GOLD::$1724.75 UP $10.00 The quote is London spot price

Silver$15.14 UP 0 CENTS

Closing access prices: London spot

i)Gold : $1730.50 LONDON SPOT 4:30 pm

ii)SILVER: $15.24//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

APRIL comex gold price CLOSE 1.30 PM: $XX

MAY COMEX GOLD: 1732.30 1:30 PM

JUNE GOLD: $1742.50 CLOSE 1.30 PM// SPREAD SPOT/FUTURE JUNE: $17.75.//PREMIUMS WENT DOWN AGAIN

CLOSING SILVER FUTURE MONTH

SILVER APRIL COMEX CLOSE: XXX

SILVER MAY COMEX CLOSE; $15.30-…1:30 PM.//SPREAD SPOT/FUTURE MAY: 16 CENTS PER OZ//PREMIUMS DOWN AGAIN

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2800. usa per oz

and silver; $31.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

DO NOT PAY ANY ATTENTION TO WHAT THE CROOKS ARE DOING AT THE COMEX AND LONDON LBMA..PHYSICAL IS THE NAME OF THE GAME AND NOTHING ELSE

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 58/432

issued: 288

EXCHANGE: COMEX

CONTRACT: APRIL 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,728.700000000 USD

INTENT DATE: 04/22/2020 DELIVERY DATE: 04/24/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

118 H MACQUARIE FUT 25

132 C SG AMERICAS 70

159 C ED&F MAN CAP 9

657 C MORGAN STANLEY 9

657 H MORGAN STANLEY 90

661 C JP MORGAN 288 58

685 C RJ OBRIEN 6

686 C INTL FCSTONE 71 20

690 C ABN AMRO 65 123

737 C ADVANTAGE 6 11

800 C MAREX SPEC 2

878 C PHILLIP CAPITAL 1

905 C ADM 10

____________________________________________________________________________________________

TOTAL: 432 432

MONTH TO DATE: 31,007

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 432 NOTICE(S) FOR 43200 OZ (1.343 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 31,007 NOTICES FOR 3,100,700 OZ (95.10 TONNES)

SILVER

FOR APRIL

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 806 for 4,025,000 oz

BITCOIN MORNING QUOTE $7099 DOWN 17

BITCOIN AFTERNOON QUOTE.: $7528 UP $403

GLD AND SLV INVENTORIES:

WITH GOLD UP $10.00: AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD//

GLD: 1,042.46 TONNES OF GOLD//

WITH SILVER UP 0 CENTS TODAY: AND WITH NO SILVER AROUND

ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV:

A DEPOSIT OF 2.891 MILLION OZ INTO THE SLV//

RESTING SLV INVENTORY TONIGHT:

SLV: 413.665 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A STRONG SIZED 1933 CONTRACTS FROM 139,607 UP TO 141,540 AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE GOOD SIZED GAIN IN OI OCCURRED WITH OUR CONSIDERABLE 42 CENT GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS DUE TO SOME BANKER SHORT COVERING PLUS A CONSIDERABLE EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION ALONG WITH OUR ZERO GAIN IN SILVER OZ STANDING. WE HAD A VERY GOOD NET GAIN IN OUR TWO EXCHANGES OF 3001 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A STRONG AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: MARCH: 00 AND MAY: 850 AND JULY: 0 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 850 CONTRACTS. WITH THE TRANSFER OF 850 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 850 EFP CONTRACTS TRANSLATES INTO 4.250 MILLION OZ ACCOMPANYING:

1.THE 42 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.145 MILLION OZ INITIALLY STANDING FOR APRIL

WEDNESDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 42 CENTS).. BUT, OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE SOME SILVER LONGS FROM THEIR POSITIONS, AS WE DID HAVE A GOOD NET GAIN OF 2783 CONTRACTS OR 13.915 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

OUR SPREADING OPERATION HAS NOW SWITCHED INTO SILVER…..

SPREADING OPERATION FOR OUR NEWCOMERS:

WE HAVE NOW COMMENCED IN SILVER THE ILLEGAL SPREADING OPERATION \ FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW STOPPED IN GOLD AS THEY NOW BEGIN TO MORPH INTO SILVER AS WE HEAD TOWARDS THE NEW FRONT MONTH WILL BE MAY.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF APRIL. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

15,326 CONTRACTS (FOR 15 TRADING DAYS TOTAL 15,326 CONTRACTS) OR 76.63 MILLION OZ: (AVERAGE PER DAY: 1021 CONTRACTS OR 5.108 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF APRIL: 76.63 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 10.95% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 970,11 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP SO FAR 76.63 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

EXCHANGE FOR PHYSICAL ISSUANCE THIS MONTH IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1933, WITH THE CONSIDERABLE 42 CENT GAIN IN SILVER PRICING AT THE COMEX ///WEDNESDAY… THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 850 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A STRONG SIZED OI CONTRACTS ON THE TWO EXCHANGES: 2783 CONTRACTS (WITH OUR 42 CENT GAIN IN PRICE)

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 850 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A STRONG INCREASE OF 1933 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 42 CENT GAIN IN PRICE OF SILVER/ AND A CLOSING PRICE OF $15.14 // TUESDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.7050 BILLION OZ TO BE EXACT or 100.7% of annual global silver production (ex Russia & ex China).

FOR THE NEW MAR DELIVERY MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR nil OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.145 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 4023 CONTRACTS TO 497,181 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE GAIN OF COMEX OI OCCURRED WITH OUR STRONG COMEX GAIN IN PRICE OF $40.75 /// COMEX GOLD TRADING// WEDNESDAY// WE HAD CONSIDERABLE BANKER SHORT COVERING , A GOOD INCREASE IN GOLD OZ STANDING AT THE COMEX, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A GOOD EX. FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR STRONG GAIN IN THE PAPER PRICE OF GOLD.

WE HAD NO ISSUANCE OF OUR NEW 4 GC CONTRACT

WE GAINED A STRONG 7231 CONTRACTS (22.49 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3208 CONTRACTS:

CONTRACTS, FEB> 0 CONTRACTS; MARCH 00 APRIL: 0. MAY: 0, AND JUNE 3208.; DEC 0 AND ALL OTHER MONTHS ZERO//TOTAL: 3208. The NEW COMEX OI for the gold complex rests at 497,181. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7231 CONTRACTS: 4023 CONTRACTS INCREASED AT THE COMEX AND 3208 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 7231 CONTRACTS OR 22.49 TONNES. WEDNESDAY, WE HAD HUGE GAIN OF $40.75 IN GOLD TRADING……

AND WITH THAT GAIN IN PRICE, WE HAD A STRONG SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 22.49 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (ROSE $40.75). AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WERE UNSUCCESSFUL (SEE BELOW).

4 GC ISSUANCE: ZERO

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A GOOD SIZED INCREASE IN EXCHANGE FOR PHYSICALS (3208) ACCOMPANYING THE GAIN IN COMEX OI (4023 OI): TOTAL GAIN IN THE TWO EXCHANGES: 8263 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)A STRONG INCREASE IN STANDING AT THE GOLD COMEX FOR THE FRONT APRIL MONTH, 3) ZERO LONG LIQUIDATION AND …ALL OF THIS WAS COUPLED WITH THAT STRONG GAIN IN GOLD PRICE TRADING//WEDNESDAY

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 66,505 CONTRACTS OR 6,650,500 oz OR 206.85 TONNES (15 TRADING DAYS AND THUS AVERAGING: 4433 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAY(S) IN TONNES: 206.85 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 206.85/3550 x 100% TONNES =5.82% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 2529.75 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 206.85 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 1933 CONTRACTS FROM 139,607 UP TO 141,540 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

ALL OF THE GAIN IN COMEX OI WAS DUE TO 1) SOME BANKER SHORT COVERING , 2) THE ISSUANCE OF A GOOD SIZED NUMBER OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A ZERO INCREASE IN SILVER OZ STANDING AT THE COMEX FOR APRIL AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 850 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR FEB. 0; FOR MAR 0: AND MAY: 850; JULY: 0 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 850 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE STRONG COMEX OI GAIN OF 1933 CONTRACTS TO THE 850 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 2783 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 13.915 MILLION OZ!!! WITH THE STRONG GAIN IN PRICE///

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 42 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// WEDNESDAY. WE ALSO HAD A GOOD SIZED 850 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 5.48 POINTS OR 0.19% //Hang Sang CLOSED UP 83,96 POINTS OR 0.35% /The Nikkei closed UP 291.49 POINTS OR 1.52%//Australia’s all ordinaires CLOSED DOWN .02%

