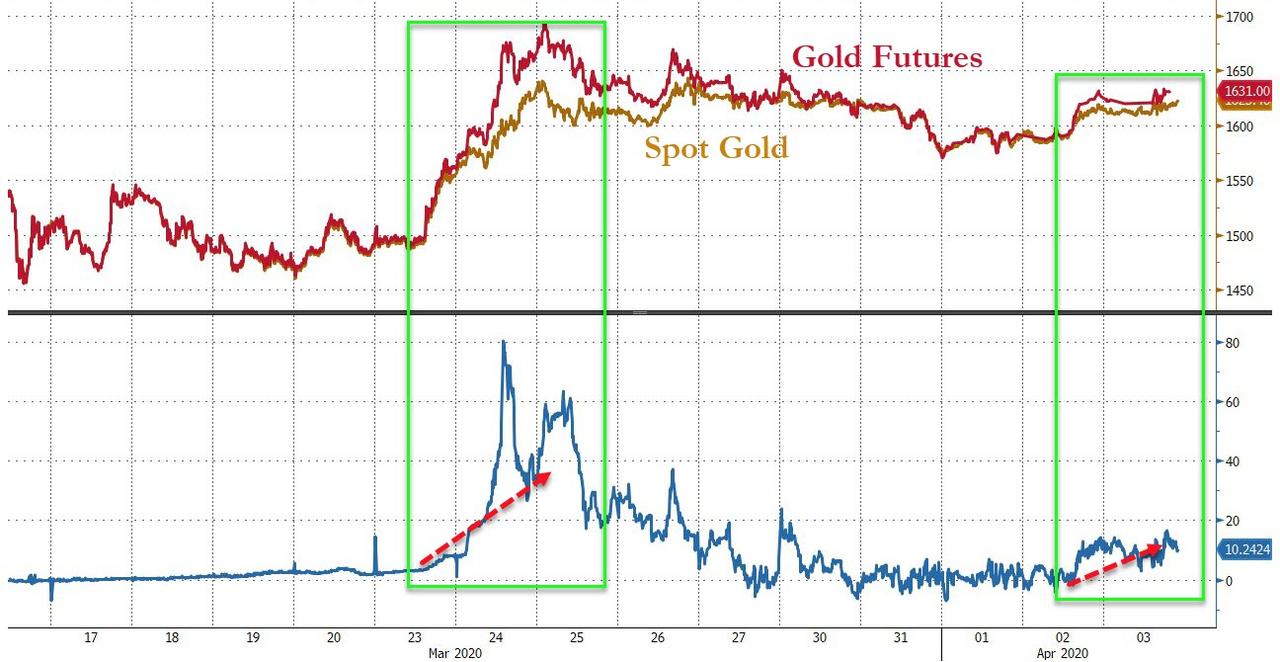

GOLD::$1620.30 UP $7.80 The quote is London spot price

Silver:$14.35//DOWN $.15 London spot price

Closing access prices: London spot

i)Gold : $1621.10 LONDON SPOT 4:30 pm

ii)SILVER: $14.41//LONDON SPOT 4:30 pm

APRIL comex gold price CLOSE 1.30 PM: $1631.0

JUNE GOLD: $1645.50 CLOSE 1.30 PM

SILVER MAY COMEX CLOSE; $14.48…1:30 PM.

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2100. usa per oz

and silver; $28.00 per oz//

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 1083/2590

issued: 1271

EXCHANGE: COMEX

CONTRACT: APRIL 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,625.700000000 USD

INTENT DATE: 04/02/2020 DELIVERY DATE: 04/06/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 H GOLDMAN 456

104 C MIZUHO 1

118 H MACQUARIE FUT 231

132 C SG AMERICAS 8

152 C DORMAN TRADING 1

323 C HSBC 3

323 H HSBC 638

355 C CREDIT SUISSE 34

657 C MORGAN STANLEY 8 21

661 C JP MORGAN 1271 1083

661 H JP MORGAN 427

685 C RJ OBRIEN 8

686 C INTL FCSTONE 366 38

686 H INTL FCSTONE 20

690 C ABN AMRO 20 192

709 C BARCLAYS 12

800 C MAREX SPEC 11 24

880 H CITIGROUP 199

905 C ADM 1 87

____________________________________________________________________________________________

TOTAL: 2,580 2,580

NUMBER OF NOTICES FILED TODAY FOR MAR CONTRACT: 2580 NOTICE(S) FOR 258,000 OZ (8.0254 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 24,489 NOTICES FOR 2,448,900 OZ (76.170 TONNES)

SILVER

FOR APRIL

11 NOTICE(S) FILED TODAY FOR 55,000 OZ/

total number of notices filed so far this month: 753 for 3,765,000 oz

BITCOIN MORNING QUOTE $6966 UP $170

BITCOIN AFTERNOON QUOTE.: $6783 DOWN $14

GLD AND SLV INVENTORIES:

WITH GOLD UP $7.80: AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

WE HAD ANOTHER STRONG DEPOSIT OF 3.22 TONNES

GLD: 971,97 TONNES OF GOLD//

WITH SILVER DOWN 15 CENTS TODAY: AND WITH NO SILVER AROUND

A BIG CHANGE IN SILVER INVENTORY TONIGHT//

A DEPOSIT: OF 746,000 OZ INTO THE SLV INVENTORY

RESTING SLV INVENTORY TONIGHT:

SLV: 395.572 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A CONSIDERABLE SIZED 1582 CONTRACTS FROM 138,473 UP TO 140,055 AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE CONSIDERABLE GAIN IN OI OCCURRED WITH OUR 65 CENT GAIN IN SILVER PRICING AT THE COMEX. WE HAD ZERO LONG LIQUIDATION. IT SEEMS THAT THE GAIN IN OI IS DUE TO BANKER SHORT COVERING PLUS A FAIR EXCHANGE FOR PHYSICAL ISSUANCE ALONG WITH A STRONG GAIN IN SILVER OZ STANDING. WE HAD A GOOD NET GAIN IN OUR TWO EXCHANGES OF 1990 CONTRACTS (SEE CALCULATIONS BELOW)

WE HAVE ALSO WITNESSED A STRONG AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: MARCH: 00 AND MAY: 280 AND JULY: 0 ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 280 CONTRACTS. WITH THE TRANSFER OF 280 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 280 EFP CONTRACTS TRANSLATES INTO 1.400 MILLION OZ ACCOMPANYING:

1.THE 65 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.015 MILLION OZ INITIALLY STANDING FOR APRIL

THURSDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 65 CENTS).. AND, OUR OFFICIAL SECTOR/BANKERS WERE TOTALLY UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS, AS WE DID HAVE A STRONG NET GAIN OF 1862 CONTRACTS OR 9.310 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER.

OUR SPREADING OPERATION HAS NOW SWITCHED INTO SILVER…..

SPREADING OPERATION FOR OUR NEWCOMERS:

WE HAVE NOW COMMENCED IN SILVER THE ILLEGAL SPREADING OPERATION \ FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW STOPPED IN GOLD AS THEY NOW BEGIN TO MORPH INTO SILVER AS WE HEAD TOWARDS THE NEW FRONT MONTH WILL BE MAY.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF APRIL. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

2199 CONTRACTS (FOR 3 TRADING DAYS TOTAL 2199 CONTRACTS) OR 10.995 MILLION OZ: (AVERAGE PER DAY: 733 CONTRACTS OR 3.665 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF APRIL: 10.995 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 1.57% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 904.48 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP SO FAR 10.995 MILLION OZ.

