GOLD:$1717.90 DOWN $19.10 The quote is London spot price

Silver:$15.35//DOWN 45 CENTS London spot price

Closing access prices: London spot

i)Gold : $1714.00 LONDON SPOT 4:30 pm

ii)SILVER: $15.47//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

APRIL comex gold price CLOSE 1.30 PM: $1725.10

MAY COMEX GOLD: 1729.20 1:30 PM

JUNE GOLD: $1741.00 CLOSE 1.30 PM// SPREAD SPOT/FUTURE JUNE: $23.10

CLOSING SILVER FUTURE MONTH

SILVER APRIL COMEX CLOSE: 15.70/

SILVER MAY COMEX CLOSE; $15.52…1:30 PM.//SPREAD SPOT/FUTURE MAY: 17 CENTS PER OZ

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2600. usa per oz

and silver; $31.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 41/552

issued: 96

EXCHANGE: COMEX

CONTRACT: APRIL 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,756.700000000 USD

INTENT DATE: 04/14/2020 DELIVERY DATE: 04/16/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

132 C SG AMERICAS 24

657 C MORGAN STANLEY 10

657 H MORGAN STANLEY 479

661 C JP MORGAN 96 41

686 C INTL FCSTONE 16 3

690 C ABN AMRO 412 1

737 C ADVANTAGE 10 4

800 C MAREX SPEC 3

905 C ADM 5

____________________________________________________________________________________________

TOTAL: 552 552

MONTH TO DATE: 29,410

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 552 NOTICE(S) FOR 55,200 OZ (1.716 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 29,410 NOTICES FOR 2,941,000 OZ (91.477 TONNES)

SILVER

FOR APRIL

5 NOTICE(S) FILED TODAY FOR 25,000 OZ/

total number of notices filed so far this month: 806 for 4,025,000 oz

BITCOIN MORNING QUOTE $6750 DOWN 169

BITCOIN AFTERNOON QUOTE.: $6731 DOWN $130

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $19.10: AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

WE HAD ANOTHER STRONG DEPOSIT OF 7.89 TONNES (PAPER TONNES/NOT REAL STUFF)

GLD: 1,117.59 TONNES OF GOLD//

WITH SILVER DOWN 45 CENTS TODAY: AND WITH NO SILVER AROUND

TWO HUGE DEPOSITS OF SILVER WAS ADDED TO OUR SLV INVENTORY TONIGHT: A)1.679 MILLION OZ

AND B) 5.222 MILLION OZ

RESTING SLV INVENTORY TONIGHT:

SLV: 415.437 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A STRONG SIZED 3308 CONTRACTS FROM 140,169 UP TO 143,477 AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE STRONG SIZED GAIN IN OI OCCURRED WITH OUR HUGE 51 CENT GAIN IN SILVER PRICING AT THE COMEX. WE HAD ZERO LONG LIQUIDATION. IT SEEMS THAT THE GAIN IN COMEX OI IS DUE TO BANKER SHORT COVERING PLUS A CONSIDERABLE EXCHANGE FOR PHYSICAL ISSUANCE ALONG WITH A STRONG GAIN IN SILVER OZ STANDING. WE HAD A VERY STRONG NET GAIN IN OUR TWO EXCHANGES OF 4025 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A STRONG AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: MARCH: 00 AND MAY: 668 AND JULY: 0 ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 791 CONTRACTS. WITH THE TRANSFER OF 668 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 668 EFP CONTRACTS TRANSLATES INTO 3.340 MILLION OZ ACCOMPANYING:

1.THE 51 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.145 MILLION OZ INITIALLY STANDING FOR APRIL

TUESDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 51 CENTS).. AND, OUR OFFICIAL SECTOR/BANKERS WERE TOTALLY UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS, AS WE DID HAVE A VERY STRONG NET GAIN OF 3976 CONTRACTS OR 19.88 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER JUDGING BY THE HUGE GAIN IN PRICE.

OUR SPREADING OPERATION HAS NOW SWITCHED INTO SILVER…..

SPREADING OPERATION FOR OUR NEWCOMERS:

WE HAVE NOW COMMENCED IN SILVER THE ILLEGAL SPREADING OPERATION \ FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW STOPPED IN GOLD AS THEY NOW BEGIN TO MORPH INTO SILVER AS WE HEAD TOWARDS THE NEW FRONT MONTH WILL BE MAY.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF APRIL. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

10,232 CONTRACTS (FOR 9 TRADING DAYS TOTAL 10,232 CONTRACTS) OR 51.160 MILLION OZ: (AVERAGE PER DAY: 1136 CONTRACTS OR 5.684 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF APRIL: 51.160 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 7.30% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 944.64 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP SO FAR 51.16 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3308, WITH THE HUGE $0.51 GAIN IN SILVER PRICING AT THE COMEX /TUESDAY… THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 668 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A VERY STRONG SIZED OI CONTRACTS ON THE TWO EXCHANGES: 4025 CONTRACTS (WITH OUR 51 CENT GAIN IN PRICE)

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 668 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 3308 OI COMEX CONTRACTS.AND ALL OF THIS DEMAND HAPPENED WITH A 51 CENT GAIN IN PRICE OF SILVER/ AND A CLOSING PRICE OF $15.80 // TUESDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY AS WELL AS A GOOD INCREASE IN QUEUE JUMPING//AMOUNT STANDING!!

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.7005 BILLION OZ TO BE EXACT or 100.2% of annual global silver production (ex Russia & ex China).

FOR THE NEW MAR DELIVERY MONTH/ THEY FILED AT THE COMEX: 5 NOTICE(S) FOR 25,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.145 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1863 CONTRACTS TO 489,965 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE GAIN OF COMEX OI OCCURRED WITH OUR VERY STRONG COMEX GAIN IN PRICE OF $23.55 /// COMEX GOLD TRADING// TUESDAY// WE HAD CONSIDERABLE BANKER SHORT COVERING ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A GOOD EX. FOR PHYSICAL ISSUANCE AND THIS WAS COUPLED WITH OUR STRONG GAIN IN THE PAPER PRICE OF GOLD.

WE HAD NO ISSUANCE OF OUR NEW 4 GC CONTRACT

WE GAINED A GOOD 3071 CONTRACTS (9.552 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 4047 CONTRACTS:

CONTRACTS, FEB> 0 CONTRACTS; MARCH 00 APRIL: 0. MAY: 0, AND JUNE 4047.; DEC 0 AND ALL OTHER MONTHS ZERO//TOTAL: 4047. The NEW COMEX OI for the gold complex rests at 489,965. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2,184 CONTRACTS: 1863 CONTRACTS DECREASED AT THE COMEX AND 4047 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 2184 CONTRACTS OR 6.793 TONNES. TUESDAY, WE HAD A HUGE GAIN OF $23.55 IN GOLD TRADING……

AND WITH THAT HUGE GAIN IN PRICE, WE HAD A GOOD SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 6.973 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (ROSE $23.55). AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WERE UNSUCCESSFUL (SEE BELOW).

