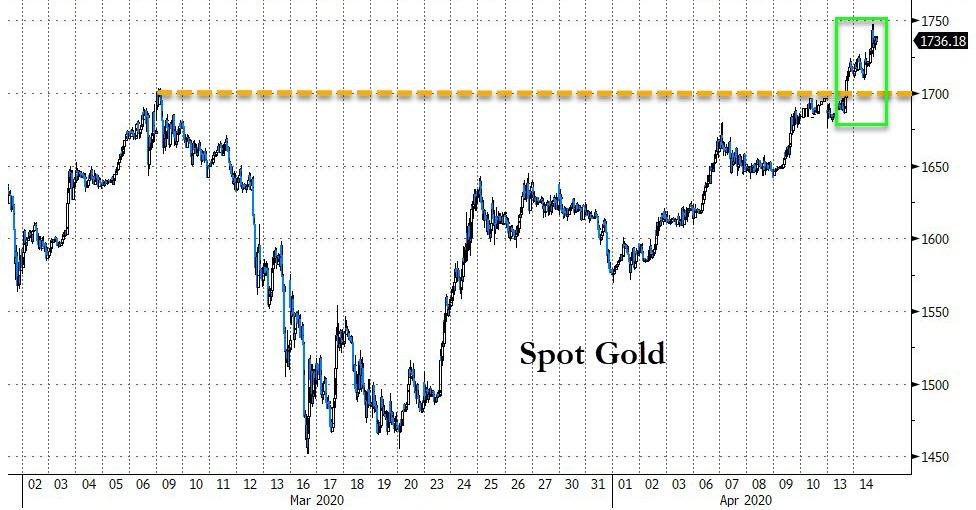

GOLD:$1737.00 UP $23.55 The quote is London spot price

Silver:$15.80//UP $.51 London spot price

Closing access prices: London spot

i)Gold : $1728.00 LONDON SPOT 4:30 pm

ii)SILVER: $15.75//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

APRIL comex gold price CLOSE 1.30 PM: $1750.30

MAY COMEX GOLD: 1756.00 1:30 PM

JUNE GOLD: $1769.70 CLOSE 1.30 PM// SPREAD SPOT/FUTURE JUNE: $32.70

CLOSING SILVER FUTURE MONTH

SILVER APRIL COMEX CLOSE: 16.07/

SILVER MAY COMEX CLOSE; $1613…1:30 PM.//SPREAD SPOT/FUTURE MAY: 33 CENTS PER OZ

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2600. usa per oz

and silver; $31.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 140/738

ISSUED: 333

DLV615-T CME CLEARING

BUSINESS DATE: 04/13/2020 DAILY DELIVERY NOTICES RUN DATE: 04/13/2020

PRODUCT GROUP: METALS RUN TIME: 20:22:08

EXCHANGE: COMEX

CONTRACT: APRIL 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,744.800000000 USD

INTENT DATE: 04/13/2020 DELIVERY DATE: 04/15/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

132 C SG AMERICAS 2 21

657 C MORGAN STANLEY 11

657 H MORGAN STANLEY 541

661 C JP MORGAN 333 140

686 C INTL FCSTONE 9 9

690 C ABN AMRO 327 11

737 C ADVANTAGE 20 10

800 C MAREX SPEC 12 3

878 C PHILLIP CAPITAL 1

905 C ADM 24 2

____________________________________________________________________________________________

TOTAL: 738 738

MONTH TO DATE: 28,858

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 738 NOTICE(S) FOR 73,800 OZ (2.295 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 28,858 NOTICES FOR 2,885,800 OZ (89.76 TONNES)

SILVER

FOR APRIL

0 NOTICE(S) FILED TODAY FOR NIL OZ/

total number of notices filed so far this month: 801 for 4,005,000 oz

BITCOIN MORNING QUOTE $6825 DOWN 11

BITCOIN AFTERNOON QUOTE.: $6893 UP $64

GLD AND SLV INVENTORIES:

WITH GOLD UP $23.55: AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

WE HAD ANOTHER STRONG DEPOSIT OF 15.51 TONNES (PAPER TONNES/NOT REAL STUFF)

GLD: 1009.70 TONNES OF GOLD//

WITH SILVER UP 51 CENTS TODAY: AND WITH NO SILVER AROUND

A HUGE DEPOSIT OF SILVER WAS ADDED TO OUR SLV INVENTORY TONIGHT: 6.155 MILLION OZ

RESTING SLV INVENTORY TONIGHT:

SLV: 408.536 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A SMALL SIZED 389 CONTRACTS FROM 139,780 UP TO 140,169 AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE SMALL SIZED GAIN IN OI OCCURRED WITH OUR STRONG 21 CENT FALL IN SILVER PRICING AT THE COMEX. WE HAD ZERO LONG LIQUIDATION. IT SEEMS THAT THE GAIN IN COMEX OI IS DUE TO BANKER SHORT COVERING PLUS A CONSIDERABLE EXCHANGE FOR PHYSICAL ISSUANCE ALONG WITH A STRONG GAIN IN SILVER OZ STANDING. WE HAD A STRONG NET GAIN IN OUR TWO EXCHANGES OF 1222 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A STRONG AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: MARCH: 00 AND MAY: 791 AND JULY: 0 ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 791 CONTRACTS. WITH THE TRANSFER OF 791 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 791 EFP CONTRACTS TRANSLATES INTO 3.955 MILLION OZ ACCOMPANYING:

1.THE 21 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.125 MILLION OZ INITIALLY STANDING FOR APRIL

MONDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL 21 CENTS).. AND, OUR OFFICIAL SECTOR/BANKERS WERE TOTALLY UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS, AS WE DID HAVE A STRONG NET GAIN OF 1180 CONTRACTS OR 5.900 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER JUDGING BY THE HUGE GAIN IN PRICE.

OUR SPREADING OPERATION HAS NOW SWITCHED INTO SILVER…..

SPREADING OPERATION FOR OUR NEWCOMERS:

WE HAVE NOW COMMENCED IN SILVER THE ILLEGAL SPREADING OPERATION \ FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW STOPPED IN GOLD AS THEY NOW BEGIN TO MORPH INTO SILVER AS WE HEAD TOWARDS THE NEW FRONT MONTH WILL BE MAY.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF APRIL. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

9564 CONTRACTS (FOR 8 TRADING DAYS TOTAL 9564 CONTRACTS) OR 47.820 MILLION OZ: (AVERAGE PER DAY: 1196 CONTRACTS OR 5.977 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF APRIL: 47.820 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 6.83% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 941.30 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP SO FAR 47.820 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 389, DESPITE THE CONSIDERABLE $0.21 LOSS IN SILVER PRICING AT THE COMEX /MONDAY… THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 791 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A STRONG SIZED OI CONTRACTS ON THE TWO EXCHANGES: 1180 CONTRACTS (DESPITE OUR 21 CENT LOSS IN PRICE)

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 791 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 389 OI COMEX CONTRACTS.AND ALL OF THIS DEMAND HAPPENED WITH A 21 CENT LOSS IN PRICE OF SILVER/ AND A CLOSING PRICE OF $15.29 // MONDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY AS WELL AS A GOOD INCREASE IN QUEUE JUMPING//AMOUNT STANDING!!