RESULT: WE HAD A CONSIDERABLE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1582, WITH THE $0.65 GAIN IN SILVER PRICING AT THE COMEX /THURSDAY… THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 280 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A STRONG TOTAL OI CONTRACTS ON THE TWO EXCHANGES: 1862 CONTRACTS (WITH THE 65 CENT GAIN IN PRICE)

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 280 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1582 OI COMEX CONTRACTS.AND ALL OF THIS DEMAND HAPPENED WITH A 65 CENT GAIN IN PRICE OF SILVER/ AND A CLOSING PRICE OF $14.50 // THURSDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY AS WELL AS A HUGE INCREASE IN QUEUE JUMPING!!

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.700 BILLION OZ TO BE EXACT or 100.0% of annual global silver production (ex Russia & ex China).

FOR THE NEW MAR DELIVERY MONTH/ THEY FILED AT THE COMEX: 11 NOTICE(S) FOR 55,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.015 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL 185 CONTRACTS TO 490,140 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE GAIN OF COMEX OI OCCURRED WITH OUR COMEX GAIN IN PRICE OF $31.80 /// COMEX GOLD TRADING// THURSDAY// WE HAD CONSIDERABLE BANKER SHORT COVERING ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A FAIR EX. FOR PHYSICAL ISSUANCE AND YET THIS WAS COUPLED WITH THAT STRONG ADVANCE IN THE PAPER PRICE OF GOLD. THUS THE GAIN ON THE COMEX WAS DUE TO CONSIDERABLE BANKER SHORT COVERING, ZERO LONG LIQUIDATION, A STRONG INCREASE IN GOLD OZ STANDING AND OUR NORMAL GAIN IN EXCHANGE FOR PHYSICALS (POSITIVE), . WE GAINED A FAIR 2,714 CONTRACTS (8.441 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 2529 CONTRACTS:

CONTRACTS, FEB> 0 CONTRACTS; MARCH 00 APRIL: 0. MAY: 0, AND JUNE 2529.; DEC 0 AND ALL OTHER MONTHS ZERO//TOTAL: 2529. The NEW COMEX OI for the gold complex rests at 490,140. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2,714 CONTRACTS: 185 CONTRACTS INCREASED AT THE COMEX AND 2529 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 2,714 CONTRACTS OR 8.441 TONNES. THURSDAY, WE HAD A CONSIDERABLE GAIN OF $31.80 IN GOLD TRADING……

AND WITH THAT CONSIDERABLE GAIN IN PRICE, SURPRISINGLY WE HAD A GOOD SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 8.441 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (ROSE $31.80). AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WERE UNSUCCESSFUL ( SEE BELOW)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A FAIR SIZED INCREASE IN EXCHANGE FOR PHYSICALS (2529) ACCOMPANYING THE TINY GAIN IN COMEX OI.(185 OI): TOTAL GAIN IN THE TWO EXCHANGES: 2,714 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)A MONSTROUS STANDING AT THE GOLD COMEX FOR THE FRONT APRIL MONTH, 3) ZERO LONG LIQUIDATION AND …ALL OF THIS WAS COUPLED WITH THAT HUGE GAIN IN GOLD PRICE TRADING//THURSDAY

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 14,737 CONTRACTS OR 1,473,700 oz OR 45.84 TONNES (3 TRADING DAYS AND THUS AVERAGING: 4912 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES: 45.84 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 45.84/3550 x 100% TONNES =1.29% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS EXPLODED THIS MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 2368.74 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (//(*AND A NEW ALL TIME RECORD ISSUANCE)

APRIL TOTAL EFP. ISSUANCE: 45.84 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest in SILVER ROSE BY A CONSIDERABLE SIZED 1582 CONTRACTS FROM 138,473 UP TO 140,055 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

ALL OF THE GAIN IN COMEX OI WAS DUE TO 1) HUGE BANKER SHORT COVERING , 2) THE ISSUANCE OF A FAIR SIZED NUMBER OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A STRONG INCREASE IN SILVER OZ STANDING AT THE COMEX FOR APRIL AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 280 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR FEB. 0; FOR MAR 0: AND MAY: 280; JULY: 00 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 280 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1582 CONTRACTS TO THE 280 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 1862 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 9.330 MILLION OZ!!! AND WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ// SEPT: 43.030 MILLION OZ///OCT: 7.32 MILLION OZ//NOV 2.63 MILLION OZ//DEC: 20.970 MILLION OZ//JAN: 5.075 MILLION OZ//FEB: 1.480 MILLION OZ//MAR: 23.005 MILLION OZ//APRIL 4.015 MILLION OZ//

RESULT: A CONSIDERABLE SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 65 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// THURSDAY. WE ALSO HAD A VERY FAIR SIZED 280 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON. THE ENTIRE LOSS OF COMEX OI WAS DUE TO SPREADER LIQUIDATION AND THAT HUGE ISSUANCE OF EX. FOR PHYSICALS.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED DOWN 16.65 POINTS OR 0.60% //Hang Sang CLOSED DOWN 43.95 POINTS OR 0.19% /The Nikkei closed UP 1.47 POINTS OR 0.01%//Australia’s all ordinaires CLOSED DOWN 1.57%

/Chinese yuan (ONSHORE) closed DOWN at 7.0924 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 67.0924 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1143 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED/CORONAVIRUS : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

LET US BEGIN:

i) Into BRINKS: 35,077.394 OZ

ii) Into HSBC: 2499.96 oz

iii) Into Malca 433,998.000 oz or 13,500 kilobars

and a phony entry…

total gold withdrawals; NIL oz

ADJUSTMENTS: 2

a)out of Brinks: 35,013.098 oz was adjusted out of the customer and this landed into the dealer of Brinks

b) Out of Malca: 62,879.532 oz was adjusted out of the dealer and this lands into the customer account of Malca

NEW PLEDGED GOLD: BRINKS

3027.500 OZ REMOVED TO THE PLEDGED ACCOUNT JAN 10.2020/Brinks

176,211.457 oz NOW PLEDGED JAN 21.2020/HSBC 5.4807 TONNES

341,434.443 oz PLEDGED MARCH 2020 JPMORGAN: 10.62 TONNES

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234

TOTAL PLEDGED GOLD NOW IN EFFECT: 560,194.208 OZ OR 17.424 TONNES

And now for the wild silver comex results

Total COMEX silver OI ROSE BY A CONSIDERABLE SIZED 1582 CONTRACTS FROM 138,501 DOWN TO 140,140 (AND MOVING CLOSER TO THE NEW ALL TIME RECORD OI FOR SILVER SET ON FEB 25.2020(244,710) ECLIPSING OUR PREVIOUS RECORD, AUGUST 25/2018 RECORD (244,196). THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9.2018/ 243,411 CONTRACTS) . OUR CONSIDERABLE OI COMEX GAIN TODAY OCCURRED WITH OUR 65 CENT INCREASE IN PRICING/THURSDAY. THE GAIN IN OI OCCURRED WITH 1) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS 2) STRONG INCREASE IN SILVER OZ STANDING AT THE COMEX, 3) HUGE BANKER SHORT COVERING COUPLED ZERO LONG LIQUIDATION.

WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF APRIL

.APRIL ACTIVE DELIVERY MONTH.

