sells 10,000 contracts in 30 seconds?'”

Meanwhile, Hemke says, “Baghdad Bob” financial market letter writers contrive technical analysis explanations for the strange market action, since any candid analysis of it would reveal to their subscribers the uselessness of the technical analysis they’re selling.

Gleason’s interview with Hemke is posted at Money Metals Exchange’s internet site here:

https://www.moneymetals.com/podcasts/2019/10/04/bank-liquidity-crunch-co…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

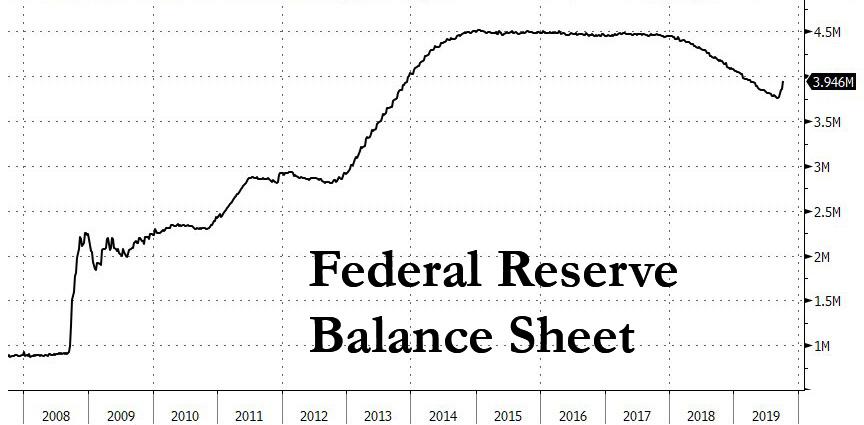

Powell announces QE4 but does not call it QE 4..POMO equals QE4

(zerohedge)

Watch Live: Fed Chair Powell Announces QE4 (But Don’t Call It QE4)

Update: Fed Chair Powell appears to have announced QE4 (but do not call it QE4!):

Discussing the liquidity shortage and repo-calyps, Powell said:

While a range of factors may have contributed to these developments, it is clear that without a sufficient quantity of reserves in the banking system, even routine increases in funding pressures can lead to outsized movements in money market interest rates. This volatility can impede the effective implementation of monetary policy, and we are addressing it. Indeed, my colleagues and I will soon announce measures to add to the supply of reserves over time. Consistent with a decision we made in January, our goal is to provide an ample supply of reserves to ensure that control of the federal funds rate and other short-term interest rates is exercised primarily by setting our administered rates and not through frequent market interventions. Of course, we will not hesitate to conduct temporary operations if needed to foster trading in the federal funds market at rates within the target range.

…

“I want to emphasize that growth of our balance sheet for reserve management purposes should in no way be confused with the large-scale asset purchase programs that we deployed after the financial crisis. Neither the recent technical issues nor the purchases of Treasury bills we are contemplating to resolve them should materially affect the stance of monetary policy…”

Roughly translated:Don’t confuse balance sheet growth for “reserve management” with balance sheet growth for “stock market management”

None of this should come as a surprise as we warned in September that “The Fed Will Restart QE In November: This Is How It Will Do It.”

…In the chart below, Goldman summarizes its projections of the Fed’s future gross Treasury purchases. The blue bars show reinvestment of maturing UST, which occur via add-on Treasury auctions. The red bars show reinvestment of maturing MBS, which occur via the secondary market.

The grey bars are where things get fun as they show permanent OMOs to support trend growth of the Fed’s balance sheet, which will occur via intervention of the Fed’s markets desk in the secondary market.

Here, similar to Bank of America, Goldman assumes a roughly $15bn/month rate of permanent OMOs, enough to support trend growth of the balance sheet plus some additional padding over the first two years to increase the size of the balance sheet by $150bn, restoring the reserve buffer and eliminating the current need for temporary OMOs.

That strategy would result in balance sheet growth of roughly $180bn/year and net UST purchases by the Fed (the sum of the red and grey bars) of roughly $375bn/year over the next couple of years.

And so, in just two months QE… pardon the Fed’s open market purchases of Treasurys, will return after a 5 years hiatus. Just don’t call it QE, whatever you do.

* * *

For the first time since a slew of economic data released over the past week helped ratchet up odds for another Fed rate cut in October, Fed Chairman Jerome Powell will speak Tuesday at the National Association for Business Economics’ annual meeting in Denver.