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.7005 BILLION OZ TO BE EXACT or 100.2% of annual global silver production (ex Russia & ex China).

FOR THE NEW MAR DELIVERY MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.125 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2,910 CONTRACTS TO 491,828 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE GAIN OF COMEX OI OCCURRED WITH OUR STRONG COMEX GAIN IN PRICE OF $27.65 /// COMEX GOLD TRADING// MONDAY// WE HAD CONSIDERABLE BANKER SHORT COVERING ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A GOOD EX. FOR PHYSICAL ISSUANCE AND THIS WAS COUPLED WITH OUR STRONG GAIN IN THE PAPER PRICE OF GOLD.

WE HAD NO ISSUANCE OF OUR NEW 4 GC CONTRACT

WE GAINED A GOOD 5871 CONTRACTS (18.26 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2971 CONTRACTS:

CONTRACTS, FEB> 0 CONTRACTS; MARCH 00 APRIL: 0. MAY: 0, AND JUNE 2971.; DEC 0 AND ALL OTHER MONTHS ZERO//TOTAL: 2971. The NEW COMEX OI for the gold complex rests at 491,828. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5,871 CONTRACTS: 2,910 CONTRACTS INCREASED AT THE COMEX AND 2961 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 5871 CONTRACTS OR 18.26 TONNES. MONDAY, WE HAD A HUGE GAIN OF $27.65 IN GOLD TRADING……

AND WITH THAT HUGE GAIN IN PRICE, WE HAD A GOOD SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 18.26 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (ROSE $27.65). AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WERE UNSUCCESSFUL (SEE BELOW).

4 GC ISSUANCE: ZERO

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A FAIR SIZED INCREASE IN EXCHANGE FOR PHYSICALS (2971) ACCOMPANYING THE FAIR GAIN IN COMEX OI (2,961 OI): TOTAL GAIN IN THE TWO EXCHANGES: 5,871 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)A MONSTROUS INCREASE IN STANDING AT THE GOLD COMEX FOR THE FRONT APRIL MONTH, 3) ZERO LONG LIQUIDATION AND …ALL OF THIS WAS COUPLED WITH THAT HUGE GAIN IN GOLD PRICE TRADING//MONDAY

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 44,802 CONTRACTS OR 4,480,200 oz OR 139.35 TONNES (8 TRADING DAYS AND THUS AVERAGING: 5600 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES: 139.35 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 139.35/3550 x 100% TONNES =3.92% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 2462.15 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 139.35 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A SMALL SIZED 389 CONTRACTS FROM 139,780 UP TO 140,169 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

ALL OF THE GAIN IN COMEX OI WAS DUE TO 1) HUGE BANKER SHORT COVERING , 2) THE ISSUANCE OF A GOOD SIZED NUMBER OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A ZERO INCREASE IN SILVER OZ STANDING AT THE COMEX FOR APRIL AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 791 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR FEB. 0; FOR MAR 0: AND MAY: 791; JULY: 00 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 791 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE SMALL COMEX OI GAIN OF 389 CONTRACTS TO THE 791 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 1180 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 5.900 MILLION OZ!!! AND WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ// SEPT: 43.030 MILLION OZ///OCT: 7.32 MILLION OZ//NOV 2.63 MILLION OZ//DEC: 20.970 MILLION OZ//JAN: 5.075 MILLION OZ//FEB: 1.480 MILLION OZ//MAR: 23.005 MILLION OZ//APRIL 4.125 MILLION OZ//

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 21 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// MONDAY. WE ALSO HAD A GOOD SIZED 791 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 44.24 POINTS OR 1.59% //Hang Sang CLOSED UP 135.07 POINTS OR 0.56% /The Nikkei closed UP 595.41 POINTS OR 3.13%//Australia’s all ordinaires CLOSED UP 1.89%

/Chinese yuan (ONSHORE) closed DOWN at 7.0573 /Oil DOWN TO 21.92 dollars per barrel for WTI and 31.50 for Brent. Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0573 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0587 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

total gold withdrawals; 257.21 oz

We had 3 kilo transactions

We had zero 4 KC bar transaction

ADJUSTMENTS: 2

customer up to the dealer

HSBC: 64,052.514 oz was adjusted up to the dealer from the customer account

Brinks: 5594.274 oz adjusted up to the dealer from the customer account

The front month of APRIL saw its open interest register 1185 contracts for a LOSS of ONLY 52 contacts. We had 454 notices filed yesterday so we GAINED A VERY STRONG 402 contracts or AN ADDITIONAL 40,200 oz will stand at the comex as these guys refused to morph into London based forwards and they also negated a fiat bonus

May saw its ANOTHER GAIN of 915 contracts to stand at 4278.

We had 738 notices filed today for 73,800 oz

To calculate the INITIAL total number of gold ounces standing for the APRIL /2020. contract month, we take the total number of notices filed so far for the month (28,858) x 100 oz , to which we add the difference between the open interest for the front month of APRIL. (1185 CONTRACTS ) minus the number of notices served upon today (738 x 100 oz per contract) equals 2,926,000 OZ OR 91.01 TONNES) the number of ounces standing in this active month of APRIL

thus the INITIAL standings for gold for the APRIL/2020 contract month:

No of notices served (28,858)x 100 oz) 1185 OI for the front month minus the number of notices served upon today (738 x 100 oz which equals 2,926,000 oz standing OR 91.01 TONNES in this active delivery month which is a great amount for gold standing for a APRIL. delivery month.

THIS GREATLY SURPASSES THE PREVIOUS RECORD OF 42. TONES OF GOLD STANDING IN ANY MONTH

We gained 402 contracts OR an additional 40200 OZ WILL STAND AT THE COMEX as these guys decided it best to look for metal on the this side of the pond, first before travelling to London..

NEW PLEDGED GOLD: BRINKS

3027.500 OZ REMOVED TO THE PLEDGED ACCOUNT JAN 10.2020/Brinks

176,211.457 oz NOW PLEDGED JAN 21.2020/HSBC 5.4807 TONNES

341,434.443 oz PLEDGED MARCH 2020 JPMORGAN: 10.62 TONNES

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234

TOTAL PLEDGED GOLD NOW IN EFFECT: 560,194.208 OZ OR 17.424 TONNES

total dealer deposits: 0 oz

total dealer withdrawals: 0 oz

i)we had 0 deposits into the customer account

into JPMorgan: 0

ii)into everybody else; 0

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.819 million oz of total silver inventory or 50.04% of all official comex silver. (160.819 million/321.170 million

total customer deposits today: 607,477.800 oz

we had 3 withdrawals:

total withdrawals; 156,224.283 oz

We had 0 adjustments: and all from the dealer to the customer:

total dealer silver: 82.147 million

total dealer + customer silver: 319.769 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The total number of notices filed today for the APRIL 2020. contract month is represented by 0 contract(s) FOR NIL oz

To calculate the number of silver ounces that will stand for delivery in APRIL we take the total number of notices filed for the month so far at 801 x 5,000 oz = 4,005,000 oz to which we add the difference between the open interest for the front month of APRIL.(24) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL/2019 contract month: 801 (notices served so far) x 5000 oz + OI for front month of APRIL (24)- number of notices served upon today (0) x 5000 oz of silver standing for the APRIL contract month.equals 4,125,000 oz.

WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ OF SILVER WILL STAND AT THE COMEX.

TODAY’S ESTIMATED SILVER VOLUME: 81,251 CONTRACTS //

FOR YESTERDAY: 68,629 CONTRACTS..,CONFIRMED VOLUME

YESTERDAY’S CONFIRMED VOLUME OF 68,629 CONTRACTS EQUATES to 343 million OZ 49.0% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -0.76% ((APRIL 14/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.40% to NAV: (APRIL 14/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 0.76%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.91 TRADING 15.85///DISCOUNT 0.35

END

And now the Gold inventory at the GLD/

APRIL 14/WITH GOLD UP $23.55 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 15.51 TONNES WAS ADDED TO THE GLD INVENTORY/INVENTORY RESTS AT 1009.70 TONNES//THIS IS THE 10TH STRAIGHT STRONG DEPOSIT//THIS IS A FRAUDULENT VEHICLE..THEY HAVE NO PHYSICAL GOLD IN THE TRUST..

APRIL 13//WITH GOLD UP $27.65 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 5.36 TONNES WAS ADDED TO THE GLD//INVENTORY RESTS AT 994.19 TONNES

APRIL 9 WITH GOLD UP $37.30 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 2.92 TONNES WAS ADDED TO THE GLD//GOLD INVENTORY RESTS TONIGHT AT..988.63 TONNES

APRIL 8/WITH GOLD DOWN $.60//ANOTHER HUGE CHANGE IN GOLD INVENTORY/;; A STRONG 1.45 TONNES WAS ADDED TO THE GLD/GOLD INVENTORY RESTS AT 985.71 TONNES

APRIL 7/WITH GOLD UP $.30: ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.27 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 984.26 TONNES

APRIL 6//WITH GOLD UP $32.00//ANOTHER STRONG DEPOSIT INTO THE GLD; A HUGE 7.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT : 978.99 TONNES

APRIL 3//WITH GOLD UP $7.80 TODAY//ANOTHER STRONG DEPOSIT OF 3.22 TONNES INTO THE GLD/INVENTORY RESTS AT 971.97 TONNES

APRIL 2//WITH GOLD UP $31.80 TODAY: ANOTHER STRONG DEPOSIT OF 1.75 TONNES INTO THE GLD//INVENTORY RESTS AT 968.75 TONNES

APRIL 1/WITH GOLD DOWN $7.70 TODAY: ANOTHER CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.62 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 967.00 TONNES

MARCH 31//WITH GOLD DOWN $32.70//A MONSTROUS PAPER DEPOSIT OF 10.84 TONNES INTO THE GLD//INVENTORY RESTS AT 964.38 TONNES

MARCH 30/WITH GOLD DOWN $6.10 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 953.54 TONNES

MARCH 27.WITH GOLD DOWN $16.40: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A HUGE DEPOSIT OF 4.39 TONES INTO THE GLD/INVENTORY RESTS AT 953.54 TONES

MARCH 26//WITH GOLD UP $24.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 13.17 TONNES INTO THE GLD/INVENTORY RESTS AT 949.15 TONNES

MARCH 25/WITH GOLD DOWN $11.40 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.99 TONES INTO THE GLD INVENTORY////INVENTORY RESTS AT 935.98 TONNES

MARCH 24//WITH GOLD UP $67.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 15.80 TONNES OF GOLD INTO GLD////INVENTORY RESTS AT 923.99 TONNES..THIS PROVES THAT THE GLD IS A FRAUD AS LONDON SUSPENDED DELIVERY AS WELL AS ALL REFINERS. THEY HAD NO WAY OF GETTING ANY PHYSICAL OZ INTO ITS INVENTORY//

MARCH 23//WITH GOLD UP $76.00 TODAY: A HUGE PAPER WITHDRAWAL OF 21.50 TONNES FROM THE GLD////INVENTORY RESTS AT 908.19 TONNES

MARCH 20//WITH GOLD UP $5.50//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 7.46 TONNES FROM THE GLD////INVENTORY RESTS AT 922.23 TONNES

MARCH 19/WITH GOLD DOWN 90 CENTS: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 929.84 TONNES

MARCH 18/WITH GOLD DOWN $48.00: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 929.84 TONNES

MARCH 17/WITH GOLD UP $37.60: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM GLD INVENTORY//INVENTORY RESTS AT 929.84 TONNES

MARCH 16/WITH GOLD DOWN $30.00/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 12.59 TONNES/INVENTORY RESTS AT 931.59 TONNES

MARCH 13//WITH GOLD DOWN $73.60: A HUGE WITHDRAWAL OF 9.02 TONNES OF PAPER GOLD FROM THE GLD//

INVENTORY RESTS AT 944.18 TONNES

MARCH 12/WITH GOLD DOWN $55.05 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/953.26 TONNES

MAR 11/WITH GOLD DOWN $14.95?/A HUGE WITHDRAWAL OF 10.53 TONNES//INVENTORY RESTS AT 953.26 TONNES

MARCH 10/WITH GOLD DOWN $14.25//A HUGE 8.00 TONNES OF PAPER GOLD DEPOSIT INTO THE GLD//INVENTORY RESTS AT 963.79

MARCH 9//WITH GOLD UP $1.50 : NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 955.60 TONNES

March 6/WITH GOLD UP $6.25 A MASSIVE 21.37 PAPER TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 955.60 TONNES

MARCH 5/WITH GOLD UP $25.40//NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS TONIGHT AT 934.23 TONNES

MARCH 4//WITH GOLD DOWN 1 DOLLAR: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.23 TONNES//

MARCH 3//WITH GOLD UP 48.55 TODAY; NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.23 TONNES

MARCH 2//WITH GOLD UP $27.00// no change in gold inventory at the gld//inventory remains at 934.23 tonnes

FEB 28/WITH GOLD DOWN $73.00 WE LOST NO GOLD FROM THE GLD/INVENTORY REMAINS 934.23 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

APRIL 14/2020/ 1009.70 tonnes*

IN LAST 798 TRADING DAYS: +63.36 NET TONNES HAVE BEEN REMOVED FROM THE GLD

LAST 698 TRADING DAYS;+238.34 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

APRIL 14./WITH SILVER UP 51 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A MASSIVE PAPER DEPOSIT OF XXX MILLION OZ//INVENTORY RESTS AT 408.536 MILLION OZ//

APRIL 13//WITH SILVER DOWN 29 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 6.155 MILLION OZ////INVENTORY RESTS AT 408.536 MILLION OZ//

APRIL 9/WITH SILVER UP 60 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUGE DEPOSIT OF 1.84 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 402.381 MILLION OZ.

APRIL 8//WITH SILVER DOWN 21 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 401.541 MILLION OZ///

APRIL 7/WITH SILVER UP 26 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.766 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 395.826 MILLION OZ

APRIL 6/WITH SILVER UP 50 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 395.826 MILLION OZ.