THE FRONT MONTH OF APRIL HAS A TOTAL OPEN INTEREST OF 61 CONTRACTS, AND AS SUCH GAINED 5 CONTRACTS. WE HAD 18 NOTICES SERVED UPON YESTERDAY SO WE AGAIN, GAINED 23 CONTRACTS OR 115,000 OZ WILL STAND AT THE COMEX AS THEY REFUSED TO MORPH INTO LONDON BASED CONTRACTS AS THEY LOOK FOR METAL ON THIS SIDE OF THE POND.

THE BIG CONTRACT OF MAY SAW ITS OI RISE BY 443 UP TO 77,779.

JUNE SAW A GAIN OF 0 CONTRACTS REMAINING AT 5.

We, today, had 11 notice(s) FILED for 55,000, OZ for the MAR, 2019 COMEX contract for silver

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory |

372,352.885 oz

CNT

DELAWARE

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

299,871.140 oz

CNT

|

| No of oz served today (contracts) |

11

CONTRACT(S)

(55,000 OZ)

|

| No of oz to be served (notices) |

50 contracts

250,000 oz)

|

| Total monthly oz silver served (contracts) | 753 contracts

3,765,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

total dealer deposits: 0 oz

total dealer withdrawals: 0 oz

i)we had 1 deposits into the customer account

into JPMorgan: 0

ii)into CNT: 299,871.140 OZ

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.819 million oz of total silver inventory or 50.04% of all official comex silver. (160.819 million/321.170 million

total customer deposits today: 600,971.200 oz

we had 2 withdrawals:

total withdrawals; 372,352.895 oz

We had 0 adjustments: and all from the dealer to the customer:

total dealer silver: 82.178 million

total dealer + customer silver: 321.097 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The total number of notices filed today for the APRIL 2020. contract month is represented by 11 contract(s) FOR 55,000 oz

To calculate the number of silver ounces that will stand for delivery in APRIL we take the total number of notices filed for the month so far at 753 x 5,000 oz = 3,765,000 oz to which we add the difference between the open interest for the front month of APRIL.( 61) and the number of notices served upon today 11 x (5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL/2019 contract month: 753 (notices served so far) x 5000 oz + OI for front month of APRIL (61)- number of notices served upon today (11) x 5000 oz of silver standing for the APRIL contract month.equals 4,015,000 oz.

WE GAINED 23 CONTRACTS OR AN ADDITIONAL 115,000 OZ OF SILVER WILL STAND AT THE COMEX.

TODAY’S ESTIMATED SILVER VOLUME: 22,705 CONTRACTS //

FOR YESTERDAY: 66,541 CONTRACTS..,CONFIRMED VOLUME

YESTERDAY’S CONFIRMED VOLUME OF 66,541 CONTRACTS EQUATES to 332 million OZ 47.5% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO +1.53% ((APRIL 3/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.03% to NAV: (APRIL 3/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into POSITIVE/ 1.53%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 14.82 TRADING 14.86///PREMIUM 0.25

END

And now the Gold inventory at the GLD/

APRIL 3//WITH GOLD UP $7.80 TODAY//ANOTHER STRONG DEPOSIT OF 3.22 TONNES INTO THE GLD/INVENTORY RESTS AT 971.97 TONNES

APRIL 2//WITH GOLD UP $31.80 TODAY: ANOTHER STRONG DEPOSIT OF 1.75 TONNES INTO THE GLD//INVENTORY RESTS AT 968.75 TONNES

APRIL 1/WITH GOLD DOWN $7.70 TODAY: ANOTHER CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.62 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 967.00 TONNES

MARCH 31//WITH GOLD DOWN $32.70//A MONSTROUS PAPER DEPOSIT OF 10.84 TONNES INTO THE GLD//INVENTORY RESTS AT 964.38 TONNES

MARCH 30/WITH GOLD DOWN $6.10 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 953.54 TONNES

MARCH 27.WITH GOLD DOWN $16.40: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A HUGE DEPOSIT OF 4.39 TONES INTO THE GLD/INVENTORY RESTS AT 953.54 TONES

MARCH 26//WITH GOLD UP $24.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 13.17 TONNES INTO THE GLD/INVENTORY RESTS AT 949.15 TONNES

MARCH 25/WITH GOLD DOWN $11.40 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.99 TONES INTO THE GLD INVENTORY////INVENTORY RESTS AT 935.98 TONNES

MARCH 24//WITH GOLD UP $67.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 15.80 TONNES OF GOLD INTO GLD////INVENTORY RESTS AT 923.99 TONNES..THIS PROVES THAT THE GLD IS A FRAUD AS LONDON SUSPENDED DELIVERY AS WELL AS ALL REFINERS. THEY HAD NO WAY OF GETTING ANY PHYSICAL OZ INTO ITS INVENTORY//

MARCH 23//WITH GOLD UP $76.00 TODAY: A HUGE PAPER WITHDRAWAL OF 21.50 TONNES FROM THE GLD////INVENTORY RESTS AT 908.19 TONNES

MARCH 20//WITH GOLD UP $5.50//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 7.46 TONNES FROM THE GLD////INVENTORY RESTS AT 922.23 TONNES

MARCH 19/WITH GOLD DOWN 90 CENTS: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 929.84 TONNES

MARCH 18/WITH GOLD DOWN $48.00: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 929.84 TONNES

MARCH 17/WITH GOLD UP $37.60: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM GLD INVENTORY//INVENTORY RESTS AT 929.84 TONNES

MARCH 16/WITH GOLD DOWN $30.00/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 12.59 TONNES/INVENTORY RESTS AT 931.59 TONNES

MARCH 13//WITH GOLD DOWN $73.60: A HUGE WITHDRAWAL OF 9.02 TONNES OF PAPER GOLD FROM THE GLD//

INVENTORY RESTS AT 944.18 TONNES

MARCH 12/WITH GOLD DOWN $55.05 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/953.26 TONNES

MAR 11/WITH GOLD DOWN $14.95?/A HUGE WITHDRAWAL OF 10.53 TONNES//INVENTORY RESTS AT 953.26 TONNES

MARCH 10/WITH GOLD DOWN $14.25//A HUGE 8.00 TONNES OF PAPER GOLD DEPOSIT INTO THE GLD//INVENTORY RESTS AT 963.79

MARCH 9//WITH GOLD UP $1.50 : NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 955.60 TONNES

March 6/WITH GOLD UP $6.25 A MASSIVE 21.37 PAPER TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 955.60 TONNES

MARCH 5/WITH GOLD UP $25.40//NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS TONIGHT AT 934.23 TONNES

MARCH 4//WITH GOLD DOWN 1 DOLLAR: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.23 TONNES//

MARCH 3//WITH GOLD UP 48.55 TODAY; NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.23 TONNES

MARCH 2//WITH GOLD UP $27.00// no change in gold inventory at the gld//inventory remains at 934.23 tonnes

FEB 28/WITH GOLD DOWN $73.00 WE LOST NO GOLD FROM THE GLD/INVENTORY REMAINS 934.23 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

APRIL 3/2020/ 971.97 tonnes*

IN LAST 792 TRADING DAYS: +27.28 NET TONNES HAVE BEEN REMOVED FROM THE GLD

LAST 692 TRADING DAYS;+202.26 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

APRIL 3//WITH SILVER DOWN 15 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 746,000 OZ INTO THE SLV//INVENTORY RESTS AT 395.826 MILLION OZ

APRIL 2/WITH SILVER UP 65 CENTS; A SMALL CHANGE TODAY..A WITHDRAWAL OF .335 MILLION OZ TO PAY FOR FEES//INVENTORY RESTS AT 394.826 MILLION OZ/

APRIL 1/WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 395.181 MILLION OZ//

MARCH 31/WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 1.679 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 375.181 MILLION OZ//

MARCH 30/WITH SILVER DOWN 44 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 393.502 MILLION OZ.