Just before Powell speaks, the odds of a rate cut in October hovered just over 75%.

Source: Bloomberg

If Powell is truly data-dependent and seeking insurance for the trade deal, then recent events suggest he will be more dovish than hawkish…

Source: Bloomberg

As macro data surprises begin to disappoint serially…

Source: Bloomberg

Following Powell’s prepared remarks, there will be a brief Q&A. Powell is expected to begin speaking at around 2:30 PM ET.

Powell’s comments come on the heels of Chicago Fed’s Evans’ comments that “certainly, asset valuations are quite high.”

end

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

S&P Futures, Global Stocks Tumble As China Trade Deal Hopes Crash And Burn

It started off well enough, with lots of “optimism” that a trade deal was just around the corner thanks to flashing red headlines from first Larry Kudlow and then China on Monday. However, shortly after 3am ET it all started going terribly wrong as first we got some negative Brexit news, when a Downing Street source said that unless the EU compromises and does a Brexit deal shortly, then the UK will leave the EU without a deal, which was then followed by the main event, namely China’s Ministry of Commerce saying to “stay tuned” for Beijing’s retaliation after the US placed eight Chinese technology companies on its “entity list” which now need to be licensed to access US technology exports.

That was just the start however, as China also said it will halt NBA broadcasts, further souring the mood music ahead of the trade talks scheduled this week, while shortly after the SCMP reported that this week’s trade talks were as good as dead when a “source” told the South China Morning Post that the Chinese delegation may cut short their stay in Washington, removing the possible chance of the talks extending into Friday evening as the delegation would be expected to head to the airport instead of departing at some point on Saturday.

Then, just moments later, Bloomberg doubled down on its originally refuted of soft capital controls by the US on China, when it reported that the Trump administration “is moving ahead with discussions around possible restrictions on capital flows into China, with a particular focus on investments made by U.S. government pension funds” adding that “the efforts are advancing even after American officials pushed back strongly against a Bloomberg News report late last month that a range of such limits was under review. Trump officials last week held meetings on the issue just hours after White House adviser Peter Navarro dismissed the report as “fake news,” and zeroed in on how to prevent U.S. government retirement funds from financing China’s economic rise.”

Faced with this mountain of evidence that the odds of even a watered down deal being announced this week are virtually nil, futures plunged, with the Emini sliding from session highs of 2,950 to as low as 2,910, wiping out almost all post-payrolls gains…

… while global markets had deteriorated to a sea of read despite a solid Asian session.

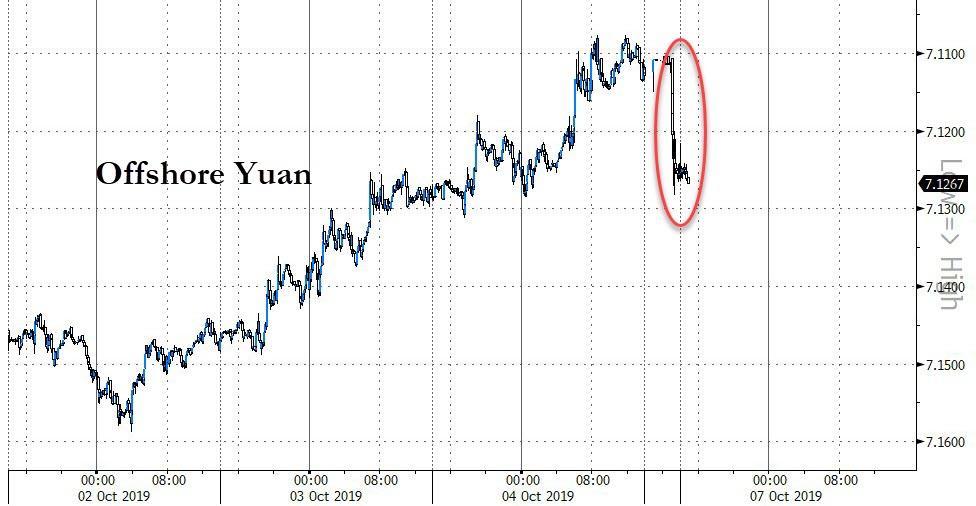

The news also slammed the offshore yuan, which tumbled 0.5% after earlier climbing the most in a month:

The barrage of negative news hit the European STOXX 600 index, which dropped as much as 1%, with Germany’s trade-sensitive DAX hit hard despite earlier data showing an unexpected rise in industrial output. Mixed corporate news added to the woes, with LSE shares tumbling 6% after Hong Kong pulled out of its takeover bid for the exchange, while Germany biotech Qiagen has plunged 16.5% to three-year lows after a sales warning.