APRIL 3//WITH SILVER DOWN 15 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 746,000 OZ INTO THE SLV//INVENTORY RESTS AT 395.826 MILLION OZ

APRIL 2/WITH SILVER UP 65 CENTS; A SMALL CHANGE TODAY..A WITHDRAWAL OF .335 MILLION OZ TO PAY FOR FEES//INVENTORY RESTS AT 394.826 MILLION OZ/

APRIL 1/WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 395.181 MILLION OZ//

MARCH 31/WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 1.679 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 375.181 MILLION OZ//

MARCH 30/WITH SILVER DOWN 44 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 393.502 MILLION OZ.

MARCH 27/WITH SILVER DOWN 5 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTROUS PAPER DEPOSIT OF 8.115 MILLION OZ INTO THE SLV../INVENTORY RESTS AT 393.502 MILLION OZ//

MARCH 26/WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 385.387 MILLION OZ///

MARCH 25/WITH SILVER UP 44 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSITS OF 7.369 MILLION OZ AND 2.239 MILLION OZ OF PAPER SILVER INTO THE SLV////INVENTORY RESTS AT 385.387 MILLION OZ//

MARCH 24//WITH SILVER UP 100 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 375.779 MILLION OZ///

MARCH 23//WITH SILVER UP 70 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.332 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 375.779 MILLION OZ

MARCH 20//WITH SILVER UP 39 CENTS TODAY: 2 HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A PAPER WITHDRAWAL OF 1.026 MILLION OZ FROM THE SLV AND THEN A PAPER ADDITION OF 3.638 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 373.447 MILLION OZ//

MARCH 19/WITH SILVER UP 38 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: ANOTHER 5.597 MILLION OZ OF SILVER VAPOUR ADDED TO THE SLV INVENTORY//INVENTORY RESTS AT 370.835 MILLION OZ/

MARCH 18//WITH SILVER DOWN 75 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTROUS 12.035 MILLION PAPER OZ ADDED INTO INVENTORY//INVENTORY RESTS AT 365.238 MILLION OZ//

MARCH 17/WITH SILVER DOWN 20 CENTS TODAY; A BIG CHANGES IN SILVER INVENTORY AT THE SLV; A WITHDRAWAL OF 3.735 MILLION OZ FROM THE SLV INVENTORY: INVENTORY RESTS AT 353.203 MILLION OZ///

MARCH 16/WITH SILVER DOWN 177 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESETS AT 356.938 MILLION OZ//

MARCH 13//WITH SILVER DOWN 155 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.893 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 356.938 MILLION OZ;

MARCH 12/WITH SILVER DOWN 77 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.119 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 359.828 MILLION OZ

MARCH 11/SILVER DOWN 16 CENTS: A SMALL WITHDRAWAL OF .467 MILLION OZ AT THE SLV/INVENTORY RESTS AT 360.947 MILLION OZ//

MARCH 10/WITH SILVER DOWN 10 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 361.414 MILLION OZ//

MARCH 9/NO CHANGE IN INVENTORY LEVELS: SLV INVENTORY RESTS AT 361.414 MILLION OZ//

MARCH 6//WITH SILVER DOWN 10 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 361.414 MILLION OZ

MARCH 5//WITH SILVER UP 15 CENTS TODAY; A SMALL WITHDRAWAL DUE TO FEES ETC//INVENTORY RESTS TONIGHT AT 361.414 MILLION OZ..

MARCH 4/SILVER SILVER UP 3 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 361.880 MILLION OZ//

MARCH 3/WITH SILVER UP 44 CENTS//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: A LOSS OF 5.75 MILLION OZ FROM THE SLV../INVENTORY RESTS AT 361.880 MILLION OZ

MARCH 2//WITH SILVER UP 18 CENTS//NO CHANGE IN SILVER INVENTORY AT THE SLV..INVENTORY RESTS AT 367.632 MILLION OZ//

FEB 28/ WITH SILVER DOWN 18 CENTS: a loss of 1.867 million oz//inventory rests at 367.632 million oz

APRIL 14.2020:

SLV INVENTORY RESTS TONIGHT AT

408.536 MILLION OZ.

END

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 6.03/ and libor 6 month duration 1.23

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – 4.80

no gold to be found..only gold vapour!

XXXXXXXX

12 Month MM GOFO

+ 2.83%

LIBOR FOR 12 MONTH DURATION: 1.05

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -1.78

gold non existent

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Gold Surges To New Record Highs in Euros at €1,581/oz and $1,726/oz in Dollars

◆ Gold prices surged to new all time record highs in euros and other digital fiat currencies today due to concerns about the outlook for risk assets and currencies in an era of unprecedented economic and monetary risk.

◆ Gold prices rose to a more than seven-year high in dollars today at $1,726/oz (see chart below) as mounting fears of a steeper global economic downturn due to draconian government lock downs increase and highlight gold bullion’s safe haven qualities.

◆ Gold surged to €1,581/oz (see chart above) as the single currency came under selling pressure as concerns deepen about Italy and other periphery nation’s banks and economies and due to increased risks to the euro and the monetary union.

◆ Gold surged to £1,375 per ounce and is testing gold’s record high in sterling which is £1,381.75/oz as the beleaguered pound also came under selling pressure due to concerns about the UK economy.

◆ Strong safe haven demand for gold continues due to concerns about the outlook for the UK, EU and global economy, the unprecedented monetary response of the ECB, the BoE and the other central banks and growing concerns that digital currencies will be devalued in the coming months and years.

◆ Gold reached year highs in dollars and gold prices are up over 14% in euro terms so far in 2020, building on the 22.7% gains in euros seen in 2019 (see table below).

◆ Strong safe haven demand continues due to concerns about the outlook for the UK, EU and global economy, the unprecedented monetary response of the ECB, the BoE and the other central banks and growing concerns that digital currencies will be devalued in the coming months and years.

◆ Gold is now the top performing asset in 2020 year to date, having risen 16% in dollar terms, 19% in euro terms, 21.7% in pounds and by more in other fiat currencies as the virus tips debt laden economies into financial and economic crises

NEWS and COMMENTARY

Gold Rises as a Safe Haven in Troubled Economic Times

Gold climbs to over 7-year high on coronavirus-led economic worries

Gold climbs to over 7-year high on coronavirus-led economic worries

Six U.S. states to coordinate gradual reopening after coronavirus shutdown

Risk averse investors and gold ‘bugs’ vindicated by coronavirus rally

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

09-Apr-20 1662.50 1680.65, 1339.48 1348.22 & 1529.00 1538.13

08-Apr-20 1649.05 1647.80, 1328.27 1330.27 & 1517.00 1513.14

07-Apr-20 1652.20 1649.25, 1344.23 1333.75 & 1519.53 1511.21

06-Apr-20 1636.60 1648.30, 1330.72 1341.06 & 1515.49 1526.66

03-Apr-20 1609.75 1613.10, 1310.66 1315.97 & 1490.47 1495.34

02-Apr-20 1588.05 1616.80, 1277.59 1307.02 & 1452.27 1489.72

01-Apr-20 1594.25 1576.55, 1288.95 1270.23 & 1457.94 1442.86

31-Mar-20 1604.65 1608.95, 1299.61 1296.81 & 1461.52 1468.81

30-Mar-20 1624.35 1618.30, 1312.56 1305.97 & 1466.88 1466.02

27-Mar-20 1621.20 1617.30, 1325.33 1316.16 & 1473.18 1469.48

Editors Note: The shortage of gold bullion coins and bars continues and may deepen as prices move higher. It is not just smaller one ounce bullion coins and bars that are difficult to source but also larger gold and silver bars including gold kilo bars (32.15 ozs) worth and 1,000 oz silver bars. Due to our direct relationships with government mints and refineries we continue to source large bars and some gold coins and bars in 1 oz formats.

