GOLD$1712.00 DOWN $12.75 The quote is London spot price

Silver:$15.15 UP 1 CENT

Today is comex options expiry so again the crooks whack.

This Thursday is OTC/LBMA options expiry

Closing access prices: London spot

i)Gold : $1715.50 LONDON SPOT 4:30 pm

ii)SILVER: $15.19//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

APRIL comex gold price CLOSE 1.30 PM: $XX

MAY COMEX GOLD: 1710.80 1:30 PM

JUNE GOLD: $1723.20 CLOSE 1.30 PM// SPREAD SPOT/FUTURE JUNE: $11.20.//PREMIUMS WENT DOWN AGAIN

CLOSING SILVER FUTURE MONTH

SILVER APRIL COMEX CLOSE: XXX

SILVER MAY COMEX CLOSE; $15.23…1:30 PM.//SPREAD SPOT/FUTURE MAY: 8 CENTS PER OZ//PREMIUMS DOWN AGAIN

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2800. usa per oz

and silver; $31.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

DO NOT PAY ANY ATTENTION TO WHAT THE CROOKS ARE DOING AT THE COMEX AND LONDON LBMA..PHYSICAL IS THE NAME OF THE GAME AND NOTHING ELSE

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 49/151

issued 40

EXCHANGE: COMEX

CONTRACT: APRIL 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,723.500000000 USD

INTENT DATE: 04/24/2020 DELIVERY DATE: 04/28/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

132 C SG AMERICAS 38

159 C ED&F MAN CAP 1

357 C WEDBUSH 1

657 C MORGAN STANLEY 9

661 C JP MORGAN 40 49

686 C INTL FCSTONE 14 5

690 C ABN AMRO 85 2

737 C ADVANTAGE 4

905 C ADM 3

991 H CME 51

____________________________________________________________________________________________

TOTAL: 151 151

MONTH TO DATE: 31,442

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT: 151 NOTICE(S) FOR 15,100 OZ (0.4696 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 31,442 NOTICES FOR 3,144,200 OZ (97.79 TONNES)

SILVER

FOR APRIL

6 NOTICE(S) FILED TODAY FOR 30,000 OZ/

total number of notices filed so far this month: 832 for 4,160,000 oz

BITCOIN MORNING QUOTE $7718 UP 29

BITCOIN AFTERNOON QUOTE.: $7702 UP $7

GLD AND SLV INVENTORIES:

WITH GOLD DOWN $12.75: AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

WE HAD ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD//

A PHONY PAPER GOLD DEPOSIT OF 5.85 TONNES

GLD: 1,048.31 TONNES OF GOLD//

WITH SILVER UP 1 CENT TODAY: AND WITH NO SILVER AROUND

TWO SMALL PAPER WITHDRAWALS IN SILVER INVENTORY AT THE SLV: 373,000 OZ AND LATE IN THE AFTERNOON: 466,000 OZ

RESTING SLV INVENTORY TONIGHT:

SLV: 412.826 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A SMALL SIZED 323 CONTRACTS FROM 142,976 UP TO 143,299 AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE SMALL SIZED GAIN IN OI OCCURRED WITH OUR 3 CENT GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS DUE TO SOME BANKER SHORT COVERING PLUS A CONSIDERABLE EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION ALONG WITH OUR ZERO GAIN IN SILVER OZ STANDING. WE HAD A VERY GOOD NET GAIN IN OUR TWO EXCHANGES OF 2,108 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A STRONG AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: MARCH: 00 AND MAY: 1192 AND JULY: 0 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1192 CONTRACTS. WITH THE TRANSFER OF 1192 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1192 EFP CONTRACTS TRANSLATES INTO 5.96 MILLION OZ ACCOMPANYING:

1.THE 3 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.160 MILLION OZ INITIALLY STANDING FOR APRIL

FRIDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 3 CENTS).. BUT, OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE SOME SILVER LONGS FROM THEIR POSITIONS, AS WE DID HAVE A VERY GOOD NET GAIN OF 1515 CONTRACTS OR 7.575 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

OUR SPREADING OPERATION HAS NOW SWITCHED INTO SILVER…..

SPREADING OPERATION FOR OUR NEWCOMERS:

WE HAVE NOW COMMENCED IN SILVER THE ILLEGAL SPREADING OPERATION \ FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW STOPPED IN GOLD AS THEY NOW BEGIN TO MORPH INTO SILVER AS WE HEAD TOWARDS THE NEW FRONT MONTH WILL BE MAY.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF APRIL. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

17,218 CONTRACTS (FOR 17 TRADING DAYS TOTAL 17,218 CONTRACTS) OR 86.09 MILLION OZ: (AVERAGE PER DAY: 1001 CONTRACTS OR 5.008 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF APRIL: 86.09 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 12.29% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 979,58 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP SO FAR 86.09 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

EXCHANGE FOR PHYSICAL ISSUANCE THIS MONTH IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 323, WITH OUR 3 CENT GAIN IN SILVER PRICING AT THE COMEX ///FRIDAY… THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1192 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A STRONG SIZED OI CONTRACTS ON THE TWO EXCHANGES: 1515 CONTRACTS (WITH OUR 3 CENT GAIN IN PRICE)

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 1192 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A GOOD INCREASE OF 323 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 3 CENT GAIN IN PRICE OF SILVER/ AND A CLOSING PRICE OF $15.17 // FRIDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.7050 BILLION OZ TO BE EXACT or 100.7% of annual global silver production (ex Russia & ex China).

FOR THE NEW MAR DELIVERY MONTH/ THEY FILED AT THE COMEX: 6 NOTICE(S) FOR 30,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.160 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A TINY SIZED 114 CONTRACTS TO 498,089 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE TINY LOSS OF COMEX OI OCCURRED DESPITE OUR CONSIDERABLE COMEX LOSS IN PRICE OF $4.90 /// COMEX GOLD TRADING// FRIDAY// WE HAD CONSIDERABLE BANKER SHORT COVERING , A GOOD INCREASE IN GOLD OZ STANDING AT THE COMEX, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A GOOD EX. FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED DESPITE OUR LOSS IN THE PAPER PRICE OF GOLD.

WE HAD NO ISSUANCE OF OUR NEW 4 GC CONTRACT

WE GAINED A GOOD 2698 CONTRACTS (8.3919 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 2812 CONTRACTS:

CONTRACTS, FEB> 0 CONTRACTS; MARCH 00 APRIL: 0. MAY: 0, AND JUNE 2812.; DEC 0 AND ALL OTHER MONTHS ZERO//TOTAL: 2812. The NEW COMEX OI for the gold complex rests at 498,089. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2698 CONTRACTS: 114 CONTRACTS DECREASED AT THE COMEX AND 2812 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 2698 CONTRACTS OR 8.3919 TONNES. FRIDAY, WE HAD A CONSIDERABLE LOSS OF $4.90 IN GOLD TRADING……

AND WITH THAT LOSS IN PRICE, WE HAD A STRONG SIZED GAIN IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 8.3919 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT FELL $4.90). AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WERE UNSUCCESSFUL (SEE BELOW).

4 GC ISSUANCE: ZERO

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A GOOD SIZED INCREASE IN EXCHANGE FOR PHYSICALS (2812) ACCOMPANYING THE LOSS IN COMEX OI (114 OI): TOTAL GAIN IN THE TWO EXCHANGES: 2698 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)A STRONG INCREASE IN STANDING AT THE GOLD COMEX FOR THE FRONT APRIL MONTH, 3) ZERO LONG LIQUIDATION AND …ALL OF THIS WAS COUPLED WITH THAT CONSIDERABLE LOSS IN GOLD PRICE TRADING//FRIDAY

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 73,484 CONTRACTS OR 7,348,400 oz OR 228.56 TONNES (17 TRADING DAYS AND THUS AVERAGING: 4322 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES: 228.56 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 228.56/3550 x 100% TONNES =6.43% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 2551.46 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 228.56 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A SMALL SIZED 323 CONTRACTS FROM 142,976 UP TO 143,299 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

ALL OF THE GAIN IN COMEX OI WAS DUE TO 1) SOME BANKER SHORT COVERING , 2) THE ISSUANCE OF A GOOD SIZED NUMBER OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A SMALL INCREASE IN SILVER OZ STANDING AT THE COMEX FOR APRIL AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 1192 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR FEB. 0; FOR MAR 0: AND MAY: 1192; JULY: 0 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1192 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE GOOD COMEX OI GAIN OF 916 CONTRACTS TO THE 1192 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 1515 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 7.574 MILLION OZ!!! WITH THE 3 GAIN IN PRICE///

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 3 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// FRIDAY. WE ALSO HAD A GOOD SIZED 1192 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 6.97 POINTS OR 0.25% //Hang Sang CLOSED UP 448.81 POINTS OR 1.88% /The Nikkei closed UP 521.22 POINTS OR 2.71%//Australia’s all ordinaires CLOSED UP 1.65%

/Chinese yuan (ONSHORE) closed DOWN at 7.0832 /Oil DOWN TO 14.04 dollars per barrel for WTI and 20.35 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0832 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0883 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%//FED INITIATES MASSIVE QE

total dealer deposits: nil oz

total dealer withdrawals: nil oz

i)we had 2 deposits into the customer account

into JPMorgan: 0

ii)into DELAWARE: 31,036.000

III) Into Scotia: 606,504.100 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.819 million oz of total silver inventory or 50.04% of all official comex silver. (160.819 million/321.170 million

total customer deposits today: 637,540.100 oz

we had 3 withdrawals:

i Out of Brinks: 812,812.02 oz

ii) Out of CNT: 242,078.120

iii) Out of Delaware: 25,364.193 oz

total withdrawals; 1,080 ,254.333 oz

We had 0 adjustments: and all from the dealer to the customer:

total dealer silver: 81.137 million

total dealer + customer silver: 316.103 million oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

The total number of notices filed today for the APRIL 2020. contract month is represented by 6 contract(s) FOR 30,000 oz

To calculate the number of silver ounces that will stand for delivery in APRIL we take the total number of notices filed for the month so far at 832 x 5,000 oz = 4,160,000 oz to which we add the difference between the open interest for the front month of APRIL.(6) and the number of notices served upon today 6 x (5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL/2019 contract month: 832 (notices served so far) x 5000 oz + OI for front month of APRIL (6)- number of notices served upon today (6) x 5000 oz of silver standing for the APRIL contract month.equals 4,160,000 oz.