Ironically, Europe’s losses followed healthy gains in Asia, where Japan’s Nikkei climbed 1.0% while MSCI’s broadest index of Asia-Pacific shares outside Japan rose 0.55%, led by gains in tech shares in South Korea and Taiwan. Hong Kong extended gains after the territory’s leader said she had no plans to introduce other laws using the emergency regulation ordnance, as it’s too early to say the anti-mask law is ineffective. On the other hand, reports, citing the Chief Executive, noted that the Chinese military could step in if the ongoing protests in the city get worse. The Hong Kong leader also noted that during Golden week, the number of visitors declined 50% Y/Y.

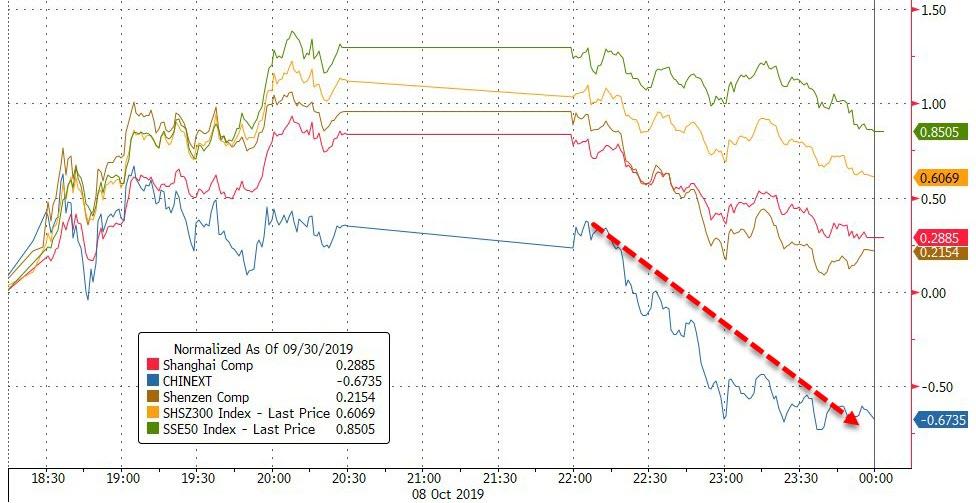

Also of note, China mainland stocks returned from a week-long holiday with a 0.6% rise. The National Holiday celebrations also offered a rare respite to China’s retail sector, with spending on goods and dining returning to growth this year. Yet the latest PMI survey showed China’s services sector grew at its slowest pace in seven months in September, offering little momentum to an economy that has been expanding at its weakest pace in almost three decades.

Source: Bloomberg

Emerging-market stocks advanced as Chinese markets re-opened after a week-long holiday, with most closing as investors still basked in the glow of the positive trade deal sentiment, as China confirmed that a high-level delegation had already left for the talks in Washington, while President Donald Trump said “we’ll see” if a deal could be reached. Of course, all that changed in subsequent hours, but it was too late to hit the majority of EM stocks.

All this happens, of course, as negotiations are getting under way ahead of a scheduled increase in U.S. tariffs on $250 billion worth of Chinese goods, to 30% from 25% on Oct. 15. Trump has said the tariff increase will take effect if no progress is made in the negotiations.

“Since tariffs have been hurting trade, people are hoping Trump may postpone some of the upcoming tariffs,” said Yukino Yamada, senior strategist at Daiwa Securities. “Nevertheless, you can’t ignore that fact that, up until now, the market has underestimated Trump’s determination on tariffs.”