/Chinese yuan (ONSHORE) closed UP at 7.0813 /Oil UP TO 15.42 dollars per barrel for WTI and 21.85 for Brent. Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0813 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.0925 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

total dealer deposits: nil oz

total dealer withdrawals: nil oz

i)we had 1 deposits into the customer account

into JPMorgan: 0

ii)into Delaware; 340,058.815 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.819 million oz of total silver inventory or 50.04% of all official comex silver. (160.819 million/321.170 million

total customer deposits today: 304,058.815 oz

we had 4 withdrawals:

i Out of Delaware: 4012.170 oz

ii) Out of Int. Delaware: 4908.485 oz

iii) Out of CNT: 313,804.820 oz

iv) Out of Scotia; 600,338.700 oz

total withdrawals; 923,064.175 oz

We had 1 adjustments: and all from the dealer to the customer:

i) from CNT: 297,559.404

total dealer silver: 81.137 million

total dealer + customer silver: 316.718 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The total number of notices filed today for the APRIL 2020. contract month is represented by 0 contract(s) FOR nil oz

To calculate the number of silver ounces that will stand for delivery in APRIL we take the total number of notices filed for the month so far at 806 x 5,000 oz = 4,025,000 oz to which we add the difference between the open interest for the front month of APRIL.(23) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL/2019 contract month: 806 (notices served so far) x 5000 oz + OI for front month of APRIL (23)- number of notices served upon today (0) x 5000 oz of silver standing for the APRIL contract month.equals 4,145,000 oz.

WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ OF SILVER WILL STAND AT THE COMEX.

TODAY’S ESTIMATED SILVER VOLUME: 64,333 CONTRACTS //

FOR YESTERDAY: 60,434 CONTRACTS..,CONFIRMED VOLUME

YESTERDAY’S CONFIRMED VOLUME OF 60,434 CONTRACTS EQUATES to 302 million OZ 43.16% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -0.84% ((APRIL 22/2020)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.35% to NAV: (APRIL 22/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 0.84%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.78 TRADING 15.69///DISCOUNT 0.58

END

And now the Gold inventory at the GLD/

APRIL 23/WITH GOLD UP $10.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS TONIGHT AT 1042.46 TONNES

APRIL 22/WITH GOLD UP $40.75 TODAY:; TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A)A MONSTROUS 3.8 PAPER TONNES WERE ADDED TO THE GLD INVENTORY AND B) ANOTHER HUGE 9.07 TONNES OF PAPER GOLD ADDED LATE IN THE DAY//INVENTORY RESTS AT 1042.46 TONNES

APRIL 21/WITH GOLD DOWN $21.60 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTROUS ADDITION OF 7.9 PAPER TONNES TO THE GLD INVENTORY//INVENTORY RESTS AT 1029.59 TONNES

APRIL 20//WITH GOLD UP $10.00 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1021.69 TONNES

APRIL 17/WITH GOLD DOWN $27.80 TODAY: SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1021.69 TONNES TONNES..THE STRING OF 12 STRAIGHT STRONG DEPOSITS ENDS..

APRIL 16/WITH GOLD DOWN $4.50 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG DEPOSIT OF 4.10 TONNES WAS ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 1021.69 TONNES/12TH STRAIGHT STRONG DEPOSIT

APRIL 15//WITH GOLD DOWN $19.10 TODAY; ANOTHER HUGE CHANGE IN GOLD INVENTORY; A STRONG 7.89 TONNES WAS ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 1117.59 TONNES.//11TH STRAIGHT STRONG DEPOSIT

APRIL 14/WITH GOLD UP $23.55 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 15.51 TONNES WAS ADDED TO THE GLD INVENTORY/INVENTORY RESTS AT 1009.70 TONNES//THIS IS THE 10TH STRAIGHT STRONG DEPOSIT//THIS IS A FRAUDULENT VEHICLE..THEY HAVE NO PHYSICAL GOLD IN THE TRUST..

APRIL 13//WITH GOLD UP $27.65 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 5.36 TONNES WAS ADDED TO THE GLD//INVENTORY RESTS AT 994.19 TONNES

APRIL 9 WITH GOLD UP $37.30 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 2.92 TONNES WAS ADDED TO THE GLD//GOLD INVENTORY RESTS TONIGHT AT..988.63 TONNES

APRIL 8/WITH GOLD DOWN $.60//ANOTHER HUGE CHANGE IN GOLD INVENTORY/;; A STRONG 1.45 TONNES WAS ADDED TO THE GLD/GOLD INVENTORY RESTS AT 985.71 TONNES

APRIL 7/WITH GOLD UP $.30: ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.27 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 984.26 TONNES

APRIL 6//WITH GOLD UP $32.00//ANOTHER STRONG DEPOSIT INTO THE GLD; A HUGE 7.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT : 978.99 TONNES

APRIL 3//WITH GOLD UP $7.80 TODAY//ANOTHER STRONG DEPOSIT OF 3.22 TONNES INTO THE GLD/INVENTORY RESTS AT 971.97 TONNES

APRIL 2//WITH GOLD UP $31.80 TODAY: ANOTHER STRONG DEPOSIT OF 1.75 TONNES INTO THE GLD//INVENTORY RESTS AT 968.75 TONNES

APRIL 1/WITH GOLD DOWN $7.70 TODAY: ANOTHER CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.62 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 967.00 TONNES

MARCH 31//WITH GOLD DOWN $32.70//A MONSTROUS PAPER DEPOSIT OF 10.84 TONNES INTO THE GLD//INVENTORY RESTS AT 964.38 TONNES

MARCH 30/WITH GOLD DOWN $6.10 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 953.54 TONNES

MARCH 27.WITH GOLD DOWN $16.40: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A HUGE DEPOSIT OF 4.39 TONES INTO THE GLD/INVENTORY RESTS AT 953.54 TONES

MARCH 26//WITH GOLD UP $24.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 13.17 TONNES INTO THE GLD/INVENTORY RESTS AT 949.15 TONNES

MARCH 25/WITH GOLD DOWN $11.40 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.99 TONES INTO THE GLD INVENTORY////INVENTORY RESTS AT 935.98 TONNES

MARCH 24//WITH GOLD UP $67.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 15.80 TONNES OF GOLD INTO GLD////INVENTORY RESTS AT 923.99 TONNES..THIS PROVES THAT THE GLD IS A FRAUD AS LONDON SUSPENDED DELIVERY AS WELL AS ALL REFINERS. THEY HAD NO WAY OF GETTING ANY PHYSICAL OZ INTO ITS INVENTORY//

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

APRIL 23/ GLD INV 1042.46 tonnes*

IN LAST 805 TRADING DAYS: +96.12 NET TONNES HAVE BEEN REMOVED FROM THE GLD

LAST 705 TRADING DAYS;+271.10 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

APRIL 23/WITH SILVER UP 0 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.891 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 413.665 MILLION OZ//

APRIL 22/WITH SILVER UP 42 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY: A PAPER WITHDRAWAL OF 1.865 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 410.774 MILLION OZ//

APRIL 21//WITH SILVER DOWN 60 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER ADDITION OF 1.398 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 412.639 MILLION OZ//

APRIL 20//WITH SILVER UP 16 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.797 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 414.038 MILLION OZ//

APRIL 17/WITH SILVER DOWN 24 CENTS TODAY; A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.3999 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 16/WITH SILVER UP 5 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 15//WITH SILVER DOWN 45 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV TWO HUGE DEPOSITS: A DEPOSIT OF 1.679 MILLION OZ AND ANOTHER 5.222 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 14./WITH SILVER UP 51 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A MASSIVE PAPER DEPOSIT OF XXX MILLION OZ//INVENTORY RESTS AT 408.536 MILLION OZ//

APRIL 13//WITH SILVER DOWN 29 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 6.155 MILLION OZ////INVENTORY RESTS AT 408.536 MILLION OZ//

APRIL 9/WITH SILVER UP 60 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUGE DEPOSIT OF 1.84 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 402.381 MILLION OZ.

APRIL 8//WITH SILVER DOWN 21 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 401.541 MILLION OZ///

APRIL 7/WITH SILVER UP 26 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.766 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 395.826 MILLION OZ

APRIL 6/WITH SILVER UP 50 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 395.826 MILLION OZ.