WE GAINED 4 CONTRACTS OR AN ADDITIONAL 20,000 OZ WILL NOT STAND AT THE COMEX..

TODAY’S ESTIMATED SILVER VOLUME: 48,908 CONTRACTS //

FOR YESTERDAY: 60,579 CONTRACTS..,CONFIRMED VOLUME

YESTERDAY’S CONFIRMED VOLUME OF 60,579 CONTRACTS EQUATES to 302 million OZ 43.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO +1.19% ((APRIL 27/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO +0.19% to NAV: (APRIL 27/2020 )

Note: Sprott silver trust back into POSITIVE territory at +%-/Sprott physical gold trust is back into POSITIVE/ 1.19%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.66 TRADING 15.62///DISCOUNT 0.25

END

And now the Gold inventory at the GLD/

APRIL 27/WITH GOLD DOWN $12.75//NA HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 5.85 TONNES INTO THE GLD////INVENTORY RESTS TONIGHT AT 1048.31 TONNES

APRIL 24/WITH GOLD DOWN $4.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS TONIGHT AT 1042.46 TONNES

APRIL 23/WITH GOLD UP $10.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS TONIGHT AT 1042.46 TONNES

APRIL 22/WITH GOLD UP $40.75 TODAY:; TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A)A MONSTROUS 3.8 PAPER TONNES WERE ADDED TO THE GLD INVENTORY AND B) ANOTHER HUGE 9.07 TONNES OF PAPER GOLD ADDED LATE IN THE DAY//INVENTORY RESTS AT 1042.46 TONNES

APRIL 21/WITH GOLD DOWN $21.60 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTROUS ADDITION OF 7.9 PAPER TONNES TO THE GLD INVENTORY//INVENTORY RESTS AT 1029.59 TONNES

APRIL 20//WITH GOLD UP $10.00 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1021.69 TONNES

APRIL 17/WITH GOLD DOWN $27.80 TODAY: SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1021.69 TONNES TONNES..THE STRING OF 12 STRAIGHT STRONG DEPOSITS ENDS..

APRIL 16/WITH GOLD DOWN $4.50 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG DEPOSIT OF 4.10 TONNES WAS ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 1021.69 TONNES/12TH STRAIGHT STRONG DEPOSIT

APRIL 15//WITH GOLD DOWN $19.10 TODAY; ANOTHER HUGE CHANGE IN GOLD INVENTORY; A STRONG 7.89 TONNES WAS ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 1117.59 TONNES.//11TH STRAIGHT STRONG DEPOSIT

APRIL 14/WITH GOLD UP $23.55 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 15.51 TONNES WAS ADDED TO THE GLD INVENTORY/INVENTORY RESTS AT 1009.70 TONNES//THIS IS THE 10TH STRAIGHT STRONG DEPOSIT//THIS IS A FRAUDULENT VEHICLE..THEY HAVE NO PHYSICAL GOLD IN THE TRUST..

APRIL 13//WITH GOLD UP $27.65 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 5.36 TONNES WAS ADDED TO THE GLD//INVENTORY RESTS AT 994.19 TONNES

APRIL 9 WITH GOLD UP $37.30 TODAY: ANOTHER HUGE CHANGE IN GOLD INVENTORY: A STRONG 2.92 TONNES WAS ADDED TO THE GLD//GOLD INVENTORY RESTS TONIGHT AT..988.63 TONNES

APRIL 8/WITH GOLD DOWN $.60//ANOTHER HUGE CHANGE IN GOLD INVENTORY/;; A STRONG 1.45 TONNES WAS ADDED TO THE GLD/GOLD INVENTORY RESTS AT 985.71 TONNES

APRIL 7/WITH GOLD UP $.30: ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.27 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 984.26 TONNES

APRIL 6//WITH GOLD UP $32.00//ANOTHER STRONG DEPOSIT INTO THE GLD; A HUGE 7.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT : 978.99 TONNES

APRIL 3//WITH GOLD UP $7.80 TODAY//ANOTHER STRONG DEPOSIT OF 3.22 TONNES INTO THE GLD/INVENTORY RESTS AT 971.97 TONNES

APRIL 2//WITH GOLD UP $31.80 TODAY: ANOTHER STRONG DEPOSIT OF 1.75 TONNES INTO THE GLD//INVENTORY RESTS AT 968.75 TONNES

APRIL 1/WITH GOLD DOWN $7.70 TODAY: ANOTHER CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.62 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 967.00 TONNES

MARCH 31//WITH GOLD DOWN $32.70//A MONSTROUS PAPER DEPOSIT OF 10.84 TONNES INTO THE GLD//INVENTORY RESTS AT 964.38 TONNES

MARCH 30/WITH GOLD DOWN $6.10 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 953.54 TONNES

MARCH 27.WITH GOLD DOWN $16.40: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A HUGE DEPOSIT OF 4.39 TONES INTO THE GLD/INVENTORY RESTS AT 953.54 TONES

MARCH 26//WITH GOLD UP $24.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 13.17 TONNES INTO THE GLD/INVENTORY RESTS AT 949.15 TONNES

MARCH 25/WITH GOLD DOWN $11.40 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.99 TONES INTO THE GLD INVENTORY////INVENTORY RESTS AT 935.98 TONNES

MARCH 24//WITH GOLD UP $67.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 15.80 TONNES OF GOLD INTO GLD////INVENTORY RESTS AT 923.99 TONNES..THIS PROVES THAT THE GLD IS A FRAUD AS LONDON SUSPENDED DELIVERY AS WELL AS ALL REFINERS. THEY HAD NO WAY OF GETTING ANY PHYSICAL OZ INTO ITS INVENTORY//

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

APRIL 27/ GLD INV 1048.31 tonnes*

IN LAST 807 TRADING DAYS: +101.97 NET TONNES HAVE BEEN REMOVED FROM THE GLD

LAST 707 TRADING DAYS;+276.95 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

APRIL 27/WITH SILVER UP ONE CENT TODAY: TWO SMALL CHANGE IN SILVER INVENTORY AT THE SLV:a) A WITHDRAWAL OF 373,000 OZ FORM THE SLV// b) A SECOND WITHDRAWAL OF 466,000: ////INVENTORY RESTS AT 412.826 MILLION OZ//

APRIL 24//WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 413.665 MILLION OZ

APRIL23/WITH SILVER UP 0 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.891 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT 413.665 MILLION OZ//

APRIL 22/WITH SILVER UP 42 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY: A PAPER WITHDRAWAL OF 1.865 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 410.774 MILLION OZ//

APRIL 21//WITH SILVER DOWN 60 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER ADDITION OF 1.398 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 412.639 MILLION OZ//

APRIL 20//WITH SILVER UP 16 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.797 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 414.038 MILLION OZ//

APRIL 17/WITH SILVER DOWN 24 CENTS TODAY; A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.3999 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 16/WITH SILVER UP 5 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 15//WITH SILVER DOWN 45 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV TWO HUGE DEPOSITS: A DEPOSIT OF 1.679 MILLION OZ AND ANOTHER 5.222 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 415.437 MILLION OZ//

APRIL 14./WITH SILVER UP 51 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//A MASSIVE PAPER DEPOSIT OF XXX MILLION OZ//INVENTORY RESTS AT 408.536 MILLION OZ//

APRIL 13//WITH SILVER DOWN 29 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MASSIVE PAPER DEPOSIT OF 6.155 MILLION OZ////INVENTORY RESTS AT 408.536 MILLION OZ//

APRIL 9/WITH SILVER UP 60 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A HUGE DEPOSIT OF 1.84 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 402.381 MILLION OZ.

APRIL 8//WITH SILVER DOWN 21 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 401.541 MILLION OZ///

APRIL 7/WITH SILVER UP 26 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.766 MILLION OZ INTO THE SLV..//INVENTORY RESTS AT 395.826 MILLION OZ

APRIL 6/WITH SILVER UP 50 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 395.826 MILLION OZ.

APRIL 3//WITH SILVER DOWN 15 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 746,000 OZ INTO THE SLV//INVENTORY RESTS AT 395.826 MILLION OZ

APRIL 2/WITH SILVER UP 65 CENTS; A SMALL CHANGE TODAY..A WITHDRAWAL OF .335 MILLION OZ TO PAY FOR FEES//INVENTORY RESTS AT 394.826 MILLION OZ/

APRIL 1/WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 395.181 MILLION OZ//

MARCH 31/WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY: A DEPOSIT OF 1.679 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 375.181 MILLION OZ//

MARCH 30/WITH SILVER DOWN 44 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 393.502 MILLION OZ.