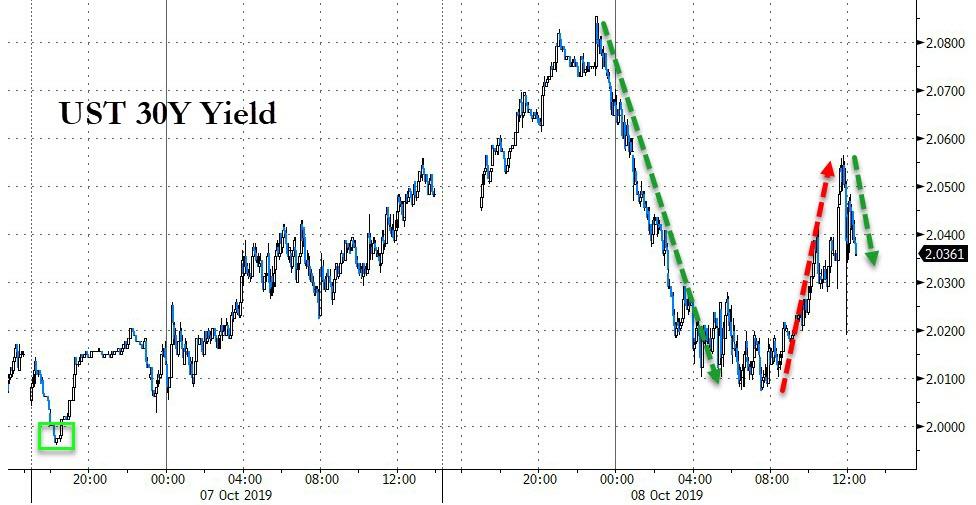

The surge in trade deal uncertainty also added to pressure in fixed income markets with German bund yields nudging lower while U.S. Treasuries yields slumped as low as 1.52% despite some $78 billion in note and bond supply slated for auction this week.

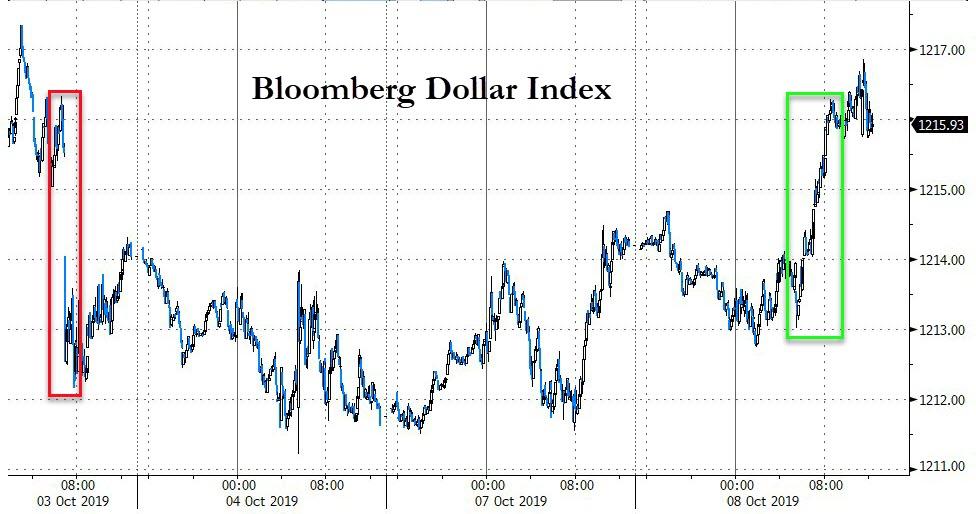

Meanwhile in currencies, the dollar initially lost momentum, dipping 0.1% against a basket of its rivals after posting its biggest single-day rise in a week in the previous session, before rebounding to unchanged. The greenback traded as low as 106.80 yen, after hitting 107.44 earlier. The euro got a boost from the healthy German industrial output data, with the single currency rising 0.2% to $1.0988, not far off the more than a two-year low hit last week.