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here

ii) Important gold commentaries courtesy of GATA/Chris Powell

A really good commentary from the Martens’ as they discuss the measly 4 month safety net for workers but Wall Street gets a 4 to 5 year bailout

(courtesy Pam and Russ Martens/GATA)

Pam and Russ Martens: Workers get 4-month safety net, Wall Street gets 4-to-5-year bailout

Submitted by cpowell on Mon, 2020-04-13 15:43. Section: Daily Dispatches

11:45a ET Monday, April 13, 2020

Dear Friend of GATA and Gold:

The disgraceful contrast between the federal governments parsimony with suddenly unemployed working people, on one hand, and its corrupt extravagance with financial interests, on the other, is masterfully detailed in today’s Wall Street on Parade report by Pam and Russ Martens. It’s headlined “American Workers Get a 4-Month Safety Net; Wall Street Gets a 4-to-5-Year Bailout” and it’s posted here:

https://wallstreetonparade.com/2020/04/american-workers-get-a-4-month-sa…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

John Kim discusses how the crooks raise margin requirements trying to cause our precious metals to fall. It is not working

(Kim/GATA)

John Kim: Comex changes margin requirements to rig gold and silver prices down

Submitted by cpowell on Mon, 2020-04-13 16:03. Section: Daily Dispatches

12:05a ET Monday, April 13, 2020

Dear Friend of GATA and Gold:

Market analyst John Kim shows today how CME Group, operator of the major U.S. futures exchanges, including the Comex, has been changing margin requirements to knock down gold and silver prices and thereby discourage contract holders from taking delivery of metal. Kim adds that CME Group is even buying metal for its own account after changing margin requirements to push prices down.

Kim urges coin and bullion dealers to stop using futures prices in the pricing of their own products, so that the physical market destroys the paper market and its manipulations at last.

Kim’s commentary is headlined “Precious Metals Dealers: If the CME Artificially Creates Dips in Paper Gold and Silver Futures Prices by Raising Margins, Stand Your Ground” and it’s posted at his internet site here:

https://maalamalama.com/wordpress/cme-artificially-creates-dips-in-paper…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

A good interview of Stuart Englert who discusses the rigged precious metals market with Chris Marcus

(Englert/Chris Marcus/GATA)

‘Rigged’ author Stuart Englert interviewed by Chris Marcus of Arcadia Economics

Submitted by cpowell on Tue, 2020-04-14 02:25. Section: Daily Dispatches

10:29p ET Monday, April 13, 2020

Dear Friend of GATA and Gold:

Over the weekend Chris Marcus of Arcadia Economics interviewed Stuart Englert, author of “Rigged,” the new book about manipulation of the monetary metals market that draws heavily on GATA’s work.

To purchase a copy, see the advertisement below.

The interview is 18 minutes long and can be viewed at YouTube here:

https://www.youtube.com/watch?v=Q17rJPR68Y8

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

iii) Other physical stories:

(courtesy SchiffGold.com)

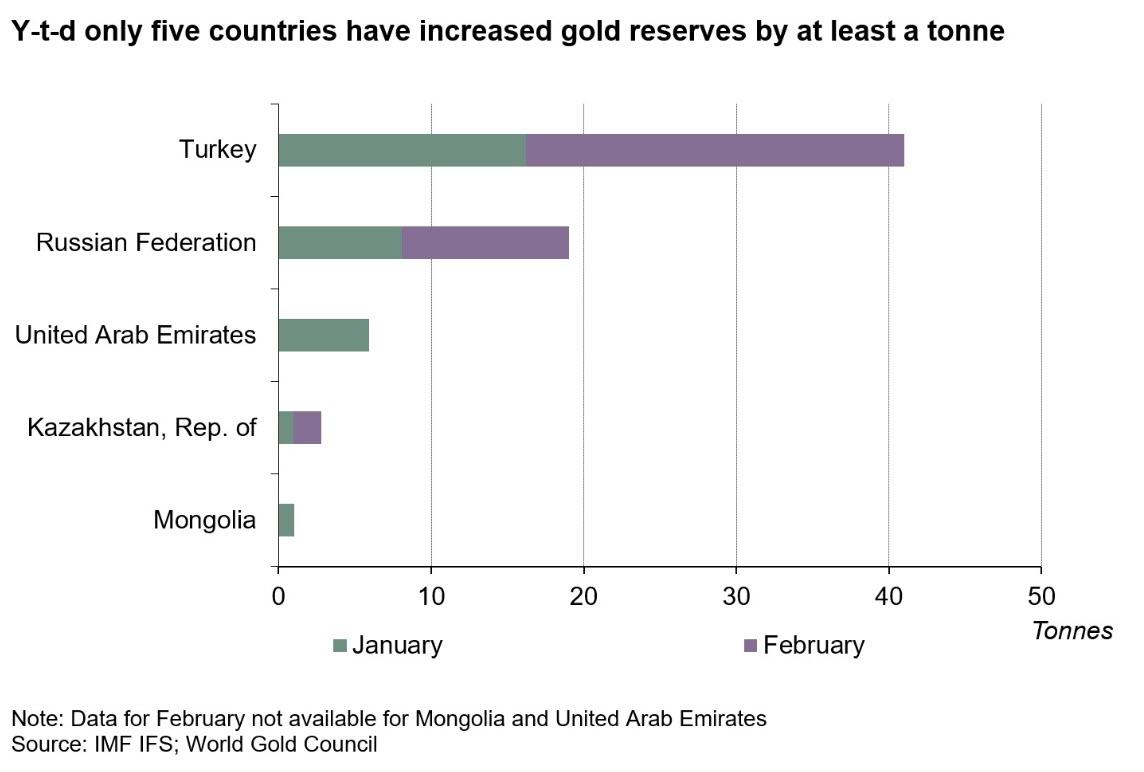

Central Banks Add More Gold To Their Reserves

Central banks continued their gold-buying spree in February, although the pace of gold purchases has slowed compared to last year’s near-record purchases.

On net, central banks globally added another 36 tons of gold to their reserves in February, according to the latest data released by the World Gold Council. That was about 33% higher than January’s total.

On the year, central banks have bought 64.5 tons of gold. That compares to 116 tons through the first two months of 2019.

Central bank demand came in at 650.3 tons in 2019. That was the second-highest level of annual purchases for 50 years, just slightly below the 2018 net purchases of 656.2 tons. According to the WGC, 2018 marked the highest level of annual net central bank gold purchases since the suspension of dollar convertibility into gold in 1971, and the second-highest annual total on record.

The World Gold Council bases its data on information submitted to the International Monetary Fund.

Turkey continued to be the biggest gold-buyer. The Turks added another 24.8 tons to their reserves in February.

Russia further increased its stockpile of yellow metal, adding another 10.9 tons to their hoard.

Russia’s quest for gold has paid off in a big way. The Russian Central Bank’s gold reserves topped $100 billion in September 2019 thanks to continued buying and surging prices.