MARCH 27/WITH SILVER DOWN 5 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A MONSTROUS PAPER DEPOSIT OF 8.115 MILLION OZ INTO THE SLV../INVENTORY RESTS AT 393.502 MILLION OZ//

MARCH 26/WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 385.387 MILLION OZ///

MARCH 25/WITH SILVER UP 44 CENTS TODAY: TWO HUGE CHANGES IN SILVER INVENTORY AT THE SLV: TWO DEPOSITS OF 7.369 MILLION OZ AND 2.239 MILLION OZ OF PAPER SILVER INTO THE SLV////INVENTORY RESTS AT 385.387 MILLION OZ//

MARCH 24//WITH SILVER UP 100 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 375.779 MILLION OZ///

APRIL 27.2020:

SLV INVENTORY RESTS TONIGHT AT

412.826 MILLION OZ.

END

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 3.56/ and libor 6 month duration 0.92

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – 2.64

GOLD’S LEASE RATES PLUMMET TO HUGE NEGATIVE

CENTRAL BANKS CALLING IN THEIR LEASES.

GOLD NON EXISTENT.

XXXXXXXX

12 Month MM GOFO

+ 1.92%

LIBOR FOR 12 MONTH DURATION: 0.94

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -.98

GOLD’S LEASE RATES PLUMMET TO HUGE NEGATIVE

CENTRAL BANKS CALLING IN THEIR LEASES.

GOLD NON EXISTENT.

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

ii) Important gold commentaries courtesy of GATA/Chris Powell

A must read…Mooney presses again the CFTC on jurisdiction over manipulative trading by the Governments/

(Chris Powell/Mooney)

CFTC: Does it have jurisdiction over manipulative trading by

government?

Submitted by cpowell on 03:54PM ET Saturday, April 25, 2020.

Section: Daily Dispatches

11:57a ET Saturday, April 25, 2020

Dear Friend of GATA and Gold:

U.S. Rep. Alex X. Mooney, R-West Virginia, is pressing the U.S.

Commodity Futures Trading Commission to answer the critical

questions about market manipulation the commission long has

refused to answer lest it expose the U.S. government’s rigging

of the futures markets and especially the gold and silver

futures markets.

In a letter dated April 13 and made public this week, Mooney

reminded the commission that it had evaded the key questions

asked in his previous letter and that the questions are capable

of yes-or-no answers:

1) Does the commission have jurisdiction over manipulative

futures trading by the U.S. government or its brokers or agents

or other governments?

2) Is the commission aware of futures trading by the U.S.

government, its brokers, or agents?

Of course these are the questions that long should have been

pressed on the commission by those who pose as financial

journalists and market analysts. That the commission refuses to

answer them would be big financial news in itself if there was

any serious financial journalism.

GATA urges those market analysts who have been skeptical of our

claims of surreptitious manipulation of the monetary metals

markets by governments and particularly the U.S. government —

claims extensively documented here —

http://gata.org/taxonomy/term/21

— to put the two critical questions to the CFTC themselves and

then report the commission’s refusal to answer. No one has any

authority to dispute gold and silver market manipulation

without having attempted such research himself.

Mooney’s new letter to the CFTC is here:

http://gata.org/files/MooneyLetter-CFTC-04-13-2020.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

To contribute to GATA, please visit:

end

With so much registered and eligible gold why is it necessary for gold bars to be flying from the Perth Mint in Australia to the comex in New to easy supply squeeze?

(Bloomberg/GATA)

Gold bars are flying from Perth Mint to New York to ease supply squeeze

Submitted by cpowell on Sat, 2020-04-25 15:37. Section: Daily Dispatches

And still the Comex’s recently touted contract for a quarter claim on a 400-ounce London Good Delivery bar hasn’t traded even once yet — and the Comex won’t say why and the news organizations that hailed the contract won’t even ask, being only propagandists, not journalists.

* * *

By David Stringer

Bloomberg News

Friday, April 24, 2020

Australia’s largest gold refinery has ramped up production of one kilogram bars to ease the supply squeeze in the United States that helped propel a surge in the premium for New York futures.

The collapse in air travel that has grounded passenger jets — frequently used to transport gold products — and virus-related disruptions to some refining capacity has tightened availability of the rectangular bars, typically used to settle the Comex futures contracts.

“We’re producing as many kilobars as we can. We’re probably churning out 7 1/2 tons of them a week at the moment and we are forward-sold well into May,” Richard Hayes, chief executive officer of the Perth Mint, said in an interview. “A very large portion of those kilobars are ending up as Comex deliveries.” …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2020-04-24/gold-bars-heading-11-…

* * *

end

Kim collectedly states that coin demand/pricing has relevance when we have no delivery at the London spot//fx facility.

(Kim/GATA)

John Kim: The persistent gold and silver price illusion

Submitted by cpowell on Sun, 2020-04-26 16:24. Section: Daily Dispatches

12:23p ET Sunday, April 25, 2020

Dear Friend of GATA and Gold:

While Voima Gold’s researcher Jan Nieuwenhuijs argued last week that coin demand has little relevance to the prices of gold and silver —

— market analyst John Kim argues today that the commonly quoted “spot” prices of the monetary metals have no relevance at all when metal really isn’t available to the public at those prices and that coin prices are the only relevant monetary metals prices if coins are the only form of metal the public can obtain.

As a result, Kim adds, the real gold price is above $1,900 per ounce, the real silver price is nearly $26 per ounce, and the gold-to-silver price ratio is not the 125-1 ratio derived from “spot” prices but the 74-1 ratio derived from coin prices.

Kim’s commentary is headlined “The Persistent Gold and Silver Price Illusion” and it’s posted at his internet site, Maalamalama.com, here:

https://maalamalama.com/wordpress/the-persistent-gold-and-silver-price-i…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee

CPowell@GATA.org

end

iii) Other physical stories:

https://www.jsmineset.com/2020/04/27/nothing-but-crickets-from-the-cme-lords-of-common-core/

Nothing But Crickets From The CME Lords Of Common Core

Posted April 27th, 2020 at 9:11 AM (CST) by J. Johnson & filed under General Editorial.

Great and Wonderful Monday Morning Folks,

Gold is recovering from a British hangover but only after a high of $1,745.80 was reached with the London low at $1,728.80 with the “now” price at $1,734.40, down $1.20. Silver is still trading in the positive, even after hitting the side of my screen to see if the price was stuck, with the trade at $15.50, up 5.5 cents after reaching a high of $15.635 with the London low at $15.410. The US Dollar broke below par with the trade at 99.970, down 46.4 points, recovering from a low at 99.84 with the high start at 100.370. Of course all this happened already, before 5 am pst, the Comex open, the London lows, and after 21+ years of absolute proof that the EuroCurrency has retained only 15% of what it was worth when it was conceived against the price of Gold. I’m quite certain the Euro-leaders are patting themselves on the back for this too.

In Venezuela, Gold’s price now sits at 17,322.32, showing a 233.7 Bolivar pullback with Silver’s price reduced by 1.249 with its current value at 154.806 Bolivar. Argentina’s Peso now has Gold valued at 115,096.11 Pesos, offering those that delayed their buying a 1,411.80 discount from Friday’s quote with Silver at 1,028.78 Peso’s, a reduction of only 6.64. Turkey’s Lira price for Gold is trading at 12,114.65 showing a 138.56 T-Lira pullback with Silver losing 0.657 Lira with the price set at 108.261.

April Silver Delivery Demands now sit at 6 fully paid for contracts waiting for receipts and with No Volume up on the board so far this morning. This proves 15 out of 21 demands for physical, were finally fulfilled on Friday even after the Comex Lords of Math posted a Volume of 10 on Friday but gave no price for that 10-lot trade. We are forced to believe this is an exit/entry spread trade because that is what the CME-people tell us it is. As a reminder, we have spoken at length to these people, including real former licensed pit brokers. They all tell us the prices of spread trades are not necessary to post because they only profit off the differences, with my query, “how can anyone have a profit or loss if there is no price to post?” How can I do that in my account? We always get nothing but crickets from the CME Lords of Common Core. Silver’s Overall Open Interest gained another 805 more short contracts in order to control the price with the count now at 143,893 Overnighters. What a coincidence it is to see the Open Interest always gain on the day the Sellers of Calls need a lower price in order to not pay. Especially since today is that day the sellers of these derivatives, settle out by buying back their sold May Call Options. The day this turns, will be a day to remember.

April Gold’s Delivery Demands now sit at 203 fully paid for contracts waiting for receipts and with a Volume of 66 up on the board with a trading range between $1,731.90 and $1,720.00 with the last single lot sell order, so far today, at the low. Friday’s final trading range for the delivery month was between $1,744.00 and $1,714.40 with the last registered trade at $1,723.50 yet that famous “adjusted close” was done at the low, as usual, and with a total Volume count at 221. Gold’s Overall Open Interest also gained more shorts in order to keep things under control with the count now at 499,428 Overnighters showing a gain of 472 more shorts, as we wait for tomorrows count to “not show” any manipulations on the Precious Metals Options Expiration Day. Maybe more concerning is the spread between the COMEX spot price and the next few month’s trades, which should be looked at and with suspicion, with April’s discounted price being $1,720.00 with May’s price at $1,724.30, with June’s price way up at $1,735.80 showing a huge spread of $15.80, between the 2 big delivery months. We are now being led to believe that these past 2 months of staying in place, with a large portion of the mining industry being shuttered because of the airborne CCP19, is giving everyone a better deal as the supplies are being dried up. Only in an Algo trading world can this occur, because it goes against all common sense!