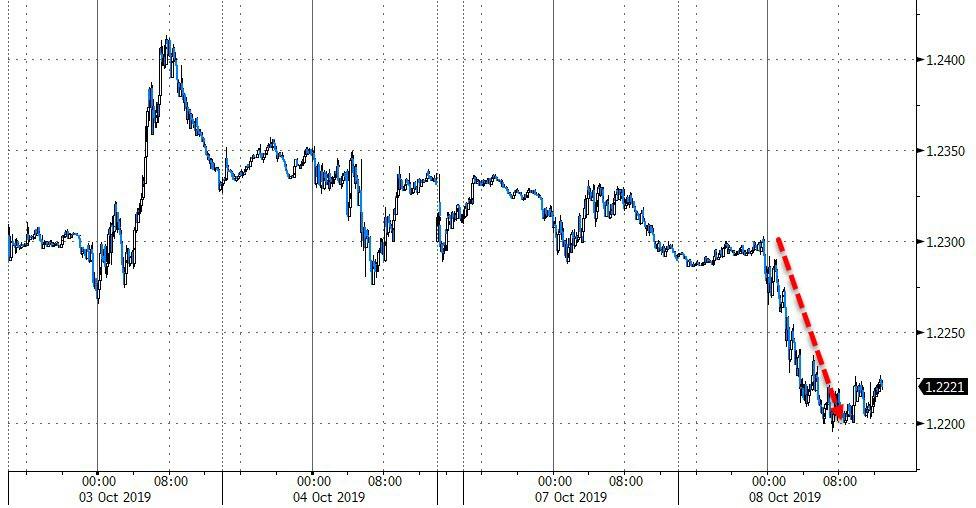

Besides the yuan, the other big mover was the pound sterling which traded at $1.2217, after Boris Johnson told German Chancellor Angela Merkel a Brexit deal is essentially impossible if the EU demands Northern Ireland should stay in the bloc’s customs union. The call between the leaders, at 8 a.m. Tuesday, came after a text message from one of the prime minister’s officials, reported by the Spectator magazine, said his government is preparing for talks to collapse.

Elsewhere, the lira was poised for its first advance in three days, clawing back some of Monday’s losses, which were fueled by concern Turkey’s planned incursion into Syria will deepen a rift between Washington and Ankara. The Turkish Defense Ministry said all preparations are complete for the military operation into Syria, while reports stated that US does not endorse any Turkish operations in northern Syria, according to a senior administration officials who added that US troops will be withdrawn from the Turkey-Syria border, not out of Syria entirely.

Looking ahead, markets will be keenly watching comments from U.S. Federal Reserve Chairman Jerome Powell later in the day, who’s speaking at the annual meeting of the National Association for Business Economics, after some weak U.S. data last week raised concerns the U.S. economy may be heading towards a protracted slowdown. Other central bank speakers include the Fed’s Evans and Kashkari. There’ll be September’s PPI reading and the NFIB small business optimism index, while from Canada there’s September housing starts and August building permits. Expected data include PPI. Helen of Troy is reporting earnings.

Market Snapshot

- S&P 500 futures down 0.5% to 2,916.50

- STOXX Europe 600 down 0.2% to 382.04

- MXAP up 0.6% to 156.40

- MXAPJ up 0.6% to 500.32

- Nikkei up 1% to 21,587.78

- Topix up 0.9% to 1,586.50

- Hang Seng Index up 0.3% to 25,893.40

- Shanghai Composite up 0.3% to 2,913.57

- Sensex down 0.4% to 37,531.98

- Australia S&P/ASX 200 up 0.5% to 6,593.43

- Kospi up 1.2% to 2,046.25

- German 10Y yield fell 0.4 bps to -0.579%

- Euro up 0.2% to $1.0987

- Italian 10Y yield rose 1.9 bps to 0.512%

- Spanish 10Y yield fell 0.5 bps to 0.132%

- Brent futures little changed at $58.36/bbl

- Gold spot up 0.3% to $1,498.34

- U.S. Dollar Index down 0.1% to 98.90

Top Headline News from Bloomberg

- China signaled it would hit back after the Trump administration placed eight of the country’s technology giants on a blacklist over alleged human rights violations. Asked on Tuesday if China would retaliate over the blacklist, foreign ministry spokesman Geng Shuang told reporters “stay tuned.”

- Boris Johnson told German Chancellor Angela Merkel a Brexit deal is “essentially impossible” if the EU demands Northern Ireland should stay in the bloc’s customs union. The call between the leaders, at 8 a.m. Tuesday, came after a text message from one of the prime minister’s officials, reported by the Spectator magazine, said his government is preparing for talks to collapse.

- China’s state TV network CCTV said Tuesday that it would halt broadcasts of the National Basketball Association’s games as a backlash intensified against the U.S. league over a tweet that expressed support for Hong Kong’s pro-democracy protesters.

- The U.K. government revamped the tariffs it will levy after a no-deal Brexit following warnings from industry that its earlier plans risked making domestic producers uncompetitive.

- German industrial production unexpectedly improved in August after two months of decline, a development that will do little to alleviate concerns about intensifying trade tensions and waning business confidence.