The Russians have been buying gold for the last several years in an effort to diversify away from the US dollar. Russian gold reserves increased 274.3 tons in 2018, marking the fourth consecutive year of plus-200 ton growth. Meanwhile, the Russians sold off nearly all of its US Treasury holdings. According to Bank of America analysts, the amount of US dollars in Russian reserves fell from 46% to 22% in 2018.

Last month, the Central Bank of Russia announced it planned to suspend gold-purchases for the time being, effective April 1. But in the first week of April, Russian banks were already asking the central bank to restart gold purchases. They expressed concern over gold exports amid disruptions in the transportation industry due to the coronavirus pandemic. National Finance Association head Vasily Zablotsky told Reuters that banks are “facing problems” exporting gold as there are also fewer cargo flights and transportation costs have doubled.

Other buyers of gold in February included:

- Bulgaria – 0.3 tons

- Greece – 0.1 tons

- Kazakhstan – 1.8 tons

- Qatar – 1.6 tons

The only major seller was Uzbekistan at 3.1 tons.

The People’s Bank of China did not report any gold purchases for the fifth straight month. It’s not uncommon for China to go silent and then suddenly announce a large increase in reserves.

Many analysts believe China holds far more gold than it officially reveals. As Jim Rickards pointed out on Mises Daily back in 2015, many people speculate that China keeps several thousand tons of gold “off the books” in a separate entity called the State Administration for Foreign Exchange (SAFE). Given the political dynamics and the ongoing trade war, it seems unlikely the Chinese suddenly stopped increasing their gold reserves in 2016.

The WGC said it expects central banks to remain net-buyers of gold in 2020, but likely at a slower pace than the record levels we’ve seen over the past two years.

“We often get asked if central bank demand will be sustained. The past two months clearly suggest gold continues to be an important component of foreign reserves despite heightened levels of demand in recent years. But like everyone else, the recent market instability and uncertainty will be at the forefront of central bankers’ mind.”

Of course, it is difficult to tell how the economic impacts of the coronavirus pandemic will impact things down the road. It is possible that a rapid devaluation of the dollar due to Federal Reserve quantitative easing could drive central banks to dump dollars in exchange for gold.

Earlier this year, World Gold Council director of market intelligence Alistair Hewitt said there are two major factors driving central banks to buy gold – geopolitical instability and extraordinarily loose monetary policy.

Central banks are looking toward gold to balance some of that risk. We’ve also got negative rates and yields for a large number of sovereign bonds.”

Central bank policy has become significantly looser since Hewitt made that observation.

Peter Schiff has talked about central bank gold-buying. He has noted that the US went off the gold standard in 1971, but he thinks the world is going to go back on it.

The days where the dollar is the reserve currency are numbered and we’re going back to basics. You know, everything old is new again. Gold was money in the past and it will be money again in the future, and central banks that are smart enough to read that writing on the wall are increasing their gold reserves now.”

Ron Paul made a similar point in an episode of the Liberty report. He said foreign central banks are increasingly gravitating to sound money like gold and ripping themselves away from the Fed’s dollar.

The central banks of the world are looking at gold again.”

END-

A must view: Alasdair Macleod…

END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Futures Jump As Chinese Trade Data Unexpectedly Outperforms; All Eyes On Bank Earnings

Global stocks jumped and US equity futures traded just around 2,800 on Tuesday after Chinese trade data came in better than expected and some countries tried to restart their economy by partly lifting restrictions aimed at containing the coronavirus outbreak.

Wall Street indexes ended mixed on Monday. The Dow and S&P 500 fell, but a 6.2% gain in Amazon shares helped the Nasdaq end higher.

“The pullback in US equities should come as no surprise in light of last week’s historic rally,” said Mark Haefele, chief investment officer at UBS Wealth Management, noting the S&P 500 posting its best weekly performance since 1974. “Sentiment will zigzag until there is more clarity on formal measures to reopen major economies. More broadly, even though global markets have rebounded, it is difficult to say with any certainty whether the bottom has been reached.”

European stock markets opened stronger, with the pan-European STOXX 600 index rising 0.6% to its highest since March 11, with Spanish shares gaining 1.5% as some businesses re-opened, although shops, bars and public spaces were set to stay closed until at least April 26. Market sentiment was boosted by data showing China’s exports fell only 6.6% in March from a year ago, less than the expected 14% plunge. Imports fell 0.9% compared with expectations for a 9.5% drop.

The gains in Europe took MSCI’s All-Country World Index .MIWD00000PUS, which tracks shares across 49 countries, up 0.5%.

The Stoxx Europe 600 Basic Resources index is among leading sector gainers after China disclosed numbers showing trade performed better than expected in March, with China exports declining 6.6% in dollar terms in March from a year earlier (exp.-13.9%) while imports fell 0.9% (exp. -9.8%), the customs administration said Tuesday, indicating that supply chains may be adapting better than thought. Specifically, this is the data that China reported:

- Exports: -6.6% yoy in March vs Bloomberg consensus -13.9%. January-February: -17.2% yoy. Month-over-month export growth: +5.4% non-annualized in March vs. -7.8% in January-February.

- Imports: -0.9% yoy in March vs consensus: -9.5%. January-February: -4.0% yoy. Month-over-month imports growth: +0.8% non-annualized in March vs. -2.6% in January-February.

- Trade balance: US$+19.9bn NSA vs consensus US$+20.0bn in March. January-February: US$-7.1bn.

“Although further slowdown in the pandemic’s spreading may keep sentiment supported, we are still reluctant to trust a long-lasting recovery, and we prefer to take things day by day,” said Charalambos Pissouros, analyst at JFD Group.

Earlier in the session, MSCI’s broadest index of Asia-Pacific shares excluding Japan rose 1.3% to its highest in a month, up 20% from a four-year low on March 19. Chinese shares gained, with the blue-chip index up 1.2%. Australian shares were up 1.7% and Japan’s Nikkei rose 2.8%. Hong Kong’s Hang Seng was up 0.9%.

Earnings season kicks off this week with some of the world’s biggest banks reporting, giving investors their first glimpse of how bad the hit to global profits will be. Fidelity International analysts expect earnings to almost halve at companies globally this year. While Goldman Sachs Group forecasts advanced economies will shrink about 35% this quarter, investors are focusing on whether trillions of dollars in stimulus and rescue plans will fuel a rally in risk assets when the infections curve flattens.

In addition to the start of earnings season which begins with JPM reporting today, investors are also eyeing the easing of virus-related restrictions in some regions for further trading cues. In Europe, thousands of shops across Austria are set to re-open on Tuesday. Spain recorded its smallest proportional daily rise in the number of deaths and new infections since early March and let some businesses return to work on Monday.

In the United States, which has recorded the highest number of casualties from the virus in the world, President Donald Trump said on Monday his administration was close to completing a plan to re-open the U.S. economy. However, some state governors say the decision to restart businesses lies with them.In the latest developments, India and France extended their lockdowns and the British government is weighing similar steps.

In rates, 10Y yields dipped modestly to 0.75%, while Italian bonds fell after a report that the government is set to seek a significant deficit deviation. Bunds dropped as markets rose.