4 GC ISSUANCE: ZERO

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A GOOD SIZED INCREASE IN EXCHANGE FOR PHYSICALS (4047) ACCOMPANYING THE FAIR LOSS IN COMEX OI (1863 OI): TOTAL GAIN IN THE TWO EXCHANGES: 2184 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)A MONSTROUS INCREASE IN STANDING AT THE GOLD COMEX FOR THE FRONT APRIL MONTH, 3) ZERO LONG LIQUIDATION AND …ALL OF THIS WAS COUPLED WITH THAT HUGE GAIN IN GOLD PRICE TRADING//TUESDAY

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 48,849 CONTRACTS OR 4,884,900 oz OR 151.94 TONNES (9 TRADING DAYS AND THUS AVERAGING: 5427 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES: 151.94 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 151.94/3550 x 100% TONNES =4.28% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 2474.84 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 151.94 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 3308 CONTRACTS FROM 140,169 UP TO 143,477 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

ALL OF THE GAIN IN COMEX OI WAS DUE TO 1) HUGE BANKER SHORT COVERING , 2) THE ISSUANCE OF A GOOD SIZED NUMBER OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A ZERO INCREASE IN SILVER OZ STANDING AT THE COMEX FOR APRIL AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 668 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR FEB. 0; FOR MAR 0: AND MAY: 668; JULY: 00 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 668 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE STRONG COMEX OI GAIN OF 3308 CONTRACTS TO THE 668 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 3976 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 19.88 MILLION OZ!!! AND WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ// SEPT: 43.030 MILLION OZ///OCT: 7.32 MILLION OZ//NOV 2.63 MILLION OZ//DEC: 20.970 MILLION OZ//JAN: 5.075 MILLION OZ//FEB: 1.480 MILLION OZ//MAR: 23.005 MILLION OZ//APRIL 4.145 MILLION OZ//

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 51 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// TUESDAY. WE ALSO HAD A GOOD SIZED 668 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 16.11 POINTS OR 0.57% //Hang Sang CLOSED DOWN 290.06 POINTS OR 1.19% /The Nikkei closed DOWN 88.72 POINTS OR 0.45%//Australia’s all ordinaires CLOSED DOWN .35%

/Chinese yuan (ONSHORE) closed DOWN at 7.0620 /Oil DOWN TO 19.57 dollars per barrel for WTI and 28.46 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0620 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0681 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: 0 oz

total dealer withdrawals: 0 oz

i)we had 0 deposits into the customer account

into JPMorgan: 0

ii)into everybody else; 0

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.819 million oz of total silver inventory or 50.04% of all official comex silver. (160.819 million/321.170 million

total customer deposits today: 607,477.800 oz

we had 2 withdrawals:

total withdrawals; 658,651.269 oz

We had 2 adjustments: and all from the dealer to the customer:

i) Scotia: 354,301.800 oz

ii) CNT: 4941.700

total dealer silver: 81.788 million

total dealer + customer silver: 319.111 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The total number of notices filed today for the APRIL 2020. contract month is represented by 5 contract(s) FOR 25000 oz

To calculate the number of silver ounces that will stand for delivery in APRIL we take the total number of notices filed for the month so far at 806 x 5,000 oz = 4,025,000 oz to which we add the difference between the open interest for the front month of APRIL.(28) and the number of notices served upon today 5 x (5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL/2019 contract month: 806 (notices served so far) x 5000 oz + OI for front month of APRIL (28)- number of notices served upon today (5) x 5000 oz of silver standing for the APRIL contract month.equals 4,145,000 oz.

WE GAINED 4 CONTRACTS OR AN ADDITIONAL 20,000 OZ OF SILVER WILL STAND AT THE COMEX.

TODAY’S ESTIMATED SILVER VOLUME: 58,997 CONTRACTS //

FOR YESTERDAY: 93,250 CONTRACTS..,CONFIRMED VOLUME

YESTERDAY’S CONFIRMED VOLUME OF 93,250 CONTRACTS EQUATES to 466 million OZ 66.7% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO +1.24% ((APRIL 15/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO +0.17% to NAV: (APRIL 14/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into POSITIVE/ 1.24%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.76 TRADING 15.79///PREMIUM TO NAV: 0.21

END

And now the Gold inventory at the GLD/

APRIL 15//WITH GOLD DOWN $19.10 TODAY; ANOTHER HUGE CHANGE IN GOLD INVENTORY; A STRONG 7.89 TONNES WAS ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 1117.59 TONNES.//11TH STRAIGHT STRONG DEPOSIT

APRIL 14/WITH GOLD UP $23.55 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 15.51 TONNES WAS ADDED TO THE GLD INVENTORY/INVENTORY RESTS AT 1009.70 TONNES//THIS IS THE 10TH STRAIGHT STRONG DEPOSIT//THIS IS A FRAUDULENT VEHICLE..THEY HAVE NO PHYSICAL GOLD IN THE TRUST..

APRIL 13//WITH GOLD UP $27.65 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 5.36 TONNES WAS ADDED TO THE GLD//INVENTORY RESTS AT 994.19 TONNES

APRIL 9 WITH GOLD UP $37.30 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 2.92 TONNES WAS ADDED TO THE GLD//GOLD INVENTORY RESTS TONIGHT AT..988.63 TONNES

APRIL 8/WITH GOLD DOWN $.60//ANOTHER HUGE CHANGE IN GOLD INVENTORY/;; A STRONG 1.45 TONNES WAS ADDED TO THE GLD/GOLD INVENTORY RESTS AT 985.71 TONNES

APRIL 7/WITH GOLD UP $.30: ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.27 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 984.26 TONNES

APRIL 6//WITH GOLD UP $32.00//ANOTHER STRONG DEPOSIT INTO THE GLD; A HUGE 7.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT : 978.99 TONNES

APRIL 3//WITH GOLD UP $7.80 TODAY//ANOTHER STRONG DEPOSIT OF 3.22 TONNES INTO THE GLD/INVENTORY RESTS AT 971.97 TONNES

APRIL 2//WITH GOLD UP $31.80 TODAY: ANOTHER STRONG DEPOSIT OF 1.75 TONNES INTO THE GLD//INVENTORY RESTS AT 968.75 TONNES

APRIL 1/WITH GOLD DOWN $7.70 TODAY: ANOTHER CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.62 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 967.00 TONNES

MARCH 31//WITH GOLD DOWN $32.70//A MONSTROUS PAPER DEPOSIT OF 10.84 TONNES INTO THE GLD//INVENTORY RESTS AT 964.38 TONNES

MARCH 30/WITH GOLD DOWN $6.10 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 953.54 TONNES

MARCH 27.WITH GOLD DOWN $16.40: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A HUGE DEPOSIT OF 4.39 TONES INTO THE GLD/INVENTORY RESTS AT 953.54 TONES

MARCH 26//WITH GOLD UP $24.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 13.17 TONNES INTO THE GLD/INVENTORY RESTS AT 949.15 TONNES

MARCH 25/WITH GOLD DOWN $11.40 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.99 TONES INTO THE GLD INVENTORY////INVENTORY RESTS AT 935.98 TONNES

MARCH 24//WITH GOLD UP $67.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 15.80 TONNES OF GOLD INTO GLD////INVENTORY RESTS AT 923.99 TONNES..THIS PROVES THAT THE GLD IS A FRAUD AS LONDON SUSPENDED DELIVERY AS WELL AS ALL REFINERS. THEY HAD NO WAY OF GETTING ANY PHYSICAL OZ INTO ITS INVENTORY//

MARCH 23//WITH GOLD UP $76.00 TODAY: A HUGE PAPER WITHDRAWAL OF 21.50 TONNES FROM THE GLD////INVENTORY RESTS AT 908.19 TONNES

MARCH 20//WITH GOLD UP $5.50//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 7.46 TONNES FROM THE GLD////INVENTORY RESTS AT 922.23 TONNES

MARCH 19/WITH GOLD DOWN 90 CENTS: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 929.84 TONNES

MARCH 18/WITH GOLD DOWN $48.00: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 929.84 TONNES

MARCH 17/WITH GOLD UP $37.60: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM GLD INVENTORY//INVENTORY RESTS AT 929.84 TONNES

MARCH 16/WITH GOLD DOWN $30.00/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 12.59 TONNES/INVENTORY RESTS AT 931.59 TONNES

MARCH 13//WITH GOLD DOWN $73.60: A HUGE WITHDRAWAL OF 9.02 TONNES OF PAPER GOLD FROM THE GLD//

INVENTORY RESTS AT 944.18 TONNES

MARCH 12/WITH GOLD DOWN $55.05 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/953.26 TONNES