- Japanese investors sold a record amount of Spanish bonds in August, seeking to lock in profits from five months of purchases while pivoting more toward U.S. debt.

Asian equities traded higher across the board despite a lacklustre handover from Wall Street where stocks were choppy but ultimately closed in the red amid trade war jitters after the US blacklisted Chinese governmental and commercial organisations over treatment of the Muslim minority community. ASX 200 (+0.4%) was kept afloat by miners amid favourable price action in base metals, whilst Nikkei 225 (+1.0%) was bolstered on the back of a weaker Yen and after US and Japan signed a limited trade deal on agricultural and digital trade. Hang Seng (+0.2%) and Shanghai Comp (+0.3%) returned from a long weekend and played catchup to the NFP-induced upside in the prior session. The former was buoyed by heavyweights Geely Auto after dealers noted a pickup in sales during Golden Week, whilst HKEX shares rose in excess of 2% after it dropped its GBP 32bln bid for LSE, as the boards of the two companies were “unable to engage”. Meanwhile, Mainland China saw upside despite the Caixin Services metric falling short of forecasts, as an improvement in the Composite metric signalled the strongest rate of growth since April. Furthermore, South Korea’s KOSPI (+0.8%) showed a strong performance as the index was supported by tech giant Samsung Electronics, who’s shares spiked higher by 1% after its Q3 guidance topped analyst expectations, albeit it still noted that its profits will likely plunge 56% Y/Y. Finally, core fixed-income futures drifted lower and tracked the risk sentiment around the market with UST and Bund futures poised to close Asia trade near session lows.

Top Asian News

- Hillhouse-Backed Genor Said to Seek Up to $1 Billion Valuation

- Samsung Billionaire Heir to Cede Board Seat Before Legal Probe

Major European Bourses (Euro Stoxx 50 -0.9%) are lower, with the region shrugging off a positive AsiaPac hand over, as trade jitters return to the forefront following the flurry of headlines yesterday evening. This morning, China’s Ministry of Commerce said to stay tuned for a blacklist retaliation to the recent US decision to list 28 Chinese governmental and commercial organisations, including Hikvision, to the entity list over treatment of the Muslim Uighur community. Further contributing to the downbeat tone, SCMP reported that China is toning down expectations head of US/China trade talks, and even though the round of talks will take place this week, a source says that the Chinese delegation is already planning to cut short its stay in Washington by one night. Moreover, Chinese negotiator Liu He will not carry the title of “special envoy” for President Xi Jinping at the meeting, which the article speculated is an early indication that the vice-premier has not been given any particular instructions from China’s leader. Separately, but also contributing some downside to global equities, was a return of no deal Brexit fears, with UK/EU talks seemingly approaching collapse and the UK government vowed to pursue a no deal exit unless the EU compromises. The confluence of negatives saw DAX Dec’ 19 futures lose the 12000 handle. Moving forward, further impetus likely to come in the form of Fed speak (including Powell at 19.30 BST) and Minutes tomorrow and US/China trade talks, US CPI and ECB Minutes on Thursday. Sectors are lower apart from Telecoms (unch.). In terms of individual movers; Airbus (+0.7%) shares were supported by a strong delivery update. Wirecard (-2.8%) initially moved higher after the Co. announced an increase to its Vision 2025 targets, before paring gains alongside the market. EasyJet (-6.3%) shares fell after a trading update; on the face of it the update appeared strong, however investors noted that they had been expecting firmer guidance, while also suggesting that the co.’s decision to not to have a conference call was a mistake. London Stock Exchange (-4.8%) sunk on news that the Hong Kong Exchange and Clearing will no longer proceed with their offer for the Co. Uniper (-8.2%) shares fell and Fortum (-0.2%) initially rose after the former announced it had agreed to acquire a majority stake in the latter, before falling with the market.

