GOLD:$1714.75 UP $40.75 The quote is London spot price

Silver:$15.14 UP 42 CENTS

Closing access prices: London spot

i)Gold : $1715.50 LONDON SPOT 4:30 pm

ii)SILVER: $15.15//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

APRIL comex gold price CLOSE 1.30 PM: $1725.20

MAY COMEX GOLD: 1727.20 1:30 PM

JUNE GOLD: $1739.10 CLOSE 1.30 PM// SPREAD SPOT/FUTURE JUNE: $25.//PREMIUMS WENT UP AGAIN

CLOSING SILVER FUTURE MONTH

SILVER APRIL COMEX CLOSE: XXX

SILVER MAY COMEX CLOSE; $15.28-…1:30 PM.//SPREAD SPOT/FUTURE MAY: 20 CENTS PER OZ//PREMIUMS UP AGAIN

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2800. usa per oz

and silver; $31.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

DO NOT PAY ANY ATTENTION TO WHAT THE CROOKS ARE DOING AT THE COMEX AND LONDON LBMA..PHYSICAL IS THE NAME OF THE GAME AND NOTHING ELSE

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 158/826

issued 632

EXCHANGE: COMEX

CONTRACT: APRIL 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,678.200000000 USD

INTENT DATE: 04/21/2020 DELIVERY DATE: 04/23/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

132 C SG AMERICAS 56

657 C MORGAN STANLEY 35

657 H MORGAN STANLEY 448

661 C JP MORGAN 632 158

685 C RJ OBRIEN 3

686 C INTL FCSTONE 2 15

690 C ABN AMRO 192 68

737 C ADVANTAGE 6

800 C MAREX SPEC 2

905 C ADM 35

____________________________________________________________________________________________

TOTAL: 826 826

MONTH TO DATE: 30,575

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 826 NOTICE(S) FOR 82600 OZ (2.5692 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 30,575 NOTICES FOR 3,057,500 OZ (95.10 TONNES)

SILVER

FOR APRIL

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 806 for 4,025,000 oz

BITCOIN MORNING QUOTE $6955 UP 112

BITCOIN AFTERNOON QUOTE.: $7091 UP $249

GLD AND SLV INVENTORIES:

WITH GOLD UP $40.75: AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

WE HAD TWO HUGE TRANSACTIONS AND BOTH ARE DEPOSITS:

A) A HUGE 3.8 TONNES OF GOLD IS ADDED TO THE GLD//THE ADDITION IS NOTHING BUT A PAPER TRANSACTION//NO PHYSICAL GOLD ENTERED.//

B) A HUGE 9.07 TONNES OF PAPER GOLD ADDED TO THE GLD///

TOTAL FOR TODAY: 12.87 TONNES

GLD: 1,042.46 TONNES OF GOLD//

WITH SILVER UP 42 CENTS TODAY: AND WITH NO SILVER AROUND

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV

SURPRISINGLY: A PAPER WITHDRAWAL OF 1.865 MILLION OZ FROM THE SLV..

RESTING SLV INVENTORY TONIGHT:

SLV: 410.774 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A STRONG SIZED 2542 CONTRACTS FROM 142,149 DOWN TO 139,607 AND FURTHER FROM OUR NEW RECORD OF 244,710, (FEB 25/2020. THE GOOD SIZED LOSS IN OI OCCURRED WITH OUR CONSIDERABLE 60 CENT LOSS IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE LOSS IN COMEX OI IS DUE TO SOME BANKER SHORT COVERING PLUS A CONSIDERABLE EXCHANGE FOR PHYSICAL ISSUANCE, SOME LONG LIQUIDATION ALONG WITH OUR ZERO GAIN IN SILVER OZ STANDING. WE HAD A SMALL NET LOSS IN OUR TWO EXCHANGES OF 1302 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A STRONG AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: MARCH: 00 AND MAY: 945 AND JULY: 70 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1015 CONTRACTS. WITH THE TRANSFER OF 1015 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1015 EFP CONTRACTS TRANSLATES INTO 5.075 MILLION OZ ACCOMPANYING:

1.THE 60 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.145 MILLION OZ INITIALLY STANDING FOR APRIL

TUESDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL 60 CENTS).. BUT, OUR OFFICIAL SECTOR/BANKERS WERE SOME WHAT SUCCESSFUL IN THEIR ATTEMPT TO FLEECE SOME SILVER LONGS FROM THEIR POSITIONS, AS WE DID HAVE A NET LOSS OF 1525 CONTRACTS OR 7.635 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

OUR SPREADING OPERATION HAS NOW SWITCHED INTO SILVER…..

SPREADING OPERATION FOR OUR NEWCOMERS:

WE HAVE NOW COMMENCED IN SILVER THE ILLEGAL SPREADING OPERATION \ FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW STOPPED IN GOLD AS THEY NOW BEGIN TO MORPH INTO SILVER AS WE HEAD TOWARDS THE NEW FRONT MONTH WILL BE MAY.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF APRIL. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

14,476 CONTRACTS (FOR 14 TRADING DAYS TOTAL 14,476 CONTRACTS) OR 72.38 MILLION OZ: (AVERAGE PER DAY: 1034 CONTRACTS OR 5.170 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF APRIL: 72.38 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 10.34% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 965.87 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP SO FAR 72.38 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

EXCHANGE FOR PHYSICAL ISSUANCE THIS MONTH IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2542, WITH THE CONSIDERABLE 60 CENT LOSS IN SILVER PRICING AT THE COMEX /TUESDAY… THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1015 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE LOST A SMALL SIZED OI CONTRACTS ON THE TWO EXCHANGES: 1525 CONTRACTS (WITH OUR 60 CENT LOSS IN PRICE)

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 1015 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A STRONG DECREASE OF 2542 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 60 CENT LOSS IN PRICE OF SILVER/ AND A CLOSING PRICE OF $14.72 // TUESDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.7050 BILLION OZ TO BE EXACT or 100.7% of annual global silver production (ex Russia & ex China).

FOR THE NEW MAR DELIVERY MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR nil OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.145 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 3513 CONTRACTS TO 493,158 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE LOSS OF COMEX OI OCCURRED WITH OUR COMEX LOSS IN PRICE OF $21.60 /// COMEX GOLD TRADING// TUESDAY// WE HAD CONSIDERABLE BANKER SHORT COVERING , A GOOD INCREASE IN GOLD OZ STANDING AT THE COMEX, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A GOOD EX. FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR STRONG LOSS IN THE PAPER PRICE OF GOLD.