MARCH 27/WITH SILVER DOWN 5 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTROUS PAPER DEPOSIT OF 8.115 MILLION OZ INTO THE SLV../INVENTORY RESTS AT 393.502 MILLION OZ//

MARCH 26/WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 385.387 MILLION OZ///

MARCH 25/WITH SILVER UP 44 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSITS OF 7.369 MILLION OZ AND 2.239 MILLION OZ OF PAPER SILVER INTO THE SLV////INVENTORY RESTS AT 385.387 MILLION OZ//

MARCH 24//WITH SILVER UP 100 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 375.779 MILLION OZ///

MARCH 23//WITH SILVER UP 70 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.332 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 375.779 MILLION OZ

MARCH 20//WITH SILVER UP 39 CENTS TODAY: 2 HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A PAPER WITHDRAWAL OF 1.026 MILLION OZ FROM THE SLV AND THEN A PAPER ADDITION OF 3.638 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 373.447 MILLION OZ//

MARCH 19/WITH SILVER UP 38 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: ANOTHER 5.597 MILLION OZ OF SILVER VAPOUR ADDED TO THE SLV INVENTORY//INVENTORY RESTS AT 370.835 MILLION OZ/

MARCH 18//WITH SILVER DOWN 75 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTROUS 12.035 MILLION PAPER OZ ADDED INTO INVENTORY//INVENTORY RESTS AT 365.238 MILLION OZ//

MARCH 17/WITH SILVER DOWN 20 CENTS TODAY; A BIG CHANGES IN SILVER INVENTORY AT THE SLV; A WITHDRAWAL OF 3.735 MILLION OZ FROM THE SLV INVENTORY: INVENTORY RESTS AT 353.203 MILLION OZ///

MARCH 16/WITH SILVER DOWN 177 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESETS AT 356.938 MILLION OZ//

MARCH 13//WITH SILVER DOWN 155 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.893 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 356.938 MILLION OZ;

MARCH 12/WITH SILVER DOWN 77 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.119 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 359.828 MILLION OZ

MARCH 11/SILVER DOWN 16 CENTS: A SMALL WITHDRAWAL OF .467 MILLION OZ AT THE SLV/INVENTORY RESTS AT 360.947 MILLION OZ//

MARCH 10/WITH SILVER DOWN 10 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 361.414 MILLION OZ//

MARCH 9/NO CHANGE IN INVENTORY LEVELS: SLV INVENTORY RESTS AT 361.414 MILLION OZ//

MARCH 6//WITH SILVER DOWN 10 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 361.414 MILLION OZ

MARCH 5//WITH SILVER UP 15 CENTS TODAY; A SMALL WITHDRAWAL DUE TO FEES ETC//INVENTORY RESTS TONIGHT AT 361.414 MILLION OZ..

MARCH 4/SILVER SILVER UP 3 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 361.880 MILLION OZ//

MARCH 3/WITH SILVER UP 44 CENTS//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: A LOSS OF 5.75 MILLION OZ FROM THE SLV../INVENTORY RESTS AT 361.880 MILLION OZ

MARCH 2//WITH SILVER UP 18 CENTS//NO CHANGE IN SILVER INVENTORY AT THE SLV..INVENTORY RESTS AT 367.632 MILLION OZ//

FEB 28/ WITH SILVER DOWN 18 CENTS: a loss of 1.867 million oz//inventory rests at 367.632 million oz

APRIL 3.2020:

SLV INVENTORY RESTS TONIGHT AT

395.572 MILLION OZ.

END

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 1.93/ and libor 6 month duration 1.21

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .72

XXXXXXXX

12 Month MM GOFO

+ 1.09%

LIBOR FOR 12 MONTH DURATION: 1.06

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -.03

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Gold Bullion Coin and Bar Shortages Continue and Deepen

Editors Note: The shortage of gold bullion coins and bars continues and appears to be deepening. It is not just smaller one ounce bullion coins and bars that are sold out and increasingly unavailable but also larger gold and silver bars including gold kilo bars (32.15 ozs) worth and 1,000 oz silver bars. Refineries, government mints and brokers around the world have raised premiums.

at just $1,705 per coin based on a spot price of $1,612/oz

Gold Dealers Report Big Shortages of Small Bars and Coins

(Bloomberg) — When people are worried about the future they turn to gold to protect their savings. That’s rarely been more true than today.

Surging demand and disruptions from the coronavirus pandemic have created a shortage of the small gold bars most popular with consumers. Those who do manage to get their hands on metal have to pay up –- well above the per-ounce prices being quoted on financial markets in London and New York.

Some dealers are desperately contacting clients to see if anyone is willing to sell their gold bars and coins, and offering a rare premium over spot prices. Others have given up trying to trade altogether.

“People want to buy, not to sell gold,” said Mark O’Byrne, the founder of GoldCore, a dealer based in Dublin. “We have a buyers’ waiting list and we emailed our clients seeing who wished to sell their gold. At this time there is roughly only one or two sellers for every 99 buyers.”

Read on Bloomberg or on Yahoo Finance

| ◆ Gold and Silver Coin and Bar Premiums – What Is Happening?

◆ Premiums are higher on gold and silver coins and bars, both when you buy and when you sell, and may stay higher in the “new normal.” ◆ Bullion coin and bar premiums are not commissions and brokers only make a small component of the premium in what is a very low margin business. ◆ Beware of aggressive pricing strategies on coins and bars and focus on getting value with regard to premiums. ◆ GoldCore remains open for business and when they become available we are buying coins and bars from our government mint and large refinery suppliers and from our clients. While oremiums have surged, we have kept our premiums very competitive. We are paying 1.5% over spot gold to clients for gold kilo bars and higher premiums for smaller bars and bullion coins (1 oz). ◆ We are only selling to clients who have cleared funds on account and are on our Buyers List as we simply cannot meet the demand we are experiencing. |

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

01-Apr-20 1594.25 1576.55, 1288.95 1270.23 & 1457.94 1442.86

31-Mar-20 1604.65 1608.95, 1299.61 1296.81 & 1461.52 1468.81

30-Mar-20 1624.35 1618.30, 1312.56 1305.97 & 1466.88 1466.02

27-Mar-20 1621.20 1617.30, 1325.33 1316.16 & 1473.18 1469.48

26-Mar-20 1620.10 1634.80, 1361.37 1358.19 & 1480.12 1487.01

25-Mar-20 1620.95 1605.45, 1357.22 1371.38 & 1494.84 1486.17

24-Mar-20 1599.50 1605.75, 1362.61 1371.47 & 1472.98 1489.49

23-Mar-20 1494.50 1525.40, 1288.86 1312.91 & 1399.60 1411.00

20-Mar-20 1504.45 1494.40, 1275.32 1258.28 & 1400.34 1391.59

19-Mar-20 1480.70 1474.25, 1285.54 1257.83 & 1369.94 1365.89

18-Mar-20 1506.00 1498.20, 1254.50 1271.22 & 1367.00 1378.04

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here

ii) Important gold commentaries courtesy of GATA/Chris Powell

We brought this important development to your attention yesterday but it is worth repeating: how on earth can these guys clear? How about naked shorting where they must obtain a certificate to engage in shorting?