Top European News

- Fortum Gets Uniper Control in $2.5 Billion Deal With Funds

- U.K. Tweaks No-Deal Brexit Tariffs for Trucks, Fuel and Clothing

- Johnson Warned Against Big Tax Cuts as U.K. Faces No- Deal Shock

- German Factories Feed Unexpected Rebound in Industrial Output

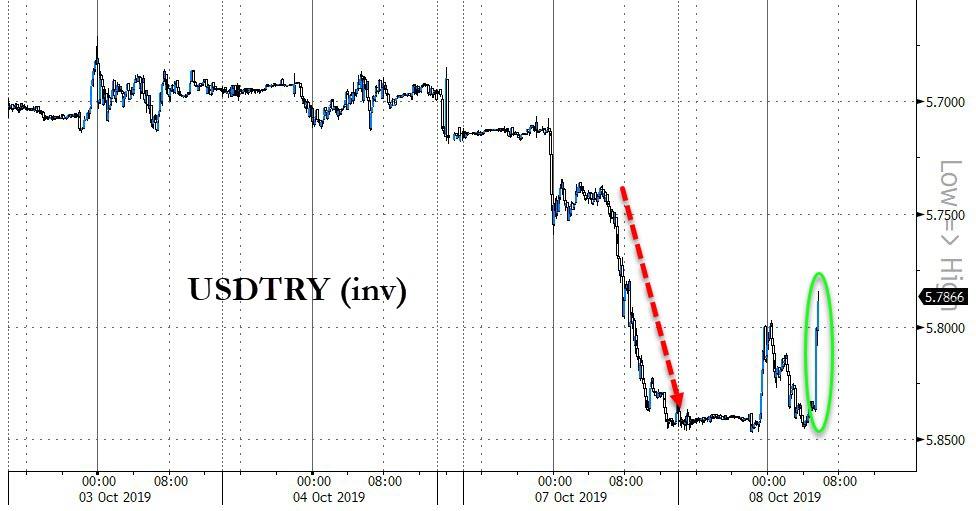

In FX, NZD/AUD/SEK/TRY – Not quite all change, but certainly some solace for the Kiwi, Aussie, Swedish Crown and Turkish Lira following a bad start to the week. Nzd/Usd has regained 0.6300+ status on the back of supportive fiscal impulses as the NZ Finance Minister flagged a 4 bn budget surplus overshoot against target overnight, while Aud/Usd is hovering above 0.6750 in wake of mixed Chinese Caixin PMIs and an uptick in NAB business conditions. Elsewhere, Eur/Sek has eased back from 10.8900+ peaks towards 10.8500 with the aid of some encouraging Swedish data (private/services production and Usd/Try retreated from around 5.8450 to sub-5.8000 at one stage after US President Trump threatened to decimate the Turkish economy if it crosses the line in Northern Syria.

- GBP – In stark contrast to all the above, no deal Brexit risk has put the Pound back on the rack amidst reports that German Chancellor Merkel deems that a breakthrough on the Irish backstop is now highly unlikely, while other headlines contend that an agreement may be dead in the water full stop. In response, Cable lost grip of the 1.2300 handle and filled bids at 1.2275 before ploughing through more between 1.2260-50 on the way through 1.2230, while Eur/Gbp spiked to just over 0.8980 and beyond 500 mn option expiries at 0.8965.

- CHF/EUR/JPY – All firmer against the Dollar even though the DXY nudged back over 99.000 ahead of US PPI and Fed Chair Powell, with an element of underlying safe-haven demand underpinning the Franc, Yen and Euro awaiting US-China trade talks alongside the aforementioned Brexit negotiations on the cusp of collapsing. Usd/Chf is closer to 0.9900, Eur/Usd near the top end of a 1.0965-95 band and Usd/Jpy eyeing 107.00 again from circa 107.45 earlier. Note, latest SCMP reports confirms earlier talk that Beijing is not looking for any major deal and propose to cut their stay short, with Liu He not attending in the guise of special envoy that would imply no remit or agenda to sign off on a full trade agreement.

- NOK/CAD – The Norwegian Krona and Loonie are both holding relatively steady around 10.0400 vs the single currency and 1.3300 vs the Greenback respectively, with the former largely taking comments from Norges Bank Governor Olsen in stride as he underlined guidance for rates to remain on hold after September’s hike, barring the option to reverse the tightening move if economic developments deteriorated significantly. Meanwhile, Canadian housing starts and building permits are due and may provide the Cad with some independent direction or at least a distraction.