In commodities crude was up 0.85% at $22.55 a barrel, compared with a January peak of $63.27. Brent rose 1.3% to $32.16 a barrel. Oil prices rose around 1% after the U.S. Energy Information Administration (EIA) predicted shale output in the world’s biggest crude producer would fall by a record amount in April, adding to cuts from other major producers. Gold prices clung to highs not seen in more than seven years at $1,720.1 an ounce.

In currencies, the dollar extended losses on the back of the U.S. Federal Reserve’s massive new lending program. It weakened against the Japanese yen to 107.7. The euro was up 0.2% at $1.0929. The risk-sensitive Australian dollar jumped 0.6% to $0.6420.

Expected data include import and export prices. Fastenal, J&J, JPMorgan and Wells Fargo are among companies reporting results.

Market Snapshot

- S&P 500 futures up 1.3% to 2,793.75

- MXAP up 1.6% to 143.26

- MXAPJ up 1.3% to 461.49

- Nikkei up 3.1% to 19,638.81

- Topix up 2% to 1,433.51

- Hang Seng Index up 0.6% to 24,435.40

- Shanghai Composite up 1.6% to 2,827.28

- Sensex down 1.5% to 30,690.02

- Australia S&P/ASX 200 up 1.9% to 5,488.11

- Kospi up 1.7% to 1,857.08

- STOXX Europe 600 up 0.9% to 334.66

- German 10Y yield fell 0.3 bps to -0.35%

- Euro up 0.04% to $1.0918

- Italian 10Y yield fell 6.0 bps to 1.419%

- Spanish 10Y yield rose 3.2 bps to 0.814%

- Brent futures down 0.3% to $31.64/bbl

- Gold spot up 0.3% to $1,720.80

- U.S. Dollar Index down 0.1% to 99.21

Top Overnight News from Bloomberg

- Bloomberg’s monthly survey puts contraction in the euro area at more than 10% in the January-June period, with most of the hit – – 8.3% — in the second quarter. Even with an expected rebound later in the year, the bloc’s output will still decline more than 5% in 2020

- U.K. Foreign Secretary Dominic Raab told reporters it was likely to carry on and the government’s chief scientific adviser saying he expects the daily rate of deaths to continue to rise

- The Federal Reserve will start buying commercial paper on Tuesday, just as Wall Street braces for an earnings season likely blighted by the coronavirus outbreak

- Japanese Prime Minister Shinzo Abe said he wanted to start cash handouts for individuals and businesses hurt by the coronavirus pandemic as soon as May

- China has started the process of potentially merging its two biggest brokerage firms to create a company that can better compete with the global investment banks as the country opens up its financial markets, according to people familiar with the matter

Asian equity markets were positive across the board as sentiment picked up from the holiday lull and as the region digested the mostly better than expected Chinese trade data, but with some of the gains capped heading into the start of US earnings season and as participants pondered how soon the US will reopen its economy. ASX 200 (+1.9%) was led by strength in gold miners after the precious metal surged above the USD 1700/oz level to its highest in more than 7 years, while Nikkei 225 (+3.1%) outperformance was fuelled by favourable currency moves with SoftBank shares also reversing the initial glut of sell orders that followed its preliminary results that showed the first loss in 15 years. Hang Seng (+0.6%) and Shanghai Comp. (+1.6%) conformed to the regional optimism after the latest trade figures showed a much narrower than expected contraction in Exports and a surprise expansion to CNY-denominated Imports, although there were mixed comments from the customs bureau which noted there are signs of recovery for China’s foreign trade which is resilient but also warned of increasing uncertainties and that trade is encountering larger difficulties which cannot be underestimated. On the coronavirus front, China recently approved 2 experimental coronavirus vaccines to enter clinical trials and Beijing was said to have resumed all of the city’s 2130 major construction projects. Finally, 10yr JGBs were subdued in tandem with the downside in T-notes amid gains in riskier assets, but with losses stemmed after somewhat improved demand at the enhanced liquidity auction for long to super-long JGBs.

Top Asian News

- China’s Trade Fell Less Than Expected Even as Virus Spread

- India’s Modi Says Nationwide Lockdown Extended Through May 3

- Indonesia Surprises by Holding Key Rate, Cuts Reserve Ratio

- Air Arabia Is Said to Seek State Aid and Delay New Venture

- World’s Most Battered Corners in Bull Zone on Newfound Optimism

European equities remain mostly firm following a broad pickup in sentiment across APAC and US regions, with the former also aided by better-than-forecast Chinese trade data overnight. That being said, eyes turn to the resumption of earning season to gauge the initial impact of the virus outbreak on large-cap businesses. For reference, states-side earnings today include Johnson & Johnson (4.1% weighting in DJIA), JP Morgan (2.9% weighting in DJIA) and Wells Fargo. Back to Europe, UK’s FTSE 100 (-0.4%) lags regional peers as a firmer Sterling weighs on exporters, whilst reports also noted that the UK gov’t is poised to extend its lockdown to May 7th, although some reports over the weekend touted May 25th. Other European bourses see broad-based gains, with some possibly underpinned by comments from EU’s Competition Chief Vestager, who said member countries should purchase stakes in companies to repel the threat of Chinese takeovers. Broader sectors are somewhat mixed with underperformance in the Energy Sector, whilst Healthcare names lead the gains thus far. The sector breakdown does not give much by way of additional colour, although Travel & Leisure resume its downbeat performance as the sectors see no reprieve for the near future, whilst Carnival (-7.0%) sees pressure after the group is to extend its suspension on North American cruises. In terms of individual movers; AstraZeneca (+6.0%) props up the healthcare sector as shares were bolstered at the open after the Co. said its Tagrisso Adjuvant trial has been overwhelmingly positive. Separately, Co’s Koselugo has been approved in the US for paediatric patients with a rare genetic condition. Finally, the Co. has also initiated the Calavi clinical trials with Calquence against COVID-19. Renault (+3.0%) remains firm despite a cancellation to FY19 dividend after the Co. is to transfer its 50% stake in Dongfeng Renault to Dongfeng in a non-binding memorandum. Publicis (-0.3%) saw losses at the open after reporting that organic revenue dell 2.9% YY, although the Co. launched a EUR 500mln cost reduction plan. Accor (-2%) saw early-morning pressure after French Finance Minister Le Maire said he cannot say when hotels and restaurants will reopen. Note: Eurex and Deutsche Boerse have been experiencing technical problems that are being investigated.

Top European News

- Austria Tests Easing Lockdown With Some Stores Reopening Tuesday

- GAM Accelerates Cuts as Assets Plunge by $13 Billion in Quarter

- Norwegian Air Plunges 63% on Plan to Convert Debt to Equity

- Crisis in Russia Puts $13 Billion of Remittances at Risk

- Crisis Gives Germany Sense of Vindication for ‘Black Zero’

In FX, the Dollar remains depressed after last Thursday’s mega Fed stimulus package and ramp up in Gold through the Usd1700/oz threshold to fresh 7 year peaks, with the DXY unable to regain a foothold above 99.500 within a 99.432-121 range amidst selective risk-on flows in wake of latest COVID-19 updates, the eventual OPEC+ crude output accord and Eurozone Finance Ministers finally agreeing on a substantial fiscal stimulus package. Ahead, US import export prices are scheduled, but unlikely to prompt much, if any reaction, but Wednesday’s data releases are top tier.