WE HAD NO ISSUANCE OF OUR NEW 4 GC CONTRACT

WE GAINED A GOOD 1255 CONTRACTS (3.906 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4768 CONTRACTS:

CONTRACTS, FEB> 0 CONTRACTS; MARCH 00 APRIL: 0. MAY: 0, AND JUNE 4768.; DEC 0 AND ALL OTHER MONTHS ZERO//TOTAL: 4768. The NEW COMEX OI for the gold complex rests at 493,158. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1255 CONTRACTS: 1255 CONTRACTS DECREASED AT THE COMEX AND 4768 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 1255 CONTRACTS OR 3.903 TONNES. TUESDAY, WE HAD CONSIDERABLE LOSS OF $21.60 IN GOLD TRADING……

AND DESPITE THAT LOSS IN PRICE, WE HAD A FAIR SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 3.903 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (FELL $21.60). AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WERE UNSUCCESSFUL (SEE BELOW).

4 GC ISSUANCE: ZERO

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A GOOD SIZED INCREASE IN EXCHANGE FOR PHYSICALS (4768) ACCOMPANYING THE LOSS IN COMEX OI (3513 OI): TOTAL GAIN IN THE TWO EXCHANGES: 2495 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)A STRONG INCREASE IN STANDING AT THE GOLD COMEX FOR THE FRONT APRIL MONTH, 3) ZERO LONG LIQUIDATION AND …ALL OF THIS WAS COUPLED WITH THAT STRONG LOSS IN GOLD PRICE TRADING//TUESDAY

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 63,297 CONTRACTS OR 6,329,700 oz OR 196.88 TONNES (14 TRADING DAYS AND THUS AVERAGING: 4521 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAY(S) IN TONNES: 196.88 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 196.88/3550 x 100% TONNES =5.54% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 2519.78 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 196.88 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 2542 CONTRACTS FROM 142,149 DOWN TO 139,607 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

ALL OF THE LOSS IN COMEX OI WAS DUE TO 1) SOME BANKER SHORT COVERING , 2) THE ISSUANCE OF A GOOD SIZED NUMBER OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A ZERO INCREASE IN SILVER OZ STANDING AT THE COMEX FOR APRIL AND 4) SOME LONG LIQUIDATION

EFP ISSUANCE 1015 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR FEB. 0; FOR MAR 0: AND MAY: 945; JULY: 70 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1015 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE STRONG COMEX OI LOSS OF 2542 CONTRACTS TO THE 1015 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL LOSS OF 1525 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 7.635 MILLION OZ!!! WITH THE STRONG LOSS IN PRICE///

RESULT: A GOOD SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 60 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// TUESDAY. WE ALSO HAD A GOOD SIZED 1015 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 16.97 POINTS OR 0.60% //Hang Sang CLOSED UP 99.81 POINTS OR 0.42% /The Nikkei closed DOWN 142.83 POINTS OR 0.74%//Australia’s all ordinaires CLOSED DOWN .09%

/Chinese yuan (ONSHORE) closed UP at 7.0826 /Oil UP TO 11.28 dollars per barrel for WTI and 19.20 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 7.0826 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0983 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

finally we get a proper silver inventory report

total dealer deposits: nil oz

total dealer withdrawals: nil oz

i)we had 0 deposits into the customer account

into JPMorgan: 0

ii)into everybody else; 0

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.819 million oz of total silver inventory or 50.04% of all official comex silver. (160.819 million/321.170 million

total customer deposits today: 0 oz

we had 1 withdrawals:

i Out of Delaware: 15,975.900 oz

total withdrawals; 15,975.900 oz

We had 2 adjustments: and all from the dealer to the customer:

i) from CNT: 297,364.546 oz

ii) Out of Int. Delaware: 4908.485

total dealer silver: 81.434 million

total dealer + customer silver: 317.337 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The total number of notices filed today for the APRIL 2020. contract month is represented by 0 contract(s) FOR nil oz

To calculate the number of silver ounces that will stand for delivery in APRIL we take the total number of notices filed for the month so far at 806 x 5,000 oz = 4,025,000 oz to which we add the difference between the open interest for the front month of APRIL.(23) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL/2019 contract month: 806 (notices served so far) x 5000 oz + OI for front month of APRIL (23)- number of notices served upon today (0) x 5000 oz of silver standing for the APRIL contract month.equals 4,145,000 oz.

WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ OF SILVER WILL STAND AT THE COMEX.

TODAY’S ESTIMATED SILVER VOLUME: 55,051 CONTRACTS //

FOR YESTERDAY: 91,446 CONTRACTS..,CONFIRMED VOLUME

YESTERDAY’S CONFIRMED VOLUME OF 91,446 CONTRACTS EQUATES to 457 million OZ 65.3% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -0.35% ((APRIL 22/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO +0.15% to NAV: (APRIL 22/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 0.35%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.63 TRADING 15.42///DISCOUNT 1.33

END

And now the Gold inventory at the GLD/

APRIL 22/WITH GOLD UP $40.75 TODAY:; TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A)A MONSTROUS 3.8 PAPER TONNES WERE ADDED TO THE GLD INVENTORY AND B) ANOTHER HUGE 9.07 TONNES OF PAPER GOLD ADDED LATE IN THE DAY//INVENTORY RESTS AT 1042.46 TONNES

APRIL 21/WITH GOLD DOWN $21.60 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTROUS ADDITION OF 7.9 PAPER TONNES TO THE GLD INVENTORY//INVENTORY RESTS AT 1029.59 TONNES

APRIL 20//WITH GOLD UP $10.00 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1021.69 TONNES

APRIL 17/WITH GOLD DOWN $27.80 TODAY: SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1021.69 TONNES TONNES..THE STRING OF 12 STRAIGHT STRONG DEPOSITS ENDS..

APRIL 16/WITH GOLD DOWN $4.50 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG DEPOSIT OF 4.10 TONNES WAS ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 1021.69 TONNES/12TH STRAIGHT STRONG DEPOSIT

APRIL 15//WITH GOLD DOWN $19.10 TODAY; ANOTHER HUGE CHANGE IN GOLD INVENTORY; A STRONG 7.89 TONNES WAS ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 1117.59 TONNES.//11TH STRAIGHT STRONG DEPOSIT

APRIL 14/WITH GOLD UP $23.55 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 15.51 TONNES WAS ADDED TO THE GLD INVENTORY/INVENTORY RESTS AT 1009.70 TONNES//THIS IS THE 10TH STRAIGHT STRONG DEPOSIT//THIS IS A FRAUDULENT VEHICLE..THEY HAVE NO PHYSICAL GOLD IN THE TRUST..