In commodities, the crude complex is lower on Tuesday, after negative news flow on the US/China trade and Brexit front spurring risk off. WTI Nov’19 futures broke below yesterday’s USD 52.60/bbl lows and technicians will now be eyeing support just ahead of the USD 52.00/bbl handle. Meanwhile, Brent Nov’ 19 futures are probing support at USD 58.00/bbl. In terms of geopolitical developments, news flow still appears focussed on the US’ recent decision to pull troops out of Northern Syria, which opens the door for a Turkish offensive against Kurdish forces in the area (reports allege the offensive had already begun), rather than on the US/Iran/Saudi picture; given Syria’s lack of oil it remains unlikely that these developments will have much of a baring on crude prices. In supply news, the North Sea’s Buzzard Oilfield remains closed, according to its operator, and there is still no timeline for its return to normal operations. Gold prices have reclaimed the USD 1500/oz mark assisted by the aforementioned trade and Brexit jitters, after reports that China is ready to do a deal on the parts of the negotiations both sides agree upon (and is prepared to set out a timetable for the harder issues to be worked out next year) triggered a lurch lower during US hours on Monday. Copper prices saw upside overnight on decent Chinese Caixin PMI data helped to moderate concerns about an economic slowdown in the country, but has since given up the majority of its overnight gains.

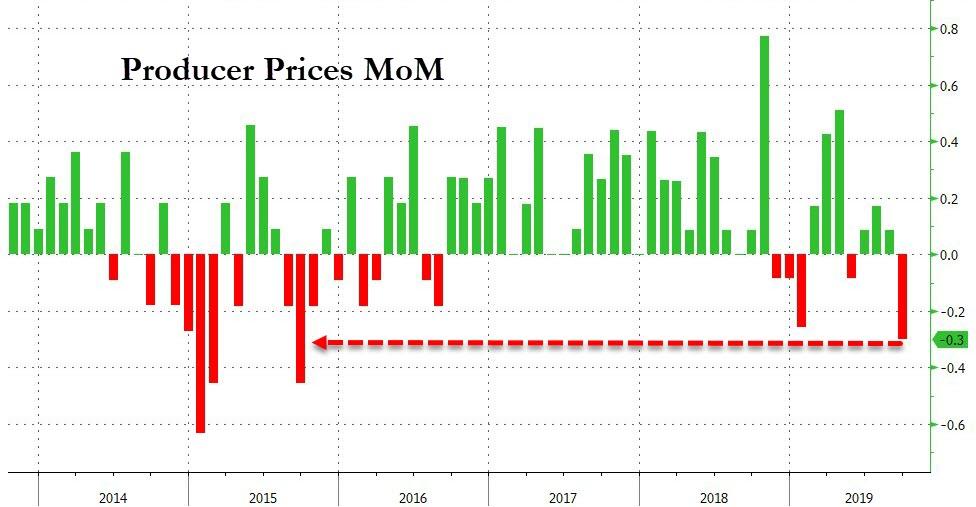

US Event Calendar

- Oct. 8-Oct. 11: Monthly Budget Statement, est. $96.5b, prior $119.1b

- 8:30am: PPI Final Demand MoM, est. 0.1%, prior 0.1%;

- PPI Ex Food and Energy MoM, est. 0.2%, prior 0.3%

- PPI Ex Food, Energy, Trade MoM, est. 0.2%, prior 0.4%

- 8:30am: PPI Final Demand YoY, est. 1.8%, prior 1.8%

- PPI Ex Food and Energy YoY, est. 2.3%, prior 2.3%

- PPI Ex Food, Energy, Trade YoY, prior 1.9%

DB’s Jim Reid concludes the overnight wrap

I’m in need of motivational words from readers this morning. 5 months ago I set off on a journey of betterment and fulfilment but over the last few days I’ve had a wobble, become disillusioned and now need reassurance that I’ve picked the right path. Yes at 45, with three young kids, a full time (demanding) job and numerous other claims on my time I decided to completely remodel my 35 year old golf swing. After starting this process as a 5-handicapper back in early May, yet another poor round this past weekend has seen me move up to 7. Every time I tee the ball up at the moment I’ve got no idea how wild it’s going to be. Most evenings I stand in front of a mirror and do 30-40 minutes of practise swings before videoing it at the end to see the progress. My wife thinks I’m crazy. On camera it’s looking pretty good but on the course I’ve been struggling for months and have given myself tennis elbow for good measure with all the swinging. Oh and I’ve even moved to live opposite my golf course to try to find time to get better. So if you’ve made a big effort to try to get better at something and have experienced big lows before eventually seeing a euphoric payoff then I’ll be delighted to hear from you as I need it to motivate myself through the upcoming winter months.