(Chris Powell/GATA)

U.S. stock clearinghouse suspends certificate repatriation

Submitted by cpowell on Thu, 2020-04-02 23:32. Section: Daily Dispatches

7:33p ET Thursday, April 2, 2020

Dear Friend of GATA and Gold:

The Depository Trust & Clearing Corp., which stores most stock certificates and settles most securities transactions in the United States, has suspended all securities repatriation services since March 23 and announced on March 28 that these services will remain suspended until at least April 6. The suspension was attributed to difficulties arising from the virus epidemic sweeping the world.

So anyone who wants to take possession of stock certificates or transfer them to the possession of someone else is out of luck for the time being.

…

This is a situation that gold advocate and mining entrepreneur Jim Sinclair of JSMineset.com often warned against years ago.

The DTCC says all the rest of its services remain operational, though in recent years some investors and corporate officials have complained that those services include facilitating naked short selling.

In an update on the DTCC’s internet site dated March 28 —

https://www.dtcc.com/dtcc-connection/articles/2020/march/18/continuing-t…

— DTCC President and Chief Executive Officer Michael C. Bodson says:

“Due to ongoing concerns related to the COVID-19 virus, we have taken the decision to extend the suspension of all physical processing services until, at the earliest, Monday April 6, 2020.

“DTC requests that participants and transfer agents not send certificates via messenger, courier services, or U.S. Postal Service to DTC until further notice as DTC will not have a mechanism to accept or perform any transaction processing.

“Further details are provided in Important Notice B13161-20: Temporary Suspension of All DTC Physical Securities Processing. This notice supersedes important notice B#13153-20 distributed on March 26, 2020, announcing the re-opening of physical processing, which is no longer accurate.

“All other DTC services remain business as usual. DTCC remains open and we continue to provide uninterrupted access to our products and services to our clients across the globe. Further details are provided in the Physical Securities Processing FAQ (3/30/2020).”

Of course this is hardly the only company that has been hobbled in some way by the virus epidemic, and with luck things will get back to normal everywhere in a few months. But in the meantime the ultimate proof of the ownership of most stock shares in the United States is not available and hypothecation and rehypothecation of shares may become even easier.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Mexico to all some projects to be mined deemed essential

(Reuters/GATA)

Mexican miners to keep working essential projects amid virus closures, sources tell Reuters

Submitted by cpowell on Thu, 2020-04-02 23:45. Section: Daily Dispatches

By Diego Ore

Reuters

Wednesday, April 1,

https://www.reuters.com/article/health-coronavirus-mexico-mining/mexican…

MEXICO CITY — Mexico’s mining sector, one of the country’s major industries, will be able to continue operating projects deemed to be essential during the public health crisis caused by the coronavirus, two government officials told Reuters.

President Andres Manuel Lopez Obrador’s administration this week declared a health emergency due to the viral outbreak which requires that non-essential work be shut down or minimized.

…

But the mining sector, responsible for about 4 percent of Mexico’s gross domestic product, will be able to continue with some projects in an effort to avoid the “paralyzation” of future operations as well as to promote mine safety, the sources said.

END

A must read: Pat Heller collectedly states that both London and New York gold/silver markets defaulted on gold deliveries

(Pat Heller /Liberty Coin/GATA)

Pat Heller: Did the London/New York markets default on gold deliveries?

Submitted by cpowell on Fri, 2020-04-03 03:55. Section: Daily Dispatches

11:55p ET Thursday, April 2, 2020

Dear Friend of GATA and Gold:

Veteran coin and bullion dealer Pat Heller of Liberty Coin Service in Lansing, Michigan, today provides via Numismatic News an excellent summary of the critical tightness in the physical gold and silver markets and the scheming being done by the London Bullion Market Association and the New York Commodities Exchange to conceal what are effectively defaults on futures contracts.

…

Of the mysterious “exchange for physicals” mechanism by which most Comex gold futures contracts now are settled — or, really, transferred off the exchange’s books for private resolution in London — Heller writes:

“There are some logistical problems with delivering a London gold contract. First, London gold contracts are for 400-ounce bars whereas the Comex contracts are for 100-ounce bars.

“Second, like the Comex, the LBMA also has a huge shortage of physical gold to deliver against maturing contracts called for delivery. As a consequence, a higher percentage of London gold contracts is being settled for cash than in years past.

“Even worse from the standpoint of the LBMA is that the negotiated cash settlements now are for an increasing premium above the spot price than in the past. What that means is that short sellers of contracts in the London market were already suffering financially when the Comex passed along its gold contracts.

“In response to the initial news of the lack of London market gold deliveries Tuesday last week, the physical gold market developed a large bid/ask spot-price spread — as much as $100 that day. The bid/ask spot-price spreads also widened for silver, platinum, and palladium. As of Wednesday this week these spot-price spreads are much slimmer, though those for gold and silver are still larger than they were before Tuesday last week.”

Heller concludes: “The sum total of all the developments at the LBMA and Comex last week reinforces that there is a huge shortage of physical gold (and, by extension, silver) inventories available to cover all promises for delivery. As more people are willing to pay ever-higher premiums to get their hands on bullion-priced physical coins and ingots, the risk of collapse — a formal default — of the “paper” gold and silver markets is also rising.”

Heller’s analysis is headlined “Did the London/New York Markets Default On Gold Deliveries?” and it’s posted at Numismatic News here:

https://www.numismaticnews.net/article/did-the-london-new-york-markets-d…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

iii) Other physical stories:

The following is a must read..we are basically having another London Gold Pool fiasco as in London unalllocated holders are lining up to convert their unallocated gold/silver into real metal. In New York, a massive 80 tonnes of gold is standing and you can bet the farm that they too will try to convert the paper gold into real metal.

a must read..

Ronan Manly.

“Panic Stations”: What Are The LBMA And COMEX Trying To Hide?

Submitted by Ronan Manly,

Between 1962 and 1968, a cartel of central banks from the US and Europe ran a price manipulation scheme in London, aiming to keep the price of gold at $35 per ounce. They did this by constant intervention into the market, pooling their gold reserves to sell down the market. Conceived and coordinated at the Bank for International Settlements (BIS) in Switzerland by the G10 central bank governors, the dirty work of actual gold market intervention was done by the Pool’s agent, the Bank of England gold trading desk in London.

The syndicate, known as the London Gold Pool was successful until it wasn’t, with the beginning of the end in early March 1968 as the huge run on gold became a tidal wave with sterling and US dollar weakness. On 10 March 1968, a Sunday, the consortium released a statement claiming that: “the London Gold Pool reaffirm their determination to support the pool at a fixed price of $35 per ounce”. At the same time, Fed chairman William McChesney Martin even vowed that the US would defend the Pool “to the last ingot”.

The Pool then proceeded to airlift hundreds of tonnes of gold bars from the US Treasury’s Fort Knox to RAF Mildenhall, which they dumped into the London market for the rest of the week (March 11 -14). With all the Good Delivery Gold siphoned off to the Market (actually a consortium of European merchant banks), the Rothschild and the Bank of England pulled the plug, and the London Gold Pool collapsed on the evening of 14 March 1968, ushering in an era of free market gold prices.

Moral of the story, don’t believe the pronouncements of the powers that be in the London and US gold markets, especially during a crisis.

Fast forward to today, and the parallels of the Pool with the modern bullion bank cartel, the London Bullion Market Association (LBMA) and CME’s Commodity Exchange (COMEX) are uncanny. In the space of a week, the LBMA – COMEX nexus, which together control price discovery in the global gold market through their combination of fractionally backed synthetic unallocated gold, and cash settled gold futures, has issued two statements to try to placate the gold market, each one more panic stricken.