APRIL 13//WITH GOLD UP $27.65 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 5.36 TONNES WAS ADDED TO THE GLD//INVENTORY RESTS AT 994.19 TONNES

APRIL 9 WITH GOLD UP $37.30 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 2.92 TONNES WAS ADDED TO THE GLD//GOLD INVENTORY RESTS TONIGHT AT..988.63 TONNES

APRIL 8/WITH GOLD DOWN $.60//ANOTHER HUGE CHANGE IN GOLD INVENTORY/;; A STRONG 1.45 TONNES WAS ADDED TO THE GLD/GOLD INVENTORY RESTS AT 985.71 TONNES

APRIL 7/WITH GOLD UP $.30: ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.27 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 984.26 TONNES

APRIL 6//WITH GOLD UP $32.00//ANOTHER STRONG DEPOSIT INTO THE GLD; A HUGE 7.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT : 978.99 TONNES

APRIL 3//WITH GOLD UP $7.80 TODAY//ANOTHER STRONG DEPOSIT OF 3.22 TONNES INTO THE GLD/INVENTORY RESTS AT 971.97 TONNES

APRIL 2//WITH GOLD UP $31.80 TODAY: ANOTHER STRONG DEPOSIT OF 1.75 TONNES INTO THE GLD//INVENTORY RESTS AT 968.75 TONNES

APRIL 1/WITH GOLD DOWN $7.70 TODAY: ANOTHER CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.62 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 967.00 TONNES

MARCH 31//WITH GOLD DOWN $32.70//A MONSTROUS PAPER DEPOSIT OF 10.84 TONNES INTO THE GLD//INVENTORY RESTS AT 964.38 TONNES

MARCH 30/WITH GOLD DOWN $6.10 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 953.54 TONNES

MARCH 27.WITH GOLD DOWN $16.40: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A HUGE DEPOSIT OF 4.39 TONES INTO THE GLD/INVENTORY RESTS AT 953.54 TONES

MARCH 26//WITH GOLD UP $24.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 13.17 TONNES INTO THE GLD/INVENTORY RESTS AT 949.15 TONNES

MARCH 25/WITH GOLD DOWN $11.40 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.99 TONES INTO THE GLD INVENTORY////INVENTORY RESTS AT 935.98 TONNES

MARCH 24//WITH GOLD UP $67.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 15.80 TONNES OF GOLD INTO GLD////INVENTORY RESTS AT 923.99 TONNES..THIS PROVES THAT THE GLD IS A FRAUD AS LONDON SUSPENDED DELIVERY AS WELL AS ALL REFINERS. THEY HAD NO WAY OF GETTING ANY PHYSICAL OZ INTO ITS INVENTORY//

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

APRIL 22/ GLD INV 1042.46 tonnes*

IN LAST 804 TRADING DAYS: +96.12 NET TONNES HAVE BEEN REMOVED FROM THE GLD

LAST 704 TRADING DAYS;+271.10 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

APRIL 22/WITH SILVER UP 42 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY: A PAPER WITHDRAWAL OF 1.865 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 410.774 MILLION OZ//

APRIL 21//WITH SILVER DOWN 60 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER ADDITION OF 1.398 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 412.639 MILLION OZ//

APRIL 20//WITH SILVER UP 16 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.797 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 414.038 MILLION OZ//

APRIL 17/WITH SILVER DOWN 24 CENTS TODAY; A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.3999 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 16/WITH SILVER UP 5 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 15//WITH SILVER DOWN 45 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV TWO HUGE DEPOSITS: A DEPOSIT OF 1.679 MILLION OZ AND ANOTHER 5.222 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 14./WITH SILVER UP 51 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A MASSIVE PAPER DEPOSIT OF XXX MILLION OZ//INVENTORY RESTS AT 408.536 MILLION OZ//

APRIL 13//WITH SILVER DOWN 29 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 6.155 MILLION OZ////INVENTORY RESTS AT 408.536 MILLION OZ//

APRIL 9/WITH SILVER UP 60 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUGE DEPOSIT OF 1.84 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 402.381 MILLION OZ.

APRIL 8//WITH SILVER DOWN 21 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 401.541 MILLION OZ///

APRIL 7/WITH SILVER UP 26 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.766 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 395.826 MILLION OZ

APRIL 6/WITH SILVER UP 50 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 395.826 MILLION OZ.

APRIL 3//WITH SILVER DOWN 15 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 746,000 OZ INTO THE SLV//INVENTORY RESTS AT 395.826 MILLION OZ

APRIL 2/WITH SILVER UP 65 CENTS; A SMALL CHANGE TODAY..A WITHDRAWAL OF .335 MILLION OZ TO PAY FOR FEES//INVENTORY RESTS AT 394.826 MILLION OZ/

APRIL 1/WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 395.181 MILLION OZ//

MARCH 31/WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 1.679 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 375.181 MILLION OZ//

MARCH 30/WITH SILVER DOWN 44 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 393.502 MILLION OZ.

MARCH 27/WITH SILVER DOWN 5 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTROUS PAPER DEPOSIT OF 8.115 MILLION OZ INTO THE SLV../INVENTORY RESTS AT 393.502 MILLION OZ//

MARCH 26/WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 385.387 MILLION OZ///

MARCH 25/WITH SILVER UP 44 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSITS OF 7.369 MILLION OZ AND 2.239 MILLION OZ OF PAPER SILVER INTO THE SLV////INVENTORY RESTS AT 385.387 MILLION OZ//

MARCH 24//WITH SILVER UP 100 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 375.779 MILLION OZ///

APRIL 22.2020:

SLV INVENTORY RESTS TONIGHT AT

410.774 MILLION OZ.

END

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 1.69/ and libor 6 month duration 1.02

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .67

GOLD UNAVAILABLE//CENTRAL BANKS CALLING IN THEIR GOLD LEASES.

XXXXXXXX

12 Month MM GOFO

+ 0.96%

LIBOR FOR 12 MONTH DURATION: 0.99

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.03

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Gold Will Reach $3,000/oz: “Fed Can’t Print Gold” and Is “Ultimate Store Of Value” – Bank of America

The shortage of small and large gold bullion coins and bars continues and may deepen as prices move higher and we enter the next phase of the crisis – a massive economic crisis.