APRIL 3//WITH SILVER DOWN 15 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 746,000 OZ INTO THE SLV//INVENTORY RESTS AT 395.826 MILLION OZ

APRIL 2/WITH SILVER UP 65 CENTS; A SMALL CHANGE TODAY..A WITHDRAWAL OF .335 MILLION OZ TO PAY FOR FEES//INVENTORY RESTS AT 394.826 MILLION OZ/

APRIL 1/WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 395.181 MILLION OZ//

MARCH 31/WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 1.679 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 375.181 MILLION OZ//

MARCH 30/WITH SILVER DOWN 44 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 393.502 MILLION OZ.

MARCH 27/WITH SILVER DOWN 5 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTROUS PAPER DEPOSIT OF 8.115 MILLION OZ INTO THE SLV../INVENTORY RESTS AT 393.502 MILLION OZ//

MARCH 26/WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 385.387 MILLION OZ///

MARCH 25/WITH SILVER UP 44 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSITS OF 7.369 MILLION OZ AND 2.239 MILLION OZ OF PAPER SILVER INTO THE SLV////INVENTORY RESTS AT 385.387 MILLION OZ//

MARCH 24//WITH SILVER UP 100 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 375.779 MILLION OZ///

APRIL 23.2020:

SLV INVENTORY RESTS TONIGHT AT

413.665 MILLION OZ.

END

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.95/ and libor 6 month duration 0.99

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – 1.96

gold scarce//central banks calling in their leaves

XXXXXXXX

12 Month MM GOFO

+ 1.61%

LIBOR FOR 12 MONTH DURATION: 0.97

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -.64

gold scarce//central banks calling in their leases.

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

GATA supporters have a special connection with The Calandra Report

Submitted by cpowell on Wed, 2020-04-22 16:31. Section: Daily Dispatches

Subscribe at a discount this week, gain insights about gold and silver minters, and help GATA.

* * *

12:29p ET Wednesday, April 22, 2020

Dear Friend of GATA and Gold:

Monetary metals mining company shares are taking off as governments are issuing infinite money, and Thom Calandra of The Calandra Report is connecting with newly subscribed GATA members and sharing with them his insights about producing gold and silver mines and gold and silver explorers in the Yukon, Quebec, Nevada, Mexico, Ghana, and elsewhere.

Thom’s special discount subscription offer for GATA members remains open this week, and a current sample of The Calandra Report is here:

https://thomcalandra.com/ecuador-villages-explorer-to-raise-covid-19-cas…

The Calandra Report has a heavy emphasis on the miners, and at least until that danged virus came around, it was a rare week when Thom wasn’t inspecting and questioning them in places far and wide.

…

Thom is a longtime supporter of GATA, and if you subscribe to The Calandra Report this week, you’ll get the special discounted price and help GATA as well.

Thom will split with GATA a one-year discounted subscription fee of $169 paid by GATA supporters who subscribe.

That is, for each GATA supporter who subscribes, Thom will contribute $85 to GATA.

The regular price of The Calandra Report is $229 yearly, so this offer is doubly a bargain. To avail yourself of it, visit PayPal here:

https://www.paypal.com/cgi-bin/webscr?cmd=_s-xclick&hosted_button_id=588….

In addition to The Calandra Report, GATA supporters who subscribe this week will receive two bonuses.

— Thom’s frequent “TCR Collateral” missives, which include material from his notebook about financial people, companies, and commodities.

— A special recent issue of The Calandra Report that describes what Thom believes are substantially undervalued gold, silver, zinc, and copper mining companies, as well as a rising biomedical company with a promising new anti-inflammation drug, Antibe Therapeutics.

Check out Thom’s personal message below.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

Hello Alpha-GATAs. I have supported GATA since the early 2000s. Over the years GATA Chairman Bill Murphy, Secretary/Treasurer Chris Powell, and I have shared ideas, panel appearances, and even a drink or three.

So I’d like you to join The Calandra Report community. It has been going since 2011, and since 1998 from MarketWatch.com, which I co-founded.

Here’s a small biography:

https://thomcalandra.com/about-thom-calandra/

Here’s a subscription offer exclusively for GATA supporters, like the offer we made last year — that added GATA supporters from the United States, Canada, the United Kingdom, and the Bahamas.

You’ll get the twice-weekly private reports for one year for $169 — along with “TCR Collateral” letters — and GATA will receive fully half of that amount: $85.

To accept this offer and help GATA, please go here:

https://www.paypal.com/cgi-bin/webscr?cmd=_s-xclick&hosted_button_id=588…

Please e-mail me with testimonials, ideas, and names: thom@thomcalandra.com

Thank you. I think you will make money.

— Thom Calandra

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

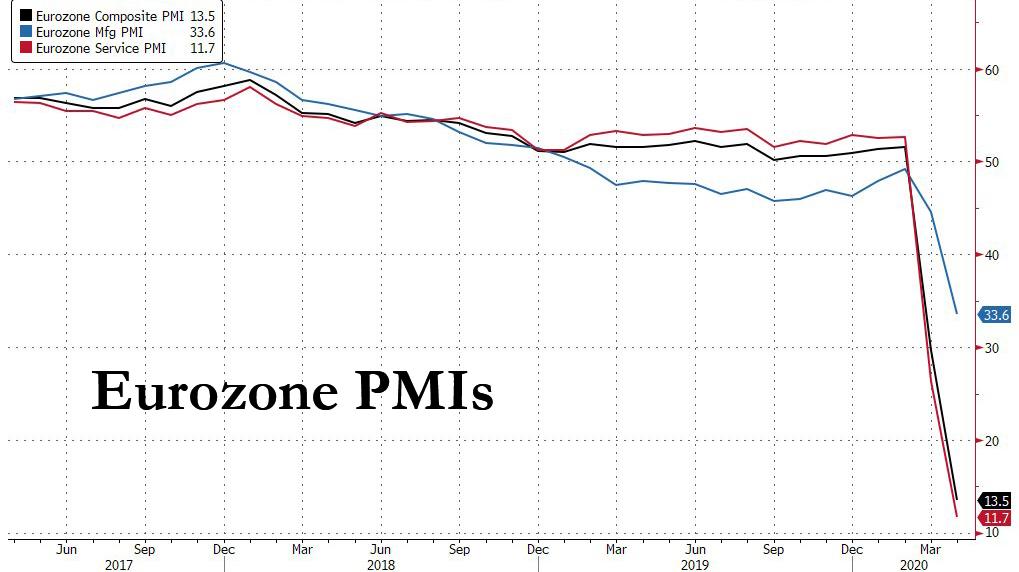

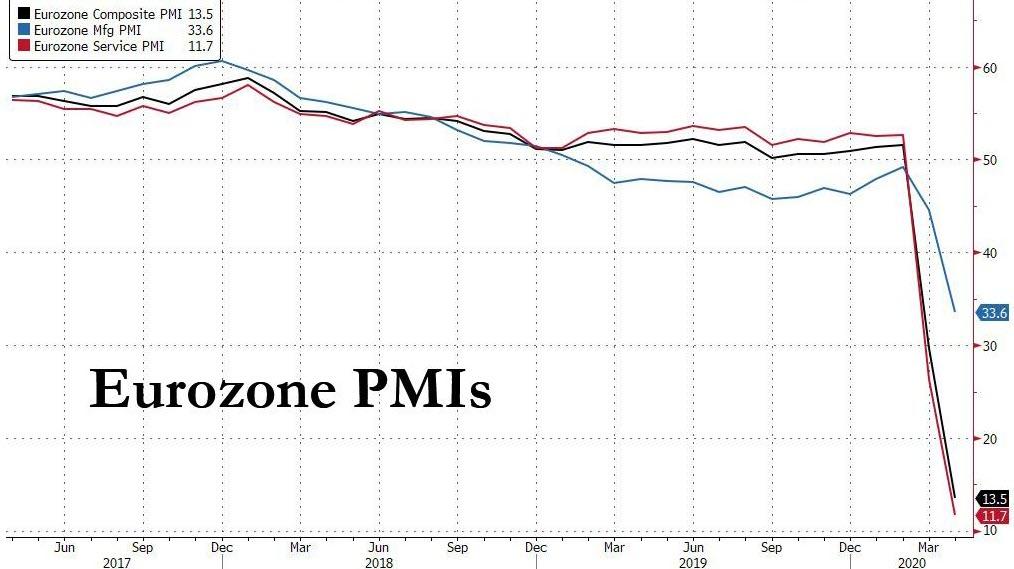

Futures Flat Despite Record Eurozone Business Collapse Ahead Of Latest Claims Shocker

US equity futures and global stock markets were surprisingly uneventful on Thursday on the back of a continued modest rebound in oil prices despite a record collapse in European business activity, as investors braced for another staggering jobless claims report as sweeping lockdown measures hammer economic growth.