MAR 11/WITH GOLD DOWN $14.95?/A HUGE WITHDRAWAL OF 10.53 TONNES//INVENTORY RESTS AT 953.26 TONNES

MARCH 10/WITH GOLD DOWN $14.25//A HUGE 8.00 TONNES OF PAPER GOLD DEPOSIT INTO THE GLD//INVENTORY RESTS AT 963.79

MARCH 9//WITH GOLD UP $1.50 : NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 955.60 TONNES

March 6/WITH GOLD UP $6.25 A MASSIVE 21.37 PAPER TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 955.60 TONNES

MARCH 5/WITH GOLD UP $25.40//NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS TONIGHT AT 934.23 TONNES

MARCH 4//WITH GOLD DOWN 1 DOLLAR: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.23 TONNES//

MARCH 3//WITH GOLD UP 48.55 TODAY; NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.23 TONNES

MARCH 2//WITH GOLD UP $27.00// no change in gold inventory at the gld//inventory remains at 934.23 tonnes

FEB 28/WITH GOLD DOWN $73.00 WE LOST NO GOLD FROM THE GLD/INVENTORY REMAINS 934.23 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

APRIL 15/2020/ 1117.59 tonnes*

IN LAST 799 TRADING DAYS: +71.25 NET TONNES HAVE BEEN REMOVED FROM THE GLD

LAST 699 TRADING DAYS;+246.23 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

APRIL 15//WITH SILVER DOWN 45 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV TWO HUGE DEPOSITS: A DEPOSIT OF 1.679 MILLION OZ AND ANOTHER 5.222 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 14./WITH SILVER UP 51 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A MASSIVE PAPER DEPOSIT OF XXX MILLION OZ//INVENTORY RESTS AT 408.536 MILLION OZ//

APRIL 13//WITH SILVER DOWN 29 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 6.155 MILLION OZ////INVENTORY RESTS AT 408.536 MILLION OZ//

APRIL 9/WITH SILVER UP 60 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUGE DEPOSIT OF 1.84 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 402.381 MILLION OZ.

APRIL 8//WITH SILVER DOWN 21 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 401.541 MILLION OZ///

APRIL 7/WITH SILVER UP 26 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.766 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 395.826 MILLION OZ

APRIL 6/WITH SILVER UP 50 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 395.826 MILLION OZ.

APRIL 3//WITH SILVER DOWN 15 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 746,000 OZ INTO THE SLV//INVENTORY RESTS AT 395.826 MILLION OZ

APRIL 2/WITH SILVER UP 65 CENTS; A SMALL CHANGE TODAY..A WITHDRAWAL OF .335 MILLION OZ TO PAY FOR FEES//INVENTORY RESTS AT 394.826 MILLION OZ/

APRIL 1/WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 395.181 MILLION OZ//

MARCH 31/WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 1.679 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 375.181 MILLION OZ//

MARCH 30/WITH SILVER DOWN 44 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 393.502 MILLION OZ.

MARCH 27/WITH SILVER DOWN 5 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTROUS PAPER DEPOSIT OF 8.115 MILLION OZ INTO THE SLV../INVENTORY RESTS AT 393.502 MILLION OZ//

MARCH 26/WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 385.387 MILLION OZ///

MARCH 25/WITH SILVER UP 44 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSITS OF 7.369 MILLION OZ AND 2.239 MILLION OZ OF PAPER SILVER INTO THE SLV////INVENTORY RESTS AT 385.387 MILLION OZ//

MARCH 24//WITH SILVER UP 100 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 375.779 MILLION OZ///

MARCH 23//WITH SILVER UP 70 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.332 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 375.779 MILLION OZ

MARCH 20//WITH SILVER UP 39 CENTS TODAY: 2 HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A PAPER WITHDRAWAL OF 1.026 MILLION OZ FROM THE SLV AND THEN A PAPER ADDITION OF 3.638 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 373.447 MILLION OZ//

MARCH 19/WITH SILVER UP 38 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: ANOTHER 5.597 MILLION OZ OF SILVER VAPOUR ADDED TO THE SLV INVENTORY//INVENTORY RESTS AT 370.835 MILLION OZ/

MARCH 18//WITH SILVER DOWN 75 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTROUS 12.035 MILLION PAPER OZ ADDED INTO INVENTORY//INVENTORY RESTS AT 365.238 MILLION OZ//

MARCH 17/WITH SILVER DOWN 20 CENTS TODAY; A BIG CHANGES IN SILVER INVENTORY AT THE SLV; A WITHDRAWAL OF 3.735 MILLION OZ FROM THE SLV INVENTORY: INVENTORY RESTS AT 353.203 MILLION OZ///

MARCH 16/WITH SILVER DOWN 177 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESETS AT 356.938 MILLION OZ//

MARCH 13//WITH SILVER DOWN 155 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.893 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 356.938 MILLION OZ;

MARCH 12/WITH SILVER DOWN 77 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.119 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 359.828 MILLION OZ

MARCH 11/SILVER DOWN 16 CENTS: A SMALL WITHDRAWAL OF .467 MILLION OZ AT THE SLV/INVENTORY RESTS AT 360.947 MILLION OZ//

MARCH 10/WITH SILVER DOWN 10 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 361.414 MILLION OZ//

MARCH 9/NO CHANGE IN INVENTORY LEVELS: SLV INVENTORY RESTS AT 361.414 MILLION OZ//

MARCH 6//WITH SILVER DOWN 10 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 361.414 MILLION OZ

MARCH 5//WITH SILVER UP 15 CENTS TODAY; A SMALL WITHDRAWAL DUE TO FEES ETC//INVENTORY RESTS TONIGHT AT 361.414 MILLION OZ..

MARCH 4/SILVER SILVER UP 3 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 361.880 MILLION OZ//

MARCH 3/WITH SILVER UP 44 CENTS//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: A LOSS OF 5.75 MILLION OZ FROM THE SLV../INVENTORY RESTS AT 361.880 MILLION OZ

MARCH 2//WITH SILVER UP 18 CENTS//NO CHANGE IN SILVER INVENTORY AT THE SLV..INVENTORY RESTS AT 367.632 MILLION OZ//

FEB 28/ WITH SILVER DOWN 18 CENTS: a loss of 1.867 million oz//inventory rests at 367.632 million oz

APRIL 15.2020:

SLV INVENTORY RESTS TONIGHT AT

415.437 MILLION OZ.

END

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 5.32/ and libor 6 month duration 1.16

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – 4.16

gold non existent..only gold vapour exists!

XXXXXXXX

12 Month MM GOFO

+ 2.73%

LIBOR FOR 12 MONTH DURATION:1.03

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -1.70%

gold non existent

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Safe Haven Gold To Protect As ‘Great Lockdown’ To Create Great Depression

NEWS and COMMENTARY

Gold slips as investors lock in profits, recession fears cap losses

Gold’s Powerful Rally Brings $1,800 Into View

Gold rallies to over 7-year high as virus sparks depression fears

Goldman says downturn will be four times worse than the financial crisis

Asia shares take a breather, China cuts medium-term rates

Oil in the age of coronavirus: a U.S. shale bust like no other

Trump cuts WHO funding over coronavirus, global toll mounts

Three top Wall Street banks have $7.4 trillion in off-balance-sheet exposures

Gold Sparkles as “The Great Lockdown” Hammers the Global Economy

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

14-Apr-20 1715.85 1741.90, 1367.36 1383.07 & 1567.91 1588.26

09-Apr-20 1662.50 1680.65, 1339.48 1348.22 & 1529.00 1538.13

08-Apr-20 1649.05 1647.80, 1328.27 1330.27 & 1517.00 1513.14

07-Apr-20 1652.20 1649.25, 1344.23 1333.75 & 1519.53 1511.21

06-Apr-20 1636.60 1648.30, 1330.72 1341.06 & 1515.49 1526.66

03-Apr-20 1609.75 1613.10, 1310.66 1315.97 & 1490.47 1495.34

02-Apr-20 1588.05 1616.80, 1277.59 1307.02 & 1452.27 1489.72

01-Apr-20 1594.25 1576.55, 1288.95 1270.23 & 1457.94 1442.86

31-Mar-20 1604.65 1608.95, 1299.61 1296.81 & 1461.52 1468.81

30-Mar-20 1624.35 1618.30, 1312.56 1305.97 & 1466.88 1466.02

Editors Note: The shortage of gold bullion coins and bars continues and may deepen as prices move higher. It is not just smaller one ounce bullion coins and bars that are difficult to source but also larger gold and silver bars including gold kilo bars (32.15 ozs) worth and 1,000 oz silver bars. Due to our direct relationships with government mints and refineries we continue to source large bars and some gold coins and bars in 1 oz formats.

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here

ii) Important gold commentaries courtesy of GATA/Chris Powell

Very important: Wall Street banks are not well capitalized and they have 7.4 trillion dollars in off balance sheet exposure. This exposure will now come into play with the global economy screeching to a halt

(Pam and Russ Martens/Wall Street on Parade/GATA)

Pam and Russ Martens: Three top Wall Street banks have $7.4 trillion in off-balance-sheet exposures

Submitted by cpowell on Tue, 2020-04-14 17:23. Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Tuesday, April 14, 2020

In the past few weeks everyone from Federal Reserve Chairman Jerome Powell to U.S. Treasury Secretary Steve Mnuchin to former Fed Chairwoman Janet Yellen to bank analyst Mike Mayo have appeared on television to tell the American people that the big banks on Wall Street are well capitalized. To put it in Janet Yellen’s exact words on CNBC last Thursday, “We have a strong, well-capitalized banking system.”

…

These folks have to keep repeating this mantra because the public is getting curious as to why the New York Fed has had to pump a cumulative $9 trillion in cash into these Wall Street banks, since September 17 of last year, if they are so well capitalized. Can big banks actually be well capitalized and have no liquid money to make loans — the key function of a bank? As we have regularly noted, the Fed’s trillions of dollars in cash infusions to the banks began months before there was any coronavirus outbreak anywhere in the world.

The reality is that the U.S. banking system looks well capitalized only if federal regulators, banking analysts, and the mainstream business press put blinders on and don’t look at what’s hiding in off-balance-sheet items at the banking behemoths on Wall Street — the same fatal mistake they all made in the years leading up to the 2008 collapse. …

… For the remainder of the report:

https://wallstreetonparade.com/2020/04/three-of-the-biggest-banks-on-wal…

END

Craig Hemke is stating the obvious: the comex is broken: they have asked the CFTC not to disclose that they cannot deliver any gold/silver.

(Craig Hemke/Sprott/GATA)

Craig Hemke at Sprott Money: Comex search and seizure

Submitted by cpowell on Wed, 2020-04-15 00:28. Section: Daily Dispatches

8:30p ET Tuesday, April 14, 2020

Dear Friend of GATA and Gold:

The TF Metals Report’s Craig Hemke, writing tonight at Sprott Money, says the New York Commodities Exchange has been caught without enough metal to deliver against contracts and now has asked the U.S. Commodity Futures Trading Commission not to disclose how the exchange is papering things over, still without delivering.

Hemke writes: “The scramble for physical gold (and silver) is on and if you don’t hold it, you don’t own it. All of this bank and exchange scheming should prove, once and for all, that there is no transparency, fairness, and honest operation within the bullion bank fractional-reserve and digital-derivative pricing scheme. Instead, there are lies, cover-ups, distortions, illusions, charades, deceptions, tricks, gimmicks, counterfeits, deceit, duplicity, and frauds.”

Hemke’s commentary is headlined “Comex Search and Seizure” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/comex-search-seizure-craig-hemke-april-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

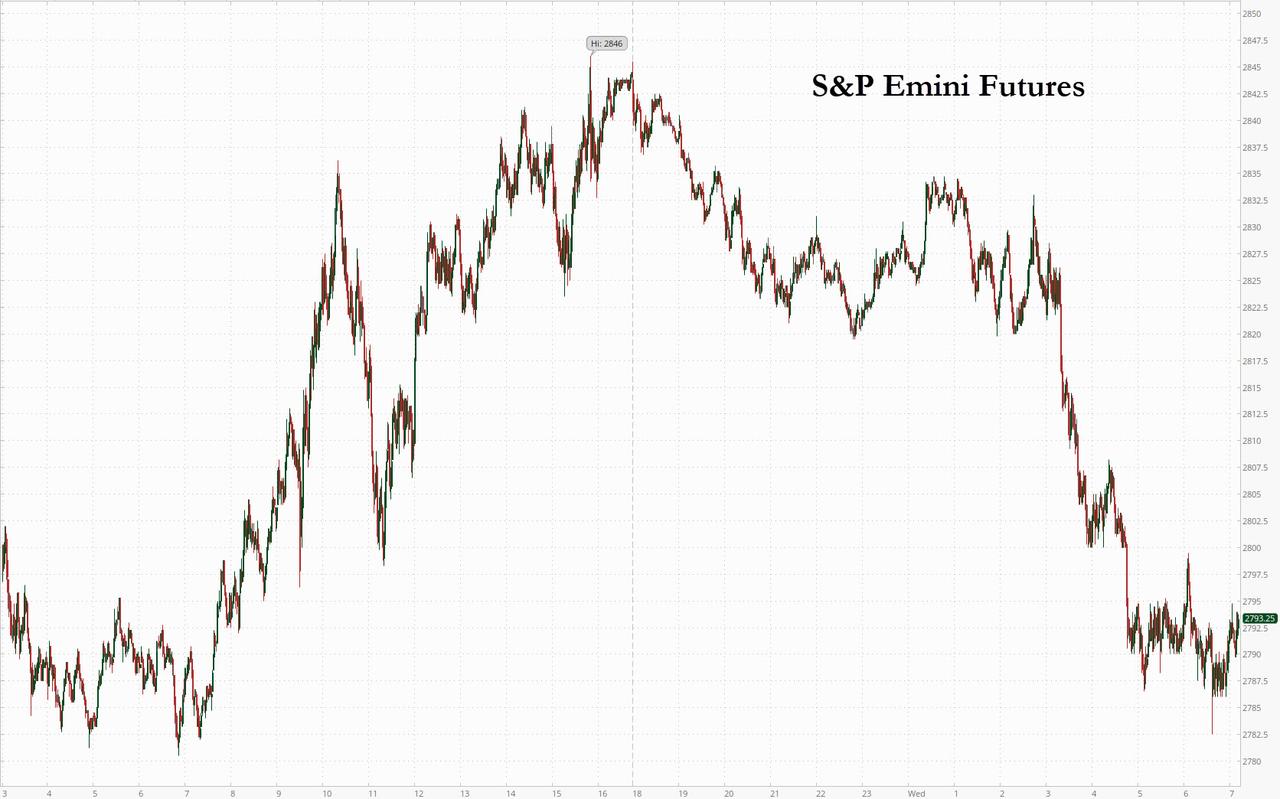

Global Markets Tumble Amid Dismal Earnings After WTI Crashes To 18 Year Low

US index futures slumped on Wednesday for a second time this week, reversing Tuesday’s sharp gains after a plunge in oil prices pressured energy stocks ahead of what is expected to be a dismal round of first-quarter earnings reports. The dollar and Treasuries gained as investors fled risk assets, while WTI crude plunged below $20, to the lowest level since 2002 after the IEA said oil demand will drop by over 9 million barrels a day this year, wiping out a decade of consumption growth.

Contracts on all three major U.S. gauges retreated after the S&P 500 closed at a one-month high on Tuesday, with the Emini trading back under 2,800. UnitedHealth Group, the biggest U.S. health insurer, reported a fall in quarterly profit, but its shares rose 2.6% in premarket trading as it maintained its 2020 profit outlook at a time when major companies have withdrawn forecasts due to the coronavirus pandemic. J.C. Penney slumped 14.7% as sources said the retailer was exploring filing for bankruptcy protection after the virus outbreak upended its turnaround plans.

The S&P 500 index climbed about 30% from its March trough, lifted by a raft of U.S. monetary and fiscal stimulus and on early signs that coronavirus cases were peaking in some hotspots, but is still down about 16% from its record high. The index jumped another 3% on Tuesday on hopes the Trump administration could move to ease lockdowns as the outbreak showed signs of ebbing. However, hotspot New York later sharply raised its official virus death toll to more than 10,000. Oil majors Exxon Mobil Corp and Chevron slipped about 3% as oil prices tumbled, pressured by reports suggesting persistent oversupply and collapsing global demand.

JPMorgan Chase and Wells Fargo kicked off the earnings season on Tuesday by reporting a slump in quarterly profits and setting aside billions of dollars to cover potential loan defaults. Moments ago Bank of America joined them (post coming shortly).

“It’s really going to be about forward guidance,” Erin Gibbs, president and CEO at Gibbs Wealth Management LLC, said on Bloomberg TV. “What we’re really going to be looking for is, are companies giving us an idea of when they think they’ll return to profitability, or, are they talking about more layoffs?”

In Europe, the Stoxx Europe 600 index headed for its first drop in six sessions, led by energy companies, as crude oil in New York fell below $20 a barrel amid a global slump in demand. French shares fell 0.9% as France became the fourth country to report more than 15,000 deaths due to the coronavirus after Italy, Spain and the United States. ASML Holding NV, a supplier to Samsung Electronics Co., reported a 40% drop in first-quarter earnings and refrained from providing guidance amid uncertainty caused by the pandemic. Dutch GPS and digital mapping company TomTom shed 2.7% after saying it expected negative free cash flow this year and lower revenue from its automotive and consumer businesses due to the pandemic. London-based asset manager Jupiter Fund Management dropped 5.6% after reporting an 18.3% drop in assets under management in the first quarter as fears over the pandemic rattled financial markets.

Much economic damage has also already been done, with the International Monetary Fund predicting the world this year would suffer its steepest downturn since the Great Depression of the 1930s. Ahead of a steady stream of results due in the coming weeks, signs of corporate stress caused by the pandemic are widespread.

“A lot of good news has been priced in and we’re due for some consolidation, particularly as we head into earnings season as we all know the numbers will not be good,” Francois Savary, chief investment officer at Swiss wealth manager Prime Partners.

Earlier in the session, Asian stocks fell, led by energy and finance, after rising in the last session. Shares in Tokyo were little changed, Chinese and Hong Kong stocks slipped, with the Shanghai Composite Index retreating 0.6%, with Baotou Huazi Industry and Wuxi Shangji Automation posting the biggest slides. Australian equities dropped as a record slump in consumer confidence reminded investors of the impact of the pandemic on spending. The yuan dipped after China’s central bank eased policy further. Markets in the region were mixed, with Taiwan’s Taiex Index and India’s S&P BSE Sensex Index rising, and Jakarta Composite and Thailand’s SET falling.

European Union and U.S. federal officials are drafting plans to lift restrictions in an effort to mitigate the economic devastation, even as global virus infections edge closer to the 2 million mark. The earnings season should provide a better sense of how the pandemic will affect commerce as the global economy heads for a deep recession. Johnson & Johnson, JPMorgan Chase & Co.and Wells Fargo & Co. offered a mixed picture Tuesday, with Goldman Sachs Group Inc., Citigroup Inc. and Bank of America Corp. next up.

The big overnight mover was WTI, which tumbled fell below $20 a barrel after the International Energy Agency said demand would slump by a record this year despite a historic production cut deal. WTI futures fell as much as 4.5% in New York to the lowest since 2002. Oil demand will drop by over 9 million barrels a day this year, wiping out a decade of consumption growth, the IEA said, exhausting storage by mid-year. While Saudi Arabia and other Gulf producers have pledged to cut supply starting next month, they continue to flood the market in April. Stockpiles are rising everywhere and weakening key physical market gauges. New York oil futures moved deeper into contango, signaling an expanding glut, while swap prices indicate North Sea cargoes are trading at bumper discounts.

The IEA said consumption in April will fall by almost a third to the lowest level since 1995, and make this year the worst in the history of the oil market. Despite OPEC+’s efforts to balance supply, global inventories will accumulate by 12 million barrels a day in the first half of the year and “overwhelm the logistics of the oil industry” in the coming weeks, it warned. The massive OPEC+ deal to cut production starts next month. Until then the battle for market share persists with Abu Dhabi cutting its crude pricing for Asia. It follows a similar move by Saudi Arabia earlier in the week.

In Rates, 10Y Yields dropped as low as 0.67% after trading closing at 0.75% on Tuesday. Italian bonds remained under pressure amid lingering disappointment with the half-a-trillion euro plan to support coronavirus-hit economies agreed by euro zone finance ministers last week. Italy’s 2-year bond yield was last up 5 basis points to 0.89% after rising nearly 20 bps on Tuesday Ten-year yields were flat at 1.79%. The closely watched gap with Germany’s 10-year bond yield, effectively the risk premium Italy pays investors, continued to rise, last at nearly 220 bps, the highest since mid-March.

In FX, the dollar surged after several days of losses, as investors sought safety in the world’s reserve currency amid a wave of risk-off sentiment sweeping across global markets, with commodity currencies tumbling and oil prices sliding below $20 per barrel. The pound fell almost 1%, snapping a two-day advance. The Bloomberg Dollar Spot Index jumps as much as 0.8%, after three days of losses, as European stocks tumbled alongside U.S. equity futures as what is expected to be a turbulent earnings season gets underway. The BBDXY was last up 0.7%, with the dollar outperforming all Group-of-10 currencies; 10-year Treasury yield fell eight basis points to 0.67%.

The Australian dollar tumbled during Asian hours, and the Norwegian krone followed suit as oil prices slid with the International Energy Agency warning that a glut may overwhelm storage despite the recent OPEC deal. It says global oil demand will plunge by a record 9% this year due to coronavirus lockdowns

The pound and euro both fell versus the dollar, with sterling unwinding around half of this week’s rally as the U.K. Office for Budget Responsibility warned that Britain’s economic output could shrink 13% this year. “The combination of weak economic data and cautious corporate earnings outlook could put the latest risk rally to the test and may even help the safe- haven USD,” said Valentin Marinov, a strategist at Credit Agricole. “The rally in commodity currencies is starting to look overextended and could be put to the test in the near term.” Cable fell as much as 1% to $1.2499, though still up around 0.6% this week. EUR/USD declined 0.5% to $1.0931 with the Stoxx Europe 600 index dropping for the first time in five trading days.

Gold prices fell on Wednesday as investors locked in profits after strong recent gains which sent the yellow metal just shy of its 2011 all time high. It was last at $1,721 an ounce.

Expected data include retail sales and industrial production. Bank of America, Citigroup and Goldman Sachs are among companies reporting earnings.

Market Snapshot

- S&P 500 futures down 1.9% to 2,788.75

- STOXX Europe 600 down 1.2% to 329.77

- MXAP down 0.3% to 143.35

- MXAPJ down 0.5% to 460.62

- Nikkei down 0.5% to 19,550.09

- Topix up 0.04% to 1,434.07

- Hang Seng Index down 1.2% to 24,145.34

- Shanghai Composite down 0.6% to 2,811.17

- Sensex up 0.4% to 30,796.51

- Australia S&P/ASX 200 down 0.4% to 5,466.67

- Kospi up 1.7% to 1,857.08

- Brent futures down 4.2% to $28.35/bbl

- Gold spot down 0.8% to $1,713.56

- U.S. Dollar Index up 0.4% to 99.32

- German 10Y yield fell 3.9 bps to -0.416%

- Euro down 0.4% to $1.0935

- Italian 10Y yield rose 19.2 bps to 1.611%

- Spanish 10Y yield fell 0.4 bps to 0.839%

Top Overnight News from Bloomberg

- IEA says oil glut may overwhelm storage despite OPEC+ cut and revised global demand for 2020 to 90.5m b/d, from previous 99.9m

- Germany is set to agree on an extension of nationwide lockdown measures until at least May 3 as the government debates with regional leaders on how to gradually relax restrictions on public life in the coming weeks.

- Spain reported the biggest increase in the number of coronavirus cases in six days on Wednesday, while the daily death toll declined. There were more than 5,000 new infections in the 24 hours through Wednesday, taking the total to 177,633, according to Health Ministry data. The number of fatalities rose by 523 to 18,579, compared to Tuesday’s increase of 637

- The IMF wants policy makers to avoid repeating the Depression-era mistake of ratcheting back budget deficits. Instead, it’s urging them to ramp up fiscal stimulus when the coronavirus contagion starts to abate

Asian equity markets traded cautiously as the region failed to follow through on the optimism seen on Wall St where all major indices posted firm gains as liquidity conditions normalized from the Easter break and after comments from President Trump stoked optimism for the US to re-open its economy soon. Nonetheless, the momentum petered out in Asia trade with ASX 200 (-0.4%) dragged lower by heavy losses in the energy sector after WTI crude prices dipped another 7% and briefly tested the USD 20.00/bbl level on demand concerns and with financials subdued after poor earnings results from their stateside peers. Nikkei 225 (-0.5%) exporters were hampered by the ill-effects of a firmer currency and amid the global production shutdown extensions, while KOSPI remained closed for National Assembly elections which is seen as a referendum for President Moon and the government’s handling of the coronavirus outbreak. Elsewhere, Hang Seng (-1.2%) and Shanghai Comp. (-0.6%) traded rangebound and conformed to the indecisive regional tone despite PBoC’s efforts in which it conducted a CNY 100bln 1-year Medium-term Lending Facility at a reduced rate of 2.95% (Prev. 3.15%), while the first phase of its previously announced 100bps targeted RRR cut took effect today but this was also unsuccessful in spurring momentum. Finally, 10yr JGBs were pressured from the open and proceeded lower before finding support near the 152.00 level, while the BoJ Rinban announcement provided little inspiration with the central bank only in the market for JPY 400bln in up to 3yr maturities.

Top Asian News

- China Adds Cash to Banking System, Cuts Interest Rate on Loans

- India Farm Output Lone Bright Spot in an Economy Set to Shrink

- Albayrak Says Turkey Hasn’t Sought Help From Any Institution

European equities extend on losses seen at the cash open (Euro Stoxx 50 -2.1%), after a similarly (albeit to a lesser extent) handover from Asia, as the positive sentiment all Wall Street U-turned overnight. US equity futures also succumb to the broad risk aversion, with E-Mini S&P and Dow June futures back below the 2800 and 23500 marks respectively heading into more earnings. Back to Europe, bourses see broad-based losses with FTSE 100 (-2.4%) seeing more pronounced downside among the majors as the index is pressured by its large-cap Energy, Financial and Material names – three sectors which see steep losses in Europe, with the former the laggard amid price action in the energy complex. Similarly, financials suffer amid the lower yield environment and materials fall due to declines across the base metals. The sectors also clearly reflect risk aversion, as defensive fare considerably better than the cyclicals. In terms of the sector breakdown, Oil & Gas reside at the bottom, followed by the Travel & Leisure as lockdowns across some countries are set to be extended. In terms of individual movers. ASML (-1.8%) conformed to the decline in the region after opening higher post-earnings, in which its revenue and net printed relatively in-line with estimates, whilst suspending its Q2 buybacks but keeping its three-year programme intact. The CEO also noted that demand outlook is currently unchanged, and the group has not encountered any pushouts or cancellations this year, the group’s order intake remains strong. Sticking with earnings, TomTom (-7.3%) sees hefty losses amid dismal earnings after missing on all its company compiled estimates, withdrawing guidance and suspending share buybacks indefinitely. Finally, Adidas (-1.9%) received approval for a syndicated EUR 3bln loan from KFW contingent on a suspension of dividends.

Top European News

- Germany Likely to Extend National Lockdown Measures Until May 3

- Germany Mulls Easing Curbs as Europe’s Virus Struggle Progresses

- Energy Shares Drag European Stocks Lower After Five- Day Rally

- Swedish Debt Plan Triggers Backlash as Fiscal Hawks Under Attack

In FX, tthe Dollar was already clawing back losses across the board, but in particular relative to high beta and commodity based counterparts as Gold lost its lustre above Usd 1750/oz, but a more pronounced pull-back in crude prices following a bearish IEA monthly report gave the Greenback an extra fillip with the DXY back within striking distance of 99.500 compared to 98.828 lows. However, the index may encounter some technical resistance around recent recovery highs and run in to fundamental hurdles given bleak forecasts for upcoming US retail sales and ip data, not to mention the downside bias vs consensus.

- AUD/NZD/CAD/NOK/RUB/MXN – Aside from renewed risk aversion fuelled by the aforementioned about-turn in oil and metals, the Aussie has been undermined independently by a sharp deterioration in consumer sentiment per Westpac’s April survey, while the Kiwi is down in sympathy even though the Aud/Nzd cross has reversed from circa 1.0570 towards 1.0500. Aud/Usd got tantalisingly close to a hefty 1 bn 0.6450 option expiry at one stage, but now appears more inclined to hit 0.6300 and Nzd/Usd is even nearer 0.6000 from 0.6100+ overnight. Elsewhere, the Loonie is back below 1.4000 vs 1.3876 and still nervous ahead of the BoC, Eur/Nok is hovering just shy of 11.5000, Usd/Rub is pivoting 74.0000 and Usd/Mxn is paring back following a marginal breach of 23.9800.

- GBP/EUR/CHF/JPY – Also victims of the Buck’s broad revival, but to varying degrees as Cable reverses from 1.2630 to test 1.2500 and the Euro wanes 10 pips or so before 1.1000 to 1.0920, though not far enough to disturb decent expiry interest between 1.0890-1.0900 (1.3 bn). However, Eur/Usd may lose more momentum on a closing basis if the pair cannot reclaim 1.0950 and a Fib level just above, while the Pound will be eyeing the resumption of Brexit trade negotiations with the EU. Turning to the Franc, gains vs the Dollar have been eroded within a 0.9597-0.9648 range, but not against the single currency as prior support around 1.0550 seems to be morphing into a Eur/Chf cap. Similarly, the Yen has retained a solid safe-haven premium in cross terms, but Usd/Jpy failed to extend through 107.00 and subsequently rebounded to 107.50 or so amidst reports of fresh long positions being instigated on trading platforms.

- SEK/EM – Firmer than expected Swedish CPI metrics have helped the Swedish Krona evade much of the general risk-off positioning, but no such luck for Lira or Rand with the latter succumbing to further heavy post-SARB rate cut depreciation in wake of the SA Government supposedly reneging on wage deals according to the PSU.

In commodities, WTI and Brent futures gave up gains early-doors having had somewhat of a rangebound APAC session. Desks argue that participants are realizing that the OPEC+ cuts are not going to balance the markets over Q2, whilst cuts outside the group are more likely to be market-driven, thus the curtailments are to be gradual as opposed to immediate. Elsewhere, the oil and gas regulator in Texas – the Texas Railroad Commission – voiced disagreement on whether mandated cuts should be implemented. Bigger producers largely opted for market-driven declines whilst the smaller players supported cuts. Whilst the situation in Texas will be followed, Oklahoma are to conduct a meeting on 11th May to discuss mandated output curbs. Prices saw renewed pressure upon the release of the IEA Monthly Oil Market Report which stated that global oil demand is set to fall by a record 9.3mln BPD in 2020. Both the EIA and IEA unsurprisingly cut world oil demand outlook, although the latter by a considerably larger amount than the former, which forecasts a fall of 5.6mln BPD this year. The Agency also stated that it can reach SPR purchases of 200mln BPD over the next three months – a longer timeframe than the touted 2 months by the Saudi Energy Minister. The report also echoed some recent comments from IEA Chief Birol, stating that no feasible agreement could cut supply by enough to offset the near-term decline in demand. The OPEC Monthly report is set to be released on April 16th; participants will be on the lookout for synchrony among the three reports. Meanwhile, the weekly Private Inventories added further fuel to the bearish bias after printing a larger-than-expected build of 13.1mln vs. Exp. +11.7mln. WTI and Brent prices saw a fresh bout of weakness which coincided with the IEA report, with the former hitting levels last seen in 2002. WTI resides below USD 20/bbl and printed a current base at around USD 19.15/bbl. Brent front-month dipped below USD 28/bbl amid the concoction of bearish factors. Over in the metals complex, spot gold succumbs to a firmer Dollar alongside potential retracement of its recent rally, with prices closer to USD 1700/oz, having risen to a whisker away from USD 1750/oz (USD 1747/oz at best) in the prior session. Separately, Copper prices are under pressure from USD action alongside the risk aversion seen across the market. The red metal still resides above USD 2.25/lb having waned off overnight highs of USD 2.34/lb.

US Event Calendar

- 8:30am: Retail Sales Advance MoM, est. -8.0%, prior -0.5%

- Retail Sales Ex Auto MoM, est. -5.0%, prior -0.4%;

- Retail Sales Ex Auto and Gas, est. -5.2%, prior -0.2%

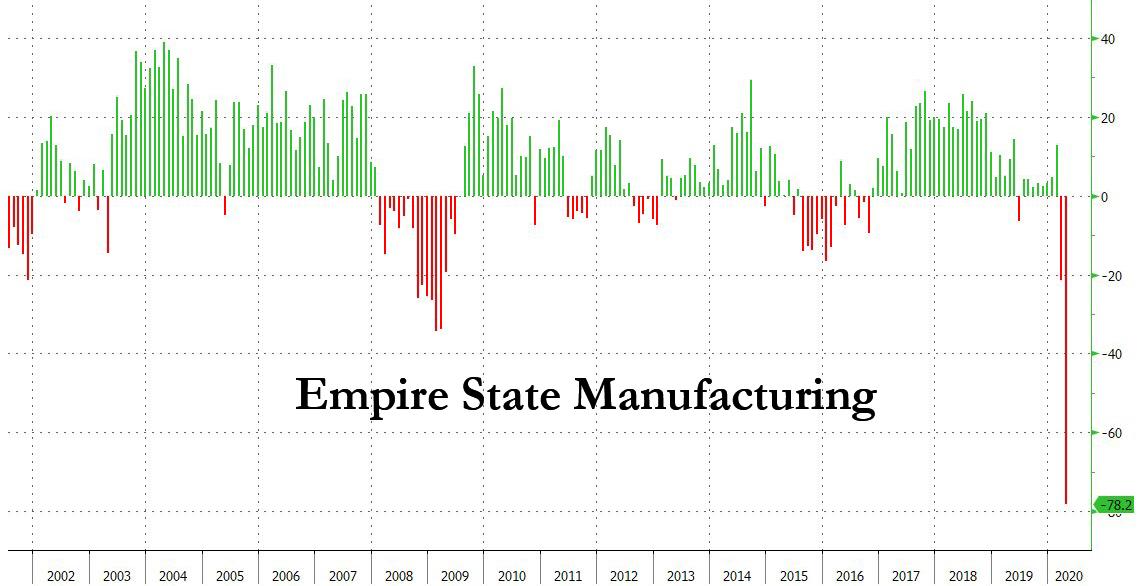

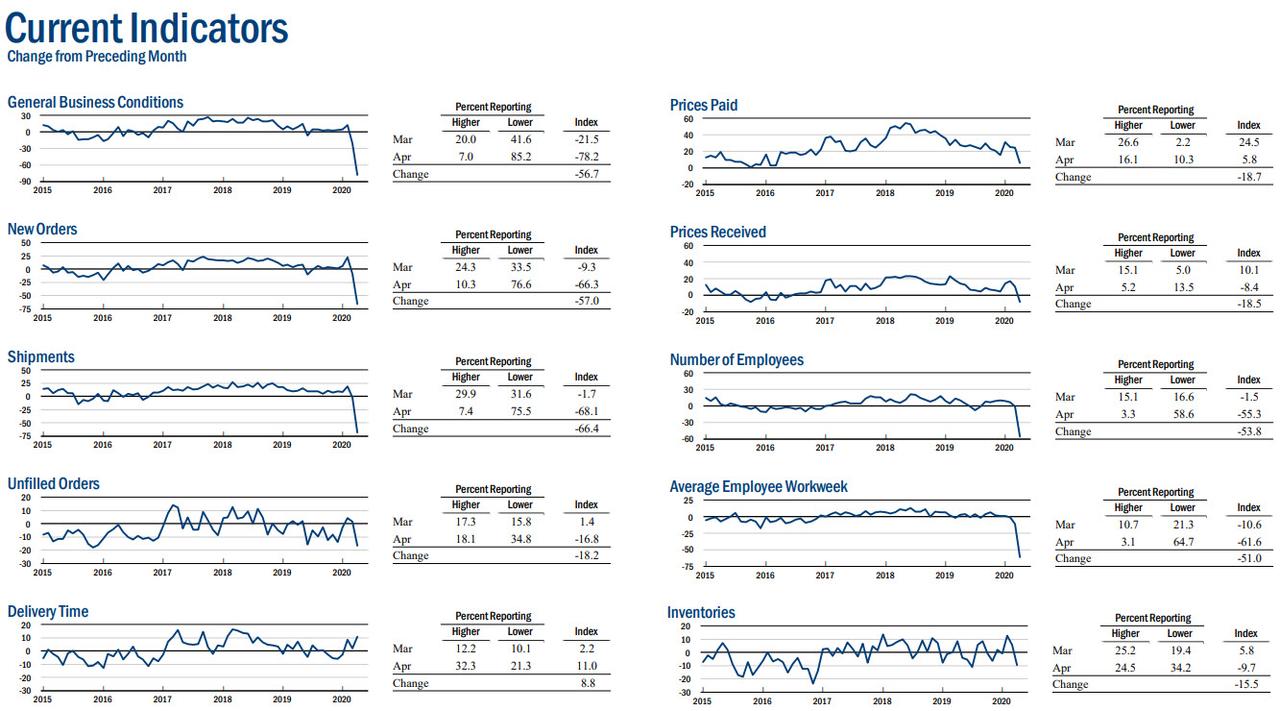

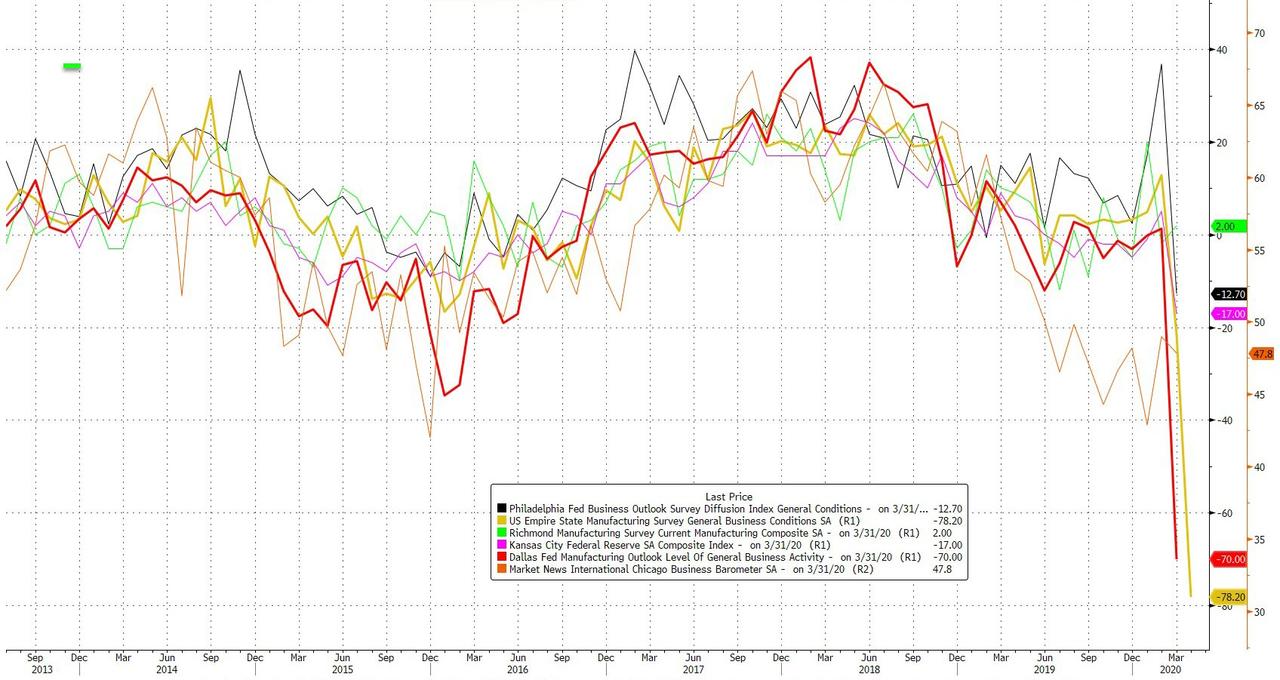

- 8:30am: Empire Manufacturing, est. -35, prior -21.5

- 9:15am: Industrial Production MoM, est. -4.0%, prior 0.6%; Capacity Utilization, est. 74.0%, prior 77.0%

- 10am: Business Inventories, est. -0.4%, prior -0.1%

- 10am: NAHB Housing Market Index, est. 55, prior 72

- 2pm: U.S. Federal Reserve Releases Beige Book

- 4pm: Net Long-term TIC Flows, prior $20.9b; Total Net TIC Flows, prior $122.9b

DB’s Jim Reid concludes the overnight wrap

Global equity markets advanced further yesterday as the market decided that flattening new case and fatality growth rates pretty much everywhere across the developed world is more important at the moment than working out how successful the exit strategies will be and how protracted the economic impact will be. Equities also liked comments from White House economic adviser Kudlow suggesting Mr Trump will make some “important announcements” over the next few days regarding state guidelines on reopening the economies even if Director of the National Institute of Allergy and Infectious Diseases, Anthony Fauci, said that a May 1 target to reopen is “a bit overly optimistic” for many areas of the country.

Overall it feels like we’re pricing in closer to a “V-shaped” recovery at the moment but it’s clearly difficult to disentangle the impact that the extraordinary support from the authorities is having. The Fed’s kitchen sink is still reverberating around markets. All is not well everywhere though as Italy and Oil had a bad day yesterday as we’ll touch on below.

The very latest on the coronavirus shows the growth rate of both new cases and fatalities over the past 24 hours were the lowest since the first week of March, before the outbreaks had really spread around Europe or the US. Global cases rose by 3.1% or by just over 60,000 cases to just shy of 2 million. Meanwhile fatalities rose by 5.8% or nearly 6,890 people globally, meaning the number of people confirmed to have passed away from Covid-19 now sits at 126,557. For more see our Corona Crisis Daily.

The S&P 500 ended the session up a further +3.06% to put it +27.20% above its closing low back on March 23rd. Meanwhile the VIX index of volatility continued to decline, falling for the 7th time in the last 8 sessions as it reached its lowest level in over 5 weeks (at 37.89). Over in Europe, the STOXX 600 (+0.61%) also nearly made it into bull market territory as well, before giving up some of its gains at the end of the session to put it up +19.40% since its own closing low on March 18th.

The moves higher for equities came as earnings season saw a number of companies report even if there was some mixed results. JPMorgan Chase reported that net income was $2.9bn, down 69% on the same quarter a year ago, with an $8.3bn provision for credit losses, up from just $1.5bn a year ago. Total trading revenues were +32% on Q1 2019, which beat investor day guidance of up mid-teens. The stock was -3.17% as bank stocks broadly were sold (S&P 500 Bank Industry group down -2.22%) in favour of Technology and Consumer stocks (both over +4%) for the second day in a row. Over at Wells Fargo (-4.40%), net income was $653m, down from $5.9bn in Q1 2019, while their own provision expense for credit losses was $4.0bn. Meanwhile Johnson & Johnson (+4.02%) lowered their 2020 guidance, now seeing full-year operational sales of $79.2-$82.2bn, down from $85.8-86.6bn back in January, but increased their dividend. The increased dividend and comments around a possible coronavirus vaccine saw sentiment in the stock improve even as guidance was cut. They are aiming to have a single-dose vaccine available for broad use early in 2021, and also is testing two backup vaccine candidates. They aim to produce 600 to 800 million doses in the first half of next year alone according to comments released after their earnings announcement. Today the main earnings highlights will be from UnitedHealth Group, Bank of America, ASML, Citigroup and Goldman Sachs.

Markets in Asia have been a bit less enthusiastic with most major bourses close to flat this morning. That includes the Nikkei (+0.07%), Hang Seng (-0.11%) and Shanghai Comp (-0.15%) while the ASX is down a steeper (-1.08%). In currencies, the Australian dollar is down -0.50% following data that showed Australia’s household sentiment fell to 75.6 in April (from 91.9 in last month), the biggest fall in the 47-year history of the survey. In commodities, Brent crude oil prices are up +1.28% this morning while most base metals are also trading up with iron ore +0.83%.

Overnight, China added another drip of stimulus to its economy with the PBoC injecting CNY 100bn via the one-year medium-term lending facility in to the economy at a rate of 2.95% vs 3.15% previously. The operation comes ahead of CNY 200bn of loans maturing on Friday.

In other news, the Washington Post is reporting that Federal health officials have begun drafting plans to end social-distancing measures and reopen businesses called the “Framework for Reopening America”. The document describes a phased program that would split the country into areas based on risk, with low-, moderate- and high-risk sections. Low-risk areas could open first, no earlier than May 1, with moderate- and high-risk areas later. The report added that the document says that none of the steps should be taken until widespread testing capabilities are in place. Futures on the S&P 500 are trading down -0.51% this morning.

Prior to this, President Trump announced during his press briefing yesterday that he would be instructing his administration to stop all funding for the World Health Organization on the basis that the body should not have taken China’s data at “face value” and that they failed to share information on the coronavirus early enough. According to WHO, the US has given $893 million to the organization in the current 2-year funding cycle.

Sticking with the US, after the market closed yesterday major US airlines and the Treasury reached an initial agreement on the aid that the government votes on in the recently passed fiscal stimulus bill. There is a total of $25billion in payroll assistance being allocated across all major airlines. Airlines that agreed to participate also included Alaska Air Group, Delta Air Lines, JetBlue Airways, United Airlines Holdings, Allegiant Airlines, Frontier Airlines, Hawaiian Airlines and SkyWest. Further, American Airlines Group and Delta Airlines said overnight that they will get $5.8bn and $5.4bn in support respectively. That accounts to almost 45% of the agreed assistance. Delta Chief Executive Officer Ed Bastian said in a message to employees that “The funding, along with self-help measures we have taken, will prevent furloughs and pay rate reductions through the end of September, despite the 95% drop we’ve seen in passenger traffic.” Shares of American Airlines (+10.7%), Delta (+9.29%) and JetBlue (+16%) are all up in afterhours trade along with those of other carriers.