Last week, as the contango between COMEX futures and London spot gold blew up to a nearly $100 differential, and London market maker bid-ask spot spreads blew out to $100, the LBMA in a rush to deflect attention, issued a statement claiming that:

“The London gold market continues to be open for business. There has, however, been some impact on liquidity arising from price volatility in Comex 100oz futures contracts. LBMA has offered its support to CME Group to facilitate physical delivery in New York and is working closely with COMEX and other key stakeholders to ensure the efficient running of the global gold market.”

As we asked at the time last week:

- Why is the LBMA colluding with the COMEX?

- How can the London gold market be open for business if LBMA market makers are not providing liquidity in spot gold

- Why is the LBMA deflecting attention from the London market and pinning the focus on the COMEX?

- Why does the LBMA want to facilitate physical delivery in New York when its remit is the London Gold Market (loco London)?

- Who are the other key stakeholders that the LBMA and COMEX are colluding with?

Then yesterday, April 1, for a second the LBMA and CME issued an unprecedented second statement, more desperate than the first, with the pair seemingly running scared:

“LBMA AND CME GROUP COMMENT ON HEALTHY GOLD STOCKS IN NEW YORK AND LONDON

CME Group and LBMA..will continue to coordinate efforts as market circumstances evolve. Together, both CME Group and LBMA are actively taking measures to ensure the continued efficient operation of global gold markets during this unprecedented time.

LBMA reports record gold stocks

Gold stocks in London remain healthy with the latest published numbers showing record stocks of 8,326 tonnes of gold, which is equivalent to 666,045 standard 400-ounce gold bars. Visit the LBMA website for more information.

CME Group depositories open and gold stocks near record high

CME Group’s New York depositories are operating normally as they have been deemed essential businesses and deliveries are occurring as planned. As of March 30, 2020, our depositories currently hold 9.2 million ounces of gold (with 5.6 million ounces eligible), nearing a record high in terms of stock levels…”

London Gold Pool – Bank for International Settlements (BIS), Basel

Never before has the gold market seen such panic from the paper gold conductors, and all this in the presence of record physical gold demand, cleared out gold bars and coin inventories across the entire gold supply chain, closed down precious metals mints and refineries, and a price disconnect between the physical and paper gold markets.

The fact that the LBMA – COMEX tag team which front for the modern bullion bank cartel have to comment not once, but twice in a week about the health of gold inventories in London and New York means they are panicking. It’s unprecedented.

And this comes after the bullion banks placed disinformation into the media last week about needing to physical deliver gold bars from London to New York (hint – In modern times the US never imports physical gold from the UK), and were panicked into moving the goalposts with the launch of a new CME COMEX futures contract that brazenly tries to prop up COMEX GC 100 trading with the figment of fractional delivery of 400 oz gold bars that sit in London. Not to mention that on Monday this week, after CME published a COMEX vault report that had 400 oz bar categories listed for all the vaults, but with absolutely no 400 oz gold bars listed, and we mentioned it here on ZeroHedge, the CME then panicked and pulled the 400 oz version of the report, reverting back within an hour to the original version

The entire LBMA – CME Group statement about healthy gold stocks is, in the words of Francis Bacon – “of Simulation and Dissimulation” – simulation being a pretense of what is not, and dissimulation being a concealment of what is.

The LBMA reference to 8326 tonnes of gold in its network of London vaults is completed misleading.

- This figure is from 31 December 2019, which is 3 months ago

- Of this 8326 tonnes figure, 5373 tonnes (65%) represents gold held by central banks at the bank of England, and another 1895 tonnes represents gold backing Exchange Traded Funds held in London LBMA vaults, such as the vaults of HSBC and JP Morgan. Subtracting these leaves 1057 tonnes (13% of total). This 1057 is just the maximum possible London float and does not itself exclude allocated gold held by entities such as sovereign wealth funds, investment institutions, ultra wealthy and family offices. I am hearing from the London gold market sources that the real LBMA bullion bank float is less than 500 tonnes and maybe be as low as 200 – 300 tonnes.

Looking at the COMEX data and vaults, as always, COMEX has very low gold holdings. The 9.2 mn ozs number which CME refers to in the above statement (actually 9.245 mn ozs) is only 287 tonnes of gold. Of that figure (which refers to Tuesday 31 March), 114 tonnes was in the Registered, meaning there already are vault warrants issued against that.

The other 5.6 mn ozs (actually 5.85 mn ozs) is ‘Eligible gold’, but eligible just means any gold that happens to be in the approved COMEX vaults that is in the form of kilo bars or 100 oz bars. It could be anything. It is already owned by entities, which would include mints, refiners, and jewellery companies, and eligible gold may have nothing to do with COMEX or CME.

There are now over 2.19 mn ounces of Comex contracts standing for delivery in April (stops issued) – that’s 68 tonnes..and increasing.

BullionStar@BullionStarThis LBMA statement is reminiscent of the empty reassurances of the London Gold Pool in early 1968 that it had adequate gold to cap (suppress) the gold price at $35 per oz. With colossal losses, the Pool collapsed on 15 March 1968, ushering in an era of free market gold prices. https://twitter.com/lbmaexecutive/status/1245430814143381509 …

LBMA@lbmaexecutiveLBMA and @CMEGroup comment on healthy #gold stocks in New York and London. Read the latest gold market update here – https://bit.ly/2JtGrNB

From this latest April Fool’s Day statement, we can conclude that the LBMA is terrified that unallocated investors who have claims on LBMA bullion banks, will line up to take allocation of gold in London, while the CME is terrified that COMEX futures contract holders will increasingly try to take physical delivery of gold in New York (not just delivery of warrants but actually withdrawing the gold bars out of the COMEX vaults.

In March 1968 during the last days of the London Gold Pool, the cartel of central banks kept playing while the ship began to sink, brazenly saying that “the London Gold Pool reaffirm their determination to support the pool.”

This time around, with their “healthy stocks of gold in London and New York” (you can be the judge of that), “the LBMA has offered its support to CME Group”. It therefore seems that while history doesn’t repeat itself, it often rhymes.

Volume on all futures contracts after a jobs report

|

9:55 AM (1 minute ago) |

|

||

|

||||

Record low volumes in every financial, equity, metals and currency contracts today after a BLS.

Algos are reprogramming for sell or are broken and everyone that could change their models are not working

or the liquidity is so thin its like a avalanche waiting to happen

Kevin

The Comex Does Not Trade Gold

April 3, 2020Financial Markets, Gold, Market Manipulation, Precious MetalsComex, LBMA, silver

Unequivocally, gold does not trade on the Comex. The Comex trades paper gold derivatives. It is a futures and options exchange on which a small amount of 100 oz. gold bars change ownership each contract month. The transfer of title is facilitated by the creation of an electronic record called a “warrant.” But even these “warrants” which assign title to specific bars are derivatives. Presumably gold is “delivered” to the parties who stand for delivery (the “stopper”). But that “delivery” most commonly is the electronic transfer of a warrant from the entity short a paper gold contract to the entity who is long the same.

Because the CME and the CFTC do not place a limitation on the number of paper gold contracts – 100 ozs per contract – in relation to the amount of gold reported in Comex vaults – the price discovery function has been largely removed. As an example, as of Wednesday there were 489,955 open contracts representing 48.9mm ozs of gold, or 1531 tons (roughly 50% of the amount of gold annually produced globally). Lucky for the Comex, less than 1% of the open interest in any given month stands for delivery.