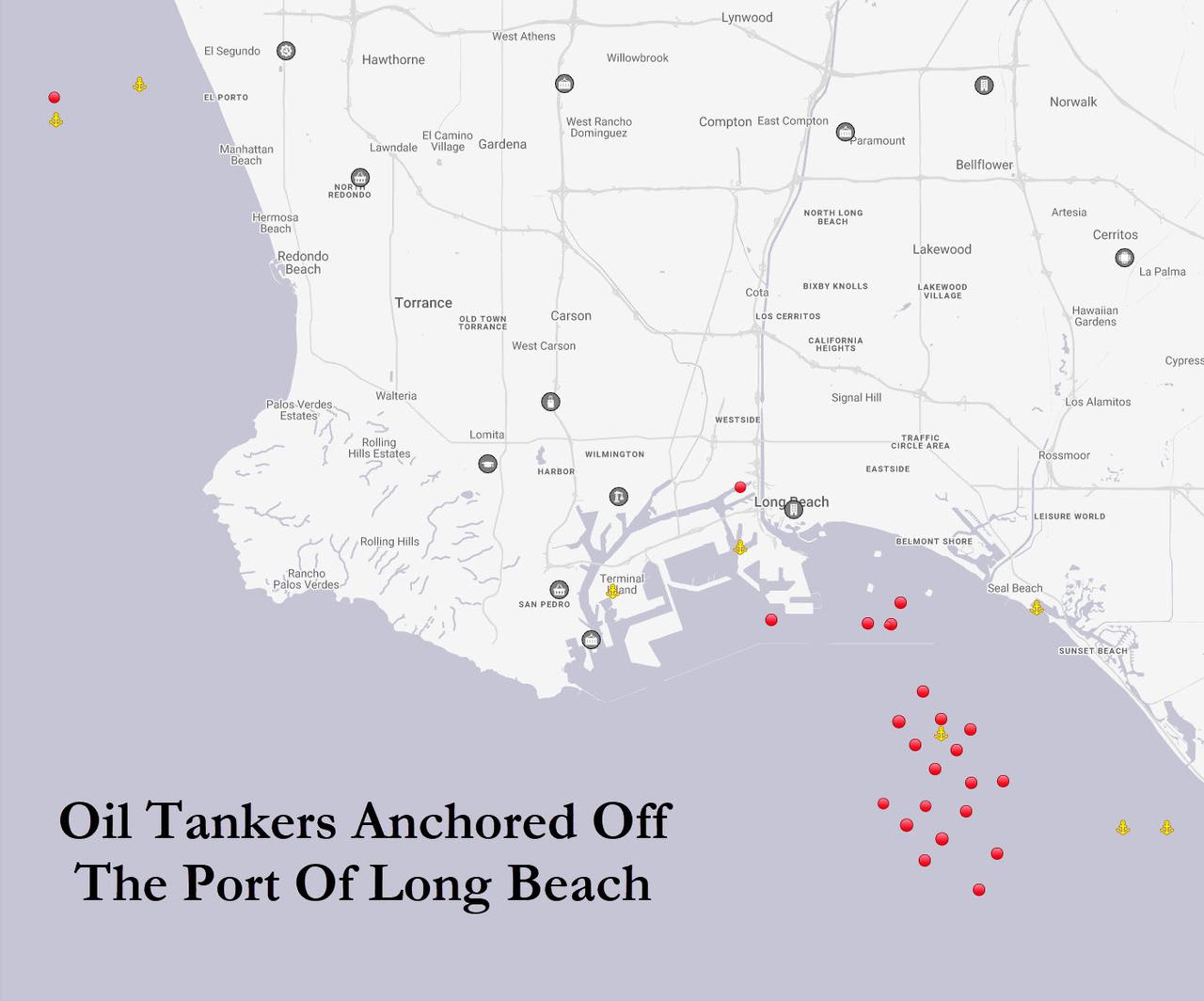

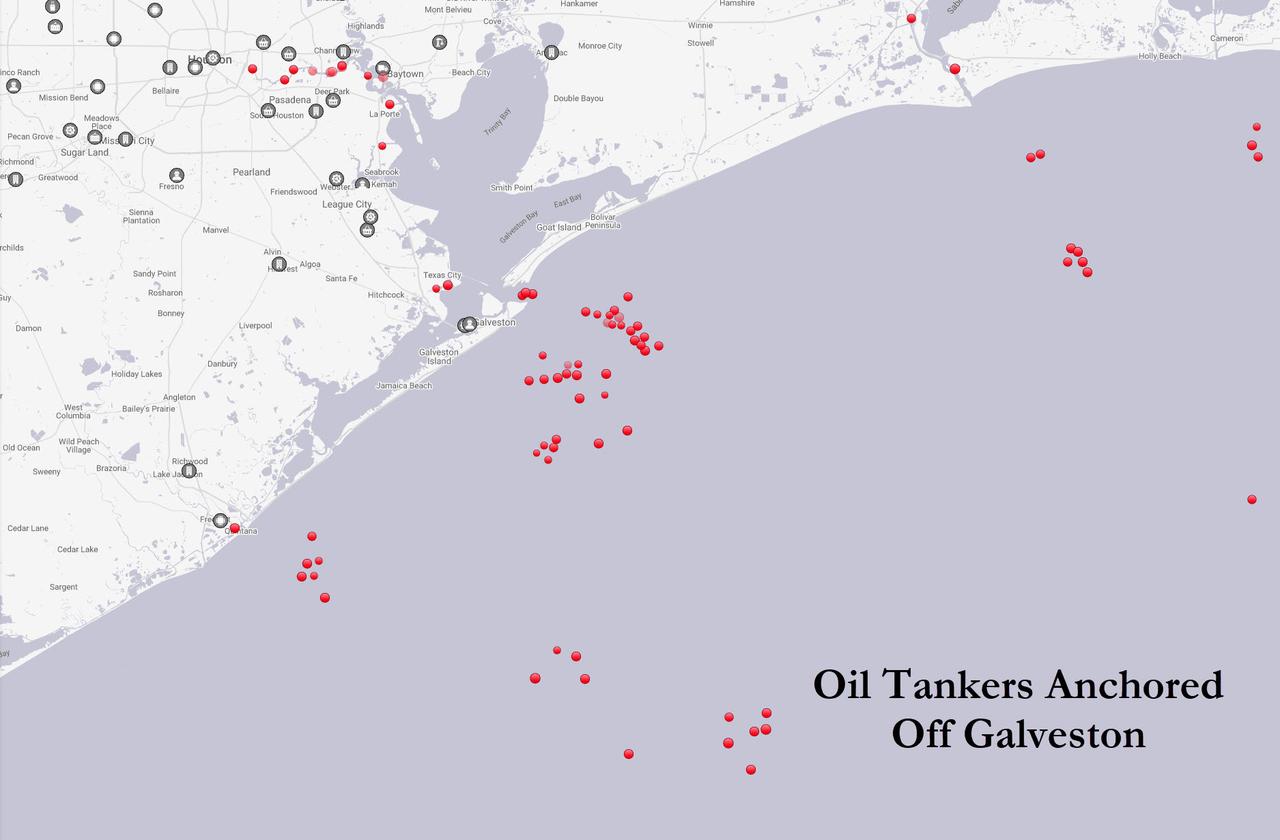

Not only are the precious metals numbers way off kilter, so is the rest of the central banking system, as their print promoters tell everyone they need more cash as the BOJ Launches another round of Unlimited QE, as we see more supertankers off our California coast and as our nations real estate market has had nothing to show with everyone staying in place. Tom Barrack, whose Colony Capital owns $50 billion in a real estate portfolio, used the word “chaos”, but we think the better term would be “Funny you Ask, there’s No Bid”.

Tomorrow is the last day to buy into the April Delivery system for both Silver and Gold. I’ve always thought that when Mr. Resolute wanted to make a real hard statement, it would be on the last day of delivery of any given month. Yeah, I’m waiting for it, and I would wager the shorts in $40k suites are phinkstering about it too. Alas, Mr. Resolute(s) may want to survive this too, so I guess it depends on your level of continence or is it confidence? Let’s find out what the future holds, so in the meantime, hold on tight to the real. Lose no sleep over being away from the markets while the world rushes into bankruptcy. Keep that smile on your face and a positive attitude in your head no matter what, and as always…

Stay Strong!