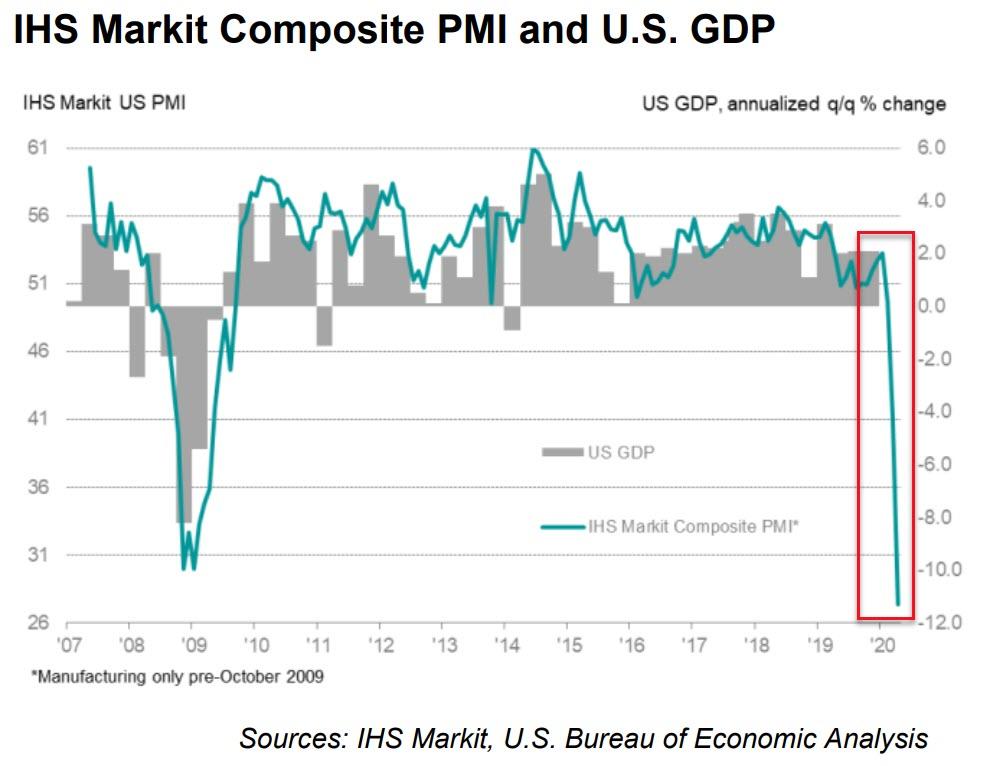

The S&P500 jumped on Wednesday on a recovery in oil prices and signs Congress was set to pass $500 billion more in relief for small businesses and hospitals. The bill is expected to clear the House of Representatives later in the day. Still, the benchmark index is 17% below its February record high as statewide shutdowns sparked layoffs and crushed consumer spending.Surveys on U.S. manufacturing and services firms are likely to mirror dismal readings from Asia and Europe issued earlier on Thursday. As noted earlier, a composite European business index plunged to its lowest print on record.

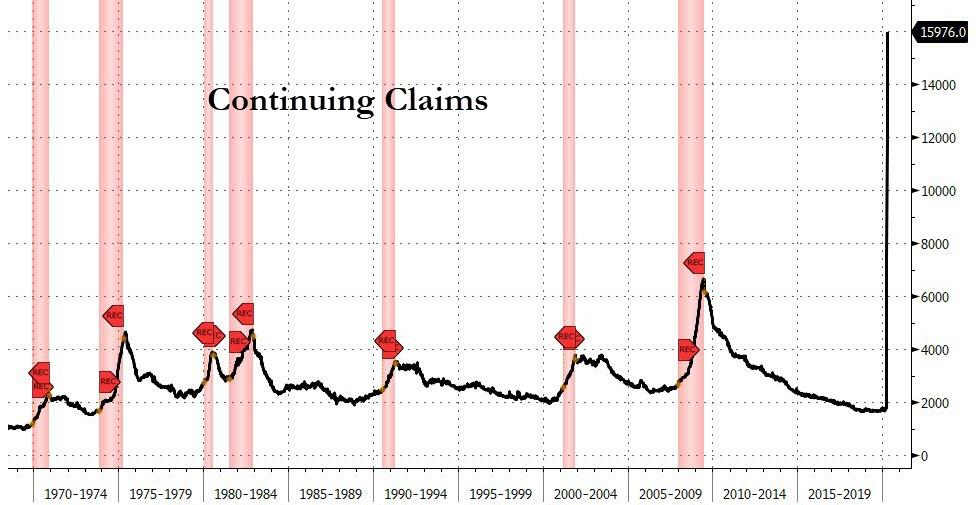

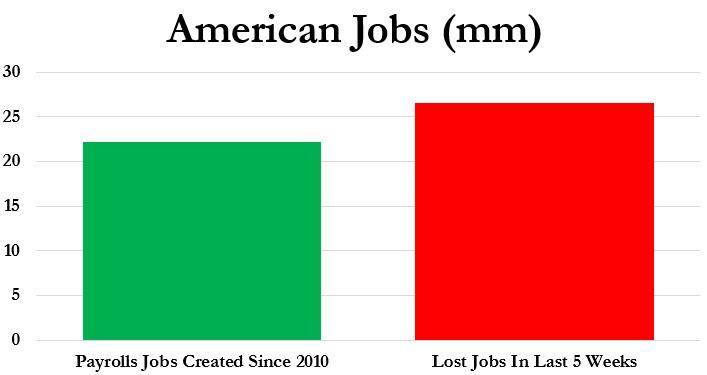

Data set to be announced shortly is also likely to show a record 26 million Americans sought unemployment benefits over the last five weeks, confirming that all the jobs created during the longest employment boom in U.S. history were wiped out in about a month.

Retailer Target Corp tumbled 7% in premarket trading despite a surge in digital sales in March and April which offset a slump in-store sales. Eli Lilly gained 1.5% as it reported a jump in first-quarter sales, boosted by its diabetes drug and also benefiting from customers stockpiling its medicines during the pandemic.

Europe’s Stoxx 600 Index drifted as the abovementioned PMI index plunged far more than economists anticipated. Credit Suisse slipped after the bank said first-quarter profitability rose but that it’s taking a greater than expected $1 billion in writedowns and provisions for bad loans after the pandemic.

Earlier in the session, Asian stocks gained, led by materials and energy, after rising in the last session. Most markets in the region were up, with Japan’s Topix Index gaining 1.4% and India’s S&P BSE Sensex Index rising 1.2%, while Shanghai Composite dropped 0.2%. The Topix gained 1.4%, with Jeans Mate and Showcase Inc/Japan rising the most. The Shanghai Composite Index retreated 0.2%, with Xinjiang Winka Times Department Store and Zhejiang Meilun Elevator posting the biggest slides.

Crude futures jumped for a second day despite a swelling global glut.

Looking ahead, investors will focus on the latest weekly jobless numbers from Washington that are estimated at 4.5 million. While governments across the world have pledged more than $8 trillion to fight the pandemic, a sharper picture of a crippled global economy is emerging from unprecedented layoffs, chaos in the oil market, poor European data and a mixed bag of corporate earnings, as Bloomberg summarizes.

There were some good news on the virus front, where New York fatalities were at the lowest rate since early April, while Treasury Secretary Steven Mnuchin said he anticipates most of the economy will restart by the end of August. House lawmakers on Thursday are set to pass another round of aid. Infections and deaths spiked higher in Spain, home to the world’s most extensive outbreak after the U.S., even amid its sixth week of strict lockdown.

The most important event today is the long-awaited European Council summit via videoconference this afternoon, where the big question will be over how the idea of a European Recovery Fund is financed. Yesterday, Bloomberg News reported that theCommission would propose a €2 trillion plan that would in part use the bloc’s 7-year multi-annual budget with a €300bn recovery fund included, but also establish a new temporary financing mechanism that would raise up to €320bn. However, this could prove controversial given the issuance of joint debt, to which the northern member states are strongly reluctant.