At the beginning of the contract “roll” period, there was well in excess of 200,000 April contracts open representing over 20 million ozs of gold. If 50% of these longs decided to stand for delivery because the Comex appears to be only entity with gold deliverable in quantities, not only would the gold determined to be free and clear of encumbrances and conforming to Comex delivery specs – i.e. “registered” gold – be wiped out but the entire Comex gold stock would be wiped out. But there’s just one problem. The “eligible” gold – gold not registered – belongs to someone else who does not want that gold loaned, leased or hypothecated.

If the Comex regulated the open interest such that the amount of open interest was tied to the amount of gold in Comex vaults – since theoretically eligible gold can be registered – the resultant introduction of price discovery would force the price of gold much higher – higher to a level at which the price functions to balance supply and demand – not paper supply/demand in the form of printed contracts – but physical supply/demand based on the amount of gold sitting in Comex vaults as reported by the Comex vault operators. Given that apparently there’s not much gold in London and a massive imbalance between paper gold and physical gold on the Comex, it would likely require a significantly higher gold price to balance the physical gold supply and demand.

Currently a run on Comex gold appears to be starting, notwithstanding the Comex’s attempt to kick this can down the road with the use of Exchange For Physicals (EFPs) and Privately Negotiated Transactions (PNTs). But EFPs/PNTs are nothing more than second order derivatives created to sidestep the delivery of Comex bars. In fact the EFPs were used largely to transfer the settlement liability of a Comex contract to the LBMA.

Physical gold thus in fact does not trade on the Comex. Rather, the Comex is nothing more than a derivatives exchange with a small amount of physical gold relative to the notional value of the derivatives created.

As with the rest of the paper Ponzi schemes created by the banks and Central Banks, the Comex’s derivatives house of cards has always been fated to collapse. Based on all indications plus the signs of desperation emanating from the Comex and the LBMA, the collapse has begun. This will ultimately lead to much higher prices for gold and silver. Note: this situation started to unfold well before the virus crisis.

***

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

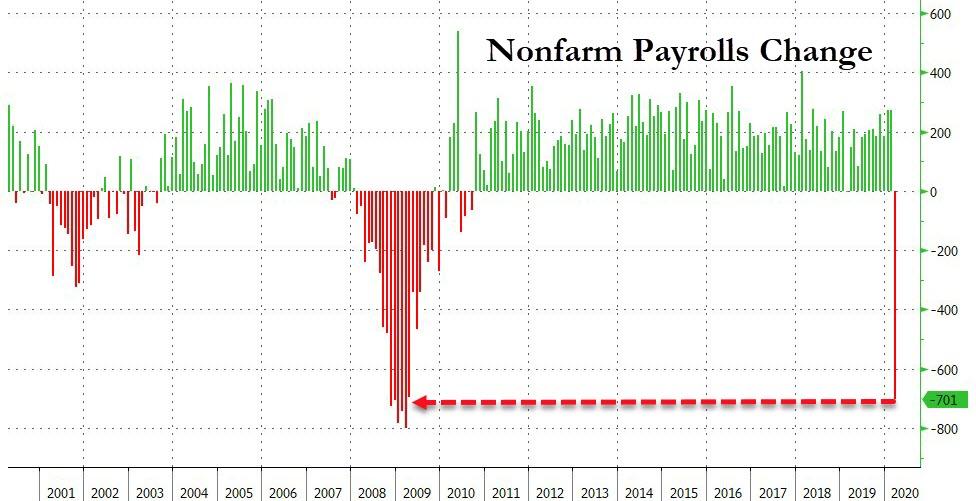

Futures Slide As European Economy Craters, Dollar Surges: All Eyes On Payrolls

S&P futures have erased much of yesterday’s late day ramp alongside European stocks with investors awaiting data on non-farm payrolls and business activity to assess the extent of the economic hit from the coronavirus pandemic which has now infected more than a million people around the world. Bond yields dropped and the dollar surged as attempts to ease liquidity strains appear to be failing again as traders hunkered down ahead of March payrolls data that are expected to decline for the first time since 2010. And while the NFP will be bad, it is already old news in light of the last two initial jobless claims which showed 10 million layoffs in just the past two weeks.

The drop erased some of Wall Street’s Thursday 2% rally when oil soared on hints of a Saudi-Russia deal, but doubts returned on whether the rebound would last as demand tapers off due to the health crisis. Walt Disney said on Thursday it would furlough some U.S. employees this month, while sources said luxury retailer Neiman Marcus was stepping up preparations to seek bankruptcy protection.

Putting the past month in context, one month ago, on March 3, there were 92,000 coronavirus cases primarily in China. Today there are over one million cases worldwide, with the US and EU account for the biggest portions. In the US, over 75% of individuals and 90% of GDP is under a stay at home order, including 38 state-wide orders.

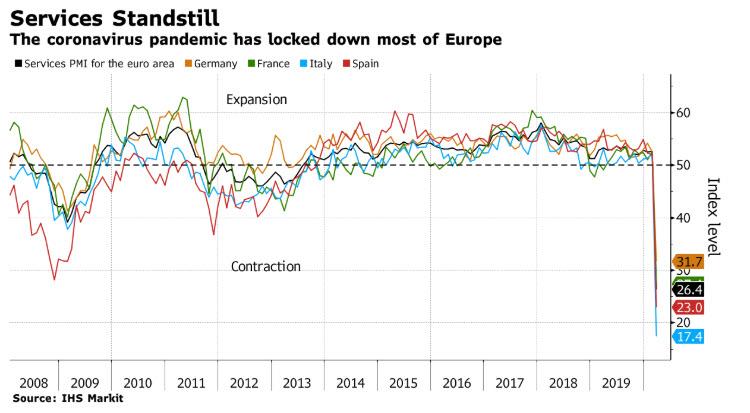

The Stoxx 600 index slumped following service PMI reports showing an unprecedented slump in the euro-area economy last month with insurers and energy shares pacing declines. Markit said its monthly measures of services and manufacturing points to an annualized economic contraction of about 10%. With new business, confidence and employment all down, there is “worse inevitably to come in the near future,” it said.

Markit’s composite Purchasing Managers Index fell to 29.7 in March, it said Friday, even lower than initially estimated. That’s down from 51.6 in February and far below the 50 line that divides growth from contraction. Almost every country in the survey had a record-low reading.

“No countries are escaping the severe downturn,” said Chris Williamson, chief business economist at IHS Markit. “But the especially steep decline in Italy’s service sector PMI to just 17.4 likely gives a taste of things to come for other countries as closures and lockdowns become more prevalent and more strictly enforced in coming months.”

The reports capped a gloomy week for Europe’s economy, where figures showed manufacturing in a deep recession, huge jumps in jobless claims, and thousands of companies in Germany cutting hours for workers.

The measure for services, which includes hotels and restaurants, was at 26.4, with Italy dropping to just 17.4.

Earlier in the session, Asian stocks fell, led by consumer discretionary and finance, after falling in the last session. Markets in the region were mixed, with Singapore’s Straits Times Index and Australia’s S&P/ASX 200 falling, and Jakarta Composite and Thailand’s SET rising. The Topix declined 0.4%, with Insource and Helios Techno falling the most. The Shanghai Composite Index retreated 0.6%, with Qibu and Chimin Health Management posting the biggest slides.