Jeremiah Johnson

end

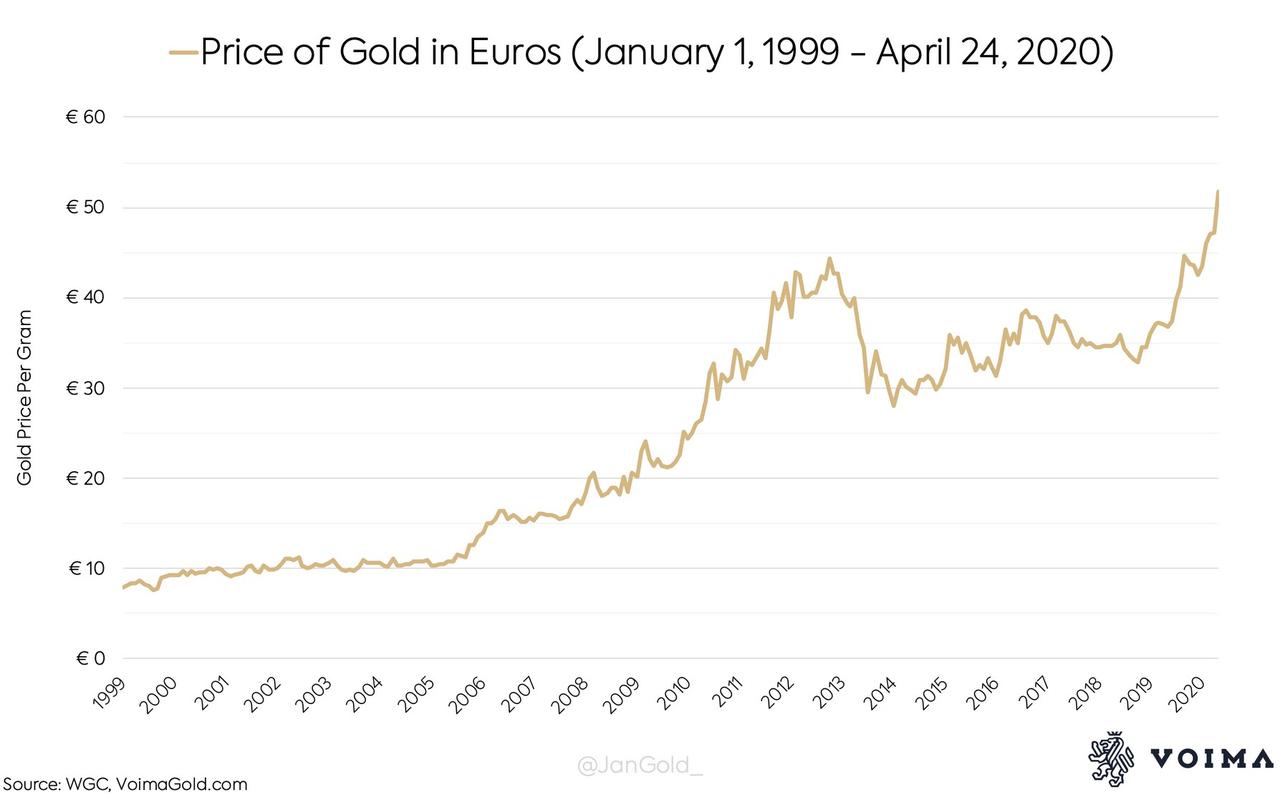

Since Inception, The Euro Has Devalued 85% Against Gold

Authored by Jan Nieuwenhuijs for Voima Insight,

Technically, the euro was launched on January 1, 1999, although euro notes and coins started circulating in January of 2002.

The first gold price recorded in 1999 was €7,879 euros per Kg – or €7.88 euros per gram (we’ll use euros per gram as the gold price in the remainder of this article). By now, the gold price has crossed €51 euros per gram. A new all-time high.

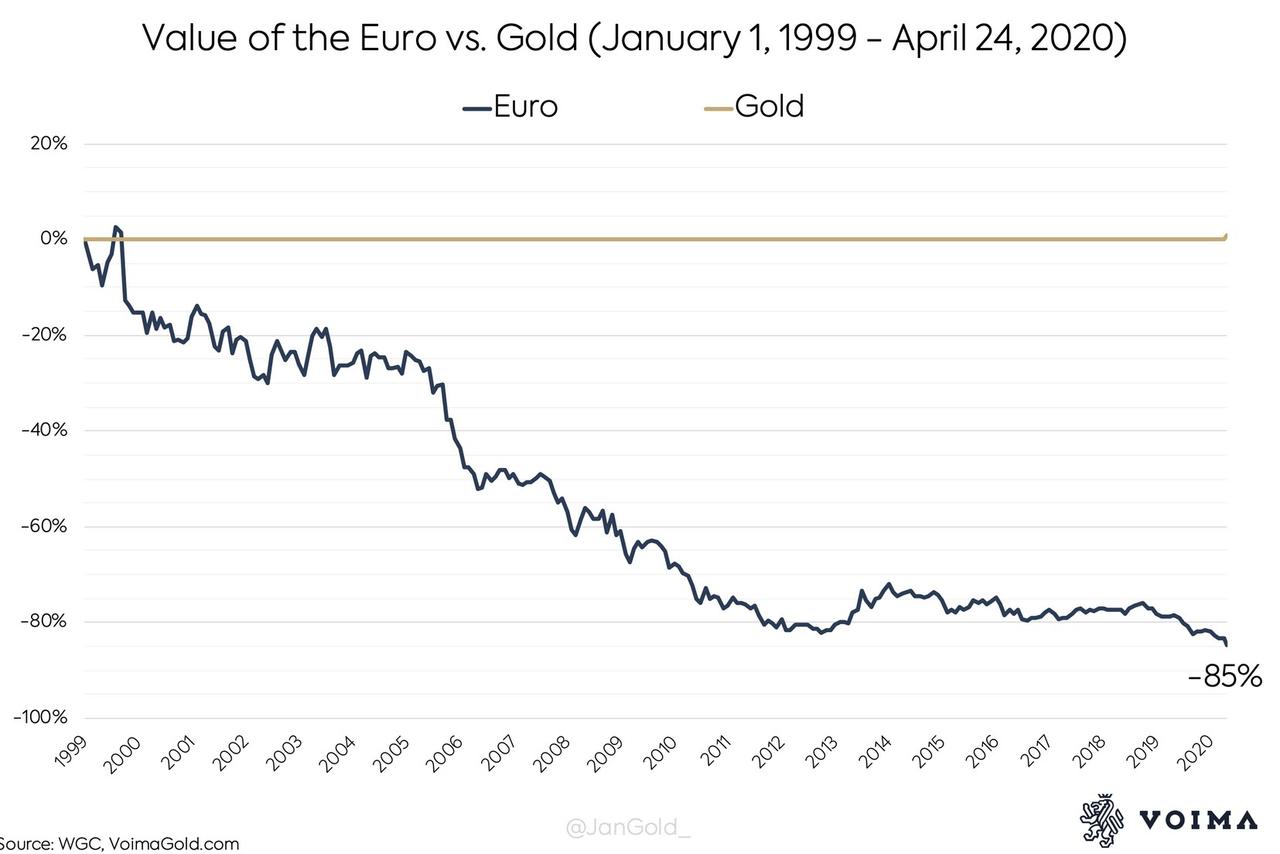

Over the course of 20 years, the price of gold in euros has increased by 555%. From a historic perspective the euro is a young currency, but already lost 85% of its value against gold. This reveals the instability of fiat money.

To evaluate by how much the euro has devalued against gold, it must be measured in gold terms (because a currency can’t devalue by more than 100%). In 1999 it took 0.13 gram to buy one euro; today only 0.02 gram. The result is that the euro lost 85% of its value versus gold. In the chart below you can see the euro’s descent versus gold since 1999.

Measuring the value of currencies against each other is interesting, but most important is what this means for the purchasing power of currencies locally. The end goal of every participant in the economy is goods and services. What truly matters for a currency is its purchasing power. We will compare the purchasing power of euros versus gold in the eurozone.

Many people think that euros only lose purchasing power when a bank needs to be paid to store the euros. In other words, if the interest rate on a bank account is negative. This is called “the money illusion.” In reality, one has to subtract consumer price inflation from the interest rate, to arrive at the real interest rate. For the sake of simplicity, let’s say the current interest rate for most savers is zero, minus one percent inflation, is -1%. Currently, euros approximately lose 1% of their purchasing power per year.

Jan Nieuwenhuijs@JanGold_A friend just told me his bank account might be charged with “negative interest rates” in the future. Outraged he was. I told him inflation was eating away his money for years now, with interest rates at zero. It seemed he didn’t “want” to understand this is the same thing.

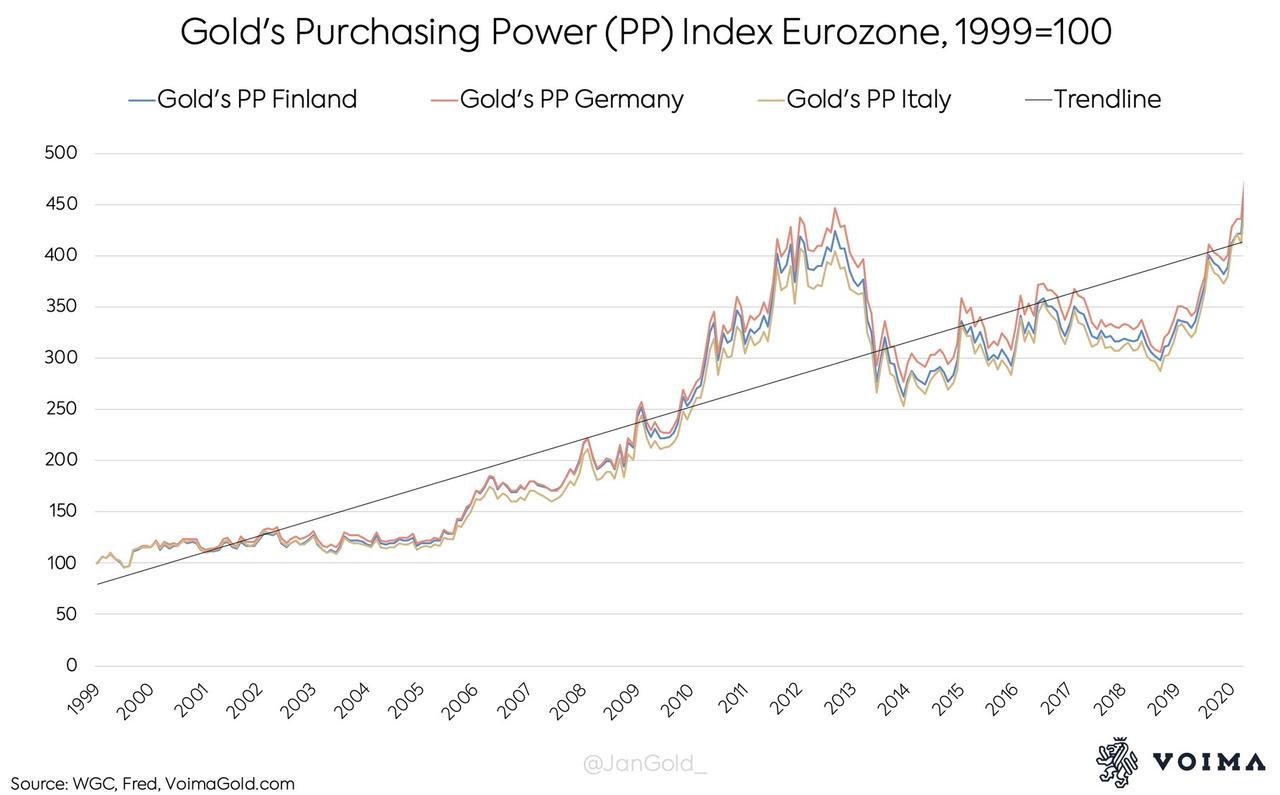

Now, let’s have a look at gold. Over the past 12 months the gold price has increased by 39%. Subtracted by 1% inflation, is 38%. In one year the purchasing power of gold has increased by 38% in the eurozone (minus storage costs, that is). However, the gold price doesn’t go up by 39% every year, it can even go down for some years. Nevertheless, gold’s purchasing power has greatly increased over the past 20 years. Which is why physical gold should be seen as a long-term reserve asset.

To reveal gold’s purchasing power in the eurozone I have adopted an index. First, I divided the gold price by consumer prices, and then created an index with a base of 100 in the year 1999. I have computed gold’s purchasing power index for Finland, Germany and Italy. Because consumer prices slightly differ for the selected countries, the purchasing power of gold in these countries is not exactly equal. Though, I found gold’s purchasing power is roughly the same for the entire eurozone.

First and foremost, you can see gold’s purchasing power has increased in the eurozone since 1999. This means that the price of gold has outpaced consumer prices. From the index number you can see that gold’s purchasing power, on average, has increased by a staggering 350% (450 – 100) over 20 years. The gold price can be volatile, at times, but over longer periods of time it preserves its purchasing power, with the benefit that it doesn’t have any counterparty risk, so it withstands every crisis.

* * *

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Futures Surge As BOJ Goes Full Brrr, States Reopen While Oil Craters

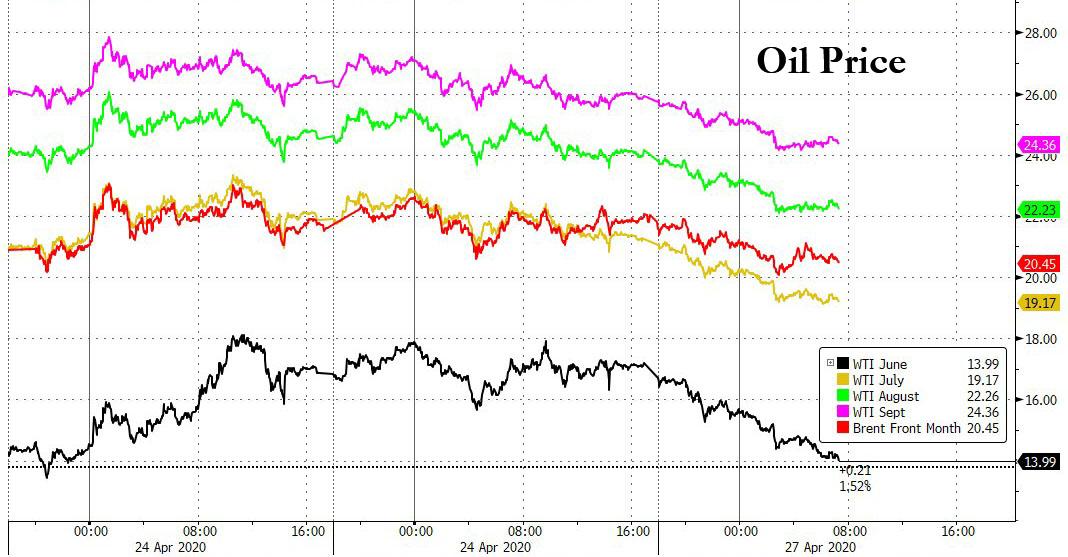

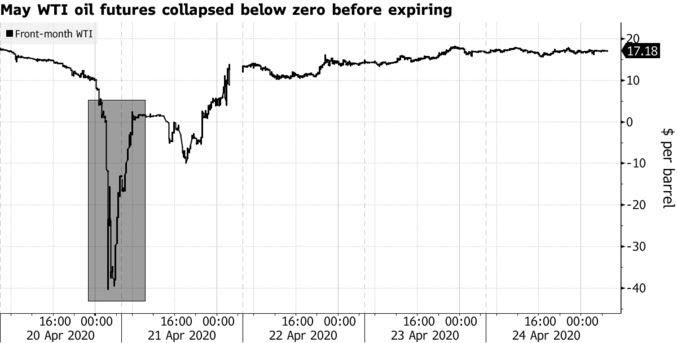

S&P futures climbed alongside stocks in Europe and Asia to start the week after the BOJ went full Brrr earlier when the central bank announced it would buy unlimited amount of bonds (even though nobody actually wants to sell to the BOJ) as more state and countries edged toward reopening, even as earnings season is shaping up to be an even greater disaster than expected (US EPS of -24% yoy is coming in some 9% lower than consensus expectations), while oil prices plunged again, with the June WTI contract plunging below $13.

Futures for the three main US benchmarks all pointed to a second day of gains with the Emini approaching its resistance level around 2850 amid continued talk of easing the lockdowns that have been used to help contain the coronavirus…

… and as investors turned to quarterly earnings reports from marquee companies including Apple and Microsoft later this week, which however Goldman warned over the weekend have surged too much, too fast and that will result in the next market crash.

The Stoxx Europe 600 Index also rose after missing out on a late Wall Street rally on Friday. Deutsche Bank AG rallied after joining other investment banks by beating first quarter earnings expectations, even as it warned about looming loan defaults. Bayer AG raised the specter of “considerable liquidity challenges” as it continues to deal with litigation related to Roundup weedkiller. Still, shares gained as the company said its core earnings per share target is unchanged for now, with the effect of Covid-19 impossible to assess. Adidas AG fluctuated after forecasting the first quarterly loss in over four years as more than two-thirds of the German athletic wear maker’s stores remain closed.

Earlier in the session, Asian stocks gained, led by industrials and materials, after falling in the last session. The Topix gained 1.8%, with Mitani Sangyo and eBook Initiative rising the most after the BOJ announced earlier that it would go “full BRRRR” as it removed limits on its purchases of government bonds and ramped up its scope for buying corporate debt and commercial paper. And in delightful irony to this “all in” easing move, the yen strengthened.

David Ingles

✔@DavidInglesTV

The Bank of Japan going all in pretty much:

– removes limits on JGB buys

– raises limits on corporate bond, CP buys

– removes price momentum from forward guidanceLooks like one of the world’s biggest “bond funds” is about to get bigger.

David Ingles

✔@DavidInglesTV

Relative to the size of its economy, the BOJ’s pretty much gone “hold my biru”

Elsewhere, the Shanghai Composite Index rose 0.2%, with Kingswood Enterprise and China First Heavy Industries posting the biggest advances.

Data over the weekend showed coronavirus deaths slowed the most in more than a month in Spain, Italy and France, and all three countries have signaled tentative moves to reopen their economies. Italian stocks were among the biggest winners and its bonds outperformed after the nation dodged a credit rating downgrade late on Friday.

In the US too, many more U.S. states have looked to reopen businesses as the health crisis wreaks havoc on the economy, with the White House forecasting a staggering jump in the nation’s monthly jobless rate. Although trillions of dollars in stimulus have helped the benchmark S&P 500 recover nearly 30% from its March trough, analysts say further gains might be limited unless there is progress on developing treatments for the deadly disease.

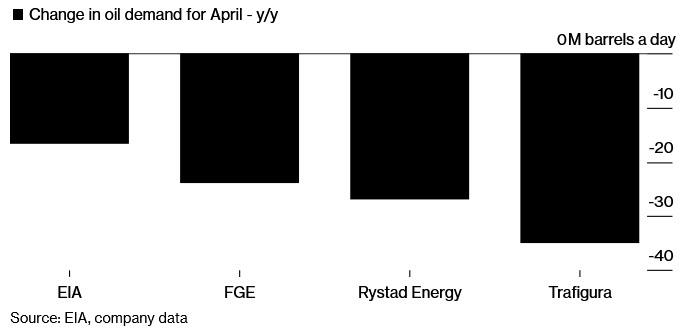

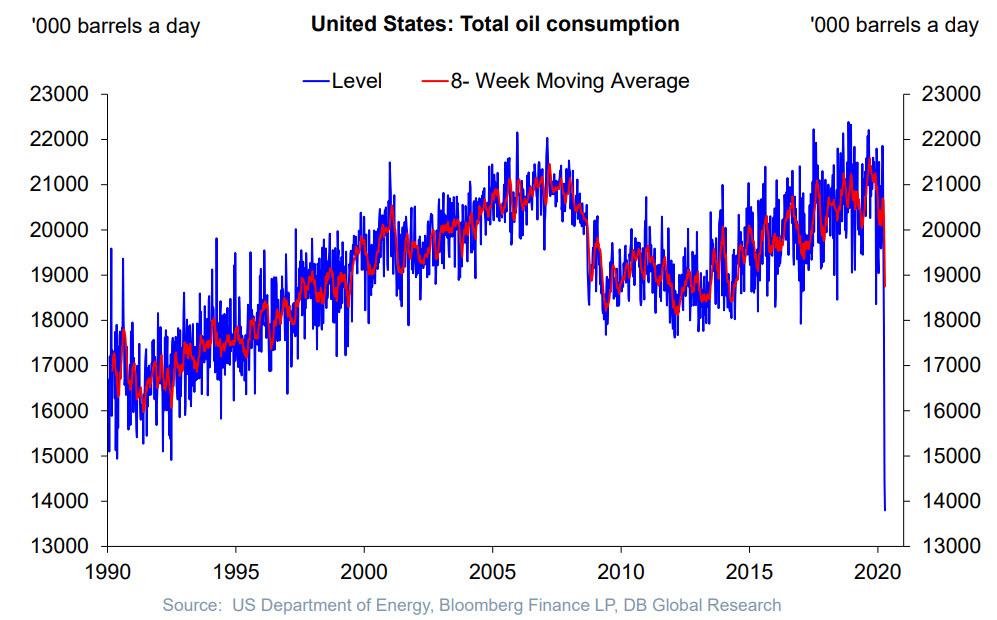

In commodities, as noted earlier, the big mover was again oil which did buckled the general risk on mood and plunged below $14, which as noted over the weekend is a problem as “The Oil Price Is A Rare Indicator Of What Is Still Real In This Market”

It’s a busy week, with the Federal Reserve and European Central Bank due to announce policy decisions following the BOJ as the battle against the pandemic continues. Several major economies will release GDP numbers, while corporate earnings will keep flooding in.