In rates, Treasuries steadied while commodity currencies advanced on a rise in oil prices; Spanish bonds extended an advance, leading peripheral outperformance over euro-area peers; bunds erased declines after French PMIs missed median estimates. Gilts fell then rose after the U.K. DMO announced it will raise in four months of debt sales almost as much as it did during the height of the global financial crisis.

In FX, the Bloomberg dollar index inched up, erasing losses after coming under pressure from short covering in crosses into the London open. The euro fell after much worse than anticipated German consumer confidence data. The Norwegian krone shrugged off a plunge in industrial confidence and rose versus all major peers. Australian and New Zealand dollars traded higher against the greenback as the recovery in oil futures sparked short covering among commodity currencies

Looking at the day ahead, and along with the aforementioned European Council meeting, PMIs and initial jobless claims from the US, other data releases include Germany’s GfK consumer confidence reading for May, the UK’s public sector net borrowing for March, along with the US new home sales for March and April’s Kansas City Fed manufacturing activity index. From central banks, we’ll hear from the BoE’s Vlieghe, while earnings out today include Intel, Eli Lilly and Company, NextEra Energy and Union Pacific.

Market Snapshot

- S&P 500 futures down 0.1% to 2,786.75

- STOXX Europe 600 down 0.1% to 329.81

- MXAP up 0.8% to 142.65

- MXAPJ up 0.5% to 460.76

- Nikkei up 1.5% to 19,429.44

- Topix up 1.4% to 1,425.98

- Hang Seng Index up 0.4% to 23,977.32

- Shanghai Composite down 0.2% to 2,838.50

- Sensex up 1.4% to 31,805.19

- Australia S&P/ASX 200 down 0.08% to 5,217.11

- Kospi up 1% to 1,914.73

- German 10Y yield fell 0.3 bps to -0.41%

- Euro down 0.2% to $1.0800

- Italian 10Y yield fell 7.6 bps to 1.902%

- Spanish 10Y yield fell 8.9 bps to 1.048%

- Brent futures up 7% to $21.80/bbl

- Gold spot up 0.6% to $1,724.11

- U.S. Dollar Index up 0.1% to 100.44

Top Overnight News from Bloomberg

- Confidence among European businesses and consumers is in free fall as shutdowns to contain the coronavirus push the economy into recession

- The Federal Reserve’s beefed-up swap program is having some unintended consequences, especially in Europe. It helped bring down the cost of dollars to such an extent they’re cheaper to borrow in cross-currency markets than any major currency. But that’s driving opportunistic players to tap local markets to swap into dollars, which ends up elevating domestic borrowing costs

- The effect of the U.K.’s emergency spending to combat coranavirus began to show up in public finance data for March, as a jump in spending caused the budget deficit to widen more than expected

- The U.K. government is to survey 20,000 households in a bid to track the spread of the coronavirus in Britain, five weeks after it abandoned a strategy of community testing for the disease

Asian equity markets mostly benefitted from the more constructive handover from Wall St where sentiment rebounded in tandem with oil prices amid touted bargain buying and increased US-Iran geopolitical risks after US President Trump instructed the US Navy to destroy any and all Iranian gunboats if they harass US ships at sea, with the Senate’s recent passage of the USD 480bln relief bill also adding to the bout of optimism stateside. ASX 200 (-0.1%) advanced at the open but with gains later pared after mixed data releases, as well as weakness in defensives and the largest weighted financials sector. Nikkei 225 (+1.5%) traded higher although upside was restricted by an indecisive currency and following abysmal PMIs in which Manufacturing PMI posted its worst reading since 2009 and both Services and Composite PMIs were at record lows, while the KOSPI (+1.0%) outperformed after it eventually shrugged off the largest contraction for South Korea GDP in more than 11 years. Elsewhere, Hang Seng (+0.4%) and Shanghai Comp. (-0.2%) were indecisive with price action kept rangebound amid a lack of fresh drivers and continued PBoC liquidity inaction, while Hong Kong policymakers remained focused on defending the currency peg. Finally, 10yr JGBs initially weakened amid the early broad optimism but then recovered from lows as the regional stock indices retraced some of the gains and following stronger results at 2yr JGB auction.

Top Asian News

- South Korea’s Economy Shrinks Most Since 2008 Amid Pandemic

- Singapore Traders Say They’re Healthy Amid Hin Leong Saga

- Operation Twist Returns to Send India’s Bond Yields Plunging

The optimism seen in the APAC session faded as European trade went underway [Euro Stoxx 50 -0.1%], with the deterioration attributed to a string of dismal April Flash PMIs across the region and as participants look ahead to the Eurogroup summit later today (Primer available on the Newsquawk headline feed). A meeting which could see disagreement over the rollout of the European Recovery Fund – officials touting a launched in 2021; however, Italy stated they cannot wait until June 2020 for approval. European bourses trade mixed with no standout under/outperformers, whilst broader sectors also paint a mixed picture and fail to reflect a clear risk tone – albeit the energy sector outperforms as the complex continues to post gains. The breakdown also sees a similarly mixed picture – again with Oil & Gas leading the gains. A slew of earnings were reported in the pre-market, including prelim figures for Daimler (+0.9%) and Software AG (+0.8%), whilst Renault (+2.3%), Orange (+0.5%), Pernod Ricard (+0.3%), Accor (+1.1%), Swedbank (-0.7%), Volvo (-7.0%) all reported quarterly numbers – with Renault firmer despite a downbeat earnings release on reports Renault CEO is to unveil cost-cutting measures next month, whilst Volvo is pressured after substantially missing on its EPS and adj. operating profit expectations. Moving to Credit Suisse’s (-2.2%) earnings, the group topped net income forecasts but reported a deterioration in revenue and a Q1 loan loss provision over double its expectations. That being said, market volatility saw its FICC and Equity trading and sales both higher in excess of 20% YY. Elsewhere, Wirecard (+8.0%) sees itself at the top of the DAX after an independent audit of the Co. has uncovered no substantial findings with regards to questionable accounting methods; however, the full report is yet to be published. Results from the audit are now expected for April 27th and the Co’s FY results are to be published on April 30th. Finally, Tullow Oil (+30%) opened with gains above 60% and holds its place at the top of the Stoxx 600 after divesting its stake in Uganda to reduce net debt, whilst also seeing tailwinds from favourable price action in oil.

Top European News

- Europe’s Virus Lockdown Hits Economy, Leaves Businesses Reeling

- Immofinanz Names Investor Ronny Pecik as New Chief Executive

- Orban Blinks After Decade Fighting Foreign Sway Over Economy

In FX, the single currency is languishing at the bottom of the G10 table and looking precarious under 1.0800 vs the Dollar not to mention across the board as Eur/crosses teeter over psychological or key technical levels, like Eur/Chf on the verge of 1.0500, Eur/Jpy edging towards 116.00 and even Eur/Gbp testing the 200 DMA (0.8736). Much worse than anticipated preliminary Eurozone PMIs, and particularly poor services sector prints have undermined the Euro, but Eur/Usd is holding in just above or around chart supports ahead of 1.0750 in the form of April 6’s so called reaction low at 1.0769 and a 1.0757 Fib retracement level, for now, with some additional buffers provided by option expiries extending from 1.0800-1.0790 to 1.0750 in 3.1 bn and 1.2 bn respectively.

- NZD/AUD/JPY/GBP – The Kiwi and Aussie continue to see-saw vs their US counterpart, with the former recovering from a stop-induced slide overnight after 0.5900 held and subsequently retesting resistance ahead of 0.6000, while the latter was able to withstand weak PMIs with the aid of trade data revealing a much wider surplus as exports outpaced imports nearly 3-fold. Aud/Usd has reclaimed 0.6300+ status and briefly extended gains to circa 0.6370 before fading alongside Aud/Nzd ahead of 1.0650. Meanwhile, the Yen continues to retain an underlying safe-haven bid between 108.00 and 107.50 with decent option expiry interest also keeping the pair contained (1 bn at 107.50 and 1.6 bn from 107.85 to 108.00). Elsewhere, Sterling has (somehow) taken bleak UK PMI and CBI surveys in stride and resisting Greenback advances after Cable came close to filling bids touted at 1.2300, though this could be due to the aforementioned Eur/Gbp correction from recent 0.8800+ peaks rather than anything especially or uniquely Pound positive.