Of note, China announced more stimulus when the PBOC unveiled another targeted (and expected) cut in the reserve requirement ratio (RRR) of 100bp for small-to-medium banks, unleashing RMB 400bn liquidity in total. It will also lower the interest paid on excess reserves to 0.35% from 0.72%, the first cut since November 2008. The announcement today followed Premier Li’s comments at the State Council meeting on March 31, in line with expectations

While economic data is now of secondary importance as the US descends into a (hopefully brief) depression, traders will be eyeing today’s jobs report which will end a historic 113 straight months of employment growth as stringent measures to control the coronavirus pandemic shuttered businesses and factories, confirming a recession is underway. However, as previewed earlier, today’s Payrolls report will not fully reflect the full extent of the layoffs as it covers data until March 12.

With lockdowns for many economies around the world expected to go on for longer, data are showing the severity of the impact. Nearly 10 million people in the U.S. have lost their jobs in the past two weeks, while the virus continues to pressure corporate balance sheets. American Airlines will slash international flying as far out as the end of August as the pandemic batters travel demand through the normally busy summer season.

After that, at 10 a.m. ET we will get the ISM’s non-manufacturing activity index which likely dropped to 44 in March from 57.3 in February. A reading below 50 indicates contraction in the services sector, which accounts for more than two-thirds of U.S. economic activity.

“We are not going to have the real recovery in the market until what we think is the peak in the amount of infections and deaths,” Stephen Dover, head of equities at Franklin Templeton, said on Bloomberg TV. “We are going to continue to have very wide volatility until we can get over this uncertainty.”

In rates, ten-year Treasury yields are steady around 0.6%, while German equivalents are little changed at minus 0.44%

In FX, the dollar surged against all Group-of-10 peers, heading for a weekly advance, on rising demand for the world’s reserve currency after global coronavirus cases surged past 1 million. The Bloomberg Dollar Spot Index rose 0.5% for the day, bringing its weekly advance to 2.2%. Antipodean currencies led losses in the basket, while the pound slid the most in two weeks. The yen weakened alongside the euro, pound and Swiss franc.

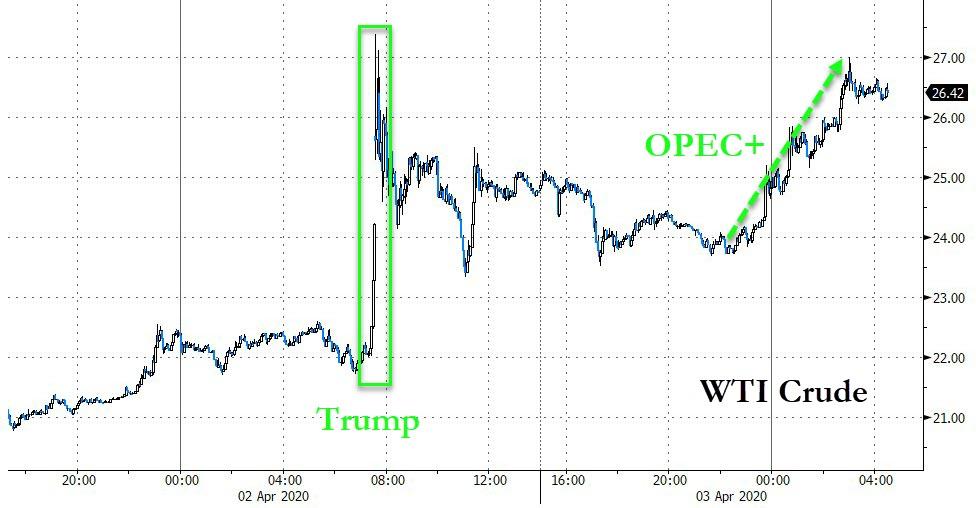

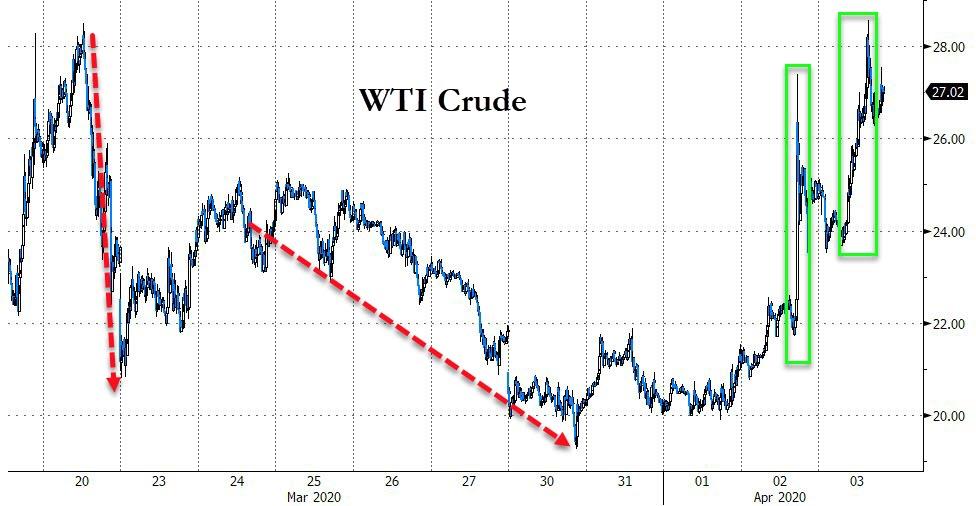

In commodities, crude oil fluctuated following the biggest jump on record a day earlier, but jumped over 10% on news the OPEC+ coalition will hold a virtual meeting on Monday.

Expected data include non-farm payrolls, unemployment, and PMIs. Constellation Brands is reporting earnings

Market Snapshot

- S&P 500 futures down 1.3% to 2,484.50

- STOXX Europe 600 down 0.6% to 310.07

- MXAP down 0.5% to 132.75

- MXAPJ down 0.5% to 429.35

- Nikkei up 0.01% to 17,820.19

- Topix down 0.4% to 1,325.13

- Hang Seng Index down 0.2% to 23,236.11

- Shanghai Composite down 0.6% to 2,763.99

- Sensex down 1.8% to 27,753.84

- Australia S&P/ASX 200 down 1.7% to 5,067.48

- Kospi up 0.03% to 1,725.44

- German 10Y yield fell 0.7 bps to -0.44%

- Euro down 0.5% to $1.0805

- Italian 10Y yield fell 4.2 bps to 1.296%

- Spanish 10Y yield unchanged at 0.709%

- Brent futures up 5.9% to $31.71/bbl

- Gold spot down 0.2% to $1,611.34

- U.S. Dollar Index up 0.5% to 100.68

Top Overnight News

- The euro-area economy is in a slump of unprecedented scale, which may worsen further as lockdowns to contain the coronavirus are extended. IHS Markit said its monthly measure of services and manufacturing points to an annualized economic contraction of about 10%

- Oil advanced above $32 a barrel in London as OPEC+ scheduled an urgent meeting next week to try and stem the crude market’s rout, with an output cut of 10% of global production being discussed

- U.K. services industries shrank at the fastest pace in at least two decades as the destruction of the coronavirus took hold. IHS Markit’s Purchasing Managers Index for the sector fell to 34.5 last month, the steepest downturn since the survey began in 1996

- The European Central Bank’s 750 billion euro ($811 billion) emergency bond-buying program is the “central pillar” of its response to the coronavirus crisis, but Europe also needs continent-wide fiscal action, Finnish governor Olli Rehn said on Friday

- The People’s Bank of China needs to make a more complete evaluation before taking a decision to change the rate paid on bank deposits, a senior official said in Beijing Friday

- The cost of the coronavirus pandemic could be as high as $4.1 trillion, or almost 5% of global gross domestic product, depending on the disease’s spread through Europe, the U.S. and other major economies, the Asian Development Bank said