Due to our direct relationships with leading refineries and as Authorised Distributors of government mints, we continue to sell gold bars (1 oz, kilo and 400 oz) and silver bars (1,000 oz) and gold coins including Gold Sovereigns and Britannias (late May delivery) and Gold Nuggets or Kangaroos in volume. Online trading is suspended and you must call our trading trade to order coins and bars for delivery and storage. Our premiums have risen to reflect the rise in wholesale premiums from our mint and refinery partners, but we continue to have some of the most competitive premiums in the world.

NEWS and COMMENTARY

Gold to Reach $3,000—50% Above Its Record, Bank of America Says

“Fed Can’t Print Gold”: BofA Calls Gold “Ultimate Store Of Value”, Raises Price Target To $3,000

London, Gold Hub for Centuries, Eyes Delivery ‘Around the World’

Billionaire Ray Dalio says coronavirus marks the start of a technology driven ‘Brave New World’

Central Banks Have Pumped An Annualized $23.4 Trillion Into The Financial System

US Oil Fund drops 25% after changing structure again as popular ETF tries to stave off collapse

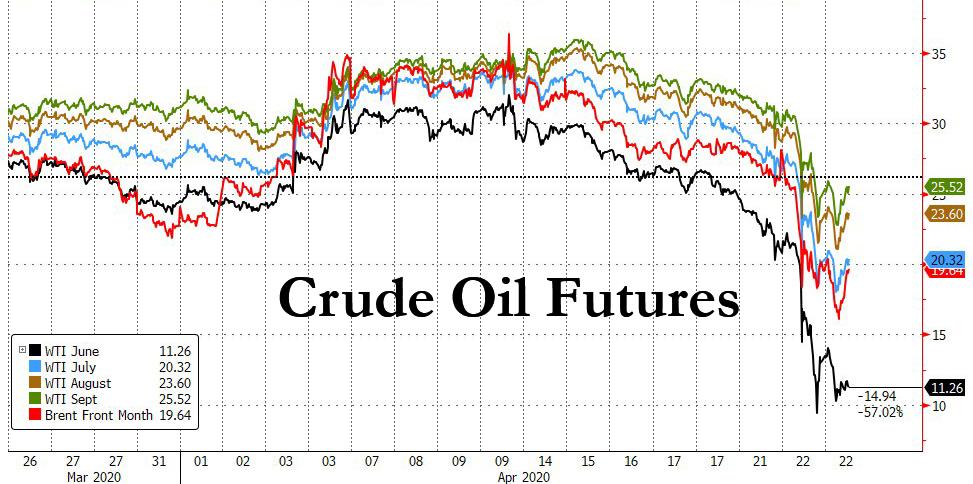

How could a futures contract for crude oil fall to minus $37 a barrel?

The Experts Have No Idea How Many COVID-19 Cases There Are

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

21-Apr-20 1678.60 1682.05, 1328.16 1364.82 & 1548.00 1547.82

20-Apr-20 1684.95 1686.20, 1349.14 1355.70 & 1547.63 1551.98

17-Apr-20 1693.15 1692.55, 1362.48 1354.04 & 1564.47 1555.79

16-Apr-20 1717.85 1759.50, 1378.57 1382.91 & 1581.45 1589.06

15-Apr-20 1712.25 1718.65, 1367.92 1377.33 & 1566.02 1580.99

14-Apr-20 1715.85 1741.90, 1367.36 1383.07 & 1567.91 1588.26

09-Apr-20 1662.50 1680.65, 1339.48 1348.22 & 1529.00 1538.13

08-Apr-20 1649.05 1647.80, 1328.27 1330.27 & 1517.00 1513.14

07-Apr-20 1652.20 1649.25, 1344.23 1333.75 & 1519.53 1511.21

06-Apr-20 1636.60 1648.30, 1330.72 1341.06 & 1515.49 1526.66

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here

ii) Important gold commentaries courtesy of GATA/Chris Powell

Most analysts are looking for a drop in the value of the dollar

London’s Financial Times/GATA)

Dollar’s long-term prospects turn gloomy, analysts say

Submitted by cpowell on Tue, 2020-04-21 15:30. Section: Daily Dispatches

By Eva Szalay and Colby Smith

Financial Times, London

Tuesday, April 21, 2020

The U.S. dollar is heading for a drop toward the end of this year, according to strategists, in what would mark a reversal from a record-breaking surge when coronavirus first washed over markets.

The world’s most important currency shot higher in March, reaching its strongest ever point when stock and bond markets suffered the most intense phase of the pandemic’s impact. A month later, the dollar — widely considered a haven in times of stress — remains unusually strong.

But some analysts and investors are confident that the tide will soon shift, after central banks around the world acted to ease the flow of dollars around the financial system. Big cuts in U.S. interest rates, which are much larger than those in other big economies, are also likely to drag down the dollar in the coming months, they say.

“The most bearish outcome for the dollar is that the global economy recovers as expected and the U.S. Federal Reserve stays dovish,” said Eric Stein, a portfolio manager at Eaton Vance. “We are seeing some of the conditions for a weaker dollar slotting into place.” …

… For the remainder of the report:

https://www.ft.com/content/3e994fd6-4dd2-4f0e-97bc-462aad04fafc

END

Believe it or not but the huge demand for gold and silver coins only represents 8% of demand

(Jan Nieuwenhuijs/GATA)

Jan Nieuwenhuijs: Coin demand of little relevance to the gold price

Submitted by cpowell on Tue, 2020-04-21 16:22. Section: Daily Dispatches

12:21p ET Tuesday, April 21, 2020

Dear Friend of GATA and Gold:

Voima Gold researcher Jan Nieuwenhuijs writes today that demand for gold and silver coins has little influence on the price of the monetary metals because coins constitute only about 8 percent of demand, far less than the institutional demand for metal in the wholesale market.

Of course institutional demand in the wholesale market is enormously distorted by the fractional-reserve gold and silver banking system, in which a vast imaginary supply is created, a supply many times larger than the actual metal available. Nieuwenhuijs’ commentary today disparaging the regard for coin prices does not acknowledge this.

…

So which prices are more distorted — retail coin prices or wholesale prices for gold not actually delivered? What is the real price of real gold?

Voima is in the gold business, so one can always contact the company to see if it’s selling at the “spot” price anything you can hold in your hand that feels more like metal than paper.