- USD – The Buck may be primed for a fall after the latest US initial claims release and/or Markit PMIs, but for now the DXY is establishing a more assured base on the 100.000 handle and building momentum through 100.500, albeit with indirect traction from the Euro underperformance noted above and more pronounced Franc depreciation below 0.9700 through 0.9750.

- SCANDI/EM – The Scandi Crowns are back on the front foot as crude prices continue to stabilise and sharp falls in Swedish sentiment indicators are acknowledged, but partially taken in context when compared to the starker deterioration elsewhere in Europe. However, in contrast to crude-related recoveries for EM currencies like the Rouble, COVID-19 contagion has intensified in SA where the Rand is back under 19.0000 vs the Dollar in the run up to President Ramaphosa setting out plans to re-open the economy after rolling out fiscal stimulus representing around 10% of the country’s GDP..

In commodities, WTI and Brent front month futures trade on a firmer footing as geopolitical risks continue to be priced in following US President Trump’s tweet regarding his order to the US Navy to shoot down all Iranian gunboats that harass US vessels. Aside from that, the underlying fundamentals remain broadly unchanged. The supply glut remains, and storage space remains scarce. “Given the glut we have in the oil market, it is difficult to see this offering lasting support to the market, unless the situation does escalate further” – ING says. Elsewhere and in fitting with recent source reports, Saudi Aramco has started to implement the OPEC+ pact ahead of its inauguration on May 1st. Aramco will be lower output to 8.5mln BPD, the output level mentioned under the terms of the of the deal – markets are yet to see if other producers follow suit, with Kuwait the only other country to publicly announce their early cuts thus far. WTI resides around USD 15.5/bbl having had briefly topped USD 16/bbl in early trade ahead of yesterday’s high of USD 16.18/bbl. Brent futures meanwhile meander just above 22/bbl after printing a current intraday high at USD 23.22/bbl. Elsewhere, spot gold remains relatively steady north of USD 1700/oz thus far and briefly topped 1725/oz. Meanwhile, copper trades on a firmer footing after Anglo American’s copper production showed a YY decline, meanwhile, Antofagasta also stated it expects copper output this year towards the lower end of its guidance.

US Event Calendar

- 8:30am: Initial Jobless Claims, est. 4.5m, prior 5.25m; Continuing Claims, est. 16.7m, prior 12m

- 9:45am: Bloomberg Economic Expectations, prior 46.5; Bloomberg Consumer Comfort, prior 44.5

- 9:45am: Markit US Manufacturing PMI, est. 35, prior 48.5

- 9:45am: Markit US Services PMI, est. 30, prior 39.8

- 9:45am: Markit US Composite PMI, prior 40.9

- 10am: New Home Sales, est. 644,000, prior 765,000; New Home Sales MoM, est. -15.82%, prior -4.4%

- 11am: Kansas City Fed Manf. Activity, est. -37, prior -17

DB’s Jim Reid concludes the overnight wrap

This working from home routine is good for productivity if not my social skills. My wife won’t get too close to me at the moment as I refuse to shave off a four week old bristly beard. We’ll see who holds out the longest. On the productivity front we published two quick notes yesterday. The first ( link here ) where we rank the severity of this pandemic relative to 24 we’ve found going back over 2000 years and make some observations of where it’ll end up and also some markers for the future. Secondly we published a chart looking at 150 years of oil prices in nominal and real terms ( link here ). This week the price of oil in nominal terms was lower than it was in 1870 and at any point in history. The note shows what inflation and the S&P 500 have done over the same period for comparison. Guess before you look at the answer. At least how many figures the latter runs into in percentage terms. If anyone can think of a financial related asset that still trades today that had a lower price this week than it did 150 years ago then I will give them a virtual prize. Even if you can think of one from 100 or even 50 years ago.

We’ll come back to oil a little later but the most important event today is the long-awaited European Council summit via videoconference this afternoon, where the big question will be over how the idea of a European Recovery Fund is financed. Yesterday, Bloomberg News reported that the Commission would propose a €2 trillion plan that would in part use the bloc’s 7-year multi-annual budget with a €300bn recovery fund included, but also establish a new temporary financing mechanism that would raise up to €320bn. However, this could prove controversial given the issuance of joint debt, to which the northern member states are strongly reluctant.

Frankly, if we saw a full agreement today that would be a surprise but progress and something that Italy can sign up to will be the key. In his blog on Monday, DB’s Mark Wall said that while he expects an eventual agreement on a recovery fund, it would be a positive surprise if the important details were agreed today, since the question of burden sharing is politically complex and the ECB’s purchases are absorbing market pressure for now. Mark says that the things to watch out for are the size, speed and structure of the fund, but he thinks joint bonds are unlikely for obvious reasons due to the Northern states current lack of desire to go down that route. We’ve also seen increasing speculation around grants recently, which could be the principle means of buying solidarity, but that would also lead to tough debates around the ratio of grants to loans within the Recovery Fund and eligibility for the grants. This would fit into the idea that we shouldn’t expect a fully detailed agreement today.

Ahead of that, sovereign debt continued to sell off in Europe yesterday, though it should be noted that Italian BTPs actually outperformed, with yields falling by -7.7bps by the end of the session. Nevertheless, in the rest of southern Europe sovereign bond spreads moved wider, with the spread of Spanish (+6.3bps) debt over bunds reaching its highest level since the aftermath of the Brexit vote back in June 2016. Having said that they did complete a successful syndicated deal which would have led to pressure elsewhere in the curve – similar to Italy on Tuesday. The ECB last night said it would accept some HY bonds as collateral if they were rated IG before April 7th and stay above BB. This clearly looks designed to mainly help Italy if they get downgraded to HY over the coming weeks or months. Next stop is S&P’s review of their BBB rating due to be announced tomorrow. Finishing off on sovereigns, 10yr Treasury yields rose by +5.0bps yesterday, up from their second-lowest closing level ever the previous day to reach 0.619%.

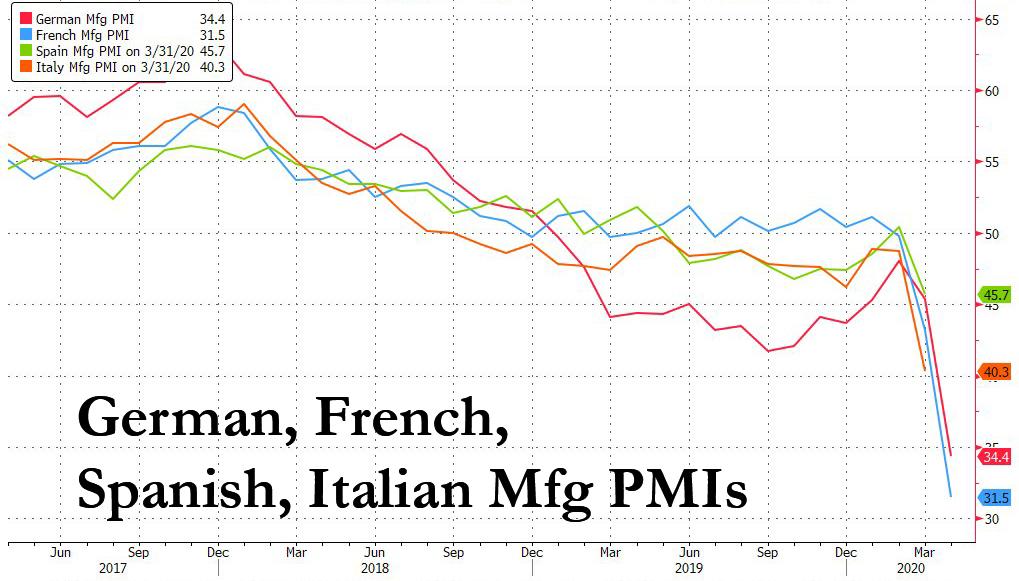

Staying on today, we’ll also get the much-anticipated April flash PMIs this morning. For our readers who thought that the March readings were dire, today’s numbers are likely to show an even bigger deterioration. That’s because when the surveys were taken back in March, plenty of economies hadn’t actually fully locked down yet, or only did so towards the latter part of the survey. The one country that was in a full lockdown for the March survey was Italy, where the services PMI fell to 17.4, which gives you some idea of how low these could go today. Given that these are diffusion indices they lose some meaning in extreme events as they don’t give a scale of the severity of declines (and rebounds when they occur) just whether things were worse or better than the prior month for the various respondents.