- GBP – The Pound is off best levels, but still the best performing G10 currency after UK PM Johnson’s discharge from hospital. Cable remains comfortably above the 1.2500 handle and briefly crossed the 50 DMA at 1.2568 to print a fresh 1.2575 recovery high before reports from the ONS emerged raising the number of fatalities in England and Wales by 15% vs NHS figures published to April 3rd, while Eur/Gbp is back above 0.8700 from circa 0.8784 at one stage awaiting revised GDP and deficit estimates from the OBR under various coronavirus scenarios due at 12.00BST.

- ZAR – In contrast to Sterling, Rand gains against the Buck were initially reversed from 18.0000+ to just shy of 18.2000 in wake of an unexpected 100 bp SARB rate cut that was announced via social media and came after May’s scheduled policy meeting was brought forward. However, Usd/Zar subsequently soared beyond 18.3300 as Central Bank Governor Kganyago

- JPY/EUR/CHF/AUD/NZD – All firmer vs the Greenback, as the Yen defies improved risk sentiment to hold at the upper end of 107.79-39 parameters, but not quite close enough to disturb decent option expiry interest protecting 107.00 at 107.05 (1.1 bn). Note, no real rection to latest BoJ source talk about increased and wider QE remits at this month’s meeting that might include expanding the range of assets accepted for collateral. Similarly, the Euro is hovering closer to the top of 1.0957-06 confines and the Franc nearer 0.9637 than 0.9679 even though latest weekly Swiss sight deposits indicate significantly more intervention by domestic banks on behalf of the SNB. Elsewhere, some loss of overnight momentum forged on the back of Chinese trade revealing a surprise rise in Yuan denominated imports for the Aussie and Kiwi, but both retaining sight of big figure/psychological resistance marks at 0.6400 and 0.6100 respectively.

- CAD/NOK/SEK – In keeping with the rather muted response following knee-jerk relief in oil on the aforementioned OPEC+ pact, the Loonie is paring advances from around 1.3863 to sub-1.3900 as attention switches towards tomorrow’s BoC meeting and the prospect of downbeat/dovish guidance, assuming no further action. Meanwhile, the Norwegian Krona has also retreated from almost 11.1700 vs the Euro to 11.2800, but its Swedish peer showing a bit more resilience above 10.9000 due to signs of the case and death count from nCoV flattening.

- EM – The Lira is struggling to contain losses below 5.7900 amidst heightened coronavirus contagion and the Turkish banking regulator slashing FX swap and derivative limits, while the already unstable political backdrop has been rocked by the resignation of the country’s Interior Minister.

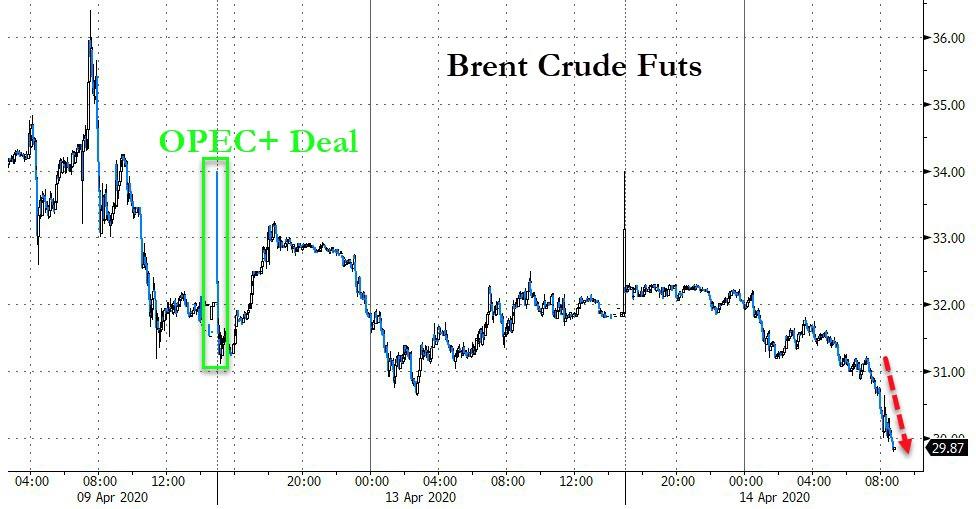

In commodities, WTI and Brent front-month futures reverse course after initially eking mild gains following the fallout of the OPEC+ and G20 ad-hoc meetings which failed to spur a rally but more-so stemmed declines in the complex (in the short-term at least). As a recap for European players, OPEC+ agreed to cut joint output by 9.7mln BPD, starting on 1 May 2020, for an initial period of two months that concludes on 30 June 2020. For the subsequent period of 6 months, from 1 July 2020 to 31 December 2020, the total adjustment agreed will be 7.7mln BPD. It will be followed by a 5.8mln BPD cut from 1 January 2021 to 30 April 2022. The baseline for the calculation of the adjustments is the oil production of October 2018, except for the Kingdom of Saudi Arabia and Russia, both with the same baseline level of 11.0mln BPD. The agreement will be valid until 30 April 2022; however, the extension of this agreement will be reviewed during December 2021. Saudi, UAE and Kuwait all pledged voluntary over-compliance, whilst G20 is to curtail output by some 3.7mln BPD. Yesterday, Saudi Aramco cut their OSPs for several grades for the second month in a row despite the output cut deal; albeit, OSPs for all grades to the US were raised. The Arab Light discount to Asia reflects the supply glut. Furthermore, Russian Energy Minister Novak said he met with domestic oil producers and they supported the OPEC+ deal, while he added that total oil output cuts in May-June will total between 15-20mln BPD. WTI straddled around USD 22.50/bbl in early trade before briefly dipping below USD 22/bbl, whilst Brent meanders just below USD 31.50/bbl, having confirmed to the modest sell-off during the session The difference between the contracts meanwhile remains wider to the tune of around USD 9.50/bbl vs. a pre-OPEC sub-5/bbl number. Elsewhere, spot gold holds onto a bulk of yesterday’s gains and remains north of USD 1700/oz and near recently-set 7yr highs given USD weakness and as investors stock up on the yellow metal following the liquidity-induced declines last month. Copper meanwhile has given up the gains seen during the APAC session after Freeport-McMoRan said it will temporarily shut its Chino copper mine (produced 88k tons of copper in 2019) due to the virus outbreak, albeit the red metal remains caged in a narrow 2.3250-2.3480 band.

US Event Calendar

- 8:30am: Import Price Index MoM, est. -3.2%, prior -0.5%; Import Price Index YoY, est. -5.0%, prior -1.2%

- 8:30am: Export Price Index MoM, est. -1.9%, prior -1.1%; Export Price Index YoY, prior -1.3%

DB’s Jim Reid concludes the overnight wrap

I hope you all had a relaxing if probably a little strange Easter. Today is actually 10 years to the day that the second more dramatic eruption of Icelandic volcano Eyjafjallajökull occurred. The following day all European air travel was shut down for a week. Imagine if you’d had a big trip planned for your 40th or 50th birthday that week, saw it cancelled and vowed that in 10 years’ time you’d celebrate your next major landmark with an even bigger trip to make up for it. I feel for you this week it’s that’s you!! I certainly won’t be arranging a big trip for mid-April 2030!