Nieuwenhuijs’ commentary is headlined “Coin Demand of Little Relevance to the Gold Price” and it’s posted here:

https://www.voimagold.com/insight/coin-demand-of-little-relevance-to-the…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Craig Hemke correctly stated that oil went no bid. He questions whether gold will go no offer..that is nobody will want to part with physical gold

(Courtesy Craig Hemke/Sprott)

Craig Hemke at Sprott Money: Oil went no bid, so can gold go no offer?

Submitted by cpowell on Tue, 2020-04-21 21:26. Section: Daily Dispatches

5:20p ET Tuesday, April 21, 2020

Dear Friend of GATA and Gold:

Yesterday the oil futures market went no bid, apparently for the first time in history, and with oil storage facilities full everywhere, trapped longs who weren’t ready to take delivery had to pay others to do so. With the world’s economy crippled by virus epidemic regulations, nobody wanted what used to be called black gold. You had to pay people to take oil off your hands.

…

Today the TF Metals Report’s Craig Hemke, writing at Sprott Money wonders if another unprecedented phenomenon could happen in the gold futures market — wonders if, amid increasing signs of scarcity of metal as world money supplies explode to infinity, the gold futures market could go no offer, with nobody willing to sell, or at least not to sell anywhere near current prices.

Hemke writes: “We now know that quite literally anything is possible in 2020 — from global pandemics to economic collapse to QE to infinity to -$40 crude. As such a complete implosion and restructuring of the global pricing scheme for precious metal is not out of the question in the weeks and months ahead.”

Hemke’s analysis is headlined “Crude Collapse Concerns Comex” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/crude-collapse-concerns-comex-craig-hem…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Butler angry at the CME and CFTC for allowing the banks to win on that huge oil fall

(Courtesy Ted Butler)

Ted Butler: Common sense and the CME Group

Submitted by cpowell on Tue, 2020-04-21 23:50. Section: Daily Dispatches

By Ted Butler

SilverSeek.com

Tuesday, April 21, 2020

Monday’s spectacular and unprecedented collapse of oil prices is, rightly so, the subject of nonstop commentary. Already considered depressed on Friday’s close, at $18.27 per barrel, the he May NYMEX crude oil futures contract, at Monday’s official settlement price, had fallen to negative $37.63, down $55.90.

Most observers asked how the heck this was possible — how could a futures contract for crude oil fall to minus $37 a barrel?

…

The process by which the negative price was determined was illegitimate, as is the exchange on which it trades, the NYMEX, as well as the owner-operator of the exchange, the CME Group (which also owns and operates the COMEX).

Yes, I’m fully-aware that the CME Group runs the largest energy and precious metals derivatives exchanges in the world, but since when did size alone guarantee integrity and legitimacy? …

… For the remainder of the analysis:

http://silverseek.com/commentary/common-sense-and-cme-group-17911

Common Sense and the CME Group

|

April 21, 2020 – 1:21pm

Monday’s spectacular and unprecedented collapse of oil prices is, rightly so, the subject of non-stop commentary. Already considered depressed on Friday’s close, at $18.27/bbl., the May NYMEX crude oil futures contract, at Monday’s official settlement price, had fallen to negative $37.63, down $55.90.

Most observers asked was how the heck was this possible – how could a futures contract for crude oil fall to minus $37 a barrel? The process by which the negative price was determined was illegitimate, as is the exchange on which it trades, the NYMEX, as well as the owner-operator of the exchange, the CME Group (which also owns and operates the COMEX). Yes, I’m fully-aware that the CME Group runs the largest energy and precious metals derivatives exchanges in the world, but since when did size alone guarantee integrity and legitimacy?

On Friday’s close, the May crude oil contract had 108,593 open contracts (1000 barrels per contract). On Monday’s close, 13,044 contracts remained open, meaning 95,549 contracts were closed out in Monday’s trading. While it’s impossible to determine from public data how many of those contracts were closed out at negative prices, clearly the longs got crushed and the short holders raked in profits. In trying to determine who was long and short going into Monday’s spectacular price collapse, data from the exchange and CFTC, in the form of the Commitments of Traders and Bank Participation reports are the best source.

Data from the most recent April Bank Participation Report (for positions as of April 7), indicate that 4 US commercial banks held a gross short position of 323,674 contracts or 13.8% of total NYMEX crude oil open interest. In addition, 20 foreign banks held a gross short position of 284,069 contracts or 12.1% of total open interest. Combined, US and foreign commercial banks held a gross short position of 607,743 contracts or 25.9% of total open interest. Since commercial banks held such a large share of the short position in NYMEX crude oil contracts, it is reasonable to conclude they were among the biggest winners in the spectacular oil collapse. The question is whether the big banks were just lucky to be in the right place at the right time, or had much to do with the spectacular collapse?

https://www.cftc.gov/MarketReports/BankParticipationReports/deaapr20f

A week or so ago, on April 8, the CME Group announced that it was prepared for the possibility of crude oil prices going negative and was making appropriate arrangements. Appropriate arrangements? What could possibly be appropriate about negative prices? Negative commodity prices are never legitimate, regardless of the stories concocted to explain them away. Next thing we’ll hear from the CME is why gold and silver prices could trade at less than zero. I doubt that would occur if the exchange’s big insiders weren’t short.

https://www.cmegroup.com/notices/clearing/2020/04/Chadv20-152.html#pageNumber=1

The real culprits are those who have sold us a bill of goods, particularly the exchange operators (the CME Group) and those profiting from the phony computer-generated high frequency trading that has come to dominate the price discovery process. Particularly shameful has been the role of the CFTC, which sits by and lets the CME and the banks (especially JPMorgan) do whatever they want.

This move to negative oil prices (which undoubtedly benefitted JPM again) should concern just about everyone. There is absolutely nothing legitimate about negative oil prices and all the soothing stories about there being no storage only makes negative prices legitimate if we suspend our common sense. It was essentially a less than one day phenomenon that caught unsuspecting longs out of position and unprepared for the impossible to imagine. That’s not legitimate price discovery; that’s little more than highway robbery. It’s time we demand that the CFTC get off its butt and put an end to the phony pricing.

Ted Butler

April 21, 2020

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

S&P Futures Rebound As Oil Buyers Emerge

&P futures rebounded alongside European and Asian stocks on Wednesday as oil pared its recent historic losses and upbeat quarterly earnings reports lifted investor sentiment following a two-day selloff due to a record crash in oil prices, even as companies warned of more pain in the coming months. Treasurys and the dollar dropped while gold gained, rising above $1700.

Emini futures climbed after the cash index dropped more than 3% a day earlier, when investors shrugged off the progress of a fresh relief package to counter the economic hit from the coronavirus. The Stoxx Europe 600 Index rose broadly in the wake of Tuesday’s slump.

Earlier in the session, Asian stocks gained, led by energy and communications, after falling in the last session. Markets in the region were mixed, with India’s S&P BSE Sensex Index and Jakarta Composite rising, and Japan’s Topix Index and Australia’s S&P/ASX 200 falling. The Topix declined 0.6%, with Istyle and Financial Products Group falling the most. The Shanghai Composite Index rose 0.6%, with Junzheng Energy and Ningbo Construction posting the biggest advances

The S&P 500 index fell nearly 5% in the first two days of the week as May WTI contracts plunged below zero for the first time ever, and the benchmark Brent hovered near 1999-lows, triggering alarm about the hit to the global economy from a near halt in business activity.

Texas Instruments headed higher in thin premarket trading as it reported better-than-expected first-quarter results and said a strong inventory allowed it to be prepared for the disruptions caused by the pandemic. Netflix deemed a “stay-at-home” stock as the wide restrictions boost demand for online streaming services, more than doubled its own projections for new customers in the first quarter. However, its shares fell 2% as the company failed to translate the subscriber surge into additional revenues, while forecasting a weaker second half if the lockdown measures were to be lifted. Chipotle reported soaring digital and home delivery sales and said it had enough cash and liquidity to get through the next year.

Trader attention remains glued to oil, with Brent crude erasing a tumble that reached as much as 17% overnight, while West Texas oil also pared most of its slide, even though the June contract was trading just above single digits.

Yesterday, OPEC Delegates discussed the oil market crisis within a conference call; although the call was reportedly not designed to make a new oil decision and they were said to consider a May 10th meeting for further production cuts. Furthermore, Saudi, UAE, and Kuwait did not take part in the call and a delegate noted that OPEC+ members will be unable to start production cuts earlier because April’s oil production is already committed for export contracts. Meanwhile, the Iraq Energy Minister said OPEC+ could take additional steps to absorb the oil surplus but added that taking further measures by producer countries depends on global market development and compliance by other OPEC+ and other non-member producers with the oil cut deal. Russia again downplayed the gravitas of the oil market situation. Elsewhere, the fallout from the Texas Railroad Commission meeting saw two out of three Texas Oil and Gas regulators stated they are not ready to vote on oil output cuts today and they are to revisit the issue on May 5th. Sticking with North America, sources stated that producers in Alberta, Canada have reportedly already voluntarily cut 400k-700k BPD, according to Energy Intel. The contracts saw further downside as EU trade got underway, with WTI June resided under USD 11/bbl whilst Brent held onto losses of over 10% and eyed USD 17/bbl to the downside; however, since then we have recovered somewhat in what has been choppy trade for the complex but, ultimately, are in proximity to the lows – particularly for WTI, which ekes mild gains at the time of writing

The one thing that can definitively send oil sharply higher is a reopening in the global economy, and to this end, governments are devising ways to return people to work even as they discover infections are more extensive than they insisted only weeks ago. The coronavirus killed two people in California in early and mid-February, suggesting the pathogen was circulating in the U.S. weeks earlier than health officials thought. While Germany and a few other countries are moving to relax lockdown measures to contain outbreaks, Singapore – a global standard bearer for taming the deadly illness early on – has now become home to Southeast Asia’s largest recorded outbreak and is racing to regain control.

Meanwhile, corporate earnings have been mixed. Consumer-goods companies from brewers to paint-makers sounded notes of caution on spending. Heineken NV canceled its interim dividend, while Kering said it doesn’t see a recovery in the U.S. or Europe before at least June or July after sales at its flagship brand Gucci tumbled.

“There’s no way you can predict earnings right now,” Michael Cuggino, portfolio manager at Pacific Heights Asset Management LLC, said on Bloomberg TV. “It’s virtually impossible until we have more visibility with respect to how to world comes out of the coronavirus on the other side.”

Treasuries edged lower along with the dollar and European bonds fell. As Bloomberg reported yesterday, European policymakers plan to hold a call on Wednesday evening where they may discuss whether to accept junk-rated debt as collateral from lenders. Related to that, Italian bond yields and the risk premium the sovereign pays on its debt rose on Wednesday as the funding of the already heavily indebted country’s coronavirus stimulus plans remained uncertain. It may take European Union countries until the summer or even longer to agree on how to finance an economic recovery from the coronavirus pandemic as major disagreements still persist, an official with the bloc said on Wednesday.

“What we’re generally seeing is that there is less possibility that we are going to get some sort of conclusion on Thursday and even beyond that,” said Peter McCallum, rates strategist at Mizuho, referring to an EU summit on Thursday where measures to support coronavirus-hit economies will be discussed.

Yields across Italy’s curve rose, with the 10-year yield up as much as 10 basis points to 2.27%, a new peak since March 18, when the ECB announced its emergency purchase programme after trading hours. The gap between its 10-year bond yield and Germany’s – effectively the risk premium Italy pays – rose as high as 271 basis points, just five basis points away from touching their highest since the announcement of the emergency measures.

Spanish bonds extended declines and underperformed euro-area debt after the nation’s Treasury launched a massive 10-year syndicated debt sale.

In FX, a dollar gauge snapped two days of gains as European stock markets and U.S. equity futures rebounded. The dollar slipped versus all G10 peers; The Australian dollar advanced against its Group-of-10 peers after leveraged funds covered short positions exposed by better-than- expected retail sales data. Japan’s government bonds rose as the slump in oil prices raised concern about the global economic outlook, prompting demand for haven assets; the yen advanced for the first time in three days. Economic data include mortgage applications. AT&T, Thermo Fisher and Biogen are among companies reporting earnings.