We’ve already had a taste for how the PMIs look in Asia overnight where Japan’s flash services PMI slid to 22.8 (vs. 33.8 last month), a record low, while the manufacturing PMI printed at 43.7 (vs. 44.8 last month). The accompanying text highlighted that “PMI data for Japan tells us that the crippling economic impact from the global coronavirus pandemic intensified in April,” and “the decline in combined output across both manufacturing and services was the strongest ever recorded by the survey in almost 13 years of data collection.” Meanwhile, Australia’s services PMI also printed at a record low of 19.6 (vs. 38.5 last month) while the manufacturing reading came in at 45.6 (vs. 49.7 last month).

In other overnight news, Bloomberg is reporting that Germany’s government has agreed on an additional EUR 10bn stimulus package that would temporarily reduce value added taxes for restaurants and increase the amount of money paid as state wage support as part of a seven-point plan to fine-tune the government’s economic crisis response. Elsewhere, Singapore’s trade and industry minister Chan Chun Sing said that the country is bracing for a sharper economic contraction this year than an earlier forecast of as much as a -4% slump. We also got South Korea’s Q1 2020 GDP print this morning which printed at -1.4% qoq (vs. -1.5% qoq expected), the worst contraction since the GFC. Elsewhere, the US Treasury Secretary Steven Mnuchin said that he expects most of the US economy will restart by the end of August.

Asian markets are trading mixed this morning with the Nikkei (+0.74%), Hang Seng (+0.23%) and Kospi (+0.47%) all up while the ASX (-0.38%) and Shanghai Comp (-0.06%) are in the red. In FX, the Australian dollar is down -0.32% following the PMI data. Elsewhere, futures on the S&P 500 are down -0.42% while yields on 10y USTs are down -1.8bps to 0.603%.

The final expected highlight today comes from the weekly initial jobless claims in the US, which have become an important high frequency indicator over the last month. Over the last 4 weeks, a cumulative total of more than 22m claims have been made, which is around the number of jobs that were created in the decade of expansion. So it’s no exaggeration to call the scale of the declines unprecedented. For today, our US economists are forecasting claims at 5m, which would be down from last week’s 5.245m, and if realised would mark the 3rd consecutive week that the number has fallen, which would suggest we could be past the most rapid period of job losses for now. The S&P 500 rose by +0.58% last Thursday for a 4th successive positive close on multi-million claims day. The previous 3 Thursdays came in at +6.24%, +2.28% and +3.41% for the S&P 500. Will the streak extend for a 5th straight week?

With all that to come later, markets rebounded yesterday following their poor start to the week, with the S&P 500 (+2.29%), the NASDAQ (+2.81%) and the STOXX 600 (+1.53%) all moving higher. Energy stocks led the rebound on both sides of the Atlantic thanks to another day of sizeable swings in oil markets, where Brent Crude managed to pare back its losses from a 21-year low to actually end the session up +5.38% at $20.37/barrel. June and July WTI saw even larger rises, up by +19.10% and +10.70% respectively to $13.78 and $20.69/barrel. June WTI is up a further +4.28% this morning to $14.37. The catalyst seemed to be a tweet from President Trump, who said that “I have instructed the United States Navy to shoot down and destroy any and all Iranian gunboats if they harass our ships at sea.” While geopolitics has rather moved out of the headlines since the start of the year, it’s worth noting that it was only last week that the US Central Command said in a statement that 11 Iranian ships crossed the bows and sterns of US vessels at close range. So one to keep an eye on. In related news, the largest oil-ETF, USO, has altered its fund holdings further away from near-term WTI. The fund has over $3 billion in AUM and is the largest single-holder of WTI futures according to Bloomberg. The ETF will now roll exposure to August and September, while lowering June and July, in order to shield itself from the price action in near-term contracts. Oil ETFs have been a hot topic over the last couple of days given the recent turmoil. When these were structured no-one could have contemplated a negative price on the contracts they invested in. It’s fair to say it’s caused some chaos.

There wasn’t a lot in the way of data yesterday, though we did get the European Commission’s advance consumer confidence reading for April, which plummeted to -22.7, its lowest level since March 2009. Otherwise, we got February’s FHFA house price index for the US, which saw a +0.7% increase month-on-month before the impact of the pandemic began to be felt. And in the UK, the CPI reading for March fell to 1.5% as expected, down from 1.7% in February.

Corporate earnings were mixed again. Chipotle Mexican Grill (+12.44%) rose after 1Q digital sales grew over 80% yoy and EPS came in well ahead of analyst’s estimates at $3.17 vs. $3.08 expected. Heineken (-3.05%) cancelled its interim dividend, while volumes were down 14% and net income fell 69%. Kering (-4.92%) announced on its earnings call that it doesn’t expect a recovery in the U.S. or Europe before at least June or July, while sales at its brand Gucci tumbled 23% year-over-year. The company did announce that sales in mainland China turned positive this month as tourist spending rose.

To the day ahead now, and along with the aforementioned European Council meeting, PMIs and initial jobless claims from the US, other data releases include Germany’s GfK consumer confidence reading for May, the UK’s public sector net borrowing for March, along with the US new home sales for March and April’s Kansas City Fed manufacturing activity index. From central banks, we’ll hear from the BoE’s Vlieghe, while earnings out today include Intel, Eli Lilly and Company, NextEra Energy and Union Pacific.

3A/ASIAN AFFAIRS

i)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 5.48 POINTS OR 0.19% //Hang Sang CLOSED UP 83,96 POINTS OR 0.35% /The Nikkei closed UP 291.49 POINTS OR 1.52%//Australia’s all ordinaires CLOSED DOWN .02%

/Chinese yuan (ONSHORE) closed UP at 7.0813 /Oil UP TO 15.42 dollars per barrel for WTI and 21.85 for Brent. Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0813 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.0925 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

JAPAN

Japan’s PMI collapses to record lows and thus we should expect a huge 10% crash on its GDP

(zerohedge)