“This coming week will be huge from a macro data perspective and the extent to which the global economy has been floored by Covid-19,” said Simon Ballard, chief economist at First Abu Dhabi Bank. “Until we are clearly past the peak of the outbreak, on a global scale, and can feasibly deem the pathogen to be contained and there to be no meaningful risk of a second wave of infection, we believe a defensive investment strategy will remain the most appropriate.”

Focus this week will also be on a two-day Federal Reserve meeting ending on Wednesday, although expectations are low for more easing by the central bank. About a third, or some 173 companies in the S&P 500 are scheduled to report quarterly earnings later in the week, including Apple, Amazon.com, Microsoft, Boeing, Ford, General Electric and Chevron. Overall analysts expect a decline of nearly 15% in first-quarter earnings of S&P 500 companies – a number which so far is roughly 25% – with profits for the energy sector estimated to have slumped 68%.

In FX, the dollar weakened broadly and Treasuries slipped as risk sentiment improved on the prospect of an easing of lockdown restrictions around the globe. The Bloomberg Dollar Spot Index dropped the most in more than a week, with the greenback weakening against all Group-of-10 peers; EUR/USD rose a second day. Bunds slipped while European peripheral debt continued to lead euro-area gains; Italian bonds and stocks climbed after S&P Global Ratings left the nation’s credit rating unchanged, delaying the risk of a downgrade toward junk to later this year. The pound rose in its longest winning streak in a month as U.K. Prime Minister Boris Johnson’s return to work fueled speculation he may consider moving toward lifting the lockdown. The Australian dollar outperformed all G-10 peers and rose to a 6-week high versus the greenback as easing coronavirus-related restrictions in two states spurred optimism that the outbreak was slowing in the nation. The New Zealand dollar also advanced, partly by cross flows versus Aussie amid thin liquidity due to public holiday. Japan’s bonds advanced, led by five- and 10-year maturities, as the Bank of Japan scrapped the limitation on its JGB purchases to support the economy; the BOJ also ramped up its purchases of corporate debt

Expected data include Dallas Fed Manufacturing Activity. F5 Networks and Universal Health are among companies reporting earnings.

Market Snapshot

- S&P 500 futures up 0.9% to 2,855.00

- STOXX Europe 600 up 1.4% to 334.34

- MXAP up 1.9% to 144.33

- MXAPJ up 1.8% to 464.18

- Nikkei up 2.7% to 19,783.22

- Topix up 1.8% to 1,447.25

- Hang Seng Index up 1.9% to 24,280.14

- Shanghai Composite up 0.3% to 2,815.50

- Sensex up 1.9% to 31,910.86

- Australia S&P/ASX 200 up 1.5% to 5,321.40

- Kospi up 1.8% to 1,922.77

- German 10Y yield rose 0.5 bps to -0.468%

- Euro up 0.2% to $1.0842

- Brent Futures down 4.3% to $20.52/bbl

- Italian 10Y yield fell 14.6 bps to 1.664%

- Spanish 10Y yield fell 6.5 bps to 0.887%

- Brent Futures down 2.5% to $20.90/bbl

- Gold spot down 0.5% to $1,721.49

- U.S. Dollar Index down 0.4% to 99.94

Top Overnight News from Bloomberg

- Italy will start easing lockdown restrictions next week and Germany reopened some schools on Monday as new cases and fatalities drop in Europe. In Britain, Premier Johnson returned to work and urged the public not to let up on social distancing measures

- Despite the Bank of Japan ramping up its stimulus measures on Monday, the dollar-yen has slid into a bearish death cross technical pattern. The currency pair’s 50-day moving average dropped below its 200-day equivalent, which could signal more downside if the move holds

- Nearly one-third of U.S. business economists expect operations at their companies will return to normal within five to eight weeks, though almost as many say it’s likely to be three to six months before coronavirus- mitigation efforts wind down in earnest

- The top two trade groups representing major retailers such as Walmart Inc., Target Corp. and Best Buy Co. are calling on U.S. governors to adopt uniform reopening standards as the pandemic subsides

- Market manipulation is still on the rise in the U.K. even after a decade of crackdowns onschemes to rig foreign-exchange rates and other key benchmarks. And the coronavirus pandemic could make things worse

- A collapse in the volume of short-term IOUs issued by European companies and a dramatic shortening in their maturities show the region’s commercial paper market remains under stress

Asian equity markets were mostly positive with sentiment underpinned by optimism regarding the reopening of global economies after some US states began to reopen businesses and with Italy, Spain and France preparing to ease restrictions after recording their lowest death tolls in a month. ASX 200 (+1.5%) was led higher by tech and industrials with sentiment also supported by loosening of lockdown measures after Queensland announced to permit some outings from next Saturday. However, upside was initially restricted by weakness in the largest weighted financials sector after big 4 bank NAB posted a 51% slump in cash profit and unveiled plans for a substantial share placement, while Nikkei 225 (+2.7%) outperformed amid a weaker currency and the BoJ policy announcement where the central bank announced further measures including a shift to unlimited bond buying as widely speculated. Hang Seng (+1.9%) and Shanghai Comp. (+0.3%) were also higher with Hong Kong surging as its government was said to consider easing social distancing controls and the mainland somewhat lagged after weak Chinese Industrial Profits which contracted by almost 35% Y/Y. Finally, 10yr JGBs were initially lower amid the gains in stocks and similar pressure in T-notes, although JGBs prices were later boosted after the BoJ policy announcement in which the central bank also upped its corporate bond and commercial paper purchases with the maximum limits of purchases from a single issuer upped to JPY 500bln and JPY 300bln respectively from JPY 100bln.

Top Asian News

- BOJ Vows to Buy as Many Bonds as Needed in Stimulus Move

- China Industrial Profits Dropped by More Than a Third in March

- Alibaba Is Said to Demote Top Exec After Probe into Scandal

- India Will Probably Miss Deficit Goal, RBI Chief Tells Cogencis

European equities trade comfortably on a firmer footing [Euro Stoxx 50 +2.2%], as the risk-appetite from the APAC session followed through and intensifies as European economies near an easing lockdown measures – with Italy to begin its lifting from May 4th, Spain relieving some of its strictest measures and UK to reportedly update on measures as early as this week. Bourses see broad-based gains but Italy’s FTSE MIB (+2.5%) modestly outperforms after S&P refrained from downgrading the country’s rating on Friday. Sectors all reside in positive territory, with Financials leading the gains – propped up by Deutsche Bank (+11.2%) earnings – whilst energy underperforms amid price action in the oil complex. This performance is also reflected in the sector breakdown with Banks the outperformer and Oil & Gas the laggard, Travel & Leisure resides towards the top amid lockdown lifts across Europe and US. In terms of individual movers, earnings see more focus on German firms; DAX-giant Bayer (+2.7%) sees impetus from Q1 revenue and adj. EBITDA topping analyst estimates, and improvement in EPS and gains across all its units – the Co. accounts for 6.8% of the DAX 30. Adidas (+2.5%) conformed to the broad risk-appetite after nursing opening losses of over 3%, which initially emanated from dismal earnings alongside a failure to provide FY20 guidance. Adidas noted that 70% of its global stores remain shut. Deutsche Bank (+11.2%) shares soar on an early earnings release in which Q1 pre-tax posted a profit of EUR 206mln vs. Exp. loss 269mln, albeit the group notes that it is unlikely to meet its FY20 leverage ratio target of 4.5%. A spokesman said the release of key metrics was due to a significant divergence with analyst forecasts – Commerzbank (+6.5%) rises in sympathy. Elsewhere, Lufthansa (+7.2%) was propelled at the open after Germany’s Economy Minister stated the group must get a chance to return to profitability, whilst the Co. is also seeking a EUR 290mln loan from the Belgium gov’t for its Belgian subsidiary. Similarly, Air France-KLM (+4.7%) and Renault (+5%) see upside after the French gov’t announced a EUR 7bln package for the former, whilst mulling a EUR 5bln loan guarantee for the latter. On the flip side, Airbus (-1.5%) is pressured amid comments from its CEO regarding the severity of the group’s position – stating that the Co. is “bleeding cash” at a rate which threatens the Co’s existence, adding that a third of its business has been lost in the past few weeks.

Top European News

- Why the World’s Highest Virus Death Rate Is in Europe’s Capital

- Deutsche Bank Warns of Loan Defaults After Surprise Profit

- Johnson Returns to Work Urging Britain to Maintain Lockdown

- Rally in Italy’s Bonds Is Only Knee-Jerk Reprieve: Markets Live

In FX, the Greenback has retreated further against G10 counterparts and almost across the board, with the DXY struggling to retain grip or sight of the 100.000 mark within a 100.320-99.847 range amidst an upturn in broad risk sentiment that is only really being tainted by more weakness in crude oil on bearish supply/storage-demand dynamics.

- AUD/NZD – The Aussie and Kiwi are both seemingly reaping the rewards of relative progress and success on the coronavirus front as the respective Governments eye reopening schedules. Aud/Usd is now firmly back above 0.6400 and pivoting 0.6450, while Nzd/Usd is straddling 0.6050 and Aud/Nzd is probing above 1.0650 on Anzac Day. Note, NZ markets return on Tuesday and will be looking towards trade data for some fundamental direction/impetus in the same vein as Australia’s preliminary report last week.

- GBP – The next best major and the Pound could well be receiving another Boris boost as the UK PM returns to his official residence to resume duties with an encouraging update on Britain’s battle to combat COVID-19. Cable has reclaimed 1.2400+ status and Eur/Gbp is meandering between 0.8754-10 parameters with the cross retreating below its 200 DMA again.

- CAD/JPY/EUR – The Loonie is also outpacing its US peer even though oil prices are tanking again, with Usd/Cad under 1.4100 ahead of somewhat dated Canadian securities balances for February, while the Yen has strengthened in wake of the BoJ policy meeting despite further stimulus via QE as speculated ahead of the event. Usd/Jpy got close to 107.00 before a mild bounce that could have been option expiry related given 1.2 bn rolling off at the strike, but also technical as strong chart support sits just beneath the round number circa 106.93/92 (April 15th and 1st lows). On the flip-side, 2 bn expiries from 107.50 to 107.60 may cap the headline pair, while the Euro has 1.1 bn at 1.0800 to provide a cushion alongside a raft of options in to the Fed and ECB on Wednesday and Thursday respectively.

- CHF/NOK/SEK – The Swiss Franc and Norwegian Krona are marginal underperformers following latest weekly sight deposits revealing another significant rise in bank coffers, while the latter is eyeing the aforementioned weakness in crude, like the Russian Rouble. However, the Swedish Crown continues to hold up better on the premise that the Riksbank will stick to its guns on rates tomorrow in favour of non-standard policy measures should the situation warrant more than already implemented. Hence, Usd/Chf idling within a 0.9744-13 band, Eur/Chf off recent near 1.0500 lows between 1.0532-58, Eur/Nok rotating around 11.5000, Usd/RUB encircling 74.5000 and Eur/Sek still suppressed sub-10.9000.

- EM – Some much needed respite for the Rand that has pared declines from 19.1000+ amidst the aforementioned revival in risk appetite, but Usd/Zar may be impacted by thinner than normal volumes due to SA’s Freedom Day holiday, while the Hong Dollar remains close to the top of its peg vs the Dollar prompting the HKMA to intervene again.

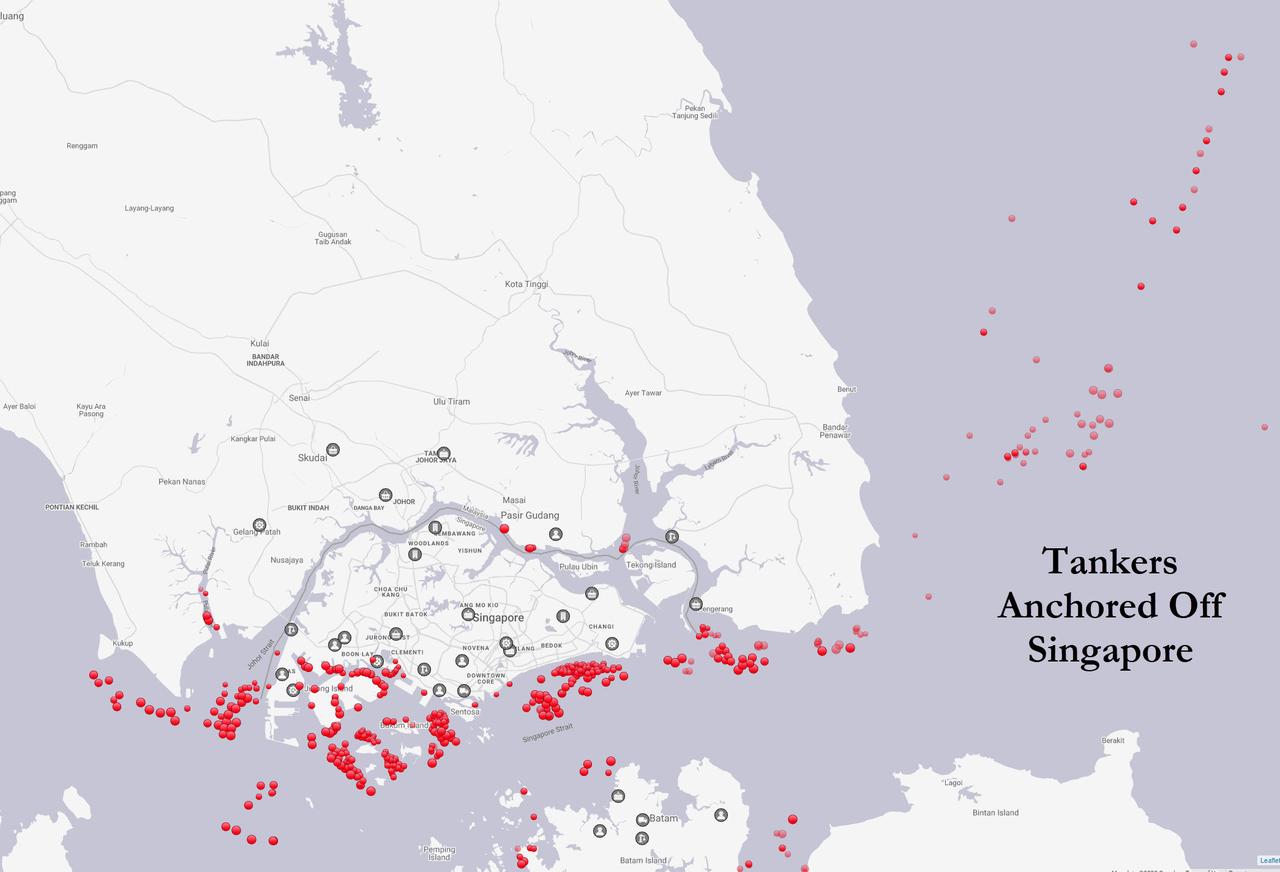

Inn commodities, WTI and Brent front-month futures have resumed selling off as storage scarcity continues to weigh on investor sentiment – with the former underperforming amid reports that Cushing, Oklahoma, may hit full capacity soon. Goldman Sachs believes that storage capacity limits could be tested in as little as three weeks. This week also sees the official implementation of the OPEC+ reduction pact, but some members, including Saudi, have brought forward cuts in a bid to somewhat stabilise the price rout. ING, among other desks, believes that the move is “helpful, [but] it will have little impact on the oil balance in the short term.” Nonetheless, despite the recent geopolitically induced upside in prices – underlying fundamentals remain unchanged. That being said, with major economies set to loosen lockdown restrictions, pressure on demand could start to ease – early signs could be seen in China as refinery activity at independent refiners has been hitting record levels in the Shandong region. WTI June briefly dipped below USD 14.50/bbl to a current base at USD 14.18/bbl (vs. high USD 16.98/bbl), whilst its Brent counterpart sees declines in tandem having tested USD 20/bbl to the downside in early trade (vs. high USD 21.91/bbl). Elsewhere, spot gold sees losses despite a softer Buck, with desks attributing the pressure to improved risk appetite on countries lifting COVID-19 measures. The yellow metal remains comfortably north of USD 1700/oz, having waned off highs of around USD 1720/oz. Copper prices meanwhile remain in the green but somewhat subdued amid a slump in Chinese Industrial profits – prices edging towards USD 2.37/lb vs. high of around USD 2.39/lb. Finally, Dalian iron ore futures recovered as stocks of the raw material fell to their lowest in over 9 months.

US Event Calendar

- 10am: Revisions: Retail Trade

- 10:30am: Dallas Fed Manf. Activity, est. -75, prior -70

DB’s Jim Reid concludes the overnight wrap

It’s hard to believe it’ll be May on Friday. It only feel like yesterday that it was January and the age of innocence. This week we’ll be bombarded with a peak week of Q1 earnings, the big 3 central banks having policy meetings, China PMIs and Q1 GDP growth in Europe/US. Our annual 2020 Default Study has also just been published so please keep an eye out for that.

Before we preview all of the above, one of the most interesting things I read this weekend was a fairly simple piece that explained that the saviour of the world’s health services – namely PPE – is a product of polypropylene and thus the oil and gas sector. It is in effect single-use plastic. Yet I’ve not heard anyone complain about the impact on the environment of trying to produce as much of it as possible. When we discussed in our 2020 climate change related Davos note (link here ) about the difficult global warming dilemmas ahead, we noted that the very things that have helped pollute the atmosphere over the last couple of centuries have also improved the health and wealth of all humans beyond recognition relative to our forefathers. Before the industrial revolutions being a human was a bleak existence for the vast majority. In the Davos note we speculated as to whether humans would soon realise the economic trade-offs necessary if they really wanted to halt global warming. The covid-19 experience has kicked the debate into the long grass for now but I suppose we’re learning a bit more about what life would be like without growth during these lockdowns and also interestingly that single use plastics can be worshiped if used to save lives. Fascinating to see and think about.