Market Snapshot

- S&P 500 futures up 1.2% to 2,764.25

- STOXX Europe 600 up 1.1% to 327.88

- MXAP up 0.2% to 141.41

- MXAPJ up 0.7% to 457.74

- Nikkei down 0.7% to 19,137.95

- Topix down 0.6% to 1,406.90

- Hang Seng Index up 0.4% to 23,893.36

- Shanghai Composite up 0.6% to 2,843.98

- Sensex up 1.9% to 31,216.92

- Australia S&P/ASX 200 unchanged at 5,221.25

- Kospi up 0.9% to 1,896.15

- Brent Futures down 9.2% to $17.56/bbl

- Gold spot up 0.6% to $1,695.43

- U.S. Dollar Index down 0.1% to 100.16

- German 10Y yield rose 2.0 bps to -0.457%

- Euro down 0.02% to $1.0856

- Brent Futures down 9.2% to $17.56/bbl

- Italian 10Y yield rose 21.4 bps to 1.978%

- Spanish 10Y yield rose 10.4 bps to 1.108%

Top Overnight News

- Singapore reported more than 1,000 new cases for the third straight day. New coronavirus cases in Germany stayed close to a three-week low as the country begins gradually lifting lockdown measures

- The U.K. bond market looks set to face a flood of bond sales that dwarfs the current record for government borrowing set during the global financial crisis

- ECB policy makers will hold a call on Wednesday evening where they may discuss whether to accept junk-rated debt as collateral from lenders

- The euro area’s run of record-breaking government bond sales has continued in Spain, highlighting that demand for the region’s higher-yielding securities remains robust, when the price is right

- Global funding markets are beginning to diverge — easing in the U.S. while still showing signs of stress in Europe

- Oil’s plunge below zero for the first time in history has broken the models that many traders rely on to calculate risk. For Wall Street’s biggest banks, that has meant a franticscramble over the past 24 hours to recalculate the value and riskiness of their trading books

Asian equity markets initially extended on losses as the subdued tone rolled over once again from Wall St where sentiment was pressured by the continued oil market rout, but initially finished relatively mixed. Price action included the WTI June contract prices briefly slipping to single digits and with underperformance in tech amid President Trump’s plans for an immigration ban given the sector’s reliance on foreign talent. ASX 200 (U/C) and Nikkei 225 (-0.7%) were weaker with Australia dragged lower by the mining related sectors and as corporate updates trickled in with Beach Energy also suffering from softer quarterly production, while the Japanese benchmark briefly fell below 19k as the recent detrimental currency flows reverberated across exporter names. Hang Seng (+0.4%) and Shanghai Comp. (+0.6%) conformed to the subdued global risk tone but with losses in the mainland limited by anticipation of further support after Chinese President Xi pledged stronger macro policy tools to soften the epidemic fallout and the State Council noted that China will boost targeted assistance to those in need, as well as small businesses. Finally, 10yr JGBs advanced as the took advantage of the weakness in stocks and amid the BoJ’s presence in the market today for JPY 710bln of JGBs heavily concentrated in 3yr-10yr maturities.

Top Asian News

- China’s Banks Hit by Increase in Bad Loans in First Quarter

- India Eases Up on Currency Intervention, Protecting Reserves

- Bank Indonesia Says IDR Exchange Rate Stability Maintained

- Bank Indonesia Makes First Direct Purchase of Government Bonds

European equity futures see tailwinds from the turnaround in sentiment at the end of the APAC session (Euro Stoxx 50 +1.1%), with US equity futures also posting gains in excess of 1% in early trade. Sectors see broad-based gains, albeit energy lags as the complex remains under pressure from storage scarcity. In term of the breakdown, Tech names lead the gains following earnings from STMicroelectronics (+6.2%), whilst the sector also sees tailwinds from Texas Instruments (+3.0% pre-mkt), with the former, despite misses on its metrics, noted that Q1 was exited with stable net financial position, over USD 2.5bln in liquidity and available credit facilities above USD 1bln. Looking at other movers, Roche (+1.7%) is supported post earnings in which it topped estimates and pharma sales rose 7% YY. The Co. also stated that Clinical Phase III study to evaluate the safety and efficacy of Actemra/Roactemra in severe COVID-19 pneumonia is ongoing in several countries, with results expected in early summer, adding there is capacity for a rapid increase of production. On the flip side, Credit Suisse (+0.4%) is hampered vs. the region after it stated it is to take an additional EUR 900mln loan loss provisions in Q1. Finally, other earnings-related movers include Akzo Nobel (+7.9%), Ericsson (+6.4%) and Kering (-5.42), the latter reported a decline in Gucci sales of 23.2% YY.

Top European News

- Spain Follows Italy With Record-Setting Bond Demand at Sale

- EU Braces for Tense Call as Leaders Given No Plan to Work On

- Heineken Pulls Payout, Kering’s Gucci Sales Slump: Earnings Wrap

In FX, another swing in broad risk sentiment amidst less pronounced pressure on oil and other commodities has aided the latest Aussie, Kiwi and Loonie recovery, but with the former also benefiting from a short squeeze in wake of a record rise in retail sales per preliminary data for March. Aud/Usd took some time to digest the release and acknowledge the fact that stock-piling for COVID-19 boosted consumption, but subsequently breached 0.6300 on the way to circa 0.6350 with stops tripped above 0.6325 and macro fund offers over 0.6340 absorbed along the way. Meanwhile, Nzd/Usd retested 0.6000, albeit with a lag as Aud/Nzd rebounded from sub-1.0550 to around 1.0580, and Usd/Cad has retreated between 1.4237-1.4139 parameters on the aforementioned relative stability in crude prices ahead of Canadian CPI.

- GBP/SEK/NOK – Sterling has unwound some of its recent underperformance on technical rather than fundamental grounds given Cable remaining above the 30 DMA (1.2257) and revisiting 1.2300+ levels, while Eur/Gbp has reversed towards 0.8800 as the DXY meanders within a tight band on the 100.000 handle and single currency continues to straddle 1.0850. Similarly, the Scandis are seeing some reprieve from oil and pandemic risk aversion, with Eur/Nok and Eur/Sek both off highs near 11.5950 and 10.9700 respectively and the Swedish Krona weighing up more unconventional Riksbank easing in the form of municipal QE in the run up to next week’s official policy meeting.

- JPY/EUR/CHF – All sticking to pretty narrow and well trodden recent confines vs the Dollar, as the Yen flits from 107.86 to 107.52, Euro hovers below 1.0900 and above 1.0800 amidst decent option expiry interest at the former (1.5 bn) and 1.0825 (1 bn), and Franc pivots 0.9700.

- EM – Softer than expected SA CPI has not hindered the Rand amidst the overall upturn in risk appetite, but the Lira is treading more cautiously into the CBRT even though the Central Bank has already lifted FX swap limit transactions to 30% from 20% in what may be an effort to keep Usd/Try under 7.0000 in the event that rates are cut again, as widely expected, but perhaps more than the -50 bp consensus. On that note, the Mexican Peso seems to have taken Banxico’s emergency ½ point ease in stride or at least lubricated by the less fractious state of trade in crude markets.

- Australian Retail Sales (Mar P) 8.2% (Prev. 0.5%); largest increase on record. ABS said the March sales data indicated unprecedented demand for food retailing industry. (Newswires)

In commodities, WTI and Brent front month futures remain choppy, but ultimately mixed this morning, with WTI swinging between gains and losses whilst Brent remained in the red for the entirety of the session thus far. Yesterday, OPEC Delegates discussed the oil market crisis within a conference call; although the call was reportedly not designed to make a new oil decision and they were said to consider a May 10th meeting for further production cuts. Furthermore, Saudi, UAE, and Kuwait did not take part in the call and a delegate noted that OPEC+ members will be unable to start production cuts earlier because April’s oil production is already committed for export contracts. Meanwhile, the Iraq Energy Minister said OPEC+ could take additional steps to absorb the oil surplus but added that taking further measures by producer countries depends on global market development and compliance by other OPEC+ and other non-member producers with the oil cut deal. Russia again downplayed the gravitas of the oil market situation. Elsewhere, the fallout from the Texas Railroad Commission meeting saw two out of three Texas Oil and Gas regulators stated they are not ready to vote on oil output cuts today and they are to revisit the issue on May 5th. Sticking with North America, sources stated that producers in Alberta, Canada have reportedly already voluntarily cut 400k-700k BPD, according to Energy Intel. The contracts saw further downside as EU trade got underway, with WTI June resided under USD 11/bbl whilst Brent held onto losses of over 10% and eyed USD 17/bbl to the downside; however, since then we have recovered somewhat in what has been choppy trade for the complex but, ultimately, are in proximity to the lows – particularly for WTI, which ekes mild gains at the time of writing. Looking at the metals market, spot gold benefits from the Dollar pullback and reclaimed its USD 1700/oz handle. While copper trades subdued around USD 2.25/bbl, with miner Antofagasta stating that Q1 copper production rose almost 5% YY.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 7.3%

- 9am: FHFA House Price Index MoM, est. 0.3%, prior 0.3%

DB’s Jim Reid concludes the overnight wrap

Markets stuck to the risk-off theme once again yesterday, as a negative cocktail of oil market turmoil, weak corporate earnings and concerns about Europe conspired to make this a more difficult week so far for equities. Indeed, with the S&P 500 down a further -3.07% yesterday, that means the index has had its worst start to a week for 5 weeks, back when markets were at their most tumultuous. And in another warning sign, the VIX index has also had its largest 2-day increase since it hit its peak back in mid-March.

All eyes were on oil once again yesterday, where governments tried unsuccessfully to contain the rout. Brent Crude fell below $20/barrel for the first time since 2002 and down -24.40% on the day. Things haven’t gotten any better overnight where it’s down another -12.62% to $16.89/bbl. May WTI settled yesterday at $10.01 but the previous day’s shenanigans (lows of -$37.63) extended into the June contract which was down -43.37% to $11.57 and is trading at $10.90 this morning. As our oil analyst Michael Hsueh pointed out the previous evening, negative pricing could extend into the June contract so the sharp move wasn’t a surprise.

OPEC ministers did not decide on any new policy measures on an unscheduled call last night, which followed reports earlier in the day that they’d start their planned output cuts immediately rather than waiting until the start of May. In a joint closing statement the ministers said that they should “continue holding such consultations”, but it remains unclear if any country has the ability or the inclination to cut further than what is expected to come on May 1. Meanwhile President Trump tweeted that “We will never let the great U.S. Oil & Gas Industry Down”, and that he’d instructed the Energy and Treasury Secretaries “to formulate a plan which will make funds available so that these very important companies and jobs will be secured long into the future!” Unsurprisingly, oil-producing currencies took a hit once again, with the Russian Ruble (-2.00%) and the Norwegian Krone (-1.85%) both suffering against the US dollar.

Other global equity markets joined the S&P lower, with the NASDAQ (-3.48%), the STOXX 600 (-3.39%) and the DAX (-3.99%) all seeing major declines. One sector that had a bad day were European banks, with the STOXX Banks index down -4.60% at its lowest ever level since the index began in the late 1980s, having now lost almost half its value since the start of this year. The overall risk-off came against the backdrop of some weak corporate earnings. Netflix surged +12% right after the closing bell, but within 2 hours had given the entire post-market rally to be back near unchanged. The online streaming company announced nearly 16 million subscribers (nearly double consensus estimates of 8.47 million), but the company’s guidance did not deliver as the company is forecasting a number of subscriptions will be cancelled when confinement ends. Going through the other highlights, Coca Cola (-2.24%) said that they’d experienced a global volume decline of around 25% since the start of April with sales outside the home suffering thanks to the pandemic. Lockheed Martin (-2.32%) lowered their sales outlook, while HCA Healthcare (-4.50%) withdrew their 2020 guidance and suspended their quarterly dividend programme. In Europe, PSA (+0.26%) said that they expected the European vehicle market to shrink by 25% this year, as they announced a 15.6% decline in their Q1 sales.

The overnight session has seen markets in Asia follow Wall Street’s lead however the good news is that the declines are more modest. Indeed the Nikkei (-1.06%), Hang Seng (-0.50%), Shanghai Comp (-0.16%), ASX (-0.14%) and Kospi (-0.81%) are all posting small declines. Elsewhere, futures on the S&P 500 are up +0.30% while yields on 10y USTs are down -1.8bps to 0.553%.

In other news, the US senate passed $484bn in new pandemic relief funds yesterday. President Trump said soon after that he would sign the legislation and then turn to the next round of stimulus which is said to include aid to state and local governments and coronavirus caregivers, amongst others. The bill is likely to be voted on in the House today before it moves to President Trump’s desk. Trump also said in an overnight press conference that he’ll ask larger companies to return money they accessed from the federal stimulus package because it was intended to help small businesses while at the same conference Treasury Secretary Mnuchin threatened “severe consequences” for such companies. Trump also gave clarity on his decision on stopping immigration, saying the pause will be in effect for 60 days and will apply only to individuals seeking permanent residency with some exceptions and he will likely sign the order today.

Ahead of tomorrow afternoon’s European Council videoconference, there was a Reuters story yesterday which said that EU member states were moving closer to an agreement that would see the next long-term budget used for a stimulus package, rather than being done through coronabonds or some other form of joint debt issuance. However, the report also said that leaders continue to disagree on the implementation and “seem virtually certain to defer any final decision”. This was later backed up by Italian Prime Minister Conte, who said he didn’t think that leaders would manage to reach a “definitive solution” tomorrow. However he did say he was ready to work with the EU on a new ESM line which was seen as conciliatory.