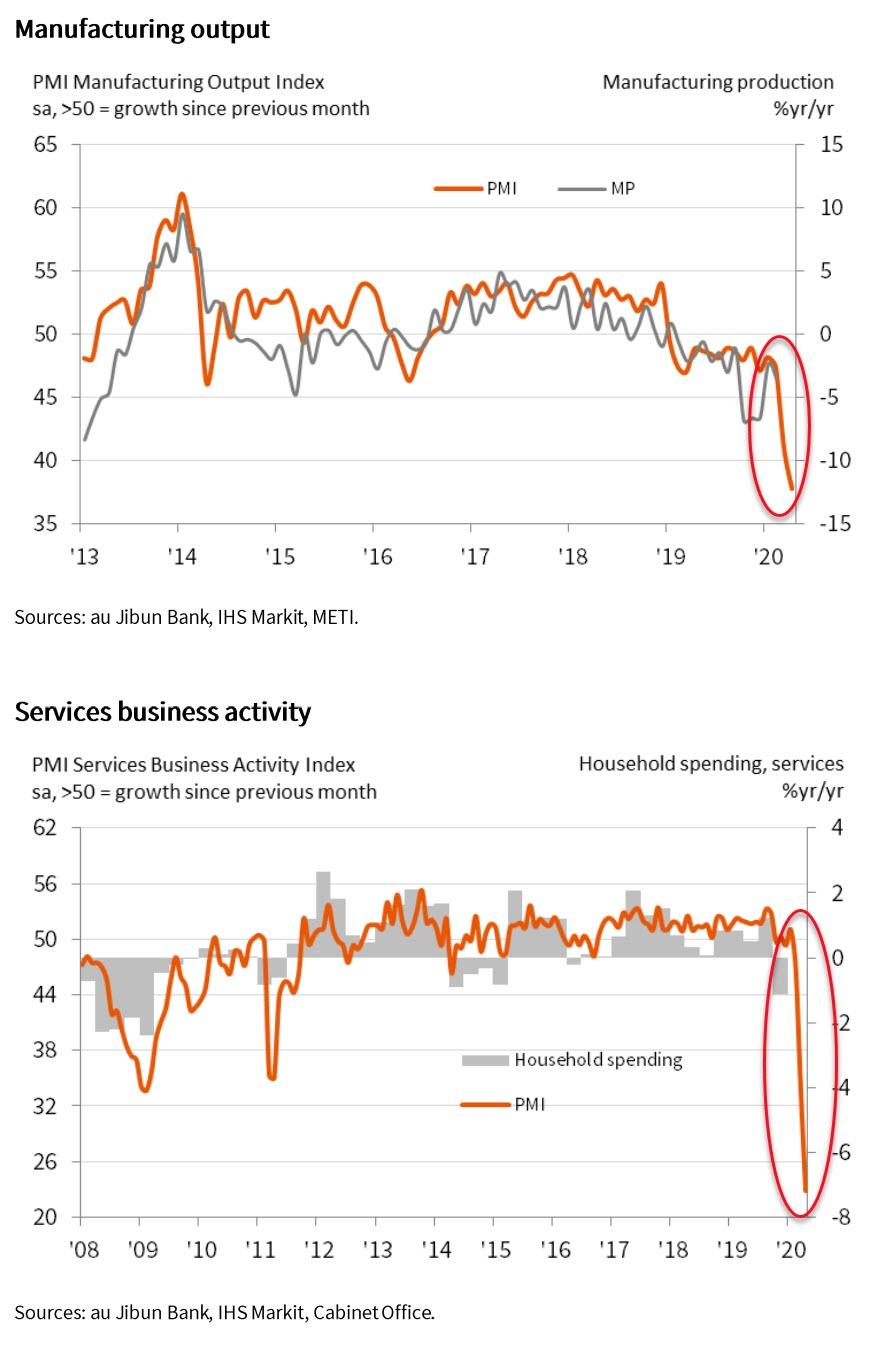

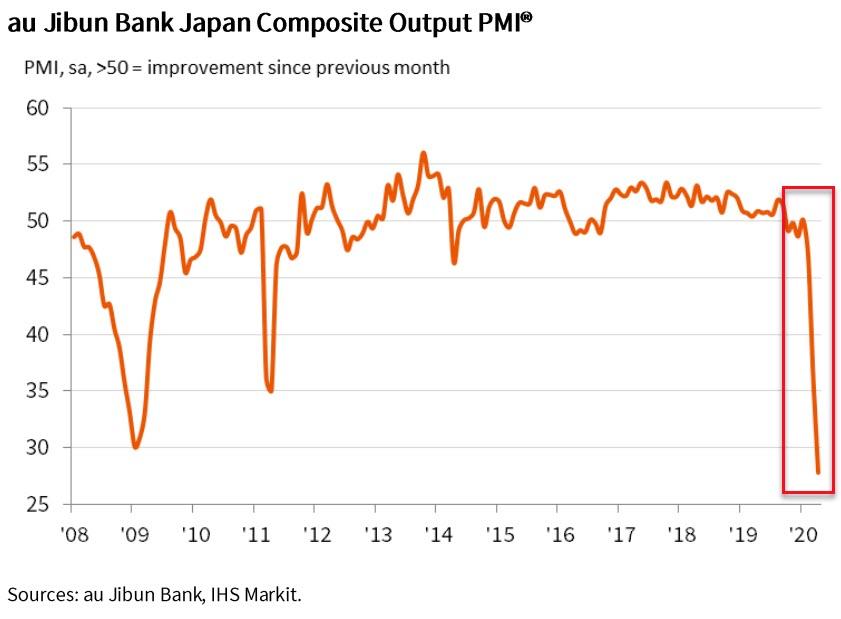

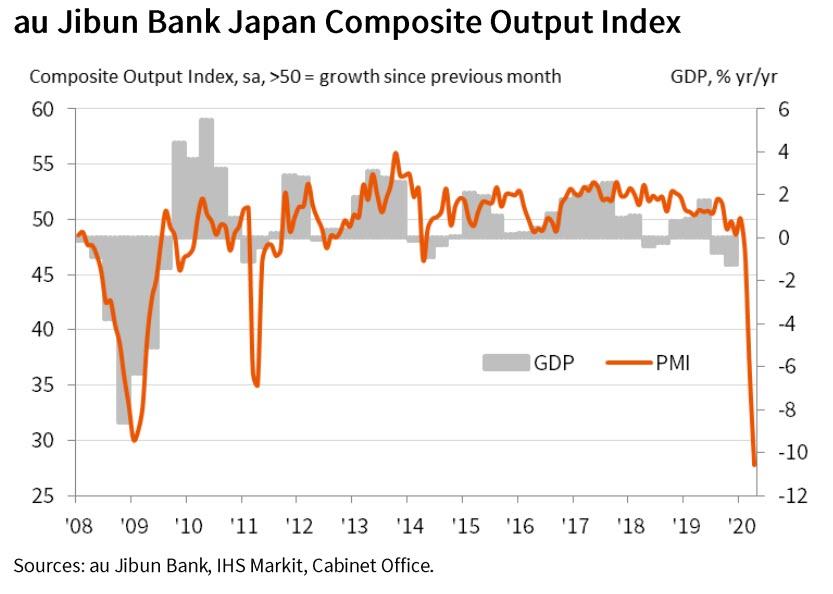

Japanese PMI Collapses To Record Low, Signals 10% Crash In GDP

After China’s ugliest GDP print ever, and the collapse of US economic surprise index data, it should be no real surprise that Japan’s manufacturing and services industry PMIs would plunge (despite the “everything’s fine, the Olympics is imminent” narrative puked forth by the government for most of the month).

But, to crash to record lows is something else…

- Japan’s April flash manufacturing purchasing managers’ index falls to 43.7 from 44.8 in March – Lowest reading since April 2009

- Japan’s April flash services purchasing managers’ index falls to 22.8 from 33.8 in March – Lowest reading since series began

Which combined to leave Japan’s April flash composite purchasing managers’ index plunging to to 27.8 from 36.2 in March – the lowest reading since records began.

Across the indices everything was a disaster…

Commenting on the latest survey results, Joe Hayes, Economist at IHS Markit, said:

“PMI data for Japan tell us that the crippling economic impact from the global corona virus pandemic intensified in April. Furthermore, the data show us the initial impact of Japan’s lockdown. The survey was conducted between 7 and 21 April The 7th was the day Prime Minister Abe announced a state of emergency in some parts of Japan, although this was upgraded to a nationwide state of emergency on the 16th and extended the lockdown to the whole country. ”

“The decline in combined output across both manufacturing and services was the strongest ever recorded by the survey in almost 13 years of data collection, surpassing declines seen during the global financial crisis and in the aftermath of the 2011 tsunami.”

Overall, GDP looks set to decline at an annual rate in excess of 10% in the second quarter…

And it is not about to get better anytime soon:

“The current state of emergency will stay in place until 6May, although given Japan’s lagged response relative to other parts of the world, one would expect this to be extended, meaning the harsh economic effects are likely to drag out further.”

end

JAPAN

Bank of Japan launches unlimited QE and that should send gold/silver to the moon!!

(zerohedge)

3 C CHINA

CHINA/USA

Figures! China sends to the USA ‘contaminated COVID test kits..bacterial growth in many!

(ZEROHEDGE)

China Sends US “Contaminated” COVID Test-Kits

It’s bad enough that China has frozen exports of medical equipment to the US during the pandemic. Now a new report sheds light on some COVID-19 test kits from the country that were sent “contaminated.”

The South China Morning Post (SCMP) said the University of Washington School of Medicine (UW Medicine) “went to extraordinary lengths to airlift tens of thousands of Covid-19 testing kits” during the start of the US outbreak to only discover last week that some of the tests are tainted.

“I’ve just recommended everyone who has these things pause and not use them at all,” said Geoff Baird, the interim chair of the UW Department of Laboratory Medicine, who led the group to secure the tests. “I can’t say I’m not disappointed.”

Baird told SCMP that a colleague informed him on April 16 that some of the “liquid in vials he had sent appeared to have changed in color.” In shock, he said he stormed out of his office down to the UW Medicine storage facility where the test kits were being held and started to “tear through boxes.”

He said many of the vials looked “fine,” but a “small percentage of them had turned to an orange or yellow color, rather than hot pink,” which indicated bacterial growth and, ultimately, contamination.

Baird also had scientists add novel coronavirus to the contaminated vials and compared to uncontaminated liquid.

The conclusions, he said: “There’s absolutely no difference.”

After that, Baird immediately suspended future orders with the Chinese manufacturer.

Anita Nadelson, the Seattle businesswoman who helped the university secure the tests, said the Chinese firm would refund their money.

“They’re working diligently to identify and cure the issue,” Nadelson said. “We vetted these as best we could. It’s an unexpected turn on both sides.”

Baird said the contamination is concentrated in the specimen-preserving liquid, which makes no contact with patients, adding that “we don’t expect there’s any real mechanism of harm to patients.”

He said S. maltophilia was the bacterium found in the contaminated vials: