GOLD:$1685.60 DOWN $27.80 The quote is London spot price

Silver: $15.16//DOWN 24 CENTS

The quote is London spot price

Closing access prices: London spot

i)Gold : $1685.00 LONDON SPOT 4:30 pm

ii)SILVER: $15.16//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

APRIL comex gold price CLOSE 1.30 PM: $1718.50

MAY COMEX GOLD: 1725.20 1:30 PM

JUNE GOLD: $1735.10 CLOSE 1.30 PM// SPREAD SPOT/FUTURE JUNE: $21.10

CLOSING SILVER FUTURE MONTH

SILVER APRIL COMEX CLOSE: 15.42/

SILVER MAY COMEX CLOSE; $15.60-…1:30 PM.//SPREAD SPOT/FUTURE MAY: 20 CENTS PER OZ

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2600. usa per oz

and silver; $31.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

DO NOT PAY ANY ATTENTION TO WHAT THE CROOKS ARE DOING AT THE COMEX AND LONDON LBMA..PHYSICAL IS THE NAME OF THE GAME AND NOTHING ELSE

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 3/80

issued 0

EXCHANGE: COMEX

CONTRACT: APRIL 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,720.400000000 USD

INTENT DATE: 04/16/2020 DELIVERY DATE: 04/20/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

099 H DB AG 55

132 C SG AMERICAS 8 2

657 C MORGAN STANLEY 1

657 H MORGAN STANLEY 72

661 C JP MORGAN 3

686 C INTL FCSTONE 13

690 C ABN AMRO 2

737 C ADVANTAGE 1

905 C ADM 3

____________________________________________________________________________________________

TOTAL: 80 80

MONTH TO DATE: 29,635

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 80 NOTICE(S) FOR 8,000 OZ (0.2488 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 29,635 NOTICES FOR 2,963,500 OZ (92.177 TONNES)

SILVER

FOR APRIL

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 806 for 4,025,000 oz

BITCOIN MORNING QUOTE $7074 DOWN 25

BITCOIN AFTERNOON QUOTE.: $7057 DOWN $45

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $27.80: AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

SURPRISINGLY NO GOLD LEAVES THE GLD//

GLD: 1,021.69 TONNES OF GOLD//

WITH SILVER DOWN 24 CENTS TODAY: AND WITH NO SILVER AROUND

A WITHDRAWALS OF 1.3999 MILLION OZ/

RESTING SLV INVENTORY TONIGHT:

SLV: 414.038 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A GOOD SIZED 751 CONTRACTS FROM 140,358 UP TO 141,102 AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE GOOD SIZED GAIN IN OI OCCURRED WITH OUR STRONG 24 CENT GAIN IN SILVER PRICING AT THE COMEX. WE HAD ZERO LONG LIQUIDATION. IT SEEMS THAT THE GAIN IN COMEX OI IS DUE TO SOME BANKER SHORT COVERING PLUS A CONSIDERABLE EXCHANGE FOR PHYSICAL ISSUANCE ALONG WITH A ZERO GAIN IN SILVER OZ STANDING. WE HAD A GOOD NET GAIN IN OUR TWO EXCHANGES OF 1781 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A STRONG AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: MARCH: 00 AND MAY: 1030 AND JULY: 0 ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1030 CONTRACTS. WITH THE TRANSFER OF 1030 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1030 EFP CONTRACTS TRANSLATES INTO 5.150 MILLION OZ ACCOMPANYING:

1.THE 24 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.145 MILLION OZ INITIALLY STANDING FOR APRIL

FRIDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL 24 CENTS).. AND, OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE SOME SILVER LONGS FROM THEIR POSITIONS, AS WE DID HAVE A GOOD NET GAIN OF 1781 CONTRACTS OR 8.905 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

OUR SPREADING OPERATION HAS NOW SWITCHED INTO SILVER…..

SPREADING OPERATION FOR OUR NEWCOMERS:

WE HAVE NOW COMMENCED IN SILVER THE ILLEGAL SPREADING OPERATION \ FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW STOPPED IN GOLD AS THEY NOW BEGIN TO MORPH INTO SILVER AS WE HEAD TOWARDS THE NEW FRONT MONTH WILL BE MAY.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF APRIL. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

12,837 CONTRACTS (FOR 12 TRADING DAYS TOTAL 12,837 CONTRACTS) OR 64.185 MILLION OZ: (AVERAGE PER DAY: 1167 CONTRACTS OR 5.684 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF APRIL: 64.185 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 9.16% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 957.68 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP SO FAR 64.185 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 751, WITH THE CONSIDERABLE 24 CENT FALL IN SILVER PRICING AT THE COMEX /FRIDAY… THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1030 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A GOOD SIZED OI CONTRACTS ON THE TWO EXCHANGES: 1781 CONTRACTS (WITH OUR 5 CENT GAIN IN PRICE)

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 1030 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 751 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 5 CENT GAIN IN PRICE OF SILVER/ AND A CLOSING PRICE OF $15.16 // THURSDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.7050 BILLION OZ TO BE EXACT or 100.7% of annual global silver production (ex Russia & ex China).

FOR THE NEW MAR DELIVERY MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR nil OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.145 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A TINY SIZED 417 CONTRACTS TO 491,454 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE LOSS OF COMEX OI OCCURRED WITH OUR COMEX LOSS IN PRICE OF $27.80 /// COMEX GOLD TRADING// FRIDAY// WE HAD CONSIDERABLE BANKER SHORT COVERING ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A GOOD EX. FOR PHYSICAL ISSUANCE AND THIS WAS COUPLED WITH OUR LOSS IN THE PAPER PRICE OF GOLD.

WE HAD NO ISSUANCE OF OUR NEW 4 GC CONTRACT

WE GAINED A GOOD 1799 CONTRACTS (5.59 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2216 CONTRACTS:

CONTRACTS, FEB> 0 CONTRACTS; MARCH 00 APRIL: 0. MAY: 0, AND JUNE 2216.; DEC 0 AND ALL OTHER MONTHS ZERO//TOTAL: 2216. The NEW COMEX OI for the gold complex rests at 491,454. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1799 CONTRACTS: 417 CONTRACTS DECREASED AT THE COMEX AND 2216 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 1852 CONTRACTS OR 5.59 TONNES. THURSDAY, WE HAD HUGE LOSS OF $27.80 IN GOLD TRADING.…..

AND WITH THAT LOSS IN PRICE, WE HAD A GOOD SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 5.59 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (FELL $27.80). AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WERE UNSUCCESSFUL (SEE BELOW).

4 GC ISSUANCE: ZERO

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A GOOD SIZED INCREASE IN EXCHANGE FOR PHYSICALS (2216) ACCOMPANYING THE TINY LOSS IN COMEX OI (417 OI): TOTAL GAIN IN THE TWO EXCHANGES: 1799 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)A STRONG INCREASE IN STANDING AT THE GOLD COMEX FOR THE FRONT APRIL MONTH, 3) ZERO LONG LIQUIDATION AND …ALL OF THIS WAS COUPLED WITH THAT LOSS IN GOLD PRICE TRADING//FRIDAY

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 53,906 CONTRACTS OR 5,390,600 oz OR 167.67 TONNES (12 TRADING DAYS AND THUS AVERAGING: 4900 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES: 167.67 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 167.67/3550 x 100% TONNES =4.72% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 2490.57 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 167.67 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GOOD SIZED 751 CONTRACTS FROM 140,351 UP TO 141,102 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

ALL OF THE LOSS IN COMEX OI WAS DUE TO 1) SOME BANKER SHORT COVERING , 2) THE ISSUANCE OF A GOOD SIZED NUMBER OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A ZERO INCREASE IN SILVER OZ STANDING AT THE COMEX FOR APRIL AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 1030 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR FEB. 0; FOR MAR 0: AND MAY: 1030; JULY: 00 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1030 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE GOOD COMEX OI GAIN OF 751 CONTRACTS TO THE 1030 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD GAIN OF 1827 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 8.9055 MILLION OZ!!! AND WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ// SEPT: 43.030 MILLION OZ///OCT: 7.32 MILLION OZ//NOV 2.63 MILLION OZ//DEC: 20.970 MILLION OZ//JAN: 5.075 MILLION OZ//FEB: 1.480 MILLION OZ//MAR: 23.005 MILLION OZ//APRIL 4.145 MILLION OZ//

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 24 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// FRIDAY. WE ALSO HAD A STRONG SIZED 1030 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 18.56 POINTS OR 0.66% //Hang Sang CLOSED UP 373,55 POINTS OR 1.56% /The Nikkei closed UP 607.06 POINTS OR 3.15%//Australia’s all ordinaires CLOSED UP 1.41%

/Chinese yuan (ONSHORE) closed DOWN at 67.0740 /Oil UP TO 18.35 dollars per barrel for WTI and 28.47 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0740 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0787 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: 0 oz

total dealer withdrawals: 0 oz

i)we had 1 deposits into the customer account

into JPMorgan: 0

ii)into CNT; 625,592.490 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.819 million oz of total silver inventory or 50.04% of all official comex silver. (160.819 million/321.170 million

total customer deposits today: 625,592.490 oz

we had 3 withdrawals:

total withdrawals; 801,847.613 oz

We had 1 adjustments: and all from the dealer to the customer:

i) From CNT 5111,800 oz from dealer to customer

total dealer silver: 81.788 million

total dealer + customer silver: 317.926 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The total number of notices filed today for the APRIL 2020. contract month is represented by 0 contract(s) FOR nil oz

To calculate the number of silver ounces that will stand for delivery in APRIL we take the total number of notices filed for the month so far at 806 x 5,000 oz = 4,025,000 oz to which we add the difference between the open interest for the front month of APRIL.(23) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL/2019 contract month: 806 (notices served so far) x 5000 oz + OI for front month of APRIL (23)- number of notices served upon today (0) x 5000 oz of silver standing for the APRIL contract month.equals 4,145,000 oz.

WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ OF SILVER WILL STAND AT THE COMEX.

TODAY’S ESTIMATED SILVER VOLUME: 49,396 CONTRACTS //

FOR YESTERDAY: 55,840 CONTRACTS..,CONFIRMED VOLUME

YESTERDAY’S CONFIRMED VOLUME OF 55,840 CONTRACTS EQUATES to 279 million OZ 39.8% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO +0.86% ((APRIL 17/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO +0.51% to NAV: (APRIL 17/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into POSITIVE/ 0.86%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.45 TRADING 15.37///DISCOUNT 0.31

END

And now the Gold inventory at the GLD/

APRIL 17/WITH GOLD DOWN $27.80 TODAY: SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT XXX TONNES..THE STRING OF 12 STRAIGHT STRONG DEPOSITS ENDS..

APRIL 16/WITH GOLD DOWN $4.50 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG DEPOSIT OF 4.10 TONNES WAS ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 1021.69 TONNES/12TH STRAIGHT STRONG DEPOSIT

APRIL 15//WITH GOLD DOWN $19.10 TODAY; ANOTHER HUGE CHANGE IN GOLD INVENTORY; A STRONG 7.89 TONNES WAS ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 1117.59 TONNES.//11TH STRAIGHT STRONG DEPOSIT

APRIL 14/WITH GOLD UP $23.55 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 15.51 TONNES WAS ADDED TO THE GLD INVENTORY/INVENTORY RESTS AT 1009.70 TONNES//THIS IS THE 10TH STRAIGHT STRONG DEPOSIT//THIS IS A FRAUDULENT VEHICLE..THEY HAVE NO PHYSICAL GOLD IN THE TRUST..

APRIL 13//WITH GOLD UP $27.65 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 5.36 TONNES WAS ADDED TO THE GLD//INVENTORY RESTS AT 994.19 TONNES

APRIL 9 WITH GOLD UP $37.30 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 2.92 TONNES WAS ADDED TO THE GLD//GOLD INVENTORY RESTS TONIGHT AT..988.63 TONNES

APRIL 8/WITH GOLD DOWN $.60//ANOTHER HUGE CHANGE IN GOLD INVENTORY/;; A STRONG 1.45 TONNES WAS ADDED TO THE GLD/GOLD INVENTORY RESTS AT 985.71 TONNES

APRIL 7/WITH GOLD UP $.30: ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.27 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 984.26 TONNES

APRIL 6//WITH GOLD UP $32.00//ANOTHER STRONG DEPOSIT INTO THE GLD; A HUGE 7.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT : 978.99 TONNES

APRIL 3//WITH GOLD UP $7.80 TODAY//ANOTHER STRONG DEPOSIT OF 3.22 TONNES INTO THE GLD/INVENTORY RESTS AT 971.97 TONNES

APRIL 2//WITH GOLD UP $31.80 TODAY: ANOTHER STRONG DEPOSIT OF 1.75 TONNES INTO THE GLD//INVENTORY RESTS AT 968.75 TONNES

APRIL 1/WITH GOLD DOWN $7.70 TODAY: ANOTHER CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.62 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 967.00 TONNES

MARCH 31//WITH GOLD DOWN $32.70//A MONSTROUS PAPER DEPOSIT OF 10.84 TONNES INTO THE GLD//INVENTORY RESTS AT 964.38 TONNES

MARCH 30/WITH GOLD DOWN $6.10 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 953.54 TONNES

MARCH 27.WITH GOLD DOWN $16.40: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A HUGE DEPOSIT OF 4.39 TONES INTO THE GLD/INVENTORY RESTS AT 953.54 TONES

MARCH 26//WITH GOLD UP $24.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 13.17 TONNES INTO THE GLD/INVENTORY RESTS AT 949.15 TONNES

MARCH 25/WITH GOLD DOWN $11.40 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.99 TONES INTO THE GLD INVENTORY////INVENTORY RESTS AT 935.98 TONNES

MARCH 24//WITH GOLD UP $67.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 15.80 TONNES OF GOLD INTO GLD////INVENTORY RESTS AT 923.99 TONNES..THIS PROVES THAT THE GLD IS A FRAUD AS LONDON SUSPENDED DELIVERY AS WELL AS ALL REFINERS. THEY HAD NO WAY OF GETTING ANY PHYSICAL OZ INTO ITS INVENTORY//

MARCH 23//WITH GOLD UP $76.00 TODAY: A HUGE PAPER WITHDRAWAL OF 21.50 TONNES FROM THE GLD////INVENTORY RESTS AT 908.19 TONNES

MARCH 20//WITH GOLD UP $5.50//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 7.46 TONNES FROM THE GLD////INVENTORY RESTS AT 922.23 TONNES

MARCH 19/WITH GOLD DOWN 90 CENTS: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 929.84 TONNES

MARCH 18/WITH GOLD DOWN $48.00: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 929.84 TONNES

MARCH 17/WITH GOLD UP $37.60: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM GLD INVENTORY//INVENTORY RESTS AT 929.84 TONNES

MARCH 16/WITH GOLD DOWN $30.00/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 12.59 TONNES/INVENTORY RESTS AT 931.59 TONNES

MARCH 13//WITH GOLD DOWN $73.60: A HUGE WITHDRAWAL OF 9.02 TONNES OF PAPER GOLD FROM THE GLD//

INVENTORY RESTS AT 944.18 TONNES

MARCH 12/WITH GOLD DOWN $55.05 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/953.26 TONNES

MAR 11/WITH GOLD DOWN $14.95?/A HUGE WITHDRAWAL OF 10.53 TONNES//INVENTORY RESTS AT 953.26 TONNES

MARCH 10/WITH GOLD DOWN $14.25//A HUGE 8.00 TONNES OF PAPER GOLD DEPOSIT INTO THE GLD//INVENTORY RESTS AT 963.79

MARCH 9//WITH GOLD UP $1.50 : NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 955.60 TONNES

March 6/WITH GOLD UP $6.25 A MASSIVE 21.37 PAPER TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 955.60 TONNES

MARCH 5/WITH GOLD UP $25.40//NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS TONIGHT AT 934.23 TONNES

MARCH 4//WITH GOLD DOWN 1 DOLLAR: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.23 TONNES//

MARCH 3//WITH GOLD UP 48.55 TODAY; NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.23 TONNES

MARCH 2//WITH GOLD UP $27.00// no change in gold inventory at the gld//inventory remains at 934.23 tonnes

FEB 28/WITH GOLD DOWN $73.00 WE LOST NO GOLD FROM THE GLD/INVENTORY REMAINS 934.23 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

APRIL 17/2020/ 1021.69 tonnes*

IN LAST 801 TRADING DAYS: +75.35 NET TONNES HAVE BEEN REMOVED FROM THE GLD

LAST 701 TRADING DAYS;+250.33 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

APRIL 17/WITH SILVER DOWN 24 CENTS TODAY; A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.3999 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 16/WITH SILVER UP 5 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 15//WITH SILVER DOWN 45 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV TWO HUGE DEPOSITS: A DEPOSIT OF 1.679 MILLION OZ AND ANOTHER 5.222 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 14./WITH SILVER UP 51 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A MASSIVE PAPER DEPOSIT OF XXX MILLION OZ//INVENTORY RESTS AT 408.536 MILLION OZ//

APRIL 13//WITH SILVER DOWN 29 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 6.155 MILLION OZ////INVENTORY RESTS AT 408.536 MILLION OZ//

APRIL 9/WITH SILVER UP 60 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUGE DEPOSIT OF 1.84 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 402.381 MILLION OZ.

APRIL 8//WITH SILVER DOWN 21 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 401.541 MILLION OZ///

APRIL 7/WITH SILVER UP 26 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.766 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 395.826 MILLION OZ

APRIL 6/WITH SILVER UP 50 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 395.826 MILLION OZ.

APRIL 3//WITH SILVER DOWN 15 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 746,000 OZ INTO THE SLV//INVENTORY RESTS AT 395.826 MILLION OZ

APRIL 2/WITH SILVER UP 65 CENTS; A SMALL CHANGE TODAY..A WITHDRAWAL OF .335 MILLION OZ TO PAY FOR FEES//INVENTORY RESTS AT 394.826 MILLION OZ/

APRIL 1/WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 395.181 MILLION OZ//

MARCH 31/WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 1.679 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 375.181 MILLION OZ//

MARCH 30/WITH SILVER DOWN 44 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 393.502 MILLION OZ.

MARCH 27/WITH SILVER DOWN 5 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTROUS PAPER DEPOSIT OF 8.115 MILLION OZ INTO THE SLV../INVENTORY RESTS AT 393.502 MILLION OZ//

MARCH 26/WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 385.387 MILLION OZ///

MARCH 25/WITH SILVER UP 44 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSITS OF 7.369 MILLION OZ AND 2.239 MILLION OZ OF PAPER SILVER INTO THE SLV////INVENTORY RESTS AT 385.387 MILLION OZ//

MARCH 24//WITH SILVER UP 100 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 375.779 MILLION OZ///

MARCH 23//WITH SILVER UP 70 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.332 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 375.779 MILLION OZ

MARCH 20//WITH SILVER UP 39 CENTS TODAY: 2 HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A PAPER WITHDRAWAL OF 1.026 MILLION OZ FROM THE SLV AND THEN A PAPER ADDITION OF 3.638 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 373.447 MILLION OZ//

MARCH 19/WITH SILVER UP 38 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: ANOTHER 5.597 MILLION OZ OF SILVER VAPOUR ADDED TO THE SLV INVENTORY//INVENTORY RESTS AT 370.835 MILLION OZ/

MARCH 18//WITH SILVER DOWN 75 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTROUS 12.035 MILLION PAPER OZ ADDED INTO INVENTORY//INVENTORY RESTS AT 365.238 MILLION OZ//

MARCH 17/WITH SILVER DOWN 20 CENTS TODAY; A BIG CHANGES IN SILVER INVENTORY AT THE SLV; A WITHDRAWAL OF 3.735 MILLION OZ FROM THE SLV INVENTORY: INVENTORY RESTS AT 353.203 MILLION OZ///

MARCH 16/WITH SILVER DOWN 177 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESETS AT 356.938 MILLION OZ//

MARCH 13//WITH SILVER DOWN 155 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.893 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 356.938 MILLION OZ;

MARCH 12/WITH SILVER DOWN 77 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.119 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 359.828 MILLION OZ

MARCH 11/SILVER DOWN 16 CENTS: A SMALL WITHDRAWAL OF .467 MILLION OZ AT THE SLV/INVENTORY RESTS AT 360.947 MILLION OZ//

MARCH 10/WITH SILVER DOWN 10 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 361.414 MILLION OZ//

MARCH 9/NO CHANGE IN INVENTORY LEVELS: SLV INVENTORY RESTS AT 361.414 MILLION OZ//

MARCH 6//WITH SILVER DOWN 10 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 361.414 MILLION OZ

MARCH 5//WITH SILVER UP 15 CENTS TODAY; A SMALL WITHDRAWAL DUE TO FEES ETC//INVENTORY RESTS TONIGHT AT 361.414 MILLION OZ..

MARCH 4/SILVER SILVER UP 3 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 361.880 MILLION OZ//

MARCH 3/WITH SILVER UP 44 CENTS//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: A LOSS OF 5.75 MILLION OZ FROM THE SLV../INVENTORY RESTS AT 361.880 MILLION OZ

MARCH 2//WITH SILVER UP 18 CENTS//NO CHANGE IN SILVER INVENTORY AT THE SLV..INVENTORY RESTS AT 367.632 MILLION OZ//

FEB 28/ WITH SILVER DOWN 18 CENTS: a loss of 1.867 million oz//inventory rests at 367.632 million oz

APRIL 17.2020:

SLV INVENTORY RESTS TONIGHT AT

414.038 MILLION OZ.

END

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 4.00/ and libor 6 month duration 1.13

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – 2.87

gold non existent//central banks will call in all of their leased gold.

XXXXXXXX

12 Month MM GOFO

+ 2.22%

LIBOR FOR 12 MONTH DURATION: 0.98

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -1.24

gold non existent//central banks will now call in their leased gold

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

U.S. Mint Halts Gold and Silver Coin Production; Supply Shortages Deepen and Premiums High

The shortage of small and large gold bullion coins and bars continues and may deepen as prices move higher and we enter a financial crisis. The U.S. Mint suspending gold coin production now along with silver coin production (see below) will exacerbate the strong demand and limited supply challenges and may lead to premiums remaining elevated.

Due to our direct relationships with leading refineries and as Authorised Distributors of government mints, we continue to sell gold bars (1 oz, kilo and 400 oz) and silver bars (1,000 oz) and gold coins including Gold Britannias and Sovereigns and Gold Nuggets or Kangaroos in volume. Our premiums have risen to reflect the rise in wholesale premiums from our mint and refinery partners, but we continue to have some of the most competitive premiums in the world.

NEWS and COMMENTARY

U.S. Mint Plant Halts Gold Coin Output Just as Demand Is Surging (see chart below)

Gold on track for 2nd weekly gain on global recession fears

Virus threatens to hit economy harder than war and flu in 1918

A double recession? Economies risk debt crises after stimulus spending

Gold Still Shines 50 Years After Nixon. Will Netflix?

Bullion banks hemorrhaging silver on Comex

Here are the contracts showing how $4.5 trillion in stimulus was outsourced to Wall Street

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

16-Apr-20 1717.85 1759.50, 1378.57 1382.91 & 1581.45 1589.06

15-Apr-20 1712.25 1718.65, 1367.92 1377.33 & 1566.02 1580.99

14-Apr-20 1715.85 1741.90, 1367.36 1383.07 & 1567.91 1588.26

09-Apr-20 1662.50 1680.65, 1339.48 1348.22 & 1529.00 1538.13

08-Apr-20 1649.05 1647.80, 1328.27 1330.27 & 1517.00 1513.14

07-Apr-20 1652.20 1649.25, 1344.23 1333.75 & 1519.53 1511.21

06-Apr-20 1636.60 1648.30, 1330.72 1341.06 & 1515.49 1526.66

03-Apr-20 1609.75 1613.10, 1310.66 1315.97 & 1490.47 1495.34

02-Apr-20 1588.05 1616.80, 1277.59 1307.02 & 1452.27 1489.72

01-Apr-20 1594.25 1576.55, 1288.95 1270.23 & 1457.94 1442.86

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here

ii) Important gold commentaries courtesy of GATA/Chris Powell

Pam and Russ Martens explain how the $4.5 trillion stimulus money was outsourced to Wall Street

(Pam and Russ Marten/Wall Street on Parade/GATA)

Pam and Russ Martens: Here are the contracts showing how $4.5 trillion in stimulus was outsourced to Wall Street

Submitted by cpowell on Thu, 2020-04-16 16:22. Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Thursday, April 16, 2020

Bloomberg News has an article up today with the headline: “The Fed Loves Main Street As Much As Wall Street This Time.” The article is accompanied with a graphic of Fed Chair Jerome Powell shooting equal amounts of money at Main Street and Wall Street.

Nothing could be further from the truth.

…

Despite the headline, the article, by Peter Coy, offers not a scintilla of evidence to support the premise that Main Street is getting a fair shake from the Fed. What the article does do is adopt the talking points the Fed has used in every press release it has issued on a new funding facility rollout — that the money will (through some magical and invisible and unexplained hand of the market Gods) make its way to American workers and households.

It’s all bunk. Here’s what is actually happening.

The stimulus bill (CARES Act) stipulates that the U.S. Treasury will provide $454 billion of the $2.2 trillion total to the Federal Reserve. That $454 billion will be the loss-absorbing capital to leverage the Fed’s purchases of toxic debt from Wall Street to a maximum of 10 times or $4.54 trillion.

So already Main Street is behind. Main Street is getting $2.2 trillion minus $454 billion for Wall Street and $46 billion for airlines and “national security” businesses, likely meaning Boeing. That leaves $1.7 trillion versus the $4.54 trillion that will be offered to Wall Street, or $2.84 trillion more heading to bail out Wall Street. …

… For the remainder of the report:

https://wallstreetonparade.com/2020/04/here-are-the-contracts-showing-ho…

* * *

END

A must read..Alasdair Macleod discusses the huge derivatives facing our crooked banks and how they are desperate to cover their huge losses.

Alasdair Macleod..

Alasdair Macleod: The looming derivatives crisis

Submitted by cpowell on Thu, 2020-04-16 18:46. Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, St. Helier, Jersey, Channel Islands

Thursday, April 16, 2020

The powerful forces of bank credit contraction are at the heart of a rapidly evolving financial crisis in global derivatives, whose gross value is over $600 trillion — an unimaginable sum. Central banks are on course to destroy their currencies through unlimited monetary expansion, lethal for bullion banks with fractionally reserved unallocated gold accounts, while being dramatically short of Comex futures.

This article explains the dynamics behind the current crisis in precious metal derivatives, and why it is the observable part of a wider derivative catastrophe that is caught in the tension between contracting bank credit and infinite monetary inflation. …

… For the remainder of the report:

https://www.goldmoney.com/research/goldmoney-insights/the-looming-deriva…

The looming derivative crisis

The powerful forces of bank credit contraction are at the heart of a rapidly evolving financial crisis in global derivatives, whose gross value is over $600 trillion; an unimaginable sum. Central banks are on course to destroy their currencies through unlimited monetary expansion, lethal for bullion banks with fractionally reserved unallocated gold accounts, while being dramatically short of Comex futures.

This article explains the dynamics behind the current crisis in precious metal derivatives, and why it is the observable part of a wider derivative catastrophe that is caught in the tension between contracting bank credit and infinite monetary inflation.

Introduction

One of the scares at the time of the Lehman crisis was that insolvent counterparties risked collapsing the whole over-the-counter derivative complex. It was for this reason that AIG, a non-bank originator of many derivative contracts, had to be bailed out by the Fed. By a mixture of good judgement and fortune a derivative crisis was averted, and by consolidating some of the outstanding positions, the gross value of OTC derivatives was subsequently reduced.

According to the Bank for International Settlements, in mid-June last year all global OTC contracts outstanding were still unimaginably large at $640 trillion, a massive sum in anyone’s book. It is unlikely to have changed much by today. But in bank balance sheets only a net figure is usually shown, and you have to search the notes to financial statements to find evidence of gross exposure. It is the gross that matters, because each contract bears counterparty risk, sometimes involving several parties, and derivative payment failures could make the payment failures now evident in disrupted industrial supply chains look like small beer.

Deutsche Bank’s 2019 balance sheet gives us an excellent example of how they are accounted for in commercial banks. It conceals derivative exposure under the headings “Trading assets” and “Trading liabilities” on the balance sheet. You have to go into the notes to discover that under Trading assets, derivative financial instruments total €80.848bn, and under Trading liabilities, derivative financial instruments total €81.910bn, a difference of €1.062bn This is relatively trivial for a bank with a balance sheet of €777bn.

But wait, there is another table that breaks derivative exposure down even further into categories, and it turns out the earlier figures are consolidated totals. The true total of OTC derivatives and exchange traded derivatives to which the bank is exposed is €37.121 trillion. That is nearly thirty-five thousand times the €1.062bn netted difference in the balance sheet. And when you bear in mind that valuing OTC derivatives is somewhat subjective, or as the cynics say, mark to myth, it invalidates the valuation exercise.

Clearly, by taking the mildest of a positive approach to derivatives held as assets, and a slightly more conservative approach to valuing derivatives on the liabilities side, that 35,000:1 leverage at the balance sheet level can make an enormous difference.

Now let us take our imagination a little further. A large number of these derivatives will have commercial entities as counterparties, businesses that have been shut down by the coronavirus since the balance sheet date. With the German economy already heading into recession before the coronavirus closed down much of the global economy, Deutsche Bank’s risk of losses arising from its derivative position could turn out to be in the trillions, not the one billion netted difference shown on the balance sheet.

Not only is there the emergence of counterparty failures to deal with, but there are ever-changing fair values, which will particularly reflect interest rate spreads increasing for Deutsche Bank’s €30.25 trillion interest rate-linked derivatives. We cannot know whether it is net positive or negative for shareholders. And with balance sheet gearing of assets 22 times larger than share capital very little change could wipe them out.

Deutsche Bank is not alone in presenting derivative risk in this manner: it is the elephant in many bank boardrooms. As a weak link, Deutsche is a relevant illustration of risks in the banking system. Since the Lehman crisis, its senior management has been on the back foot, retreating from businesses they could neither control nor understand. They have also made very public mistakes in precious metals, which is our next topic.

Gold derivatives in crisis

While a struggling bank like Deutsche provides us with a laboratory experiment for how a derivative virus can kill a bank, we are now seeing it kill off bullion banks in real time. A rising gold price, out of the control normally imposed by expandable derivatives, has effectively gone bid only in any size. We are told this is due to COVID-19 shutting mines and refineries and disrupting logistics, and so is purely temporary. The LBMA and CME which runs Comex have been issuing calming statements and even announced the introduction of a new 400-ounce gold futures contract alleged to ease the supply shortage.

In short, the gold derivative establishment is panicking. The swaps position on Comex shows why.

With their net short position in very dangerous territory, Comex swaps are badly wrongfooted at a time when the Fed and other central banks have announced unlimited monetary inflation, signalling a paradigm shift in the relationship between sound and unsound money. For ease of reference and to understand their relevance, a swap dealer is defined by the Commodity Futures Trading Commission, which collates the figures, as follows:

An entity that deals primarily in swaps for a commodity and uses the futures markets to manage or hedge risks associated with those swap transactions. The swap dealer’s counterparties may be speculative traders, like hedge funds, or traditional commercial clients that are managing risk arising from their dealings in the physical commodity.

Therefore, a swap dealer is one that operates across derivative markets, and typically will trade in London forwards as well as on Comex. In a nutshell, it describes a bullion bank’s trading desk.

In a further piece of disinformation this week, Jeff Christian, head of CPM Group, in an obviously staged interview for MacroVoices claimed that traders in London were forced by their banks to cover trading risk in the futures market as a condition of their funding. The implication was shorts on Comex are matched to longs in London’s forward market and therefore not a problem. This may be true of an independent trader looking for arbitrage opportunities between markets but is not how it works in a bank.[i]

The mechanics of gold derivative trading

A bank which has bullion business will almost certainly have a trading desk and be a member of the LBMA. Look at it from a banker’s point of view. The bank has business flows in gold, which requires access to the market and a dealing capability. He will employ one or more gold traders with acknowledged expertise to manage the desk. As a profit centre and because a skilled trader will require it, he will give the desk discretionary trading limits and monthly or quarterly profit targets. Part of the deal with the desk is profits will be struck net of the cost of funding the book, usually a reference to Libor, which is effectively the marginal cost to the bank of expanding its credit to back the dealers’ positions.

When the gold desk has established a profitable track record, the banker will be eager to raise the trading desk’s position limits. For bullion banking this has been going on for years, and while individual trading desks come and go, traders now have a large degree of dealing autonomy. It is not, as Mr Christian misinforms us, just a covered arbitrage business between forwards in London and futures in America.

The LBMA lists twelve market makers, all of which are well-known banks. There are thirty-one other banks, some of which run trading desks which take positions. It is worth noting that dealing in gold is normally one of many banking and trading activities undertaken by an LBMA member bank, including forex trading with which this activity is very similar. All of them are funded by the expansion of bank credit, which is the point of having a banking licence.

Turning to Comex, according to CTFC data there are a maximum of 28 swap dealers which recently have been active in gold futures, either with long or short positions. These numbers tie in nicely with the likely number of trading desks and designated market makers in the banks which are LBMA members.

An LBMA member bank will have physical bullion business and is likely to offer allocated and unallocated accounts to customers. Since the point of banking is to operate a fractional reserve-based customer service, a bullion bank discourages allocated (custodial) accounts, usually by making them an expensive way for customers to hold bullion. Unallocated accounts, which under fractional reserve banking will be a multiple of gold or gold derivatives in the possession of the bank, becomes the bank’s standard customer offering.

One of the benefits of LBMA membership is it gives a bullion bank access to paper markets, so that it can replace physical bullion held against unallocated client accounts with long positions for forward settlement, positions that can be rolled and rolled without ever having to take delivery. Another benefit is access to leased gold from central banks which store bullion in the Bank of England’s vault.

One can begin to see why dealings between LBMA members are so significant, recently hitting 60 million ounces a day, the equivalent of 1,866 tonnes. This represents dealings between LBMA members only and excludes dealings between a member and a non-member. In the distant past they were included in LBMA estimates, which inflated the numbers even further by a factor of about five times.

All this is done on minimum bullion liquidity, which when you take away central bank gold, physical ETF custodial bullion, as well as bullion owned or allocated to miscellaneous institutions, family offices and private individuals stored in London bullion vaults, is not the 8,326 tonnes claimed in a recent LBMA press release designed to calm the markets, but is almost certainly significantly less than a thousand tonnes.

Clearly, running long positions for forward settlement has become a substitute for backing unallocated accounts with a fractional amount of physical metal. While the trading books in London keep the plates spinning in their dangerously geared operation, the profit opportunities on Comex have become a separate matter instead of just a hedging facility.

Officially described as speculators, but better described as suckers, gold and silver futures are the medium for a repeating cycle whereby market makers supply them contracts by drawing on the ability of their banks to create bank credit out of thin air. Once the suckers run out of buying power, the market makers pull the rug out from under them, taking out their stop-loss points. It has been an immensely profitable exercise for swap dealers.

Fortunately for swap dealers, the suckers have short memories. Until last year, it was a frequently repeated exercise, leading to a blasé attitude. Corruption among traders had become rife and they began to be caught spoofing and rigging the fix against bank customers. Dealers were sacked, fined and jailed. Deutsche Bank were fined and forced out of the twice-daily fix. A JPMorgan trader pleaded guilty last August to manipulating the precious metals markets for nine years. Another with the same firm had pleaded guilty the previous October. In the past five years federal prosecutors have brought twelve spoofing cases against sixteen defendants, most pleading guilty.

This corruption is typical of end-of-cycle behaviour, when the derivative ringmasters in precious metals believe they have risen above the law. The point behind the current crisis unfolding in the gold derivative markets is the scam has fully run its course, and the bankers in charge of bullion desks will be increasingly concerned of the reputational damage.

How the ending of the gold derivative scam started

In the past, bullion banks always managed to put a lid on open interest, returning it from an overbought 600,000 contracts to under 400,000 contracts, in the process getting an even book or exceptionally going long, ready for the next pump-and-dump cycle. But then something changed. Last year, the pump-and-dump schemes of the bullion banks’ trading desks went awry, with open interest rocketing to nearly 800,000 contracts by January this year. After several failed attempts, in June 2019 gold had broken above $1350, which encouraged the speculators to chase the price up even further. The interest rate outlook then softened along with the global economy, and by early September, with open interest threatening to rise above the historically high 650,000 level, the Fed was forced to inject inflationary liquidity into the US banking system through repos. At its peak on 23 January 2020, the sum of all short positions on Comex was the equivalent of 2,488 tonnes of gold, worth $125bn. The suckers were finally breaking the banks, who held the bulk of the shorts. This can be seen in the chart below of Comex open interest

It was imperative that the position be brought under control, and accordingly, it appears that central banks, presumably at the behest of the Bank of England, arranged for gold to be leased to the bullion banks to ease liquidity pressures. And then trading desks were hit by a perfect storm.

The coronavirus put large swathes of the global economy into lockdown, disrupting payment chains in industrial production. This meant that formerly solvent businesses now face collapse and are turning en masse to their banks for liquidity. The bankers’ natural instinct is no longer the pursuit of profit, but fear of losses, and they now have an overwhelming desire to contract outstanding bank credit. In a panic, the Fed cut the Fed funds rate to the zero bound and promised unlimited liquidity support in a desperate attempt to avoid a deflationary spiral. Meanwhile, our swaps traders in gold futures were caught record short, the worst possible position for them given the evolving situation.

The coup de grâce has now come from their banking superiors. Despite the efforts of the Fed to persuade them otherwise, bankers in their lending have become strongly risk-averse and know they will be forced to commit bank credit to failing corporations against their instincts. For this reason, they are taking every opportunity to reduce their balance sheet exposure to other activities. One of the first divisions to suffer is bound to be bullion bank desks running short positions, synthetic in London and actual on Comex, which are wholly inappropriate at a time of massive monetary inflation.

It is this last pressure that has led to an unusual combination of collapsed open interest, shown in the chart above, and rising gold prices, accompanied by a persistent premium of $40 or more over the spot price in London. Clearly, there is good reason for the LBMA and the CME to panic. If the gold price rises much further, there will be bullion desks, managing shorts on Comex and fractionally reserved positions in London, at risk of bankrupting their employers.

The Comex contract, which anchors itself to physical gold through the option of physical delivery at expiry, will face enormous challenges when the active June contract expires at the end of next month. At expiry, the speculators have a chance to obtain delivery. Normally, when the spot price is lower than the future, only the insane would insist on delivery at the higher price. But with very low availability of bullion and price premiums for delayed delivery common, London is being rapidly drained of physical liquidity as well. It is like a good old-fashioned one-two boxing combination: first the Comex market is delivered a body-blow, and then the LBMA gets an uppercut.

Many central banks who have stored their earmarked gold at the Bank of England will be unhappy as well, having leased their gold in the expectation it would stabilise the bullion market. They will not do it again for an interesting reason: gold leasing rates have turned strongly negative, with the two-month rate currently minus 3.7%.[ii] No sensible entity is going to pay a lessor to lease its gold and will want leased gold returned instead. Therefore, the availability of gold for leasing is now cut off and gold already leased will need to be returned if delivered to the lessors, or unencumbered if it remained in the Bank of England’s vaults as is the normal leasing practice.

Gold liquidity in London will then disappear entirely, at which point those with a claim to custodial gold will hope that their property rights remain protected.

Broader implications of the failure of gold derivatives

This article has gone into some detail why Comex and the LBMA face their current difficulties, and why liquidity is vanishing. For any bank with large unallocated gold liabilities, bearing in mind they are fractionally reserved mostly against derivatives instead of bullion, these problems are likely to lead to their withdrawal from the market. ABN-Amro is already reported to have closed its customers’ accounts, having forced them to sell positions, and other banks will surely follow.

The gold derivative market is probably the largest foreign exchange cross after the US dollar euro. But it is also the most fundamental of all monetary exchange markets. The relationship was famously captured in John Exter’s inverse pyramid, which showed how the world’s credit obligations were all supported on a diminishingly small apex of gold.

The liquidity pressures that result from banks trying to reduce their balance sheets also affects other derivative markets, and from our discourse on Deutsche Bank’s balance sheet, we can see that the whole banking system is in a very precarious position with respect to derivatives. While we survived the Lehman crisis with only one investment bank failing, the collapse of industrial production of goods and services due to lockdowns to control the spread of the coronavirus will almost certainly lead to multiple bank failures. Bankers are staring into an abyss.

For central banks, monetary inflation is everywhere the solution. Bank rescues, payment chain failures, the furloughing of millions of employees, helicopter money to bail out whole populations, money to bail out governments, money to support all categories of financial assets: the list is endless in scope and infinite in quantity. The survival of the global financial system is at stake. If it survives, state-issued money will have been destroyed. But then what is the point of owning financial assets valued in valueless currency?

While this process of monetary destruction would have reasonably been expected to evolve over time, the coronavirus has accelerated it. The fate of the $640 trillion derivative mountain recorded by the Bank for International Settlements is sealed and will be settled through bank bankruptcies and state-directed elimination. In observing the train wreck that is precious metal derivative markets, we are at Act 1 Scene 1 of a rapidly-evolving and dramatic derivatives tragedy.

end

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Futures Soar On Reopening, Corona Cure Optimism; Ignore Mountains Of Bad News

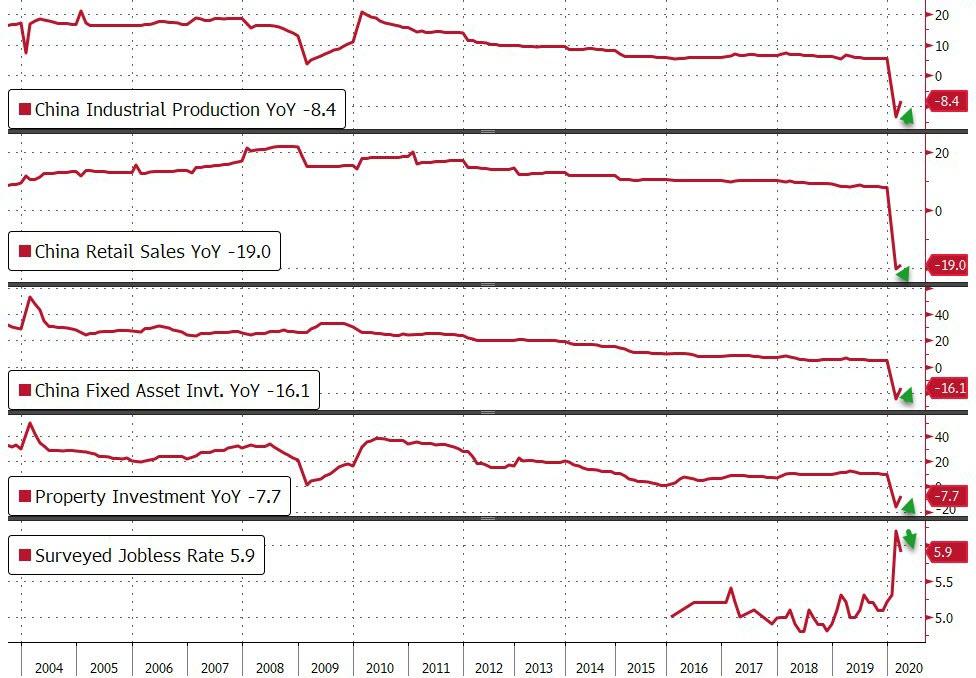

Even though the Gilead “miracle drug” report was refuted by the company itself, which slammed the market-moving Statnews article (sourced reportedly from hedge funds who were seeking to take profit in GILD) as “anecdotal reports with no statistical power”, and even though Trump’s plans to reopen the country turned out to be far less pressing than expected, with Trump effectively handing power into the hands of states, this morning futures and global stocks have continued their move higher after blasting off last night on the Gilead/reopening speculation, with the euphoria persisting overnight as the small steps toward restarting the world’s largest economy helped investors look past mixed progress on curbing the coronavirus and the latest dismal data from China, where GDP posted its first contraction in four decades, sliding 6.8% or more than expected.

The data from China showed the world’s second-largest economy shrank for the first time since at least 1992 because of the coronavirus woes. GDP contracted 6.8% in the quarter year-on-year, more than expected, and 9.8% from the previous quarter. Retail sales also fell more than expected in March, but industrial output dipped only slightly, suggesting its manufacturing sector at least is recovering more quickly.

As WTI oil slumped, further extending its divergence with Brent…

… the dollar tried to rebound and bond yields were generally unchanged, US equity futures rallied nearly 100 points, or 4%, from the Thursday close and approached the limit-up lock on several occasions, reflecting optimism that major economies will slowly start lifting lockdown restrictions and signs of medical progress against the virus.

The week is ending on an optimistic note after the White House set guidelines to reopen the economy, though it has yet to ensure that widespread testing will be available as many business leaders have urged. The president is under pressure, with 22 million Americans applying for jobless benefits in a month, erasing a decade worth of job creation. At the same time, infections have surged in Russia, Germany and Singapore. Investors also assessed a report that Gilead Sciences is seeing improvements in a group of coronavirus patients being treated with its drug, although the company itself refuted the report. German Chancellor Angela Merkel this week announced tentative steps to begin returning the country to normal.

“The market is a bit optimistic right now,” David Bailin, chief investment officer at Citi Private Bank, said on Bloomberg TV. “Ultimately we have to have really great coordination in order to see any real improvement in the economy.”

Prior to Friday’s cash open, the S&P 500 was up 0.4% this week and set for a second straight weekly gain – its first back-to-back weekly gain since before the market turmoil began in February – despite an unprecedented collapse in the US (and Chinese) economy, and 22 million people laid off in the past month, as investors scour first-quarter earnings to find signs of the novel coronavirus outbreak’s effects on companies’ balance sheets.

In Europe, the Stoxx 600 Index also climbed 2.6%, entering a bull market, after it rose 20% from its March lows, with the travel and leisure sector leading the gains although all 19 industry groups were in the green. Banking stocks helped the Stoxx Europe 600 Index jump to a session high as lenders are said to seek to avert stashing billions for soured loans; the banks subgroup surges as much as 4.3%. European lenders are set to report comparatively small increases in loan loss reserves in the first quarter and plan a similar approach during the rest of the year, Bloomberg News reports, citing senior bankers and regulators.

European countries have “no choice” but to set up a fund that “could issue common debt with a common guarantee”, French President Emmanuel Macron told the Financial Times on Thursday. Failure to do so would lead to populists winning elections in Italy, Spain, and possibly France, he also warned.

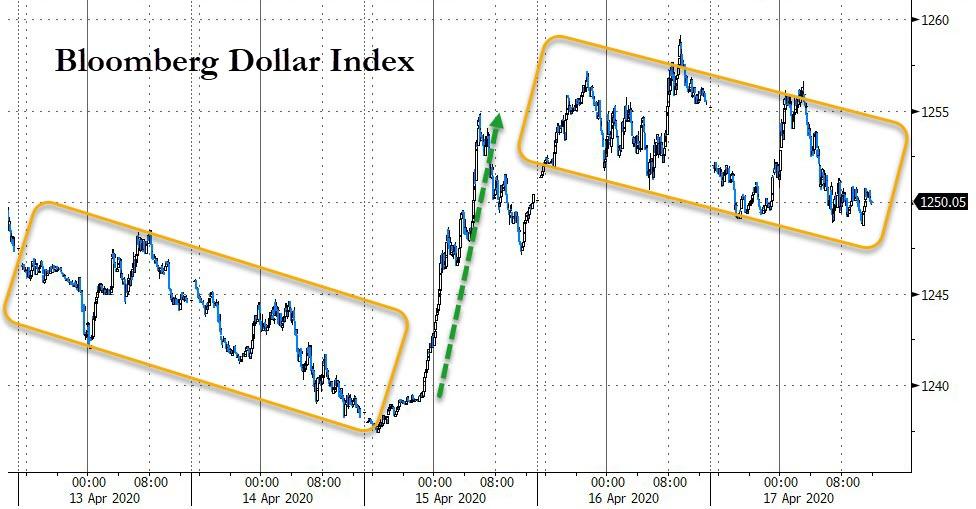

Yields on ultra-safe 10-year U.S. Treasuries US10YT=RR and German Bunds rose slightly, while Treasury futures TYc1 and the dollar firmed against the yen JPY=EBS, in another tentative sign of investor optimism.

“The market continues to look through terrible data… on anticipation of economies reopening,” said Steen Jakobsen, Chief Investment Officer at Saxo Bank. “And hopes that a new drug treatment will help lift longer term uncertainty about the COVID-19 pandemic.”

Earlier in the session, Asian stocks gained as traders shrugged off the catastrophic China GDP data noted above, led by IT and materials, after falling in the last session. All markets in the region were up, with Jakarta Composite gaining 3.4% and South Korea’s Kospi Index rising 3.1%. The Topix gained 1.4%, with Riken Technos and Kichiri Holdings & Co Ltd rising the most. The Shanghai Composite Index rose 0.7%, with Zhejiang Xinneng Solar Photovoltaic Technology and Jiangsu Boxin Investing posting the biggest advances.

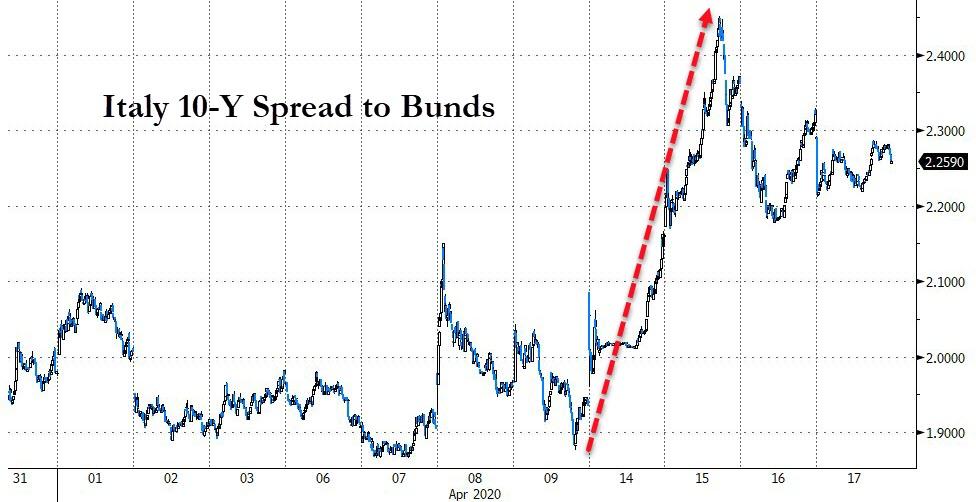

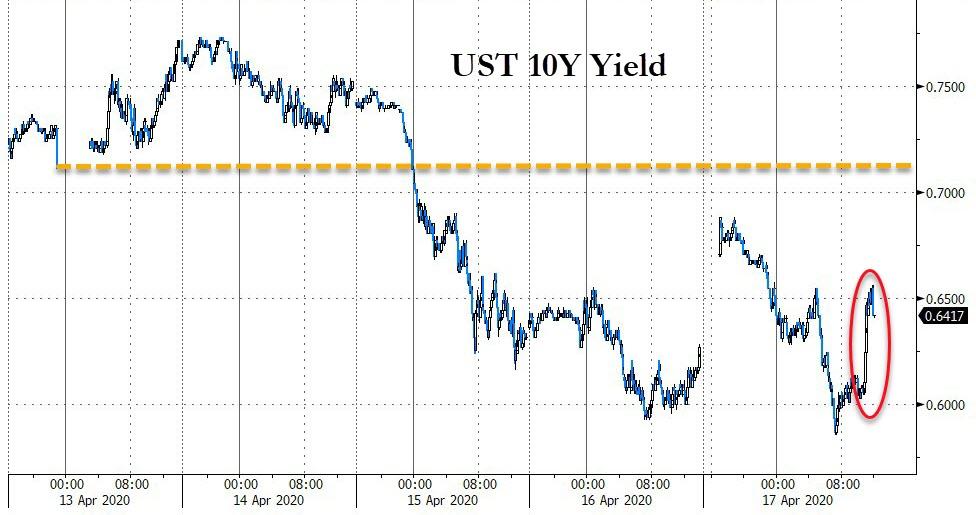

In rates, the 10Y yield initially bounced sharply from its 0.62% close rising almost as high as 0.69% before reversing virtually all gains. Italian bond markets, which have been under pressure as the country’s virus difficulties push its debt-to-GDP ratio towards 150%, also rallied as France expressed support for joint euro zone debt issuance.

In commodities, spot gold fell 1.5% to $1,692 per ounce too and with investors looking to take on more risk industrial metal copper jumped 4% on track for its best week since February 2019. No such luck for battered oil markets however. WTI futures slumped 8% to an 18-year low after OPEC had lowered of its global demand forecast on Thursday, and Brent crude slipped back under $28 a barrel having been up nearly 3% at one point. OPEC now sees a contraction of global demand of 6.9 million barrels per day (bpd) this year due to the coronavirus outbreak.

“Downward risks remain significant, suggesting the possibility of further adjustments, especially in the second quarter,” OPEC said of the demand forecast.

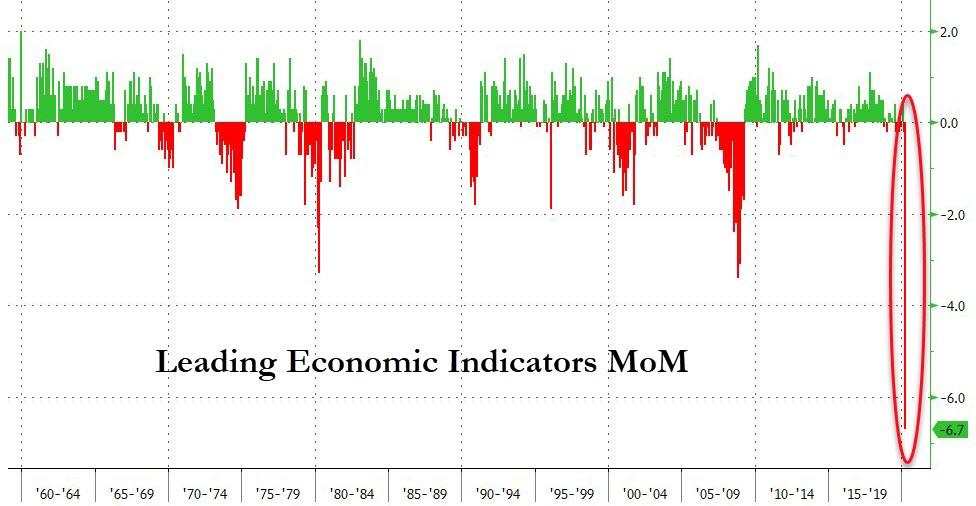

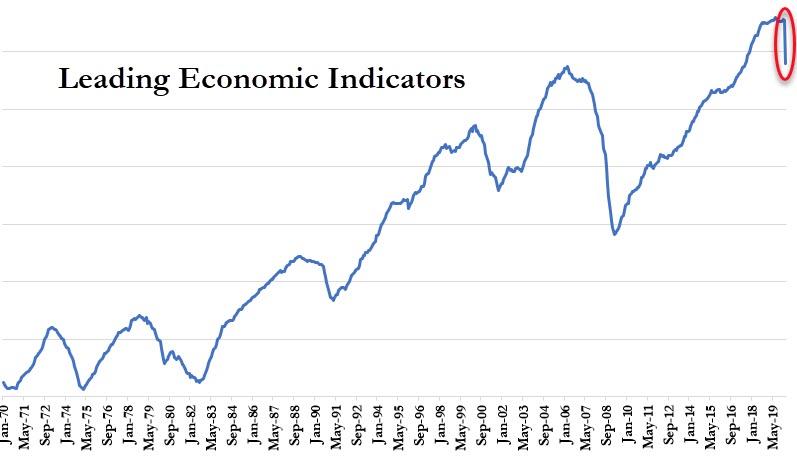

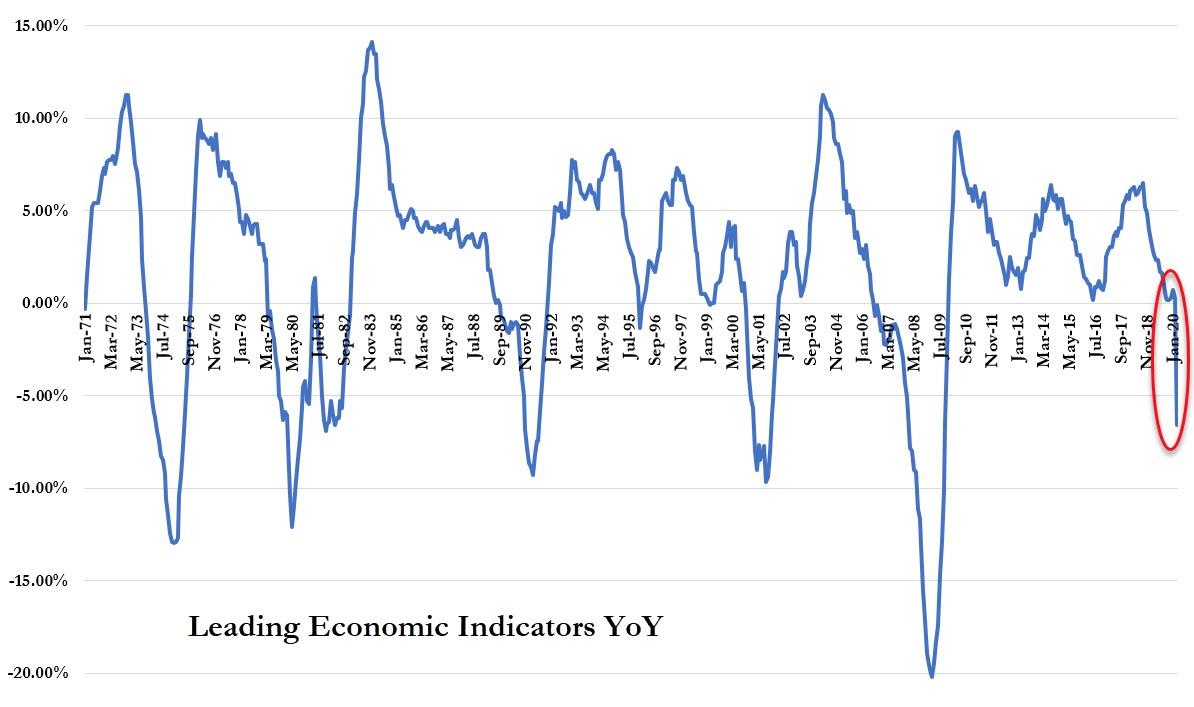

Looking at the day ahead, the data releases include new car registrations for March in the EU27, the Italian trade balance for February and the final Euro Area CPI reading for February. From the US we’ll also get the leading index for March. From central banks, we’ll hear from the Fed’s Bullard and the ECB’s Rehn.

Market Snapshot

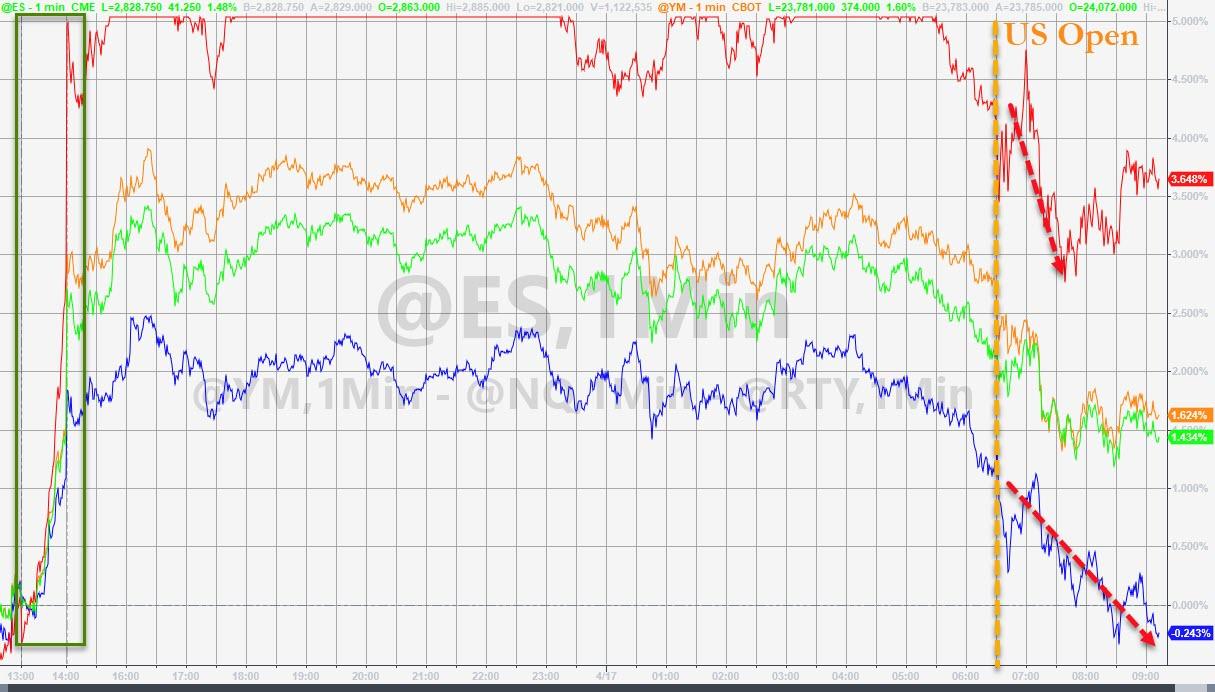

- S&P 500 futures up 2.6% to 2,859.50

- STOXX Europe 600 up 2.5% to 333.14

- MXAP up 1.8% to 144.79

- MXAPJ up 2% to 468.07

- Nikkei up 3.2% to 19,897.26

- Topix up 1.4% to 1,442.54

- Hang Seng Index up 1.6% to 24,380.00

- Shanghai Composite up 0.7% to 2,838.49

- Sensex up 1.8% to 31,166.28

- Australia S&P/ASX 200 up 1.3% to 5,487.54

- Kospi up 3.1% to 1,914.53

- German 10Y yield fell 0.2 bps to -0.476%

- Euro down 0.09% to $1.0830

- Italian 10Y yield fell 5.0 bps to 1.659%

- Spanish 10Y yield unchanged at 0.831%

- Brent futures down 0.3% to $27.73/bbl

- Gold spot down 1.3% to $1,695.70

- U.S. Dollar Index up 0.1% to 100.13

Top Overnight News